Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TEXTILE INDUSTRY

Represented by,

Jayesh Patil

Akshay Dayma

Omkar Barge

Nishad Karambelkar

Dnyaneshwar Aru

Pooja Pawar

Harita Buddhadev

“ENTREPRENEURS”

NATURE OF INDUSTRY

The Textile industry in India traditionally, after agriculture, is the

only industry that has generated huge employment for both skilled

and unskilled labour in textiles. The textile industry continues to

be the second largest employment generating sector in India. It

offers direct employment to over 35 million in the country.

The textile industry or apparel industry is primarily concerned

with the production of yarn, and cloth and the subsequent design

or manufacture of clothing and their distribution. The raw material

may be natural, or synthetic using products of the chemical

industry.

NATURE OF COMPETITION

TOTAL VALUE OF MARKET 20,000 CR

• Branded Market

• 5000Cr :value of apparel Market .

Organized Market

• Non Branded Market

• 15000Cr: value of apparel Market.

Unorganized Market

PLAYERS IN THE INDUSTRY

Leaders:ARVIND MILLS

BOMBAY DYEING

VARDHMAN GROUP OF COMPANIES

Challengers:

RAYMOND

GRASIM INDUSTRIES

Followers:FABINDIA

RELIANCE INDUSTRY

Nichers:

MYSORE SILK (KSIC)

LAKSHMI MILLS

JCT LIMITED

STRATEGIES FOLLOWED

By Market Leaders:

1.

Focuses on jeans, as Arvind is a worlds 3rd

largest jeans manufacturers, Creating youth

oriented brand.

2.

“PQSDM” strategy adopted. Selling in maximum

volumes.

STRATEGIES FOLLOWED

By Leaders:

3.

Focuses on retail selling & online selling.

Apparels as well as durable clothing.

By Challengers:

1.

Bringing a new brands covering all segments

of

apparel. Premium Indian brands.

STRATEGY FOLLOWED

By Challengers:

2.

Active in tire 2 cities. Created a premium brand

Value. Retail outlets in large numbers.

By Followers:

1.

Ethnic wear specialization, online branding.

Mainly focuses on upper class people.

STRATEGY FOLLOWED

By Followers:

2.

Works only one iconic brand.

By Nichers :

1.

Has existence since 1910. Focuses on

providing

raw material textile yarn.

STRATEGIES FOLLOWED

By Nichers:

2.

Produces Mulberry silk. 70% production of

Mulberry silk is produced by Mysore Silk.

3.

Presence since 1946, Has lot of low cost brands.

Spread over the rural areas.

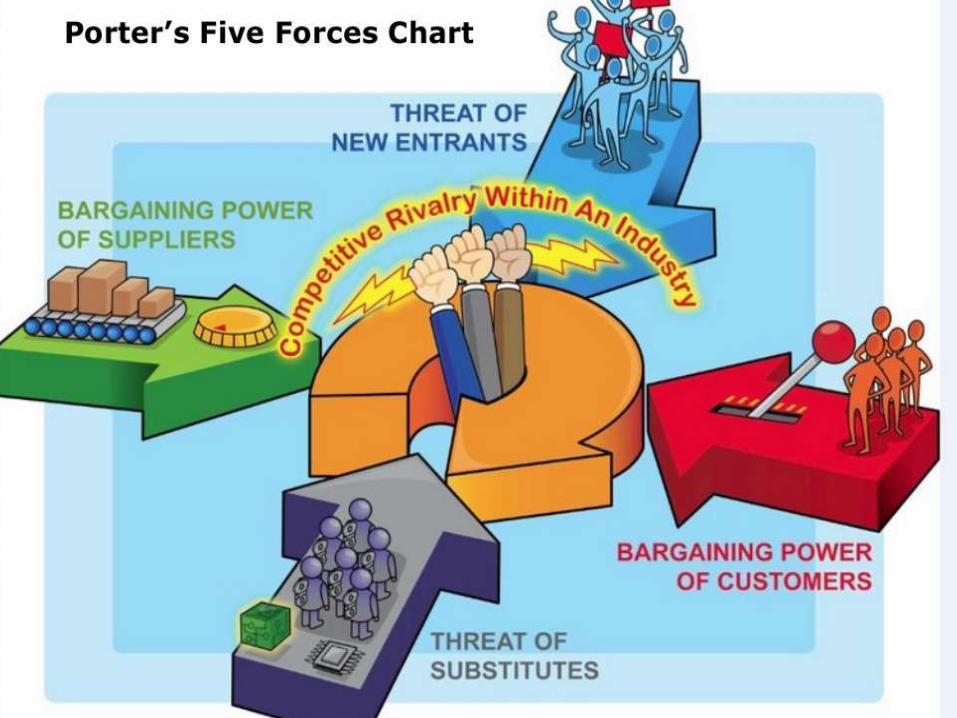

BARGAINING POWER OF BUYER

High demand of appeals and home textiles in

the US and EU market.

India, in particular, is likely to benefit from the

rising demand in the home textiles and apparels

segment, wherein it has competitive edge

against its neighbor. Nonetheless, a rapid

slowdown in the denim cycle poses risks to

fabric players.

The two-fold increase in global textile trade is

also likely to drive India's exports growth.

BARGAINING POWER OF SUPPLIER

High availability of cotton and low labor cost,.

India is the third largest producer of cotton in

the world after China and US and has the

largest area under cultivation.

India has an abundant supply of locally

grown long staple cotton, which lends it a

cost advantage in the home textile and

apparels segments.

THREAT FROM NEW ENTRANCE

No barrier in the domestic market, New

capacities coming up.

smaller players who cannot venture into the

global markets are flooding the domestic

markets with excess supply, thus weakening

the pricing scenario.

In the quota free regime, capacity expansion

is the name of the game in the textile sector.

THREAT OF SUBSTITUTES

Competition from low cost producing nations

like Pakistan and Bangladesh.

Low cost producing countries like Pakistan and

Bangladesh (labour cost 50% cheaper) are also

posing a threat to India's exports demand.

Infact, players like Arvind Mills have already

started feeling the pinch as overseas buyers

have started shifting to 'alternative sources',

thus impacting their incremental volume off-

takes.

COMPETITIVE RIVALRY

Quota free regime competition from China.

India's logistic disadvantage due to its geographical location can give it a major thumbs-down in global trade.

The country is distant from major markets as compared to its global competitors like Mexico, Turkey and China, which are located in relatively close vicinity to major global markets of US, Europe and Japan.

POSITIONING STRATEGY

Arvind Textiles:

Present in most of the segments of the market.

With an array of international brands like Lee,

Arrow, Tommy Hilfiger, Wrangler and domestic

brands like Newport, Flying Machine, Ruf n Tuf.

Bombay Dyeing:

It has over 500+ local and international brands. They

sell the product online as well as offline.

They have tied up with Jabong, price panda etc. They have

also got award about offering best product at best price to

the customer.

POSITIONNG STRATEGY

Vardhman:

VTL and its subsidiaries have 20 manufacturing

facilities across India and employ ~25,000

People.

VTL is a market leader in its various product

Offerings.

VTL has forged global alliances with leading textile

companies such as American & Efird (A&E) Inc USA,

Marubeni & Toho Rayon, Japan and Nisshinbo,

Japan.

Related Documents