The CDM: a review of its development and status of the carbon markets Dr. Oscar Coto II National CDM Workshop Belize August 2011

The CDM: a review of its development and status of the carbon markets Dr. Oscar Coto II National CDM Workshop Belize August 2011.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The CDM: a review of its development and status of the

carbon markets

Dr. Oscar Coto

II National CDM Workshop

Belize

August 2011

Topics

1. Responses to climate change and the CDM

2. Current trends in the CDM

3. Status of the carbon markets and expectations

Source: CC Sinthesys Report IPCC (2007)

Increase on key parameters

Relevant subject

Responses based on international and local levels, efficient and effective, with equity

both in

Mitigation as well as Adaptation

Responding to Climate Change

• Long and complex international negotiations

• UNFCCC in 1992

• The Kyoto Protocol in 1997

• On-going negotiations and dilemmas

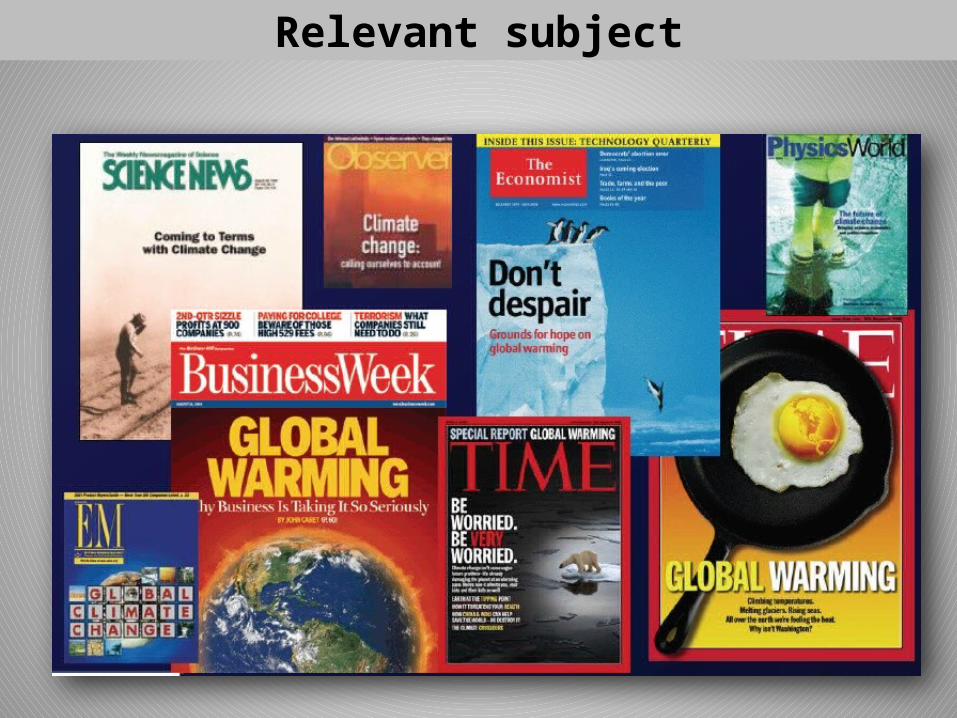

Looking back in time … mitigation responses

Carbon Financing

• Area of environmental financing

• Explores implications of living in a carbon constrained world, emissions of GHG carry a price due to externalities

• Apply to emission reductions projects and associated transactions under the carbon markets

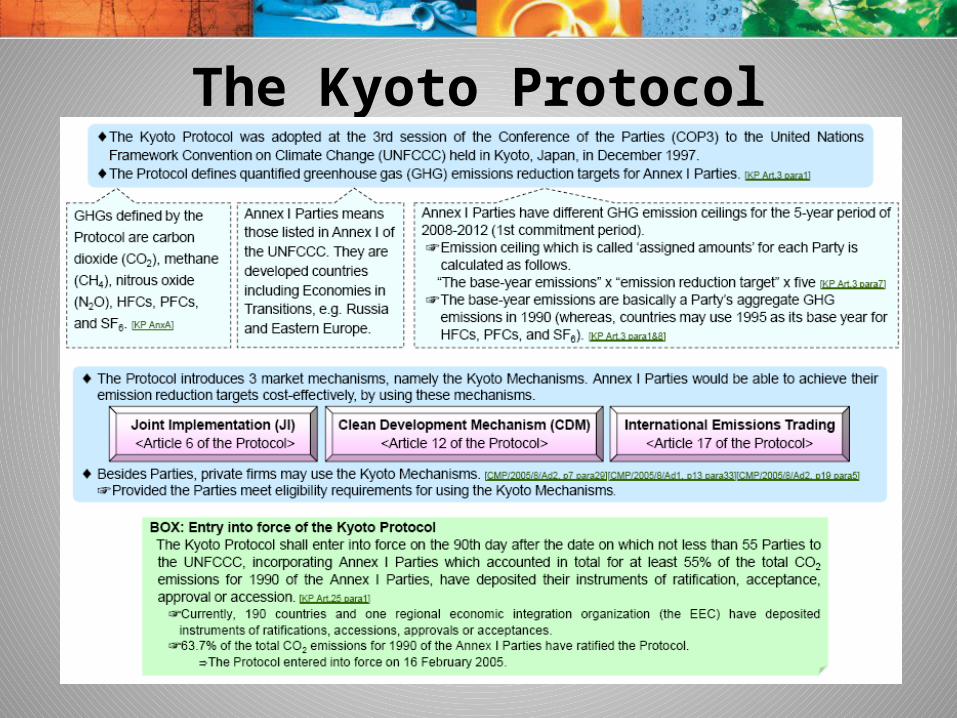

The Kyoto Protocol

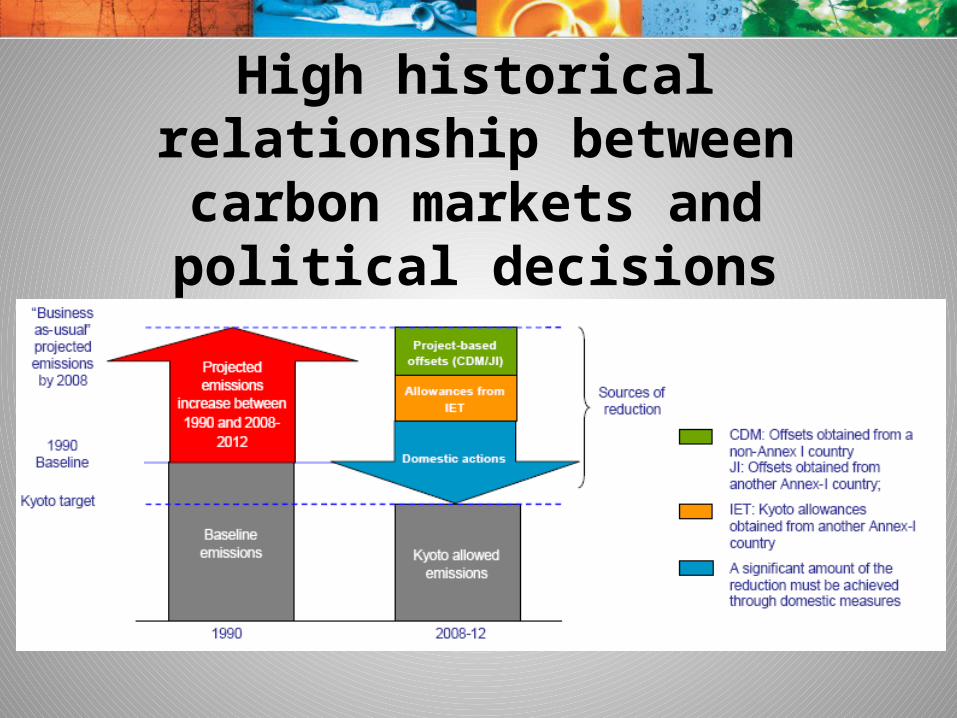

High historical relationship between carbon markets and

political decisions

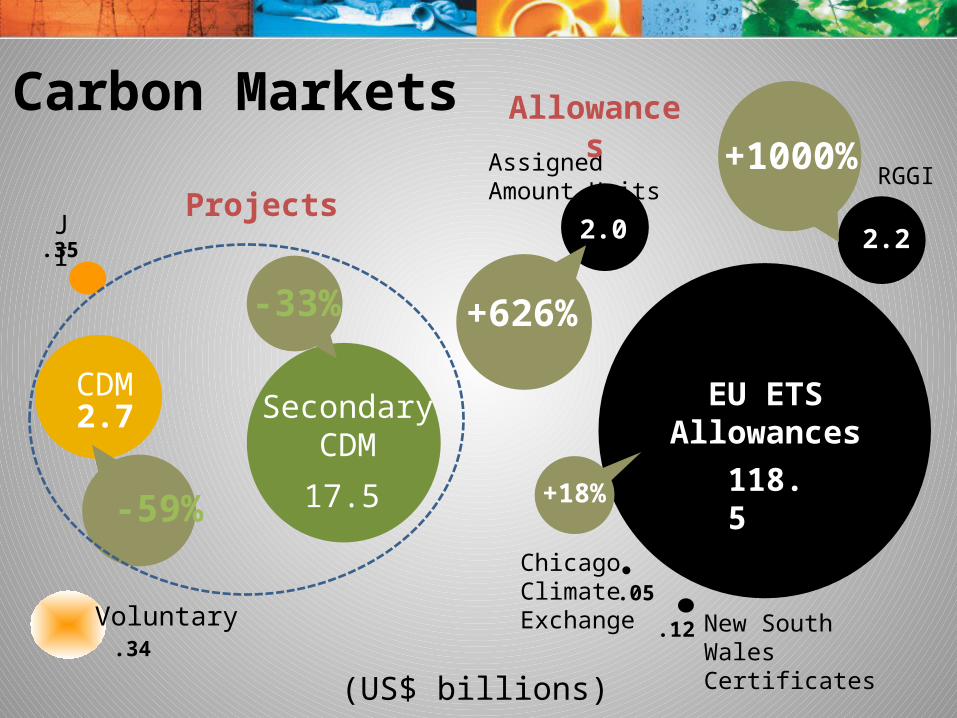

Carbon Markets

3main markets in existence

Voluntary emission reduction certificates

Emission allowancesProject based emission reductions

certificates

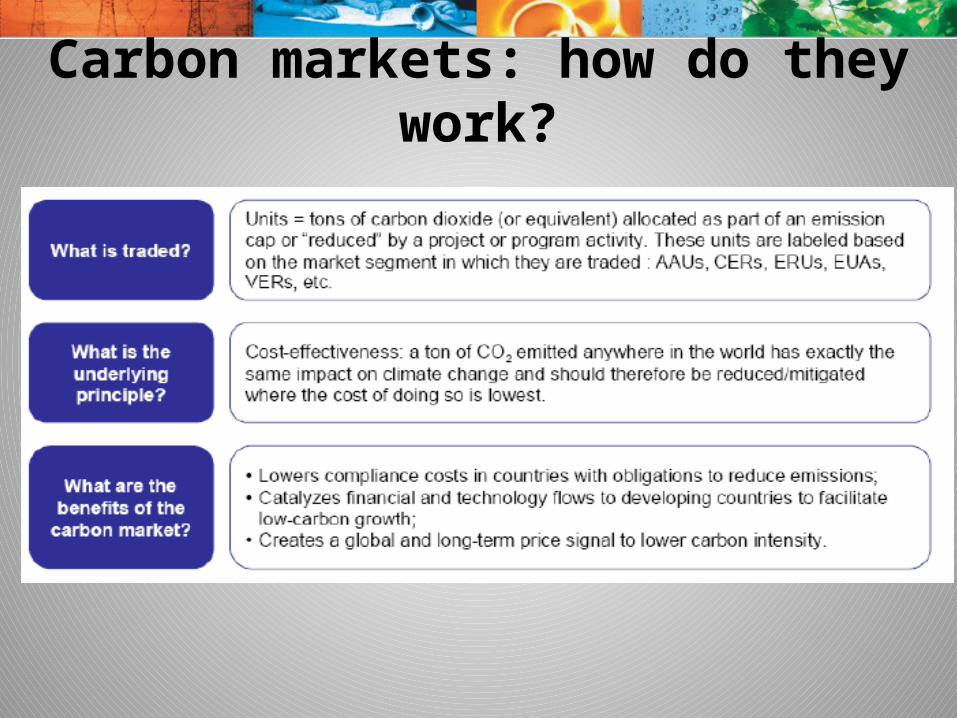

Carbon markets: how do they work?

ChicagoClimateExchange New South Wales

Certificates.12

Carbon Markets

CDM2.7

EU ETS Allowances

118.5

Voluntary.34

SecondaryCDM

17.5

JI.35

.05

-59% +18%

Assigned Amount Units

2.0

RGGI

2.2

-33%

+1000%

+626%

(US$ billions)

Projects

Allowances

General historic trends

• 2010 stalls for the first time• Domination of european systems

The Clean Development Mechanism (CDM)

¿Then, What is it?

• Global effort to resolve an issue of public interest through application of a market based mechanism

• Supply of CERs located in the developing world can be bought by developed countries for their assumed compliance

• Based on principles of cost effectiveness for the develop world and contribution to sustainable development in the developing world

• Aiming at contributing to the objectives of the UNFCCC (stabilization of GHG concentrations

• Several types of implications

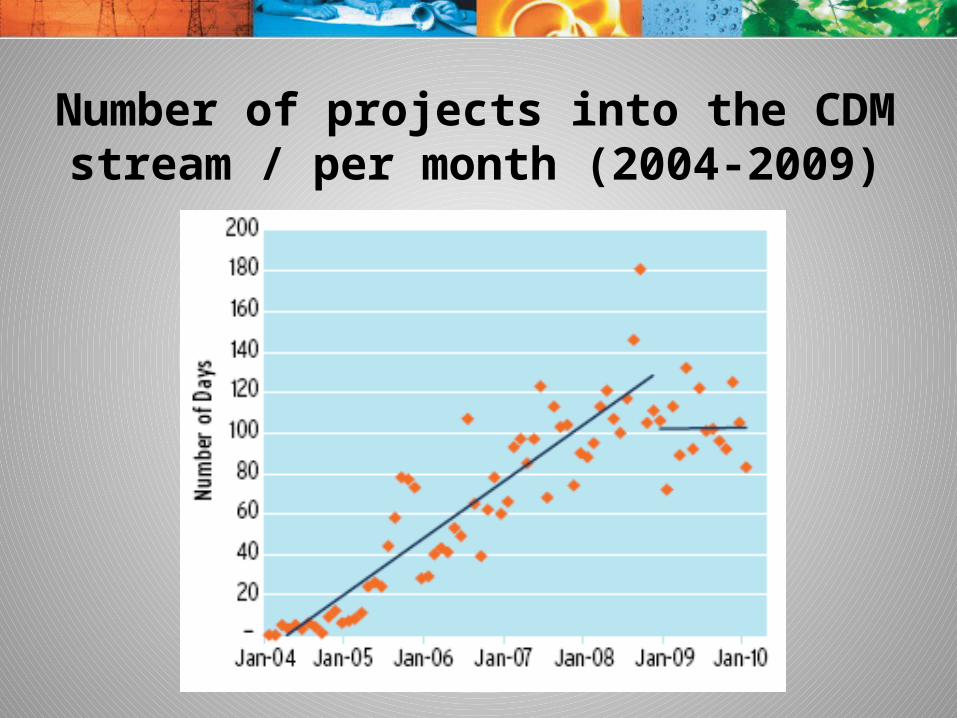

Number of projects into the CDM stream / per month (2004-2009)

Recent trends 0

- 5

5 -

10

10

- 2

5

25

- 6

0

60

- 1

00

10

0 -

50

0

50

0 -

10

00

10

00

- 5

00

0

50

00

- 1

00

00

> 1

00

00

0

500

1000

1500

2000

2500

Number of projects with in different size intervals

ktCO2 per year

Nu

mb

er

of

pro

jec

ts

Q1

-04

Q3

-04

Q1

-05

Q3

-05

Q1

-06

Q3

-06

Q1

-07

Q3

-07

Q1

-08

Q3

-08

Q1

-09

Q3

-09

Q1

-10

Q3

-10

Q1

-11

0

10

20

30

40

50

60

70

New project in Latin America entering the pipeline each quarter

Latin America

Brazil

Mexico

Pro

ject

s

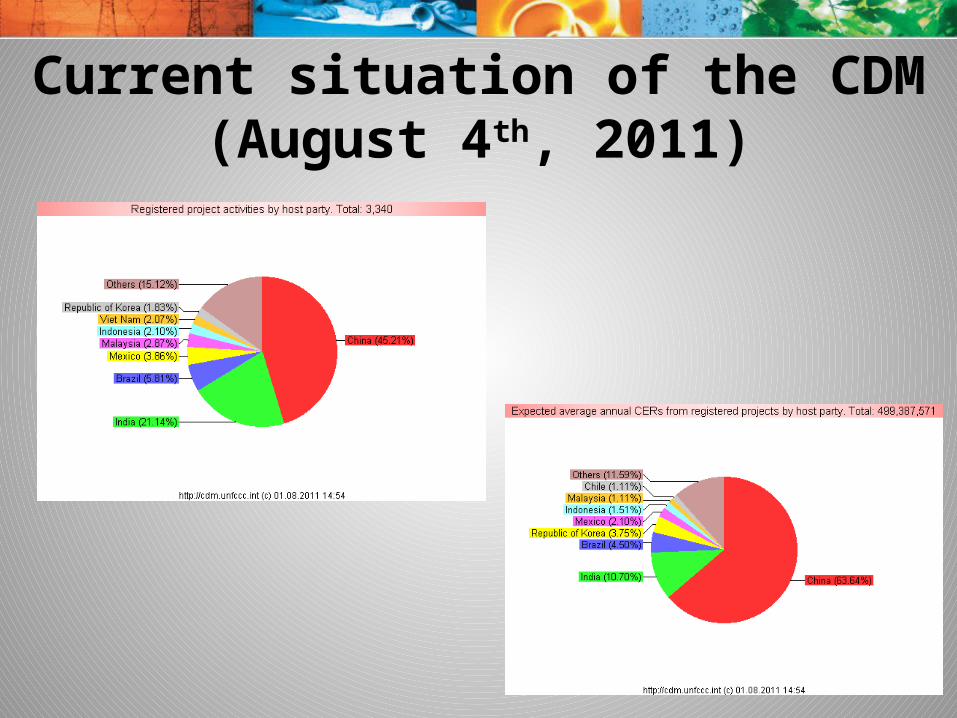

Current situation of the CDM(August 4th, 2011)

Who´s selling CDM CERs?

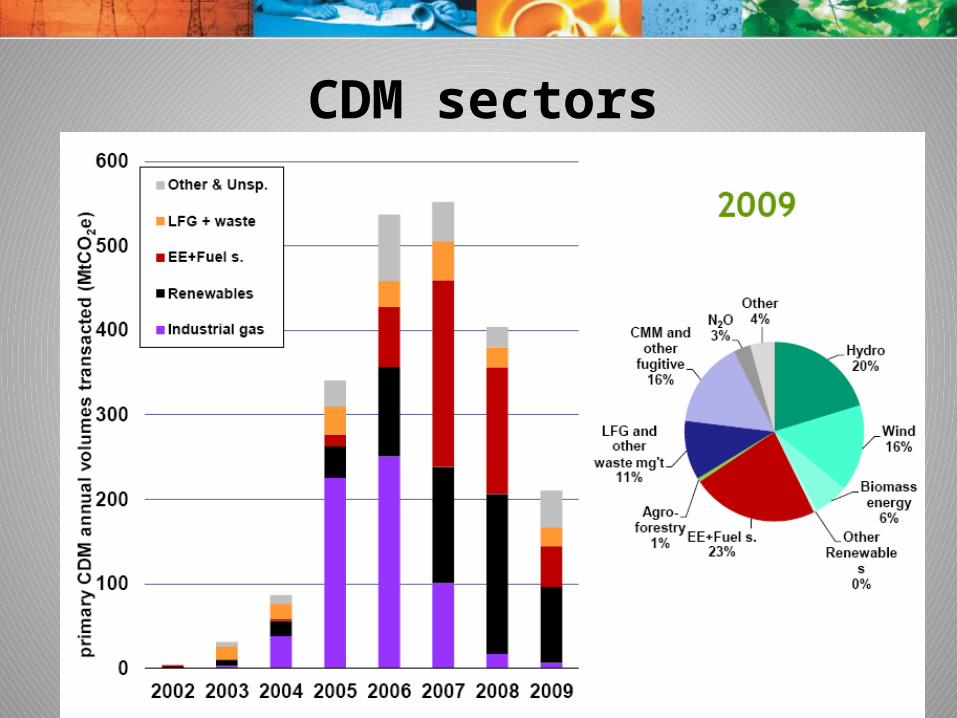

CDM sectors

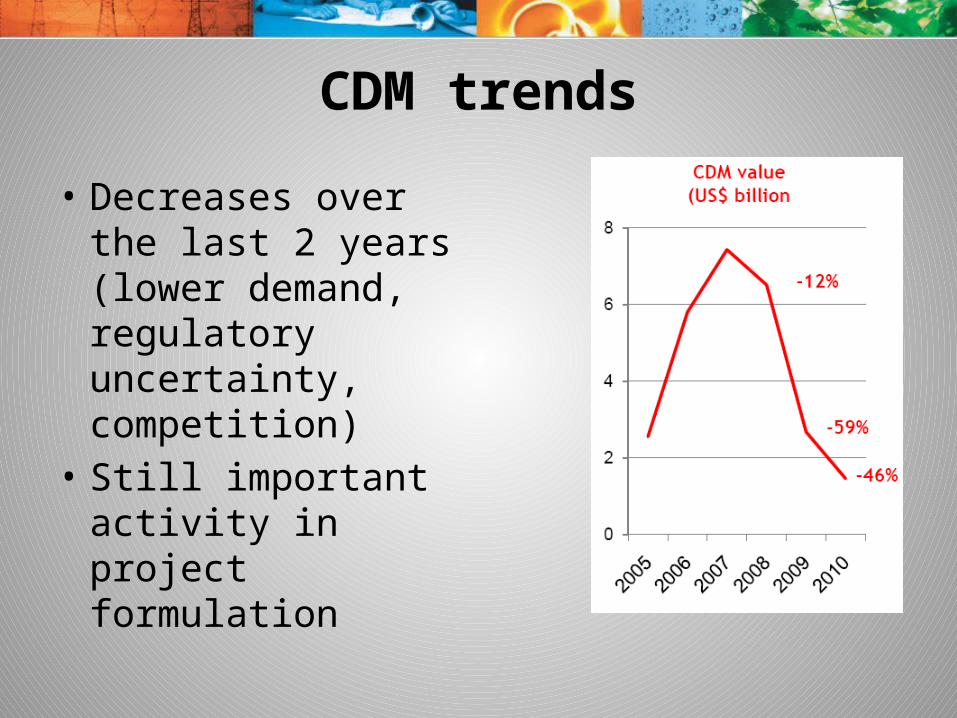

CDM trends

• Decreases over the last 2 years (lower demand, regulatory uncertainty, competition)

• Still important activity in project formulation

CER price continues to be indexed to the European signals

CER post 2012 high quality vintage

6-7 Euro

CER futures with a medium risk

7-8.5 Euro

CER futures with low risk 8.5-10 Euro

CER registered CDM projects

10,5-11 Euro

CER spot market 9.33 Euros

CDM CER prices

Source CDM Highlights, GIZ (July 2011)

The future of the carbon markets

Uncertainties Dependencies Expectations

At the project level …

Carbon revenue is an additional source of earnings

Relationship between

investment and net present

value of carbon contract for

different types of projects

(World Bank experience)

Carbon revenues and project returns

What is going on with the CDM?

• Regulatory decisions out of COP 16 in Cancun

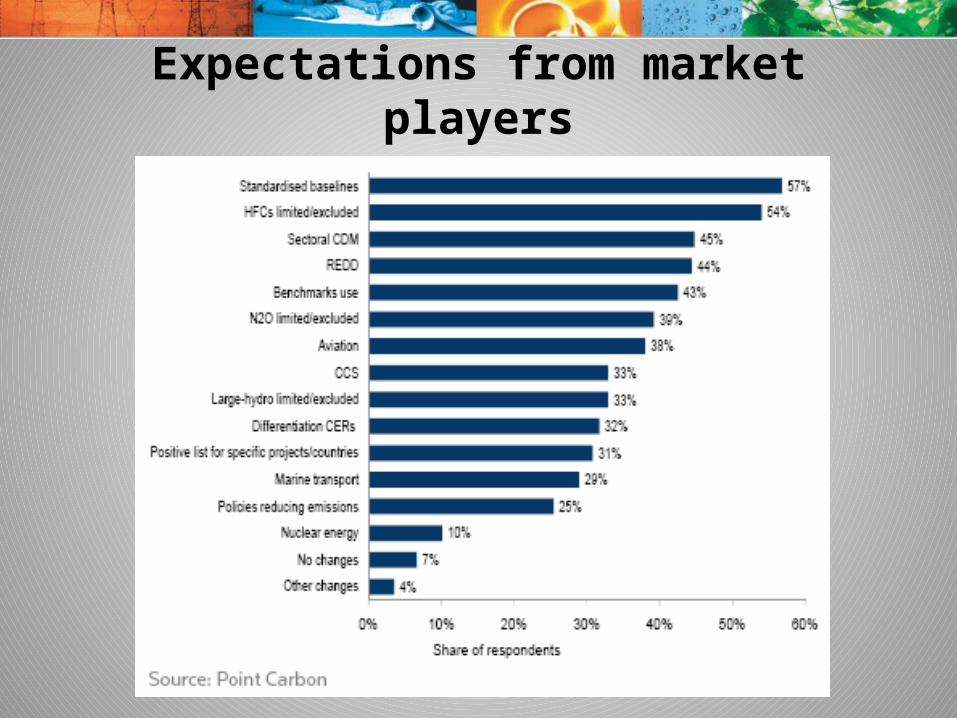

• Expectations from market players

Decisions related to CDM

• Regional distribution• Integrity of the CDM and its requirements• Objectivity, efficiency of the CDM and its

requirements• Enhance transparency of the CDM• Out reach• Simplification and standardization• Inclusion of CCS in CDM (Decision 7/CMP.6)

Expectations from market players

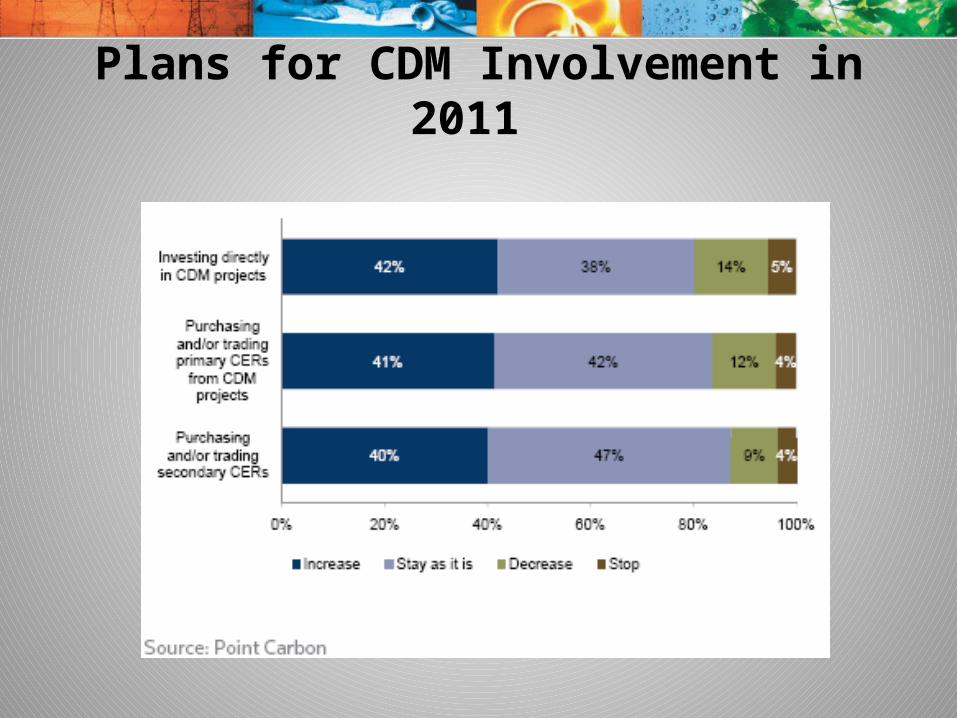

Plans for CDM Involvement in 2011

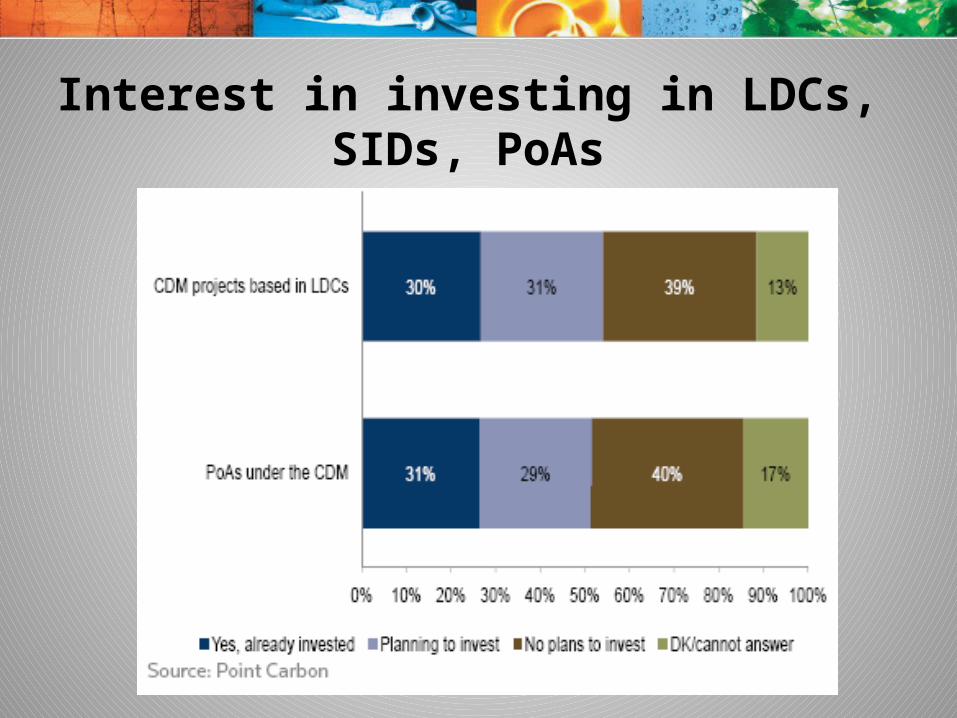

Interest in investing in LDCs, SIDs, PoAs

Concluding Remarks

• Continued interest but challenging issues

• Attention to regulatory developments

• Act now !! if you have a sound project

Related Documents