THAILAND EQUITY RESEARCH Page | 1 | PHILLIP SECURITIES (THAILAND) Closing Price(Bt) 14.00 Target Price(Bt) 14.00 (+1.18%) COMPANY DATA O/S Shares (mn) : 2,800 Market Cap. (Btmn) : Market Cap. (USDmn) : 52‐WK Hi/Lo (Bt) : 15.8/8 3M Average Daily T/O (mn) : 32.70 Par Value (Bt) : 1.00 MAJOR SHAREHOLDERS (%) 1. Vitoorapakorn Holding Co., 60.0 2. Pawat Vitoorapakorn 3.3 3. Teerawat Vitoorapakorn 2.3 PRICE PERFORMANCE (%) 1MTH 3MTH 1YR ABS 10% 53% 69% REL TO SET INDEX 8% 68% 108% PRICE VS SET INDEX Source: Bloomberg, PSR KEY FINANCIALS FYE Mar FY15 FY16E FY17E FY18E Sales(Btmn) 6,913 8,795 11,164 13,381 Net Profit(Btmn) 629 1,539 2,031 2,698 EPS (Bt) 0.27 0.55 0.73 0.96 P/E (X) 51.9 25.5 19.3 14.5 BVPS (Bt) 2.93 3.39 4.01 4.83 P/B (X) 4.8 4.1 3.5 2.9 DPS (Bt) 0.08 0.16 0.22 0.29 Dividend Yield (%) 0.6 1.2 1.6 2.1 ROE (%) 10.50 17.41 19.63 21.82 Debt/Equity (X) 0.79 0.69 0.59 0.48 Source: Company, PSR Est. **Multiples and yields are based on latest closing price VALUATION METHOD PE'58/59 25x (g=25%) Danai Tunyaphisitchai, CFA Capital Market Investment Analyst # 2375 Tel: 66 2 635 1700 # 481 Thanatphat Suksrichavalit Assistant Analyst 03 February 2016 39,200 1,097 27 November 2015 Neutral 0 10 20 30 40 50 60 Feb‐13 Feb‐14 Feb‐15 Feb‐16 EPG TB EQ UI TY SETI (rebased) Eastern Polymer Group Thailand’s leader in polymer & plastic conversion innovations THAILAND | SET | CONMAT | INITIATION OF COVERAGE BLOOMBERG EPG TB l REUTERS EPG.BK Thailand’s leader in polymer & plastic conversion innovations EPG is a holding company mainly investing in innovative polymer and plastic conversion business. Most of its revenue comes from the following three wholly owned subsidiaries: (1) Aeroflex (AFC), a producer of thermal insulation, (2) Aeroklas (ARK), a manufacturer and supplier of auto parts and accessories and (3) Eastern Polypack (EPP), which is engaged in the packing business. Note that all subsidiaries are involved in the conversion of downstream plastic pellets into products for various industries both at home and abroad and reaped the benefit of a recent drop in oil prices. In addition, innovations and patents for the development of products made from polymers and plastics have also kept EPG in front and stay competitive in the global arena. ARK set to be a rising star in the next three years ARK is a OEM,ODM and REM manufactuer and distributor of auto parts and accessories. The product design and development will be carried out by Aeroklas under its patents. Its product offerings are parts of pick‐ up trucks including the likes of bed liner, canopy and side step, the latest product supplied directly to Ford. Last year Aeroklas acquired a 100% stake in TJM, a well‐known supplier of offroad accessories in Australia. With TJM, there is potential for Aeroklas to see explosive growth in the next three years. 2QFY15/16 net profit up 47.45% q‐q and 198.88% y‐y to Bt424.3mn helped by the benefit of lower oil prices EPG delivered a strong set of financial results in 2QFY15/16 ending Sep 2015. For the period, net profit clocked in at Bt424.3mn, up 47.45% q‐q and 198.88% y‐y. Total revenue leapt 35.42% y‐y on the back of a strong showing from Aeroklas helped by revenue contribution from the recently acquired TJM. Total costs rose at slower pace than revenue at 20.32% y‐y thanks to a retreat in raw material costs along with oil prices and production economy of scale. For the whole of FY15/16, we expect its earnings to be strong driven by direct parts orders from automaker during the year and growth from TJM. Our forecast puts its FY15/16 net profit at Bt1,539mn or Bt0.55/share, up 103.57% y‐y. Initiation of coverage with ‘NEUTRAL’ rating and FY15/16 target price of Bt14/share We set a FY15/16 target price of Bt15/share for EPG. The target is based on a PEG of 1x assuming a profit CAGR of 25% over the next three years. Even though much of its fundamental value appears to have already been reflected in the current share price, its long‐term growth profile however looks promising as there remains scope for EPG to pull in more orders from other automakers in Thailand, which is the world’s biggest production base for pick‐up trucks and the expansion of TJM should keep growth rolling along the road ahead. At the end of the day, we initiate our coverage of EPG with a ‘NEUTRAL’ rating. Ref. No.: CO2016_0097

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THAILAND EQUITY RESEARCH

Page | 1 | PHILLIP SECURITIES (THAILAND)

Closing Price(Bt) 14.00

Target Price(Bt) 14.00 (+1.18%)

COMPANY DATA

O/S Shares (mn) : 2,800

Market Cap. (Btmn) :

Market Cap. (USDmn) :

52‐WK Hi/Lo (Bt) : 15.8/8

3M Average Daily T/O (mn) : 32.70

Par Value (Bt) : 1.00

MAJOR SHAREHOLDERS (%)

1. Vitoorapakorn Holding Co., 60.0

2. Pawat Vitoorapakorn 3.3

3. Teerawat Vitoorapakorn 2.3

PRICE PERFORMANCE (%)

1MTH 3MTH 1YR

ABS 10% 53% 69%

REL TO SET INDEX 8% 68% 108%

PRICE VS SET INDEX

Source: Bloomberg, PSR

KEY FINANCIALS

FYE Mar FY15 FY16E FY17E FY18E

Sales(Btmn) 6,913 8,795 11,164 13,381

Net Profit(Btmn) 629 1,539 2,031 2,698

EPS (Bt) 0.27 0.55 0.73 0.96

P/E (X) 51.9 25.5 19.3 14.5

BVPS (Bt) 2.93 3.39 4.01 4.83

P/B (X) 4.8 4.1 3.5 2.9

DPS (Bt) 0.08 0.16 0.22 0.29

Dividend Yield (%) 0.6 1.2 1.6 2.1

ROE (%) 10.50 17.41 19.63 21.82

Debt/Equity (X) 0.79 0.69 0.59 0.48

Source: Company, PSR Est.

**Multiples and yields are based on latest closing price

VALUATION METHOD

PE'58/59 25x (g=25%)

Danai Tunyaphisitchai, CFA

Capital Market Investment Analyst # 2375

Tel: 66 2 635 1700 # 481

Thanatphat Suksrichavalit

Assistant Analyst

03 February 2016

39,200

1,097

27 November 2015

Neutral

0

10

20

30

40

50

60

Feb‐13 Feb‐14 Feb‐15 Feb‐16

EPG TB EQUITY SETI (rebased)

Eastern Polymer Group

Thailand’s leader in polymer & plastic conversion innovations

THAILAND | SET | CONMAT | INITIATION OF COVERAGE BLOOMBERG EPG TB l REUTERS EPG.BK

Thailand’s leader in polymer & plastic conversion innovations EPG is a holding company mainly investing in innovative polymer and plastic conversion business. Most of its revenue comes from the following three wholly owned subsidiaries: (1) Aeroflex (AFC), a producer of thermal insulation, (2) Aeroklas (ARK), a manufacturer and supplier of auto parts and accessories and (3) Eastern Polypack (EPP), which is engaged in the packing business. Note that all subsidiaries are involved in the conversion of downstream plastic pellets into products for various industries both at home and abroad and reaped the benefit of a recent drop in oil prices. In addition, innovations and patents for the development of products made from polymers and plastics have also kept EPG in front and stay competitive in the global arena. ARK set to be a rising star in the next three years ARK is a OEM,ODM and REM manufactuer and distributor of auto parts and accessories. The product design and development will be carried out by Aeroklas under its patents. Its product offerings are parts of pick‐up trucks including the likes of bed liner, canopy and side step, the latest product supplied directly to Ford. Last year Aeroklas acquired a 100% stake in TJM, a well‐known supplier of offroad accessories in Australia. With TJM, there is potential for Aeroklas to see explosive growth in the next three years. 2QFY15/16 net profit up 47.45% q‐q and 198.88% y‐y to Bt424.3mn helped by the benefit of lower oil prices EPG delivered a strong set of financial results in 2QFY15/16 ending Sep 2015. For the period, net profit clocked in at Bt424.3mn, up 47.45% q‐q and 198.88% y‐y. Total revenue leapt 35.42% y‐y on the back of a strong showing from Aeroklas helped by revenue contribution from the recently acquired TJM. Total costs rose at slower pace than revenue at 20.32% y‐y thanks to a retreat in raw material costs along with oil prices and production economy of scale. For the whole of FY15/16, we expect its earnings to be strong driven by direct parts orders from automaker during the year and growth from TJM. Our forecast puts its FY15/16 net profit at Bt1,539mn or Bt0.55/share, up 103.57% y‐y. Initiation of coverage with ‘NEUTRAL’ rating and FY15/16 target price of Bt14/share We set a FY15/16 target price of Bt15/share for EPG. The target is based on a PEG of 1x assuming a profit CAGR of 25% over the next three years. Even though much of its fundamental value appears to have already been reflected in the current share price, its long‐term growth profile however looks promising as there remains scope for EPG to pull in more orders from other automakers in Thailand, which is the world’s biggest production base for pick‐up trucks and the expansion of TJM should keep growth rolling along the road ahead. At the end of the day, we initiate our coverage of EPG with a ‘NEUTRAL’ rating.

Ref. No.: CO2016_0097

Page | 2 | PHILLIP SECURITIES (THAILAND)

Eastern Polymer Group INITIATION OF COVERAGE

Investment Thesis 1. EPG is a holding company mainly investing in downstream plastic conversion for various

industries. The benefit of a recent drop in oil prices also gave margins a lift. 2. The acquisition of TJM in Australia has opened up more business opportunities for ARK

through its own distribution channel. Direct parts orders from domestic automaker Ford has also left room for ARK to pull in more orders from other carmakers, pointing to strong growth outlook ahead. Growth prospects also remain strong for AFC and EPP. Our forecast puts EPG’s FY15‐16 total sales growth at 25.3% y‐y while total costs are expected to rise at a slower pace than sales at a mere 13.1% y‐y.

3. We set a FY15/16 target price of Bt14/share for EPG. The target is based on a PEG of 1x, assuming an explosive earnings growth over the next three years at a CAGR of 25%. We initiate our coverage of EPG with a ‘NEUTRAL ‘rating as much of its fundamental value appears to have already been reflected in the current share price.

Business overview EPG is a holding company mainly investing in innovative polymer and plastic conversion business. Most of its revenue comes from the following three wholly owned subsidiaries: (1) Aeroflex (AFC), a producer of thermal insulation, (2) Aeroklas (ARK), a manufacturer and supplier of auto parts and accessories, and (3) Eastern Polypack (EPP), which is engaged in the packing business. AFC, the world’s third largest producer of thermal insulation AFC is the world’s third largest producer of insulation. Its key product is thermal insulation. AFC is also the only producer that has developed a special type of insulation made from Ethylene Propylene Diene Methylene (EPDM) after a long period of R&D. Its superior technology provides several advantages over its competitors. Its insulation rubber can withstand temperature range from ‐200C to 125C and strong humidity with weather condition resistance and environmentally friendly properties.Its rubber insulations are extensively used to keep temperature in air‐conditioning industry as an insulation for air conducting system, indoor chilled/hot water pipings. In addition, it can also be applied as acoustic absorber to reduce noised generated by equipment, air movement and the expansion and contraction noise of sheet metal duct. In 2014, AFC captured a 65% share of the domestic insulation market in Thailand. Domesic sales contributed 30% of its total revenue and the rest from overseas sales. AFC had a 10% share of the global insulation market behind only Armacell (America) and K‐Flex (Italy) which produced Nitrile Butadiene Rubber (NBR) insulations. However, special characteristics of EPDM insulations and various global patents make AFC’s products competitive especially among price‐insensitive clients as part of the efforts to avoid price war and keep margins high. Figure 1: Aeroflex’s thermal insulation

Source: EPG Construction industry still in strong growth mode in Asia Demand for thermal insulation products is closely tied to growth in the global construction industry which is forecast to grow at an average annual clip of 4.1% and value at up to US$10.4trn in 2018, according to Business Monitor and EPG. The construction industry in Asia is expected to grow the most among other regions at 5%, well above the global industry’s average.

Page | 3 | PHILLIP SECURITIES (THAILAND)

Eastern Polymer Group INITIATION OF COVERAGEARK, a global leading supplier of auto parts and accessories ARK is the world leading manufacturer and supplier of auto parts and accessories. It operates as an original equipment manufactuer (OEM)/original design manufacturer (ODM) and replacement equipment manufactuer (REM) under the ‘AEROKLAS’ brand. The design and development of products are based on its own patents. Its product offersings are parts of pick‐up trucks or SUVs including the likes of bed liner, canopy and deck cover. Figure 2: Aeroklas’s auto parts and accessories

Source: EPG Acquisition of TJM to bring its former glory back to life In 2015, ARK acquired a 100% stake in TJM, a well‐known supplier of offroad accessories in Australia. TJM is a top two player in the Australian car accessories market in terms of sales and it has well established sales channels with 58 branded distributors and 27 licensed stores across Australia, allowing ARK to take advantage of its sales channels to expand its presence into Australia. In 1HFY15/16, ARK earned revenue of Bt468.4mn. Figure 3: TJM branded branch in Australia Source: TJM Stable revenue growth profile with product acceptance from carmaker ARK of late supplied side step to one of the global car brands Ford in Thailand. Side step is one of the key components in the assembly of its latest car model launched last year. With ODM production, margins are higher than those of OEM production. Direct orders from Ford has given ARK room for further growth and enhances its revenue stability throughout the production cycle of each car model which normally lasts 5‐8 years in addition to car accessories business. Currently ARK has more than 300 clients in its car accessories business, reflecting the acceptance of product quality and increasing opportunities for ARK to receive new orders from other clients. EPP, a leader in disposable plastic packaging for food and beverage with state‐of‐the‐art technology EPP is a high‐quality manufacturer and distributor of disposable plastic packaging for food and beverage such as drinking cups, plates and bowls. Its products are of higher quality with unique design from its competitors. EPP counts McDonald, KFC, Yam Yam and CP as its major clients. Its products are also distributed through more than 200 sale agents in Thailand and exported to overseas markets i.e. Australia, Singapore and Myanmar.

Page | 4 | PHILLIP SECURITIES (THAILAND)

Eastern Polymer Group INITIATION OF COVERAGEFigure 4: EPP products

Source: EPG One of the EPP’s major products are plastic sheets used as raw materials in forming into products for various industries, mostly construction and automotive accessories. Figure 5: Correlation between packaging consumption in F&B industry and global GDP

Sources: World Bank, EPG The chart shows that average growth in the F&B packaging market has outstripped global GDP growth, leaving rooom for EPP to grow ahead amid a steady rise in demand. EPP has a 10%‐15% share of the F&B packaging market in Asia and it retains its position as the number one leader in the domestic F&B packaging market with a market share of 35%‐40%. JV with Japan’s producers of automotive rubber parts EPG also earns revenue from JV with Japanese Automotive part supplier i) Sumitomo Rico of Japan, one of the world’s biggest producers of automotive anti‐vibration rubber parts.It has a 20% stake in Tokai Eastern Rubber (Thailand) Co (TER), a JV with Sumitomo Rico, which produces shock absorbing rubber and fuel hoses for motorcycles and vehicles for distribution in Thailand and Japan. ii) EPG also owns a 27% stake in Zeon Advanced Polymix Co (ZAP), a producer and distributor of rubber compound for natural and artificial rubber used in various industries i.e. anti‐vibration rubber, seals, car doors including rubber parts used in construction site. Its investments in JVs generated profits of up to Bt229.1mn to EPG in FY14/15. Profits from JVs also came in at Bt121.9mn in 1HFY15/16. The prospect of a pickup in the auto industry also reflects more growth potential for JVs. R&D key to business growth EPG has continued to place greater importance on R&D as it has a clear policy to set aside 1% of its total sales for R&D. The continued launch of new products onto the market including Aeroroof, a thermal insulation for roof and full box set in car accessories business, which add value to its products, has also enhanced EPG’s competitive advantage in the long run.

Page | 5 | PHILLIP SECURITIES (THAILAND)

Eastern Polymer Group INITIATION OF COVERAGE Revenue structure The following is a revenue breakdown by business over the past three years. Figure 6: Revenue breakdown

Revenue(Btmn) Apr12-Mar13 %

Apr13-Mar14 %

Apr14-Mar15 %

Apr15-Mar16 %

Y12/13 Y13/14 Y14/15 1H15/16 Aeroflex 2,043.9 30.3% 2,133.6 32.4% 2,295.2 33.2% 1,334.7 30.7% Aeroklas 2,590.2 38.4% 2,281.5 34.6% 2,404.8 34.8% 1,717.9 39.6% Eastern Polypack 2,116.1 31.3% 2,176.7 33.0% 2,212.7 32.0% 1,290.4 29.7% Total 6,750.2 100.0% 6,591.8 100.0% 6,912.8 100.0% 4,343.1 100.0% Source: PSR,EPG 2QFY15/16 net profit up 47.45% q‐q and 198.88% y‐y to Bt424.3mn helped by the benefit of lower oil prices EPG delivered a strong set of financial results in 2QFY15/16 ending Sep 2015. For the period, net profit clocked in at Bt424.3mn, up 47.45% q‐q and 198.88% y‐y. Side step orders from Ford led ARK to achieved revenue growth of up to 41.4%. For 1HFY15/16, its net profit came in at Bt712.1mn, up 135.9% from Bt301.8mn in 1HFY14/15 as sales grew 25.3% y‐y and cost of sales rose at a slower pace than sales at a mere 13.1% y‐y, benefiting from lower raw materials prices and production economies of scale on the back of higher operating run rates. Falling oil prices a boon for EPG Falling oil prices pushed prices of plastic pellets, EPG’s raw materials lower, giving a big boost to its gross and net profit margins from 4QFY14/15 onwards. In 2015, oil prices fell precipitously to US$40/barrel from US$60/barrel. Figure 7: EPG profitability metrics

Source: PSR,EPG Solid financial profile puts EPG in position to cash in on future growth Following market listing on Dec 24, 2014, its D/E ratio dropped sharply to 0.5x in FY14/15 from 1.9x in FY13/14 as part of the IPO proceeds was used to pay back some interest‐bearing debt and fund its future investments. FY15/16 net profit seen at Bt1,539mn, up 103.57% y‐y Explosive earnings growth is expected in the next three years according to EPG’s growth strategy. ARK would act as a key growth catalyst for EPG. In 2QFY15/16, ARK achieved revenue growth of 19.1% q‐q and 61.4% y‐y boosted by new orders and revenue

Page | 6 | PHILLIP SECURITIES (THAILAND)

Eastern Polymer Group INITIATION OF COVERAGEcontribution from JTM. For the whole of FY15/16, we expect EPG to deliver net profit of Bt1,545mn. The forecast is based on the following assumptions: (1) Full‐year total sales will grow 25.3% y‐y on the back of growth in car accessorieis

business run by ARK following the consolidation of TJM with revenue growth of at least 20% a year and direct orders from Ford which would be gradually realized as revenue over the remaining course of the year. By our estimate, we see scope for ASK to achieve revenue growth of 50% y‐y. For AFC and EPP, we assume revenue growth of 15% and 20% y‐y respectively.

(2) Cost of sales will rise 13.1% y‐y, benefiting from lower raw materials costs and production economies of scale on the back of higher operating run rates.

The 1HFY15/16 net profit of Bt712.1mn accounted for only 46.27% of our full‐year target as TJM was still in the process of organizational restructuring when SG&A expenses remained high and profits dropped and orders from Ford just came in during 2QFY15/16. As the above headwinds are likely to be only temporary, we expect EPG’s earnings growth to be strong in 2HFY15/16. Initiation of coverage with ‘NEUTRAL’ rating and FY15/16 target price of Bt14/share We set a FY15/16 target price of Bt14/share for EPG. The target is based on a PEG of 1x assuming a profit CAGR of 25% over the next three years. Even though much of its fundamental value appears to have already been reflected in the current share price, its long‐term growth profile however looks promising as there remains scope for EPG to pull in more orders from other automakers in Thailand, which is the world’s biggest production base for pick‐up trucks and the expansion of TJM should keep growth rolling along the road ahead. At the end of the day, we initiate our coverage of EPG with a ‘NEUTRAL’ rating. Risk factors 1. Swings in raw materials prices 2. FX volatility 3. Rapid technology changes 4. Dependence on highly volatile construction and auto industries

Page | 7 | PHILLIP SECURITIES (THAILAND)

Eastern Polymer Group INITIATION OF COVERAGE

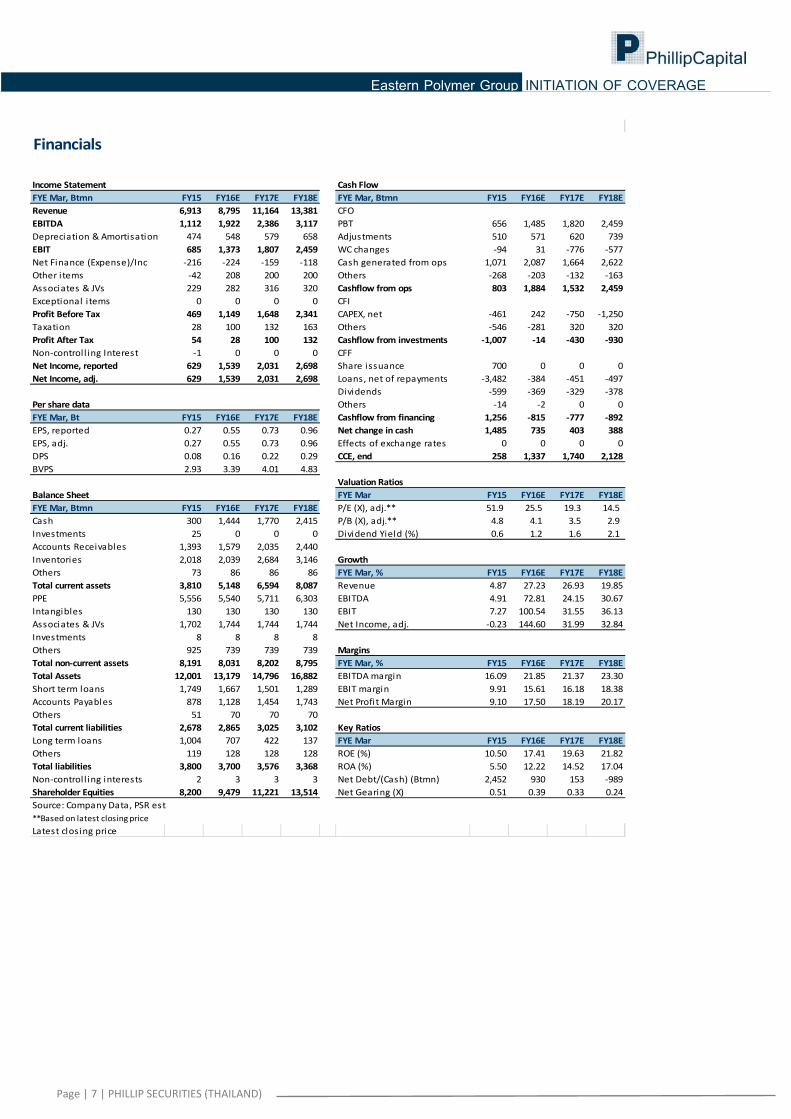

Financials

Income Statement Cash Flow

FYE Mar, Btmn FY15 FY16E FY17E FY18E FYE Mar, Btmn FY15 FY16E FY17E FY18E

Revenue 6,913 8,795 11,164 13,381 CFO

EBITDA 1,112 1,922 2,386 3,117 PBT 656 1,485 1,820 2,459

Depreciation & Amortisation 474 548 579 658 Adjustments 510 571 620 739

EBIT 685 1,373 1,807 2,459 WC changes ‐94 31 ‐776 ‐577

Net Finance (Expense)/Inc ‐216 ‐224 ‐159 ‐118 Cash generated from ops 1,071 2,087 1,664 2,622

Other i tems ‐42 208 200 200 Others ‐268 ‐203 ‐132 ‐163

Associates & JVs 229 282 316 320 Cashflow from ops 803 1,884 1,532 2,459

Exceptional i tems 0 0 0 0 CFI

Profit Before Tax 469 1,149 1,648 2,341 CAPEX, net ‐461 242 ‐750 ‐1,250

Taxation 28 100 132 163 Others ‐546 ‐281 320 320

Profit After Tax 54 28 100 132 Cashflow from investments ‐1,007 ‐14 ‐430 ‐930

Non‐controll ing Interest ‐1 0 0 0 CFF

Net Income, reported 629 1,539 2,031 2,698 Share issuance 700 0 0 0

Net Income, adj. 629 1,539 2,031 2,698 Loans, net of repayments ‐3,482 ‐384 ‐451 ‐497

Dividends ‐599 ‐369 ‐329 ‐378

Per share data Others ‐14 ‐2 0 0

FYE Mar, Bt FY15 FY16E FY17E FY18E Cashflow from financing 1,256 ‐815 ‐777 ‐892

EPS, reported 0.27 0.55 0.73 0.96 Net change in cash 1,485 735 403 388

EPS, adj. 0.27 0.55 0.73 0.96 Effects of exchange rates 0 0 0 0

DPS 0.08 0.16 0.22 0.29 CCE, end 258 1,337 1,740 2,128

BVPS 2.93 3.39 4.01 4.83

Valuation Ratios

Balance Sheet FYE Mar FY15 FY16E FY17E FY18E

FYE Mar, Btmn FY15 FY16E FY17E FY18E P/E (X), adj.** 51.9 25.5 19.3 14.5

Cash 300 1,444 1,770 2,415 P/B (X), adj.** 4.8 4.1 3.5 2.9

Investments 25 0 0 0 Dividend Yield (%) 0.6 1.2 1.6 2.1

Accounts Receivables 1,393 1,579 2,035 2,440

Inventories 2,018 2,039 2,684 3,146 Growth

Others 73 86 86 86 FYE Mar, % FY15 FY16E FY17E FY18E

Total current assets 3,810 5,148 6,594 8,087 Revenue 4.87 27.23 26.93 19.85

PPE 5,556 5,540 5,711 6,303 EBITDA 4.91 72.81 24.15 30.67

Intangibles 130 130 130 130 EBIT 7.27 100.54 31.55 36.13

Associates & JVs 1,702 1,744 1,744 1,744 Net Income, adj. ‐0.23 144.60 31.99 32.84

Investments 8 8 8 8

Others 925 739 739 739 Margins

Total non‐current assets 8,191 8,031 8,202 8,795 FYE Mar, % FY15 FY16E FY17E FY18E

Total Assets 12,001 13,179 14,796 16,882 EBITDA margin 16.09 21.85 21.37 23.30

Short term loans 1,749 1,667 1,501 1,289 EBIT margin 9.91 15.61 16.18 18.38

Accounts Payables 878 1,128 1,454 1,743 Net Profit Margin 9.10 17.50 18.19 20.17

Others 51 70 70 70

Total current liabilities 2,678 2,865 3,025 3,102 Key Ratios

Long term loans 1,004 707 422 137 FYE Mar FY15 FY16E FY17E FY18E

Others 119 128 128 128 ROE (%) 10.50 17.41 19.63 21.82

Total liabilities 3,800 3,700 3,576 3,368 ROA (%) 5.50 12.22 14.52 17.04

Non‐controll ing interests 2 3 3 3 Net Debt/(Cash) (Btmn) 2,452 930 153 ‐989

Shareholder Equities 8,200 9,479 11,221 13,514 Net Gearing (X) 0.51 0.39 0.33 0.24

Latest closing price

Source: Company Data, PSR est

**Based on latest closing price

Page | 8 | PHILLIP SECURITIES (THAILAND)

Eastern Polymer Group INITIATION OF COVERAGE

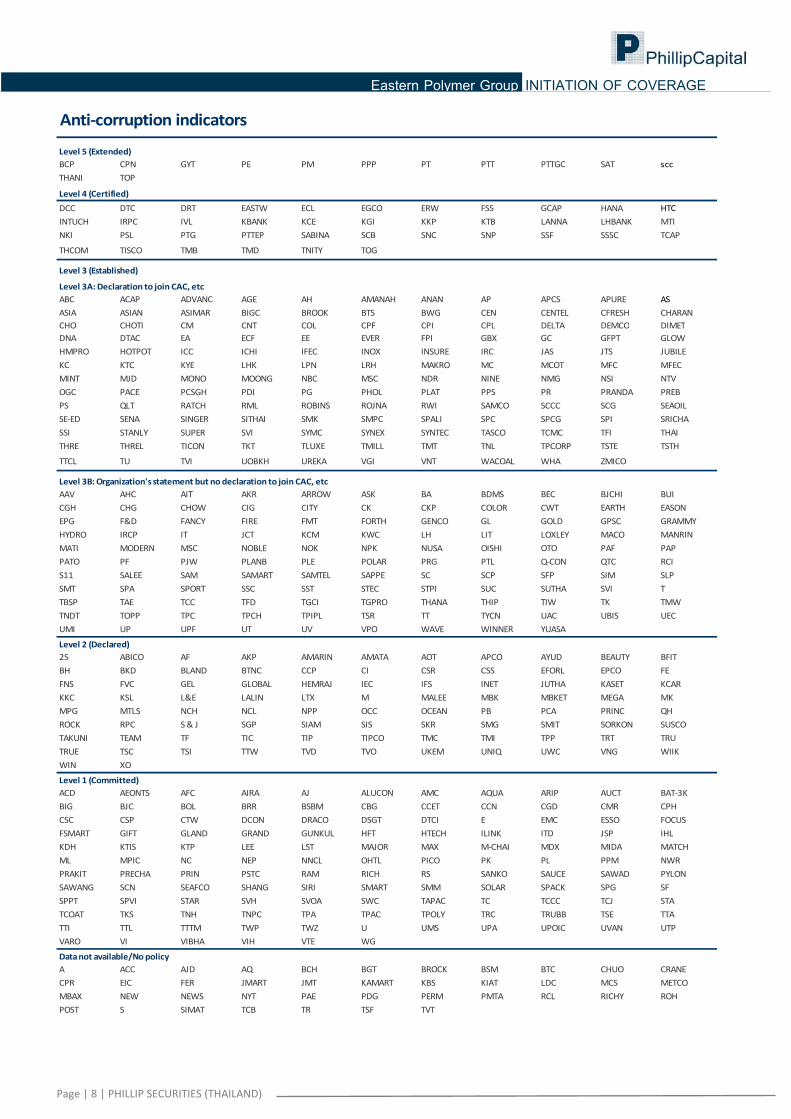

Anti‐corruption indicators

Level 5 (Extended)

BCP CPN GYT PE PM PPP PT PTT PTTGC SAT scc

THANI TOP

Level 4 (Certified)

DCC DTC DRT EASTW ECL EGCO ERW FSS GCAP HANA HTC

INTUCH IRPC IVL KBANK KCE KGI KKP KTB LANNA LHBANK MTI

NKI PSL PTG PTTEP SABINA SCB SNC SNP SSF SSSC TCAP

THCOM TISCO TMB TMD TNITY TOG

Level 3 (Established)

Level 3A: Declaration to join CAC, etc

ABC ACAP ADVANC AGE AH AMANAH ANAN AP APCS APURE AS

ASIA ASIAN ASIMAR BIGC BROOK BTS BWG CEN CENTEL CFRESH CHARAN

CHO CHOTI CM CNT COL CPF CPI CPL DELTA DEMCO DIMET

DNA DTAC EA ECF EE EVER FPI GBX GC GFPT GLOW

HMPRO HOTPOT ICC ICHI IFEC INOX INSURE IRC JAS JTS JUBILE

KC KTC KYE LHK LPN LRH MAKRO MC MCOT MFC MFEC

MINT MJD MONO MOONG NBC MSC NDR NINE NMG NSI NTV

OGC PACE PCSGH PDI PG PHOL PLAT PPS PR PRANDA PREB

PS QLT RATCH RML ROBINS ROJNA RWI SAMCO SCCC SCG SEAOIL

SE‐ED SENA SINGER SITHAI SMK SMPC SPALI SPC SPCG SPI SRICHA

SSI STANLY SUPER SVI SYMC SYNEX SYNTEC TASCO TCMC TFI THAI

THRE THREL TICON TKT TLUXE TMILL TMT TNL TPCORP TSTE TSTH

TTCL TU TVI UOBKH UREKA VGI VNT WACOAL WHA ZMICO

Level 3B: Organization's statement but no declaration to join CAC, etc

AAV AHC AIT AKR ARROW ASK BA BDMS BEC BJCHI BUI

CGH CHG CHOW CIG CITY CK CKP COLOR CWT EARTH EASON

EPG F&D FANCY FIRE FMT FORTH GENCO GL GOLD GPSC GRAMMY

HYDRO IRCP IT JCT KCM KWC LH LIT LOXLEY MACO MANRIN

MATI MODERN MSC NOBLE NOK NPK NUSA OISHI OTO PAF PAP

PATO PF PJW PLANB PLE POLAR PRG PTL Q‐CON QTC RCI

S11 SALEE SAM SAMART SAMTEL SAPPE SC SCP SFP SIM SLP

SMT SPA SPORT SSC SST STEC STPI SUC SUTHA SVI T

TBSP TAE TCC TFD TGCI TGPRO THANA THIP TIW TK TMW

TNDT TOPP TPC TPCH TPIPL TSR TT TYCN UAC UBIS UEC

UMI UP UPF UT UV VPO WAVE WINNER YUASA

Level 2 (Declared)

2S ABICO AF AKP AMARIN AMATA AOT APCO AYUD BEAUTY BFIT

BH BKD BLAND BTNC CCP CI CSR CSS EFORL EPCO FE

FNS FVC GEL GLOBAL HEMRAJ IEC IFS INET JUTHA KASET KCAR

KKC KSL L&E LALIN LTX M MALEE MBK MBKET MEGA MK

MPG MTLS NCH NCL NPP OCC OCEAN PB PCA PRINC QH

ROCK RPC S & J SGP SIAM SIS SKR SMG SMIT SORKON SUSCO

TAKUNI TEAM TF TIC TIP TIPCO TMC TMI TPP TRT TRU

TRUE TSC TSI TTW TVD TVO UKEM UNIQ UWC VNG WIIK

WIN XO

Level 1 (Committed)

ACD AEONTS AFC AIRA AJ ALUCON AMC AQUA ARIP AUCT BAT‐3K

BIG BJC BOL BRR BSBM CBG CCET CCN CGD CMR CPH

CSC CSP CTW DCON DRACO DSGT DTCI E EMC ESSO FOCUS

FSMART GIFT GLAND GRAND GUNKUL HFT HTECH ILINK ITD JSP IHL

KDH KTIS KTP LEE LST MAJOR MAX M‐CHAI MDX MIDA MATCH

ML MPIC NC NEP NNCL OHTL PICO PK PL PPM NWR

PRAKIT PRECHA PRIN PSTC RAM RICH RS SANKO SAUCE SAWAD PYLON

SAWANG SCN SEAFCO SHANG SIRI SMART SMM SOLAR SPACK SPG SF

SPPT SPVI STAR SVH SVOA SWC TAPAC TC TCCC TCJ STA

TCOAT TKS TNH TNPC TPA TPAC TPOLY TRC TRUBB TSE TTA

TTI TTL TTTM TWP TWZ U UMS UPA UPOIC UVAN UTP

VARO VI VIBHA VIH VTE WG

Data not available/No policy

A ACC AJD AQ BCH BGT BROCK BSM BTC CHUO CRANE

CPR EIC FER JMART JMT KAMART KBS KIAT LDC MCS METCO

MBAX NEW NEWS NYT PAE PDG PERM PMTA RCL RICHY ROH

POST S SIMAT TCB TR TSF TVT

Page | 9 | PHILLIP SECURITIES (THAILAND)

Eastern Polymer Group INITIATION OF COVERAGE

Anti‐corruption indicators

Level 5 : Extended

Anti‐corruption policies extend to business partners, dealers, and distributors.

Level 4 : Certified

Anti‐corruption policies can be engaged by audit committee and auditors approved by the SEC.

Anti‐corruption policies are certified by CAC and independent assurance providers.

Level 3 : Established

Anti‐corruption corruption policies cover anti‐bribery, and communications and educating all employees anti‐corruption policies.

Level 3A Public out statement to join CAC, etc.

Level 3B Declare statement and organization’s anti‐corruption policies but no intention to join CAC, etc.

Level 2 : Declared

Declare statement to participate CAC against corruption.

Level 1 : Committed

Organization and Board of Directors’ statements against corruption and not getting involve in any malpractices.

Assessment

Anti‐corruption progress indicator for listed companies is a part of SEC’s commitment to create sustainability in anti‐corruption and to become a role model to any

related business. The progress indicators comprise of five levels: 1) Committed, 2) Declared, 3) Established, 4) Certified, and 5) Extended. These indicators will

encourage listed firms to formulate anti‐corruption policies to opt out of corruption, and investors can determine their investment based on anti‐corruption indicator

or avoid investment in listed firms that could get involve in corruption.

PHILLIP SECURITIESS (THAILAND) | 10 | P a g e

Eastern Polymer Group INITIATION OF COVERAGE

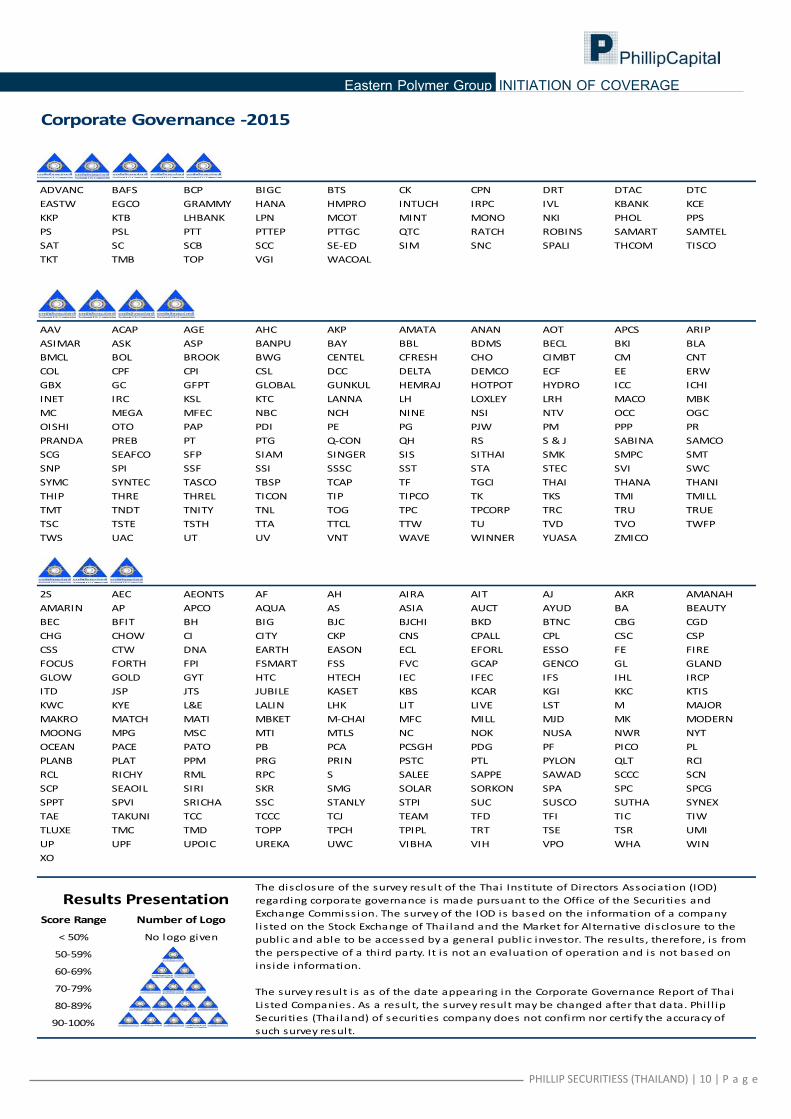

Corporate Governance ‐2015

ADVANC BAFS BCP BIGC BTS CK CPN DRT DTAC DTC

EASTW EGCO GRAMMY HANA HMPRO INTUCH IRPC IVL KBANK KCE

KKP KTB LHBANK LPN MCOT MINT MONO NKI PHOL PPS

PS PSL PTT PTTEP PTTGC QTC RATCH ROBINS SAMART SAMTEL

SAT SC SCB SCC SE‐ED SIM SNC SPALI THCOM TISCO

TKT TMB TOP VGI WACOAL

AAV ACAP AGE AHC AKP AMATA ANAN AOT APCS ARIP

ASIMAR ASK ASP BANPU BAY BBL BDMS BECL BKI BLA

BMCL BOL BROOK BWG CENTEL CFRESH CHO CIMBT CM CNT

COL CPF CPI CSL DCC DELTA DEMCO ECF EE ERW

GBX GC GFPT GLOBAL GUNKUL HEMRAJ HOTPOT HYDRO ICC ICHI

INET IRC KSL KTC LANNA LH LOXLEY LRH MACO MBK

MC MEGA MFEC NBC NCH NINE NSI NTV OCC OGC

OISHI OTO PAP PDI PE PG PJW PM PPP PR

PRANDA PREB PT PTG Q‐CON QH RS S & J SABINA SAMCO

SCG SEAFCO SFP SIAM SINGER SIS SITHAI SMK SMPC SMT

SNP SPI SSF SSI SSSC SST STA STEC SVI SWC

SYMC SYNTEC TASCO TBSP TCAP TF TGCI THAI THANA THANI

THIP THRE THREL TICON TIP TIPCO TK TKS TMI TMILL

TMT TNDT TNITY TNL TOG TPC TPCORP TRC TRU TRUE

TSC TSTE TSTH TTA TTCL TTW TU TVD TVO TWFP

TWS UAC UT UV VNT WAVE WINNER YUASA ZMICO

2S AEC AEONTS AF AH AIRA AIT AJ AKR AMANAH

AMARIN AP APCO AQUA AS ASIA AUCT AYUD BA BEAUTY

BEC BFIT BH BIG BJC BJCHI BKD BTNC CBG CGD

CHG CHOW CI CITY CKP CNS CPALL CPL CSC CSP

CSS CTW DNA EARTH EASON ECL EFORL ESSO FE FIRE

FOCUS FORTH FPI FSMART FSS FVC GCAP GENCO GL GLAND

GLOW GOLD GYT HTC HTECH IEC IFEC IFS IHL IRCP

ITD JSP JTS JUBILE KASET KBS KCAR KGI KKC KTIS

KWC KYE L&E LALIN LHK LIT LIVE LST M MAJOR

MAKRO MATCH MATI MBKET M‐CHAI MFC MILL MJD MK MODERN

MOONG MPG MSC MTI MTLS NC NOK NUSA NWR NYT

OCEAN PACE PATO PB PCA PCSGH PDG PF PICO PL

PLANB PLAT PPM PRG PRIN PSTC PTL PYLON QLT RCI

RCL RICHY RML RPC S SALEE SAPPE SAWAD SCCC SCN

SCP SEAOIL SIRI SKR SMG SOLAR SORKON SPA SPC SPCG

SPPT SPVI SRICHA SSC STANLY STPI SUC SUSCO SUTHA SYNEX

TAE TAKUNI TCC TCCC TCJ TEAM TFD TFI TIC TIW

TLUXE TMC TMD TOPP TPCH TPIPL TRT TSE TSR UMI

UP UPF UPOIC UREKA UWC VIBHA VIH VPO WHA WIN

XO

Score Range

< 50%

50‐59%

60‐69%

70‐79%

80‐89%

90‐100%

The disclosure of the survey result of the Thai Institute of Directors Association (IOD)

regarding corporate governance is made pursuant to the Office of the Securities and

Exchange Commission. The survey of the IOD is based on the information of a company

l isted on the Stock Exchange of Thailand and the Market for Alternative disclosure to the

public and able to be accessed by a general public investor. The results, therefore, is from

the perspective of a third party. It is not an evaluation of operation and is not based on

inside information.

The survey result is as of the date appearing in the Corporate Governance Report of Thai

Listed Companies. As a result, the survey result may be changed after that data. Phil l ip

Securities (Thailand) of securities company does not confirm nor certify the accuracy of

such survey result.

No logo given

Number of Logo

Results Presentation

PHILLIP SECURITIESS (THAILAND) | 11 | P a g e

Eastern Polymer Group INITIATION OF COVERAGE

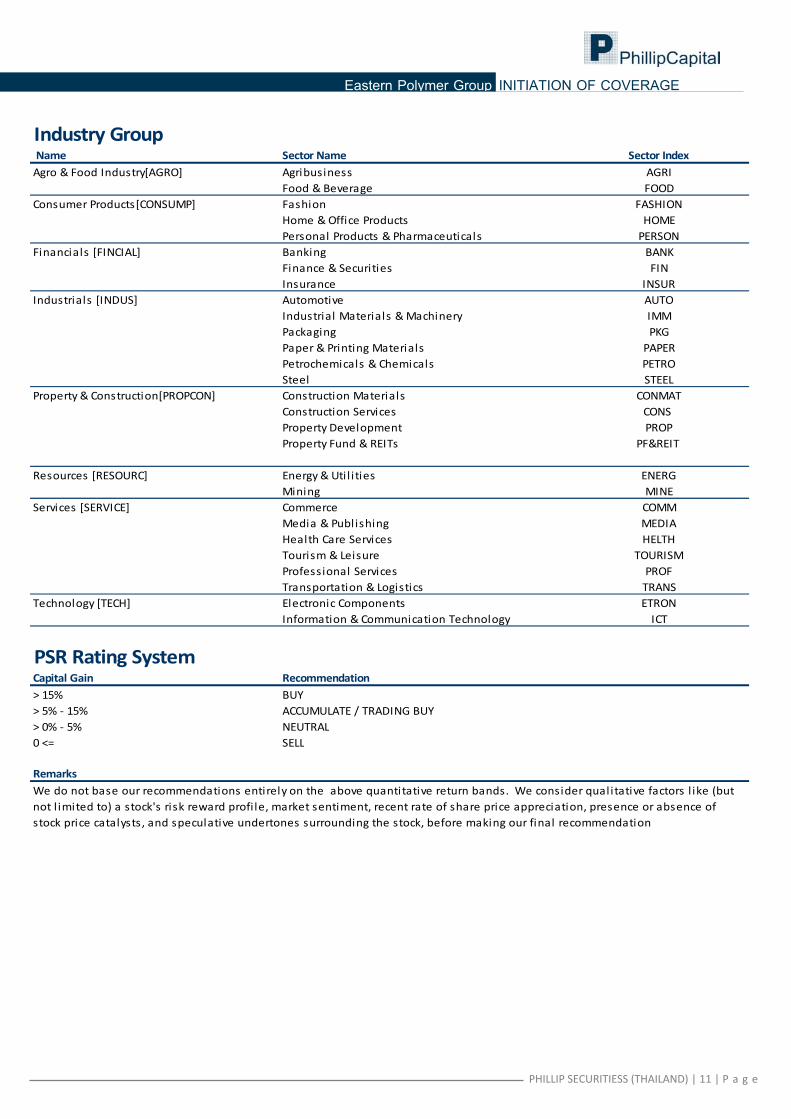

Industry Group Name Sector Name Sector Index

Agro & Food Industry[AGRO] Agribusiness AGRI

Food & Beverage FOOD

Consumer Products[CONSUMP] Fashion FASHION

Home & Office Products HOME

Personal Products & Pharmaceuticals PERSON

Financials [FINCIAL] Banking BANK

Finance & Securities FIN

Insurance INSUR

Industrials [INDUS] Automotive AUTO

Industrial Materials & Machinery IMM

Packaging PKG

Paper & Printing Materials PAPER

Petrochemicals & Chemicals PETRO

Steel STEEL

Property & Construction[PROPCON] Construction Materials CONMAT

Construction Services CONS

Property Development PROP

Property Fund & REITs PF&REIT

Resources [RESOURC] Energy & Util ities ENERG

Mining MINE

Services [SERVICE] Commerce COMM

Media & Publishing MEDIA

Health Care Services HELTH

Tourism & Leisure TOURISM

Professional Services PROF

Transportation & Logistics TRANS

Technology [TECH] Electronic Components ETRON

Information & Communication Technology ICT

PSR Rating SystemCapital Gain Recommendation

> 15% BUY

> 5% ‐ 15% ACCUMULATE / TRADING BUY

> 0% ‐ 5% NEUTRAL

0 <= SELL

Remarks

We do not base our recommendations entirely on the above quantitative return bands. We consider qualitative factors l ike (but

not l imited to) a stock's risk reward profi le, market sentiment, recent rate of share price appreciation, presence or absence of

stock price catalysts, and speculative undertones surrounding the stock, before making our final recommendation

PHILLIP SECURITIESS (THAILAND) | 12 | P a g e

Eastern Polymer Group INITIATION OF COVERAGE

Research Team Fundamental Analyst Reg No. Tel Sector Sasikorn Charoensuwan, CFA, CAIA

Capital Market Investment Analyst #9744 662 635 1700 Ext 480 Consumer, Commerce

Rutsada Tweesaengsakulthai Securities Investment Analyst #17972 662 635 1700 Ext 482 ICT, Energy, Health Care Danai Tunyaphisitchai, CFA Capital Market Investment Analyst #2375 662 635 1700 Ext 481 Construction Materials, Property Development Naree Apisawaittakan Securities Investment Analyst #17971 662 635 1700 Ext 484 Agro & Food, Electronics Siam Tiyanont Securities Investment Analyst #17970 662 635 1700 Ext 483 Transportation, Media &

Publishing Ornmongkol Tantitanatorn Capital Market Investment Analyst #34100 662 635 1700 Ext 491 Automotive, Energy,

Packaging Adisorn Muangparnchon Securities Investment Analyst #18577 662 635 1700 Ext 497 Banking, Securities &

Finance, Insurance Vichuda Siriployprakray Securities Investment Analyst #55956 662 635 1700 Ext 525 Commerce, Food &

Beverages, Tourism Hathaichanoke Moonwong Assistant Analyst

Kunanon Juntarapartsavorn Assistant Analyst

Thanatphat Suksrichavali Assistant Analyst

Strategy Teerada Charnyingyong Securities Investment Analyst #9501 662 635 1700 Ext 487 Chutikarn Santimetvirul Derivatives Investment Analyst #37928 662 635 1700 Ext 494 Werajak Jungkiatkajorn Capital Market Investment Analyst #28087 662 635 1700 Ext 495 Rittiporn Songsermsawad Securities Investment Analyst #39756 662 635 1700 Ext 527 Phoobate Wiriyayuttama Securities Investment Analyst #63404 662 635 1700 Ext 498

Technical Sasima Hattakitnikorn Securities Investment Analyst #8328 662 635 1700 Ext 490 Kanoksak Vutipan Capital Market Investment Analyst #32423 662 635 1700 Ext 485

Database & Production Manunpat Yuenyongwatanakorn Sutiporn Oupkaew Kanittha Sriwong

Translation Chaiyot Ingkhasorarat Naowarat Angurasuchon

PHILLIP SECURITIESS (THAILAND) | 13 | P a g e

Eastern Polymer Group INITIATION OF COVERAGE

Domestics OfficesBangkok Offices

Head Offi ce 15th Fl ., Vorawa t Bldg. Te l : 0 2635 1700 , 0 2268 0999

Srina ka ri ndr 17th Fl ., Modernform Tower Te l : 0 2722 8344‐53

Vipha vadi 15th Fl ., Lao Peng Nguan Tower 1 Te l : 0 2618 8400

Yaowa ra t 19th Fl ., Kanchanadha t Bldg. Te l : 0 2622 7833

Bangkapi 1 8th Fl ., The Ma l l Offi ce Tower‐Bangkapi Te l : 0 2363 3263

Bangkapi 2 9th Fl ., The Ma l l Offi ce Tower‐Bangkapi Te l : 0 2363 3269

Hua Lumphong 4th Fl ., Tang Hua Pa k Bldg., 320 Rama 4 Rd. Te l : 0 2639 1200

Rangs i t G Fl ., Room#PLZ.G.SHP065A Future Pa rk Rangs i t Te l : 0 2958 5040

Sindhorn 19th Fl ., Sindhorn Tower 3 Bui l d ing, Te l : 0 2650 9717

Si am Dis covery 11s t Floor, Uni t A2, Siam Tower,Te l : 02 658 0776

Centra lWorld Branch 999/9 The Offi ce s a t Centra lWorld, 17 FL. Uni t ML 1707, Rama 1 Rd, Pa tumwan Bangkok 10330

Provincial Offices

Cha ing Ma i 313/15 Moo6 Cha ing Ma i – Lamphun Nong Hoi , Te l 053‐141969

Khon Kaen 4th Fl ., Kow Yoo Hah Bldg.Te l : 0 4332 5044‐8

Phi s anulok 2nd Fl ., Tha i Si va ra t Bldg., Te l : 0 5524 3646

Had Ya i 4th Fl ., Southla nd Rubber Bldg., Te l : 0 7423 4095‐99110

Had Ya i ‐ Pe tka s em 3rd Fl ., Uni t 3D, Reda r Group Bldg., Te l : 0 7422 3044

La emchabang 53/112, 53/114 Moo 9, Tungsukl a , Sri ra cha , Chonburi 20230

Chumporn Inves tor Cente r 25/45 Krom Luang Chumporn Rd.,Te l : 0 7757 0652‐3

Overseas OfficesSINGAPORE Phi l l i p Securi ti e s Pte Ltd Ra ffl e s Ci ty Tower Te l : (65) 6533 6001 www.poems .com.s g

HONG KONG Phi l l i p Securi ti e s (HK) Ltd 11/F Uni ted Centre 95 Queensway, Te l (852) 22776600 www.phi l l i p .com.hk

MALAYSIA Phi l l i p Capi ta l Management Sdn Bhd, Block B Leve l 3 Megan Avenue Te l (603) 21628841 www.poems .com.my

JAPAN Phi l l i p Securi ti e s Japan, Ltd 4‐2 Nihonba shi Kabuto ‐cho, Chuo ‐ku, Tokyo Te l (81‐3) 36662101

INDONESIA PT Phi l l i p Securi ti e s Indones i a ANZ Tower Leve l 23B, Te l (62‐21) 57900800 www.phi l l i p .co.i d

CHINA Phi l l i p Financi a l Advi s ory (Shangha i ) Co. Ltd Ocean Tower Uni t 2318 Te l (86‐21) 51699200 www.phi l l i p .com.cn

FRANCE King & Sha xson Capi ta l Limi ted 3rd Fl r, 35 Rue de l a Bienfa i s ance Te l (33‐1) 45633100

UNITED KINGDOM King & Sha xson Capi ta l Limi ted 6th Fl r, Candlewi ck House , Te l (44‐20) 7426 5950 www.kingandsha xson.com

UNITED STATES Phi l l i p Futures Inc The Chi ca go Boa rd of Trade Bui l di ng Te l +1.312.356.9000

AUSTRALIA Phi l l i pCapi ta l Aus tra l i a Leve l 37, Col l i ns Stree t, Melbourne , Te l (613) 96298380 Fwww.phi l l i pca pi ta l .com.au

SRI LANKA Asha Phi l l i p Securi ti e s Ltd Leve l 4, Mi l l ennium House , Te l : (+94) 11 2429 100 aps l@ashaphi l l i p .ne t

TURKEY Hak Menkul Ki ymetl e r A.Ş Dr.Cemi l Bengü Cad. Te l : (+90) (212) 296 84 84 (pbx) a kmenkul@hakmenkul .com.tr

INDIA Phi l l i pCapi ta l (India ) Pri va te Limi ted No. 1, C‐ Block, 2nd Floor,Modern Cente r , Ja cob Ci rcl e , K. K. Marg,

Maha l a xmi Mumba i 400011 Te l : (9122) 2300 2999 Webs i te : www.phi l l i pca pi ta l .i n

DUBAI Phi l l i pCapi ta l (India ) Pvt Ltd.601, Whi te Crown Bui ld i ng Duba i UAE. Maha la xmi Mumba i 400011

Te l : (9122) 2300 2999 Webs i te : www.phi l l i pca pi ta l .i n

CAMBODIA Bui ld i ng No71, St 163, Sangka t Toul Sva y Prey I , Khan Chamka rmorn, Phnom Penh, Kingdom of Cambodia

Te l : (855) 23 217 942 Webs i te : www.kredi t.com.kh

PHILLIP SECURITIESS (THAILAND) | 14 | P a g e

Eastern Polymer Group INITIATION OF COVERAGE

Disclosures and Disclaimers This publication is prepared and issued by Phillip Securities (Thailand) PLC., which is regulated by SEC Thailand. References to "PST" in this report shall mean Phillip Securities (Thailand) PLC unless otherwise stated. By receiving or reading this report, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only. The copyright belongs exclusively to PST. All rights are reserved. Any unauthorized use or disclosure is prohibited. No reprinting or reproduction, in whole or in part, is permitted without the PST’s prior consent, except that a recipient may reprint it for internal circulation only and only if it is reprinted in its entirety. If you have received this documentation by mistake, please delete or destroy it., and notify the sender immediately. This report is prepared and distributed by PST for information purposes only and neither the information contained herein nor any opinion expressed should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment or derivatives. The information and opinions contained in the Report were considered by PST to be valid when published. The report also contains information provided to PST by third parties. The source of such information will usually be disclosed in the report. Whilst PST has taken all reasonable steps to ensure that this information is correct, PST does not offer any warranty as to the accuracy or completeness of such information. Any person placing reliance on the report to undertake trading does so entirely at his or her own risk and PST does not accept any liability as a result. Securities and Derivatives markets may be subject to rapid and unexpected price movements and past performance is not necessarily an indication to future performance. This report does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors must undertake independent analysis with their own legal, tax and financial advisors and reach their own decision regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. In no circumstances it be used or considered as an offer to sell or a solicitation of any offer to buy or sell the Securities mentioned in it. The information contained in the research reports may have been taken from trade and statistical services and other sources, which we believe are reliable. Phillip Securities (Thailand) PCL or any of its group/associate/affiliate companies do not guarantee that such information is accurate or complete and it should not be relied upon as such. Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Important: These disclosures and disclaimers must be read in conjunction with the research report of which it forms part. Receipt and use of the research report is subject to all aspects of these disclosures and disclaimers. Additional information about the issuers and securities discussed in this research report is available on request. Certifications: The research analyst(s) who prepared this research report hereby certifies that the views expressed in this research report accurately reflect the research analyst’s personal views about all of the subject issuers and/or securities, that the analyst have no known conflict of interest and no part of the research analyst’s compensation was, is or will be, directly or indirectly, related to the specific views or recommendations contained in this research report. Phillip Securities (Thailand) PCL, or persons associated with or connected to PST, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Thailand and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. PST, or persons associated with or connected to PST, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business from such issuers. Additionally, PST, or persons associated with or connected to PST, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments as may be mentioned in this publication.

PHILLIP SECURITIESS (THAILAND) | 15 | P a g e

Eastern Polymer Group INITIATION OF COVERAGE

PST or persons associated with or connected to PST, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment. To the extent permitted by law, PST, or persons associated with or connected to PST, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments which may be mentioned in this publication. Accordingly, information may be available to PST, or persons associated with or connected to PST, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and PST, or persons associated with or connected to PST, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. PST, or persons associated with or connected to PST, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material. Suitability and Risks: This research report is for informational purposes only and is not tailored to the specific investment objectives, financial situation or particular requirements of any individual recipient hereof. Certain securities may give rise to substantial risks and may not be suitable for certain investors. Each investor must make its own determination as to the appropriateness of any securities referred to in this research report based upon the legal, tax and accounting considerations applicable to such investor and its own investment objectives or strategy, its financial situation and its investing experience. The value of any security may be positively or adversely affected by changes in foreign exchange or interest rates, as well as by other financial, economic or political factors. Past performance is not necessarily indicative of future performance or results. Sources, Completeness and Accuracy: The material herein is based upon information obtained from sources that PST and the research analyst believe to be reliable, but neither PST nor the research analyst represents or guarantees that the information contained herein is accurate or complete and it should not be relied upon as such. Opinions expressed herein are current opinions as of the date appearing on this material and are subject to change without notice. Furthermore, PST is under no obligation to update or keep the information current. Caution: Risk of loss in trading in can be substantial. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances. For U.S. persons only: This research report is a product of Phillip Securities (Thailand) PCL which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker‐dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker‐dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account. This report is intended for distribution by Phillip Securities (Thailand ) PCL only to "Major Institutional Investors" as defined by Rule 15a‐6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor. Phillip Securities (Thailand) PCL Registered office: 15/F, Vorawat Building, 849 Silom Road, Bangrak, Bangkok 10500 Thailand

Related Documents