The Business Case for Quality Gerry Marr Chief Executive

The Business Case for Quality Gerry Marr Chief Executive.

Jan 01, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Business Case for Quality

Gerry MarrChief Executive

BUDGET - UK Economic Forecasts

35 90175 173 140 118 97

527609

792

9771130

12621370

0

200

400

600

800

1000

1200

1400

1600

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

Fiscal Year

£b

n

Net Borrowing Public sector net debt - end year

Multiplied by 5 in 2 years & represents 12.4% of GDP

c £44K for each economically active person in the UK

Calculated using latest data from National Statistics

76.2% of GDP

36.5% of GDP

c £17K for each economically active person in the UK

Budget “Building Britain’s Future”Overall UK Public

Expenditure

• £5bn additional “value for money” savings” in 2010/11

• Up to £9bn additional recurring savings by 2013/14

• Real terms growth of 0.7% between 2011/12 and 2013/14

Scottish Parliament Finance Committee -Report On Strategic Budget ScrutinyJune 2009The Centre for Public Policy for Regions (CPPR) Risk

Analysis

• “By 2013-14 the (Scottish) Budget will be between roughly £2 billion and £4 billion lower in real terms than at its peak in 2009-10.

• That represents a 7 to 13 per cent real terms cut over that four to five-year period.”

• In the period forward to 2017-18 it expects “a return to positive, but very low, real-terms growth of perhaps around 1 per cent.”

• This compares with its estimate of an average of 6 per cent per year growth in the Scottish budget over the first six or seven years of devolution.

The Balance of Quality and Cost

Responding to what patients want and need

The Healthcare Quality Strategy for Scotland

• Person-Centred - Mutually beneficial partnerships between patients, their families, and those delivering healthcare services which respect individual needs and values, and which demonstrate compassion, continuity, clear communication, and shared decision making.

• Clinically Effective - The most appropriate treatments, interventions, support, and services will be provided at the right time to everyone who will benefit, and wasteful or harmful variation will be eradicated.

• Safe - There will be no avoidable injury or harm to patients from healthcare they receive, and an appropriate clean and safe environment will be provided for the delivery of healthcare services at all times.

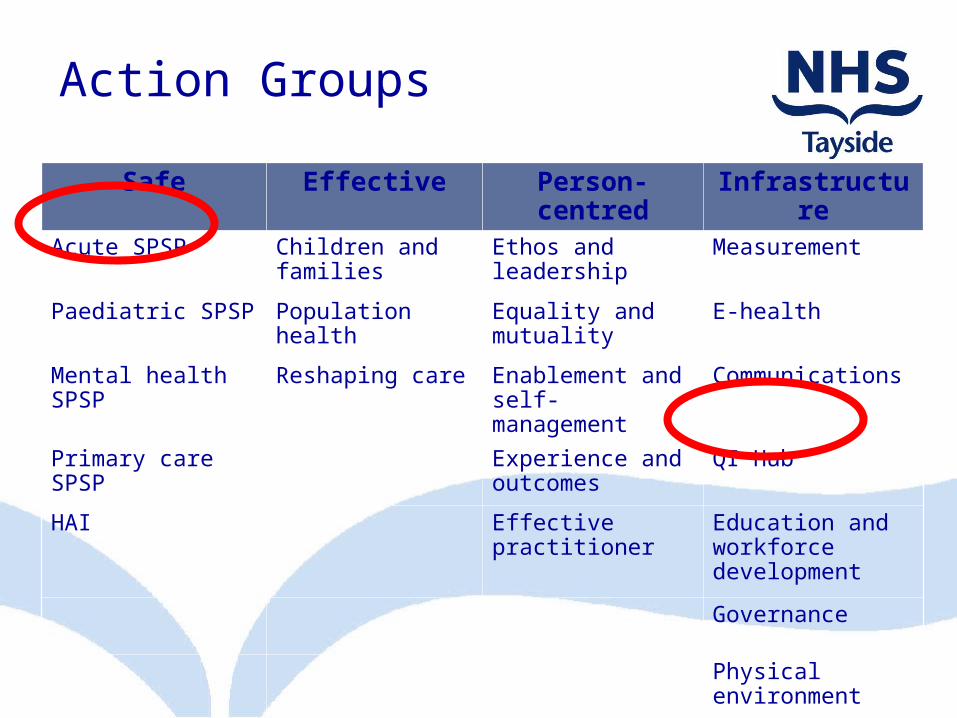

Action Groups

Safe Effective Person-centred

Infrastructure

Acute SPSP Children and families

Ethos and leadership

Measurement

Paediatric SPSP Population health

Equality and mutuality

E-health

Mental health SPSP

Reshaping care Enablement and self-management

Communications

Primary care SPSP

Experience and outcomes

QI Hub

HAI Effective practitioner

Education and workforce development

Governance

Physical environment

Aim, Objectives & ScopeThree Framework themes:

• Support – supporting our workforce.

• Enablers – identifying, sharing, sustaining good practice.

• Cost reductions – reducing variation, waste and harm.

Framework objectives:• Quality is not

compromised,• NHSScotland will achieve

financial balance over the SR10 period,

• NHS Boards are supported in achieving efficiency targets and improving services, and

• Central co-ordination of support, monitoring, benefits realisation and challenge will be available to NHS Boards.

“To improve the overall quality and efficiency of NHSScotland while ensuring good value for money and achieving financial targets.”

Tackling Variation – high cost, high volume services

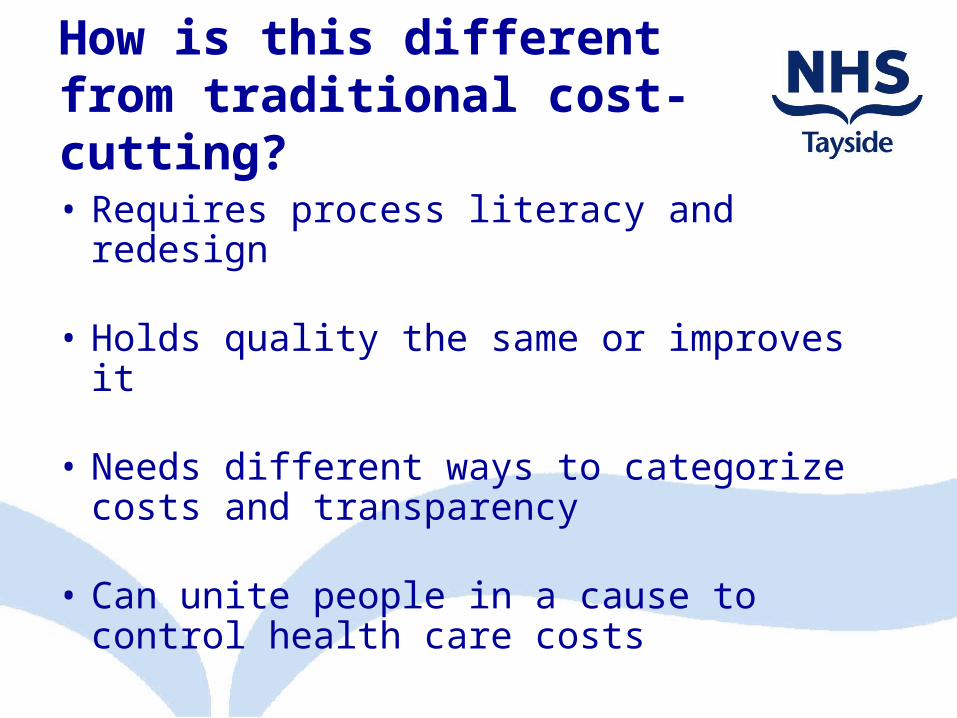

How is this different from traditional cost-cutting?

• Requires process literacy and redesign

• Holds quality the same or improves it

• Needs different ways to categorize costs and transparency

• Can unite people in a cause to control health care costs

The paradox of plentyWhat do higher spending regions -- and systems -- get?

Technical quality worseNo more elective surgeryMore hospital stays, visits, specialist use, tests

Content / Quality of Care1,2

Slightly higher mortalityNo better function

Health Outcomes1,2

Worse communication among physiciansGreater difficulty ensuring continuity of careGreater difficulty providing high quality careGreater perception of scarcity

Physician’s perceptions5

Patient-perceived quality1,3 Lower satisfaction with hospital careWorse access to primary care

Trends over time4 Greater growth in per-capita resource useLower gains in survival (following AMI)

(1) Ann Intern Med: 2003; 138: 273-298 (2) Health Affairs web exclusives, October 7, 2004(3) Health Affairs, web exclusives, Nov 16, 2005(4) Health Affairs web exclusives, Feb 7, 2006(5) Ann Intern Med: 2006; 144: 641-649

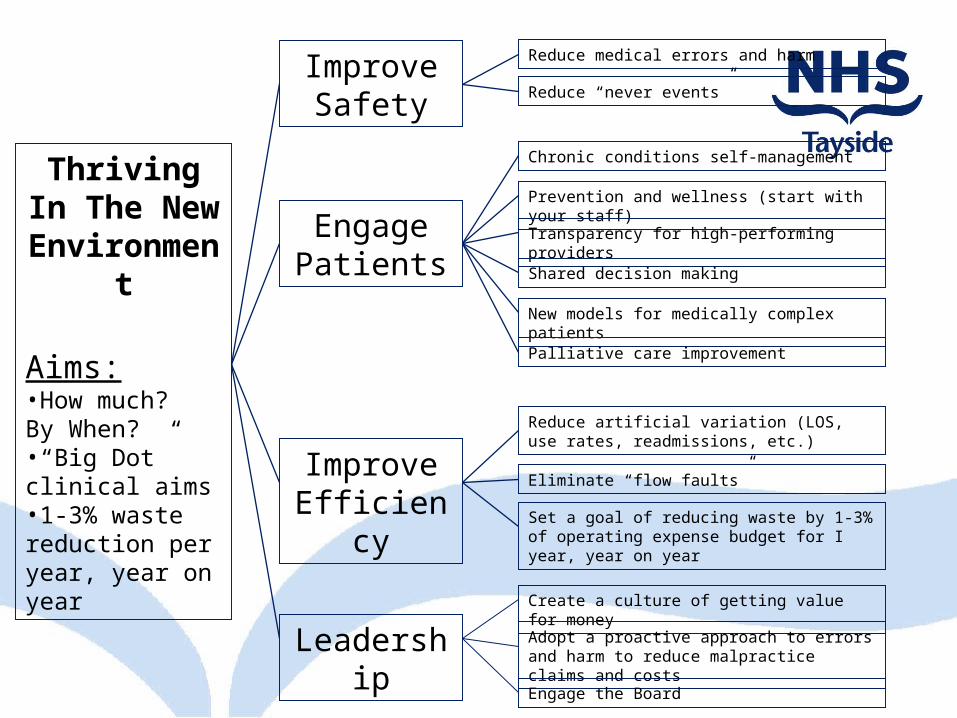

Thriving In The New

Environment

Aims:•How much? By When?•“Big Dot” clinical aims•1-3% waste reduction per year, year on year

Improve Safety

Engage Patients

Improve Efficiency

Leadership

Reduce medical errors and harm

Reduce “never events”

Chronic conditions self-management

Prevention and wellness (start with your staff)

Transparency for high-performing providers

Shared decision making

New models for medically complex patients

Palliative care improvement

Reduce artificial variation (LOS, use rates, readmissions, etc.)

Eliminate “flow faults”

Set a goal of reducing waste by 1-3% of operating expense budget for I year, year on year

Create a culture of getting value for money

Adopt a proactive approach to errors and harm to reduce malpractice claims and costs

Engage the Board

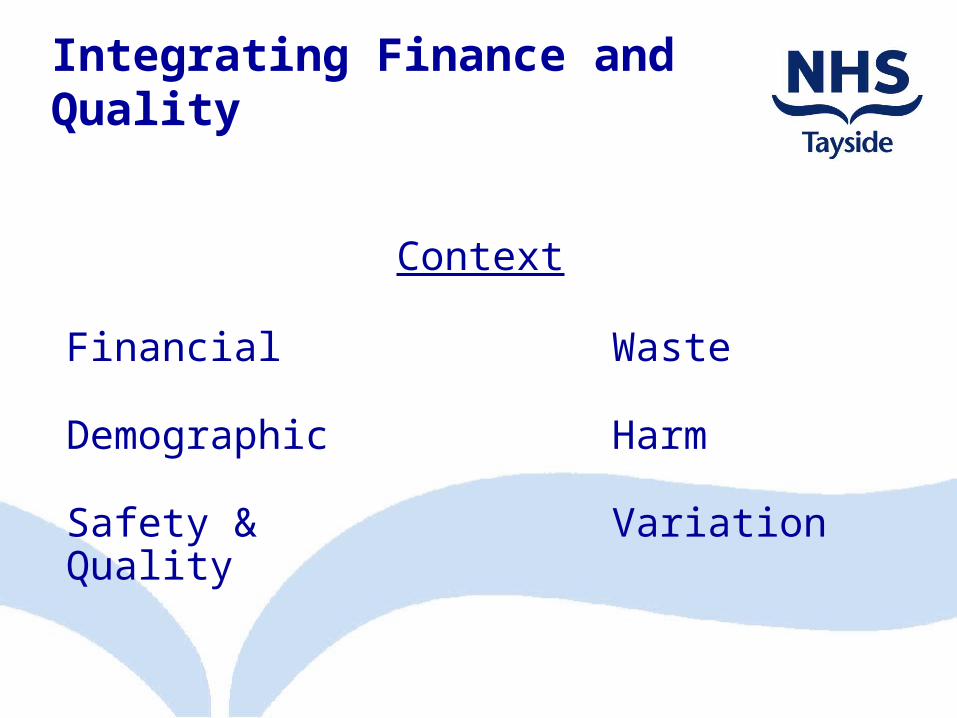

Integrating Finance and Quality

Context

Financial Waste

Demographic Harm

Safety & Quality Variation

Demographic change for population aged 65+ ScotlandPotential impact on emergency bed numbers 2007-2031

0

2000

4000

6000

8000

10000

12000

14000

16000

Y/E Mar 2007 Projected2011

Projected2016

Projected2021

Projected2026

Projected2031

Year

Be

ds

9%24%

41%61%

84%

NHS Tayside+148 beds 2016+517 beds 2031

Healthcare demand is growing

A new NinewellsHospital by 2031!

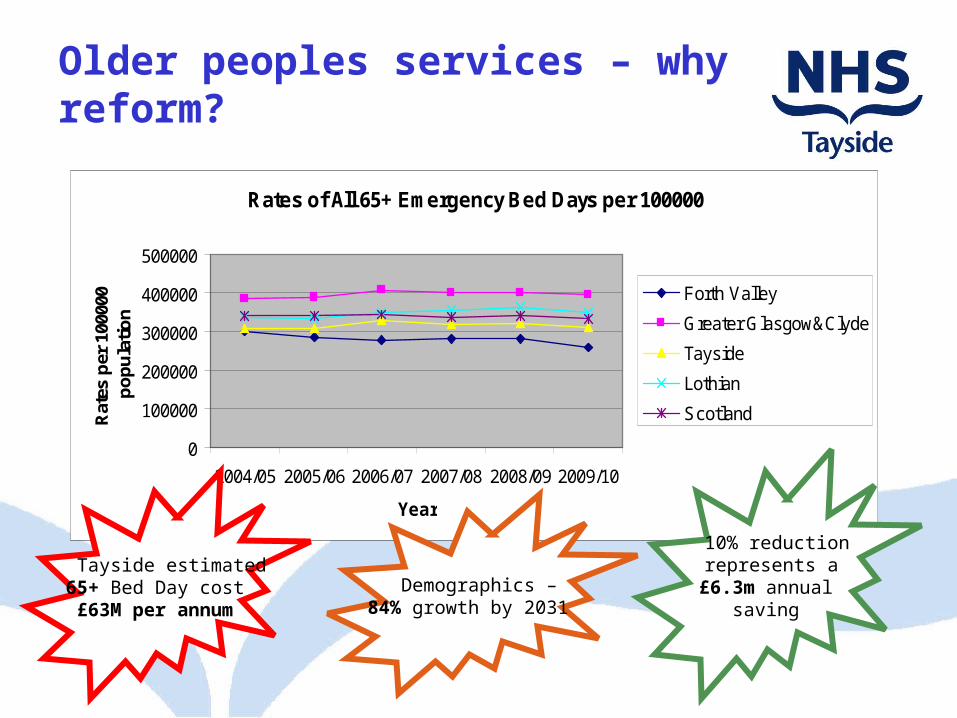

Older peoples services – why reform?

Rates of All 65+ Emergency Bed Days per 100000

0

100000

200000

300000

400000

500000

2004/05 2005/06 2006/07 2007/08 2008/09 2009/10

Year

Rat

es p

er 1

0000

0 p

op

ula

tio

n

Forth Valley

Greater Glasgow&Clyde

Tayside

Lothian

Scotland

Tayside estimated65+ Bed Day cost£63M per annum

10% reduction represents a£6.3m annual

saving Demographics –

84% growth by 2031

= Constraint

A&E

in-patient

out-patient

rehab

day case

acute services

acutereceiving

ward(Med/Surg)

MIU

SAS

OOH

OOH, urgent & emergency services (community)

NHS 24

GDP

GP

Community Pharmacists

family health services

Optom

refer to GP

sub-contractout-reach

Specialist acute care

tertiary services

routinedischarge

complexdischarge

LocalAuthorities

Partner & Vol organisations

refer on-going community care

Walk-In

RadiologyEndoscopy

GP referral

GP direct

access

GP referral

day patient

OutpatientClinic

Community Services – partnership model with LA

Home Visit

district nursinghealth visitingspecialist nursingAHP (e.g. physio, OT)

elderly care

Care in the community

Community (day) Hospitals

mental health

Day Patient

Inpatient

other

OutpatientClinic

Community Services – partnership model with LA

Home Visit

district nursinghealth visitingspecialist nursingAHP (e.g. physio, OT)

elderly care

Care in the community

Community (day) Hospitals

mental health

Day Patient

Inpatient

other

Laboratory

GP feedback

Tayside Whole System Model - Imbalance

= Queue Before Activity

= Target Challenge

= Trend in Volume

= Known Issue

= Suspected Issue

Q

T

Areas of Imbalance:

1. Queues in the system• Referral to 1st Appointment• Admission queues post

Decision to admit (Ward 15)

• Awaiting inpatient beds in the Community

2. Performance Vs. Target• Utilisation of some

community beds• 18 week RTT• Internal targets on

Turnaround

3. Trends• Increasing trend in GP

referrals up 12%• Urgent & Emergency

admissions up 7%

4. Constraints• Average Length of Stay in

Community Hospitals is 21 days

• Availability of data

T

T

acutereceiving

ward(Med/Surg)

out-patient

Q

routinedischarge

complexdischarge

Q

T

Q

C

Q

Q

C

Evidence of Waste in Healthcare Systems

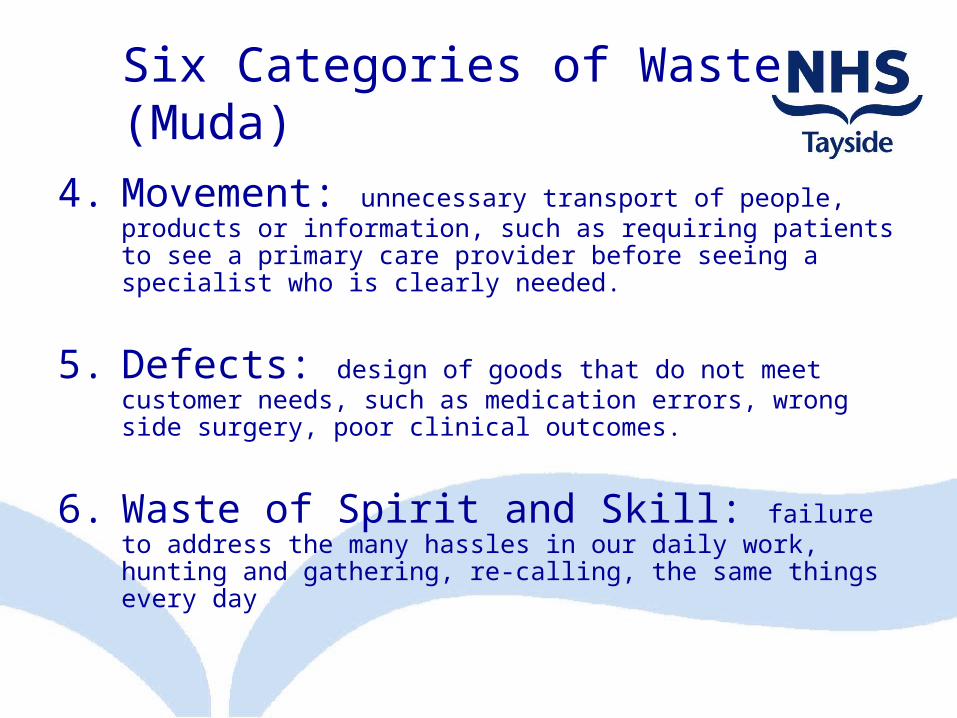

Six Categories of Waste (Muda)

1. Delay: idle time spent waiting for something, such as utilization reviews, insurer payments, test results, patient bed assignments, OR prep, medical appointments.

2. Re-work: performing the same task a second time, such as re-testing, re-scheduling, re-filing of lost claim forms, re-writing of patient demographic data, multiple bed moves.

3. Overproduction: manufacturing of products or information that is not needed, such as precautionary “defensive” medical tests, surplus medications, excessive levels of paperwork.

Cont.

4. Movement: unnecessary transport of people, products or information, such as requiring patients to see a primary care provider before seeing a specialist who is clearly needed.

5. Defects: design of goods that do not meet customer needs, such as medication errors, wrong side surgery, poor clinical outcomes.

6. Waste of Spirit and Skill: failure to address the many hassles in our daily work, hunting and gathering, re-calling, the same things every day

Six Categories of Waste (Muda)

• 27% of New Outpatient appointments are being wasted!

Are there significant Outpatient Capacity losses?

Increase Capacity of Outpatient Clinics?

Opportunity?

0.0

5.0

10.0

15.0

20.0

25.0

Discharged AWAITING TESTRESULT

REFD OTHERCLIN/HOSP

DNA-Total Could Not Wait - FA REFER TO OTHERHOSP

%

New

Return

Evidence of Clinical Variation in Healthcare Systems

Are there significant variations in hospital expenditure by GP practice?

0

200

400

600

800

1,000

1,200

Practices

£ p

er

we

igh

ted

he

ad

Emergency Elective

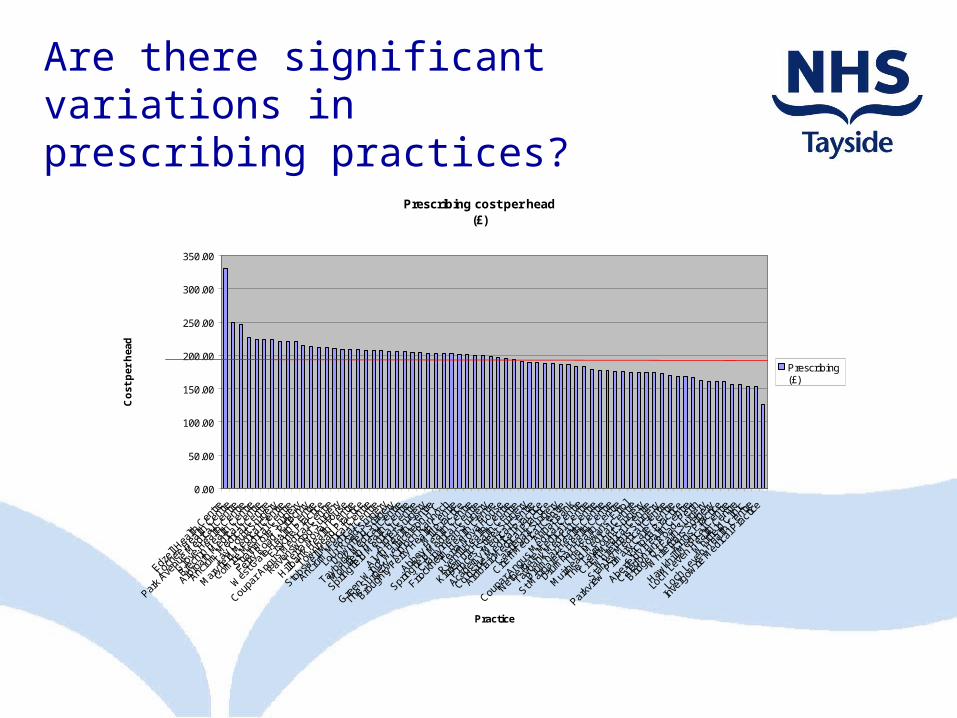

Are there significant variations in prescribing practices?

Prescribing cost per head(£)

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

Edzell

Hea

lth C

entre

Loch

ee H

ealth

Cen

tre

Park A

venu

e M

edica

l Cen

tre

Grove

Hea

lth C

entre

Brech

in Hea

lth C

entre

Arbro

ath

Med

ical C

entre

Ancru

m M

edica

l Cen

tre

Tay C

ourt

Surge

ry

Mar

yfield

Med

ical C

entre

Comrie

Med

ical C

entre

Strath

mor

e Sur

gery

Ferry

Roa

d, P

itloch

ry

Wes

t Gat

e Hea

lth C

entre

Erskin

e Pra

ctice

Coupa

r Ang

us M

edica

l Cen

tre

Raven

swoo

d Sur

gery

Terra

Nov

a Hou

se

Hillban

k Hea

lth C

entre

Townh

ead

Practi

ce

Stobs

well M

edica

l Cen

tre

Ancru

m M

edica

l Cen

tre

Lour

Roa

d Sur

gery

Downf

ield

Surge

ry

Tayba

nk M

edica

l Cen

tre

Mon

ifieth

Hea

lth C

entre

Spring

field

Med

ical C

entre

Ardler

Sur

gery

Alyth

Health

Cen

tre

Green

Wing

, Wall

acet

eon

H.C

The S

urge

ry, K

inloc

h Ran

noch

Broug

hty F

erry

Hea

lth C

entre

Mill

Practi

ce

Abbey

Hea

lth C

entre

Spring

field

Med

ical C

entre

Craigv

inean

Sur

gery

Friock

heim

Hea

lth C

entre

Terra

Nov

a Hou

se

Ryehil

l Hea

lth C

entre

Kirriem

uir H

ealth

Cen

tre

Prince

s Stre

et S

urge

ry

Acade

my M

edica

l Cen

tre

Coldsid

e M

edica

l Pra

ctice

Ardbla

ir M

edica

l Pra

ctice

Castle

gait S

urge

ry

Crieff

Med

ical C

entre

Annat

Ban

k

Coupa

r Ang

us M

edica

l Cen

tre

Nethe

rgat

e M

edica

l Cen

tre

Tayba

nk M

edica

l Cen

tre

Drum

har H

ealth

Cen

tre

St Mar

gare

t's H

ealth

Cen

tre

Drum

har H

ealth

Cen

tre

The R

owan

s, Erro

l

Muir

head

Med

ical C

entre

The T

aym

ount

Sur

gery

Crieff

Med

ical C

entre

Whit

efria

rs S

urge

ry

Stanle

y Med

ical C

entre

Parkv

iew P

rimar

y Car

e Cen

tre

Victor

ia Pra

ctice

Aberfe

ldy H

ealth

Cen

tre

Caledo

nian

Road,

Per

th

Bridge

Of E

arn

Surge

ry

Whit

efria

rs S

urge

ry

Kings P

racti

ce

Hawkh

ill M

edica

l Cen

tre

Loch

Lev

en H

ealth

Cen

tre

Whit

field

Clinic

Loch

Lev

en H

ealth

Cen

tre

Inve

rgow

rie M

edica

l Pra

ctice

Practice

Co

st p

er h

ead

Prescribing (£)

Average £194.5

Are there significant variations in clinical practices in

prescribing medicines?

GIC per 1000 Patients during the period:-July 2008 to September 2008

£0

£10,000

£20,000

£30,000

£40,000

£50,000

£60,000

£70,000

1309

111

005

1283

111

096

1010

610

708

1319

511

645

1193

111

382

1221

011

861

1357

110

799

1018

211

058

1362

113

335

1130

610

233

1117

113

284

1263

311

486

1323

111

433

1450

111

823

1141

410

322

1165

010

407

1116

610

498

1044

510

125

1028

611

289

1304

913

532

1228

110

638

1434

212

991

1370

612

493

1424

910

002

1456

913

975

1366

010

751

1036

114

037

1394

110

553

1003

613

369

1384

813

891

1136

314

291

1349

613

481

1001

710

835

1290

113

142

Practice Reference (CHP)

Cos

t per

100

0 P

atie

nts

Variation in Gross Ingredient Cost (GIC) per 1,000 patients across practices

Are there significant variations in clinical

practices in prescribing medicines?

Variation by Defined Daily Dose per 1000 patients

Hypnotics and Anxiolytics DDDs per 1000 Patients during the period:-July 2008 to September 2008

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1100

512

633

1221

010

445

1283

110

182

1109

611

058

1165

011

306

1333

511

931

1141

412

281

1397

510

106

1079

911

861

1040

713

369

1128

910

708

1117

111

363

1384

811

433

1164

514

249

1403

710

125

1304

914

342

1349

610

361

1032

210

036

1001

713

941

1357

114

291

1000

211

166

1182

310

751

1028

612

991

1348

110

498

1370

613

195

1353

210

233

1148

611

382

1328

413

660

1063

810

835

1450

113

891

1362

112

901

1055

313

091

1249

313

231

1314

214

569

Practice Reference (CHP)

DD

Ds

per

1000

Pat

ient

s

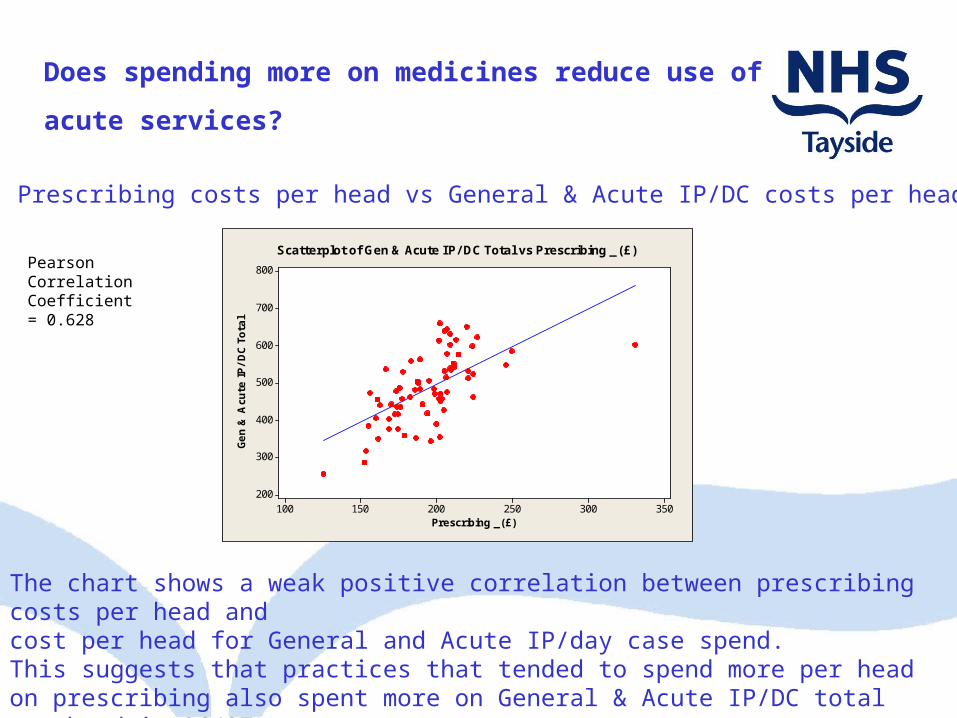

Prescribing _(£)

Gen &

Acu

te IP/DC T

ota

l

350300250200150100

800

700

600

500

400

300

200

Scatterplot of Gen & Acute IP/ DC Total vs Prescribing _ (£)Pearson Correlation Coefficient = 0.628

The chart shows a weak positive correlation between prescribing costs per head andcost per head for General and Acute IP/day case spend.This suggests that practices that tended to spend more per head on prescribing also spent more on General & Acute IP/DC total per head in 06/07

Prescribing costs per head vs General & Acute IP/DC costs per head

Does spending more on medicines reduce use of

acute services?

Examples of Variation in Clinical Practice

• Poly pharmacy

• Referral patterns into acute specialist care

• Rates of admissions in over 65 years

• Lengths of stay in over 65 years

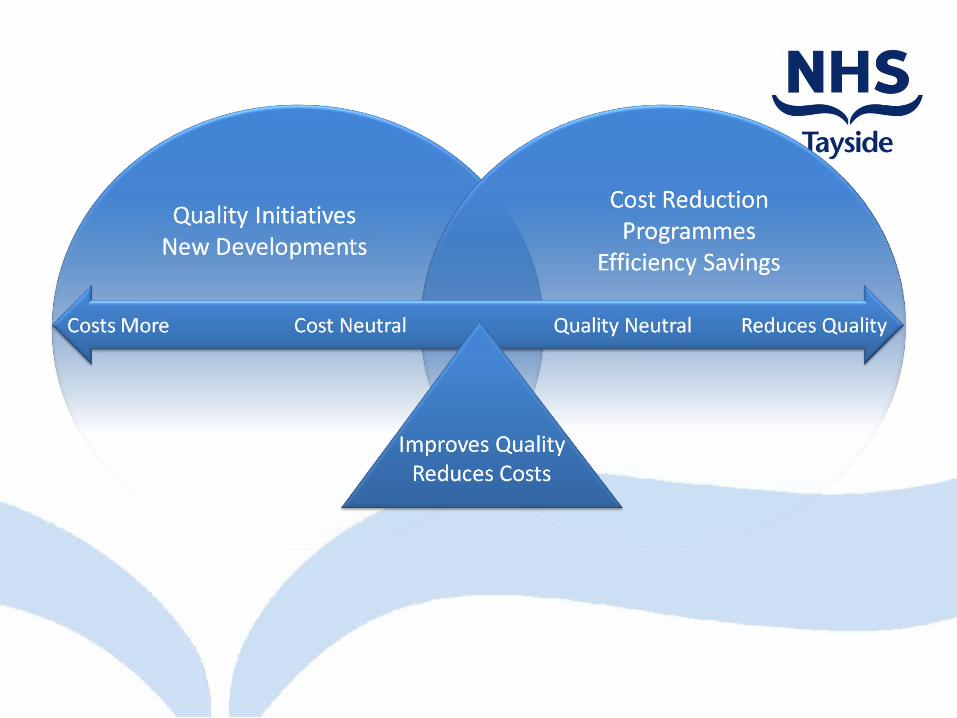

Achieving Quality Improvement and Cost ReductionDeveloping and Improving Services

QUALITY INITIATIVES COST REDUCTION PROGRAMMESNEW DEVELOPMENTS EFFICIENCY SAVINGS

1 2 3 4 5

Costs more Cost neutral Improves quality Quality neutral Reduces & reduces costs quality

Improving Quality and Reducing Costs

Our Choice

Surviving – the 5%

Thrive – the 95%

TACTICAL STRATEGIC

DEALING WITH THE 5%

SPENDING THE 95% BETTER

PRODUCTIVITY & EFFICIENCY

CRES

SERVICE OPTIMISATION

TRANSFORMATION

2009 - 2011

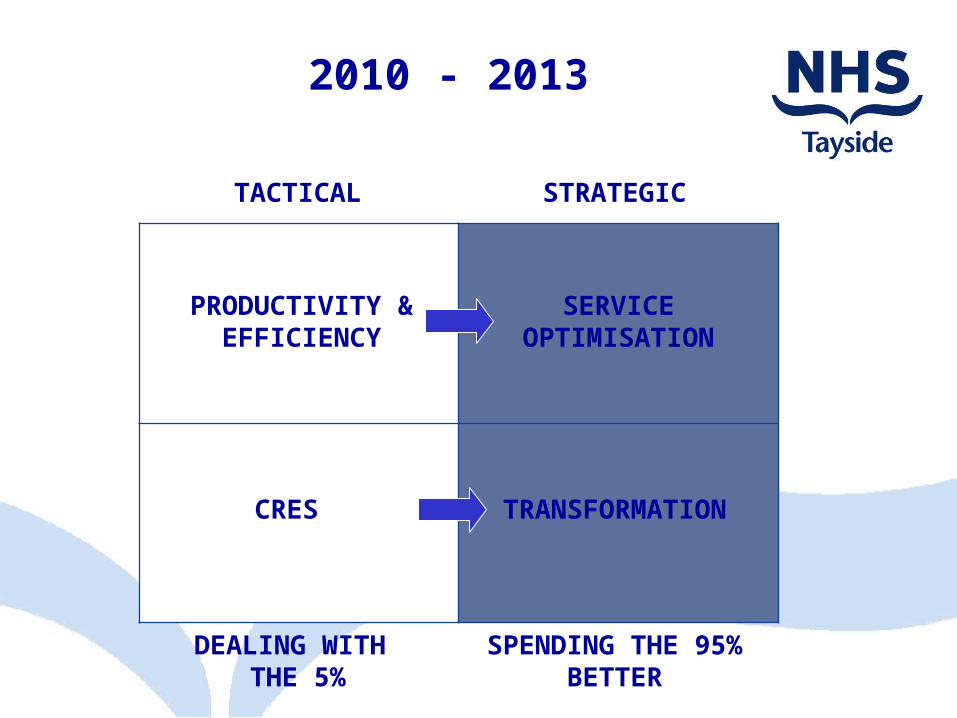

2010 - 2013

TACTICAL STRATEGIC

DEALING WITH THE 5%

SPENDING THE 95% BETTER

PRODUCTIVITY & EFFICIENCY

CRES

SERVICE OPTIMISATION

TRANSFORMATION

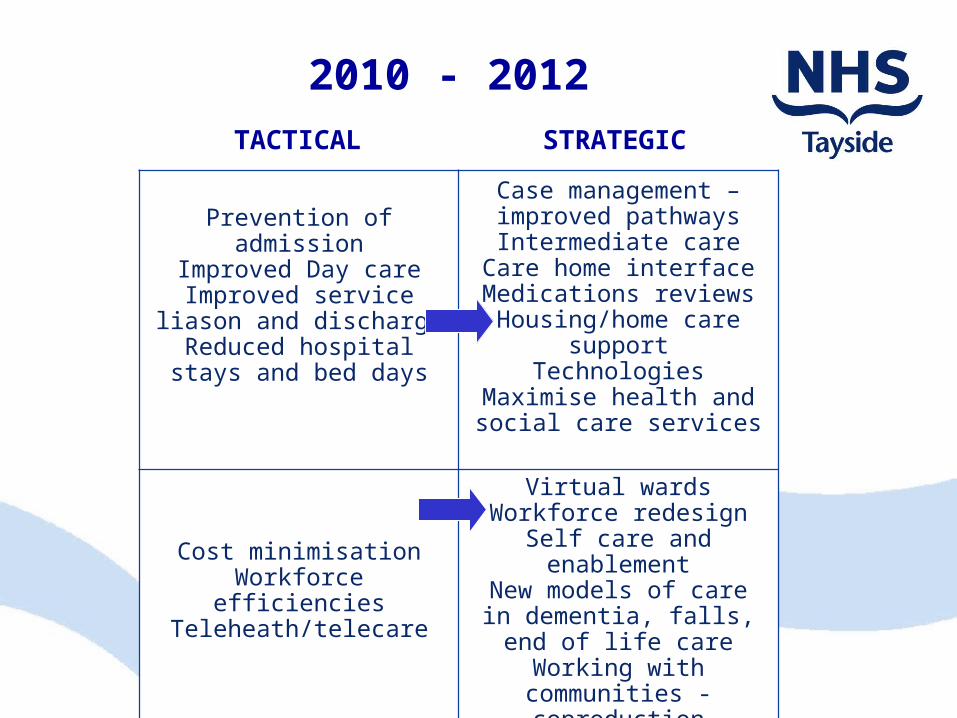

2010 - 2012TACTICAL STRATEGIC

DEALING WITH THE 5%

SPENDING THE 95% BETTER

Prevention of admissionImproved Day care

Improved service liason and discharge

Reduced hospital stays and bed days

Case management – improved pathwaysIntermediate care

Care home interfaceMedications reviewsHousing/home care

supportTechnologies

Maximise health and social care services

Cost minimisationWorkforce efficiencies

Teleheath/telecare

Virtual wardsWorkforce redesign

Self care and enablement

New models of care in dementia, falls, end of

life careWorking with communities - coproduction

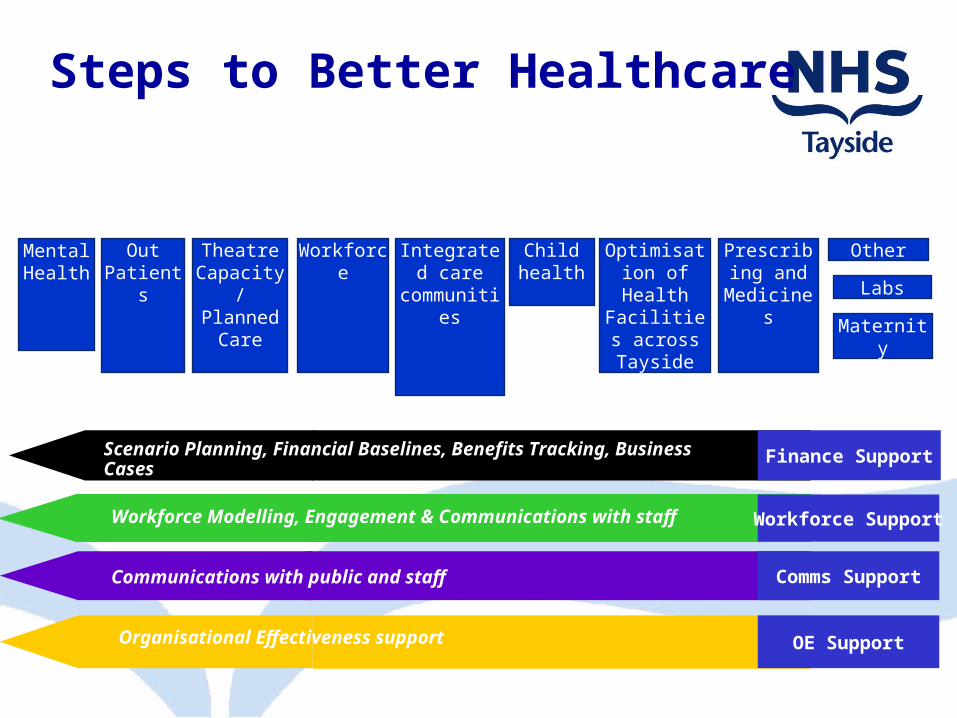

Steps to Better Healthcare

Mental Health

OutPatients

Theatre Capacity / Planned

Care

Workforce Integrated care

communities

Child health

Optimisation of Health Facilities across Tayside

Prescribing and

Medicines

Finance Support

Workforce Support

Scenario Planning, Financial Baselines, Benefits Tracking, Business Cases

Workforce Modelling, Engagement & Communications with staff

Comms SupportCommunications with public and staff

Other

OE SupportOrganisational Effectiveness support

Labs

Maternity

There Is No Recession In Innovation

“Fortunes are NOT made in the boom times...That

is merely the collection period. Fortunes are

made in depressions or lean times when the wise

man overhauls his mind, his methods, his

resources, and gets in training for the race to

come."

George Wood Bacon

Related Documents