The Cartagena Declaration, The Baker Plan, and U.S. Bank Security Returns: An Empirical Investigation William H. Sackley and M. Kabir Hassan ABSTRACT This paper examines the impact of the Cartagena Declaration by 11 Latin American countries and the Baker Plan for resolving the LDC debt problem on the security returns of major U.S. banks. An event parameter approach is employed to investigate two hypotheses, the new-information and the rational-pricing hypotheses, using daily stock market data. Sample banks are grouped into three portfolios depending on their LDC exposure. The results indicate that bank stock returns adjust quickly to new information. Also, there is rational investor reaction to observed events that were neither borrower-nor lender-induced. Those banks displaying greater exposure to LDC loans were affected in a direct and proportionately greater manner. Introduction This research empirically investigates the effects of two events related to the Latin American debt crisis on the stock returns of major U.S. banks. The first event occurred on June 24, 1984, when 11 Latin American countries issued a joint declaration regarding their large external debt at Cartagena, Bolivia. The second event occurred on October 7, 1985, when U.S. Treasury Secretary James Baker proposed a plan for dealing with the LDC debt problem in Seoul, Korea. Previous studies have examined the reactions of bank security returns to events which were either borrower induced (debt moratoria), lender induced (loan-loss provisions) or both borrower and lender induced (debt reschedulings), and in which either the borrower, the lender, or both parties made wealth maximizing decisions concerning their debt problems. However, in the two events examined in this study neither the borrower nor the lender were involved directly in the resolution of the impending William H. Sackley is Assistant Professor of Finance, University of Southern Mississippi, Hattiesburg, MS 39406.. M. Kabir Hassan is Assistant Professor of Finance, University of New Orleans, New Orleans, [.,4 70148. 51

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Cartagena Declaration, The Baker Plan, and U.S. Bank Security Returns: An Empirical Investigation

William H. Sackley and M. Kabir Hassan

ABSTRACT

This paper examines the impact of the Cartagena Declaration by 11 Latin American countries and the Baker Plan for resolving the LDC debt problem on the security returns of major U.S. banks. An event parameter approach is employed to investigate two hypotheses, the new-information and the rational-pricing hypotheses, using daily stock market data. Sample banks are grouped into three portfolios depending on their LDC exposure. The results indicate that bank stock returns adjust quickly to new information. Also, there is rational investor reaction to observed events that were neither borrower-nor lender-induced. Those banks displaying greater exposure to LDC loans were affected in a direct and proportionately greater manner.

Introduction

This research empirically investigates the effects of two events related to the Latin American debt crisis on the stock returns of major U.S. banks. The first event occurred on June 24, 1984, when 11 Latin American countries issued a joint declaration regarding their large external debt at Cartagena, Bolivia. The second event occurred on October 7, 1985, when U.S. Treasury Secretary James Baker proposed a plan for dealing with the LDC debt problem in Seoul, Korea. Previous studies have examined the reactions of bank security returns to events which were either borrower induced (debt moratoria), lender induced (loan-loss provisions) or both borrower and lender induced (debt reschedulings), and in which either the borrower, the lender, or both parties made wealth maximizing decisions concerning their debt problems. However, in the two events examined in this study neither the borrower nor the lender were involved directly in the resolution of the impending

William H. Sackley is Assistant Professor of Finance, University of Southern Mississippi, Hattiesburg, MS 39406.. M. Kabir Hassan is Assistant Professor of Finance, University of New Orleans, New Orleans, [.,4 70148.

51

JOURNAL OF ECONOMICS AND FINANCE

debt crisis. The examination of these two new and unexplored events sheds more light on the Latin American debt crisis and U.S. bank security returns.

This study employs an event parameter approach to investigate two hypotheses which are similar to those of Bruner and Simms (1987). The new-information hypothesis holds that bank security returns anticipate significant and rapid responses to an event. The rational-pricing hypothesis holds that investors can discriminate among banks with and without Latin debt exposure.

This paper differs from other studies on the international debt crisis and bank stock returns in two important ways. First, we follow Aharony and Swary (1983) by classifying three groups of banks--multinational money-center banks, regional wholesale banks and regional consumer banks. Multinational banks are heavily exposed to Less Developed Countries' (LDC) debt, the regional banks are mildly exposed to LDC debt and the regional consumer banks are typically unexposed or nominally exposed to LDC debt. Second, this paper examines the effects of additional event announcements related to the Latin American debt crisis which, to our knowledge, have not been investigated before in the empirical literature. The two hypotheses can be tested by examining these portfolio returns around the event announcement dates.

This paper is organized as follows: Section II analyzes the motivation of the research and the two event dates. An historical survey of literature is provided in Section III. The data and methodology are discussed in Section IV. The empirical results and their implications are analyzed in Section V. Section VI contains the summary and conclusions.

Motivation and Analysis of Events

Motivation of Research

The 1980s represented the decade of the international debt crisis which was triggered by the Mexican debt moratorium on August 19, 1982. Since then, several Latin American countries have participated in debt-reschedulings with their creditor banks. Initially, LDC loans were profitable, but beginning in the early 1980s, problems emerged as countries fell behind on interest payments. In the early stages of the debt crisis, banks were discouraged by governments from taking remedial action on problem LDC loans. Rather, they were encouraged to "roll over loans" so the debtor countries could remain current on payments. However, in 1987 remedial actions were taken when Brazilian problem loans were placed on non-accrual status. Additions to loan-loss reserves, sales of LDC loans and debt-equity swaps were initiated by banks to reduce their LDC debt exposure.

Before 1983, the Securities and Exchange Commission (SEC) did not require banks to reveal the composition of their international loan portfolios. Investors knew only through the financial press that large banks were making loans to LDCs, but they did not know individual banks' loan exposure by country. Therefore, information structures surrounding events before 1983 are likely to be different from post- 1983 events. In post- 1983, due to the existence of disclosure, secondary markets

52

The Cartagena Declaration, The Baker Plan, and U.S. Bank Securit~ Returns

for LDC loans, debt rescheduling and improvement in information technology, markets are likely to be more efficient and adjust prices more rapidly and reliably. The existence of some private information before 1983 causes the capital market tests of such events to be tests of strong-form efficiency. Greater LDC disclosure causes capital market tests of post-1983 events to be tests of semi-strong form efficiency. This research tests two post-1983 events, and therefore the tests of these two events are of semi-strong market efficiency.

The international debt problem remains a serious concern of U.S. banks. With the advent of a new world order, the U.S. multinational banks are likely to play major roles in the development of Eastern Europe and the Commonwealth of Soviet States. This is likely to initiate intense competition among multinational banks in the world financial market. Moreover, the Basle Accord of 1988 among twelve industrialized nations is expected to have a major impact on many international banks--obliging them to choose between raising additional capital or lowering the risk profile of their asset portfolios.

The international capital adequacy standards resulting from the Basle Agreement have the potential to impact significantly the financial structure, lending policy, and the competitive capacity of banks in industrialized nations. Therefore, the market assessment of bank stock returns is expected to be one major factor in changing international financial markets. Undercapitalized banks under the Basle Accord may lose market share to well-capitalized banks.

An examination of market reactions of bank stock returns related to a series of international debt events will help facilitate assessment of capital adequacy and competitiveness in the international credit markets. In addition, the events that we study are exogenous to the lender-borrower relationship, and, as such, are not as common in banking event studies. They provide the ideal test for the effect of contagion: when the bank stock returns respond to common but exogenous events like the Cartagena Declaration and the Baker Plan without regard for the extent of individual bank's exposure levels.

Since contagion effects have been found in some banking studies (for example, Karafiath, Mynatt and Smith 1991), it is important to compare these results to previous studies, and discern any differences. Consequently, additional evidence against contagion effects may lead to an important public policy implication. Such implication is that it is not necessary to protect underexposed or non-exposed banks, whether large or small. Absence of contagion effects, therefore, suggests that the market can distinguish among the exposure levels of different banks and the response is proportional to exposure.

Analysis of Events

The two events related to the Latin American Debt Crisis (Latin American Cartagena Declaration and Baker Plan) are exogenous to the borrower-lender relationship. The events relate to the decisions which are not directly undertaken by both borrowers and lenders. These are external to the banking system, and are likely to influence bank security returns indirectly. A brief description of these two events

53

JOURNAL OF ECONOMICS AND FINANCE

and their dates are explained below. The event announcement dates are taken from The Wall Street Journal.

Cartagena Declaration

The Cartagena Declaration by 11 Latin debtor countries on June 21, 1984, stated that (a) debt servicing should not exceed a particular percentage of export revenues, and, (b) debt reschedulings should include preferential interest rates and longer maturity. This declaration was the first joint document that clearly indicated the promise of these countries to fulfill their debt obligations. However, the calls for reduction in interest rates and preferential terms in rescheduling may increase investor uncertainty about the LDC loan portfolio. The effect of this event on bank security returns is determined by the interaction of positive and negative effects; therefore, the impact of this event on bank stock returns is uncertain.

Baker Plan

On October 7, 1985, the U.S. Secretary of the Treasury proposed a tripartite strategy for dealing with the debt problem, calling for structural adjustment by debtor countries, additional lending by banks, and financial support from international agencies and industrialized countries. The importance of this event lies in its timeliness. The U.S. proposal came at a period when political and financial strains were intensifying in Latin America. The Cartagena group of Latin American countries was drafting a unified approach to tackle the debt problem. The Peruvian President, Alan Garcia, declared in July 1985 that his country would limit debt payments to 10 percent of export earnings. The Mexican President forecasted in September 1985 that the debt crisis would be heightened unless a new formula was found to deal with Latin American debtors. This event may exert a positive effect on bank stock returns because it signifies a positive step from the U.S. Government to address the LDC debt problem.

Review of Literature

The literature contains several papers on different dimensions of the LDC debt crisis. Mexico's Debt Moratorium in August 1982 generated five event studies. Schoder and VanKudre (1986) examined the announcement and found the effects to be negative but insignificant. Their results are consistent with an information-leakage hypothesis which implies there would not be significant announcement effects. Cornell and Shapiro (1986) tested monthly, annual, and biannual returns around the announcement and found that Latin American debt exposure is a significant determinant in annual and biannual bank returns but not for shorter periods. They postulated a "dribs and drabs" hypothesis whereby negative information was slowly released throughout 1982 and 1983. Therefore, they argued that event study methods would understate the effects of Latin American exposure on the relative pricing of bank equities.

54

The Cartagena Declaration, 77ze Baker Plan, and U.S. Bank Security Returns

Bruner and Simms (1987) and also Smirlock and Kaufold (1987) tested daily returns around the announcement and found a significant negative market reaction to Mexican debt default. Kyle and Wirick (1990) used pooled data and a generalized least squares method to find a delayed reaction to the Mexican announcement.

The Brazilian Debt Moratorium announcement on February 20, 1987, generated three event study papers. Mansur, Cochran and Cahill (1988-1989) examined the announcement and found significant negative effects, which supports the new- information hypothesis. Musumeci and Sinkey (1990b) tested for announcement effects and found significant negative returns for money-center banks. They found no evidence of investor-contagion because the relationship between exposure and returns was significantly negative. They also found no relationship between returns and non-Brazilian debt exposure, and that abnormal returns were positively related to capital adequacy.

Karafiath, Mynatt and Smith (1991) employed both traditional event study methodology and a generalized least squares regression, using Brazilian exposure as an explanatory variable for abnormal returns to examine the effects of the Brazilian default announcement. They found a significant negative abnormal return for high- exposure banks on the event date. However, the stock market reactions for low- and no-exposure were insignificant, which implies that not all relative information was contained in the disclosure announcement. In addition, they found evidence of a contagion effect related to size--abnormal returns and size of banks were negatively correlated. Mansur, Cochran and Seagers (1990) studied the effects of Argentinean debt rescheduling using an event study approach. They found significant negative abnormal returns around the announcement date.

The May 1987 Citicorp announcement of addition to loan-loss reserves generated three studies. Madura and McDaniel (1989) found a significant positive return for money-center banks and argued that the market recognized an improvement in operating cash-flows. In addition, the announcement could convey to the market that banks would write off problem loans sooner than formerly anticipated by investors. When write-offs occur, the banks would stop paying taxes on accounting profits that are unlikely to be realized as economic profits. Moreover, the banks would recover excess taxes previously paid because of the overstatement of profit for tax purposes. These two anticipated tax reductions would improve the present value of the operational cash-flow stream and increase stock prices.

Musumeci and Sinkey (1990a) found no significant positive returns for either money-center or regional bank stock portfolios on the announcement date but found a significant positive return on the day following the announcement date for money- center banks. Grammatikos and Saunders (1990) found a heterogeneous effect on the announcement day. They found two significant variables in explaining cross-sectional regressions to be the position of the bank on the LDC rescheduling committee and the size of the bank's LDC exposure. Wetmore and Brick (1991) examined the addition to loan-loss reserves by Bank of Boston in December of 1987. They found that a portfolio of low-exposure banks experiences a significant positive abnormal return while a portfolio of high-exposure banks experiences a significant negative abnormal return. During their study period, most of the mildly exposed banks

55

JOURNAL OF ECONOMICS AND FINANCE

reduced their LDC loan portfolio, leaving the LDC exposure to a small group of highly exposed banks with little capital to reduce their LDC exposure.

Madura, White and McDaniel (1991) found that Citicorp's announcement of a $3 billion increase in loan-loss reserve adversely affected British Bank share prices. Musumeci and Sinkey (1990a) detected a favorable reaction of U.S. money-center banks to this announcement. They attributed the opposite reactions to differences in tax and accounting provisions imposed by these two countries. The ability to reap tax benefits from boosting loan-loss reserves is more constrained for British banks than U.S. banks because of strict limitations on charge-offs of LDC loans by British banks. They argue that the strategy of a bank in one country may not only influence other banks in that country, but foreign banks as well.

The empirical results of this research support both the new-information and rational-pricing hypothesis. That is, the bank security returns react to events rapidly, and the returns of the highly exposed bank portfolio are more affected than those of unexposed and moderately-exposed bank portfolios.

Data and Methodology

Data

We examine the effects of events related to Latin American debt crisis on bank stock prices using an event parameter approach as described by Binder (1985). All banks in the sample are first categorized as either multinational, regional wholesale or regional consumer by relying on the classification followed by Solomon Brothers. The multinational banks are highly exposed, the regional wholesale banks are moderately exposed and the regional consumer banks are unexposed or nominally exposed to Latin American debt. These banks are listed either on the New York Stock Exchange, American Stock Exchange or Over-the-Counter exchange.

This three way classification of sample banks has the advantage of observing differences among the three groups. Sinkey and Greenwalt (1991) provide evidence that loan-loss experience and risk taking behavior between money center banks and regional banks are different. In addition, Schoder and VanKudre (1986) argue that this classification is superior to exposure level information to explain the stock price response of exposed banks. Our sample size is comparable to those used in previous studies in which sample size varies from 20 to 24 banks.

Table 1 presents the list of sample banks, their classifications, and percentage of foreign loans in each portfolio, l It can be seen from Table 1 that the average foreign debt-exposure of multinational banks is about 33 percent of their total loans in December 1988. In contrast, this exposure ratio is about 4 percent for regional wholesale and about 2 percent for regional consumer banks. Data on event announcement dates were collected from The Wall Street Journal. The data on stock returns were compiled from the Center for Research in Security Prices (CRSP) data tapes.

56

The Cartagena Declaration, The Baker Plan, and U.S. Bank Security Returns

TABLE 1

PORTFOLIO COMPOSITION OF SAMPLE BANKS, AND FOREIGN LOAN EXPOSURE AS A PERCENT OF TOTAL LOANS

December 31~ 1986

MULTINATIONAL CLASSIFICATION 3 I. 16 %

December 31 r 1988

32.75 %

1. Bank of Boston 17.00 30.00 2. Bank of New York 13.00 22.00 3. Bank of America 28.00 27.00 4. Bankers Trust NY 36.00 42.00 5. Chase Manhattan 46.00 36.00 6. Chemical NY 30.40 23.30 7. Citicorp * 35.00 8. First Chicago 23.00 17.00 9. Manufacturers Hanover 32.00 35.00 10. J.P. Morgan & Co. 55.00 58.00 11. Republic NY ** 35.00

REGIONAL WHOLESALE CLASSIFICATION 7.16 % 3.58 %

1. First Fidelity Banking Corp. 2.00 1.90 2. NBD Bancorp 10.00 8.00 3. Norwest Corp. 5.00 1.00 4. Ameritrust 2.80 1.00 5. Northern Trust Inc. 16.00 6.00

REGIONAL CONSUMER CLASSIFICATION 3. i 1% 1.43 %

1. Barnett Banks 0.10 *** 2. First Interstate 8.00 4.00 3. Signet Banking Corp. 5.00 3.00 4. Wells Fargo & Co. 5.60 1.60 5. Baybanks 0.00 0.00 6. US Bancorp 0.00 0.00

Notes: * = Proportion unavailable but presumably high; 46% of consolidated income derived from foreign loans. ** = Proportion unavailable but assumably high; institution stated to have "primary emphasis" on international banking. *** = LDC exposure explicitly stated as zero percent of total loan portfolio.

Event Parameter Approach

In traditional event study methodology, abnormal returns are calculated as the errors from a market model during the event period and the errors are then cross- sectionally averaged in event time. The hypothesis that the average abnormal return equals zero is tested, using a cross-sectional estimate o f the standard deviation o f the error terms. The fact that the traditional event study method assumes that the errors are independent and identically distributed is questionable for three reasons. First, the abnormal returns (expectations of the error terms) are likely to differ across firms. Second, Fama (1976) shows that error variance differs across firms. Finally,

57

JOURNAL OF ECONOMICS AND FINANCE

the error terms will not be independent if the event occurs during the same calendar time for a group of firms in the same industry.

Binder (1985) discusses a multivariate regression model that parameterizes the abnormal return from a specific event. We adopt a variant of this model and call this an "event parameter" approach. The event parameter approach explicitly predicts the stochastic return generating process on the occurrence or non-occurrence of specific events. This conditioning is accomplished by including dummy variables in the market model equation. The dummy variables assume values of one on the dates of event occurrence and zero otherwise. The coefficients on the dummy variables measure the effect(s) of the events on stock returns. This effect or effects may represent an abnormal return with regard to the estimated parameters (slope and intercept). Alternately, it may represent a structural change: that is, a shift in the slope, the intercept, or both. However, we refer to significant coefficients on dummy variables as abnormal returns without distinguishing between constant or shifting parameters. This approach allows the individual abnormal returns to differ across firms. This multivariate regression model assumes that the error terms are independent and identically distributed within each equation, but contemporaneous covariances of the error terms across equations are nonzero.

In the event parameter approach, abnormal returns are obtained by adding a vector of (0,1) dummy variables to the fight hand side of the traditional market model. Arbitrarily defining an event date as day 0, the model is estimated over a 147-day interval from day -143 to day +3. Each day, s, in the event period (day -3 to day +3) is assigned a dummy variable D s that is equal to 1 on day s only and is zero elsewhere. The estimated regression coefficient on each dummy D s is equal to the difference between the actual and estimated values of the security return on day s. Since the entire event window is 'dummied out, ' the observations in the estimation period do not influence the estimates of the intercept and slope (beta). Only those observations without dummies (day -143 to day +3 except the event window) determine the values of the intercept and slope.

Using the event parameter approach, the following equation is estimated for each portfolio j:

where:

$= +3

1~j$ = ~j + ~jRmlt + E "~jsDst + e'jt' t = - -143 t o +3 $= -3

(1)

g j t

Ds t

average return on portfolio j , day t, OLS estimate of the intercept, OLS estimate of the slope coefficient, return to equal weighted market index on day t, (CRSP EWRETD), OLS estimate of the coefficient on the dummy variable Dst , or abnormal return (AR) for portfolio j on day s, dummy variable that is set equal to 1 on days in the event window and is zero elsewhere,

58

The Cartagena Declaration, The Baker Plan, and U.S. Bank Security Returns

ejt = residual for portfolio j on date t. (With dummy variable technique, the residual is by definition zero for any event window between t = - 3 t o t = + 3 . )

The abnormal returns, ARs, for each portfolio j are then accumulated through time to form cumulative abnormal returns, CARs, from day M to N,

S=N - -

s = M

A t-test is applied to each AR t and CARr~ to test for their significance. The t-tests of the hypotheses that the ARS and CARMn equal zero are equivalent to F-tests that the average abnormal returns during an announcement period equal zero.

Results and Implications

This section reports both daily average abnormal portfolio returns for seven days (-3 to +3) and cumulative average abnormal portfolio returns for three event windows (-1 to + 1, -2 to +2, -3 to +3) for each event announcement day related to the Latin American Debt crisis. In addition, this section will analyze the implications of these findings and their relevance to the two previously stated hypotheses.

Latin American Cartagena Declaration

The stock market event study results reported in Table 2 concerning the Cartagena Declaration suggest that market participants had already anticipated the likely effects of the Cartagena Declaration in response to news and events in the preceding months. None of the three portfolios show any significant ARs or CARs in any of the event windows, except the multinational group, which shows significant negative ARs at the 1% level on day + 1. However, this effect evaporates rapidly. These results are, therefore, consistent with the information-leakage hypothesis.

Baker Plan

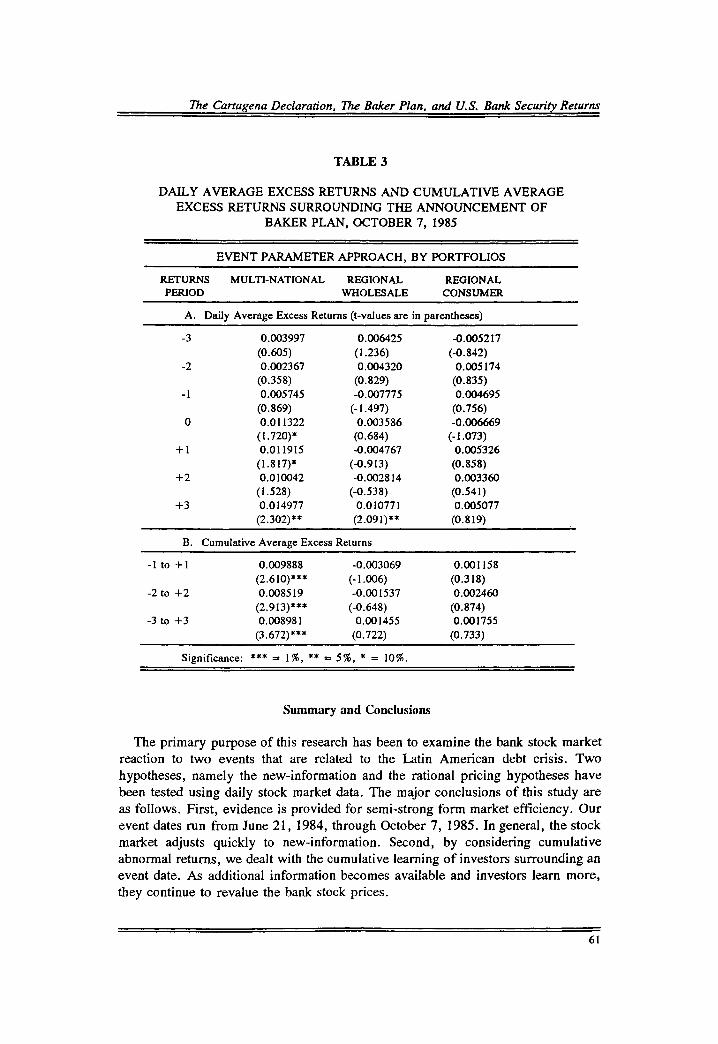

The results of bank equity market reaction to the announcement of the Baker Plan are reported in Table 3. Because this announcement outlines a comprehensive strategy to resolve the debt crisis, the market is expected to react positively. The results also support this idea. The regional consumer group shows no significant response to this announcement either in ARs or CARs. The regional wholesale group shows significant positive ARs at the 5% level on day +3, but insignificant CARs in all three event windows. However, the ARs for the multinational group are significantly positive for days 0 and + 1 at the 10% level and for day +3 at the 5% level. In addition, this group shows significant positive CARs at the 1% levels in all three event windows.

59

JOURNAL OF ECONOMICS AND FINANCE

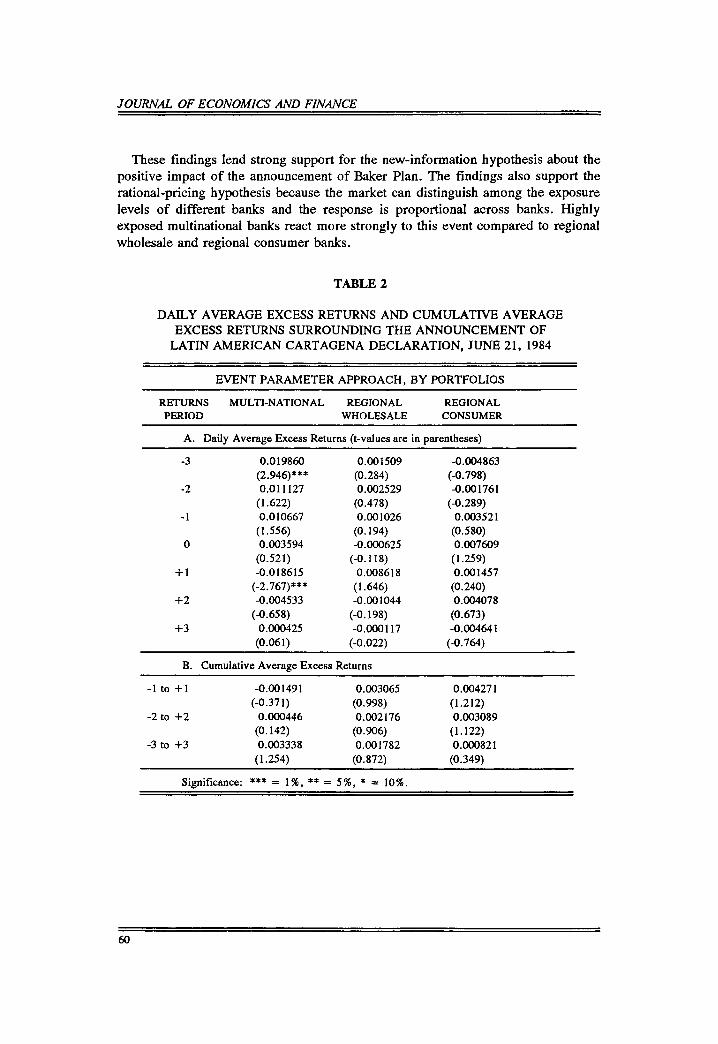

These f indings lend s t rong suppor t for the new- in fo rma t ion hypo thes i s about the

pos i t ive impac t o f the announcement o f Baker Plan. The f ind ings also suppor t the

ra t iona l -p r ic ing hypothes i s because the marke t can d is t inguish a m o n g the exposu re

levels o f d i f ferent banks and the r e sponse is p ropor t iona l ac ross banks . High ly

exposed mul t ina t ional banks react m o r e s t rongly to this event c o m p a r e d to regional

who le sa l e and reg iona l c o n s u m e r banks .

TABLE 2

DAILY AVERAGE EXCESS RETURNS AND CUMULATIVE AVERAGE EXCESS RETURNS SURROUNDING THE ANNOUNCEMENT OF

LATIN AMERICAN CARTAGENA DECLARATION, JUNE 21, 1984

EVENT PARAMETER APPROACH, BY PORTFOLIOS

RETURNS MULTI-NATIONAL REGIONAL REGIONAL PERIOD WHOLES ALE CONS UMER

A. Daily Average Excess Returns (t-values are in parentheses)

-3 0.019860 0.001509 -0.004863 (2.946)*** (0.284) (-0.798)

-2 0.011127 0.002529 -0.001761 (1.622) (0.478) (-0.289)

- 1 0.010667 0.001026 0.003521 ( 1.556) (0.194) (0.580)

0 0.003594 -0.000625 0.007609 (0.521) (-0.118) (1.259)

+1 -0.018615 0.008618 0.001457 (-2.767)*** (1.646) (0.240)

+2 -0.004533 -0.001044 0.004078 (-0.658) (-0.198) (0.673)

+3 0.000425 -0.000117 -0.004641 (0.061) (-0.022) (-0.764)

B. Cumulative Average Excess Returns

-1 to +1 -0.001491 0.003065 0.004271 (-0.371) (0.998) (1.212)

-2 to +2 0.000446 0.002176 0.003089 (0.142) (0.906) (1.122)

-3 to +3 0.003338 0.001782 0.000821 (1.254) (0.872) (0.349)

Significance: *** = 1%, ** = 5%, * = 10%.

60

The Cartagena Declaration, The Baker Plan, and U.S. Bank Securit~ Returns

TABLE 3

DAILY AVERAGE EXCESS RETURNS AND CUMULATIVE AVERAGE EXCESS RETURNS SURROUNDING THE ANNOUNCEMENT OF

BAKER PLAN, OCTOBER 7, 1985

EVENT PARAMETER APPROACH, BY PORTFOLIOS

RETURNS MULTI-NATIONAL REGIONAL REGIONAL PERIOD WHOLESALE CONSUMER

A. Daily Average Excess Returns (t-values are in parentheses)

-3 0.003997 0.006425 -0.005217 (0.605) (1.236) (.0.842)

-2 0.002367 0.004320 0.005174 (0.358) (0.829) (0.835)

- 1 0.005745 -0.007775 0.004695 (0.869) (- 1.497) (0.756)

0 0.011322 0.003586 -0.006669 (1.720)* (0.684) (- 1.073)

+ 1 0.011915 -0.004767 0.005326 (1.817)* (-0.913) (0.858)

+2 0.010042 -0.002814 0.003360 (1.528) (.0.538) (0.541)

+3 0.014977 0.010771 0.005077 (2.302)** (2.091)** (0.819)

B. Cumulative Average Excess Returns

-1 to +1 0.009888 .0.003069 0.001158 (2.610)*** (-1.006) (0.318)

-2 to +2 0.008519 -0.001537 0.002460 (2.913)*** (-0.648) (0.874)

-3 to +3 0.008981 0.001455 0.001755 (3.672)*** (0.722) (0.733)

Significance: *** = 1%, ** = 5%, * = 10%.

Summary and Conclusions

The primary purpose of this research has been to examine the bank stock market reaction to two events that are related to the Latin American debt crisis. Two hypotheses, namely the new-information and the rational pricing hypotheses have been tested using daily stock market data. The major conclusions of this study are as follows. First, evidence is provided for semi-strong form market efficiency. Our event dates run from June 21, 1984, through October 7, 1985. In general, the stock market adjusts quickly to new-information. Second, by considering cumulative abnormal returns, we dealt with the cumulative learning of investors surrounding an event date. As additional information becomes available and investors learn more, they continue to revalue the bank stock prices.

61

JOURNAL OF ECONOMICS AND FINANCE

It should be noted that because contagion effects have been previously documented, market efficiency cannot be assumed a priori. The result that the market for bank stocks is semi-strong form efficient indicates that bank managers should not in general take added precautions to either delay or downplay their involvement with troubled international loans. In the short run, the market exposure will be accurately diagnosed, on the average, by investors.

Finally, the evidence indicates that markets reacted rationally when adjusting the valuation of U.S. bank stocks for events that were neither borrower-induced nor lender-induced. Thus, those banks displaying greater exposure to LDC loans were affected in a direct and proportionately greater manner.

Acknowledgements

The authors wish to thank Larry Cordell and Mike Madaris for comments on earlier drafts of this paper. Special thanks are offered to the editor, James T. Lindley, and to two anonymous referees for comments and suggestions that significantly contributed to the paper.

NOTES

1Information on foreign proportion of loan portfolios was taken from Moody's Handbook of Common Stocks, Winter 1987 and Winter 1989-1990 editions. These proportions represent maximum exposure, which in most, if not all, cases will be an overstatement of LDC loan exposure.

REFERENCES

Binder,

Bruner,

Aharony, Joseph, and Itzhak Swary. "Contagion Effects of Bank Failures: Evidence from Capital Markets." Journal of Business 56 (July 1983): 305-322.

John J. "On the Use of the Multivariate Regression Model in Event Studies." Journal of Accounting Research 23 (Spring 1985): 370-383.

Robert F., and John M. Simms, Jr . "The International Debt Crisis and Bank Security Returns in 1982." Journal of Money, Credit and Banking 19 (February 1987): 46-55.

Cornell, Bradford, and Alan C. Shapiro. "The Reaction of Bank Stock Prices to the International Debt Crisis." Journal of Banking and Finance 10 (March 1986): 55-73.

Fama, Eugene F. Foundations of Finance. New York: Basic Books, 1976.

Grammatikos, Theoharry, and Anthony Saunders. "Additions to Bank Loan-Loss Reserves: Good News or Bad News?" Journal of Monetary Economics 25 (March 1990): 289-304.

62

The Cartagena Declaration, The Baker Plan, and [1.S. Bank Security Returns

Karafiath, Imre, Ross Mynatt, and Kenneth L. Smith. "The Brazilian Default Announcement and the Contagion Effect Hypothesis." Journal of Banking and Finance 15 (June 1991): 699-716.

Kyle, Steven C., and Ronald G. Wirick. "The Impact of Sovereign Risk on the Market Valuation of U.S. Bank Equities." Journal of Banking and Finance 14 (October 1990): 761-780.

Madura, Jeff, and William R~ McDaniel. "Market Reaction to Increased Loan Loss Reserves at Money Center Banks." Journal of Financial Services Research 3 (December 1989): 359-369.

Madura, Jeff, Ann Marie Whyte, and William McDaniel. "Reaction to British Bank Share Prices to Citicorp's Announced $3 Billion Increase in Loan-Loss Reserves." Journal of Banking and Finance 15 (February 1991): 151-163.

Mansur, Iqbal, StevenJ. Cochran, and David T. Cahill. "The Relationship Between Bank Equity Returns and the Brazilian Interest Payments Moratorium." Journal of Applied Business Research 9 (Winter 1988-89): 52-58.

Mansur, Iqbal, Steven J. Cochran and David K. Seagers. "The Relationship Between the Argentinean Debt Rescheduling Announcement and Bank Equity Returns." The Financial Review 25 (May 1990): 321-334.

Musumeci, James J. , and Joseph F. Sinkey, Jr . "The International Debt Crisis and Bank Loan-Loss-Reserve Decisions: The Signaling Content of Partially Anticipated Events." Journal of Money, Credit and Banking 22 (August 1990): 370-387.

Musumeci, James J., and Joseph F. Sinkey, Jr . "The International Debt Crisis, Investor Contagion and Bank Security Returns in 1987: The Brazilian Experience." Journal of Money, Credit and Banking 22 (May 1990): 209-220.

Schoder, Stewart, and Prashant VanKudre. "The Market for Bank Stocks and Banks' Disclosure to Cross Border Exposure: the 1982 Mexican Debt Crisis." Studies in Banking and Finance 3 (1986): 179-202.

Sinkey, Joseph F., Jr . , and Mary Brady Greenwalt. "Loan-loss Experience and Risk- taking Behavior at Large Commercial Banks." Journal of Financial Services Research 5 (March 1991): 43-59.

Smirlock, Michael, and Howard Kaufoid. "Bank Foreign Lending, Mandatory Disclosure Rules, and the Reaction of Bank Stock Prices to the Mexican Debt Crisis." Journal of Business 60 (July 1987): 347-364.

Wet.more, Jill L., and John R. Brick. "LDC Write-off Effects and Bank Stock Returns: The Bank of Boston Decision." The Quarterly Journal of Business and Economics 30 (Spring 1991): 90-110.

63

Related Documents