1 The The 7 7 Twelve Twelve Portfolio Portfolio The Benefits of Low Correlation The Benefits of Low Correlation Craig Craig L L . . Israelsen Israelsen , , Ph Ph . . D D . . Brigham Young University Brigham Young University www www . . 7 7 TwelvePortfolio TwelvePortfolio . . com com 41 41 slides slides

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

The The 77TwelveTwelve PortfolioPortfolio The Benefits of Low CorrelationThe Benefits of Low Correlation

Craig Craig LL. . IsraelsenIsraelsen, , PhPh..DD.. Brigham Young UniversityBrigham Young University

wwwwww..77TwelvePortfolioTwelvePortfolio..comcom

41 41 slidesslides

2

This document is a research report presenting portfolio research and analysis.

This document is neither investment advice nor an investment solicitation.

Implementation of the 77TwelveTwelve portfolio is no guarantee of performance.

---------------------------------------------------------------------------------------------

This is a copyrighted document, copying for redistribution is prohibited unless written permission is

obtained from Craig L. Israelsen.

Copyright © 2008 Craig L. Israelsen

All rights reserved

Presentation OverviewPresentation Overview

►►Part One provides a historical context of the Part One provides a historical context of the

benefits of a multibenefits of a multi--assetasset, , low correlation low correlation

portfolioportfolio..

►►Part Two introduces the Part Two introduces the 77TwelveTwelve PortfolioPortfolio, ,

a multia multi--assetasset, , low correlation global low correlation global

portfolioportfolio.. 3

Part OnePart One

4

5

Historical Asset ReturnsHistorical Asset Returns

38-Year Period from 1970-2007

Annualized Return (%)

Std Dev of Annual Returns

Growth of $10,000

REIT 12.38 18.45 843,476

Commodities 12.02 23.93 747,183

US Small Stock 11.74 21.68 678,684

US Large Stock 11.08 16.62 542,040

International Stock 10.86 21.54 503,316

Bonds (Intermediate) 8.10 5.39 193,131

Cash 6.29 3.07 101,701

Inflation 4.62 3.08 55,618

6

DataData

►► LargeLarge--cap US equitycap US equity represented by the Srepresented by the S&&P P 500500 IndexIndex..

►► SmallSmall--cap US equitycap US equity represented by the Ibbotson Small Companies Index represented by the Ibbotson Small Companies Index from from 19701970--19781978, , and the Russell and the Russell 20002000 Index from Index from 19791979--20072007. .

►► NonNon--US equityUS equity represented by the MSCI EAFE Indexrepresented by the MSCI EAFE Index. .

►► Real estateReal estate represented by the NAREIT Index from represented by the NAREIT Index from 19701970--19771977 and the Dow and the Dow Jones Wilshire REIT Index from Jones Wilshire REIT Index from 19781978--20072007..

►► CommoditiesCommodities represented by the Goldman Sachs Commodities Index represented by the Goldman Sachs Commodities Index ((GSCIGSCI). ). As of February As of February 66, , 20072007, , the GSCI became the Sthe GSCI became the S&&P GSCI Commodity IndexP GSCI Commodity Index..

►► UU..SS. . intermediate term bondsintermediate term bonds represented by the Ibbotson Intermediate represented by the Ibbotson Intermediate Term Bond Index from Term Bond Index from 19701970--7373 and the Lehman Brothers Intermediate Term and the Lehman Brothers Intermediate Term Government Bond index from Government Bond index from 19741974--20072007. .

►► CashCash represented by represented by 33--month Treasury Billsmonth Treasury Bills. .

7

Historical Upside and DownsideHistorical Upside and Downside

1970-2007

Largest One-Year Gain (%)

Worst One-Year Loss (%)

Worst 3-Year

Cum Loss (%)

Bonds 25.42 (1.75) 6.43

Cash 15.58 1.05 4.22

Commodities 74.96 (35.75) (26.06)

REIT 48.99 (23.44) (28.30)

US Large Stock 37.58 (26.47) (37.61)

US Small Stock 57.40 (30.90) (42.22)

International Stock 69.44 (23.45) (43.32)

8

Benefit Benefit #1#1

When built correctlyWhen built correctly, ,

multimulti--asset portfolios achieve asset portfolios achieve

low aggregate correlation low aggregate correlation

among the internal assetsamong the internal assets..

9

10

Correlation of Correlation of Major Asset ClassesMajor Asset Classes ((19701970--20072007))

Large US Equity

Small US Equity

Non-US Equity

US Bonds

Cash REIT

Small US Equity .74

Non-US Equity .59 .47

US Bonds .21 .05 -.11

Cash .05 .01 -.12 .42

REIT .39 .71 .25 .00 -.05

Commodities -.28 -.32 -.14 -.20 .00 -.24

Aggregate (Average) Correlation in Equal-Weighted 7-Asset Portfolio = 0.12

11

Correlation Correlation MattersMatters Commodities and small US stock had a similar Commodities and small US stock had a similar 3838--year returnyear return——but blending commodities with large US stock was far more benefibut blending commodities with large US stock was far more beneficial cial

because commodities has a lower correlation to large US stock because commodities has a lower correlation to large US stock ((--00..2828) ) than does small US stock than does small US stock ((00..7474).). Growth of $10,000 1970-2007

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

S&P 500 50% S&P 500/50% Small US 50% S&P 500/50% GSCI

38-Year Returns:

S&P 500 11.08%

Small US 11.74%

GSCI 12.02%

Correlation:

S&P 500/Small US = 0.74

S&P 500/Commodities = -0.28

12

Performance Performance During During

Accumulation Accumulation PhasePhase

Individual Assets Individual Assets

vsvs. .

Typical PortfoliosTypical Portfolios

vsvs. .

MultiMulti--Asset Asset PortfolioPortfolio

13

Year

Large US Equity

Small US Equity

Non-US Equity

Intermediate Term US Bonds

Cash Real Estate Commodities Equally

Weighted Multi-Asset Portfolio

1970 3.92 (17.40) (11.66) 16.90 6.80 (4.00) 15.17 1.39

1971 14.30 16.50 29.59 8.70 4.53 15.52 21.08 15.75

1972 19.00 4.40 36.35 5.20 4.24 8.01 42.43 17.09

1973197319731973 (14.69) (30.90) (14.92) 4.60 7.46 (15.52) 74.96 1.57

1974197419741974 (26.47) (19.90) (23.16) 7.03 8.35 (21.42) 39.51 (5.15)

1975 37.23 52.80 35.39 8.33 6.08 19.29 (17.22) 20.27

1976 23.93 57.40 2.54 11.74 5.23 47.56 (11.92) 19.50

1977 (7.16) 25.40 18.06 3.00 5.52 22.43 10.37 11.09

1978 6.57 23.50 32.62 2.23 7.67 10.98 31.61 16.45

1979 18.61 43.07 4.75 6.59 10.86 48.99 33.81 23.81

1980 32.50 38.60 22.58 6.65 12.71 33.12 11.08 22.46

1981 (4.92) 2.03 (2.28) 10.79 15.58 17.88 (23.01) 2.30

1982 21.55 24.95 (1.86) 25.42 11.66 20.91 11.56 16.31

1983 22.56 29.13 23.69 8.22 9.24 32.17 16.26 20.18

1984 6.27 (7.30) 7.38 14.29 10.33 21.89 1.05 7.70

1985 31.73 31.05 56.16 18.00 7.97 6.50 10.01 23.06

1986 18.67 5.68 69.44 13.06 6.29 19.75 2.05 19.28

1987 5.25 (8.80) 24.63 3.61 6.13 (6.59) 23.77 6.86

1988 16.61 25.02 28.27 6.40 7.06 17.48 27.94 18.40

1989 31.69 16.26 10.54 12.68 8.67 2.72 38.28 17.26

1990 (3.10) (19.48) (23.45) 9.56 7.99 (23.44) 29.08 (3.26)

14

Year Large US

Equity Small US

Equity Non-US Equity

Intermediate Term US

Govt Bonds Cash Real Estate Commodities

Equally Weighted Multi-Asset Portfolio

1991 30.47 46.04 12.13 14.11 5.68 23.84 (6.13) 18.02

1992 7.62 18.41 (12.17) 6.93 3.59 15.13 4.42 6.28

1993 10.08 18.88 32.56 8.17 3.12 15.14 (12.33) 10.80

1994 1.32 (1.82) 7.78 (1.75) 4.45 2.66 5.29 2.56

1995 37.58 28.45 11.21 14.41 5.79 12.24 20.33 18.57

1996 22.96 16.49 6.05 4.06 5.26 37.05 33.92 17.97

1997 33.36 22.36 1.78 7.72 5.31 19.66 (14.07) 10.87

1998 28.58 (2.55) 19.93 8.49 5.02 (17.01) (35.75) 0.96

1999 21.04 21.26 27.03 0.49 4.87 (2.58) 40.92 16.15

2000200020002000 (9.10) (3.02) (14.17) 10.47 6.32 31.04 49.74 10.18

2001200120012001 (11.89) 2.49 (21.44) 8.42 3.67 12.35 (31.93) (5.48)

2002200220022002 (22.10) (20.48) (15.94) 9.64 1.68 3.58 32.07 (1.65)

2003 28.69 47.25 38.59 2.29 1.05 36.18 20.72 24.97

2004 10.88 18.33 20.25 2.33 1.43 33.16 17.28 14.81

2005 4.91 4.55 13.54 1.68 3.34 13.82 25.55 9.63

2006 15.79 18.37 26.34 3.84 5.07 35.97 (15.09) 12.90

2007 5.49 (1.57) 11.17 8.47 4.77 (17.56) 32.67 6.21

Benefit Benefit #2#2

When built correctlyWhen built correctly, ,

multimulti--asset portfolios asset portfolios

achieve achieve equityequity--like returns like returns

with with bondbond--like risklike risk..

15

16

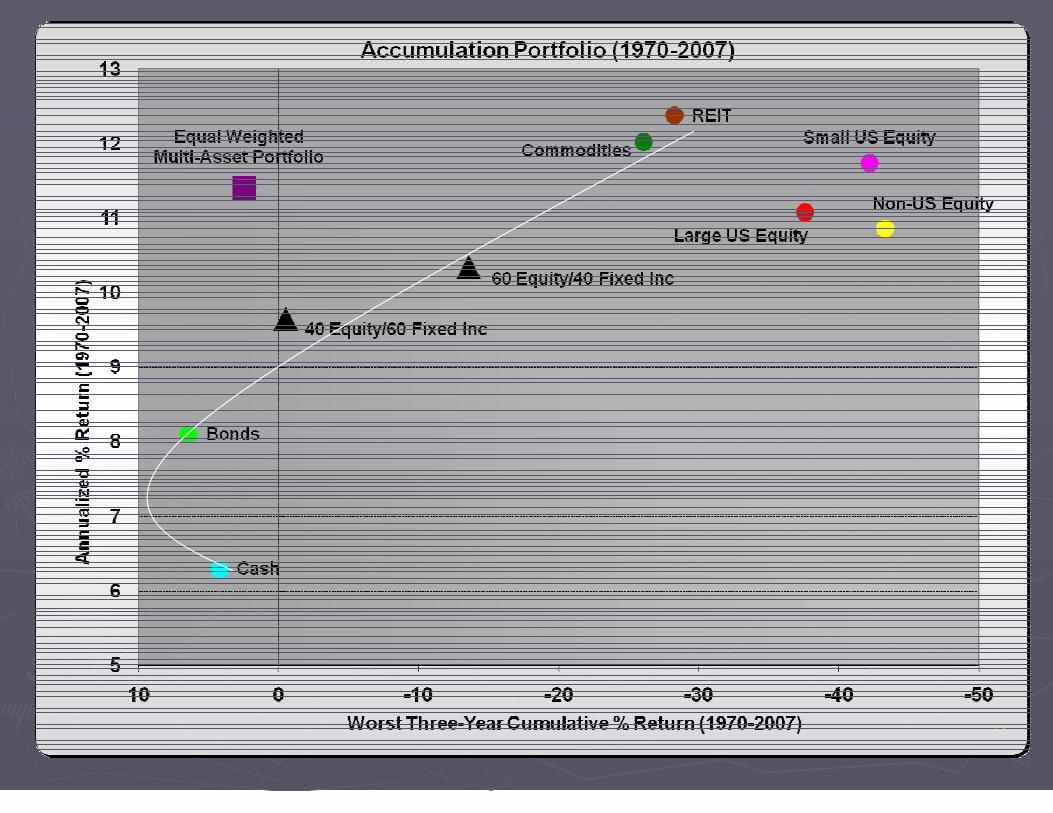

MultiMulti--Asset Portfolio vsAsset Portfolio vs. . Single AssetsSingle Assets

1970-2007

Large US Equity

Small US Equity

Non-US Equity

US Bonds

Cash Real Estate

Commodities

Equally Weighted 7-Asset Portfolio

38-Year Average Annualized %

Return 11.08 11.74 10.86 8.10 6.29 12.38 12.02 11.41

38-Year Standard Deviation of

Annual Returns 16.62 21.68 21.54 5.39 3.07 18.45 23.93 8.60

Number of Years with Negative

Returns 8 11 10 1 0 8 9 4

Worst One-Year % Return (26.47) (30.90) (23.45) (1.75) 1.05 (23.44) (35.75) (5.48)

Worst Three-Year Cumulative %

Return (37.61) (42.22) (43.32) 6.43 4.22 (28.30) (26.06) 2.43

WhatWhat’’s Different in s Different in 20082008? ? Commodities and real estate are not helping as much as in prior Commodities and real estate are not helping as much as in prior downturnsdownturns..

17

Year

Large US Equity

Small US Equity

Non-US Equity

Intermediate US Govt Bonds

Cash Real

Estate Commodities

Equally Weighted

Multi-Asset Portfolio

1973197319731973 (14.69) (30.90) (14.92) 4.60 7.46 (15.52) 74.96 1.57

1974197419741974 (26.47) (19.90) (23.16) 7.03 8.35 (21.42) 39.51 (5.15)

2000200020002000 (9.10) (3.02) (14.17) 10.47 6.32 31.04 49.74 10.18

2001200120012001 (11.89) 2.49 (21.44) 8.42 3.67 12.35 (31.93) (5.48)

2002200220022002 (22.10) (20.48) (15.94) 9.64 1.68 3.58 32.07 (1.65)

YTD YTD YTD YTD

Oct Oct Oct Oct 31313131

2008200820082008

(32.9) (29.1) (42.0) 4.8 1.5 (30.5) (28.3) (22.34)

18

Portfolio (Equity/

Fixed Income)

Large US Stock

Small US Stock

Non-US Stock

Bonds

Cash

60/4060/40

30%30%

15%15%

15%15%

30%30%

10%10%

40/6040/60

20%20%

10%10%

10%10%

50%50%

10%10%

Typical Typical MultiMulti--Asset PortfoliosAsset Portfolios

19

20

Performance in Performance in PostPost--RetirementRetirement

Distribution Distribution PhasePhase

Various Portfolios Various Portfolios

vsvs. .

MultiMulti--Asset PortfolioAsset Portfolio

Benefit Benefit #3#3

When built correctlyWhen built correctly, , multimulti--asset asset

portfolios are portfolios are durabledurable during the during the

postpost--retirement distribution phaseretirement distribution phase..

DurableDurable = = Growth Growth + + Downside ResistanceDownside Resistance

21

22

Distribution Portfolio (1970-2007)

1

2

3

4

5

6

EW

CW

40/60

60/40

6%

7%

8%

9%

10%

11%

12%

10% 15% 20% 25% 30% 35% 40% 45% 50% 55%

Frequency of Loss (as measured by % Change in Year-to-Year Account Value)

Inte

rnal R

ate

of R

etu

rn (

1970-2

007)

1 = One-asset portfolio (100% Cash) 2 = Two-asset portfolio (50% each Bonds, Cash) 3 = Three-asset portfolio (33% each Cash, Bonds, Large US Stock) 4 = Four-asset portfolio (25% each Cash, Bonds, Large US Stock, Small US Stock) 5 = Five-asset portfolio (20% each Cash, Bonds, Large US Stock, Small US Stock, Non-US Stock) 6 = Six-asset portfolio (16.7% each Cash, Bonds, Large US Stock, Small US Stock, Non-US Stock, REIT) EW = Seven-asset equal-weighted portfolio (14.3% each Cash, Bonds, Large US Stock, Small US Stock, Non-US Stock, REIT, Commodities) CW = Seven-asset custom-weighted portfolio (12% Large US, 8% Small US, 10% Non-US, 5% REIT, 5% Commodities, 40% Bond, 20% Cash) 60/40 = 30% Large US, 15% Small US, 15% Non-US, 30% Bond, 10% Cash 40/60 = 20% Large US, 10% Small US, 10% Non-US, 50% Bond, 10% Cash

$500,000 Initial Portfolio Value 5% withdraw rate 3% inflation rate of annual withdrawal

23

►►Minimizing Minimizing frequency of lossfrequency of loss and and size of size of

portfolio lossportfolio loss while generating robust while generating robust

performance are distinct benefits of low performance are distinct benefits of low

correlation portfolioscorrelation portfolios——provided that each provided that each

asset is assigned a asset is assigned a meaningful allocationmeaningful allocation..

►►Recovering from large losses is more Recovering from large losses is more

difficult in distribution portfoliosdifficult in distribution portfolios----when when

money is being systematically withdrawnmoney is being systematically withdrawn..

24

Portfolio Loss

Needed Average Annual % Return to Restore Original Portfolio Balance

WITHDRAWAL Portfolio First Year Withdrawal of 5% of initial balance, 3% increase of annual withdrawal

Within Within 1 1 YearYear

Within Within 2 2 YearsYears

Within Within 3 3 YearsYears

Within Within 4 4 YearsYears

Within Within 5 5 YearsYears

-5% 16.8% 11.1% 9.3% 8.4% 8.0%

-10% 23.7% 14.4% 11.5% 10.1% 9.4%

-15% 31.4% 18.0% 13.9% 12.0% 10.9%

-20% 40.2% 22.0% 16.5% 14.0% 12.5%

-25% 50.2% 26.4% 19.4% 16.1% 14.3%

Portfolio Loss

BUY-and-HOLD Portfolio

Within 1 Year

Within 2 Years

Within 3 Years

Within 4 Years

Within 5 Years

-5% 5.3% 2.6% 1.7% 1.3% 1.0%

-10% 11.1% 5.4% 3.6% 2.7% 2.1%

-15% 17.6% 8.5% 5.6% 4.1% 3.3%

-20% 25.0% 11.8% 7.7% 5.7% 4.6%

-25% 33.3% 15.5% 10.1% 7.5% 5.9%

25

Portfolio (Equity/

Fixed Income)

Large US Stock

Small US Stock

Non-US Stock

Bonds Cash

60/4060/40 30%30% 15%15% 15%15% 30%30% 10%10%

40/6040/60 20%20% 10%10% 10%10% 50%50% 10%10%

20/8020/80 10%10% 5%5% 5%5% 60%60% 20%20%

0/1000/100 0%0% 0%0% 0%0% 70%70% 30%30%

Example Distribution Example Distribution PortfoliosPortfolios

26

Final Outcomes Final Outcomes Are Very Are Very Dependent on Timing of ReturnsDependent on Timing of Returns

Final Account Value During Each 20-Year Period

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

20-Year Period Ending in...

60% Equity/40% Fixed Income 40% Equity/60% Fixed Income 20% Equity/80% Fixed Income 100% Fixed Income

60/40

40/60

20/80

0/100

DISTRIBUTION PORTFOLIO $500,000 Initial Portfolio Value 5% withdraw rate 3% inflation rate of annual withdrawal

1975-1994

27

Distribution Portfolio GoalsDistribution Portfolio Goals Stabilize Returns to Minimize Timing DependenceStabilize Returns to Minimize Timing Dependence

Maintain Robust Performance to Increase Portfolio LongevityMaintain Robust Performance to Increase Portfolio Longevity

(5)

0

5

10

15

20

25

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

40/60 Equal-Weighted 7 Asset Portfolio

3-Year Annualized Rolling Returns

1970-2007

Ave. 3-Yr Return Ave. 3-Yr Std Dev

40 Equity/60 Fixed Income 9.8% 4.3% 7-Asset EW Portfolio 11.7% 4.4%

Part TwoPart Two

28

29

Building Building a a MultipleMultiple--Asset Asset

Low Low Correlation Correlation PortfolioPortfolio

The The 77TwelveTwelve PortfolioPortfolio

►►77 Core Asset ClassesCore Asset Classes

withwith

►►1212 Underlying FundsUnderlying Funds

30

TheThe 7Twelve PortfolioPortfolio A A MultipleMultiple--Asset Asset Global PortfolioGlobal Portfolio

Approximately 60% of the Portfolio Allocation in Equity and Diversifying Assets

Approximately 40% of the Portfolio Allocation in Bonds and Cash

US Equity

Non-US Equity

Real Estate

Resources US

Bonds Non-US Bonds

Cash

Large

Companies Developed

Markets Global

Real Estate Natural

Resources US Aggregate

Bonds International

Bonds US Money

Market

Medium-sized

Companies Emerging

Markets Commodities

Inflation

Protected

Bonds

Small

Companies

31

Large US

Mid US

Small US

Non-US Developed

Non-US

Emerging

Global

Real Estate

Natural

Resources Commodities

US

Aggregate Bonds

Inflation

Protected Bonds

Non-US

Bonds

Mid US 0.58

Small US 0.88 0.38

Non-US Developed 0.65 0.16 0.48

Non-US Emerging 0.50 (0.18) 0.50 0.74

Global Real Estate 0.70 0.46 0.74 0.19 0.17

Natural Resources 0.47 0.37 0.48 0.53 0.69 0.35

Commodities 0.14 0.25 0.12 0.09 0.34 0.35 0.59

US Aggregate Bonds (0.39) 0.05 (0.17) (0.68) (0.83) 0.05 (0.61) (0.24)

Inflation Protected Bonds

(0.47) 0.01 (0.27) (0.54) (0.42) (0.02) (0.08) 0.38 0.63

Non-US Bonds (0.20) (0.20) (0.10) 0.25 (0.09) (0.11) (0.17) (0.09) 0.36 0.42

US Money Market (0.13) 0.29 (0.24) (0.35) (0.32) (0.35) (0.15) (0.22) 0.08 (0.22) (0.50)

7Twelve CorrelationCorrelation Aggregate Correlation = 0.09 Using annual returns from 1998-2007

32

7Twelve Portfolio

-30%

-20%

-10%

0%

10%

20%

30%

40%

0% 20% 40% 60% 80% 100% 120%

10-Year Standard Deviation of Return

10-Y

ear

An

nu

alized

Retu

rn

1,979 distinct mutual funds with at least 10 years of performance as of December 31, 2007

Red dot is 7Twelve portfolio

33

Calendar Year Total % Return

7Twelve Portfolio

American Funds Capital Income Builder

Fidelity Global Balanced

S&P 500 Index

1998 0.10 17.75 13.90 28.62

1999 15.47 23.03 7.96 21.07

2000 12.26 (5.97) 5.60 (9.06)

2001 2.17 (8.15) (2.49) (12.02)

2002 2.31 (6.15) (7.74) (22.15)

2003 28.61 29.90 24.38 28.50

2004 17.46 13.67 12.55 10.74

2005 12.31 9.00 6.44 4.77

2006 15.13 13.70 11.92 15.64

2007 12.46 13.77 7.70 5.39

10-Year Annualized Return

11.54 9.35 7.69 5.83

Correlation to S&P 500 Index

.50 .94 .89 1.00

34

Accumulation 7Twelve Portfolio

35

Distribution 7Twelve Portfolio $100,000 Initial Account Value, 5% Initial Withdrawal, 3% Annual Increase in Withdrawal

Age of Investor ���� Under Age 50

Age 50-60

Age 60-70

Over Age 70

Comparison Funds

Portfolio Mix ����

100% 7Twelve

80% 7Twelve 10% TIPS 10% Cash

60% 7Twelve 20% TIPS 20% Cash

40% 7Twelve 30% TIPS 30% Cash

American Funds Capital Income

Builder A (CAIBX)

Fidelity Global

Balanced (FGBLX)

Accumulation Portfolio (1998 – 2007)

10-Year Average Annualized Return (%)

11.54 10.40 9.23 8.03

10.06 9.35

Worst One-Year % Loss 0.10 0.99 1.88 2.77

(2.78) (8.15)

Distribution Portfolio (1998 – 2007) ($100,000 initial value, 5% annual withdrawal, 3% annual increase in withdrawal)

Internal Rate of Return (%) 10.24 9.28 8.30 7.29

8.90 8.46

Worst One-Year Portfolio Loss

($4,899) ($4,010) ($3,122) ($2,233)

($8,118) ($15,267)

Correlation (1998 – 2007)

Correlation to S&P 500 0.50 0.45 0.37 0.19 0.44 0.94 36

As of October As of October 3131, , 20082008

37

Master 7TwelveTM Portfolios Year-to-Date

Total % Return as of October 31, 2008

10-Year Annualized % Return as of

October 31, 2008

100% 7Twelve (27.72) 8.19

80% 7Twelve, 10% TIPS, 10% Cash (22.72) 7.69

60% 7Twelve, 20% TIPS, 20% Cash (17.73) 7.08

40% 7Twelve, 30% TIPS, 30% Cash (12.74) 6.39

Comparison Funds

American Funds Capital Income Builder (CAIBX)

(30.15) 5.48

Fidelity Global Balanced (FGBLX)

(24.57) 5.38

T. Rowe Price Personal Strategy Balanced (TRPBX)

(27.77) 3.57

Vanguard Balanced (VBINX)

(21.37) 2.98

Vanguard 500 Index (VFINX)

(32.87) 0.32

38

DJIA hit allDJIA hit all--time high on Oct time high on Oct 99, , 20072007

365 days later…(Thursday Oct 9, 2008)

Trailing 1-year Return as of Oct 9, 2008

►DJIA -39.4%

►S&P 500 -40.6%

►100% 7Twelve -25.9%

►40/30/30 7Twelve* -10.4% * 40% 7Twelve, 30% TIPS, 30% Cash

39

40

11) ) Portfolio logistics are very straightPortfolio logistics are very straight--forwardforward::

�� EquallyEqually--weightedweighted, , annually rebalancedannually rebalanced. .

�� Using cash flows to accomplish rebalance increases tax efficiencUsing cash flows to accomplish rebalance increases tax efficiencyy..

22) ) No reliance upon tactical skill or No reliance upon tactical skill or timingtiming. .

33)) Represents the core Represents the core ““modulemodule”” of any portfolio pre or post retirementof any portfolio pre or post retirement..

ExamplesExamples: : 80%80% 77TwelveTwelve, , 20%20% individual stocksindividual stocks 60%60% 77TwelveTwelve, , 20%20% TIPSTIPS, , 20%20% cashcash 50%50% 77TwelveTwelve, , 30%30% fixed annuityfixed annuity, , 20%20% cashcash

44) ) Can be built using actively managed fundsCan be built using actively managed funds, , passively managed index passively managed index

fundsfunds, , ETFsETFs, , ETNsETNs, , or CTFs or CTFs ((collective trust fundscollective trust funds).).

55) ) Sets upper and lower boundaries for number of portfolio holdingsSets upper and lower boundaries for number of portfolio holdings::

�� ((77 asset classes employing asset classes employing 1212 underlying fundsunderlying funds) )

7Twelve Portfolio

41

The The 77TwelveTwelve PortfolioPortfolio The Benefits of Low CorrelationThe Benefits of Low Correlation

Craig Craig LL. . IsraelsenIsraelsen, , PhPh..DD.. Brigham Young UniversityBrigham Young University

EmailEmail:: craigcraig@@77TwelvePortfolioTwelvePortfolio..comcom

WebWeb:: wwwwww..77TwelvePortfolioTwelvePortfolio..comcom

Related Documents