The 2006 Health Insurance Reform in the Netherlands – introducing universal coverage Prof. Peter P. Groenewegen, PhD Dublin, December 6, 2010

The 2006 Health Insurance Reform in the Netherlands – introducing universal coverage Prof. Peter P. Groenewegen, PhD Dublin, December 6, 2010.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The 2006 Health Insurance Reform in the Netherlands – introducing

universal coverage

Prof. Peter P. Groenewegen, PhD

Dublin, December 6, 2010

Health care insurance law

• Introduced on 1 January 2006• Abolition of distinction between

private and public insurance• Insurance under private law with

public limiting conditions• Obligation for every citizen to take

health insurance• Part of larger reform, aiming at

higher quality and lower costs

Dutch health insurance until 2006

Public insurance (65%):• obligatory for all

employees and dependents below income ceiling;

• no risk selection;• no premium

differentiation;• premiums largely income

related with small nominal premium

• administered through sickness funds

Private insurance (35%):• not obligatory;• for people above income

ceiling;• admitted after risk

selection;• premium differentiation• premiums nominal and

risk related• administered through

damage insurance companies and sickness funds

Introduction period

• Large number of switchers (18%); now stabilized at former levels of appr. 4%

• No big administrative problems for insurance organisations

• More administrative problems for GPs (concurrent change of payment system)

Why did it run so smoothly?

• Long history: starting in 1987• From early 1990’s: many small

steps in regulation• Anticipation and adaptation by key

actors in the systemThese steps made insurance reform

both possible and inevitable

The fate of the Dekker committee report 1987

• 1988 government accepts the Dekker plans.• 1989 shift of government coalition from

Christian-democrats and conservative liberals to Christian-democrats, labour party and liberal democrats.

• 1990 adapted Dekker plan, known as plan Simons.

• 1993 end of plan Simons.• 1994 shift of government coalition to labour,

liberal democrats, and conservative liberals; no-regret policy of small steps.

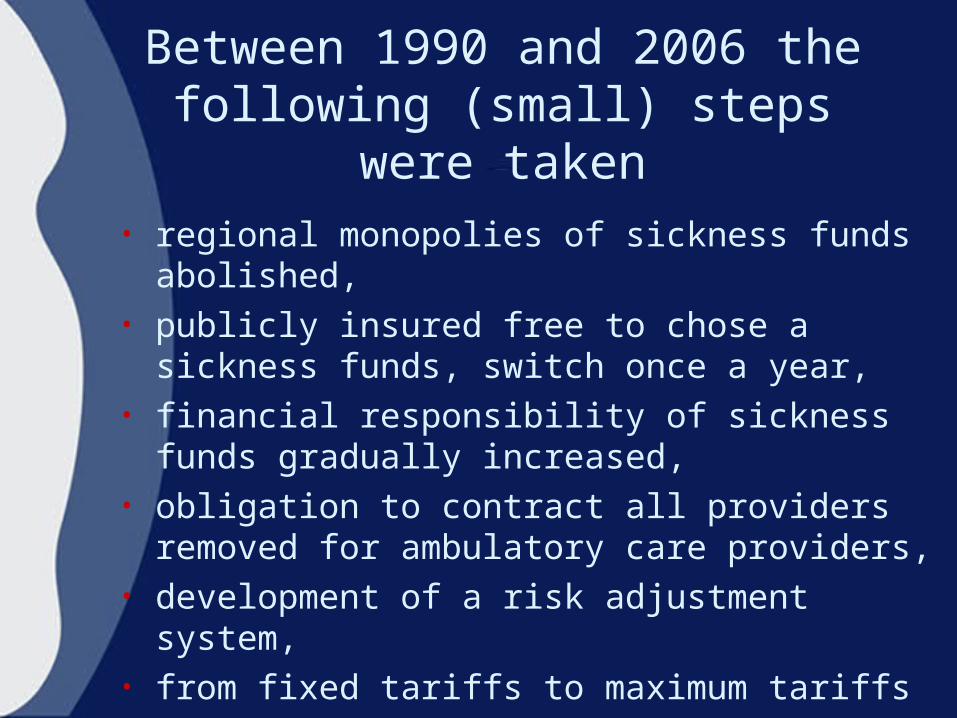

Between 1990 and 2006 the following (small) steps were

taken• regional monopolies of sickness funds

abolished, • publicly insured free to chose a sickness

funds, switch once a year,• financial responsibility of sickness funds

gradually increased,• obligation to contract all providers

removed for ambulatory care providers,• development of a risk adjustment system,• from fixed tariffs to maximum tariffs

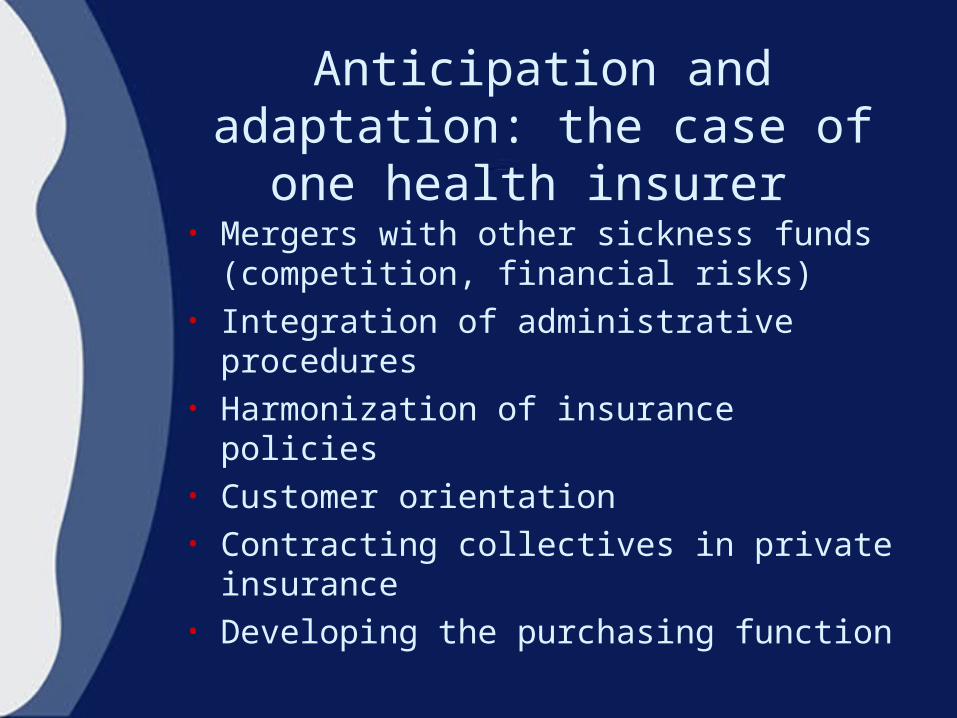

Anticipation and adaptation: the case of one health

insurer • Mergers with other sickness funds

(competition, financial risks)• Integration of administrative

procedures• Harmonization of insurance policies• Customer orientation• Contracting collectives in private

insurance• Developing the purchasing function

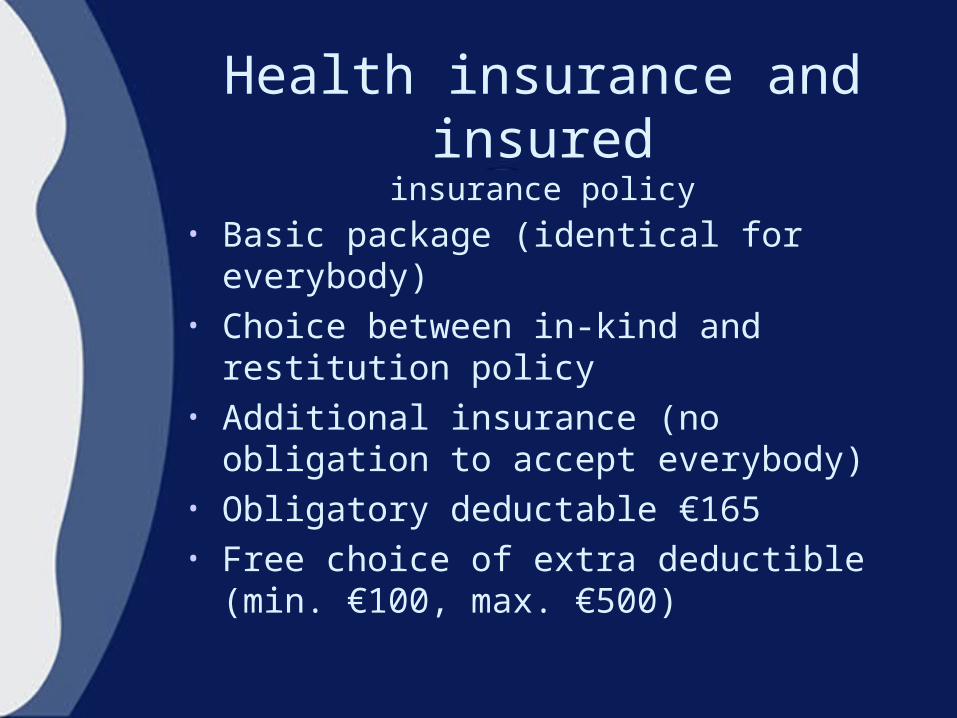

Universal health insurance after

1 January 2006

• Basic package (identical for everybody)

• Choice between in-kind and restitution policy

• Additional insurance (no obligation to accept everybody)

• Obligatory deductable €165• Free choice of extra deductible

(min. €100, max. €500)

Health insurance and insured

insurance policy

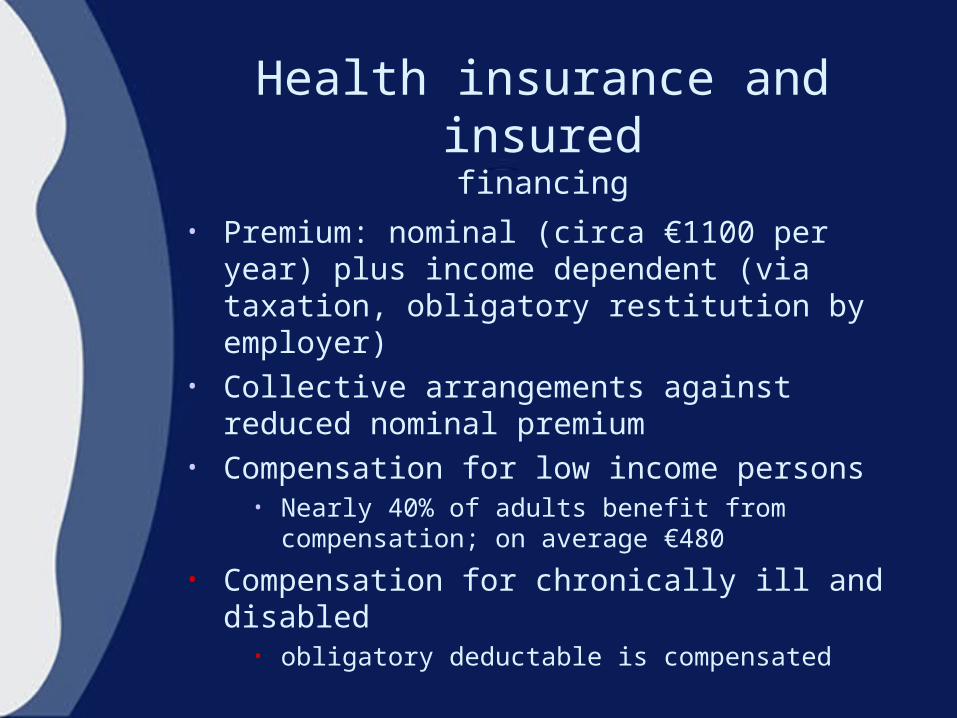

Health insurance and insuredfinancing

• Premium: nominal (circa €1100 per year) plus income dependent (via taxation, obligatory restitution by employer)

• Collective arrangements against reduced nominal premium

• Compensation for low income persons• Nearly 40% of adults benefit from

compensation; on average €480

• Compensation for chronically ill and disabled

• obligatory deductable is compensated

Health insurance and insuredaccess

• Obligation to accept everybody, risk selection and premium differentiation forbidden

• Free choice between insurance organizations

• Risk equalization between insurers• Possibilities for risk selection

• Additional insurance• Collective insurance• Preferred provider contracts

Uninsured• May 2006: 173.000• May 2007: 151.000• May 2008: 153.000• May 2009: 152.000• Approx. 1% of total

population• Over-representation

of migrants and younger people

Bad payers• Dec. 2006: 190.000• Dec. 2007: 240.000• Dec. 2008: 279.000• Dec. 2009: 318.500• Approx. 2% of adult

population• Over-

representation of migrants, social security dependents, one-parent families

Health insurance and insured

access

6%

3%2%

29%

21%

13%

9%

5%4%

6%

4%2%

4%

1%

8%

till 39 years 40 - 64 years 65 years and over

switched (2005)

switched (2006)

switched (2007)

switched (2008)

switched (2009)

Source: Dutch Health Care Consumer Panel

Health insurance and insuredswitching health insurer

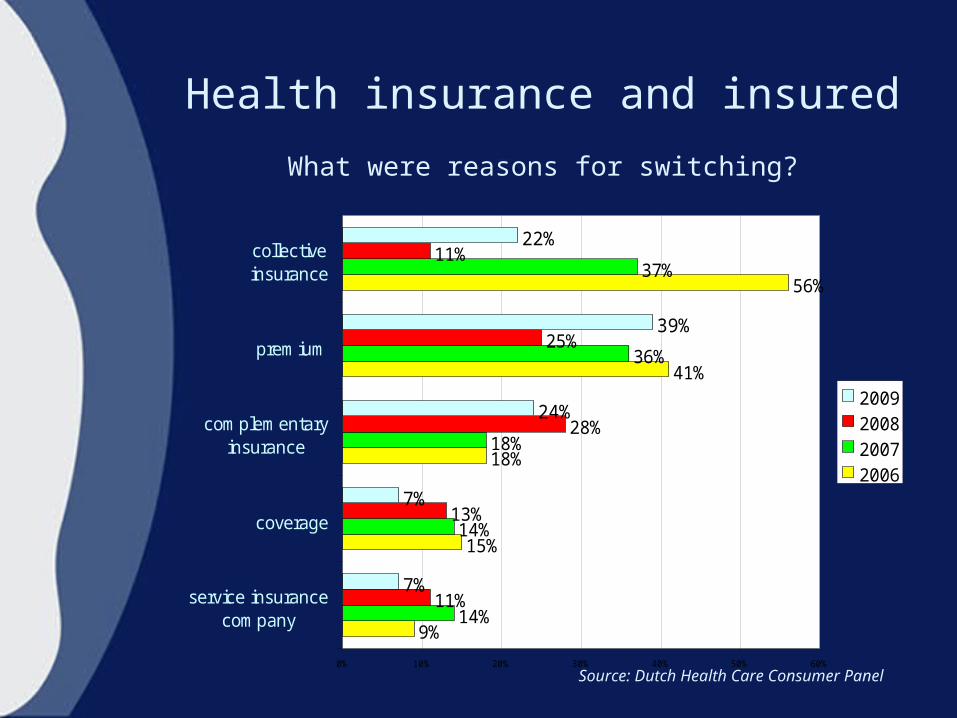

Health insurance and insured What were reasons for switching?

9%

15%

18%

41%

56%

14%

14%

18%

36%

37%

11%

13%

28%

25%

11%

7%

7%

24%

39%

22%

0% 10% 20% 30% 40% 50% 60%

service insurancecompany

coverage

complementaryinsurance

premium

collectiveinsurance

2009200820072006

Source: Dutch Health Care Consumer Panel

Health insurance and insured Collectives

• Employers• Patient organizations• Unions• All other kinds of groups (lotteries,

stores, etc)• 65% has collective insurance • Discount on average 7%

2%

72%

10%

4%

12%

patient organizationemployerunionmunicipalityother

Source: Dutch Health Care Consumer Panel

Health insurance and insured Collectives

• For employers : premium, discount for basic and additional insurance were most important

• For patient organizations: service, coverage and discount for additional insurance were most important

Source: questionnaire amongst 42 organizations. Van Ruth, De Jong and Groenewegen, 2007

Health insurance and insured Collectives

• Employers base their choice on price• Patient organizations value content• Quality improvement is possible

through patient organizations efforts• However, they are a minority, and

mobilize less insured • It took more effort and they received

lower discounts

Health insurance and insured Collectives

Health insurers and providerscontracts and financing

• Obligation to contract enough care to provide for insured with in-kind policy

• Obligation to mediate between providers and insured with restitution policy

• Preferred provider contracts• For 34% of hospital care prices are

negotiable

• Health insurers need information about performance of providers

• Performance information is still scarce

• Examples: Consumer Quality-index and indicators required by the Health Care Inspectorate

• Contracts can then be related to performance indicators

Health insurers and providers

contracts and financing

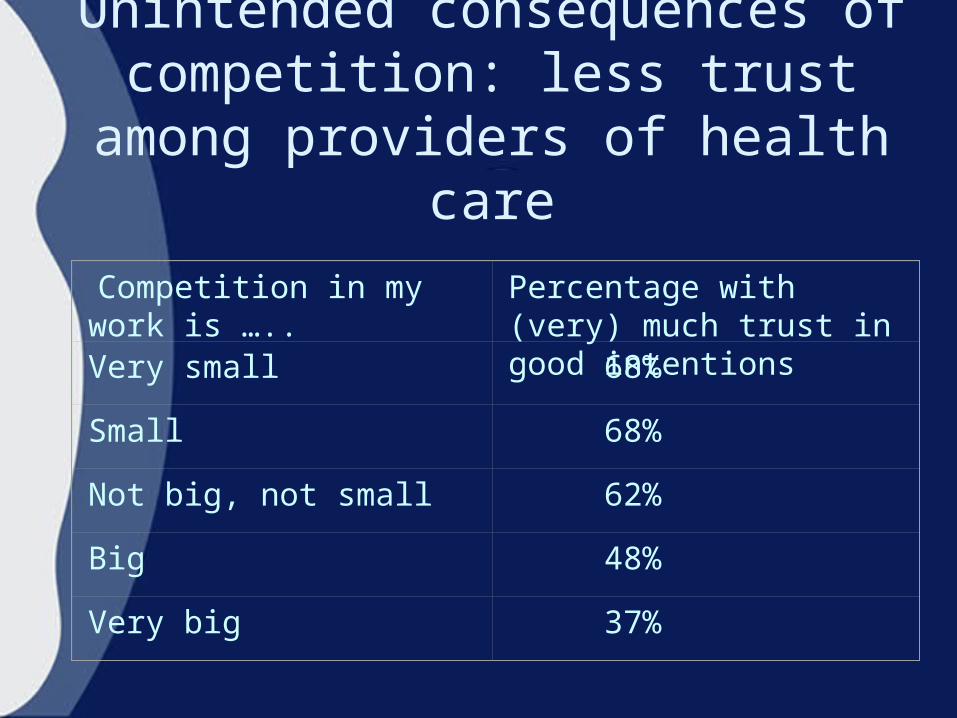

• Erosion of mutual trust, affecting the willingness to cooperate

• Crowding out of professional values• Much supervision – high costs, low

trust

Health insurers and providers

unintended consequences of competition

Competition in my work is …..

Percentage with (very) much trust in good intentions

Very small 68%

Small 68%

Not big, not small 62%

Big 48%

Very big 37%

Unintended consequences of competition: less trust among

providers of health care

Provider and patientaccess

• Gate keeping system: no free access to specialist care

• Freedom of choice of provider can be restricted for insured with in-kind policy

• Insurance organization may have negotiated specific care programmes

Can insurers guide patients?• There are positive incentives: the

obligatory deductable is not paid for preferred providers

• Only few examples of insurance policies with selective contracting

Provider and patientaccess

Effects of reforms: Quality of care

• Quality is hardly part of negotiations between insurers and providers, price is most important

• Insured choose their insurer based on premium, not on quality

Effects of reforms: Cost containment

Cost containment is difficult in demand driven system

• Micro versus macro efficiency: Prices may decrease, volume is increasing

Options in case of increasing costs:- restriction of basic package- shifts towards additional insurance

- increased cost sharing- decreased compensation for lower income people

Conclusions

• Smooth introduction (after 15 years of small steps)

• It is still work in progress; monitoring is very important

• Long term (unintended) consequences unknown

• Quality of care is hardly included in negotiations

• Cost containment is difficult

Related Documents