ed: CK / sa: CT, PY SET : 1,571.05 Analyst Chanpen SIRITHANARATTANAKUL +662 657 7824 [email protected] Thailand Research Team +662 657 7831 [email protected] Key Indices Current % Chng SET Index 1571.05 0.48% SET 100 Index 2223.24 0.49% SET 50 Index 985.53 0.47% Bt/US$ Exchange Rate 35.65 -0.37% Daily Volume (m shrs) 12,644 Daily Turnover (US$m) 1,946 Source: SET, DBS Vickers Market Key Data (%) EPS Gth Div Yield 2015A (16.9) 3.1 2016F 35.8 3.0 2017F 7.1 3.1 (x) PER EV/EBITDA 2015A 20.9 8.8 2016F 15.5 8.4 2017F 14.5 7.9 Source: DBS Vickers STOCKS Source: DBS Vickers, Bloomberg Finance L.P. Closing price as of 30 Dec 2016 DBS Group Research . Equity 6 Jan 2017 Thailand Market Focus Strategy Refer to important disclosures at the end of this report Bottom-up selection still key Our 12-month SET Index target is at 1650, representing 15.6x 2017F earnings Expect market EPS growth of 7% for 2017 Five themes for investment in 2017 Top 10 picks: ANAN, AOT, CK, CPALL, GL, IVL, MTLS, SCC, TISCO, and TKN. 2016 recap. The Thai market was the best performing market in the region in 2016, with the SET Index rising 19.8% vs 3.5% gain for regional peers. The strong performance was due to the strong corporate EPS growth of c. 36% boosted by energy, petrochem and transportation sector and the return of foreign investors into the market. Mid/small-cap stocks (+64.8%) strongly outperformed large-cap ones (+18.9%), thanks to their superior earnings growth outlook. Expect 7% corporate EPS growth for 2017. Looking forward to 2017, we expect market earnings to grow 7%. Our current earnings growth forecast is 15% for 2017. We believe the key difference was mainly in the banking and energy sector, due to different in provisioning and oil price assumptions. Based on our conservative 7% EPS growth, our SET Index target is now 1650, based on 15.6x earnings in 2017. Five themes for 2017 investment. We have five themes for investment in 2017. They are (i) infrastructure upcycle – The rising infrastructure spending in 2017 should be a key catalyst for construction contractors like CK, SCC, STEC (ii) superior earnings growth outlook – Those fit the themes are ANAN, FN, IVL, WORK, MTLS, TKN, BEAUTY (iii) strong tourism – Beneficiaries are AOT, ERW (iv) strong US dollar – This should benefit exporters like IVL, HANA, TU (v) CLMV exposure – GL, BEAUTY, CBG Top ten picks. Our top ten picks are Ananda Development (ANAN), Airports of Thailand (AOT), Ch. Karnchang (CK), CP All (CPALL), Group Lease (GL), Indorama Ventures (IVL), Muangthai Leasing (MTLS), Siam Cement (SCC), Tisco Group (TISCO), and Taokaenoi Marketing (TKN). Price Mkt Cap Target Price Performance (%) Bt US$m Bt 3 mth 12 mth Rating Ananda Development 4.94 458 5.60 2.1 24.6 BUY Airports of Thailand 398.00 15,826 455.00 (1.5) 17.5 BUY Ch. Karnchang 31.00 1,462 40.00 5.1 13.8 BUY CP ALL 62.50 15,627 75.00 2.5 47.0 BUY Group Lease Public Co Ltd 57.25 2,431 88.00 81.6 339.5 BUY Indorama Ventures 33.50 4,489 42.00 9.2 57.5 BUY Muangthai Leasing Pcl 24.70 1,458 32.00 42.1 28.7 BUY Siam Cement 496.00 16,567 580.00 (8.4) 9.6 BUY TISCO Financial Group 60.25 1,343 65.00 4.7 37.3 BUY Taokaenoi Food & Marketing 28.00 1,076 32.00 17.8 na BUY

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ed: CK / sa: CT, PY

SET : 1,571.05

Analyst Chanpen SIRITHANARATTANAKUL +662 657 7824 [email protected] Thailand Research Team +662 657 7831 [email protected]

Key Indices

Current % Chng

SET Index 1571.05 0.48%

SET 100 Index 2223.24 0.49%

SET 50 Index 985.53 0.47%

Bt/US$ Exchange Rate 35.65 -0.37%

Daily Volume (m shrs) 12,644

Daily Turnover (US$m) 1,946

Source: SET, DBS Vickers Market Key Data

(%) EPS Gth Div Yield

2015A (16.9) 3.1

2016F 35.8 3.0

2017F 7.1 3.1

(x) PER EV/EBITDA

2015A 20.9 8.8

2016F 15.5 8.4

2017F 14.5 7.9

Source: DBS Vickers STOCKS

Source: DBS Vickers, Bloomberg Finance L.P.

Closing price as of 30 Dec 2016

DBS Group Research . Equity

6 Jan 2017

Thailand Market Focus

Strategy Refer to important disclosures at the end of this report

Bottom-up selection still key

Our 12-month SET Index target is at 1650,

representing 15.6x 2017F earnings

Expect market EPS growth of 7% for 2017

Five themes for investment in 2017

Top 10 picks: ANAN, AOT, CK, CPALL, GL, IVL, MTLS,

SCC, TISCO, and TKN.

2016 recap. The Thai market was the best performing market in

the region in 2016, with the SET Index rising 19.8% vs 3.5% gain

for regional peers. The strong performance was due to the

strong corporate EPS growth of c. 36% boosted by energy,

petrochem and transportation sector and the return of foreign

investors into the market. Mid/small-cap stocks (+64.8%) strongly

outperformed large-cap ones (+18.9%), thanks to their superior

earnings growth outlook.

Expect 7% corporate EPS growth for 2017. Looking forward

to 2017, we expect market earnings to grow 7%. Our current

earnings growth forecast is 15% for 2017. We believe the key

difference was mainly in the banking and energy sector, due to

different in provisioning and oil price assumptions. Based on our

conservative 7% EPS growth, our SET Index target is now 1650,

based on 15.6x earnings in 2017.

Five themes for 2017 investment. We have five themes for

investment in 2017. They are

(i) infrastructure upcycle – The rising infrastructure spending in

2017 should be a key catalyst for construction contractors like

CK, SCC, STEC

(ii) superior earnings growth outlook – Those fit the themes are

ANAN, FN, IVL, WORK, MTLS, TKN, BEAUTY

(iii) strong tourism – Beneficiaries are AOT, ERW

(iv) strong US dollar – This should benefit exporters like IVL,

HANA, TU

(v) CLMV exposure – GL, BEAUTY, CBG

Top ten picks. Our top ten picks are Ananda Development

(ANAN), Airports of Thailand (AOT), Ch. Karnchang (CK), CP All

(CPALL), Group Lease (GL), Indorama Ventures (IVL), Muangthai

Leasing (MTLS), Siam Cement (SCC), Tisco Group (TISCO), and

Taokaenoi Marketing (TKN).

Price Mkt Cap Target Price Performance (%)

Bt US$m Bt 3 mth 12 mth Rating

Ananda

Development 4.94 458 5.60 2.1 24.6 BUY

Airports of Thailand 398.00 15,826 455.00 (1.5) 17.5 BUY

Ch. Karnchang 31.00 1,462 40.00 5.1 13.8 BUY

CP ALL 62.50 15,627 75.00 2.5 47.0 BUY

Group Lease Public

Co Ltd 57.25 2,431 88.00 81.6 339.5 BUY

Indorama Ventures 33.50 4,489 42.00 9.2 57.5 BUY

Muangthai Leasing

Pcl 24.70 1,458 32.00 42.1 28.7 BUY

Siam Cement 496.00 16,567 580.00 (8.4) 9.6 BUY

TISCO Financial

Group 60.25 1,343 65.00 4.7 37.3 BUY

Taokaenoi Food &

Marketing 28.00 1,076 32.00 17.8 na BUY

Market Focus

Page 2

Our top picks

Our top picks strongly outperformed the market in 2016.

Our portfolio has posted an impressive 45% price return since

March 2016 when we started to track our monthly performance,

vs the market’s 12% rise during the same period.

Among our best picks in 2016 were Group Lease (GL), Ananda

Development (ANAN), The Erawan Group (ERW), Ladprao

Hospital (LPH), Taokaenoi Marketing (TKN), LH Hotel Leasehold

REIT (LHHOTEL), etc.

Cumulative price returns of our stock picks vs the market

Source: DBS Vickers

Stock picks for 2017. Looking forward into 2017, we believe

bottom-up selection remains the key. We have top ten picks for

the market based on five investment themes. These include (i)

infrastructure upcycle, (ii) superior earnings growth outlook, (iii)

strong tourism, (iv) strong US dollar, and (v) CLMV exposure.

The top ten picks are ANAN, AOT, CK, CPALL, GL, IVL, MTLS, SCC,

TISCO and TKN.

ANAN is our top pick in the residential property counter, thanks to

its strong earnings growth of 51% this year, supported by rising

contribution from its JV with Mitsui Fudosan. ANAN’s revenue

visibility is also the highest in the sector, supported by its large

backlog on hand which is equivalent to 74% of estimated transfers

in 2017.

AOT should continue to benefit from the strong tourism outlook

amid calmer politics. The company’s plan to split par from Bt10 to

Bt1, subject to shareholders’ approval on 27 January 2017, should

help improve the stock’s trading liquidity and be a near-term

catalyst for the share price.

CK should be a prime beneficiary of rising infrastructure spending

in Thailand. Group Lease (GL) remains one of our top picks in the

Thai market, thanks to its aggressive expansion into neighbouring

countries which should result in strong earnings growth outlook.

We like CPALL for its dominant position in fast growing convenient

store format with FY15-18F CAGR of 21%. The stock is also very

resilient to the slowing economy and generates strong annual cash

flow of c. Bt34bn.

GL offers a good example of a company that has been very

successful in expanding into CLMV countries. The company is one

of the largest motorcycle HP players in Thailand. GL has grown its

businesses aggressively in Cambodia, has the No.1 market share in

Laos, has recently started a finance business in Indonesia, has just

acquired 100% of a microfinance company in Myanmar and 30%

of a finance company in Sri Lanka, and aims to become the world

finance company in the foreseeable future.

We like IVL for its improving outlook of core earnings, driven by

high value-added products and its leading position in global market

for PET/Polyester and automotive-related specialty products. We

believe the market remains too pessimistic on its core EBITDA

margin and its re-rating in 2017F is likely. The strong baht against

the greenback is also positive for the company, as the company

derives most of its revenue in US dollar.

MTLS’ asset quality remains solid with low NPL and high coverage

ratio. We expect the company to report strong earnings growth of

51% this year.

We also like SCC on its solid earnings performance and financial

position, and healthy ROE and EPG on its improving earnings

outlook, driven by the automotive plastic segment. Key catalyst for

the stock is new orders from European automakers which will

launch SUV cars in 2017-18.

TISCO is our top pick in the banking sector. We like the stock for

its potential loan growth turnaround, improving asset quality, and

high ROE.

We expect TKN’s earnings to jump 52% this year, on the back of

the capacity expansion from the new plant. Note that the new

plant under BOI promotional privileges will come online in 1Q17

and double the company’s existing capacity.

80

90

100

110

120

130

140

150

160

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

De

c-1

6

Market

Our portfolio

Market Focus

Page 3

Stock picks for 2017

Mkt Price Target % PE PBV Div Yield ROE

Bloomberg Cap 30 Dec Price Upside (x) (x) (%) (x)

Code (US$m) (Bt) (Bt) 16F 17F 16F 17F 16F 17F 16F Rcmd

ANAN TB 463 4.94 5.60 13% 11.3 7.5 1.7 1.4 2.6 4.0 17.6 BUY

AOT TB 15,998 398.00 455.00 14% 29.1 25.2 4.7 4.1 1.1 1.2 17.0 BUY

CK TB 1,478 31.00 40.00 29% 24.0 26.7 2.3 2.2 1.2 1.1 10.2 BUY

CPALL TB 15,798 62.50 75.00 20% 34.6 28.0 13.0 11.4 2.0 2.5 40.2 Buy

GL TB 2,457 57.25 88.00 54% 79.6 42.5 10.8 6.5 0.5 0.6 14.0 BUY

IVL TB 4,538 33.50 42.00 25% 10.0 16.1 1.8 1.7 3.5 2.2 18.9 BUY

MTLS TB 1,473 24.70 32.00 30% 37.6 25.0 7.9 6.4 1.0 1.2 22.7 BUY

SCC TB 16,747 496.00 580.00 17% 11.2 11.6 2.5 2.2 3.6 3.5 23.9 BUY

TISCO TB 1,357 60.25 65.00 8% 9.6 8.2 1.5 1.4 4.0 4.1 17.0 BUY

TKN TB 1,087 28.00 32.00 14% 51.5 33.9 18.0 14.9 1.2 1.8 37.6 BUY

Source: Company, DBS Vickers

Market Focus

Page 4

Stock Picks

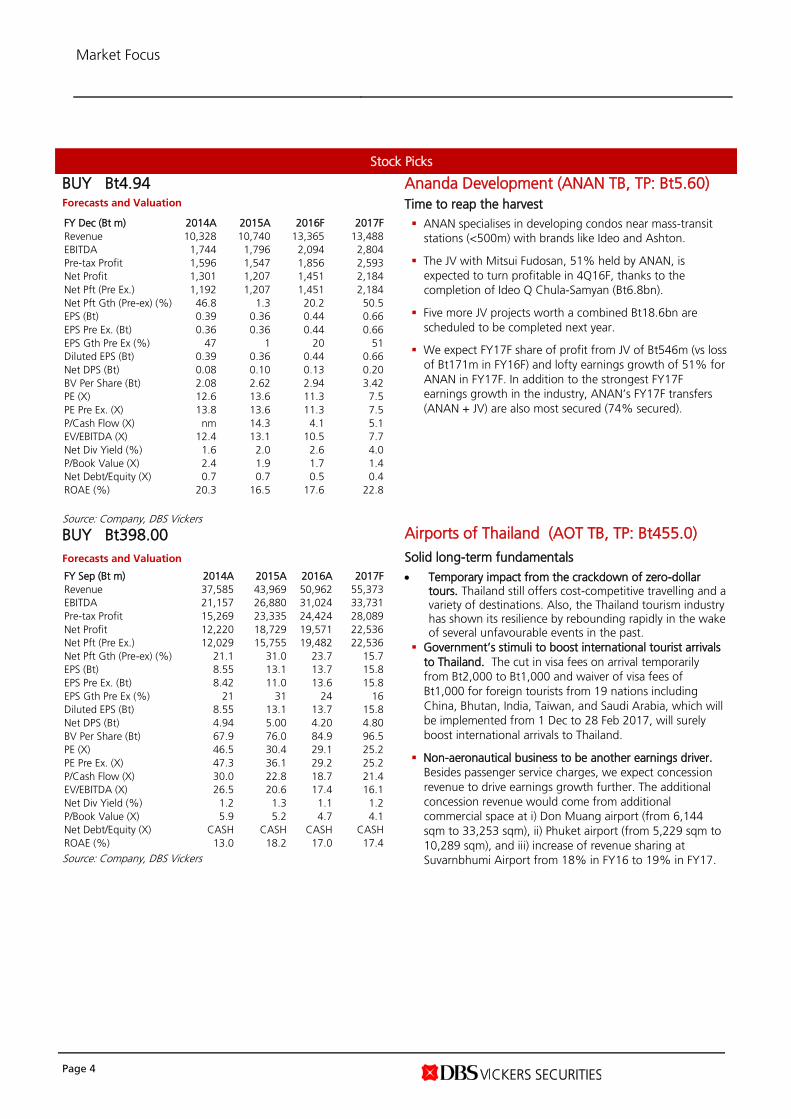

BUY Bt4.94 Forecasts and Valuation

Ananda Development (ANAN TB, TP: Bt5.60)

Time to reap the harvest

FY Dec (Bt m) 2014A 2015A 2016F 2017F

Revenue 10,328 10,740 13,365 13,488

EBITDA 1,744 1,796 2,094 2,804

Pre-tax Profit 1,596 1,547 1,856 2,593

Net Profit 1,301 1,207 1,451 2,184

Net Pft (Pre Ex.) 1,192 1,207 1,451 2,184

Net Pft Gth (Pre-ex) (%) 46.8 1.3 20.2 50.5

EPS (Bt) 0.39 0.36 0.44 0.66

EPS Pre Ex. (Bt) 0.36 0.36 0.44 0.66

EPS Gth Pre Ex (%) 47 1 20 51

Diluted EPS (Bt) 0.39 0.36 0.44 0.66

Net DPS (Bt) 0.08 0.10 0.13 0.20

BV Per Share (Bt) 2.08 2.62 2.94 3.42

PE (X) 12.6 13.6 11.3 7.5

PE Pre Ex. (X) 13.8 13.6 11.3 7.5

P/Cash Flow (X) nm 14.3 4.1 5.1

EV/EBITDA (X) 12.4 13.1 10.5 7.7

Net Div Yield (%) 1.6 2.0 2.6 4.0

P/Book Value (X) 2.4 1.9 1.7 1.4

Net Debt/Equity (X) 0.7 0.7 0.5 0.4

ROAE (%) 20.3 16.5 17.6 22.8

Source: Company, DBS Vickers

ANAN specialises in developing condos near mass-transit

stations (<500m) with brands like Ideo and Ashton.

The JV with Mitsui Fudosan, 51% held by ANAN, is

expected to turn profitable in 4Q16F, thanks to the

completion of Ideo Q Chula-Samyan (Bt6.8bn).

Five more JV projects worth a combined Bt18.6bn are

scheduled to be completed next year.

We expect FY17F share of profit from JV of Bt546m (vs loss

of Bt171m in FY16F) and lofty earnings growth of 51% for

ANAN in FY17F. In addition to the strongest FY17F

earnings growth in the industry, ANAN’s FY17F transfers

(ANAN + JV) are also most secured (74% secured).

BUY Bt398.00

Forecasts and Valuation

Airports of Thailand (AOT TB, TP: Bt455.0)

Solid long-term fundamentals

FY Sep (Bt m) 2014A 2015A 2016A 2017F

Revenue 37,585 43,969 50,962 55,373

EBITDA 21,157 26,880 31,024 33,731

Pre-tax Profit 15,269 23,335 24,424 28,089

Net Profit 12,220 18,729 19,571 22,536

Net Pft (Pre Ex.) 12,029 15,755 19,482 22,536

Net Pft Gth (Pre-ex) (%) 21.1 31.0 23.7 15.7

EPS (Bt) 8.55 13.1 13.7 15.8

EPS Pre Ex. (Bt) 8.42 11.0 13.6 15.8

EPS Gth Pre Ex (%) 21 31 24 16

Diluted EPS (Bt) 8.55 13.1 13.7 15.8

Net DPS (Bt) 4.94 5.00 4.20 4.80

BV Per Share (Bt) 67.9 76.0 84.9 96.5

PE (X) 46.5 30.4 29.1 25.2

PE Pre Ex. (X) 47.3 36.1 29.2 25.2

P/Cash Flow (X) 30.0 22.8 18.7 21.4

EV/EBITDA (X) 26.5 20.6 17.4 16.1

Net Div Yield (%) 1.2 1.3 1.1 1.2

P/Book Value (X) 5.9 5.2 4.7 4.1

Net Debt/Equity (X) CASH CASH CASH CASH

ROAE (%) 13.0 18.2 17.0 17.4

Source: Company, DBS Vickers

Temporary impact from the crackdown of zero-dollar tours. Thailand still offers cost-competitive travelling and a variety of destinations. Also, the Thailand tourism industry has shown its resilience by rebounding rapidly in the wake of several unfavourable events in the past.

Government’s stimuli to boost international tourist arrivals

to Thailand. The cut in visa fees on arrival temporarily

from Bt2,000 to Bt1,000 and waiver of visa fees of

Bt1,000 for foreign tourists from 19 nations including

China, Bhutan, India, Taiwan, and Saudi Arabia, which will

be implemented from 1 Dec to 28 Feb 2017, will surely

boost international arrivals to Thailand.

Non-aeronautical business to be another earnings driver.

Besides passenger service charges, we expect concession

revenue to drive earnings growth further. The additional

concession revenue would come from additional

commercial space at i) Don Muang airport (from 6,144

sqm to 33,253 sqm), ii) Phuket airport (from 5,229 sqm to

10,289 sqm), and iii) increase of revenue sharing at

Suvarnbhumi Airport from 18% in FY16 to 19% in FY17.

Market Focus

Page 5

BUY Bt31.00 Forecasts and Valuation

Ch. Karnchang (CK TB, TP: 40.0)

King of infrastructure plays

FY Dec (Bt m) 2014A 2015A 2016F 2017F

Revenue 32,951 34,912 47,389 44,833

EBITDA 3,776 3,178 4,981 5,978

Pre-tax Profit 2,700 2,719 2,559 2,154

Net Profit 2,296 2,193 2,184 1,968

Net Pft (Pre Ex.) 992 182 2,184 1,968

Net Pft Gth (Pre-ex) (%) nm (81.7) 1,102.2 (9.9)

EPS (Bt) 1.36 1.29 1.29 1.16

EPS Pre Ex. (Bt) 0.59 0.11 1.29 1.16

EPS Gth Pre Ex (%) nm (82) 1,102 (10)

Diluted EPS (Bt) 1.39 1.33 1.32 1.19

Net DPS (Bt) 0.35 0.40 0.39 0.35

BV Per Share (Bt) 11.3 12.1 13.2 14.0

PE (X) 22.9 23.9 24.0 26.7

PE Pre Ex. (X) 52.9 289.1 24.0 26.7

P/Cash Flow (X) 48.4 nm nm 377.5

EV/EBITDA (X) 23.7 32.0 23.5 20.1

Net Div Yield (%) 1.1 1.3 1.2 1.1

P/Book Value (X) 2.7 2.6 2.3 2.2

Net Debt/Equity (X) 1.9 2.3 2.8 2.8

ROAE (%) 12.9 11.1 10.2 8.5

Source: Company, DBS Vickers

We see abundant opportunities for CK, thanks to the

rollout of infrastructure projects – especially the MRT

works which CK has a strong competitive edge. We expect

the infrastructure spending in FY17 to reach Bt500bn

CK has gained 32% market share of the bidding result of

the Bt77bn MRT orange line, which is the highest market

share among other major contractors

Additionally, we expect CK to secure the M&E system and

O&M service* contracts for the blue line extension project,

worth Bt25bn, from Bangkok Expressway and Metro PCL

(BEM TB), this year

* Operations Service and Maintenance (O&M); Mechanical and

Electrical (M&E)

Reiterate BUY; currently CK is the top pick in the

contractor sector. Our target price of Bt40.0 is based on

SOP valuation, comprising Bt15 for the construction

business and Bt25 for its investment.

BUY Bt62.50 Forecasts and Valuation

CPALL (CPALL TB, TP: Bt75.00)

Persistent strength

FY Dec (Bt m) 2014A 2015A 2016F 2017F

Revenue 357,766 391,817 436,663 492,038

EBITDA 26,802 32,554 35,880 41,077

Pre-tax Profit 12,589 16,884 19,963 25,017

Net Profit 10,200 13,682 16,219 20,094

Net Pft (Pre Ex.) 9,823 13,687 16,219 20,094

Net Pft Gth (Pre-ex) (%) (10.7) 39.3 18.5 23.9

EPS (Bt) 1.13 1.52 1.80 2.24

EPS Pre Ex. (Bt) 1.09 1.52 1.80 2.24

EPS Gth Pre Ex (%) (11) 39 19 24

Diluted EPS (Bt) 1.13 1.52 1.80 2.24

Net DPS (Bt) 0.82 1.07 1.26 1.57

BV Per Share (Bt) 3.43 4.16 4.82 5.49

PE (X) 55.3 41.0 34.6 28.0

PE Pre Ex. (X) 57.2 41.0 34.6 28.0

P/Cash Flow (X) 21.3 17.9 18.3 16.5

EV/EBITDA (X) 27.3 22.5 20.3 17.7

Net Div Yield (%) 1.3 1.7 2.0 2.5

P/Book Value (X) 18.2 15.0 13.0 11.4

Net Debt/Equity (X) 4.7 4.0 3.4 3.0

ROAE (%) 34.3 40.2 40.2 43.4

Source: Company, DBS Vickers

Driven by aggressive expansion plan. CPALL continues to

aggressively expand the number of outlets. It plans to roll

out at least 700 stores p.a. and has a target to reach

12,000 stores in the next three years.

Expanding margins. CPALL’s gross margin should be

healthy, thanks to economies of scale from a larger

network and increasing contribution from higher-margin

products such as ready-to-eat meals and health and beauty

items.

Healthier balance sheet. CPALL issued perpetual

debentures worth c.Bt10bn in Nov to refinance its existing

debts. The perpetual debenture would be classified as

equity and will lower its debt to equity (we expect the end-

2016 ratio to fall from 4.5x in 3Q16 to 3.5x). Interest

expenses on the perpetual debenture will not be booked in

P&L statements, but instead flow from retained earnings in

the balance sheet. However, this should have only a

minimal impact on its ability to pay dividends.

Market Focus

Page 6

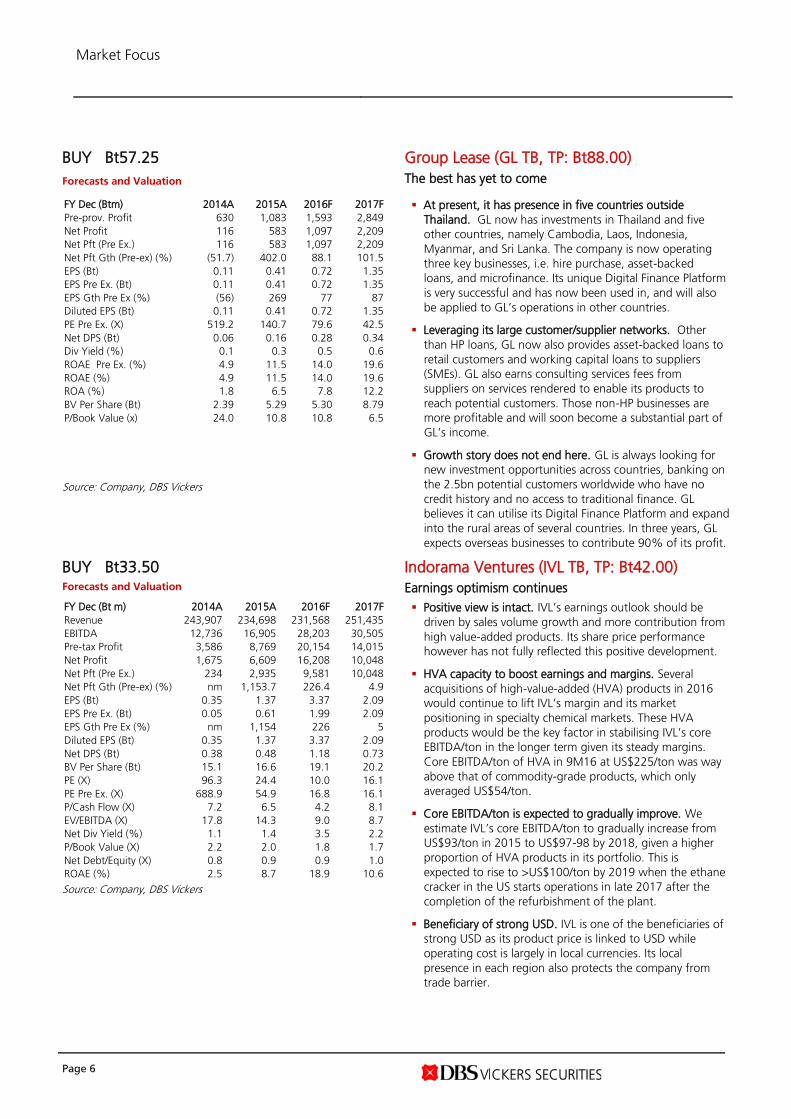

BUY Bt57.25

Forecasts and Valuation

Group Lease (GL TB, TP: Bt88.00)

The best has yet to come

FY Dec (Btm) 2014A 2015A 2016F 2017F

Pre-prov. Profit 630 1,083 1,593 2,849

Net Profit 116 583 1,097 2,209

Net Pft (Pre Ex.) 116 583 1,097 2,209

Net Pft Gth (Pre-ex) (%) (51.7) 402.0 88.1 101.5

EPS (Bt) 0.11 0.41 0.72 1.35

EPS Pre Ex. (Bt) 0.11 0.41 0.72 1.35

EPS Gth Pre Ex (%) (56) 269 77 87

Diluted EPS (Bt) 0.11 0.41 0.72 1.35

PE Pre Ex. (X) 519.2 140.7 79.6 42.5

Net DPS (Bt) 0.06 0.16 0.28 0.34

Div Yield (%) 0.1 0.3 0.5 0.6

ROAE Pre Ex. (%) 4.9 11.5 14.0 19.6

ROAE (%) 4.9 11.5 14.0 19.6

ROA (%) 1.8 6.5 7.8 12.2

BV Per Share (Bt) 2.39 5.29 5.30 8.79

P/Book Value (x) 24.0 10.8 10.8 6.5

Source: Company, DBS Vickers

At present, it has presence in five countries outside

Thailand. GL now has investments in Thailand and five

other countries, namely Cambodia, Laos, Indonesia,

Myanmar, and Sri Lanka. The company is now operating

three key businesses, i.e. hire purchase, asset-backed

loans, and microfinance. Its unique Digital Finance Platform

is very successful and has now been used in, and will also

be applied to GL’s operations in other countries.

Leveraging its large customer/supplier networks. Other

than HP loans, GL now also provides asset-backed loans to

retail customers and working capital loans to suppliers

(SMEs). GL also earns consulting services fees from

suppliers on services rendered to enable its products to

reach potential customers. Those non-HP businesses are

more profitable and will soon become a substantial part of

GL’s income.

Growth story does not end here. GL is always looking for

new investment opportunities across countries, banking on

the 2.5bn potential customers worldwide who have no

credit history and no access to traditional finance. GL

believes it can utilise its Digital Finance Platform and expand

into the rural areas of several countries. In three years, GL

expects overseas businesses to contribute 90% of its profit.

BUY Bt33.50 Forecasts and Valuation

Indorama Ventures (IVL TB, TP: Bt42.00)

Earnings optimism continues

FY Dec (Bt m) 2014A 2015A 2016F 2017F

Revenue 243,907 234,698 231,568 251,435

EBITDA 12,736 16,905 28,203 30,505

Pre-tax Profit 3,586 8,769 20,154 14,015

Net Profit 1,675 6,609 16,208 10,048

Net Pft (Pre Ex.) 234 2,935 9,581 10,048

Net Pft Gth (Pre-ex) (%) nm 1,153.7 226.4 4.9

EPS (Bt) 0.35 1.37 3.37 2.09

EPS Pre Ex. (Bt) 0.05 0.61 1.99 2.09

EPS Gth Pre Ex (%) nm 1,154 226 5

Diluted EPS (Bt) 0.35 1.37 3.37 2.09

Net DPS (Bt) 0.38 0.48 1.18 0.73

BV Per Share (Bt) 15.1 16.6 19.1 20.2

PE (X) 96.3 24.4 10.0 16.1

PE Pre Ex. (X) 688.9 54.9 16.8 16.1

P/Cash Flow (X) 7.2 6.5 4.2 8.1

EV/EBITDA (X) 17.8 14.3 9.0 8.7

Net Div Yield (%) 1.1 1.4 3.5 2.2

P/Book Value (X) 2.2 2.0 1.8 1.7

Net Debt/Equity (X) 0.8 0.9 0.9 1.0

ROAE (%) 2.5 8.7 18.9 10.6

Source: Company, DBS Vickers

Positive view is intact. IVL’s earnings outlook should be

driven by sales volume growth and more contribution from

high value-added products. Its share price performance

however has not fully reflected this positive development.

HVA capacity to boost earnings and margins. Several

acquisitions of high-value-added (HVA) products in 2016

would continue to lift IVL’s margin and its market

positioning in specialty chemical markets. These HVA

products would be the key factor in stabilising IVL’s core

EBITDA/ton in the longer term given its steady margins.

Core EBITDA/ton of HVA in 9M16 at US$225/ton was way

above that of commodity-grade products, which only

averaged US$54/ton.

Core EBITDA/ton is expected to gradually improve. We

estimate IVL’s core EBITDA/ton to gradually increase from

US$93/ton in 2015 to US$97-98 by 2018, given a higher

proportion of HVA products in its portfolio. This is

expected to rise to >US$100/ton by 2019 when the ethane

cracker in the US starts operations in late 2017 after the

completion of the refurbishment of the plant.

Beneficiary of strong USD. IVL is one of the beneficiaries of

strong USD as its product price is linked to USD while

operating cost is largely in local currencies. Its local

presence in each region also protects the company from

trade barrier.

Market Focus

Page 7

BUY Bt24.70

Forecasts and Valuation

Muangthai Leasing (MTLS TB, TP: Bt32.00)

Stellar growth

FY Dec (Btm) 2014A 2015A 2016F 2017F

Pre-prov. Profit 694 1,056 2,065 3,140

Net Profit 544 825 1,392 2,098

Net Pft (Pre Ex.) 544 825 1,392 2,098

Net Pft Gth (Pre-ex) (%) 54.8 51.6 68.7 50.8

EPS (Bt) 0.32 0.39 0.66 0.99

EPS Pre Ex. (Bt) 0.32 0.39 0.66 0.99

EPS Gth Pre Ex (%) 39 21 69 51

Diluted EPS (Bt) 0.32 0.39 0.66 0.99

PE Pre Ex. (X) 76.8 63.5 37.6 25.0

Net DPS (Bt) 0.13 0.20 0.25 0.30

Div Yield (%) 0.5 0.8 1.0 1.2

ROAE Pre Ex. (%) 15.5 15.3 22.7 28.3

ROAE (%) 15.5 15.3 22.7 28.3

ROA (%) 7.4 7.5 7.3 6.8

BV Per Share (Bt) 3.02 2.67 3.12 3.86

P/Book Value (x) 8.2 9.3 7.9 6.4

Source: Company, DBS Vickers

Aggressive branch expansion. MTLS targets to have 1,600

branches by end-2016 and 2,200 by end-2017. In 3Q16,

279 branches were added, making the total number at

1,515.

Robust balance sheet. Its strong balance sheet is the key

factor to support the company’s aggressive business

expansion (NPL=0.95%; coverage ratio >280%; and D/E

ratio=2.4x at end-3Q16).

Strong growth in portfolio and earnings. We expect

MTLS's loan portfolio and EPS to expand 87%/46% and

69%/51% respectively in FY16/17F

BUY, with Bt32.00 TP. Our TP is based on GGM (21%

ROE, 10% growth, and 11% cost of equity).

BUY Bt496.00 Forecasts and Valuation

Siam Cement (SCC TB, TP: Bt580.00)

Lift from regional presence

FY Dec (Bt m) 2014A 2015A 2016F 2017F

Revenue 487,545 439,614 424,972 448,236

EBITDA 67,256 89,639 95,657 99,105

Pre-tax Profit 41,928 59,793 67,112 66,367

Net Profit 33,615 45,400 53,212 51,264

Net Pft (Pre Ex.) 33,615 45,400 53,212 51,264

Net Pft Gth (Pre-ex) (%) (8.0) 35.1 17.2 (3.7)

EPS (Bt) 28.0 37.8 44.3 42.7

EPS Pre Ex. (Bt) 28.0 37.8 44.3 42.7

EPS Gth Pre Ex (%) (8) 35 17 (4)

Diluted EPS (Bt) 28.0 37.8 44.3 42.7

Net DPS (Bt) 12.5 16.0 17.8 17.2

BV Per Share (Bt) 148 172 199 225

PE (X) 17.7 13.1 11.2 11.6

PE Pre Ex. (X) 17.7 13.1 11.2 11.6

P/Cash Flow (X) 12.5 8.8 7.7 8.2

EV/EBITDA (X) 11.8 8.9 8.3 8.0

Net Div Yield (%) 2.5 3.2 3.6 3.5

P/Book Value (X) 3.4 2.9 2.5 2.2

Net Debt/Equity (X) 0.8 0.7 0.5 0.5

ROAE (%) 19.8 23.7 23.9 20.1

Source: Company, DBS Vickers

Chemical segment still the key earnings driver. The

chemical segment including its associate in Indonesia could

still be the key driver for earnings, the cement and building

materials segment is expected to provide upside potential

to profit in 2017-18F given more cement demand for

infrastructure projects in Thailand and ASEAN.

Focusing on adding high value-added products. SCC has

continued to emphasise its strategic move to increase the

proportion of HVA products in its portfolio since 2004 in

order to reduce volatility from commodity-grade products,

and improve margins. Revenue from HVA products already

accounted for 38% of total revenue.

Strong presence in CLMV market. SCC has been proactive

in expanding its business into Cambodia, Laos, Myanmar

and Vietnam (CLMV) with revenue contribution from this

market accounting for 12.8% of total sales revenue in

9M16. This was mainly from cement business; capacity in

this market accounts for 20% of total cement capacity. Its

first cement plant in the CLMV market started operations

in 2007 in Cambodia. A new plant in Laos will commence

operations in 1H17.

Market Focus

Page 8

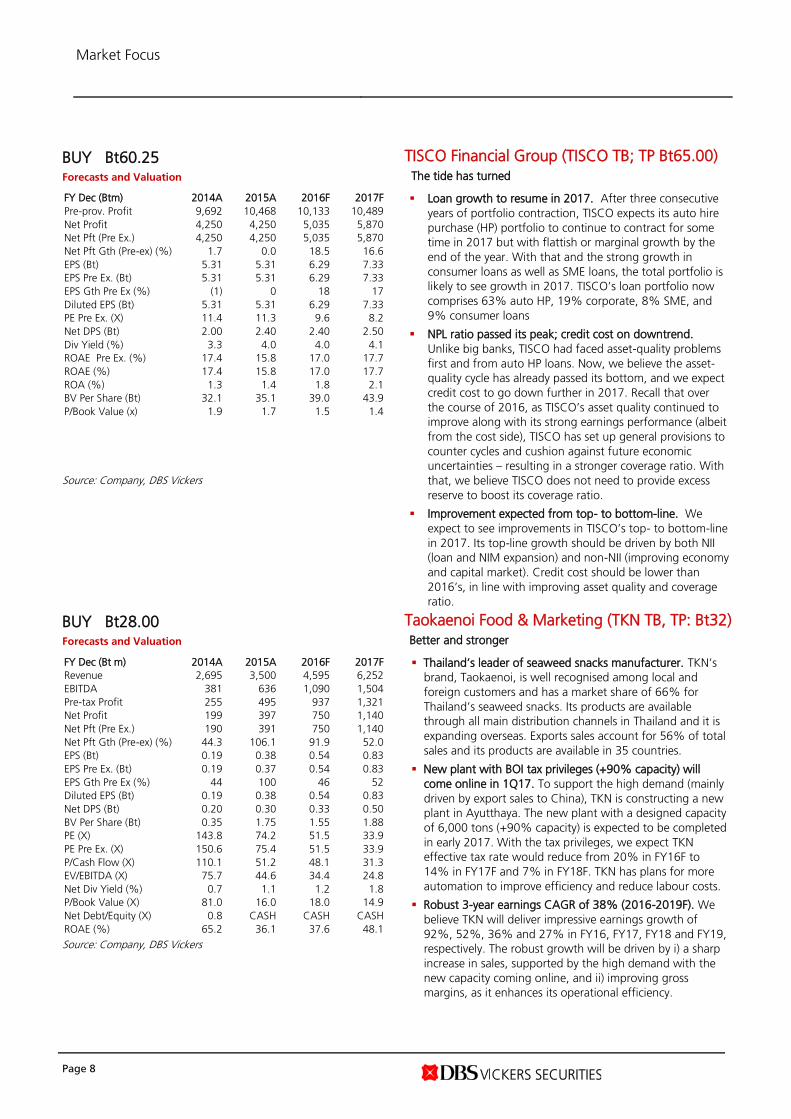

BUY Bt60.25 Forecasts and Valuation

TISCO Financial Group (TISCO TB; TP Bt65.00) The tide has turned

FY Dec (Btm) 2014A 2015A 2016F 2017F

Pre-prov. Profit 9,692 10,468 10,133 10,489

Net Profit 4,250 4,250 5,035 5,870

Net Pft (Pre Ex.) 4,250 4,250 5,035 5,870

Net Pft Gth (Pre-ex) (%) 1.7 0.0 18.5 16.6

EPS (Bt) 5.31 5.31 6.29 7.33

EPS Pre Ex. (Bt) 5.31 5.31 6.29 7.33

EPS Gth Pre Ex (%) (1) 0 18 17

Diluted EPS (Bt) 5.31 5.31 6.29 7.33

PE Pre Ex. (X) 11.4 11.3 9.6 8.2

Net DPS (Bt) 2.00 2.40 2.40 2.50

Div Yield (%) 3.3 4.0 4.0 4.1

ROAE Pre Ex. (%) 17.4 15.8 17.0 17.7

ROAE (%) 17.4 15.8 17.0 17.7

ROA (%) 1.3 1.4 1.8 2.1

BV Per Share (Bt) 32.1 35.1 39.0 43.9

P/Book Value (x) 1.9 1.7 1.5 1.4

Source: Company, DBS Vickers

Loan growth to resume in 2017. After three consecutive

years of portfolio contraction, TISCO expects its auto hire

purchase (HP) portfolio to continue to contract for some

time in 2017 but with flattish or marginal growth by the

end of the year. With that and the strong growth in

consumer loans as well as SME loans, the total portfolio is

likely to see growth in 2017. TISCO’s loan portfolio now

comprises 63% auto HP, 19% corporate, 8% SME, and

9% consumer loans

NPL ratio passed its peak; credit cost on downtrend.

Unlike big banks, TISCO had faced asset-quality problems

first and from auto HP loans. Now, we believe the asset-

quality cycle has already passed its bottom, and we expect

credit cost to go down further in 2017. Recall that over

the course of 2016, as TISCO’s asset quality continued to

improve along with its strong earnings performance (albeit

from the cost side), TISCO has set up general provisions to

counter cycles and cushion against future economic

uncertainties – resulting in a stronger coverage ratio. With

that, we believe TISCO does not need to provide excess

reserve to boost its coverage ratio.

Improvement expected from top- to bottom-line. We

expect to see improvements in TISCO’s top- to bottom-line

in 2017. Its top-line growth should be driven by both NII

(loan and NIM expansion) and non-NII (improving economy

and capital market). Credit cost should be lower than

2016’s, in line with improving asset quality and coverage

ratio.

BUY Bt28.00 Forecasts and Valuation

Taokaenoi Food & Marketing (TKN TB, TP: Bt32) Better and stronger

FY Dec (Bt m) 2014A 2015A 2016F 2017F

Revenue 2,695 3,500 4,595 6,252

EBITDA 381 636 1,090 1,504

Pre-tax Profit 255 495 937 1,321

Net Profit 199 397 750 1,140

Net Pft (Pre Ex.) 190 391 750 1,140

Net Pft Gth (Pre-ex) (%) 44.3 106.1 91.9 52.0

EPS (Bt) 0.19 0.38 0.54 0.83

EPS Pre Ex. (Bt) 0.19 0.37 0.54 0.83

EPS Gth Pre Ex (%) 44 100 46 52

Diluted EPS (Bt) 0.19 0.38 0.54 0.83

Net DPS (Bt) 0.20 0.30 0.33 0.50

BV Per Share (Bt) 0.35 1.75 1.55 1.88

PE (X) 143.8 74.2 51.5 33.9

PE Pre Ex. (X) 150.6 75.4 51.5 33.9

P/Cash Flow (X) 110.1 51.2 48.1 31.3

EV/EBITDA (X) 75.7 44.6 34.4 24.8

Net Div Yield (%) 0.7 1.1 1.2 1.8

P/Book Value (X) 81.0 16.0 18.0 14.9

Net Debt/Equity (X) 0.8 CASH CASH CASH

ROAE (%) 65.2 36.1 37.6 48.1

Source: Company, DBS Vickers

Thailand’s leader of seaweed snacks manufacturer. TKN’s

brand, Taokaenoi, is well recognised among local and

foreign customers and has a market share of 66% for

Thailand’s seaweed snacks. Its products are available

through all main distribution channels in Thailand and it is

expanding overseas. Exports sales account for 56% of total

sales and its products are available in 35 countries.

New plant with BOI tax privileges (+90% capacity) will

come online in 1Q17. To support the high demand (mainly

driven by export sales to China), TKN is constructing a new

plant in Ayutthaya. The new plant with a designed capacity

of 6,000 tons (+90% capacity) is expected to be completed

in early 2017. With the tax privileges, we expect TKN

effective tax rate would reduce from 20% in FY16F to

14% in FY17F and 7% in FY18F. TKN has plans for more

automation to improve efficiency and reduce labour costs.

Robust 3-year earnings CAGR of 38% (2016-2019F). We

believe TKN will deliver impressive earnings growth of

92%, 52%, 36% and 27% in FY16, FY17, FY18 and FY19,

respectively. The robust growth will be driven by i) a sharp

increase in sales, supported by the high demand with the

new capacity coming online, and ii) improving gross

margins, as it enhances its operational efficiency.

Market Focus

Page 9

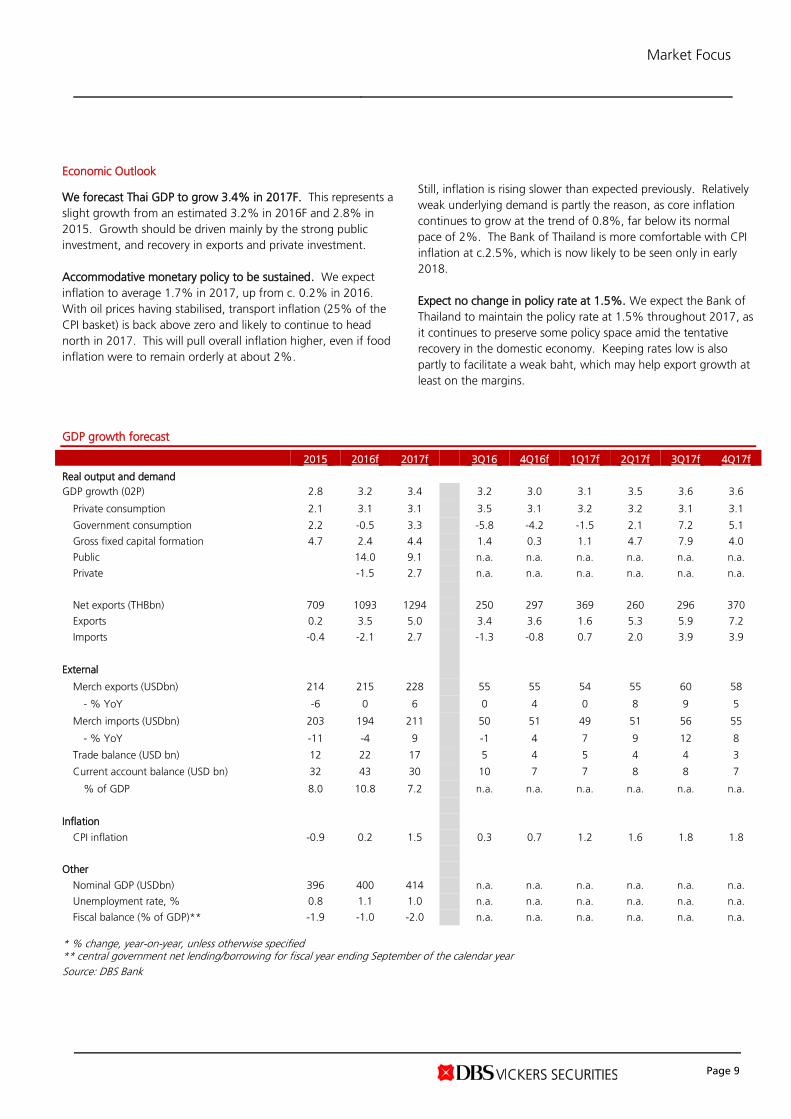

Economic Outlook

We forecast Thai GDP to grow 3.4% in 2017F. This represents a

slight growth from an estimated 3.2% in 2016F and 2.8% in

2015. Growth should be driven mainly by the strong public

investment, and recovery in exports and private investment.

Accommodative monetary policy to be sustained. We expect

inflation to average 1.7% in 2017, up from c. 0.2% in 2016.

With oil prices having stabilised, transport inflation (25% of the

CPI basket) is back above zero and likely to continue to head

north in 2017. This will pull overall inflation higher, even if food

inflation were to remain orderly at about 2%.

Still, inflation is rising slower than expected previously. Relatively

weak underlying demand is partly the reason, as core inflation

continues to grow at the trend of 0.8%, far below its normal

pace of 2%. The Bank of Thailand is more comfortable with CPI

inflation at c.2.5%, which is now likely to be seen only in early

2018.

Expect no change in policy rate at 1.5%. We expect the Bank of

Thailand to maintain the policy rate at 1.5% throughout 2017, as

it continues to preserve some policy space amid the tentative

recovery in the domestic economy. Keeping rates low is also

partly to facilitate a weak baht, which may help export growth at

least on the margins.

GDP growth forecast

2015 2016f 2017f

3Q16 4Q16f 1Q17f 2Q17f 3Q17f 4Q17f

Real output and demand

GDP growth (02P) 2.8 3.2 3.4

3.2 3.0 3.1 3.5 3.6 3.6

Private consumption 2.1 3.1 3.1

3.5 3.1 3.2 3.2 3.1 3.1

Government consumption 2.2 -0.5 3.3

-5.8 -4.2 -1.5 2.1 7.2 5.1

Gross fixed capital formation 4.7 2.4 4.4

1.4 0.3 1.1 4.7 7.9 4.0

Public

14.0 9.1

n.a. n.a. n.a. n.a. n.a. n.a.

Private

-1.5 2.7

n.a. n.a. n.a. n.a. n.a. n.a.

Net exports (THBbn) 709 1093 1294

250 297 369 260 296 370

Exports 0.2 3.5 5.0

3.4 3.6 1.6 5.3 5.9 7.2

Imports -0.4 -2.1 2.7

-1.3 -0.8 0.7 2.0 3.9 3.9

External

Merch exports (USDbn) 214 215 228

55 55 54 55 60 58

- % YoY -6 0 6

0 4 0 8 9 5

Merch imports (USDbn) 203 194 211

50 51 49 51 56 55

- % YoY -11 -4 9

-1 4 7 9 12 8

Trade balance (USD bn) 12 22 17

5 4 5 4 4 3

Current account balance (USD bn) 32 43 30

10 7 7 8 8 7

% of GDP 8.0 10.8 7.2

n.a. n.a. n.a. n.a. n.a. n.a.

Inflation

CPI inflation -0.9 0.2 1.5

0.3 0.7 1.2 1.6 1.8 1.8

Other

Nominal GDP (USDbn) 396 400 414

n.a. n.a. n.a. n.a. n.a. n.a.

Unemployment rate, % 0.8 1.1 1.0

n.a. n.a. n.a. n.a. n.a. n.a.

Fiscal balance (% of GDP)** -1.9 -1.0 -2.0

n.a. n.a. n.a. n.a. n.a. n.a.

* % change, year-on-year, unless otherwise specified ** central government net lending/borrowing for fiscal year ending September of the calendar year

Source: DBS Bank

Market Focus

Page 10

Earnings Outlook

2016F universe net profit growth estimated at 36%. The strong

earnings growth would be boosted largely by the Energy sector,

mainly from PTTEP and PTT.

Earnings should continue to grow, albeit at a much slower pace

of 7% in 2017. Our current forecast is a bit conservative

compared with consensus earnings growth of 15% for 2017.

We believe the key difference was mainly in the banking and

energy sector, due to different in provisioning and oil price

assumptions.

Earnings growth by sector*

YE Dec (Btm) FY15A FY16F FY17F FY16F

Gwt

FY17F

Gwt

Banking 168,413 172,810 185,241 3% 7% Finance 4,003 5,115 7,036 28% 38% Con. Mat. 50,478 56,102 54,395 11% -3% Chemicals 27,112 38,579 36,653 42% -5% Contractors 6,049 4,604 5,556 -24% 21% Property 42,709 42,140 45,536 -1% 8% - Commercial 7,880 9,201 10,092 17% 10% - Residential 32,976 32,421 34,532 -2% 7% - Industrial 1,853 518 912 -72% 76% Property Fund 21,374 25,351 27,338 19% 8% Energy 18,959 150,708 161,145 695% 7% Media 164 281 436 72% 55% Commerce 24,795 29,308 35,232 18% 20% Transport 11,186 33,157 38,320 196% 16% Tourism 1,874 2,283 2,710 22% 19% Telecom 46,521 34,530 32,651 -26% -5% Electronics 13,019 11,909 13,033 -9% 9% Food 23,798 26,519 28,606 11% 8% Health Care Services

12,120 12,875 14,708 6% 14%

Total 475,892 646,271 688,595 36% 7%

Source: Companies and DBS Vickers * Companies under DBSV coverage

Valuation

Thai market is now trading at 2017F PE of 14.5x. This is slightly

higher than the 10-year average PE of 14.3x. Compared to

regional markets, the Thai market’s PE is higher than the regional

average PE of 14.0x.

Our SET Index target is at 1650. This is based on our conservative

2017 EPS growth of 7% and a PE of 15.5x based on 0.5SD of

historical average.

Regional comparison: PE vs. EPS growth

EPS Gth (%) PE (x)

16F 17F 16F 17F

Singapore (4.7) 12.1 16.1 14.4

HK HSI (5.2) 11.8 11.9 10.7

HK HSCCI (Red) (6.8) 25.7 12.4 9.9

HK HSCEI (H) (5.6) 9.2 7.6 6.9

CSI300 (1.3) 13.5 14.2 12.5

SH Comp 7.0 13.6 14.8 13.0

SZ Comp (5.2) 11.8 11.9 10.7

Malaysia 0.2 9.2 17.2 15.8

Thailand 35.8 7.1 15.5 14.5

Indonesia 18.4 17.5 15.6 13.3

Simple Average 3.3 13.2 13.7 12.7

Source: DBS Bank, DBS Vickers

Valuation by sector*

PE (x)

YE Dec FY15A FY16F FY17F

Banking 10.0 10.1 9.4 Finance 40.0 32.4 24.5 Con. Mat. 12.4 11.1 11.5 Chemicals 16.4 11.5 12.2 Contractors 20.4 26.8 22.2 Property 13.9 14.1 13.1 - Commercial 32.3 27.7 25.2 - Residential 9.6 9.9 9.3 - Industrial 11.4 41.3 23.5 Property Fund 16.1 14.5 13.5 Energy 112.8 13.8 12.6 Media 111.6 66.1 43.1 Commerce 36.1 30.7 25.5 Transport 72.3 24.4 21.1 Tourism 34.6 28.4 24.0 Telecom 12.4 16.7 17.7 Electronics 16.6 18.2 16.6 Food 21.2 19.4 18.0 Health Care Services 44.1 41.1 36.0 Total 20.9 15.5 14.5 Source: SET, DBS Vickers * Companies under DBSV coverage

SET: PE band

Source: SET, DBS Vickers

5

7

9

11

13

15

17

19

21

0

200

400

600

800

1,000

1,200

1,400

1,600

2016F

SET Index (LHS)P/E (x)Median (14.3x)Median+0.5SD (15.7x)Median-0.5SD (13x)

SET P/E Ratio

Market Focus

Page 11

Market Overview and Outlook

2016 Recap

The best performer in the region in 2016. The SET Index surged

19.8% in 2016, making it the best-performing market in the

region. It outperformed regional peers which rose 3.5% during

the same period. The rally was due mainly to the return of

foreign fund flows to the Thai market.

Foreign investors were net buyers of Bt77.9bn of the Thai market

in 2016. Local retail investors were net sellers with the net sell

position amounting to Bt94.6bn. Local institutional investors

were also net sellers, with a net sell position of Bt8.7bn. In terms

of proprietary trading, brokers were net buyers of Bt25.4bn.

The market was led by Paper (+84.5%), Mining (+62.1%),

Professional Services (+51.0%), and Commerce (+41.0%). The

key underperformers in 2016 were Media (-7.9%), and Insurance

(-4.0%).

Mid- and Small-cap stocks led the rally. In 2016, the FTSE

Mid/Small Cap index surged 63%, while the FTSE Large cap

index grew 17%.

SET Index performance vs peers

Dec 2016 2016

Dax 7.9% 6.9%

FTSE 5.3% 14.4%

Nikkei 4.4% 0.4%

Dow Jones 3.3% 13.4%

S&P 500 1.8% 9.5%

NASDAQ 1.1% 7.5%

Indo 2.9% 15.3%

Korea 2.2% 3.3%

SET 2.2% 19.8%

Malay 1.4% -3.0%

Phil 0.9% -1.6%

Taiwan 0.1% 11.0%

India -0.1% 1.8%

Sing -0.8% -0.1%

MXFEJ -2.5% 3.5%

HK -3.5% 0.4%

Shanghai -4.5% -12.3%

H-shares -4.5% -2.8%

Source: Bloomberg Finance L.P., DBS Vickers

Sector performance

Sector Dec 2016 2016

AGRI 18% 58%

STEEL 16% 47%

ETRON 7% 19%

PKG 7% 44%

MINE 7% 62%

PERSON 7% 39%

AUTO 5% 6%

ENERG 5% 38%

PAPER 4% 85%

BANK 4% 18%

CONMAT 3% 1%

MEDIA 3% -8%

HOME 3% 8%

INSUR 3% -4%

IMM 2% 6%

SET 2% 20%

ICT 2% 5%

PROP 2% 5%

PETRO 2% 36%

FOOD 1% 35%

CONS 1% 0%

COMM 1% 41%

FASHION -1% -1%

HELTH -1% 9%

FIN -1% 34%

TOURISM -2% -4%

PROF -2% 51%

PF&REIT -2% 10%

TRANS -2% 15%

Source: Bloomberg Finance L.P., DBS Vickers

Market Focus

Page 12

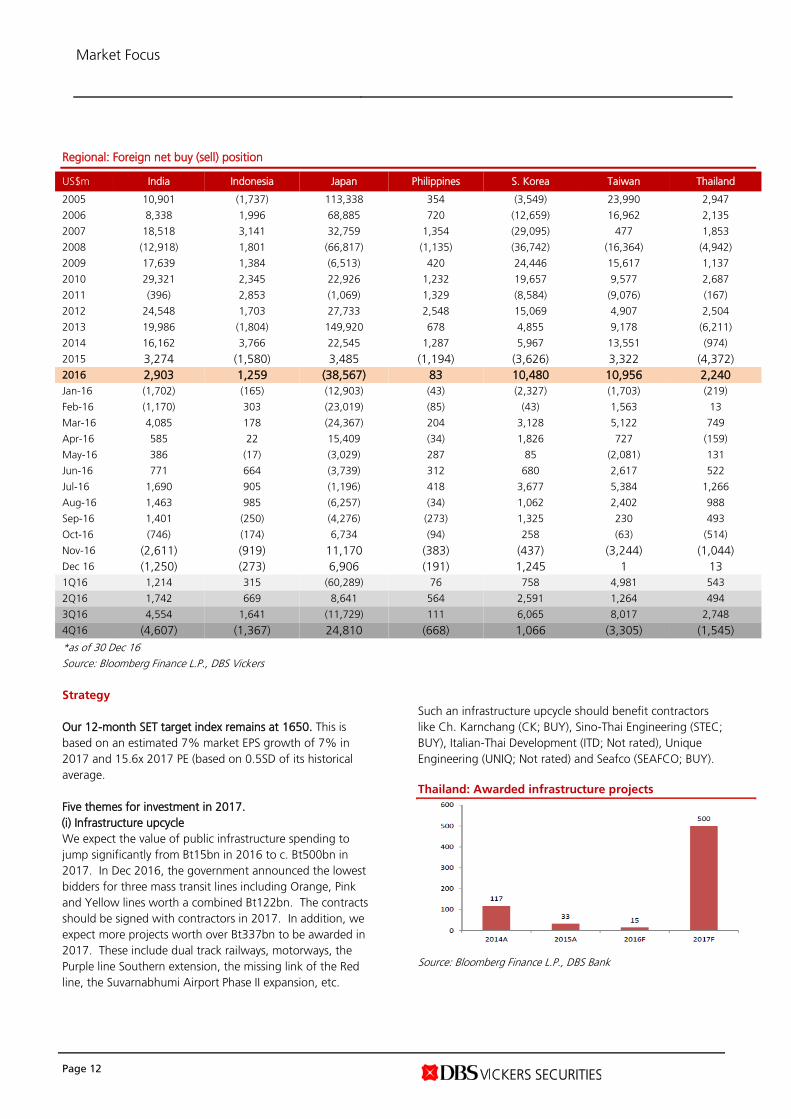

Regional: Foreign net buy (sell) position

US$m India Indonesia Japan Philippines S. Korea Taiwan Thailand

2005 10,901 (1,737) 113,338 354 (3,549) 23,990 2,947

2006 8,338 1,996 68,885 720 (12,659) 16,962 2,135

2007 18,518 3,141 32,759 1,354 (29,095) 477 1,853

2008 (12,918) 1,801 (66,817) (1,135) (36,742) (16,364) (4,942)

2009 17,639 1,384 (6,513) 420 24,446 15,617 1,137

2010 29,321 2,345 22,926 1,232 19,657 9,577 2,687

2011 (396) 2,853 (1,069) 1,329 (8,584) (9,076) (167)

2012 24,548 1,703 27,733 2,548 15,069 4,907 2,504

2013 19,986 (1,804) 149,920 678 4,855 9,178 (6,211)

2014 16,162 3,766 22,545 1,287 5,967 13,551 (974)

2015 3,274 (1,580) 3,485 (1,194) (3,626) 3,322 (4,372)

2016 2,903 1,259 (38,567) 83 10,480 10,956 2,240

Jan-16 (1,702) (165) (12,903) (43) (2,327) (1,703) (219)

Feb-16 (1,170) 303 (23,019) (85) (43) 1,563 13

Mar-16 4,085 178 (24,367) 204 3,128 5,122 749

Apr-16 585 22 15,409 (34) 1,826 727 (159)

May-16 386 (17) (3,029) 287 85 (2,081) 131

Jun-16 771 664 (3,739) 312 680 2,617 522

Jul-16 1,690 905 (1,196) 418 3,677 5,384 1,266

Aug-16 1,463 985 (6,257) (34) 1,062 2,402 988

Sep-16 1,401 (250) (4,276) (273) 1,325 230 493

Oct-16 (746) (174) 6,734 (94) 258 (63) (514)

Nov-16 (2,611) (919) 11,170 (383) (437) (3,244) (1,044)

Dec 16 (1,250) (273) 6,906 (191) 1,245 1 13

1Q16 1,214 315 (60,289) 76 758 4,981 543

2Q16 1,742 669 8,641 564 2,591 1,264 494

3Q16 4,554 1,641 (11,729) 111 6,065 8,017 2,748

4Q16 (4,607) (1,367) 24,810 (668) 1,066 (3,305) (1,545)

*as of 30 Dec 16

Source: Bloomberg Finance L.P., DBS Vickers

Strategy

Our 12-month SET target index remains at 1650. This is

based on an estimated 7% market EPS growth of 7% in

2017 and 15.6x 2017 PE (based on 0.5SD of its historical

average.

Five themes for investment in 2017.

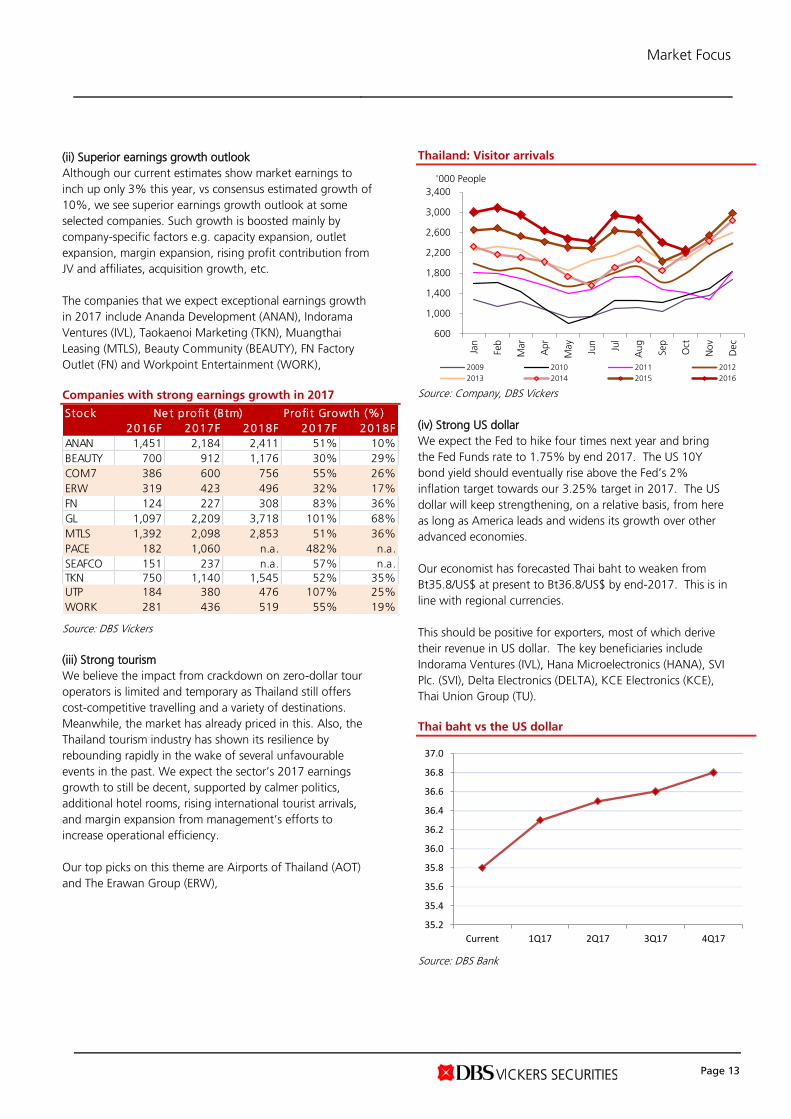

(i) Infrastructure upcycle

We expect the value of public infrastructure spending to

jump significantly from Bt15bn in 2016 to c. Bt500bn in

2017. In Dec 2016, the government announced the lowest

bidders for three mass transit lines including Orange, Pink

and Yellow lines worth a combined Bt122bn. The contracts

should be signed with contractors in 2017. In addition, we

expect more projects worth over Bt337bn to be awarded in

2017. These include dual track railways, motorways, the

Purple line Southern extension, the missing link of the Red

line, the Suvarnabhumi Airport Phase II expansion, etc.

Such an infrastructure upcycle should benefit contractors

like Ch. Karnchang (CK; BUY), Sino-Thai Engineering (STEC;

BUY), Italian-Thai Development (ITD; Not rated), Unique

Engineering (UNIQ; Not rated) and Seafco (SEAFCO; BUY).

Thailand: Awarded infrastructure projects

Source: Bloomberg Finance L.P., DBS Bank

Market Focus

Page 13

(ii) Superior earnings growth outlook

Although our current estimates show market earnings to

inch up only 3% this year, vs consensus estimated growth of

10%, we see superior earnings growth outlook at some

selected companies. Such growth is boosted mainly by

company-specific factors e.g. capacity expansion, outlet

expansion, margin expansion, rising profit contribution from

JV and affiliates, acquisition growth, etc.

The companies that we expect exceptional earnings growth

in 2017 include Ananda Development (ANAN), Indorama

Ventures (IVL), Taokaenoi Marketing (TKN), Muangthai

Leasing (MTLS), Beauty Community (BEAUTY), FN Factory

Outlet (FN) and Workpoint Entertainment (WORK),

Companies with strong earnings growth in 2017

Source: DBS Vickers

(iii) Strong tourism

We believe the impact from crackdown on zero-dollar tour

operators is limited and temporary as Thailand still offers

cost-competitive travelling and a variety of destinations.

Meanwhile, the market has already priced in this. Also, the

Thailand tourism industry has shown its resilience by

rebounding rapidly in the wake of several unfavourable

events in the past. We expect the sector’s 2017 earnings

growth to still be decent, supported by calmer politics,

additional hotel rooms, rising international tourist arrivals,

and margin expansion from management’s efforts to

increase operational efficiency.

Our top picks on this theme are Airports of Thailand (AOT)

and The Erawan Group (ERW),

Thailand: Visitor arrivals

Source: Company, DBS Vickers

(iv) Strong US dollar

We expect the Fed to hike four times next year and bring

the Fed Funds rate to 1.75% by end 2017. The US 10Y

bond yield should eventually rise above the Fed’s 2%

inflation target towards our 3.25% target in 2017. The US

dollar will keep strengthening, on a relative basis, from here

as long as America leads and widens its growth over other

advanced economies.

Our economist has forecasted Thai baht to weaken from

Bt35.8/US$ at present to Bt36.8/US$ by end-2017. This is in

line with regional currencies.

This should be positive for exporters, most of which derive

their revenue in US dollar. The key beneficiaries include

Indorama Ventures (IVL), Hana Microelectronics (HANA), SVI

Plc. (SVI), Delta Electronics (DELTA), KCE Electronics (KCE),

Thai Union Group (TU).

Thai baht vs the US dollar

Source: DBS Bank

Stock Profi t Growth (%)

2016F 2017F 2018F 2017F 2018F

ANAN 1,451 2,184 2,411 51% 10%

BEAUTY 700 912 1,176 30% 29%

COM7 386 600 756 55% 26%

ERW 319 423 496 32% 17%

FN 124 227 308 83% 36%

GL 1,097 2,209 3,718 101% 68%

MTLS 1,392 2,098 2,853 51% 36%

PACE 182 1,060 n.a. 482% n.a.

SEAFCO 151 237 n.a. 57% n.a.

TKN 750 1,140 1,545 52% 35%

UTP 184 380 476 107% 25%

WORK 281 436 519 55% 19%

Ne t profi t (Btm)

600

1,000

1,400

1,800

2,200

2,600

3,000

3,400

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Au

g

Sep

Oct

No

v

Dec

'000 People

2009 2010 2011 2012

2013 2014 2015 2016

35.2

35.4

35.6

35.8

36.0

36.2

36.4

36.6

36.8

37.0

Current 1Q17 2Q17 3Q17 4Q17

Market Focus

Page 14

(v) CLMV exposure

Despite the weak economic growth at home, a number of

listed companies have ventured into high-growth CLMV

countries to expand their revenue and profit. Thailand’s

GDP is estimated to grow 3.4% in 2017, vs Cambodia

7.1%, Laos 7.1%, Myanmar 8.3% and Vietnam 6.0%.

CLMV have more exciting GDP growth vs Thailand

Source: OECD, DBS Vickers

Companies that have been very successful in expanding into

CLMV include Group Lease (GL), Carabao Group (CBG),

Beauty Community (BEAUTY), Charoen Pokphand Foods

(CPF), Amata Corporation (AMATA), Ch.Karnchang (CK),

and Siam Cement (SCC).

Sector weighting. We recommend that investors be

Overweight on the Construction Contractors, Finance, and

Commerce sectors. These sectors should see strong earnings

growth outlook next year. We rate Media, Telecom and

REIT sectors as Underweight.

SET: Our sector weightings

Source: DBS Vickers

Country

2016 2016F 2017F

Cambodia 7.0 7.1 7.1

Laos 7.4 7.1 7.3

Myanmar 8.7 8.3 8.4

Vietnam 6.7 6.0 6.2

Thailand 2.8 3.2 3.4

Re a l GDP Growth (%)

Sector Reason Top buys

Overweight

Contractor Beneficiary of rising government infrastructure spending CK, STEC

Finance Strong earnings growth outlook GL, MTLS

Commerce Recovering consumption CPALL, BEAUTY

Neutral

Bank Prefer smaller banks to big banks TISCO, TCAP

Building Materials Supported by high value-added and innovative products SCC

Electronics Beneficiary of weak baht HANA, SVI

Energy Market has factored in oil price recovery assumption BCP, PTT

Foods Strong recovery in domestic meat prices and shrimp units TKN

Healthcare Positive outlook but stretched valuation LPH, BDMS

Petrochemicals Olefins chain in good shape, attractive valuation IVL, EPG

Property Prefer those with strong earnings growth outlook ANAN, LH

Transportation Prefer airport to airline AOT, AAV, BEM

Tourism Prefer company with exceptional growth ERW

Underweight

Telecom Fierce competition continues -

REITs Yield spread have compressed, amidst rising bond yields CPNRF, LHHOTEL

Media High competition WORK

Market Focus

Page 15

Sector Update

Tourism Sector

Overweight

Analyst Namida ARTISPONG +662 657 7833 [email protected]

Price Target Price PE

2017F

Div Yld

2017F

EPS CAGR 15-17

(Bt) (Bt) Rec (x) (%) (%)

AOT TB 398.00 455.00 BUY 25.2 1.2 9.7 CENTEL TB 39.75 47.00 BUY 23.5 1.7 16.8 MINT TB 35.75 50.00 BUY 24.1 1.2 -3.7

Source: Company, DBS Vickers

SET Index vs Tourism Sector Stocks

Source: SET, DBS Vickers

Thailand: Visitor arrivals

Source: Company, DBS Vickers

Tourism still going strong 2016 target was revised down

Expect international tourist arrivals to Thailand to

continue to grow

Overweight tourism sector with ERW as top pick

Outlook

2016 target was revised down. Following the passing of

our beloved late King in Oct 2016, hotel operators have

revised down its 2016 revenue target given the expected

impact on their operations in 4Q16 from cancellations of

hotel rooms and postponements of hotel-related activities at

conventions. Meanwhile, Thailand’s Tourism Ministry has

revised down 2016 international tourist arrivals to Thailand

from 34m to 32.4m (+8.4% y-o-y) due to impact from

crackdown on zero-dollar tours. Nevertheless, several

stimulus packages were launched in 4Q16 by the

government to boost consumer spending such as tax break

for domestic tourists for travelling in Thailand and the cut in

visa fees on arrival temporarily for many countries.

Look beyond to 2017. We believe the impact from

crackdown on zero-dollar tours and mourning period is

limited and temporary, as Thailand still offers cost-

competitive travelling and a variety of destinations.

Meanwhile, the market has already priced in this. Also, the

Thailand tourism industry has shown its resilience by

rebounding rapidly in the wake of several unfavourable

events in the past. We expect the sector’s 2017 earnings

growth to still be decent supported by additional hotel

rooms, rising international tourist arrivals, and margin

expansion from management’s efforts to increase

operational efficiency.

ERW is our top buy. Its earnings are now more resilient

given its diversification into lower-end hotel segments. Rising

international tourist arrivals to Thailand would help drive

ERW’s hotel operations as it has the highest exposure to

Thailand's tourism sector. ERW is also taking its first step

overseas into the Philippines in 4Q16. ERW targets to have

20 hotels in the Philippines by FY20F; including three in

Manila that are now under construction. In the next five

years, 13% of EBITDA is expected to be contributed by assets

in the Philippines.

We remain a buy call on AOT. We believe the recent share

price has already priced in concerns over the impact of the

crackdown on zero-dollar tours. The cut in visa fees on arrival

temporarily for foreign tourists from 19 nations including

China, Bhutan, India, Taiwan, and Saudi Arabia, which will

be implemented from 1 Dec to 28 Feb 2017, will surely boost

international arrivals to Thailand.

80%

90%

100%

110%

120%

130%

Jan

-16

Feb

-16

Mar-

16

Ap

r-1

6

May-

16

Jun-1

6

Jul-1

6

Au

g-1

6

Sep

-16

Oct

-16

Nov-

16

Dec-

16

Jan

-17

SET Index AOT TB CENTEL TB MINT TB

600

1,000

1,400

1,800

2,200

2,600

3,000

3,400

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Au

g

Sep

Oct

No

v

Dec

'000 People

2009 2010 2011 2012

2013 2014 2015 2016

Market Focus

Page 16

Construction Sector

Overweight

Analyst Apichaya KETRUTTANABORVORN +662 657 7823 [email protected]

Price Target

Price PE

2017F

Div Yld

2017F

EPS CAGR 15-17

(Bt) (Bt) Rec (x) (%) (%)

CK TB 31.00 40.00 BUY 26.0 1.1 -5.3 STEC TB 27.75 31.00 BUY 28.2 1.8 -0.8 ITD TB* 4.92 NR NR 1.98 0.0 -26.7 UNIQ TB* 19.80 NR NR 19.7 2.0 27.6

* no coverage

Source: Company, DBS Vickers

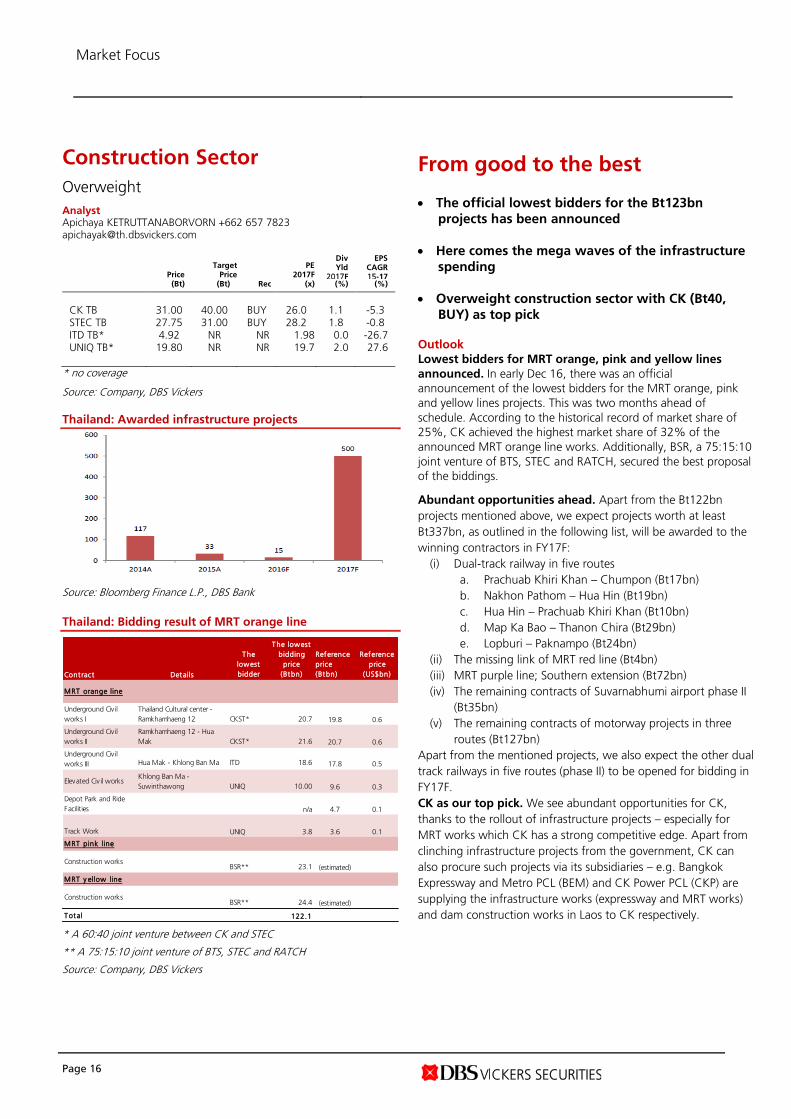

Thailand: Awarded infrastructure projects

Source: Bloomberg Finance L.P., DBS Bank

Thailand: Bidding result of MRT orange line

* A 60:40 joint venture between CK and STEC

** A 75:15:10 joint venture of BTS, STEC and RATCH

Source: Company, DBS Vickers

From good to the best The official lowest bidders for the Bt123bn

projects has been announced

Here comes the mega waves of the infrastructure

spending

Overweight construction sector with CK (Bt40,

BUY) as top pick

Outlook

Lowest bidders for MRT orange, pink and yellow lines

announced. In early Dec 16, there was an official

announcement of the lowest bidders for the MRT orange, pink

and yellow lines projects. This was two months ahead of

schedule. According to the historical record of market share of

25%, CK achieved the highest market share of 32% of the

announced MRT orange line works. Additionally, BSR, a 75:15:10

joint venture of BTS, STEC and RATCH, secured the best proposal

of the biddings.

Abundant opportunities ahead. Apart from the Bt122bn

projects mentioned above, we expect projects worth at least

Bt337bn, as outlined in the following list, will be awarded to the

winning contractors in FY17F:

(i) Dual-track railway in five routes

a. Prachuab Khiri Khan – Chumpon (Bt17bn)

b. Nakhon Pathom – Hua Hin (Bt19bn)

c. Hua Hin – Prachuab Khiri Khan (Bt10bn)

d. Map Ka Bao – Thanon Chira (Bt29bn)

e. Lopburi – Paknampo (Bt24bn)

(ii) The missing link of MRT red line (Bt4bn)

(iii) MRT purple line; Southern extension (Bt72bn)

(iv) The remaining contracts of Suvarnabhumi airport phase II

(Bt35bn)

(v) The remaining contracts of motorway projects in three

routes (Bt127bn)

Apart from the mentioned projects, we also expect the other dual

track railways in five routes (phase II) to be opened for bidding in

FY17F.

CK as our top pick. We see abundant opportunities for CK,

thanks to the rollout of infrastructure projects – especially for

MRT works which CK has a strong competitive edge. Apart from

clinching infrastructure projects from the government, CK can

also procure such projects via its subsidiaries – e.g. Bangkok

Expressway and Metro PCL (BEM) and CK Power PCL (CKP) are

supplying the infrastructure works (expressway and MRT works)

and dam construction works in Laos to CK respectively.

Cont ract Details

The

lowest

bidder

The lowest

bidding

price

(Btbn)

Reference

price

(Btbn)

Reference

price

(US$bn)

Underground Civ il

works I

Thailand Cultural center -

Ramkhamhaeng 12 CKST* 20.7 19.8 0.6

Underground Civ il

works II

Ramkhamhaeng 12 - Hua

Mak CKST* 21.6 20.7 0.6

Underground Civ il

works III Hua Mak - Khlong Ban Ma ITD 18.6 17.8 0.5

Elevated Civ il worksKhlong Ban Ma -

Suwinthawong UNIQ 10.00 9.6 0.3

Depot Park and Ride

Facilities n/a 4.7 0.1

Track Work UNIQ 3.8 3.6 0.1

Construction worksBSR** 23.1 (estimated)

Construction worksBSR** 24.4 (estimated)

Total 122.1

MRT orange line

MRT pink line

MRT y ellow line

Market Focus

Page 17

Finance Sector

Overweight

Analyst Thaninee SATIRAREUNGCHAI, CFA +662 657 7837 [email protected]

Price Target

Price PE

2017F

Div Yld

2017F

EPS CAGR 15-17

(Bt) (Bt) Rec (x) (%) (%)

AEONTS TB 103.50 130.00 BUY 9.5 3.6 2.5 GL TB 57.25 88.00 BUY 42.5 0.6 81.9 MTLS TB 24.70 32.00 BUY 25.0 1.2 59.5

Source: Company, DBS Vickers

SET Index vs Finance Stocks

Source: SET, DBS Vickers

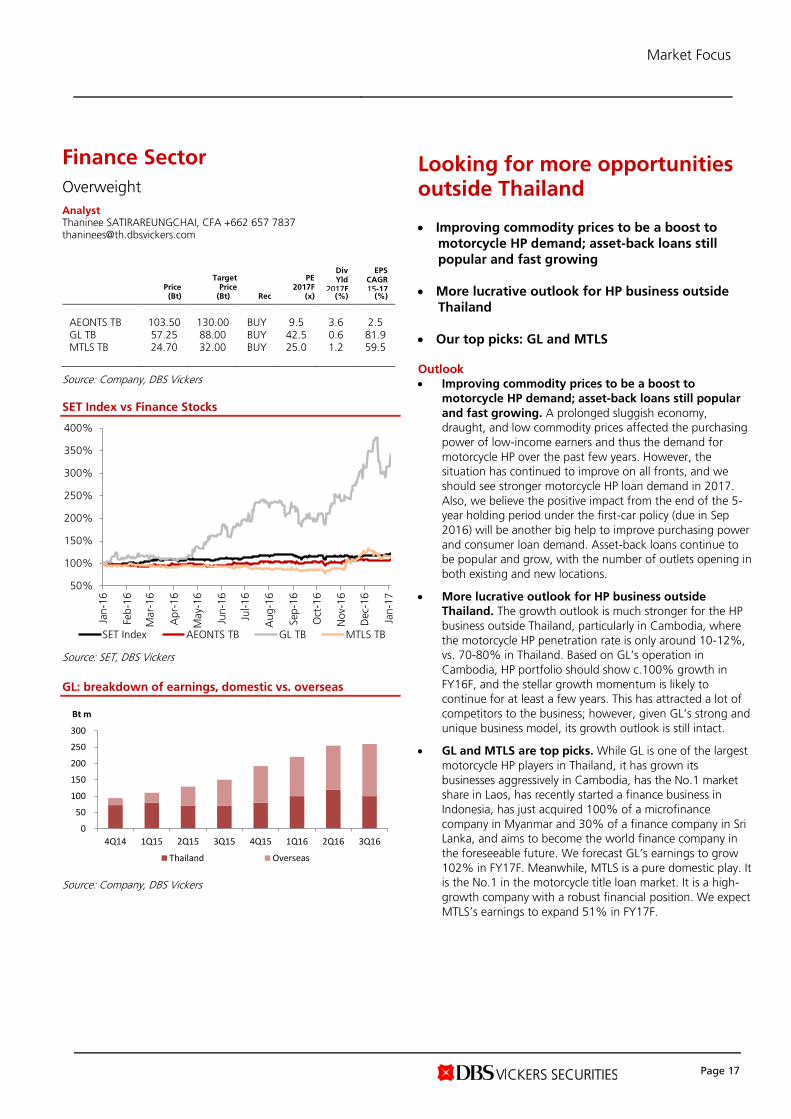

GL: breakdown of earnings, domestic vs. overseas

Source: Company, DBS Vickers

Looking for more opportunities outside Thailand Improving commodity prices to be a boost to

motorcycle HP demand; asset-back loans still

popular and fast growing

More lucrative outlook for HP business outside

Thailand

Our top picks: GL and MTLS

Outlook

Improving commodity prices to be a boost to

motorcycle HP demand; asset-back loans still popular

and fast growing. A prolonged sluggish economy,

draught, and low commodity prices affected the purchasing

power of low-income earners and thus the demand for

motorcycle HP over the past few years. However, the

situation has continued to improve on all fronts, and we

should see stronger motorcycle HP loan demand in 2017.

Also, we believe the positive impact from the end of the 5-

year holding period under the first-car policy (due in Sep

2016) will be another big help to improve purchasing power

and consumer loan demand. Asset-back loans continue to

be popular and grow, with the number of outlets opening in

both existing and new locations.

More lucrative outlook for HP business outside

Thailand. The growth outlook is much stronger for the HP

business outside Thailand, particularly in Cambodia, where

the motorcycle HP penetration rate is only around 10-12%,

vs. 70-80% in Thailand. Based on GL’s operation in

Cambodia, HP portfolio should show c.100% growth in

FY16F, and the stellar growth momentum is likely to

continue for at least a few years. This has attracted a lot of

competitors to the business; however, given GL’s strong and

unique business model, its growth outlook is still intact.

GL and MTLS are top picks. While GL is one of the largest

motorcycle HP players in Thailand, it has grown its

businesses aggressively in Cambodia, has the No.1 market

share in Laos, has recently started a finance business in

Indonesia, has just acquired 100% of a microfinance

company in Myanmar and 30% of a finance company in Sri

Lanka, and aims to become the world finance company in

the foreseeable future. We forecast GL’s earnings to grow

102% in FY17F. Meanwhile, MTLS is a pure domestic play. It

is the No.1 in the motorcycle title loan market. It is a high-

growth company with a robust financial position. We expect

MTLS’s earnings to expand 51% in FY17F.

50%

100%

150%

200%

250%

300%

350%

400%

Jan

-16

Feb

-16

Mar-

16

Ap

r-1

6

May-

16

Jun-1

6

Jul-1

6

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec-

16

Jan

-17

SET Index AEONTS TB GL TB MTLS TB

0

50

100

150

200

250

300

4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Bt m

Thailand Overseas

Market Focus

Page 18

Banking Sector

Neutral

Analyst Thaninee SATIRAREUNGCHAI, CFA +662 657 7837 [email protected]

Price Target

Price PE

2017F

Div Yld

2017F

EPS CAGR 15-17

(Bt) (Bt) Rec (x) (%) (%)

BBL TB 159.50 180.00 BUY 9.0 4.4 -0.3 KBANK TB 177.50 195.00 BUY 12.5 2.3 -7.4 KKP TB 59.00 70.00 BUY 8.4 6.8 34.0 KTB TB 17.70 18.60 HOLD 9.5 4.0 -5.8 TMB TB 2.10 2.30 HOLD 11.7 2.9 -8.3 SCB TB 152.50 167.00 BUY 10.8 3.6 0.7 TISCO TB 60.25 65.00 BUY 8.2 4.1 17.5 TCAP TB 44.00 53.00 BUY 7.4 4.8 13.5

Source: Company, DBS Vickers

SET Index vs Banking Sector

Source: SET, DBS Vickers

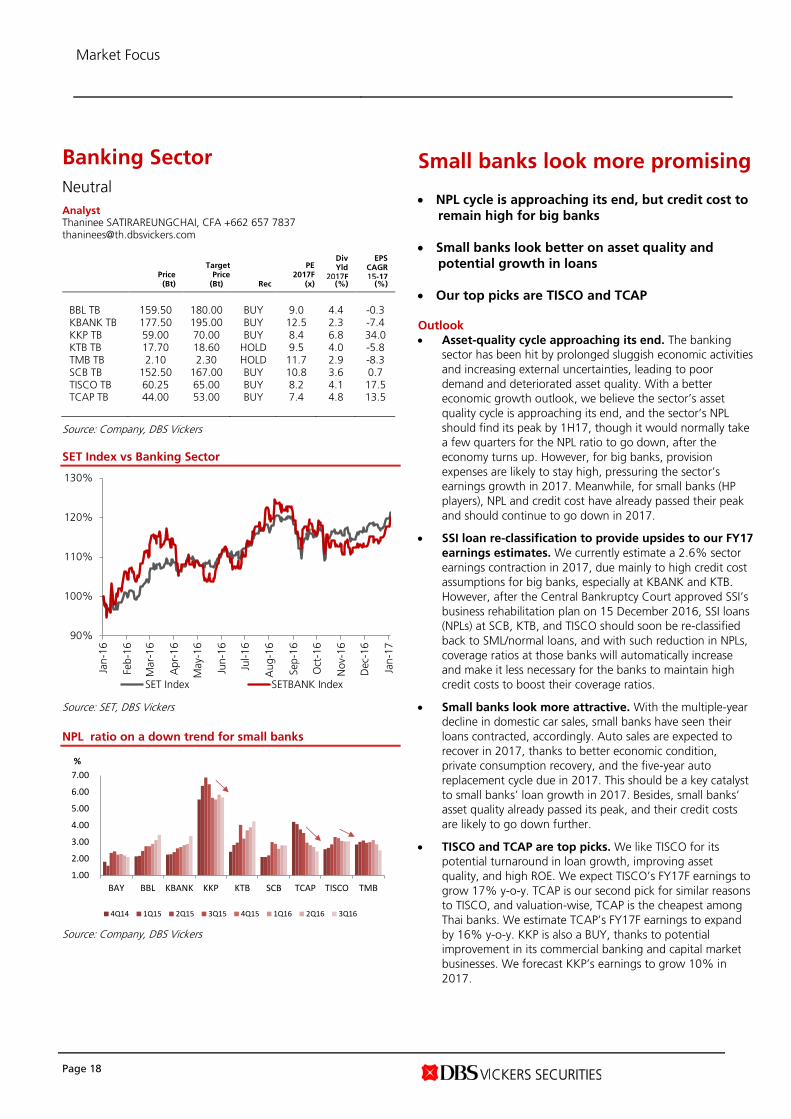

NPL ratio on a down trend for small banks

Source: Company, DBS Vickers

Small banks look more promising NPL cycle is approaching its end, but credit cost to

remain high for big banks

Small banks look better on asset quality and

potential growth in loans

Our top picks are TISCO and TCAP

Outlook

Asset-quality cycle approaching its end. The banking

sector has been hit by prolonged sluggish economic activities

and increasing external uncertainties, leading to poor

demand and deteriorated asset quality. With a better

economic growth outlook, we believe the sector’s asset

quality cycle is approaching its end, and the sector’s NPL

should find its peak by 1H17, though it would normally take

a few quarters for the NPL ratio to go down, after the

economy turns up. However, for big banks, provision

expenses are likely to stay high, pressuring the sector’s

earnings growth in 2017. Meanwhile, for small banks (HP

players), NPL and credit cost have already passed their peak

and should continue to go down in 2017.

SSI loan re-classification to provide upsides to our FY17

earnings estimates. We currently estimate a 2.6% sector

earnings contraction in 2017, due mainly to high credit cost

assumptions for big banks, especially at KBANK and KTB.

However, after the Central Bankruptcy Court approved SSI’s

business rehabilitation plan on 15 December 2016, SSI loans

(NPLs) at SCB, KTB, and TISCO should soon be re-classified

back to SML/normal loans, and with such reduction in NPLs,

coverage ratios at those banks will automatically increase

and make it less necessary for the banks to maintain high

credit costs to boost their coverage ratios.

Small banks look more attractive. With the multiple-year

decline in domestic car sales, small banks have seen their

loans contracted, accordingly. Auto sales are expected to

recover in 2017, thanks to better economic condition,

private consumption recovery, and the five-year auto

replacement cycle due in 2017. This should be a key catalyst

to small banks’ loan growth in 2017. Besides, small banks’

asset quality already passed its peak, and their credit costs

are likely to go down further.

TISCO and TCAP are top picks. We like TISCO for its

potential turnaround in loan growth, improving asset

quality, and high ROE. We expect TISCO’s FY17F earnings to

grow 17% y-o-y. TCAP is our second pick for similar reasons

to TISCO, and valuation-wise, TCAP is the cheapest among

Thai banks. We estimate TCAP’s FY17F earnings to expand

by 16% y-o-y. KKP is also a BUY, thanks to potential

improvement in its commercial banking and capital market

businesses. We forecast KKP’s earnings to grow 10% in

2017.

90%

100%

110%

120%

130%

Jan

-16

Feb

-16

Mar-

16

Ap

r-1

6

May-

16

Jun-1

6

Jul-1

6

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec-

16

Jan

-17

SET Index SETBANK Index

1.00

2.00

3.00

4.00

5.00

6.00

7.00

BAY BBL KBANK KKP KTB SCB TCAP TISCO TMB

%

4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Market Focus

Page 19

Real Estate Sector

Neutral

Analyst Wasu MATTANAPOTCHANART +66 2657 7826 [email protected]

Price Target

Price PE

2017F

Div Yld

2017F

EPS CAGR 15-17

(Bt) (Bt) Rec (x) (%) (%)

ANAN TB 4.94 5.60 BUY 7.5 4.0 34.5 AP TB 7.50 8.50 BUY 7.1 4.9 12.8 LALIN TB 4.62 4.90 BUY 7.5 6.4 19.3 LH TB 9.80 11.50 BUY 13.4 6.0 3.9 LPN TB 12.10 8.60 SELL 12.6 4.0 -23.4 PF TB 0.90 1.05 HOLD 13.6 4.2 18.4 PRIN TB 1.44 1.61 BUY 7.2 5.1 92.2 PSH TB 22.50 27.00 BUY 6.7 7.5 -0.9 QH TB 2.58 2.70 HOLD 7.7 5.8 7.3 RML TB 1.42 1.13 FV 7.6 1.6 -13.6 SC TB 3.42 3.78 HOLD 7.6 6.1 2.2 SIRI TB 1.66 1.32 FV

VALUED

10.1 5.0 -20.0 SPALI TB 25.00 25.00 HOLD 8.0 4.7 11.1

Source: Company, DBS Vickers

SET Index vs Real Estate Sector Stocks

Source: SET, DBS Vickers

Selective BUYs on companies with strong FY17F profits Downward revisions of 2016 targets were

prevalent

Earnings growth expected to improve in FY17F

ANAN, LH and PSH are our top picks

Outlook

Downward revisions of 2016 targets were prevalent.

The SETPROP Index and all eight property developers under

our coverage have underperformed the SET Index in 2016.

Given elevated household-debt level (c.80%) and falling

Consumer Confidence Index during the first six months of

the year (from 76.1 in Dec-15 to 71.6 in Jun 16), developers

were ready to launch most of their condominium projects in

late-3Q16 and 4Q16. However, things took turn for the

worse in 4Q16 since the passing of the late king; marketing

activities were almost non-existent during the 30 days after

13 Oct, and consumer confidence began to fall again. As a

result, developers cut their combined 2016 targets of

transfers by 7%, presales by 15% and new launches by

11%. The developers are expected to end FY16F with

meagre earnings growth of 3%.

Earnings growth expected to improve in FY17F. The

sector’s normalised profit growth is expected to accelerate

slightly to 6% in FY17F, thanks to the outstanding growth

at ANAN (+51%), AP (+28%) and LH (+15%). A major

positive catalyst for the sector in 2017 is that the owners of

the tax-exempt first cars under the government programme

that ran from Sep 11 to Dec 12 will already have repaid

most of their debt, leading to improved mortgage

borrowers’ profiles.

ANAN, LH and PSH are our top picks. Thanks to the JV

turnaround, ANAN (BUY, Bt5.60 TP) is expected to have the

strongest earnings growth in the industry next year at 51%;

its FY17F transfers (including JV’s) of Bt24.1bn (+45% y-o-y)

are already 74% secured, implying the highest revenue

visibility in the industry. For LH, our FY17F earnings of

Bt8.8bn (+6% y-o-y) could be raised substantially if we

include potential gains on sales of i) Grande Centre Point

Ratchadamri Hotel (c.Bt900m gain), and ii) a rental

apartment in the US. PSH (BUY, Bt27.0 TP) is a yield play

with 7.5% FY17F yield and 21% potential upside to our TP.

80%

90%

100%

110%

120%

130%

Jan

-16

Feb

-16

Mar-

16

Ap

r-1

6

May-

16

Jun-1

6

Jul-1

6

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec-

16

Jan

-17

SET Index SETPROP Index

Market Focus

Page 20

Healthcare Sector

Neutral

Analyst Apichaya KETRUTTANABORVORN +662 657 7823 [email protected]

Price Target

Price PE

2017F

Div Yld

2017F

EPS CAGR 15-17

(Bt) (Bt) Rec (x) (%) (%)

BH TB 181.00 160.00 FV 33.6 1.5 6.9 BDMS TB 23.10 27.50 BUY 36.4 1.1 11.4 CHG TB 2.86 3.30 BUY 43.6 1.6 15.8 RJH TB 25.50 30.00 BUY 27.7 1.4 61.2 LPH TB 9.65 10.90 BUY 34.4 1.7 44.7

Source: Company, DBS Vickers

Healthcare sector: FY17 earnings growth

Source: Bloomberg Finance L.P., DBS Bank

National population and proportion of elderly

Source: Company, DBS Vickers

Domestic demand remains the key driver Expect the middle-income focused hospitals to

outperform the premium hospital

Low-risk business with a long-term growth story

Maintain Neutral on the sector; with BDMS, CHG

and RJH as top picks

Outlook

Expect the middle-income focused hospitals to offer

healthy growth after its major investment in FY16. We

expect the middle-income-focused hospitals, i.e. CHG, LPH,

RJH, and including BDMS due to its well-diversified portfolio,

to outperform the premium hospitals. This was on the back

of (i) strong domestic demand growth especially for the mid-

tier hospitals, given the economic slowdown, and (ii) the

capacity expansion and the increasing revenue intensity from

the major investments in FY16.

Upside risk from the potential increase of the

reimbursed rate of social security system (SSS). Given

that the payment structure was revised in 2012 and a

number of private hospitals have exited the SSS scheme, we

expect an increase in the reimbursed rate. However, we

have not included this in our forecast. The hospitals that will

benefit from the increase in the reimbursed rate of SSS are

CHG, LPH and RJH.

Limited growth for premium hospitals. We are

concerned that the medical tourist volume will remain soft,

given weak oil prices and the global economic slowdown.

The premium hospitals, especially BH, should have limited

growth at least for the next three years. This is on the back

of the decline in the number of Middle East patients, which

account for 20% of BH's revenue and offer high margins.

Ageing society, a long-term catalyst. A higher

population of older people is inevitable in Thailand, and this

will help support demand for medical services in the long

run despite c.1% population growth p.a. The Office of the

National Economic and Social Development Board (NESDB)

expects 23% of the country’s population (15m people) to be

older than 60 years old in 2025, up from 14% (9m) in 2017.

10%

6.0%

26%

24%

19%

0%

5%

10%

15%

20%

25%

30%

BDMS BH CHG LPH RJH

Market Focus

Page 21

Telecommunications Sector

Underweight

Analyst Wasu MATTANAPOTCHANART +66 2657 7826 [email protected]

Price Target

Price PE

2017F

Div Yld

2017F

EPS CAGR 15-17

(Bt) (Bt) Rec (x) (%) (%)

ADVANC TB 147.00 154.00

HOLD 15.8 5.1 -16.0 ILINK TB 21.00 24.00 BUY 15.8 2.1 29.8 SAMTEL TB 9.95 9.50 FV 20.2 3.0 -13.1 DTAC TB 37.75 33.00 FV 29.6 2.5 -28.4 TRUE TB* 7.15 NR NR nm 0.0 nm DIF TB 14.00 16.60 BUY 13.5 7.4 11.2 JASIF TB 11.70 11.20 BUY 12.0 8.3 6.6

* no coverage

Source: Company, DBS Vickers

SET Index vs Telecommunications Sector Stocks

Source: SET, DBS Vickers

Revenue market share in Thailand (mobile market)

Source: Company, DBS Vickers

Fierce competition continues TRUE successfully stole market share from

competitors

Aggressive competition to switch to post-paid

market in 2017

Prefer telecom infrastructure funds to mobile

operators

ILINK, a bet on one sizeable project

Outlook

TRUE successfully stole market share from competitors

in 2016. The three mobile operators are expected to end the

year with <8% growth of service income. The first half saw

exceptionally high volume of handset subsides/giveaways for

prepaid customers by all three operators. While ADVANC

and TRUE introduced free handsets (with a minimal amount

of required upfront top-ups) at the beginning of 2016,

DTAC gave handsets away much later than its competitors

(in April) and ended the campaign earlier too (in August).

Given DTAC’s rather passive stance and ADVANC’s

vulnerability (no 900MHz licence until 2H16), TRUE has

raised its revenue market share from 21.7% in 4Q15 to

25.3% in 3Q16, on par with DTAC’s 25.5%.

Aggressive competition to switch to post-paid market

in 2017. We estimate that around 15m handsets were given

to clients for free by the three operators in 1H16. As a

result, most prepaid subscribers that wanted to have new

devices or switch network would likely have done so already.

As the prepaid market is becoming saturated with new

devices, we expect the aggressive competition to switch to

the post-paid market where the operators could demand

customers to stay with them longer by selling on-contract

devices; in fact, this trend has already started. In Oct 16,

ADVANC and TRUE started selling iPhone 7 at 10% discount

with 12-month contract; older models are being sold at up

to 30% discount to the off-contract prices.

Prefer telecom infrastructure funds to mobile

operators. The two telecom infrastructure funds – DIF

(BUY, Bt16.60 TP) and JASIF (HOLD, Bt11.20 TP) – are

immune from fierce competition in the mobile market and

have guaranteed streams of until 2025-27. Our top pick is

currently DIF, thanks to the 19% upside to the TP, 7% yield

and potential asset injection from TRUE in FY17F.

ILINK, a bet on one sizeable project. We expect ILINK’s

earnings to jump 75% next year on the back of Samui

underground and AOT projects; the two account for 29% of

FY17F revenue. While the AOT project was already awarded

in July 2016, winning the Samui project – expected to be

approved by the Cabinet in 1Q17 – could be a major catalyst

for ILINK next year.

80%

90%

100%

110%

120%

130%

Jan

-16

Feb

-16

Mar-

16

Ap

r-1

6

May-

16

Jun-1

6

Jul-1

6

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec-

16

Jan

-17

SET Index SETICT Index

Market Focus

Page 22

Electronics Sector

Neutral

Analyst NANTIKA WIANGPHOEM +662 657 7823 [email protected]

Price Target

Price PE

2017F

Div Yld

2017F

EPS CAGR 15-17

(Bt) (Bt) Rec (x) (%) (%)

SVI TB 5.10 5.20 BUY 14.9 3.4 -37.7 DELTA TB 81.50 76.00 HOL

D 16.1 4.0 -3.2

HANA TB 39.50 31.00 HOLD

15.7 3.8 -1.0 KCE TB 122.00 121.00 BUY 18.2 2.2 32.4

Source: Company, DBS Vickers

SET Index vs Electronics Sector Stocks

Source: SET, DBS Vickers

11M16 electronic export sales

Products (USD m) 11M15 11M16 % change

Computer 225 202 -9.9%

Computer parts & accessories 13,377 12,275 -8.2%

Integrated circuits & parts 7,077 7,008 -1.0%

Printed circuits 1,223 1,126 -7.9%

Telecommunication equipment 3,274 3,273 0.0%

Other electrical apparatus 4,203 4,509 7.3%

Total 29,379 28,393 -3.4%

Source: Company, DBS Vickers

A recovery that is priced in Electronics market gets back on track

Baht depreciation, better margin

Stretched valuation for the sector

Outlook

Electronics export sales started registering growth