www.coveredbondreport.com July 2011 Fall of the sovereign Will covered bonds rise amid the ruin? CRD IV Everything to play for Canada Rules and legislates ICMA Anti-whispering campaign The Covered Bond Report

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.coveredbondreport.com July 2011

Fall of the sovereign

Will covered bonds rise amid the ruin?

CRD IVEverything to play for

CanadaRules and legislates

ICMAAnti-whispering campaign

The CoveredBond Report

Covered bonds?

Highly rated covered bonds backed by mortgages

Average LTV of 60.5%

Match-funded structure

Core capital ratio of 18.6%

Largest mortgage bond issuer in Europe

nykredit.com/ir

Figures as of 17 March 2011

July 2011 The Covered Bond Report 1

CONTENTS

FROM THE EDITOR

3 It’s all in the timing

MONITOR

5 Legislation & regulation

11 Ratings

15 Market

20 People

22

5

15

Cover StorySOVEREIGNS VERSUS COVERED

22 Fall of the sovereign

Sue Rust reports.

The CoveredBond Report

2 The Covered Bond Report July 2011

The CoveredBond Report

30

CRD IV: GAME ON

30 Everything to play for

Neil Day

CANADIAN MOMENTUM

36 Canada rules and legislates

Maiya Keidan

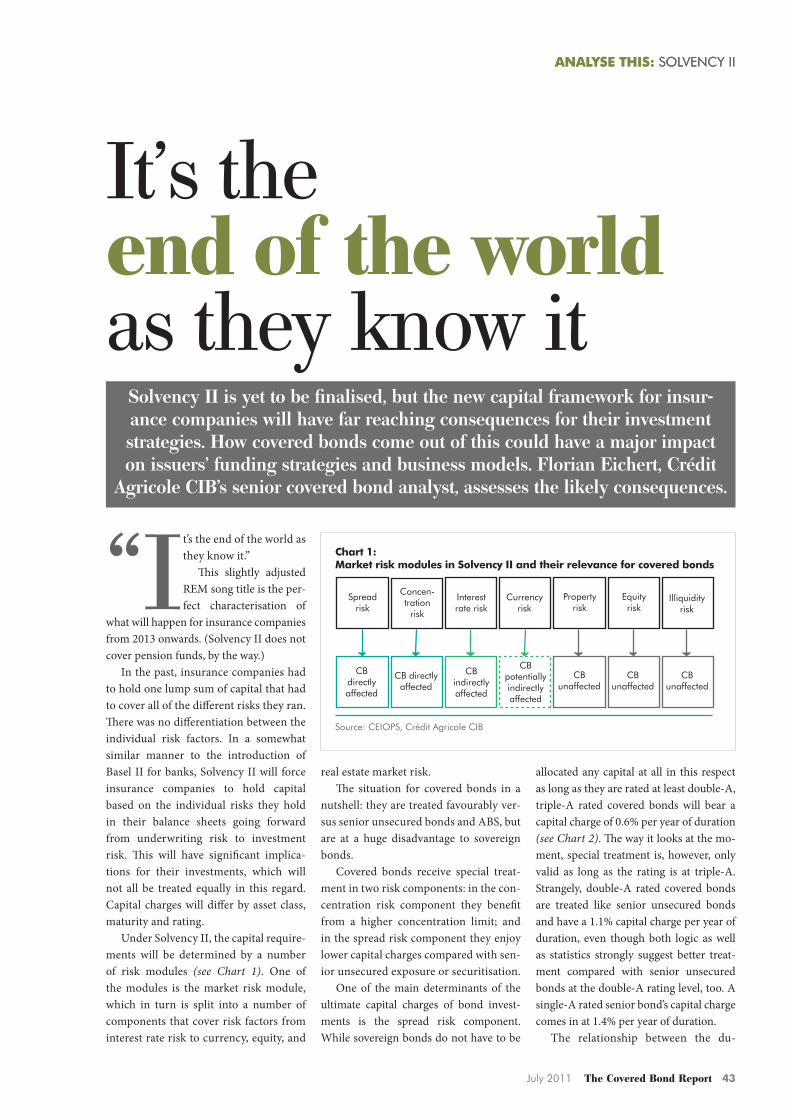

ANALYSE THIS: SOLVENCY II

42 It’s the end of the world as they know it

FULL DISCLOSURE

49 From fairway to oche

36

42

CONTENTS

FROM THE EDITOR

July 2011 The Covered Bond Report 3

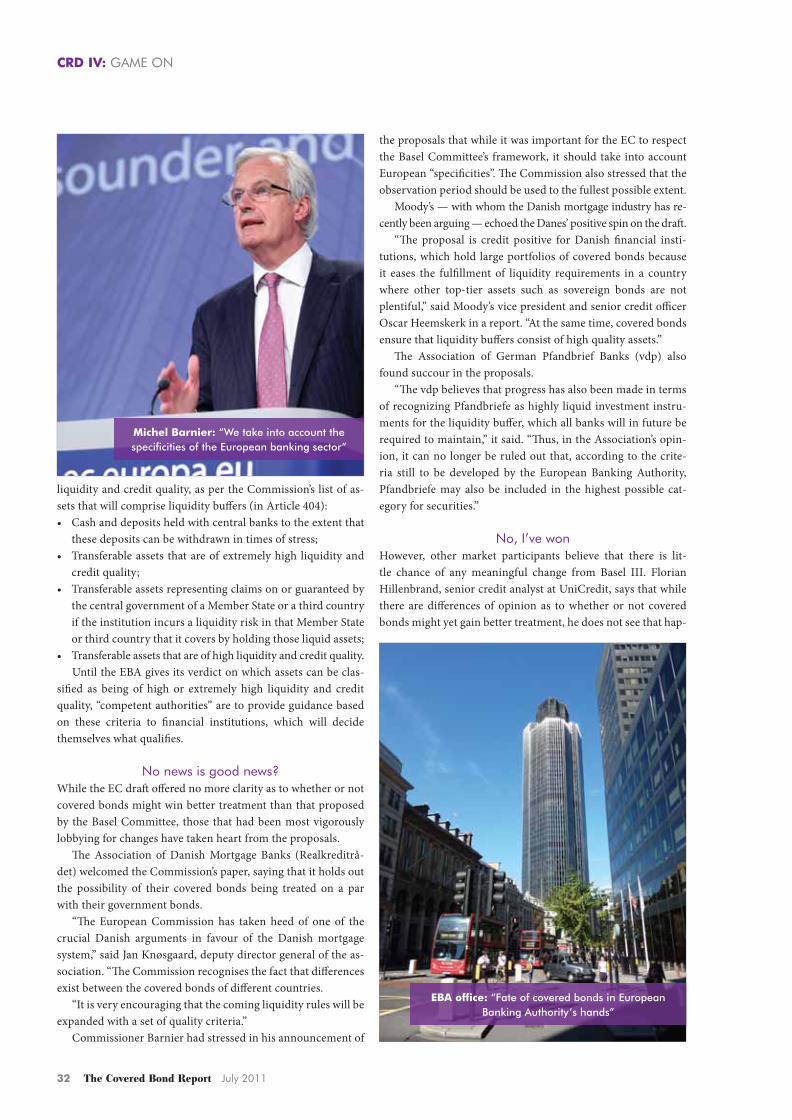

Would the European Commission’s

CRD IV proposals have been more

definite in a less uncertain world?

Merely publishing a timely

and relevant magazine is fraught

enough without the fate of the

euro-zone changing on a daily basis. Producing an inter-

national framework that will see the financial system safely

through its ups and Lehmans is asking for trouble at any

time — even more so when a euro-zone sovereign is on the

verge of defaulting.

Small wonder that the EC passed on most of the big

decisions, leaving the European Banking Authority to

carry the can. Would Commissioner Barnier really have

stood up and declared sovereign debt to be the nec plus ultra of liquid assets a day before haircuts for Greek

bondholders were revealed?

That said, leaked drafts of the EC proposals seen by

The Covered Bond Report suggest that the decision to

leave open a final definition of liquid assets was not taken

at the last minute. However, this should only give en-

couragement to covered bond supporters, some of whom

have already taken heart from being offered a second op-

portunity to lobby for better treatment.

What the Commission did lay down, though, was a

tough wish-list for the EBA to use when examining which

asset classes are fit for liquidity buffers. To name but three: a

proven record of price stability; maximum bid/ask spreads;

and transparent pricing and post-trade information.

While the list of criteria is welcome in that it gives

everyone a clearer idea of what needs to be done to win

over the EBA, satisfying them will be no easy task. Is the

covered bond industry up to the challenge?

Four years have now passed since the onset of the

crisis and in many of these areas little progress has been

made. Less time remains until implementation in 2015,

let alone until the EBA reports back to the Commission.

The clock is ticking.

It’s all in the timing

The CoveredBond Reportwww.coveredbondreport.com

EditorialManaging Editor Neil Day

+44 20 7415 [email protected]

Deputy Editor Sue [email protected]

Reporter Maiya [email protected]

Design & ProductionCreative Director: Garrett FallonSenior Designer: Sheldon Pink

PrintingWyndeham Grange Ltd

Advertising [email protected]

Subscriber [email protected]

The Covered Bond Report is a Newtype Media publication

25, Finsbury Business Centre40 Bowling Green Lane

London EC1R 0NE+44 20 7415 7185

www.coveredbondreport.com July 2011

Fall of the sovereign

Will covered bonds rise amid the ruin?

CRD IVEverything to play for

CanadaRules and legislates

ICMAAnti-whispering campaign

The CoveredBond Report

The CoveredBond Report

Did you know that The Covered Bond Report has its own database of benchmarks?

Did you know that we link directly from bond data to relevant coverage?

Did you know that we include price guidance, book sizes and distribution statistics?

Did you know that you can run league tables by country and currency?

To register for trial access to The Covered Bond Report, visit news.coveredbondreport.com or contact Neil Day, Managing Editor, at [email protected]. And don’t forget: if you are an investor in covered bonds you can qualify for free access to the website.

The Covered Bond Report is not only a magazine, but also a website providing news, analysis and data on the market.

July 2011 The Covered Bond Report 5

MONITOR: LEGISLATION & REGULATION

Stark and potentially unbridgeable di-

visions between the FDIC and covered

bond proponents led by Republican Con-

gressman Scott Garrett were laid bare as

the House Financial Services Committee

passed the United States Covered Bonds

Act of 2011 on 22 June.

Garrett complained of a breakdown in

communications with the regulator while

former HFSC chairman Democrat Bar-

ney Frank tried to introduce two amend-

ments at the behest of the FDIC that the

Republican said would render the bill

ineff ective.

And although FDIC chairman Sheila

Bair’s term of offi ce ended in July, cov-

ered bond supporters already fear that

her expected successor, Martin Gruen-

berg, will adopt a similar stance and

place obstacles in the way of the develop-

ment of a US market.

Garrett’s bill — co-sponsored by

Democrat Carolyn Maloney — was ulti-

mately passed by a comfortable 44 votes

to seven, but the potential pitfalls facing

the proposed legislation on its way to

being signed into law were laid bare by

votes on Frank’s amendments. Although

Garrett warned that “you would no long-

er have a covered bond marketplace” if

the amendments were passed, they were

only narrowly defeated, each by 28 ayes

to 26 nays.

Frank’s amendments would have giv-

en the FDIC more far-reaching powers

than those envisaged in Garrett’s legisla-

tion. Frank said that his fi rst amendment

had been draft ed in close co-operation

with the FDIC, which he said was con-

cerned not with the concept of covered

bonds, but the extent to which it and the

Deposit Insurance Fund are protected.

The amendments would have al-

lowed the FDIC to repudiate covered

bonds following a bank default and

would have capped maximum overcol-

lateralisation levels and after the hearing

Moody’s backed up Garrett by saying

that “both would have hurt the develop-

ment of the market”.

“Th e repudiation power in the re-

jected amendment was better for inves-

tors than the FDIC’s current repudiation

power because the amendment required

the FDIC to pay off investors in full rather

than up to the market value of the cover

pool,” said the rating agency. “However,

the amendment would have exposed in-

vestors to an early pay-off , which existing

covered bond investors do not want.

“Furthermore, a cap on the amount

of overcollateralisation would reduce the

resiliency of covered bonds, preventing

issuers from adding collateral to main-

tain the credit strength of the covered

bonds if the issuer deteriorates.”

Concerns addressed ‘time and time again’

Garrett pointed out that an earlier ver-

sion of the bill that had contained less

protection for the FDIC had been passed

by the committee last year under the

chairmanship of Barney Frank with bi-

partisan support, including that of Frank.

Garrett went on to say that he noted

that Frank had enjoyed “a positive work-

ing relationship and dialogue with the

FDIC”, before saying:

“Would that it be the case that we had

continued to have that relationship with

the FDIC as well. I thought we had it for a

long period of time and members on the

other side of the aisle, their staff knows

that we engaged in numerous hours of

staff to staff discussions on various por-

tions of the bill, but I will point out that

that for some reason or another, despite

those ongoing discussions that we were

able to continue to have on a member to

member and staff to staff member level

here in the House, the FDIC, for what-

ever reason, decided to stop responding

to our staff ’s e-mails.

“So as of last week those aspects of

discussions that we would want to have

with the FDIC came to an abrupt halt.

We were sending over e-mails as to what

UNITED STATES

FDIC fi ght ahead after bill passes

Will Martin Gruenberg take over Sheila Bair’s position?

“The FDIC decided to stop responding to our staff’s e-mails”

Legislation & Regulation

6 The Covered Bond Report July 2011

MONITOR: LEGISLATION & REGULATION

we thought we could do to improve the

bill to make changes to address their

concerns, and those ended at that point

in time.”

Garrett went on to say that while he

was pleased that member to member dis-

cussions could continue, he could not sup-

port Frank’s amendment because of what

he said it would lead to: “Th ere would not

be any investors interested in the market-

place were this amendment to pass.”

He said that Frank’s amendments

would introduce too much uncertainty

into the instruments, such that investors

would either not be interested in them or

only at a price that would not make them

viable. He went on to point out several

ways in which the diff erent versions of

bills he has introduced had progressively

included more and more concessions

to the FDIC over more than two years,

“time and time again”.

HFSC chairman, Republican Spen-

cer Bachus, also said that the com-

mittee had “tried very hard to accom-

modate the FDIC”, which had, he said,

only the day before indicated that it

had three problems with the bill that

were being addressed.

Reconciliation impossible?Frank responded by acknowledging that

there was a clear diff erence of opinion

between the FDIC and those pushing for

covered bonds. He said that those sup-

porting the bill had “overestimated” the

extent to which agreement with the FDIC

had been reached.

Two amendments that offered con-

cessions to the FDIC were nevertheless

approved.

One, from Democrat Carolyn

Maloney, co-sponsor of the bill, extends

from 180 days to one year the period the

FDIC has to fi nd an institution to take

over a covered bond programme in the

event it is appointed conservator or re-

ceiver of a failed issuer.

Maloney said that the FDIC support-

ed the amendment, which she said was

designed to give the regulator as much

fl exibility as possible and to protect the

Deposit Insurance Fund. Th e FDIC had

argued that it is more diffi cult to sell off

a covered bond programme than other

banks’ assets and products, particularly if

a number of institutions are failing.

An amendment allowing a covered

bond issuer’s regulator to place a cap on

covered bond issuance relative to total

assets was approved. Th is was introduced

by Republican John Campbell, who had

expressed disapproval of the bill in a sub-

committee markup in May but ultimately

voted in favour of the bill. He said that

the possibility of including a number had

been discussed, but that this would be left

to regulators rather than legislated for.

Th e FDIC has previously set a 4% limit.

The end of Bair’s term as chairman

had held out the prospect of a change in

the FDIC’s position, but there have al-

ready been signs that acting chairman

Martin Gruenberg will adopt a similar

position to his predecessor. DBRS, for

example, suggested this might be the

case in mid-July when discussing lob-

bying of the FDIC to relinquish its first

right to cover pool assets in the event of

an issuer default.

“Vice chairman of the FDIC Martin

Gruenberg, who some believe will be

President Obama’s choice to succeed

Chairman Bair, recently reiterated a

variation of this position stating that in

the event of a bank failure, the FDIC,

and not investors, should have first

rights to any excess collateral included

in a covered-bond offering,” said the

rating agency.

Th ere are also fears that time could be

running out for legislation to be passed

in this Congress. While the HFSC vote

and Republican control should smooth

the bill’s passage through the House of

Representatives, observers are less cer-

tain about the Senate.

“Th e length of the remaining legisla-

tive calendar has become a serious con-

sideration, particularly for Senate ac-

tion,” said Jerry Marlatt, senior of counsel

at Morrison Foerster. “Th e Senate has not

previously considered a covered bond

bill and, accordingly, there is much to be

done for the Senate staff to be prepared

to take informed positions on a bill. Per-

haps the most important factor in mov-

ing a bill quickly through the Senate will

be who sponsors the bill.

“As previously reported, Senator

Charles Schumer (D-NY), who is a key

senator on the Senate Banking Com-

mittee, has said that he would consider

introducing a covered bond statute.

Sponsorship by Senator Schumer would

greatly enhance the prospects for the bill

moving quickly.”

“The legislative calendar has

become a serious consideration”

Barney Frank: supporters of bill overestimated any agreement with FDIC

July 2011 The Covered Bond Report 7

AUSTRIA

Forum discusses steps to uniform lawMoves towards harmonising Austria’s covered bonds under a single law were discussed at the first conference of the Österreichisches Pfandbrief und Cov-ered Bond Forum at the end of May.

According to DZ Bank covered bond analyst Michael Spies, representatives of the Austrian central bank (Oesterrei-chische Nationalbank) and the finance ministry said that the harmonisation of laws governing Austrian covered bonds would be on their agenda.

Martin Schweitzer, speaking on be-half of the Österreichisches Pfandbrief und Covered Bond Forum, told The Covered Bond Report that a single cov-ered bond law was not imminent but

would be the ultimate outcome of work to improve the Austrian framework.

“We are heading towards one law,” he said. “But before that there will definitely be intermediary steps to further harmo-nise the existing ‘two-plus’ frameworks.

“There will be harmonisation in terms of transparency, in terms of fur-ther quality improvements.”

Austrian covered bonds are either Pfandbriefe issued under the Mortgage Banking Act, which in 2005 brought together the old Mortgage Banking Act and the Pfandbrief Law, or Fundi-erte Bankschuldverschreibungen. Er-ste Group Bank and UniCredit Bank Austria, for example, issue under the

Mortgage Banking Act, while Kommu-nalkredit Austria and Bawag PSK issue Fundierte Bankschuldverschreibungen.

The Österreichisches Pfandbrief und Covered Bond Forum was launched in January by Austria’s leading covered bond issuers, representing Bawag PSK, Erste Group, Kommunalkredit Austria, Österreichische Volksbanken, Raiffeisen Bankengruppe, UniCredit Bank Austria, and Hypoverband.

Schweitzer said that the forum would not only be working on legisla-tive changes.

“It’s about transparency in the market, speaking with one voice, and being vis-ible on the European stage,” he said.

MONITOR: LEGISLATION & REGULATION

The prospect of standalone covered bond

issuance from South Korean banks has

increased following the release of covered

bond guidelines by the country’s regula-

tors in late June.

The Financial Services Commission

(FSC) and Financial Supervisory Service

(FSS) described the guidelines as part of

measures to implement “Comprehensive

Measures on Household Debt”.

“The guidelines are intended to pro-

vide a framework for covered bond issu-

ances, diversifying banks’ financing in-

struments and encouraging banks to offer

more long term and fixed rate mortgage

loans instead of short term and floating

rate ones,” said the FSC and the FSS.

The “best practice guidelines” run to a

mere two pages, but contain rules on key

features of issuance — see box.

Issuers permitted under the guidelines

include banks, agricultural and fishery

co-operatives, the Korean Development

Bank, Export-Import Bank of Korea, In-

dustrial Bank of Korea, and securitisation

vehicles under the Act on Asset-Backed

Securitization.

The cover pool may comprise: first

priority mortgage loans with maximum

secured amounts of 120% or more of the

actual loan amount, a 70% loan-to-value

cap, and no delinquencies in excess of 60

days; cash; ABS backed by such mortgage

loans or cash; mortgage backed bonds is-

sued by Korea Housing Finance Corpora-

tion (KHFC); and mortgage backed secu-

rities issued by KHFC.

“After monitoring the issuances of cov-

ered bonds in the future, we will have fur-

ther discussions on whether to come up

with legally binding regulations on cov-

ered bond issuances,” said the regulators.

Jerome Cheng, vice president, senior

credit officer at Moody’s, told The Covered

Bond Report that the establishment of a

covered bond framework has been under

discussion for quite some time.

“Market participants have been lobby-

ing government to enact a law or publish

guidelines,” he said. “From market par-

ticipants’ perspective, having guidelines

will allow originators to structure covered

bonds with a higher degree of certainty.

“The guidelines, which we have not yet

assessed, should give additional comfort

to investors.”

Previously only one Korean bank has

issued a covered bond on a standalone

basis — Kookmin Bank, with a $1bn is-

sue in 2009. State-run KHFC sold a sec-

ond international covered bond issue — a

$500m five year — on 18 July, but its issu-

ance is under an act governing the insti-

tution and the bond is backed by pooled

collateral from its member banks.

SOUTH KOREA

Korean rules raise solo supply hopesKey features of Korea’s guidelines:

or greater

of total liabilities

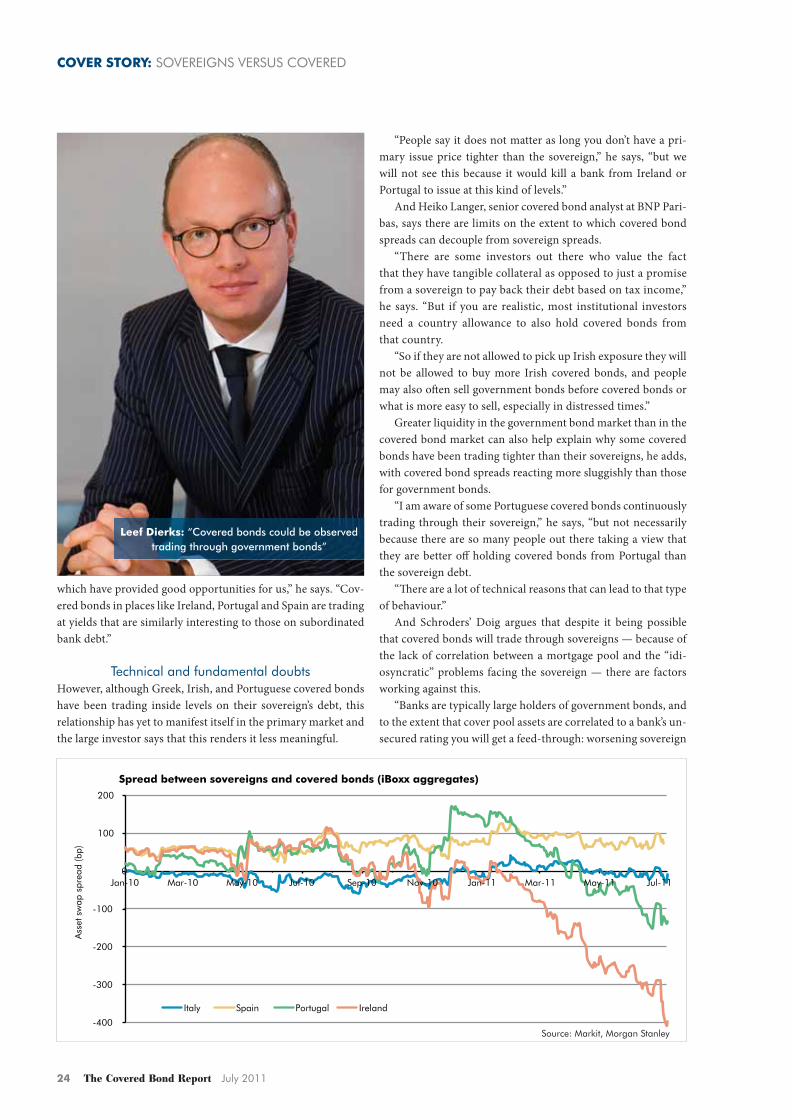

“Covered bonds could be observed trading through government bonds” page 24

8 The Covered Bond Report July 2011

MONITOR: LEGISLATION & REGULATION

ECBC DATA

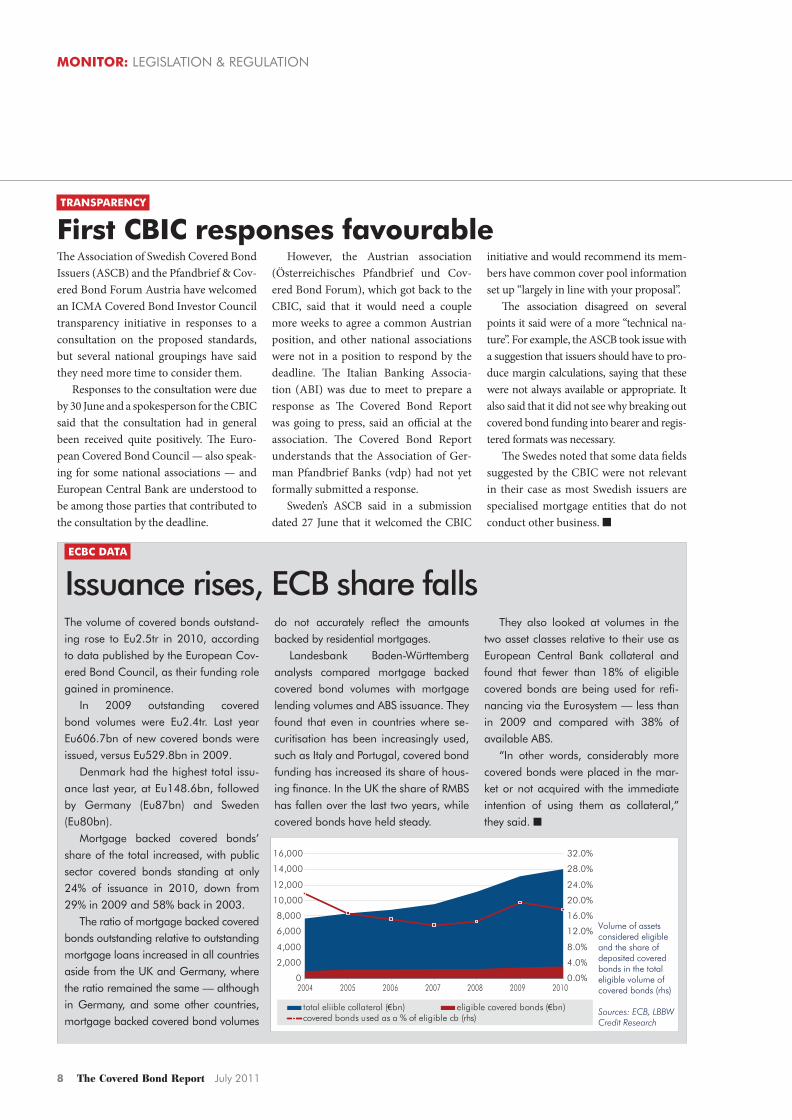

Issuance rises, ECB share fallsThe volume of covered bonds outstand-ing rose to Eu2.5tr in 2010, according to data published by the European Cov-ered Bond Council, as their funding role gained in prominence.

In 2009 outstanding covered bond volumes were Eu2.4tr. Last year Eu606.7bn of new covered bonds were issued, versus Eu529.8bn in 2009.

Denmark had the highest total issu-ance last year, at Eu148.6bn, followed by Germany (Eu87bn) and Sweden (Eu80bn).

Mortgage backed covered bonds’ share of the total increased, with public sector covered bonds standing at only 24% of issuance in 2010, down from 29% in 2009 and 58% back in 2003.

The ratio of mortgage backed covered bonds outstanding relative to outstanding mortgage loans increased in all countries aside from the UK and Germany, where the ratio remained the same — although in Germany, and some other countries, mortgage backed covered bond volumes

do not accurately reflect the amounts backed by residential mortgages.

Landesbank Baden-Württemberg analysts compared mortgage backed covered bond volumes with mortgage lending volumes and ABS issuance. They found that even in countries where se-curitisation has been increasingly used, such as Italy and Portugal, covered bond funding has increased its share of hous-ing finance. In the UK the share of RMBS has fallen over the last two years, while covered bonds have held steady.

They also looked at volumes in the two asset classes relative to their use as European Central Bank collateral and found that fewer than 18% of eligible covered bonds are being used for refi-nancing via the Eurosystem — less than in 2009 and compared with 38% of available ABS.

“In other words, considerably more covered bonds were placed in the mar-ket or not acquired with the immediate intention of using them as collateral,” they said.

The Association of Swedish Covered Bond

Issuers (ASCB) and the Pfandbrief & Cov-

ered Bond Forum Austria have welcomed

an ICMA Covered Bond Investor Council

transparency initiative in responses to a

consultation on the proposed standards,

but several national groupings have said

they need more time to consider them.

Responses to the consultation were due

by 30 June and a spokesperson for the CBIC

said that the consultation had in general

been received quite positively. The Euro-

pean Covered Bond Council — also speak-

ing for some national associations — and

European Central Bank are understood to

be among those parties that contributed to

the consultation by the deadline.

However, the Austrian association

(Österreichisches Pfandbrief und Cov-

ered Bond Forum), which got back to the

CBIC, said that it would need a couple

more weeks to agree a common Austrian

position, and other national associations

were not in a position to respond by the

deadline. The Italian Banking Associa-

tion (ABI) was due to meet to prepare a

response as The Covered Bond Report

was going to press, said an official at the

association. The Covered Bond Report

understands that the Association of Ger-

man Pfandbrief Banks (vdp) had not yet

formally submitted a response.

Sweden’s ASCB said in a submission

dated 27 June that it welcomed the CBIC

initiative and would recommend its mem-

bers have common cover pool information

set up “largely in line with your proposal”.

The association disagreed on several

points it said were of a more “technical na-

ture”. For example, the ASCB took issue with

a suggestion that issuers should have to pro-

duce margin calculations, saying that these

were not always available or appropriate. It

also said that it did not see why breaking out

covered bond funding into bearer and regis-

tered formats was necessary.

The Swedes noted that some data fields

suggested by the CBIC were not relevant

in their case as most Swedish issuers are

specialised mortgage entities that do not

conduct other business.

TRANSPARENCY

First CBIC responses favourable

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2004 2005 2006 2007 2008 2009 20100.0%

4.0%

8.0%

12.0%

16.0%

20.0%

24.0%

28.0%

32.0%

total eliible collateral (€bn) eligible covered bonds (€bn)covered bonds used as a % of eligible cb (rhs)

Volume of assets considered eligible and the share of deposited covered bonds in the total eligible volume of covered bonds (rhs)

Sources: ECB, LBBW Credit Research

July 2011 The Covered Bond Report 9

MONITOR: LEGISLATION UK

The Investment Management Asso-

ciation believes UK Regulated Covered

Bonds lack “the very high degree of

certainty” that should be expected of a

regulated product, and that the frame-

work needs more significant changes

than those being proposed in a review.

In its response to a consultation on

proposals announced in April by HM

Treasury and the Financial Services Au-

thority, which ended on 1 July, the IMA

said that it was unfortunate that, as be-

fore the UK framework’s introduction

in 2008, it was not pre-consulted on re-

form proposals.

“Th is is unfortunate since it would ap-

pear that an assumption has been made

that the regime needs little change, where-

as we would argue that it might benefi t

from more signifi cant change,” said Jane

Lowe, the IMA’s director of markets.

The association outlined several con-

cerns relating to the transparency and

structure of UK RCBs, and urged HM

Treasury to tackle these, even if such re-

form was not envisaged in the timetable

for the review of the framework.

“For investors, the RCB regime is

lacking the very high degree of certainty

that should be expected of a regulated

product,” said the IMA. “For issuers, the

regime runs the risk that over time it

will fail to attract long term stable inves-

tors into the product.

“If the impact of bank resolution and

bail-in extends also to the RCB regime,

this is likely to lead to a gradual with-

drawal of long term investors from bank

funding, leaving banks with a different

and probably less stable investor base.”

Some market participants had sug-

gested that such bail-in questions might

have been sufficiently addressed when

the review was announced. However,

the IMA said that the introduction of

bail-ins of senior debt might affect the

RCB regime and that to maintain inves-

tor confidence the RCB should be clear-

ly carved out of bail-in requirements.

“This is particularly important as

in contrast to many EU RCB regimes,

a UK RCB is a senior unsecured bond

and only becomes ‘secured’ by way of a

guarantee on ‘default’,” said the associa-

tion. “In a special resolution situation,

this means that the guarantee may not

be triggered under the relevant contract

because the issuer is not deemed to be

in default.”

Investor data demands confl ictThe IMA said that covered bonds have

been increasingly taken up by its mem-

bers in the past year but that they have

not found the documentation “user-

friendly”.

“Key information is frequently bur-

ied deep within detailed prospectuses

(400+ pages is not unusual),” said the

IMA. “Whilst they are able to manage

this, we question why it should be nec-

essary for a regulated product.”

The association argues in favour of

disclosure of loan level data in line with

Bank of England requirements.

“This is a much needed measure to

improve investor confidence and trans-

parency for Regulated Covered Bonds,”

it said.

However, the Covered Bond Investor

Council said in a response to the con-

sultation that loan-by-loan disclosure

of cover pool assets, as required by the

Bank of England, “would contaminate

the reputation of high quality the cov-

ered bonds product has in the market”.

Asset backed securitisation (ABS)

products and covered bonds need to

be distinguished, it said, in particular

with respect to the level of information

required.

“Covered bond pools need to be

monitored by investors but maybe not

nearly as frequently as ABS pools as

long as the pool is fairly elitist from

its creation onwards and substitution

mechanisms are in place,” said the coun-

cil, which has called for aggregated data

it believes would be more useful. The

dynamic nature of cover pools makes

regular loan-level disclosure superflu-

ous, it added.

Th e level of transparency that inves-

tors should be provided with was the

only point of contention raised in the

CBIC’s submission, with the council say-

ing that it is “generally positive” toward

the changes proposed by the review.

RCB REVIEW

IMA cites weaknesses in UK consultationJane Lowe: “It might benefi t

from more signifi cant change.”

“Key information is frequently buried”

“Sovereign investors are more vulnerable to potential haircuts” page 25

10 The Covered Bond Report July 2011

MONITOR: LEGISLATION & REGULATION

Recent amendments to Spain’s legal

framework for mortgage loans weaken

creditors’ recourse to low income borrow-

ers, but preserves full recourse mecha-

nisms in the Spanish market, according to

Fitch and Moody’s.

Spain’s parliament passed a resolu-

tion, Royal Decree 8/2011, on 30 June

that, among other changes, increases the

threshold of defaulted borrower income

that is ring-fenced from a claiming credi-

tor. The new law became effective on 7

July, and was put forward by the ruling So-

cialist party, the main opposition People’s

Party and Catalan group Convergencia i

Union, demonstrating widespread sup-

port for the move.

Alvaro Gil, director, covered bonds at

Fitch, said that a motivation behind ini-

tiatives to end or modify full recourse was

the large number of legal cases for repos-

sessions since 2008. There have also been

recent protests in support of borrowers

facing repossession.

According to statistics from the Span-

ish judicial system cited by Moody’s, the

number of foreclosures reached 93,000 in

2010, up 260% from 2007 levels. Fitch said

that legal cases for repossessions since

2008 totalled 240,000.

Under Spanish law mortgage borrow-

ers remain personally liable for their debt

after foreclosure, instead of being able, as

is the case in some countries, to discharge

that debt in bankruptcy.

“Full recourse to current and future as-

sets and income of the obligor is system-

atically used by banks to ensure full re-

covery on defaulted mortgages when the

foreclosed property value at auction does

not cover the outstanding debt,” said Car-

los Masip, director, RMBS at Fitch.

The rating agency said that although

newly approved changes to Spain’s mort-

gage loan framework may reduce the

strength of full recourse from a cashflow

perspective, in particular for low income

borrowers in negative equity situations,

it continues to consider the Spanish debt

market as one featuring full recourse.

“Fitch recognises that there are many

disincentives that a sensible borrower will

consider before defaulting on its mortgage

loan to take advantage of the newly-ap-

proved measures,” it said.

Such disincentives include the alterna-

tive costs of occupancy such as property

rental or the potential loss of fiscal ben-

efits, according to Fitch.

“The full recourse mechanism over

borrower’s existing and future assets per-

sists by law, and would disqualify default-

ed borrowers from owning other assets or

from generating additional income in the

future,” it said.

In Fitch’s view the new law could trig-

ger a tightening effect on mortgage under-

writing policies, in particular with regards

to loan-to-value ratios for low income

borrowers.

Moody’s said that the revised frame-

work introduces three main changes. A

first involves raising the threshold that full

recourse to a defaulted borrower’s exist-

ing and future income is applicable to, a

change that Moody’s described as “cur-

tailing the rights of creditors to attach the

wages of borrowers who default on their

mortgage loans”.

But it said that this measure will have

a negligible impact on the Spanish RMBS

market because most of a mortgage loan’s

recovery stems from the effective sale of

a property, and not from the personal li-

ability remaining against a mortgage bor-

rower if the foreclosure process ends with

any debt outstanding.

The new framework also raises the

minimum percentage of the property

value – from 50% to 60% – at which a

bank can repossess a mortgaged property

if the foreclosure process ends with no

offers. Carlos Terre, director, structured

credit at Fitch, said this will shift poten-

tial losses from the obligors’ side to the

banks’ side, but that the rating agency

considers the effect on recovery assump-

tions to be neutral.

Moody’s highlighted a third amend-

ment, which reduces the amount that a

party has to deposit upfront to participate

at a property auction.

“Lowering the liquidity require-

ment may attract more bidders; the third

amendment may thus be considered cred-

it-positive, so long as it forms an incentive

for third parties to bid at mortgage auc-

tions,” said Moody’s.

SPAIN

Full recourse withstands populist move

Source: Plataforma Afectados por la Hipoteca

“Incentives to repay are still in force”

July 2011 The Covered Bond Report 11

SOLVENCY II

Covered to keep shine despite low returns

MONITOR: RATINGS

Bayerische Landesbank put on hold a

new covered bond issue on 6 July in re-

sponse to Moody’s that morning plac-

ing its Pfandbrief ratings on review for

downgrade alongside those of three oth-

er public sector banks.

“Since announcing a 10 year Jumbo

Öff entliche Pfandbriefe transaction yes-

terday, BayernLB has achieved a strong

momentum in the shadow order book

process,” the issuer said in a statement.

“However, the issuer has decided to delay

marketing the transaction following the

Moody’s announcement this morning.

“BayernLB would like to express their

thanks to those investors who have al-

ready shown their support. Th e decision

was taken in the interest of protecting

BayernLB’s investor base.”

Crédit Agricole, Credit Suisse, Deut-

sche Bank and Royal Bank of Scotland

had the mandate for the transaction and

a syndicate offi cial at one of the leads said

that preparations for the transaction had

gone very well, and that the decision to not

proceed was taken solely on the basis of

Moody’s action, which he described as “ab-

solutely unprecedented” and “ridiculous”.

“We had a good IoI book and were

ready to go,” he said.

BayernLB’s mortgage and public sec-

tor covered bonds are rated triple-A by

Moody’s, but the ratings were placed on

review for possible downgrade alongside

those of Pfandbriefe issued by HSH Nor-

dbank, WestLB, and Deutsche Kredit-

bank, aft er Moody’s placed the respective

issuer ratings on review for downgrade

the previous week.

A covered bond analyst described

Moody’s action with respect to BayernLB’s

public sector Pfandbriefe as a sign of the

rating agency’s willingness “to go the edge”

given that the rating of the public sector

covered bonds could sustain a three notch

issuer downgrade before being cut, accord-

ing to the rating agency’s methodology.

MOODY’S

‘Unprecedented’ move blocks BayernLB deal

BayernLB: “Had a good IoI book and was ready to go.”

Full implementation in 2013 of Sol-

vency II rules in their latest iteration

could lower the appeal of covered bonds

on the basis of their capital-adjusted

returns and thereby render them more

expensive to issue, according to Fitch.

However, the rating agency said in a

June report that the security the asset

class off ers means they will remain at-

tractive to insurers.

Th is dynamic would be one among

many — such as a shift from long term

to shorter term debt, and an increase in

the attractiveness of higher rated corpo-

rate debt and government bonds — that

would occur as a result of insurers, the

largest investor group in Europe, mak-

ing signifi cant changes to their asset

portfolios to optimise their capital posi-

tions, according to Fitch.

In a summary introducing the re-

port, the rating agency said that an in-

crease in the attractiveness of covered

bonds would be one of the main eff ects

of insurers adjusting their asset portfo-

lios to optimise capital positions.

However, in a section dedicated to

covered bonds the rating agency said

that although triple-A rated covered

bonds have a lower capital charge than

other corporates, “the charge is rela-

tively punitive compared with the risk

and returns currently available, making

them less attractive than other bonds on

a pure return-on-capital basis under the

(credit) spread module” (see chart).

With banks under pressure to in-

crease funding, a reduction in demand

could increase covered bond pricing,

the report added.

However, Fitch ended its assessment

of the impact on covered bonds on a

positive note, saying that the asset class

is likely to remain attractive to insurers

because of their “very safe nature”.

Comparison of Bond Returns under Solvency II (Taking into account cost of capital)

Issuer (Dated) Duration Rating Category Standalone capital charge* –standard formula (%)

Spread overswap (bps)

Return onequity (%)

Tesco (2014) 2.5 ‘A’ 3.5% (2* , 1.4%) 50 14.0

BAA (2041) 14 ‘A’ 19.6% (14*, 1.4%) 200 10.2

Deutsche Bank covered bond (2018) 6 ‘AAA’ 3.6% (6*, 0.6%) 10 7.8

* assuming duration matching using swaps. Source: Bloomberg, Fitch

Ratings

12 The Covered Bond Report July 2011

MONITOR: RATINGS

A revised approach to Danish covered

bonds from Moody’s resulting in nega-

tive rating actions has raised tensions

with Danish issuers, leading to Realkredit

Danmark terminating its collaboration

with the rating agency and others seeking

ways to escape the rating pressure.

Moody’s on 10 June increased the refi -

nancing margins and lowered the Timely

Payment Indicator (TPI) from “very

high” to “high” for the covered bonds

of fi ve Danish issuers, citing increased

refi nancing risk due to a material rise in

adjustable-rate mortgage (ARM) loans,

and reduced systemic support and cred-

itworthiness.

Among measures taken by Danish

mortgage banks in response to Moody’s

move was Realkredit Danmark’s decision

to drop the rating agency.

“Realkredit Danmark has discussed

the fundamentals of the matter with

Moody’s in order to understand the ra-

tionale behind its rating model, but has

concluded that the parties disagree about

the fundamentals,” it said on 23 June.

Moody’s went on to cut three Danish

mortgage credit institutions’ issuer rat-

ings on 1 July and lowered covered bonds

issued out of BRFkredit Capital Centre E

from Aa1 to Aa2.

However, with the Danish commu-

nity increasingly vocal in its criticism

of the rating agency, Moody’s put out a

special comment on the Danish covered

bond system in which its strengths were

highlighted.

“Despite weakening issuer credit

strength and our assessment of increased

refi nancing risk, the position of Den-

mark as having one of the strongest cov-

ered bond frameworks in Europe has not

changed,” said Moody’s, adding that the

new refi nancing margins are the lowest

in Europe and that the TPIs are among

the highest in Europe.

Moody’s methodological revisions

coincide with increased scrutiny of

Denmark’s mortgage financing system

by the country’s central bank, which has

highlighted a reduction in refinancing

risk linked to ARM loans and a reduc-

tion in risks surrounding continuous

loan-to-value requirements as ways in

which financial stability needs to be

strengthened.

Th ese recommendations and Moody’s

changes were among “future business

conditions” cited by Nykredit Realkredit

in an announcement from 21 June setting

out a fi ve point operational plan. Th is in-

cludes funding ARM loans with bonds is-

sued out of a special capital centre so that

these “may be given an independent, and

possibly lower, rating leading to lower

overcollateralisation requirements as a

result of Moody’s announcement”.

Surprised and confusedRealkredit Danmark will also establish a

new capital centre for the fi nancing of its

ARM loans, but in contrast to Nykredit

decided not to continue its collaboration

with Moody’s.

“Th e decision was taken because

Moody’s, as a result of its model calcula-

tions, demanded that Realkredit Danmark

provide an additional excess cover of

Dkr32.5bn (Eu4.36bn) if it wanted to keep

its current AAA rating,” said the issuer.

Realkredit Danmark said that it is in the

position to provide excess cover through

the issuance of junior covered bonds or

through a loan from its parent, Danske

Bank, but Moody’s on 14 July placed on re-

view for downgrade covered bonds issued

out of the issuer’s Capital Centre S because

the collateral had not yet been added.

Other rating agencies could gain from

the fall-out, with Realkredit Danmark

potentially turning from Moody’s to

Fitch — Standard & Poor’s already rates

its covered bonds AAA.

BRFkredit is in talks with S&P about

rating its capital centres aft er saying that

it was “surprised and unable to under-

stand” Moody’s actions. Th e move was

announced on 6 July as one of a pack-

age of measures from BRFkredit, which

Moody’s cut to Baa3 on 1 July.

Th e bank said that it will keep Moody’s

as a “co-operation partner” and establish

a new capital centre (H) that will prima-

rily refi nance ARM loans, in line with

Nykredit Realkredit’s and Realkredit

Danmark’s plans.

Th e issuer had made a commitment

in the documentation of covered bonds

issued out of capital centre E to maintain

a Aa1 rating by injecting capital if nec-

essary, but BRFkredit said that Moody’s

methodology made achieving such a rat-

ing impossible.

DENMARK

Danes up in arms amid Moody’s fall-out

Moody’s offi ces in New York

“The parties disagree about the

fundamentals”

July 2011 The Covered Bond Report 13

MONITOR: RATINGS

COUNTERPARTY CRITERIA

S&P hears warnings about proposals’ effectStandard & Poor’s proposals for assess-ing counterparty risk in covered bonds would have a disproportionate effect on ratings compared with asset-liability mismatch (ALMM) risk, issuers and in-vestors have told the rating agency.

They consider counterparty risk to be mainly an issuer risk, with investors pleased at the prospect of increased trans-parency about derivative counterparty risks in programmes, said S&P in an interim re-port published on 7 June.

However, the rating agency said that the majority of investors and issuers ap-peared to view counterparty risk as sec-ondary to an issuer’s ability to pay its covered bond obligations.

“Most investors and issuers consid-ered that counterparty risk, if assessed using the 2011 request for comment as

currently proposed, would have a dis-proportionate effect on covered bond ratings compared with asset-liability mismatch risk, as assessed using the ‘2009 ALMM criteria’,” said S&P.

DZ Bank analyst Jörg Homey drew at-tention to S&P disclosing that many issuers would consider the move to cap covered bond ratings by reference to the rating agency’s new counterparty criteria as — in Homey’s words — an “over-reaction”.

S&P said it will respond to feedback “by changing the criteria if we deem it necessary, by explaining the original pro-posals more clearly to remove ambiguity, or by leaving the proposals unchanged”.

Homey said that programmes where the issuer acts as a counterparty will be hit particularly hard.

“The decisive question in this case

is probably going to be whether S&P is satisfi ed by the precautions taken to replace the bank as counterparty for its own cover assets in the event of a downgrade,” he said.

Increased issuance of covered bonds and

renewed repo activity raise asset encum-

brance issues, according to Fitch, but the

rating agency sees the trend easing, even

if bank funding costs remain elevated.

Regulatory reforms, increased risk aver-

sion and other measures pushing the asset

class to the fore have led to greater use of

covered bonds, said the rating agency in a

report in June, adding that the increased

take-up of the asset class will hit a peak.

“Fitch believes that the limited supply

of high quality cover pool assets and na-

tional regulatory limits, if properly mon-

itored and enforced, serve as checks to

the use of covered bonds, allaying some

investor concerns over high issuance vol-

umes in recent months,” it said.

Th e rating agency said that a high de-

pendence on secured funding could con-

strain ratings and that an over-reliance

on this type of fi nancing could encumber

most assets on the company’s balance

sheet, reducing overall fi nancial fl exibility.

“In addition, a high concentration of

secured fi nancing increases the risk that

unsecured creditors could be adversely af-

fected as secured creditors may have prior-

ity claims to higher-quality assets,” it said.

“If the industry shift s to a signifi cantly

higher level of secured funding versus his-

torical levels, Issuer Default Ratings (IDRs)

could come under pressure and unsecured

debt ratings could fall below the IDR due to

lower recovery expectations.”

Fitch nevertheless noted the benefi ts

covered bonds can carry for issuers from

a ratings perspective.

“Most global trading banks did not

have a covered bond programme prior

to the crisis, but many have established

such programmes in the past two years,”

it said. “As such, the use of covered bonds

by these banks remains limited, but rep-

resents a funding source off ering poten-

tial diversifi cation and maturity exten-

sion benefi ts. Th is potential has yet to be

fully tapped by these banks.”

FITCH

Encumbrance a concern, but checks exist

Jörg Homey: Rating cap seen as “over-reaction”

New Issuance in Debt Markets (Euro Zone) Excludes issues <USD50mCovered bonds (not retained) Covered bonds (retained) Senior unsecured debt(USDbn)

700600500400300200100

0

Source: Dealogic, Fitch

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

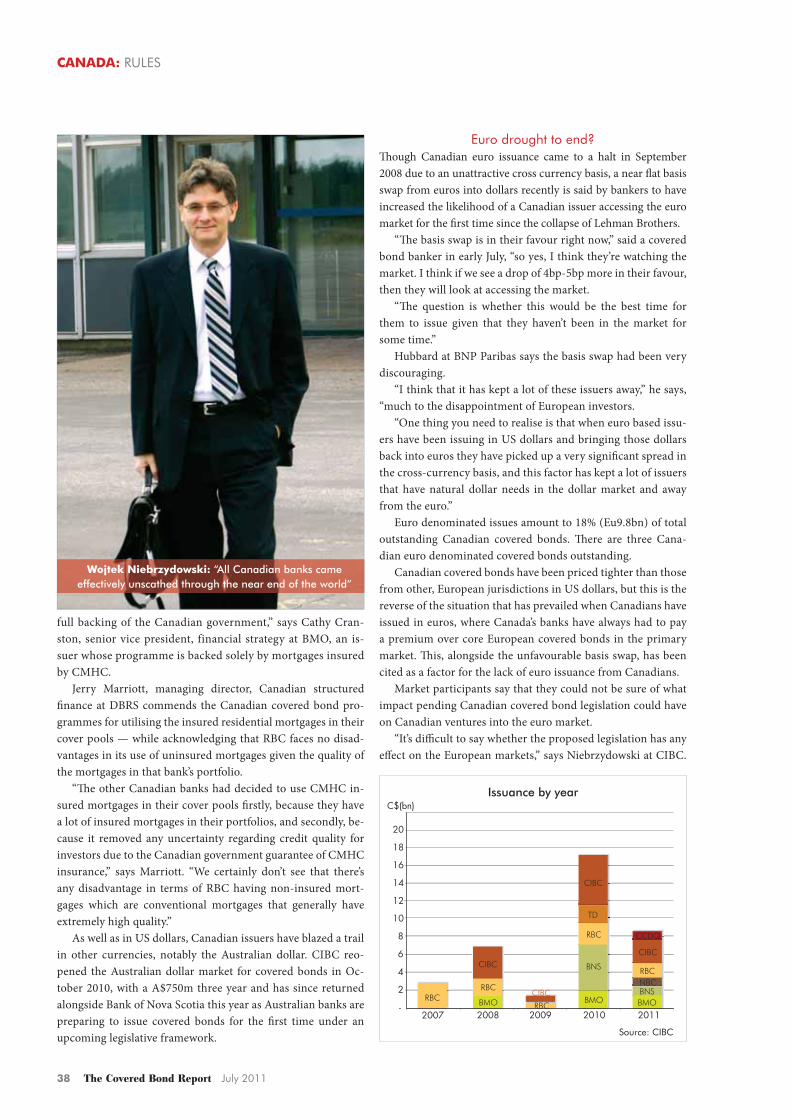

“You look at the debt-to-GDP ratio in Canada, it’s very impressive indeed” page 39

14 The Covered Bond Report July 2011

MONITOR: RATINGS

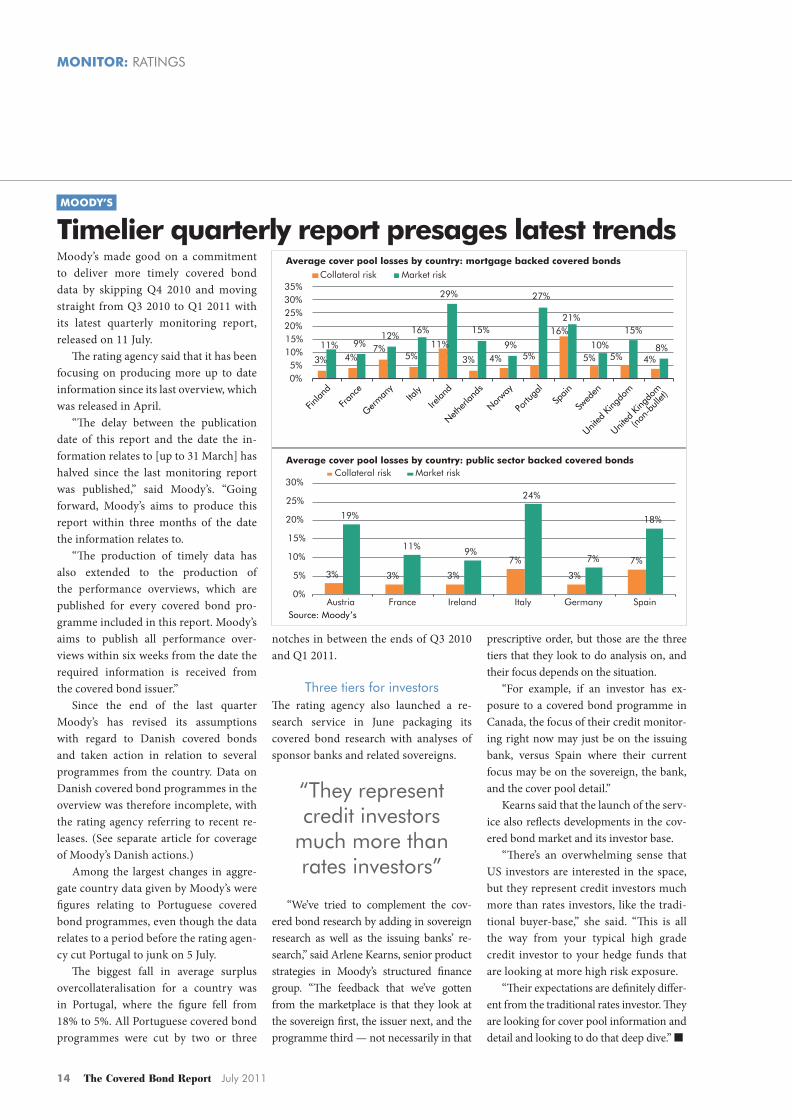

Moody’s made good on a commitment

to deliver more timely covered bond

data by skipping Q4 2010 and moving

straight from Q3 2010 to Q1 2011 with

its latest quarterly monitoring report,

released on 11 July.

The rating agency said that it has been

focusing on producing more up to date

information since its last overview, which

was released in April.

“The delay between the publication

date of this report and the date the in-

formation relates to [up to 31 March] has

halved since the last monitoring report

was published,” said Moody’s. “Going

forward, Moody’s aims to produce this

report within three months of the date

the information relates to.

“The production of timely data has

also extended to the production of

the performance overviews, which are

published for every covered bond pro-

gramme included in this report. Moody’s

aims to publish all performance over-

views within six weeks from the date the

required information is received from

the covered bond issuer.”

Since the end of the last quarter

Moody’s has revised its assumptions

with regard to Danish covered bonds

and taken action in relation to several

programmes from the country. Data on

Danish covered bond programmes in the

overview was therefore incomplete, with

the rating agency referring to recent re-

leases. (See separate article for coverage

of Moody’s Danish actions.)

Among the largest changes in aggre-

gate country data given by Moody’s were

figures relating to Portuguese covered

bond programmes, even though the data

relates to a period before the rating agen-

cy cut Portugal to junk on 5 July.

The biggest fall in average surplus

overcollateralisation for a country was

in Portugal, where the figure fell from

18% to 5%. All Portuguese covered bond

programmes were cut by two or three

notches in between the ends of Q3 2010

and Q1 2011.

Three tiers for investorsThe rating agency also launched a re-

search service in June packaging its

covered bond research with analyses of

sponsor banks and related sovereigns.

“We’ve tried to complement the cov-

ered bond research by adding in sovereign

research as well as the issuing banks’ re-

search,” said Arlene Kearns, senior product

strategies in Moody’s structured finance

group. “The feedback that we’ve gotten

from the marketplace is that they look at

the sovereign first, the issuer next, and the

programme third — not necessarily in that

prescriptive order, but those are the three

tiers that they look to do analysis on, and

their focus depends on the situation.

“For example, if an investor has ex-

posure to a covered bond programme in

Canada, the focus of their credit monitor-

ing right now may just be on the issuing

bank, versus Spain where their current

focus may be on the sovereign, the bank,

and the cover pool detail.”

Kearns said that the launch of the serv-

ice also reflects developments in the cov-

ered bond market and its investor base.

“There’s an overwhelming sense that

US investors are interested in the space,

but they represent credit investors much

more than rates investors, like the tradi-

tional buyer-base,” she said. “This is all

the way from your typical high grade

credit investor to your hedge funds that

are looking at more high risk exposure.

“Their expectations are definitely differ-

ent from the traditional rates investor. They

are looking for cover pool information and

detail and looking to do that deep dive.”

MOODY’S

Timelier quarterly report presages latest trendsAverage cover pool losses by country: mortgage backed covered bonds

Average cover pool losses by country: public sector backed covered bonds

3% 4%7%

5%11%

3% 4% 5%

16%

5% 5% 4%

11% 9%12%

16%

29%

15%

9%

27%

21%

10%

15%

8%

0%5%

10%15%20%25%30%35%

Collateral risk Market risk

3% 3% 3%

7%

3%

7%

19%

11% 9%

24%

7%

18%

0%

5%

10%

15%

20%

25%

30%

Austria France Ireland Italy Germany Spain

Collateral risk Market risk

Finlan

d

Fran

ce

Germ

any

Italy

Irelan

d

Nether

lands

Norway

Portu

gal

Spain

Swed

en

United

King

dom

United

King

dom

(non-

bulle

t)

Source: Moody’s

“They represent credit investors

much more than rates investors”

July 2011 The Covered Bond Report 15

MONITOR: MARKET

Syndicate bankers are awaiting the details

of prospective ICMA best practice guide-

lines to see if primary market practices

will have to change in ways that could in-

crease execution risk for covered bonds,

resulting in issuers having to pay higher

new issue premiums.

Th e International Capital Market Asso-

ciation (ICMA) is working toward a set of

best practice guidelines aimed at increas-

ing transparency in new issues, through

changes to the way in which information

is communicated at various stages of the

new issue process. Any such guidelines

could aff ect the practice of price whisper-

ing, with the release of updates on order

book sizes also under scrutiny.

Banks’ eff orts to get in line with the

impending guidelines have already had an

impact on the primary market.

When Landesbank Baden-Württem-

berg sold a debut benchmark mortgage

Pfandbrief on 4 July, a Eu500m six year

deal, leads Natixis, LBBW, Royal Bank

of Scotland and UniCredit launched the

deal without having gone out with a price

whisper, despite market conditions being

fragile, if stable.

Jörg Huber, head of funding and investor

relations, treasury at LBBW, said that initial

feedback was positive, but non-committal in

the absence of a pricing indication.

“Unfortunately there was recently an

ICMA announcement recommending not

to use price whispers,” he told Th e Cov-

ered Bond Report, “which makes it quite

diffi cult to fi nd the right clearing level.

“Th is meant that we couldn’t inform

the sales teams what our initial pricing

ideas were to get relevant feedback, so

it took a bit longer to establish what the

right level was.”

Th is was deemed to be represented

by the 18bp-19bp over mid-swaps range,

with the leads taking indications of inter-

est at that level and order books growing

quickly once they were offi cially opened,

according to Huber. Th e deal was ulti-

mately priced at 18bp over on the back of

a Eu750m order book.

“We hit it spot-on, but the proce-

dure could have been smoother,” he said.

“Th ese kinds of guidelines are harming

the proper evaluation process, but we had

to deal with that.”

Go the extra mileRuari Ewing, director, primary markets,

market practice and regulatory policy at

the International Capital Market Associa-

tion (ICMA), told Th e Covered Bond Re-

port that the association had in October

2010 added an explanatory memorandum

on pre-sounding, bookbuilding and allo-

cations to its handbook, and that several

roundtables with investors had been con-

ducted over the past couple of years, most

recently in May.

“Banks are now continuing their dis-

cussions internally, with some already

starting to draw conclusions and move

ahead with new practices,” he said.

One practice being scrutinised is that

of price whispers, which Ewing character-

ised as an interim step aft er pre-sounding

but before bookbuilding has begun on the

basis of offi cial guidance. He said that the

practice of price whispers had emerged in

response to the fi nancial and sovereign

debt crises.

“In an easy market you can go straight

to guidance, but in volatile markets you’re

dealing with a completely diff erent kettle

of fi sh,” he said.

Although price whispers can be shared

with many market participants, some are

arguing that the information needs to be

communicated to a larger audience, ac-

cording to Ewing.

“Th e aim is to go out much wider with

a whisper than before,” he said. “With in-

creasing volatility there is a feeling that it is

important to go the extra mile. Under the

old system you could always miss a hand-

ful of accounts, and this new approach is

trying to wrap up that residual end.”

In practice this means that banks are

looking at ways to modify their commu-

nication to better reach transactions’ tar-

get audiences, said Ewing, which could

involve sending information as they have

been doing but also potentially dissemi-

nating it by way of news-feeds, among

other options.

Th e Covered Bond Report under-

stands that ICMA has been seeking to

release a formal publication that would

most likely be in the form of an addition

to the association’s primary market hand-

book. However, it is not clear how detailed

or prescriptive this might be.

Broadbrush adoptionAlthough fi nal guidelines have not been

drawn up, syndicate offi cials said that

market participants have already been im-

plementing what one banker described as

“broadbrush” changes to new issue prac-

ICMA

Anti-whispering campaign ‘counterproductive’

Jörg Huber: “These kinds of guidelines are harming the proper

evaluation process.”

Market

16 The Covered Bond Report July 2011

MONITOR: MARKET

tices in line with where discussions have

been heading.

Syndicate bankers described ICMA’s

position as aiming to ensure that everyone

who could be involved in a transaction has

access to public information, with inves-

tors pushing to do away with whispers and

other practices that could involve them

being made privy to inside information

and/or wall-crossed. ICMA explains wall-

crossing as being sounded for a potential

transaction on the basis of information

that may amount to inside information

and that could make investors subject to

legal restrictions, such as restrictions on

trading in related securities.

A syndicate offi cial said that one out-

come of discussions taking place could be

that the term “whisper” is no longer used,

partly on account of its connotations of

secrecy.

Terminology is not likely to be the

only feature of primary market activity

set to change, however, with a syndicate

banker saying that the ideas under dis-

cussion will also change the dynamics of

pre-sounding.

“Pre-sounding will be on a more public

basis,” he said. “Th e process will be slightly

diff erent, designed to make it more trans-

parent.”

Another syndicate offi cial said that IC-

MA’s guidelines had left him unimpressed

because of the increased execution risk

they would involve for borrowers. Inves-

tors, on the other hand, deemed infor-

mation such as price whispers and order

book updates to be relevant.

Th e guidelines were “slightly confusing

and counterproductive”, said the syndicate

offi cial.

Th e debate in part echoes that that took

place in the covered bond market last year

when the Covered Bond Investor Council

(CBIC) in January 2010 called for an end

to the practice of building shadow order

books based on price whispers.

A leading covered bond investor told

Th e Covered Bond Report that his posi-

tion remained unchanged today and that

he is still dissatisfi ed with what he called

pre-sounding. It was unfair for only a

handful of investors to be given prelimi-

nary pricing thoughts, while others only

belatedly received this information and

had little time to place orders given short

bookbuilding periods, he said.

While issuers are eager to avoid execu-

tion risk, the portfolio manager said that

he did not consider there to be any stigma

attached to not completing a deal or hav-

ing to widen pricing, and that this could in

any case also happen if a new issue project

had been pre-sounded.

He urged a return to traditional deal

execution methods, citing high issuance

volumes this year and the lack of failed

transactions

“Th e crisis mode for covered bonds

doesn’t make sense,” he said.

Less fear of failure?Making it more diffi cult to arrive at the ap-

propriate initial guidance for a transaction

by prohibiting discreet discussions with a

small number of key investors would in-

crease execution risk or the risk of an issu-

er fi nding itself in a position where it has

to pull a deal. Th is could result in issuers

having to pay higher new issue premiums

to reduce such risks.

But some bankers questioned whether,

or the degree to which, any new measures

would aff ect new issues, saying that price

whispers already spread quickly and wide-

ly, perhaps reaching more market partici-

pants and journalists than was intended.

“To all intents and purposes, how

many deals have been out where you

haven’t heard a price whisper?” asked one

syndicate offi cial. “A cynic would argue

that if it is not in writing then it is easier to

more elegantly step back or adjust levels,

but I’m not 100% convinced by that.

“When it’s announced, it’s announced.”

Others said that those pulling deals

could in future be less stigmatised for

doing so. One syndicate banker said that

market participants’ judgements of pulled

deals had already eased over the past three

years, and that such occurrences were less

conversational.

He identifi ed the return of retention

deals as a possible outcome of any new

guidelines on the communication of up-

dates on order book sizes — something

that bankers said is also being debated. Th e

Covered Bond Report understands that

lead manager and trading orders being in-

cluded in order books that may otherwise

not be fully covered is a focus of scrutiny.

Th e syndicate offi cial said that a po-

tential clampdown on including lead

manager orders in order book sizes and/

or potentially requiring such orders to be

identifi ed separately could lead to the re-

turn of retention deals because such rules

would make it more diffi cult for banks to

give the impressions that deals are being

successfully handled in pot format.

“The crisis mode for covered bonds

doesn’t make sense.”

Ruari Ewing: “The aim is to go out much wider with a whisper.”

July 2011 The Covered Bond Report 17

MONITOR: MARKET

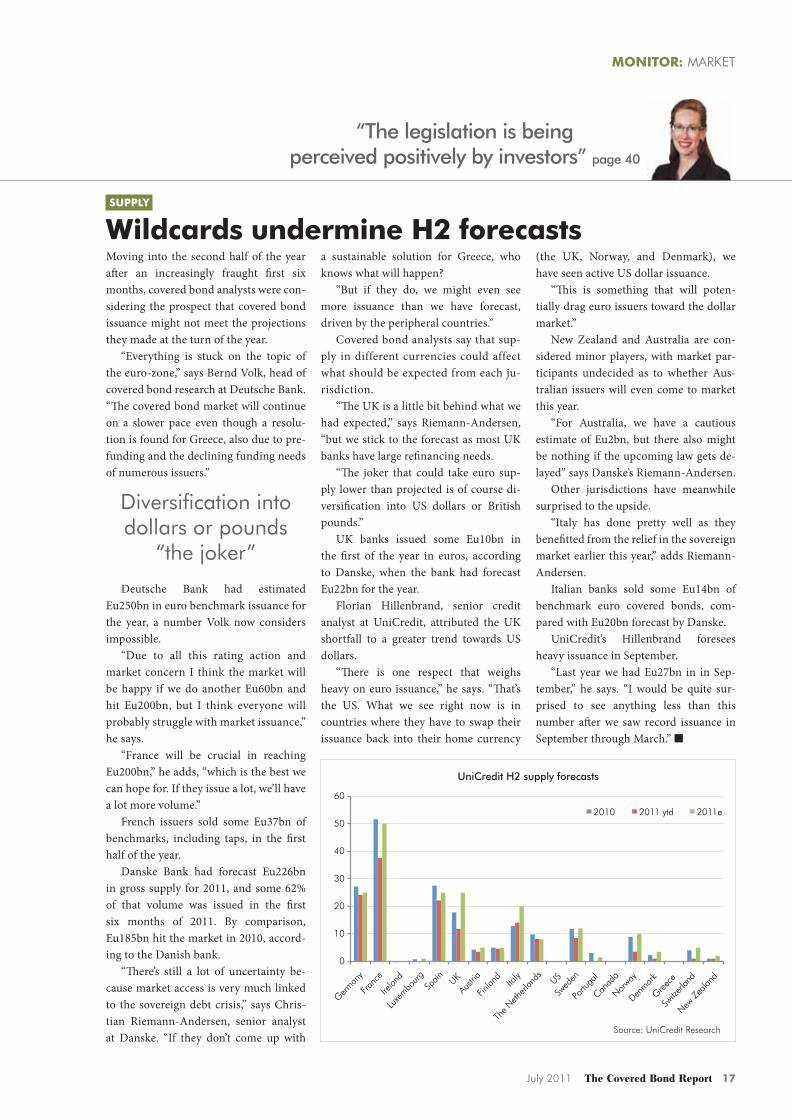

Moving into the second half of the year

after an increasingly fraught first six

months, covered bond analysts were con-

sidering the prospect that covered bond

issuance might not meet the projections

they made at the turn of the year.

“Everything is stuck on the topic of

the euro-zone,” says Bernd Volk, head of

covered bond research at Deutsche Bank.

“The covered bond market will continue

on a slower pace even though a resolu-

tion is found for Greece, also due to pre-

funding and the declining funding needs

of numerous issuers.”

Deutsche Bank had estimated

Eu250bn in euro benchmark issuance for

the year, a number Volk now considers

impossible.

“Due to all this rating action and

market concern I think the market will

be happy if we do another Eu60bn and

hit Eu200bn, but I think everyone will

probably struggle with market issuance,”

he says.

“France will be crucial in reaching

Eu200bn,” he adds, “which is the best we

can hope for. If they issue a lot, we’ll have

a lot more volume.”

French issuers sold some Eu37bn of

benchmarks, including taps, in the first

half of the year.

Danske Bank had forecast Eu226bn

in gross supply for 2011, and some 62%

of that volume was issued in the first

six months of 2011. By comparison,

Eu185bn hit the market in 2010, accord-

ing to the Danish bank.

“There’s still a lot of uncertainty be-

cause market access is very much linked

to the sovereign debt crisis,” says Chris-

tian Riemann-Andersen, senior analyst

at Danske. “If they don’t come up with

a sustainable solution for Greece, who

knows what will happen?

“But if they do, we might even see

more issuance than we have forecast,

driven by the peripheral countries.”

Covered bond analysts say that sup-

ply in different currencies could affect

what should be expected from each ju-

risdiction.

“The UK is a little bit behind what we

had expected,” says Riemann-Andersen,

“but we stick to the forecast as most UK

banks have large refinancing needs.

“The joker that could take euro sup-

ply lower than projected is of course di-

versification into US dollars or British

pounds.”

UK banks issued some Eu10bn in

the first of the year in euros, according

to Danske, when the bank had forecast

Eu22bn for the year.

Florian Hillenbrand, senior credit

analyst at UniCredit, attributed the UK

shortfall to a greater trend towards US

dollars.

“There is one respect that weighs

heavy on euro issuance,” he says. “That’s

the US. What we see right now is in

countries where they have to swap their

issuance back into their home currency

(the UK, Norway, and Denmark), we

have seen active US dollar issuance.

“This is something that will poten-

tially drag euro issuers toward the dollar

market.”

New Zealand and Australia are con-

sidered minor players, with market par-

ticipants undecided as to whether Aus-

tralian issuers will even come to market

this year.

“For Australia, we have a cautious

estimate of Eu2bn, but there also might

be nothing if the upcoming law gets de-

layed” says Danske’s Riemann-Andersen.

Other jurisdictions have meanwhile

surprised to the upside.

“Italy has done pretty well as they

benefitted from the relief in the sovereign

market earlier this year,” adds Riemann-

Andersen.

Italian banks sold some Eu14bn of

benchmark euro covered bonds, com-

pared with Eu20bn forecast by Danske.

UniCredit’s Hillenbrand foresees

heavy issuance in September.

“Last year we had Eu27bn in in Sep-

tember,” he says. “I would be quite sur-

prised to see anything less than this

number after we saw record issuance in

September through March.”

SUPPLY

Wildcards undermine H2 forecasts

0

10

20

30

40

50

60

German

y

Franc

e

Irelan

d

Luxe

mbour

g

Spain

UK

Austr

ia

Finlan

d Ita

ly

The N

etherl

ands

US

Swed

en

Portu

gal

Canad

a

Norway

Denmar

k

Greece

Switz

erlan

d

New Z

ealan

d

2010 2011 ytd 2011e

UniCredit H2 supply forecasts

Source: UniCredit Research

Diversification into dollars or pounds

“the joker”

“The legislation is being perceived positively by investors” page 40

18 The Covered Bond Report July 2011

MONITOR: MARKET

Westpac NZ fi nally came to the market

with its fi rst covered bond in early June

aft er postponing its plans in February,

but hopes of further supply from New

Zealand were dashed when ANZ Nation-

al postponed a debut, euro denominated

deal on 22 June.

In February Westpac NZ had cited

poor market conditions and an earth-

quake in New Zealand when delaying its

inaugural covered bond. But at its second

attempt, Westpac NZ’s leads — Barclays

Capital, BNP Paribas and UBS — built a

book of Eu1.3bn for the Eu1bn fi ve year

issue and priced it at 75bp over mid-

swaps on 9 June.

A Bank of New Zealand seven year

was the only other New Zealand covered

bond outstanding in euros and a syndi-

cate offi cial at one of Westpac NZ’s leads

said that this was trading in the low 70s

mid over swaps. BNZ issued its Eu1bn

seven year at 62bp over mid-swaps last

November.

A syndicate offi cial away from the

leads suggested pricing was more real-

istic than when Westpac NZ had previ-

ously approached the market.

“Th at was aft er the Christchurch

earthquake, but I don’t think they really

had a trade then,” he says.

Bankers said that they were somewhat

surprised at the level Westpac NZ needed

to pay given its qualities, and struggled to

explain why the New Zealand banks did

not trade tighter.

“Th e bank is relatively small,” suggest-

ed one, “even if it’s part of a bigger group,

and the fact that it is non-ECB collateral

doesn’t help.”

Th e New Zealand sector faced further

challenges in June when ANZ National

postponed a new issue project until aft er

the summer in light of rapidly deteriorat-

ing market conditions aft er having gone

on a roadshow for a debut covered bond.

A syndicate banker familiar with the

New Zealand bank’s plans said that feed-

back from the roadshow had been “quite

strong” but that as a well funded issuer

ANZ felt it did not need to rush to launch

a deal in such uncertain markets.

Aussie cheer for BNZ, DnB NorBNZ found conditions closer to home

more conducive, selling a debut, A$700m

(Eu512m) fi ve year covered bond at 88bp

over swaps on 7 June via HSBC, RBC and

RBS. Th is was larger than the A$500m

originally targeted, with oversubscrip-

tion also allowing pricing at the tight end

of the guidance of 88bp-90bp.

Comparing this with Westpac NZ’s

euro benchmark launched two days later,

a banker away from the two deals said

that BNZ’s level translated to around

30bp over Euribor, meaning that it had

saved about 45bp versus where Westpac

NZ had funded in euros.

DnB Nor Boligkreditt also found suc-

cess in Aussie dollars, becoming the fi rst

European issuer to sell a covered bond

in the currency since the onset of the fi -

nancial crisis when it sold a A$600m fi ve

year at 85bp over mid-swaps on 8 June

via ANZ, Deutsche Bank and HSBC.

“Th e target was to print a deal like

this, with a A$500m minimum size,”

Th or Tellefsen, senior vice president and

head of long term funding at DnB Nor,

told Th e Covered Bond Report. “For us

it’s all about investor diversifi cation.”

He said that the pricing was more or

less in line with what DnB Nor could

achieve in the US dollar covered bond

market or in euros. Th e proceeds of the

Australian dollar issue were swapped to

dollar Libor at 61bp — DnB Nor issued

a fi ve year dollar benchmark at the end

of March at 66bp over that was trading in

the high 50s.

AUSTRALIA/NEW ZEALAND

Westpac NZ on, but ANZ off, as Kiwis travel

Westpac NZ rescue helicopter

DnB Nor, Oslo

July 2011 The Covered Bond Report 19

MONITOR: MARKET

Issuers found the euro primary market in-

creasingly challenging through June and

the fi rst half of July, as investors retreated

fi rst to only names from core jurisdictions

and then onto the sidelines completely.

Greece proved to be a major wrecking

ball as the market awaited Greek prime

minister George Papandreou’s attempt to

withstand a vote of confi dence on 19 June

by reshuffl ing his cabinet and then pushing

through a new austerity package on 29 June.

A relief rally on the back of the success-

ful initiatives allowed Eu1bn plus of cov-

ered bond funding to be raised by Caisse

de Refi nancement de l’Habitat and BNP

Paribas Home Loans SFH, but the diffi -

culty of tapping into even such issuance

windows was demonstrated when Fin-

land’s OP Mortgage Bank struggled to get

a Eu1bn seven year away at the same time.

But worse was to come as fears of con-

tagion spread. Aft er Landesbank Baden-

Württemberg and CM-CIC Home Loan

SFH sold benchmarks in the fi rst full

week of July, benchmark euro issuance

came to a standstill.

“It’s a very quiet, very political mar-

ket,” said Christoph Alenfeld, syndicate

offi cial at DZ Bank. “It’s really turned

sour lately, and given the political situa-

tion, no one is really surprised by this.”

June had started well for Italian banks,

with UniCredit and Credito Emiliano

selling benchmarks — the latter its debut

covered bond. But the country took a hit

on 24 June when Moody’s placed covered

bond programmes of fi ve Italian fi nan-

cial institutions on review for possible

downgrade — the republic’s Aa2 rating

had been put on review a week earlier —

dashing the hopes of compatriots queu-

ing to issue.

However, Italy’s travails in the covered

bond market were minor in comparison

with Spain’s. Only one Spanish issuer ap-

proached the market and it found the

environment unwelcoming: a Eu1bn fi ve

year issue for Santander backed by public

sector collateral was widely criticised as

poorly timed and aggressively priced.

“Just because one day the indices are

trading better, it doesn’t mean that inves-

tors are going to wake up and decide that,

just having sold Spain, they are going to

start buying again,” said a syndicate offi -

cial away from the leads. “I wouldn’t have

recommended going ahead unless I want-

ed to be left with Eu100m on my book.”

However, some market participants

said that the overall performance of the

asset class in the face of tough economic

conditions had shown it in a positive light.

“Th e covered bond market has shown

a great amount of resilience to the situ-

ation in southern Europe,” said Per Høg

Jensen, vice president, DCM origination

at Danske Bank. “It’s a good testimony

to the market that deals still are getting

done in the covered space.”

He cited as an example a Eu500m fi ve

year mortgage Pfandbrief from newcom-

er ING-DiBa, which had been warmly re-

ceived on 22 June, with the order books

more than twice subscribed in spite of

what some market participants consid-

ered tight pricing.

EUROS

Issuers steer clear of Greek wrecking ball

Prime minister George Papandreou: survived two tests

0

100

200

300

400

500

600

700

800

900

11-rpA11-naJ01-tcO01-luJ

bp

iBoxx € France Covered Structured iBoxx € Netherlands Covered iBoxx € Portugal CoverediBoxx € Spain Covered iBoxx € UK Covered iBoxx € France Covered LegaliBoxx € Hypothekenpfandbriefe iBoxx € Ireland Covered iBoxx € Norway CoverediBoxx € Oeffentliche Pfandbriefe iBoxx € Sweden Covered iBoxx € Italy Covered

Spread performance by sector

Source: UniCredit Research

“OC ceiling could negatively impact investor confi dence” page 41

20 The Covered Bond Report July 2011

MONITOR: PEOPLE & INSTITUTIONS

LBBW

Rath heads for Commerz

Former UBS credit trader Michael Rudd

has joined RBC Capital Markets as a

director of its fi xed income platform in

New York.

Rudd will work closely with Catherine

Chere, a credit trader in London. RBC

said this will better enable it to provide

clients with the ability to trade covered

bonds and Yankee banks.

In January RBC hired Ben Colice as

head of covered bonds origination from

Barclays Capital.