The Credit Rating Agencies Between Crisis and Resurrection of International Finance Problems and Perspectives by Giovanni Ferri & Punziana Lacitignola (University of Bari – Italy) [Lezione 10 del corso di Economia delle scelte di portafoglio] Presentation largely drawn on Ferri- Lacitignola Le agenzie di rating tra crisi e rilancio della finanza globale, Bologna, Il Mulino, 2009.

The Credit Rating Agencies Between Crisis and Resurrection of International Finance Problems and Perspectives by Giovanni Ferri & Punziana Lacitignola.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Credit Rating Agencies Between Crisis and Resurrection of International Finance

Problems and Perspectives

by Giovanni Ferri & Punziana Lacitignola

(University of Bari – Italy)[Lezione 10 del corso di Economia delle scelte di portafoglio]

Presentation largely drawn on Ferri-Lacitignola Le agenzie di rating tra crisi e rilancio della finanza globale, Bologna, Il Mulino, 2009.

2

Key Questions in Presentation:

Why are Credit Rating Agencies (CRAsCRAs) key to capital markets? Set up (industry structure & regulation) of the Global CRAsGlobal CRAs

(Moody’s; S&P; Fitch;DBR) Main allegationsMain allegations of the literature on GCRAsGCRAs: some are groundedsome are grounded in

the evidence Are GCRAs GCRAs enough for capital market development or do we need

Regional CRAsRegional CRAs? (Europe vs. Asia) How about GCRAsGCRAs specializing in multinationalsmultinationals & Regional CRAsRegional CRAs

in smaller-sized regional issuersregional issuers? National CRAs & the development of national financial markets CRAs responsibility and regulation matter

3

Why are CRAsCRAs key to capital markets?

RatingsRatings are an essentialessential lubricant for financial marketsfinancial markets as they reduce information asymmetryinformation asymmetry that investors undergo vis-à-vis issuers; they determine the cost of borrowing

Though perfectible (see below) ratings greatly enhance market information on issuers: unexpected rating changes affect level-volatility of bond-share price (Kliger & Sarig 2000) and credit default swaps (Hull et al. 2004; Norden and Weber 2004); bond downgrades cause negative abnormal stock returns (Dichev & Piotroski 2001, Ferri & Lacitignola, 2007)

Boot et al. (2004): in multiple equilibria states the rating is a coordinating mechanism, providing a “focal point” for firms and investors, thanks to the implicit contract relationship (monitor-renegotiate) but Carlson & Hale (2004) reach opposite conclusions

4

Set up of the Global CRAsGlobal CRAs – 1 – 1

Origin of the GCRAs Interaction with financial markets Regulatory evolution Industrial organization of GCRAs Some description of GCRAs’ ratings

Origin of the GCRAs (Sylla, 2001)

First rating in 1909 by John Moody: US financial markets needed certification after 1907 crisis

5

Set up of the Global CRAsGlobal CRAs – 2 – 2

Interaction with financial marketsTo reduce information asymmetries in financial markets, CRAs issue

credit ratings on sovereigns, other public entities, banks, corporates and structured finance (SF) products.

The rating is an estimate of the issuer’s ability to honor its future interest and capital payments

For issuers, ratings affect interest rate spreads (Ederington et al, 1987; Sy, 2002; Gonzalez at al, 2004) & the extent of available investment flows

To the latter extent, it is key whether the rating is investment grade or not (speculative grade)

Are corporate & SF ratings different? (Violi, 2004)

6

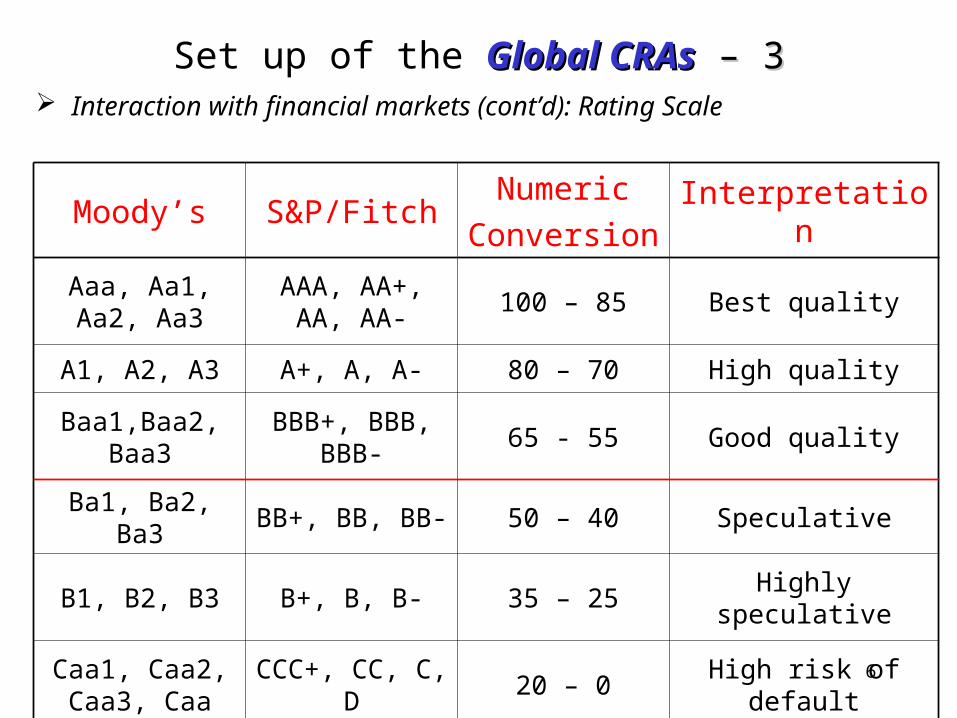

Set up of the Global CRAsGlobal CRAs – 3 – 3 Interaction with financial markets (cont’d): Rating Scale

Moody’s S&P/FitchNumeric

ConversionInterpretation

Aaa, Aa1, Aa2, Aa3

AAA, AA+, AA, AA-

100 – 85 Best quality

A1, A2, A3 A+, A, A- 80 – 70 High quality

Baa1,Baa2, Baa3BBB+, BBB,

BBB-65 - 55 Good quality

Ba1, Ba2, Ba3 BB+, BB, BB- 50 – 40 Speculative

B1, B2, B3 B+, B, B- 35 – 25 Highly speculative

Caa1, Caa2, Caa3, Caa

CCC+, CC, C, D 20 – 0 High risk of default

7

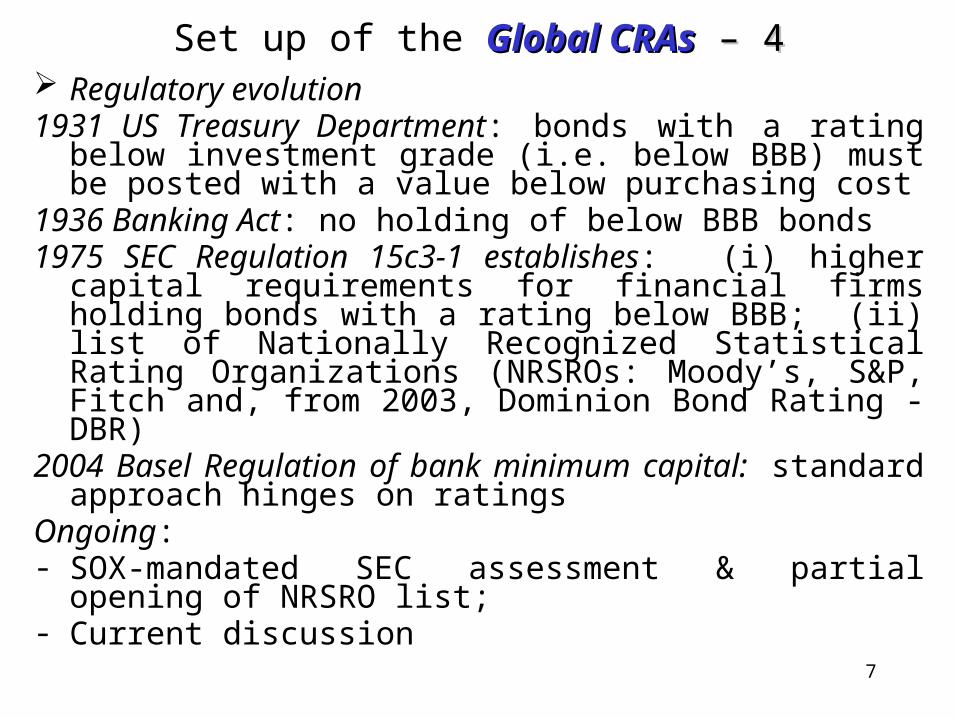

Set up of the Global CRAsGlobal CRAs – 4 – 4 Regulatory evolution1931 US Treasury Department: bonds with a rating below

investment grade (i.e. below BBB) must be posted with a value below purchasing cost

1936 Banking Act: no holding of below BBB bonds1975 SEC Regulation 15c3-1 establishes: (i) higher capital

requirements for financial firms holding bonds with a rating below BBB; (ii) list of Nationally Recognized Statistical Rating Organizations (NRSROs: Moody’s, S&P, Fitch and, from 2003, Dominion Bond Rating - DBR)

2004 Basel Regulation of bank minimum capital: standard approach hinges on ratings

Ongoing:- SOX-mandated SEC assessment & partial opening of NRSRO list;- Current discussion

8

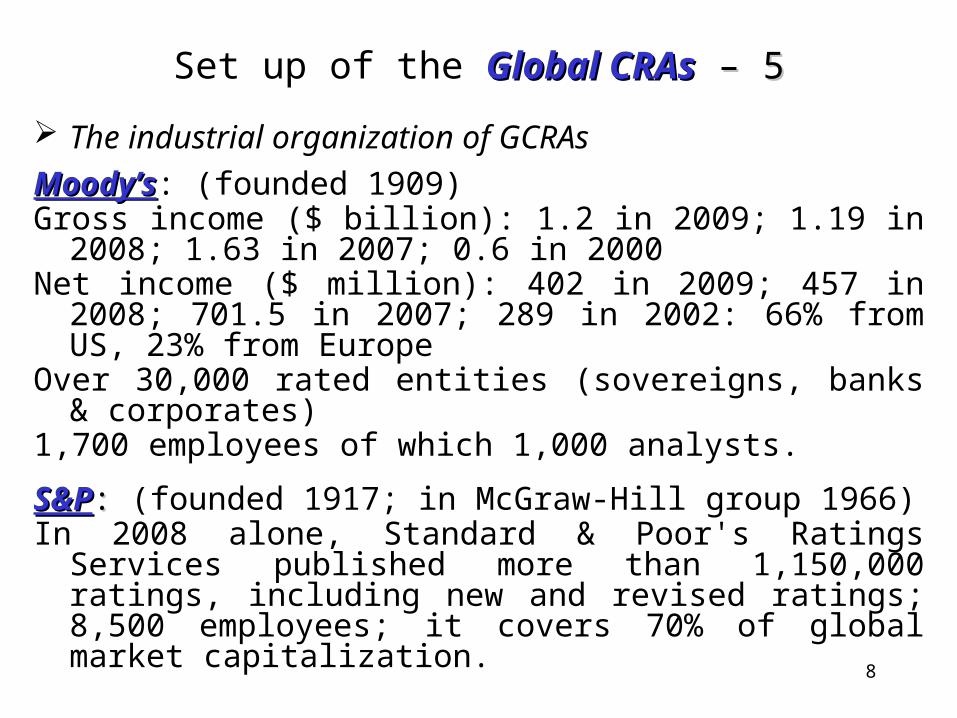

Set up of the Global CRAsGlobal CRAs – 5 – 5

The industrial organization of GCRAs

Moody’sMoody’s: (founded 1909)Gross income ($ billion): 1.2 in 2009; 1.19 in 2008; 1.63 in 2007; 0.6

in 2000Net income ($ million): 402 in 2009; 457 in 2008; 701.5 in 2007;

289 in 2002: 66% from US, 23% from EuropeOver 30,000 rated entities (sovereigns, banks & corporates)1,700 employees of which 1,000 analysts.

S&PS&P: : (founded 1917; in McGraw-Hill group 1966)In 2008 alone, Standard & Poor's Ratings Services published more

than 1,150,000 ratings, including new and revised ratings; 8,500 employees; it covers 70% of global market capitalization.

9

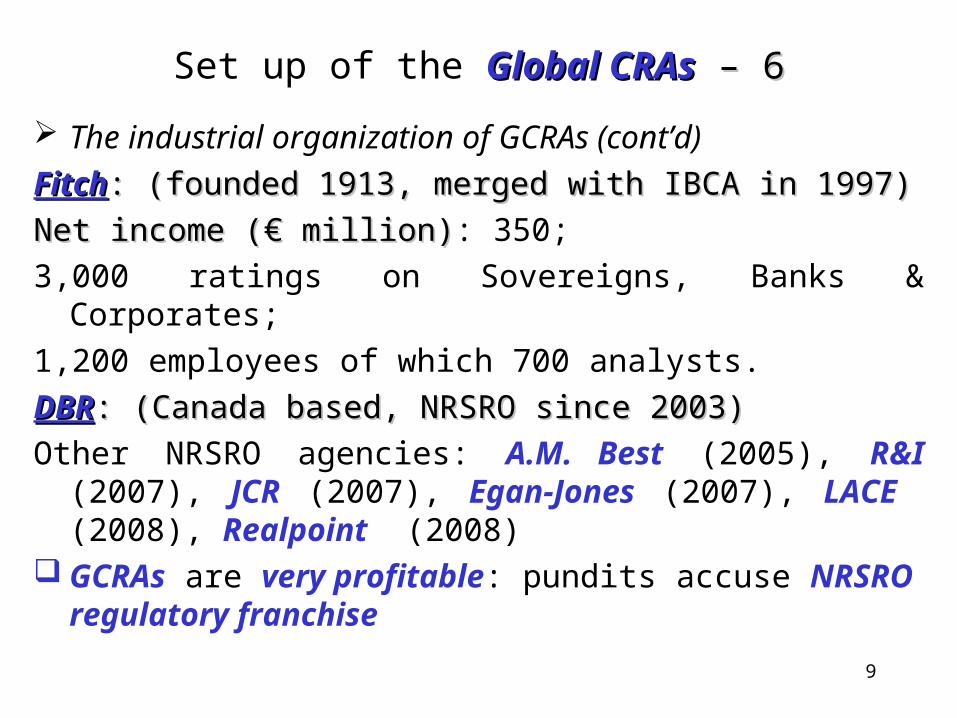

Set up of the Global CRAsGlobal CRAs – 6 – 6

The industrial organization of GCRAs (cont’d)

FitchFitch: (founded 1913, merged with IBCA in 1997): (founded 1913, merged with IBCA in 1997)

Net income (€ million)Net income (€ million): 350;

3,000 ratings on Sovereigns, Banks & Corporates;

1,200 employees of which 700 analysts.

DBRDBR: (Canada based, NRSRO since 2003): (Canada based, NRSRO since 2003)

Other NRSRO agencies: A.M. Best (2005), R&I (2007), JCR (2007), Egan-Jones (2007), LACE (2008), Realpoint (2008)

GCRAs are very profitable: pundits accuse NRSRO regulatory franchise

10

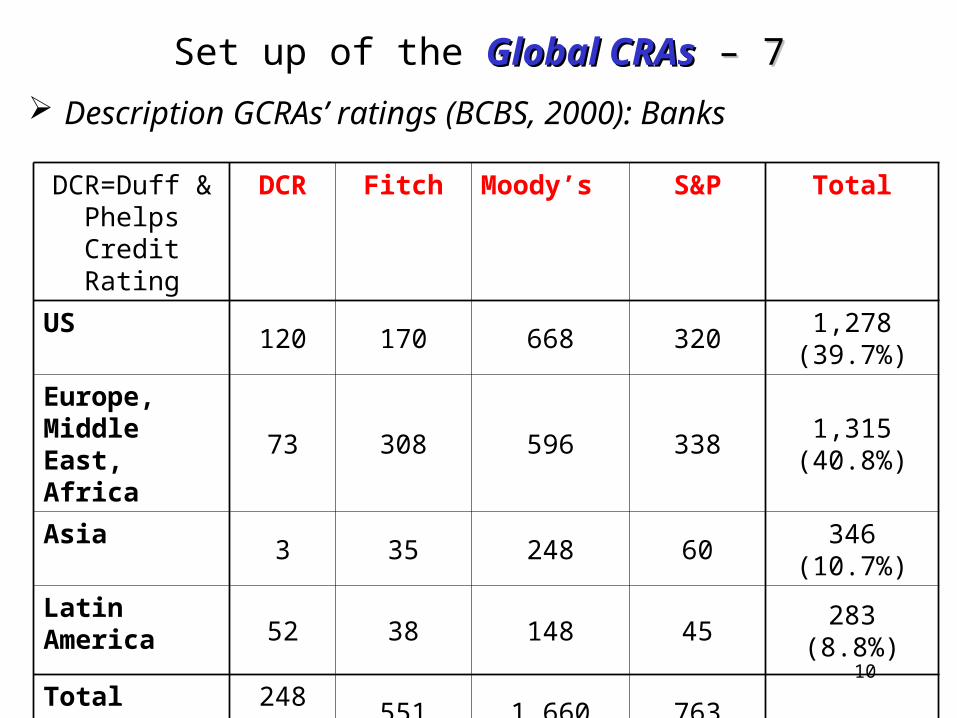

Set up of the Global CRAsGlobal CRAs – 7 – 7

Description GCRAs’ ratings (BCBS, 2000): Banks

DCR=Duff & Phelps Credit

Rating

DCR Fitch Moody’s S&P Total

US 120 170 668 320 1,278 (39.7%)

Europe, Middle East, Africa

73 308 596 338 1,315 (40.8%)

Asia 3 35 248 60 346 (10.7%)

Latin America52 38 148 45 283 (8.8%)

Total 248 (7.7%)

551 (17.1%)

1,660 (51.5%)

763 (23.7%)

3,222

11

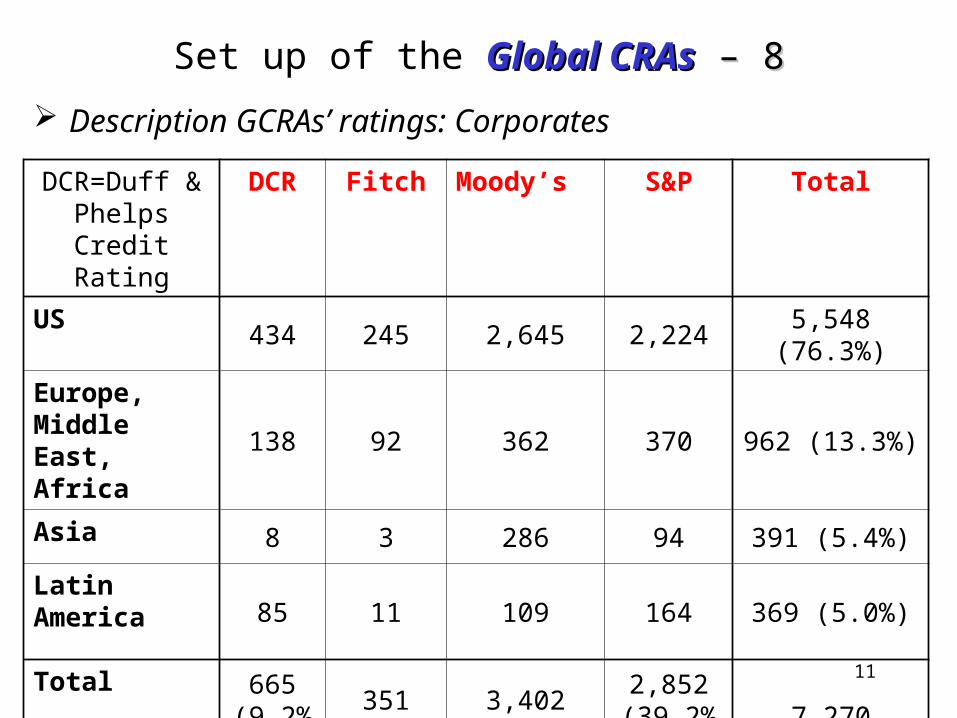

Set up of the Global CRAsGlobal CRAs – 8 – 8

Description GCRAs’ ratings: Corporates

DCR=Duff & Phelps Credit

Rating

DCR Fitch Moody’s S&P Total

US 434 245 2,645 2,224 5,548 (76.3%)

Europe, Middle East, Africa

138 92 362 370 962 (13.3%)

Asia 8 3 286 94 391 (5.4%)

Latin America85 11 109 164 369 (5.0%)

Total665

(9.2%)351

(4.8%)3,402

(46.8%)2,852

(39.2%)7,270

12

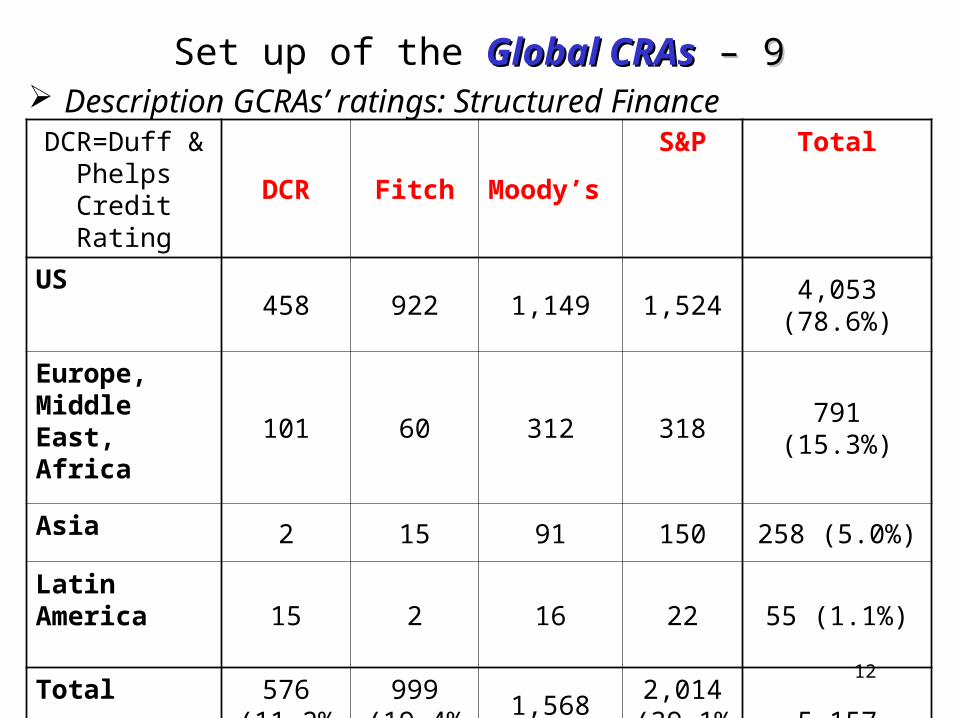

Set up of the Global CRAsGlobal CRAs – 9 – 9 Description GCRAs’ ratings: Structured Finance

DCR=Duff & Phelps Credit

RatingDCR Fitch Moody’s

S&P Total

US458 922 1,149 1,524 4,053 (78.6%)

Europe, Middle East, Africa 101 60 312 318 791 (15.3%)

Asia 2 15 91 150 258 (5.0%)

Latin America15 2 16 22 55 (1.1%)

Total 576 (11.2%)

999 (19.4%)

1,568 (30.4%)

2,014 (39.1%)

5,157

13

Set up of the Global CRAsGlobal CRAs – 10 – 10

Some description of GCRAs’ ratings

- Highly concentrated industry with Moody’s and S&P playing as leaders (US Dept of Justice labeled it “partner monopoly”), Fitch and DCR as distanced followers [Norden & Weber (2004): reviews for downgrade by S&P and Moody’s have largest impact on credit default swaps and shares];

- Though bank ratings are also important, the bulk of GCRAs’ business is in corporates and structured finance

- GCRAs’ business is for almost ¾ US based with bank ratings more geographically widespread

14

Set up of the Global CRAsGlobal CRAs – 11 – 11

M&A of GCRAs increased concentration

- In 2000 Fitch buys DCR, Thomson BankWatch; Looking at ratings in emerging economies

- Differences across regions of the world: GCRAs’ penetration is highest in Europe, smallest in Asia, intermediate in Latin America and Africa

- The number of ratings is much larger in Asia (and Latin America), where GCRAs’ penetration is lower, than in Europe

- GCRAs moving from branches to subsidiaries

15

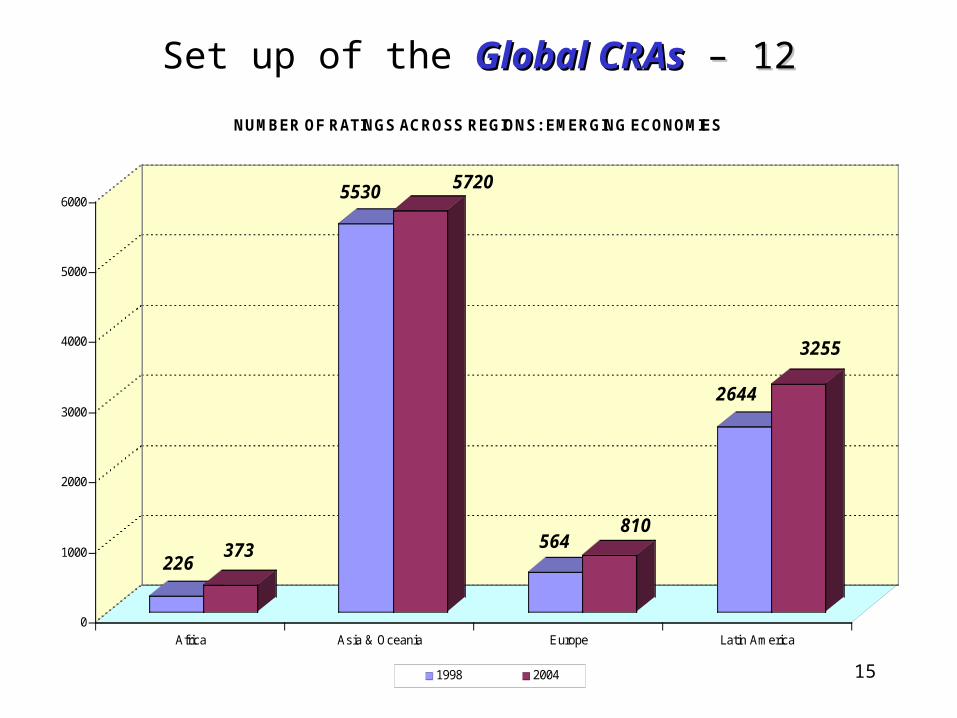

Set up of the Global CRAsGlobal CRAs – 12 – 12

226373

5530 5720

564810

2644

3255

0

1000

2000

3000

4000

5000

6000

Africa Asia & Oceania Europe Latin America

NUMBER OF RATINGS ACROSS REGIONS: EMERGING ECONOMIES

1998 2004

16

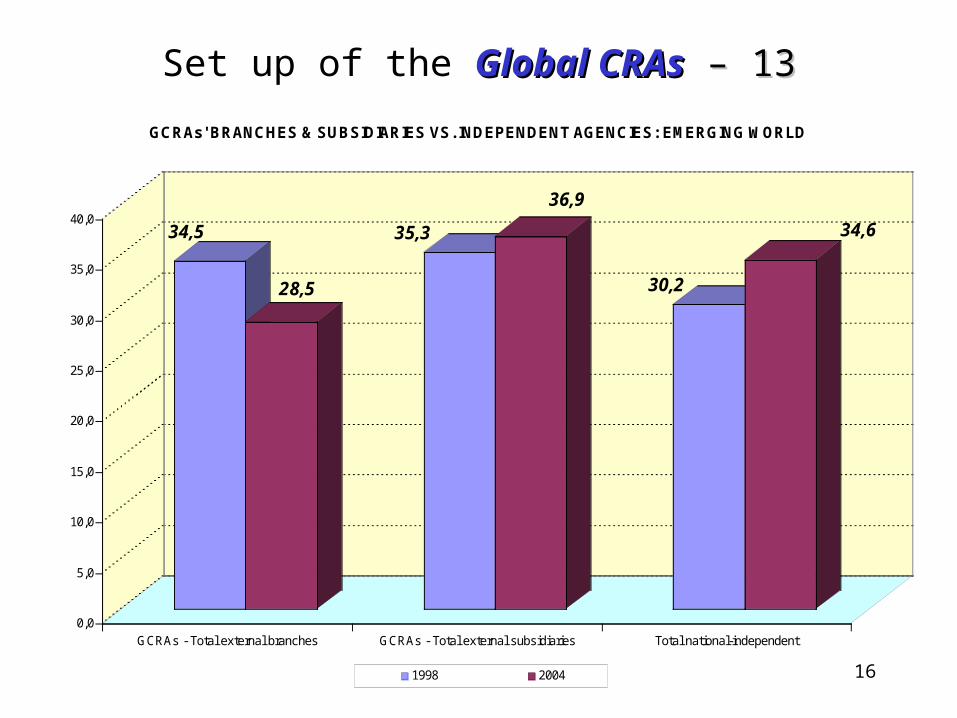

Set up of the Global CRAsGlobal CRAs – 13 – 13

34,5

28,5

35,3

36,9

30,2

34,6

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

% MARKET SHARE

GCRAs - Total external branches GCRAs - Total external subsidiaries Total national-independent

GCRAs' BRANCHES & SUBSIDIARIES VS. INDEPENDENT AGENCIES: EMERGING WORLD

1998 2004

17

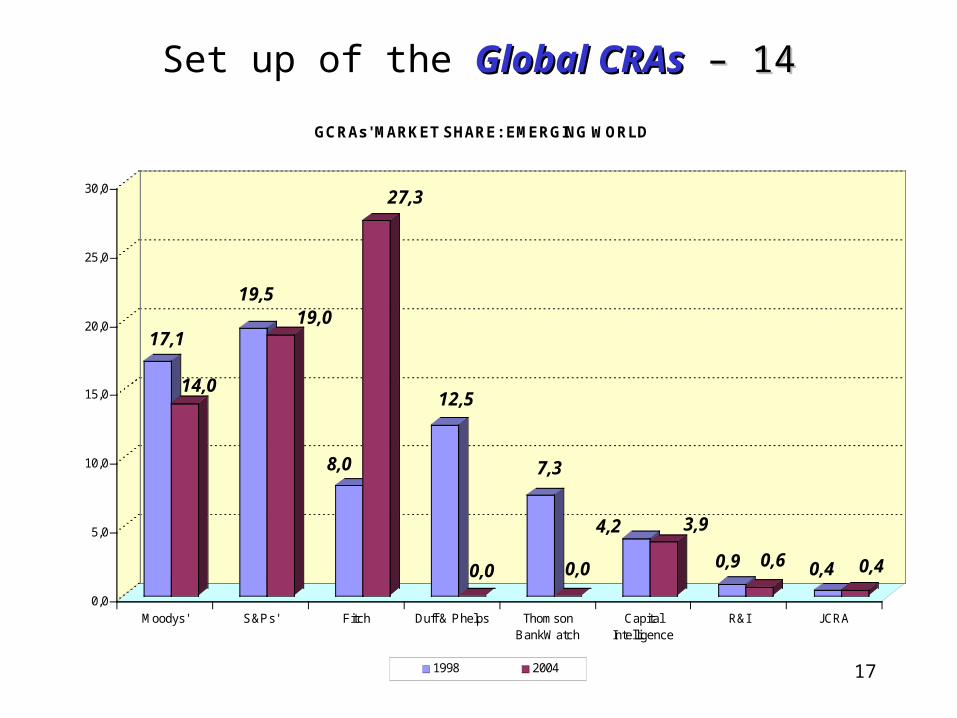

Set up of the Global CRAsGlobal CRAs – 14 – 14

17,1

14,0

19,519,0

8,0

27,3

12,5

0,0

7,3

0,0

4,2 3,9

0,9 0,6 0,4 0,4

0,0

5,0

10,0

15,0

20,0

25,0

30,0

% MARKET SHARE

Moodys' S&Ps' Fitch Duff & Phelps ThomsonBankWatch

CapitalIntelligence

R&I JCRA

GCRAs' MARKET SHARE: EMERGING WORLD

1998 2004

18

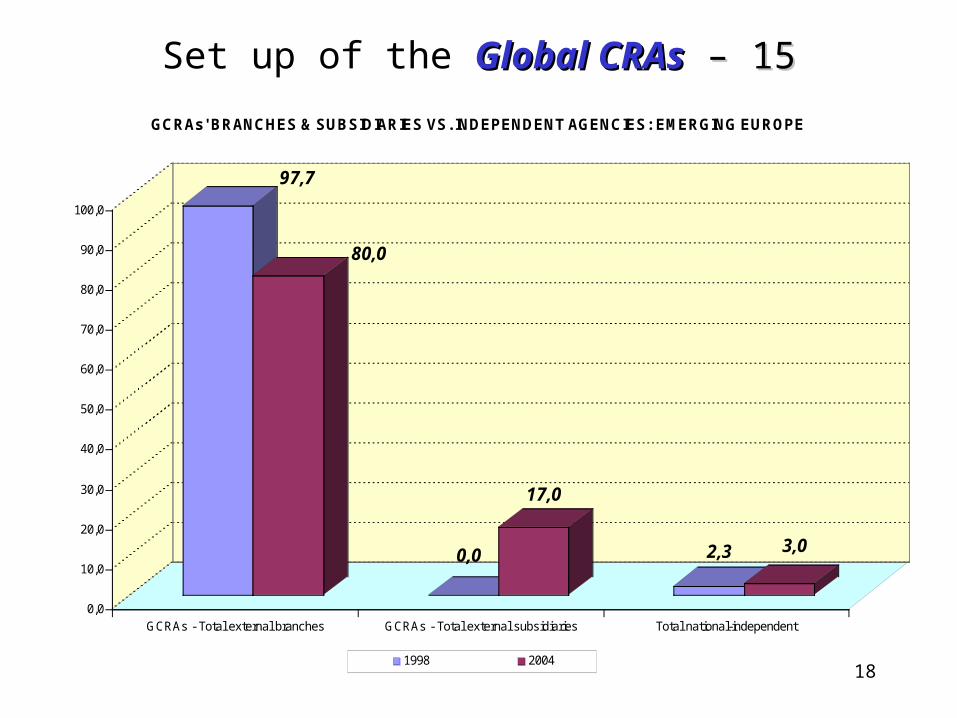

Set up of the Global CRAsGlobal CRAs – 15 – 15

97,7

80,0

0,0

17,0

2,3 3,0

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

% MARKET SHARE

GCRAs - Total external branches GCRAs - Total external subsidiaries Total national-independent

GCRAs' BRANCHES & SUBSIDIARIES VS. INDEPENDENT AGENCIES: EMERGING EUROPE

1998 2004

19

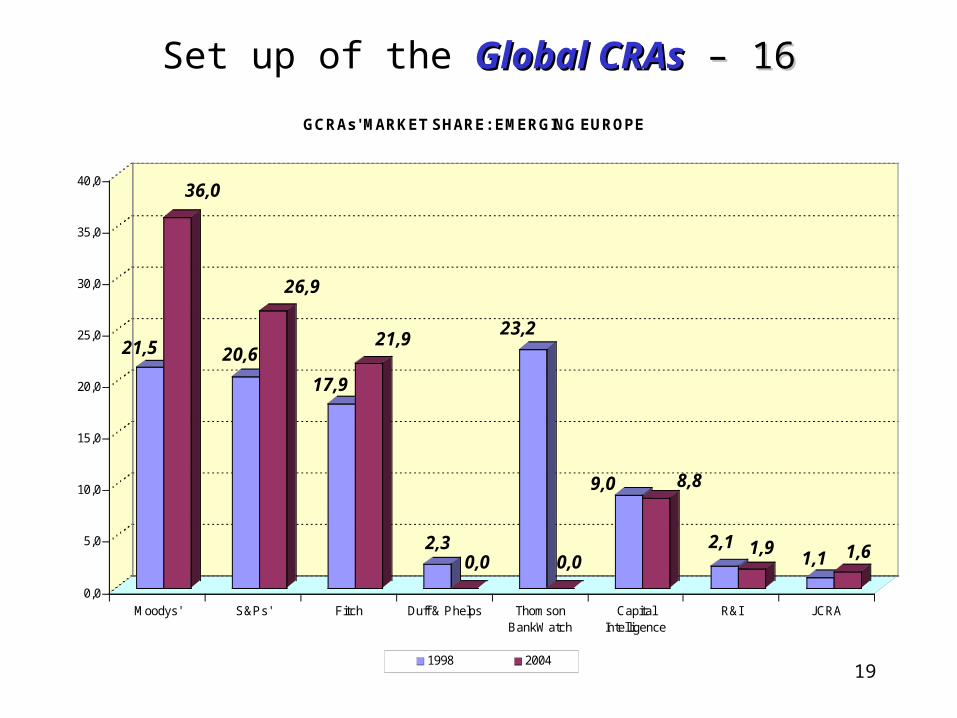

Set up of the Global CRAsGlobal CRAs – 16 – 16

21,5

36,0

20,6

26,9

17,9

21,9

2,30,0

23,2

0,0

9,0 8,8

2,1 1,91,1 1,6

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

% MARKET SHARE

Moodys' S&Ps' Fitch Duff & Phelps ThomsonBankWatch

CapitalIntelligence

R&I JCRA

GCRAs' MARKET SHARE: EMERGING EUROPE

1998 2004

20

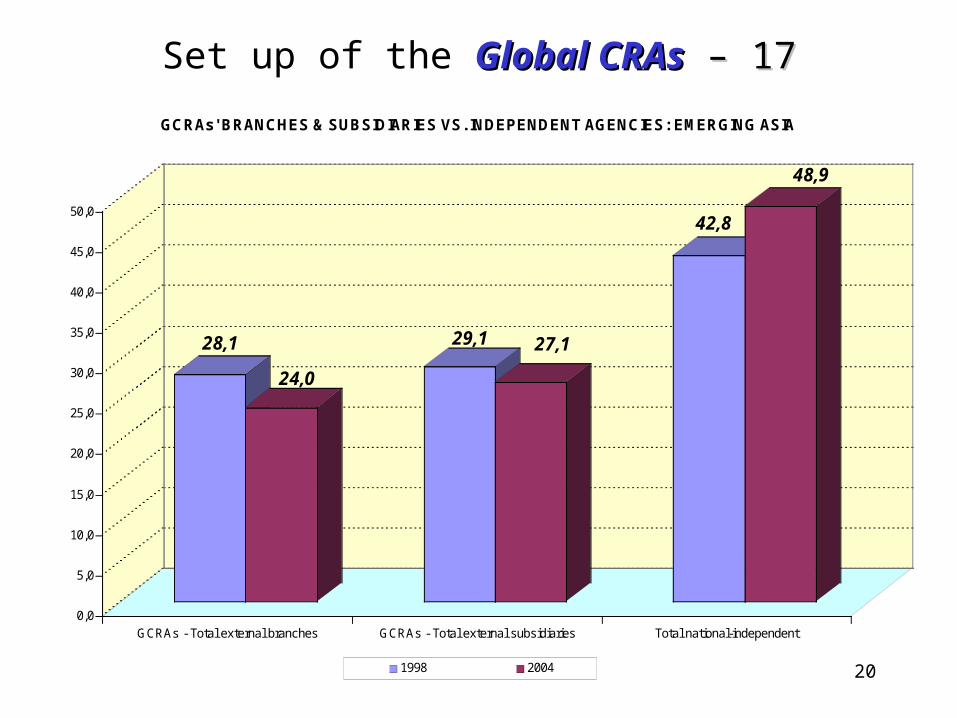

Set up of the Global CRAsGlobal CRAs – 17 – 17

28,1

24,0

29,1 27,1

42,8

48,9

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

50,0

% MARKET SHARE

GCRAs - Total external branches GCRAs - Total external subsidiaries Total national-independent

GCRAs' BRANCHES & SUBSIDIARIES VS. INDEPENDENT AGENCIES: EMERGING ASIA

1998 2004

21

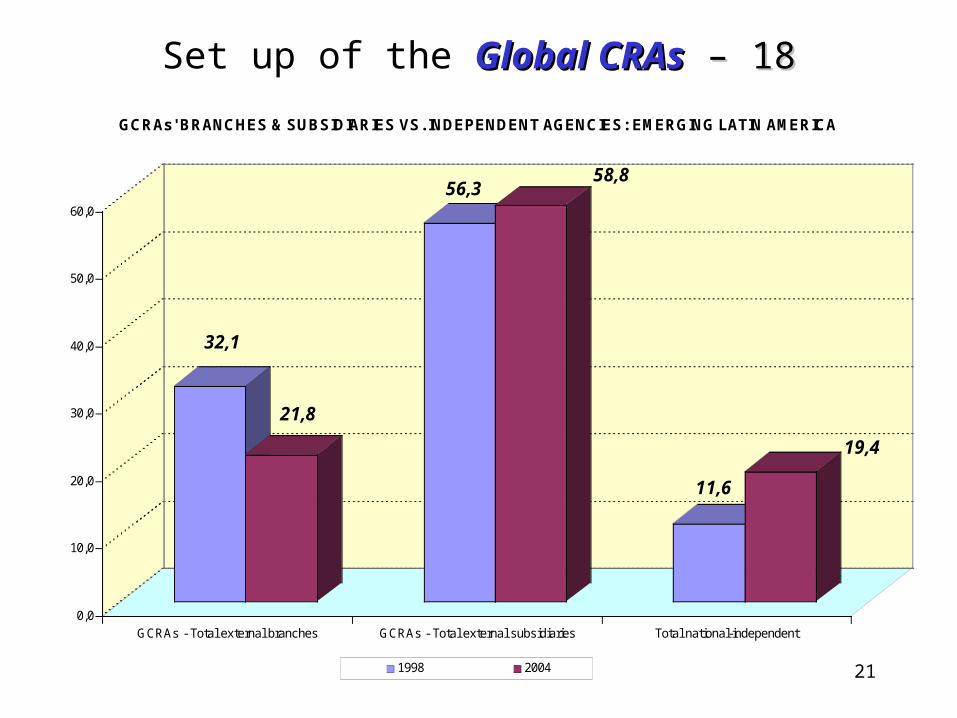

Set up of the Global CRAsGlobal CRAs – 18 – 18

32,1

21,8

56,358,8

11,6

19,4

0,0

10,0

20,0

30,0

40,0

50,0

60,0

% MARKET SHARE

GCRAs - Total external branches GCRAs - Total external subsidiaries Total national-independent

GCRAs' BRANCHES & SUBSIDIARIES VS. INDEPENDENT AGENCIES: EMERGING LATIN AMERICA

1998 2004

22

Main allegationsMain allegations on GCRAs GCRAs – 1

GCRAs’GCRAs’ track record:US: best (some exceptions); other OECD: good; Emerging Countries: not so good/evolvingMain complaints for ratings outside US:Too latePro-cyclicalPrivate ratings too linked to sovereigns’Lower info quality of private ratingsGCRAs under-invest in info processingAnticompetitive practices & conflicts of interest

23

Main allegationsMain allegations on GCRAs GCRAs – 2

Too late: GCRAs followed the market rather than forewarn it in the Asian financial crisis (IMF, 1999; BIS, 1999; Bhatia, 2002) [& Enron, Worldcom etc.]

On GCRAs’ failures, Bhatia (2002) notices that: (i) sovereign ratings result from one-size-fits-all ranking process; (ii) improvement in methodology/disclosure after the EA crisis may wish well for the future

Bissoondoyal-Bheenick (2004): generally, private rating changes have little/no market impact

Bongini et al (2002): stock prices & ratings did not outpace backward looking balance sheet information to assess bank fragility in the EA crisis

24

Main allegationsMain allegations on GCRAs GCRAs – 3

Too late: GCRAs follow the market (cont’d)

Sovereign downgrades follow (rather than lead) currency crises but do better at predicting defaults (Reinhart, 2002; Sy, 2004) → currency instability raises default risk (Reinhart, 2002 but not Sy, 2004); downgrades of structured products done after markets collapsed

25

Main allegationsMain allegations on GCRAs GCRAs – 4

Pro-cyclical: Late recognition of problems may lead GCRAs to downgrade emerging countries (both sovereigns & companies) excessively vis-à-vis what deserved by their fundamentals so GCRAs may exacerbate cycles & downturns in emerging countries

- Macro evidence: Monfort & Mulder (2000); Mulder & Perrelli (2001); Ferri, Liu & Stiglitz (1999); Kaminsky & Schmukler (2002); Kräussl (2003) [but: Mora (2004) questions some of this evidence for the EA crisis pointing to rating stickiness (in line with a conservative hypothesis, Löffler 2004); Hu et al. (2004): sovereign ratings were insufficiently conservative before the Asian and Russian crises]

26

Main allegationsMain allegations on GCRAs GCRAs – 5

Pro-cyclical: (cont’d)- Reisen & von Maltzan (1999) are among the first authors to argue

about the boom & bust cycle triggered by procyclical sovereign ratings

- Zhang (2003): GCRAs had assigned over-generous ratings to Argentina, & their downgrade lagged market

- Block & Vaaler (2004) find that GCRAs downgrade developing countries more often in election years as viewing elections negatively, raising developing democracies’ cost of capital

- Wei (2003) proposes a new multi-factor methodology to come up with a-cyclical ratings; because of assumptions he is criticized by Amato & Furfine (2004): for all US firms rated by S&P they find that ratings do not generally exhibit excess sensitivity to the business cycle.

27

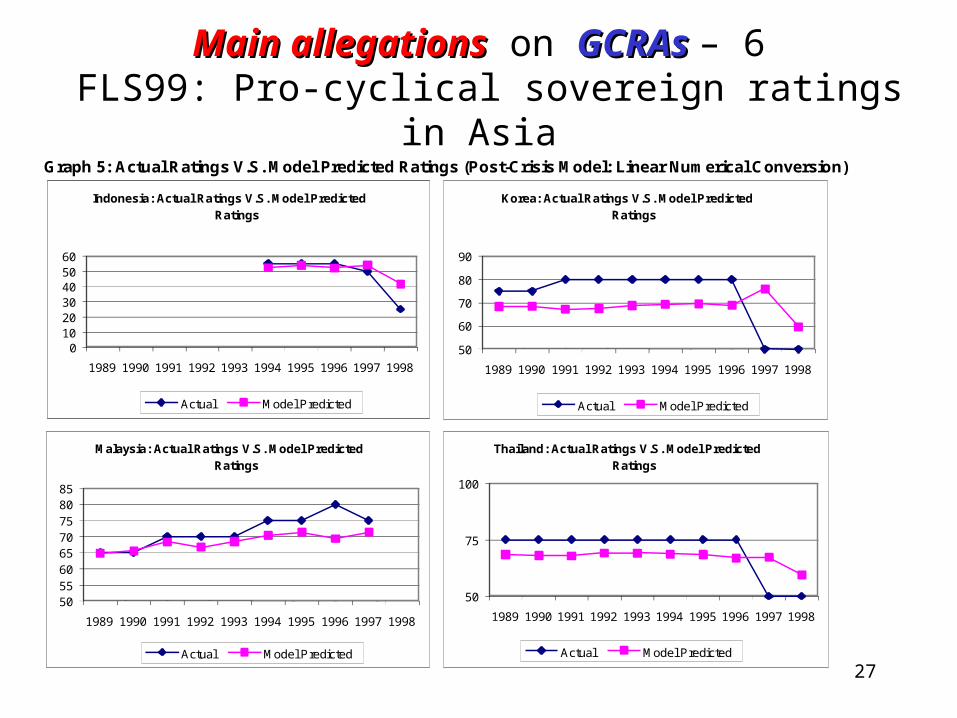

Main allegationsMain allegations on GCRAs GCRAs – 6 FLS99: Pro-cyclical sovereign ratings in Asia

Graph 5: Actual Ratings V.S. Model Predicted Ratings (Post-Crisis Model: Linear Numerical Conversion)

Malaysia: Actual Ratings V.S. Model Generated Ratings

50 55 60 65 70 75 80 85

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 Actual Model Predicted

Indonesia: Actual Ratings V.S. Model Generated Ratings

0 10 20 30 40 50 60

Actual Model Predicted

Thailand: Actual Ratings V.S. Model Predicted Ratings

50

75

100

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

Actual Model Predicted

Malaysia: Actual Ratings V.S. Model Predicted Ratings

50 55 60 65 70 75 80 85

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 Actual Model Predicted

Indonesia: Actual Ratings V.S. Model Predicted Ratings

0 10 20 30 40 50 60

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

Actual Model Predicted

Korea: Actual Ratings V.S. Model Predicted Ratings

50 60 70 80 90

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

Actual Model Predicted

28

Main allegationsMain allegations on GCRAs GCRAs – 7

Private ratings too linked to sovereigns’

- Sovereign downgrades cause firm-level downgrades (that are sticky to sovereign upgrades instead) only in emerging economies via a ‘domicile effect’ (Nickell et al. 2000), possibly excessive sovereign downgrades exert a negative impact on the cost of capital for emerging economies’ private sector and the new Basel criteria will amplify this impact (Ferri-Liu-Majnoni, 2001)

29

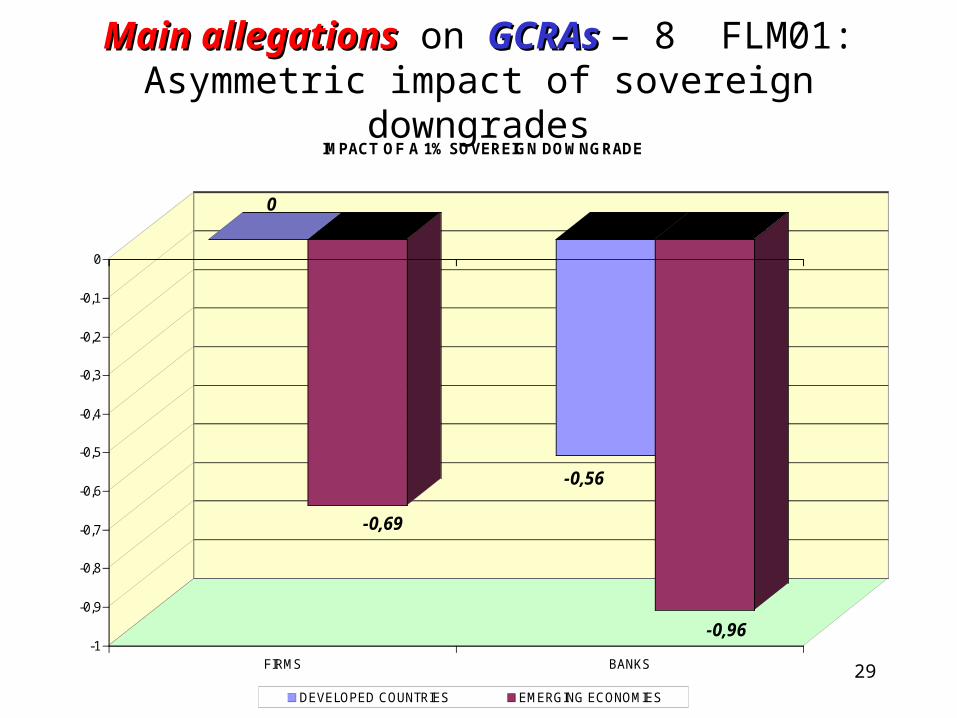

Main allegationsMain allegations on GCRAs GCRAs – 8 FLM01:Asymmetric impact of sovereign downgrades

0

-0,69

-0,56

-0,96-1

-0,9

-0,8

-0,7

-0,6

-0,5

-0,4

-0,3

-0,2

-0,1

0

FIRMS BANKS

IMPACT OF A 1% SOVEREIGN DOWNGRADE

DEVELOPED COUNTRIES EMERGING ECONOMIES

30

Main allegationsMain allegations on GCRAs GCRAs – 9

Lower info quality of private ratings

A lot of asymmetry in determinants of firm ratings in developed vs. emerging countries: firm specific risk dominates/sovereign risk negligible for developed countries’ firms while the opposite holds for emerging countries information content of firm ratings is much smaller in emerging countries (Ferri & Liu, 2003)

31

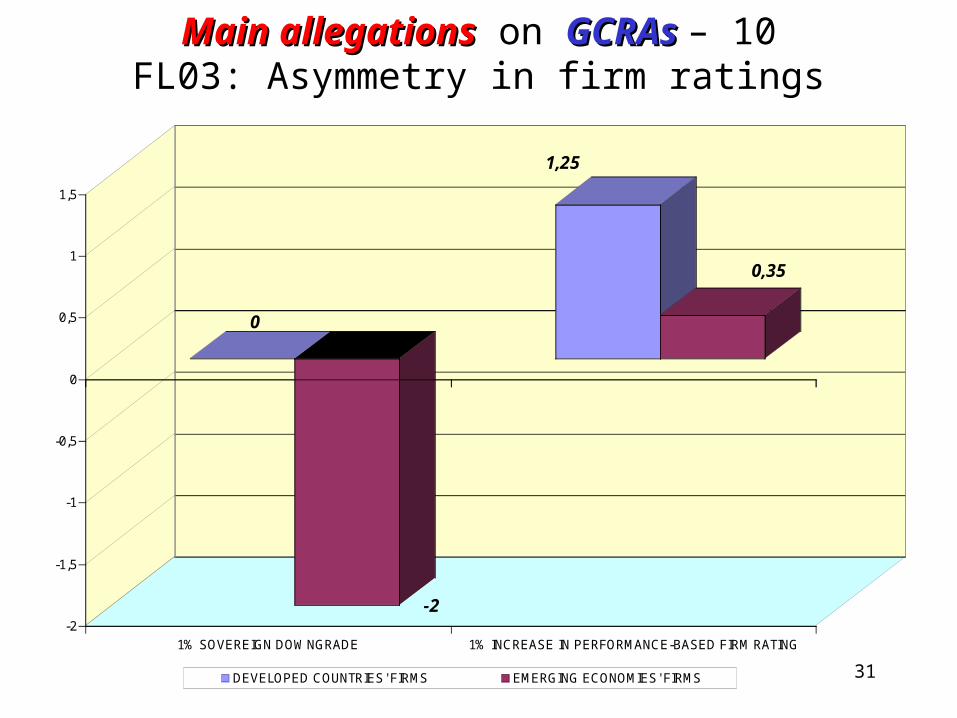

Main allegationsMain allegations on GCRAs GCRAs – 10FL03: Asymmetry in firm ratings

0

-2

1,25

0,35

-2

-1,5

-1

-0,5

0

0,5

1

1,5

1% SOVEREIGN DOWNGRADE 1% INCREASE IN PERFORMANCE-BASED FIRM RATING

DEVELOPED COUNTRIES' FIRMS EMERGING ECONOMIES' FIRMS

32

Main allegationsMain allegations on GCRAs GCRAs – 11

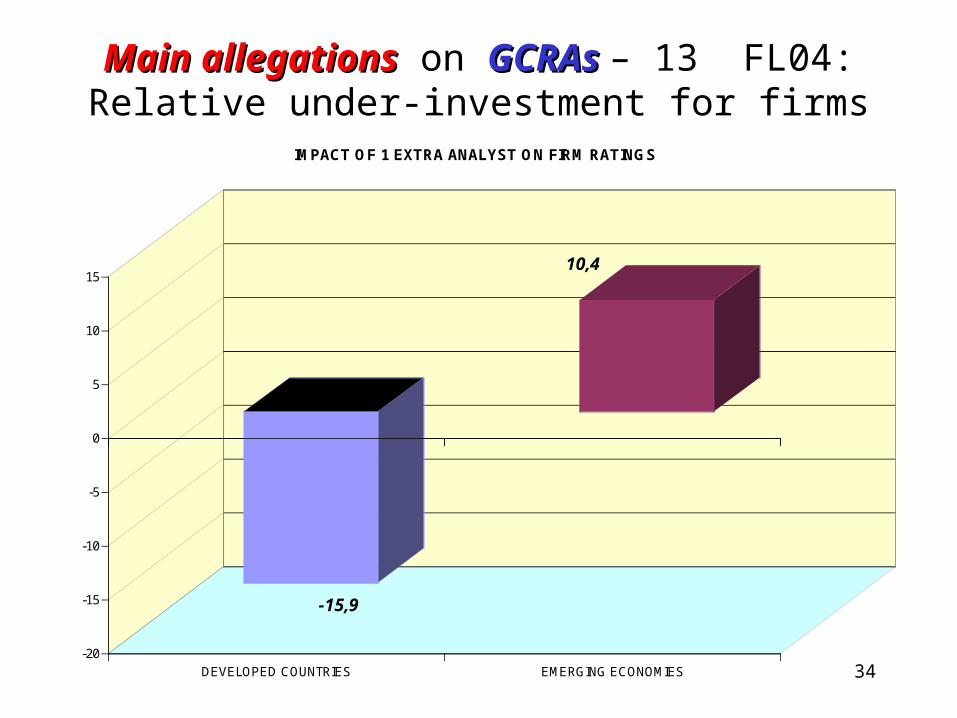

GCRAs under-invest in emerging countries: Vis-à-vis developed countries, fewer analysts for sovereigns ( absolute under-investment) and firm ratings positively related to the number of analysts while the opposite holds for developed countries’ firms relative under-investment in emerging countries (Ferri, 2004; Ferri & Liu, 2004, using data from Moody’s)

33

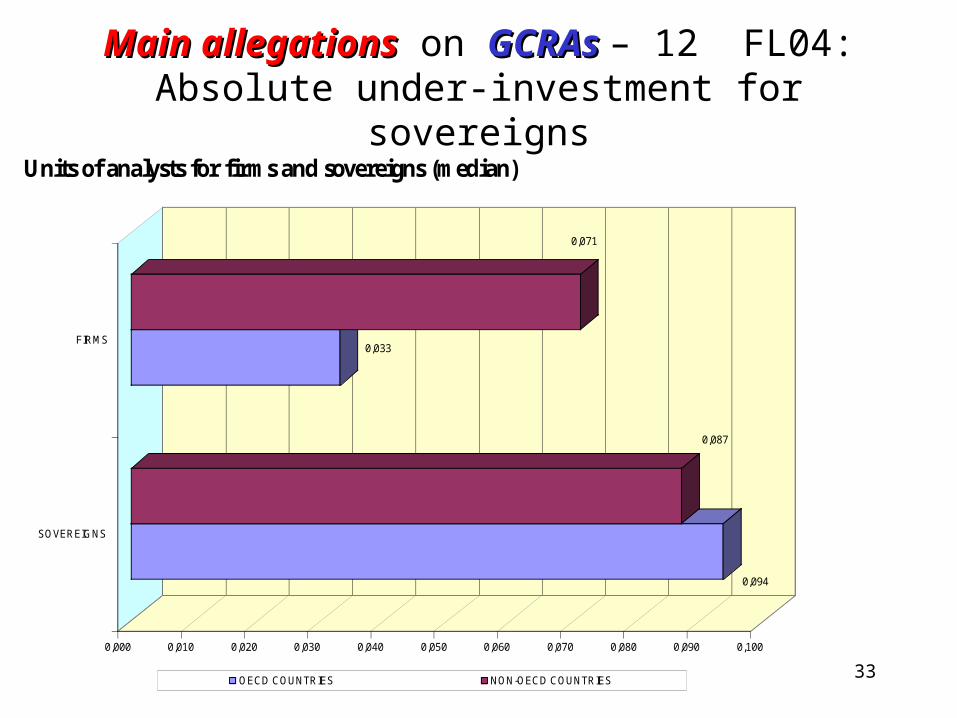

Main allegationsMain allegations on GCRAs GCRAs – 12 FL04:Absolute under-investment for sovereigns

Units of analysts for firms and sovereigns (median)

0,094

0,087

0,033

0,071

0,000 0,010 0,020 0,030 0,040 0,050 0,060 0,070 0,080 0,090 0,100

SOVEREIGNS

FIRMS

OECD COUNTRIES NON-OECD COUNTRIES

34

Main allegationsMain allegations on GCRAs GCRAs – 13 FL04:Relative under-investment for firms

-15,9

10,4

-20

-15

-10

-5

0

5

10

15

% POINTS ON RATINGS SCALED 0-100

DEVELOPED COUNTRIES EMERGING ECONOMIES

IMPACT OF 1 EXTRA ANALYST ON FIRM RATINGS

35

Main allegationsMain allegations on GCRAs GCRAs – 14Anticompetitive practices & conflicts of interest

- Sometimes GCRAs promote their business via questionable unsolicited ratings (revised up only if the company pays its fee). Dumping practice to conquer foreign markets (home market is protected by NRSRO regulation)? Poon (2003): unsolicited ratings for Japanese issuers lower than solicited ratings even controlling for differences in sovereign risk & key financial ratios of the rated entity. Issuers looks for better rating among CRAs (rating shopping, Skerta &Veldkamp, 2009)- Issuers of securities pay for credit ratings a fee based on the size of issue → potential conflict of interest (Burnie & Langsam 2004); Covitz & Harrison (2003): no evidence of conflict of interest

36

Main allegationsMain allegations on GCRAs GCRAs – 15

Anticompetitive & conflict of interest (cont’d)

- Sometimes private contracts contain “NRSRO rating triggers” causing adverse consequences, such as the shortening of debt repayment schedules → since the trigger is usually around the investment grade threshold, this may induce the rating agency to be reluctant to downgrade

Johnson (2003): compares downgrading actions by an NRSRO CRA vs. a non-NRSRO CRA at the investment grade threshold, the data suggest the former hesitates (vis-à-vis the latter) to downgrade issuers to speculative grade

37

Main allegationsMain allegations on GCRAs GCRAs – 16

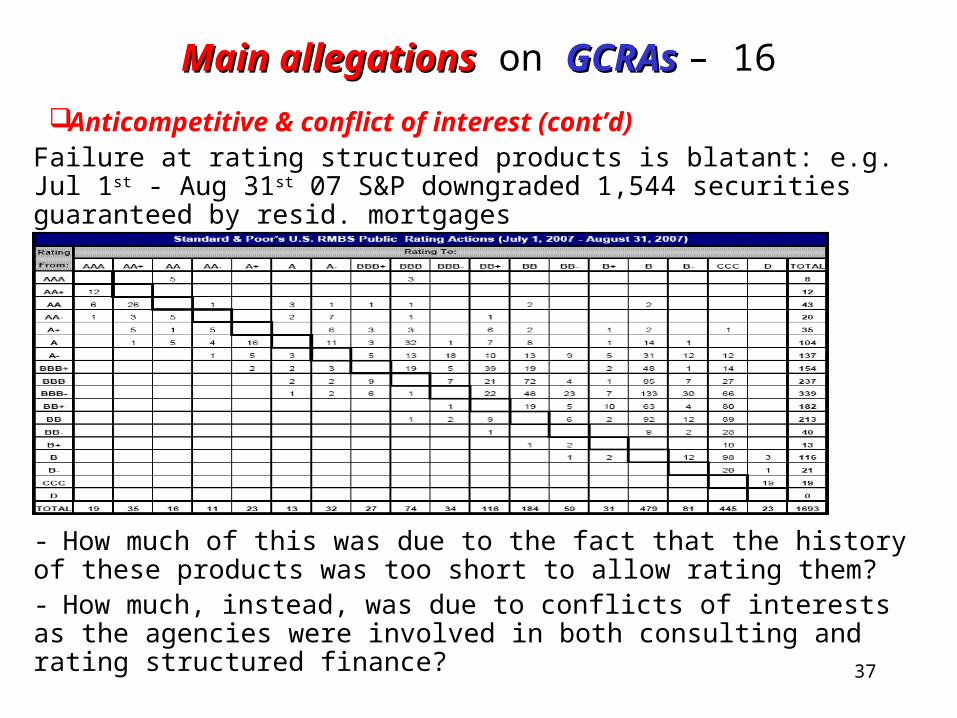

Anticompetitive & conflict of interest (cont’d)Failure at rating structured products is blatant: e.g. Jul 1st - Aug 31st 07 S&P downgraded 1,544 securities guaranteed by resid. mortgages

- How much of this was due to the fact that the history of these products was too short to allow rating them?- How much, instead, was due to conflicts of interests as the agencies were involved in both consulting and rating structured finance?

38

Main allegationsMain allegations on GCRAs GCRAs – 17

For extreme chastising views on GCRAs see:Partnoy (1999): “the reputational capital view of credit rating agencies is not supported by history or economic analysis. Credit rating agencies have not survived for six decades because they produce credible and accurate information. They have not maintained good reputations based on the informational content of their credit ratings. Instead, the credit rating agencies have thrived, profited, and become exceedingly powerful because they have begun selling regulatory licenses, i.e., the right to be in compliance with regulation. Credit ratings therefore are an excellent example of how not to privatize a regulatory function … Never has too little, too late, been so powerful”

White (2001) demands full liberalization dropping NRSRO list

39

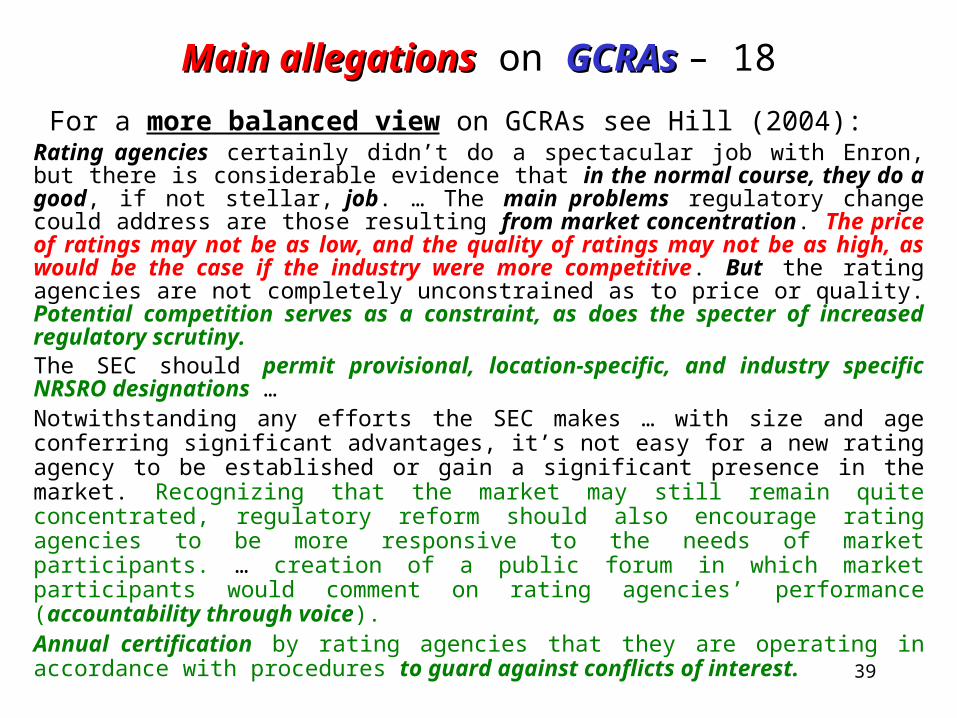

Main allegationsMain allegations on GCRAs GCRAs – 18

For a more balanced view on GCRAs see Hill (2004):Rating agencies certainly didn’t do a spectacular job with Enron, but there is considerable evidence that in the normal course, they do a good, if not stellar, job. … The main problems regulatory change could address are those resulting from market concentration. The price of ratings may not be as low, and the quality of ratings may not be as high, as would be the case if the industry were more competitive. But the rating agencies are not completely unconstrained as to price or quality. Potential competition serves as a constraint, as does the specter of increased regulatory scrutiny.The SEC should permit provisional, location-specific, and industry specific NRSRO designations …Notwithstanding any efforts the SEC makes … with size and age conferring significant advantages, it’s not easy for a new rating agency to be established or gain a significant presence in the market. Recognizing that the market may still remain quite concentrated, regulatory reform should also encourage rating agencies to be more responsive to the needs of market participants. … creation of a public forum in which market participants would comment on rating agencies’ performance (accountability through voice).Annual certification by rating agencies that they are operating in accordance with procedures to guard against conflicts of interest.

40

Regional CRAsRegional CRAs & capital market development 1

In light of the shortcomings of the GCRAs & of the fact that they are even less accountable abroad than in the US market, one may ask whether Regional CRAsRegional CRAs are needed for capital market development

Answers differ between Europe vs. Asia: while in Europe short-lived national credit rating agencies were sooner or later acquired by the GCRAs, many Asian countries still have their own national credit rating agencies, even if no truly regional agency exists yet

Specifically, Japan has the 2 largest & long lived

41

Regional CRAsRegional CRAs & capital market development 2

How do the Regional CRAsRegional CRAs compare to GCRAs?Japanese CRAs Japanese CRAs often accused of being too lenient to local issuers

with respect to GCRAs, but:BCBS (2000): Outside of the US, Japanese rating agencies are

among the oldest and most active. Data availability has thus attracted the attention of researchers. In this case, analysis has uncovered some fairly large differences between Japanese agencies and non-Japanese agencies, which seem to be tougher on the local issuers. Nevertheless, there may be fewer differences across agencies about relative riskiness, as there is evidence that both Japanese and non-Japanese ratings are highly correlated with market-determined credit spreads.

[This was already pointed out by Kawai (1997), Packer & Reynolds (1997), Packer (2000)]

42

Regional CRAsRegional CRAs & capital market development 3

In recent years, Japanese CRAs Japanese CRAs have been awarded prizes (over & above GCRAs) by JP Morgan for their work on the Samurai bond market

Shin & Moore (2003): find a systematic bias upward for the two Japanese rating agencies (RAs) and show the bias cannot be explained by keiretsu belonging; however, when they estimate a rating determination equation the discriminating power of the Japanese RAs as measured by the adj R2 is no lower than for Moody's or S&P

Do national companies perceive a difference between GCRAs & Regional CRAsRegional CRAs? (JCIF survey, 2001)

43

Regional CRAsRegional CRAs & capital market development 4

5 Factors Viewed As Most Important (in %) In Selecting Rating Agency (average; data for 2001)

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

Influence & Recognition Rating Fairness Global Activity Industrial Specialization Designated Rating Company

Japanese Rating Agencies GCRAs

44

Still shallow EU financial mkts: 1995 vs. 2005

University of Bari

RATIO (%) OF PRIVATE BONDS OUTSTANDING TO GDP

83,9

23,0 21,7

31,9 30,1

8,311,213,2

21,9

5,9 7,1

41,7 40,2

2,7

10,8

115,2

0,0

20,0

40,0

60,0

80,0

100,0

120,0

Total Bonds - 1995 Total Bonds - 2005 Corporate Bonds - 1995 Corporate Bonds - 2005

USA Asia Asia excluding Japan Euro Area

• post EMU progress of Euroland private securities markets lower than expected (Hartmann et al. 2003; Cappiello et al. 2006)

• The rest is drawn from Ferri & Lacitignola (2007)

45

Factors behind private bond market development

Various factors may promote the development of private bond markets:

• By removing exchange rate risks, EMU was a main promoting factor ... but it’s not the only one ...

• Asset management seeking diversification and higher return

• Better market infrastructure, such as corporate ratings becoming more widespread

46

Main features of GRAs and NRAs

• GRAs (established since 1909):

- Apply a “standardized” rating methodology across countries regardless the environment in which firms operate

• NRAs (established since 1985):

- Have a comparative advantage to access more appropriate knowledge of local environment (Packer, 2000)

- Originated with the support of regulation (Kurosawa, 1999)

- Lower fees than those applied by GRAs (JCIF, 2001)

- Less independent, most of them are owned by financial institutions (Kurosawa, 1999)

47

Specifically for Japanese financial markets:- combination of NRA and GRA ratings predicts spreads on

securities’ secondary market trading more accurately than any of the two classes taken separately (Packer, 2000)

- NRA ratings are more related to rated companies’ financial ratios than GRA ratings (Packer, 2000)

- In the opinion of Japanese corporations, NRAs do not differ from GRAs in terms of market influence and recognition (JCIF, 2001)

- Impact on abnormal returns larger for rating changes enacted by NRAs vis-à-vis those enacted by GRAs (Lacitignola, 2007)

Market impact of GRAs and NRAs

48

By enlarging the number of rated companies, both GRAs and NRAs may actively CONTRIBUTE to FINANCIAL MARKET DEVELOPMENT

Markets seem to take into account both NRA and GRA ratings when pricing securities (JCIF,

2001)

49

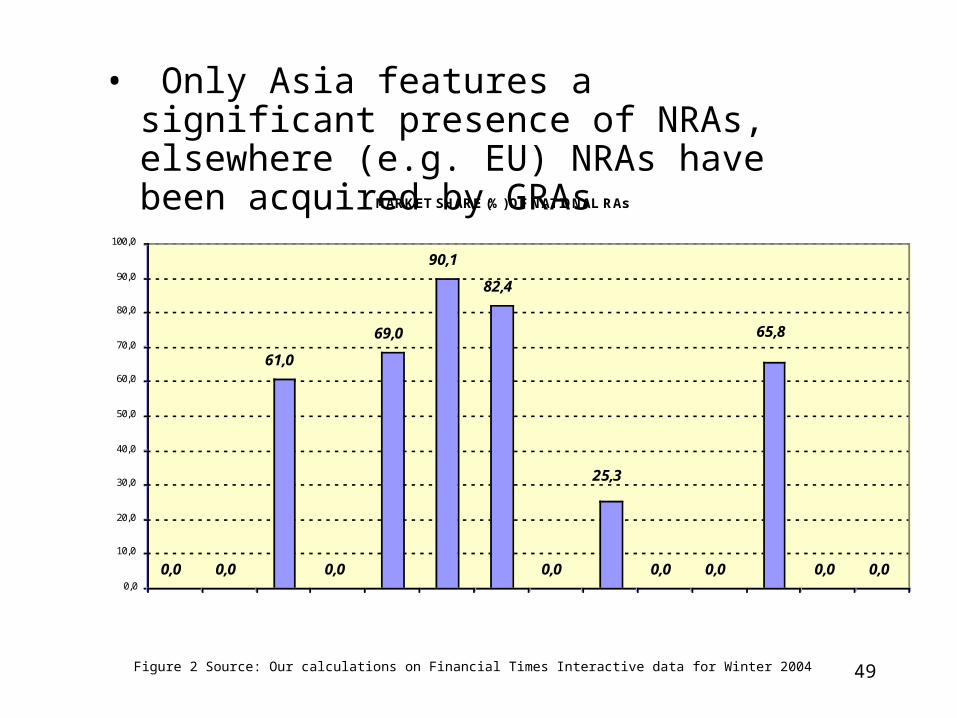

• Only Asia features a significant presence of NRAs, elsewhere (e.g. EU) NRAs have been acquired by GRAs

MARKET SHARE (%) OF NATIONAL RAs

0,0 0,0

61,0

0,0

69,0

90,1

82,4

0,0 0,0 0,0 0,0 0,0

65,8

25,3

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

China-MainlandHong Kong-China

India

Indonesia

Israel KoreaMalaysia Pakistan

Philippines SingaporeTaipei-China

Thailand Turkey Vietnam

Figure 2 Source: Our calculations on Financial Times Interactive data for Winter 2004

50

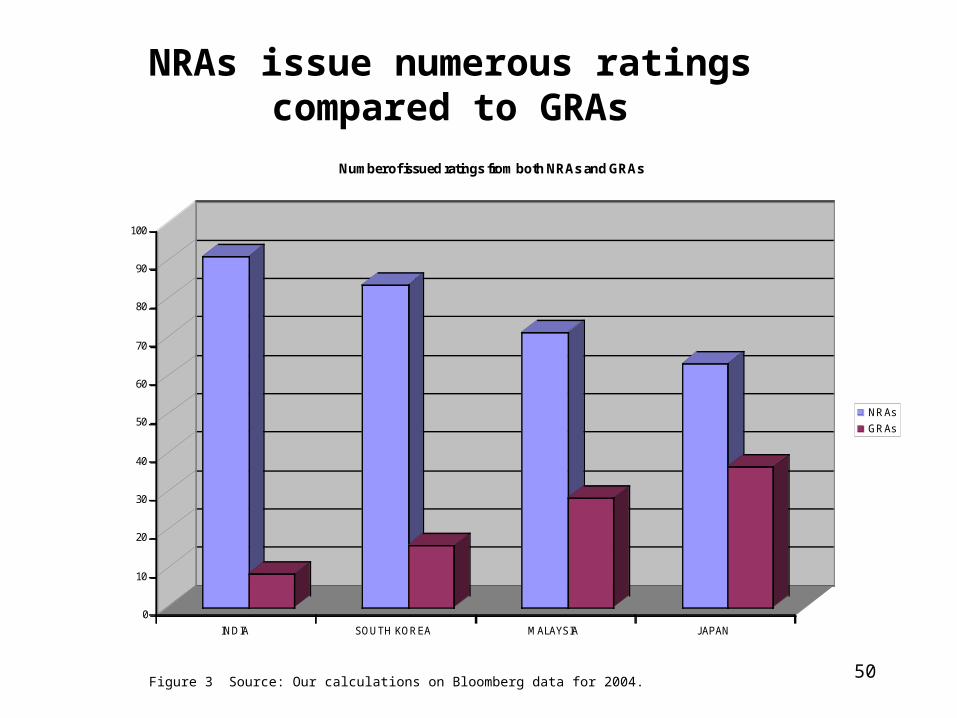

NRAs issue numerous ratings compared to GRAs

0

10

20

30

40

50

60

70

80

90

100

INDIA SOUTH KOREA MALAYSIA JAPAN

Number of issued ratings from both NRAs and GRAs

NRAs

GRAs

Figure 3 Source: Our calculations on Bloomberg data for 2004.

51

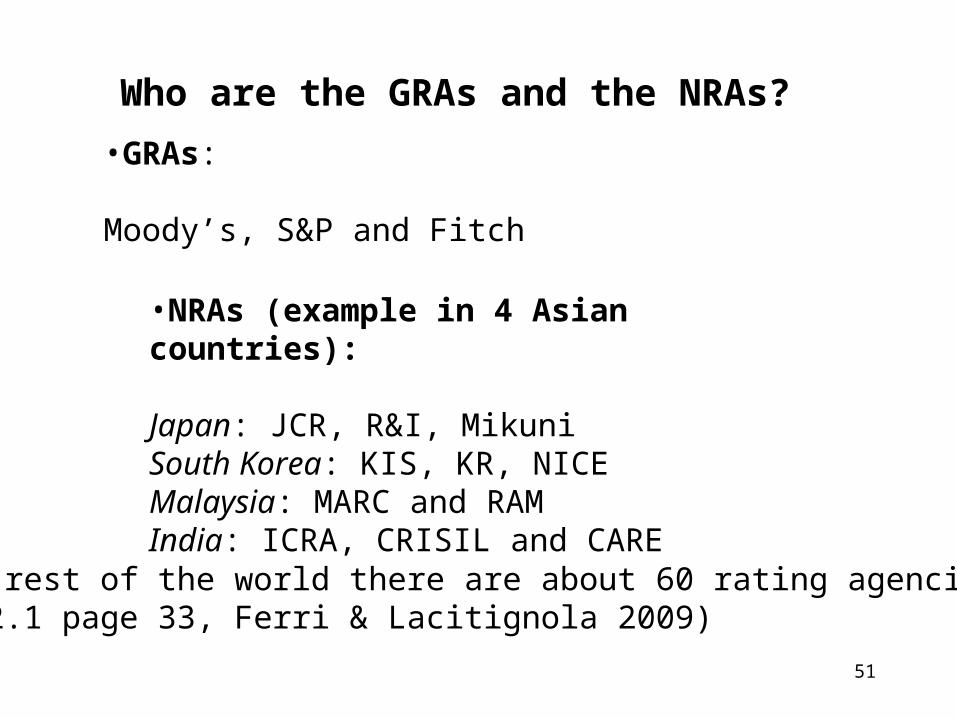

•GRAs:

Moody’s, S&P and Fitch

•NRAs (example in 4 Asian countries):

Japan: JCR, R&I, MikuniSouth Korea: KIS, KR, NICEMalaysia: MARC and RAMIndia: ICRA, CRISIL and CARE

Who are the GRAs and the NRAs?

In the rest of the world there are about 60 rating agencies(tab. 2.1 page 33, Ferri & Lacitignola 2009)

52

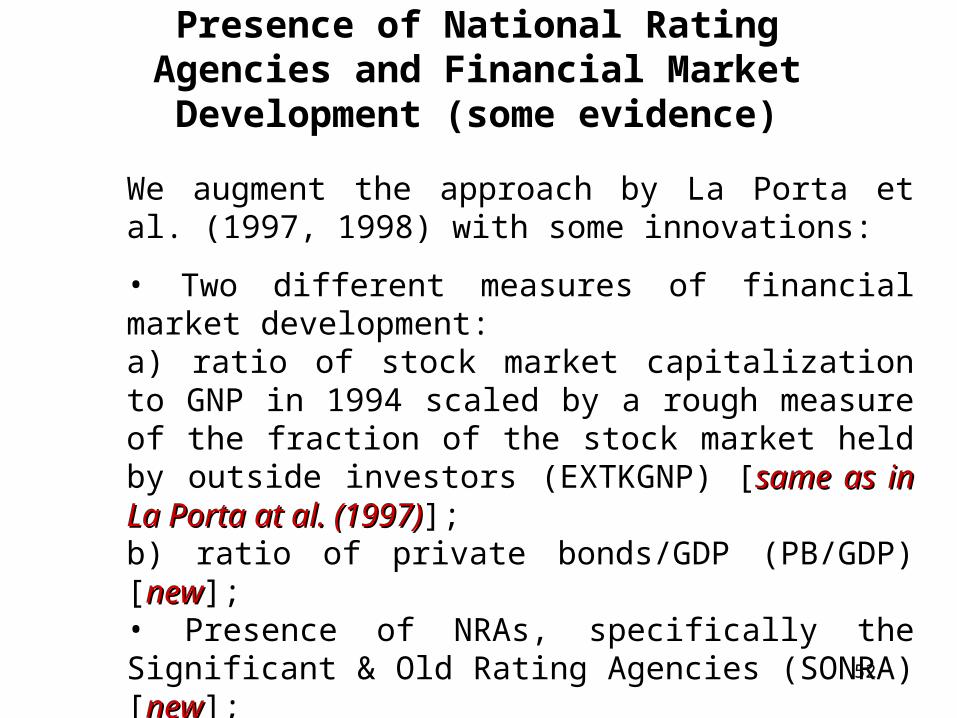

Presence of National Rating Agencies and Financial Market Development (some

evidence)

We augment the approach by La Porta et al. (1997, 1998) with some innovations:

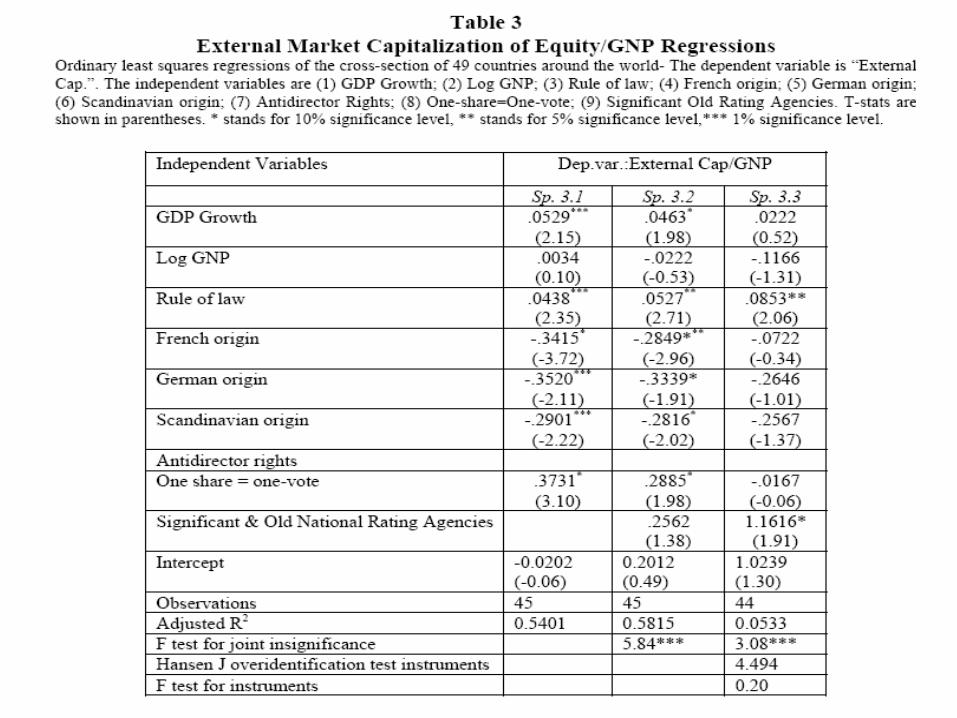

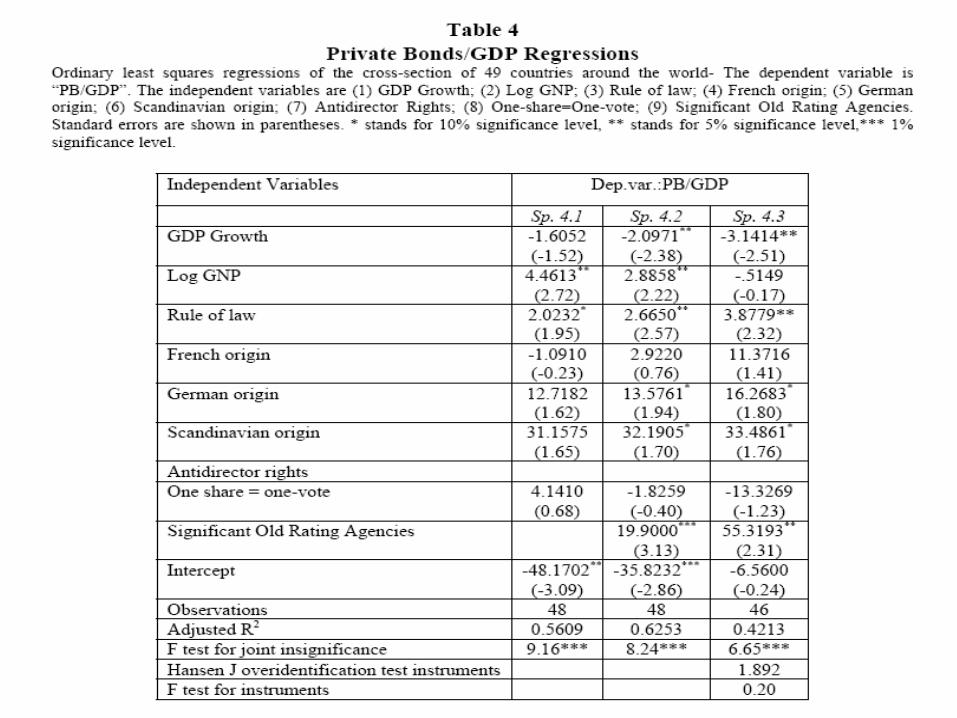

• Two different measures of financial market development:a) ratio of stock market capitalization to GNP in 1994 scaled by a rough measure of the fraction of the stock market held by outside investors (EXTKGNP) [same as in La Porta at al. same as in La Porta at al. (1997)(1997)];b) ratio of private bonds/GDP (PB/GDP) [newnew];• Presence of NRAs, specifically the Significant & Old Rating Agencies (SONRA) [newnew];• We use both the OLS estimation and the Instrumental variable estimation [newnew].

53

54

55

Results:

• In both specifications, using different dependent variables, the presence of NRAs (with the rule of law variable) has significant effects on financial markets. Effects are confirmed also in the Instrumental Variable regressions;

• NRAs’ impact on financial markets is larger when dependent variable PB/GDP, i.e. it seems that ratings contribute even more to private bond markets development than to stock market development (measure problems?)

• NRAs seem an important factor to promote financial market development

56

The Business Specificity of National Rating Agencies: Evidence From Asia

• GRAs tend to specialize in companies which are larger/more internationalized for two reasons:

- Reputation

- Larger/internationalized companies are typically the clients with which they do business (fees are related to the amount of issued debt)

• NRAs focusing on local/smaller entities are more cost effective and are able to capture the business specificity of their clientele

GRAs and NRAs may be complementary and specialize in different clientele.

57

We investigate this hypothesis using:

• Rating data for India, Japan, Korea and Malaysia

• Listed non-financial corporations only

• All rating issuer which have a rating either from GRAs or from NRAs or from both

• Issuer size measured by total asset in 2002

• A proxy for the degree of internationalization (e.g. if the issuer is listed in a foreign country)

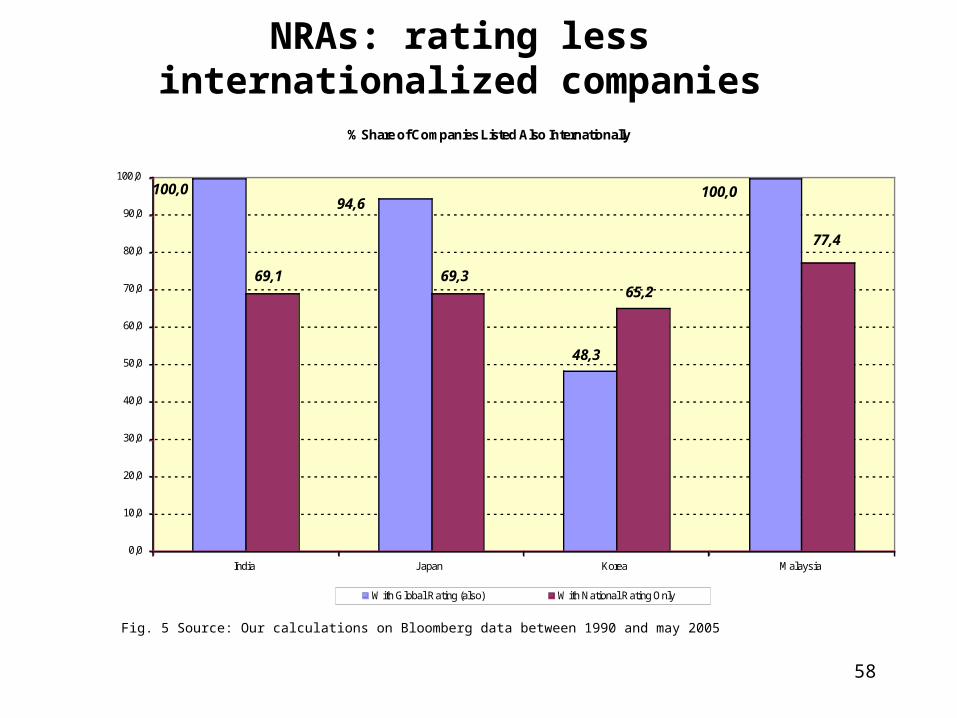

Results are depicted in fig. 5

The Business Specificity of NRAs: Evidence From Asia (cont’d)

58

% Share of Companies Listed Also Internationally

48,3

69,1 69,365,2

100,094,6

100,0

77,4

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

India Japan Korea Malaysia

With Global Rating (also) With National Rating Only

Fig. 5 Source: Our calculations on Bloomberg data between 1990 and may 2005

NRAs: rating less internationalized companies

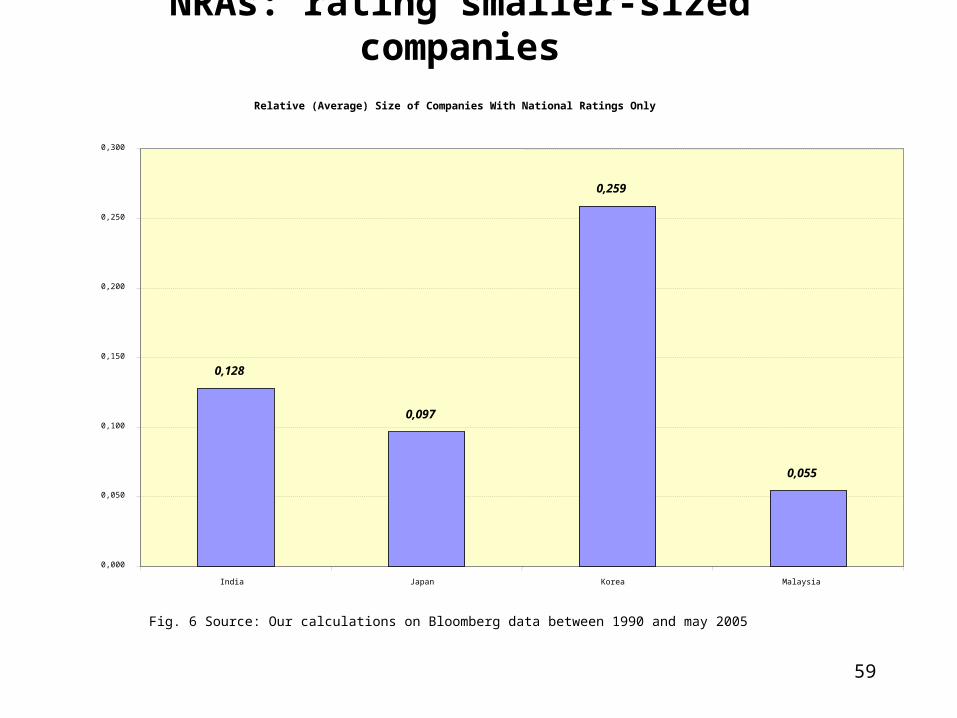

59

Relative (Average) Size of Companies With National Ratings Only

0,128

0,097

0,259

0,055

0,000

0,050

0,100

0,150

0,200

0,250

0,300

India Japan Korea Malaysia

Fig. 6 Source: Our calculations on Bloomberg data between 1990 and may 2005

NRAs: rating smaller-sized companies

60

Results:

• Among the companies obtaining a rating (also) from GRAs the share of companies listed also internationally is significantly larger than among companies receiving a rating only from NRAs (only exception Korea distortive national regulation);

• The average size of the companies obtaining a rating only from NRAs is much smaller than that of those companies receiving a rating (also) from GRAs.

61

To conclude on this part

(a) in a La Porta et al. (1997) framework, the presence of NRAs associates with more developed financial markets (in terms of both stock market capitalization and extent of private bond issuance)

(b) focusing on Asia, we identify a specialization pattern whereby NRAs concentrate on rating smaller-sized/domestic-focused companies while GRAs devote themselves to rating larger/more internationalized companies

62

CRAs responsibility and regulation matter 1

• Rating agencies’ behavior has come (again) under scrutiny; they failed to forewarn markets, downgrades were too late and excessively (procyclical effect)

• CRAs rating business has grown at a high rate in the last three years especially in the structured product sector; in 2009 Moody’s rated 96,000 structured finance obligations, its profits tripled from 1996 to 2006 (Lowenstein, 2008) (difficulties of evaluation and conflicts of interest)

63

CRAs responsibility and regulation matter 2

• The switch from Originate to hold (OTH) to Originate to Distribute (OTD) model had perverse effects on screening and monitoring incentive (transferred-risk)

• Conflicts of interest are even stronger in structured products: CRAs were both advisors in the determination of capital enhancement and structuring of products and raters (does it work?)

64

CRAs responsibility and regulation matter 3

• CRAs have underestimated the implicit risk of structured product (fire sale and systemic liquidity issues)

• In rating structured products (complex and opaque) they relaxed the “mark to market” model in favor of the “mark to model” with over-optimistic assumptions

• Class-actions by investor against CRAs

CRAs claim that ratings are opinions protected by the First Amendment of the US Constitution

65

CRAs responsibility and regulation matter 4

• As far as ratings had important systemic effects, regulators (SEC, IOSCO, Basel commission, CESR) got involved in new regulation proposal (protection of market stability, and the role of financial information provider of CRAs)

• In 2009 the court of South-district of New York declared that CRAs cannot hide their responsibility under the First Amendment of the US Constitution

66

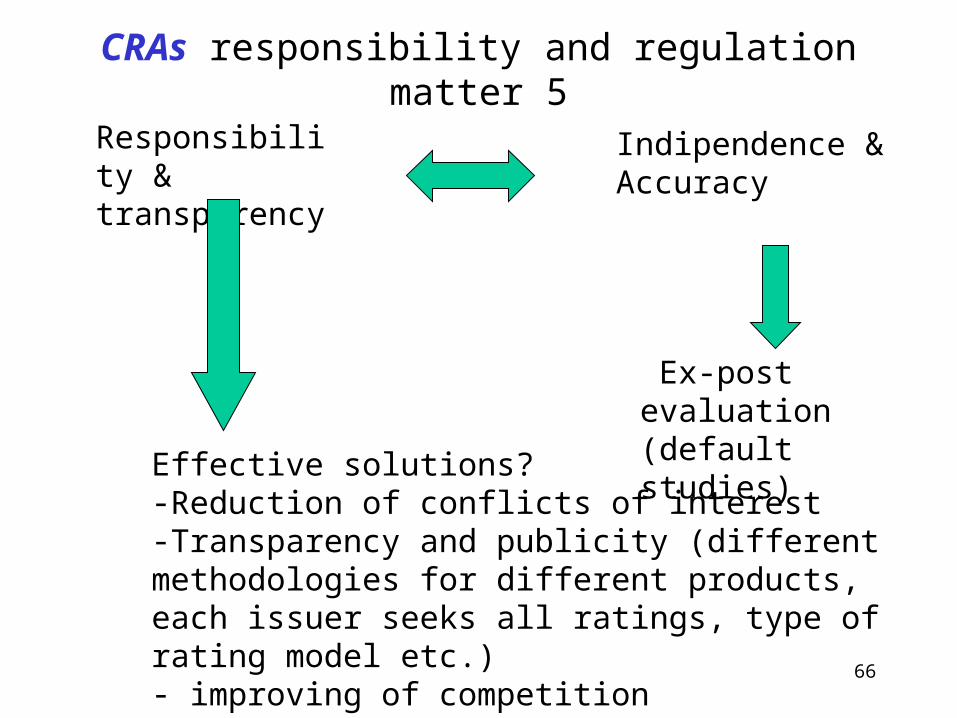

CRAs responsibility and regulation matter 5

Responsibility & transparency

Indipendence &Accuracy

Ex-post evaluation(default studies)

Effective solutions?-Reduction of conflicts of interest-Transparency and publicity (different methodologies for different products, each issuer seeks all ratings, type of rating model etc.)- improving of competition- awareness in using ratings by market participants

67

CRAs responsibility and regulation matter 5

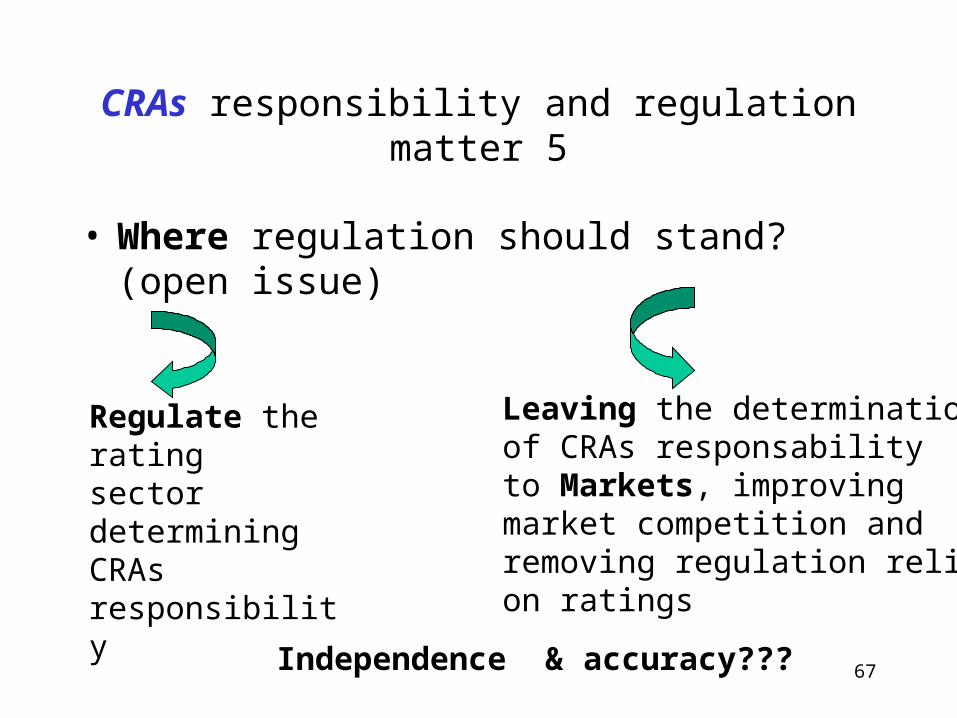

• Where regulation should stand? (open issue)

Regulate the rating sector determining CRAs responsibility

Leaving the determinationof CRAs responsability to Markets, improving market competition and removing regulation relianceon ratings

Independence & accuracy???

68

References - 1

Amato & Furfine (2004) Are credit ratings procyclical?, JBF.Ammer & Packer (2000) How Consistent Are Credit Ratings? A Geographic and Sectoral Analysis of

Default Risk, FRB WP 668.Bhatia (2002) Sovereign Credit Rating Methodology: An Evaluation, IMF WP 170.BCBS (1999) Supervisory Lessons To Be Drawn From The Asian Crisis, Basel Committee on Banking

Supervision WP 2, June.BCBS (2000) Credit Ratings And Complementary Sources of Credit Quality Information, Basel

Committee on Banking Supervision WP 3, August.Bissoondoyal-Bheenick (2004) Rating timing differences between the two leading agencies: Standard

and Poor’s and Moody’s, Emerging Markets Review.Block & Vaaler (2004) The price of democracy: sovereign risk ratings, bond spreads and political

business cycles in developing countries, Journal of International Money and Finance.Bongini, Laeven & Majnoni (2002) How good is the market at assessing bank fragility? A horse race

between different indicators, JBF.Boot, Milbourn & Schmeits (2004) Credit Ratings as Coordinating Mechanism, July WP.Burnie & Langsam (2004), How SOX affects investing through credit rating agencies, Journal of

Corporate Accounting and Finance.

Cappiello, Hördahl, Kadareja & Manganelli (2006) The impact of the Euro on Financial Markets, ECB wp No. 598.

Carlson & Hale (2004) Courage to Capital? A Model of the Effects of Rating Agencies on Sovereign Debt Roll–over, Yale University, mimeo.

Covitz & Harrison (2003) Testing Conflicts of Interest at Bond Ratings Agencies with Market Anticipation: Evidence that Reputation Incentives Dominate, FRB WP 200368.

69

References - 2

Dichev & Piotroski (2001) The long-run stock returns following bond ratings changes, Journal of Finance.

Ederington, Yawitz & Roberts (1987) The Informational Content of Bond Ratings”, Journal of Financial Research.

Ferri (2004) More Analysts, Better Ratings: Do Rating Agencies Invest Enough in Less Developed Countries?, Journal of Applied Economics.

Ferri & Lacitignola (2007) Does Europe Need Its Own Rating Agencies?, presented at the XVI International Tor Vergata Conference on Banking and Finance.

Ferri & Liu (2004) Assessing the Effort of Rating Agencies in Emerging Economies: Some Empirical Evidence, European Journal of Finance.

Ferri & Liu (2003) How Do Global Credit Rating Agencies Rate Firms from Developing Countries?, Asian Economic Papers, December.

Ferri, Liu & Majnoni (2001) The Role of Rating Agency Assessments in Less Developed Countries: Impact of The Proposed Basel Guidelines, Journal of Banking and Finance, 25, 115-48.

Ferri, Liu & Stiglitz (1999) The Procyclical Role of Rating Agencies: Evidence from the East Asian Crisis, Economic Notes, 28, 335-56.

Ferri & Lacitignola (2009) Le agenzie di rating tra crisi e rilancio della Finanza Globale, ed. Il Mulino.Gonzalez, Haas, Johannes, Persson, Toledo, Violi, Wieland & Zins (2004) Market Dynamics Associated

With Credit Ratings A Literature Review, ECB occasional paper.

Hartmann, Maddaloni & Manganelli (2003) The Euro area Financial System: structure, integration and policy initiatives, ECB wp No. 230.

Hill (2004) Regulating the Rating Agencies, Washington University Law Quarterly.

70

References - 3

Hu, Kiesel & Perraudin (2004) The estimation of transition matrices for sovereign credit ratings, JBF.Hull, Predescu & White (2004) The relationship between credit default swap spreads, bond yields, and credit rating

announcements, JBF.IMF (1999) Capital Market Developments, IMF, Washington DC.JCIF (1999, 2000, 2001) Characteristics & Appraisal of Major Rating Companies.Johnson (2003) An examination of rating agencies’ actions around the investment-grade boundary, FRB Kansas City

RWP 03-01.Kaminsky & Schmukler (2002) Emerging Market Instability: Do Sovereign Ratings Affect Country Risk and Stock

Returns?, The World Bank Economic Review.Kawai (1997) Link Between Spreads and Ratings in the Samurai Bond Market, published in Japanese.Kawai (2002) Recent Issues on Credit Rating Agencies in Asia, JBF.Kliger & Sarig (2000) The Information Value of Bond Ratings, Journal of FinanceKräussl (2003) Do Credit Rating Agencies Add to the Dynamics of Emerging Market Crises?, Center for Financial

Studies (Goethe-Universität Frankfurt am Main), WP 18.Kurosawa Y.(1999) Economics of rating (in giapponese), Tokyo, PHP Research Institute Inc.Lacitignola (2007) The Role of Information in Financial Markets: New Investigations on the Function of Rating

Agencies, Ph.D. thesis, University of Bari. Löffler (2004) Avoiding the rating bounce: why rating agencies are slow to react to new information, Journal of

Economic Behavior & Organization.

Lowenstein R. (2008) Triple-A-Failure, in «New York Times Magazine», 27 aprile.Mulder & Perrelli (2001) Foreign Currency Credit Ratings for Emerging Market Economies; IMF: WP 191.Monfort & Mulder (2000) The Impact of Using Sovereign Ratings by Credit Rating Agencies on the Capital

Requirements for Banks: a Study of Emerging Market Economies, IMF WP/69.Mora (2004) Sovereign Credit Ratings: Guilty beyond Reasonable Doubt?, American University of Beirut, mimeo

71

References - 4

Nickell, Perraudin & Varotto (2000) Stability of rating transitions, JBF.Norden & Weber (2004) Informational efficiency of credit default swap and stock markets:

The impact of credit rating announcements, JBF.Packer & Reynolds (1997) The Samurai Bond Market, Current Issues in Economics &

Finance, FRBNY, June.Packer (2000) Credit Ratings and the Japanese Corporate Bond Market, IMES DP E-9.Partnoy (1999) The Siskel and Ebert of Financial Markets?: Two Thumbs Down for the

Credit Rating Agencies, Washington University Law Quarterly.Poon (2003) Are unsolicited credit ratings biased downward?, JBF.Reinhart (2002) Default, Currency Crises and Sovereign Credit Ratings, NBER WP 8738.Reisen & von Maltzan (1999) Boom and Bust and Sovereign Ratings, International

Finance.Schaede (2004) The “Middle Risk Gap” and Financial System Reform: Small Firm

Financing in Japan, IMES DP E-11.Shin & Moore (2003) Explaining credit rating differences between Japanese and U.S.

agencies, Review of Financial Economics.

Skreta V. e L. Veldkamp (2009), Rating Shopping and Asset Complexity: a Theory of Ratings Inflation, Journal of Monetary Economics, forthcoming.

Sy (2002) Emerging market bond spreads and sovereign credit ratings: reconciling market views with economic fundamentals, Emerging Markets Review.

Sy (2004) Rating the rating agencies: Anticipating currency crises or debt crises?, JBF.

72

References - 5Sylla (2001) A Historical Primer on the Business of Credit Ratings, Conference on “The

Role of Credit Reporting Systems in the International Economy” World Bank, March 1-2.

Violi (2004) Credit Ratings Transition in Structured Finance, Banca d’Italia, mimeo.Wei (2003) A multi-factor, credit migration model for sovereign and corporate debts,

Journal of International Money and Finance.White (2001) The Credit Rating Industry: An Industrial Organization Analysis, NYU Stern

Business School, wp.Zhang (2003) What did the credit market expect of Argentina default? Evidence from

default swap data; FRB WP 25.

Related Documents