1 | THE CATTLE CRUSH AND REVERSE CRUSH WHAT IS THE CATTLE CRUSH? The cattle crush trade seeks to replicate the gross margin of a typical feedlot operation by calculating the spread between input costs and the output sale price. For a typical feedlot, the two primary inputs are feeder cattle and corn while the output is live cattle, which are sent to market once the feeding process ends. The long crush trade combines taking a long position in feeder cattle and corn with corresponding short positions in live cattle. The approximate ratio of corn, feeder cattle and live cattle therefore is as follows: 2 corn and 3 feeder cattle to 6 live cattle. Calculating the number of contracts to purchase in order to even all legs of the trade requires making some assumptions and it is not perfect. After all, we are talking about live animals that differ in terms of weight and speed at which they reach market weights. The cattle crush (and reverse cattle crush), or the cattle feeding spread, is a trade that is more familiar to feedlot risk managers than financial investors. However, going forward we propose that: • The cattle crush will continue to have commercial appeal for feedlot operators • The cattle crush presents a great investment opportunity for investors that are comfortable trading multi contract positions (spreads). In the past, the opportunity that this trade presents as a financial investment has been often overlooked or underappreciated. Livestock and feed markets have become much more volatile in recent years, and this has led to increased use of futures by hedgers and better opportunities for speculators. For hedgers, the trade closely mimics the natural dynamics of the cattle feeding industry and is used to minimize operational risk. For speculators, the trade presents significant variability, both intrinsic and seasonal, to make it an interesting investment opportunity. Furthermore, by spreading positions in feeder cattle and corn against live cattle, lowers the performance bond (margin) required to hold the outright positions. Bottom line: The ‘cattle crush’ trade merits further review given the historical potential of the trade and the margin efficiencies that can be achieved. For those market participants who regularly trade the cattle crush, the recent volatility in livestock and feed markets has made the last three months a particularly interesting period. The value of the spread jumped some 54% in a two- week period in January and then pulled back just as much in the last two weeks (see chart), underscoring the potential for profit in the current volatile market environment. THE CATTLE CRUSH AND REVERSE CRUSH: An Industry Hedging Tool And A Financial Investment Opportunity Cattle Crush: Aug 2014 Live Cattle 6 Aug ‘14 Live Cattle - 3 Apr ‘14 Feeder Cattle - 2 May ‘14 Corn Daily Closing Values for the Past Three Month All three legs of the trade have been impacted by both the short term drivers led by weather and retail demand as well as the long term undercurrent of a shrinking U.S. herd and expanding global demand for beef. Author: Len Steiner

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1 | THE CATTLE CRUSH AND REVERSE CRUSH

WHAT IS THE CATTLE CRUSH?

The cattle crush trade seeks to replicate the gross

margin of a typical feedlot operation by calculating the

spread between input costs and the output sale price.

For a typical feedlot, the two primary inputs are feeder

cattle and corn while the output is live cattle, which are

sent to market once the feeding process ends. The long

crush trade combines taking a long position in feeder

cattle and corn with corresponding short positions in

live cattle. The approximate ratio of corn, feeder cattle

and live cattle therefore is as follows: 2 corn and 3

feeder cattle to 6 live cattle. Calculating the number

of contracts to purchase in order to even all legs of the

trade requires making some assumptions and it is not

perfect. After all, we are talking about live animals that

differ in terms of weight and speed at which they reach

market weights.

The cattle crush (and reverse cattle crush), or the cattle

feeding spread, is a trade that is more familiar to feedlot

risk managers than financial investors. However, going

forward we propose that:

• The cattle crush will continue to have commercial

appeal for feedlot operators

• The cattle crush presents a great investment

opportunity for investors that are comfortable trading

multi contract positions (spreads).

In the past, the opportunity that this trade presents as

a financial investment has been often overlooked or

underappreciated. Livestock and feed markets have

become much more volatile in recent years, and this has

led to increased use of futures by hedgers and better

opportunities for speculators. For hedgers, the trade

closely mimics the natural dynamics of the cattle feeding

industry and is used to minimize operational risk. For

speculators, the trade presents significant variability, both

intrinsic and seasonal, to make it an interesting investment

opportunity. Furthermore, by spreading positions in feeder

cattle and corn against live cattle, lowers the performance

bond (margin) required to hold the outright positions.

Bottom line: The ‘cattle crush’ trade merits further review

given the historical potential of the trade and the margin

efficiencies that can be achieved.

For those market participants who regularly trade the

cattle crush, the recent volatility in livestock and feed

markets has made the last three months a particularly

interesting period. The value of the spread jumped some

54% in a two- week period in January and then pulled

back just as much in the last two weeks (see chart),

underscoring the potential for profit in the current volatile

market environment.

THE CATTLE CRUSH AND REVERSE CRUSH: An Industry Hedging Tool And A Financial Investment Opportunity

Cattle Crush: Aug 2014 Live Cattle 6 Aug ‘14 Live Cattle - 3 Apr ‘14 Feeder Cattle - 2 May ‘14 Corn

Daily Closing Values for the Past Three Month

All three legs of the trade have been impacted by both the

short term drivers led by weather and retail demand as

well as the long term undercurrent of a shrinking U.S. herd

and expanding global demand for beef.

Author: Len Steiner

2 | THE CATTLE CRUSH AND REVERSE CRUSH

The cattle crush spread for August 2014 Live Cattle, which is what we showed on page 1, may be calculated as follows:

Cattle Crush = (6 * Live Cattle) – (3 * Feeder Cattle) – (2 * Corn)

On February 25, the closing prices for the specific contracts were as follows:

August 2014 Live Cattle: $131.68/cwt

April 2014 Feeder Cattle: $172.525/cwt

May 2014 Corn: $4.6125/bu.

This implies the following cattle crush:

Cattle Crush = (6*400*131.68) – (3*500*172.525) – (2 * 5000*4.6125)

Crush = $11,108/trade

or $0.278/cwt of live cattle (40k lb.) or $0.222/cwt of feeder cattle (50k lb.)

The size of the live cattle contract is 40,000 pounds,

which implies a different number of animals depending

on their size. For the sake of simplicity, let’s assume

the average weight of steers by the time they come to

market is about 1,335 pounds (in 2013 the Kansas Feedlot

Performance survey pegged the average live steer weight

at 1,368 pounds while the average heifer weight was 1,228

pounds). This would mean the live cattle contract covers

30 live cattle. The feeder cattle contract size is 50,000

pounds, or 67 head based on an average weight of 750

pounds per feeder cattle. Again, for the sake of simplicity,

the ratio of live cattle to feeder cattle in this spread is

assumed at 2:1 (2 live per 1 feeder). The 67 head of cattle

in the feeder cattle contract will need to be fed a given

supply of corn to bring them to market weight. While

each steer is different, a rough estimate is that to feed

a steer from about 750 pounds to 1335 pounds you will

need about 50 bushels of corn (1 bushel of corn has 56

pounds of corn by definition). And since the size of one

corn contract is 5,000 bushels (or 280,000 pounds), it is

sufficient to cover the feeding of 100 feeder cattle.

Calculating the Cattle Crush: An Example

3 | THE CATTLE CRUSH AND REVERSE CRUSH

IMPLICATIONS OF THE CATTLE CRUSH FOR FINANCIAL INVESTORS

We performed a very limited analysis of the cattle crush for four cattle crush spreads for 2012 and 2013 (see page

3). In all we analyzed eight different spreads. The results of that analysis are graphically shown on page 3. We

started with live cattle that would be traded in February, April, June and August and then selected the feeder cattle

and corn contracts that would best work for the spread trade. The feeder cattle purchased is about 5-6 months

earlier than the live cattle contract while corn will fall somewhere in between. Based on the analysis of these four

spreads for 2012 and 2013, the potential returns varied from a little over $9,000 to almost $18,000. Again, this is for

a spread that involved three legs of 2 long corn, 3 long feeder cattle and 6 short live cattle.

For some investors, the potential return is often viewed in relation to the money required to put the trade on. If

bought separately, the margin requirement on the trades outlined above would be:

Live cattle: $1,013 x 6 contracts = $6,078 ($1,013 is initial margin for 1 live cattle contract)

Feeder cattle: $2,025 x 3 contracts = $6,075 ($2,025 is initial margin for 1 feeder cattle contract)

Corn: $2,363 x 2 contracts = 4,726 ($2,363 is initial margin for 1 live cattle contract)

Outright: $16,879

As a spread: $5,595*

*Because the spread trade requires taking both short and long positions, it is eligible for a spread credit. The exact

credit would have to be recalculated at the time of the trade and varies depending on both the size of the trade and

the months covered. To get some sense as to the margin required for one of the spreads in our analysis, we ran it

through the SPAN system. For a spread of 2 Long Corn (March 2014), 3 Long Feeder Cattle (January 2014) and 6

Short Live Cattle (June 2014), the initial requirement was $5,595.

Furthermore, it is worth noting that the spread involves generally liquid contracts. Both live cattle and corn are very

heavily traded. The volume in the feeder cattle market is less, especially for deferred contracts but overall volume

still makes this a viable spread trade.

4 | THE CATTLE CRUSH AND REVERSE CRUSH

CATTLE CRUSH(2,3,6) DAILY VALUES AND POTENTIAL PROFITS

Cattle Crush: Feb 2012 Live Cattle 6 Feb ‘12 Live Cattle - 3 Sep ‘11 Feeder Cattle - 2 Dec ‘11 Corn

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-

Mar ‘11 Apr ‘11 May ‘11 Jun ‘11 Jul ‘11 Aug ‘11

$16,283

Time Period is 120 Days from Expiration Month of Feeder Cattle Contract

Cattle Crush: Apr 2012 Live Cattle 6 Apr ‘12 Live Cattle - 3 Nov ‘11 Feeder Cattle - 2 Dec ‘11 Corn

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-

May ‘11 Jun ‘11 Jul ‘11 Aug ‘11 Sep ‘11 Oct ‘11

$12,623

Time Period is 120 Days from Expiration Month of Feeder Cattle Contract

Cattle Crush: Jun 2012 Live Cattle 6 Jun ‘12 Live Cattle - 3 Jan ‘12 Feeder Cattle - 2 Mar ‘12 Corn

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-

May ‘11 Jun ‘11 Jul ‘11 Aug ‘11 Sep ‘11 Oct ‘11

$9,118

Time Period is 120 Days from Expiration Month of Feeder Cattle Contract

Cattle Crush: Aug 2012 Live Cattle 6 Aug ‘12 Live Cattle - 3 Apr ‘12 Feeder Cattle - 2 May ‘12 Corn

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-

$(5,000)

$17,953

Oct ‘11 Nov ‘11 Dec ‘11 Jan ‘12 Feb ‘12 Mar ‘12

Time Period is 120 Days from Expiration Month of Feeder Cattle Contract

Cattle Crush: Aug 2013 Live Cattle 6 Aug ‘13 Live Cattle - 3 Apr ‘13 Feeder Cattle - 2 May ‘13 Corn

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-

Oct ‘12 Nov ‘12 Dec ‘12 Jan ‘13 Feb ‘13 Mar ‘13

$11,013

Time Period is 120 Days from Expiration Month of Feeder Cattle Contract

Cattle Crush: Jun 2013 Live Cattle 6 Jun ‘13 Live Cattle - 3 Jan ‘13 Feeder Cattle - 2 Mar ‘13 Corn

May ‘12 Jun ‘12 Jul ‘12 Aug ‘12 Sep ‘12 Oct ‘12

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-

$9,138

Time Period is 120 Days from Expiration Month of Feeder Cattle Contract

Cattle Crush: Apr 2013 Live Cattle 6 Apr ‘13 Live Cattle - 3 Nov ‘12 Feeder Cattle - 2 Dec ‘12 Corn

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-

May ‘12 Jun ‘12 Jul ‘12 Aug ‘12 Sep ‘12 Oct ‘12

$15,123

Time Period is 120 Days from Expiration Month of Feeder Cattle Contract

Cattle Crush: Feb 2013 Live Cattle 6 Feb ‘13 Live Cattle - 3 Sep ‘12 Feeder Cattle - 2 Dec ‘12 Corn

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-

Mar ‘12 Apr ‘12 May ‘12 Jun ‘12 Jul ‘12 Aug ‘12

$12,685

Time Period is 120 Days from Expiration Month of Feeder Cattle Contract

5 | THE CATTLE CRUSH AND REVERSE CRUSH

SEASONALITY

Recognizing the seasonality of the cattle crush would

allow financial investors to focus on those trades that

have the biggest profit potential. Moore Research

Center Inc. (MRCI) provided us with a list of cattle crush

trades. Their analysis simplifies the crush even more by

using a ratio of 1 Corn, 1 Feeder Cattle and 2 Live Cattle

but it serves to illustrate the overall profitability of a

given spread and the window during which a specific

spread is most profitable. For instance, MRCI looked

at the following spread: Long April Feeder Cattle, Long

May Corn and Short 2 August Live Cattle. It identified as

the best entry date March 10 and the best exit date as

April 4. In the last 30 years, executing this spread during

this time period has yielded a profit in 24 of the past 30

years, with an average profit of $1,061.98. (see page 6).

MRCI provides results of a reverse crush trade, as well.

For instance, a trade of Short August Feeder cattle, Short

December Corn and Long 2 December cattle with an

entry date of July 2 and exit date of July 25 provided a

profit in 27 of the last 30 years, with an average profit for

winning trades at $757.35 (see Appendix 1). You can find

more such trades on the MRCI website:

http://www.mrci.com/client/spdpat/catcru/s0005.php

FUNDAMENTALS AND OPPORTUNITIES

The cattle crush trade goes to the heart of the

fundamentals in the cattle feeding business. For a

feedlot risk management manager, the crush spread

provides an opportunity to lock in a margin. Informa

Economics issued their assessment of the cattle

industry and noted that recent positive feedlot margins

were unsustainable and their expectation was for “cattle

feeding margins to slip deep into negative territory once

again as spring turns into summer.” Their argument for

eroding feeding margins in the next few months was

predicated on two major factors: 1) the recent price

spike is a bubble and 2) there is “vast overcapacity” in

the cattle feeding business.

A financial investor may use the cattle crush to either

trade this particular view of the market or bet against it.

And they can do so at a lower cost than simply buying

futures outright. The full analysis from Informa is

attached in Appendix 2. In addition, the CME sponsored

DailyLivestockReport.com provides daily updates of

the fundamentals in the cattle market as well, which a

financial investor could use as a resource to create an

opinion of the economics in the feedlot business.

CONCLUSION

The cattle crush is an interesting option for financial

investors as it provides the opportunity to trade in a

market that is liquid; has significant volatility; benefits

from a notable reduction in margin requirements; and

allows market participants to express their opinion of

both the cattle and grain markets. Weather concerns

have the potential to inject significant volatility in the

grain and feeder cattle markets this spring and summer.

Also, current live cattle prices are trading at all-time

record highs but the fear/speculation is that eventually

the consumer will walk away from beef. Finally, the

global beef market is in turmoil now that China has

emerged as one of the biggest world beef buyers.

Chinese food trade policy is a highly politicized issue and

this has made global beef trade even more volatile than

it normally is. And volatility is likely to be the name of

the game in the cattle market for the foreseeable future.

The information contained herein is believed to be reliable and the views expressed within this document reflect

judgments at this time and are subject to change without notice.

6 | THE CATTLE CRUSH AND REVERSE CRUSH

APPENDIX 1 A Cattle Crush Trading Strategy: Calculations Made by MRCI (Moore Research Center Inc)

Best Best Worst Worst

Cont Entry Entry Exit Exit Profit Equity Equity Equity Equity

Year Date Price Date Price Amount Date Amount Date Amount

2013 3/8/2013 6426 4/5/2013 4935 -1491 3/19/2013 1365 4/4/2013 -1536

2012 3/8/2012 9115 4/5/2012 12494 3378.5 4/4/2012 3758.5 3/29/2012 -235

2011 3/8/2011 7554 4/6/2011 10520 2966 4/6/2011 2966 3/16/2011 -2519

2010 3/8/2010 -930 4/6/2010 -335 595 3/26/2010 942.5 3/16/2010 -727.5

2009 3/9/2009 -2361 4/6/2009 194 2555 3/31/2009 3223.5

2008 3/10/2008 3088 4/4/2008 3384 296.5 3/28/2008 1011.5 3/20/2008 -1222.5

2007 3/8/2007 -1821 4/5/2007 -1596 225 3/16/2007 1461 4/2/2007 -157.5

2006 3/8/2006 -416 4/6/2006 1414 1830 3/31/2006 1911 3/13/2006 -732.5

2005 3/8/2005 -3313 4/6/2005 -1854 1459 4/4/2005 1625 3/28/2005 -215

2004 3/8/2004 -1325 4/6/2004 977 2302.5 4/5/2004 2369

2003 3/10/2003 -3785 4/4/2003 -2865 920 4/4/2003 920 3/13/2003 -336

2002 3/8/2002 -4418 4/5/2002 -3185 1233.5 4/4/2002 1787.5

2001 3/8/2001 -3546 4/6/2001 -3834 -287.5 3/12/2001 152.5 3/16/2001 -844

2000 3/8/2000 -2393 4/6/2000 -2436 -43.5 3/17/2000 739 3/28/2000 -192.5

1999 3/8/1999 -3199 4/6/1999 -3193 6 3/30/1999 507.5 3/15/1999 -56.5

1998 3/9/1998 -2513 4/6/1998 -3895 -1382.5 4/1/1998 -1613.5

1997 3/10/1997 -2168 4/4/1997 -984 1184 4/1/1997 1287.5 3/12/1997 -128.5

1996 3/8/1996 -2115 4/4/1996 -1655 460 4/1/1996 790 3/15/1996 -303.5

1995 3/8/1995 -3540 4/6/1995 -2909 631.5 4/6/1995 631.5 3/24/1995 -268.5

1994 3/8/1994 -3793 4/6/1994 -3783 10 3/29/1994 532.5 4/4/1994 -232.5

1993 3/8/1993 -3601 4/6/1993 -3889 -287.5 4/2/1993 42.5 3/17/1993 -1456.5

1992 3/9/1992 -3204 4/6/1992 -2920 283.5 3/26/1992 677.5 3/16/1992 -124

1991 3/8/1991 -2980 4/5/1991 -1683 1296.5 4/5/1991 1296.5 3/21/1991 -268.5

1990 3/8/1990 -4381 4/6/1990 -3138 1243.5 4/6/1990 1243.5

1989 3/8/1989 -3004 4/6/1989 -2310 693.5 4/4/1989 997.5 3/10/1989 -427.5

1988 3/8/1988 -3764 4/6/1988 -3040 723.5 4/4/1988 1261

1987 3/9/1987 -5594 4/6/1987 -6234 -640 3/26/1987 595 4/3/1987 -745

1986 3/10/1986 -3456 4/4/1986 -2350 1106 4/4/1986 1106 3/27/1986 -1155

1985 3/8/1985 -4401 4/4/1985 -4320 81 3/11/1985 431 3/26/1985 -669

1984 3/8/1984 114 4/6/1984 122 7.5 3/9/1984 188.5 3/27/1984 -902.5

80

1061.98 24

-688.67 6

711.85 30

S E A S O N A L T E N D E N C IE S A R E A C O M P O S IT E O F S O M E O F T H E M O R E C O N S IS T E N T C O M M O D IT Y F UT UR E S S E A S O N A L S T H A T H A VE O C C UR R E D O VE R T H E P A S T 15 Y E A R S . T H E R E A R E US UA L L Y UN D E R L Y IN G F UN D A M E N T A L C IR C UM S T A N C E S T H A T O C C UR A N N UA L L Y T H A T T E N D T O C A US E T H E F UT UR E S M A R K E T S T O R E A C T IN A S IM IL A R

D IR E C T IO N A L M A N N E R D UR IN G A C E R T A IN C A L E N D A R P E R IO D O F T H E Y E A R . E VE N IF A S E A S O N A L T E N D E N C Y O C C UR S IN T H E F UT UR E , IT M A Y N O T R E S UL T IN A P R O F IT A B L E T R A N S A C T IO N A S F E E S , A N D T H E T IM IN G O F T H E E N T R Y A N D L IQUID A T IO N M A Y IM P A C T O N T H E R E S UL T S . N O R E P R E S E N T A T IO N IS B E IN G M A D E T H A T A N Y A C C O UN T H A S IN T H E P A S T O R WIL L IN T H E F UT UR E A C H IE VE P R O F IT S UT IL IZ IN G T H E S E S T R A T E G IE S . N O R E P R E S E N T A T IO N IS B E IN G M A D E T H A T P R IC E P A T T E R N S WIL L

R E C UR IN T H E F UT UR E . H Y P O T H E T IC A L P E R F O R M A N C E R E S UL T S H A VE M A N Y IN H E R E N T L IM IT A T IO N S , S O M E O F WH IC H A R E D E S C R IB E D B E L O W. N O R E P R E S E N T A T IO N IS B E IN G M A D E T H A T A N Y A C C O UN T WIL L O R IS L IK E L Y T O A C H IE VE P R O F IT S O R L O S S E S S IM IL A R T O T H O S E S H O WN . IN F A C T , T H E R E A R E F R E QUE N T L Y S H A R P D IF F E R E N C E S

B E T WE E N H Y P O T H E T IC A L P E R F O R M A N C E R E S UL T S A N D T H E A C T UA L R E S UL T S S UB S E QUE N T L Y A C H IE VE D B Y A N Y P A R T IC UL A R T R A D IN G P R O G R A M . O N E O F T H E L IM IT A T IO N S O F H Y P O T H E T IC A L P E R F O R M A N C E R E S UL T S IS T H A T T H E Y A R E G E N E R A L L Y P R E P A R E D WIT H T H E B E N E F IT O F H IN D S IG H T . IN A D D IT IO N , H Y P O T H E T IC A L

T R A D IN G D O E S N O T IN VO L VE F IN A N C IA L R IS K , A N D N O H Y P O T H E T IC A L T R A D IN G R E C O R D C A N C O M P L E T E L Y A C C O UN T F O R T H E IM P A C T O F F IN A N C IA L R IS K IN A C T UA L T R A D IN G . F O R E X A M P L E , T H E A B IL IT Y T O WIT H S T A N D L O S S E S O R A D H E R E T O A P A R T IC UL A R T R A D IN G P R O G R A M IN S P IT E O F T R A D IN G L O S S E S A R E M A T E R IA L P O IN T S

WH IC H C A N A L S O A D VE R S E L Y A F F E C T A C T UA L T R A D IN G R E S UL T S . T H E R E A R E N UM E R O US O T H E R F A C T O R S R E L A T E D T O T H E M A R K E T S IN G E N E R A L O R T O T H E IM P L E M E N T A T IO N O F A N Y S P E C IF IC T R A D IN G P R O G R A M WH IC H C A N N O T B E F UL L Y A C C O UN T E D F O R IN T H E P R E P A R A T IO N O F H Y P O T H E T IC A L P E R F O R M A N C E R E S UL T S

A N D A L L O F WH IC H C A N A D VE R S E L Y A F F E C T A C T UA L T R A D IN G R E S UL T S . R E S UL T S N O T A D J US T E D F OR C O M M IS S IO N A N D S L IP P A G E .

Average Profit on Winning Trades Winners

Average Loss on Trades Losers

Average Net Profit Per Trade Total trades

Buy Apr Feeder Cattle(CME) / Buy May Corn(CBOT) / Sell 2 Aug Live Cattle(CME)Enter on approximately 03/08 - Exit on approximately 04/06

Percentage Correct

7 | THE CATTLE CRUSH AND REVERSE CRUSH

A Reverse Cattle Crush Trading Strategy: Calculations Made by MRCI (Moore Research Center Inc)

Best Best Worst Worst

Cont Entry Entry Exit Exit Profit Equity Equity Equity Equity

Year Date Price Date Price Amount Date Amount Date Amount

2013 7/2/2013 1347 7/26/2013 2144 797.5 7/26/2013 797.5 7/9/2013 -490

2012 7/2/2012 -5753 7/27/2012 -4422 1330 7/26/2012 1386 7/5/2012 -538.5

2011 7/5/2011 -2110 7/27/2011 -5315 -3205 7/6/2011 360 7/27/2011 -3205

2010 7/2/2010 480 7/27/2010 1296 816 7/20/2010 1000 7/9/2010 -517.5

2009 7/2/2009 3145 7/27/2009 3234 88.5 7/7/2009 387.5 7/9/2009 -835

2008 7/2/2008 -2875 7/25/2008 1031 3906 7/23/2008 4496 7/7/2008 -195

2007 7/2/2007 4000 7/27/2007 4186 186 7/25/2007 572.5 7/13/2007 -1064

2006 7/3/2006 2076 7/27/2006 2724 647.5 7/26/2006 966.5 7/12/2006 -301

2005 7/5/2005 2061 7/27/2005 3234 1172.5 7/25/2005 1612.5 7/7/2005 -536

2004 7/2/2004 2726 7/27/2004 4003 1276.5 7/22/2004 2027.5 7/12/2004 -1187.5

2003 7/2/2003 5634 7/25/2003 5933 300 7/23/2003 402.5 7/9/2003 -418.5

2002 7/2/2002 4251 7/26/2002 4893 642.5 7/11/2002 701.5

2001 7/2/2001 5038 7/27/2001 5224 186 7/20/2001 318.5 7/12/2001 -866.5

2000 7/3/2000 4478 7/27/2000 4893 416 7/10/2000 726

1999 7/2/1999 4226 7/27/1999 4581 355 7/12/1999 546.5 7/23/1999 -166

1998 7/2/1998 5138 7/27/1998 5788 650 7/21/1998 1097.5 7/8/1998 -50

1997 7/2/1997 5364 7/25/1997 5607 244 7/10/1997 617.5 7/15/1997 -537.5

1996 7/2/1996 3246 7/26/1996 4943 1696.5 7/26/1996 1696.5 7/15/1996 -732.5

1995 7/3/1995 4845 7/27/1995 4988 142.5 7/7/1995 212.5 7/12/1995 -402.5

1994 7/5/1994 6199 7/27/1994 6257 59 7/15/1994 325 7/22/1994 -185

1993 7/2/1993 4794 7/27/1993 4780 -13.5 7/13/1993 437.5 7/7/1993 -55

1992 7/2/1992 4015 7/27/1992 4539 523.5 7/23/1992 708.5

1991 7/2/1991 4769 7/26/1991 3916 -852.5 7/5/1991 132.5 7/26/1991 -852.5

1990 7/2/1990 4304 7/27/1990 4635 331.5 7/20/1990 927.5 7/10/1990 -117.5

1989 7/3/1989 3830 7/27/1989 5230 1400 7/25/1989 1530

1988 7/5/1988 2096 7/27/1988 3896 1800 7/27/1988 1800 7/6/1988 -85

1987 7/2/1987 6548 7/27/1987 6625 77.5 7/7/1987 345 7/20/1987 -410

1986 7/2/1986 4749 7/25/1986 5480 731.5 7/22/1986 959 7/9/1986 -228.5

1985 7/2/1985 4499 7/26/1985 4541 42.5 7/9/1985 739

1984 7/2/1984 3373 7/27/1984 4003 630 7/20/1984 1016 7/9/1984 -5

90

757.35 27

-1357 3

545.92 30

S E A S O N A L T E N D E N C IE S A R E A C O M P O S IT E O F S O M E O F T H E M O R E C O N S IS T E N T C O M M O D IT Y F UT UR E S S E A S O N A L S T H A T H A VE O C C UR R E D O VE R T H E P A S T 15 Y E A R S . T H E R E A R E US UA L L Y UN D E R L Y IN G F UN D A M E N T A L C IR C UM S T A N C E S T H A T O C C UR A N N UA L L Y T H A T T E N D T O C A US E T H E F UT UR E S M A R K E T S T O R E A C T IN A S IM IL A R

D IR E C T IO N A L M A N N E R D UR IN G A C E R T A IN C A L E N D A R P E R IO D O F T H E Y E A R . E VE N IF A S E A S O N A L T E N D E N C Y O C C UR S IN T H E F UT UR E , IT M A Y N O T R E S UL T IN A P R O F IT A B L E T R A N S A C T IO N A S F E E S , A N D T H E T IM IN G O F T H E E N T R Y A N D L IQUID A T IO N M A Y IM P A C T O N T H E R E S UL T S . N O R E P R E S E N T A T IO N IS B E IN G M A D E T H A T A N Y A C C O UN T H A S IN T H E P A S T O R WIL L IN T H E F UT UR E A C H IE VE P R O F IT S UT IL IZ IN G T H E S E S T R A T E G IE S . N O R E P R E S E N T A T IO N IS B E IN G M A D E T H A T P R IC E P A T T E R N S WIL L

R E C UR IN T H E F UT UR E . H Y P O T H E T IC A L P E R F O R M A N C E R E S UL T S H A VE M A N Y IN H E R E N T L IM IT A T IO N S , S O M E O F WH IC H A R E D E S C R IB E D B E L O W. N O R E P R E S E N T A T IO N IS B E IN G M A D E T H A T A N Y A C C O UN T WIL L O R IS L IK E L Y T O A C H IE VE P R O F IT S O R L O S S E S S IM IL A R T O T H O S E S H O WN . IN F A C T , T H E R E A R E F R E QUE N T L Y S H A R P D IF F E R E N C E S

B E T WE E N H Y P O T H E T IC A L P E R F O R M A N C E R E S UL T S A N D T H E A C T UA L R E S UL T S S UB S E QUE N T L Y A C H IE VE D B Y A N Y P A R T IC UL A R T R A D IN G P R O G R A M . O N E O F T H E L IM IT A T IO N S O F H Y P O T H E T IC A L P E R F O R M A N C E R E S UL T S IS T H A T T H E Y A R E G E N E R A L L Y P R E P A R E D WIT H T H E B E N E F IT O F H IN D S IG H T . IN A D D IT IO N , H Y P O T H E T IC A L

T R A D IN G D O E S N O T IN VO L VE F IN A N C IA L R IS K , A N D N O H Y P O T H E T IC A L T R A D IN G R E C O R D C A N C O M P L E T E L Y A C C O UN T F O R T H E IM P A C T O F F IN A N C IA L R IS K IN A C T UA L T R A D IN G . F O R E X A M P L E , T H E A B IL IT Y T O WIT H S T A N D L O S S E S O R A D H E R E T O A P A R T IC UL A R T R A D IN G P R O G R A M IN S P IT E O F T R A D IN G L O S S E S A R E M A T E R IA L P O IN T S

WH IC H C A N A L S O A D VE R S E L Y A F F E C T A C T UA L T R A D IN G R E S UL T S . T H E R E A R E N UM E R O US O T H E R F A C T O R S R E L A T E D T O T H E M A R K E T S IN G E N E R A L O R T O T H E IM P L E M E N T A T IO N O F A N Y S P E C IF IC T R A D IN G P R O G R A M WH IC H C A N N O T B E F UL L Y A C C O UN T E D F O R IN T H E P R E P A R A T IO N O F H Y P O T H E T IC A L P E R F O R M A N C E R E S UL T S

A N D A L L O F WH IC H C A N A D VE R S E L Y A F F E C T A C T UA L T R A D IN G R E S UL T S . R E S UL T S N O T A D J US T E D F OR C O M M IS S IO N A N D S L IP P A G E .

Average Profit on Winning Trades Winners

Average Loss on Trades Losers

Average Net Profit Per Trade Total trades

Buy 2 Feb Live Cattle(CME) / Sell Sep Feeder Cattle(CME) / Sell Dec Corn(CBOT)Enter on approximately 07/02 - Exit on approximately 07/27

Percentage Correct

8 | THE CATTLE CRUSH AND REVERSE CRUSH

APPENDIX 2

CURRENT CATTLE & BEEF MARKETFUNDAMENTALS

The perfect storm developed in the cattle and beef markets during late December and January. An air pocket in supply that

most market participants failed to see coming began to develop shortly after New Year’s Day. Holiday-shortened kill schedules

combined with some nasty winter weather to greatly restrict the availability of beef in the wholesale market. At the same time,

beef buyers who were anticipating the normal seasonal lull in pricing after the holidays had drawn inventories down, expecting

to buy product cheaper after the first of the year. The final piece of the puzzle belonged to consumers who hit retail stores

aggressively to stock up in advance of approaching winter weather. The result was a strong demand surge that coincided with

very short supply and sent both cattle and beef prices to all-time record highs.

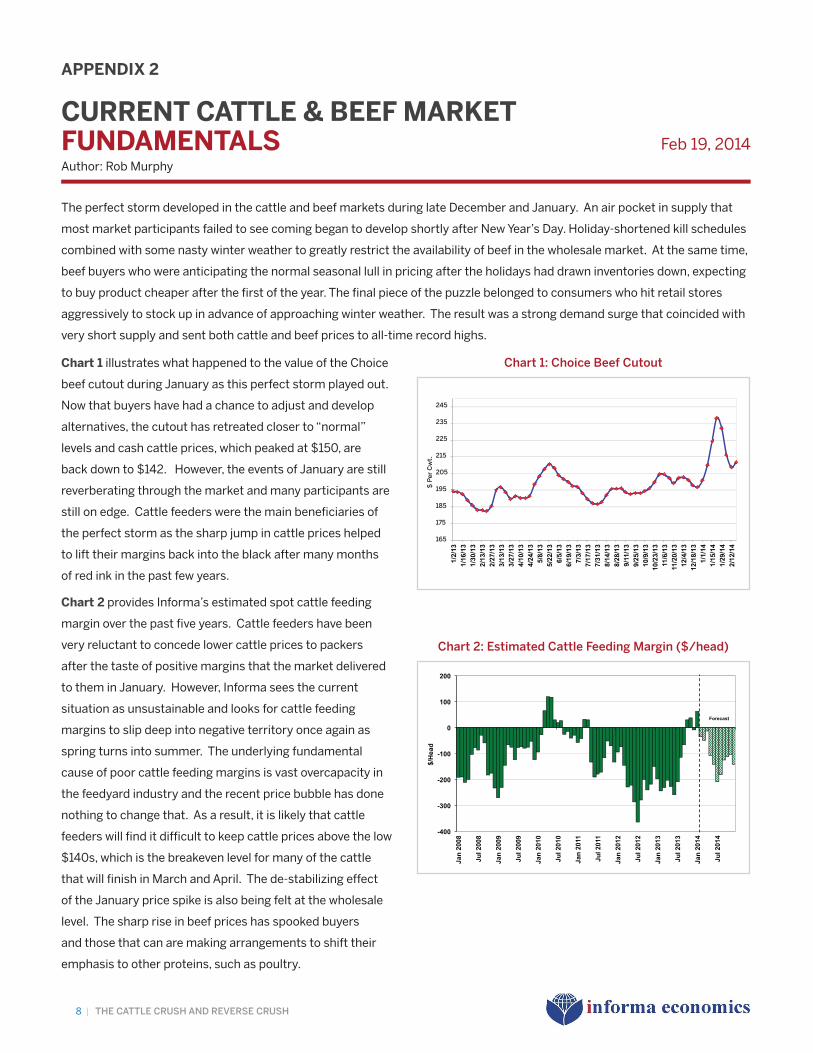

Chart 1 illustrates what happened to the value of the Choice

beef cutout during January as this perfect storm played out.

Now that buyers have had a chance to adjust and develop

alternatives, the cutout has retreated closer to “normal”

levels and cash cattle prices, which peaked at $150, are

back down to $142. However, the events of January are still

reverberating through the market and many participants are

still on edge. Cattle feeders were the main beneficiaries of

the perfect storm as the sharp jump in cattle prices helped

to lift their margins back into the black after many months

of red ink in the past few years.

Chart 2 provides Informa’s estimated spot cattle feeding

margin over the past five years. Cattle feeders have been

very reluctant to concede lower cattle prices to packers

after the taste of positive margins that the market delivered

to them in January. However, Informa sees the current

situation as unsustainable and looks for cattle feeding

margins to slip deep into negative territory once again as

spring turns into summer. The underlying fundamental

cause of poor cattle feeding margins is vast overcapacity in

the feedyard industry and the recent price bubble has done

nothing to change that. As a result, it is likely that cattle

feeders will find it difficult to keep cattle prices above the low

$140s, which is the breakeven level for many of the cattle

that will finish in March and April. The de-stabilizing effect

of the January price spike is also being felt at the wholesale

level. The sharp rise in beef prices has spooked buyers

and those that can are making arrangements to shift their

emphasis to other proteins, such as poultry.

Feb 19, 2014

Chart 1: Choice Beef Cutout

1/2/

13

1/16

/13

1/30

/13

2/13

/13

2/27

/13

3/13

/13

3/27

/13

4/10

/13

4/24

/13

5/8/

13

5/22

/13

6/5/

13

6/19

/13

7/3/

13

7/17

/13

7/31

/13

8/14

/13

8/28

/13

9/11

/13

9/25

/13

10/9

/13

10/2

3/13

11

/6/1

3 11

/20/

13

12/4

/13

12/1

8/13

1/

1/14

1/

15/1

4 1/

29/1

4 2/

12/1

4

245

235

225

215

205

195

185

175

165

1/2/131/16/131/30/132/13/132/27/133/13/133/27/134/10/134/24/135/8/135/22/136/5/136/19/137/3/137/17/137/31/138/14/138/28/139/11/139/25/1310/9/1310/23/1311/6/1311/20/1312/4/1312/18/131/1/141/15/141/29/142/12/14

Chart 2: Estimated Cattle Feeding Margin ($/head)

-400

-300

-200

-100

0

100

200

Jan

2008

Jul 2

008

Jan

2009

Jul 2

009

Jan

2010

Jul 2

010

Jan

2011

Jul 2

011

Jan

2012

Jul 2

012

Jan

2013

Jul 2

013

Jan

2014

Jul 2

014

$/H

ead

Forecast

Author: Rob Murphy

9 | THE CATTLE CRUSH AND REVERSE CRUSH

Chart 3 gives Informa’s estimate of average net packer

margins since last summer. Those margins have been

negative since Labor Day, except for the brief spike that

packers enjoyed in January when beef prices escalated

faster than the cattle market. That has since faded and

packers find themselves facing significant financial pain

once again. Packers face their own overcapacity issues

and will continue to struggle financially until more plants

shut down. The recent announcement that National Beef

will stop slaughtering at its Brawley, California plant in early

April may help to a small degree, but Informa believes that

at least one, and possibly two, more large slaughter plants

need to shutter before packer margins can consistently

move into positive territory.

Chart 4 shows that kills have been well below last year

since late summer and the Informa forecast is for more

of the same over the next couple of months. It will take

a while for all aspects of the market to return to some

semblance of equilibrium following the January shock, but

the general tone of the market should be one of struggle:

feeders struggling to keep their head above water, packers

struggling to right their ship, and retailers and consumers

struggling with high beef prices. While Informa’s forecast

looks for some slight softening of cattle prices in the next

few weeks, the weather remains a wild card and could easily

goose the market higher with little notice. That said, the

longer-term picture is quite bullish, driven by shrinking cattle

supplies in the face of an improving domestic economy.

In the interim, look for packers to keep pulling back on the throttle with respect to kills and they will likely maintain this

strategy as long as it takes to raise beef prices and/or lower cattle prices. Last week’s estimated slaughter of 539,000 head

was the smallest non-holiday kill week in modern times.

It is also very likely that the rally in wholesale beef prices will result in retail stores raising prices to consumers and that

will have a dampening effect on consumption. In the short-run, cattle prices may be buoyed by continued harsh weather,

but within a few weeks that will be behind us and prices could drift lower. Packers certainly have an incentive to keep the

pressure on cattle prices.

Chart 3: Estimated Net Packer Margin

-80

-60

-40

-20

0

20

40

60

80

7/3/

13

7/17

/13

7/31

/13

8/14

/13

8/28

/13

9/11

/13

9/25

/13

10/9

/13

10/2

3/13

11/6

/13

11/2

0/13

12/4

/13

12/1

8/13

1/1/

14

1/15

/14

1/29

/14

2/12

/14

$ Pe

r Hea

d

Chart 4: Weekly Cattle Slaughter, YOY Comparison

(85)

(65)

(45)

(25)

(5)

15

35

55

75

95

430

480

530

580

630

680

02/1

3/13

02/2

7/13

03/1

3/13

03/2

7/13

04/1

0/13

04/2

4/13

05/0

8/13

05/2

2/13

06/0

5/13

06/1

9/13

07/0

3/13

07/1

7/13

07/3

1/13

08/1

4/13

08/2

8/13

09/1

1/13

09/2

5/13

10/0

9/13

10/2

3/13

11/0

6/13

11/2

0/13

12/0

4/13

12/1

8/13

01/0

1/14

01/1

5/14

01/2

9/14

02/1

2/14

02/2

6/14

03/1

2/14

03/2

6/14

Diff

eren

ce (T

hou

Hd)

Thou

sand

Hea

d

Date

Current Yr Minus Last Yr Current Yr Last Yr Forecast

This copyrighted material is intended for the use of clients of Informa Economics only and may not be reproduced or electronically transmitted to other companies

or individuals, whole or in part, without the prior written permission of Informa Economics. The information contained herein is believed to be reliable and the views

expressed within this document reflect judgments at this time and are subject to change without notice. Informa Economics does not guarantee that the information

contained herein is accurate or complete and it should not be relied upon as such.

Related Documents