The Basics: Supply & Demand Economics of the Firm

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Basics: Supply & Demand

Economics of the Firm

Introducing homo economicus….also known as “Economic Man”

Economic man is a RATIONAL being

The Fundamental Rule of Economics: Individuals are rational beings and therefore respond to incentives – i.e. they respond to opportunities with Economic Profit

Economic Profit = (Expected) Benefit – Opportunity Cost

Opportunity cost = Direct (Money) Costs + Implicit Costs

In other words, think about opportunity cost as the value of ALL the resources that have been consumed

Example: What would be the opportunity cost of attending Notre Dame as an undergraduate? Do students have an incentive to go to Notre Dame?

Item Average 2011/2012 Expense

Tuition and Fees $41,420

Room & Board $11,390

Books & Supplies $950

Personal Expenses $1,000

Transportation $500

Total $55,260

$55,260 x 4 = $221,040

Is this right?

So if you wanted a 10% return on your college education, you would need to earn $22,000 a year more per year after college

Example: What is IBM’s opportunity cost? Is IBM earning economic profit?

Item 2010*

Net Sales 99,870

Cost of Goods Sold (49,358)

Depreciation (4,831)

Gross Income 45,681

Selling, General, and Adm. Expense (27,025)

Operating Income 18,656

Interest Income/Expense 1,067

Pretax Income 19,723

Income Taxes (4,890)

Net Income 14,833* In Millions

Current Stock Price: $166Shares Outstanding: 1,287M

“Economics deals with the Allocation of scarce resources to satisfy unlimited wants”

“You can’t always get what you want…”

- Mick Jagger

Consumers have limited incomes to spend on a wide variety of goods and services (both now and in the future)

Workers have a finite number of hours in the day to work, relax, go to school, etc

Firms have finite capacity and limited financial resources, to produce goods and services

The economy as a whole has a finite number of resources trying to satisfy a population with unlimited wants!

Efficiency vs. Equity

An allocation of resources that maximum total welfare

An allocation of resources provides a “fair” distribution of welfare

Under certain circumstances, the free market process guarantees this

Can we trust markets to produce a desirable outcome?

If we can’t have everything we want, so we need to decide what to do with the limited resources we do have.

Efficiency vs. Equity

An allocation of resources that maximum total welfare

An allocation of resources provides a “fair” distribution of welfare

What does this mean from a business perspective? That is, why should we care?

If we have an efficient outcome, there are no opportunities to create wealth.

With inefficient outcomes, there are wealth creating opportunities.

From a business standpoint, an inefficiency offers an opportunity to create wealth by moving resources to higher value uses! This is done through voluntary transactions.

Suppose that you own a Porsche that you value at $65,000, but I value at $80,000

My Value - $80,000

Your Value - $65,000

The sale of your car creates $15,000 of new wealth. The sale price determines how that wealth is allocated between us

Sale Price = $75,000

Consumer Surplus = $5,000

Producer Surplus = $10,000

Again, think about efficiency as allocating resources to their highest value

VS.

Suppose that Exxon acquires drilling rights within a remote area where there will be negligible environmental damage in the traditional sense

The Sierra club files a lawsuit to block the drilling (Their personal serenity has been threatened by the knowledge that the oil is being removed from it’s natural habitat)

If you are the judge, who should prevail?

If Exxon Wins:• Exxon stockholders

gain• Workers gain from

added jobs• Motorists see falling

gasoline prices

If Exxon Wins:• Sierra club members

lay awake at night screaming

$10M

$5M

VS.

A ruling against Exxon in this example would be inefficient – a missed opportunity to make everyone better off.

“A subtle but damaging factor in this is the dominance of economists at business schools. Although there is no evidence that economists are less ethical than members of other discipline, approaching the world through the dollar sign does make people more cynical”*

Amitai Etzioni, “When it comes to Ethics, B-Schools Get an F”, Washington Post, August 4, 2002

“In 2006, when Notre Dame played Michigan, the south bend Marriott charged $649 per night - $500 above its usual rate of $149”*

* Ilan Brat, “Notre Dame Football introduces its Fans to Inflationary Spiral”, Wall Street Journal, September 6, 2006

Ethicist Joe Holt responds…

“It is an act of moral abdication for businesses to pretend that they have no choice but to charge as much as they can based on supply and demand”

Cost = $100/Night

ALL voluntary transactions create wealth!!

Value = $700/Night

Price = $150

Consumer Surplus = $550

Producer Surplus = $50

Price = $650

Consumer Surplus = $50

Producer Surplus = $550

Either way, $600 of wealth is created!

Cost = $100/Night

Cost = $100/Night

Cost = $100/Night

Value = $1000/Night Value = $800/Night

Value = $600/Night

Value = $200/Night

Value = $400/Night

You have three rooms to rent. How do you set the price to create the most wealth?

Cost = $100/Night

Cost = $100/Night

Cost = $100/Night

Value = $600/Night

Value = $1000/Night

Value = $800/Night

CS = $400

CS = $200

PS = $500

PS = $500

CS = $500

CS = $600PS = $1500

At a $600 per night price we create $2100 of wealth

Cost = $100/Night

Cost = $100/Night

Cost = $100/Night

Value = $600/Night

Value = $1000/Night

Value = $800/Night

CS = $850

CS = $650

PS = $50

PS = $50

PS = $50

At a $150 per night price we could create $2100 of wealth

CS = $1950PS = $150

CS = $450

Cost = $100/Night

Cost = $100/Night

Cost = $100/Night

Value = $600/Night

Value = $200/Night

Value = $400/Night

CS = $50

CS = $250

PS = $50

PS = $50

PS = $50

At a $150 per night price we could create $900 of wealth

CS = $750PS = $150

CS = $450

Charles Darwin vs. Adam Smith: Efficiency and the Competitive Marketplace

"Greed captures the essence of the evolutionary spirit."

-Gordon Gekko

What do we mean by a competitive market?

#1: Many buyers and sellers – no individual buyer/firm has any real market power

#2: Homogeneous products – no variation in product across firms

#3: No barriers to entry – it’s costless for new firms to enter the marketplace

#4: Perfect information – prices and quality of products are assumed to be known to all producers/consumers

#5: No Externalities –ALL costs/benefits of the product are absorbed by the consumer

#6: Transactions are costless – buyers and sellers incur no costs in an exchange

Can you think of situations where all these assumptions hold?

50 Fish/hr300 Max/Day

30 Fish/hr300 Max/Day

20 Fish/hr160 Max/Day

Lets try an example…suppose that you are a fisherman. Top catch larger quantities of fish, you have to go farther from shore and your catch per hour drops

Zone A Zone B Zone C

You bought a boat for $1,000Maintenance on the boat is $50/DayYou pay $16/hour in labor costsYou pay $20/hour for fuel and other expenses

What costs are fixed, sunk, and variable?

50 Fish/hr300 Max/Day

30 Fish/hr300 Max/Day

20 Fish/hr160 Max/Day

Lets try an example…suppose that you are a fisherman. Top catch larger quantities of fish, you have to go farther from shore and your catch per hour drops

Boat = $50Labor = $16/hrGas = $20/hr

Lets take this section by section…

Zone A Zone B Zone C

Quantity Total Cost Fixed Cost Variable Cost

Average Total Cost

Average Variable Cost

Marginal Cost

0 $50 $50 $0 --- --- ---

1 $50.72 $50 $.72 $50.72 $.72 $.72

2 $51.44 $50 $1.44 $25.72 $.72 $.72

3 $52.16 $50 $2.16 $17.39 $.72 $.72

Zone A FishHrFish

hr/72$.

/50

/36$

# of Fish

Dollars

FC$50

TC

VC = $.72*F

# of Fish

Dollars

AVC = MC$.72

ATC

AFC = $50

F

Let’s try and picture this…

0 0

50 Fish/hr300 Max/Day

30 Fish/hr300 Max/Day

20 Fish/hr160 Max/Day

Lets try an example…suppose that you are a fisherman. Top catch larger quantities of fish, you have to go farther from shore and your catch per hour drops

Boat = $50Labor = $16/hrGas = $20/hr

Lets take this section by section…

Zone A Zone B Zone C

Quantity TC FC VC ATC AVC MC300 $266 $50 $216 $0.88 $0.72 $.72

301 $267.20 $50 $217.20 $0.88 $0.72 $1.20

302 $268.40 $50 $218.40 $0.88 $0.72 $1.20

303 $269.60 $50 $219.60 $0.88 $0.73 $1.20

Zone B FishHrFish

hr/20.1$

/30

/36$

# of Fish

Dollars

FC$50

TC

VC =$266 + $1.20*F

# of Fish

Dollars

MC$1.20ATC

AFC = $50

F

Let’s try and picture this…

300 300

$266

$.72

AVC$.88

50 Fish/hr300 Max/Day

30 Fish/hr300 Max/Day

20 Fish/hr160 Max/Day

Lets try an example…suppose that you are a fisherman. Top catch larger quantities of fish, you have to go farther from shore and your catch per hour drops

Boat = $50Labor = $16/hrGas = $20/hr

Lets take this section by section…

Zone A Zone B Zone C

Quantity TC FC VC ATC AVC MC600 $626 $50 $576 $1.04 $.96 $1.20

601 $627.80 $50 $577.80 $1.04 $.96 $1.80

602 $629.60 $50 $579.60 $1.04 $.96 $1.80

603 $631.40 $50 $581.40 $1.04 $.96 $1.80

Zone C FishHrFish

hr/80.1$

/20

/36$

# of Fish

Dollars

FC$50

TC

VC =$576 + $1.80*F

# of Fish

Dollars

MC$1.80

ATC

AFC = $1,000

F

Let’s try and picture this…

600 600

$576

$.96

AVC$1.04

# of Fish

Dollars

FC$50

TC

# of Fish

Dollars

MC

$.72

All together…

0 0

$1.20

Slope = 1.80

Slope = 1.20

Slope = .72

300 600

$1.80ATCAVC

300 600

Perfectly competitive firms are “price takers”. They see a market price and can’t change it. Suppose that the market price is $1.20.

Fish Price Total Revenue Total Cost Profit0 $1.20 $0 $50 -$50

1 $1.20 $1.20 $50.72 -$49.52

2 $1.20 $2.40 $51.44 -$49.04

3 $1.20 $3.60 $52.16 -$48.56

300 $1.20 $360 $266 $94

301 $1.20 $361.20 $267.20 $94

302 $1.20 $362.40 $268.40 $94

303 $1.20 $363.60 $269.60 $94

600 $1.20 $720 $626 $94

601 $1.20 $721.20 $627.80 $93.40

602 $1.20 $721.40 $629.60 $91.80

603 $1.20 $721.60 $631.40 $90.20

# of Fish

Dollars

$50

TC

# of Fish

Dollars

-$50

We are looking to maximize profits where profits are the difference between total revenues and total costs

0 0

$0Slope = 1.80

Slope = 1.20

Slope = .72

300 600

$94

300 600

TR

Profit

Marginal revenue is greater than marginal cost

Profits are increasing

Marginal revenue is equal to marginal cost

Profits are maximized

Marginal revenue is less than marginal cost

Profits are decreasing

We could also go at this by looking at costs and benefits at the margin. For a perfectly competitive firm the market price equals marginal revenue.

Fish Total Cost Total Revenue Marginal Revenue Marginal Cost

0 $50 $0 $1.20 $.72

1 $50.72 $1.20 $1.20 $.72

2 $51.44 $2.40 $1.20 $.72

3 $52.16 $3.60 $1.20 $.72

300 $266 $360 $1.20 $.72

301 $267.20 $361.20 $1.20 $1.20

302 $268.40 $362.40 $1.20 $1.20

303 $269.60 $363.60 $1.20 $1.20

600 $626 $720 $1.20 $1.20

601 $627.80 $721.20 $1.20 $1.80

602 $629.60 $721.40 $1.20 $1.80

603 $631.40 $721.60 $1.20 $1.80

# of Fish

Dollars

-$50

Lets plot out marginal revenues and costs rather than total costs and revenues…

0

$0

$94

300 600

Dollars

MC

$.72

0

$1.20

$1.80

300 600

MR

Profit

Marginal revenue is greater than marginal cost

Profits are increasing

Marginal revenue is equal to marginal cost

Profits are maximized

Marginal revenue is less than marginal cost

Profits are decreasing

# of Fish

Dollars

When we talk about a supply curve we are talking about the profit maximizing decisions of individual firms at prevailing market prices

0

$1.20

300 600

Dollars

MC

$.72

0

$1.20

$1.80

300 600

MR

At a market price of $1.20, MR = MC for any quantity of fish between 300 and 600

At a market price of $1.20, this firm will be willing to supply any quantity of fish between 300 and 600

Perfectly competitive firms are “price takers”. They see a market price and can’t change it. Suppose that the market price is $0.72.

Fish Price Total Revenue Total Cost Profit

0 $0.72 $0 $50 -$50

1 $0.72 $0.72 $50.72 -$50

2 $0.72 $1.44 $51.44 -$50

3 $0.72 $2.16 $52.16 -$50

300 $0.72 $216 $266 -$50

301 $0.72 $216.72 $267.20 -$50.48

302 $0.72 $217.44 $268.40 -$50.96

303 $0.72 $218.16 $269.60 -$51.44

600 $0.72 $432 $626 -$194

601 $0.72 $432.72 $627.80 -$195.08

602 $0.72 $433.44 $629.60 -$196.16

603 $0.72 $434.16 $631.40 -$197.24

# of Fish

Dollars

$50

TC

# of Fish

Dollars

-$50

All together…

0 0

$0

Slope = 1.80

Slope = 1.20

Slope = .72

300 600 300 600

TR

Profit

Marginal revenue is equal to marginal cost

Marginal revenue is less than marginal cost

Profits are maximized

Profits are decreasing

Perfectly competitive firms are “price takers”. They see a market price and can’t change it. Suppose that the market price is $.72.

Fish Total Cost Total Revenue Marginal Revenue Marginal Cost

0 $50 $0 $.72 $.72

1 $50.72 $0.72 $.72 $.72

2 $51.44 $1.44 $.72 $.72

3 $52.16 $2.16 $.72 $.72

300 $266 $216 $.72 $.72

301 $267.20 $216.72 $.72 $1.20

302 $268.40 $217.44 $.72 $1.20

303 $269.60 $218.16 $.72 $1.20

600 $626 $432 $.72 $1.20

601 $627.80 $432.72 $.72 $1.80

602 $629.60 $433.44 $.72 $1.80

603 $631.40 $434.16 $.72 $1.80

All together…

Dollars

MC

$.72

0

$1.20

$1.80

300 600

MR

Dollars

-$50

0

$0

300 600

Profit

Marginal revenue is equal to marginal cost

Marginal revenue is less than marginal cost

Profits are maximized

Profits are decreasing

# of Fish

Dollars

When we talk about a supply curve we are talking about the profit maximizing decisions of individual firms at prevailing market prices

0

$1.20

300 600

Dollars

MC

$.72

0

$1.20

$1.80

300 600

MR

At a market price of $.72, MR = MC for any quantity of fish between 0 and 300

At a market price of $.72, this firm will be willing to supply any quantity of fish between 0 and 300

$.72

# of Fish

Dollars

When we talk about a supply curve we are talking about the profit maximizing decisions of individual firms at prevailing market prices

0

$1.20

300 600

Dollars

MC

$.72

0

$1.20

$1.80

300 600

MR

At a market price of $1.80, MR = MC for any quantity of fish between 600 and 760

At a market price of $1.80, this firm will be willing to supply any quantity of fish between 600 and 760

$.72

$1.80

# of Fish

Dollars

What if the prevailing market was $1.35?

0

$1.35

300 600

Dollars

MC

0

$1.35

300 600

MR

At a market price of $1.35, 600 fish are profitable to supply, but the 601st is not!

At a market price of $1.35, this firm will be willing to supply exactly 600 fish.

# of Fish

Dollars

So we can get an individual firm’s supply curve by following marginal costs! Suppose that there are 1000 fishermen in the village – all with the same costs.

0

$1.80

300 600

Individual Supply

$1.20

$.72

# of Fish

Dollars

0

$1.80

300,000 600,000

Market Supply

$1.20

$.72

Market supply adds up the decisions of each individual firm at each prevailing market price

So where do prices come from? We need to know how many fish people are actually willing to buy at any prevailing market price.

# of Fish

Dollars

0

$1.80

500,000 900,000

$1.20

$.72

150,000

A demand curve is just a record of how much the market collectively is willing to buy at any given market price

Price Fish

$2.00 50,000

$1.80 150,000

$1.50 200,000

$1.20 500,000

$1.00 540,000

$.72 600,000

$.50 700,000

# of Fish

Dollars

0

$1.80

300,000 600,000

$1.20

$.72

In equilibrium, total supply should equal total demand. If not, the price will adjust.

Supply

Demand

Price Fish

$2.00 50,000

$1.80 150,000

$1.50 200,000

$1.20 500,000

$1.00 540,000

$.72 600,000

$.50 700,000

At a $1.80 price, fishermen will bring at least 600,000 fish to the market, but only 150,000 will get sold – the price needs to drop

At a $.72 price, fishermen will bring at most 300,000 fish to the market, but 600,000 are demanded– the price needs to rise

In equilibrium, total supply should equal total demand

The market determines the equilibrium price of $1.20 and 500,000 fish sold by the 1,000 fishermen

Market

Dollars

0

$1.80

300,000 600,000

$1.20

$.72

Demand

Supply

500,000

Dollars

$.72

0

$1.20

$1.80

300 600

Individual

At the prevailing market price of $1.20, each fisherman supplies between 300 and 600 fish

MC

MR

Dollars

$.72

0

$1.20

$1.80

300 600

MC

MR

Fish Total Revenue Total Cost Profit

300 $360 $266 $94

301 $361.20 $267.20 $94

302 $362.40 $268.40 $94

303 $363.60 $269.60 $94

$144

Boat = $50Labor = $16/hrGas = $20/hr

FishHrFish

hr/20.1$

/30

/36$

* Labor Productivity = 30 Fish/Hr

Price= $1.20

- Gas Cost = $0.67

Labor’s Value Added= $0.53

$16/hr = hourly wage

Producer Surplus = $144

- Fixed Cost = $50

Accounting Profit= $94

$94

$1,000*100 = 9.4% Return

A Few Diagnostics…

Is this fisherman earning economic profits?

# of Fish

Dollars

0

$1.80

300,000 600,000

$1.20

$.72

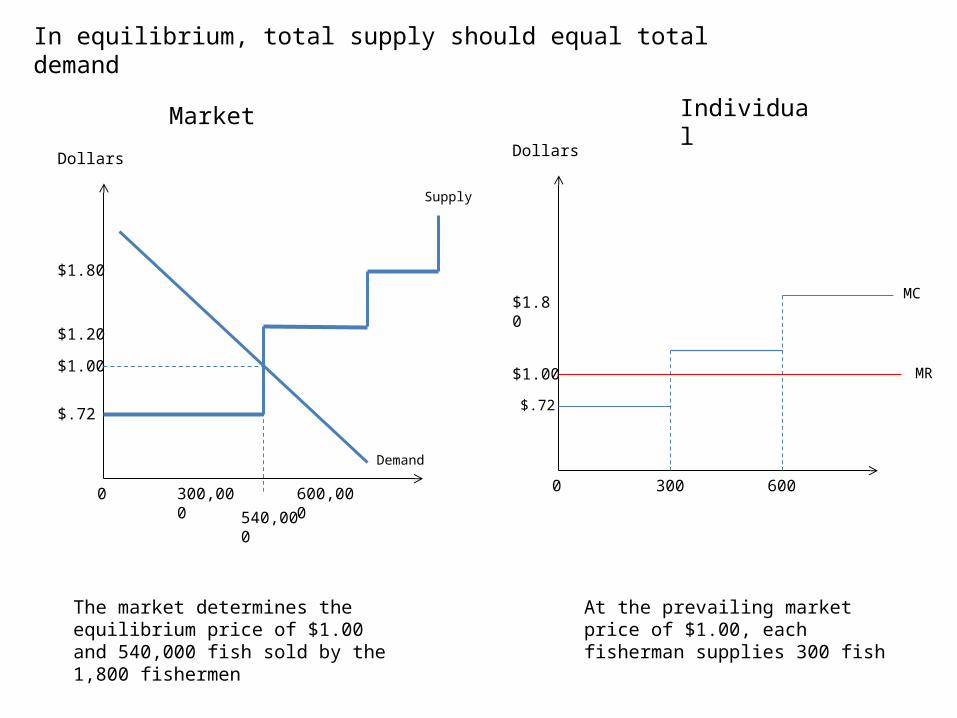

Suppose that the excess returns causes 800 more fishermen (all with identical costs) to enter the market.

Supply

Demand

Price Fish

$2.00 50,000

$1.80 150,000

$1.50 200,000

$1.20 500,000

$1.00 540,000

$.72 600,000

$.50 700,000

540,000 1,080,000 1,368,000

In equilibrium, total supply should equal total demand

The market determines the equilibrium price of $1.00 and 540,000 fish sold by the 1,800 fishermen

Market

Dollars

0

$1.80

300,000 600,000

$1.00

$.72

Demand

Supply

540,000

Dollars

$.72

0

$1.00

$1.80

300 600

Individual

At the prevailing market price of $1.00, each fisherman supplies 300 fish

MC

MR

$1.20

Dollars

$.72

0

$1.00

$1.80

300 600

MC

MR

$84

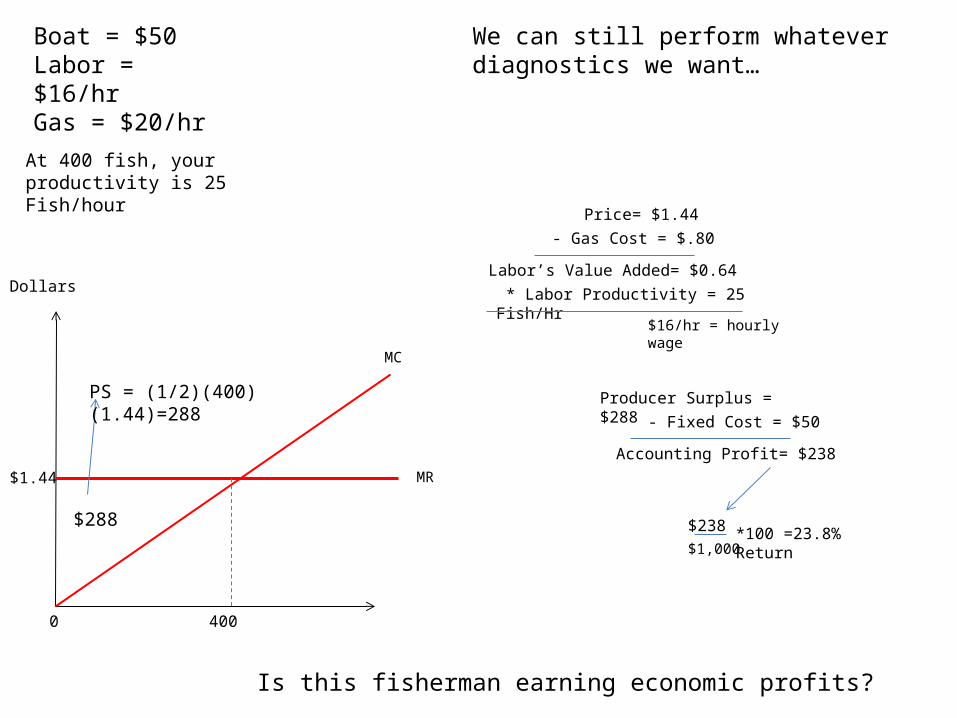

Boat = $50Labor = $16/hrGas = $20/hr

FishHrFish

hr/72$.

/50

/36$

Fish Price Total Revenue Total Cost Profit

0 $1.00 $0 $50 -$50

1 $1.00 $1.00 $50.72 -$49.72

2 $1.00 $2.00 $51.44 -$49.44

3 $1.00 $3.00 $52.16 -$49.16

300 $1.00 $300 $266 $34

* Labor Productivity = 50 Fish/Hr

Price= $1.00

- Gas Cost = $0.40

Labor’s Value Added= $0.60

$30/hr > hourly wage

Producer Surplus = $84

- Fixed Cost = $50

Accounting Profit= $34

$34

$1,000*100 = 3.4% Return

A Few Diagnostics…

Dollars

MC

$.72

0

$1.20

$1.80

300 600

Let’s see if we can’t generalize this a bit. We want marginal costs to be increasing – this reflects decreasing labor productivity at the margin

# of Fish

Dollars

FC$50

TC

0 300 600

# of Fish

Dollars

TC

# of Fish

Dollars

-$50

All together…

0 0

$0

Slope = 1.20

300 600

$94

300 600

TR

Profit

F*

F*

We are still looking for where marginal revenue equals marginal costs (i.e. the slopes are the same)

Dollars

-$50

0

$0

300 600

Profit

Dollars

MC

0

F*MRP*

F*

All together…

We are still looking for where marginal revenue equals marginal costs

# of Fish

Dollars

0

P*

Dollars

MC

0

P* MR

F* F*

Supply

For any market price (which is marginal revenue for a perfectly competitive firm, there is a profit maximizing quantity where MR = MC

That optimizing quantity becomes a point on that firms supply curve

# of Fish

Dollars

0

Individual Supply

P*

# of Fish

Dollars

0

Market Supply

P*

We still aggregate decisions across individual suppliers to get market supply (again, assume 1,000 fishermen)

F 1000*F

SupplySupply

In equilibrium, total supply should equal total demand

The market determines the equilibrium price of $1.44 and 400,000 fish sold by the 1,000 fishermen

Market

Dollars

0

$1.44*

Demand

Supply

400,000*

Dollars

0

1.44*

Individual

At the prevailing market price of $1.44, each fisherman supplies 400 fish

MC

MR

400

Dollars

0

$1.44

400

MC

MR

Boat = $50Labor = $16/hrGas = $20/hr

* Labor Productivity = 25 Fish/Hr

Price= $1.44

- Gas Cost = $.80

Labor’s Value Added= $0.64

$16/hr = hourly wage

Producer Surplus = $288

- Fixed Cost = $50

Accounting Profit= $238

$238

$1,000*100 =23.8% Return

We can still perform whatever diagnostics we want…

Is this fisherman earning economic profits?

At 400 fish, your productivity is 25 Fish/hour

PS = (1/2)(400)(1.44)=288

$288

# of Fish

Dollars

0

$1.44

Suppose that the excess returns causes 800 more fishermen (all with identical costs) to enter the market.

Supply

Demand

400,000

$1.03

576,000

Dollars

0

$1.44

400320720,000

Dollars

0

$1.03

320

MC

MR

Boat = $50Labor = $16/hrGas = $20/hr

* Labor Productivity = 35 Fish/Hr

Price= $1.03

- Gas Cost = $.57

Labor’s Value Added= $0.46

$16/hr = hourly wage

Producer Surplus = $165

- Fixed Cost = $50

Accounting Profit= $115

$115

$1,000*100 =11.5% Return

We can still perform whatever diagnostics we want…

At 320 fish, your productivity is 35 Fish/hour

PS = (1/2)(320)(1.03)=165

$165

Suppose that we have three fishermen with different productivities. Each bought a boat for $1,000 and have the same costs as before.

30 Fish/hr300 Max/Day

20 Fish/hr200 Max/Day

10 Fish/hr100 Max/Day

Boat = $50Labor = $16/hrGas = $20/hr

$1.20 per fish

$1.80 per fish

$3.60 per fish

Each of the above fishermen will provide fish to the marketplace as long as the market price is equal to or greater to their marginal cost

Dollars

0

$3.60

$1.80

$1.20

Fish

300 500 600

For a market price that is at least $1.20, but below $1.80, only fisherman #1 sells fish. He can supply up to 300

For a market price that is at least $1.80, but below $3.60, fisherman #1 sells 300 fish and fisherman #2 sells up to 200 fish.

For a market price that is at least $3.60, fisherman #1 sells 300 fish, fisherman #2 sells 200 fish and fisherman #3 sells 100 fish

All a supply curve really does is order production from lowest cost to highest cost

Dollars

0

$3.60

$1.80

$1.20

Fish

300 500 600

Adding a demand curve will give us the equilibrium price and identify the fisherman who participate in the market as well as the fisherman’s economic profits

Demand

Supply

$3.00

Boat = $50Labor = $16/hrGas = $20/hr Producer Surplus = $540

- Fixed Cost = $50

Accounting Profit= $490

$490

$1,000*100 = 49% Return

Fisherman #1

PS= $540- Fixed Cost = $50

Accounting Profit= $190

$190

$1,000*100 = 19% Return

Fisherman #2

Producer Surplus = $240

PS= $240

PSQS Quantity Supplied

“Is a function of”

Market Price (+)

A Supply Function represents the rational decisions made by a profit maximizing firm(s).

Quantity

Price

S

A supply curve naturally ranks potential suppliers from lowest marginal costs to higher marginal costs

Lower cost producers are in this portion – they will make the largest profits

Higher cost producers are in this portion – they will make the lowest profits (if they participate in the marketplace)

Quantity

Price

S

A supply curve naturally ranks potential suppliers from lowest marginal costs to higher marginal costs

Example: Cell Phones

Company Price EPS EPS/P (%) ROE ROA

Sprint $3.11 (1.05) 33% 21% .06%

Verizon $34.62 $2.23 6.4% 16% 5%

AT&T $28.44 $3.44 12% 18% 4.5%

By the same token, a demand curve naturally ranks potential consumers from highest valuation to lowest valuation. Suppose that we have three potential consumers of rats.

Would pay up to $25/rat. Can consume 100 rats per week.

Would pay up to $10/rat. Can consume 50 rats per week.

Would pay up to $1/rat. Can consume 20 rats per week.

What would this demand curve look like?

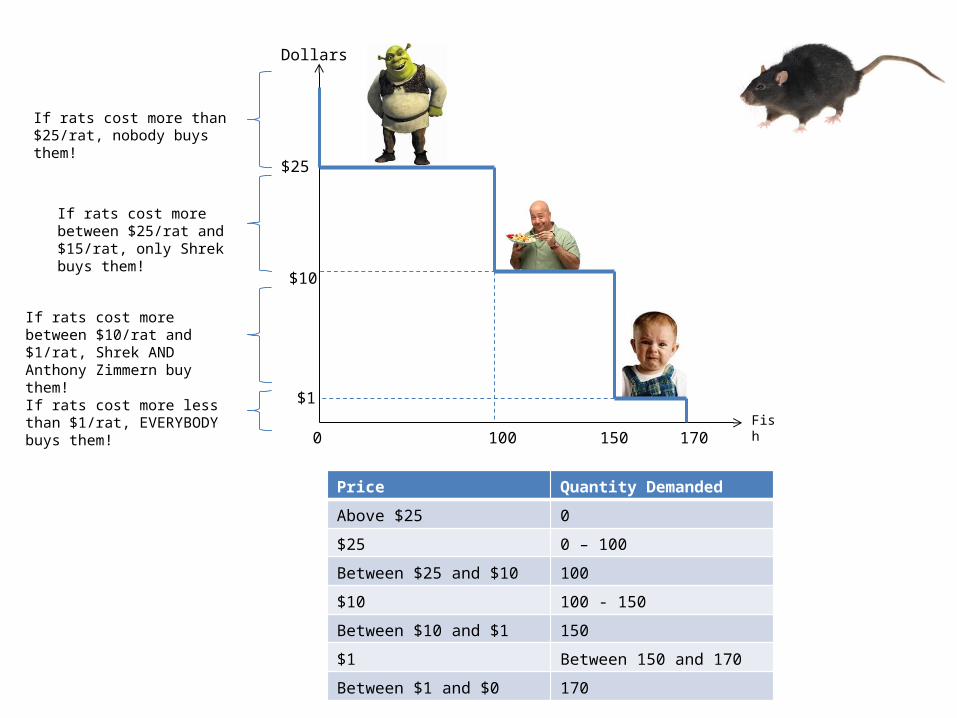

Dollars

0

$25

$1Fish

100 150 170

$10

If rats cost more than $25/rat, nobody buys them!

If rats cost more between $25/rat and $15/rat, only Shrek buys them!

If rats cost more between $10/rat and $1/rat, Shrek AND Anthony Zimmern buy them!

If rats cost more less than $1/rat, EVERYBODY buys them!

Price Quantity Demanded

Above $25 0

$25 0 – 100

Between $25 and $10 100

$10 100 - 150

Between $10 and $1 150

$1 Between 150 and 170

Between $1 and $0 170

Dollars

0

$25

$1Fish

100 150 170

$10

For any market price, we know how many rats are sold and how much each consumer benefits from the market (consumer surplus)

$15

At a market price of $15

Shrek buys 100 rats for $15 apiece. He saves $10 per rat for a total of $1000 in savings (surplus)

Neither the baby of Anthony Zimmern are willing to buy rats for $15.

CS = $1000

Dollars

0

$25

$1Fish

100 150 170

$10

For any market price, we know how many rats are sold and how much each consumer benefits from the market (consumer surplus)

$5

At a market price of $5

Shrek buys 100 rats for $5 apiece. He saves $20 per rat for a total of $2000 in savings (surplus)

Anthony Zimmern buys 50 rats for $5. He saves $5 per rat for a total of $250 in surplus

The baby still is unwilling to buy rats!CS = $2000

CS = $250

Quantity

Price

PDQD Quantity Demanded

“Is a function of”

Market Price (-)

A Demand Function represents the rational decisions made by a representative consumer(s)

D

Consumers with high valuations are located here

Consumers with low valuations are located here

Key Point: Demand curves represent marginal utility (what we are willing to pay for one additional unit). Consumer surplus measures total value.

Quantity

Price

DQuantity

Price

D

Water Diamonds

S

SP*

P*

Example: The Diamond/Water Paradox

Market Equilibrium: There exists a price where supply equals demand – the market will find this price automatically.

Quantity

Price

D

S

P*

Q*

At a price above the equilibrium price, supply is greater than demand. A surplus drives the price down

At a price above the equilibrium price, demand is greater than supply. A surplus drives the price up

Let’s suppose that we are talking about the market for bananas.

Quantity

Price

D

S

$5

1,000

$8

$2

There was a pound of bananas sold that cost $3 to supply and was valued by someone at $7. This transaction created $4 of wealth - $2 went to a seller (producer surplus) and $2 went to a buyer (consumer surplus)

There was a pound of bananas sold that cost $2 to supply and was valued by someone at $8. This transaction created $6 of wealth - $3 went to a seller (producer surplus) and $3 went to a buyer (consumer surplus)

$3

$7

Would this transaction be wealth creating?

Efficiency vs. Equity

An allocation of resources that maximum total welfare

An allocation of resources provides a “fair” distribution of welfare

Under certain circumstances, the market process guarantees this

Can we trust markets to produce a desirable outcome?

Recall an earlier discussion about allocations of resources.

Competitive markets provide efficient outcomes in that every wealth creating transaction was undertaken. In other words, consumer surplus and producer surplus are maximized.

Quantity

Price

D

S

$5

1,000

$0

$12

Consumer Surplus = (1/2)*($12- $5)*1,000

$3,500

Producer Surplus = (1/2)*($5- $0)*1,000

$2,500

Note that $6,000 of wealth was created by this market!

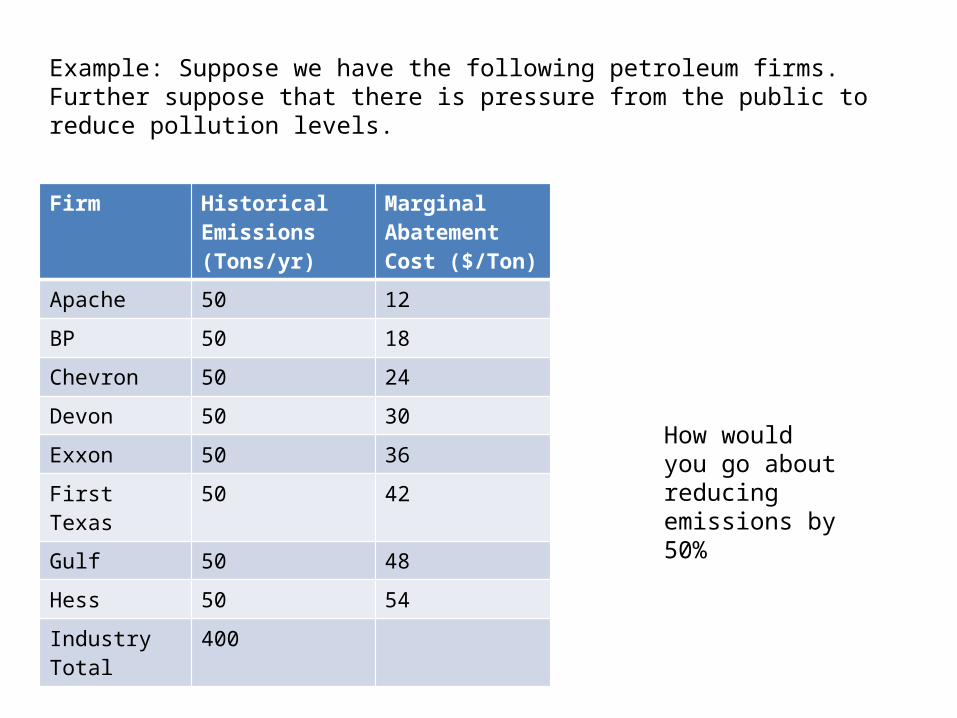

Firm Historical Emissions (Tons/yr)

Marginal Abatement Cost ($/Ton)

Apache 50 12

BP 50 18

Chevron 50 24

Devon 50 30

Exxon 50 36

First Texas 50 42

Gulf 50 48

Hess 50 54

Industry Total 400

Example: Suppose we have the following petroleum firms. Further suppose that there is pressure from the public to reduce pollution levels.

How would you go about reducing emissions by 50%

Apache

BP

Chevron

Devon

Exxon

First

Gulf

Hess

$ Per Unit Pollution Reduction

Quantity of Emissions Reduction

$12

$18

$24

$30

$36

$42

$48

$54

The cheapest way to reduce pollution by 50% would be to require the cheapest 4 firms to reduce their emissions completely and let the other four firms continue as in the past

Problems: • Unfair• Requires information on

abatement costs

Firm Historical Emissions (Tons/yr)

Marginal Abatement Cost ($/Ton)

Tons of emission to be reduced

Total abatement cost

Apache 50 12 25 300

BP 50 18 25 450

Chevron 50 24 25 600

Devon 50 30 25 750

Exxon 50 36 25 900

First Texas 50 42 25 1,050

Gulf 50 48 25 1,200

Hess 50 54 25 1,350

Industry Total 400 200 6,600

We could follow an “across the board” emission reduction program (note: pollution taxes would have the same basic effect)

Example: Cap and Trade as a solution to pollution reduction.Firm Historical

Emissions (Tons/yr)

Marginal Abatement Cost ($/Ton)

Apache 50 12

BP 50 18

Chevron 50 24

Devon 50 30

Exxon 50 36

First Texas 50 42

Gulf 50 48

Hess 50 54

Industry Total 400

Could BP profit from selling a pollution permit to Gulf? What should the selling price be?

Let markets work for you!!!

Apache

BP

Chevron

Devon

Exxon

First

Gulf

Hess

$ Per Unit Pollution Reduction

Quantity of Emissions Reduction

Hess

Gulf

First

Exxon

Devon

Chevron

BP

ApacheD

S

The Market for pollution permits

$12

$18

$24

$30

$36

$42

$48

$54

Equ

ilibr

ium

pric

e ra

nge

$33

Firm Historical Emissions (Tons/yr)

Marginal Abatement Cost ($/Ton)

Initial Permit Holdings

Permits Sold

Permits Bought

Final Permit Holdings

Required Emission Reduction

Emission Abatement Cost

Apache 50 12 25 25 0 0 50 $600

BP 50 18 25 25 0 0 50 $900

Chevron 50 24 25 25 0 0 50 $1200

Devon 50 30 25 25 0 0 50 $1500

Exxon 50 36 25 0 25 50 0 $0

First Texas

50 42 25 0 25 50 0 $0

Gulf 50 48 25 0 25 50 0 $0

Hess 50 54 25 0 25 50 0 $0

Industry Total

400 200 100 100 400 200 $4,200

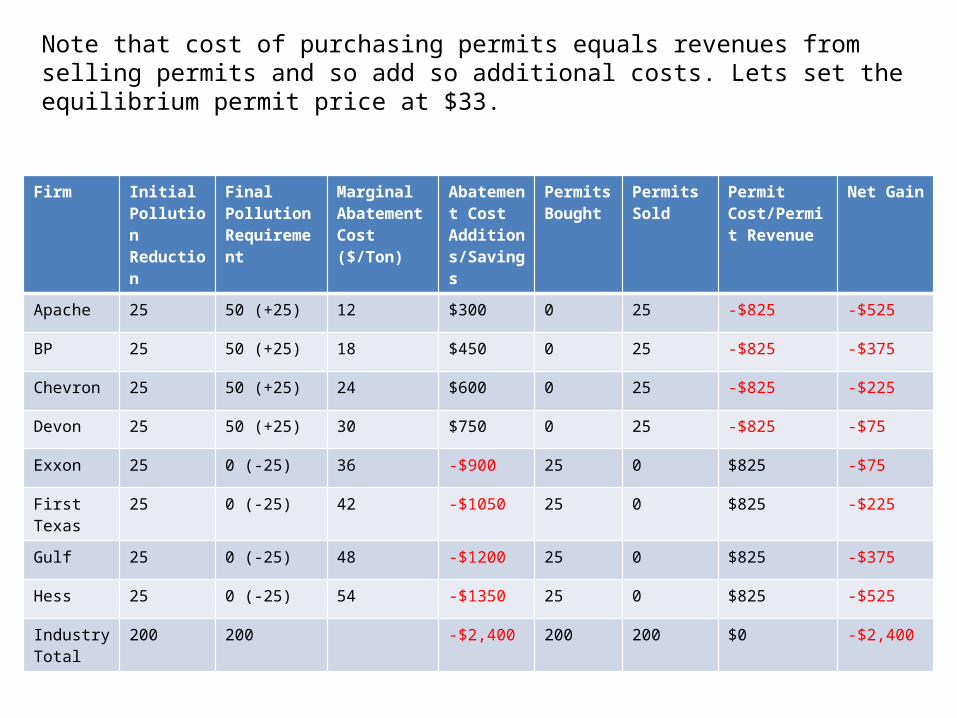

The cap and trade program lowered the cost of pollution reduction by $2,400 (from $6,600 to $4,200).

Firm Initial Pollution Reduction

Final Pollution Requirement

Marginal Abatement Cost ($/Ton)

Abatement Cost Additions/Savings

Permits Bought

Permits Sold

Permit Cost/Permit Revenue

Net Gain

Apache 25 50 (+25) 12 $300 0 25 -$825 -$525

BP 25 50 (+25) 18 $450 0 25 -$825 -$375

Chevron 25 50 (+25) 24 $600 0 25 -$825 -$225

Devon 25 50 (+25) 30 $750 0 25 -$825 -$75

Exxon 25 0 (-25) 36 -$900 25 0 $825 -$75

First Texas 25 0 (-25) 42 -$1050 25 0 $825 -$225

Gulf 25 0 (-25) 48 -$1200 25 0 $825 -$375

Hess 25 0 (-25) 54 -$1350 25 0 $825 -$525

Industry Total

200 200 -$2,400 200 200 $0 -$2,400

Note that cost of purchasing permits equals revenues from selling permits and so add so additional costs. Lets set the equilibrium permit price at $33.

Apache

BP

Chevron

Devon

Exxon

First

Gulf

Hess

$ Per Unit Pollution Reduction

Quantity of Emissions Reduction

Hess

Gulf

First

Exxon

Devon

Chevron

BP

ApacheD

S

The consumer/producer surplus represents the gains by all firms

$12

$18

$24

$30

$36

$42

$48

$54

$33

$525

$375$225

$75

$225

$375

$525

$75

We could do this numerically as well…

PQD 2100

Every $1 increase in price lowers demand by 2 units

PQS 3

Every $1 increase in price raises supply by 3 units

In Equilibrium SD QQ PP 32100 P510020$P 60202100 DQ

60203 SQ

Price

Quantity

S

D

$20

60

PQD 2100 PQS 4

Consumer and producer surplus give us a numerical value of a marketplace…

Price

Quantity

S

D

$20

60

$50

$0

Note: a $50 price will set quantity demanded equal to zero.

Consumer Surplus

900$20$50$602

1

CS

Producer Surplus

600$0$20$602

1

PS

$900

$600

Demand is not simply a function of price, but is, instead, a function of many variables

• Income• Prices of other goods

(Substitutes vs. Compliments)

• Tastes • Future Expectations• Number of Buyers

,...PDQD

“Is a function of”

Price Demand Shifters

Quantity

Price

$10

100

D(…)

Holding all the demand shifters constant at some level, quantity demanded at a price of $10 is 100

120

At the initial price of $10, but with a new value for one of the demand shifters, quantity demanded has risen to 120 (An increase in demand)

D(.’.)

Example: Increase in Demand

Supply is not simply a function of price, but is, instead, a function of many variables

• Technology• Input prices• Number of sellers

,...PDQS

“Is a function of”

Price Supply Shifters

Quantity

Price

$10

100

S(…)

Holding all the supply shifters constant at some level, quantity supplied at a price of $10 is 100

80

At the initial price of $10, but with a new value for one of the supply shifters, quantity demanded has fallen to 80

S(.’.)

Marginal costs

Example: Decrease in Supply

# of Rooms

Rate per night

000,50$ID

Example: How would the loss in income during the last recession impact the hotel industry?

...S

$150

50,000

000,75$ID

40,000

At the current $150 market price, supply is still 50,000, but with a lower level of income, demand has fallen to 40,000

At the new income level of $50,000, $150 can no longer be the equilibrium price

The decrease in income (which causes a decrease in demand) causes a drop in sales and a drop in market price

# of Rooms

Rate per night

000,50$ID

Example: How would the loss in income during the last recession impact the hotel industry?

...S

$150

50,000

000,75$ID

45,000

$125

Pounds

Price per pound

...D

Example: How would a drop in the wage rate in Columbia influence the price of coffee?

8$wS

$5

10,000 18,000

At the current $5 market price, supply has risen to 18,000, but demand is still at 10,000

At the wage level of $6, $5 can no longer be the equilibrium price

6$wS

Pounds

Price per pound

...D

Example: How would a drop in the wage rate in Columbia influence the price of coffee?

8$wS

$5

10,000 16,000

The lower wage (which causes an increase in supply) , results in a lower price and higher sales

6$wS

$4

Demand curves slope downwards – this reflects the negative relationship between price and quantity. Elasticity of Demand measures this effect quantitatively

Quantity

Price

$2.50

5

000,50$ID

$2.75

4

%20100*5

54

%10100*50.2

50.275.2

210

20

%

%

P

QDD

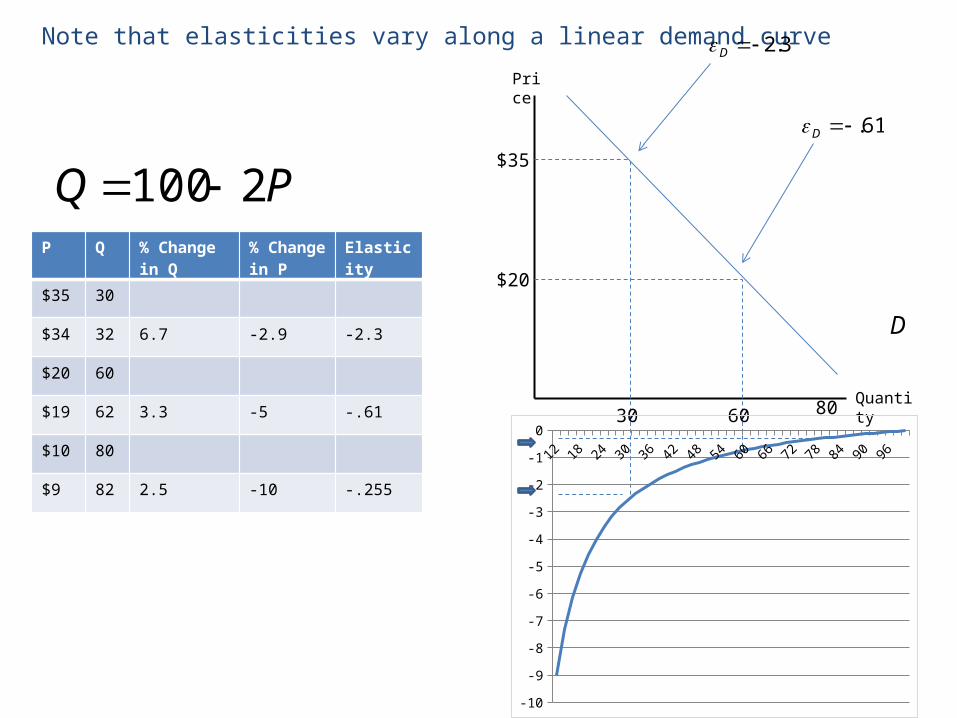

Note that elasticities vary along a linear demand curve

Quantity

Price

$35

30

D

3.2D

60 80

$20

61.D

PQ 2100 P Q % Change in

Q% Change in P

Elasticity

$35 30

$34 32 6.7 -2.9 -2.3

$20 60

$19 62 3.3 -5 -.61

$10 80

$9 82 2.5 -10 -.255

12 18 24 30 36 42 48 54 60 66 72 78 84 90 96

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

Supply curves slope upwards – this reflects the positive relationship between price and quantity. Elasticity of Supply measures this effect quantitatively

%25100*200

200250

%50100*00.2

00.200.3

5.50

25

%

%

P

QSs

Quantity

Price

$2.00

200

S

$3.00

250

Yom Kippur war oil embargo

Iranian Revolution/ Iran Iraq War Gulf War

OPEC Cuts

911

PDVSA StrikeIraq WarAsian Expansion

Example: What effect would a shutdown of oil production in Iran have on oil prices?

It would be foolish to consider the entire oil market as perfectly competitive, but perhaps considering the non-OPEC market as perfectly competitive market is not entirely crazy

Country Joined OPEC

Production (Bar/D)

Algeria 1969 2,180,000

Angola 2007 2,015,000

Ecuador 2007 486,100

Iran 1960 3,707,000

Iraq 1960 2,420,000

Kuwait 1960 2,274,000

Libya 1962 1,875,000

Nigeria 1971 2,169,000

Qatar 1961 797,000

Saudi Arabia 1960 10,870,000

United Arab Emirates

1967 3,046,000

Venezuela 1960 2,643,000

There are around 100 Non-OPEC countries producing collectively 55 Bar/D.

Country Production (BBD)

Russia 9,810,000

United States 8,514,000

China 3,795,000

India 3,720,000

Canada 3,350,000

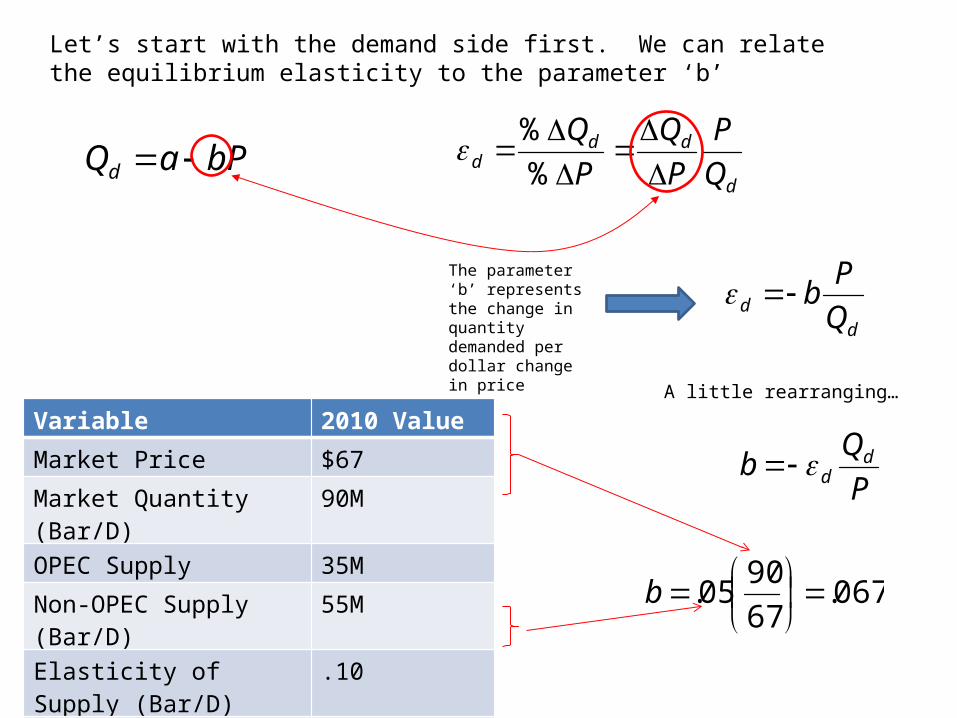

Suppose that we consider the following supply demand model:

bPaQd

Parameters to be estimated

dPcQs

Parameters to be estimated

To estimate four parameters, we need four pieces of information

Variable 2010 Value

Market Price $67

Market Quantity (Bar/D) 90M

OPEC Supply 35M

Non-OPEC Supply (Bar/D) 55M

Elasticity of Supply (Bar/D) .10

Elasticity of Demand -.05

Competitive SupplyDemand OPEC Supply

35sQ

Side Note: Elasticity and linear demand/supply curves

Quantity

Price

30

D

80

PQ 2100

$35

P

QDD

%

%

Q

% P

PP

%

Q

P

P

QD

Every $1 price increase lowers sales by 2 units

3.230

352

D

P

Q

bPaQd

Let’s start with the demand side first. We can relate the equilibrium elasticity to the parameter ‘b’

d

ddd Q

P

P

Q

P

Q

%

%

The parameter ‘b’ represents the change in quantity demanded per dollar change in price

dd Q

Pb

A little rearranging…

P

Qb d

d

067.67

9005.

b

Variable 2010 Value

Market Price $67

Market Quantity (Bar/D) 90M

OPEC Supply 35M

Non-OPEC Supply (Bar/D) 55M

Elasticity of Supply (Bar/D) .10

Elasticity of Demand -.05

PaQd 067.

Now that we know ‘b’, we can find ‘a’

Again, a little rearranging…

PQa d 067.

5.9467067.90 a

PQd 067.5.94

We are halfway home!

Variable 2010 Value

Market Price $67

Market Quantity (Bar/D) 90M

OPEC Supply 35M

Non-OPEC Supply (Bar/D) 55M

Elasticity of Supply (Bar/D) .10

Elasticity of Demand -.05

dPcQs

Repeat the process with the supply side. We can relate the equilibrium elasticity to the parameter ‘d’

s

sss Q

P

P

Q

P

Q

%

%

The parameter ‘c’ represents the change in quantity supplied per dollar change in price

ss Q

Pd

A little rearranging…

P

Qd s

s

082.67

5510.

d

We’re estimating the non-OPEC supply, so be sure to use only the non-OPEC quantity!

Variable 2010 Value

Market Price $67

Market Quantity (Bar/D) 90M

OPEC Supply 35M

Non-OPEC Supply (Bar/D) 55M

Elasticity of Supply (Bar/D) .10

Elasticity of Demand -.05

PcQs 082.

Now that we know ‘d’, we can find ‘c’

Again, a little rearranging…

PQc s 082.

5.4967082.55 c

PQs 082.5.49

That’s it!

Variable 2010 Value

Market Price $67

Market Quantity (Bar/D) 90M

OPEC Supply 35M

Non-OPEC Supply (Bar/D) 55M

Elasticity of Supply (Bar/D) .10

Elasticity of Demand -.05

Suppose that we consider the following supply demand model:

PQd 067.5.94 PQs 082.5.49

Let’s double check our results

Variable 2010 Value

Market Price $67

Market Quantity (Bar/D)

90

Competitive SupplyDemand OPEC Supply

35sQ

67$

149.10

082.5.4935067.5.94

P

P

PP

QQ sd

9067067.5.94 dQ

Now, back to the original question. Suppose that Iran’s oil supply is shut down. OPEC supply drops by 4 BBD

PQd 067.5.94 PQs 082.5.49

Now factor that into the Supply/Demand Model

Variable

Market Price $94

Market Quantity (Bar/D)

88

Competitive SupplyDemand OPEC Supply

31sQ

94$

149.14

082.5.4931067.5.94

P

P

PP

QQ sd

8894067.5.94 dQ

Quantity

Price S

D

67$*P

90

'D

86 88

94$'P

Now, back to the original question. Suppose that Iran’s oil supply is shut down. OPEC supply drops by 4 BBD

Variable

Market Price $94

Market Quantity (BBD)

88

OPEC Quantity 31

Non-OPEC Quantity 57

The drop in OPEC supply pushes price up which gives non-OPEC countries the incentive to increase supply

Partial Equilibrium vs. General Equilibrium

Quantity

Price S

D

*P

*Q

'D

Suppose that effective advertising increased the demand for lemonade. What would happen.

A rise in demand should increase sales and increase the price right? Is that all?

Partial equilibrium deals with a disturbance in one market. General Equilibrium recognizes that markets interact with one another and looks at the interrelations between markets

Quantity

Price S

D

*P

*Q

'D

A rise in demand for lemonade should increase sales and increase the price.

Price

Quantity

D

S Price

Quantity

D

S

Sugar Lemons

The rise in lemonade sales should raise demand for lemons and sugar which increases their prices

This increase in marginal costs should lower supply, right!

Where would you rather live? South Bend or Chicago?

Why?

What’s better in Chicago?

Pretty much everything is better in Chicago!

What’s better in South Bend?

It’s cheaper in South Bend!

The indifference principle states that once everything is accounted for, every city must be equally desirable. Otherwise, who would choose to live in an inferior city.

Houses

S

D

000,86$

Houses

Median Home Price S

D

000,238$

South Bend Housing marketChicago Housing Market

Lets say that the key advantage to South Bend is its low housing costs. If Chicago was still preferred, South Bend residents would start moving to Chicago – this will magnify the benefits of South Bend (cheaper housing)

Median Home Price

The difference between housing costs should just offset any advantages Chicago has!

Renting vs. Buying a House….what’s the better move?

Houses

S

D

000,120$

Rentals

Median Rent

S

D

600$

South Bend Housing marketChicago Housing MarketMedian

Home Price

Suppose that the median rental rate is $600 per month ($7200 per year) and the current mortgage rate is 6%

000,120$06.

7200$P

Can you spot the housing bubble?

Question: Are we in an ‘Education Bubble”?

Can we really justify the rapidly rising costs of college tuition or are students getting in over their heads taking out loans that they will never be able to afford?

Employees

Salary

S

D

000,26$

Employees

Salary S

D

000,38$

Enrollment

Tuition

D

S

$15,000

High School Labor Force College Educated Labor Force

Universities

Can these markets be in equilibrium?

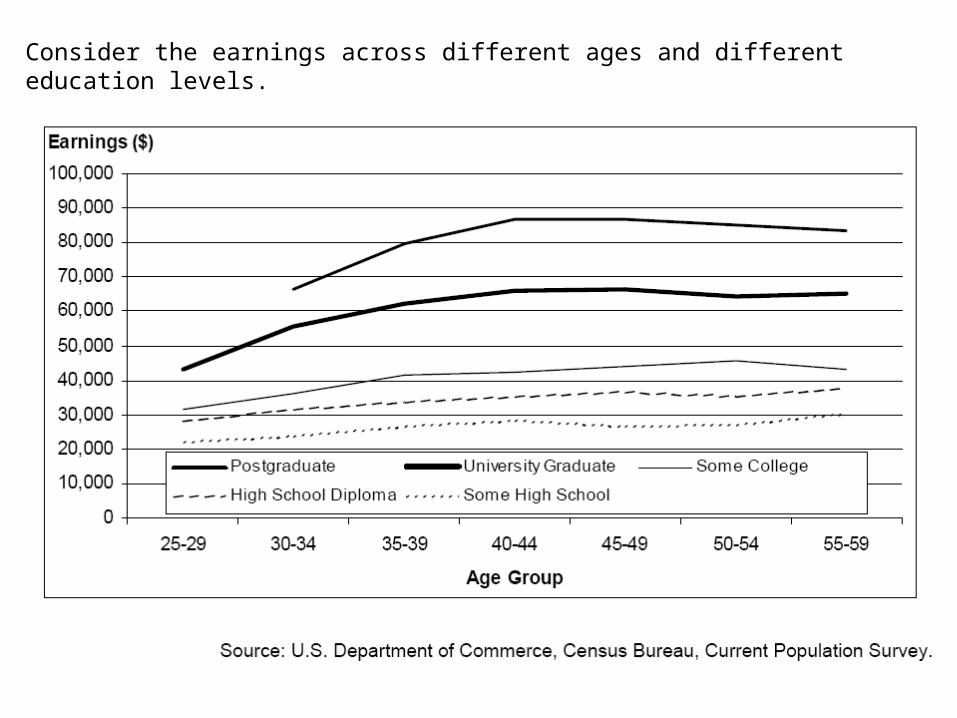

Consider the earnings across different ages and different education levels.

Age Group

Attainment 25-29 30-34 35-39 40-44 45-49 50-54 55-59

College $43,121 $55,440 $62,244 $65,973 $66,280 $64,254 $65,240

High School $28,097 $31,366 $33,443 $35,283 $36,316 $35,270 $37,573

Differential $15,024 $24,074 $28,801 $30,690 $29,964 $28,984 $27,667

x 5 = $75,120

x 5 = $144,005

x 5 = $153,450

x 5 = $149,820

x 5 = $144,920

x 5 = $138,335

x 5 = $120,370 =$926,020

This isn’t really right because you don’t get all this money up front

386,350$

05.1

667,27$...

05.1

024,15$

05.1

024,15$3954 PV

You receive the first payment 4 years from now

Lets assume that you could earn 5% elsewhere

What are the costs of going to college?

Cost Annual Expense

Tuition $15,000

Lost Wages $20,000

Books, Fees, etc $1,000

Room & Board $5,000

This is not a relevant cost…you would have paid this anyways!!!

$36,000 x 4 = $144,000Note: we really should discount these costs as well!

386,350$

05.1

667,27$...

05.1

024,15$

05.1

024,15$3954 PV

So, a college education costs $144,000 and yields $350,386 in (discounted) lifetime benefits! Seems worth it!

Alternatively, we can think about the annual salary differential for a college graduate like the annual payout on a bond. The annual return to a college education would be like calculating the return necessary so that the PV of the wage differential equals the cost

Cost Annual Expense

Tuition $15,000

Lost Wages $20,000

Books, Fees, etc $1,000$36,000 x 4 = $144,000

Note: we really should discount these costs as well!

000,144$

1

667,27$...

1

024,15$

1

024,15$3954

iiiPV

Annual return %11i

Thought of as an investment, a college education pays 11% per year!!

Employees

Salary

S

D

000,26$

Employees

Salary S

D

000,38$

Enrollment

Tuition

D

S

$15,000

High School Labor Force College Education Labor Force

Universities

If the costs of college were truly less than the benefits, we would see more people go to school

Wage differentials would fall and college tuitions would increase

Employees

Salary

S

D

000,26$

Employees

Salary S

D

000,38$

Enrollment

Tuition

D

S

$15,000

High School Labor Force College Education Labor Force

Universities

What we are seeing is a steady increase in demand for skilled labor as demand for unskilled labor falls

Wage differentials continue to increase as college tuitions increase

The Average Shopping cart in the US today is approximately three times as big as its 1975 counterpart

Ralph Nader has argued that this is a prime example of consumers being manipulated by unscrupulous capitalists – bigger carts shame consumers into bigger purchases.

What’s wrong with this argument?

Microsoft’s new Xbox 360 gaming console was released in North America on November 22 at a retail price of $299.99. Available supply sold out almost immediately as Christmas shoppers stood in line for this year’s hot item. (Microsoft has increased its sales target from 3M units to 6M units).

What’s odd about this??

On December 22, 2001, Richard Reid was arrested trying to blow up an American Airlines flight from Paris to Miami with a bomb hidden in his shoes.

Many human rights groups have fought heavily against the practice of racial profiling by airline security

Isn’t there a better way to secure the safety of our airplanes? (Hint: could we create a marketplace?)

Paul “Freck” Morgan started a website in 2001 offering a $20 Pay Per View event…..to watch him cut off his feet with a homemade guillotine.

Note: The site turned out to be a hoax…Paul never actually went through with it!

How should we feel about this entrepreneurial effort? (i.e. could we/should we repress this market?)

Related Documents