“The Michigan Model” Research Seminar in Quantitative Economics University of Michigan Ann Arbor, MI 48109 734-764-2567 Gabriel M. Ehrlich, Director lsa.umich.edu/econ/rsqe George A. Fulton & Saul H. Hymans Directors Emeriti THE U.S. AND MICHIGAN OUTLOOK FOR 2018-2020 PREPARED FOR PRESENTATION AT THE CONSENSUS REVENUE ESTIMATING CONFERENCE LANSING, MICHIGAN JANUARY 11, 2018 BY GABRIEL EHRLICH GEORGE FULTON DANIIL MANAENKOV MICHAEL MCWILLIAMS ADITI THAPAR

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

“The Michigan Model”

Research Seminar in Quantitative Economics University of Michigan Ann Arbor, MI 48109

734-764-2567

Gabriel M. Ehrlich, Director lsa.umich.edu/econ/rsqe

George A. Fulton & Saul H. Hymans Directors Emeriti

THE U.S. AND MICHIGAN OUTLOOK FOR 2018-2020

PREPARED FOR PRESENTATION AT THE CONSENSUS REVENUE ESTIMATING CONFERENCE

LANSING, MICHIGAN JANUARY 11, 2018

BY

GABRIEL EHRLICH GEORGE FULTON

DANIIL MANAENKOV MICHAEL MCWILLIAMS

ADITI THAPAR

Research Seminar in Quantitative Economics

The U.S. and Michigan Outlook for 2018–2020Consensus Revenue Estimating Conference

Lansing, MichiganJanuary 11, 2018

Current State of the Economy

RSQE: January 2018

Real Output GrowthSteady But Not Spectacular

Percent

RSQE: January 2018

High Business and Consumer Sentiment

RSQE: January 2018

Light Trucks Lead the WayAuto Sales are Weak

Millions of units sold, SAAR

0

5

10

15

20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Light Vehicles

Autos

Trucks

RSQE: January 2018

Unemployment RateTrending Down Since Around 2010

Percent

0

2

4

6

8

10

12

14

16

18

20

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

U-3 (headline) unemployment rate U-6 unemployment rate

RSQE: January 2018

Monthly Payroll Job GainsSlow Deceleration as Labor Market Tightens

Thousands

-1000

-800

-600

-400

-200

0

200

400

600

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

RSQE: January 2018

Healthy and Tightening Labor marketsPercent

RSQE: January 2018

Some Labor Market Slack RemainsPercent

RSQE: January 2018

Unspectacular Nominal Earnings Growth Even As Labor Markets Tighten

Percent

1

1.5

2

2.5

3

3.5

4

4.5

5

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Growth of hourly earning of production and nonsupervisory private sectoremployees

Growth of hourly earning of all private sector employees

Percent

RSQE: January 2018

Percent

Flat Real Earnings

RSQE: January 2018

Underlying Inflation Remains MutedPercent

Key Inputs into the Forecast

RSQE: January 2018

Federal funds rate path

• Latest rate hike in December, 2017

• Three 25 basis point hikes in 2018, two in 2019

New leadership at the Fed in 2017

• Jerome Powell is widely expected to be confirmed by the Senate as the next Fed chair

• We expect continuity in conduct of monetary policy

Monetary Policy

RSQE: January 2018

Market Interest Rates

0.4

1.21.5

2.0

2.5

3.0

2.12.4

2.5

3.03.3

3.53.8 3.9

4.1

4.64.9

5.1

0

2

4

6

2016 2017 2018 2019 2020

Forecast

Percent

3-Month T-bill

10 Year T-Note

Conv. Mortgage

RSQE: January 2018

Estimated $1.456 trillion in deficit increases over 2018-27• Using a “dynamic” score lowers the cost by about $385 billion

• Including extra interest payments adds $314 billion

• Growth impact likely front-loaded

Key business tax provisions, most are permanent:• Sharply lower corporate rate: to 21% down from 35%

• 100% investment expensing for 5 years

• International tax reform – significant revenue raiser

• Several common deductions are limited, also raising some revenue

Fiscal PolicyTax Cuts and Jobs Act (TCJA) Enacted

RSQE: January 2018

Personal tax provisions, most sunsetting in 2026:• Somewhat lower rates in most income brackets

• Lower rate on pass-through business income

• Expanded child tax credit

• ACA individual mandate penalty set to $0

By fiscal year 2019, budget deficit widens by over $200 billion

Busy January for Congress. We do not expect a shutdown

Infrastructure spending deal possible in 2018

Fiscal PolicyTax Cuts and Jobs Act (TCJA) Enacted

RSQE: January 2018

Federal Budget, NIPA Basis(Billions of Dollars)

FY’16 FY’17 FY’18 FY’19 FY’20Current receipts 3455.9 3557.3 3592.4 3708.2 3892.8 % change 1.8 2.9 1.0 3.2 5.0

Current expenditures 4116.7 4217.3 4398.0 4593.7 4792.7 % change 3.1 2.4 4.3 4.4 4.3 Consumption 963.9 971.4 992.2 1009.7 1026.6 % change 0.8 0.8 2.1 1.8 1.7 Transfer payments 2630.8 2693.5 2808.2 2920.7 3040.5 % change 3.4 2.4 4.3 4.0 4.1

Surplus (+) or deficit (-) -660.8 -660.0 -805.6 -885.5 -899.8 Percent of GDP -3.6 -3.4 -4.0 -4.2 -4.1

Forecast

RSQE: January 2018

Price of Oil(West Texas Intermediate Crude)

49.355.3

58.0 59.0 61.0 63.0

20

30

40

50

60

70

80

90

2016 2017 2018 2019 2020

Forecast

Dollars/Barrel

43.3

52.6

54.5

*Implicit deflator for petroleum & products

50.2

WTIImports*

16.95.1

12.221.8

6.712.7

3.42.0

3.31.8

4th Quarter to 4th Quarter % Change

56.5

RSQE: January 2018

2.22.6

2.1 1.8 1.7

6.7 6.8 6.5 6.3 6.2

0

2

4

6

8

10

2016 2017 2018 2019 2020

Five Foreign Economies* China

Percent

Foreign GDP Growth Rates

*Weighted Real GDP: Canada, Mexico, Japan, UK, Germany

RSQE: January 2018

Single-Family Home Prices(National Case-Shiller Index)

184.4

136.7

197.8

157.2

102.4

136.0

60

80

100

120

140

160

180

200

220

240

60

80

100

120

140

160

180

200

220

240

2000 2005 2010 2015 2020

Forecast

Index, 2000q1 = 100, SA

Nominal Index

Real Index

RSQE U.S. Forecast for 2018-20

RSQE: January 2018

Annual Real GDP Growth

1.5

2.32.6

2.31.9

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2016 2017 2018 2019 2020

Percent

RSQE: January 2018

Quarterly Real GDP Growth

1.8

3.2

2.7

2.3

2.01.8

0

1

2

3

4

2016 2017 2018 2019 2020

Forecast

1.8 2.5 2.4 2.1 1.84th Quarter to 4th Quarter Growth Rate of Real GDP (%)

Percent, AR

RSQE: January 2018

Nonfarm Payroll Employment Gains and Unemployment Rate

170 174 181167

132109

4.7

4.1 4.1 3.9 3.9 3.9

3

4

5

6

7

0

100

200

300

2016 2017 2018 2019 2020

Forecast

PercentThousands of Jobs per Month

2.3 2.0 2.1 1.8 1.54th Quarter to 4th Quarter Job Change (Millions)

Unemployment Rate

Avg. Monthly Job Gains*

* 1/3 the change in quarterly value

RSQE: January 2018

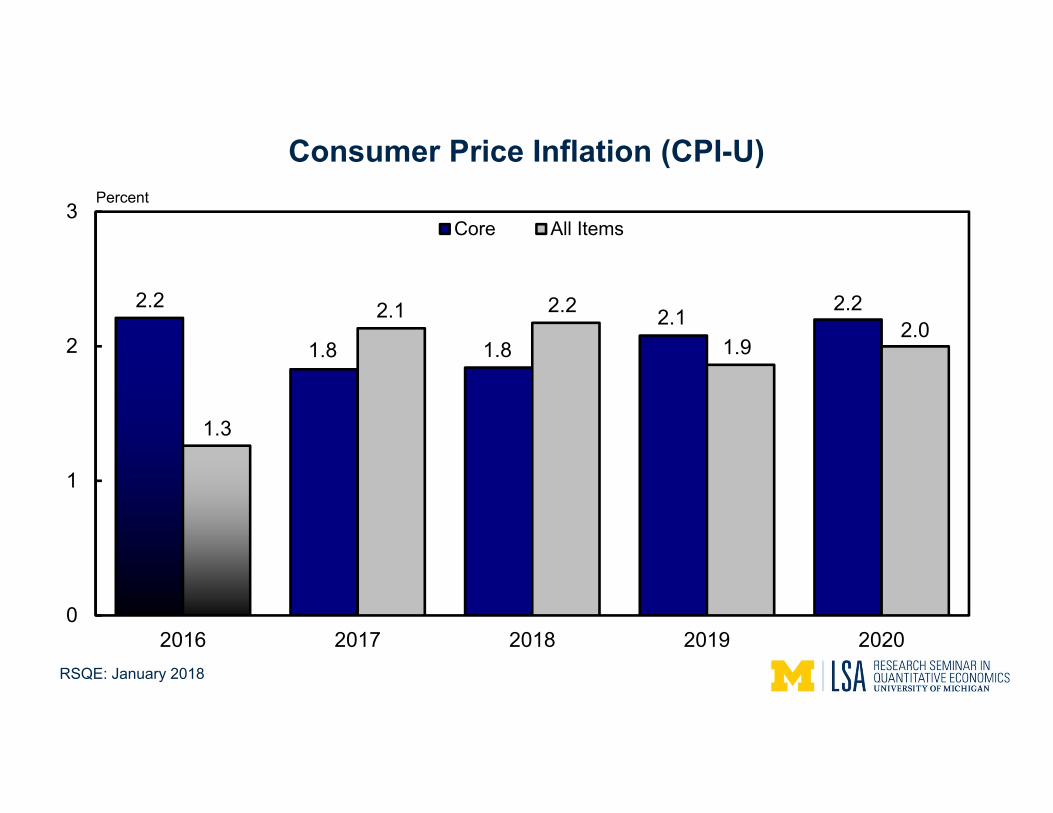

2.2

1.8 1.82.1 2.2

1.3

2.1 2.2

1.92.0

0

1

2

3

2016 2017 2018 2019 2020

Core All ItemsPercent

Consumer Price Inflation (CPI-U)

RSQE: January 2018

Level in 2016 (billions of chained 2009 dollars)EquipmentTotal Structures Intellectual Property

Growth of Nonresidential Fixed Investment

-0.6

4.7 4.63.8

3.2

-3.4

4.7 5.1

2.2 1.9

-4.1

5.3

3.1

4.8

3.1

6.3

4.15.1 5.2 5.0

-6

-4

-2

0

2

4

6

8

2016 2017 2018 2019 2020

Percent

2210.4 1047.8 446.4 720.4

RSQE: January 2018

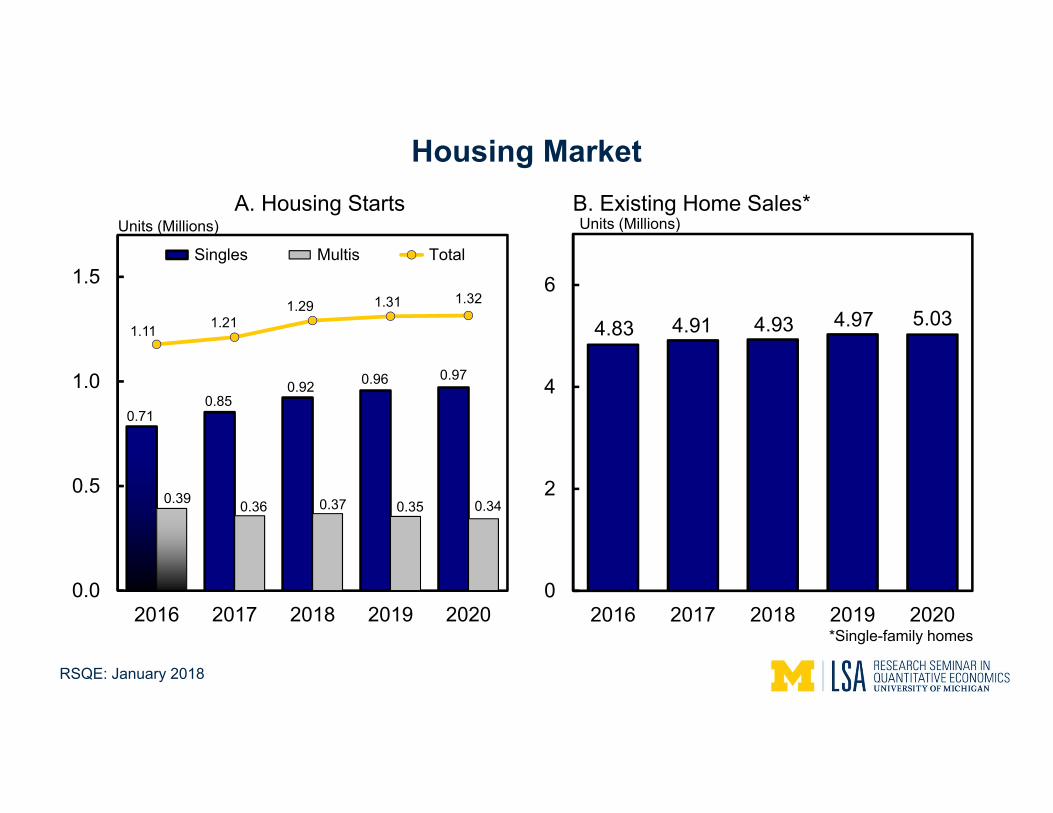

Housing Market

0.710.85

0.92 0.96 0.97

0.39 0.36 0.37 0.35 0.34

1.11 1.211.29 1.31 1.32

0.0

0.5

1.0

1.5

2016 2017 2018 2019 2020

Singles Multis Total

4.83 4.91 4.93 4.97 5.03

0

2

4

6

2016 2017 2018 2019 2020

A. Housing StartsUnits (Millions) Units (Millions)

B. Existing Home Sales*

*Single-family homes

RSQE: January 2018

6.96.1 5.9 5.6 5.4

10.6 11.1 11.4 11.5 11.7

17.5 17.2 17.3 17.1 17.1

0

4

8

12

16

20

2016 2017 2018 2019 2020

Autos Lt. Trucks Total

Units (Millions)

Light Vehicle Sales

RSQE: January 2018

Oil Prices and Geopolitical Risks

Fiscal Policy

Monetary Policy

Trade Policy

Abnormal weather

Risks to Our Outlook

Research Seminar in Quantitative Economics

The Michigan Economic Outlook For 2018–20

Consensus Revenue Estimating Conference

January 11, 2018

Motor Vehicle Industry Revisited

0

5

10

15

20

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

U.S. Light Vehicle Sales, 1990–2020Millions of Units

17

'91 '93 '95 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

RSQE: January 2018

17.5 17.2 17.3 17.1 17.1

7.5 7.2 7.3 7.2 7.2

02468

101214161820

2016 2017 2018 2019 2020

U.S. Light Vehicle SalesTotal vs. Detroit Three, 2016–20

Millions of Units

Total Detroit ThreeAnnual % Detroit Three

market share

42.742.1

42.342.0

42.2

RSQE: January 2018

Michigan Outlook

1.9

3.0

1.01.01.3

1.0 1.1 0.9

0

1

2

3

4

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 42016 2017 2018’15 2019 2020

1.5 2.3 1.0 0.9 1.1

62.1 96.8 44.1 41.6 51.7

4th Quarter to 4th Quarter Growth Rate (%)

4th Quarter to 4th Quarter Change (Thousands)1.1

49.8

Michigan Wage and Salary Employment GrowthAnnual Rate (%)

Forecast

RSQE: January 2018

2020 Census

Change in Payroll Employment by Industry Sector(Thousands of jobs)

Change in Payroll Employment by Industry Sector(Thousands of jobs)

2015q4–2016q4

2016q4–2017q4

2017q4–2018q4

2018q4–2019q4

Total jobs 97 44 42 50 52Manufacturing 9 2 -5 -2 -1

Trade, transportation, utilities 8 1 4 8 9Professional & business svcs. 22 14 18 18 18Construction 8 5 6 6 6

Leisure & hospitality 16 6 5 7 9Government 5 3 315 3

Private educ. & health svcs. 9 5 6 5 4

2019q4–2020q4

RSQE: January 2018

3

4

5

6

7

8

9

10

11

12

3,500

4,000

4,500

5,000

'91 '93 '95 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

Total Jobs(Thousands)

Sales(Millions of Units)

Michigan Total Jobs andDetroit Three Sales of Light Vehicles

1991 to 2020

Total jobsSales

Forecast

RSQE: January 2018

3,8003,9004,0004,1004,2004,3004,4004,5004,6004,7004,800

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Michigan Wage and Salary EmploymentFirst Quarter of 2000 to Fourth Quarter of 2020

Thousands of jobsForecastPeak ’00q2

Loss: ’00q2–’09q3 = 858,100

Trough ’09q3

’20q4

’17q3

Gain:’09q3–’20q4 = 722,700(84% of jobs lost)

RSQE: January 2018

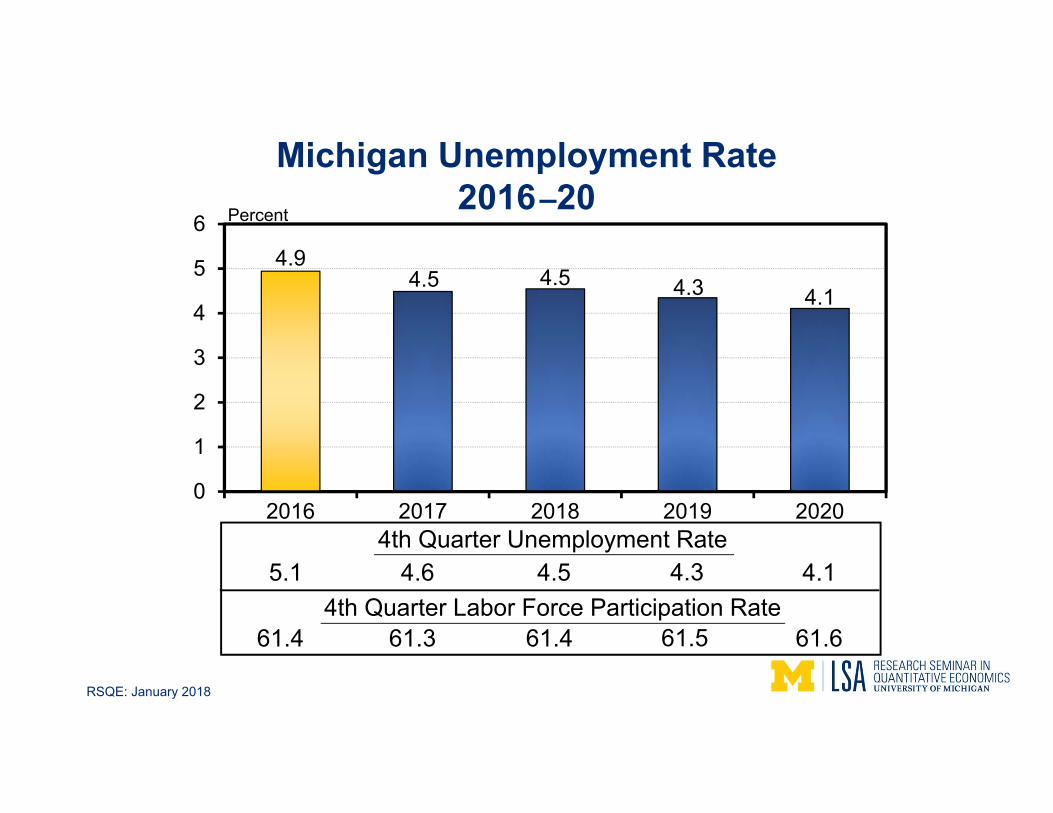

4.94.5 4.5 4.3 4.1

0

1

2

3

4

5

6

2016 2017 2018 2019 2020

Michigan Unemployment Rate2016–20Percent

5.1

61.4

4.6

61.3

4.5

61.4

4.1

61.6

4th Quarter Unemployment Rate

4th Quarter Labor Force Participation Rate4.3

61.5

RSQE: January 2018

Percent

Real Disposable Income

1.30.8

3.03.4

2.9

0

1

2

3

4

5

6

1.61.9 2.0

1.6 1.7

0

1

2

3

4

5

6

Michigan Inflation and Income Growth

Detroit CPI

Percent

2.8 2.8

4.7 4.8 4.8

0

1

2

3

4

5

6 Percent

Personal Income

2016 2017 2018 2019 2020

RSQE: January 2018

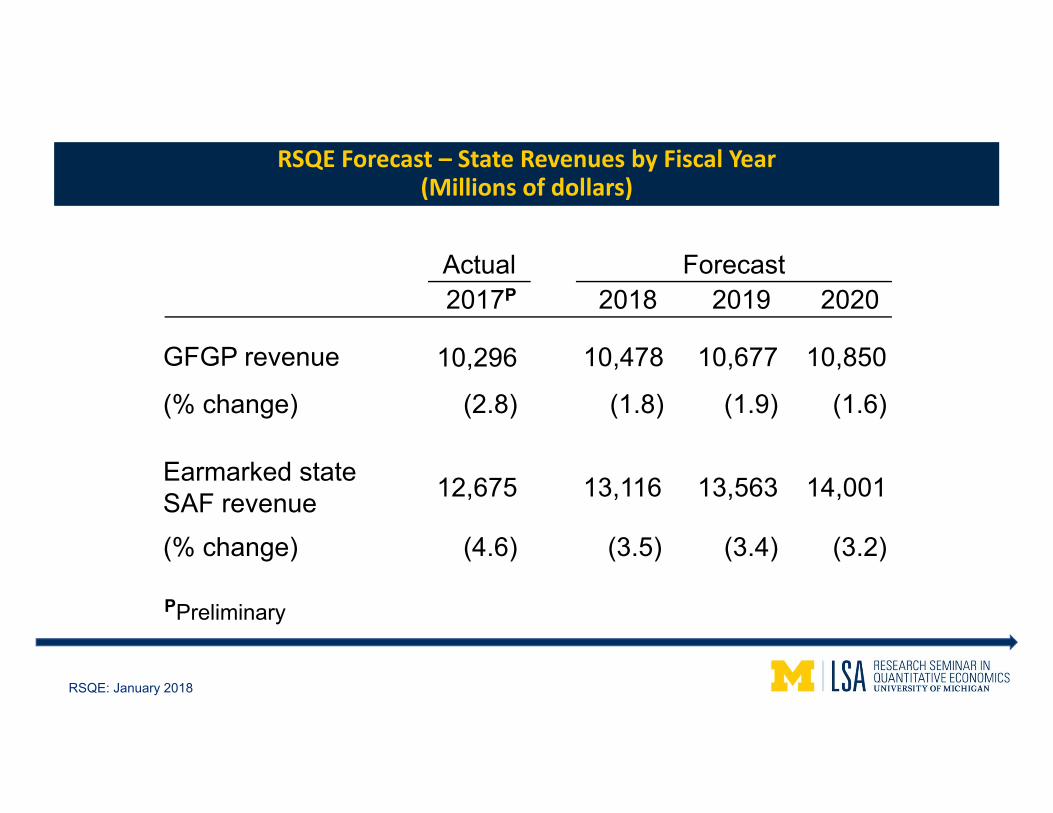

State Revenue Outlook

Actual Forecast2017P 2018 2019 2020

GFGP revenue

(% change)

10,296

(2.8)

10,478

(1.8)

10,677

(1.9)

10,850

(1.6)

Earmarked stateSAF revenue(% change)

12,675

(4.6)

13,116

(3.5)

13,563

(3.4)

14,001

(3.2)

PPreliminary

RSQE Forecast – State Revenues by Fiscal Year(Millions of dollars)

RSQE Forecast – State Revenues by Fiscal Year(Millions of dollars)

RSQE: January 2018

• Uncertainty about federal monetary & fiscal policy

• Risks associated with oil prices & the auto industry

• Potential effects of NAFTA withdrawal

Risks to the ForecastRisks to the Forecast

RSQE: January 2018

Simulating the Effects of Potential NAFTA Withdrawal

NAFTA Withdrawal AssumptionsNAFTA Withdrawal Assumptions

• Two scenarios: “soft” withdrawal and “hard” withdrawal

Soft HardTariffs Mexican and U.S. tariffs on

each other’s imports go to MFN levels

Retaliatory tariffs of 25% on imports of automobiles and parts;15% tariff on all other US exports

Effect on assemblies 520,000 light truck assemblies leave Mexico

600,000 light truck and 900,000‐1,000,000 auto assemblies leave Mexico

Peso Depreciates by 4% Depreciates by 10%Detroit Three Share Falls 0.6 percentage points Falls 1.8 percentage points

RSQE: January 2018

6.4

1.32.9 2.2

-7.0

-3.9

0.7

-3.8

-9-7-5-3-113579

Total Manufacturing Prof. & Bus.Svcs.

Other

Michigan Payroll Employment Effects of NAFTA Withdrawal Scenarios – 2020

Soft Withdrawal Hard Withdrawal

Thousands of Jobs

RSQE: January 2018

0.08

0.18

0.09

0.20

0.11

-0.24

-0.34

-0.25

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

Detroit CPI PersonalIncome

Real DisposableIncome

GFGP & SAFTaxes

Michigan Price, Income, and Tax Effects of NAFTA Withdrawal Scenarios – 2020

Percent

Soft Withdrawal Hard Withdrawal

RSQE: January 2018

lsa.umich.edu/econ/rsqelsa.umich.edu/econ/rsqe

Related Documents