The Age of Reason: Financial Decisions Over the Lifecycle Sumit Agarwal Federal Reserve Bank of Chicago John Driscoll Federal Reserve Board Xavier Gabaix NYU and NBER David Laibson Harvard and NBER The views expressed in this paper are not necessarily those of the Federal Reserve Bank of Chicago or of the Federal Reserve Board. May 2008

The Age of Reason: Financial Decisions Over the Lifecycle Sumit Agarwal Federal Reserve Bank of Chicago John Driscoll Federal Reserve Board Xavier Gabaix.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Age of Reason:Financial Decisions Over the Lifecycle

Sumit Agarwal Federal Reserve Bank of Chicago

John Driscoll Federal Reserve Board

Xavier Gabaix NYU and NBER

David Laibson Harvard and NBER

The views expressed in this paper are not necessarily those of the Federal Reserve Bank of Chicago or of the Federal Reserve Board.

May 2008

“Performance” peaks.

• Baseball: 29 (James 2003)• Mathematicians, theoretical physicists, and lyric poets:

early 30s (Simonton 1988). • Chess players: mid-30s (Charness and Bosman 1990). • Autocratic rulers: early 40s (Simonton 1988). • Novelists: 50 (Simonton 1988).• Economists?

– 20s (Hamermesh and Oster 1998)– Nobel-Prize-winners (Weinberg & Galenson 2005)

• “Conceptual” laureates: 43• “Experimental” laureates: 61

Our findings:

• Financial “performance” rises then declines with age• Performance:

– negotiate low (borrowing) interest rates– pay fewer fees

• This regularity is confirmed for 10 separate types of financial choices

• On average, financial performance peaks at age 53

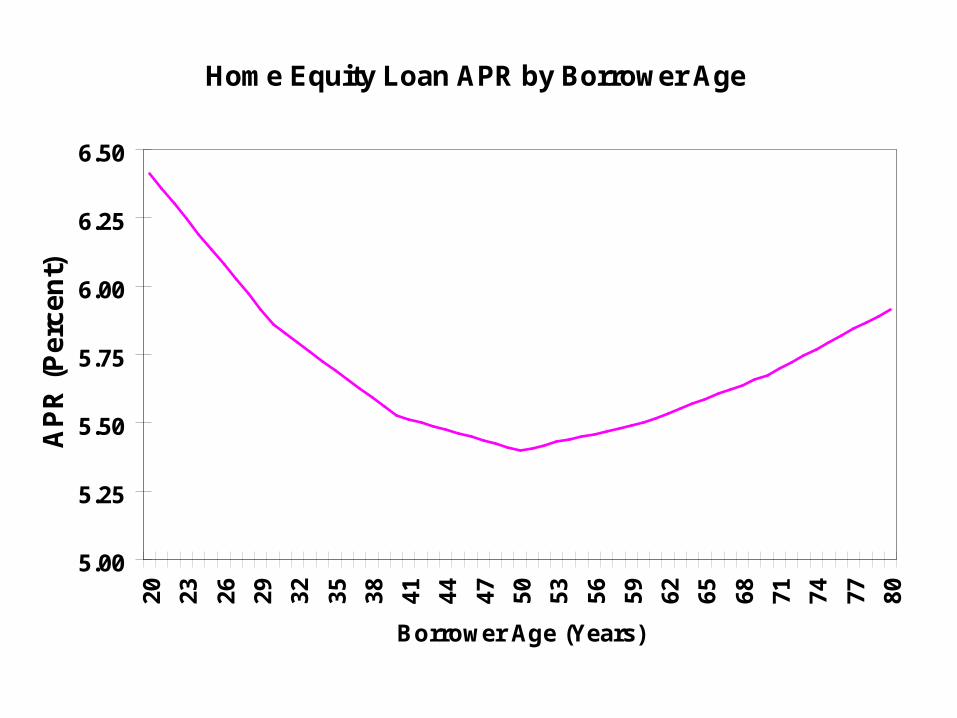

(1,2) Home Equity Loans and Home Equity Credit Lines

• Proprietary data from large financial institutions• 75,000 contracts for home equity loans and lines of

credit, from March-December 2002• We observe:

– Contract terms: APR and loan amount– Borrower demographic information: age, employment status,

years on the job, home tenure, home state location– Borrower financial information: income, debt-to-income ratio– Borrower risk characteristics: FICO (credit) score, loan-to-value

(LTV) ratio

Home Equity Loan APR by Borrower Age

5.00

5.25

5.50

5.75

6.00

6.25

6.5020 23 26 29 32 35 38 41 44 47 50 53 56 59 62 65 68 71 74 77 80

Borrower Age (Years)

AP

R (

Pe

rce

nt)

Home Equity Credit Line APR by Borrower Age

4.00

4.25

4.50

4.75

5.00

5.25

5.5020 23 26 29 32 35 38 41 44 47 50 53 56 59 62 65 68 71 74 77 80

Borrower Age (Years)

AP

R (

Pe

rce

nt)

(3) “Eureka”: Learning to Avoid Interest Charges on Balance Transfer Offers

• Balance transfer offers: borrowers pay lower APRs on balances transferred from other cards for 6-9 months

• New purchases on card have higher APRs• Payments go towards balance transferred first, then

towards new purchases• Optimal strategy: make no new purchases on card to

which balance has been transferred

Eureka: Predictions

• Borrowers may not initially understand card terms• Borrowers learn about terms through usage

– We will see “eureka” moments: new purchases on balance-transfer cards drop to zero in the month after borrowers “figure out” how to optimize

• Study: 14,798 balance transfer accounts over the period January 2000 to December 2002

Fraction of Borrowers in Each Age Group Experiencing a Eureka Moment, by Month

0%

10%

20%

30%

40%

50%

60%

18 to 24 25 to 34 35 to 44 45 to 64 Over 65Borrower Age Category

Per

cen

t o

f B

orr

ow

ers

Month One Month TwoMonth Three Month FourMonth Five Month SixNo Eureka

(4,5,6) Fee payments

• We examine payments of three types of credit card fees:– Late payment fees– Over credit limit fees– Cash advance fees

• We again see U-shaped patterns by age• The opportunity cost model (younger and older adults

have more time to avoid fees) would predict the opposite pattern

• 3.9 million month-borrower observations on credit card purchases from January 2002 through December 2004

Frequency of Fee Payment by Borrower Age

0.15

0.17

0.19

0.21

0.23

0.25

0.27

0.29

0.31

0.33

0.352

02

32

62

93

23

53

84

14

44

75

05

35

65

96

26

56

87

17

47

78

0

Borrower Age (Years)

Fe

e F

req

ue

nc

y (

pe

r m

on

th)

Late Fee

Over Limit Fee

Cash Advance Fee

(7) Auto Loans

• Proprietary data from several large financial institutions• 6,996 loans for purchase of new and used autos• We observe:

– Contract terms: APR and loan amount– Borrower demographic information: borrower age

and state of residence– Borrower financial information: income, debt-to-

income ratio– Borrower risk characteristics: FICO score– Automobile characteristics: value, age, model, make

and year.

Auto Loan APR by Borrower Age

8.00

8.25

8.50

8.75

9.00

9.25

9.50

Borrower Age (Years)

AP

R (

Pe

rce

nt)

(8) Credit Card APRs

• Proprietary data from a large financial institution that issues credit cards nationally

• 128,000 accounts over a 36 month period from 1/2002 to 12/2004

• We observe:– Card terms: APR, fees paid– Borrower risk information: FICO (credit) score, card balances,

other debt– Borrower demographic information: age, gender, income

Credit Card APR by Borrower Age

17.00

17.25

17.50

17.75

18.00

18.25

18.502

02

32

62

93

23

53

84

14

44

75

05

35

65

96

26

56

87

17

47

78

0

Borrower Age (Years)

AP

R (

Pe

rce

nt)

(9) Mortgage APRs

• Proprietary data from a large financial institution that originates first mortgages in Argentina

• 4,867 fixed-rate, first-mortgage loans on owner-occupied properties between June 1998 and March 2000

• We observe:– Contract terms: APR and loan amount– Borrower demographic information: age, employment status,

years on the job, home tenure, home location– Borrower financial information: income, debt-to-income ratio– Borrower risk characteristics: Veraz (credit) score, loan-to-value

(LTV) ratio

Mortgage APR by Borrower Age

11.50

11.75

12.00

12.25

12.50

12.75

13.002

02

32

62

93

23

53

84

14

44

75

05

35

65

96

26

56

87

17

47

78

0

Borrower Age (Years)

AP

R (

Pe

rce

nt)

(10) Small Business Credit Card APRs

• Proprietary data set from several large financial institutions that issue small business credit cards nationally

• 11,254 accounts originated between 5/2000 and 5/2002• Most businesses are small and owned by single families• We observe:

– Credit card terms: APR– Borrower demographic information: age– Borrower risk information: credit score, total number

of cards, total card balance– Business information: years in business

Small Business Credit Card APR by Borrower Age

14.50

14.75

15.00

15.25

15.50

15.75

16.00

20

23

26

29

32

35

38

41

44

47

50

53

56

59

62

65

68

71

74

77

80

Borrower Age (Years)

AP

R (

Pe

rce

nt)

U-shape for financial mistakes in 10 examples

– Home equity loans – Home equity lines of credit– Eureka moments for balance transfers– Late payment fees– Over credit limit fees– Cash advance fees– Auto loans– Credit cards– Small business credit cards– Mortgages

US: Rising Role of DC PlansPrivate-Sector Workers

1979 1990 2004

Only10%

30%

50%

70%

Pension type (as a proportion of all pensioned workers)

Only

Breakdown of Retirement Assets in US Market (year-end 2007)

Total US Retirement Assets: $17.4 trillion

Pension plans forGovernment Employees:

$4.4 trillion

Private pension plans: $13.0 trillion

IRA: $4.6 trillionDC: $4.4 trillion

Annuities: $1.6 trillion

DB Assets:$2.4 trillion

Other Assets:$10.6 trillion

Source: ICI, December 2007

Most Retirement Savings is inIndividual Accounts

Total US Retirement Assets: $17.4 trillion

All DB Pensions $4.6 trillion

Individual accounts: $12.8 trillion

Source: ICI, December 2007

$100 bills on the sidewalkChoi, Laibson, Madrian (2004)

• Employer match is an instantaneous, riskless return on investment

• Particularly appealing if you are over 59½ years old

– Have the most experience, so should be savvy

– Retirement is close, so should be thinking about saving

– Can withdraw money from 401(k) without penalty

• We study seven companies and find that on average, half of employees over 59½ years old are not fully exploiting their employer match

– Average loss is 1.6% of salary per year

• Educational intervention has no effect

Conclusion• U-shape for mistakes in all 10 examples• Others have confirmed this pattern in their data sets:

– Fiona Scott-Morton (auto loans)– Luigi Guiso (portfolio choice)– Lucia Dunn (credit cards)

• Implications for public policy– 401(k)’s– IRA rollover accounts– Annuitization– Medicare, especially Part D– Social Security Privatization– Regulation of financial advisors

Related Documents