ELSEVIER Labour Economics 3 (I 996) 319-336 LABOUR ECONOMICS The determinants of chief executive compensation in transitional economies" Evidence from Bulgaria Derek C. Jones a, Takao Kato b,c,. a Hamilton College, Clinton, NY 13323, USA b Colgate UniversiO', Hamilton, NY 13346, USA Jerome Levy Economics Institute, Annondale-on-Hudson, USA Accepted 19 June 1996 Abstract Using new panel data, we present the first econometric evidence on the determinants of CEO compensation in transitional economies. Using standard specifications, CEO pay is found to be positively related to size, but not to profitability. In specifications adapted to transitional economies, CEO compensation is found to be positively related to size and productivity. The estimated pay elasticities of productivity are equal to or slightly greater than those of size, pointing to the importance of productivity as a determinant of CEO compensation in transitional economies. CEO pay is found to be more strongly tied to productivity when the firm is privatized. JEL classification: M12; J31; L21; P31; 052; P50 Keywords." Executive compensation; Managerial pay; Transitional economies; Bulgaria; Managerial labor markets * Corresponding author. Phone: (+1) 315-824-7562; fax: (+1) 315-824-7033; TKATO @ CENTER.COLGATE.EDU. 0927-5371/96/$15.00 Copyright © 1996 Elsevier Science B.V. All rights reserved. Pll S0927-537 1(96)00015-2 e-mail:

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

E L S E V I E R Labour Economics 3 (I 996) 319-336

LABOUR ECONOMICS

The determinants of chief executive compensation in transitional economies"

Evidence from Bulgaria

Derek C. Jones a, Takao Kato b,c,. a Hamilton College, Clinton, NY 13323, USA

b Colgate UniversiO', Hamilton, NY 13346, USA Jerome Levy Economics Institute, Annondale-on-Hudson, USA

Accepted 19 June 1996

Abstract

Using new panel data, we present the first econometric evidence on the determinants of CEO compensation in transitional economies. Using standard specifications, CEO pay is found to be positively related to size, but not to profitability. In specifications adapted to transitional economies, CEO compensation is found to be positively related to size and productivity. The estimated pay elasticities of productivity are equal to or slightly greater than those of size, pointing to the importance of productivity as a determinant of CEO compensation in transitional economies. CEO pay is found to be more strongly tied to productivity when the firm is privatized.

JEL classification: M12; J31; L21; P31; 052; P50

Keywords." Executive compensation; Managerial pay; Transitional economies; Bulgaria; Managerial labor markets

* Corresponding author. Phone: (+1) 315-824-7562; fax: (+1) 315-824-7033; TKATO @ CENTER.COLGATE.EDU.

0927-5371/96/$15.00 Copyright © 1996 Elsevier Science B.V. All rights reserved. Pll S0927-537 1(96)00015-2

e-mail:

320 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

I. Introduction

The crucial importance of diverse issues concerning the managerial function in Soviet Type Economies (STEs) has long been recognized. Researchers have investigated diverse topics including appropriate reward systems for managers (e.g. Granick, 1954; Berliner, 1957) with special emphasis on the role of incentive systems for managers (e.g. Bonin, 1976; Weitzman, 1976). Equally the vital contribution of the managerial labor market to the success of overall reform during transition has been widely noted (e.g. Aghion et al., 1994; Roland and Sekkat, 1992). Unfortunately to date detailed knowledge, of the nature and effects of the managerial labor market both during planning in STEs and during early transition typically has been scant - for example note the need to derive information on managers during communism from Russian emigres, e.g. Linz (1988). The need to improve our limited understanding of what is actually happening in the managerial labor market during early transition in the economies of the former USSR and Eastern and Central Europe is also clearly evident in the transition literature (e.g. Pinto et al., 1993). It is against this background that the aim of this paper can be understood. By drawing on a new survey, we respond to the weaknesses of the available data and contribute to the literature by reporting the first econometric evidence on the determinants of executive compensation for an economy during the fading days of communism and the early stages of transition, and during a period before mass privatization.

We continue in the next section by briefly reviewing some of the key issues that have appeared in the literature concerning management in communist coun- tries and economies in transition. Next we describe what are most unusual data - for a panel of firms, with corresponding data at the chief executive level. We use these data to estimate two way fixed effects models (including both group effects and time effects). To examine hypotheses on the determinants of chief executive pay we begin by estimating specifications similar to those used in studies of managers in western countries. Then we estimate specifications that have been adapted to reflect the special circumstances of transitional economies. Our findings for the early stages of transition are most interesting. We find that chief executive compensation is positively related to size (measured by employment and sales) and productivity. The estimated pay elasticities of size of around 0.3 are compara- ble to what has been found for firms in advanced market economies. More importantly, we find consistently that chief executive compensation becomes more strongly tied to productivity when the firm is no longer completely state owned. We find no significant relationship of pay to profitability (measured by the return on assets and the profit margin).

D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336 321

2. Management under communism and during early transition: conceptual framework

The managerial labor market in a STE was believed to have a number of features. 1 While top mangers of ' f irms' were as clearly identifiable as their western counterparts, managers in STEs were posited to have much more limited autonomy or scope for discretionary power than top executives in western firms. In large part this resulted from the structure of STEs. The success of key economic agents including top executives was measured not by their ability to make profits but rather by their ability to fulfill plans, where plans were largely developed at higher levels in heavily bureaucratized and very hierarchical systems. In addition, reflecting the dominance of state-owned firms, the government acted as a monop- sonist in the managerial labor market, with managers appointed by the communist party (or its agents, such as ministries). Frequently managers had little experience in the sector of the firm they managed (Linz, 1988).

Managerial reward systems in STEs were distinguished by several attributes. Pay was mainly a base wage, with limited variation with respect to success indicators such as plan fulfillment. Consistent with egalitarian values, the pay of top managers was a low multiple of the average wage (Chapman, 1979). Indeed not only was the chief executive pay affected by the phenomenon of wage levelling, but in many industries in the past chief executives were not even the highest paid.

Theorists have pointed out how these arrangements would be expected to result in acute incentive and motivational problems for managers (e.g. Bonin, 1976; Weitzman, 1976). A substantial gap would emerge between behavior in a propri- etary fashion (as called for under the official ideology) and the reality of risk aversion and the pursuit of a quiet life (Kornai, 1992). Partly because of asymmetries in information between managers and planners, a 'ratchet effect' would emerge with extensive managerial slack (e.g. Ickes and Samuelson, 1987; Litwack, 1991). In turn, several systemic inefficiencies were predicted including diverse pathologies of production (e.g. Putterman, 1993).

At the same time, this portrayal of the conventional wisdom of the way things were in the managerial labor market under communism is typically based on limited evidence, often of a case study or anecdotal nature. This was the case for example with studies including Granick (1954) and Berliner (1957), and the studies of Russian emigres (e.g. Linz, 1988).

Some have noted the crucial importance of incentive systems (including

i There are many good accounts of the basic model of a STE, including the way that the managerial labor market was believed to work therein, for example, Campbell (1991). Here we portray relevant features of this conventional wisdom, as well as pertinent changes that might have been expected to occur both during reform of and transition away from STEs.

322 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

executive pay) for managers in order to facilitate successful overall reform during early transition (e.g. Aghion et al., 1994). For instance, more market-oriented managerial behavior will be encouraged when executive compensation is struc- tured so as to provide pecuniary incentives for managers to pursue profitability. In the context of early transition, downsizing of overstaffed state owned firms and productivity increases appear to be key ingredients of successful reform. Arguably such adjustments will be facilitated when executive compensation is structured so as to reward managers for rational downsizing and productivity increases.

Moreover, it is believed that reform of executive contracts is only one ingredi- ent of change. In order to produce well motivated management who will engage in intelligent restructuring, other complementary changes are needed. These measures include policies to change enterprise ownership (privatization) and the context within which firms operate (especially macro stabilization, new competition policies, and reform of the banking and taxation system). Equally recent empirical studies have pointed to the potentially important role of differences in manage- ment behavior in accounting for at least some of the differences in firm adjustment during early transition (e.g. Pinto et al., 1993; Estrin et al., 1995). Arguably such differences at least in part reflect differences in management quality that, in turn, are linked with differences in the structure of executive compensation.

Also, up to now very little detailed evidence has been furnished on what is actually happening in managerial labor markets during transition. For most countries, the focus has been on aspects of corporate governance. Most studies (e.g. Ash and Hare (1994) and Blasi (1995) for Russia) find that even where there has been mass privatization, relative to other stakeholders, managers have consid- erable power. Arguably this is more than is usually held to be appropriate for the proper functioning of a market economy (Nuti, 1995). For Bulgaria, where privatization has been quite limited (Jones and Rock, 1994), evidence also suggests that in the typical firm managers exercise enormous influence (Jones, 1995). 2

However, both the conventional wisdom about the way the managerial labor market was thought to operate in a STE, as well as beliefs about changes in practice during early transition, typically are based on limited evidence. Often these are case studies (e.g. the studies by Lawrence et al. (1990) for Russia) or surveys that may not be representative of general trends (e.g., Jones et al. (1995) for Bulgaria and Linz, 1995 for Russia). In any event, there do not appear to be any recent applied studies that formally test hypotheses about managerial labor markets in transitional economies. 3

2 For both Russia (Jones and Weisskopf, 1996) and Bulgaria (Jones, 1995) managers of private firms do not seem to have more influence than do managers of state firms.

3 For China, Groves et al. (1995) provide the first econometric evidence on the nature of its managerial labor market.

D. C. Jones, T. Kato / Labour Economics 3 (1996) 319-336 323

3. The data

To help to improve our limited knowledge in the general area of executive pay, this study uses data from what is one of the first probability panel data sets for transitional economies. This panel data set was assembled by merging three data bases: (i) the Bulgarian Management Survey (BMS); (ii) the Bulgarian Economic Survey (BES); and (iii) the Bulgarian Labor Flexibility Survey (BLFS). The BLFS was a project sponsored by the ILO to assess microeconomic changes in labor practices in Bulgarian industry. The BLFS involved 490 establishments, selected to ensure a nationally and sectorally representative sample. Specifically, the population was defined as all state-owned (in 1989) Bulgarian manufacturing organizations (SOEs) that operated in the so-called 'productive' sector 4 and had more than 80 employees in 1992, the year of the first wave of data collection.

The sampling design for enterprises operated at two levels. First, five groups of the 320 municipal districts in Bulgaria were selected on the bases of geographic and urban variability, reproducing aggregate country-wide industry distributions, and minimizing data collection costs (Sofia, Pernik, Pleven, Burgas and Plovdiv). Second, within each of the five regions, population enumeration lists of SOEs were compiled by the Central Statistical Bureau. The number of sampled firms per region was set to reproduce the population proportions of firms per region in 1989 (the first year for which data were gathered). The five regions contained a population of 727 SOEs. Within each region, within major industry categories, firms were ordered by size and the approximate two-thirds largest were selected up to the sample size of 490. Thus the sample contains 69% of the population of firms, but selected to reproduce population distributions by region and industry. In terms of employment, the sample SOEs contain about 95% of all SOE employees in the five regions in 1989.

The BMS collected survey data from the chief executive officers in the same 490 Bulgarian firms. A wide variety of questions were asked including informa- tion about chief executives, including pay and the method and terms of appoint- ment. Data were also gathered concerning some finn characteristics, for example the form of enterprise ownership. By comparison, the focus of the BES was the collection of detailed financial balance sheet and income statement data. These data in the BES include measures of size, productivity, and profitability. By merging the three data bases there are 203 firms for which complete information on all the variables used in the econometric analysis for each year from 1989 through 1992 are available. 5

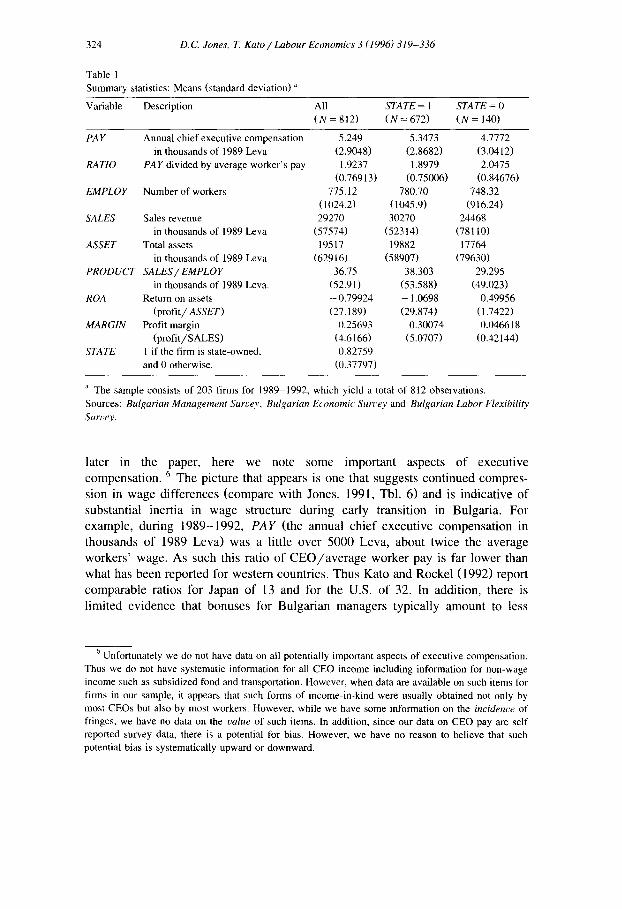

While descriptive statistics (as reported in Table 1) will be discussed more fully

4 In STEs 'productive' output mainly comprised produced tangible goods. Most services, e.g. health, education and administration, were regarded as non-productive.

5 The reduction in sample size is entirely due to lack of availability of some of the variables.

324 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

Table 1 Summary statistics: Means (standard deviation) '~

Variable Description All STATE = I S T A T E = 0

(N = 812) (N = 672) (N = 140)

PAY Annual chief executive compensation 5.249 5.3473 4.7772 in thousands of 1989 Leva (2.9048) (2.8682) (3.0412)

RATIO PAY divided by average worker's pay 1.9237 1.8979 2.0475 (0.76913) ( 0 . 7 5 0 0 6 ) (0.84676)

EMPLOY Number of workers 775.12 780.70 748.32 (1024.2) (1045.9) (916.24)

SALES Sales revenue 29270 30270 24468 in thousands of 1989 Leva (57574) (52314) (78110)

ASSET Total assets 19517 19882 17764 in thousands of 1989 Leva (62916) (58907) (79630)

PRODUCT SALES~EMPLOY 36.75 38.303 29.295 in thousands of 1989 Leva. (52.91) (53.588) (49.023)

ROA Return on assets -0.79924 - 1.0698 0.49956 (profit/ASSET) (27.189) (29.874) (1.7422)

MARGIN Profit margin 0.25693 0 .30074 0.046618 (profit/SALES) (4.6166) (5.0707) (0.42144)

STATE 1 if the firm is state-owned, 0.82759 and 0 otherwise. (0.37797)

a The sample consists of 203 firms for 1989-1992, which yield a total of 812 observations. Sources: Bulgarian Management Surt,ey, Bulgarian Economic Sun:ey and Bulgarian Labor Flexibili~' Surz,ey.

later in the paper, here we note some impor tan t aspects o f execut ive

compensa t ion . 6 The picture that appears is one that sugges ts con t inued compres -

sion in wage d i f fe rences (compare wi th Jones, 1991, Tbl. 6) and is indicat ive of

substantial inertia in wage structure during early t ransi t ion in Bulgaria. For

example , dur ing 1989-1992 , P A Y (the annual ch ie f execut ive compensa t ion in

thousands o f 1989 Leva) was a little over 5000 Leva, about twice the average

workers ' wage. As such this ratio of C E O / a v e r a g e worker pay is far lower than

what has been repor ted for wes tern countr ies . Thus Kato and Rockel (1992) report

comparab le ratios for Japan o f 13 and for the U.S. o f 32. In addit ion, there is

l imited ev idence that bonuses for Bulgarian managers typically amount to less

6 Unfortunately we do not have data on all potentially important aspects of executive compensation. Thus we do not have systematic information lbr all CEO income including information for non-wage income such as subsidized food and transportation. However, when data are available on such items for firms in our sample, it appears that such forms of income-in-kind were usually obtained not only by most CEOs but also by most workers. However, while we have some information on the incidence of fringes, we have no data on the ealue of such items. In addition, since our data on CEO pay are self reported survey data, there is a potential for bias. However, we have no reason to believe that such potential bias is systematically upward or downward.

D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336 325

than 30 percent of total pay (Jones et al., 1995). Hence, the differences in the total remuneration ratios between Bulgaria and Western countries may be even greater than these comparisons based on pay alone suggest. Note also that executive pay in state firms is on average higher than executive pay in corporatized firms (by about 12 percent).

While data collection for this panel of firms is an on-going exercise, in this study we use data derived for the years 1989-1992. These data were gathered in the first two waves of data collection. The first wave was administered during 1992. Then data were assembled for 1991 (the most recent year for which annual economic information were available) as well as (retrospectively) for 1990 and 1989. In the second wave of data collection in 1993, comparable information were collected for 1992.

4. Determinants of executive compensation

4.1. Considering only size and standard performance measures

We begin with the simplest specification typically used in studies of executive compensation of western firms:

ln( PA Yit) = fl ln( SlZEit) + y PERFORMaNCEit + oti + "r, + uit (1)

where PAYit = chief executive pay of firm i in year t; SIZEit = size of firm i in year t; PERFORMANCE~t = standard firm performance measures such as stock market returns and various accounting profitability measures of firm i in year t; c~ i = firm specific fixed effects; and ~'t = year effects. For the disturbance term, uit, we assume ui, ~ NID(0, o,2).

SIZE and PERFORMANCE are standard variables that have been included in prior empirical studies of executive compensation in the U.S., the U.K., Japan and other advanced market economies. 7 PERFORMANCE is measured either by stock market returns or by various accounting measures such as ROA (Return On Assets), and is almost always included as a possible determinant of executive compensation in the literature. This reflects the fact that the application of the principal-agent theory to the design of executive compensation contracts in general predicts a positive correlation between managerial pay and some observ- able measures of the well-being of shareholders. However, while most studies do

7 Ehrenberg and Milkovich (1987) and Rosen (1990) provide thorough reviews of the large body of evidence on U.S. executive compensation. Evidence on other countries is relatively scarce. For recent evidence on the U.K., see Main (1991), Gregg et al. (1993), Conyon and Gregg (1993). For evidence on Japan, see Kato and Rockel (1992), Kaplan (1994), Ang and Constand (1993), Hebner and Kato (1994), Kato (1994). For evidence on Spain, see Angel and Fumas (1994).

326 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

find a significant positive correlation between pay and performance, the correla- tion is often very small in magnitude and thus difficult to easily reconcile with principal-agent models. Studies also find that the estimated sensitivity of pay to stock market returns is usually lower than the estimated sensitivity of pay to accounting measures. For example, Rosen (1990) in reviewing various studies finds that the effects on log of pay of the rate of return to shareholders are in the 0.10-0.15 range, whereas the estimated sensitivity of pay to accounting measures are in the 1.0-1.2 range. For our study, only accounting profitability measures such as ROA are used since stock market measures are irrelevant to STEs in transition like Bulgaria. 8

SIZE, measured either by total assets, by sales or by employment, is also often considered in the literature. Typically this reflects the fact that the executive compensation literature began as a result of the early managerialist debates over the firm objective (sales versus profits). Most studies find significant positive correlations between size and pay. Again, Rosen (1990) in summarizing findings on the estimated elasticities of pay with respect to scale finds a typical value of about 0.25. SIZE (more specifically employment) may be particularly relevant to STEs. Under communism, being a chief executive of a larger firm with many more employees arguably means more political power, and thus an improved ability to obtain higher pay from the state.

We use a two-way fixed effects model. Year dummy variables (L) are included to capture technological change and other shocks that are common to all firms as well as possible measurement errors of inflation. Firm specific fixed effects ( a i) are included to capture time invariant firm specific factors that may affect chief executive pay. 9 Since all chief executives in our estimates have been chief executives at the same firm from 1989 through 1992, firm specific fixed effects include, for instance, managerial style/corporate strategy and innate ability of chief executives. ~0

We estimate Eq. (1) by merging data from the aforementioned three surveys (the BMS, the BLFS, and the BES). For 1989 through 1992, we successfully

8 Since the accounting practices used in pre-transition Bulgaria differ from conventional approaches used in the west, potentially there are many difficulties in using standard accounting measures of explanatory variables such as profitability and assets. However, in some work, measures of key variables have been adapted to the special circumstances of transition economies. For example Pinto et al. (1993) construct several measures of 'profitability'. In this paper we follow this literature and construct similar measures.

9 F tests refute the joint exclusion of year dummy variables and firm specific fixed effects at the 5 percent level for all specifications reported in the paper.

10 This absence of managerial turnover stands in stark contrast to the situation in advanced market economies where managerial turnover is often quite substantial (see, for instance, Kaplan (1994, p. 522).

D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336 327

assembled a balanced four-year panel of 203 firms. Descriptive statistics for key variables are summarized in Table 1, where all value variables are in 1989 leva. ll

Our data allow us to use three alternative size measures: (i) E M P L O Y (number of workers); (ii) SALES ( income from sales in thousands of 1989 leva); and (iii) ASSET (the total assets in thousands of 1989 leva). Our preferred size measure in the context of transitional economies is EMPLOY. First, the political power of the chief executive may be posit ively correlated with the number of his or her workers. The determination of chief executive pay may be highly political, especially for those state-controlled firms. If so, employment may be the most relevant size measure. In addition, for reasons such as the reliabili ty of asset valuation during transition, employment measure may be subject to less measure- ment error than other size measures. Table 1 shows that our sample of firms are quite large (for instance, the average f inn employs almost 800 workers.)

For PERFORMANCE, as mentioned above, we are not faced with the standard issue of stock market versus accounting measure simply because the stock market measures are irrelevant to the Bulgarian economy for the period under considera- tion. We use two standard accounting measures of profitability: (i) ROA (Return On Assets), defined as gross profit divided by total assets; and (ii) MARGIN (profit margin), defined as gross profit divided by sales. The average ROA is negative whereas the average MARGIN is positive. A closer look at the data reveals that this discrepancy was caused in large part by a sharp drop in profits in 1992 for those firms with small assets. When one uses MARGIN, however, the opposite pattern appears. Though we are not entirely sure how to interpret this discrepancy, it clearly points to the importance of sensitivity analysis to identify how responsive the results are to the selection of the performance measure.

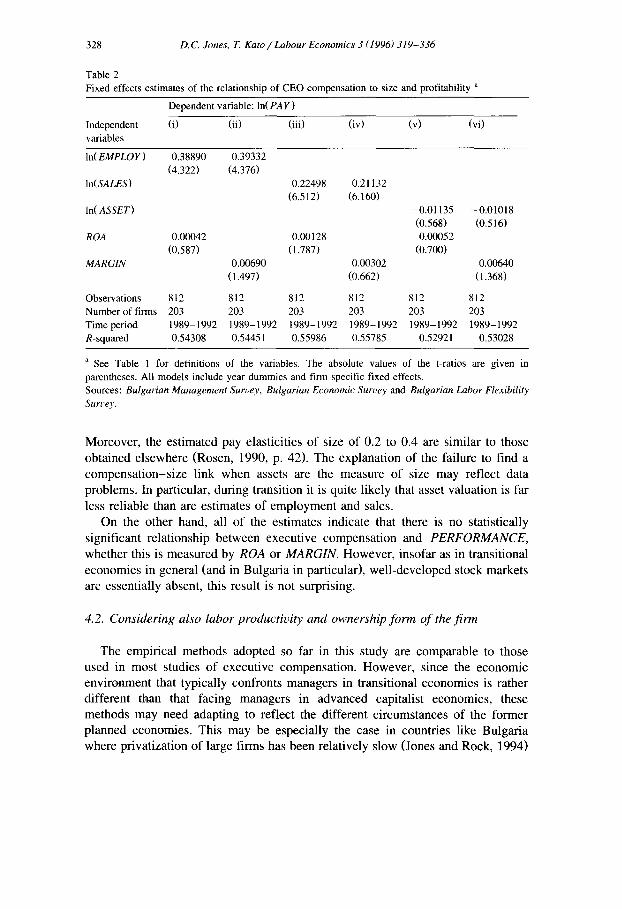

We estimated six specifications of Eq. (1), depending on the selection of the size measure and the performance measure. Columns (i) and (ii) of Table 2 show the results when E M P L O Y is used as a size measure. Likewise, columns (iii) and (iv) present the results when SALES measures size and columns (v) and (vi) show the results when ASSET is the size measure. Columns (i), (iii) and (v) show the results when ROA is used as a performance measure whereas columns (ii), (iv) and (vi) present the results when MARGIN is the measure of performance.

When size is measured by employment or sales, we find evidence of a positive and highly significant relationship between chief executive pay and firm size. These results are not sensitive to the choice of the PERFORMANCE variable.

1~ Data series for countries in transition have well-known problems and estimates of key series such as the CPI often differ, especially for the fading days of communism. For the results presented in the paper, the PPI from PLANECON is used to deflate sales and productivity, whereas the CPI from PLANECON is used to deflate executive pay and assets. However, since all price indices are aggregate price indices and the same for all firms in a given year, the price indices simply add a constant to log variables that is picked up by our year dummy variables. Thus, insofar as Eq. (1) is concerned, the results do not depend on the choice of price indices.

328 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

Table 2 Fixed effects estimates of the relationship of CEO compensation to size and profitability a

Dependent variable: In( PAY )

Independent (i) (ii) (iii) (iv) (v) (vi) variables

In(EMPLOY) 0,38890 0.39332 (4,322) (4.376)

In(SALES) 0.22498 0.21132 (6.512) (6.160)

In(ASSET) -0.01135 -0.01018 (0.568) (0.516)

ROA 0.00042 0.00128 0.00052 (0.587) (1.787) (0.700)

MARGIN 0.00690 0.00302 0.00640 (1.497) (0.662) (1.368)

Observations 812 812 812 812 812 812 Number of firms 203 203 203 203 203 203 Time period 1989-1992 1989-1992 1989-1992 1989-1992 1989-1992 1989-1992 R-squared 0.54308 0.54451 0.55986 0.55785 0.52921 0.53028

a See Table 1 for definitions of the variables. The absolute values of the t-ratios are given in parentheses. All models include year dummies and firm specific fixed effects. Sources: Bulgarian Management Survey, Bulgarian Economic Survey and Bulgarian Labor Flexibility Survey.

Moreover, the estimated pay elasticities of size of 0.2 to 0.4 are similar to those obtained elsewhere (Rosen, 1990, p. 42). The explanation of the failure to find a compensation-size link when assets are the measure of size may reflect data problems. In particular, during transition it is quite likely that asset valuation is far less reliable than are estimates of employment and sales.

On the other hand, all of the estimates indicate that there is no statistically significant relationship between executive compensation and PERFORMANCE, whether this is measured by ROA or MARGIN. However, insofar as in transitional economies in general (and in Bulgaria in particular), well-developed stock markets are essentially absent, this result is not surprising.

4.2. Considering also labor productivity and ownership form of the firm

The empirical methods adopted so far in this study are comparable to those used in most studies of executive compensation. However, since the economic environment that typically confronts managers in transitional economies is rather different than that facing managers in advanced capitalist economies, these methods may need adapting to reflect the different circumstances of the former planned economies. This may be especially the case in countries like Bulgaria where privatization of large firms has been relatively slow (Jones and Rock, 1994)

D.C. Jones, T. Kato / Labour Economics 3 (l 996) 319-336 329

and where capital markets are embryonic. In particular, in the face of transition and eventual privatization, increasing labor productivity (via labor shedding and/or increased work intensity) may be a prime goal of the firm and their chief executives. Hence, measures of firm performance other than those customarily used in studies of executive compensation may be relevant. Thus, we consider labor productivity, PRODUCT as an alternative firm performance measure.

Furthermore, to test whether movements away from complete state ownership of firms influences executive compensation, we create a dummy variable, STATE, t, which takes a value of one if the firm is directly and solely owned by governments (central and municipal), and zero otherwise. Other forms of ownership include private (limited or unlimited liability legal forms), independent cooperatives, and other joint-stock firms partly owned by governments. During 1989-1992, a significant number of firms (about 20 percent of the firms in our sample) changed ownership status from STATE = t to STATE = 0. Hence this allows us to estimate the effects on chief executive compensation of privatization and corporatization (going from STATE = 1 to STATE = 0), separate from firm specific fixed effects.

Specifically, we estimate the following augmented chief executive compensa- tion equation:

In(PaY.t) =/3 In( SIZEit ) + y PERFORMANCEi, + 6 In( PRODUCTit )

+ rl STATEi, +/3,~ STATEi, * ln(SIZEi,)

+ 3(~ STATEit * PERFORMANCEit

+ ~s STATEit * In( PRODUCTit ) + ce i + "r, + "it (2)

where PRODUCTit = labor productivity of firm i in year t. The elasticity of pay with respect to SIZE for firms with STATE = 0 (or not

state-owned) is thus given by /3 whereas the one for firms with STATE = 1 (or state-owned) is given by /3 +/3.~. Likewise, the semi-elasticity of pay with respect to PERFORMANCE for firms that are not state-owned is given by y whereas the one for state-owned firms is given by y + T~. ~2 Furthermore, the elasticity of pay with respect to PRODUCT for firms that are not state-owned is given by 6 whereas the one for state-owned firms is given by 6 + 6~. ~3

One may predict that privatization and corporatization will increase the impor- tance of firm performance measures such as profitability and productivity in the determination of executive compensation (Z, 6~ < 0) whereas decreasing the importance of more traditional, political factors such as firm size (/3~ > 0). Moreover, one may argue that increased competition introduced by privatization

12 The term, 'semi-elasticities' is from Rosen (1990). 13 One may wish to add further interaction terms involving year effects and STATE to explore

whether the timing of privatization may affect the level of chief executive compensation. Unfortu- nately, reduced degree of freedom and multicollinearity make the parameter estimates rather imprecise.

330 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

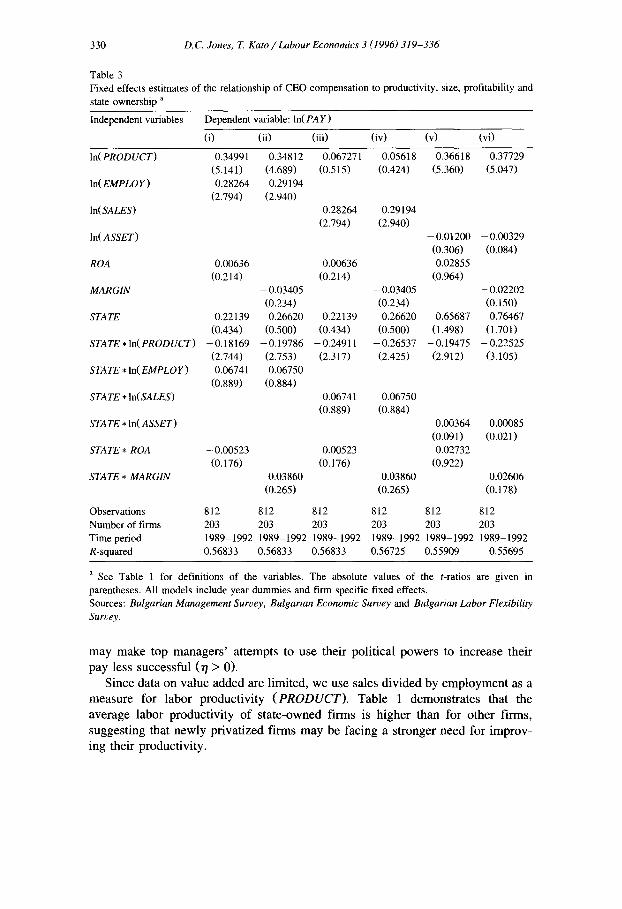

Table 3 Fixed effects estimates of the relationship of CEO compensation to productivity, size, profitability and state ownership a

Independent variables Dependent variable: In(PAY)

(i) (ii) (iii) (iv) (v) (vi)

In(PRODUCT) 0.34991 0.34812 (5.141) (4.689)

In(EMPLOY) 0.28264 0.29194 (2.794) (2.940)

In(SALES)

In(ASSET)

ROA 0.00636 (0.214)

MARGIN - 0.03405 (0.234)

STATE 0.22139 0.26620 (0.434) (0.500)

STATE*In(PRODUCT) -0.18169 -0.19786 (2.744) (2.753)

STATE*In(EMPLOY) 0 .06741 0.06750 (0.889) (0.884)

STATE * In(SALES)

STATE * In(ASSET)

STATE * ROA - 0,00523 (0,176)

STATE * MARGIN

Observations Number of firms Time period R-squared

0.067271 0.05618 0.36618 0.37729 (0.515) (0.424) (5.360) (5.047)

0.28264 0.29194 (2.794) (2.940)

0.00636 (0.214)

-0.03405 (0.234)

0.22139 0.26620 (0.434) (0.500)

-0.24911 -0.26537 (2.317) (2.425)

-0.01200 - 0.00329 (0.306) (0.084) 0.02855

(0.964) -0.02202 (0.150)

0.65687 0.76467 (1.498) (1.701)

-0.19475 -0.22525 (2.912) (3.105)

0.06741 0.06750 (0.889) (0.884)

0.00364 0.00085 (0.091) (0.021)

-0.00523 -0.02732 (0.176) (0.922)

0.03860 0.03860 0.02606 (0.265) (0.265) (0.178)

812 812 812 812 812 812 203 203 203 203 203 203 1989-1992 1989-1992 1989-1992 1989-1992 1989-1992 1989-1992 0.56833 0.56833 0.56833 0.56725 0.55909 0.55695

a See Table 1 for definitions of the variables. The absolute values of the t-ratios are given in parentheses. All models include year dummies and firm specific fixed effects. Sources: Bulgarian Management Survey, Bulgarian Economic Survey and Bulgarian Labor Flexibility Survey.

may make top managers ' at tempts to use their poli t ical powers to increase their

pay less successful ( r / > 0).

Since data on value added are l imited, we use sales d iv ided by emp loymen t as a

measure for labor product ivi ty ( P R O D U C T ) . Table 1 demonstra tes that the

average labor product ivi ty o f s ta te-owned f irms is h igher than for other firms,

suggest ing that newly pr ivat ized f i rms may be facing a s t ronger need for improv- ing their product ivi ty.

D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336 331

Furthermore, Table 1 shows that P A Y of CEOs in state-owned firms on average is higher than the pay of other CEOs, suggesting that privatization and corporatization may be making top management ' s attempts to use their political power to raise their pay less successful. The table also shows that state-owned firms are larger than other firms, and that state-owned firms on average earn a lower ROA than other firms.

As before, we estimated six specifications of Eq. (2), depending on the selection of the SIZE measure and P E R F O R M A N C E measure. Table 3 summa- rizes the results. 14 Perhaps the most noteworthy and consistent finding concerns the link of executive compensation to productivity ( P R O D U C T ) . Except when size is measured by sales, we find a positive and significant link between CEO pay and productivity. This relationship is not sensitive to the selection of the PER-

F O R M A N C E variable. The estimated elasticities of pay with respect to productiv- ity are rather substantial, ranging from 0.35 to 0.38 (or a 10 percent increase in productivity will result in a almost 4 percent increase in CEO pay). As shown below, the estimated elasticities of pay with respect to productivity is similar or slightly higher than the estimated elasticities of pay with respect to size.

Furthermore, for all specifications, we consistently find negative and significant coefficients on the interaction term involving STATE and In(PRODUCT) . In other words, the link between executive compensation and productivity is significantly weaker for state-owned firms than for other firms. In turn, compared to top executives in privatized and corporatized firms, this points to a weaker incentive for CEOs in state-owned firms to engage in rational downsizing and productivity increases. 15

Turning to the p a y - s i z e link, we continue to find evidence of a positive and significant relationship between CEO compensation and firm size except for when size is measured by assets. 16 These results are again not sensitive to the choice of the P E R F O R M A N C E variable. Furthermore, the estimated size elasticity of around 0.3 is again similar to those obtained in advanced market economies (Rosen, 1990, p. 42).

From Table 3 we also see that, in all estimates, the estimated coefficients on the interaction terms involving STATE and SIZE are never significantly different from

14 F tests refute the join exclusion of the interactive terms (or /3~, 3(,, and 6~ = 0) at the 5 percent level for all six specifications reported in Table 3.

15 There is a problem of possible endogeneity of some of the regressors (in particular, STATE and PRODUCT). A common response to that problem is to perform an estimation using instrumental variables; unfortunately, no suitable instruments were available. Very little attempt has been made to account for the possible endogeneity of the regressors in the literature of executive compensation in advanced market economies.

16 Since In(PRODUCT) is equal to In(SALES)- In(EMPLOY), the estimated coefficients in specifi- cation (i) in Table 3 are the same as those in (iii), except for In(PRODUCT) and STATE * In(PROD- UCT). Likewise, the estimated coefficients in (ii) are identical to those in (iv) except for In(PROD- UCT) and STATE * In(PRODUCT).

332 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

zero. As such, this finding implies that there is no evidence that the pay-s ize sensitivity is different for firms that are completely state owned and those firms that are either privatized or corporatized.

In turn, the findings on performance (measured by profitability) and on labor productivity, together suggest that during early transition the measure of firm performance that is more relevant in influencing executive compensation appears to be productivity rather than profitability.

The last findings we examine concern the role of different forms of ownership. Here we note that the estimated coefficients on STATE are always positive. This suggests that competition introduced by movement away from traditional struc- tures of state ownership towards corporatization and full privatization may be making top management ' s attempts to use their power to raise their pay less successful. However, except for estimates for one specification (reported in column vi), typically the estimated coefficients are not very significant. Substitut- ing the estimates of r/, f3~, %, and ¢5~ and the mean values for In(SIZE), P E R F O R M A N C E , and I n ( P R O D U C T ) into t 1 + [35 I n ( S I Z E ) + % PERFORMANCE + 6~ In(PRODUCT), and using a simple formula, [exp{~7 + t~In(SIZE) + %PERFORMANCE + 6~in(PRODUCT)} - 1] × 100, the sizes of the impact of STATE on PAY are estimated to be 7.890, 7.942, 7.888, 7.939, 10.977, and 7.738 percent, respectively. In other words, privatization is estimated to reduce chief executive pay by 8 to 11 percent, other things being equal.

Finally, we report briefly the results of additional sensitivity analyses. First, unlike in the simpler specifications with no interactive terms, the price index does matter when the deflated variables are multiplied by STATE. To see if our key results are sensitive to the particular CPI that is used to deflate executive pay and assets, we used an alternative CPI (from UNICEF) instead of the CPI from PLANECON. Reassuringly this alternative procedure did not produce any appre- ciable difference in results. For instance, when firm size is measured by employ- ment and assets, the est imated coefficients on I n ( P R O D U C T ) and STATE * In (PRODUCT) were again found positive and significant, and negative and significant, respectively. Specifically, the estimated coefficients on In(PROD- UCT) and STATE * In (PRODUCT) (and the absolute values of t-ratios in paren- theses) are as follows: with specification (i), 0.34989 (5.141) and -0 .18167 (2.744); with specification (ii), 0.34810 (4.689) and - 0 . 1 9 7 8 4 (2.752); with specification (v), 0.36978 (5.419) and -0 .20029 (2.982); and with specification (vi), 0.38241 (5.106) and -0 .23197 (3.177). tv

iv We also repeated the same analysis: (i) using CPI from PLANECON to deflate all variables; (ii) using CPI from UNICEF to deflate all variables; and (iii) using PPI to deflate all variables. When firm size is measured by employment and assets, the estimated coefficients on In(PRODUCT) and STATE *In(PRODUCT) were always found positive and significant, and negative and significant, respectively.

D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336 333

The second set of sensitivity analyses were undertaken to see if our results are sensitive to the choice of the profit measure. Here we attempted to use net profit instead of gross profit. Unfortunately, data on net profit are far less consistently provided for sample firms than are data on gross profit. Hence the use of net profit results in a rather drastic reduction of the sample size (from 812 to 232). In spite of the substantially reduced sample size, when firm size is measured by employ- ment and assets, the estimated coefficients on In(PRODUCT) and STATE * In (PRODUCT) were again found positive and significant, and negative and significant, respectively. Specifically, the estimated coefficients on In( PROD-

UCT) and STATE * In (PRODUCT) (and the absolute values of t-ratios in paren- theses) are as follows: with specification (i), 0.68140 (3.162) and -0.49669 (2.745); with specification (ii), 0.60492 (2.865) and -0.44459 (2.440); with specification (v), 0.74560 (3.540) and -0.55410 (3.163) and with specification (vi), 0.68662 (3.319) and -0.50846 (2.875).

5. Summary and implications

Using a probabilistic panel survey of firms with matching information for chief executives, we estimate two-way fixed effects models and present the first econometric evidence for a transitional economy on the determinants of chief executive compensation. We estimate both specifications similar to those used in studies of managers in western countries and specifications that have been adapted by the inclusion of an altemative measure of firm performance to reflect the special circumstances of transitional economies.

Using specifications similar to those typically employed in executive compensa- tion studies, CEO pay is found to be positively related to size (measured by employment and sales), but not to profitability (measured by return on assets and the profit margin). In specifications adapted to the special circumstances facing transitional economies, CEO compensation is found to be positively related to size and productivity.

The estimated pay elasticities of size of around 0.3 are comparable to what has been found for firms in advanced market economies. The estimated pay elasticities of productivity are equal or slightly greater in size than the estimated pay elasticities of size, pointing to the importance of productivity as a prime determi- nant of chief executive compensation in transitional economies.

Another important finding is that the link of CEO pay to productivity is stronger in firms that are either privatized or corporatized than in firms that remain completely state-owned and controlled. The finding is found consistently for all six specifications which use different measures of size and performance.

The strong pay-size relationships, coupled with the absence of pay-profitabil- ity relationships, suggest that executive compensation is still largely structured so

334 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

as to provide incentives for managers to increase size (or resist downsizing) and to pay no attention to profitability. On the other hand, the equally strong pay-produc- tivity relationships point to the existence of incentives for managers to increase productivity (or slow down the deterioration of productivity).

Finally, the stronger pay-productivity relationship for firms that are not state owned suggests that, as privatization progresses, top managers may become more productivity-oriented. This result is especially intriguing as Bulgaria begins to embark on a mass-privatization program. In early transition, which we study in the paper, productivity turns out to be still lower in corporatized firms, pointing to stronger demand for productivity increases, The greater link of CEO pay to productivity in corporatized firms is consistent with a bigger demand for produc- tivity increases in these firms. As privatization progresses, we predict that the stronger productivity link in privatized firms will lead to more rapid productivity growth. This will eventually make productivity in these firms higher than in state firms, and the productivity link effect will make CEO pay in privatized firms higher than in state firms. To test this prediction will require additional and more recent waves of data.

More broadly, our findings have relevance for debates concerning whether significant behavioral change is possible in firms and key economic agents in transitional economies without widespread privatization. We find that there is evidence of such changes in the forces influencing executive compensation. This finding that change is possible without widespread privatization is consistent with findings in other areas for Bulgaria including wage determination (Jones and Ilayperuma, 1994) and employment dynamics as well as for other transitional countries on issues including firm adjustment (e.g. Pinto et al. (1993) for Poland). However, as with these other studies we also find evidence of substantial inertia, in this case in the forces influencing executive compensation.

At the same time we recognize that this is an area where more research is needed. In this fast changing context, especially as privatization becomes more widespread, there is a need to continue to undertake similar exercises using more current data. In addition there is a need for research which examines whether our findings change as additional information on characteristics of executive compen- sation become available. For example, the available survey data mean that in this paper we are unable to address matters concerning the structure of CEO pay. This is a potentially important issue since other information for Bulgaria suggests that typically bonuses account for no more than about 30% of total pay during the period under examination (Jones et al., 1995). This is a much lower proportion than for top executives in western firms. Future work will use additional waves of data and investigate more diverse aspects of executive compensation such as the structure of executive pay. In future work we also plan to address several other issues. For example, by estimating regressions which include industry average labor productivity, we will investigate whether Bulgarian managers are rewarded based on the performance of their firm compared to firms in the same industry.

D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336 335

Acknowledgements

Jones acknowledges support from NSF 9010591 and Jones and Kato acknowl- edge support from the National Council for Soviet and East European Research. Kato also acknowledges support from the Jerome Levy Economics Institute. Brandon Weber and Mike Shino provided excellent research assistance. An earlier version of the paper was presented at the 1995 Allied Social Science Associations Meetings, Washington, D.C., January 6-8, 1995. The authors are grateful for comments from: participants at those meetings, especially John Haltiwanger and John Micklewright; Jeffrey Pliskin; and three anonymous referees.

References

Aghion, P., O. Blanchard and S. Burgess, 1994, The behavior of state firms in eastern Europe, pre privatization, European Economic Review 38, 1327-1349.

Ang, S. James and Richard L. Constand, 1993, Compensation and performance: The case of Japanese managers and directors, Paper presented at the Fifth Annual PACAP Finance Conference in Kuala Lumpur, Malaysia.

Angel, Pedro Ortin and Vicente Salas Fumas, 1994, Size of the firm and managerial compensation in Spanish corporations, International Journal of Industrial Organization, forthcoming.

Ash, Timothy and Paul Hare, 1994, Privatization in the Russian Federation: Changing enterprise behavior in the transition period, Cambridge Journal of Economics 18, 619-634.

Berliner, Joseph S., 1957, Factory and manager in the USSR (Harvard University Press, Cambridge, MA).

Blasi, Joseph, 1995, Russian labor-management relations: Some preliminary lessons from newly privatized enterprises, Proceedings of the 47th Annual Meeting of the Industrial Relations Research Association, 225 -234.

Bonin, John, 1976, On the design of managerial incentive systems in a decentralized planning environment, American Economic Review 66, 682-687.

Campbell, Robert W., 1991, The socialist economies in transition (Indiana University Press, Blooming- ton, IN).

Chapman, Janet G., 1979, Recent trends in Soviet industrial wage structure, In: A. Kahan and B. Ruble, eds., Industrial labor in the USSR (Pergamon, Oxford) 151-183.

Conyon, Martin J. and Paul Gregg, 1993, Pay at the top: A study of the sensitivity of top director remuneration to company specific shocks, International Journal of Industrial Organization, forth- coming.

Ehrenberg, Ronald G. and G.T. Milkovich, 1987, Compensation and firm performance, In: Morris Kleiner et al., eds., Human resources and the performance of the firm (Industrial Relations Research Association, Madison, WI) 87-122.

Estrin, Saul, Alan Gelb and Inderjit Singh, 1995, Shocks and adjustment by firms in transition: A comparative study, Journal of Comparative Economic Systems 21, 131-153.

Granick, David, 1954, Management of the industrial firm in the USSR (Columbia University Press, New York).

Gregg, P., S. Machin and S. Szymanski, 1993, The disappearing relationship between directors pay and corporate performance, British Journal of Industrial Relations 31, 1-10.

Groves, Theodore, Yongmiao Hong, and et al., 1995, China's evolving managerial labor market, Journal of Political Economy 103, 873-892.

336 D.C. Jones, T. Kato / Labour Economics 3 (1996) 319-336

Hebner, Kevin J. and Takao Kato, 1994, Insider trading and executive compensation: Theory and evidence from the U.S. and Japan, International Review of Economics and Finance, forthcoming.

Ickes, Barry and L. Samuelson, 1987, Job transfers and incentives in complex organizations: Thwarting the ratchet effect, Rand Journal of Economics 18, 275-286.

Jones, Derek C., 1991, The Bulgarian labour market in transition, International Labour Review 130, 211-226.

Jones, Derek C., 1995, Employee participation during the early stages of transition: Evidence from Bulgaria, Economic and Industrial Democracy 16, 1l 1-135.

Jones, Derek C. and Kosali llayperuma, 1994, Wage determination under plan and early transition: Evidence from Bulgaria, Working paper no. 94/5 (Hamilton College, Clinton, NY).

Jones, Derek C. and Charles Rock, 1994, Privatization in Bulgaria, In: Saul Estrin, ed., Privatization in central and eastern Europe (Longmans, London).

Jones, Derek C. and Tom Weisskopf, 1996, Employee ownership and control: Evidence from Russia, Proceedings of the Forty Eight Meeting of the Industrial Relations Research Association, forthcom- ing.

Jones, Derek C., Takao Kato and Svetlana Avramov, 1995, Managerial labor markets in transitional economies: Evidence from Bulgaria, International Journal of Manpower 16, 14-24.

Kaplan, S., 1994, Top executive rewards and firm performance: A comparison of Japan and the U.S., Journal of Political Economy 102, 510-546.

Kato, Takao, 1994, Chief executive compensation and corporate groups in Japan: New evidence from micro data, International Journal of Industrial Organization, forthcoming.

Kato, Takao and Mark Rockel, 1992, Experiences, credentials and compensation in the Japanese and U.S. managerial labor markets: Evidence from new micro data, Journal of the Japanese and International Economies 6, 30-51.

Kornai, Janos, 1992, The socialist system (Princeton University Press, Princeton, NJ). Lawrence, Paul R., Charalambos A. Vlachoutsicos et al., eds., 1990, Behind the factory walls (Harvard

Business School Press, Boston, MA). Linz, Susan, 1988, Managerial autonomy in Soviet firms, Soviet Studies 40, 175-195. Linz, Susan, 1995, Russian labor market in transition, Economic Development and Cultural Change,

693-716. Litwack, J., 1991, Discretionary behavior and Soviet economic reform, Soviet Studies 43, 255-279. Main, B., 1991, Top executive pay and performance, Managerial and Decision Economics 12,

219-229. Nuti, Mario, 1995, Employeeism: Corporate governance and employee ownership in transitional

economies, Mimeo. (London Business School, London). Pinto, Brian, Marek Belka and Stefan Krajewski, 1993, Transforming state enterprises in Poland,

Brookings Papers on Economic Activity, no. 1, 213-270. Putterman, Louis, 1993, Division of labor and welfare: An introduction to economic systems (Oxford

University Press, New York). Roland, Gerard and Khalid Sekkat, 1992, Market socialism and the managerial labor market,

Discussion paper no. 655 (Centre for Economic Policy Research, London). Rosen, Sherwin, 1990, Contracts and the market for executives, Working paper no. 3542 (NBER,

Cambridge, MA). Weitzman, Martin, 1976, The new Soviet incentive model, Bell Journal of Economics 7, 252-257.

Related Documents

![Telecommunications Legislation in Transitional and ...€¦ · Telecommunications Legislation in Transitional and Developing ]Economies Tim Schwarz David Satola ... Frequency allocation](https://static.cupdf.com/doc/110x72/5e8fc92ba2894628734abd11/telecommunications-legislation-in-transitional-and-telecommunications-legislation.jpg)