CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS Page 1 Q1. Mr. RAVI is a citizen of Australia and has been staying in India since 1/1/2014. He leaves India on 16/7/2020 to visit Australia and returns on 4/1/2021. Determine his residential status for the AY 2021- 2022 i.e. PY 2020-2021 (a) Resident and ordinary resident (b) Resident and not ordinary resident (c) Non resident (d) Person of Indian origin Q2. HUF is situated in Delhi whose Karta is Mr. Vikas has been in India since 1/1/2016 and before that he was in UK. Mr. Vikas takes all decisions regarding the working of HUF in India. Determine residential status of HUF for the AY 2021-2022 i.e. PY 2020-2021. (a) Resident and not ordinary resident (b) Resident and ordinary resident (c) Indian citizen (d) None of the above Q3. HUF is situated in Mumbai. Its karta is Mr. Aman who is of 95 years of age has delegated power to his eldest son Mr. Yogesh. Mr. Aman is in USA for his medical treatment and left India for the first time on 18/9/2019. Mr. Yogesh has full controls over affairs of HUF. Mr. Yogesh excises partial control from India and partially from Nepal. Calculate residential status of HUF and Karta Mr. Aman for the AY 2021-2022 i.e. PY 2020-2021— (a) HUF is resident, Mr. Aman is non resident (b) HUF is non-resident, Mr. Aman is non resident (c) HUF is resident and ordinary resident, Mr. Aman is non resident (d) HUF is resident and ordinary resident, Mr. Aman is resident and ordinary resident Q4. Reliance limited is a company incorporated in India and which has its registered office in Mumbai. For the AY 2020-2021 i.e. PY 2019-2020 its Place of Effective Management is in Nepal. Determine its residential status for the AY 2021-2022 i.e. PY 2020-2021. (a) Non Resident (b) Resident and ordinary resident (c) Resident and not ordinary resident TEST 2 - RESIDENTIAL STATUS & TAX INCIDENCE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 1

Q1. Mr. RAVI is a citizen of Australia and has been staying in India since 1/1/2014. He

leaves India on 16/7/2020 to visit Australia and returns on 4/1/2021. Determine his

residential status for the AY 2021- 2022 i.e. PY 2020-2021

(a) Resident and ordinary resident

(b) Resident and not ordinary resident

(c) Non resident

(d) Person of Indian origin

Q2. HUF is situated in Delhi whose Karta is Mr. Vikas has been in India since 1/1/2016 and

before that he was in UK. Mr. Vikas takes all decisions regarding the working of

HUF in India. Determine residential status of HUF for the AY 2021-2022 i.e. PY

2020-2021.

(a) Resident and not ordinary resident

(b) Resident and ordinary resident

(c) Indian citizen

(d) None of the above

Q3. HUF is situated in Mumbai. Its karta is Mr. Aman who is of 95 years of age has

delegated power to his eldest son Mr. Yogesh. Mr. Aman is in USA for his medical

treatment and left India for the first time on 18/9/2019. Mr. Yogesh has full

controls over affairs of HUF. Mr. Yogesh excises partial control from India and

partially from Nepal. Calculate residential status of HUF and Karta Mr. Aman for

the AY 2021-2022 i.e. PY 2020-2021—

(a) HUF is resident, Mr. Aman is non resident

(b) HUF is non-resident, Mr. Aman is non resident

(c) HUF is resident and ordinary resident, Mr. Aman is non resident

(d) HUF is resident and ordinary resident, Mr. Aman is resident and ordinary resident

Q4. Reliance limited is a company incorporated in India and which has its registered office

in Mumbai. For the AY 2020-2021 i.e. PY 2019-2020 its Place of Effective

Management is in Nepal. Determine its residential status for the AY 2021-2022 i.e.

PY 2020-2021.

(a) Non Resident

(b) Resident and ordinary resident

(c) Resident and not ordinary resident

TEST 2 - RESIDENTIAL STATUS & TAX INCIDENCE

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 2

(d) Resident of India

Q5. If Anirudh has stayed in India in the AY 2021- 2022 i.e. PY 2020-2021 for 181

days, and he is nonresident in 9 out of 10 years immediately preceding the current previous

year and he has stayed in India for 365 days in all in the 4 years immediately preceding

the current previous year and 420 days in all in the 7 years immediately preceding the

current previous year, his residential status for the AY 2021- 2022 i.e. PY 2020-2021

would be—

(a) Resident and ordinarily resident

(b) Resident but not ordinarily resident

(c) Non-resident

(d) Cannot be ascertained with the given information

Q6. Raman was employed in Hindustan Lever Ltd. He received a salary of Rs. 40,000pm

from 1/4/2020 to 27/9/2020. He resigned and left for Dubai for the first time on

1/10/2020 and got salary of rupee equivalent of Rs. 80,000pm from 1/10/2020 to

31/3/2021. His salary for October to December 2020 was credited in his Dubai bank

account and the salary for January to March 2021 was credited in his Bombay

account directly. He is liable to tax in respect of—

(a) Income received in India from Hindustan Lever Ltd;

(b) Income received in India and in Dubai;

(c) Income received in India from Hindustan Lever Ltd. and income directly credited in India;

(d) Income received in Dubai

Q7. A company would be a resident in India for the AY 2021-2022 i.e. PY 2020-2021 if—

(a) it is an Indian company

(b) during the year, majority of its directors are resident in India

(c) during the year, its Place of Effective Management is in India

(d) both (a) and (c)

Q8. Income accruing in London and received there is taxable in India in the case of

(a) resident and ordinarily resident only

(b) both resident and ordinarily resident and resident but not ordinarily resident

(c) both resident and non-resident

(d) non-resident

Q9. Incomes which accrue or arise outside India but received directly in India are taxable

in case of—

(a) resident and ordinarily resident only

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 3

(b) both resident and ordinarily resident and resident but not ordinarily resident

(c) non-resident

(d) All the above

Q10. Income earned from a contract negotiated by an agent in India in the name of a non-

resident but approved by such non-resident shall:

(a) be taxable in India as such income is deemed to accrue or arise in India

(b) not be taxable in India as there is no business connection in India

(c) be taxable in India only if it is received in India

(d) be taxable in India as such income accrues or arises in India

Q11. Fees for technical services paid by the Central Government will be taxable in case

of—

(a) resident and ordinarily resident only

(b) both resident and ordinarily resident and resident but not ordinarily resident

(c) non-resident

(d) All the above

Q12. Short term capital gains on sale of shares of an Indian private limited company but

received in Australia is taxable in case of—

(a) resident and ordinarily resident only

(b) both resident and ordinarily resident and resident but not ordinarily resident

(c) non-resident only

(d) All the above

Q13. Income from a business in Canada, controlled from Canada is taxable in case of

(a) resident and ordinarily resident only

(b) both resident and ordinarily resident and resident but not ordinarily resident

(c) non-resident

(d) All the above

Q14. Dividend Income from Australian company received in Australia in the year 2017,

brought to India during the AY 2021-2022 i.e. PY 2020-2021 is taxable in case of—

(a) resident and ordinarily resident only

(b) resident but not ordinarily resident

(c) non-resident

(d) None of the above

Q15. Under the Income-Tax Act, the incidence of taxation depends on—

(a) The citizenship of the tax-payer

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 4

(b) The age of the taxpayer

(c) The residential status of the tax-payer

(d) The gender of the taxpayer

Q16. A company is considered to be resident if

(a) It is an Indian Company

(b) During the previous year foreign company’s place of effective management is situated in

India

(c) (a) & (b) both

(d) Any of the above

Q17. Mr. J is a person of Indian origin and comes to India on 29/10/2020 and plans to

stay here for 185 days. During 4 years prior to PY 2020-2021 he was in India for

750 days. Earlier to that he was never in India. For AY 2021-2022 i.e. PY 2020-

2021 he shall be:

(a) Resident and ordinarily resident in India

(b) Resident but not ordinarily resident in India

(c) Non-resident

(d) None of the above

Q18. Mr. John is a citizen of India left India for France on 6/8/2020 for booking orders

on behalf of an Indian company for exporting goods. He came back to India on

5/10/2021. He had been resident in India for the past 10 years. For AY 2021-2022

i.e. PY 2020 2021 he shall be:

(a) Resident and ordinarily resident in India

(b) Resident but not ordinarily resident in India

(c) None Resident in India

(d) None of the above

Q19. Mr. Rakesh a citizen a India and is working as a crew member on an Indian ship.

During the AY 2021- 2022 i.e. PY 2020-2021 he leaves India for Germany on

15/9/2020 for holidays and returned on 1/4/2021. He had been non-resident for

the past 3 years. Earlier to that he was permanently in India. For AY 2021- 2022

i.e. PY 2020-2021 he shall be—

(a) Resident and ordinarily resident in India

(b) Resident but not ordinarily resident in India

(c) Non-resident in India

(d) None of the above

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 5

Q20. Remuneration for rendering services on a foreign ship is not taxable in India in the

case of—

(a) A resident

(b) A non-resident who is not a citizen of India

(c) Not ordinarily resident

(d) A citizen of India

Q21. Every financial year, the residential status of an assesses—

(a) May change

(b) Will certainly change

(c) Will not change

(d) None of the above

Q22. Income accruing from agriculture in a foreign country is taxable in India in case of an

assesses who is—

(a) Resident and ordinary resident

(b) Not-ordinarily resident

(c) Non-resident

(d) None of the above

Q23. Foreign income received in India during the previous year is taxable in the case of—

(a) Resident

(b) Not-ordinarily resident

(c) Non-resident

(d) All of the above

Q24. Income earned and received outside India but later on remitted to India, is taxable

in the case of—

(a) All the assesses

(b) Resident and ordinarily resident in India

(c) Non-resident

(d) None of the above

Q25. Which of the following may be a ‘Resident but not ordinarily resident’ in India—

(a) Partnership firm

(b) Joint stock company

(c) Association of persons

(d) Hindu Undivided Family

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 6

Q26. Past untaxed profit of the Previous Year 2019- 2020 brought to India in Previous

Year 2020-2021 is chargeable to tax in the AY 2021-2022 in the hands of

(a) All the assesses

(b) Resident and ordinarily resident in India

(c) Non-resident in India

(d) None of the above

Q27. Total income of a person is determined on the basis of his

(a) Residential status in India

(b) Citizenship in India

(c) Both (a) and (b) above

(d) None of the above

Q28. The following additional conditions are to be satisfied by a person to be resident and

ordinarily resident in India—

(a) He is a resident in at least any 2 out of the 10 previous years immediately preceding the

relevant previous year

(b) He has been in India for 730 days or more during the 7 previous years immediately

preceding the relevant previous year

(c) Both (a) and (b) of above

(d) None of the above

Q29. Mr. vikas an Indian citizen, who is living in Delhi since 1980, left for Japan on 1st

July, 2018 for employment. He came back to India on 1st January, 2020 on a visit

and stayed for 4 months. His residential status for the AY 2021-2022 i.e. PY 2020-

2021 would be—

(a) Resident and ordinarily resident

(b) Not ordinarily resident

(c) Non-resident

(d) Resident

Q30. Mr. Vikas earns the following Income during the PY ended 31st March, 2021.

Interest on U.K. Development Bonds (1 /4th being received in India): Rs. 2,00,000:

Profits on sale of a building in India but received in Holland: Rs. 2,00,000. The

income liable to tax for the AY 2021-2022 i.e. PY 2020-2021 if Mr. Vikas is

resident and not ordinarily resident in India, is

(a) Rs. 2,50,000

(b) Rs. 4,00,000

(c) Rs. 2,00,000

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 7

(d) Rs. 50,000

Q31. If Karta is resident and ordinarily resident in India but control and management of

HUF is situated partly outside India in the previous year, the HUF is -

(a) Resident and ordinarily resident

(b) Not ordinarily resident

(c) Non-resident

(d) Resident

Q32. Mr. Vikas is a foreign citizen. His father was born in Delhi in 1951 and mother was

born in England in 1950. His grandfather was born in Delhi in 1922. Mr. Vikas visited

India to see Taj Mahal and other historical places. He came to India on 1st

November, 2020 for 200 days. He has never come to India before. His residential

status for AY 2021-2022 i.e. PY 2020-2021 will be—

(a) Non-resident in India

(b) Not ordinarily resident in India

(c) Resident and ordinary resident in India

(d) None of the above

Q33. Mr. Rahul is a software engineer at ABC Ltd. left India on 10th August, 2020 for

the treatment of his wife. This is first time he and his wife have left India. For

Income-tax purpose residential status of Mr. Rahul for the AY 2021-2022 i.e. PY

2020-2021 will be—

(a) Resident and ordinary resident

(b) Non-resident

(c) Not ordinarily resident

(d) Cannot be determined from the given information

Q34. Residential status of an Indian company is resident in India for the year -

(a) If the place of effective management is wholly in India

(b) If part of the effective management in India

(c) Regardless of the place of effective management

(d) If it is listed on recognized stock exchange

Q35. HUF of Mr. Ram consisting of himself, his wife and 2 sons is assessed to income-tax.

The residential status of HUF would be non-resident, when -

(a) The management and control of its affairs is wholly in India

(b) The management and control of its affairs is wholly outside India

(c) The status of karta is non-resident for that year

(d) When majority of the members are nonresidents

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 8

Q36. Mr. SUBHASH who was born and brought up in India left for employment in Dubai on

20th August, 2020. His residential status in respect of the AY 2021- 2022 i.e. PY

2020-2021 would be:

(a) Resident and ordinarily resident

(b) Non-resident

(c) Not ordinarily resident

(d) None of the above

Q37. X Ltd. is an Indian company. It carries its business in Delhi and London. The place of

effective management of the company is situated in London. More than 85% of its

business income is from the business in England. If so, its residential status will be—

(a) Resident

(b) Non-resident

(c) Not ordinarily resident

(d) Foreign company

Q38. A company incorporated outside India having its place of effective management fully

situated in India in the previous year will be treated as—

(a) Resident

(b) Not ordinarily resident

(c) Non-resident

(d) None of the above

Q39. Mr. P, an Indian citizen, left India for U.K. on 1st September, 2020 to take up a

job there. His residential status for AY 2021-2022 i.e. PY 2020- 2021 would be—

(a) Resident and ordinarily resident

(b) Not ordinarily resident

(c) Non-resident

(d) None of the above

Q40. Mr. J brought into India, in the previous year, past untaxed income which was earned

in U.K. The income will be taxable if Mr. J is—

(a) An ordinarily resident

(b) A not-ordinarily resident

(c) A non-resident

(d) Non taxable

Q41. Mr. M born and brought up in India left for employment in Belgium on 31-10-2020.

He has never gone out of India, previously. What in his residential status for the AY

2021-2022 i.e. PY 2020-2021?

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 9

(a) Non-resident

(b) Not ordinarily resident

(c) Resident and ordinary resident

(d) Indian citizen

Q42. Mr. Pankaj (age 55) is Karta of HUF doing textile business at Nagpur. Mr. Pankaj is

residing in Dubai for the past 10 years and visited India for 20 days every year for

filing the Income tax return of HUF. His two, major sons take care of the day to

day affairs of the business in India. The residential status of HUF for the AY

2021-2022 i.e. PY 2020-2021 is:

(a) Non-resident

(b) Resident and ordinary resident

(c) Not ordinarily resident

(d) None of the above

Q43. Thomas Inc. of Australia borrowed money from various companies in Australia for

doing business in India by name ANS Co. Ltd., Mumbai. Thomas Inc. paid interest of

Rs. 5 lakhs to various lenders. The amount of interest paid:

(a) Has accrued in India

(b) Is exempt from tax

(c) Does not accrue in India

(d) Is taxable in Australia

Q44. A company is said to be resident in India in previous year if,

(a) It is an Indian company

(b) Its place of effective management is in India

(c) Either it is an Indian company or is place of effective management is in India.

(d) It is both an Indian company or is place of effective management is in India.

Q45. ABC Ltd. An Indian company will be ----- in India if its place of effective

management is wholly situated outside India during the previous year.

(a) Resident

(b) Non- Resident

(c) Not ordinarily Resident

(d) Any of these

Q46. The person who concludes contracts on behalf of the non-resident is known as-

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 10

(a) Concluding agent

(b) Stocking agent

(c) Indenting agent

(d) None of these

Q47. Business activity carried on with which of the following agent is not a business

connection

(a) Concluding agent

(b) Stocking agent

(c) Indenting agent

(d) None of these

Q48. Which of the following activity will be considered as business connection in India?

(a) All the operations of a firm are not carried in India

(b) An office set up by non-resident for caring out business activity in India

(c) The profits earned by assesse on supplies of fabricated platforms

(d) All of these

Q 49: Mr. Anil fulfills all conditions given in sec 6(1A). In such case he shall be treated as

…………..

a. RI

b. ROR

c. RNOR

d. NR

Q 50: Mr. Sunil is in Indian citizen. His income other than foreign source exceeds Rs 15

lakhs and not liable to pay tax in other country. His R.S. for relevant PY shall be

a. Resident

b. non-resident

c. Not ordinarily resident

d. Can’t say

CMA VIPUL SHAH TEST-2 RESIDENTIAL STATUS

Page 11

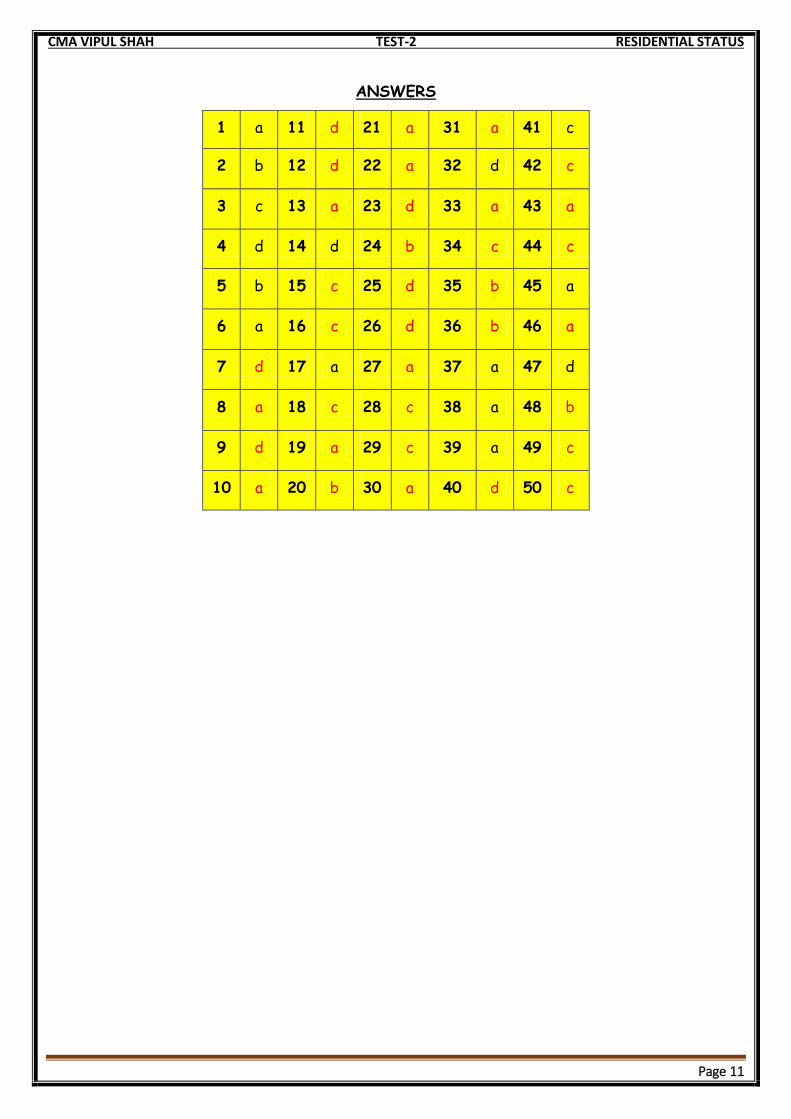

ANSWERS

1 a 11 d 21 a 31 a 41 c

2 b 12 d 22 a 32 d 42 c

3 c 13 a 23 d 33 a 43 a

4 d 14 d 24 b 34 c 44 c

5 b 15 c 25 d 35 b 45 a

6 a 16 c 26 d 36 b 46 a

7 d 17 a 27 a 37 a 47 d

8 a 18 c 28 c 38 a 48 b

9 d 19 a 29 c 39 a 49 c

10 a 20 b 30 a 40 d 50 c

Related Documents