The American Middle Class Under Stress Sherle R. Schwenninger and Samuel Sherraden New America Foundation April 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The American Middle Class Under Stress

Sherle R. Schwenninger and Samuel Sherraden

New America Foundation

April 2011

The American Dream is now to get

out of debt.

David Rosenberg

Chief Economist & Strategist, Gluskin Sheff

1

Tottering Pillars of America’s

Middle Class

1. Jobs and Wages

2. The Social Wage: Education, Health Care and Other Essential Goods

3. Wealth and Home Ownership

4. Retirement Security

5. Signs of Middle Class Decline

2

Jobs and Wages:

High Unemployment

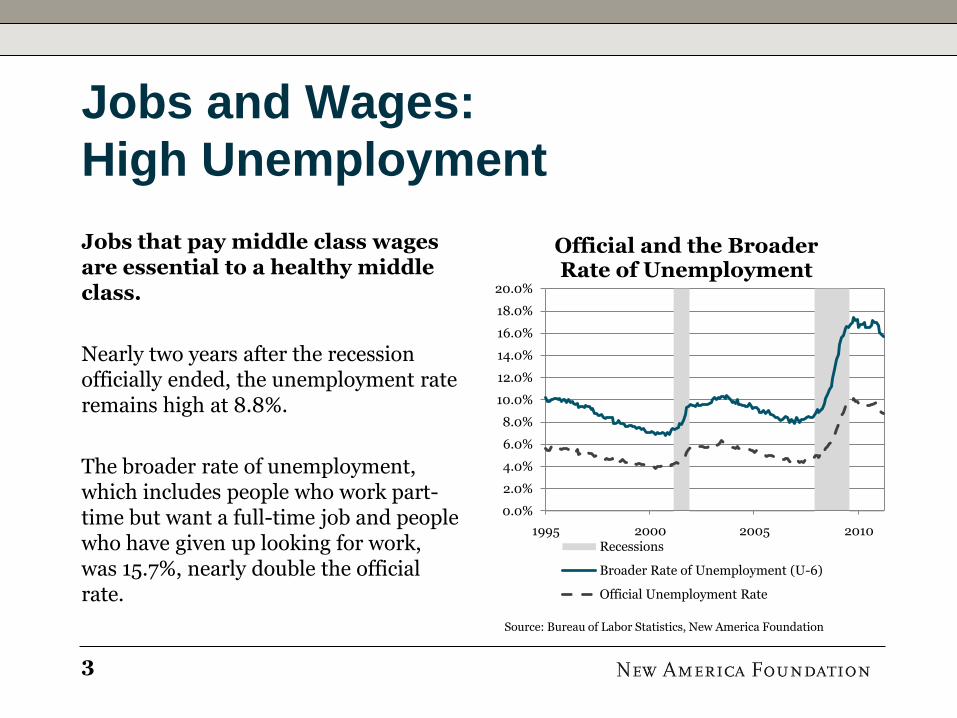

Jobs that pay middle class wages are essential to a healthy middle class.

Nearly two years after the recession officially ended, the unemployment rate remains high at 8.8%.

The broader rate of unemployment, which includes people who work part-time but want a full-time job and people who have given up looking for work, was 15.7%, nearly double the official rate.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

1995 2000 2005 2010

Official and the Broader Rate of Unemployment

Recessions

Broader Rate of Unemployment (U-6)

Official Unemployment Rate

Source: Bureau of Labor Statistics, New America Foundation

3

A Jobless Recovery

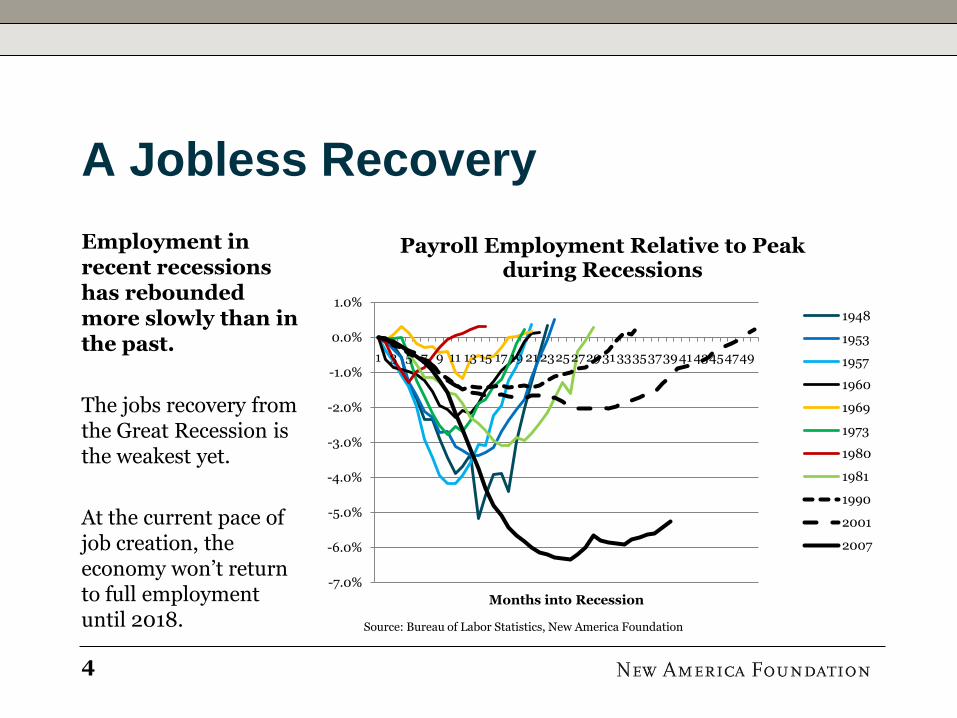

Employment in recent recessions has rebounded more slowly than in the past.

The jobs recovery from the Great Recession is the weakest yet.

At the current pace of job creation, the economy won’t return to full employment until 2018.

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

1 3 5 7 9 11 13 15 17 19 212325272931333537394143454749

Months into Recession

Payroll Employment Relative to Peak during Recessions

1948

1953

1957

1960

1969

1973

1980

1981

1990

2001

2007

Source: Bureau of Labor Statistics, New America Foundation

4

More of the Employed Have

Low-Income Jobs

Middle-income jobs are disappearing from the economy.

The share of middle-income jobs in the United States has fallen from 52% in 1980 to 42% in 2010.

Middle-income jobs have been replaced by low-income jobs, which now make up 41% of total employment.

0%

10%

20%

30%

40%

50%

60%

1980 1985 1990 1995 2000 2005 2010

Share of Total Employment

Private Sector Middle-Income

Private Sector Low-Income

Government Jobs

Source: Bureau of Labor Statistics, Westwood Capital

5

The Under-Employed American

The problem is not lack of skills, but the structure of the job market.

17 million Americans with college degrees are doing jobs that require less than the skill levels associated with a bachelor’s degree.

Just under 30% of flight attendants and 16% of telemarketers have bachelor’s degrees even though this credential is not necessary for these jobs.

OccupationPercent with

BA/BS Number

Waiter/Waitress 13.4 317,759

Flight Attendants 29.8 29,645

Laborers 5.07 118,441

Janitors 5.01 107,457

Truck Drivers 5.09 85,205

Bartenders 16 80,542

Food Preparation 7.24 63,737

Telemarketers 15.85 54,713

Postmen/women 13.95 49,452

Parking Lot Attendants 13.74 18,749

Source: Bureau of Labor Statistics

6

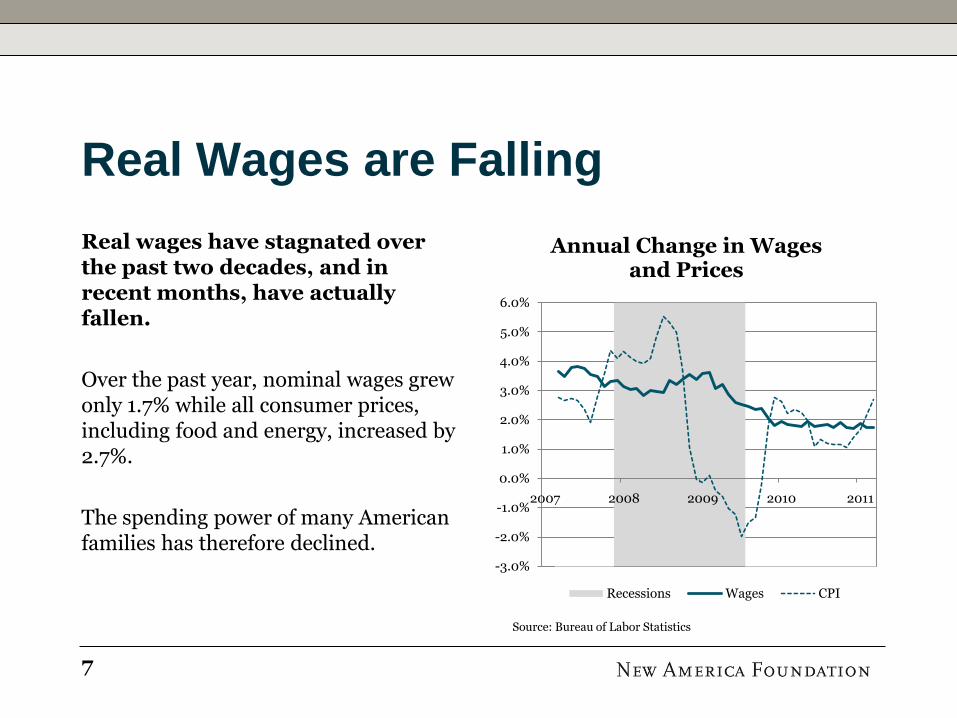

Real Wages are Falling

Real wages have stagnated over the past two decades, and in recent months, have actually fallen.

Over the past year, nominal wages grew only 1.7% while all consumer prices, including food and energy, increased by 2.7%.

The spending power of many American families has therefore declined.

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2007 2008 2009 2010 2011

Annual Change in Wages and Prices

Recessions Wages CPI

Source: Bureau of Labor Statistics

7

Government Transfers Have Partly

Offset the Stagnation of Wages

Wages and salaries have fallen from 60% of personal income in 1980 to 51% in 2010.

Government transfers have risen from 11.7% of personal income in 1980 to 18.4% in 2010, a post-War high.

There are 8.5 million people receiving unemployment insurance and over 40 million receiving food stamps.

0%

10%

20%

30%

40%

50%

60%

70%

1980 1985 1990 1995 2000 2005 2010

Share of Personal Income

Wages and Salaries

Government Transfers

Source: Bureau of Economic Analysis, New America Foundation

8

The Erosion of the Social Wage:

Rising Health Expenditures

Despite an increase in government transfers, America’s social wage has been eroded by the rising cost of health care and education.

Health care spending increased from 9.5% of personal consumption in 1980 to 16.3% in 2010.

Many households cannot afford rising insurance premiums and out-of-pocket health care costs, leaving nearly 50 million Americans without adequate health coverage.

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

1980 1985 1990 1995 2000 2005 2010

Health Care Spending as a Share of Personal

Consumption

Source: Bureau of Economic Analysis

9

Higher Education is Not

Affordable

A college education is considered necessary to get a good job, but for many families college is no longer affordable.

The average cost of one year of college is $21,000. After adjusting for inflation, it has risen 72% since 1990.

For households with incomes at the 40th and 60th percentiles, one year of college tuition makes up 54% and 40% of their annual income, respectively. 0%

10%

20%

30%

40%

50%

60%

1980 1985 1990 1995 2000 2005 2010

Cost of 1 year of College Tuition as a Share of Annual

Household Income

60th Percentile of Income

40th Percentile of Income

Source: US Census Bureau, National Center for Education Statistics

10

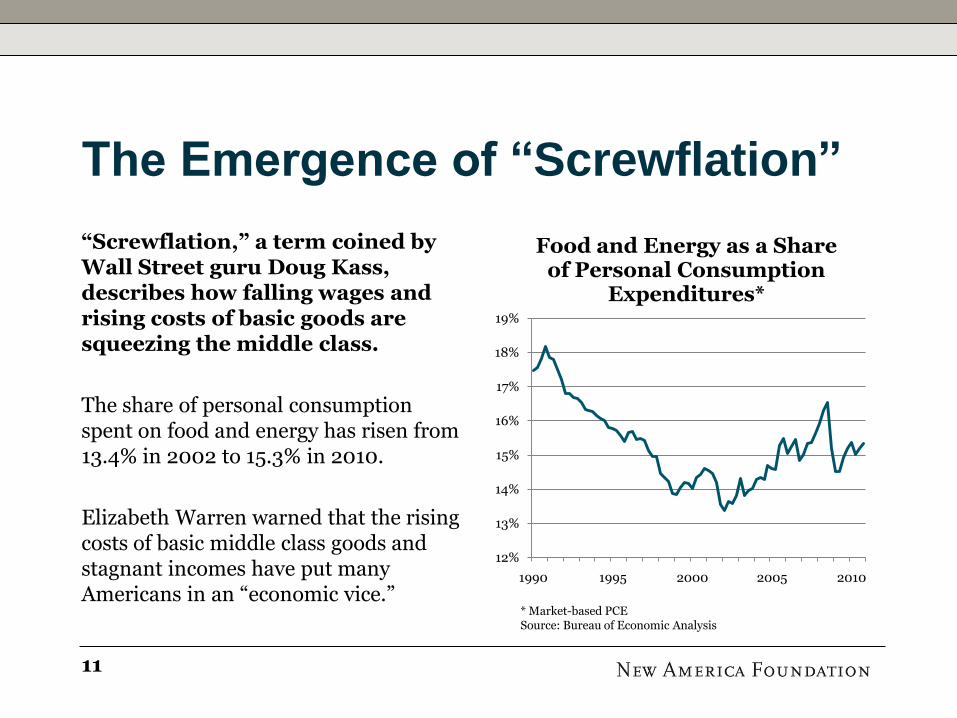

The Emergence of “Screwflation”

“Screwflation,” a term coined by Wall Street guru Doug Kass, describes how falling wages and rising costs of basic goods are squeezing the middle class.

The share of personal consumption spent on food and energy has risen from 13.4% in 2002 to 15.3% in 2010.

Elizabeth Warren warned that the rising costs of basic middle class goods and stagnant incomes have put many Americans in an “economic vice.”

12%

13%

14%

15%

16%

17%

18%

19%

1990 1995 2000 2005 2010

Food and Energy as a Share of Personal Consumption

Expenditures*

* Market-based PCESource: Bureau of Economic Analysis

11

The Great Recession Dealt a Blow

to Middle Class Wealth

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

US

D b

illi

on

s

Household Net Worth

Source: Federal Reserve

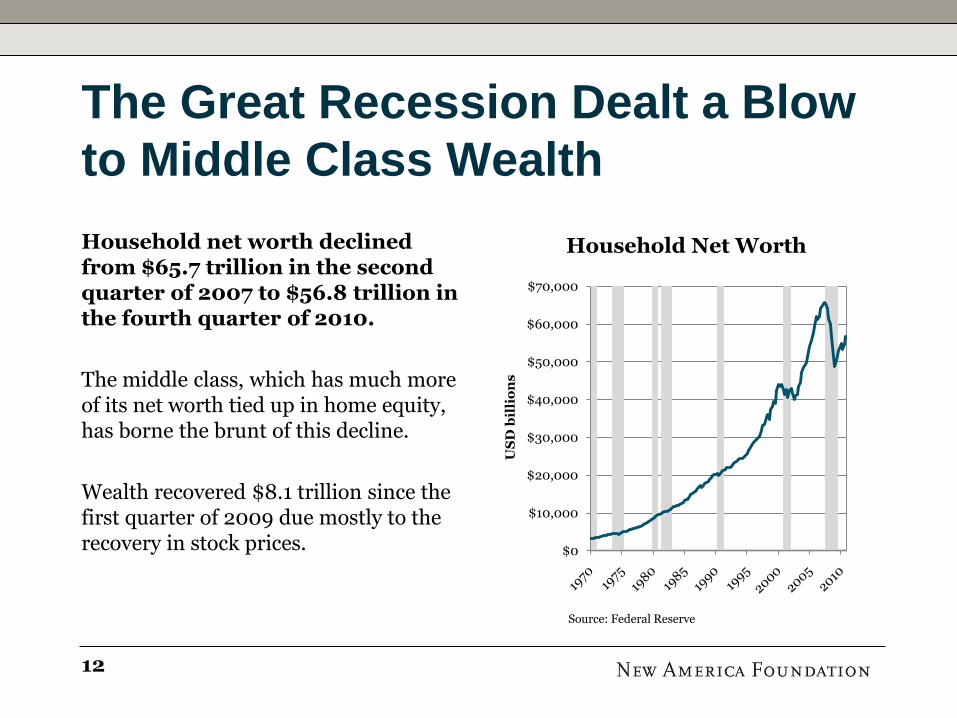

Household net worth declined from $65.7 trillion in the second quarter of 2007 to $56.8 trillion in the fourth quarter of 2010.

The middle class, which has much more of its net worth tied up in home equity, has borne the brunt of this decline.

Wealth recovered $8.1 trillion since the first quarter of 2009 due mostly to the recovery in stock prices.

12

Home Equity and Wealth

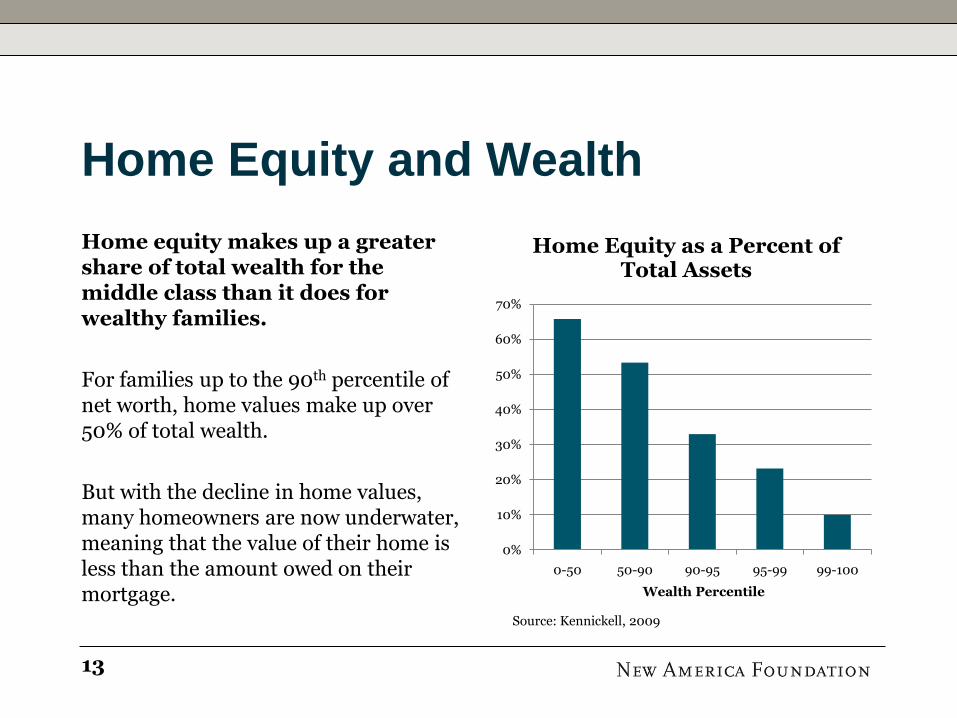

Home equity makes up a greater share of total wealth for the middle class than it does for wealthy families.

For families up to the 90th percentile of net worth, home values make up over 50% of total wealth.

But with the decline in home values, many homeowners are now underwater, meaning that the value of their home is less than the amount owed on their mortgage.

0%

10%

20%

30%

40%

50%

60%

70%

0-50 50-90 90-95 95-99 99-100

Wealth Percentile

Home Equity as a Percent of Total Assets

Source: Kennickell, 2009

13

Uneven Recovery:

Stocks & Home Prices

40

50

60

70

80

90

100

110

120

130

2006 2007 2008 2009 2010 2011

Equity and Home Prices Diverge

S&P 500 Case-Shiller Home Price Index

Source: Standard and Poors, New America Foundation

Equity markets have recovered much of their losses, but housing prices have not.

While the outlook in the equity market is uncertain, housing prices have resumed their decline and could fall another 10% to 20%, due to the pressure from the shadow inventory.

At the end of 2010, 23.1% of all residential properties with a mortgage were underwater, with total negative equity nationwide of $750 billion.

14

Deleveraging Remains a Painful

Reality

Over the past three decades, household debt as a share of disposable income increased from 68% to 116%.

Households have begun to pay down debt, but have a long way to go to get back to the 1990s average of 85% of disposable income.

0%

20%

40%

60%

80%

100%

120%

140%

1980 1985 1990 1995 2000 2005 2010

Household Debt as a Share of Disposable Income

Source: Federal Reserve, Bureau of Economic Analysis

1990-1999 = 85%

1980-1989 = 70%

Average 2000-Present = 114%

15

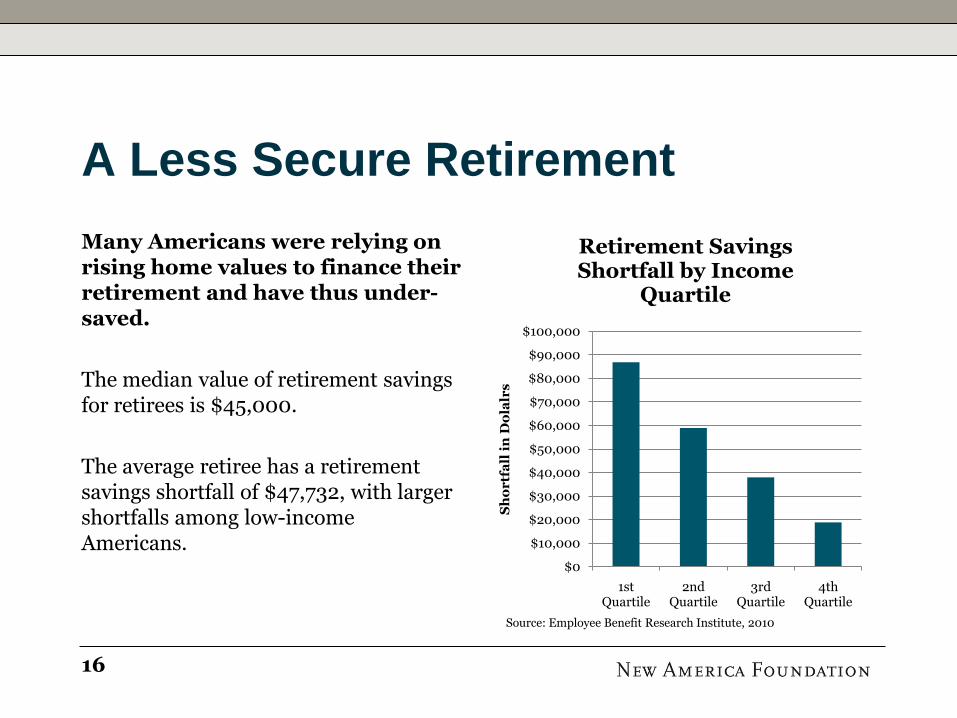

A Less Secure Retirement

Many Americans were relying on rising home values to finance their retirement and have thus under-saved.

The median value of retirement savings for retirees is $45,000.

The average retiree has a retirement savings shortfall of $47,732, with larger shortfalls among low-income Americans.

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

1st Quartile

2nd Quartile

3rd Quartile

4th Quartile

Sh

or

tfa

ll i

n D

ola

lrs

Source: Employee Benefit Research Institute, 2010

Retirement Savings Shortfall by Income

Quartile

16

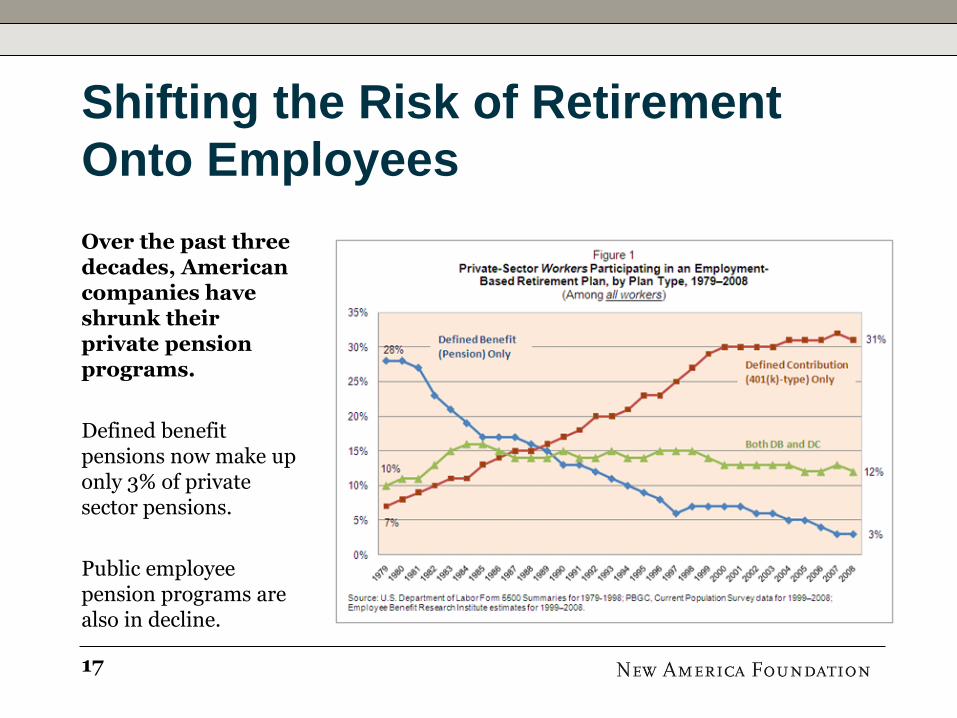

Shifting the Risk of Retirement

Onto Employees

Over the past three decades, American companies have shrunk their private pension programs.

Defined benefit pensions now make up only 3% of private sector pensions.

Public employee pension programs are also in decline.

17

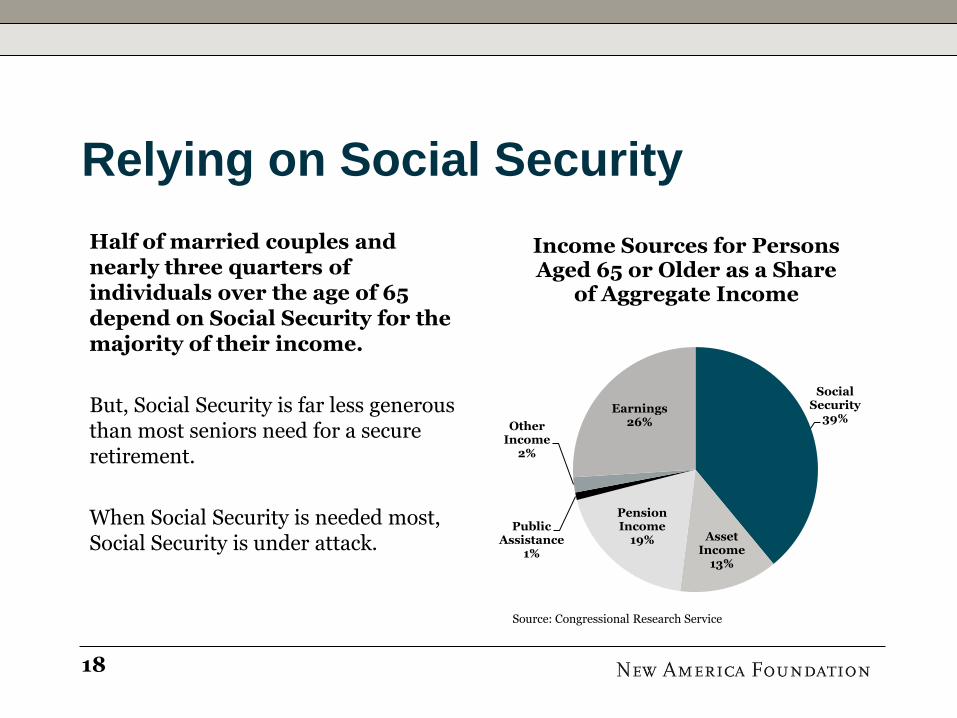

Relying on Social Security

Social Security

39%

Asset Income

13%

Pension Income

19%Public

Assistance1%

Other Income

2%

Earnings26%

Income Sources for Persons Aged 65 or Older as a Share

of Aggregate Income

Source: Congressional Research Service

Half of married couples and nearly three quarters of individuals over the age of 65 depend on Social Security for the majority of their income.

But, Social Security is far less generous than most seniors need for a secure retirement.

When Social Security is needed most, Social Security is under attack.

18

Signs of Middle Class Decline:

More at the Top, Less for the Middle

The top 1% of income earners in the United States account for 21% of aggregate income.

The wealthiest 1 percent own about 35% of the nation’s wealth.

The top 20% of income earners account for nearly 40% of total consumption.

0%

5%

10%

15%

20%

25%

30%

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Income Share of the Top 1% of Earners*

* Including capital gainsSource: Top Incomes Database, UC Berkeley

19

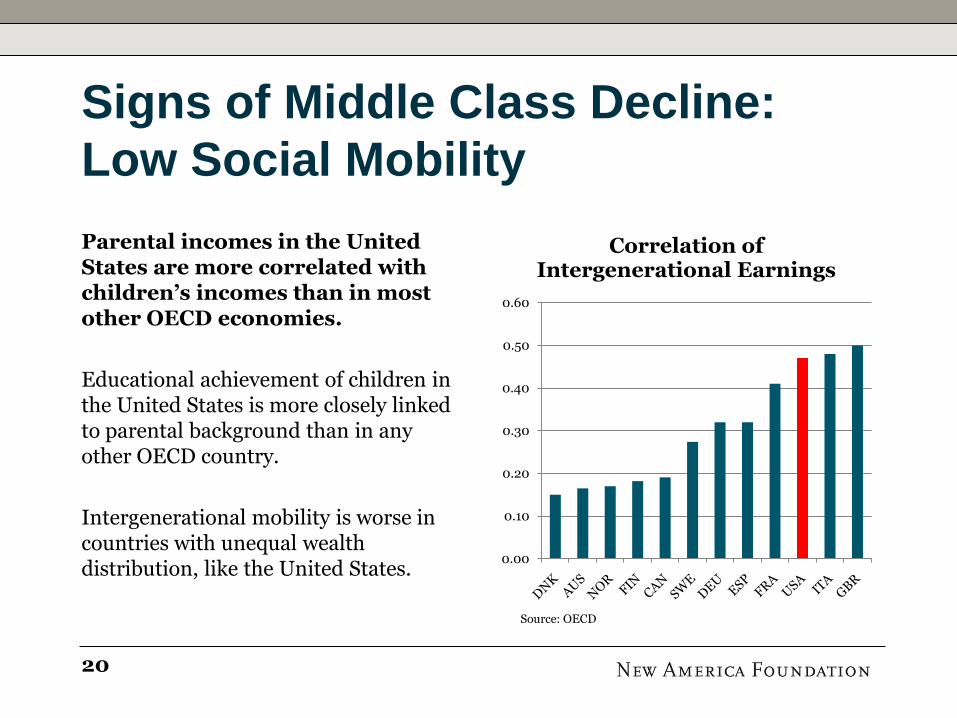

Signs of Middle Class Decline:

Low Social Mobility

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Correlation of Intergenerational Earnings

Source: OECD

Parental incomes in the United States are more correlated with children’s incomes than in most other OECD economies.

Educational achievement of children in the United States is more closely linked to parental background than in any other OECD country.

Intergenerational mobility is worse in countries with unequal wealth distribution, like the United States.

20

Related Documents