Version i pare Shqip SIGURIME Hyrje Mbi sigurimet dhe teorine mbeshtetese natyra ekonomike dhe funksionet e sigurimit Sigurimi është mënyra për të siguruar mbrojtje kundër humbjeve financiare që rezultojnë nga një shumëllojshmëri perilesh. Me blerjen e policave te sigurimit, individët dhe bizneset mund të marrin kompensim për humbjet për shkak të aksidenteve rrugore, vjedhje të pasurisë, zjarri dhe dëmtime të stuhise, shpenzimet mjekësore, dhe humbje të të ardhurave për shkak të paaftësisë ose vdekjes. Demshperblimi per humbjet gjenerohet nga fondi i sigurimeve. Sigurimi është i arsyeshem, kur ngjarjet e sigurimit (rreziqet) shkakton nevojë të konsiderueshme për para. Si një kategori ekonomike nje siguracion paraqet marrëdhënieve ekonomike, duke përfshirë format dhe metodat e krijimit të fondit të sigurimeve dhe përdorimin e tij në demshperblimin per ngjarjet e siguruara dhe duke ndihmuar njerëzit, kur disa ngjarje ndodhin në jetën e tyre. Aleksandrov A. (1998) përshkruan karakteret e meposhtme të kategorisë ekonomike te sigurimit: prania e marrëdhënieve rishpërndarese; praninë e riskut te siguruar (dhe kriterin e vlerësimit të tij); organizimin e komunitetit të sigurimit nga nenshkrues dhe siguruesit; kombinim individuale dhe interesave të sigurimit dhe grupit; përgjegjësi të bashkuar e të gjitha nenshkruesve për dëmin; përhapje e kufizuar e dëmit; rishpërndarjen e dëmtimit në hapësirë dhe kohë; kthimin e pagesave të sigurimit; vetëmjaftueshmeri të veprimtarisë së sigurimit. Faqja 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Version i pare Shqip SIGURIME

HyrjeMbi sigurimet dhe teorine mbeshtetese natyra ekonomike dhe funksionet e sigurimit Sigurimi është mënyra për të siguruar mbrojtje kundër humbjeve financiare që rezultojnë nga një shumëllojshmëri perilesh. Me blerjen e policave te sigurimit, individët dhe bizneset mund të marrin kompensim për humbjet për shkak të aksidenteve rrugore, vjedhje të pasurisë, zjarri dhe dëmtime të stuhise, shpenzimet mjekësore, dhe humbje të të ardhurave për shkak të paaftësisë ose vdekjes. Demshperblimi per humbjet gjenerohet nga fondi i sigurimeve. Sigurimi është i arsyeshem, kur ngjarjet e sigurimit (rreziqet) shkakton nevojë të konsiderueshme për para. Si një kategori ekonomike nje siguracion paraqet marrëdhënieve ekonomike, duke përfshirë format dhe metodat e krijimit të fondit të sigurimeve dhe përdorimin e tij në demshperblimin per ngjarjet e siguruara dhe duke ndihmuar njerëzit, kur disa ngjarje ndodhin në jetën e tyre. Aleksandrov A. (1998) përshkruan karakteret e meposhtme të kategorisë ekonomike te sigurimit:

prania e marrëdhënieve rishpërndarese; praninë e riskut te siguruar (dhe kriterin e vlerësimit të tij); organizimin e komunitetit të sigurimit nga nenshkrues dhe siguruesit; kombinim individuale dhe interesave të sigurimit dhe grupit; përgjegjësi të bashkuar e të gjitha nenshkruesve për dëmin; përhapje e kufizuar e dëmit; rishpërndarjen e dëmtimit në hapësirë dhe kohë; kthimin e pagesave të sigurimit; vetëmjaftueshmeri të veprimtarisë së sigurimit.

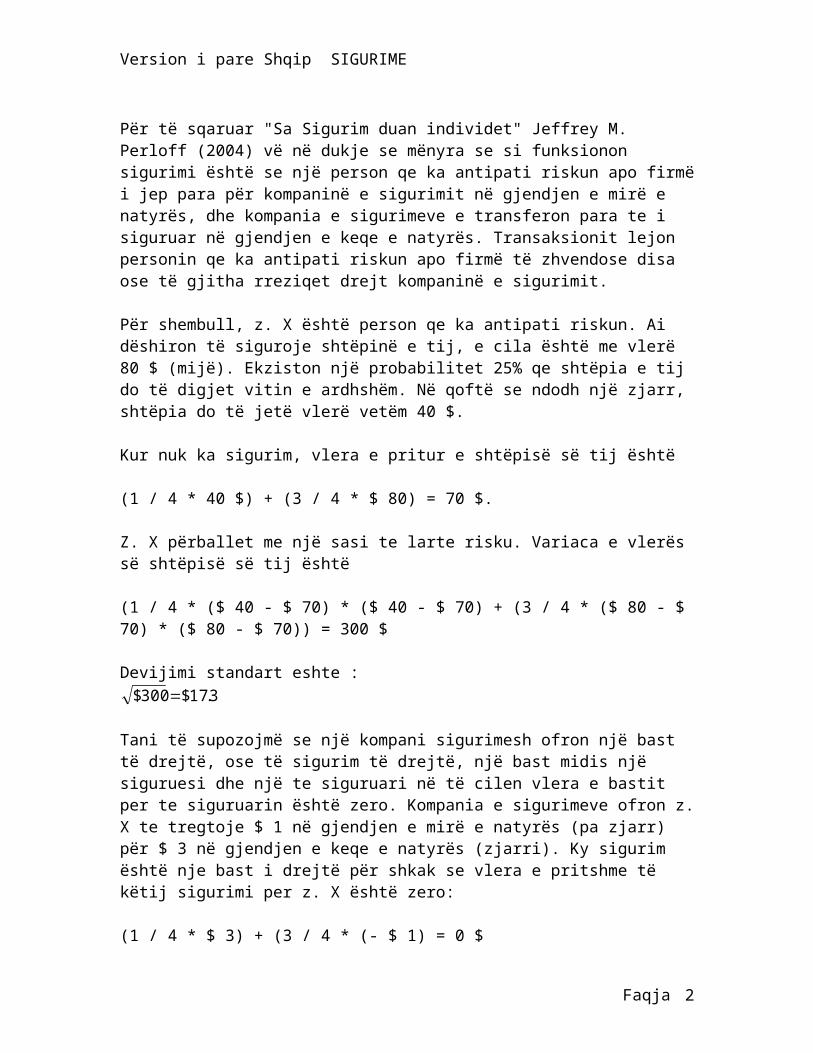

Për të sqaruar "Sa Sigurim duan individet" Jeffrey M. Perloff (2004) vë në dukje se mënyra se si funksionon sigurimi është se një person qe ka antipati riskun apo firmë i jep para për kompaninë e sigurimit në gjendjen e mirë e natyrës, dhe kompania e sigurimeve e transferon para te i siguruar në gjendjen e keqe e natyrës. Transaksionit lejon personin qe ka antipati riskun apo firmë të zhvendose disa ose të gjitha rreziqet drejt kompaninë e sigurimit. Për shembull, z. X është person qe ka antipati riskun. Ai dëshiron të siguroje shtëpinë e tij, e cila është me vlerë 80 $ (mijë). Ekziston një

Faqja 1

BEST, 26.06.10,

Hyrje Mbi sigurimet dhe teorine mbeshtetese

Version i pare Shqip SIGURIME

probabilitet 25% qe shtëpia e tij do të digjet vitin e ardhshëm. Në qoftë se ndodh një zjarr, shtëpia do të jetë vlerë vetëm 40 $. Kur nuk ka sigurim, vlera e pritur e shtëpisë së tij është (1 / 4 * 40 $) + (3 / 4 * $ 80) = 70 $. Z. X përballet me një sasi te larte risku. Variaca e vlerës së shtëpisë së tij është (1 / 4 * ($ 40 - $ 70) * ($ 40 - $ 70) + (3 / 4 * ($ 80 - $ 70) * ($ 80 - $ 70)) = 300 $ Devijimi standart eshte :

3.17$300$ Tani të supozojmë se një kompani sigurimesh ofron një bast të drejtë, ose të sigurim të drejtë, një bast midis një siguruesi dhe një te siguruari në të cilen vlera e bastit per te siguruarin është zero. Kompania e sigurimeve ofron z. X te tregtoje $ 1 në gjendjen e mirë e natyrës (pa zjarr) për $ 3 në gjendjen e keqe e natyrës (zjarri). Ky sigurim është nje bast i drejtë për shkak se vlera e pritshme të këtij sigurimi per z. X është zero: (1 / 4 * $ 3) + (3 / 4 * (- $ 1) = 0 $ Meqenese z. X është antipatik ndaj riskut, ai sigurohet plotësisht, duke blerë sigurim të mjaftueshem për të eliminuar rrezikun e tij krejt. Me këtë shumë sigurimi, ai ka të njëjtën sasi pasurie në dyja raste. Z. X i paguan kompanise se sigurimeve $ 10 në gjendje të mirë të natyrës dhe merr 30 $ në gjendje të keqe. Në gjendje të mirë, ai ka një shtëpi me vlerë 80 $ minus 10 $ qe ai i paguan kompanise se sigurimeve, për një pasuri neto prej 70 $. Nëse ndodh zjarrit, ai ka një shtëpi me vlerë 40 $ plus një pagesë nga kompania e sigurimeve e 30 $, për një pasuri neto, përsëri, 70 $. Vlera e pritur e z. X me kete sigurim te drejtë eshte $ 70, e njëjtë me vlerën pritur pa sigurim. Varianca qe ai ndesh bie nga $ 300 pa sigurim ne $ 0 me sigurim. Z. X është më mirë me sigurim, sepse ai e ka të njëjtën vlerë te pritur nuk dhe përballet me asnjë risk. Jeffrey M. Perloff (2004) përshkruan se kur sigurimi i drejtë ofrohe, njerëzit antipatike ndaj riskut sigurohen plotësisht. Nëse kompanitë e sigurimit tarifojne më shumë se sa çmimi i sigurimit të drejtë, individët blejne me pak sigurim.

Faqja 2

Version i pare Shqip SIGURIME

Për shkak se kompanitë e sigurimit nuk ofrojnë sigurim të drejtë, shumica e njerëzve nuk jane te siguruar plotësisht. Një kompani e sigurimi nuk mund të qëndroje ne treg, nëse ajo ofron sigurim të drejtë. Me sigurimin e drejtë pagesat e pritura te kompanise se sigurimeve do të jetë e barabarta me shumën qe kompania e sigurimeve mbledh. Për shkak se kompania e sigurimeve ka shpenzime operative - shpenzimet për mbajtjen e zyrave, format e printuara, punësimin e agjentëve te shitjes, dhe kështu me radhë - nese nje firmë sigurimi siguron sigurim të drejtë do të humbase para. Primet e kompanive të sigurimit duhet të jetë te larta mjaftueshem për të mbuluar shpenzimet e tyre operative, keshtu qe sigurimit është më pak se e drejtë për të siguruarin. Sa mund të tarifojne kompanite e sigurimit për sigurimin? Një kompani monopoli sigurimesh mund t'i ngarkoje një shumë deri në primin të rrezikut qe një person është i gatshëm të paguajnë për të shmangur riskun. Sa më shumë antipatik ndaj riskut te jete nje individ, më teper nje kompani sigurimi monopol ka per te tarifuar. Nëse ka shumë kompani të sigurimit qe konkurrojnë për tregun, çmimi i një policë sigurimi është më pak se maksimumi qe individët antipatik ndaj riskut janë të gatshëm të paguajnë, por perseri mjaftaftueshmerisht e lartë se firma të mbuloje shpenzimet e tyre operuese. Në shumë vende në zhvillim, sigurimi nuk është i përhapur dhe është interesante për të hetuar arsyet e vazhdueshmerise se sigurimit te paket te te varfërit. Kështu, çështja hulumtimi i kësaj teze është si më poshtë: Pse shumica e të varfërve në Shqipëri jane te me sigurim te paket ?

nxjerje nga libri bundos pershtat :

Për fat të keq jo të gjitha risqet janë të sigurueshme. Që një risk te jetë i sigurueshëm duhet të plotesohen disa kërkesa. Nga këndvështrimi i siquruesit për risqet e sigurueshëm kërkohet që: -Objektet të jenë në sasi dhe cilësi që të lejojnë një përllogaritje te perafërt të probabilitetit të humbjes. Kështu, në qoftë se numri i objekteve është i vogël, atëherë siguruesi do të jetë subjekt i një pasigurie të njëjtë me atë të të siguruarit. Gjithashtu, cilësia e objekteve për t'u siguruar duhet të jetë e njëjtë në menyrë që të formulohen statistika ndihmëse për humbjet. - Humbja, duhet të jete aksidentale dhe jo e qellimshme.- Kur ndodh humbja duhet të jetë e përcaktuesbme dhe e matshme.-_Objektet e siguruara nuk duhet të jenë subjekt i dëmtimeve të rreme, pra, të stimuluara.Nqa këndveshtrjmi i të siguruarit, risqet duhet të plotësojnëdy kushte:-Humbja potenciale duhet të jetë e madhe, aq sa të shkaktoje dem financiar.

Faqja 3

BEST, 28.06.10,

Materiale ++ nga libri bundos

Version i pare Shqip SIGURIME

- Propabilitetii humbjes nuk duhet të jete shume i madh. Një nga prirjet të siquruarve është të mos sigurohen ndaj humbje me propabilitet të madh ndodhjeje, sepse kosto e transferimi do të ishte tepër e lartë. Sa më e mundshme të jetë humbja, aq më e sigurt është ndodhja e saj. Sa më e sigurt të jetë kjo ndodhje, aq më i lartë do të jetë primi përkatës.

Mrojtja nga risqet

Funksioni kryesor i sigurimeve është që ato të veprojnë simekanizma për transferimin e riskut. Por edhe pse e transferojnë rrezikun ato nuk mund ta shmangin një plagosje ose një sëmundje, kështu që ato mund ta mbrojnë individin nga fatkeqësitë e jetës. Në një masë të konsiderueshme mund të mbrohet ajo që zoteron personi, kryesisht pasuria edhe kjo nëpërmjet dëmshpërblimit. Streset mendore dhe fizike si dhe sëmundjet mund të paksohen në qoftë se individi ka njohuritë e nevojshme për sëmundjet dhe merr masa parandaluese për to.Një pasuri, por edhe një individ me gjendje shëndetësore të keqësuar mund të mbrohen në qoftë se personi apo biznesi që përfaqëson ai, blejnë një policë sigurimi, që të mbrojnë pasurinë nga faktorët njerëzore (vjedhje ose dëmtime me dashje), kundrejt aksidenteve (zjarr ose përplasje automjetesh), ndaj stuhisë dhe përmbytjeve ose ndaj sëmundjeve dhe paaftesisë për të punuar.Mundesia për të pësuar një humbje apo dëm material lidhet me rritjen e numrit të incidenteve si dhe me mundësinë e ndodhjes së tyre. Rritja e numrit të rreziqeve lidhet me një numër të madh veçorish indlvknrale, mendore, fizike dhe pasurore të personit ose kompanisë.Sigurimet mbrojnë pasurinë materiale duke i dhënë zoteruesit të saj burimet për të zëvendësuar humbjen që i është shkaktuar. Ato mbrojnë një person për të cilin nevojiten shpenzime për t'ia kthyer shëndetin në gjëndjen e tij normale ose për të siguruar rehatinë si invalid. Nga ana tjetër, sigurimet mbrojnë edhe personat, të cilët nuk janë në moshë për të punuar duke u siguruar të ardhura në formën e pensioneve, duke i përfshirë punonjesit në skemat e produktit të sigurimeve.Koncepti i mbrojtjes së sigurimeve është një marrëveshje për zhdëmtim në para ose për zëvëndësim për të mbajtur pasurinë e të siguruarit në të njejtat kushte edhe pas ndodhjes së ngjarjes së siguruar.Të gjitha pasuritë e një pronari, si: toka, ndërtesat, pajisjet,llogaritë bankare, veshjet, aksionet, autoveturat, patentat e produkteve që prodhohen për herë të parë, si dhe vlerat që zotëruesi përfiton nga përdorimi i pasurisë së tij mund të sigurohen. Ato mund të mbrohen ndaj një rreziku të veçantë ose ndaj disa rreziqeve njëherësh duke u siguruar kundrejt tij. Për t'u siguruar e mbrojtur zotëruesi do të shpenzojë vetëm primin e sigurimit, që duhet t'i paguajë një shoqërie sigurimi.

Kontrata e sigurimit është një letër e nënshkruar ngapalët, ku përcaktohet rreziku, objekti i siguruar, rrethanat dheperiudha për të cilën ai sigurohet, personi që e siguron dhe pjesa e rrezikut që ai pergatitet te pranoje.

Faqja 4

Version i pare Shqip SIGURIME

11.1 Bazat Ligjore

Siç do t'a theksojmë edhe më vonë veprimtaritë siguruese nëvendin tonë janë kryer edhe përpara vitit 1991 madje edhe përpara vitit 1944. Por në këtë kapitull ne do të flasim për bazat ligjore të sigurimeve pas vitit 1991, vit i cili është i lidhur me ndarjen e veprimtarisë së sigurimeve nga arkat e kursimeve dhe krijimin e shoqërisë së parë siguruese, Instituti i Sigurimeve, që ende vazhdon të jetë e vetmja shoqëri siguruese me kapital publik.Instituti i Sigurimeve (INSIG-u) u themelua në bazë të ligjit Nr. 7461 datë 23. 7. 1991. Por, duke filluar nga qershori i vitit 1999 në bazë të ligjit Nr. 8081 date 7.03.1996 "Për veprimtaritë e Sigurimeve dhe Risigurimeve", ai ka adaptuar formën e shoqërisë anonime shtetërore dhe funksionon në përputhje me dispozitën përkatëse të liaiit Nr. 7638 datë 19.11. 1992. "Për shoqëritë treatare".Le të ndalemi pak më hollësisht në ligjin Nr. 8081 datë 7.03. 1996, pasi ky ligj aktualisht përbën aktin ligjor bazë mbi të cilin ushtrojnë veprimtarinë siguruese jo vetëm INSIG-u por edhe të gjitha shoqëritë e tjera private të sigurimeve të krijuara pas vitit1998.Në këtë ligj përcaktohen parimet dhe rregullat e përgjithshmeqë lidhen me sipërmarrjet në fushën e sigurimeve. Mbi bazën e dispozitave të përcaktuara në këtë ligj, shoqëritë siguruese ushtrojnë veprimtarinë e si,gurimeve të drejtpërdrejta që kanë për objekt përsonat apo jetën e tyre dhe pasurinë apo dëmet materiale, si edhe veprimtarinë që ka për objekt risigurimet.Fusha e zbatimit të këtij ligji, shtrihet për sipërmarrjet në sigurime dhe risigurime nga shoqëritë vënd ase dhe të huaja, të cilat marrin përgjegjësinë për mbulimin e rreziqeve, në bazë të kontratave të lidhura përkatësisht me të siguruarin dhe siguruesit.Në këtë ligj nuk përfshihen veprimtaritë e Institutit të Sigurimeve Shoqërore, Institutit të Sigurimit të Kujdesit Shëndetësor dhe Shoqërive, Shoqatave dhe enteve të tjera që bëjnë pjesë në një regjim sigurimesh, ndihmash apo përkrahjeje shoqërore, mbikqyrja e të cilave rregullohet me ligje të posaçme (neni 3).Sipas këtij ligji, shoqëritë siguruese vendase ose të huajaduhet të kufizojnë veprimtarinë e tyre vetëm në veprimtari siguruese dhe risiguruese si dhe në operacionet që rrjedhin drejtpërdrejt prej tyre. Nuk lejohet që ato të kryejnë veprimtari të tjera të çfarëdo lloji qofshin ato ( neni 5).Gjithashtu, sipas këtij ligji (neni 6) nuk lejohet që e njëjta shoqëri sigurimesh të kryejë sigurime për jetën dhe për pronën (jo jetën). Aktualisht vetëm INSIG -u i kryen të gjithë këto lloje sigurimesh, pasi deri në vitin 1999 ka qënë e vetmja shoqëri siguruese tek ne, prandaj i është lejuar që t'i kryej të dy këto lloje veprimtarish (jetën dhe jo jetën). Kompanitë e tjera siguruese janë të liçensuara dhe kryejnë vetëm veprimtari siguruese për pronën, pra, për jo jetën. Në vende të tjera ka edhe shoqëri sigurimesh që marrin në sigurim edhe jetën edhe jo jetën.Tarifat e primeve të sigurimit sipas ligjit (neni 12) caktohen nga vetë shoqëria e sigurimit, me përjashtim të primeve për sigurimet e detyrueshme të pasurisë ose përgjegjësisë të cilat rregullohen me ligje të veçanta (siç është përgjegjësia ndaj palëve të treta për sigurimin e automjeteve, karton i jeshil për mjetet që lëvizin jashtë vendit etj., të cilat caktohen më urdhër të ministrit të Financave).

Faqja 5

Version i pare Shqip SIGURIME

Shoqëritë e Sigurimeve që merren me sigurimin e mjeteve motorrike krijojnë një organizim, që quhet Byro Motorrike, e cila i përfaqëson këto shoqëri në tregun e brendshëm dhe në vënde e huaja si dhe kontrollon realizimin e detyrimeve që rrjedhin n Ja Konventat Ndërkombëtare për sigurim ndaj palëve të treta dhe për dëmet e shkaktuara nga aksidentet automobilistike. Deri në tetor të vitit 2001 detyrat e byrosë motorrike i ka kryer lnstituti i Sigurimeve INSIG-sh.a. Nga kjo kohë është krijuar dhe funksionon më vete Byroja Shqiptare e Sigurimeve.Shoqëritë e Sigurimit e ushtrojnë veprimtarinë e tyre duke u mbështetur edhe në mjaftë akte të tjera ligjore siç është ligji Nr. 7641 datë 1.12. 1992 "Për sigurimin e detyrueshëm të mbajtësve të mjeteve motorrike për përgjegjësinë ndaj personave të trEtë", Kodi Civil i Republikës së Shqipërisë (kreu XXIII që bën fjalë për Sigurimet), disa dekrete të Kuvendit të Shqipërisë, Vendirns të Këshillit të Ministrave, udhëzime, urdhëra dhe rregullore. Një dokument i rëndësishëm ligjor që rregullon veprimtarinë e INSIG¬ut dhe Shoqërive Siguruese është dhe Statuti i tyre për të cilin do të flasim në një paragraf të veçantë. Mbi bazën e këtyre ligjeve ushtrojnë veprimtarinë e tyre, në kushte të njëjta të gjitha Shoqëritë e Sigurimeve, qofshin këto me kapital publik apo privat ( neni 22 )

"Nga të katër miliard njerëz sot në tokë, të cilët jetojnë me më pak se dy dollarë në ditë, më pak se dhjetë million kanë akses në sigurim. "Churchill Craig, në Konferencën e Microinsurance në Tetor 2005, Mynih

.

1. Te dhena te Tregut

Treg – Sigurimet

Titull: Shumë aksidente, pak dëme të paguara

Shqipëria është ndër vendet me normën më të lartë të aksidenteve në Europë, por njëkohësisht është mes atyre vendeve ku paguhen më pak dëme për to

Nga Ersuin Shehu

Shqipëria është një ndër vendet me normën më të lartë të aksidenteve dhe të dëmtimeve nga aksidentet automobilistike në Europë. Në raport me numrin e mjeteve që figurojnë zyrtarisht të regjistruara dhe që, sipas Ministrisë së Transporteve, është rreth 350 mijë, në Shqipëri ndodhin 20 aksidente për çdo 10 mijë mjete. Por realisht norma e aksidenteve është më e lartë, për arsyen e vetme se numri i mjeteve në qarkullim, sipas statistikave të tërthorta të institucioneve, vlerësohet të jetë rreth 280 mijë. Kjo bën që norma e aksidenteve të të rritet në 25 për 10 mijë automjete. Ndërsa sipas shoqërive të sigurimit, vetëm 220 mijë automjete figurojnë të siguruara: e thënë ndryshe vetëm 220 mijë qarkullojnë me dokumentacion të rregullt. Po ta ndërtojmë raportin mbi këtë shifër, në Shqipëri ndodhin rreth 32 aksidente në 10 mijë automjete të regjistruara.

Faqja 6

BEST, 28.06.10,

Materialet e monitor kontrollo datat

BEST, 26.06.10,

Pjesa e pare Sigurimi neper rajon dhe kuptimi i nensigurimit dhe mikrosigurimet

Version i pare Shqip SIGURIME

Këto shifra janë disa herë më të larta në raport me mesataren europiane, që vlerësohet rreth 5 aksidente për 10 mijë mjete. Kjo shpeshtësi e lartë aksidentesh logjikisht të bën të mendosh se Shqipëria duhet të ketë një raport të lartë të pagesës së dëmeve për aksidentet automobilistike nga shoqëritë e sigurimit, kur dihet që sigurimi i makinës për përgjegjësi ndaj palëve të treta është i detyrueshëm. Por në të vërtetë nuk ndodh kështu. Duke iu referuar të dhënave më të fundit të Autoritetit të Mbikëqyrjes Financiare (AMF), deri në fund të muajit tetor të këtij viti, raporti mes dëmeve dhe primeve për sigurimin e brendshëm për përgjegjësitë motorike ndaj palëve të tjera (TPL) është më pak se 19.6%, ndërsa për vitin 2007 rezultonte vetëm 18.7%. Ky raport është më i ulët krahasuar me gjithë vendet e rajonit (Tabela 1).

Raporti dëme - prime në sigurimet motorrike:Shqipëri 22.8%Mesatarja BE: 75.8%

Ndërsa raporti dëme - prime për sigurimin e përgjegjësisë motorike ndaj palëve të treta, duke përfshirë edhe kartonin jeshil dhe policën kufitare, është rreth 22.8%. Këto shifra përfaqësojnë një diferencë shumë të madhe krahasuar me mesataren e Bashkimit Europian, në raportin dëme - prime në sigurimet motorike. Për vitin 2006, ky raport ishte në nivelin 75.8%, ose 3.3 herë më i lartë krahasuar me Shqipërinë, sipas të dhënave nga AMF-ja. Po t’i referohemi normës së kombinuar dëme + shpenzime për dëme ndaj primeve, mesatarja europiane është rreth 97.5%, ndërkohë që deri në vitin 2001 ishte më e lartë se 100%. Për këtë tregues të dytë në Shqipëri nuk ekzistojnë të dhëna zyrtare.

Grafik, Raporti mesatar dëme prime për vendet e BE (%)

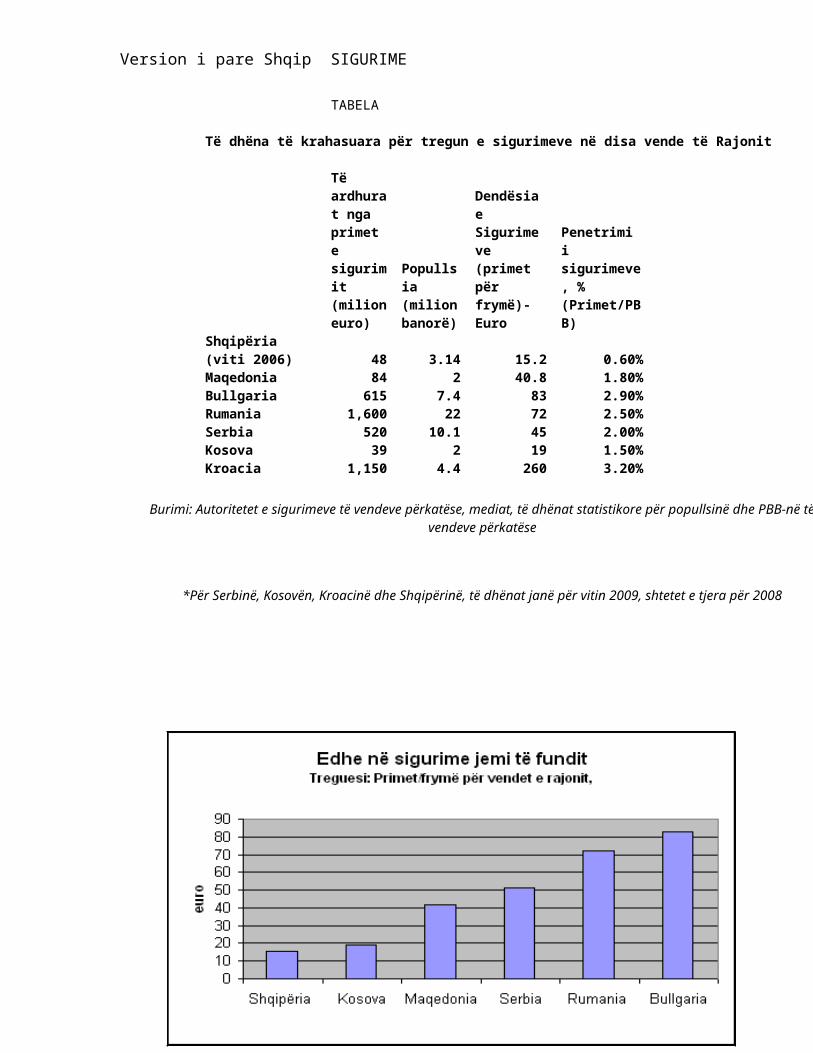

TABELA

Të dhëna të krahasuara për tregun e sigurimeve në disa vende të Rajonit

Të ardhurat nga primet e sigurimit (milion euro)

Popullsia (milion banorë)

Dendësia e Sigurimeve (primet për frymë)-Euro

Penetrimi i sigurimeve, % (Primet/PBB)

Shqipëria (viti 2006) 48 3.14 15.2 0.60%Maqedonia 84 2 40.8 1.80%Bullgaria 615 7.4 83 2.90%Rumania 1,600 22 72 2.50%Serbia 520 10.1 45 2.00%Kosova 39 2 19 1.50%

Faqja 7

Version i pare Shqip SIGURIME

Kroacia 1,150 4.4 260 3.20%

Burimi: Autoritetet e sigurimeve të vendeve përkatëse, mediat, të dhënat statistikore për popullsinë dhe PBB-në të vendeve përkatëse

*Për Serbinë, Kosovën, Kroacinë dhe Shqipërinë, të dhënat janë për vitin 2009, shtetet e tjera për 2008

Burimi: Autoritetet e sigurimeve të vendeve përkatëse, mediat, të dhënat statistikore për popullsinë dhe PBB-në të vendeve përkatëse

*Për Serbinë, Kosovën, Kroacinë dhe Shqipërinë, të dhënat janë për vitin 2007, shtetet e tjera për 2006

E dini se paguhet edhe…jeta?

Një tjetër faktor që i bën potencialisht “të kripura” dëmet nga aksidentet në Shqipëri është numri i lartë i viktimave dhe i të dëmtuarve në përgjithësi nga aksidentet rrugore. Sipas statistikave zyrtare, në vitin 2009 ndodhën 1254 aksidente me të dëmtuar në njerëz. Nga këto aksidente, janë dëmtuar 1728 persona, nga të cilët 384 kanë humbur jetën. Në këtë shifër përfshihen vetëm personat me dëmtime të rënda, sepse vetëm ata regjistrohen nga policia në rast aksidenti.Mbi 50 aksidente ne dite te ushtaraku paraqiten nga aksidentet automobilistike sipas shefit te urgjences se traumatologjise zotit Myftar Torba .Ku ka rritje gjate muajve te veres. Ardhja e emigranteve per pushime dhe shtimit te levizjes me makine , zgjatet dita, njerezit shkojne neper plazhe e pishina dhe keto i bejne dhe pas orarit te punes. Nder shkaqet kryesore sipas tij mbetet dhe perdorimi i pijeve

Faqja 8

Version i pare Shqip SIGURIME

alkolike nga drejtuesit e makinave. Per fat te keq mosha mesatare qe perben pjesen me te madhe te te aksidentuarve eshte 35-40 vjeç, por nuk mungojne as 18 vjeçaret dhe me te vjetrit. Aksidente me makine po behen vertet shqetesues – theksoi Myftar Torba.Sipas këtyre shifrave, në Shqipëri vdekjet nga aksidentet janë 12 në 100 mijë banorë. Ndërkohë, në vendet e tjera, përfshi ato të rajonit, kjo shifër është dy herë më e ulët. Në Maqedoni vdekjet nga aksidentet janë vetëm 5 në 100 mijë banorë, në Greqi 4 në 100 mijë banorë, ndërsa në Itali 2.7 në 100 mijë banorë. Në vendet e Europës Veriore, si në Angli apo në Suedi, ky raport bie në 1 viktimë për 100 mijë banorë.Por, a bën numri i madh i të dëmtuarve që të paguhen më shumë dëme nga aksidentet? Sigurisht që jo, shifrat që përmendëm më lart flasin qartë. Sipas ekspertëve të sektorit të sigurimeve, dëmi për një person të vdekur në aksident shkon mesatarisht 30-35 mijë euro. Nëse do llogarisnim se vetëm për 50% të të vdekurve në aksidente përgjegjës janë drejtuesit e mjeteve të siguruara, shoqëritë e sigurimit do të paguanin në vitin 2009 rreth 5.7 milion euro, ose 700 milion lekë: e thënë ndryshe 1.5 herë vlerën e të gjitha dëmeve të paguara për sigurimin e brendshëm motorik (TPL) gjatë vitit 2009. Në Shqipëri, ndryshe nga të gjitha vendet e zhvilluara europiane raporti i dëmshpërblimeve për humbjet njerëzore kundrejt atyre materiale vlerësohet 15% me 85% në një kohë që në vendet europiane ky raport është të paktën 50% me 50%! Kjo e bën edhe më kritike gjendjen: në Shqipëri paguhen rreth 600-700 mijë euro për njerëzit nga rreth 4 milion euro që paguhen në një vit për dëmet nga aksidentet automobilistike. Pa llogaritur në këtë mes të dëmtuarit ose të plagosurit, të cilët, sipas ligjit, do të sillnin gjithashtu shpenzime shumë të mëdha në dëme për kompanitë e sigurimit. Kjo kategori të dëmtuarish shpesh kërkon shpenzime më të mëdha se ata që vdesin në aksidente, sepse kanë nevojë për ndërhyrje kirurgjikale tepër të kushtueshme, si edhe për kujdes si invalidë për të gjithë jetën.Po pse realisht dëmi më i madh, jeta, realisht paguhet pak nga shoqëritë e sigurimit? Sipas z.Demir Osmani, ekspert i sigurisë rrugore dhe kryetar i shoqatës së Sigurisë Rrugore dhe Ambientit, ka dy shkaqe kryesore pse shoqëritë e sigurimit nuk paguajnë për personat që dëmtohen nga aksidentet. Arsyeja e parë është se shumë njerëz, për të mos thënë shumica e tyre, nuk e dinë se në dëmet që kompanitë e sigurimit duhet të paguajnë në rast aksidentesh, përfshihet edhe jeta apo dëmtimet fizike. Arsyeja e dytë, sipas z.Osmani, është edhe më shqetësuese: korrupsioni dhe manipulimet që ndodhin në vlerësimin e aksidenteve. Shumë shpesh kompanitë e sigurimit bëjnë çmos që ekspertiza të nxjerrë fajtor viktimat dhe jo përgjegjësit e aksidentit. Në këtë rast, çështja mbyllet. Z.Osmani thotë se problemi i pagesës së dëmeve për jetën dhe shëndetin është një rast tipik që kërkon rritjen e informacionit dhe kulturës qytetare për sigurimet. Shoqata e Sigurisë Rrugore, veç të tjerave, publikon shpesh edhe broshura për këtë qëllim, me financimin e OJF-ve të ndryshme të huaja. Por institucioni që është i ngarkuar me ligj për mbrojtjen dhe informimin e konsumatorit në këtë sektor, AMF, bën pak punë sensibilizuese. Sa prej jush kanë lexuar ose parë/dëgjuar ndonjë mesazh publik nga AMF për të drejtat apo në përgjithësi për sjelljen konsumatore në raport me sigurimet? Z.Varuzhan Piranjani, ekspert i tregut dhe ish-drejtor i kompanisë së sigurimeve Insig, thotë se një arsye e rëndësishme është se marrja e një dëmshpërblimi nga një shoqëri sigurimesh kërkon shumë mund, përpjekje, kohë të humbur si edhe në shumë raste jo pak para për t’i shkuar çështjes deri në fund. Këtë gjë e tregojnë proceset e shumta gjyqësore

Faqja 9

Version i pare Shqip SIGURIME

që ka ndaj kompanive të sigurimit, por që zor se gjenden në statistikat e sigurimeve apo të ndonjë kompanie dhe insitucionit që i mbikqyr ato. I “trembur” nga këto peripeci, shpesh konsumatori shqiptar merr atë çka i japin shoqëritë e sigurimeve ose heq dorë fare nga kërkimi i saj.

Aksidentet, shumica dërrmuese për faj të drejtuesve

Femrat jane burim aksidentesh automobilistike . Behet fjale per femrat qe drejtojne makinen, pasi shumica e tyre nuk jane ne aftesine e duhur per te qene shofere. Kete e pohon shefi i sherbimit te Traumatologjise, Myftar Torba, i cili theksoi se, ndonese numri i shofereve femra eshte i vogel ne raport me shoferet meshkuj, ato bejne nej numer te madh aksidentesh.”Kjo ndodh ngaqe nuk e kane shkathtesine e meshkujve dhe shpesh perfundojne ne shkaktare te aksidenteve. Vertet femrat po behen problematike ne shkaktimin e ketyre aksidenteve” – theksoi Torba.96% e aksidenteve në Shqipëri ndodhin për faj të njerëzve. Sipas statistikave të Policisë Rrugore dhe Drejtorisë së Shërbimeve të Transportit Rrugor, janë gabimet njerëzore shkaku kryesor i aksidenteve automobilistike. Ndër përgjegjësitë njerëzore, të parat janë ato të drejtuesve të mjeteve. Për faj të drejtuesve të mjeteve ndodhin 70% e totalit të aksidenteve, si pasojë e shkeljes prej tyre të rregullave të qarkullimit rrugor. Gjithnjë sipas shifrave zyrtare, 20% e aksidenteve ndodhin për faj të këmbësorëve. Vetëm 6% e aksidenteve ndodhin për shkak të mungesës së sinjalistikës apo mirëmbajtjes së rrugëve. Teknikisht edhe këto përfshihen në aksidente që ndodhin për shkak të gabimeve njerëzore. Vetëm 4% e aksidenteve ndodhin për shkaqe madhore dhe që janë jashtë mundësisë për t’u parandaluar nga njerëzit.Ekspertët thonë se janë pikërisht rrugët më të mira ato që shkaktojnë numrin më të madh të aksidenteve. Rrugët e asfaltuara mirë, me pak kthesa, sjellin edhe numrin më të madh të aksidenteve, ku shembulli tipik është rruga Fushë-Krujë – Lezhë. Sipas z.Demir Osmani, në kushte të tilla drejtuesit e mjeteve janë më të prirur për të shkelur rregullat e qarkullimit rrugor, kryesisht duke kaluar kufijtë e shpejtësisë, apo duke kryer parakalime të gabuara. Megjithatë, z.Osmani thotë se kjo nuk i shfajëson organet kompetente publike, pasi mungesa e sinjalistikës së plotë është një nga problemet më të mëdha të sistemit rrugor shqiptar. Problemet fillojnë që nga vijëzimi, mirëmbajtja e deri nga vendosja e tabelave rrugore. Ndërsa z.Piranjani vë në dukje se në vendet e zhvilluara europiane edhe shoqëritë e sigurimeve ndikojnë shumë në uljen e aksidenteve nëpërmjet disa mekanizmave të thjeshtë, të tillë si rritja e primit të sigurimit deri në dy herë në vitin e ardhshëm nëse kryen ndonjë aksident, mospagesa e dëmshpërblimit, nese nuk je i lidhur me rrip sigurie etj. Mekanizma të tillë që ndikojnë shumë në sensibilizimin e opinionit publik, pra, për pasojë edhe të uljes së rasteve të dëmtimeve nga aksidentet automobilistike.

Sigurime – Pasuria

Titull: Të “luash” me zjarrin

Megjithë shtimin e rasteve të zjarrit në biznese dhe apartamente, shqiptarët vazhdojnë të jenë pak të ndërgjegjshëm për nevojën e sigurimit

Faqja 10

Version i pare Shqip SIGURIME

Nga Ersuin Shehu

Thuhet se me zjarrin e me ujin nuk bëhet shaka. Por me sa duket, shqiptarët ende nuk janë shumë të vetëdijshëm për rreziqet që mund të vijnë nga forcat e natyrës. Sipas të dhënave zyrtare që raporton Autoriteti i Mbikëqyrjes Financiare, vlera e primeve të shkruara bruto për sigurimin nga zjarri dhe forcat e tjera të natyrës gjatë vitit 2009 ishte 517 milion lekë, ose 9.36% të totalit. Ndonëse në vlerë absolute tregu shënon një rritje me 35.6% krahasuar me vitin 2008, në peshën specifike të këtij sigurimi ndaj totalit rritja është në nivele shumë më modeste, me 0.36% më shumë krahasuar me vitin e mëparshëm.

Sipas shoqërive të sigurimit, këta tregues janë më pak se modestë, duke marrë në konsideratë volumin potencial të këtij tregu. Madje, shoqëritë e sigurimit bëjnë të ditur se pjesa dërrmuese e sigurimeve nga zjarri dhe forcat e tjera të natyrës bëhet praktikisht në mënyrë të detyruar nga bankat, për bizneset që kanë vendosur pronën e tyre si kolateral për kreditë e marra. Shoqëritë llogarisin se në Shqipëri gjenden efektivisht mbi 300 mijë shtëpi banimi dhe janë të siguruara afërsisht 17 mijë të tilla. Sipas drejtorit të përgjithshëm të shoqërisë Interalbanian, z.Bardhyl Minxhozi, rritja e numrit të apartamenteve dhe të bizneseve këto 10 vitet e fundit ka qenë dhe mbetet në ritme shumë të larta, ndërsa tendenca e rritjes për sigurimet nga zjarri dhe rreziqet e tjera të pronës mbetet relativisht e ulët. “Megjithëse shumë shpesh dëgjojmë raste të rënies së zjarrit në apartamente dhe biznese, fare pak prej tyre janë të siguruara dhe, ç'është më e keqja, në raste të tilla i kërkohet shtetit për t'u kompensuar për dëmet që ndodhin. Kjo do të thotë se kjo shkallë e ulët e sigurimeve të pronës vjen kryesisht për shkak të mentalitetit negativ dhe mosnjohjes së këtyre shërbimeve. Në kushtet e ekonomisë së tregut, duhet të paguash vetë për mbrojtjen e pasurisë tënde,” thotë z.Minxhozi.

40 euro për të siguruar një apartament

Për sigurimin e pasurisë nga zjarri dhe forcat e tjera të natyrës çmimet janë në varësi të disa faktorëve dhe kompani të ndryshme zbatojnë çmime të ndryshme. Por sidoqoftë, kosto e sigurimit është modeste në raport me dëmet që mund të shkaktohen nga zjarri apo fatkeqësitë e tjera natyrore.“Në procesin e tarifimit të rreziqeve të pronës ndikojnë disa faktorë që lidhen me shkallën e rrezikshmërisë së llojeve të ndryshme të prones, si p.sh., lloji i materialit të pronës. Gjithashtu, çmimi është edhe në varësi të vendit ku ndodhet prona, të vlerës në para të saj etj. Për banesat çmimi është mesatarisht rreth 0.5 euro për mijë, që do të thotë që një apartament me vlerë 50 mijë euro mund të kushtojë rreth 40 euro, përfshirë TVSH-në! Pra, afërsisht sa pesë karta telefoni,” -thotë z.Bardhyl Minxhozi. Z.Ogert Shkrepa nga kompania e sigurimeve Sigal thotë se çmimet po ndikohen shumë edhe nga konkurrenca midis kompanive, madje, sipas tij, në disa raste për këtë shkak çmimet shkojnë në nivele qesharake. “Gjithsesi, pavarësisht nga sa më sipër, çmimet janë shumë të arsyeshme dhe nuk janë kurrsesi një barrë që të justifikojë mossigurimin e pronës. Ky sigurim kushton nga 1 euro

Faqja 11

Version i pare Shqip SIGURIME

deri në 3 euro për 1 mijë euro të siguruara. Tarifa varet edhe nga kushtet e mbrojtjes nga zjarri, si dhe nga vendndodhja e objektit,” thotë z.Shkrepa.Viti 2007 shënoi edhe një rritje të fortë të dëmeve të paguara nga shoqëritë e sigurimit. Për dëmet nga zjarri dhe nga forcat e tjera të natyrës, gjatë vitit 2007 shoqëritë e sigurimit paguan dëme në vlerën e 125 milion lekëve, ose 318% më shumë se në vitin 2006.

Sigurimi nga zjarri, “tregu i bankave”

Sipas shoqërive të sigurimit, numri më i madh i kontratave të sigurimit nga zjarri i takon individëve, ndërsa vlera më e madhe e primeve bizneseve. Por shoqëritë nënvizojnë se vetëm një pakicë e sigurimeve nga zjarri janë realisht vullnetare. Kryesisht janë bankat, që u “imponohen” klientëve që marrin kredi për ta siguruar pasurinë ndaj zjarrit dhe forcave të tjera të natyrës.Është për t’u përmendur fakti se shumica e policave të sigurimit të pronës, afërsisht 80% e tyre, janë lëshuar për individë apo firma që e kanë të bllokuar pronën si kolateral për kredinë e marrë në bankë. Pra, është banka ajo që i detyron individët të sigurojnë pronën, në mënyrë që kredia të jetë e garantuar në rast të ndonjë fatkeqësie natyrore apo zjarri,” -thotë z.Shkrepa nga Sigal. Kontributi i rëndësishëm i bankave në këtë treg theksohet edhe nga drejtori i përgjithshëm i Interalbanian. “Një rol të madh në “popullarizimin" e sigurimeve nga zjarri po luajnë bankat, të cilat sigurimin nga zjarri si rregull e kanë si kusht për dhënien e kredive. Në këtë kontekst, edhe individët që marrin kredi për shtëpi, janë të detyruar të sigurojnë banesat nga zjarri. Kjo do të ndihmojë në një të ardhme të afërt për shtimin e këtij biznesi,” -thotë z.Minxhozi.

Nuk dinë të blejnë dhe … nuk dimë të shesim?

Në analizën e shoqërive të sigurimit, mentaliteti negativ i klientëve dhe mungesa e kulturës së sigurimeve vullnetare është pengesa kryesore për zhvillimin e tregut të sigurimit nga zjarri dhe fatkeqësitë e tjera natyrore, por pa mohuar se “faji” nuk qëndron vetëm nga njëri krah. “Megjithatë, kur një produkt nuk shitet në masën e duhur, faji kryesor është i shitësit. Kështu, kompanitë e sigurimeve, përveç marketingut, kur shesin është e domosdoshme të jenë korrekte, sidomos kur ndodh një ose disa raste zjarri duke dëmshpërblyer shpejt dhe me cilësi. Gjatë vitit 2007, ne patëm dy raste zjarri në magazina në një ditë të vetme dhe i dëmshpërblyem në rreth 100 mijë euro brenda dy-tre javësh. Në këtë mënyrë, krijohet besimi reciprok midis kompanive dhe klientëve,” thotë z. Bardhyl Minxhozi. Ndërsa shoqëria Sigal vlerëson se për të nxitur rritjen e këtij tregu nevojiten ndryshime ligjore dhe përfshirjen në skemën e sigurimeve të detyrueshme edhe sigurimet e apartamenteve nga zjarri dhe rreziqet shtesë. Sipas z.Shkrepa, shoqëria Sigal ka në planet e saj fushata aktive marketingu për të promovuar produktet e veta në këtë fushë. “Do të punojmë nëpërmjet medias së shkruar dhe vizive, shpërndarjes së fletëpalosjeve për ndërgjegjësimin e individëve dhe subjekteve për sigurimin e pronës së tyre nga ‘Zjarri dhe Katastrofat Natyrore’. Vetëm nëpërmjet sigurimit bëhet transferimi i rreziqeve

Faqja 12

Version i pare Shqip SIGURIME

nga individët ose firmat te kompanitë e sigurimit. Kjo i lejon të siguruarit të punojnë dhe të zhvillojnë biznesin e tyre të qetë. E vetmja “humbje” e pakthyeshme për klientin është primi i paguar, i cili është fare e vogël po të krahasohet me shumën e dëmit apo me shumën e fondeve rezervë për të përballuar fatkeqësitë. Nga ana tjetër, individët apo biznesmenët ndihen të lirë të investojnë kapitalet pa pasur frikën e ndonjë dëmtimi, sepse edhe po të ndodhë kështu, kompanitë e sigurimit do të kthejnë çdo gjë në gjendjen e mëparshme financiare, thotë z.Shkrepa.Ndërsa, sipas z.Minxhozi, Interalbanian për vitin 2008 synon të rritet më shumë në këtë pjesë të tregut, duke u përqendruar në një marketing më efektiv, të thjeshtë dhe të kuptueshëm për rëndësinë që kanë këto lloj sigurimesh për klientët.

Është e domosdoshme që së pari të sqarojme termat mikrofinanciare, mikrosigurim dhe nensigurim.Termi mikrofinanciar i referohet kredive dhe shërbimeve bankare për të varferit. Ajo u shpike kur Banka Grameen Muhammed Yunus filloi dhënien e kredive te vogla (mikro kredi) të varfërve në Bangladesh në mesin e viteve shtatëdhjetë. Risitë janë, përveç shkalles se vogel ishte dhenia e kredise të grupeve qe garantonin për njëri-tjetrin, në vend te kërkeses per kolateral. Per më teper kreditë kanë qenë dhe ende u jepen në mënyrë tipike grave. Fillimisht ideja e te dyjave, kreditimit të grave dhe të kreditimit pa kolateral i beri ithtarët e tij objekt tallje. Por ideja doli e suksesshme për dy arsye: Së pari, në shumicën e vendeve në zhvillim, gratë ende kanë një rol vartës në shoqëri veçanërisht në lidhje me çështjet financiare. Si pasojë, duke i dhënë mikrokredit për gratë është parë si një mjet për arritjen e fuqizimin te grave në shoqëri. Së dyti, doli se gratë e paguajne kredine të tyre ne menyre më të besueshme dhe nuk jane doreleshuar ne shpenzimin e parave (Roth et al., 2007). Në vend të kësaj, kreditë u investuar në projekte me IRR të lartë. Gjatë viteve, mikrofinanca ka evoluar për t'u bërë një produkt i pjekur financiar me një penetrim goxha te larte dhe mbulimin e njerëzve të ardhura të ulëta në shumë vende në zhvillim. Mikrosigurimi, si microkredia, kerkon zvogelim rigoroz produkteve konvencionale financiare, në këtë rast sigurimit. Për fat të keq, "e vogla është e dryshme" nuk eshte vetëm e vërtetë për shkencat natyrore, por edhe për financen: Me reduktimit të produkteve të sigurimit karakteristika percaktuese ndryshojne. Sfidat dhe veçantitë qe kjo sjell janë përpunuar ne mijera studime. Një nga shpresat e mëdha mbi mikrosigurimin është lejimit e qasjes në sigurim për ata që më parë ishin të privuar nga çdo formë formale e zhvendosjes se riskut .Një individ është referuar si i nensiguruar në qoftë se niveli aktual i sigurimit është më poshtë se niveli optimal. Ky i fundit është përcaktuar si zvogelimi më i lartë i mundshëm i atyre risqeve financiare personale duke u furnizuar me produkte të sigurimit. Ky përkufizim padyshim varet nga supozimi se primet e policave te sigurimit janë te drejta..

Faqja 13

BEST, 27.06.10,

Shpjegime rreth termave

Version i pare Shqip SIGURIME

Si verehet ne tregun e sigurimeve ne Shqiperi perhapja e sigurimit ne prefekturat me te ardhurat me te larta. (bej nje titull me te shkurter permbledhes)

Analize e meposhtme bazohet ne analizen e korelacionit midis dy variablave qe vihen re ne treg , 1) te ardhurat totale te popullsise se prefektures dhe 2) primet totale te paguara ne sigurime sipas prefektures per jeten, jo-jeten dhe ne total.Te dhenat jane marre nga Instat ne menyre te terthorte meqenese nuk ekziston nje informacion mbi te ardhurat per fryme sipas prefekturave.Duke supozuar qe shperndarja e perberjes se familjeve ne Shqiperi nuk eshte e ndryshueshme ndermjet prefekturave mund te behet nje shperndarje e te ardhurave te per fryme ne baze te te dhenave mbi familjet.Nga nje anketim qe eshte kryer nga Instat, eshte bere statistika e shperndarjes se pajisjeve elektroshtepiake neper familje sipas rretheve, nga mund te nxiren te dhena per prefekturat. Ne baze te nje statistike te dyte po nga Instat te kryer ne Shqiperi eshte gjetur sasia e shpenzimeve qe ben nje familje sipas rretheve per pajisje elektroshtepiake, nga mund te nxiren te dhenat per prefekturat.Po te supozojme qe pajisjet kane te njejten jetegjatesi dhe nevoja per shpenzime per t’i zevendesuar eshte kostante ne te gjithe Shqiperine. Gjithashtu supozojme qe shpenzimet berhen per zevendesim pajisjesh dhe jo per shtimin e tyre. Gjithsesi edhe sikur te behej per shtimin e tyre ky fenomen do te qe nje fenomen qe mund te mendohet se nuk ka ndikim ne analize sepse do te qe shume me i vogel se shpenzimet per zevendesimin e tyre. Prej ketej arrijme ne perfundimin se mund te krijohet nje koeficent nga i cili ne mund te shperndajme te ardhuren per fryme te Shqiperise sipas prefekturave perkatese dhe t’a korelojme me te dhenat e Autoritetit te Mbikqyrjes Financiare per gjeografine e primeve te sigurimit dhe te marrim nje numer qe shpjegon, sipas rezultatit te mare nga analiza, ne nje sasi te madhe shperndarjen e primeve sipas prefekturave.Menyra se si funksionon analiza eshte te tille: Nga te dhenat mbi shperndarjen e pajisjeve afatgjata sipas rretheve nxjerim te dhenat per secilen prefekuture duke ditur rrethet qe permban secila prefekture dhe popullsine perkatese marim nje mesatare te ponderuar me popullsine e secilit rreth per secilen prefekture. Perqindja e marre me lart ponderohet me pas me peshat perkatese qe ne rastin tone jane cmimet e tregut te pajisjeve elektroshtepiake (supozohet se marrja e cmimeve aktuale nuk ka ndikim ne analize sepse zbatohet parimi kontabel qe thote qe nje pajisje vlen sa vlera e saj e zevendesimit, pra çmimi i tregut) duke na dhene nje tabele vlerash qe mund te interpretohet si sasia totale e pajisjeve elektroshtepiake sipas prefekturave (nje statistike e re qe mund te kete vlera per studime sociale). Vlerat e marra konvertohen ne te dhenat e vitit 2009 duke bere nje konvertim ne baze te koeficenteve te ndryshimit te numrit popullsise sipas prefekturave. Vlerat tashme te korektuara kthehen ne vleren totale te shpenzimit, duke marre per baze perqindjen qe ze shpenzimi per elektroshtepiake sipas prefekturave. Duke supozuar se e shpenzimet jane te barabarta me te ardhurat meqenese nuk kemi arsye te themi se funksioni i kursimeve eshte i ndryshueshem ndermjet prefekturave. Duke i vendosur shenjen e barazimit tashme kemi nje tabele vlerash (pa njesi) me te cilatat mund te bejme shperndarjen e te ardhurave per fryme te Shqiperise

Faqja 14

BEST, 26.06.10,

Pjesa e dyte a) A jane vertet te nensiguruar shtresat me te ardhura me te uleta , krahasimi behet neper rrethet e ndryshme me % perkatese

Version i pare Shqip SIGURIME

sipas prefekturave. Nga te dhenat makroekonomike keta tregues gjenden kollaj per vitin 2009. Prej ketej mund te ndertojme tabelen e te ardhrave te popullsise sipas prefekturave.Tashme qe i kemi te gjitha te dhenat mund te analizojme shume thjeshte te dy variablat nepermjet kovariances se tyre lineare.Nga vlerat e kovariances mund te themi qe mendimi qe blerja e primeve varet nga te ardhurat eshte i drejte sepse me teper se 85 % ( ) e te dhenave shpjegohet nga funksioni linear . Pra mund te themi se nje person ndikohet shume nga e ardhura e tij ne vendimet qe lidhen me blerjen e produktet e tregut te sigurimeve.

Analiza e Hipotezave te meposhtme statistikore behet mbi bazen e te dhenave te mbledhura nga anketimi ne qytetin e Tiranes. Mendohet qe rezultatet qe dalin prej saj jane perfaqesuese per gjithe Shqiperine meqenese popullsia e Tiranes eshte nje popullsi heterogjene e perbere nga shtresa te ndryshme shoqerore dhe me origjine nga shumica e trevave te Shqiperise. Anketimi eshte kryer ne disa zona te ndryshme te Tiranes gjate nje periudhe nje javore me ane te zgjedhjeve rastesore. Hipotezat e meposhtme jane bere mbi bazen e supozimeve :

shpenzimet e sigurimit te individeve jane te varur nga të ardhurat e tyre vjetore, gje qe u vertetua edhe nga Analiza me Lart mendimi pozitiv reth sigurimit i individeve eshte në varësi të gjinisë së tyre mendimi pozitiv reth sigurimit i individeve eshte në varësi të moshës së tyre mendimi pozitiv reth sigurimit i individeve eshte në varësi të edukimit të tyre Personi i cili është i siguruar eshte në varësi të të ardhurave të tyre

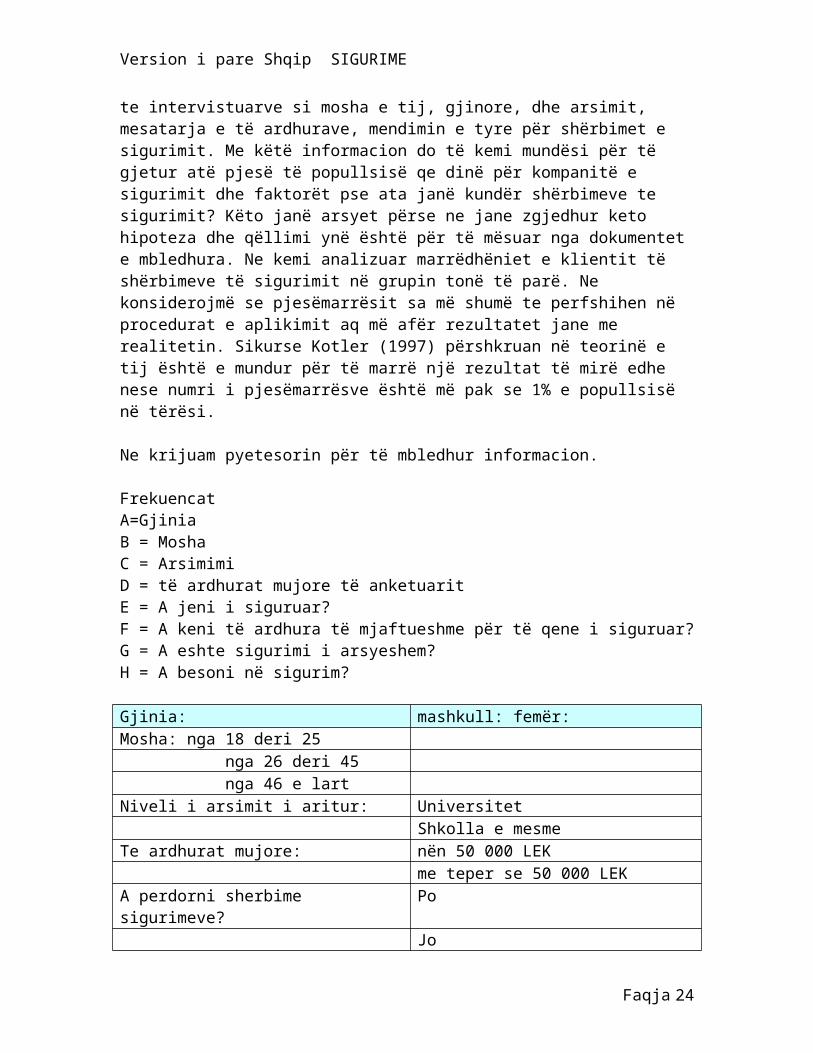

Pjesëmarrja në këtë statistike nga qyteti Tiranes përbëhej nga 400 njerëz, 378 prej tyre dhane përgjigje të plotë për pyetjen, dhe 22 prej tyre nuk deshen të përgjigjen. Mosha e te intervistuarve ishte 18 vjec e lart. Numri i pyetjeve ishte i 8 dhe ato ishin të gjitha pyetje te hapura. Pyetjeve në kete ankete ishin në lidhje me informacionin e te intervistuarve si mosha e tij, gjinore, dhe arsimit, mesatarja e të ardhurave, mendimin e tyre për shërbimet e sigurimit. Me këtë

Faqja 15

BEST, 26.06.10,

Pjesa e dyte b) Analiza statistikore e pyetesorit dhe vleresimi i hipotezave

Version i pare Shqip SIGURIME

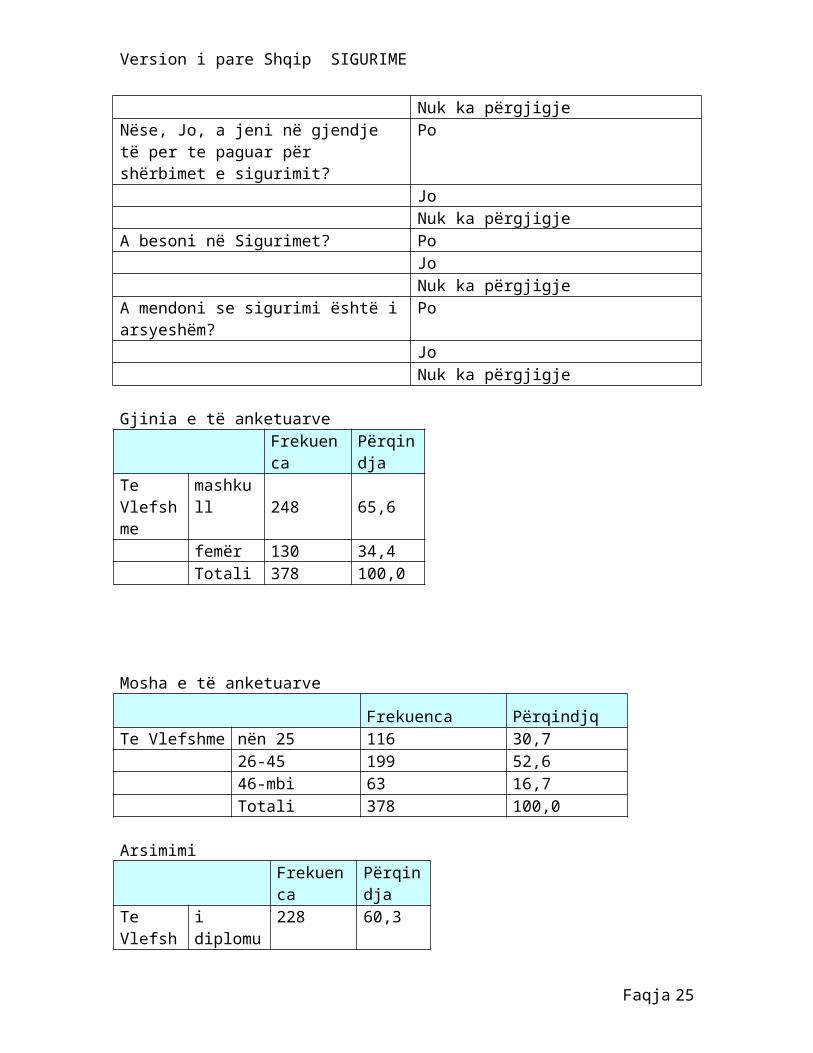

informacion do të kemi mundësi për të gjetur atë pjesë të popullsisë qe dinë për kompanitë e sigurimit dhe faktorët pse ata janë kundër shërbimeve te sigurimit? Këto janë arsyet përse ne jane zgjedhur keto hipoteza dhe qëllimi ynë është për të mësuar nga dokumentet e mbledhura. Ne kemi analizuar marrëdhëniet e klientit të shërbimeve të sigurimit në grupin tonë të parë. Ne konsiderojmë se pjesëmarrësit sa më shumë te perfshihen në procedurat e aplikimit aq më afër rezultatet jane me realitetin. Sikurse Kotler (1997) përshkruan në teorinë e tij është e mundur për të marrë një rezultat të mirë edhe nese numri i pjesëmarrësve është më pak se 1% e popullsisë në tërësi. Ne krijuam pyetesorin për të mbledhur informacion. Frekuencat A=GjiniaB = MoshaC = ArsimimiD = të ardhurat mujore të anketuaritE = A jeni i siguruar?F = A keni të ardhura të mjaftueshme për të qene i siguruar?G = A eshte sigurimi i arsyeshem?H = A besoni në sigurim? Gjinia: mashkull: femër:Mosha: nga 18 deri 25 nga 26 deri 45 nga 46 e lart Niveli i arsimit i aritur: Universitet Shkolla e mesmeTe ardhurat mujore: nën 50 000 LEK me teper se 50 000 LEKA perdorni sherbime sigurimeve? Po Jo Nuk ka përgjigjeNëse, Jo, a jeni në gjendje të per te paguar për shërbimet e sigurimit?

Po

Jo Nuk ka përgjigjeA besoni në Sigurimet? Po Jo Nuk ka përgjigjeA mendoni se sigurimi është i arsyeshëm?

Po

Jo

Faqja 16

Version i pare Shqip SIGURIME

Nuk ka përgjigje Gjinia e të anketuarve

Frekuenca

Përqindja

Te Vlefshme

mashkull 248 65,6

femër 130 34,4 Totali 378 100,0

Mosha e të anketuarve

Frekuenca PërqindjqTe Vlefshme nën 25 116 30,7 26-45 199 52,6 46-mbi 63 16,7 Totali 378 100,0 Arsimimi

Frekuenca

Përqindja

Te Vlefshme

i diplomuar

228 60,3

shkollim te mesme

150 39,7

Totali 378 100,0Te ardhurat mujore të të intervistuarve

Frekuenca

Përqindja

Te Vlefshme

nen 50.000 Lek 318 84,1

mbi 50.000 Lek

60 15,9

Totali 378 100,0A jeni i siguruar?

Frekuenca

Përqindja

Te Po 23 6,1

Faqja 17

Version i pare Shqip SIGURIME

Vlefshme Jo 355 93,9 Tota

li378 100,0

A keni të ardhura të mjaftueshme për të siguruar?

Frekuencë

Përqind

I vlefshëm

Po57 15,1

Jo 321 84,9 Tot

al378 100,0

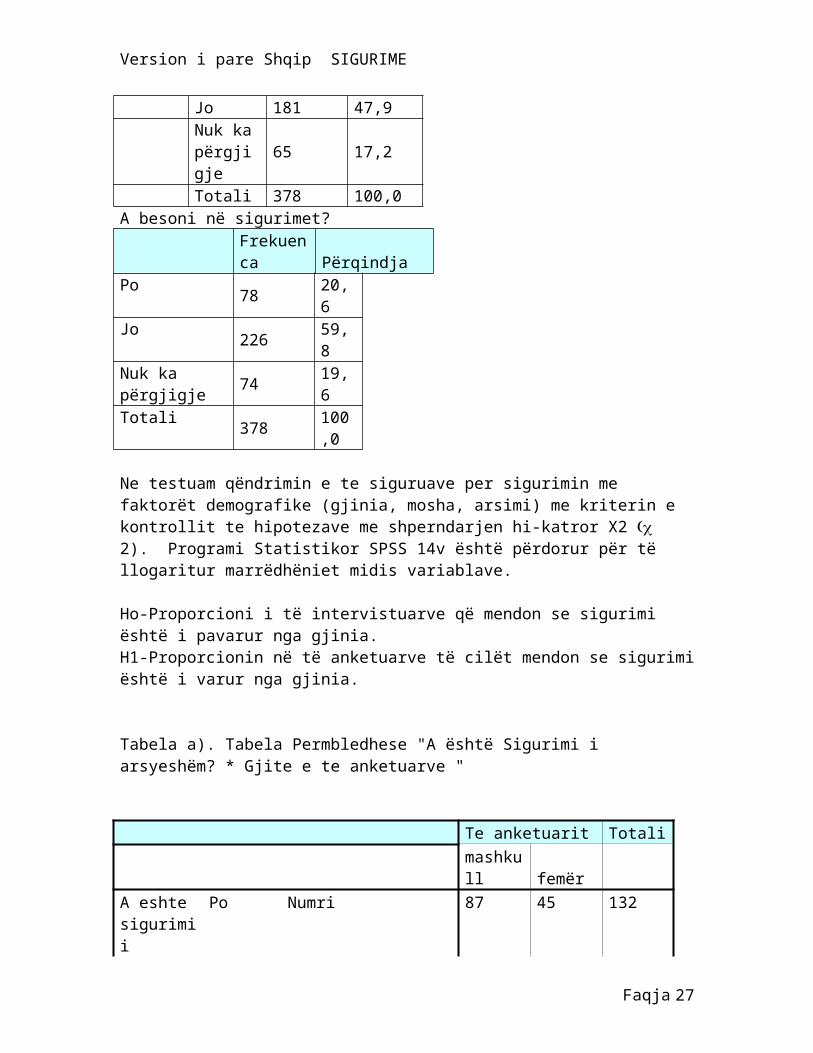

A është sigurimi i arsyeshem?

Frekuenca

Përqindja

Te Vlefshme

Po132 34,9

Jo 181 47,9 Nuk ka

përgjigje

65 17,2

Totali 378 100,0A besoni në sigurimet?

Frekuenca Përqindja

Po 78 20,6Jo 226 59,8Nuk ka përgjigje

74 19,6

Totali378

100,0

Ne testuam qëndrimin e te siguruave per sigurimin me faktorët demografike (gjinia, mosha, arsimi) me kriterin e kontrollit te hipotezave me shperndarjen hi-katror X2 2). Programi Statistikor SPSS 14v është përdorur për të llogaritur marrëdhëniet midis variablave. Ho-Proporcioni i të intervistuarve që mendon se sigurimi është i pavarur nga gjinia. H1-Proporcionin në të anketuarve të cilët mendon se sigurimi është i varur nga gjinia.

Faqja 18

Version i pare Shqip SIGURIME

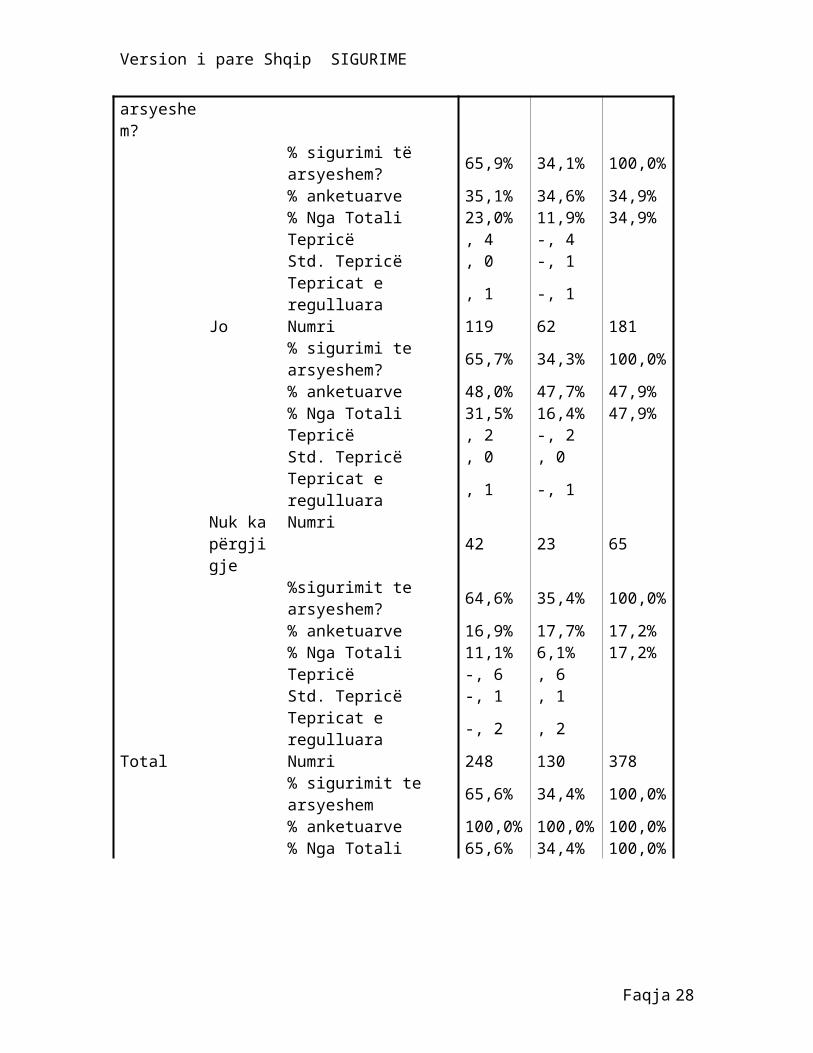

Tabela a). Tabela Permbledhese "A është Sigurimi i arsyeshëm? * Gjite e te anketuarve " Te anketuarit Totali

mashkull femër

A eshte sigurimi i arsyeshem?

Po Numri

87 45 132

% sigurimi të arsyeshem?

65,9% 34,1%100,0%

% anketuarve 35,1% 34,6% 34,9% % Nga Totali 23,0% 11,9% 34,9% Tepricë , 4 -, 4 Std. Tepricë , 0 -, 1 Tepricat e

regulluara, 1 -, 1

Jo Numri 119 62 181 % sigurimi te

arsyeshem?65,7% 34,3%

100,0%

% anketuarve 48,0% 47,7% 47,9% % Nga Totali 31,5% 16,4% 47,9% Tepricë , 2 -, 2 Std. Tepricë , 0 , 0 Tepricat e

regulluara, 1 -, 1

Nuk ka përgjigje

Numri42 23 65

%sigurimit te arsyeshem?

64,6% 35,4%100,0%

% anketuarve 16,9% 17,7% 17,2% % Nga Totali 11,1% 6,1% 17,2% Tepricë -, 6 , 6 Std. Tepricë -, 1 , 1 Tepricat e

regulluara-, 2 , 2

Total Numri 248 130 378 % sigurimit te

arsyeshem65,6% 34,4%

100,0%

% anketuarve 100,0 100,0 100,0

Faqja 19

Version i pare Shqip SIGURIME

% % % % Nga Totali

65,6% 34,4%100,0%

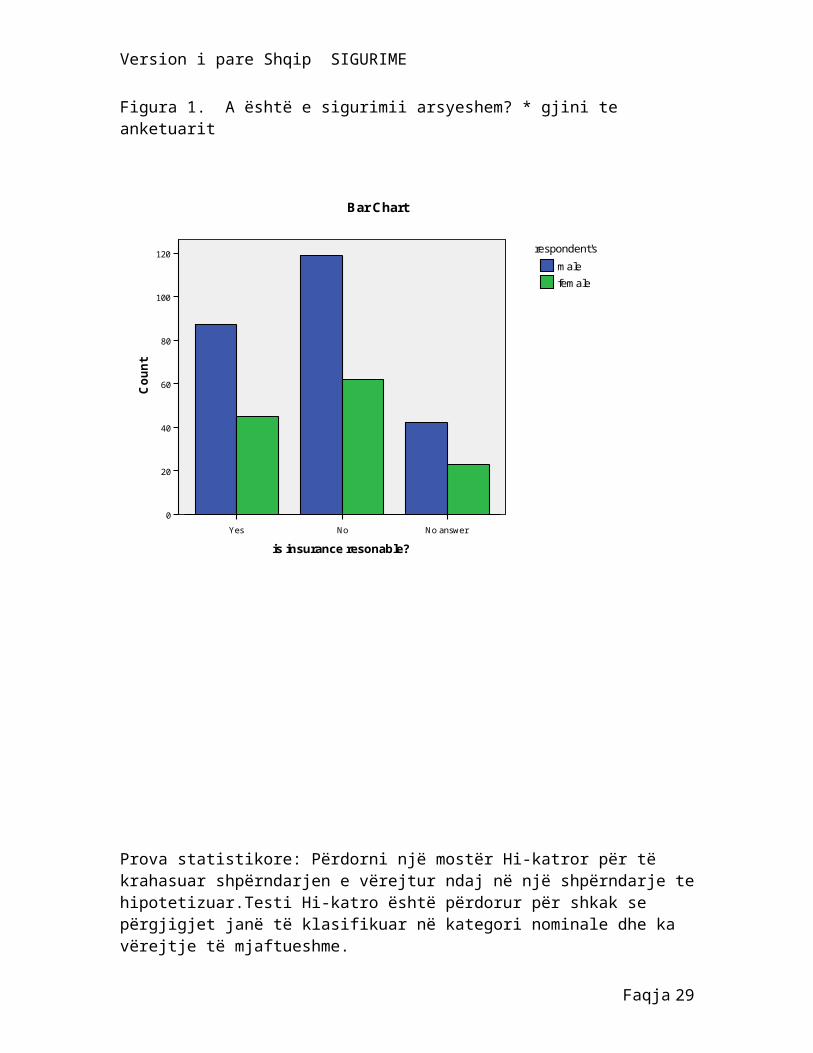

Figura 1. A është e sigurimii arsyeshem? * gjini te anketuarit

No answerNoYes

is insurance resonable?

120

100

80

60

40

20

0

Co

un

t

Bar Chart

female

male

respondent's

Prova statistikore: Përdorni një mostër Hi-katror për të krahasuar shpërndarjen e vërejtur ndaj në një shpërndarje te hipotetizuar.Testi Hi-

Faqja 20

Version i pare Shqip SIGURIME

katro është përdorur për shkak se përgjigjet janë të klasifikuar në kategori nominale dhe ka vërejtje të mjaftueshme.

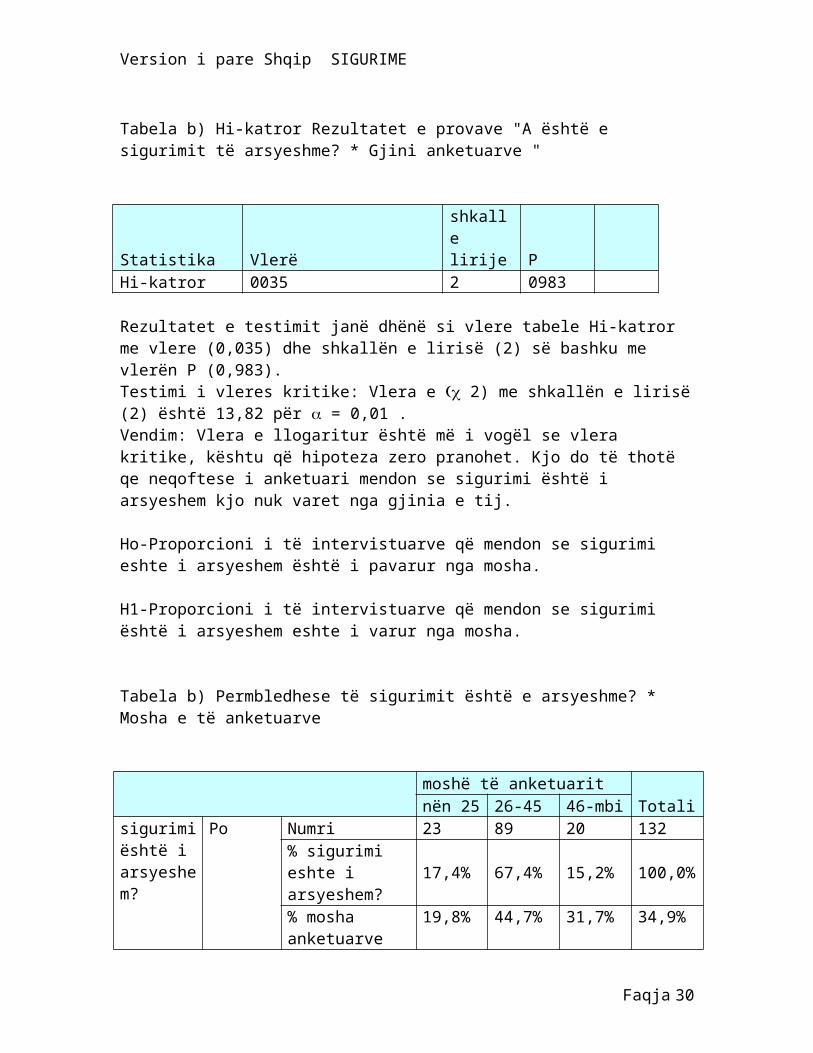

Tabela b) Hi-katror Rezultatet e provave "A është e sigurimit të arsyeshme? * Gjini anketuarve "

Statistika Vlerëshkalle lirije P

Hi-katror 0035 2 0983 Rezultatet e testimit janë dhënë si vlere tabele Hi-katror me vlere (0,035) dhe shkallën e lirisë (2) së bashku me vlerën P (0,983).Testimi i vleres kritike: Vlera e 2) me shkallën e lirisë (2) është 13,82 për = 0,01 .Vendim: Vlera e llogaritur është më i vogël se vlera kritike, kështu që hipoteza zero pranohet. Kjo do të thotë qe neqoftese i anketuari mendon se sigurimi është i arsyeshem kjo nuk varet nga gjinia e tij.

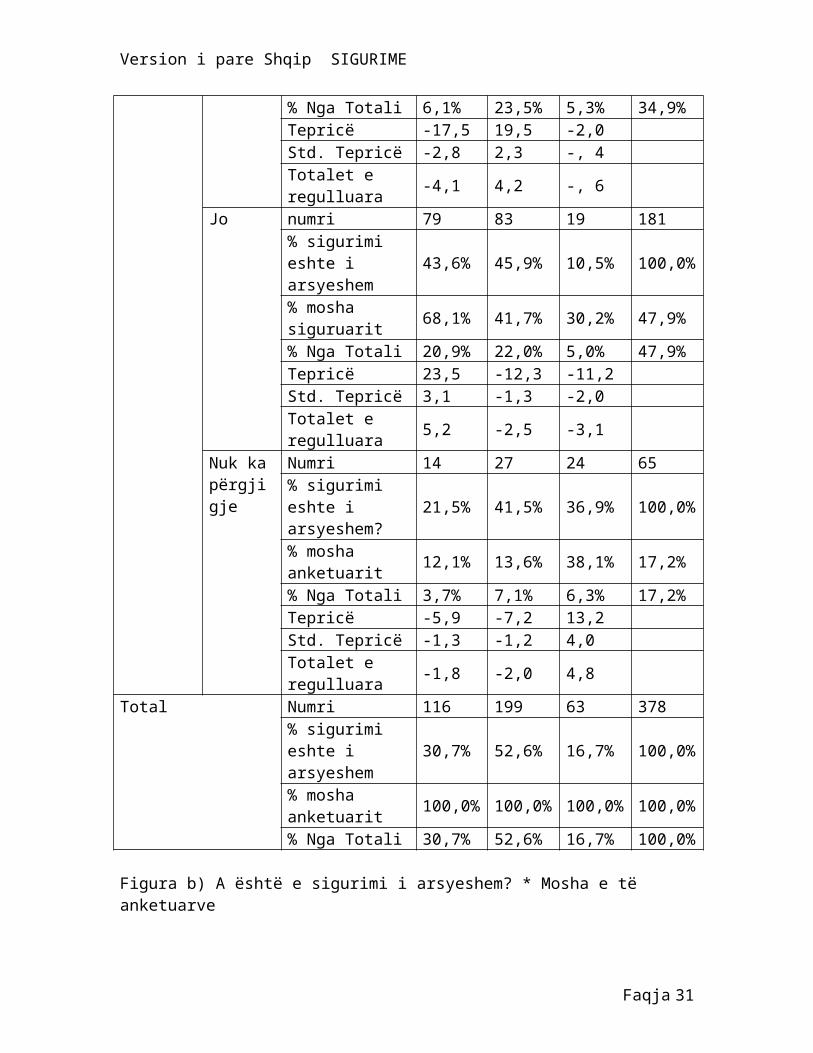

Ho-Proporcioni i të intervistuarve që mendon se sigurimi eshte i arsyeshem është i pavarur nga mosha. H1-Proporcioni i të intervistuarve që mendon se sigurimi është i arsyeshem eshte i varur nga mosha. Tabela b) Permbledhese të sigurimit është e arsyeshme? * Mosha e të anketuarve

moshë të anketuarit

Totalinën 25 26-45 46-mbisigurimi është i arsyeshem?

Po Numri 23 89 20 132% sigurimi eshte i arsyeshem?

17,4% 67,4% 15,2%100,0%

% mosha anketuarve

19,8% 44,7% 31,7% 34,9%

% Nga Totali 6,1% 23,5% 5,3% 34,9%Tepricë -17,5 19,5 -2,0 Std. Tepricë -2,8 2,3 -, 4 Totalet e regulluara

-4,1 4,2 -, 6

Jo numri 79 83 19 181% sigurimi 43,6% 45,9% 10,5% 100,0

Faqja 21

Version i pare Shqip SIGURIME

eshte i arsyeshem

%

% mosha siguruarit

68,1% 41,7% 30,2% 47,9%

% Nga Totali 20,9% 22,0% 5,0% 47,9%Tepricë 23,5 -12,3 -11,2 Std. Tepricë 3,1 -1,3 -2,0 Totalet e regulluara

5,2 -2,5 -3,1

Nuk ka përgjigje

Numri 14 27 24 65% sigurimi eshte i arsyeshem?

21,5% 41,5% 36,9%100,0%

% mosha anketuarit

12,1% 13,6% 38,1% 17,2%

% Nga Totali 3,7% 7,1% 6,3% 17,2%Tepricë -5,9 -7,2 13,2 Std. Tepricë -1,3 -1,2 4,0 Totalet e regulluara

-1,8 -2,0 4,8

Total Numri 116 199 63 378% sigurimi eshte i arsyeshem

30,7% 52,6% 16,7%100,0%

% mosha anketuarit

100,0%

100,0%

100,0%

100,0%

% Nga Totali30,7% 52,6% 16,7%

100,0%

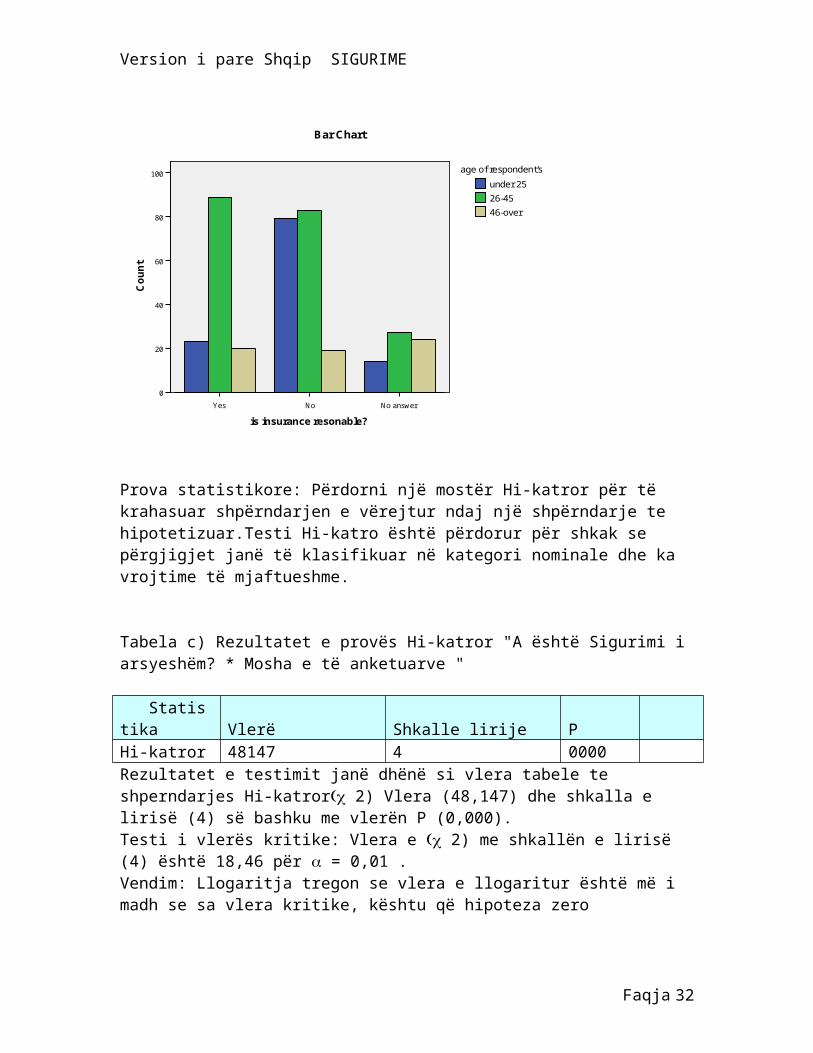

Figura b) A është e sigurimi i arsyeshem? * Mosha e të anketuarve

Faqja 22

Version i pare Shqip SIGURIME

No answerNoYes

is insurance resonable?

100

80

60

40

20

0

Co

un

tBar Chart

46-over

26-45

under 25

age of respondent's

Prova statistikore: Përdorni një mostër Hi-katror për të krahasuar shpërndarjen e vërejtur ndaj një shpërndarje te hipotetizuar.Testi Hi-katro është përdorur për shkak se përgjigjet janë të klasifikuar në kategori nominale dhe ka vrojtime të mjaftueshme. Tabela c) Rezultatet e provës Hi-katror "A është Sigurimi i arsyeshëm? * Mosha e të anketuarve " Statistika Vlerë Shkalle lirije P Hi-katror 48147 4 0000 Rezultatet e testimit janë dhënë si vlera tabele te shperndarjes Hi-katror 2) Vlera (48,147) dhe shkalla e lirisë (4) së bashku me vlerën P (0,000).Testi i vlerës kritike: Vlera e 2) me shkallën e lirisë (4) është 18,46 për = 0,01 .Vendim: Llogaritja tregon se vlera e llogaritur është më i madh se sa vlera kritike, kështu që hipoteza zero refuzohet. Nga kjo ne konkludojmë se mosha e te anketuarve ka rendesi ne vendimin e tyre ne lidhje me sigurimet .Shumica e te anketuarve (67,4%) mosha e te cileve eshte 26-45 supozojne se shërbimi i sigurimit është i domosdoshëm në jetë. Ne mund të konkludojmë se kjo pjesë e popullsisë në mënyrë aktive merr pjesë në jetën sociale dhe të biznesit, prandaj mendimi i tyre për

Faqja 23

Version i pare Shqip SIGURIME

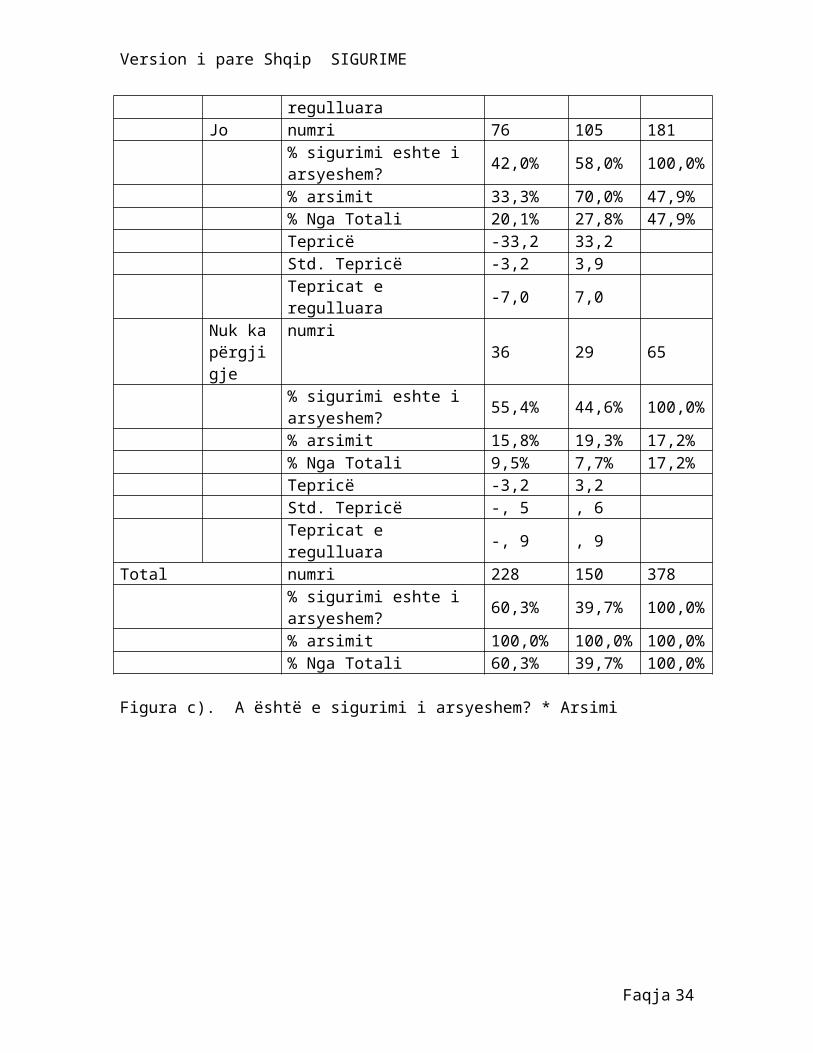

sigurim është pozitiv. Të anketuarit nën moshën 25 kanë mendim negativ për sigurim. Ne mendojmë se arsyet janë: Sipas informatave zyrtare nuk ka një lende mesimore të lidhur me sigurimin në shkolla dhe gjimnaze. Sipas hulumtimit tonë, njerezit e pa sigurua jane me teper (93,9%) se njerëzit e siguruar (6,1%). Kjo mund të thotë se nuk gjenden kushtet e tilla, për të rinjtë, qe të kenë mendimin e tyre në shoqëri. Ho-Proporcioni i të intervistuarve që mendon se sigurimi eshte i arsyeshem është i pavarur nga arsimi;H1-Proporcioni i të intervistuarve që mendon se sigurimi eshte i arsyeshem është i varur nga arsimi; Tabela c) Permbledhese "Eshte Sigurimi i arsyeshëm? * Arsimi " Arsimi Total

I diplomuar

shkollën e mesme

sigurimi është i arsyeshem?

Po numri

116 16 132

% sigurimi eshte i arsyeshem?

87,9% 12,1%100,0%

% arsimit 50,9% 10,7% 34,9% % Nga Totali 30,7% 4,2% 34,9% Tepricë 36,4 -36,4 Std. Tepricë 4,1 -5,0 Tepricat e regulluara 8,0 -8,0 Jo numri 76 105 181 % sigurimi eshte i

arsyeshem?42,0% 58,0%

100,0%

% arsimit 33,3% 70,0% 47,9% % Nga Totali 20,1% 27,8% 47,9% Tepricë -33,2 33,2 Std. Tepricë -3,2 3,9 Tepricat e regulluara -7,0 7,0 Nuk ka

përgjigje

numri36 29 65

% sigurimi eshte i arsyeshem?

55,4% 44,6%100,0%

% arsimit 15,8% 19,3% 17,2% % Nga Totali 9,5% 7,7% 17,2%

Faqja 24

Version i pare Shqip SIGURIME

Tepricë -3,2 3,2 Std. Tepricë -, 5 , 6 Tepricat e regulluara -, 9 , 9 Total numri 228 150 378 % sigurimi eshte i

arsyeshem?60,3% 39,7%

100,0%

% arsimit100,0%

100,0%

100,0%

% Nga Totali60,3% 39,7%

100,0%

Figura c). A është e sigurimi i arsyeshem? * Arsimi

No answerNoYes

is insurance resonable?

120

100

80

60

40

20

0

Co

un

t

Bar Chart

high school

graduated

education

Testi statistikor: Përdorim një mostër te tabeles Hi-katror 2) për të krahasuar shpërndarjen vërejtur me një shpërndarje te hipotetizuar .Shperndarja Hi-katror 2) është përdorur për shkak se përgjigjet janë të klasifikuar në kategori nominale, dhe ka vrojtime të mjaftueshme. Tabela d) HI-katror Rezultatet e provës "është Sigurimi i arsyeshëm? * Arsimi " Statika Vlerë shkalle lirije P

Faqja 25

Version i pare Shqip SIGURIME

Hi-katror 67956 2 0000 Rezultatet e testimit janë dhënë ne fillim si vlera tabele te Hi-katror 2) Vlera (67,956) dhe shkallën e lirisë (2) së bashku me vlerën P (0,000).Vlera kritike e testuar: Vlera e 2) me shkallën e lirisë (2) është 13,82 për =0,01 .Vendim: Vlera e llogaritur është më e madhe se vlera kritike, kështu që hipoteza zero refuzohet. Nga kjo ne konkludojmë se të anketuarit ndikohen nga arsimi në vendimin e tyre mbi sigurimet.Shumica e të anketuarve (87,9%) me arsim të lartë jane të mendimit se shërbimet e sigurimit janë të nevojshme. Ne mendojmë se arsyet janë: Shumica e universiteteve kane disa lende të biznesit si lëndët e detyruara.Shumica e studentëve zakonisht përpiqen të fillojnë biznesin e tyre ose janë të angazhuar tashmë në biznese të vogla, të mesme ose biznese të medha. Kjo është arsyeja pse ata janë të interesuar me shumë në sistemin ekonomik duke përfshirë edhe sistemin e sigurimeve.

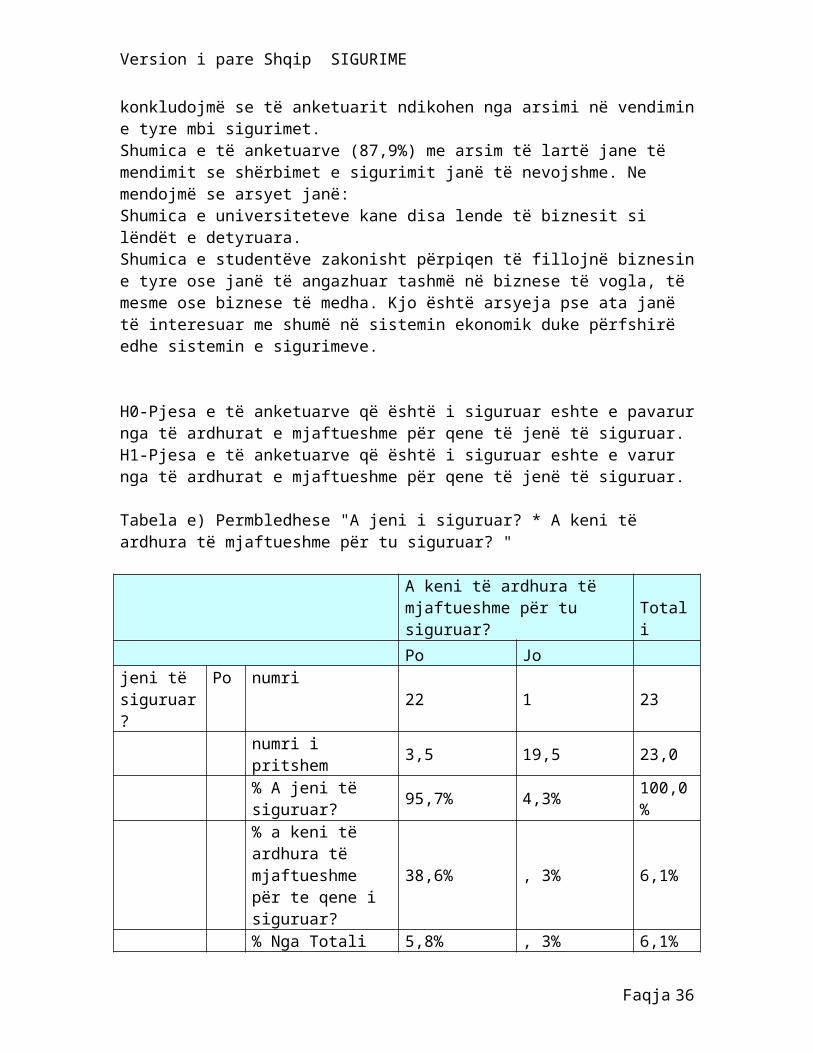

H0-Pjesa e të anketuarve që është i siguruar eshte e pavarur nga të ardhurat e mjaftueshme për qene të jenë të siguruar. H1-Pjesa e të anketuarve që është i siguruar eshte e varur nga të ardhurat e mjaftueshme për qene të jenë të siguruar. Tabela e) Permbledhese "A jeni i siguruar? * A keni të ardhura të mjaftueshme për tu siguruar? "

A keni të ardhura të mjaftueshme për tu siguruar? Totali

Po Jo jeni të siguruar?

Po numri22 1 23

numri i pritshem 3,5 19,5 23,0 % A jeni të

siguruar?95,7% 4,3%

100,0%

% a keni të ardhura të mjaftueshme për te qene i siguruar?

38,6% , 3% 6,1%

% Nga Totali 5,8% , 3% 6,1% Tepricë 18,5 -18,5

Faqja 26

Version i pare Shqip SIGURIME

Std. Tepricë 10,0 -4,2 Teprice e

regulluar11,1 -11,1

Jo numri 35 320 355 numri i pritshem 53,5 301,5 355,0 % a jeni të

siguruar?9,9% 90,1%

100,0%

% a keni të ardhura të mjaftueshme për te qene i siguruar?

61,4% 99,7% 93,9%

% Nga Totali 9,3% 84,7% 93,9% Tepricë -18,5 18,5 Std. Tepricë -2,5 1,1 tepricat e

regulluara-11,1 11,1

Total numri 57 321 378 numri i pritshem 57,0 321,0 378,0 % a jeni të

siguruar?15,1% 84,9%

100,0%

% a keni të ardhura të mjaftueshme për të qene i siguruar?

100,0% 100,0%100,0%

% Nga Totali15,1% 84,9%

100,0%

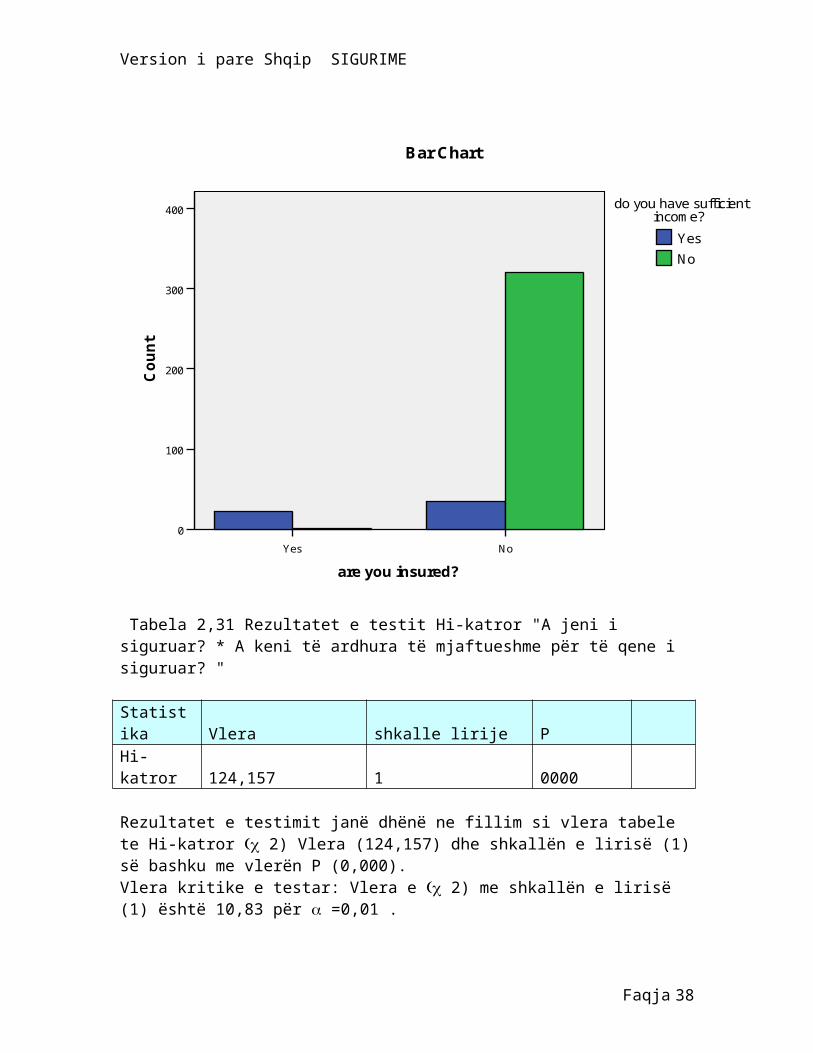

Figura e). "A jeni i siguruar? * A keni të ardhura të mjaftueshme për të qene i siguruar? "

Faqja 27

Version i pare Shqip SIGURIME

NoYes

are you insured?

400

300

200

100

0

Co

un

tBar Chart

No

Yes

do you have sufficient income?

Tabela 2,31 Rezultatet e testit Hi-katror "A jeni i siguruar? * A keni të ardhura të mjaftueshme për të qene i siguruar? " Statistika Vlera shkalle lirije P Hi-katror 124,157 1 0000 Rezultatet e testimit janë dhënë ne fillim si vlera tabele te Hi-katror 2) Vlera (124,157) dhe shkallën e lirisë (1) së bashku me vlerën P (0,000).Vlera kritike e testar: Vlera e 2) me shkallën e lirisë (1) është 10,83 për =0,01 .Vendim: Vlera e llogaritur është më i madh se vlera kritike, kështu që hipoteza zero refuzohet. Kjo do të thotë se mosperdorimi i shërbimin te sigurimit nga njerëzit varet nga mjaftueshmeria e te ardhurave te tyre për tu siguruar.

Faqja 28

Version i pare Shqip SIGURIME

Si perfundim nga analiza e anketes se mbledhur ne Tirane me pyetje te pergjithsme rreth anketuesve dhe mendimit te tyre mbi sigurimet arrijme ne perfundimet e meposhtme, po te marim si baze testimin e hipotezave me shperndarjen Hi-katror me vlera standarte :

Neqoftese personi mendon se sigurimi është i arsyeshem kjo nuk varet nga gjinia e tij .

Mosha e individeve ka rendesi ne vendimin e tyre ne lidhje me sigurimet.

Individet ndikohen nga arsimi në vendimin e tyre mbi sigurimet. Mosperdorimi i shërbimin te sigurimit nga njerëzit varet nga

mjaftueshmeria e te ardhurave te tyre për tu siguruar.

Meqenese nga Analiza rezultoi se sasia e sigurimeve qe blen nje individ ka nje varesi te larte nga te ardhurat e tij, do te qe e nevojshme qe te studionim se perse shtresa e varfer e popullsise ka nje perqasje kaq te vogel ne tregun e sigurimeve. Siç shihet dhe nga Grafiket ku jane mbivendosur primet me te ardhurat per secilen prefekture, verehet qe perveç prefektures se Tiranes pjesa tjeter e prefekturave kane nje perqindje shpenzimesh

Faqja 29

BEST, 26.06.10,

Pjesa e trete Arsyet pse nuk jane te siguruar Trajtim teorik

Version i pare Shqip SIGURIME

disa here me te vogel per sigurimet. Kjo na çon te mendojme se tregu ka nje moseficence ne kete pjese te tij.Per te gjetur perse shtresa e varfer e shqiptareve nuk jane te siguruar u ngriten kater hipoteza , te lidhura dhe me shkaqet qe parashtron shpesh dhe literatura, ne lidhje me shkaqet qe cojne ne moseficence te tregut nga te dy krahet , oferte e kerkese. Krahu i ofertes u medua se nuk kishte eficence per keto tre arye :

1) Kosto me te larta transaksioni per produktet me prime te uleta2) Zgjedhja e keqe , rriku moral dhe mashtrimi eshte me i larte per personat me te

ardhura me te uleta3) Pamundesi shkallezimi te produkteve te sigurimit per personat e varfer

Kurse krahu i kerkeses kishte vec nje arsye te vetme qe e pengonte shtresen me te ardhura te uleta qe te qasej prane ketij tregu:

4) Mungesa e antipatise ndaj riskut, mungesa e informacionit , racionlitetit dhe moskuptimi i produkteve te sigurimev

Mbi bazen e ketyre arsyeve te mesiperme u ndertuan kater hipoteza.

We in turn test the hypotheses that the market for microinsurance is impeded by (1)transaction costs, (2) adverse selection, moral hazard and fraud, (3) lack of scalability, (4) lack of risk aversion, information, understanding andrationality. We reject the first three hypotheses and find that insurers and grupet e perbashket in cooperation can reduce transaction costs, adverse selection, moral hazard and fraud to levels which make microinsurance feasible. Further we find that the products currently offered by Albanian insurers are commensurately scalable (with the exception of health insurance) and offer significant risk reduction potential to low income clients, indicating that the products offered are not ill-suited to the clients’ needs. However, we find evidence that, although risk averse, the target population for microinsurance products is widely unaware of microinsurance availability, lacks financial literacy and understanding of basic insurance concepts impeding the demand for microinsurance. Hypothesis 4 can thus not be rejected.

Since the 1970s, the academic discourse on uncertainty has gained momentum and bothimperfect information and its resulting market failures have been included into contemporary microeconomics. Though not widely discussed in academic textbooks up until now, uncertainty is the foundation of insurance theory. Two major assumptions with respect to the consumers are made in the theory of uncertainty (Mas-Collel et al., 1995). First, the expected utility theorem is assumed to hold. It states that utility functions have the expected utility form (Neumann-Morgenstern utility function), i.e. aggregate utility is equal to the sum of the probability weighted utilities of each possible outcome. Second, individuals are assumed to be risk averse. Due to risk aversion, the individual is willing to trade risk for certainty because it derives additional utility from a certain outcome (Dionne, 2000). More generally, if the price for insurance is fair, i.e. the premium equals

Faqja 30

BEST, 29.06.10,

Paragrafi me poshte vendoset ne pjeset e para te tezes

Version i pare Shqip SIGURIME

the expected indemnity payment of the insurance company, the individual prefers the certain outcome over any other outcome with non-zero variance (Schlesinger, 2006). In addition, Mossin’s theorem (1968) explains that if all preceding assumptions hold, the individual is fully insured. Loewenstein et al. (2001) argue that even if the price is not fair i.e. the insurance company keeps a profit, the individual might still opt for insurance because of potential non-pecuniary benefits (e.g. peace of mind) from being insured. Directly hinging on the assumption that insurance policies are fairly priced is the assumption that insurers themselves are risk neutral towards risk or are able to perfectlydiversify the risks they are insuring. Roth & Athreye (2005) claim that insurance companies are indeed risk neutral towards microinsurance related exposures as these are dwarfed by the size of their overall portfolio.9 Further, some risks are by definition more diversifiable than others: a very high degree of diversification can be reached for life and accident insurance while polices insulating farmers from draughts or natural disasters bear a great deal of covariant risk (Churchill et al., 2006).

Ne tregun e mikrosigurimit mund te themi se Throughout the academic literature we have reviewed, the simplest definition for microinsurance we came across is “insurance for the poor”. This is inanalogy to microcredit, which is in fact credit for the poor. Similarly, Warren Brown (2001) defines microinsurance as insurance for low-income people. Churchill et al. (2006) reinforce this point by stating that microinsurance and conventional insurance are similar except that the former referring to a clearly prescribed target market: low-income people. There is no clear cut-off point between microinsurance and conventional insurance. Microinsurance is primarily directed at people below and at the poverty line, sometimes also marginally above it. Apart from addressing different people, microinsurance is not substantially different from conventional insurance theory with respect to the major insurance characteristics. The same assumptions are made as outlined above and microinsurance is also affected by asymmetric information and market failures like adverse selection and moral hazard. In addition, due to its small scale layout microinsurance is much more exposed to transaction costs than conventional insurance (Morduch, 2002). Ne baze te punimeve te autoreve te ndyshem dhe hipotezave te meparshme, koncepti i microinsurance is a recent development in the financial industry which has evolved less then ten years ago. Due to its short history, the amount of academic literature on the topic is neither abundant nor undisputed. Currently, microinsurance is seen as the next step of financial integration of the poor after the microcredit programmes seem to become relatively well established. This section provides an overview of the previous research on microinsurance. We thereby focus on the relevant literature that relates to our research question. As such, we analyse the reasoning for underinsurance of the poor. The majority of the literature is case based and analyzes the experiences with microinsurance in different countries. Most of the studies on microinsurance are prepared by a hand full of world wide operating organizations and working groups.Four major arguments for underinsurance of the poor can be identified in the literature and are discussed subsequently. Correspondingly, we derive four hypotheses, based on these arguments, on why the poor are underinsured.

Faqja 31

Version i pare Shqip SIGURIME

1.) Transaction costThe single most important argument for underinsurance of low-income people in the literature relates to transaction costs. Morduch (2002) acknowledges that transaction costs are often preventing microinsurance from being provided by commercial insurance companies. Ahuja et al. (2005) go a step further by stating that this lack of affordability prevents the potential demand from expressing itself in the market. Microinsurance causes higher transaction costs than conventional insurance at almost every stage of the insurance transaction. Selling insurance to the poor is costly due to the large amount of low premium contracts. Servicing insurance, handling and controlling claims and paying out benefits is equally more costly (McCord, 2002). Transaction costs have to be brought down to make insurance affordable. In order to be able to provide microinsurance on a large scale, the choice of the right distribution channel is crucial (Churchill, 2006). Four different insurance distribution models are outlined in the literature: First, the insurer can distribute the policies himself. This subsequently is referred to as the direct sales channel. Second, grupet e perbashket can set up insurance schemes on their own accounts; they are most of the time operating under the radar of regulators because the latter don’t want the former to take on excessive risks. Third, mutuals can provide insurance as well. They are usually professionally managed, regulated member-owned and offer the advantage of operating close to the people. Fourth, community-based organizations can offer insurance. They are member-owned, unregulated and by their very nature very close to the clients (Roth et al., 2007). For the purpose of our analysis, we discuss the first model and then focus on a combination of both, the first and the second model, the so-called partner-agent model. Discussing the partner-agent model we mendojme se si do te funksiononte nese grupet e perbashketa do te providing close to area-wide coverage of poor and marginally poor families. Most of the literature focuses on the transaction costs the insurer is faced with. This neglects the fact that those insured also incur substantial transaction costs. We discuss the transaction costs of both parties involved, the insurer as well as the insured. The central role of transaction costs in microinsurance leads to the derivation of the firsthypothesis which is discussed in this paper:

Hypothesis 1: Transaction costs are proportionally higher for microinsurance than forconventional insurance.

2.) Adverse selection, moral hazard and fraudAdverse selection refers to an ex-ante asymmetric information problem of hidden information. Akerlof (1970) uses the analogy of the markets for used cars to illustrate that with uncertainty and information asymmetry the market does not necessarily clear resulting in an inefficient allocation. Adverse selection and moral hazard are best prevented by designing the insurance policy such that the incentives are aligned already from the outset. Examples include copayment which would render a given policy unattractive for risky insurance takers. If prevention by design is not feasible, the insured as well as the insurance will try to reduce adverse selection by signalling and screening, respectively (Jehle et al., 2001). Moral hazard is a problem of hidden action and formally is a part of principal-agent theory. It refers to postcontractual actions caused by the

Faqja 32

Version i pare Shqip SIGURIME

principle’s inability to observe the agent’s actions. Therefore, the principal has to design an incentive scheme so that the agent takes the appropriate action (Jehle et al., 2001). Fraud, i.e. deliberately causing damage or claiming damage which has not occurred is best addressed by monitoring. While moral hazard might occur due to a non-conscious change in behaviour, fraud always happens deliberately. For simplicity, despite fraud not being a market failure in a strict sense, we treat it as such for the purpose of this section.While these market failures are also prevalent in conventional insurance, they might be more important to microinsurance, preventing the microinsurance market from developing. Previous research suggests that for certain kinds of insurance, these market failures are indeed detrimental. Whenever, these market failures can not be avoided by design, means such as signalling and screening will be employed, leading to transaction cost. Because these tend to accrue as absolute costs rather than as proportions of the premium, small scale schemes are obviously hit harder. Nevertheless, there are innovative ways around both problems: Group insurance is getting more and more popular and co-payments as well as lapsing periods and first year exclusions are not uncommon (Churchill et al., 2003). Typically damage due to negligent behaviour is also excluded. According to Herrera et al. (2004), the problem is fairly small in life and accident insurance as death claims are easy to verify and the sum assured is not high enough to result into reckless behaviour. Mommens (2006) analyzes the case of cropinsurance. In agriculture, the costs of screening are very high so the insurance is unable to tell a good from a bad farmer before selling insurance (adverse selection). Moreover, high monitoring costs prevent the insurance from controlling if the farmer still takes care of the field appropriately after taking insurance. In health insurance, adverse selection, moral hazard and fraud are even more detrimental. People might be encouraged to overuse the health system or wait too long to seek medical treatment in the case of critical illness insurance (Churchill et al., 2006). In this study, we want to investigate the extent to which adverse selection, moral hazard and fraud are responsible for the underinsurance of the poor. Consequently the next hypothesis is as follows.

Hypothesis 2: Microinsurance is exposed to severer problems of adverse selection, moralhazard and fraud than is conventional insurance.

3.)ScalabilityAlthough not explicitly labelled scalability problem, previous research indicates that it might not be possible to provide some specific microinsurance policies due to the inability to scale the premium and benefits to a level that is affordable for poor people. Two conditions have to be fulfilled for microinsurance to be scalable. The premium needs to be directly related to the benefit and the benefit in turn should be somehow related to the income of the person (Churchill et al., 2003). The first condition is straight forward. If fair pricing is assumed, the condition should hold automatically. The second condition, however, is more complicated and depends on the type of insurance. While life insurance can easily be scaled down to microinsurance levels (benefits depend on income), health insurance is probably the most complicated insurance to scale down (benefits are almost not dependent on income as they have to cover a certain

Faqja 33

Version i pare Shqip SIGURIME

sickness) . In the literature, the scalability problem is often treated together with the asymmetric information and transaction cost problems. In this thesis, we want to look at all the three effects separately.The third hypothesis is therefore formulated as follows:

Hypothesis 3: Conventional insurance products can not be scaled down to the extentnecessary for providing microinsurance

4.) Risk aversion, information, understanding and rationalityThe demand for microinsurance is largely unexplored. Most of the studies are ratherqualitative in nature and not based on representative samples. Previous research givesdifferent reasons for underinsurance of the poor: First, alternative informal risk mitigationmechanisms like self-insurance11 and communal insurance are mentioned. It is acknowledged, however, that these mechanisms are inherently unstable and cover only small impact events due to idiosyncratic risks (Churchill et al., 2006). Second, lack of information and understanding seems to be a major determinant reducing effective insurance demand (Manje et al., 2002). This includes among other factors mistrust towards the insurance company due to bad experiences or word of mouth, the inability to distinguish between insurance and saving as well as the expectation to get money back at the end of the policy. Third, ignorance about insurance products and risks in life are used to explain the (partial) underinsurance (Roth et al., 2007). We want to add a discussion on rationality to this point and argue that people might think and act bounded rational or even irrational in certain situations which causes demand to fall short of what it could be.

Argumentimi per vertetetesine ose jo per secilen hipoteze :

1.) Transaction cost

Hypothesis 1: Transaction costs are proportionally higher for microinsurance than forconventional insurance In the following we examine whether transaction costs are the reason why insurance products are not offered to the poor.

First, the different kinds of transaction costs are defined. Second, we evaluate whether they are proportionally lower for microinsurance than for conventional insurance in the direct sales model. Third, the partner-agent model is introduced to show how transaction costs in microinsurance can be brought down as to ultimately reject hypothesis 1. In the context of microinsurance, transaction costs are incurred by the insurance company aswell as the insured individual. Transaction costs of the insurer include (1) educatingimperfectly informed clients on the merits of taking insurance products to reduce the financial volatility in their lives, (2) conducting due diligence and screening clients to prevent adverse selection, moral hazard and fraud and finally (3) servicing existing insurance contracts e.g. collecting and disbursing money. The clients, too, incur transaction cost largely due to (4) conducting due diligence on different insurance products pre-contract, (5) meeting documentation requirements set by the insurer and (6) costs associated with the exchange of money, most notably paying monthly or annual premiums to the insurer. We in turn discuss the six costs mentioned above and analyse

Faqja 34

Version i pare Shqip SIGURIME

the extent to which they differ when insurance products are scaled down to match the demand of the poor. This is done for two different microinsurance distribution channels: First, we look at transaction costs if the insurance offers insurance directly to the poor. Second, we analyse the costs in the socalled partner-agent model.

7.1.1 Direct Sales Model (insurance company sells insurance directly to the poor)

Transaction costs for insurance company:(1) Poor clients are on average less financially literate than wealthy ones. Consequently, the insurance agent needs to spend more time on each client increasing transaction costs for the insurance company. However, the salary of the insurance agent in the rural areas is lower, so it is unclear if transaction costs in absolute terms decrease or increase. However, due to the considerably lower scale of premium and cover transaction costs make up a larger share of the premium. (2) Pre-contractual screening and due diligence are the most common forms of transaction costs related to information asymmetries. The insurance company largely transfers these costs to the client by imposing specific documentation requirements depending on the type of insurance. Nevertheless, it has to bear the cost of collection and processing of these documents. These documents are collected in the central offices of the insurance companies so the costs of processing are probably the same independently of the size of the policy. Hence, transaction costs are higher as a proportion of premiums. As a consequence, insurance companies might be inclined to shift part of their due diligence for the lower premium policies from pre-contract to post claim (Churchill et al., 2006). This reduces the costs somewhat and we expect transaction costs to be comparable to conventional insurance in relative terms.(3) Generally speaking, the cost of collecting premiums and disbursing money in case ofadverse events should be relatively constant and independent of the size of the premiums.However, two cost factors differentiate microinsurance and conventional insurance: First,rural clients largely don’t have bank accounts so the insurance either needs a local presence or has to send an agent to collect and disburse the money. In urban areas with wealthier clients, all this is done through bank accounts. Second, lower premium products often have lower frequencies of payment reducing transaction costs. For policies with high premiums, the payments are more likely to take place on a monthly basis. Summarizing, transaction costs of premium collection and benefit disbursement are likely to be higher for microinsurance in absolute and relative terms.