Dow at 16,000: Fully Valued Stocks are now fully valued. According to the Trefis Dow— an average of the intrinsic value of all 30 Dow companies—stocks sit just about where they should. Does this mean the end of gains? No, but it does mean to expect only the dividend yield plus dividend growth rate going forward (at least on the broad indices such as the Dow and S&P 500), all of which adds up to 7%-9%. This will still seem like manna from heaven compared the return on bonds and cash. Opportunities will still abound in undervalued companies, the unloved and orphaned names that the average investor has given up for adoption. Our job is to keep looking. A cynical view is justified. After all, some ragamuffins are banished for good reason. Sorting out babies and bathwater is the only way to find the one foundling with unappreciated promise. Looking at the Dow itself is a good place to start. The index in aggregate may be fully valued, but some individual values can hide in plain sight. The most undervalued Dow component is IBM, at an appealing 25.6% discount to an estimated intrinsic value of $230: A Trefis Interactive Portfolio Report March 2014 James Berman James Berman, the president and founder of JBGlobal.com LLC, a registered investment advisory firm (SEC registered), specializes in asset management for high-net-worth indi- viduals and trusts. Mr. Berman is a faculty member in the Finance Department of NYU SCPS. He has appeared on CNBC and the Fox Business Channel and has been quoted and published in a variety of publications, including Barron's, Fortune, Bloomberg, The Huffington Post and CNN Money. Mr. Berman holds a B.A., Magna Cum Laude, Phi Beta Kappa, in English & American Literature from Harvard and a J.D. from Harvard Law School. CONTENTS Access interactive Trefis analysis to get the most from the Folio: Test our assumptions Run your own scenarios Read forecast rationale Access Trefis research Analyze company value drivers THE BERMAN VALUE FOLIO Dow at 16,000: Fully Valued 1 IBM: An Undervalued Corner of the Dow 3 Company Highlights 5 eBay 5 Arcelor-Mittal 6 CSX 7 Expedia 8 The Berman Value Folio 9

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Dow at 16,000: Fully Valued

Stocks are now fully valued. According to the Trefis Dow— an average of the intrinsic value of all 30 Dow companies—stocks sit just about where they should.

Does this mean the end of gains?

No, but it does mean to expect only the dividend yield plus dividend growth rate going forward (at least on the broad indices such as the Dow and S&P 500), all of which adds up to 7%-9%. This will still seem like manna from heaven compared the return on bonds and cash.

Opportunities will still abound in undervalued companies, the unloved and orphaned names that the average investor has given up for adoption. Our job is to keep looking. A cynical view is justified. After all, some ragamuffins are banished for good reason. Sorting out babies and bathwater is the only way to find the one foundling with unappreciated promise.

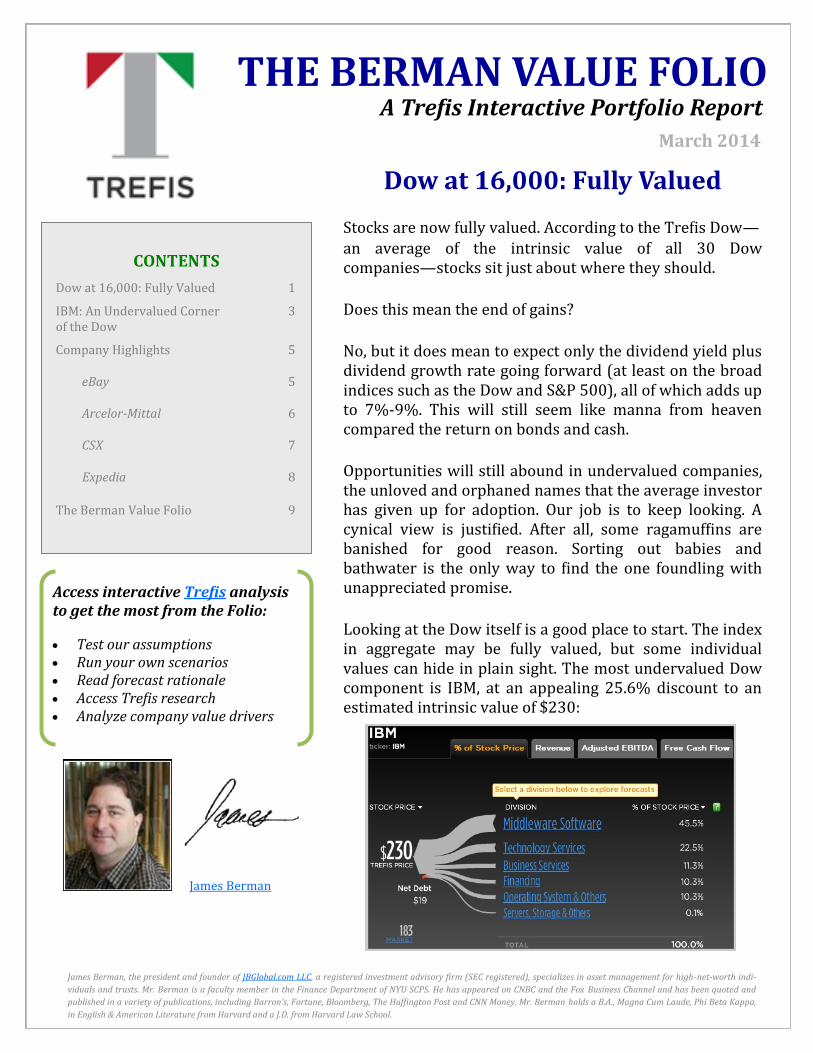

Looking at the Dow itself is a good place to start. The index in aggregate may be fully valued, but some individual values can hide in plain sight. The most undervalued Dow component is IBM, at an appealing 25.6% discount to an estimated intrinsic value of $230:

A Trefis Interactive Portfolio Report

March 2014

James Berman

James Berman, the president and founder of JBGlobal.com LLC, a registered investment advisory firm (SEC registered), specializes in asset management for high-net-worth indi-

viduals and trusts. Mr. Berman is a faculty member in the Finance Department of NYU SCPS. He has appeared on CNBC and the Fox Business Channel and has been quoted and

published in a variety of publications, including Barron's, Fortune, Bloomberg, The Huffington Post and CNN Money. Mr. Berman holds a B.A., Magna Cum Laude, Phi Beta Kappa,

in English & American Literature from Harvard and a J.D. from Harvard Law School.

CONTENTS

Access interactive Trefis analysis to get the most from the Folio:

Test our assumptions Run your own scenarios Read forecast rationale Access Trefis research Analyze company value drivers

THE BERMAN VALUE FOLIO

Dow at 16,000: Fully Valued 1

IBM: An Undervalued Corner of the Dow

3

Company Highlights 5

eBay 5

Arcelor-Mittal 6

CSX 7

Expedia 8

The Berman Value Folio 9

IBM is that perpetual tech survivor. One of the few that zigged when they needed to zig (with the occasional zag if necessary), IBM was a pioneering PC-maker after building its reputation in mainframes, but astutely sold the dying, commodified desktop business to China’s Lenovo in 2004. After former CEO John Akers took some rare wrong turns in the eighties, Lou Gerstner and then Sam Palmisano righted this iconic company. Now Virginia Rometty presides over a multinational that leads in IT hardware, software and outsourcing. Rometty has continued the Palmisano strategy of divesting low margin hardware businesses with the sale of its System X server business to Lenovo for $2.3 billion.

Certain features distinguish IBM: it’s one of the few long-lived survivors in a tech graveyard full of obsolete, formerly important brands. It has distinguished itself in measures of corporate transparency and shareholder rights, earning an unusual “exemplary” rating in stewardship from Morningstar. Yet its stock price has underperformed the S&P 500 by 31% over the past year, and by 8% annually over the past three years.

I get interested when a high quality company trails the S&P for long periods of time. It could mean protracted fundamental problems. But it could also indicate a company out of fashion with traders, trading at a juicy discount to its real value.

With IBM, which is it?

Warren Buffett announced a purchase of IBM in 2011, a rare bid for technology from a guy who has resolutely shunned the internet and software companies due to their potential for instant obsolescence. Either IBM is different or Buffett is losing his marbles. In his annual shareholder letter, Buffett praised IBM for setting tough goals and actually meeting them—a rare quality in large companies.

The real distinction, however, was IBM’s new reality as a services company—one that has customer relationships with embedded switching costs. As Buffett made clear, clients of IT companies are loathe to switch horses, given that it’s always midstream in the world of global business.

The Berman Value Folio A Trefis Interactive Portfolio Report

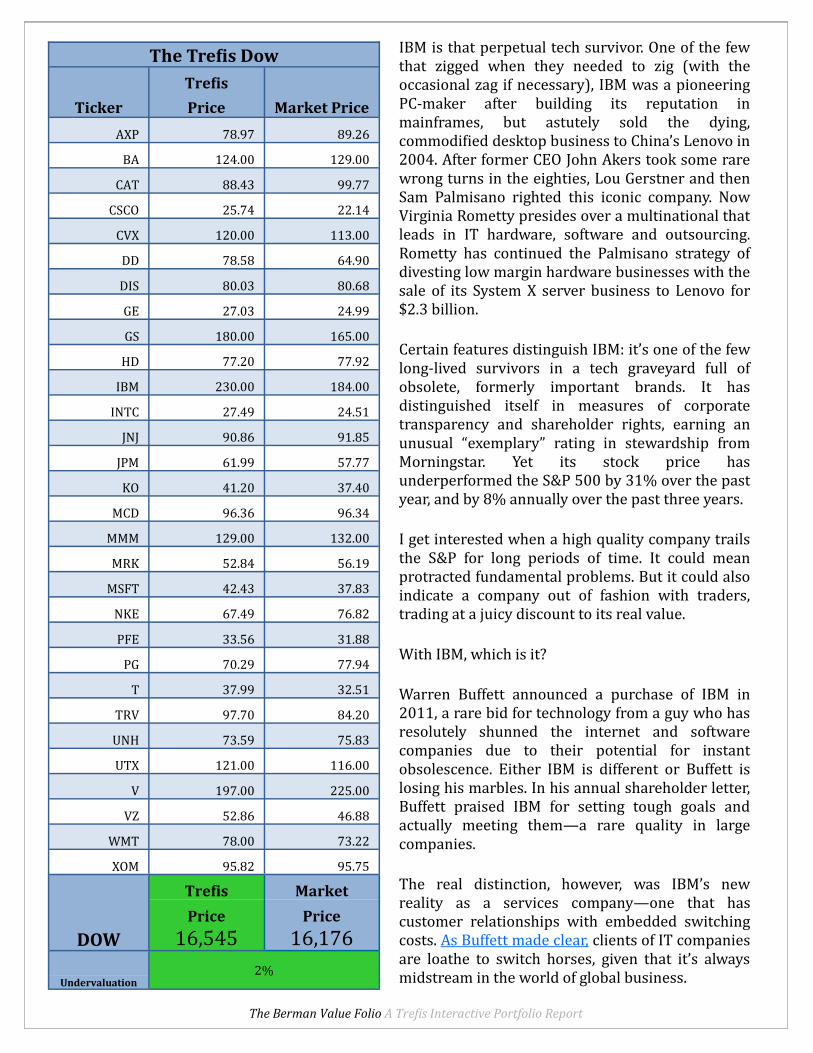

The Trefis Dow

Ticker

Trefis

Market Price Price

AXP 78.97 89.26

BA 124.00 129.00

CAT 88.43 99.77

CSCO 25.74 22.14

CVX 120.00 113.00

DD 78.58 64.90

DIS 80.03 80.68

GE 27.03 24.99

GS 180.00 165.00

HD 77.20 77.92

IBM 230.00 184.00

INTC 27.49 24.51

JNJ 90.86 91.85

JPM 61.99 57.77

KO 41.20 37.40

MCD 96.36 96.34

MMM 129.00 132.00

MRK 52.84 56.19

MSFT 42.43 37.83

NKE 67.49 76.82

PFE 33.56 31.88

PG 70.29 77.94

T 37.99 32.51

TRV 97.70 84.20

UNH 73.59 75.83

UTX 121.00 116.00

V 197.00 225.00

VZ 52.86 46.88

WMT 78.00 73.22

XOM 95.82 95.75

DOW

Trefis Market

Price Price

16,545 16,176 2%

Undervaluation

IBM: An Undervalued Corner of the Dow

The Berman Value Folio A Trefis Interactive Portfolio Report

For skeptics of IBM’s dominance, a glance at returns on equity (ROE) provides black and white reassurance. Over the past five years, IBM has achieved a stunning 71% annually. ROE measures “performance per shareholder dollar,” a better way to measure corporate success than earnings growth. IBM’s supercharged ROE has been generated not only by growing the numerator (strong operating income growth)—but also by shrinking the denominator (slimming shareholders’ equity via extensive share buybacks). Shares outstanding decline with each repurchase. As the pie grows, the pie also gets sliced into fewer pieces. There is no more beautiful combination for the equity owner.

A less impressive reason for IBM’s high ROE is its relatively high leverage. While many tech firms have negligible debt levels, IBM has over $33 billion in debt backed by a modest $11 billion in cash. As borrowing shrinks net equity, IBM’s debt-to-equity ratio has grown to 1.43, substantially higher than that of tech peers like Intel (INTC), Apple (AAPL) and Microsoft (MSFT), all of whom enjoy ratios under 0.25. Yet, IBM is not overleveraged by any means. Free cash flow of $13.8 billion covers net interest expense of only $400 million. You could say that IBM is properly leveraged while most of Silicon Valley is underleveraged. It’s a sign of IBM’s pragmatic temperament, commitment to shareholder rights and mature bearing that it commits so much money to buying back stock. And doing so at these prices is likely to add value. IBM trades at only 9 times forward earnings.

One reason that IBM’s stock has lagged is the dominance of cloud computing, which Big Blue has been slow to embrace. Cloud computing is at once IBM’s great danger and outstanding opportunity. By converting its existing software customers to the cloud, IBM may forsake rich initial set-up and consulting fees. But as Robert LeBlanc, SVP for software and cloud solutions explained to the New York Times, margins can remain attractive, even as revenue declines, due to the lower administrative costs needed to maintain the cloud. Arguably, customer switching costs remain high for cloud-based software solutions, one reason that software-as-a-service companies command such high multiples.

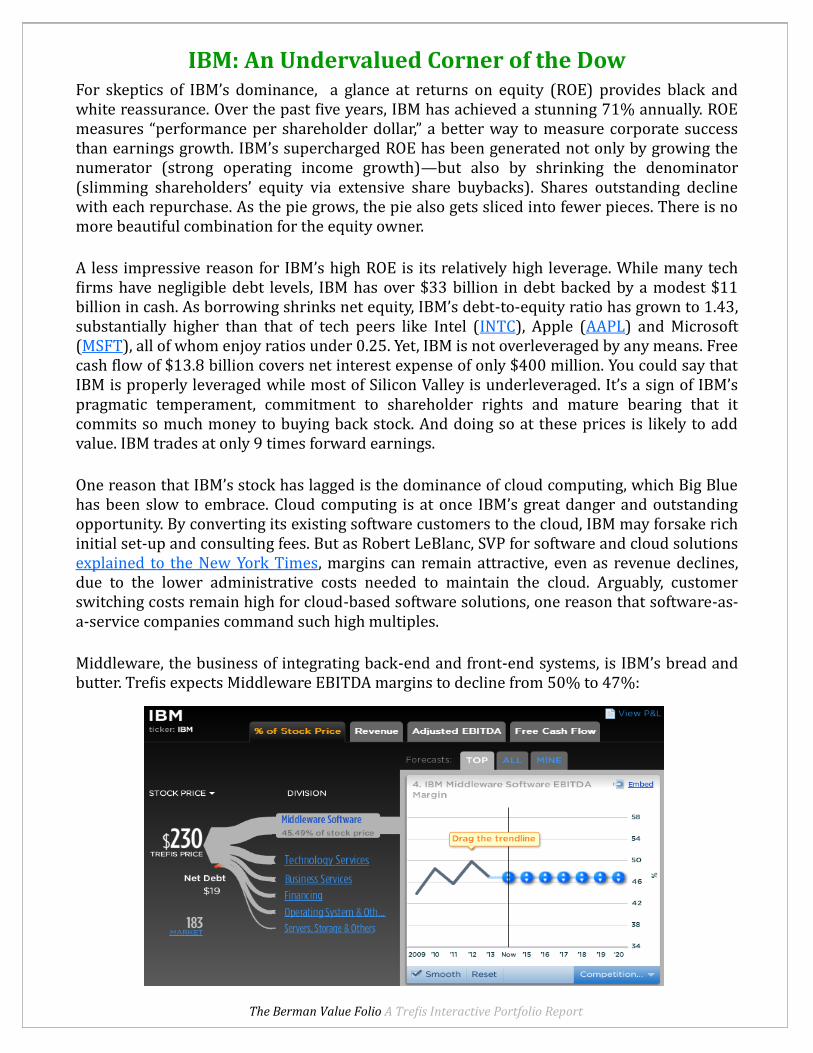

Middleware, the business of integrating back-end and front-end systems, is IBM’s bread and butter. Trefis expects Middleware EBITDA margins to decline from 50% to 47%:

Stress Testing IBM for the Cloud

The Berman Value Folio A Trefis Interactive Portfolio Report

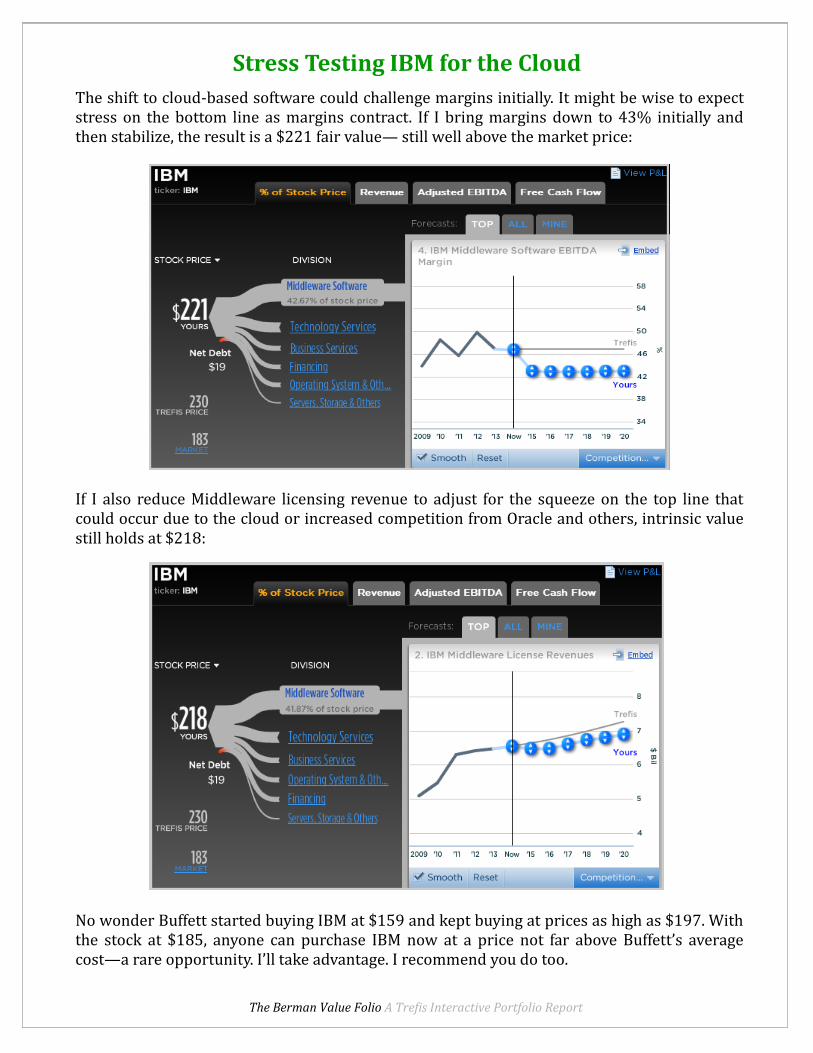

The shift to cloud-based software could challenge margins initially. It might be wise to expect stress on the bottom line as margins contract. If I bring margins down to 43% initially and then stabilize, the result is a $221 fair value— still well above the market price:

If I also reduce Middleware licensing revenue to adjust for the squeeze on the top line that could occur due to the cloud or increased competition from Oracle and others, intrinsic value still holds at $218:

No wonder Buffett started buying IBM at $159 and kept buying at prices as high as $197. With the stock at $185, anyone can purchase IBM now at a price not far above Buffett’s average cost—a rare opportunity. I’ll take advantage. I recommend you do too.

COMPANY HIGHLIGHTS

eBay

eBay (EBAY) is under pressure from activist investor Carl Icahn to spinoff PayPal, the most val-uable of the company’s divisions. CEO John Donahoe maintains that PayPal is best left in-house due to synergies with the EBAY auction platform. Icahn has ratcheted up the rhetoric many notches, parrying that Donahoe is “completely asleep or, even worse, either naï ve or willingly blind,” and alleging various conflicts of interest at EBAY’s board. The conflicts he points to could be material, and might explain a reluctant attitude on some board members to cast off PayPal. It could also just be smoke and mirrors designed to exert pressure. I agree with Icahn that PayPal, as the fastest growing and most lucrative piece of EBAY, would have its value best recognized outside the parent company. Payment platforms command high valuations and Pay-Pal is one of the best. Icahn is abrasive and impatient, but sometimes you have to love the guy.

Trefis Key Drivers:

eBay posted double-digit growth in Q4 2013 in both of its key segments - marketplaces and PayPal - despite weaker-than-expected e-commerce growth during the holiday season in the U.S. PayPal gained roughly 5.2 million active accounts in Q4, which was the highest quarterly gain of the year. Total payment volume was up by 25%, but the take rate declined slightly, resulting in revenue growth of 19%. The company plans to step up investment in PayPal in 2014, which could affect its cash flows in the short run, but should help the business maintain solid revenue growth globally as the payment market becomes increasingly competitive.

The Berman Value Folio A Trefis Interactive Portfolio Report

Market Capitalization

Annual Revenues Dividend/Yield 52 Week Range

$76.5 B $16.1 B N/A $48.06—59.27

COMPANY HIGHLIGHTS

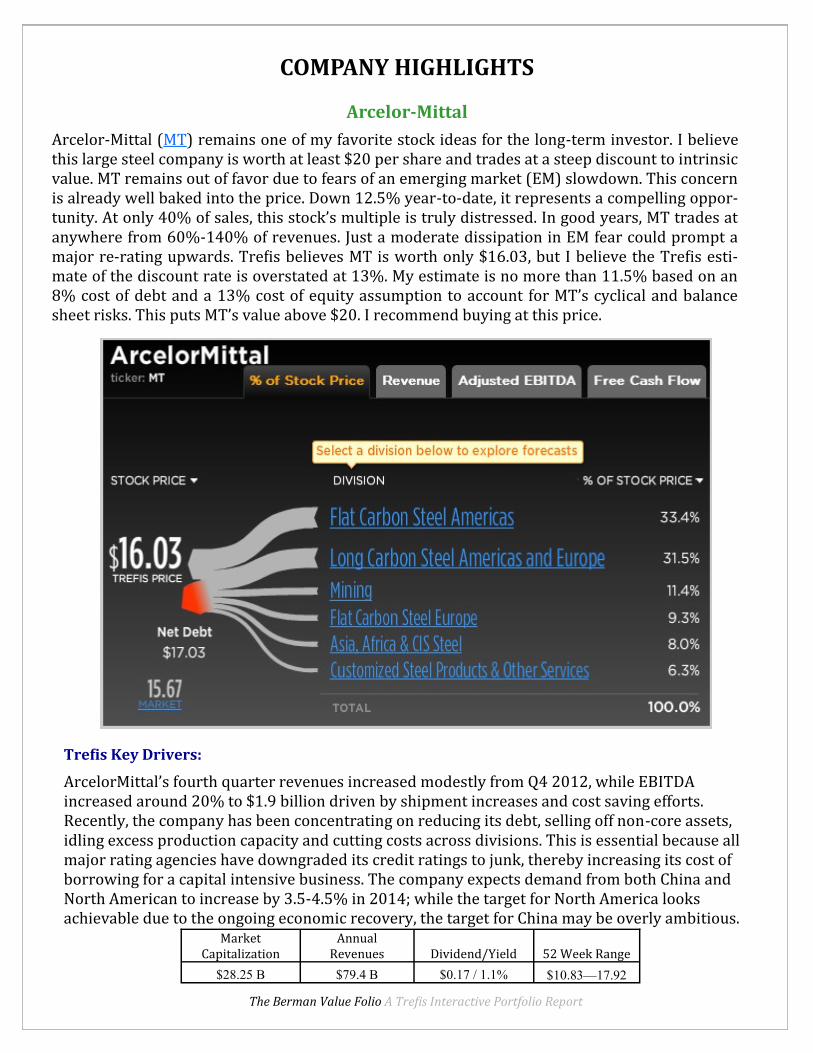

Arcelor-Mittal

Arcelor-Mittal (MT) remains one of my favorite stock ideas for the long-term investor. I believe this large steel company is worth at least $20 per share and trades at a steep discount to intrinsic value. MT remains out of favor due to fears of an emerging market (EM) slowdown. This concern is already well baked into the price. Down 12.5% year-to-date, it represents a compelling oppor-tunity. At only 40% of sales, this stock’s multiple is truly distressed. In good years, MT trades at anywhere from 60%-140% of revenues. Just a moderate dissipation in EM fear could prompt a major re-rating upwards. Trefis believes MT is worth only $16.03, but I believe the Trefis esti-mate of the discount rate is overstated at 13%. My estimate is no more than 11.5% based on an 8% cost of debt and a 13% cost of equity assumption to account for MT’s cyclical and balance sheet risks. This puts MT’s value above $20. I recommend buying at this price.

Trefis Key Drivers:

ArcelorMittal’s fourth quarter revenues increased modestly from Q4 2012, while EBITDA increased around 20% to $1.9 billion driven by shipment increases and cost saving efforts. Recently, the company has been concentrating on reducing its debt, selling off non-core assets, idling excess production capacity and cutting costs across divisions. This is essential because all major rating agencies have downgraded its credit ratings to junk, thereby increasing its cost of borrowing for a capital intensive business. The company expects demand from both China and North American to increase by 3.5-4.5% in 2014; while the target for North America looks achievable due to the ongoing economic recovery, the target for China may be overly ambitious.

The Berman Value Folio A Trefis Interactive Portfolio Report

Market Capitalization

Annual Revenues Dividend/Yield 52 Week Range

$28.25 B $79.4 B $0.17 / 1.1% $10.83—17.92

COMPANY HIGHLIGHTS

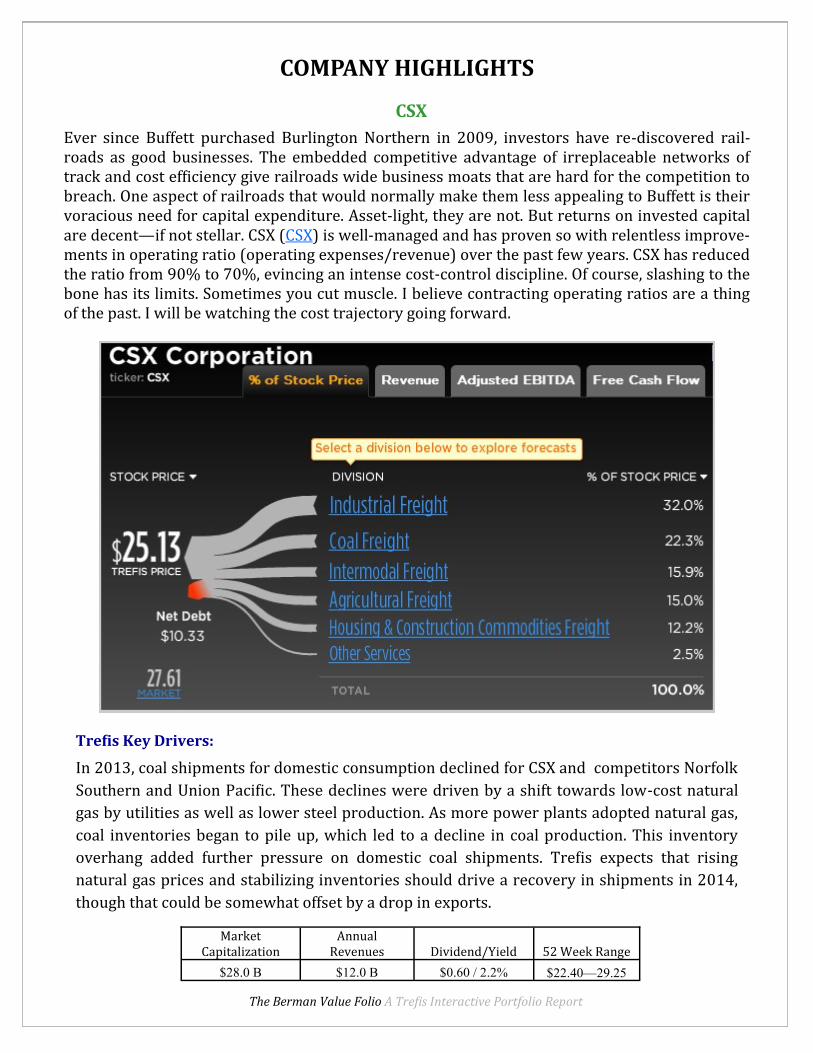

Ever since Buffett purchased Burlington Northern in 2009, investors have re-discovered rail-roads as good businesses. The embedded competitive advantage of irreplaceable networks of track and cost efficiency give railroads wide business moats that are hard for the competition to breach. One aspect of railroads that would normally make them less appealing to Buffett is their voracious need for capital expenditure. Asset-light, they are not. But returns on invested capital are decent—if not stellar. CSX (CSX) is well-managed and has proven so with relentless improve-ments in operating ratio (operating expenses/revenue) over the past few years. CSX has reduced the ratio from 90% to 70%, evincing an intense cost-control discipline. Of course, slashing to the bone has its limits. Sometimes you cut muscle. I believe contracting operating ratios are a thing of the past. I will be watching the cost trajectory going forward.

Trefis Key Drivers:

In 2013, coal shipments for domestic consumption declined for CSX and competitors Norfolk

Southern and Union Pacific. These declines were driven by a shift towards low-cost natural

gas by utilities as well as lower steel production. As more power plants adopted natural gas,

coal inventories began to pile up, which led to a decline in coal production. This inventory

overhang added further pressure on domestic coal shipments. Trefis expects that rising

natural gas prices and stabilizing inventories should drive a recovery in shipments in 2014,

though that could be somewhat offset by a drop in exports.

The Berman Value Folio A Trefis Interactive Portfolio Report

CSX

Market Capitalization

Annual Revenues Dividend/Yield 52 Week Range

$28.0 B $12.0 B $0.60 / 2.2% $22.40—29.25

COMPANY HIGHLIGHTS

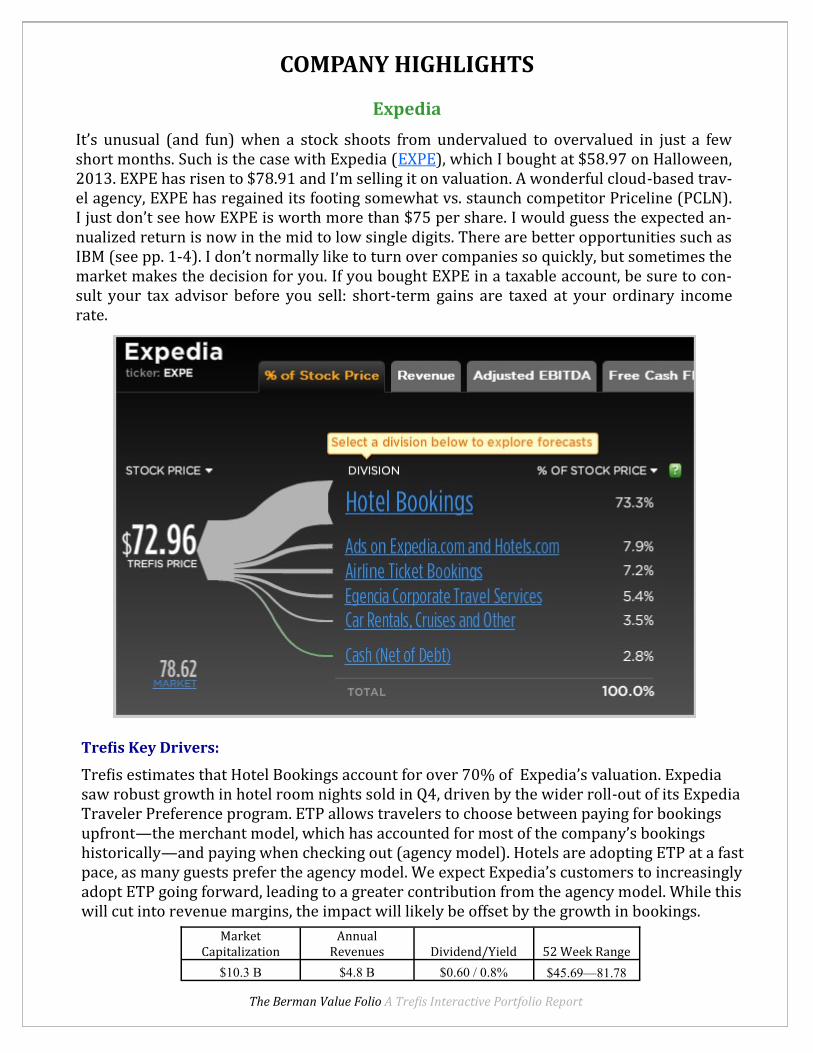

Expedia

It’s unusual (and fun) when a stock shoots from undervalued to overvalued in just a few short months. Such is the case with Expedia (EXPE), which I bought at $58.97 on Halloween, 2013. EXPE has risen to $78.91 and I’m selling it on valuation. A wonderful cloud-based trav-el agency, EXPE has regained its footing somewhat vs. staunch competitor Priceline (PCLN). I just don’t see how EXPE is worth more than $75 per share. I would guess the expected an-nualized return is now in the mid to low single digits. There are better opportunities such as IBM (see pp. 1-4). I don’t normally like to turn over companies so quickly, but sometimes the market makes the decision for you. If you bought EXPE in a taxable account, be sure to con-sult your tax advisor before you sell: short-term gains are taxed at your ordinary income rate.

Trefis Key Drivers:

Trefis estimates that Hotel Bookings account for over 70% of Expedia’s valuation. Expedia saw robust growth in hotel room nights sold in Q4, driven by the wider roll-out of its Expedia Traveler Preference program. ETP allows travelers to choose between paying for bookings upfront—the merchant model, which has accounted for most of the company’s bookings historically—and paying when checking out (agency model). Hotels are adopting ETP at a fast pace, as many guests prefer the agency model. We expect Expedia’s customers to increasingly adopt ETP going forward, leading to a greater contribution from the agency model. While this will cut into revenue margins, the impact will likely be offset by the growth in bookings.

The Berman Value Folio A Trefis Interactive Portfolio Report

Market Capitalization

Annual Revenues Dividend/Yield 52 Week Range

$10.3 B $4.8 B $0.60 / 0.8% $45.69—81.78

Total return is calculated since inception date of 12/21/2011 and includes reinvested dividends. When a stock is bought in the portfolio, it is added on an equal cash-weighted basis at the time of purchase.

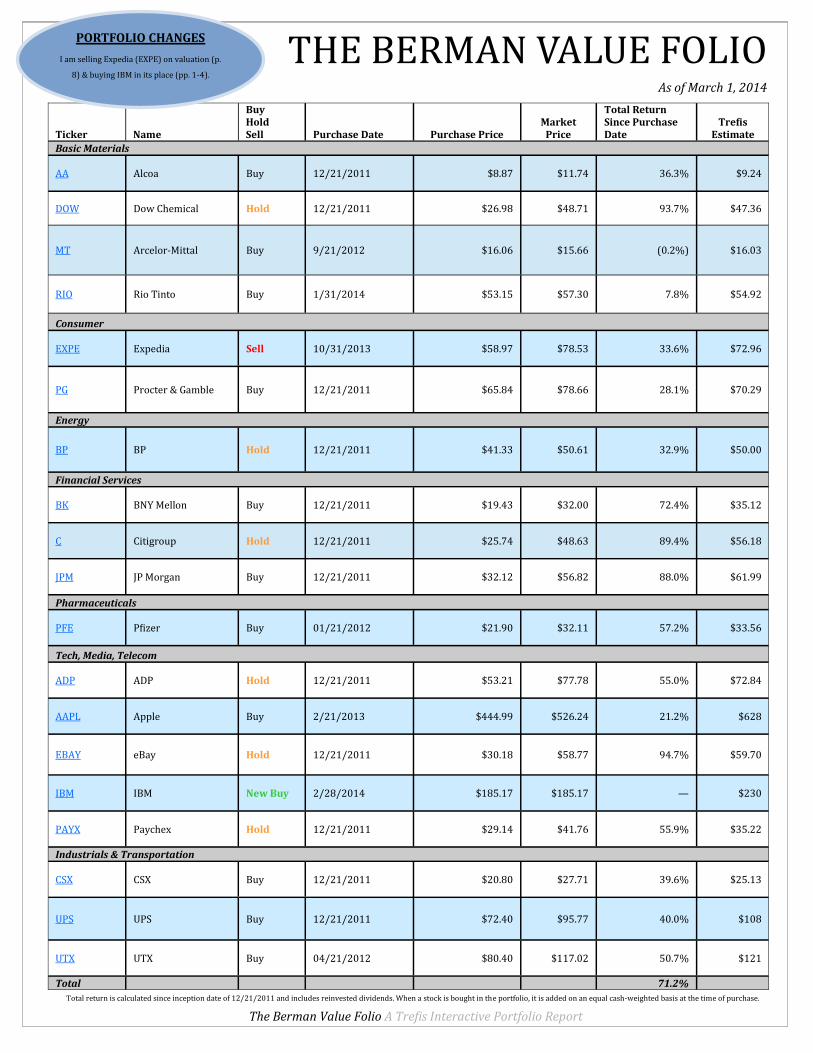

THE BERMAN VALUE FOLIO As of March 1, 2014

The Berman Value Folio A Trefis Interactive Portfolio Report

Ticker Name

Buy Hold Sell Purchase Date Purchase Price

Market Price

Total Return Since Purchase Date

Trefis Estimate

Basic Materials

AA Alcoa Buy 12/21/2011 $8.87 $11.74 36.3% $9.24

DOW Dow Chemical Hold 12/21/2011 $26.98 $48.71 93.7% $47.36

MT

Arcelor-Mittal Buy 9/21/2012 $16.06 $15.66 (0.2%) $16.03

RIO

Rio Tinto Buy 1/31/2014 $53.15 $57.30 7.8% $54.92

Consumer

EXPE Expedia Sell 10/31/2013 $58.97 $78.53 33.6% $72.96

PG Procter & Gamble Buy 12/21/2011 $65.84 $78.66 28.1% $70.29

Energy

BP BP Hold 12/21/2011 $41.33 $50.61 32.9% $50.00

Financial Services

BK BNY Mellon Buy 12/21/2011 $19.43 $32.00 72.4% $35.12

C Citigroup Hold 12/21/2011 $25.74 $48.63 89.4% $56.18

JPM JP Morgan Buy 12/21/2011 $32.12 $56.82 88.0% $61.99

Pharmaceuticals

PFE Pfizer Buy 01/21/2012 $21.90 $32.11 57.2% $33.56

Tech, Media, Telecom

ADP ADP Hold 12/21/2011 $53.21 $77.78 55.0% $72.84

AAPL Apple Buy 2/21/2013 $444.99 $526.24 21.2% $628

EBAY eBay Hold 12/21/2011 $30.18 $58.77 94.7% $59.70

IBM IBM New Buy 2/28/2014 $185.17 $185.17 — $230

PAYX Paychex Hold 12/21/2011 $29.14 $41.76 55.9% $35.22

Industrials & Transportation

CSX CSX Buy 12/21/2011 $20.80 $27.71 39.6% $25.13

UPS UPS Buy 12/21/2011 $72.40 $95.77 40.0% $108

UTX UTX Buy 04/21/2012 $80.40 $117.02 50.7% $121

Total 71.2%

PORTFOLIO CHANGES

I am selling Expedia (EXPE) on valuation (p.

8) & buying IBM in its place (pp. 1-4).

Disclaimer

The Berman Value Folio (TBVF) is published monthly and provides information and

investment ideas on stocks. All material in TBVF is Copyright 2011-13 by Trefis and

JBGlobal.com LLC and may not be reproduced in whole or in part in any form without

written consent. TBVF is written by James Berman with assistance from Trefis staff. TBVF is

distributed by both Trefis and Forbes. Forbes acts only as distributor and is not responsible

for, nor does it endorse, any TBVF content or investment ideas. All stock buys and sells are

the sole decision of James Berman. TBVF is intended for experienced investors, who

understand the risks, costs, mechanics and consequences of investing. None of the content in

this newsletter is intended to be, nor should be interpreted as, a solicitation to buy or sell

securities. The selection of portfolio stocks is based on fundamental analysis. There is,

however, no assurance that these securities will produce profits. They may instead produce

serious losses. It should not be assumed that the recommendations made in the future will be

profitable or will equal the performance of any prior securities mentioned in the TBVF. All

investing involves risk of serious loss. No graph, chart, formula or other device offered or

portrayed in TBVF can in and of itself be used to make trading or investment decisions. Any

graph, chart, formula or other device is inherently unreliable in making a trading or

investment decision due to the intrinsically misleading nature of such items.

Performance results are based on model portfolios and do not reflect actual trading. Actual

performance will vary based on a variety of factors, including market conditions and trading

costs. TBVF results may not reflect the impact that material economic and market factors

might have had on the adviser's decision-making if the adviser were actually managing

clients' money in this portfolio. TBVF contains stocks that are managed with a view towards

capital appreciation. James Berman and JBGlobal.com may manage other portfolios with

different strategies and returns that may materially differ from TBVF results with

substantially higher or lower performance. TBVF model results do not reflect the deduction

of any management fees, advisory fees, brokerage or other commissions, bid-ask spreads, tax

consequences, and any other expenses that a client would have to actually pay or would have

actually paid in a real portfolio. All return figures assume the reinvestment of all dividends.

When a stock is bought in the portfolio, it is added on an equal cash-weighted basis at the

time of purchase. Past performance does not guarantee future results. Any forward-looking

statement is inherently uncertain and cannot be relied upon as a statement of actual

performance. If you would like a spreadsheet furnishing a list of all recommendations made

by TBVF since inception on 12/21/2011, please send an email request to: [email protected].

Although all content is derived from data believed to be reliable, accuracy cannot be

guaranteed. James Berman, JBGlobal.com LLC, Insight Guru Inc., Trefis, TBVF’s publisher

and distributor(s) and their employees assume no liability whatsoever for any investment

losses as a result of securities purchased on TBVF recommendations. TBVF is not intended to

provide personalized investment advice. Readers and subscribers should consult their

financial adviser before investment.

James Berman is an investor in Insight Guru Inc., the parent company of Trefis, both

personally and through the venture fund he subadvises. James Berman, therefore, has a

financial interest in Trefis aside from his interest in TBVF. James Berman, JBGlobal.com

LLC and employees of TBVF, Insight Guru Inc., JBGlobal.com L.L.C. and Trefis may hold

positions in some or all of the stocks mentioned here, both personally and in the accounts and

funds they manage for others. No compensation for recommending particular securities,

services, or financial advisors is solicited or accepted. If you are unwilling or unable to abide

by any conditions of this disclaimer, then you may obtain a refund for the unused portion of

your subscription at any time.

The Berman Value Folio

The Berman Value Folio A Trefis Interactive Portfolio Report

Related Documents