1 Seminar in Economics The causal link between short-term and long-term inflation expectations Alexander Czombera ([email protected]) Jonas Neise ([email protected]) 6 th Semester 26 th Februrary 2015 Supervisor: Prof. Dr. Michael Frenkel Tutor: Matthias Mauch Abstract Long-run and short-run inflation expectations indicate the quality of anchoring and central bank credibility for its inflations target and expected pass-through of inflationary shocks. In this paper we provide a comprehensive literature review and find that changes and credibility of policy targets are passed through long-run and short-run expectations while shocks affect mainly short-run expectations and influence long-run expectations if they are sequential and not-accommodated. We exemplify our hypothesizes by empirical models and find that short- term expectations compared to the medium-term have a weaker link to long-term expectations.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Seminar in Economics

The causal link between short-term and long-term inflation

expectations

Alexander Czombera

Jonas Neise

6th Semester

26th Februrary 2015

Supervisor: Prof. Dr. Michael Frenkel

Tutor: Matthias Mauch

Abstract

Long-run and short-run inflation expectations indicate the quality of anchoring and central

bank credibility for its inflations target and expected pass-through of inflationary shocks. In

this paper we provide a comprehensive literature review and find that changes and credibility

of policy targets are passed through long-run and short-run expectations while shocks affect

mainly short-run expectations and influence long-run expectations if they are sequential and

not-accommodated. We exemplify our hypothesizes by empirical models and find that short-

term expectations compared to the medium-term have a weaker link to long-term

expectations.

2

Table of Contents

1. Introduction .................................................................................................................................................. 6

2. Definitions of Inflation Expectations and Expectation Forming ............................................. 8

2.1 Inflation Expectations and Expectations Forming ....................................................................... 8

2.2 Inflation Targeting and Rule-Based Monetary Policy ......................................................... 9

2.3 Practical Implication: Monetary Policy and Inflation Expectations .................................... 12

3. Interdependence Between Short-Term and Long-Term Expectations .............................. 15

3.1 Influence of Short-Term on Long-Term Expectations - Exogenous Shocks and

Credibility Proofs ...................................................................................................................................... 15

3.2 Influence of Long-Term on Short-Term Expectations – Credibility of Policy

Changes ....................................................................................................................................................... 19

3.3 Measuring Dynamics of Inflation Expectations - A Survey Approach .............................. 21

4. Implications of a Heterogeneous Currency Union on Expectation Building – The

Current Case of the Euro Area .............................................................................................................. 27

4.1 Theory and Implications ............................................................................................................... 27

5. Statistical Analysis .................................................................................................................................. 29

5.1 Data Description ............................................................................................................................... 29

5.2 Towards a Causal Link ...................................................................................................................... 34

6. Conclusion .................................................................................................................................................. 48

References ....................................................................................................................................................... 50

Appendix .......................................................................................................................................................... 55

3

List of Figures and Tables Charts

Chart 3.2.1: India Inflation Rate (CPI) 54

Chart 3.3.1: Mean of individual forecasts 54

Chart 3.3.2: Median of individual forecasts 55

Chart 3.3.3: Standard deviation of individual forecasts 55

Chart 3.3.4: Interquartile range of individual forecasts 56

Chart 3.3.5: Proportion of changes in inflation expectations per week 56

Chart 4.1.1: 10-year government bonds - nominal yields 57

Chart 4.1.2: 10-year government bonds - real yields 57

Chart 4.1.3: Inflation (change in CPI YoY) 58

Chart 4.1.4: Nominal GDP per capita growth 58

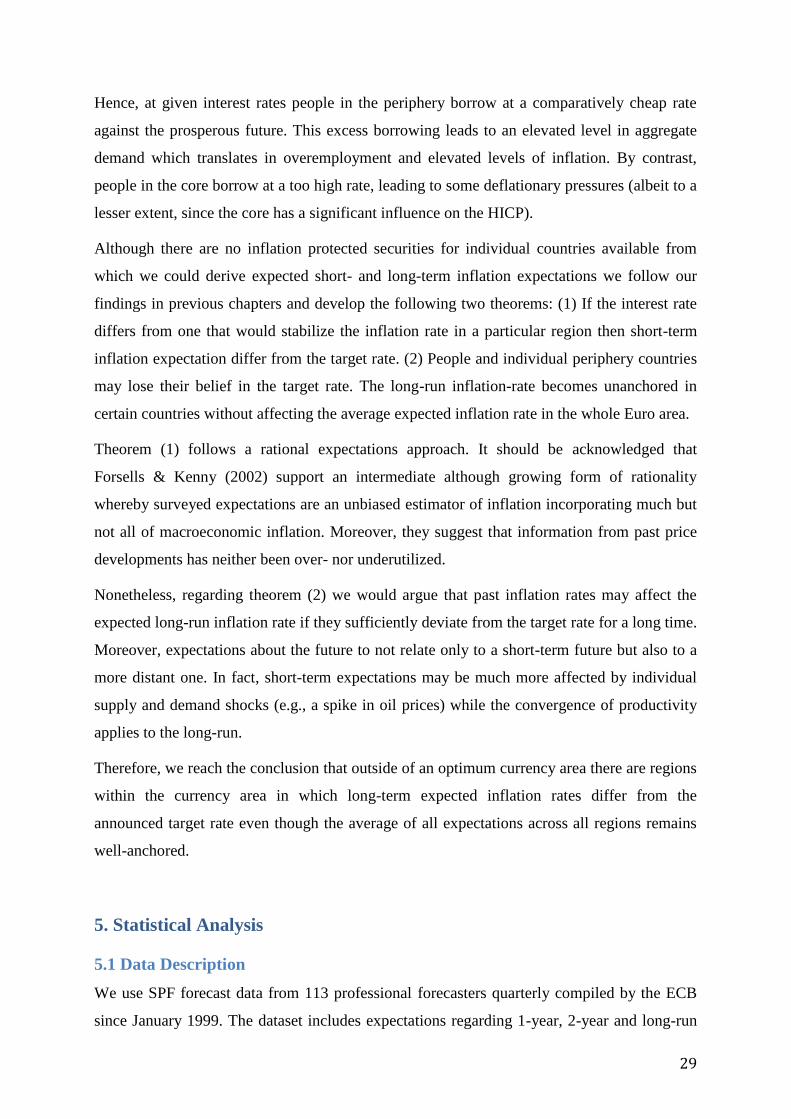

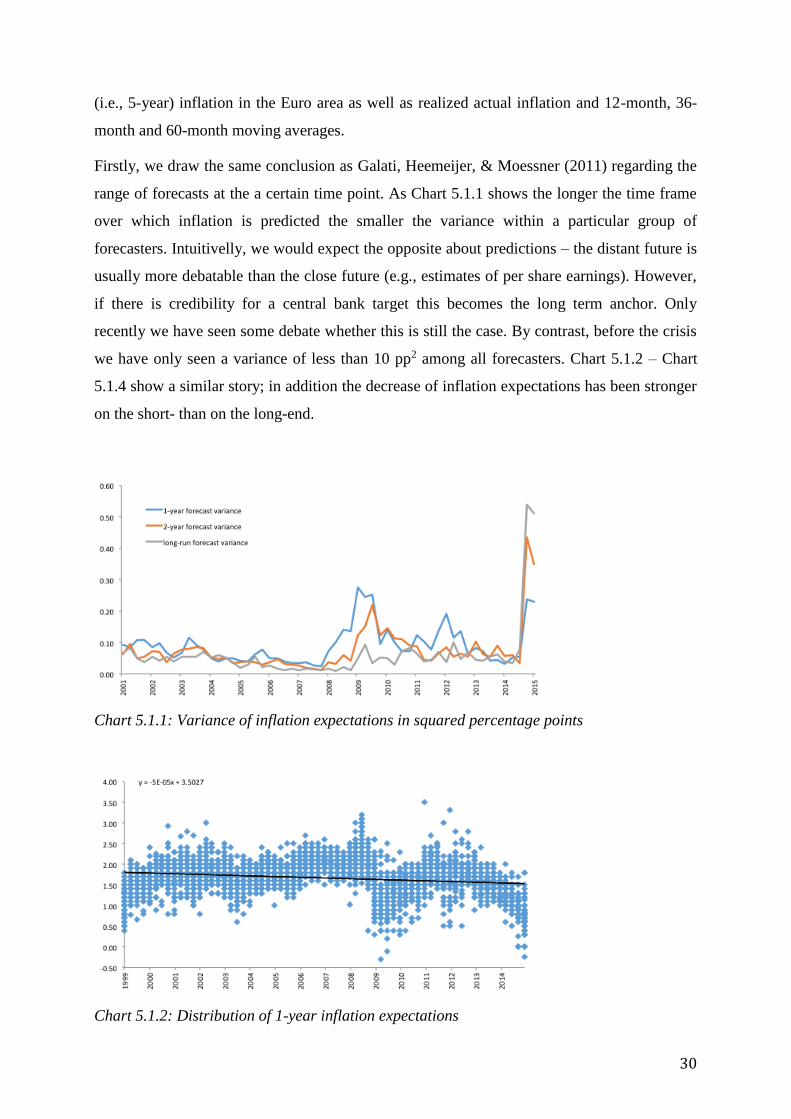

Chart 5.1.1: Variance of inflation expectations in squared percentage points 30

Chart 5.1.2: Distribution of 1-year inflation expectations 30

Chart 5.1.3: Distribution of long-run inflation expectations 31

Chart 5.1.4: Distribution of 1-year inflation expectations 31

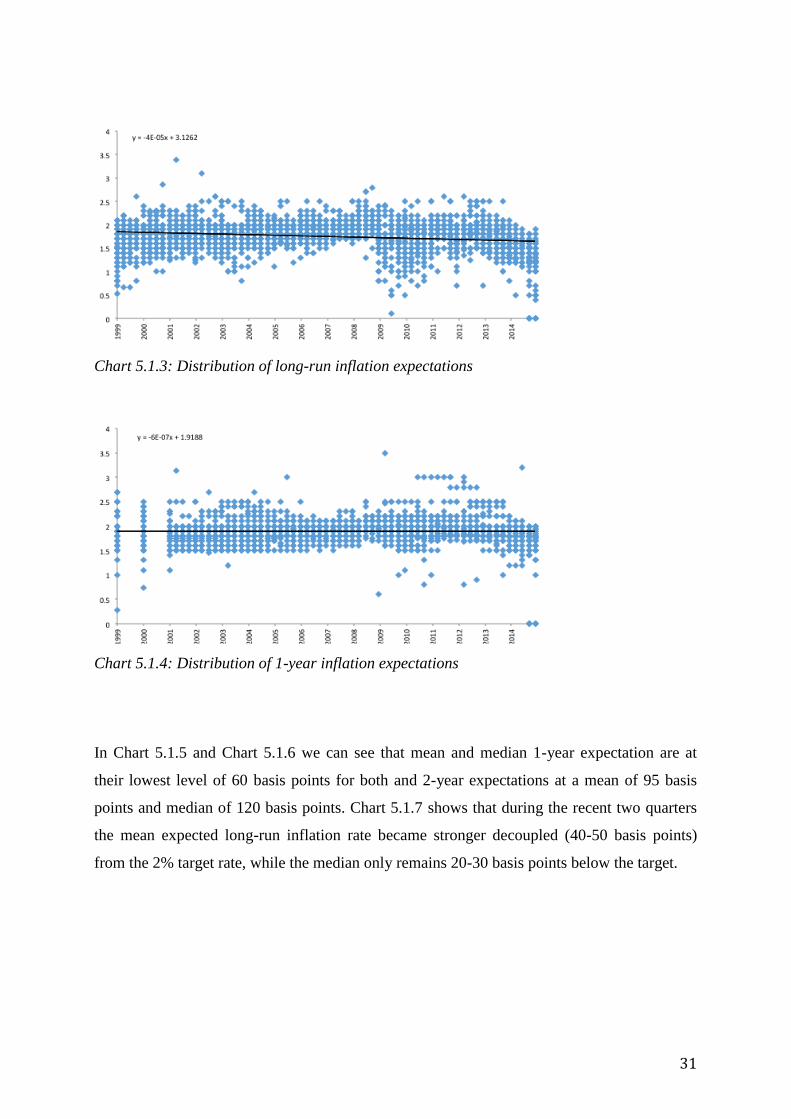

Chart 5.1.5: Mean and median 1-year inflation expectations 32

Chart 5.1.6: Mean and median 2-year inflation expectations 32

Chart 5.1.7: Mean and median long-run inflation expectations 32

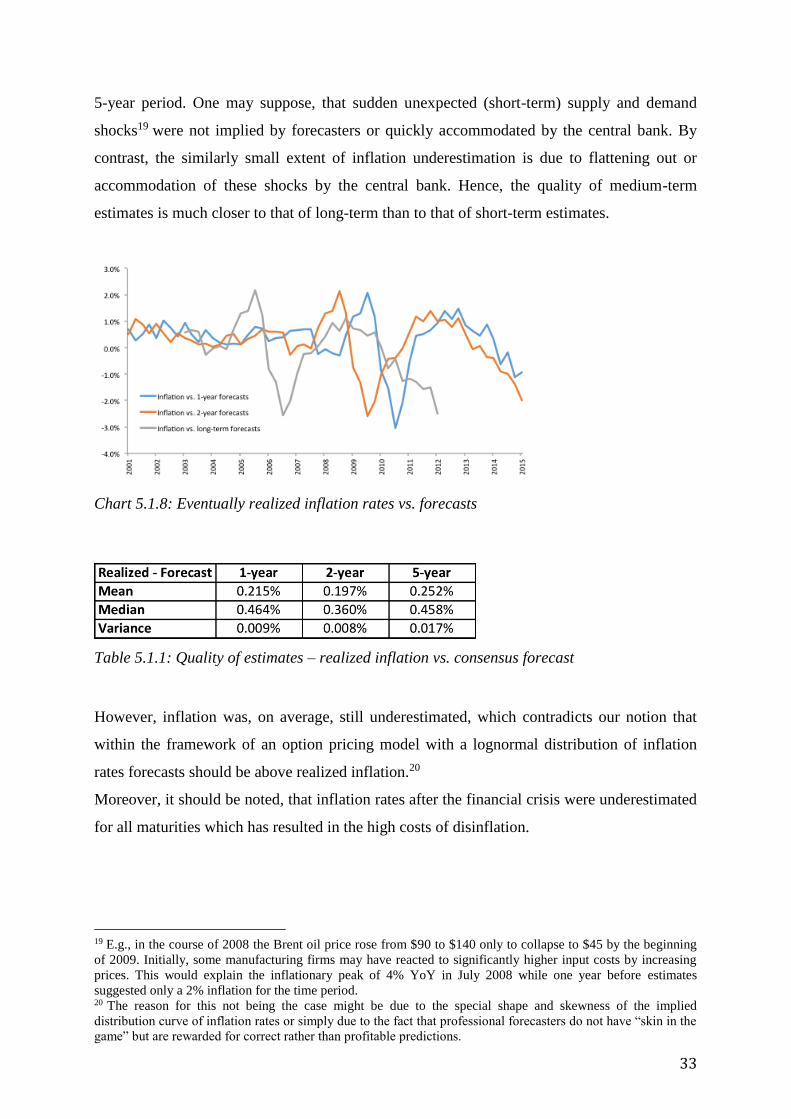

Chart 5.1.8: Eventually realized inflation rates vs. forecasts 33

Figures

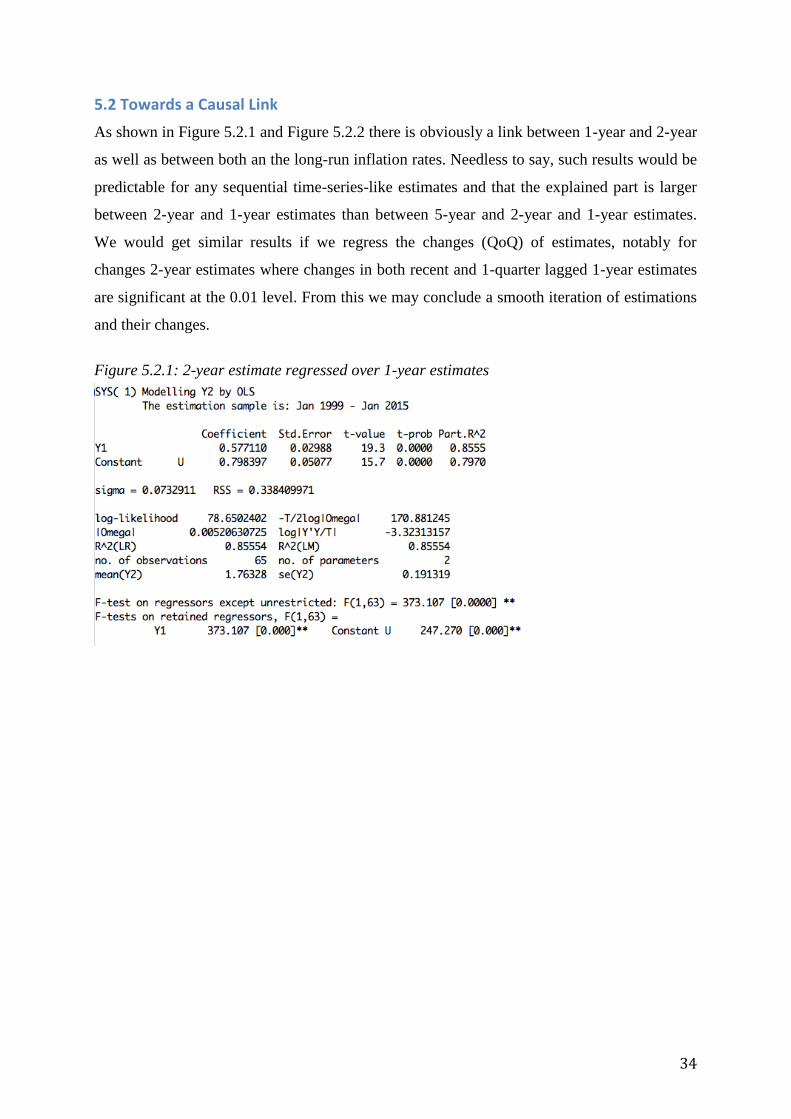

Figure 5.2.1: 2-year estimate regressed over 1-year estimates 34

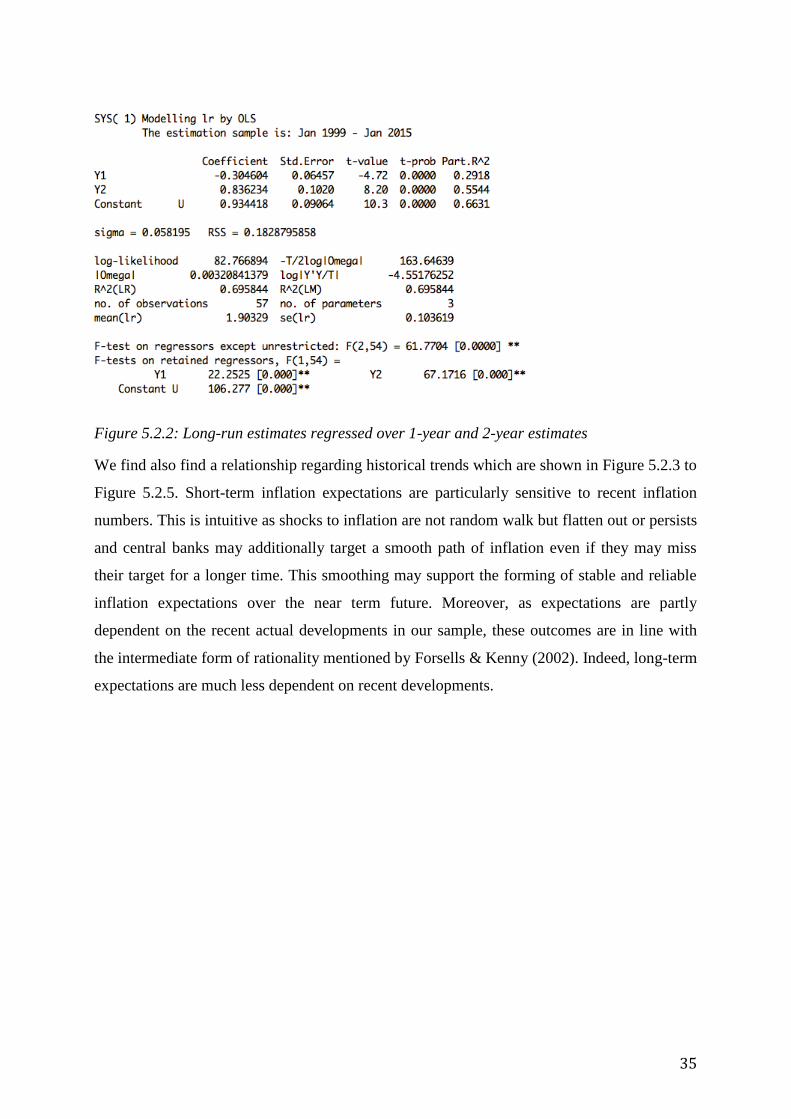

Figure 5.2.2: Long-run estimates regressed over 1-year and 2-year estimates 34

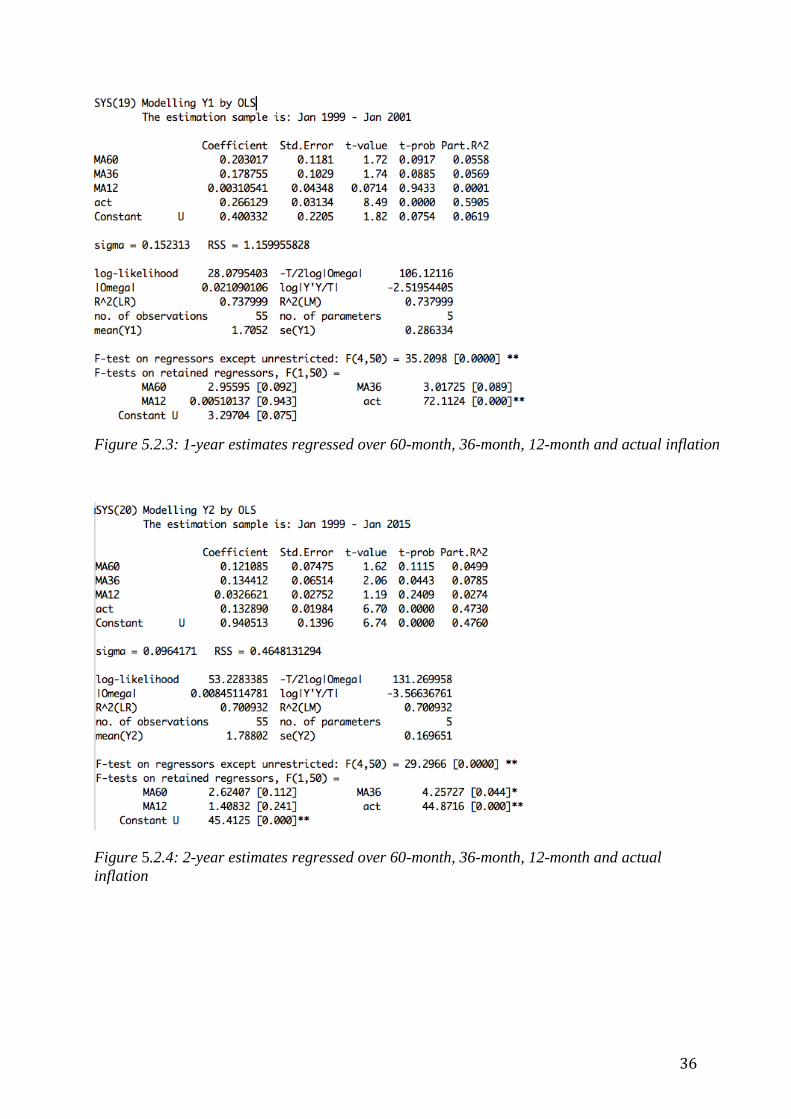

Figure 5.2.3: 1-year estimates regressed over 60-month, 36-month, 12-month and actual

inflation

35

Figure 5.2.4: 2-year estimates regressed over 60-month, 36-month, 12-month and actual

inflation

36

Figure 5.2.5: long-run estimates regressed over 60-month, 36-month, 12-month and actual

inflation

36

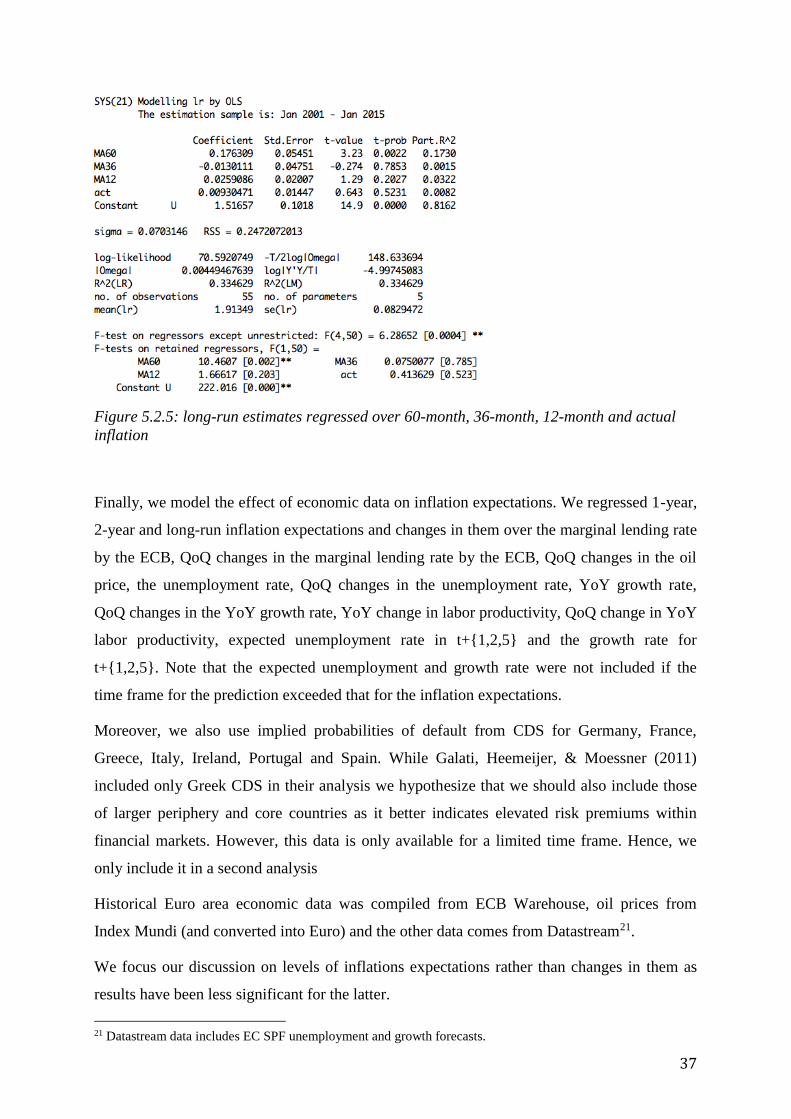

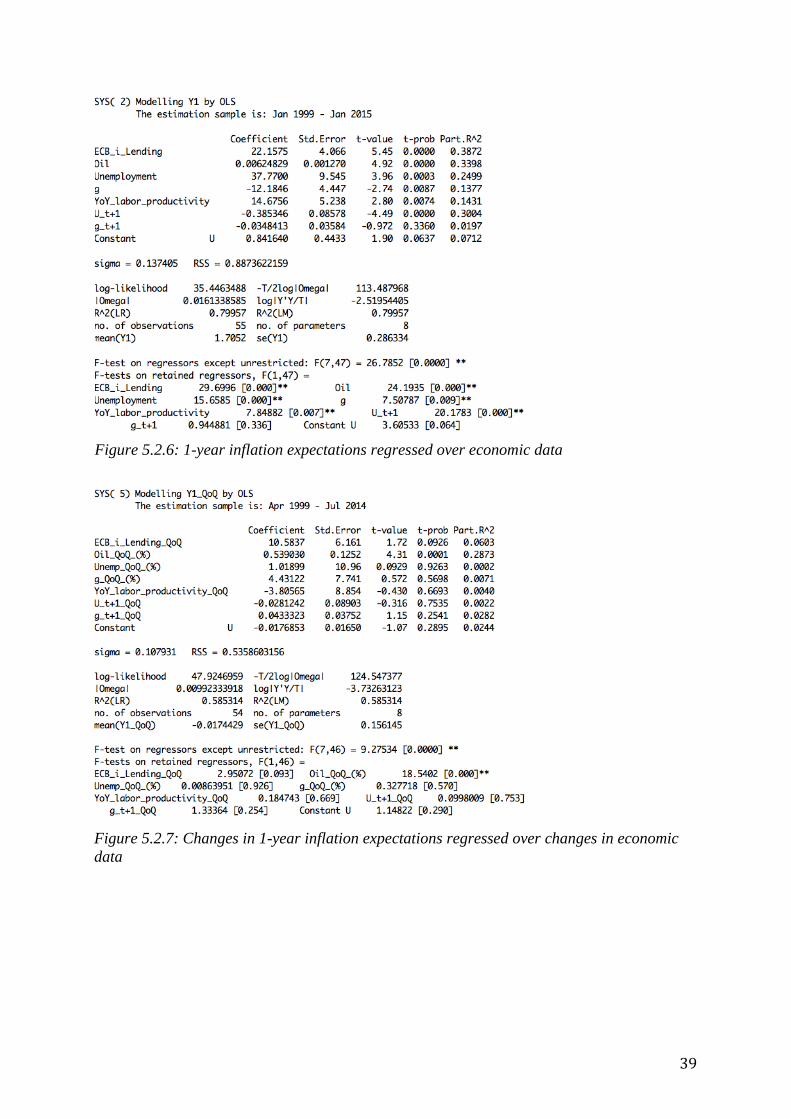

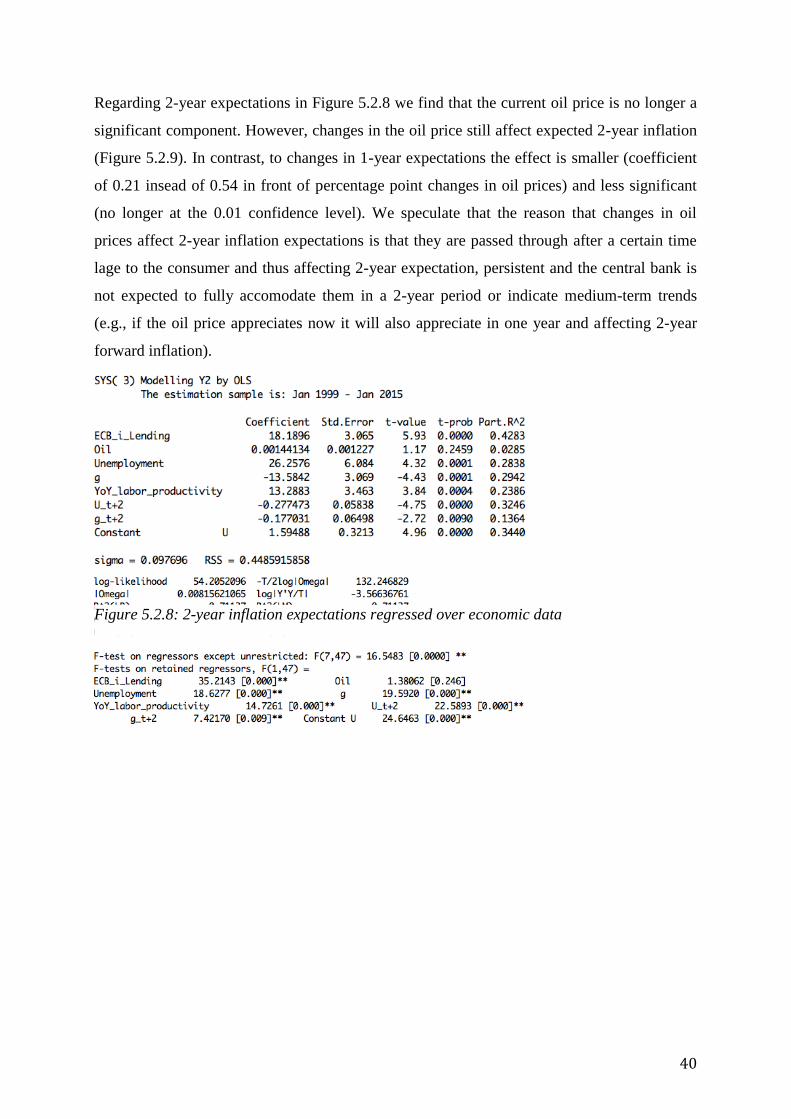

Figure 5.2.6: 1-year inflation expectations regressed over economic data 38

Figure 5.2.7: Changes in 1-year inflation expectations regressed over changes in economic

data

39

Figure 5.2.8: 2-year inflation expectations regressed over economic data 39

Figure 5.2.9: Changes in 2-year inflation expectations regressed over changes in economic

4

data 3 40

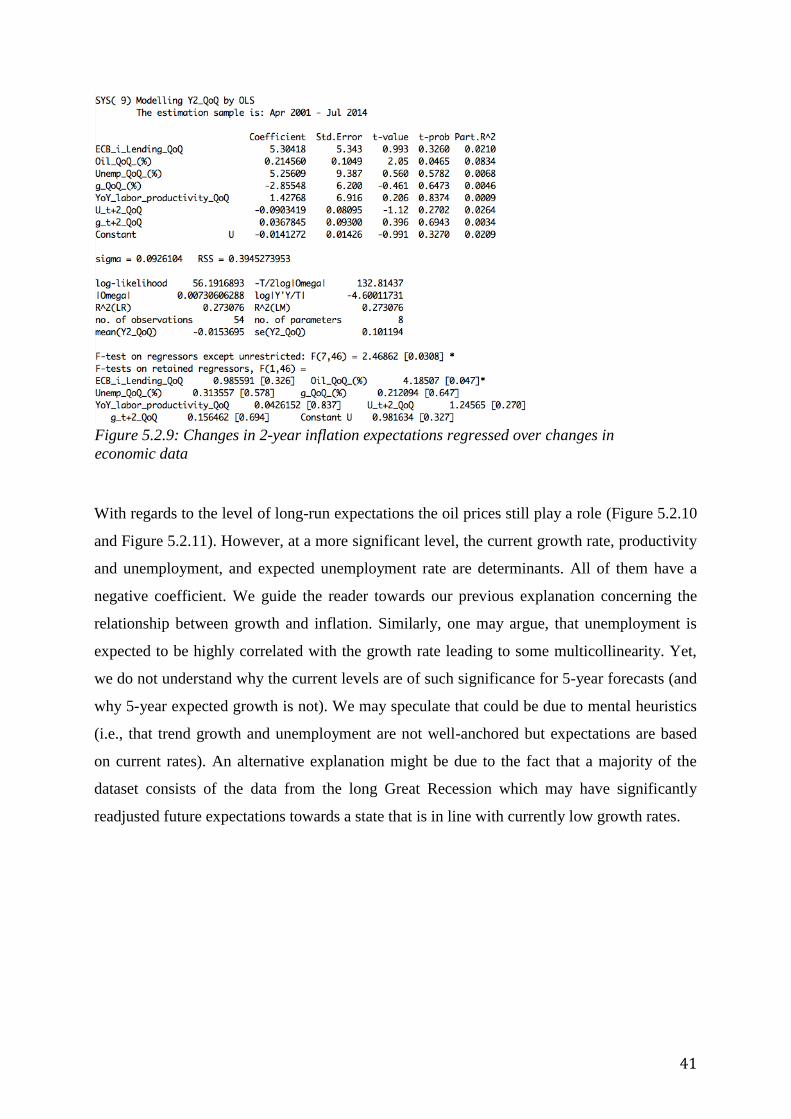

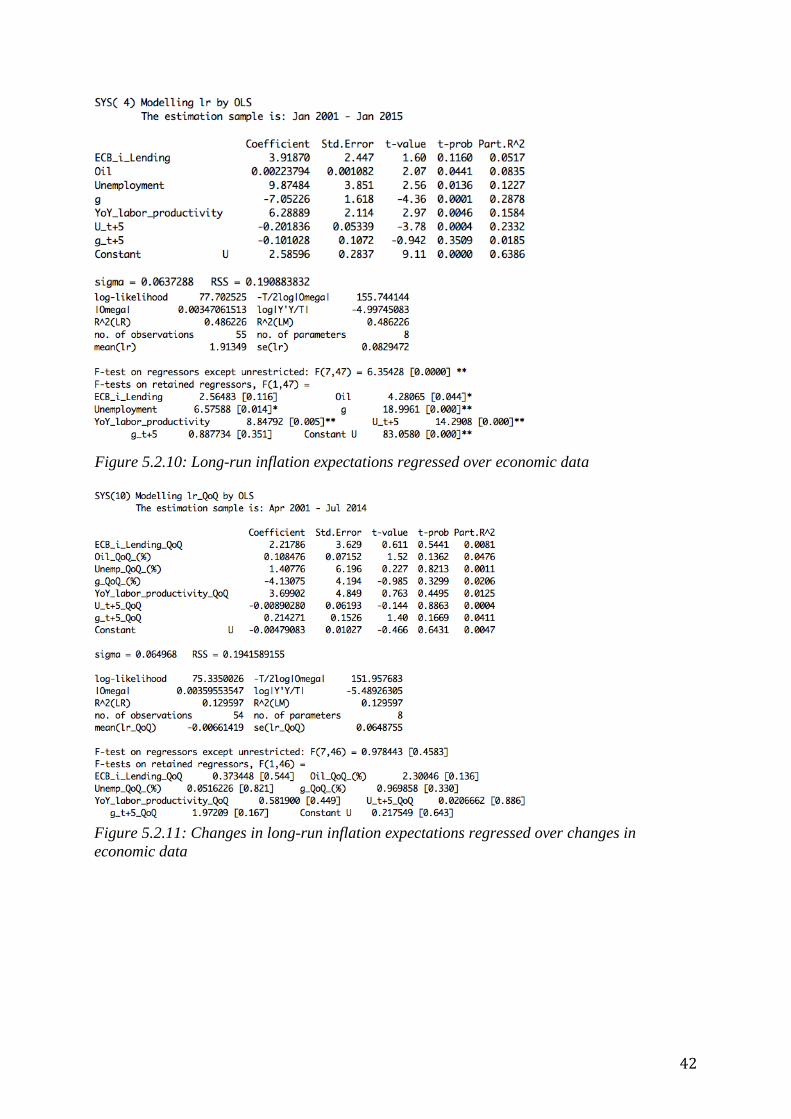

Figure 5.2.10: Long-run inflation expectations regressed over economic data 41

Figure 5.2.11: Changes in long-run inflation expectations regressed over changes in economic

data

41

Figure 5.2.12: 1-year inflation expectations regressed over probabilities of default 42

Figure 5.2.13: 2-year inflation expectations regressed over probabilities of default 43

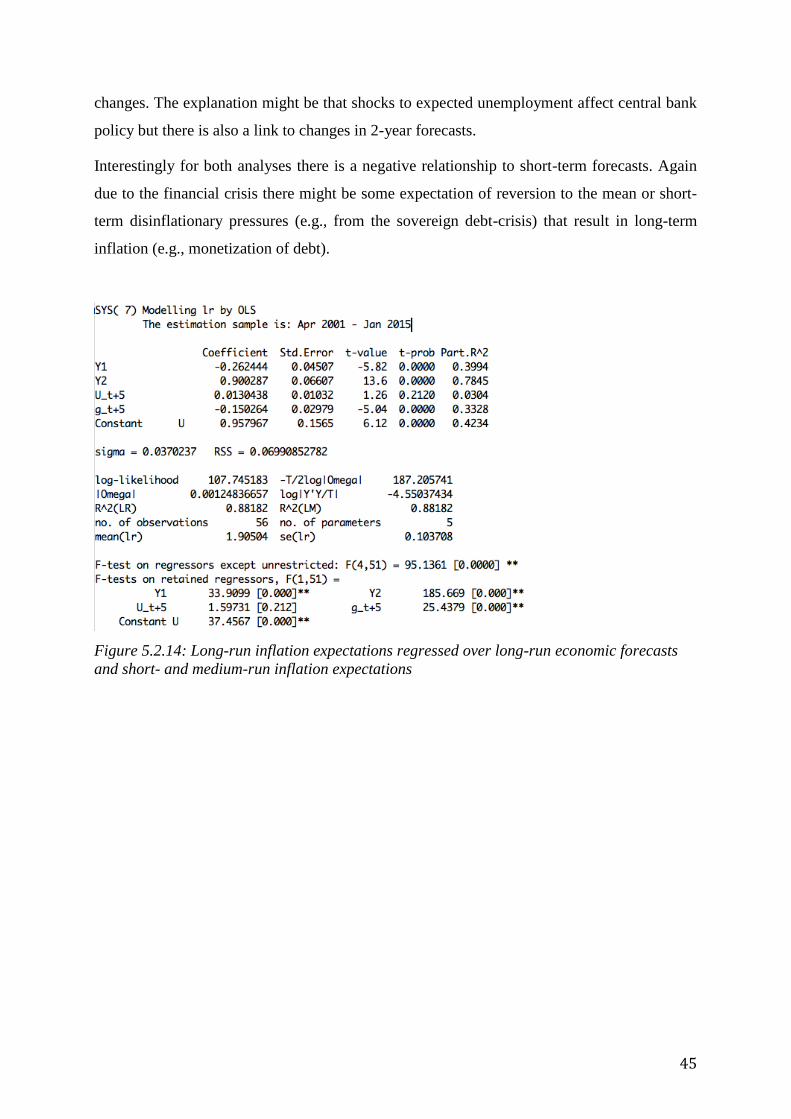

Figure 5.2.14: Long-run inflation expectations regressed over long-run economic forecasts

and short- and medium-run inflation expectations

44

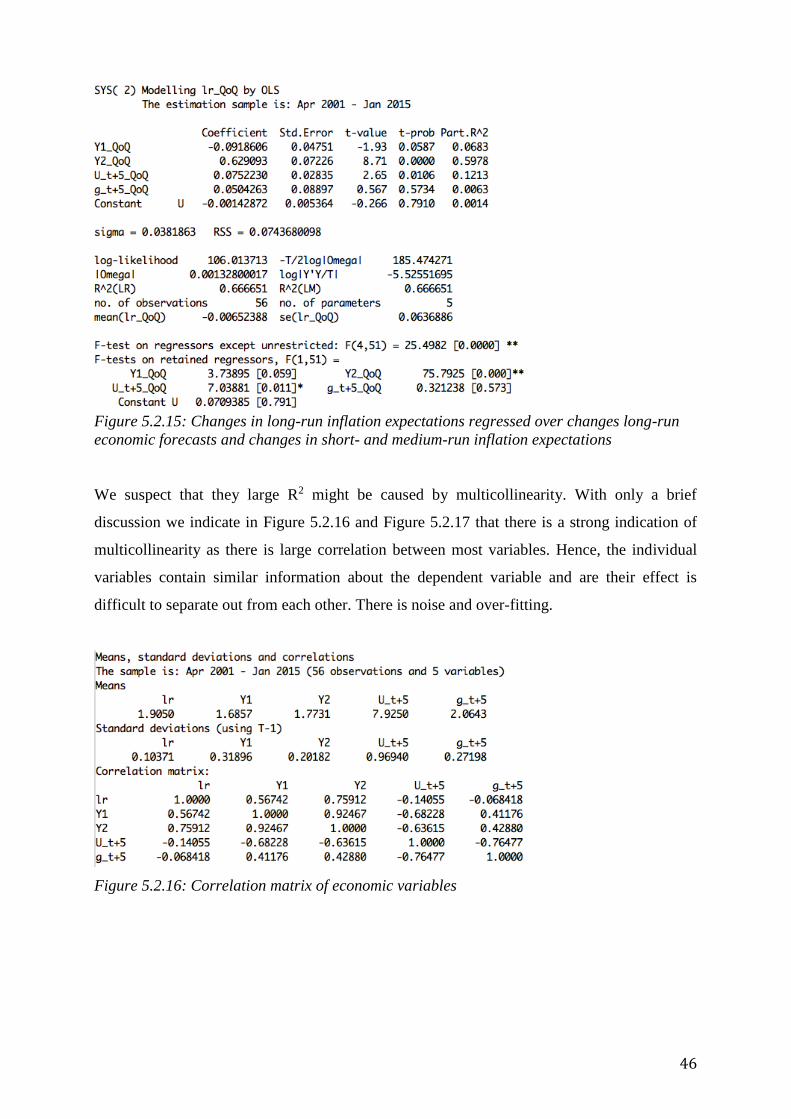

Figure 5.2.15: Changes in long-run inflation expectations regressed over changes long-run

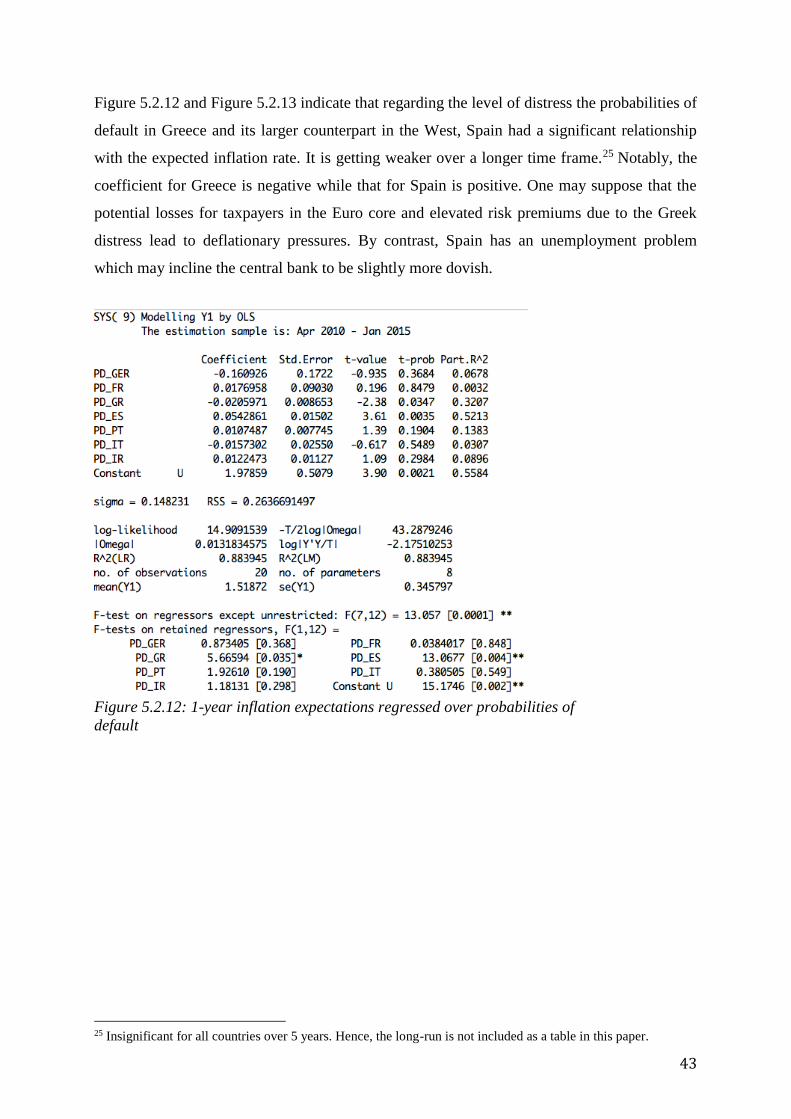

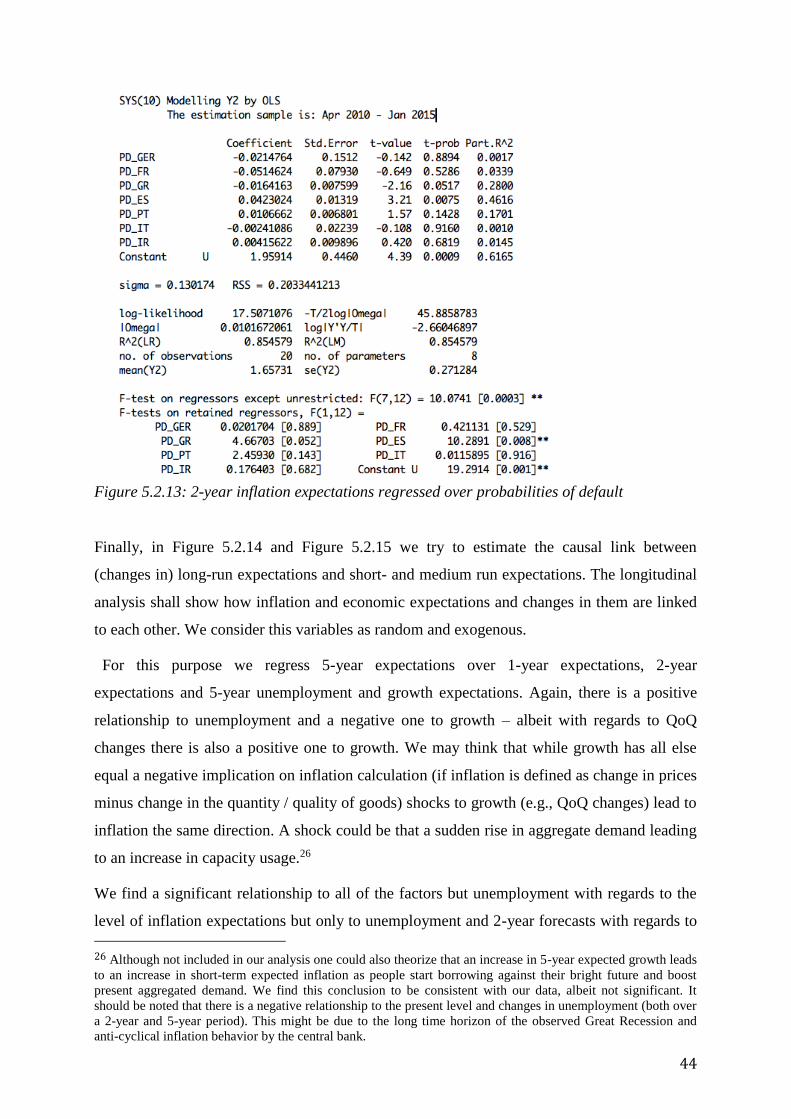

economic forecasts and changes in short- and medium-run inflation expectations

45

Figure 5.2.16: Correlation matrix of economic variables 45

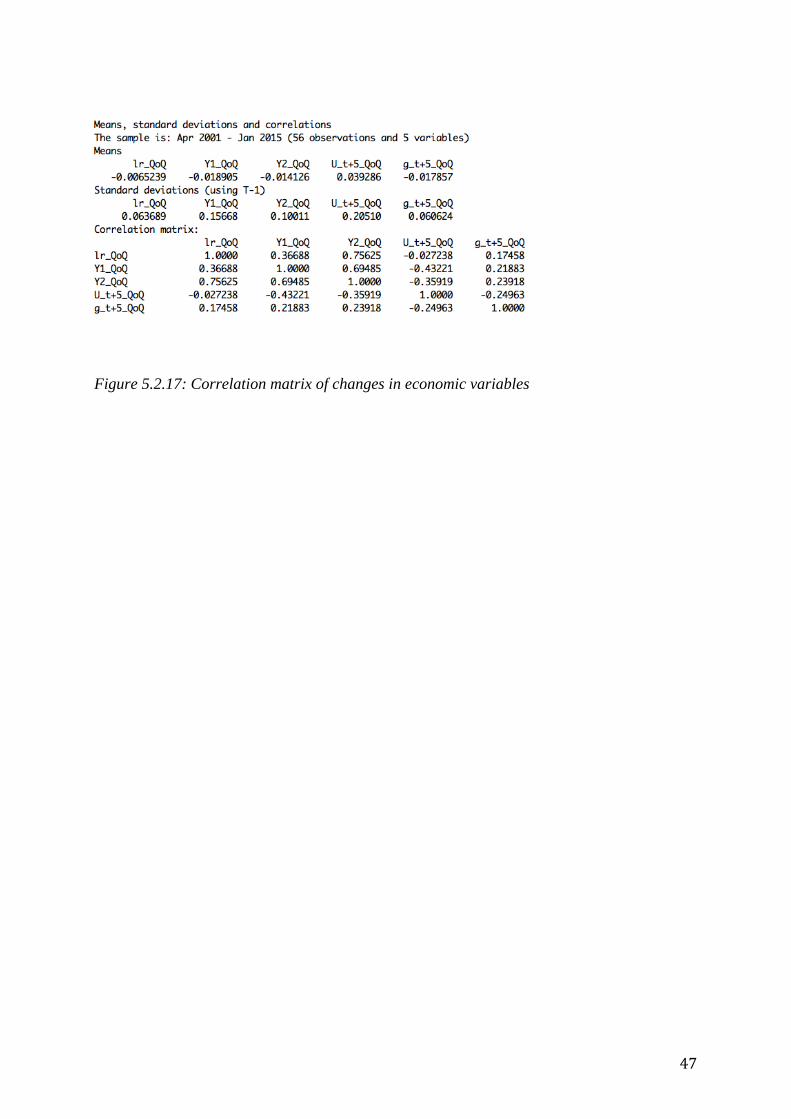

Figure 5.2.17: Correlation matrix of changes in economic variables 46

Tables

Table 5.1.1: Quality of estimates – realized inflation vs. consensus forecast 33

5

Table of Abbreviations

act actual inflation, current quarter

DNB De Nederlandsche Bank

ECB European Central Bank

ECB_i_Lending ECB Marginal Lending Facility

Fed Federal Reserve Bank

g growth rate (current, YoY)

g_t+1 1-year nominal growth expectations

g_t+2 2-year nominal growth expectations

g_t+5 5-year nominal growth expectations

LR long-run (inflation expectations)

MA12 12-month moving average (actual inflation)

MA36 36-month moving average (actual inflation)

MA60 60-month moving average (actual inflation)

NNS New Neoclassical Synthesis

Oil oil price (current, €)

OLS Ordinary Least Squares

PD_ES CDS-implied probability of default, Spain

PD_FR CDS-implied probability of default, France

PD_GER CDS-implied probability of default, Germany

PD_GR CDS-implied probability of default, Greece

PD_IR CDS-implied probability of default, Ireland

PD_IT CDS-implied probability of default, Italy

PD_PT CDS-implied probability of default, Portugal

pp percentage points

QoQ quarter on quarter change

RBC Real Business Cycle

RBI Reserve Bank of India

SPF Survey of Professional Forecasters

U_t+1 1-year unemployment expectations

U_t+2 2-year unemployment expectations

U_t+5 5-year unemployment expectations

Y1 1-year (inflation expectations)

Y2 2-year (inflation expectations9

YoY year on year change

6

1. Introduction

More than 2000 years ago Plato (1970) described expectations as a concept based on beliefs

about the future. Nowadays, these beliefs are defined as a synergetic result of behavioral and

psychological elements. The importance of expectations becomes evident when people

change their current behavior in light of their beliefs about the future. This conceptual model

has still retained its validity in economics as well since expectations about the future affect

the current behavior of economic agents.

Therefore, economic expectations are generally referred to as explicit forecasts or implicit

opinions that economic agents hold about future prices, income, taxes or the overall level of

economic activity in general. Following this approach, inflation expectations can be

determined as the view or opinion of economic agents about future inflation. As inflation is a

factor that affects almost every economic entity in an economy, inflation expectations play a

crucial role in macroeconomics and especially monetary policy.

If people form expectations that are below the realized level they spend less than they would

have done otherwise. Instead, they save more against their bright future at the given interest

rate as they believe the purchasing power of their currency holdings will not change

significantly. This leads to a decrease in aggregate demand and may translate into a self-

fulfilling disinflation.

By contrast, if they hold too high inflation expectations they will demand a higher interest rate

to compensate them for the loss in real value of their cash holdings. As the central bank may

be unwilling to increase the interest rate people will consume more (rather than save) and at

the given supply curve inflate prices. Alternatively, they may also purchase assets that

promise some type of inflation protection such as gold or real estate. However, as they usually

yield only a small real return they do not meet the preferences of all agents.

As Bernanke & Gertler (2000) note asset prices incorporate inflationary and deflationary

pressures. They suggest a model of flexible inflation targeting to assure macroeconomic and

financial stability. Such a model provides an anchor for inflation expectations and thus

reduces the effects of volatile inflation expectations on asset prices.

Inflation expectations differ with regards to the time frame. Long-run expectations are in most

developed markets anchored to some target rate set by the central bank which has

demonstrated credibility for its objective. Yet, short-run expectations may deviate from it.

Rather than being purely based on explicit policy rates they also incorporate short-term

shocks to demand, supply, and monetary policy that result in inflation or deflation after a

7

certain time lag. A central bank has to be concerned about both types of inflation

expectations: long-run expectations to guide the pricing of production and investment goods

and estimation of nominal and real returns, and short-run expectations in order to keep

markups of monopolistically competitive firms at their profit maximizing level and thus avoid

volatile adjustments in prices and employment1 in consumption goods.

In our paper we try to identify the causal link between short-term and long-term inflation

expectations. In the first part we begin with defining the terminologies around inflation and

provide some background information about the issues of inflation targeting and the debate

about a rule-based monetary policy. We introduce the concept of rational expectations and

contrast it to sticky information flows and rational inattention. Finally, we discuss the

practical relevance of well-anchored information as to execute effective monetary policy.

The second part copes with the interdependence between short-term and long-term

expectations. For this purposes we study the Great Inflation and Volcker Disinflation of the

1970s and show that short-term shocks may in fact translate into a change of both short-term

and long-term expectations if they are viewed as somehow persistent, and as a necessary

condition if the central bank loses its credibility. The case of the effect on long-term

expectations on short-term expectations is exemplified by the introduction of inflation targets

in emerging markets such as India. This sometimes occurs in the form of step-down targets to

smooth the adjustment process. In order to anchor expectations to intermediate targets it is

critical that the central bank has credibility for its final target and hence its outlined path

towards it. At the same time its credibility will also be measured whether intermediate targets

were achieved.

In our third part we discuss the effects of heterogeneous currency unions on expectations

forming. We show how asymmetric developments lead to inflation in one part of the union

and disinflation in another and thus both short-run and to some extent long-run expectation in

individual regions deviate from the policy target even though average expectations in the

union remain well-anchored.

Finally, we provide some empirical analysis based on the last 15 years of short-term and long-

term professional forecasts and include economic variables and historical variables which

confirm our earlier findings.

1 Note, that producers may accept depressed markups without adjusting prices or employment if the central bank

is expected to adjust its policy such that in the mid-term markups return to their profit-maximizing level.

8

2. Definitions of Inflation Expectations and Expectation Forming

2.1 Inflation Expectations and Expectations Forming

When examining the concept of inflation expectations, it is also of high importance to define

inflation itself more precisely. Monetary policymakers are responsible to preserve overall

price stability, which is commonly defined as low and stable inflation. This objective is

supported by a corresponding policy and therefore, policymakers need to evaluate the current

inflation rate and the overall trend in inflation. In this context, central banks differentiate

between core inflation and headline inflation. Headline inflation is calculated on an overall

price index, while core inflation excludes unprocessed food and energy prices from the index

calculation. This core inflation approach is motivated by the statistically highly price-volatile

food and energy index components due to temporary supply shocks. Prices of these goods are

not subject to stickiness – markets almost always clear by adapting prices instantly (to match

current supply and demand). Hence, short-term price fluctuations do not reveal inflation

trades but information about current supply and demand. Therefore, core inflation

communicates a more accurate picture of the underlying inflation trend in the short-term and

helps policymakers to achieve low and stable headline inflation over the long-term period.

According to academic literature there are two ways how economic agents form inflation

expectations. Mohanty (2012) defines the first approach as a variant of adaptive behavior

wherein expectations are formed by extrapolating the past and current experience into the

future. Apart from past experience, new available market information are therefore also

factored into the expectations of economic agents. In light of the term adaptive behavior, an

essential element is also that economic agents learn from their past inflation forecasting errors

(usually with regard to short-term expectation) and take these errors also into account when

forming their inflation expectations. Nevertheless, the expectation forming process is

ambiguous as economic agents may not revise their inflation expectations continuously, but

may proceed with their revisions on a periodically basis. Overall, this first variant of forming

inflation expectations is mainly determined by its backward-looking character.

The second variant of forming inflation expectations is characterized by its forward-looking

approach. This variant is commonly referred to as rational expectation forming in academic

literature. According to Muth (1961) the forming process could be considered as rational if

economic agents are forming their expectations after processing all available information and

also factoring in the reaction function of the monetary authority.

9

However, empirical research has revealed that inflation expectations are characterized by

significant errors. Neither the adaptive nor the rational expectation formation has been able to

predict the actual inflation in the past as noted by Orphanides & Williams (2004). This is

related to the fact that no economic agent has the analytical capability to conduct a perfect

forecast, which is especially true in a complex market economy that is also marked by

imperfections and uncertainty. It is consequently not possible to develop a forecasting model

that incorporates all relevant variables and makes accurate predictions about future inflation.

The difficulty of accurate predictions might also be related to inaccurate causal inference as a

central aspect of economic theory. “Expectations influence the time path of an economy and

conversely one might hypothesize that the time path influences expectations” according to

Evans & Honkapohja (2001).

Though it might not be possible to incorporate all relevant factors into a single prediction

model, it is possible to make a general statement about the behavior of variables in context of

a short-term and long-term expectation perspective. The distinction between short-term and

long-term is crucial for understanding the dynamics of inflation expectation formation.

According to Samuelson and Nordhaus (2004) the long-term contrasts with the short-term, in

which macroeconomic variables are considered as fixed. Hence, the short-term is commonly

defined as the time horizon over which parameter factors like the general price level,

contractual wage rates and other production inputs are inflexible and may not fully adjust to

the state of the economy. The short-term is not a definite time period, but an indicator

regarding the flexibility of variables involved in macroeconomic models. The long run is

defined as the conceptual time horizon over which expectations and the above mentioned

factors are flexible and have time to fully adjust to the state of the economy.

2.2 Inflation Targeting and Rule-Based Monetary Policy

A major influence on forming and anchoring of inflation expectations have been credible

implicit or explicit inflation targets. Following the successful implementation of explicit

targets in New Zealand, Chile and Canada in the early nineties a number of countries

including the United Kingdom, Finland, Sweden and Australia also adopted this type of

policy. In comparison with Germany, Japan, Switzerland and the United States these

countries previously had a poor record in fighting inflation and were now able to improve

their performance (Debelle, Masson, Savastano, & Sharma, 1998).

10

While old literature has primarily debated the attributes of various commodity standards, i.e.,

the representation of the par value of a currency unit by a certain amount of a commodity-

basket (see for example [F. D.] Graham [1942], [B.] Graham [1944], and Friedman [1951]),

recent literature has shifted the focus to inflation targets, i.e., the constant increase (within a

range or at a certain point) of the price level for a goods basket. Several academics like

McCallum (1988) and Taylor (1993) have even gone a step further by suggesting a rule-based

monetary policy that follows explicitly a mechanic operating routine in setting policy rates.

One can find arguments in Lucas (1980), White (1999), and Aoki & Nikolov (2004)2 that

such a system may eliminate monetary shocks, guarantee independent central bank policy,

prevent speculation about discretionary activist policy and mitigate feedback from past policy

mistakes. Even though Fendel & Frenkel (2006) provide some evidence that the ECB follows

the forward-looking Taylor rule in its decision making3 the current state of central bank policy

is more in line with Bernanke and Mishkin’s (1992) notion that „monetary policy rules do not

allow the monetary authorities to respond to unforeseen circumstances“. In addition, the ECB

(2001) notes with regards to the Taylor rule that its implementation could be only

incorporated in a dual mandate (as contrasted to the inflation-focus by the ECB)4. Hence, no

central bank is explicitly bounded to a specific monetary rule but rather uses such as a

supplement in its decision process.

The inflation target of the central bank provides a nominal anchor for other economic agents.

In contrast to the cases of activist monetary policy a credible target is incorporated by the

market in calculations of forward prices and costs. Bernanke, Laubach, Mishkin, & Posen

(2000) acknowledge that even small inflation rates lead to economic costs.5 However, an

occasionally debated target of 2% - that as Irwin (2014) describes originally developed out of

a historical accident – is set deliberately above zero percent to adjust for the statistical

underestimation of inflation rates and to permit negative real interest rates in a recession.

2 Interestingly, Simons (1936) developed some positive and normative arguments in favor of rule-based

monetary systems. 3 Notably, comments by Fed governor Janet Yellen that the Taylor rule provides “a rough sense of whether or

not the funds rate is at a reasonable level” (Federal Open Market Committee, 1995) and Bank of Japan board

member Nobuyuki Nakahara (justifying his dissent against a majority decision) that „some sort of explicit policy

rule, such as the Taylor rule or the McCallum rule, should be employed to help enhance communication with the

market“ (Bank of Japan, 2000). 4 Additionally, one could apply Goodfriend’s (2002) political argument regarding inflation targets to strict policy

rules: „it’s natural for any leader of an organization to worry about restricting his freedom of action in the

future“. 5 The simplified argument is that the amount of money held for transaction purposes in cash is reduced as a

larger part is invested in short-term illiquid assets. In absence of perfect foresight aggregate demand is kept

below its potential.

11

With reference to the works of Phelps (1967) and Friedman (1968), Lucas (1976) developed

his famous critique and popularized the rational expectations theory. It suggests that agents

include expected responses from policy makers in their decisions and adjust their behavior ex

ante. By contrast, the Phillips curve implies only an ex post reaction of wages and hence

allows real wages to decline in the short-term. With the flattening of the Phillips curve central

bankers began to recognize the long-run neutrality of money. In fact, with spreading

knowledge about the central bank’s inflationary cure against inflation this method became

even in the short-run ineffective.

At the same time it should be outlined that rational economic agents will not take all

information into account (in contrast to the classical homo economicus model with complete

information). Wiederholt (2010) considers this rational inattention as an optimization problem

that individuals with limited attention capacity face. From this point Sims (2003) concludes

that communication policy by the central bank is relevant. And going a step further the sticky

information model described in Mankiw & Reis (2001) suggests that prices are always

changing but pricing decisions are not always grounded on current information. Their paper

suggests that current prices may be a consequence of previous (short-term) expectations.

Hence, we may find a reason different than menu costs why short-term inflation expectations

do not translate instantly into higher inflation with the new short-term inflation expectations

being again well-anchored. Asset pricing theory would suggest that if the government

announces to purchase any gold in six months at $ 10,000 gold will instantly trade at $ 10,000

(adj. for cost of capital and storage). However, the sticky information model suggests that it

takes some time until information (e.g., about a current shocks) is fully disseminated and

processed in the market place.

This may also provide a reason why argument shifted from the activist school to the relative

passive system of credible inflation targeting to avoid inflationary shocks and results lagging

its underlying monetary policy. Mishkin (1999) shows that inflation targeting helped to

stabilize both inflation rates and expectations. According to Debelle, Masson, Savastano &

Sharma (1998) there are two prerequisites for inflation targeting: (1) independence from

government influence, and (2) independence from other mandates such as wages, exchange

rates and the level of employment. To mark its credibility some countries have additionally

adopted methods through which central bankers are softly penalized for missing it. For

example, the governor of the Bank of England has to write an open letter to the Chancellor of

the Exchequer if inflation deviates by one percentage point from the target rate.

12

Clark & Davig (2008) summarize research on the influences of inflation expectations which

include a range of variables such as energy and commodity prices, past inflation, the state of

the economy and monetary policy changes. However, one needs to differentiate between

short- run and long-run effects on expectations. The latter are usually smaller. Their research

shows that innovations to CPI inflation impose the greatest risk. Moreover, shocks to the

interest rate are a more modest variable. Shocks to energy and food prices do not impact core

inflation directly although may potentially change inflation expectations. This is a contrasted

by shocks to food prices that affect both core inflation and inflation expectations.

Clark & Davig also outline improved results for the inflation targets. Expectations seem to be

better anchored and also volatility of expectations and trend inflation is reduced (which might

be due to smaller volatility in the inflation target, changes in the strategy of monetary policy

or better understanding by the public of central banking).

A detailed view on the quality of anchoring (i.e., central bank credibility) can be found in a

recently published paper by Strohsal & Winkelmann (2015). A market implied target is

derived from break even inflation rate and compared the official target by applying an

ESTAR process. The ECB shows the best performance with a MIE of 2% while the inflation

expectations in the UK shows a weak anchor with a MIE of 4.3% even though both regions

follow the same policy target. With regards to the US, the strength of the anchor decreased for

the short-term period and increased for the longer-term during the post-Lehman period.

2.3 Practical Implication: Monetary Policy and Inflation Expectations

The European Central Bank (ECB) forms its monetary policy decisions in accordance with

the Maastricht Treaty of 1992 that states the primary objective of the European System of

Central Banks shall be to maintain price stability. The ECB defines price stability as “rates of

inflation below, but close to 2 % over the medium term”. Hence, the ECB adopted a clear and

explicit inflation target which is supported by its monetary policy actions. This approach of

monetary stabilization policy has historically resulted in a reduction of inflation and output

volatility as noted by Mishkin & Schmidt-Hebbel (2007) and is subsumed under the

guidelines of the new neoclassical synthesis (NNS) in macroeconomics. The new neoclassical

synthesis is a result of the convergence of classical macroeconomic theory involving features

such as rational expectations and real business cycle aspects and Keynesian theory involving

features such as monopolistically competitive firms, sticky price setting and monetary policy

aiming for stabilization. Goodfriend (2007) argues that the practical application of NNS in

13

forming monetary policy reinforces four main advances: the priority for price stability; the

targeting of core rather than headline inflation; the importance of credibility for low inflation;

and preemptive interest rate policy supported by transparent objectives and procedures.

Monopolistically competitive firms set their product prices as a result of their marginal cost of

production plus an additional markup. The production costs are determined by the level of

productivity, wages and material. However, the process to determine the appropriate price for

a differentiated product that maximizes the profits in every economic scenario is quite costly

as noted by Sheshinski & Weiss (1977). These costs to a firm resulting from changing prices

are referred to as menu costs. Moreover, obtaining the required information about the firms´

individual demand and cost conditions is difficult and often not realizable. And adaption for

any volatility may result in higher hiring and firing costs.

A key element of the new neoclassical synthesis is that firms will only adjust their product

prices in order to maintain a constant profit maximizing markup if aggregate demand and

marginal cost condition changes threaten to decrease or increase the actual markup

significantly and persistently away from the profit maximizing markup. However, firms move

their product prices with expected inflation over time. In contrast to the NNS, the classical

real business core (RBC) model would suggest firms to neutralize the effect of aggregate

demand and productivity shocks by adjusting their prices in order to keep the actual markup

close to the constant profit-maximizing markup. As a consequence of the firms´ behavior in

accordance with the NNS, the product markup would fluctuate in response to shocks of

aggregate demand and productivity.

In order to prevent that firms change prices and employment in response to those shocks,

Goodfriend (2007) argues that monetary policy should actively monitor and manage

aggregate demand taking aggregate productivity into account, such that marginal costs rise at

the targeted rate of inflation – then firms will automatically raise product prices at the

expected targeted rate of inflation, because they are confident that this price behavior will

keep actual markups close to the profit-maximizing markup. By managing actively the

nominal interest rate, the central bank can boost or compress aggregate demand and thus,

keep markups close to their profit-maximizing level and meet low inflation expectations.

Increasing the real interest rate has a decreasing effect on current aggregate demand due to

increasing opportunity costs of current consumption in terms of future consumption.

14

The Federal Reserve Bank focuses on core inflation6 without the effect of food and energy

prices when deciding about the appropriate measures for an efficient monetary policy.

Targeting headline inflation is not necessary given that prices for food and energy are

naturally highly volatile as there markets always clear supply and demand. They are not

subject to sticky price.7 Therefore, the central bank is recommended to stabilize employment

and markups, while the economy adjusts to food and energy price shocks independently.

Simultaneously, core inflation would also be a more stable nominal anchor for inflation

expectations.

As mentioned above, price setting is a costly matter for firms with the obvious implication

that firms care about future costs of production as well when setting prices in order to

maintain their profit-maximizing product markup. When the central bank has full credibility

for its inflation target, then firms are confident that inevitable fluctuations of the actual

markup are just temporary as monetary policy is expected to restore the optimal balance. In

effect, full central bank credibility for low core inflation targeting makes expectations about

future costs of production in the sticky price sector invariant to aggregate demand shocks with

the result that inflation expectations themselves anchor current price setting decisions to the

targeted inflation rate. As a result, credibility is important for the central bank to anchor

inflation expectations as it can only manage real interest rates with its nominal interest rate

policy. Since real interest rates represent the relative price of current to future spending, real

interest rates have a direct effect on aggregate demand. Therefore, expectations regarding

future income need to be anchored independently of the monetary policy in order to provide

the nominal interest rate policy the leverage to manage current spending, meaning current

aggregate demand. Central bank credibility can contribute at this point by anchoring expected

future product markups to profit-maximizing markups. As a consequence, expectations about

future income are anchored to productivity growth and other real business cycle factors that

are independent of monetary policy.

As argued by Williams (2003) and Wicksell (1936) stabilizing inflation is only possible if the

interest rate policy reflects the volatile natural rate of interest that keeps actual markups close

to profit-maximizing markups and supports real business cycles by effecting aggregate

demand. Inflation targeting is technically challenging, because the natural rate of interest is

6 By contrast, HICP includes headline measures. 7 Note, however, that central banks in emerging markets frequently target headline inflation. The reason is that

these goods compose such a large share of the consumption basket that changes in headline inflation are the

crucial element in individual expectation forming. Moreover, there are sometime some social-political arguments

put forward as the central bank attempts to prevent increases in food prices for the very poor as illustrated by Raj

and Misra (2011).

15

not directly observable in the markets. However, Goodfriend states that within its classical

mandate and operations the central bank can only determine the short-term interest policy,

which must exert its leverage over current aggregate demand through its leverage over longer-

term interest rates.8 He further notes that according to the expectations theory of the term

structure, longer-term interest rates move with an average of expected future short rates.

Consequently, the accurate prediction of the effect of interest rate policy on longer-term

interest rates and aggregate demand requires the central bank to understand the dynamics of

market responses to given short-term interest rate actions and the implications for the future.

For the accomplishment of this goal, communication is an essential element for the central

bank in order to achieve effective interest rate policy. Goodfriend summarizes this aspect with

the argumentation that ad hoc announcements can reinforce, but not substitute for a genuine

mutual understanding between markets and the central bank. The understanding would need

to be created on the basis of an explicit, credible low-inflation objective supported by a policy

rule – “a systematic articulation of how a central bank intends to move its short-term interest

instrument in response to macroeconomic news to achieve that objective”.

3. Interdependence Between Short-Term and Long-Term Expectations

3.1 Influence of Short-Term on Long-Term Expectations - Exogenous Shocks and

Credibility Proofs

If the central bank has a credible inflation target and inflation expectations are well-anchored

short-term price fluctuations in certain sectors do not effect long-term expectations. This price

volatility indicates shortages and surpluses of certain goods rather than inflationary trends that

are due to inappropriate monetary policy. To illustrate this proposition we will use the oil

crisis of 1973 as an example. It was handled in different ways by different central banks,

eventually culminated in a period of runaway inflation the US and was not ended before

disinflationary measures were put into place by Federal Reserve chairman Paul Volcker. By

contrast Germany and Japan showed a better inflationary performance.

8 Targeting long-term interest rates occurred under “Operation Twist” in the early sixties and recent quantitative

easing by the Fed as noted by Swanson (2011). The discussion also came up during the purchases of long-term

bonds by the Bank of Japan as remarked by Saito, Hogen & Nishiguchi (2014), and recent quantitative easing by

the ECB – albeit the latter may have been also due to practical constraints as there is not enough short-term debt

outstanding to meet its targets. However, a central bank exposes itself and the taxpayer to interest rate risk when

it purchases long-term bonds. Once it increases again interest rates this may even lead to a technical bankruptcy

as argued by Buiter (2008).

16

Inflation expectations were better anchored in the 2000s than in the 1970s. Following a

tripling of oil prices, inflation in core consumer goods (other than food and energy) rose

sharply between 1975 and 1980. However, as Clark & Nakata (2008) contrast that consumer

price inflation remained flat between 2001 and 2007 despite a quadrupling of oil prices. They

argue that better-anchored inflation expectations yield shorter-lived inflation spikes.

In contrast to endogenous shocks9 exogenous distortions come from changes in variables

outside of the aggregate demand model. In our case there is an increase in oil prices, which is

particularly threating to an oil-importing country.

After the Arab oil embargo in 1973 oil prices more than doubled. Such a shock affects both

core and headline inflation. Energy prices are not directly a part of core inflation. Their

markets instantly adjust for changes in supply and demand. Central banks do not need to

adapt interest rates in order to avoid negative consequences from sticky prices. However, oil

is also a major input material for various goods such as plastic and energy-intensive

industries. Thus, if the change in prices is persistent, then also other good markets will be

affected.

At given monetary policy it is obvious that short-run inflation expectations tend to rise.

However, long-run expectations do not change per se. Such a shock may occur within a

normal random-walk model for commodity prices. It is an unexpected and sudden move that

tends to mean-revert in the long run. Hence, there does not have to be a link between short-

term and long-term expectations.

The first oil price shock differed from this notion. Goodfriend (1993) defines an inflation

scare as a rise in expected long-run inflation which can be interfered from a „long-rate rise in

absence of an aggressive fund rate tightening“. 10 As the market anticipates persistent

inflationary pressures it adjusts the term structure of the yield curve for a sustainable up-ward

9 An example for an endogenous shock is a change in long-run productivity. In the late 90s the rapid

acceleration of computer and information technology resulted in widespread optimism about the future. This can

be exemplified by a hypothesis by Allen Greenspan: “It is the observation that there has been a perceptible

quickening in the pace at which technological innovations are applied that argues for the hypothesis that the

recent acceleration in labor productivity is not just a cyclical phenomenon or a statistical aberration, but reflects

– at least in part – a more deep-seated, still developing, shift in our economic landscape” (1996) and was

supported by for example Gordon (1999) and contemporary views on economic and historical smoothing such as

in Weber (1997) and Fukuyama (1992). As growth expectations rise a classic RBC model would suggest to

increase the long-term real interest rate (expectations) by the same number in accordance with the approximation

𝑟 = 𝜌 + 𝑔 (Goodfriend, 2004). 10 Goodfriend & King (2005) highlight the fact that the FOMC considered long-term interest rates as indicators

of inflation expectations and their credibility and viewed with concern the implied „u-turn“ as the recessioned

deepened.

17

adjustment of the federal funds rate. By contrast, the short-rate (i.e., funds rate) remains

unchanged as it is set by the central bank.11

The Federal Reserve made an attempt to reduce inflation by sequentially increasing the

federal funds rate up to almost 12% in 1979. However, it failed to stabilize the inflation rate at

already elevated level of ca. 6% (but less than the previously seen 12%) in 1977. One reason

for not aggressively increasing the interest rate may have been the recession of 1973-1975 on

the back of the supply shock. The central bank failed to defend its credibility for stable prices

and the period was dominated by stagflation.

Similar like credit controls in 1980 mentioned in Goodfriend (1993), Jimmy Carter’s (1979)

tangible and intangible demand side policies have affected aggregate demand but not cured

the inflation scare.

By the time Paul Volcker became chairman of the Fed in August 1979 oil prices would

double from 1978 to 1980 and triple until 1981 following the Iranian revolution.

Nevertheless, he was determined to fight inflation and increased the federal funds rate from

11.4% in September 1979 to 17.6% in April 1980. As it can be seen from the 30-year bond

yield this move was only considered to be temporary. The yield rose from 9.2% in September

to 12.3% in March and fell back to 11.4% in April. The interest rate peaked at 14.1% in

February 1980 when increases where paused due to a weaking economy. The fact that a

national election was upcoming may have put additional pressure on the Fed.

As a consequence the inflation scare returned with an increase in the long-rate by 2%. The

Fed promptly reacted by a sharp 3% raise in its target rate to regain its long-term credibility.

Disinflationary measures resulted in 9.9% decline of GDP in the second quarter of 1980

which was followed by an 8.4% increase in the fourth quarter on the back of easing credit

controls and monetary policy.

The disinflationary measures peaked with a 19.2% fed funds rate in 1981 which was followed

by a recession but also declining inflation rates. Albeit inflation rates had been smaller in

1984 there was another increase in the long-rate and the central bank again proved its

credibility by increasing the short-rate. Eventually, the second half of the 1980s marked a

period of maintained credibility. As Goodfriend (1993) observes the recession of 1990-1991

11 Another example for such a change in the yield curve can be sometimes found at the peak boom times when

the normally, upward sloping yield curve becomes downward sloping. The market anticipates a recession an

interest rate cuts. The flattening of the Euro yield curve in 2015 follows a similar logic: long-term growth and

inflation expectations are adjusted downwards.

18

demonstrates that this objective was achieved: The Fed was able to reduce the fed funds rate

from 8% to 3% within two years without a significant increase in inflation.

The following years thus allowed to sustain a low fed funds rate and inflation rate at the same

time. Inflation expectations had been re-anchored.

The experience in the 1970s indicates a link between short-term and long-term expectations.

Firstly, while short-term exogenous shocks do only have an effect on short-term expectations

they may translate into elevated long-term expectations if they are seen as sustaining and the

central bank lacks sufficient credibility for its target. The crucial link is the ex-ante absence of

credibility and sufficient anchoring of long-term expectations. The decrease in credibility, we

guess, may also develop if there are multiple sequentially persistent (i.e., accumulating)

inflationary shocks which the central bank does not accommodate.

Secondly, it also includes the aspect of policy changes which we will discuss later. Policy

changes and credibility proofs have a strong effect on the short-end once they are implement

but need to be in place for a sufficient time to demonstrate their credibility and thus affect

long-term expectations. Trend inflation expectations are adjusted downwards not per se by a

spike in interest rates but only if the central bank is considered to pursue a focused

disinflationary policy whenever expectations are above its target (i.e., it prioritizes the

inflation target over other objectives). Indeed, in the short-run a central bank may have to

prove its credibility even at the risk of a recession.

Clark & Davig (2008) introduce the following model for time-varying trend inflation:

𝜋𝑡∗ − 𝜋𝑡−1

∗ + 𝑣𝑡 with 𝑣𝑡 ~ 𝑁(0, 𝜎𝑣2) (1)

They argue that generally long-term inflation expectations imply the private sector’s belief in

the long-term target rate and given the long time horizon of SPF forecasts (e.g., 10 years)

these should not be influence by short-run fluctuations; especially if the central bank is

considered as credible.

The model also suggests that there is a premium for volatility which can be easier explained

within an asset or option pricing framework. The authors note that the stochastic volatility

have been declining since the late 1990s. Volatility occurs due to shocks, inefficient inflation

management or changes in targets. The study shows, that both volatility of food and energy

prices as well as short-term expectations and core inflation rose during the recent years (albeit

for the latter starting from a low base rate). By contrast, volatility of long-term expectations is

19

on a downward trend. From this interferes, that trend inflation is better anchored as it

accounts for less overall volatility.

3.2 Influence of Long-Term on Short-Term Expectations – Credibility of Policy

Changes

As already discussed in a previous sub-chapter policy changes have an effect both on the

short-end and the long-end of the expectations curve. Short-term expectations are affected by

the measures taken to implement the new target and long-term expectations change if the new

target is perceived as credible. This was exemplified by the Volcker disinflation.

Moreover, distortions to long-term expectations can occur if the central bank loses credibility

for its target even without explicitly changing it. We have already illustrated the example of

an oil crisis and the central bank only passively accommodating the shock. Now we will

continue our discussion by focusing on explicit policy changes, particularly the introduction

of inflation targets in emerging markets.

Inflation targeting has been suggested to emerging markets by Batini & Laxton (2007) and

Batini, Kuttner, & Laxton (2005) following the tradition of Mishkin’s (1999) „just do it“.

Their main argument has been that countries with historically high inflation rates would be

able to achieve smaller ones and reduce volatility of inflation expectations. Their general and

unconditioned recommendation contrasts the technical and fiscal prerequisites mentioned by

Fraga, Goldfajn, & Minella (2004). However, it should be mentioned that Ball & Sheridan,

(2004) do not find positive evidence in favor of inflation targeting as a mean to achieve low

inflation rates. Their study suggests that this objective may have been also achieved by a

regression to the mean although the authors acknowledge that future works may reach

different conclusions.

Initial research on the case of inflation targeting in India provided mixed conclusions. Kannan

(1999) argues in favor of inflation targeting albeit criticizes the contemporary WPI inflation

measure. It is outdated and deviates from a more complete CPI inflation measure. Hence, the

measure for the central bank is not the same as that on which expectations are grounded on.

Moreover, he outlines reasons for time dependent targets. These step-down inflation targets

were used to introduce the system in New Zealand, Spain, Canada and Mexico. It has to be

20

taken into account that inflation usually follows monetary policy with a time lag.

Additionally, disinflations can be costly in terms of short-term output. Yet, credibility may

also be achieved by “just doing it“ in spite of the hardships of a recession.

Mahajan, Saha, & Singh (2014) raise concerns with regards to preconditions such as an

efficient transmission mechanism, large supply and demand shocks, social costs and short-

term growth trade others. Similar arguments are set forth by Jha (2008).

In spite of this opposition Rajan (2013) explained his objective of low inflation during his

first speech as the governor of the Reserve Bank of India. Moreover, he also initiate the

issuance of inflation protected securities. In our view, this step helps to anchor inflation

expectations (at least during the term of the bonds) as with regards to these it is in the

government’s self-interest to keep inflation low in order to avoid interest expenses.12 For this

purpose a step-down target was implemented. The objective is to achieve a nominal inflation

rate of 8% by January 2015, 6% by January 2016 and 4% (+/-2%) thereafter (RBI, 2014).

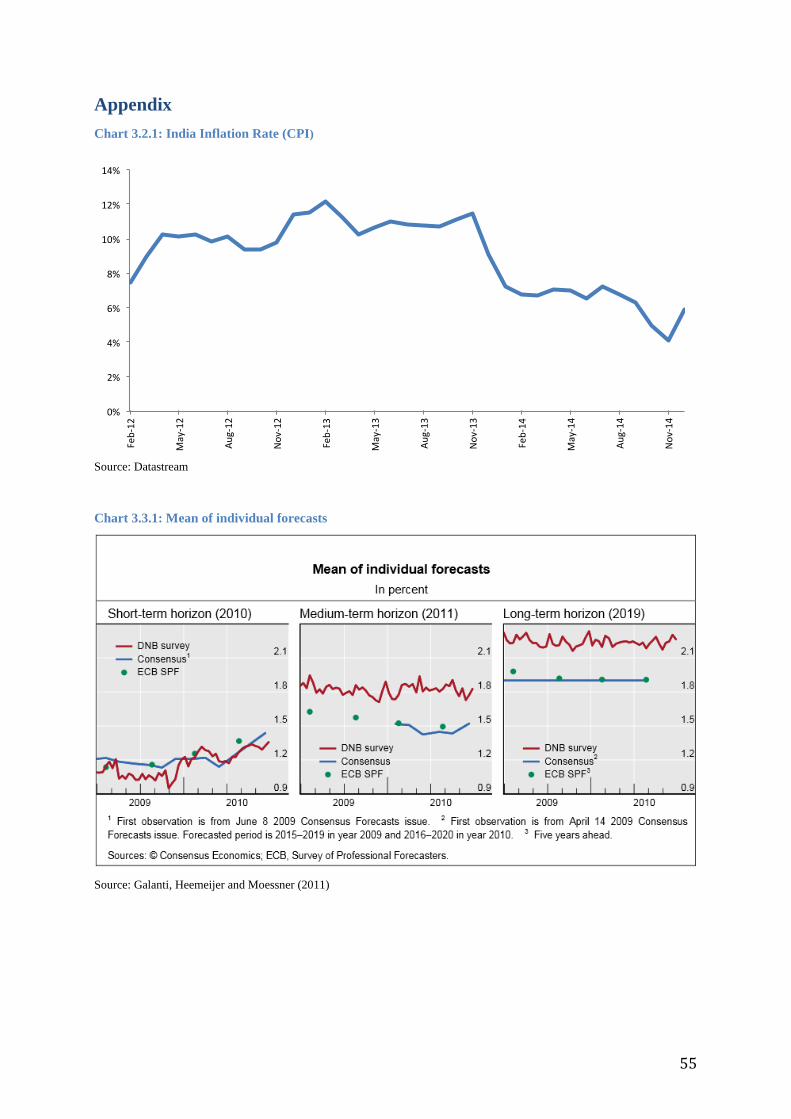

Albeit the target of 6% was considered as more difficult than that of 8% the RBI has already

accomplished (deliberately or indeliberately) it (see Chart 3.2.1 in Appendix). With sufficient

resources for the central bank and to reach its long-term targets and political will to reduce

volatility in the process of doing so the step-down targets can be perceived as credible.

At the same time a failure to achieve not more than 8% by 2015 might have resulted in a loss

of credibility for the recently celebrated central bank and his institutions. This would have

affected the 4% long-term target as the central bank would be considered to inflate beyond its

promises. At the same time the step-down target offers some of the advantages of a target

range (e.g., they possibility of managing demand without losing credibility) and that the

adjustment process is smoothed. However, for this purpose the central bank has to „remain on

track“.

To conclude our remarks on India we raise the issue that the Rupee has certain commonalities

with the Euro. Both are imperfect currency zones. Briefly relating to Mundell (1961) and van

Marrewijk, Ottens, & Schueller (2006) we are particularly concerned about the heterogeneity

across the 36 states and union territories. They differ in terms of languages, literacy rates,

political views and policies, the structure of the economy (e.g., rural and urban industries), the

12 A counter argument is that tax revenue would increase. However, in contrast to non-indexed bonds the

expense (and hence the liability) on IPS increases with the inflation rate.

21

size of the economy13 and different growth rates, legal barriers to labor mobility and home

good biases. These contrasts are subject to shocks leading to different levels of optimism and

pessimism about both the short-term and long-term future and consequently resulting in

individual inflation and deflation scares given the homogenous interest rate across

heterogeneous regions. Albeit GDP (as the weighting factor for the price index) is less

concentrated than in Europe one may still expect that a few large regions will determine the

monetary policy of the central bank at the expense of smaller ones with different economic

developments and expectations. Hence, we would expect long-term expectations better

anchored in large regions than in smaller ones.

3.3 Measuring Dynamics of Inflation Expectations - A Survey Approach

Inflation expectations are important indicators and determinants of observed inflation, but

academic literature and central banks are still arguing about the appropriate measurement of

expectations. Consequently, inferring how inflation expectations affect actual inflation

remains a difficult task as noted by Bernanke (2007). Empirical research on the measurement

of inflation expectations can basically be attributed to two approaches: the measurement of

inflation expectations based on inflation surveys such as Carlson & Parkin (1997); Branch

(2004) and the measurement of inflation expectations based on inflation-indexed financial

market instruments such as Gurkaynak, Levin & Svanson (2007); Barr & Campbell (1997).

Ang, Bekaert & Wei (2007) compared several inflation forecasting models, including simple

regime switching models and different variants of Phillips curve and term structure models,

and figured that survey measures of expected inflation provide better forecasts of inflation

than any other alternative. In addition, Forsells & Kenny (2002) analyzed survey data on

inflation expectations of consumers in the euro area and found that the observed expectations

seem to incorporate – though not always completely – the information contained in a broad

set of macroeconomic variables. In this context, survey measurements of inflation

expectations have been approved as the most direct and accurate method in terms of

forecasting power and are commonly used for research on inflation.

A research survey (DNB survey) on the formation of short-term and long-term inflation

expectations has been conducted by Galanti, Heemeijer and Moessner (2011), which provides

important information about the causal relation between short-term and long-term

13 Per capita income between Goa in the west and Bihar in the north east differs by a factor of 7.4:1 (Government

of India, 2014). By contrast, difference between the small European countries Luxembourg and Malta is only

5.5:1 (IMF, 2014).

22

expectations as well. We find the survey perfectly suited because it was taken directly after

the financial crisis and would allow to observe whether inflation expectations and especially

anchoring properties of long-term expectations have been affected by the crisis. Moreover, it

incorporates three novel features compared to existing surveys of inflation expectations: (1)

the survey has been conducted on a weekly basis between July 2009 and July 2010 and has

therefore a considerably higher frequency than surveys that have been conducted on a

monthly or quarterly basis (such as SPF and Consensus Economics). This novel feature

allows a more precise insight into the expectation formation process such as the frequency of

expectation changes over the short-term and long-term horizon. However, we acknowledge

that the survey period might appear too short. (2) The survey participants were provided with

macroeconomic information sets in order to examine the heterogeneity of inflation

expectations. (3) The survey participants received an incentive reward based on the accuracy

of their individual inflation forecasts in order to obtain most accurate survey responses.

The 129 survey participants, consisting of central bankers, academics and students, were

asked to indicate their personal expectations on short-term and long-term inflation in the euro

each week shortly after they received the information set (consisting of an updated HICP

inflation data on a national and euro area level, and - only for central bankers - an updated

Consensus mean forecasts). Below we have summarized the most important findings of the

survey and combined them with findings of other researchers in order to examine the causal

link between short-term and long-term inflation expectations.

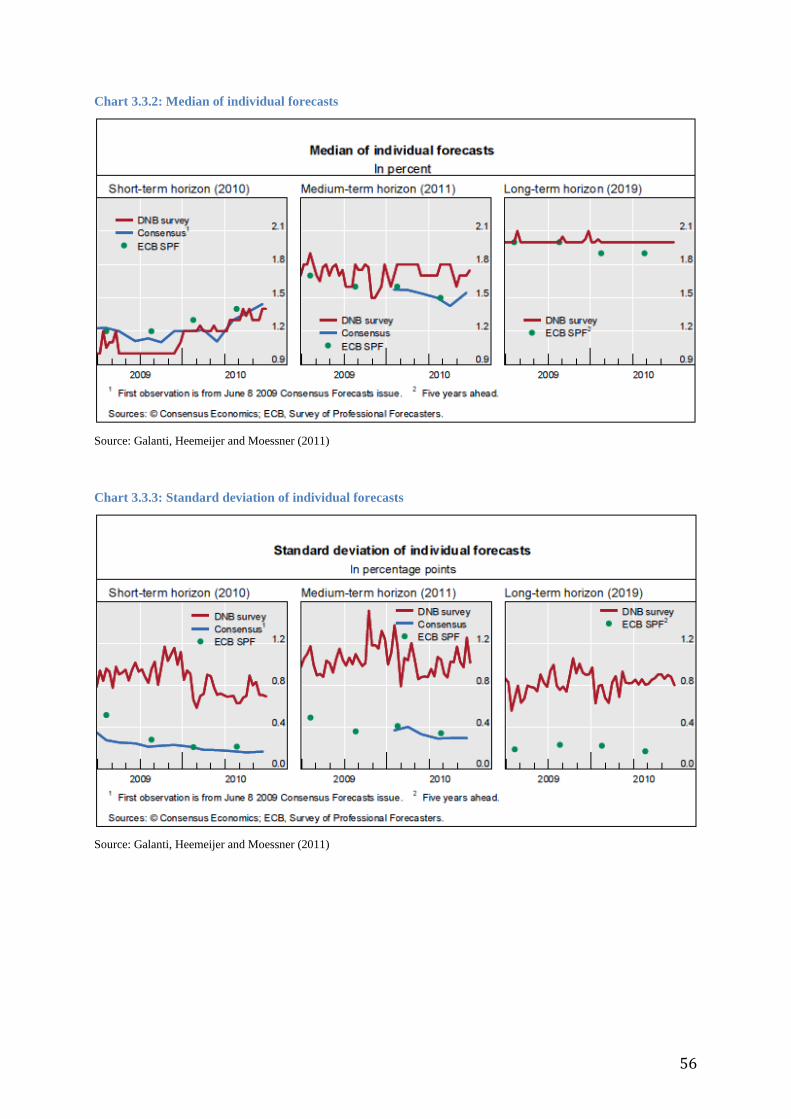

The means and medians of the survey inflation forecasts indicate a distinct tendency in the

data set (see Chart 3.3.1 & 3.3.2 in Appendix). Long-term expectations have remained fairly

stable at 2%, while the means and medians of short-term expectations started initially around

1% and increased over the survey period. Galanti, Heemeijer and Moessner argue that this

seems to suggest that participants considered the observed low levels of inflation in 2009 and

early 2010 shortly after the peak of the financial crisis to be temporary and believed the

economic climate in the euro area to gradually normalize. This observation is supported by

the clear upward trend of the short-term expectation means. The data also suggests that long-

term expectations have remained well-anchored, considering the uncertain economic situation

after the financial crisis, and have not been affected substantially by the factors that had an

impact on the formation of expectations over the short-term horizon. This conclusion is

supported by the long-term medians which are stable at the ECB´s inflation target of 2% over

almost all weeks. The fact that the long-term means are all above the target is in line with the

conclusion as according to Bernanke (2007) even long-term inflation expectations do vary

23

over time. In reality expectations are often not perfectly anchored since the extent to which

they are anchored can change, depending on economic developments and especially debates

about current and past conduct of monetary policy and limitations to its effectiveness.

Furthermore, there are also other potential explanations for deviations from a central banks´

inflation target. One explanation is illustrated by Capistràn and Timmermann (2008) as the

concept of asymmetric loss. The idea behind this concept implies different costs of over- and

under-predicting inflation across participants. If the associated costs of under-predicting

inflation are higher for a particular survey participant than the costs of over-predicting, then it

would be optimal for this participant to bias his expectation forecasts towards higher

inflation.14 As a consequence that participant would reduce the probability of more costly

under-predictions. However, participants might also be misguided by heuristics for their

inflation forecasts. Brazier et al. (2008) describe lagged inflation and a central bank´s

inflation target as two potential heuristics between which economic agents switch depending

on their past performance. Therefore, economic agents are likely to abandon their previously

selected prediction mechanism if the corresponding forecasting error has passed some

threshold.

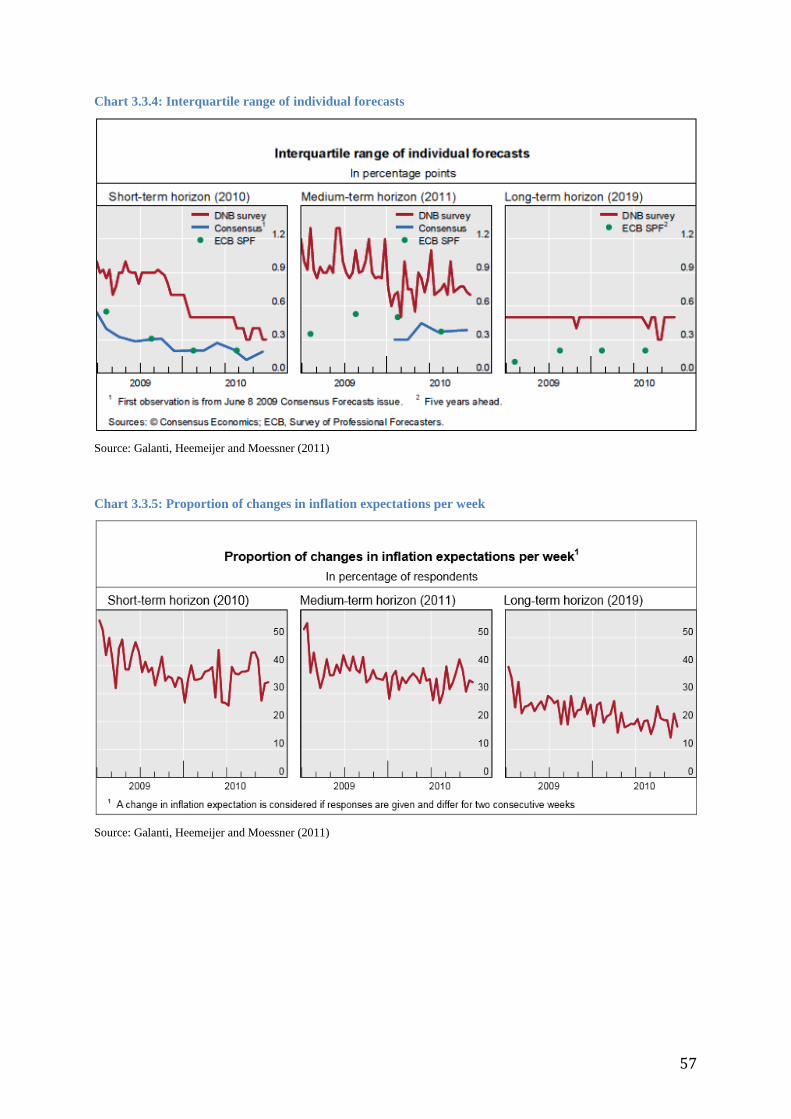

Since the survey comprises a relatively large number of participants, the obtained data results

have also been used to examine the disagreement across survey respondents. Mankiw, Reis

and Wolfers (2003) argue that disagreement regarding inflation is correlated with a great

number of macroeconomic variables and even conclude that disagreement might be a key to

understanding macroeconomic dynamics. This viewpoint is consistent with the theoretical

model of Lucas (1973) within which heterogeneity of expectations is crucial and the survey

authors were indeed able to extract important information by looking at the observed

disagreement. The standard deviation and interquartile range of the individual inflation

forecasts (see Chart 3.3.3 & 3.3.4 in Appendix) show that the disagreement within the survey

is smaller at the long-term than at the short-term. Furthermore, the disagreement measured by

the interquartile range at the long-term has remained noticeable persistent. We note that this

appears to some degree contradictive at first sight as the near future (short-term) should

intuitively be easier to forecast as the more distant long-term. This finding suggests that long-

term expectations are presumably affected by focal points such as the ECB´s inflation target

14 Intuitively, one may propose that inflation rates and the corresponding are somehow long-normally

distributed. Using a classical option pricing model this results in paying a higher premium for the call option

than for the put option. Inflation protected securities effectively provide this call (This is especially visible if one

purchases the security and shorts a corresponding fixed rate bond. The profit from this operation is π − i =[0, ∞).

24

based on its definition of price stability. On the other side, the formation of short-term

expectations seems to be more speculative from the participants´ perspective as it based more

on current macroeconomic information varying over time. However, the continuous decrease

in disagreement over the short-term horizon (see Chart 3.3.4 in Appendix) might be linked to

the provided information datasets that have been accumulated and factored into the

expectation formation process as part of adaptive learning over the survey period. There are

many examples in academic literature such as Bullard & Mitra (2002) who have shown that

the process of learning can affect the dynamics and even the potential stability of the

economy. Furthermore, these findings imply that understanding the dynamics of public

learning about the economy affects the form of optimal monetary policy (Gaspar, Smets and

Vestin, 2006). Overall, the survey results are consistent with similar research such as

Capistràn and Timmermann (2008) who analyzed different survey forecasts and remarked

that “strong differences in inflation forecasts are found even at short forecast horizons and

among professional forecasters with access to many common sources of information”.

As the survey has been conducted on a weekly basis and therefore on a comparatively high

frequency, it allows a comprehensive insight how frequent the participants revised and

changed their inflation expectations. The overall average percentage of participants who

revised and changed their expectations declines from 38.5 percent at the short-term to 23.5

percent at the long-term horizon (see Chart 3.3.5 in Appendix). This suggests that long-term

expectations are revised less frequently relative to short-term expectations in response to

macroeconomic news according to Galanti, Heemeijer and Moessner. The finding that long-

term expectations are revised less frequently than short-term expectations is also supported by

the analysis of the duration of spells when expectations remained unchanged. The mean

duration of spells of 2.4 weeks at the short-term increased to 3.4 weeks at the long-term. In

addition, the analysis of the distribution of weekly changes in inflation expectations reveals

that if participants changed their inflation expectations, the changes in long-term expectation

(mean absolute change of expectations of 0. 54%) were larger than the changes in short-term

expectations (mean absolute change of expectations of 0.47%). Comparable results have been

found by Kenny & Forsells (2004) who examined actual and expected inflation over the

period 1985-2005 and their results suggest that consumers revise their expectations and adjust

them in order to be in line with the actual inflation. Regarding the speed of adjustment they

figured that the monthly data indicates a quite low persistence in deviation of actual and

expected inflation. Therefore, the data suggest that consumers react quite quickly when

revising their expectations in response of new information and while actual and expected

25

inflation may drift apart in the short-run, they ultimately revert towards each other. We find

this consistent with the results of the survey, which show a lower duration of spells and a

lower mean absolute change of expectations at the short-term compared to the long-term.

Moreover, Kenny & Forsells also conducted an efficiency test on the data from 1985-2005

and found that consumers seem to incorporate – though not always completely – the

information contained in a broad set of macroeconomic variables. This degree of efficiency

seemed to have increased over time, but they note that this may not be interpreted as

increasing rationality over time. Inflation in the euro area has declined and become less

volatile over the last decades. In combination of greater ECB credibility, this development has

made it easier to predict future inflation overall. Again, we find this consistent with the

findings of the survey data which suggests well-anchored long-term expectations at the ECB´s

definition of price stability, illustrated by stable expectation means and medians and lower

volatility of expectations at the long-term. Furthermore, the survey participants have shown a

continuous decline in disagreement which might be linked to accumulated information sets

factored into short-term expectations over time.

An interesting approach of the DNB survey is to test whether the financial crisis has affected

the ECB´s credibility to target a stable inflation level according to its definition of price

stability of close, but below 2 percent. The survey is perfectly suited for this analysis as it has

been conducted shortly after the peak of the financial crisis in 2008 and households were

confronted with increased uncertainty. The authors presume that unprecedented monetary

easing in combination with the accumulation of large fiscal debt in the euro area, might have

undermined the confidence of economic agents in the central bank´s credibility for its

inflation target over the long-term. As discussed above, the long-term medians which are

stable at the ECB´s inflation target of 2% over almost all weeks of the survey horizon confirm

the ECB remaining credible though the long-term means are slightly above the target.

However, long-term inflation expectations can only be classified as being well-anchored if

these are not significantly affected by news about macroeconomic indicators as discussed by

Clark and Davig (2008). Therefore, the research study tested whether changes in inflation

expectations means have been associated with changes in Eurostat flash estimates as part of

the euro area HICP information. The empirical results show that changes in HICP flash

estimates have affected short-term inflation expectation means significantly at the 1 percent

level, but have not affected long-term expectation means. In this context, Bernanke (2007)

argues that inflation expectations can be classified as being anchored if they appear relatively

insensitive to new incoming data. Therefore, the result indicates that inflation expectations

26

have remained well-anchored at the long-term and the ECB could maintain its credibility for

its inflation target of close, but below 2% over the long-term.15

As just discussed above, long-term inflation expectations appear to have remained well-

anchored and were not significantly affected by macroeconomic news such as HICP flash

estimates in the aftermath of the financial crisis. However, Galanti, Heemeijer and Moessner

examined specifically in greater detail whether public deficits and the accumulation of large

fiscal debt might have affected inflation expectations. In order to investigate the influence of

debt concerns on inflation expectations, they tested changes in CDS spreads of euro area

economies and changes in Greek CDS spreads for statistically significant effect on changes of

inflation expectation means.16 The results show that changes in CDS spreads of euro area

economies had a statistically significant effect on changes of short-term inflation expectation

means (at the 1% level), but not on changes of long-term inflation expectation means.

However, while Greek CDS spreads also had a statistically significant effect on changes of

short-term inflation expectation means, they also had a significant effect at the 5%

significance level on long-term inflation expectation means. Overall, the results suggest that

short-term inflation expectations have not been immune to concerns about possible debt

monetization in order to deal with excessive public debt in Greece and in the euro area as a

whole. Moreover, concerns about the Greek sovereign debt crisis seem to have affected euro

area long-term inflation expectations as measured within the survey. Though the effect on

inflation is very small in economic terms, the results suggest that the ECB´s anchoring of

inflation expectations has not been completely insensitive to the turmoil in peripheral

sovereign bond markets in the euro area, which is again in line with Bernanke´s remark that

inflation expectations are not perfectly anchored in real economies.

We find that surveys give an appropriate impression of inflation expectations and their

development over time. With respect to the findings in this chapter we propose that the causal

link between short-term and long-term expectations can be found when looking at the quality

of expectation anchoring of central banks. The term “anchor” does not only imply stable

inflation expectations close to the central bank´s inflation target such as the ECB´s definition

of price stability of close, and below 2% over the long-term, but also insensitiveness to

15 We refer deliberately to long-term rather than the suggested medium-term to emphasize our notion on long-

term anchoring. 16 Galanti, Heemeijer and Moessner acknowledged that “a caveat within this approach of using CDS spread as a

measure of perceived risk of debt monetization through higher inflation is that expectations of debt monetization

via the printing of money by central banks, and associated expectations of higher inflation, could be associated

with lower sovereign risk, since higher inflation would lower the real burden of debt”.

27

macroeconomic variables in form of new incoming economic news. Economic agents seem to

be more confident in forecasting long-term expectation than they do at the short-term horizon.

The findings show that short-term expectations are more volatile and sensitive to

macroeconomic developments than long-term expectations in light of the difference in

relative time and flexibility of affecting variables.

4. Implications of a Heterogeneous Currency Union on Expectation

Building – The Current Case of the Euro Area

4.1 Theory and Implications

According to Petreski (2007) the Euro zone is not an optimum currency zone as qualified by

the criteria of Mundell (1961). While capital mobility is largely given, labor mobility remains

small and may thus increase the volatility in the business cycle (Burda, 1999) 17 .

Consequently, one may expect more volatile short-term inflation expectations, as the central

bank is not able to fully accommodate shocks in every single region. If the central bank fails

repeatedly to demonstrate its credibility within a particular region it risks a deviation of long-

term expectations for the explicit, global inflation target.

The Euro zone is in many ways similar to a currency peg between countries with

heterogeneous properties. Independent interest rate policy is impossible. Hence, inflation and

deflation scares may develop. In contrast to the US inflation differentials are larger and

longer-lasting in the EMU. In their position paper Darvas & Wolff (2014) argue that the ECB

should care about them, mostly to prevent contagion from deflation scares from one country

to another, and Fendel & Frenkel (2009) find some evidence that in fact it did.

Following the models by Goodfriend (2007) we find the (expected) productivity level, home

good bias and impatience as the exogenous variables that influence a country’s borrowing

behavior vis-à-vis a different country (e.g., trade surplus or deficit).18 These variables of both

countries also influence the terms of trade, and together with the interest rate employment in

the given period. For example, greater impatience lowers the terms of trade of the home

country, moves its balance of payments into the negative, increases the real interest rate –

encouraging households in the foreign country to save more and finance the former’s trade

17 As Bentivogli & Pagano (1999) argue labor mobility may not be a large problem if the currency union is not

prone to asymetric shocks or there are alternative adjustment mechanisms. 18 See formula (23) in Goodfriend (2007).

28

deficit, and boosts employment in the home country in the current period and reverses the

effect in the following period.

The terms of trade are exogenously defined by the current level of productivity, time

preference and markups in both countries and the trade deficit which itself is defined by the

current and expected productivity and markups in the home country, current and expected

home good bias and impatience in the home and the foreign country. If both countries are able

to stabilize their price level 𝑃𝐴𝐴 and 𝑃𝐵𝐵 the exchange rate 𝑒 will thus equal the terms of

trade: 𝑇 = 𝑃𝐵𝐵

𝑃𝐴𝐴 𝑒.

However, if the exchange rate is constant (e.g., currency peg or currency union), and terms of

trade are determined exogenously then at least in one country we can observe a deviation

from price stability.

Because of the impossible trinity in international economics a fixed exchange rate and free

capital movement lead to a no longer independent interest rate policy. This means, that in

order to achieve the fixed exchange rate within a no-arbitrage context, a central bank has to

mimic nominal interest changes of the currency area it wants to peg to. In a currency union

we have one single central bank and individual national banks only foster the transmission

mechanism following the rules forth by the central entity.

In the context of the EMU, the ECB has the single mandate of price stability, which is defined

as an increase of “an increase in the Harmonized Index of Consumer Prices (HICP) of below,

but close to 2%, over the medium term”. The Harmonized Index of Consumer Prices is

inevitably biased towards large countries in the core, which may in itself be homogeneous,

but heterogeneous relative to periphery countries.

Despite of convergence criteria that address interest rates, exchange rates and inflation upon

introduction of the single currency individual countries may show other developments than

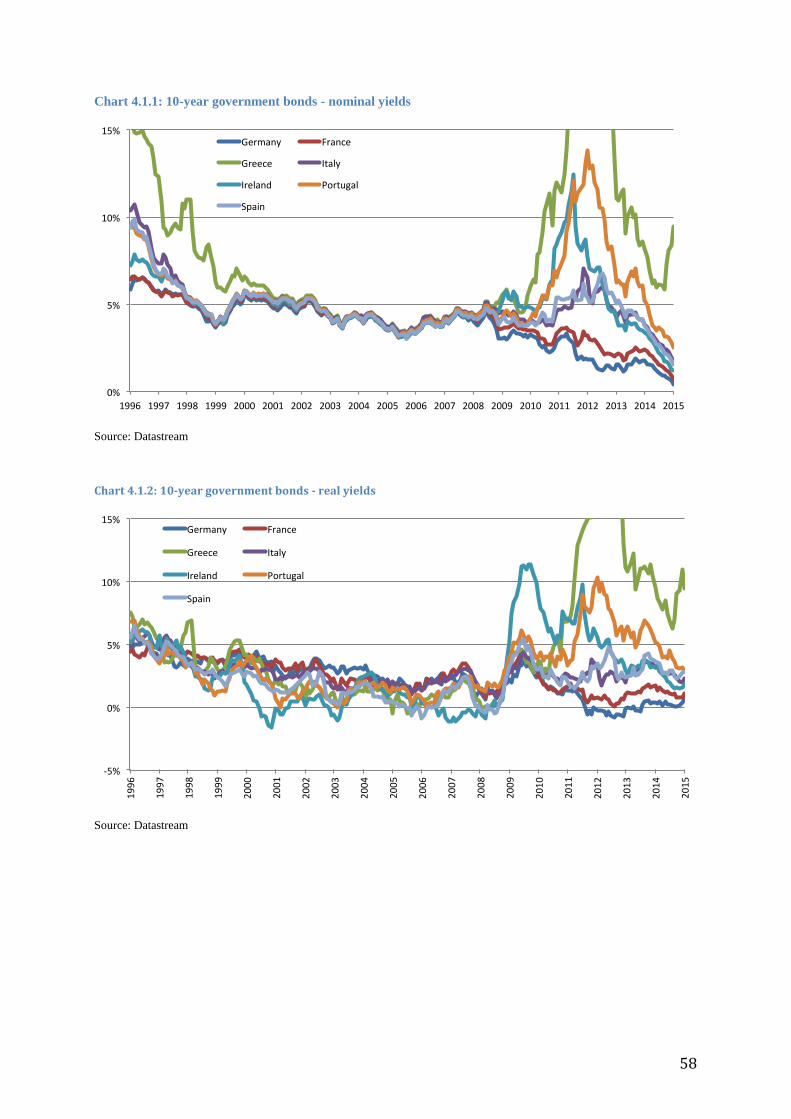

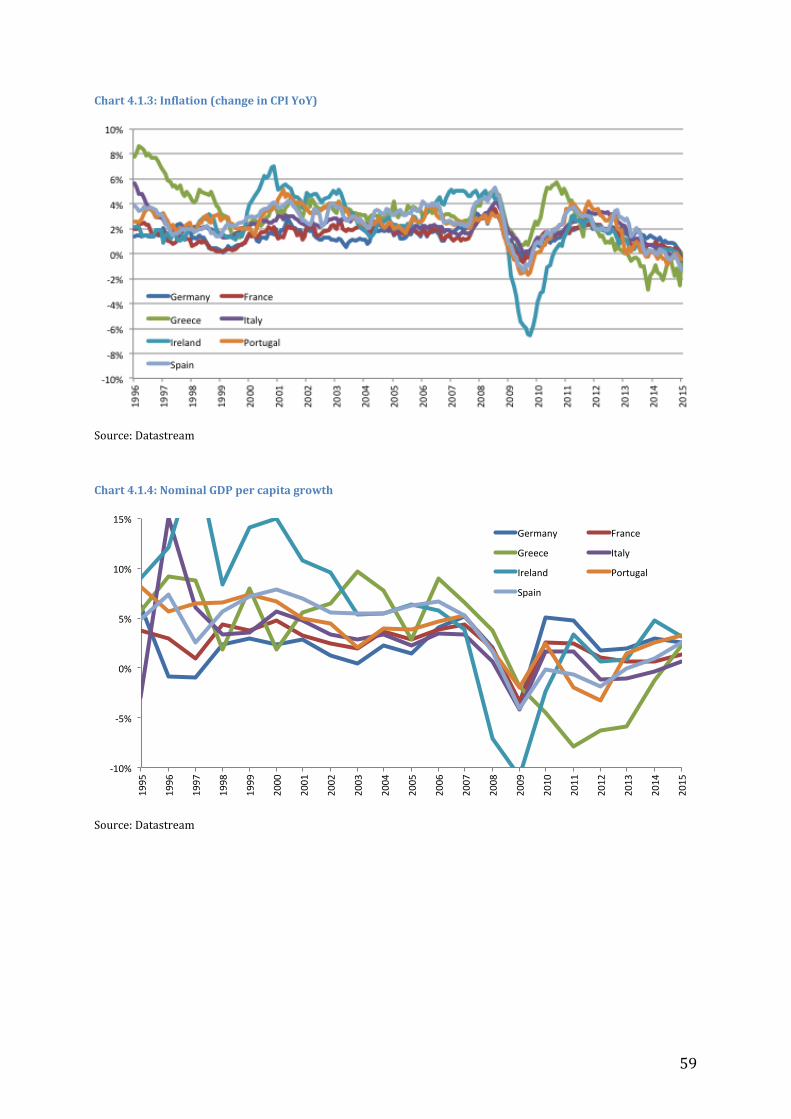

during the observation period. Initially, as Chart 4.1.1 (in Appendix) shows, there has been a

greater convergence. Nominal interest rates converged towards the German one, albeit real

interest rates continued to differ from each other (Chart 4.1.2 in Appendix) as inflation was

not harmonized in all countries (Chart 4.1.3 in Appendix).