Texas Bank Report Texas Department of Banking, Charles G. Cooper, Commissioner December 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Texas Bank ReportTexas Department of Banking, Charles G. Cooper, Commissioner December 2016

2 Texas Bank Report December 2016

Commissioner’s Comments

I am happy to report that the Department successful-ly performed its functions and fulfilled its statutory mandates for fiscal year 2016. These accomplish-

ments are due to our dedicated staff and the support of our regulated industries that want and deserve to be regulated in a professional manner. We continue to embrace the “Tough but Fair” motto.

The financial highlights on the last two pages of this report indicate that our state banks are performing reasonably well. Loans in the energy sector have come under stress, but generally our banks are adequately responding to this adversity. This continues to remind me of the importance of the “M” in the CAMELS rating system.

We will continue to work with you in the fight for “right-sized” regulation and work toward a more stan-dardized state regulatory approach in the non-deposito-ry area.

On a more personal note, the Department experienced the tragic loss of longtime examiner and friend, Dennis W. Lebo. We highlight his distinguished career in this report.

As we close out the year, I am grateful to all of those who contributed to our success and look forward to the opportunities 2017 will bring.

Charles G. CooperBanking Commissioner

December 2016 www.dob.texas.gov 3

In this issue we celebrate and remember the career of Dennis W. Lebo, who suddenly passed away in his home at the age of 66. Dennis was one of our longtime examiners, and we are deeply saddened that he is no longer with us. We had the fortune of working with him for over 43 years, and he was an integral part of the

Department of Banking.

Dennis began his career at the Department on October 1, 1973. Like most field examiners, he started off as an assistant examiner and was stationed in the Abilene district. In the twelve years that followed, Dennis advanced his career and earned his commission in September of 1976. Dennis successfully ran the Abilene district, and earned a promotion to Senior Examiner in Dallas in 1979. One year later he was promoted again to Assistant Departmental Examiner and was stationed in his hometown of Austin, and the Department’s headquarters.

In the 1980’s, the state of Texas had a banking crisis with over 500 bank failures. Dennis pro-vided experienced and effective leadership during this tumultuous period. After the banking crisis subsided, he spent most of his career in Austin. It was here that Dennis discovered his greatest skill, teaching and training assistants in the field of credit analysis. This was a talent he shared with many of his colleagues.

Dennis W. Lebo made meaningful connections with the people he worked with. We will miss his excellent sense of humor, which is recalled in the story below by one of his longtime coworkers:

“My first encounter with Dennis was when I processed travel vouchers for the Department, over 20 years ago. The State was fierce about having proof of payment attached to the voucher, which meant you better have all your receipts. Well, Dennis lost his airline ticket. So of course, he did the next best thing, he drew a picture of it on his voucher. I laughed till I cried, and we’ve been buddies ever since…things just won’t be the same without him.”

He was a man who never met a stranger. On many occasions he would call a banker for the first time, and they would be laughing and talking about cars only a few minutes into the conversation.

Commissioner Cooper remembers Dennis as, “a valued Department of Banking employee, whose tenure with the agency left a positive impact on those who had the opportunity to work with him.” He truly enjoyed his most recent responsibility as a fraud investigator. Dennis will always be a Department of Banking icon and remembered as a loyal coworker, respected mentor, and good friend; he will be missed.

By Chris Robinson

In Memoriam - a Tribute toMr. Dennis W. Lebo

4 Texas Bank Report December 2016

By Dianne Dennis

On May 11, 2016, the Financial Crimes Enforcement Network (FinCEN) issued its long-awaited “Customer Due Diligence Requirements for Financial Institutions”

rules under the Bank Secrecy Act (BSA). The final rule be-came effective on July 11, 2016, but financial institutions have until May 11, 2018 to comply with the regulations. This rule imposes four core elements of customer due diligence (CDD) that FinCEN believes should be explicit requirements in a bank’s Anti-Money Laundering (AML) program and creates a fifth pillar of the AML compliance program. These four CDD elements are:

1) Customer identification and verification;

2) Beneficial ownership identification and verification;

3) Understanding the nature and purpose of customer relationships to develop a customer risk profile; and

4) Ongoing monitoring for reporting suspicious transac-tions and, on a risk-basis, maintaining and updating information on beneficial owners.

The first element, customer identification and verification, is already an AML program requirement. The second element, beneficial ownership, is a new regulatory requirement. The third and fourth elements are currently implicit requirements, but are now explicitly required.

Beneficial Ownership - Definitions

Beneficial owners are defined by the regulation as each individ-ual who owns, directly or indirectly, 25% or more of the equity interest of the legal entity and one individual with significant responsibility to control, manage, or direct the entity. A legal entity includes a corporation, a limited liability company, or other entity that is created by filing a public document with a Secretary of State or similar office, a general partnership, and any similar business entity formed in the United States or a foreign jurisdiction.

Beginning May 11, 2018 (or what is referred to as the appli-cability date), financial institutions will be required to identify and verify the beneficial owners of legal entity customers when an account is opened. The rule does not cover existing ac-counts that were opened before the applicability date. Financial institutions will be required to establish and maintain written procedures that identify and verify the beneficial owners of legal entity customers and include the procedures in their AML compliance program.

Compliance

The financial institution may comply with the beneficial ownership regulation by completing the form in Appendix A of the Federal Register, Vol. 81, No. 91, Certification Regarding Beneficial Owners of Legal Entity Customers, Section 1010.230.

FinCEN Issues Final Customer Due Diligence Requirements for Financial Institutions

December 2016 www.dob.texas.gov 5

For any exemptions, please refer to the Federal Register, Vol. 81, No. 91.

AML Program Requirements

The third and fourth elements amend the AML program require-ments for financial institutions by explicitly requiring the insti-tution to establish risk-based procedures for conducting ongoing CDD, and to include understanding customer relationships for the purpose of developing a customer risk profile. The customer risk profile is used to develop a baseline against which custom-er activity is assessed for suspicious activity reporting. This may include information such as the type of account, type of customer, and products and services used.

Depending upon the risk, banks will be required to maintain and update customer information if, during the course of its normal monitoring, the bank detects a change in beneficial ownership information. The provision does not impose a categorical require-ment for institutions to update the customer information on a continuous or periodic basis, but rather updating is event driven and a part of normal monitoring.

The new regulation adds a fifth pillar to the AML compliance program. Financial institutions will be required to implement and maintain an AML program that minimally includes:

1) Developing a system of internal controls to assure on-go-ing compliance;

2) Independent testing for compliance by bank personnel or by an outside party;

3) Designating an individual(s) responsible for coordinating and monitoring day-to-day compliance;

4) Training appropriate personnel; and

5) Creating risk-based procedures for conducting ongoing customer due diligence, to include (but not limited to):

(i) Understanding the nature and purpose of customer relationships to develop a customer risk profile; and

(ii) Conducting ongoing monitoring to identify and report suspicious transac-tions and, on a risk basis, to maintain and update customer information.

Finally, FinCEN believes that clarifying and strengthening CDD and beneficial ownership requirements for financial institutions, advances the purpose of the BSA by assisting law enforcement on financial investigations. Law enforcement will now have more access to account information of illicit groups such as terrorist organizations, drug dealers, and money launderers. These rules will be helpful for financial institutions as well, by alleviating risks and giving further compliance with the BSA and cooperation with the Foreign Account Tax Compliance Act (FACTA). Any CDD regulatory expectations will become more consistent across sectors, and will enhance transparency of legal entities.

Sources:

The Federal Register. Volume 81. No. 91. May 11, 2016

Treasury Department Bank Secrecy Act Regulation. 31 C.F.R. Section 1010.230

6 Texas Bank Report December 2016

By Zainub Naeem

2017 is right around the corner, and with it will come a new perspective in the banking industry. As we

move further into the digital age, we must improve our meth-ods to adapt and embrace changes in technology. This fluidity will give us the edge to combat security threats, and allow us to improve organization and communication across the banking industry.

In 2014, the Department (DOB) launched the Data Exchange Portal (DEX), which allowed our regulated entities to upload correspondence to a secure portal on the Department’s website. DEX is a secure space for regulated entities and regulators to share information and documentation with the DOB. Secure data sharing is an ongoing issue in the banking and bank regu-lation industries. The sensitive subject matter that bankers and regulators handle leaves us with the challenge of finding secure, yet easy to use digital data sharing platforms. Furthermore, the Department aspires to leverage technology to improve efficien-cy, work flow, and eliminate any disruptions resulting from general website maintenance. One solution to improving this important tool was to remodel DEX with additional security features.

The DOB will be launching the newest version of DEX in the spring of 2017. The restructured DEX 2.0 program is designed to improve security, organization and communication. Entities and their representatives will continue to access this portal through the DOB’s external website. With the relaunch of DEX this spring, data sharing between banks and regulators will be considerably improved. DEX 2.0 will continue to be backed-up by a secure server that is owned and operated by the DOB. This server will have additional security enhancements, making DEX 2.0 an even safer place to share information.

Entities and their representatives will have different levels of secure access, as determined by the entities Authorized Contact and Email System (ACES) administrator. Folders and individ-ual files will contain privacy settings, and users will be able to simply drag and drop documents into a folder when uploading. One unique feature is that users can subscribe to a folder or specific file, and they will be emailed if anything changes, like when a document is uploaded. Users will also have the option to be notified when a new folder is created, allowing you to receive the latest updates.

DEX is crucial as we improve effective communication chan-nels with our federal counterparts. This platform will give us a secure space to share information, without compromising usability. We look forward to DEX’s launch this spring, and are confident that it will make a significant positive impact on banks and regulators.

Future of DEX 2.0

December 2016 www.dob.texas.gov 7

Bankers are constantly aspiring to develop innovative products and services, looking for opportunities to connect with customers, and are researching and learning about new laws and regulations. Regis-tering for quarterly webinars hosted by the Department of Banking that cover a variety of topics to promote financial education and best practices can be a helpful resource.

The webinars have numerous benefits to those in the banking industry. These one-hour events are scheduled online, and can be viewed in the comfort of your home or office. Each is free of charge, everyone is welcome to participate, and they allow the department to reach remote communities in the rural areas of Texas.

Past topics include: Cybersecurity for Money Services Business-es, Navigate Curriculum by the Federal Reserve Bank of Dallas, Children’s Savings Accounts, and Volunteer Income Tax Assistance (VITA) by the Internal Revenue Service.

The Department has a dedicated financial education web page that lists webinar opportunities. The Department’s financial education brochure is available to download and summarizes what bankers can do to be proactive in their communities. The Department encourag-es bankers and champions interested in financial literacy to contact the Financial Education Coordinator, Ms. Leilani Lim-Villegas to

subscribe to the mailing list. Every quarter, a webinar invitation with registration details is sent to state-chartered bank presidents and CEOs, in addition to the mailing subscription list.

From time to time, notices on statewide training opportunities, news, and current events are shared with mailing list subscribers. For more information on financial education in Texas, visit the Department’s financial education section of the website or email our Financial Education Coordinator.

By Leilani Lim-Villegas

Quarterly Financial Education

Webinar Subscriptions

8 Texas Bank Report December 2016

Quarterly Balance Sheet and Operating Performance Ratios for Texas State-Chartered Commercial Banks 9/30/16 Through 9/30/15

ACCOUNT DESCRIPTIONS(IN MILLIONS OF $) 9/30/16 6/30/16 3/31/16 12/31/15 9/30/15

Number of State-Chartered Banks 245 249 250 252 256Total Assets of State-Chartered Banks 254,637 248,535 244,188 246,960 244,320Number of Out-of-State, State-Chartered Banks Operating in Texas 31 28 28 28 28Total Texas Assets of Out-of-State, State-Chartered Banks Operating in Texas 62,492 57,340 57,340 57,340 57,340 Subtotal 317,129 305,875 301,528 304,300 301,660Less: Out-of-State Branch Assets/Deposits -50,569 -52,259 -52,259 -52,259 -52,259 **Total State Banks Operating in Texas 266,560 253,616 249,269 252,041 249,401

BALANCE SHEET (Tx. State-Chartered Banks)Interest-Bearing Balances 18,261 13,003 13,273 16,084 17,109Federal Funds Sold 575 685 657 646 662Trading Accounts 435 516 488 421 505Securities Held-To-Maturity 16,972 17,486 17,846 18,497 18,366Securities Available-for-Sale 46,051 45,807 45,199 45,253 43,547 Total Securities 63,023 63,293 63,045 63,750 61,913Total Loans 152,565 151,589 148,063 146,617 144,988 Total Earning Assets 234,424 228,570 225,038 227,097 224,672Premises and Fixed Assets 3,894 3,897 3,898 3,911 3,891 Total Assets 254,637 248,535 244,185 246,933 244,321Demand Deposits 29,918 27,671 26,559 30,923 27,347MMDAs 115,619 112,762 114,720 112,777 112,703Other Savings Deposits 21,324 20,646 20,469 20,117 19,648Total Time Deposits 31,524 31,674 31,370 31,441 32,893Brokered Deposits 3,390 3,315 3,093 3,077 3,086 Total Deposits 206,912 201,159 201,703 204,350 201,558Federal Funds Purchased 2,854 3,792 2,703 3,025 2,898Other Borrowed Funds 10,751 10,637 6,788 7,350 7,324 Total Liabilities 224,886 219,204 215,628 218,800 216,086Total Equity Capital 29,751 29,331 28,557 28,133 28,235Loan Valuation Reserves 1,882 1,871 1,861 1,717 1,659 Total Primary Capital 31,633 31,202 30,418 29,850 29,894Past Due Loans > 90 Days 214 207 166 153 127Total Nonaccrual Loans 1,246 1,161 1,357 938 952Total Other Real Estate 346 360 352 336 376Total Charge-Offs 383 294 138 347 207Total Recoveries 102 65 40 128 87 Net Charge-Offs 281 229 98 219 120

INCOME STATEMENTTotal Interest Income 6,073 4,028 2,004 7,708 5,794Total Interest Expense 434 283 138 508 387 Net Interest Income 5,639 3,745 1,866 7,200 5,407Total Noninterest Income 2,489 1,627 782 3,150 2,390Loan Provisions 452 388 246 395 222Salary and Employee Benefits 2,851 1,887 932 3,684 2,773Premises and Fixed Assets Expenses (Net) 607 401 198 799 600All Other Noninterest Expenses 1,725 1,141 547 2,118 1,587 Total Overhead Expenses 5,183 3,429 1,677 6,601 4,960Securities Gains (Losses) 45 33 22 19 20Net Extraordinary Items 2 4 2 0 0 Net Income 1,925 1,210 573 2,521 1,958Cash Dividends 1,143 784 497 1,381 972

RATIO ANALYSISLoan/Deposit 73.73% 75.36% 73.41% 71.75% 71.93%Securities/Total Assets 24.75% 25.47% 25.82% 25.82% 25.34%Total Loans/Total Assets 59.91% 60.99% 60.64% 59.38% 59.34%Loan Provisions/Total Loans 0.39% 0.51% 0.66% 0.27% 0.20%LVR/Total Loans 1.23% 1.23% 1.26% 1.17% 1.14%Net Charge-Offs/Total Loans 0.18% 0.15% 0.07% 0.15% 0.08%Nonperforming+ORE/Total Assets 0.71% 0.70% 0.77% 0.58% 0.60%Nonperforming+ORE/Primary Capital 5.71% 5.54% 6.16% 4.78% 4.87%Net Interest Margin 3.20% 3.28% 3.32% 3.17% 3.20%Gross Yield 4.47% 4.55% 4.56% 4.40% 4.46%Return on Assets 1.01% 0.97% 0.94% 1.02% 1.07%Return on Equity 8.61% 8.25% 8.03% 8.96% 9.22%Overhead Exp/TA 2.71% 2.76% 2.75% 2.67% 2.70%Equity/Total Assets 11.68% 11.80% 11.69% 11.39% 11.56%Primary Capital/Total Assets+LVR 12.33% 12.46% 12.36% 12.00% 12.15%*Unrealized gains/losses are already included in equity capital figures.**Total State Banks Operating in Texas includes branches of out-of-state, state-chartered banks.Data was derived from the FDIC website.

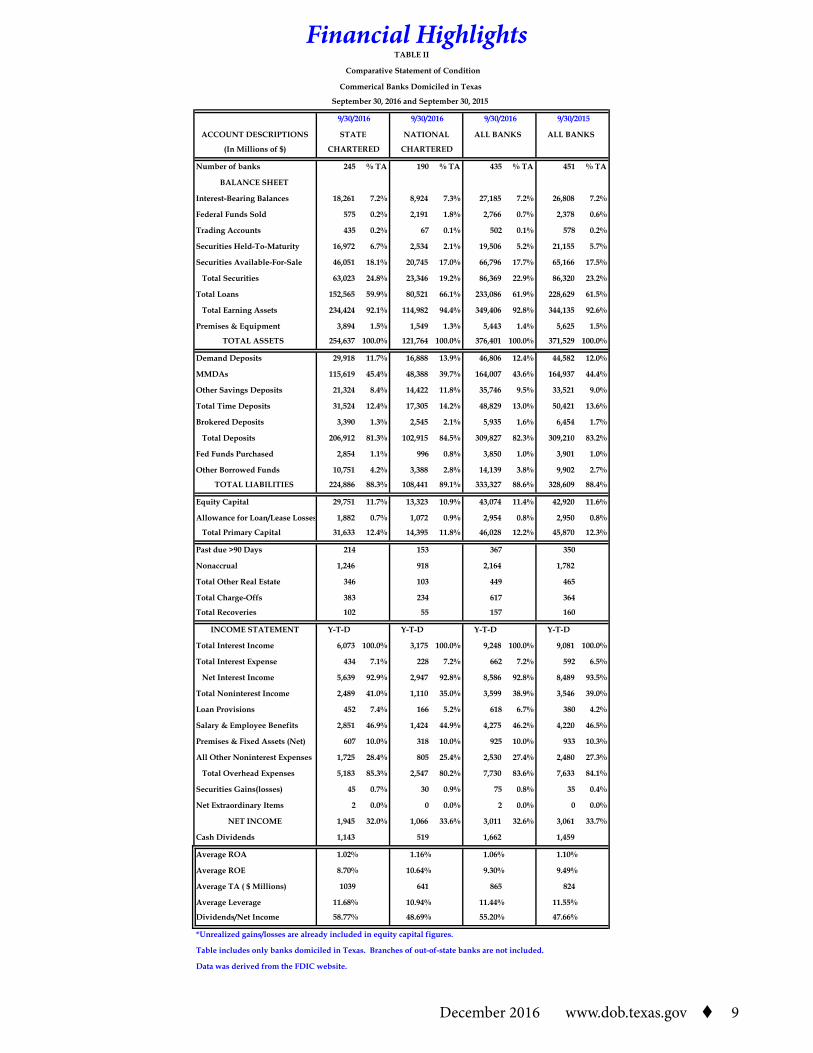

TABLE I

Financial Highlights

December 2016 www.dob.texas.gov 9

ACCOUNT DESCRIPTIONS

(In Millions of $)

Number of banks 245 % TA 190 % TA 435 % TA 451 % TA

BALANCE SHEET

Interest-Bearing Balances 18,261 7.2% 8,924 7.3% 27,185 7.2% 26,808 7.2%

Federal Funds Sold 575 0.2% 2,191 1.8% 2,766 0.7% 2,378 0.6%

Trading Accounts 435 0.2% 67 0.1% 502 0.1% 578 0.2%

Securities Held-To-Maturity 16,972 6.7% 2,534 2.1% 19,506 5.2% 21,155 5.7%

Securities Available-For-Sale 46,051 18.1% 20,745 17.0% 66,796 17.7% 65,166 17.5%

Total Securities 63,023 24.8% 23,346 19.2% 86,369 22.9% 86,320 23.2%

Total Loans 152,565 59.9% 80,521 66.1% 233,086 61.9% 228,629 61.5%

Total Earning Assets 234,424 92.1% 114,982 94.4% 349,406 92.8% 344,135 92.6%

Premises & Equipment 3,894 1.5% 1,549 1.3% 5,443 1.4% 5,625 1.5%

TOTAL ASSETS 254,637 100.0% 121,764 100.0% 376,401 100.0% 371,529 100.0%

Demand Deposits 29,918 11.7% 16,888 13.9% 46,806 12.4% 44,582 12.0%

MMDAs 115,619 45.4% 48,388 39.7% 164,007 43.6% 164,937 44.4%

Other Savings Deposits 21,324 8.4% 14,422 11.8% 35,746 9.5% 33,521 9.0%

Total Time Deposits 31,524 12.4% 17,305 14.2% 48,829 13.0% 50,421 13.6%

Brokered Deposits 3,390 1.3% 2,545 2.1% 5,935 1.6% 6,454 1.7%

Total Deposits 206,912 81.3% 102,915 84.5% 309,827 82.3% 309,210 83.2%

Fed Funds Purchased 2,854 1.1% 996 0.8% 3,850 1.0% 3,901 1.0%

Other Borrowed Funds 10,751 4.2% 3,388 2.8% 14,139 3.8% 9,902 2.7%

TOTAL LIABILITIES 224,886 88.3% 108,441 89.1% 333,327 88.6% 328,609 88.4%

Equity Capital 29,751 11.7% 13,323 10.9% 43,074 11.4% 42,920 11.6%

Allowance for Loan/Lease Losses 1,882 0.7% 1,072 0.9% 2,954 0.8% 2,950 0.8%

Total Primary Capital 31,633 12.4% 14,395 11.8% 46,028 12.2% 45,870 12.3%

Past due >90 Days 214 153 367 350

Nonaccrual 1,246 918 2,164 1,782

Total Other Real Estate 346 103 449 465

Total Charge-Offs 383 234 617 364

Total Recoveries 102 55 157 160

INCOME STATEMENT Y-T-D Y-T-D Y-T-D Y-T-D

Total Interest Income 6,073 100.0% 3,175 100.0% 9,248 100.0% 9,081 100.0%

Total Interest Expense 434 7.1% 228 7.2% 662 7.2% 592 6.5%

Net Interest Income 5,639 92.9% 2,947 92.8% 8,586 92.8% 8,489 93.5%

Total Noninterest Income 2,489 41.0% 1,110 35.0% 3,599 38.9% 3,546 39.0%

Loan Provisions 452 7.4% 166 5.2% 618 6.7% 380 4.2%

Salary & Employee Benefits 2,851 46.9% 1,424 44.9% 4,275 46.2% 4,220 46.5%

Premises & Fixed Assets (Net) 607 10.0% 318 10.0% 925 10.0% 933 10.3%

All Other Noninterest Expenses 1,725 28.4% 805 25.4% 2,530 27.4% 2,480 27.3%

Total Overhead Expenses 5,183 85.3% 2,547 80.2% 7,730 83.6% 7,633 84.1%

Securities Gains(losses) 45 0.7% 30 0.9% 75 0.8% 35 0.4%

Net Extraordinary Items 2 0.0% 0 0.0% 2 0.0% 0 0.0%

NET INCOME 1,945 32.0% 1,066 33.6% 3,011 32.6% 3,061 33.7%

Cash Dividends 1,143 519 1,662 1,459

Average ROA 1.02% 1.16% 1.06% 1.10%

Average ROE 8.70% 10.64% 9.30% 9.49%

Average TA ( $ Millions) 1039 641 865 824

Average Leverage 11.68% 10.94% 11.44% 11.55%

Dividends/Net Income 58.77% 48.69% 55.20% 47.66%

*Unrealized gains/losses are already included in equity capital figures.

Table includes only banks domiciled in Texas. Branches of out-of-state banks are not included.

Data was derived from the FDIC website.

9/30/2016 9/30/2015

ALL BANKS ALL BANKS

TABLE II

September 30, 2016 and September 30, 2015

STATE

CHARTERED

NATIONAL

CHARTERED

Comparative Statement of Condition

Commerical Banks Domiciled in Texas

9/30/2016 9/30/2016

Financial Highlights

Related Documents