OBU Research & Analysis Project The Business and Financial Performance of Jamaica Aggregates Limited for the period 2010 to 2012 A Case Study DRAFT (for feedback) Page 1 of 25

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

OBU Research & Analysis Project

The Business and Financial Performance of Jamaica Aggregates Limited

for the period 2010 to 2012

A Case Study

DRAFT (for feedback)

Page 1 of 25

OBU Research & Analysis Project

Word count: 5,400

PART 1 TOPIC & RESEARCH OBJECTIVES

Introduction

Given the experiences we have all had recently, we can presume that no

one would have predicted the construction materials industry’s destiny

of the past three years. While it has been tough, we continue to fight

(Wilson, 2012).

Lafarge invested $12M in cash for 50% ownership of Jamaica Aggregates

Limited (JAL) the joint venture with Jamaica Premix (JPM). Intentions

were to build an export facility and to begin and expand exports to

the United States. However, the strategic vision was never completely

executed (Lafarge, 2011). A receiving facility was built in 2009 but

an export facility was not built.

Lafarge’s ultimate goal is to create a profitable business with Return

on Assets above 10% or to divest its 50% share in JAL. However, there

are considerable obstacles to a potential divestment. The Jamaican

domestic market provides little value to investors due to the

perceived risk of doing business, as well as, the likely prevention of

future spending on infrastructure due to the country’s debt (Lafarge,

2011). Furthermore, it is estimated that the net worth of Jamaica

Aggregates Limited currently is far below Lafarge’s initial cash

investment of US$12 million.

Page 2 of 25

OBU Research & Analysis Project

Based on the above background, I have set out to do investigative

research in order to assess the true position of Jamaica Aggregates

Limited. Why has the joint venture not met the strategic targets set

for exports? Is the company a going concern? These are some of the

questions I would like answered.

As such, this analysis involves evaluating the company’s position and

viability from an internal business perspective and from a financial

perspective. Therefore, this research and analysis project assesses

the overall position of Jamaica Aggregates Limited.

Company Background

JAL currently has one operational plant at Yallahs and two inactive

plants at Paul Mountain and Martha Brae.

Jamaica Aggregates Limited is a producer and marketer of construction

aggregates in Jamaica and the region. The primary purpose of the Joint

Venture agreement (operational since early 2008) was to produce

construction aggregate in Jamaica and to market such products in

Jamaica and the greater Caribbean and allow for the export of such

materials to the US. The agreement identified four critical strategic

issues. This included improving the reserves at the Yallahs site,

building a port in close proximity to the site and developing two

additional sites to sustain the required target volumes (Jamaica

Aggregates, 2008).

In addition to the strategic areas mentioned above, Lafarge and JPM

had envisioned the business growing from historical levels of

approximately 1.5 million tonnes to approximately 3.4 million tonnes

by 2011 (Jamaica Aggregates, 2008).

Page 3 of 25

OBU Research & Analysis Project

JAL’s main competitor, Coast-to-Coast, also mines in the Yallahs river

and does processing opposite to the company. JAL’s main customer is

Jamaica Premix which purchases approximately 30% of total volume. The

company estimates that its market share is probably somewhere between

20 and 25%. (Jamaica Aggregates, 2012). However, as there is little

information available on this industry in Jamaica, this is difficult

to substantiate.

From a global perspective, the aggregate industry is highly

competitive and fragmented with sales generally concentrated in local

markets (Young, M.( 2006) ‘Construction Aggregates’). Jamaica is no

different.

Reason for Choosing Company and Topic

My main reason for selecting this topic is that in my capacity at the

organization as a Business Performance Manager, I wish to undertake a

detailed analysis of the entity’s viability and strategic position

within the Jamaican market. As such, this research would be a valuable

contribution to the organization. Such an analysis which studies the

company’s current status quo should enable a pro-active approach in

planning the strategy going forward

Secondly, having successfully completed my ACCA exams, I am seeking to

use this project to demonstrate my practical competences. This

research requires a demonstration of analytical ability and

interpretation of financial and non-financial information. All of

which I need to develop in furthering my professional development.

Thirdly, as I would like to further my career in economics and/or

financial analyses, this research will assist in my present and future

Page 4 of 25

OBU Research & Analysis Project

development. This research also required investigative research

techniques which is a core element in any Masters or MBA I may pursue

in the future.

Finally, as a lecturer on Performance and Financial Management, I

would like to challenge my true competence in applying this knowledge

to a real life case study.

Research Questions

TOPIC: “An evaluation of the business and financial performance of

Jamaica Aggregates Limited for the period 2009 to 2011”.

Financial Performance

1. Is the entity financially viable?

2. Are the company’s operations sustainable in the foreseeable

future?

3. How did the organization perform overall during the period under

review?

4. How does JAL perform in comparison to its comparators/industry

averages?

Business Performance

5. What are the core strengths of JAL that differentiates it from

its competitors?

6. What weaknesses and threats are hindering better performance?

7. How can these weaknesses and threats be mitigated?

8. What opportunities are available to JAL that they may capitalize

on?

Page 5 of 25

OBU Research & Analysis Project

Research Objectives and Overall Research Approach

Overall Approach

The overall research approach will include a combination of methods.

This includes interviews with key personnel at Jamaica Aggregates

Limited, ratio analyses, extensive reading on the company and its

industry, benchmarking and a SWOT analysis.

Ratio Analysis will be the main model used to address questions one

to four. In addition, for question one, Altman’s Z score will be the

primary measure used to assess the company’s financial health and

viability. Whilst for the third question, I will use trends in key

ratios, focusing mainly on liquidity and profitability. Industry

benchmarking will be done to address the fourth question. In

assessing the sustainability of operations, whilst ratio analysis

and benchmarking are essential, additional performance proxies will

be used such as EBITDA, Free Cash Flows etc. All four business

performance questions (5 – 8) will be addressed through a detailed

SWOT analysis.

INFORMATION GATHERING & ACCOUNTING/BUSINESS TECHNIQUES

Sources of Information and methods used to collect information

The main sources used to gather the information contained within this project was a combination of primary and secondary research discussed below:

Secondary Research

Company documents, discussions with key personnel, industry literature, ACCA texts and the internet.

Company documents included audited financial statements, board minutes, the joint venture agreement and business plan summaries.

Page 6 of 25

OBU Research & Analysis Project

Finally I did significant reading on the aggregate industry using the internet and researched how to perform a business and financial evaluation through the use of ACCA texts and the internet.

Primary Research

The primary documents were the Financial Statements of Jamaica Aggregates Limited and the Comparator Companies

Discussions were held with the Managing Director, who gave further insight into the joint venture operations and the ultimate vision of Lafarge for Jamaica Aggregates Limited. Several discussions were also held with the Financial Controller, who mainly gave a background and insight behind the ‘numbers’. As the financial controller has been with the organization over twenty years, his discourse was quite useful. He also provided much of the needed company records to enable this company appraisal, particularly, the audited financial statements

Being a key employee within the company also meant that I have access to certain information such as the Joint Venture Agreement, board minutes and business plan summaries.

Limitations of Information gathering

As with any research, there were several challenges faced in gatheringthe information.

The bases used for the performance assessment also have theoretical and conceptual limitations. However, this is addressed in more detail below

Also, of all the competitors contacted, no entity was willing to provide their financial information. None of these entities are listedand as such the required information was unavailable.

In the absence of competitor information, I resorted to a comparator within the region. Only one Aggregates producer of similar size was found, Polaris. However, at a glance, its performance did not seem ideal for benchmarking. As such, I choose two other companies, Vulcan Materials & Martin Marietta, of which a weighted average was done of

Page 7 of 25

OBU Research & Analysis Project

all three companies to produce an industry proxy ( for the purpose of the project).

Ethical issues

Due to the nature of this research, various issues arose whilst gathering the information. As Jamaica Aggregates Limited is not a public listed entity, essentially all the required information was confidential. Therefore, access to information needed authorization. This constraint was mitigated, however, as the researcher sought and obtained approval from the Managing Director of JAL. Additionally, theFinancial Controller was selected as the main resource person and a draft of the project submitted to the Company’s Board of Directors prior to submission.

Overall Approach

In analyzing the business performance, A SWOT analysis will be done. “A SWOT analysis is used to evaluate the Strengths, Weaknesses, Opportunities, and Threats involved in a business venture. It involves specifying the objective of the business venture and identifying the internal and external factors that are favorable and unfavorable to achieve that objective (Wikipedia). However, it must be acknowledged that there are several criticisms of SWOT. First, listed factors are neither weighted nor ranked in a traditional SWOT matrix so that critical constraints and resources are not explicit. Second, there is no quantitative index that summarizes the prospects and limitations of a system as well as provides an operational criterion for benchmarking, managing, and controlling identified SWOTs. Other limitations of SWOT Analysis include the subjectivity, integrity, and instability (over time) of listed strengths, weaknesses, opportunities, and threats (Koch, 2000).

From a financial performance perspective, trends in key ratios and industry benchmarking, focusing mainly on liquidity and profitability will be the main areas of appraisal.

Ratio analysis is useful as it provides a snapshot of a company’s performance in a simplified manner and allows for comparison with other entities within an industry. Because Ratio Analysis is based

Page 8 of 25

OBU Research & Analysis Project

upon accounting information, its effectiveness is limited by the distortions which arise in financial statements due to such things as Historical Cost Accounting and inflation. Therefore, Ratio Analysis should only be used as a first step in financial analysis, to obtain aquick indication of a firm's performance and to identify areas which need to be investigated further (Lane, 2012).

The Altman Z-score measures a company’s financial health and

viability. The variables considered include working capital, total

assets, equity value, retained earnings and sales. This is a model

developed based on a study of US firms in the manufacturing sector to

assess/predict corporate failure. A company is considered financially

sound with a score of 3 and above, whereas a score of 1.80 or less

suggests that the probability of financial catastrophe is extremely

high. If the Altman Z-Score is close to or below 3, then it would be

deemed appropriate do some serious due diligence (Accountancy Tuition

Centre, 2011).

Limitations of the Z- score

As mentioned in ATC 2011 Study System P5 Advanced Performance Management “The

model is based on historic data. It may not be appropriate therefore

for predicting future corporate failures, as industry and economic

factors may differ from that held for the sample data on which the

model is based. The text further mentions two other limitations “…many

bankruptcies are caused by internal factors…which cannot be seen in

financial statements…finance directors can manipulate the financial

statements to ensure that an acceptable Z-score is achieved”.

Two complimentary proxies will also be used to support the liquidity

and profitability evaluation. These are Free cash flows and Earnings

before interest, tax, depreciation and amortization (EBITDA).

Page 9 of 25

OBU Research & Analysis Project

Free cash flow ‘signals a company's ability to pay debt,

pay dividends, buy back stock and facilitate the growth of business -

all important undertakings from an investor's perspective. However,

while free cash flow is a great gauge of corporate health, it does

have its limits and is not immune to accounting trickery… Without a

regulatory standard for determining FCF, investors often disagree on

exactly which items should and should not be treated as capital

expenditures. Investors must therefore keep an eye on companies with

high levels of FCF to see if these companies are under-reporting

capital expenditure and R&D. Companies can also temporarily boost FCF

by stretching out their payments, tightening payment collection

policies and depleting inventories. These activities diminish current

liabilities and changes to working capital. But the impacts are likely

to be temporary. (Investopedia.com, 2010)

EBITDA is deemed a proxy for cash flows as it excludes the cost of

capital and non-cash charges on assets. This is very useful

particularly when comparing entities (as required in this project)

which different operating capacity and capital structure. However the

main limitation is that ‘ … it does not reflect changes in working

capital needed to finance inventory and receivable growth, nor does it

reflect legitimate expenses like interest and taxes’ (Atkins, n.d.).

The above techniques will be the primary medium used to facilitate an

overall evaluation of the performance of Jamaica Aggregates Limited.

Page 10 of 25

OBU Research & Analysis Project

ANALYSIS & RESEARCH FINDINGS

The review will begin with an analysis of a few key ratios, then a SWOT analysis and finalized with Benchmarking against an industry leader.

1. RATIO ANALYSIS

Liquidity Ratios

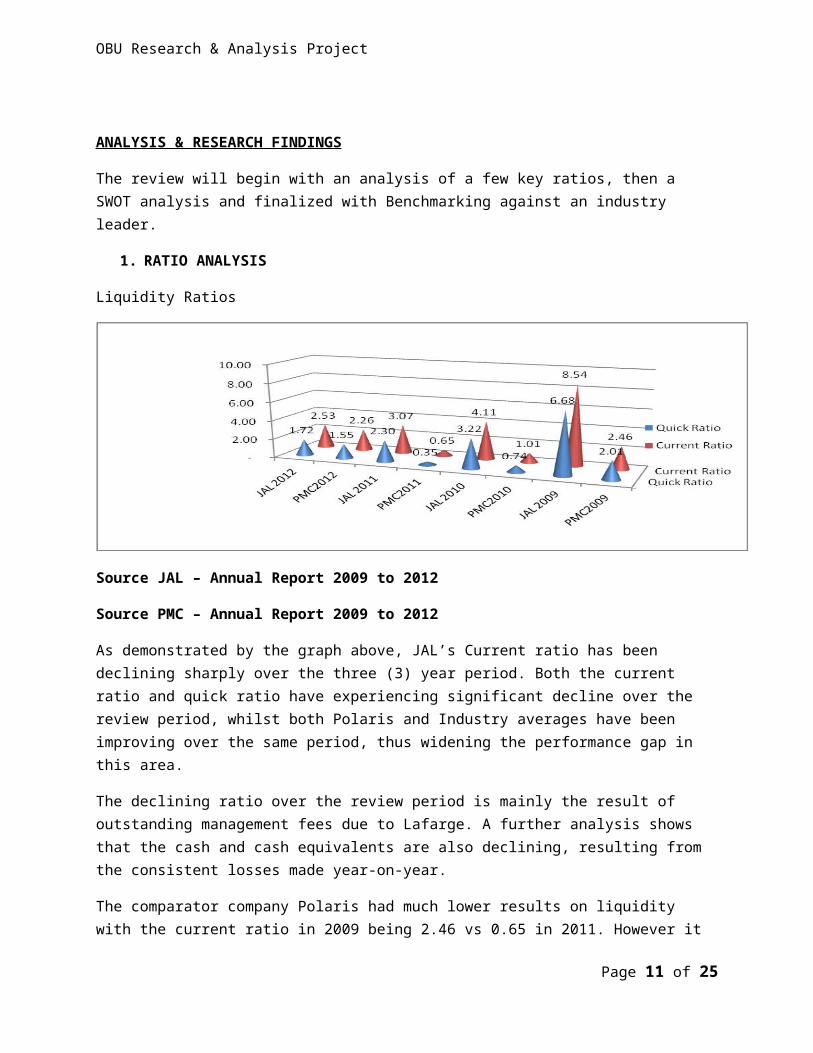

Source JAL – Annual Report 2009 to 2012

Source PMC – Annual Report 2009 to 2012

As demonstrated by the graph above, JAL’s Current ratio has been declining sharply over the three (3) year period. Both the current ratio and quick ratio have experiencing significant decline over the review period, whilst both Polaris and Industry averages have been improving over the same period, thus widening the performance gap in this area.

The declining ratio over the review period is mainly the result of outstanding management fees due to Lafarge. A further analysis shows that the cash and cash equivalents are also declining, resulting from the consistent losses made year-on-year.

The comparator company Polaris had much lower results on liquidity with the current ratio in 2009 being 2.46 vs 0.65 in 2011. However it

Page 11 of 25

OBU Research & Analysis Project

improved significantly in 2012 to 2.26 in 2012. This was in part as a result of a debt refinancing agreement in March 2012.

The working capital cycle averaged 165 days over the three year period. This is significantly higher than that of Polaris and the industry average used.

However, this is mainly a result of stock piling aggregates (increasing inventory). The main reason for this is the company need to sell aggregates when weather conditions hamper mining and processing. Additionally, stock piling is needed to inventory for Florida with the anticipation of FDOT approval and increased export sales.

The current ratio can be misleading in both a positive and negative sense i.e. a high current ratio may not be good and a low ratio may not be bad. (Loth, n.d.) This is mainly because the underlying assumption of the ratio is looking at the company’s liquidation position instead of more practically looking at it as a going concern.

Gearing

This is gearing as it specifically relates to long term debt (due in excess of 12 months) due to third parties.

With no long term obligations, Jamaica Aggregates Limited has nil gearing. An all equity financed entity generally has a relatively highcost of capital in comparison to a geared entity. As debt is perceivedto be cheaper than equity, companies usually seek an optimal gearing level. On the face of it, Jamaica Aggregates Limited would appear to have the potential for increased debt capacity. However, financial assessments performed by various financial institutions, the latest in2012 done by Scotia Bank, have all resulted in an unwillingness to provide financing. The underlying reason for this being the annual losses experienced.

It is interesting to note, that as gearing is zero, there is a currentliability that has been increasing over the years. This is the management fees due to Lafarge.

Page 12 of 25

OBU Research & Analysis Project

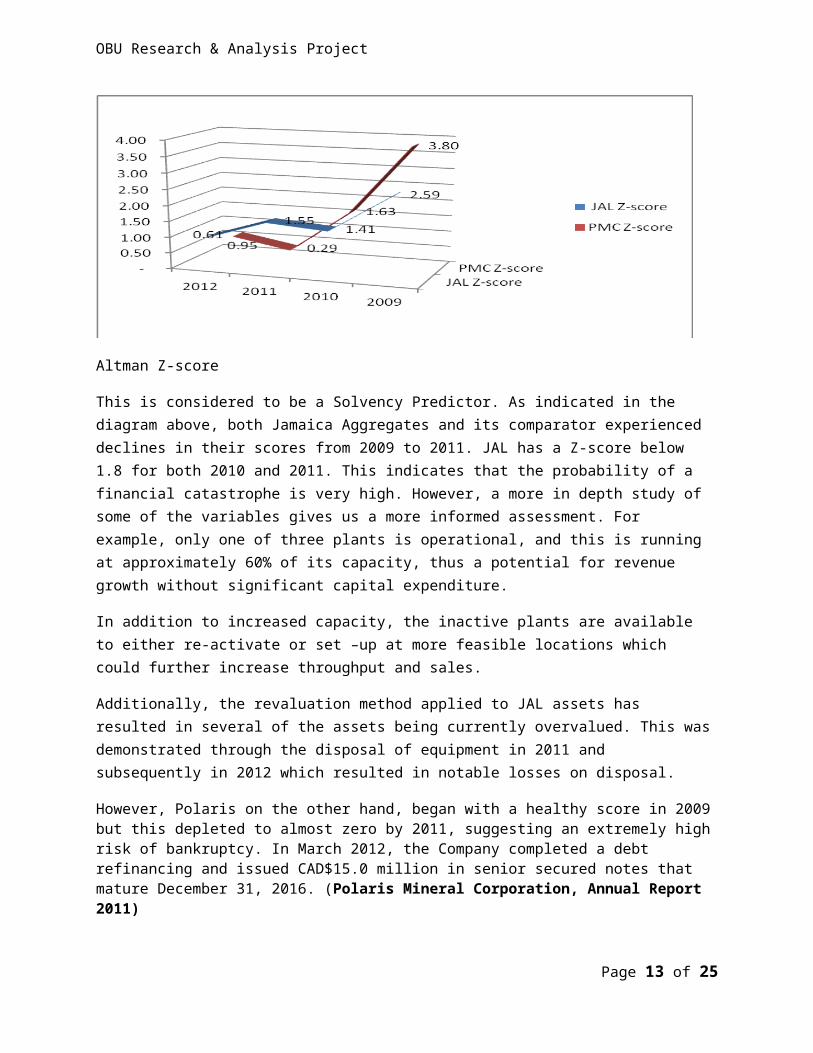

Altman Z-score

This is considered to be a Solvency Predictor. As indicated in the diagram above, both Jamaica Aggregates and its comparator experienced declines in their scores from 2009 to 2011. JAL has a Z-score below 1.8 for both 2010 and 2011. This indicates that the probability of a financial catastrophe is very high. However, a more in depth study of some of the variables gives us a more informed assessment. For example, only one of three plants is operational, and this is running at approximately 60% of its capacity, thus a potential for revenue growth without significant capital expenditure.

In addition to increased capacity, the inactive plants are available to either re-activate or set –up at more feasible locations which could further increase throughput and sales.

Additionally, the revaluation method applied to JAL assets has resulted in several of the assets being currently overvalued. This wasdemonstrated through the disposal of equipment in 2011 and subsequently in 2012 which resulted in notable losses on disposal.

However, Polaris on the other hand, began with a healthy score in 2009but this depleted to almost zero by 2011, suggesting an extremely highrisk of bankruptcy. In March 2012, the Company completed a debt refinancing and issued CAD$15.0 million in senior secured notes that mature December 31, 2016. (Polaris Mineral Corporation, Annual Report 2011)

Page 13 of 25

OBU Research & Analysis Project

Sales Volumes

2011 was deemed a recovery year throughout the industry. The business plan of December 2007 for JAL envisioned volumes growing from 1.5 million tonnes to approximately 3.4 million tonnes by 2011.

However, since 2006, the Sand and Gravel Mining industry's performancehas deteriorated sharply due to the unprecedented contraction in demand from residential and commercial construction markets. (Wilson, 2012).

At the time, target volumes were expected to be achieved through a combination of investment, operational improvements and a marketing focus. Presently, Paul Mountain and Martha Brae remain inactive. An additional mining facility on the North Coast is being sought. JamaicaPremix, JAL’s partner and largest customer, have had volumes well short of the initially projected volumes. Also, as the US aggregates and construction market is only now slowly recovering, exports were significantly below projections.

The delay in the Florida Department of Transport approval on the Yallahs aggregates has also been a major factor as to the difference in the actual vs. projected 2011 and 2012 volumes. The Business Plan was hinged mainly on having large exports to Florida.

In contrast, the comparator, Polaris, saw volumes increase from 1.42 million tonnes in 2009 to 1.73 million in 2011. (Polaris Mineral Corporation, Annual Report 2011)

Page 14 of 25

OBU Research & Analysis Project

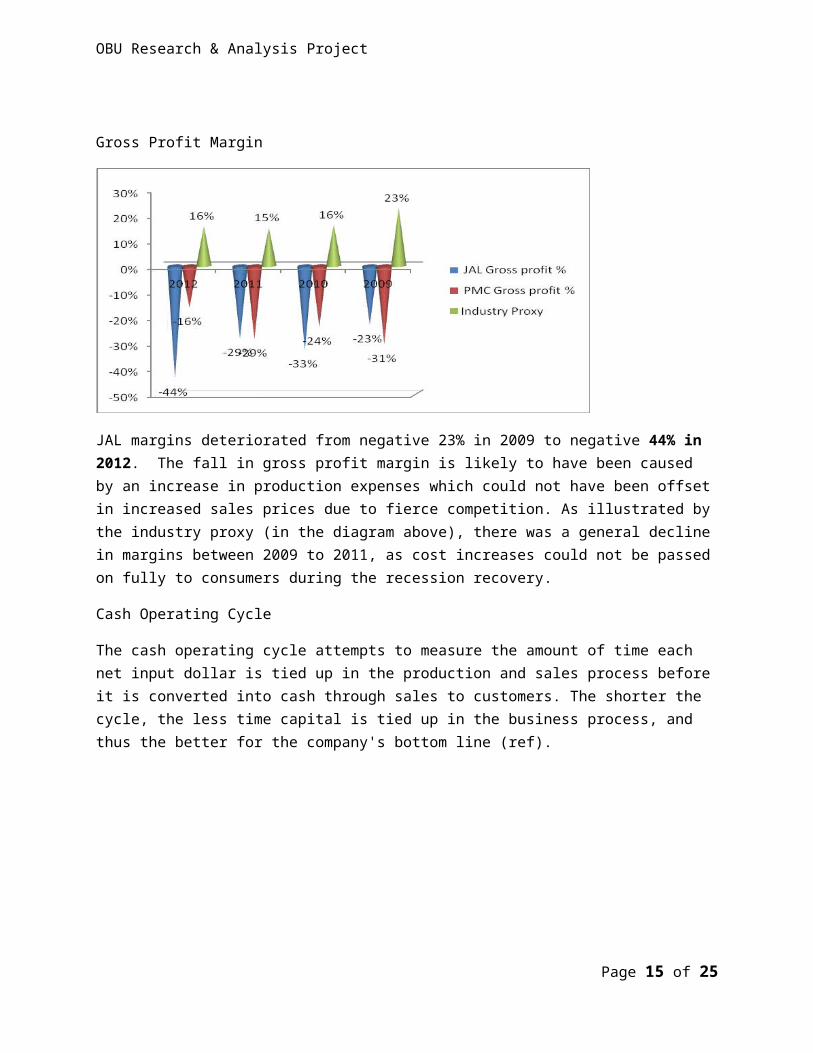

Gross Profit Margin

JAL margins deteriorated from negative 23% in 2009 to negative 44% in 2012. The fall in gross profit margin is likely to have been caused by an increase in production expenses which could not have been offsetin increased sales prices due to fierce competition. As illustrated bythe industry proxy (in the diagram above), there was a general declinein margins between 2009 to 2011, as cost increases could not be passedon fully to consumers during the recession recovery.

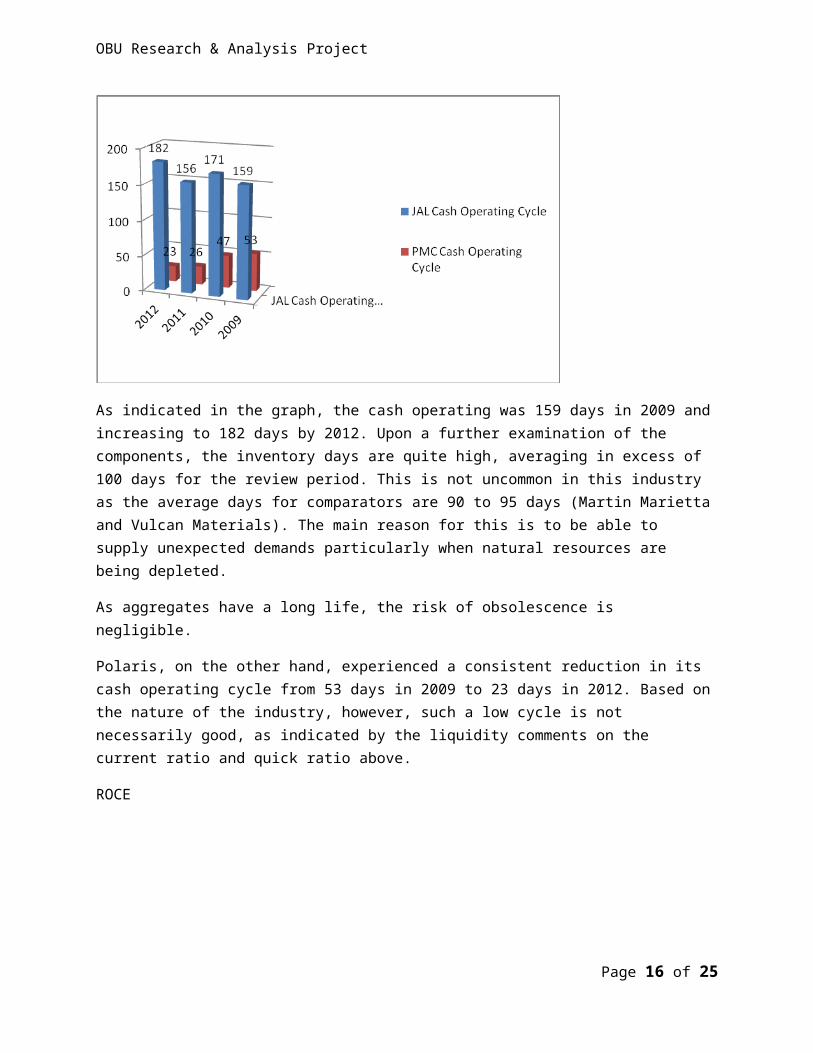

Cash Operating Cycle

The cash operating cycle attempts to measure the amount of time each net input dollar is tied up in the production and sales process beforeit is converted into cash through sales to customers. The shorter the cycle, the less time capital is tied up in the business process, and thus the better for the company's bottom line (ref).

Page 15 of 25

OBU Research & Analysis Project

As indicated in the graph, the cash operating was 159 days in 2009 andincreasing to 182 days by 2012. Upon a further examination of the components, the inventory days are quite high, averaging in excess of 100 days for the review period. This is not uncommon in this industry as the average days for comparators are 90 to 95 days (Martin Mariettaand Vulcan Materials). The main reason for this is to be able to supply unexpected demands particularly when natural resources are being depleted.

As aggregates have a long life, the risk of obsolescence is negligible.

Polaris, on the other hand, experienced a consistent reduction in its cash operating cycle from 53 days in 2009 to 23 days in 2012. Based onthe nature of the industry, however, such a low cycle is not necessarily good, as indicated by the liquidity comments on the current ratio and quick ratio above.

ROCE

Page 16 of 25

OBU Research & Analysis Project

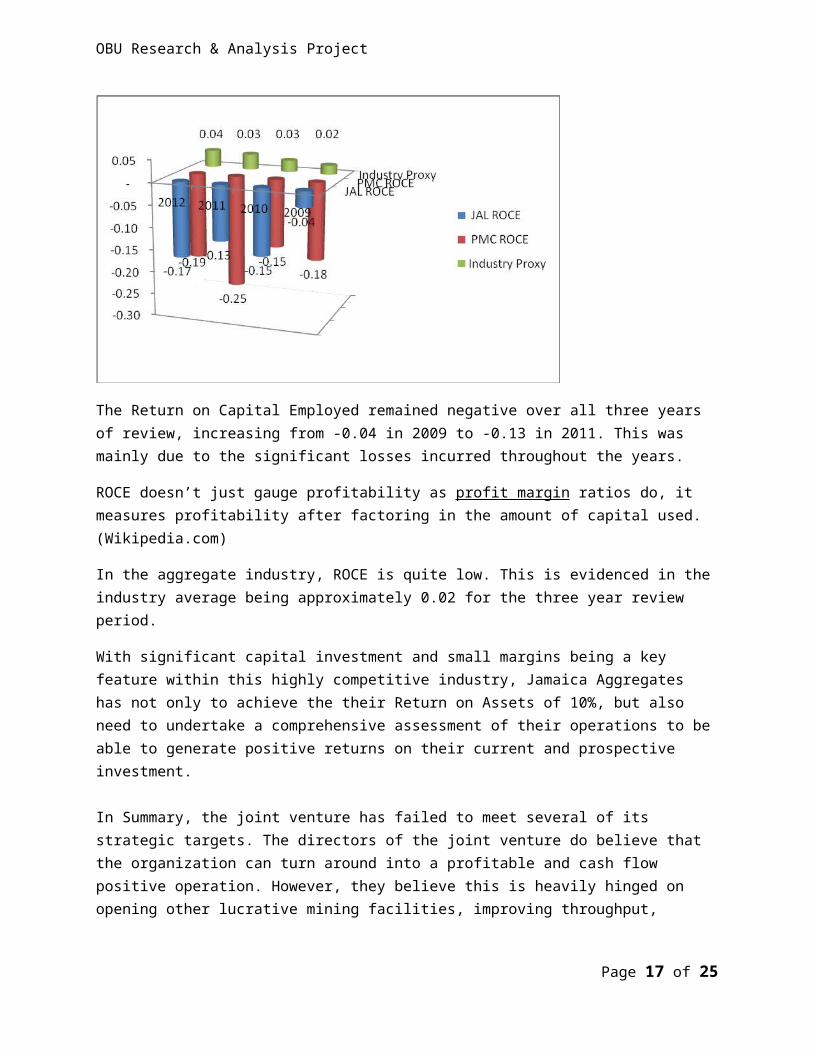

The Return on Capital Employed remained negative over all three years of review, increasing from -0.04 in 2009 to -0.13 in 2011. This was mainly due to the significant losses incurred throughout the years.

ROCE doesn’t just gauge profitability as profit margin ratios do, it measures profitability after factoring in the amount of capital used. (Wikipedia.com)

In the aggregate industry, ROCE is quite low. This is evidenced in theindustry average being approximately 0.02 for the three year review period.

With significant capital investment and small margins being a key feature within this highly competitive industry, Jamaica Aggregates has not only to achieve the their Return on Assets of 10%, but also need to undertake a comprehensive assessment of their operations to beable to generate positive returns on their current and prospective investment.

In Summary, the joint venture has failed to meet several of its strategic targets. The directors of the joint venture do believe that the organization can turn around into a profitable and cash flow positive operation. However, they believe this is heavily hinged on opening other lucrative mining facilities, improving throughput,

Page 17 of 25

OBU Research & Analysis Project

particularly sand throughput and building an export facility at Yallahs.

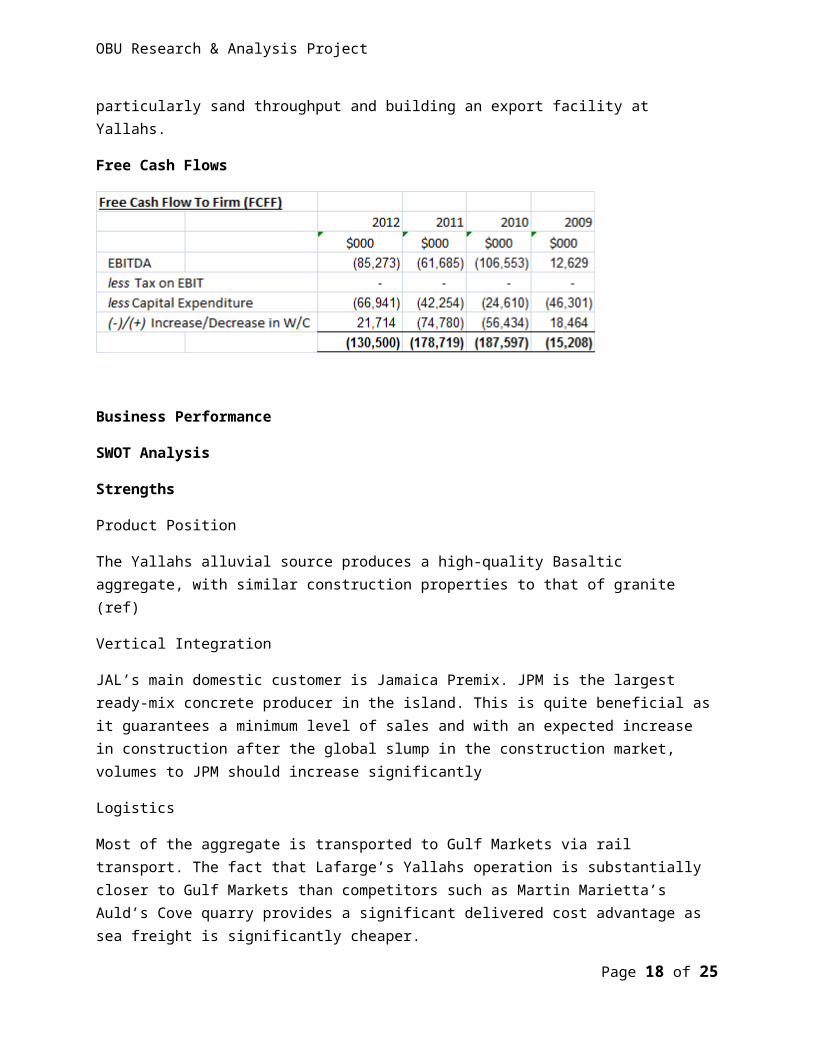

Free Cash Flows

Business Performance

SWOT Analysis

Strengths

Product Position

The Yallahs alluvial source produces a high-quality Basaltic aggregate, with similar construction properties to that of granite (ref)

Vertical Integration

JAL’s main domestic customer is Jamaica Premix. JPM is the largest ready-mix concrete producer in the island. This is quite beneficial asit guarantees a minimum level of sales and with an expected increase in construction after the global slump in the construction market, volumes to JPM should increase significantly

Logistics

Most of the aggregate is transported to Gulf Markets via rail transport. The fact that Lafarge’s Yallahs operation is substantially closer to Gulf Markets than competitors such as Martin Marietta’s Auld’s Cove quarry provides a significant delivered cost advantage as sea freight is significantly cheaper.

Page 18 of 25

OBU Research & Analysis Project

Cash Reserves

With a cash reserve position exceeding US$5 million at the end of 2011, JAL is in a fairly strong cash flow position, despite consistenttrading losses over the years.

Weaknesses

With the potential for significant growth in export sales, JAL only has access to a limited port facility, Jamaica Gypsum Quarry (JGQ). JGQ Dock cannot accommodate large vessels (maximum 10-20kt capacity). Distance is roughly 12 miles, but travel time is estimated at 1 hour under normal conditions. Maximum export tonnage from JGQ is 400-500kt due to loading inefficiencies (hauling). This situation can only be alleviated unless the strategic plan of 2008 is implemented i.e. building a port facility at Yallahs. However, there are many challenges with this, the major being capital funding.

No formalized marketing strategy has been implemented to boost domestic aggregate sales. This has resulted in Sales volume over the review period remaining relatively flat despite several new projects and in particular those awarded to China Harbour.

There is complete reliance on the Yallahs Plant for aggregates supply.Thus has resulted in significant opportunity costs. As the demand for sand is high, daily production of sand is usually sold out preventing stockpiling. So whenever there is a breakdown or routine maintenance of production equipment, aggregate sales particularly sand are lost.

Several of the critical strategic issues highlighted in the company’s business plan are off target. Of these are:

1. Developing a waterborne shipping facility at Yallahs –remains at discussion stage

2. Enhance market position through development of two additional sites - Only Yallahs plant operational to date

3. Volume targets increasing to 3.4 million tonnes by 2011 – Actual 2011 volume being a mere 18% of this target

Page 19 of 25

OBU Research & Analysis Project

Opportunities

Volume Growth

The two most lucrative sections for aggregate consumption within the domestic market is Kingston and Montego Bay. The Yallahs facility supplies Kingston and its environs. However, JAL has no strong presence on the North Coast. This market can be pursued and feasibility studies were ongoing during 2012 to establish a processingplant on that section of the island.

Florida is one of the three fastest growing markets in the U.S. MartinMarietta supplied approximately 1 million tons of aggregate to customers within the first six months of 2011. However, many asphalt players are looking for an alternative source of supply. Due to the lack of suitable material in the Gulf Coast region, customers are willing to purchase from more than one source. Therefore, the advantage of supplying surface- course aggregate not only presents itself in the opportunity to grow margins, but as an opportunity to grow demand.(ref)

Lafarge also being a major player in the United States concrete and aggregates market has started purchasing from Yallahs and this could increase exponentially once the Florida Department Of Transport (FDOT)approval is received.

Alternative Revenue

As the demand for limestone increases due to its price being 30 – 40% below that of other rock, JAL could capitalize on this demand by setting up processing facilities

Threats

The primary threat is the potential of the Cuban Economic Embargo being lifted. This is due to the substantial reserves of Granite, Basalt, and Dolomite Limestone that are known to exist in Cuba. However, operations being developed to deliver exports to the U.S. aredependent upon environmental, mining and trade restrictions Cuba may impose. (ref). This would present a significant competition for marketshare.

Page 20 of 25

OBU Research & Analysis Project

Continued failure to realize a positive return on assets and free cashflows has resulted in a rapid reduction in cash and cash equivalents threatening the company’s viability. As an example, as per business plan, Lafarge contributed US$11.5 million of which US$6.5 million was to be allocated to the Yallahs Loadout shipping facility. No investment has been made on this facility, whilst the cash and cash equivalents stood at just over U$$5 million at the end of 2011 and declined by a further US$1.8m by November 2012.

Limestone production poses another problem. As limestone processing ischeaper, many customers are opting to purchase limestone.

The cost per tonne produced continues to present a challenge. Competition is quite strong as JAL’s neighbor, Coast-to-Coast aggregates prices are approximately J$30 - $50 less per tonne. However, the cost of production continues to exceed the revenues before deducting repairs and maintenance and other operating expenses.A reason for this, however, is due to charges on the inactive plants at Martha Brae and Paul Mountain in the form of depreciation and insurance.

Another consistent threat is illegal mining operators. Such persons continue to mine in the Yallahs River without permits, lease payments are operational overheads borne by registered operators (such as mining taxes and other statutory deductions)

Barriers are moderate as environmental regulations are stringent and prevent new operations from being developed. However, lack of industrial standards makes developing a small operation fairly inexpensive. (Aggregate Production & Supply, Exeter)

Natural Resource Depletion

As Jamaica Aggregates Limited currently has one active mining operation, the availability of natural resources is a critical factor.With not much rain during the typical hurricane seasons over the last three years, these resources are being depleted rapidly. Unless a significant weather event (storm, depression or the like) occurs, thenalternative locations will be needed to process sand and gravel.

Page 21 of 25

OBU Research & Analysis Project

Harbour View Weighing Station

A station for weighing all the haulage trucks commuting between the eastern section of the island and the capital Kingston has been a workin progress during the review period and was subsequently made operational late in 2012.

The long standing culture of haulage contractors in Jamaica is that they haul up to double the manufacturers recommended capacity. This iswhat their rates are based upon, notwithstanding a minimal margin after covering operational expenses.

The weighing station will enforce compliance with the legal weight limits, thus reducing the hauler’s income per trip by 40 – 50%.

This will thus result in a significant rate increase which may be detrimental to sales volumes. The aggregates industry, locally and globally, is highly competitive with efficiencies in achieving low haulage costs being a critical success factor. Profit margins are low and cost increases generally have to be staggered when passing on to the consumer.

The introduction of the scale on the eastern end of the island only, will render the price of aggregates into the city uncompetitive with the other quarries in other sections of the island.

An increase in the haulage rates would also result in a reduction or possible elimination of exports in the Caribbean and potential exportsto the United States.

Liquidity

The continuous losses not only highlights a weakness but poses a real threat to a potential going concern problem if the company’s profitability and liquidity position are not improved during the near foreseeable future.

Industry Leader Benchmark

Vulcan Materials is an industry leader, whilst Jamaica Aggregates is alocal leader. Vulcan implements the following business strategy

Page 22 of 25

OBU Research & Analysis Project

1. Aggregate focus

- Build and hold substantial reserves; As only the Yallahs plant is active, reserves are critical in order to take advantage of potential export and local sales. This is highly possible as the plant is set up at the Yallahs river where the raw materials are mined from owned and leased lands. Our joint venture partner (Jamaica Premix Limited – concrete producer) predominantly uses Yallahs produced aggregates. This fact is reflected in Jamaica Premix’s 74% and 61% of total aggregates purchased in 2011 and 2012 respectively being from the Yallahs Plant.

- Take advantage of being the largest producer; Although Jamaica Aggregates only produces from the Yallahs Plant, it is arguably the largest aggregates distributor on the island. Additionally, as the Yallahs reserves have one of the finest quality in the region, it provides a competitive edge over other local quarries.

2. Coast-to-Coast Footprint

- Vulcan pursues this strategy by maintaining a visible presence in geographical areas that are anticipated to grow rapidly.(ref)

- Jamaica Aggregates Limited has no active marketing strategy and mainly relies on its long standing reputation. Efforts are being made to address this. Additionally, as mentioned earlier, the entity is actively seeking to set up a processing plant on the Northern end of the island. This would enable a significant coast-to coast footprint.

3. Profitable Growth

- Strategic Acquisitions; Jamaica Aggregates has done no such transaction over the review period

- Re-investment opportunities with high returns; only one non-core income generating activity is worth mentioning. This relates to an interest bearing US$ fixed deposit. However, the returns generated year-on-year is significantly declining as the investment amounts are been diverted to fill the shortfall in operational cash flows.

Page 23 of 25

OBU Research & Analysis Project

4. Focus on cost reduction

- As the aggregates industry is highly competitive, cost reduction is vital. At this end, as per Vulcan Annual Report 2011, their “knowledgeable and experienced workforce…flexible production capabilities” have allowed them to manage costs.. There is significant room for improvement in this regard as it relates to Jamaica Aggregates Limited. A recent breakeven analysis that I performed shows the following:

a. At current pricing, the annual breakeven is approximately 1.3 million tonnes.

b. 2009 to 2012 averaged 0.51 million tonnes per annum

c. As local competition increases, the main potential for growth in sales volume is in the export segment. This is demonstrated in the local prices versus international prices. The average price per tonne of aggregate regionally is US$10.25, whereas locally the average price is US$7.40. The average manufacturing cost per tonne being US$8.10 further highlights the focus on exports.

d. Negative Gross margins over the period illustrate a need to analyse the cost elements and take immediate steps the control and/or reduce expenditure. The Vulcan report mentions “cost reduction steps…in 2011…additional reductions in workforce, adjusted plant operating hours and divested operations in non-strategic markets”. These are areas that the company may need to explore in the very near future

5. Effective Land Management

To this end, Vulcan’s Annual Report states “ we believe that effective land management is both a business strategy and a social responsibility…we strive to achieve a balance between the value we create through our mining activities and the value we create through effective post-mining land management”. Jamaica Aggregates have done commendable in this regard

CONCLUSION

Page 24 of 25

OBU Research & Analysis Project

Overall, Jamaica Aggregates has performed below investors’ expectations over the review period. Sustained losses, reliance on oneprocessing plant for production, ageing equipment and declining cash flows are the major areas of concern. However, it is not all doom and gloom as the Yallahs facility has unused capacity, The Florida Department of Transport approval has been finalized which now opens the door for significant exports to Florida.

Additionally, the entity has the wherewithal to set up other processing plants without significant capital injection as there are currently two idle processing plants.

In concluding, future success of the entity is underpinned by a few variables, namely, a focus on cost reduction, increased throughput, significant increase in export volumes and a boom in the construction industry particularly in the United States and the Caribbean.

Page 25 of 25

Related Documents