98 JOURNAL OF GLOBAL MANAGEMENT JULY 2011. VOLUME 2. NUMBER 1 THE ACCOUNTANTS’ ETHICAL CODE OF CONDUCT FROM AN ISLAMIC PERSPECTIVE: CASE IN YEMEN Al-Hasan Al-Aidaros PhD Student in Accounting College of Business, Universiti Utara Malaysia. [email protected] Kamil Md. Idris Associate Professor College of Business, Universiti Utara Malaysia [email protected] Faridahwati Mohd. Shamsudin Senior Lecturer College of Business, Universiti Utara Malaysia [email protected] ABSTRACT An ethical code of conduct is developed to guide behaviors of members in or of organizations. Accountants, in this context, are not an exception. The availability of such ethical code of conduct is extremely important for both accountants and users of accounting information. However, currently in Yemen, there is no ethical code of conduct for Yemeni professional accountants. Hence, a study was conducted to develop an ethical code of conduct for Yemeni professional accountants from an Islamic perspective, given that Yemen is an Islamic country. In particular, the study sought to address the question of what constitutes the ethical code of conduct among Yemeni professional accountants. To address the question, data were collected from 386 users of accounting information in four main cities of Yemen i.e. Sana’a, Hadhramout, Taiz, and Aden. The participants were asked to indicate their expectations about what should be included in the ethical code conduct for Yemeni professional accountants. The study employed interdependency analysis, specifically exploratory factor analysis, to reveal the domains of ethical code of conduct. Results show that the ethical code of conduct consists of seven constructs, i.e. acting responsibly, honoring the public trust, acting with integrity, maintaining objectivity and independence, exercising due care, following the limits of scope and nature of services, and complying with A’del, Sabr, and Ihsan principles. The findings could be used by policy makers to develop an ethical code of conduct for Yemeni accountants to assist them with their professional work. In addition, recommendations for future research and the limitations of the study are highlighted. Keywords: Ethical code of conduct, Professional accountants, Islamic perspective, Yemen. ----------------------------------------------------------------------------------------------------------------------------------

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

98 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

THE ACCOUNTANTS’ ETHICAL CODE OF CONDUCT FROM AN ISLAMIC

PERSPECTIVE: CASE IN YEMEN

Al-Hasan Al-Aidaros

PhD Student in Accounting

College of Business, Universiti Utara Malaysia.

Kamil Md. Idris

Associate Professor

College of Business, Universiti Utara Malaysia

Faridahwati Mohd. Shamsudin

Senior Lecturer

College of Business, Universiti Utara Malaysia

ABSTRACT

An ethical code of conduct is developed to guide behaviors of members in or of organizations.

Accountants, in this context, are not an exception. The availability of such ethical code of conduct is

extremely important for both accountants and users of accounting information. However, currently in

Yemen, there is no ethical code of conduct for Yemeni professional accountants. Hence, a study was

conducted to develop an ethical code of conduct for Yemeni professional accountants from an Islamic

perspective, given that Yemen is an Islamic country. In particular, the study sought to address the

question of what constitutes the ethical code of conduct among Yemeni professional accountants. To

address the question, data were collected from 386 users of accounting information in four main cities of

Yemen i.e. Sana’a, Hadhramout, Taiz, and Aden. The participants were asked to indicate their

expectations about what should be included in the ethical code conduct for Yemeni professional

accountants. The study employed interdependency analysis, specifically exploratory factor analysis, to

reveal the domains of ethical code of conduct. Results show that the ethical code of conduct consists of

seven constructs, i.e. acting responsibly, honoring the public trust, acting with integrity, maintaining

objectivity and independence, exercising due care, following the limits of scope and nature of services,

and complying with A’del, Sabr, and Ihsan principles. The findings could be used by policy makers to

develop an ethical code of conduct for Yemeni accountants to assist them with their professional work. In

addition, recommendations for future research and the limitations of the study are highlighted.

Keywords: Ethical code of conduct, Professional accountants, Islamic perspective, Yemen.

----------------------------------------------------------------------------------------------------------------------------------

99 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

1.0 INTRODUCTION

Researchers found that accountants operate within a world of change in which corporate collapses,

business impropriety, regulatory failure and environmental disasters are prevalent. It is said that the

professional accountants were partly responsible in the collapse of several companies in the world such

as Enron, WorldCom, Global Crossing in the United States, Parmalat in Italy, One-Tel in Australia,

Almanakhah Market in Kuwait, and the Yemeni National Commercial Bank in Yemen, because their role

is to detect mistakes, frauds and to make sure that financial information, i.e. balance sheet and income

statement, are prepared according to accounting and moral/ethical standards (Martin, 2007). It can be

argued that accountants need to have a thorough appreciation of the potential implications of

professional and management decisions, and an awareness of the pressures in observing and upholding

ethical standards, which may confront individuals involved in a decision making process (Ahadiat, 1993;

Burks, 2006; Mohammed, 2008). In this respect, professional accountants have responsibility to protect

stakeholders by presenting fair and independent opinions about financial statements, because if they do

not do so, stakeholders may not be able to derive at a valid conclusion and hence make a correct

decision.

As the name suggests, an ethical code of conduct is defined by the International Federation of

Accountants (IFAC) as: “principles, values, standards, or rules of behavior that guide the decisions,

procedures and systems of an organization in a way that (a) contributes to the welfare of its key

stakeholders, and (b) respects the rights of all constituents affected by its operations” (IFAC, 2007). An

ethical code of conduct is important because stakeholders expect professional accountants to comply

with it (Delaney, 2005). Ziegenfuss and Singhapakdi (1994) found that the ethical code of conduct

influences professional accountants because they believe it guides their work. The ethical code of

conduct is also said to have more effect on professional accountants than personal moral philosophies

(Delaney, 2005). Professional accountants, like other professionals, need to comply with the ethical code

of conduct because non-compliance results in penalties (England, 1998). So, the ethical code of conduct

is an effective tool that can increase public trust in the financial reports prepared by professional

accountants (England, 1998). Whilst the main objective of the ethical code of conduct is to uphold the

integrity of accounting profession, it benefits stakeholders as well. Users of accounting information can

make decisions by using financial reports that are reliable, and professional accountants can use it as a

guide to help them in their work (Street, 2002).

Because of its significance in guiding behaviors, an ethical code of conduct for professional accountants

in Yemen can contribute toward improving the economic situation of the country. But no such ethical

code of conduct for Yemeni accountants exists (Bamashmos, 2003). Because Yemen is a Muslim country

governed by Islamic Shari’ah laws, professional accountants here are presumed to have good ethical

conducts. However, to what extent this claim is valid and holds true is subject to a scientific

investigation. And this is what the present study intends to achieve. In particular, this study attempts to

reveal what should constitute the ethical code of conduct among Yemeni professional accountants from

an Islamic perspective.

2.0 PROBLEM STATEMENT

Accountants’ behavior affects the public through the preparation of financial reports. Users of financial

report, especially decision makers, expect professional accountants to be highly competent, reliable,

and objective. Those who work in the field of accounting must not only be well qualified but must also

possess a high degree of professional integrity (Burks, 2006; Mohammed, 2008). Therefore,

100 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

accountant’s ethics are very important because the main role of accountants is to provide useful

information to users (Rahman, 2003).

At present there is no ethical code of conduct for Yemeni professional accountants in Yemen (Al-Ariqi,

2007; Alshami, 2009). The absence of this code allows accountants to interpret what constitute ethics

according to their own personal interests or values (Mohammed, 2008). It has been said that Yemeni

accountants accept bribes (Hasan, 2010), do not act responsibly to users of accounting information

(Baahroon, 2010), are careless about public interest (Zaid, 2010), work in collaboration with others

(Baantar, 2010), and sometimes do not follow Islamic principles (Ali, 2010; Mohammed, 2010). As a

result, reports produced by Yemeni accountants may be defected and unreliable. Because there is no

ethical code of conduct for Yemeni professional accountants (Alshami, 2010), Yemeni government

cannot force accountants to follow any specific behaviors.

Users of accounting information, i.e. investors, managers, members of board of directors, members of

Yemeni accountants association, and legislators and senior officials in Yemeni government believe that

an ethical code of conduct for Yemeni professional is imperative (Alkebsi, 2010; Alshami, 2010). This is

because they will not be able to make a right and good decision without reliable, accurate, and trusted

accounting information (Alaidaros, 2010; Ibrahim, 2010; Mustafa, 2010). Besides, the users feel that

they have no legal recourse for mistakes done by accountants because there is no ethical code of

conduct that specifies penalties for any wrongdoing (Bageneed, 2010; Bendool, 2010).

The Yemeni government is trying to meet several conditions and terms of Arab Gulf countries in order to

enter the Gulf union (YACPA, 2010). Making an ethical code of conduct for professional accountants

available is one of the terms that need to be met (Alkebsi, 2010; Alshami, 2010). Given these contexts, it

is necessary to know what constitutes ethics under the Islamic environment like Yemen. This study will

develop accountants’ ethical code of conduct for the benefit of users of financial reports.

3.0 PREVIOUS STUDIES ON THE ETHICAL CODE OF CONDUCT

An ethical code of conduct can be understood in different ways. An ethical code of conduct is seen as a

social agreement between the public and accountants. The accountants’ ethical code of conduct is

established to influence positively users of accounting information, i.e. investors, employees, lenders,

suppliers, customers, government, and management (Payne & Landry, 2005). Therefore, in this

perspective, accountants have responsibility to perform with the highest level of integrity and

objectivity (Bay, 1997). Alternatively, the ethical code of conduct is a means for the accounting

profession to regulate its own members and the code is thus viewed as the accountants’ way of self-

protection (Parker, 1994). In addition, the ethical code of conduct is seen as a required component of

accountants’ job (Bay, 1997). Finally, the ethical code of conduct is viewed as an accountants’ attempt

to offer for them guiding principles to assist them in formulating correct choices in complex

circumstances (Brecht, 1991).

The first major code for the accounting profession is the ethical code of conduct established by the

American Institute of Certified Public Accountants (AICPA) (Abo-ahmeed, 2006; Brown, 1999; Brown et

al., 2007; Duska & Duska, 2003; Mele, 2005; SOCPA, 2009; Venezia, 2005). Several countries such as

Taiwan, Canada, Saudi Arabia, and Jordan, have developed their own codes by using the AICPA code as a

prototype. In line with this development, the present study used the AICPA code as a basis for

organizing thoughts as well as developing accountants’ ethical code of conduct from an Islamic

perspective in Yemen.

101 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

The AICPA ethical code of conduct consists of six principles. These are explained and discussed below:

Acting responsibly means accountants, in carrying out their responsibilities as

professionals, should exercise sensitive professional and moral judgments in all their

activities (AICPA, 2009). From an Islamic perspective, however, the strength of mind of

what is useful and what is harmful cannot be left to human being reasoning alone. Human

beings’ reasoning should be exercised within the Islamic framework (Al-Qaradawi, 1985).

This means that Islam recognizes the role of reason in theorizing morality and ethics only

in a manner that confirms human existence. The reason for that is because the natural

limitations of human beings posit a strong reason for Divine direction particularly in

determining what is right and what is wrong. According to Al-Qaradawi (1985), the

rational faculties can and should only be used to match and strengthen ethics and

morality defined by Islamic Shari`ah. Within an Islamic framework, responsibilities can be

divided into three groups. First is responsibility towards God, who created human beings

and provided them with resources for their livelihoods. Second is responsibility towards

themselves. Third is responsibility towards society which involves maintenance of clients’

rights and goods, and treating everything that belongs to a consumer, his honor, his

wealth and his blood, as sacrosanct (Saeed, Ahmed, & Mukhtar, 2001). In this context, an

accountant must uphold all responsibilities towards God, him/herself, and society. Allah

(s.w.t) said: “Then shall anyone who has done an atom’s weight of good, see it. And

anyone who has done an atom’s weight of evil, shall see it” (al-Quran, 99:7/8).

Honoring the public trust is means accountants should accept the obligation to act in a

way that will serve the public interest, honor the public trust, and demonstrate

commitment to professionalism (AICPA, 2009). Islam agrees with the principle of public

interest and considers it more important than an individual interest (Al-Qaradawi, 1994).

However, a professional accountant must make sure public interests are in line with

Islamic Shari’ah. This is because some societies, according to relativism theory, consider

some actions such as bribery as ethical. In Islam, the only one who really has full

knowledge about what is right and wrong is Allah (s.w.t). The Quran (58:7) states: “Allah

has full knowledge of all things”. Even if the majority of people in this world agree that

taking bribe is acceptable for the public interest, Muslims accountants condemn this act

as not being ethical and Islamic. Allah (s.w.t) said: “if you follow the common run of those

on earth, they will lead you away from the way of Allah; they follow nothing but

conjecture” (al-Quran, 6:116).

Acting with integrity is to maintain and broaden public confidence. Accountants should

perform all professional responsibilities with the highest sense of integrity. Islam supports

this principle, i.e. integrity, for all professionals and non-professionals (Mohammed,

2005). Moreover, Muslims must behave with integrity by holding Iman (faith), as it is the

key that protects and increases a person’s integrity (Al-Qaradawi, 1994, 1985; Mawdudi,

1977). In Islam, a person has to behave in accordance to his/her Islamic beliefs as

mentioned in the Quran.

Maintaining objectivity and independence means that an accountant should be objective

in his/her work and be free from conflicts of interest in discharging his/her professional

responsibilities. An accountant in public practice should be independent in fact and

appearance when providing auditing and other attestation services (AICPA, 2009). Islam

102 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

also requires that accountants be objective and exercise independence in their opinions

without any bias (Mohammed, 2005). Allah (s.w.t) has ordered Muslims to behave fairly

with every Muslims and non-Muslims even if the person may hate him/her for doing

justice. The Quran said justice is the shortest way to achieve Iman (faith). “Be obvious

determinedly for Allah, as witnesses to fair dealing, and do not let the hate of others to

you make you swerve to wrong and depart from justice. Be just: that is next to

faithfulness” (al- Quran, 5:8). Besides, Muslims are requested to verify any information

received especially if it may affect the others negatively. Allah (s.w.t) said: “If a wicked

person comes to you with any news, ascertain the truth, lest you harm people unwittingly

and afterwards become full of repentance for what you have done” (al-Quran, 49:6). In

other word, before make any judgment, a professional accountant must make sure that

he/she has verified the information as correct and accurate.

Exercising due care by means an accountant should observe the profession’s technical and

ethical principles, try hard continually to develop competence and the quality of services,

and discharge professional responsibility to the best of the accountant’s ability (AICPA,

2009). Islam agrees with the general idea of due care principle (Mohammed, 2005). But

there are other Islamic issues related to the due care principle that are not mentioned in

the AICPA code. Firstly, accountants should perform their duty beyond the expectation of

clients because for all Muslim accountants life should be perfect as possible (Al-Qaradawi,

1994). Also, accountants believe that reward in the next life is more important than the

reward in this life such as fees or salary. Thus, professional accountants are expected to

carry out their work as best as possible not for the sake of salary or fees only. However,

that does not mean accountants should be paid lower than what they deserve. Justice

must be exercised in determining fees and rules (Mohammed, 2005). In other words,

Muslim must emulate the prophet Muhammad’s way of life in all aspects be they

economical, political, or social. Allah (s.w.t) has promised those who make perfect their

life with reward in hereafter (al-Quran, 16:30, 10:26). Also, the prophet Muhammad

reported that: “when any of you perform a work: Allah wants him to do it perfectly”

(Mohammed, 2005).

Following the limits of scope and nature of services means that accountants in public

practice should observe the principles of the code of professional conduct in determining

the scope and nature of services to be provided (AICPA, 2009). In Islam, the government

and the experts are the two groups that are legitimate in identifying the scope and nature

of services. With regard to the first group, Allah (s.w.t) has ordered Muslims to obey their

leaders. Besides Allah and his prophet Muhammad. The Quran (4:59) said: “you who

believe: Obey Allah, and obey the messenger, and those charged with authority among

you”. However, to obtain obedience, the government should practice Islamic principles

throughout (al-Quran, 4:59). In regard to the second group, i.e. accounting organization,

Allah (s.w.t) said that Muslims consult the experts who have knowledge about the thing

that they do not know (al-Quran, 21:7). In general, Islam agrees with this principle, i.e.

scope and nature of services, except that the accountants must reject any work if it is

against Islamic principles (al-Quran, 5:47). The scope and nature of services must be

within the acceptable limits of Islam (al-Quran, 5:44/45).

103 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

In brief, the code of professional accountants serves a variety of purposes both to professional

accountants and society. It is intended to appeal to such diverse interests of customers, the public, the

courts, business community, the accounting profession, and the government. These interests will

converge and at other times, diverge. Therefore, the code must anticipate the individualistic and

pluralistic relationships that exist among any or all of these interests. The above six principles are related

to the four philosophies of Western ethical theories: egoism, utilitarianism, deontology, and virtue

ethics. Western ethical philosophies provide a supplemental theoretical basis for ethical judgment in

accounting practices. Although each ethical philosophy alone fails to sufficiently guide accountants in

every ethical situation, collectively they provide a menu of principles that accountants can and should

consider when facing ethical dilemmas (Burks, 2006; Velasquez, 2006). However, while Islam generally

agrees to the principles laid out by the AICPA’s ethical code of conduct, the code remains incomplete.

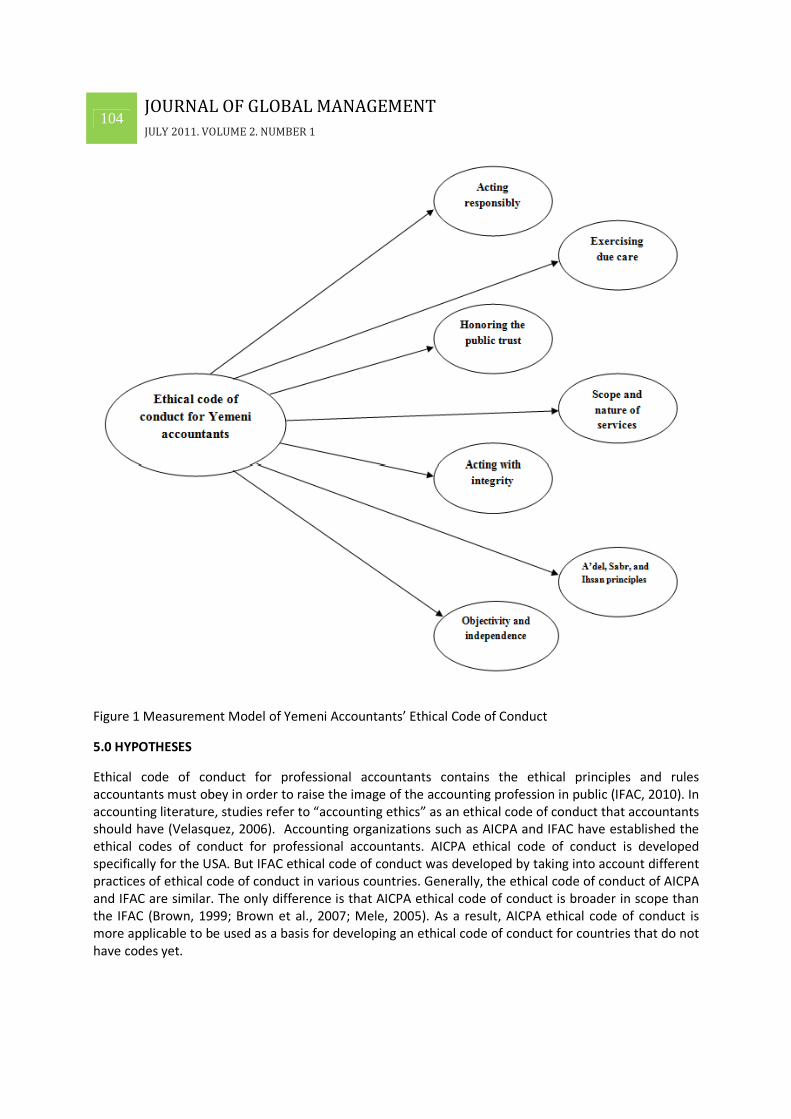

4.0 THEORETICAL FRAMEWORK

Based on previous review concerning AICPA ethical code of conduct, there are six principles, i.e. (1)

acting responsibly, (2) honoring the public trust, (3) acting with integrity, (4) maintaining objectivity and

independence, (5) exercising due care, and (6) establishing limits to the scope and nature of services

provided. Arab countries such as Jordan and Gulf countries, i.e. Saudi Arabia, Kuwait, Qatar, Bahrain,

Oman, and United Arab Emirates, are examples for countries following the same way of AICPA. These

principles are acceptable from an Islamic perspective. However, the current codes, such as AICPA code

and IFAC code, are not completely following Islamic perspective.

This study suggesting adds a new principle, i.e. complying with A’del, Sabr, and Ihsan principles, to

extend the existing code of conduct so that it is following Islamic perspective. In other word, the study

will develop a more comprehensive ethical code of conduct than AICPA ethical code of conduct by adopt

the same principles with adding a new principle, i.e. complying with A’del, Sabr, and Ihsan principles.

Therefore, the proposed measurement model for this study, which reflect Islamic perspective, will

contain seven constructs i.e. (1) acting responsibly, (2) honoring the public trust, (3) acting with

integrity, (4) maintaining objectivity and independence, (5) exercising due care, (6) following limits to

the scope and nature of services provided, and (7) complying with A’del, Sabr, and Ihsan principles.

Figure 1 shows the proposed measurement model for variables of every construct for the ethical code of

conduct.

104 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Figure 1 Measurement Model of Yemeni Accountants’ Ethical Code of Conduct

5.0 HYPOTHESES

Ethical code of conduct for professional accountants contains the ethical principles and rules

accountants must obey in order to raise the image of the accounting profession in public (IFAC, 2010). In

accounting literature, studies refer to “accounting ethics” as an ethical code of conduct that accountants

should have (Velasquez, 2006). Accounting organizations such as AICPA and IFAC have established the

ethical codes of conduct for professional accountants. AICPA ethical code of conduct is developed

specifically for the USA. But IFAC ethical code of conduct was developed by taking into account different

practices of ethical code of conduct in various countries. Generally, the ethical code of conduct of AICPA

and IFAC are similar. The only difference is that AICPA ethical code of conduct is broader in scope than

the IFAC (Brown, 1999; Brown et al., 2007; Mele, 2005). As a result, AICPA ethical code of conduct is

more applicable to be used as a basis for developing an ethical code of conduct for countries that do not

have codes yet.

105 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Because of its breadth, the researchers used AICPA ethical code of conduct as a basis to develop an

Islamic ethical code of conduct for Yemeni professional accountants. Although the AICPA ethical code of

conduct has been widely used by many countries, it still has room for continuous improvement

especially if it is to apply to Muslim countries. As discussed earlier is the code not extensive and

comprehensive enough from the Islamic perspective. The main difference is on the basis of identifying

what is right and wrong. Islam has a comprehensive point of view (al-Banna, 1940, al-Qaradawi 1996;

Yaken, 2006) of ethical issues by taking a full image of all theoretical standards. In addition, justice in

Islam is not the only basis to differentiate what is right and wrong. Sabr (patience) is another basis that

Islam considers. The Quran said: “and if you do catch them out, catch them out no worse than they

catch you out: But if you show patience, that is indeed the best (course) for those who are patient”

(16:126). Another basis is Ihsan (better, i.e. treat people better that how they treat you). The Quran

said: “Nor can goodness and evil be equal. Repel (evil) with what is better” (41:34). However, Islamic

principles are not against logical theories even if they are developed by non-Muslim scientists (al-

Qaradawi, 1996; Mawdudi, 1977).

The code with only six constructs is still considered Islamic because it emphasizes the values and

principles that Islam shares with the Western understanding (SOCPA, 2009). However, it does not

completely follow the Islamic perspective because there are other principles need to be added such

A’del, Sabr, and Ihsan. In addition, the Western ethical code of conduct does not have any problem with

some forbidden activities in Islam such as the loan interest (riba). Besides the six constructs, Islam also

gives attention to other elements, which are Iman (faith), consistency between principles and actions,

compliance with Quran and Sunnah, and focus on reward in the hereafter. Some of these elements have

been added to the Islamic ethical code of conduct.

The ethical code of conduct that developed in this study is an Islamic ethical code of conduct for several

reasons. First, all the constructs studied are based on the Islamic resources, i.e. the Quran and Sunnah.

Second, even though the study brought six constructs from Western framework/studies, the explanation

and the understanding of these constructs are not completely same. For example, the construct of

“honoring the public trust” means an accountant must act to meet the society’s interest that is

Islamically acceptable. In Islam, an accountant must not take interest (riba) even if the society thinks it is

the right thing to do. This is because interest (riba) is forbidden in Islam (al-Gazali, 2001; Al-Qaradawi,

1996; al-Quran, 2:278/279). Third, this study added a new Islamic construct to the ethical code of

conduct, i.e. the construct of “complying with A’del, Sabr, and Ihsan principles”. This construct

emphasizes the basic Islamic values that were not mentioned in the Western ethical codes of conduct.

As an example of the items that added to the Islamic ethical code of conduct, accountant should act

with sufficient knowledge on the Islamic Shari’ah regarding accounting profession to avoid recording any

action that is not acceptable in Islam. Another example, accountant should demonstrate a good model

on how a good accountant should behave according to Islamic ethics. Fourth, because the study is

conducted in Muslim country, it assumes that Iman (faith) is part of every construct. For example, in

Islam an accountant is not solely responsible to users of accounting information, but he/she is first and

foremost accountable and responsible to Allah (s.w.t) and then to others, i.e. users of accounting

information, accounting profession, and society (Mohammed, 2008). The responsibility to Allah (s.w.t)

means accountant has an ethical obligation to act and work to achieve the acceptance of the Creator,

i.e. Allah (s.w.t) (Mohammed, 2005) by following the guidance in the Quran and Sunnah.

The construct of “complying with A’del, Sabr, and Ihsan principles” added to the ethical code of conduct

in this study is very important as it significantly differentiates the code from the conventional one. The

106 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

addition is important as it emphasizes the values that Islam stresses to be incorporated in the daily

Muslim life. For example, with respect to Ihsan, it refers to the highest level of make things perfectly and

with the highest level of believing in Allah (s.w.t) (Mohammed, 2005). When an accountant has practices

Ihsan, it means that he/she is encouraged to provide perfect services beyond the expectations of the

users of accounting information (Al-Qaradawi, 1994; Mohammed, 2005).

Another example of the Islamic values is A’del. A’del is to give everyone his/her rights regardless of

his/her race, religion, financial level, and job (al-Gazali, 2001; Al-Qaradawi, 1994). A’del viewed as a

characteristic of Allah (s.w.t) (al-Qaradawi, 1996). Because of the importance of A’del, the Quran

emphasized and repeated it in many verses (Al-Qaradawi, 1994; Mohammed, 2005). As an example,

Allah (s.w.t) said: “O ye who believe! stand out firmly for Allah, as witnesses to fair dealing, and let not

the hatred of others to you make you swerve to wrong and depart from justice. Be just: that is next to

piety” (al-Quran, 5:8). It means accountant should treat his/her colleges and clients as who he/she

wants them to treat him/her. While non-Muslim accountant treats his/her client as the local regulations

ask him/her to do, Muslim accountant treats his/her client as good as he/she wants the client to treat

him/her even if the local regulations did not ask him/her to do so.

With respect to Sabr base, it required from a person to wait as he/she can as possible and considering it

as a worship to Allah (s.w.t) because Sabr is one of the reasons to get the acceptance from Allah (s.w.t)

(al-Quran, 2:153; Mohammed, 2005). The Quran said: “And if you do catch them out, catch them out no

worse than they catch you out: But if you show patience that is indeed the best (course) for those who

are patient (16:126). It is expected that professional accountant will perform the audit work even when

he/she has not yet received the audit fees for previous work done. Some of the participants of this study

disagree with the idea of continuing the work without collecting the previous fees because this is their

right. And their families are relying on this income. Islam encourages workers to have Sabr and Allah

(s.w.t) will reward accountant for having Sabr (al-Quran, 16:96; Mohammed, 2005) but Islam also

encourages Muslims to pay the workers their wages directly once they finished their work that they

have been asked to do (Al-Qaradawi, 1996).

In addition, beside the fees motivation and incentive, accountant has another motivation, i.e. religious

motivation, to comply with the ethical principles. It means accountant comply with the ethical principles

because he/she believes that his/her perfect work will be rewarded from Allah (s.w.t) in this life and in

the hereafter (al-Quran, 16:97).

The six principles above of AICPA are acceptable from the Islamic perspective. Because the study was

conducted in a Yemen, it is expected that Yemeni professional accountants will behave according to the

six principles. In addition, they are also hypothesized to comply with A’del, Sabr, and Ihsan principles,

the seventh principle introduced in the new ethical code of conduct. Thus, the first and second

hypotheses are as follows:

H1: The ethical code of conduct for Yemeni professional accountants is complex variable.

H2: The ethical code of conduct for Yemeni professional accountants should constitute at least seven

constructs.

H2a: The ethical code of conduct for Yemeni professional accountants should significantly embody the

domain “Acting responsibly”.

107 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

H2b: The ethical code of conduct for Yemeni professional accountants should significantly embody the

domain “Honoring the public trust”.

H2c: The ethical code of conduct for Yemeni professional accountants should significantly embody the

domain “Acting with integrity”.

H2d: The ethical code of conduct for Yemeni professional accountants should significantly embody the

domain “Maintaining objectivity and independence”.

H2e: The ethical code of conduct for Yemeni professional accountants should significantly embody the

domain “Exercising due care”.

H2f: The ethical code of conduct for Yemeni professional accountants should significantly embody the

domain “Establishing limits to the scope and nature of services provided”.

H2g: The ethical code of conduct for Yemeni professional accountants should significantly embody the

domain “complying with A’del, Sabr, and Ihsan principles”.

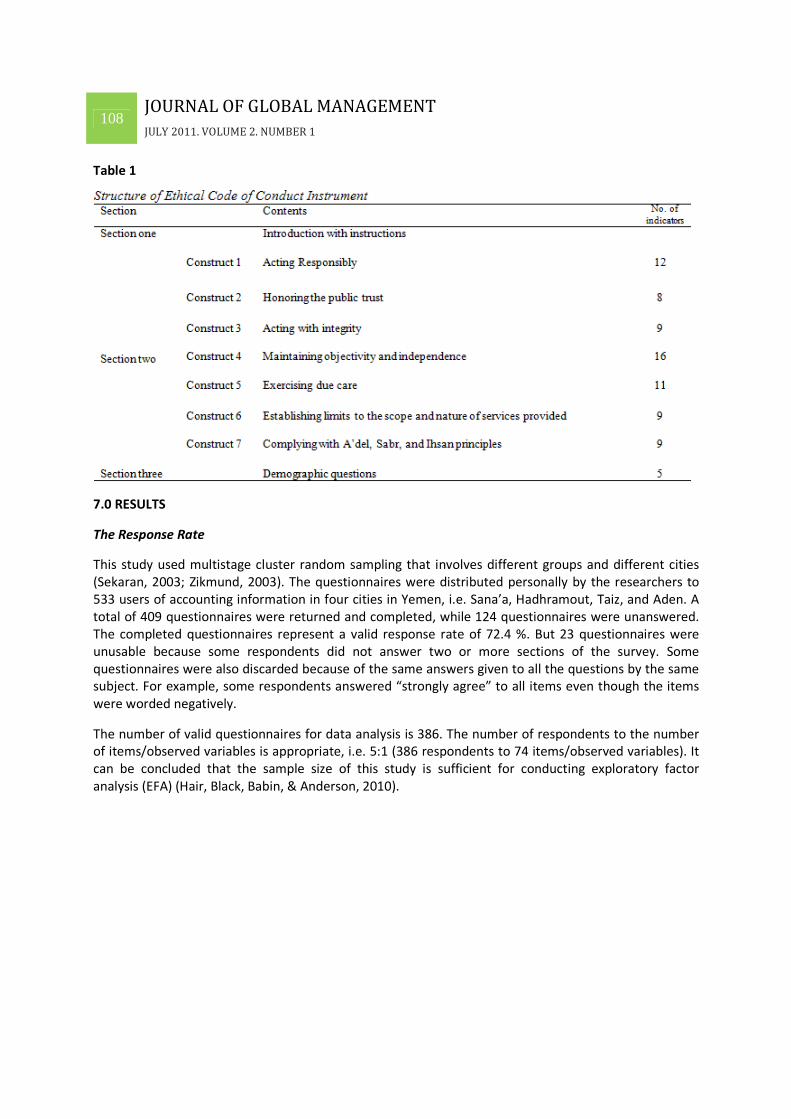

6.0 INSTRUMENTATION

To develop an ethical code of conduct for Yemeni professional accountants, this study has developed

the instrument by basing on the instrument of Brown et al. (2007). Brown developed the instrument by

using AICPA ethical code of conduct as a basis, and by comparing the two main codes of AICPA and IFAC.

He used the AICPA ethical code of conduct because it is broader in scope than the IFAC (Brown, 1999;

Mele, 2005). Additional items that reflect the Islamic perspective are included.

The instrument of ethical code of conduct deals with seven proposed constructs, i.e. acting responsibly,

honoring the public trust, acting with integrity, maintaining objectivity and independence, exercising

due care, establishing limits to the scope and nature of services provided, and complying with A’del,

Sabr, and Ihsan principles. Every construct has a number of indictors/variables as shown in Table 1.

To make sure participants read each item, one item within every construct is stated in negative form. In

other words, specific items are worded negatively to verify if the participants are responding each item

separately (Brown, 1999).

108 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Table 1

7.0 RESULTS

The Response Rate

This study used multistage cluster random sampling that involves different groups and different cities

(Sekaran, 2003; Zikmund, 2003). The questionnaires were distributed personally by the researchers to

533 users of accounting information in four cities in Yemen, i.e. Sana’a, Hadhramout, Taiz, and Aden. A

total of 409 questionnaires were returned and completed, while 124 questionnaires were unanswered.

The completed questionnaires represent a valid response rate of 72.4 %. But 23 questionnaires were

unusable because some respondents did not answer two or more sections of the survey. Some

questionnaires were also discarded because of the same answers given to all the questions by the same

subject. For example, some respondents answered “strongly agree” to all items even though the items

were worded negatively.

The number of valid questionnaires for data analysis is 386. The number of respondents to the number

of items/observed variables is appropriate, i.e. 5:1 (386 respondents to 74 items/observed variables). It

can be concluded that the sample size of this study is sufficient for conducting exploratory factor

analysis (EFA) (Hair, Black, Babin, & Anderson, 2010).

109 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

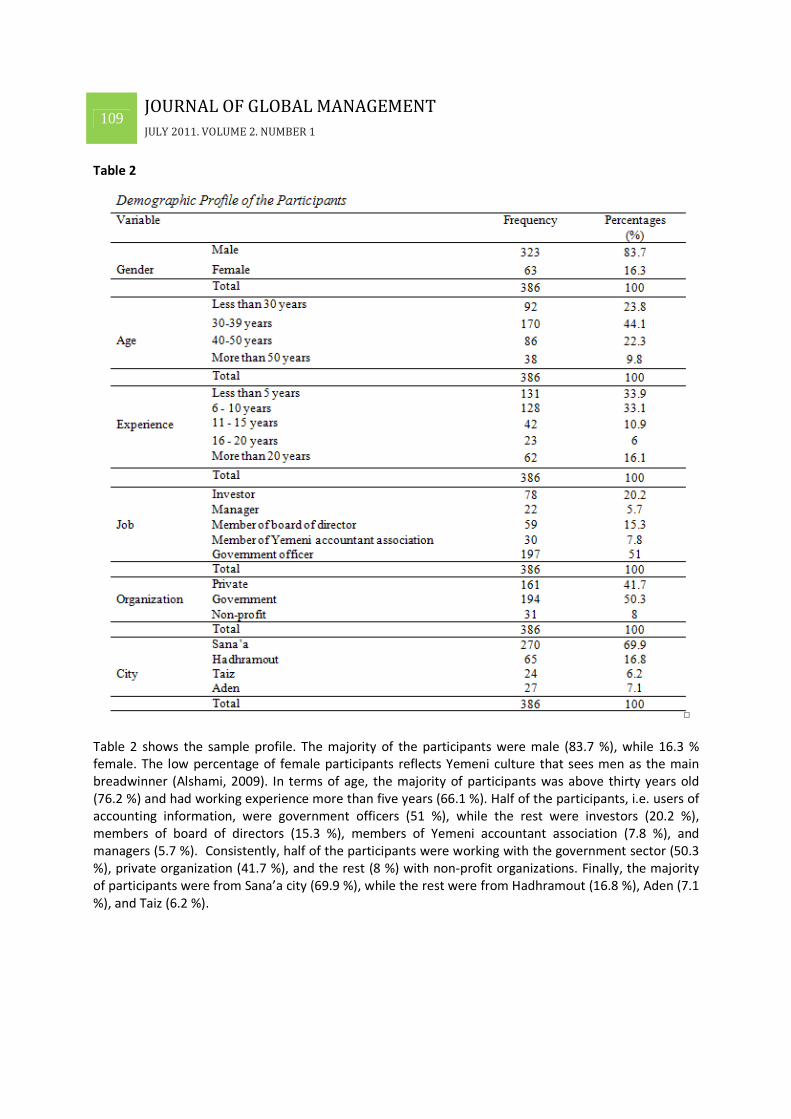

Table 2

Table 2 shows the sample profile. The majority of the participants were male (83.7 %), while 16.3 %

female. The low percentage of female participants reflects Yemeni culture that sees men as the main

breadwinner (Alshami, 2009). In terms of age, the majority of participants was above thirty years old

(76.2 %) and had working experience more than five years (66.1 %). Half of the participants, i.e. users of

accounting information, were government officers (51 %), while the rest were investors (20.2 %),

members of board of directors (15.3 %), members of Yemeni accountant association (7.8 %), and

managers (5.7 %). Consistently, half of the participants were working with the government sector (50.3

%), private organization (41.7 %), and the rest (8 %) with non-profit organizations. Finally, the majority

of participants were from Sana’a city (69.9 %), while the rest were from Hadhramout (16.8 %), Aden (7.1

%), and Taiz (6.2 %).

110 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

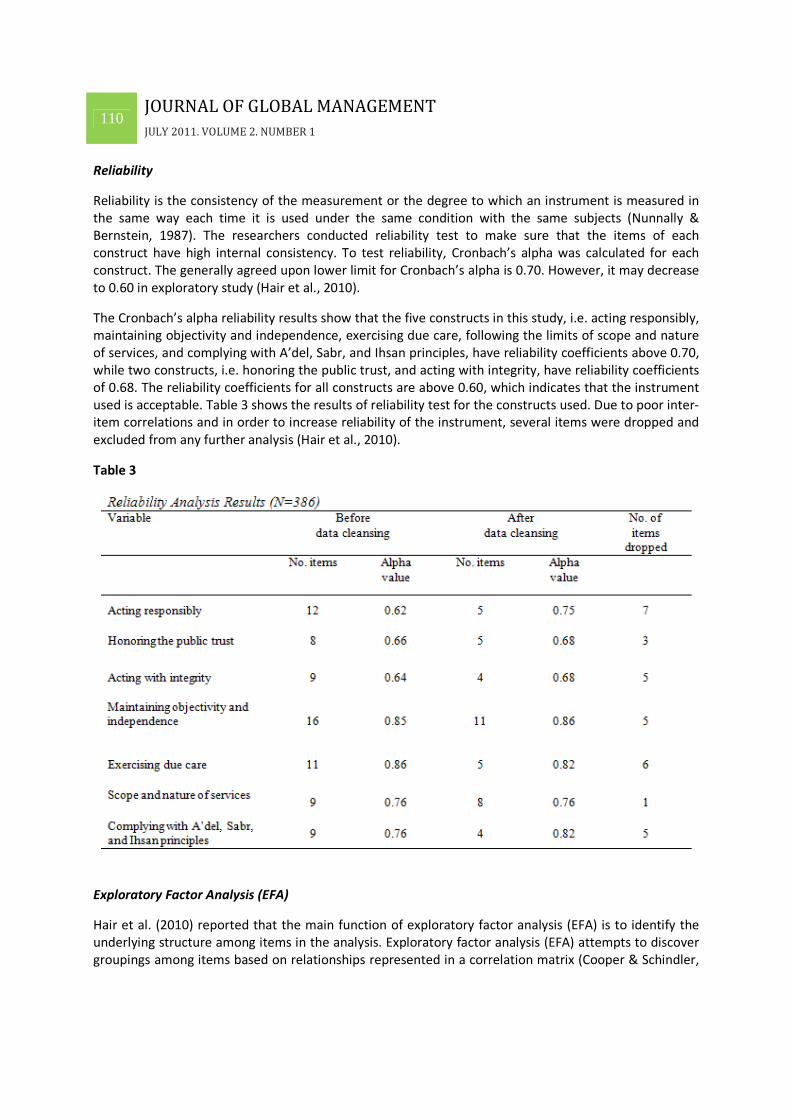

Reliability

Reliability is the consistency of the measurement or the degree to which an instrument is measured in

the same way each time it is used under the same condition with the same subjects (Nunnally &

Bernstein, 1987). The researchers conducted reliability test to make sure that the items of each

construct have high internal consistency. To test reliability, Cronbach’s alpha was calculated for each

construct. The generally agreed upon lower limit for Cronbach’s alpha is 0.70. However, it may decrease

to 0.60 in exploratory study (Hair et al., 2010).

The Cronbach’s alpha reliability results show that the five constructs in this study, i.e. acting responsibly,

maintaining objectivity and independence, exercising due care, following the limits of scope and nature

of services, and complying with A’del, Sabr, and Ihsan principles, have reliability coefficients above 0.70,

while two constructs, i.e. honoring the public trust, and acting with integrity, have reliability coefficients

of 0.68. The reliability coefficients for all constructs are above 0.60, which indicates that the instrument

used is acceptable. Table 3 shows the results of reliability test for the constructs used. Due to poor inter-

item correlations and in order to increase reliability of the instrument, several items were dropped and

excluded from any further analysis (Hair et al., 2010).

Table 3

Exploratory Factor Analysis (EFA)

Hair et al. (2010) reported that the main function of exploratory factor analysis (EFA) is to identify the

underlying structure among items in the analysis. Exploratory factor analysis (EFA) attempts to discover

groupings among items based on relationships represented in a correlation matrix (Cooper & Schindler,

111 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

2003; Zikmund, 2003). Exploratory factor analysis (EFA) is a valuable multivariate statistical method for

extracting information from large data. When items are interrelated, the researcher wants ways to

handle and manage these items, such as, grouping highly connected items together with new

components, and naming the components that represent each group of items (Hair et al., 2010). The

researcher’s assumption is that any item within every construct may be connected with other items. In

other words, EFA is a tool to bet¬ter understand the constitution of the data. It points to nice and simple

relationships that may not have been understandable from assessment of the raw data alone with

information about how many components are required to best represent the data (Hair et al., 2010).

According to Hair et al. (2010), one characteristic of exploratory factor analysis is that the components

come from statistical results, not from theory. This means that the software used in this study, i.e. SPSS,

defines the underlying structure of the data that is based on respondents’ answers. Accordingly, EFA is

conducted without knowing how many components really exist and which items belong to which

construct. The components that emerge will be labeled once the analysis is per¬formed. A large number

of variables can complicate a study because some items might measure different aspects of the same

underlying variable (Hair et al., 2010). Thus, using EFA will help the researchers identify the structure of

the Islamic ethical code of conduct.

To be acceptable for the EFA, i.e. to make sure that the results of EFA are reliable and valid, the data

have to meet several standards. These standards are reliability coefficient, anti-image correlations

matrix, communality, KMO, Bartlett’s test of sphericity, and the cumulative percentages of variance

explained. With respect to reliability, a few items have been deleted.

Anti-image correlations matrix diagonals are the negative matrix values of partial covariance and

correlations among items (Cooper et al., 2003). They reflect the degree to which the factors explain each

other. According to the rules of thumb, anti-image correlations matrix diagonals should be above 0.50

and items with values less than 0.50 must be excluded from further analysis, by deleting one item at a

time, starting with the lowest value, and then recalculating the anti-image correlations matrix again until

all values are above 0.50. In this study, only one item, i.e. item number 8 from the construct “honoring

the public trust”, was deleted and excluded from any further analysis.

The data were also checked for items communality. Communality is the estimate of its shared factor

loadings among the variables as represented by the components derived from exploratory factor

analysis (EFA) (Cooper et al., 2003). Hair et al. (2010) reported that any item that has a communal¬ity

value of less than 0.50 does not have sufficient explanation and it should be deleted and excluded from

any further analysis. The deleting procedure was carried out in the same way as what the researchers

did with anti-image correlations matrix, which means that the item with the lowest communality value

was deleted first. Then the researchers recalculated the communalities for all other items again until all

items have an acceptable level of communality with more than 0.50. The following items are the items

that were deleted and excluded from any further analysis from this study: item number 5 from the

construct “acting responsibly”, item number 7 from the construct “honoring the public trust”, four items

(number 6, 1, 2, 3) from the construct “acting with integrity”, four items (number 9, 8, 4, 3) from the

construct “maintaining objectivity and independence”, six items (number 8, 9, 3, 1, 7, 4) from the

construct “exercising due care”, item number 2 from the construct “following the limits of scope and

nature of services”, and four items (number 6, 1, 9, 8) from the construct “complying with A’del, Sabr,

and Ihsan principles”.

112 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

The next test was the Kaiser-Myer-Olkin (KMO) of Sampling Adequacy and Bartlett’s test of sphericity.

They are both indicators for evaluating the appropriateness of applying factor analysis (Cooper et al.,

2003; Zikmund, 2003). As shown in Tables 4, 5, 6, 7, 8, 9 and 10, all items for each construct are within

the acceptable level. Specifically, the KMO measure for most items for each construct is above 0.60,

which is acceptable, except for one construct, i.e. “honoring the public trust”. This measure indicates

that high proportion of variance in the items is common variance and causes the structure components

to be established effectively (Hair et al., 2010). As for the Bartlett’s test of sphericity, the results are all

significant (p value = 0.000).

Tables 4, 5, 6, 7, 8, 9 and 10, present the final results of exploratory factor analysis for every construct.

The results show that the cumulative percentages of variance explained by the components for each

construct are reasonable within the range between 0.59 and 0.80. In general, the results demonstrated

that reliability, anti-image correlations matrix, communality, KMO, Bartlett’s test of sphericity, and the

cumulative percentages of variance explained for exploratory factor analysis (EFA), are acceptable to be

used as a guide to develop the measurement model that can be examined and confirmed by using

confirmatory factor analysis (CFA).

Hair et al. (2010) reported that only items with factor loadings greater than 0.50 are considered for

specifying the measurement model. The results show that all items have factor loading greater than

0.50 which means all items can be used to specify the measurement model.

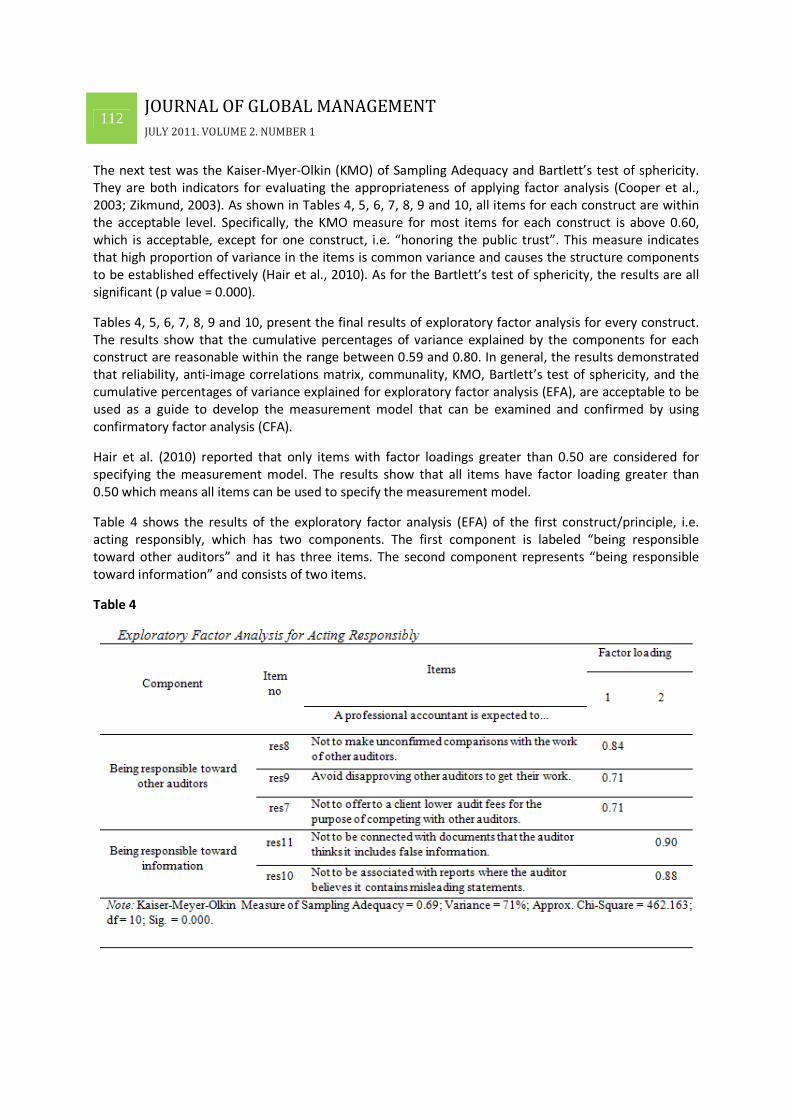

Table 4 shows the results of the exploratory factor analysis (EFA) of the first construct/principle, i.e.

acting responsibly, which has two components. The first component is labeled “being responsible

toward other auditors” and it has three items. The second component represents “being responsible

toward information” and consists of two items.

Table 4

113 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

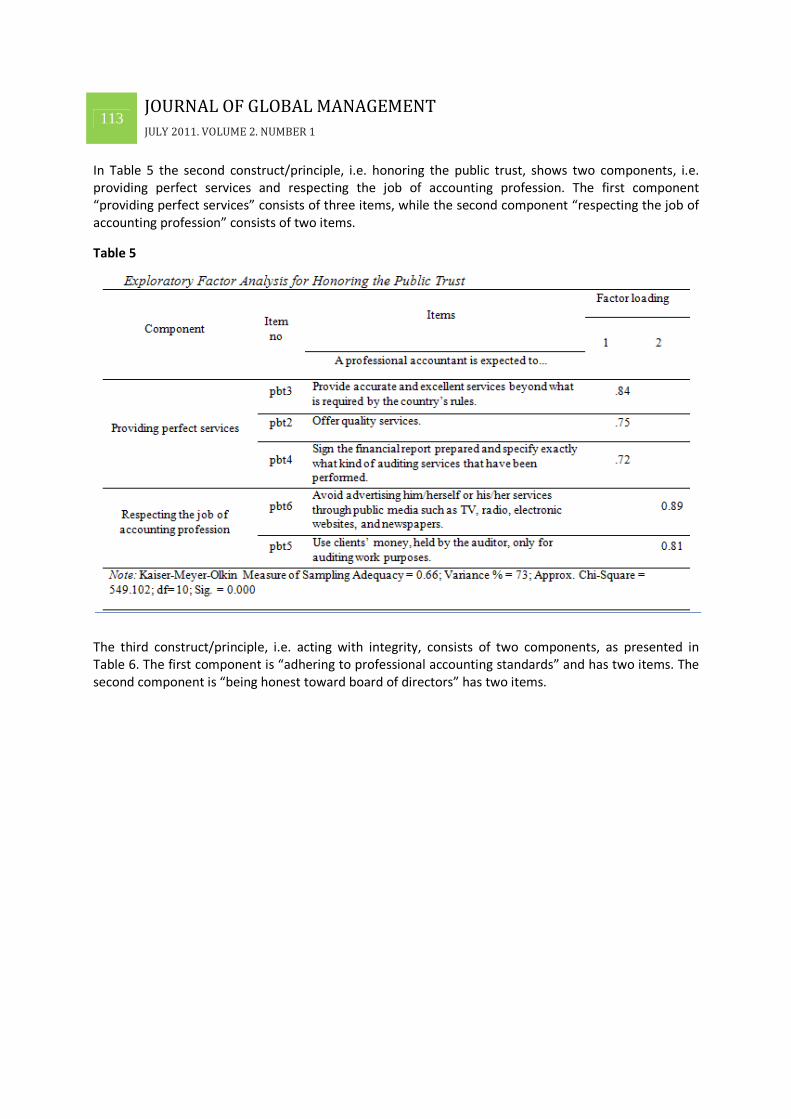

In Table 5 the second construct/principle, i.e. honoring the public trust, shows two components, i.e.

providing perfect services and respecting the job of accounting profession. The first component

“providing perfect services” consists of three items, while the second component “respecting the job of

accounting profession” consists of two items.

Table 5

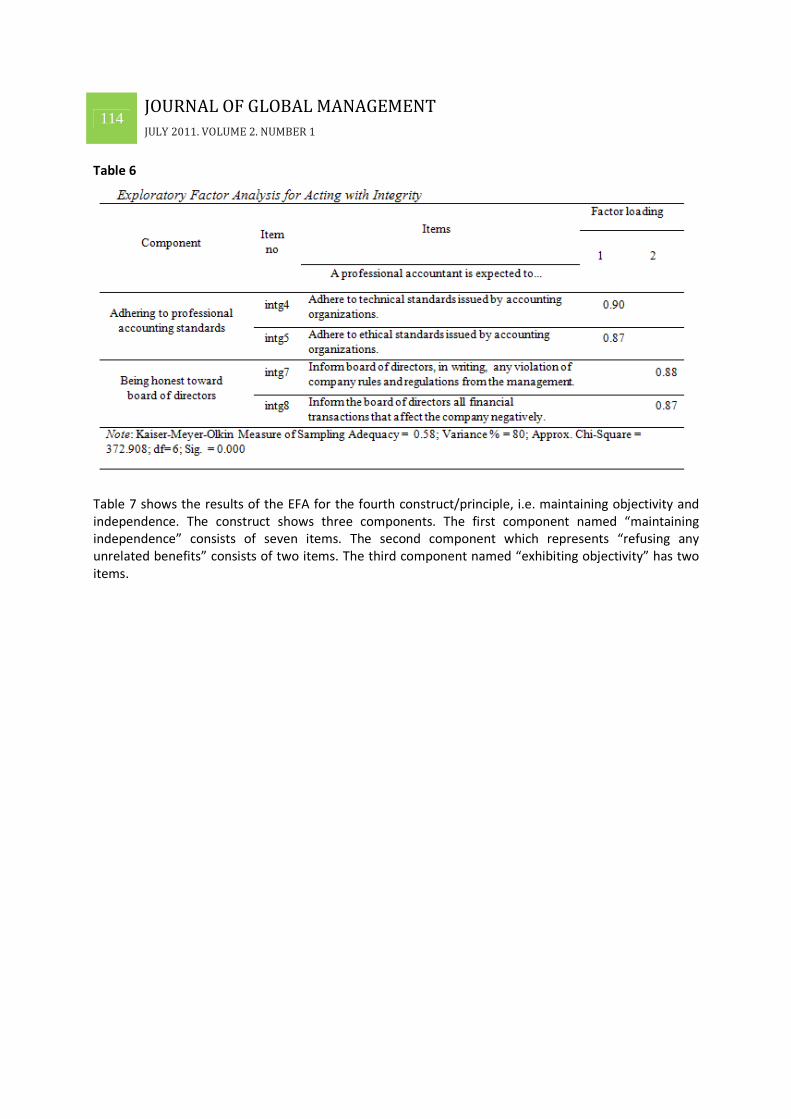

The third construct/principle, i.e. acting with integrity, consists of two components, as presented in

Table 6. The first component is “adhering to professional accounting standards” and has two items. The

second component is “being honest toward board of directors” has two items.

114 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Table 6

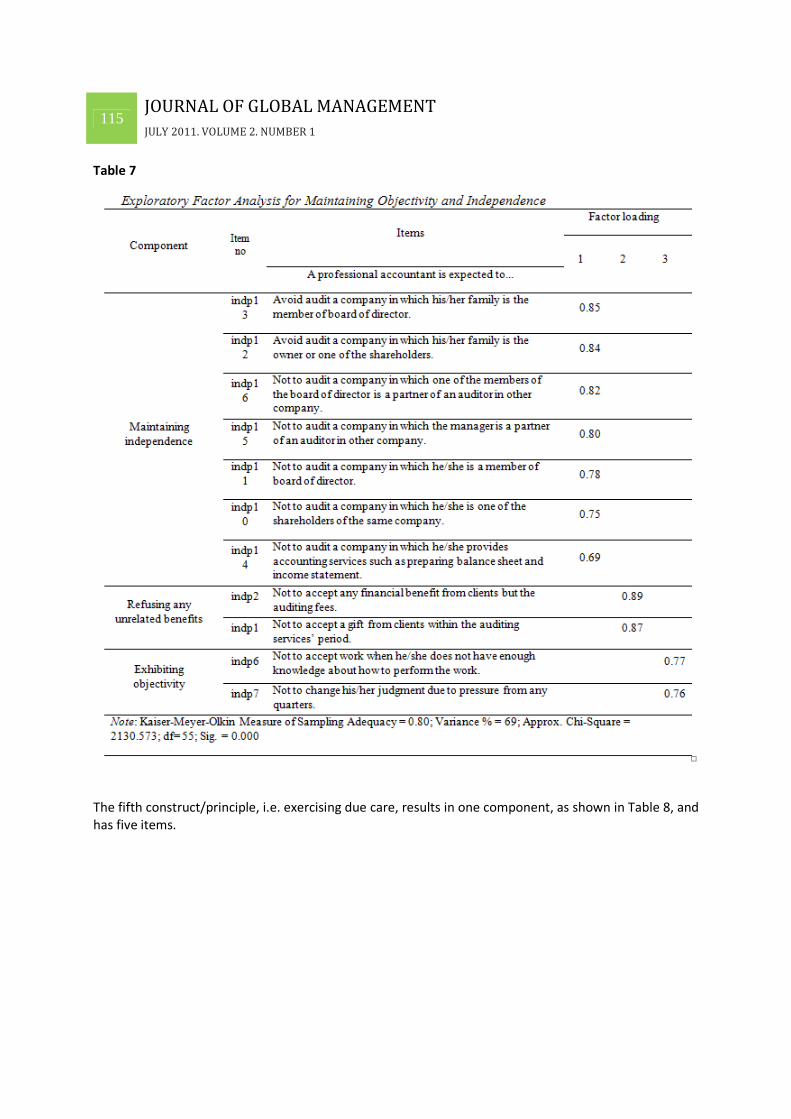

Table 7 shows the results of the EFA for the fourth construct/principle, i.e. maintaining objectivity and

independence. The construct shows three components. The first component named “maintaining

independence” consists of seven items. The second component which represents “refusing any

unrelated benefits” consists of two items. The third component named “exhibiting objectivity” has two

items.

115 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Table 7

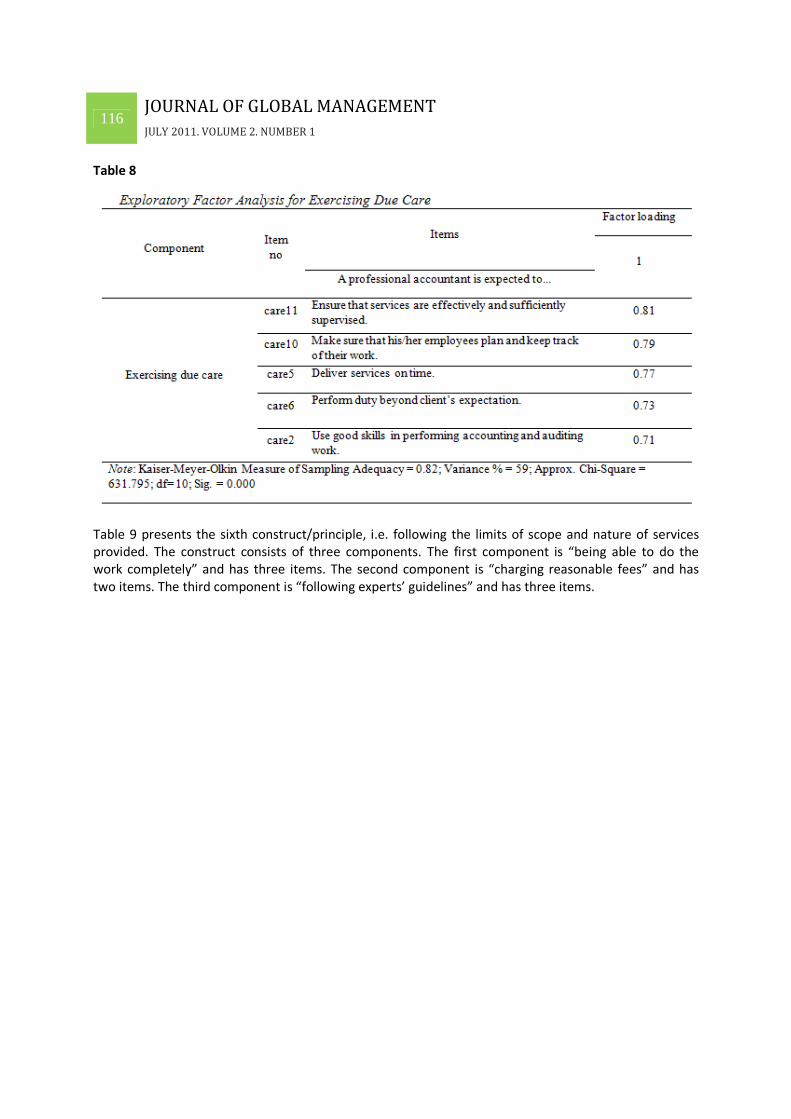

The fifth construct/principle, i.e. exercising due care, results in one component, as shown in Table 8, and

has five items.

116 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Table 8

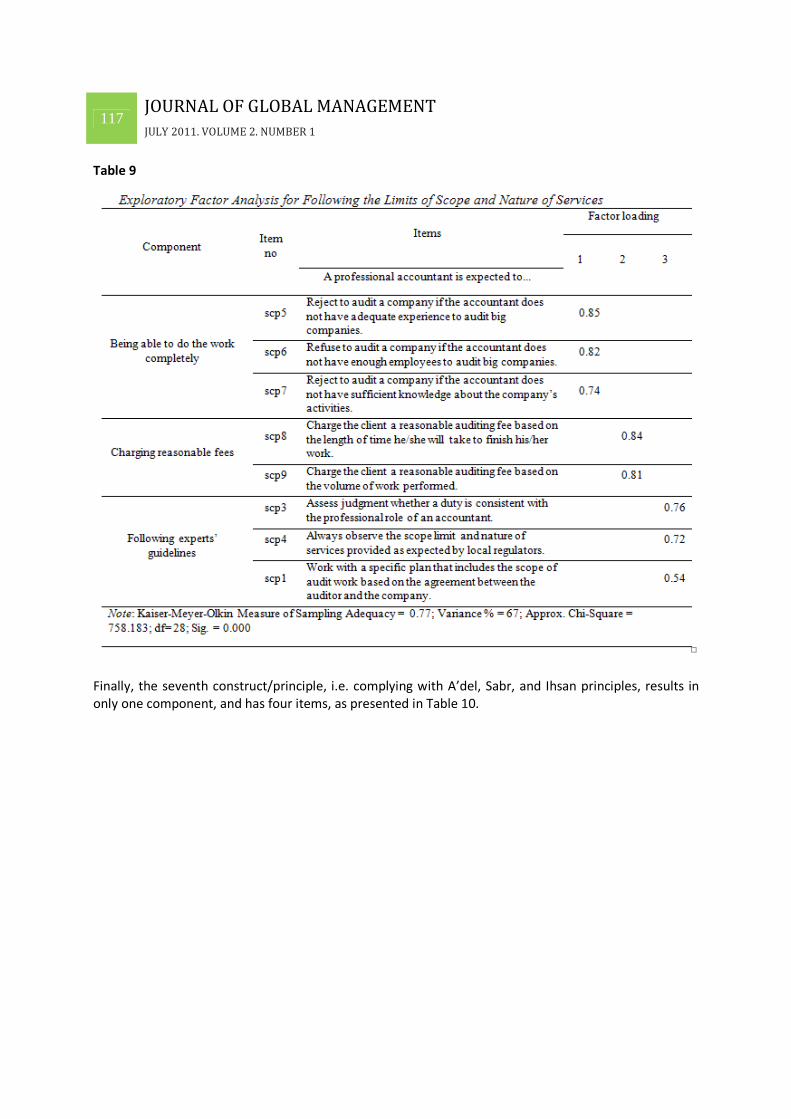

Table 9 presents the sixth construct/principle, i.e. following the limits of scope and nature of services

provided. The construct consists of three components. The first component is “being able to do the

work completely” and has three items. The second component is “charging reasonable fees” and has

two items. The third component is “following experts’ guidelines” and has three items.

117 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Table 9

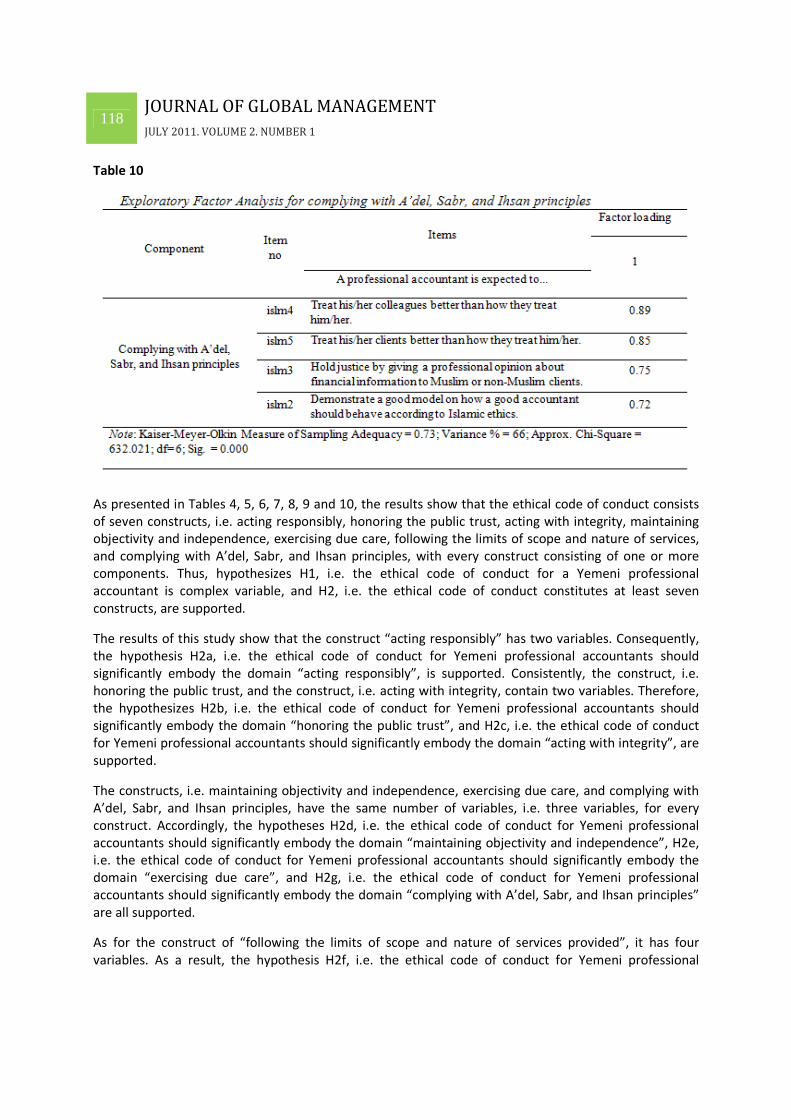

Finally, the seventh construct/principle, i.e. complying with A’del, Sabr, and Ihsan principles, results in

only one component, and has four items, as presented in Table 10.

118 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Table 10

As presented in Tables 4, 5, 6, 7, 8, 9 and 10, the results show that the ethical code of conduct consists

of seven constructs, i.e. acting responsibly, honoring the public trust, acting with integrity, maintaining

objectivity and independence, exercising due care, following the limits of scope and nature of services,

and complying with A’del, Sabr, and Ihsan principles, with every construct consisting of one or more

components. Thus, hypothesizes H1, i.e. the ethical code of conduct for a Yemeni professional

accountant is complex variable, and H2, i.e. the ethical code of conduct constitutes at least seven

constructs, are supported.

The results of this study show that the construct “acting responsibly” has two variables. Consequently,

the hypothesis H2a, i.e. the ethical code of conduct for Yemeni professional accountants should

significantly embody the domain “acting responsibly”, is supported. Consistently, the construct, i.e.

honoring the public trust, and the construct, i.e. acting with integrity, contain two variables. Therefore,

the hypothesizes H2b, i.e. the ethical code of conduct for Yemeni professional accountants should

significantly embody the domain “honoring the public trust”, and H2c, i.e. the ethical code of conduct

for Yemeni professional accountants should significantly embody the domain “acting with integrity”, are

supported.

The constructs, i.e. maintaining objectivity and independence, exercising due care, and complying with

A’del, Sabr, and Ihsan principles, have the same number of variables, i.e. three variables, for every

construct. Accordingly, the hypotheses H2d, i.e. the ethical code of conduct for Yemeni professional

accountants should significantly embody the domain “maintaining objectivity and independence”, H2e,

i.e. the ethical code of conduct for Yemeni professional accountants should significantly embody the

domain “exercising due care”, and H2g, i.e. the ethical code of conduct for Yemeni professional

accountants should significantly embody the domain “complying with A’del, Sabr, and Ihsan principles”

are all supported.

As for the construct of “following the limits of scope and nature of services provided”, it has four

variables. As a result, the hypothesis H2f, i.e. the ethical code of conduct for Yemeni professional

119 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

accountants should significantly embody the domain “following the limits of scope and nature of

services provided”, is supported.

8.0 CONCLUSIONS

Based on the above results, the following conclusion is drawn:

1. Under the Islamic environment, additional element i.e. Islamic compliance principle needs to be

included in the ethical code of conduct for accountants. This is because country like Yemen is

bound by the Shari’ah Law. The Islamic ethical code of conduct for Yemeni professional

accountants consists of seven constructs, i.e. acting responsibly, honoring the public trust, acting

with integrity, maintaining objectivity and independence, exercising due care, following the

limits of scope and nature of services, and complying with A’del, Sabr, and Ihsan principles.

Islamic ethical code of conduct is more applicable than AICPA ethical code of conduct specifically

in Muslim countries.

2. The sources of the Islamic ethical code of conduct are the Quran and Sunnah which contain a

wide framework for ethical issues. However, most Islamic studies have addressed the issue

conceptually rather than empirically. Thus, this study empirically supports the ethical concept

that is stipulated in the Quran and Sunnah. However, the results of this study cannot be

generalized to other countries because it was conducted only in Yemen and more studies need

to be done to verify and confirm the results.

3. In Islam Allah (s.w.t) created this cosmic and He is the only one who knows everything; humans’

knowledge and ability to understand are limited. Therefore, to understand how things work in

this world, people are encouraged to read, study, and understand the Creator’s catalogs, i.e. the

Quran and Sunnah.

9.0 RECOMMENDATIONS FOR FUTURE RESEARCHES

This paper has several limitations that need to be documented. First, even though this study has tried to

develop an Islamic ethical code of conduct for Yemeni professional accountants, there are certain

limitations relating to a relatively small sample that focused only on Yemen. Therefore, the results of

this study may not necessarily reflect other Muslim countries and this study only targeted professional

accountants in Yemen.

To have a bigger and clearer picture about the ethical code of conduct, further research may select two

groups of users of accounting information and professional accountants. By comparing opinions

between the users of accounting information and professional accountants may produce another

picture about the ethical issues in Yemen.

As this study was conducted only in Yemen, future studies can be conducted in other countries, i.e. Arab

and non-Arab countries. Other methods to collect the data such as interviews and observations should

be employed in other countries.

This study focused on the contents of the ethical code of conduct for Yemeni professional accountant

rather than on the factors that may affect it. Thus, it will be interesting to study the factors that affect

accountants’ ethical code of conduct such as gender, age, experience, and organization type.

120 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

ACKNOWLEDGEMENT

We would like to thank the management of Universiti Utara Malaysia, for the assistance rendered. We

also thank several Professors such as Dr. Abdullah (Lecturer in COB/ UUM/ Malaysia), Dr. Mohammed

(Dean of Education College/ Hadhramout University/ Yemen), Dr. Amatassalm (Lecturer in Girls College/

Hadhramout University/ Yemen), Dr. Alshami (lecturer in UST-Sana’a/ Yemen), and Mr. Ameen

(President of Yemeni Association for Certified Public Accountants) for the input and feedback on the

survey.

REFERENCES

Al-Quran (the holy Quran)

Alaidaros, A. (2010). The importance of ethical code of conduct for decision makers in Yemen.

Unpublished manuscript, Yemen, Hadhramout.

Abo-ahmeed, W. (2006). The extent of the auditor’s compliance in Jordan with the ethical codes of

professional conduct. Journal of Universtiy of the King Abduallah Abdalaziz, 20(2), 161-207.

Ahadiat, N., & Mackie, J. (1993). Ethics education in accounting: An investigation of the importance of

ethics as a factor in the recruiting decisions of public accounting firms. Journal of Accounting

Education, 11(2), 243-257.

AICPA. (2009). Code of ethics for professional accountants. USA: American Institute of Certified Public

Accountants. Retrieved 15-4-2010, from www.aicpa.org

Al-Ariqi. (2007). One-on-one with president of the Yemeni association of certified public accountants

Ramzi Al-Ariqi: “Companies involved in corruption should be black listed”. Yemen Times.

Retrieved 15/02/2007, from www.yementimes.com/rss.xml

Al-Banna. (1940). Messages’ group of Imam Hasan al-Banna. (1st edition). Egypt, Alexandria: Darul al-

A’aoah Publication.

Ali, Z. (2010, July 25). Are workers in Yemen following Islamic principles?. Yemen, Sana’a [Interview].

Alkebsi, I. (2010). The availability of ethical code of conduct for professional accountants in Yemen. (5th

edition). Yemen, Sana’a: Yemeni Association of Certified Public Accountants.

Al-Qaradawi, Y. (1985). The Iman (faith) and life. (1st edition). Qatar, Doha: Arabia Publication. Retrieved

15/10/2009, from www.daawa-info.net

Al-Qaradawi, Y. (1994). The priorities understanding. (1st edition). Lebanon, Beirut: alRessalh

Publication. Retrieved 15/10/2009, from www.fiseb.com

Al-Qaradawi, Y. (1996). The general characteristics of Islam. (9th edition). Lebanon, Beirut: alRessalh

Publication.

Alshami. (2009). The availability of ethical code of conduct for professional accountants in Yemen.

Yemen, Sana’a: Yemeni Association for Certified Public Accountants.

121 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Alshami, I. (2010). The availability of ethical code of conduct for professional accountants in Yemen.

Yemen, Sana’a [Interview].

Baahroon, A. (2010). Accountants ethics in Yemeni Universities. Yemen, Hadhramout [Interview].

Baantar, H. (2010). The ethics of Yemeni professional accountants in reality. Yemen, Hadhramout

[Interview].

Bageneed, O. (2010). The importance of ethical code of conduct for decision makers in Yemen. Yemen,

Hadhramout [Interview].

Bamashmos, A. (2003). International auditing standards and the potential application in the Yemen

republic. Yemen, Sana’a: The National Center for Information.

Bay, D. (1997). Determinants of ethical behavior: An experiment. Ph. D Dissertation, Washington State

University.

Bendool, A. (2010). The importance of ethical code of conduct for decision makers in Yemen. Yemen,

Hadhramout [Interview].

Brecht, H. (1991). Accountants’ duty to the public for audit negligence: Self-regulation and legal liability.

US, Florida: University of Florida.

Brown, P. (1999). The AICPA code of professional conduct and exemplification: An empirical

investigation of auditor and public perceptions. Ph. D Dissertation, University of Mississippi.

Brown, P., Stocks, M., & Wilder, W. (2007). Ethical exemplification and the AICPA code of professional

conduct: An empirical investigation of auditor and public perceptions. Journal of Business Ethics,

71(1), 39-71.

Burks, B. (2006). The impact of ethics education and religiosity on the cognitive moral development of

senior accounting and business students in higher education. Ph. D Dissertation, Nova

Southeastern University.

Cooper, D., & Schindler, P. (2003). Business research methods. (8th edition). New York: McGraw-Hill.

Delaney, J. (2005). The impact of ethics education on the moral reasoning ability of accounting students.

Ph. D Dissertation, Ambrose University.

Duska, R., & Duska, B. (2003). Accounting ethics. (1st edition). New York: Wiley-Blackwell.

England, T. (1998). An exploratory study of gaps in selected “Ethics Norms” of professional accountants.

Ph. D Dissertation, University Microfilms International.

Hair, J., Black, W., Babin, B., & Anderson, R. (2010). Multivariate data analysis: A global perspective. (7th

edition). Uper Saddle River, NJ; London: Pearson Education.

Hasan, M. (2010). The ethics of Yemeni professional accountants in reality. Yemen, Hadhramout

[Interview].

122 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Ibrahim, S. (2010). The importance of ethical code of conduct for decision makers in Yemen. Yemen,

Sana’a [Interview].

IFAC. (2007). Code of ethics for professional accountants. USA: International Federation of Accountants.

Retrieved 15/12/2007, from www.ifac.org

IFAC. (2010). Code of ethics for professional accountants. USA: International Federation of Accountants.

Retrieved 15/4/2010, from www.ifac.org

Martin, R. (2007). Through the ethics looking glass: Another view of the world of auditors and ethics.

Journal of business ethics, 70(1), 5-14.

Mawdudi. (1977). Life’s system in Islam. (7th edition). Lebanon, Beirut: alRessalh Publication.

Mele, D. (2005). Ethical education in accounting: Integrating rules, values and virtues. Journal of

Business Ethics, 57(1), 97-109.

Mohammed, A. (2010). The ethics of Yemeni professional accountants in reality. Yemen, Aden

[Interview].

Mohammed, A. (2005). The relationship between Islamic rules and accountants’ ethics. Unpublished

manuscript. Alahgaff University.

Mohammed, A. (2008). Accountants’ ethics in Yemen. Master Thesis. Universiti Utara Malaysia.

Mustafa, A. (2010). The importance of ethical code of conduct for decision makers in Yemen. Yemen,

Aden [Interview].

Nunnally, J., & Bernstein, I. (1987). Psychometric theory. (2nd edition). New York: McGraw-Hill.

Parker, L. (1994). Professional accounting body ethics: In search of the private interest. Accounting,

Organizations and Society, 19(6), 507-525.

Payne, D., & Landry, B. (2005). Similarities in business and IT professional ethics: The need for and

development of a comprehensive code of ethics. Journal of Business Ethics, 62(1), 73-85.

Rahman, A. (2003). Ethics in accounting education: Contribution of the Islamic principle of Maslahah.

IIUM Journal of Economics and Management, 11(1), 2.

Saeed, M., Ahmed, Z., & Mukhtar, S. (2001). International marketing ethics from an Islamic perspective:

A value-maximization approach. Journal of Business Ethics, 32(2), 127-142.

Sekaran, U. (2003). Research methods for business: A skill building approach. (4th edition). New York:

John Wiley and Sons.

SOCPA. (2009). Code of ethics for professional accountants. Kingdom of Saudi Arabia, Riyadh: Saudi

Organization for Certified Public Accountants Retrieved 15/10/2010, from www.socpa.org

Street, B. (2002). A comparative analysis of professional codes of ethics. Ph. D Dissertation, Central

Michigan University.

123 JOURNAL OF GLOBAL MANAGEMENT

JULY 2011. VOLUME 2. NUMBER 1

Velasquez, M. (2006). Business ethics: Concepts & cases. (6th edition). Uper Saddle River, NJ, London:

Person Education International.

Venezia, C. (2005). The ethical reasoning abilities of accounting students. The Journal of American

Academy of Business, 6(1), 200-207.

YACPA. (2010). The ethical code of conduct for professional accountants for Arab Gulf countries. The

Legal Accountant, 6th, 20-26.

Yaken. (2006). What is the meaning of my belong to Islam. Lebanon, Beirut: alRessalh Publication.

Zaid, A. (2010). The main problems of auditors in Yemen. Yemen, Taiz [Interview].

Ziegenfuss, D., & Singhapakdi, A. (1994). Professional values and the ethical perceptions of internal

auditors. Managerial Auditing Journal, 9(1), 34-44.

Zikmund William, G. (2003). Business research methods. (7th edition). Drden Press Mason. Thomson

South-Western.

Related Documents