TEL OFFSHORE TRUST 2009 Federal Income Tax Information

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TEL OFFSHORE TRUST

2009

Federal Income Tax Information

- 1 -

TEL OFFSHORE TRUST

FEDERAL INCOME TAX INFORMATION

This booklet provides 2009 tax information which will allow Unit Holders to determine their pro rata share of income and deductions attributable to their investment in TEL Offshore Trust (the “Trust”). Each Unit Holder is encouraged to read the entire booklet very carefully. The material herein is not intended and should not be construed as professional tax or legal advice. Each Unit Holder should consult the Unit Holder’s own tax advisor regarding all tax compliance matters relating to the Units.

Instructions for Schedules A, B and C

Schedule A For Unit Holders who file income tax returns on the basis of the calendar year and the cash method during 2009, the Trustee has prepared Schedule A as an EXAMPLE which summarizes the income and expenses (for depletion computation see Schedule C below) required to prepare 2009 tax returns as if the Unit Holder had held 100 Units during all of 2009. Schedule B Schedule B summarizes the quarterly income and expenses (for depletion computation see Schedule C below) on a one Unit basis. In accordance with the Partnership Agreement and the Trust Agreement, income and deductions for each quarter are deemed to be realized on the quarterly record date for that quarter and are allocated to the Unit Holders of record on that date. Therefore, Schedule B is prepared on a quarterly basis. Each Unit Holder using Schedule B should compute his tax information by using the relevant information for each quarter for which he was a Unit Holder of record. Then the results of all appropriate quarters should be combined. Schedule C Schedule C should be used by all Unit Holders to compute depletion. Schedule C summarizes quarterly depletion rates on a one Unit basis. Calendar year Unit Holders who acquired their Units in the initial distribution from Tenneco Offshore Company, Inc. and continue to own those Units should use Schedule C, Part I. Other Unit Holders who acquired their Units subsequent to the initial distribution from Tenneco Offshore Company, Inc. should use Schedule C, Part II. Unit Holders who acquired Units after October 11, 1990, may be entitled to percentage depletion on royalty income attributable to those Units and should use Schedule C, Part III. I. FEDERAL INCOME TAX INFORMATION 1. Reporting of Income and Deductions. (a) Direct Ownership Reporting. The Internal Revenue Service (“IRS”) has ruled that the Trust is a grantor trust and that the TEL Offshore Trust Partnership (“Partnership”) is a partnership for federal income tax purposes. Thus, all information is reported on the basis that the Trust is a grantor trust and the Partnership is a partnership. On that basis, each Unit Holder is taxable on his pro rata share of the income and expense of the Trust as if he were the direct owner of an undivided interest in the assets of the Trust. Moreover, for federal income tax purposes, each Unit Holder should be treated as a partner in the Partnership. As a result, each Unit Holder is required to take into account his pro rata share of all items of Partnership income and deductions in computing his federal income tax liability. The Partnership’s accrual method of accounting will control the timing of a Unit Holder’s recognition of income and expense. A Unit Holder’s own method of accounting controls the timing of recognition of Trust income and expense other than that attributable to the Partnership, however.

- 2 -

(b) Taxable Year. The Partnership determines taxable income on a calendar year basis. Therefore, Unit Holders with taxable years other than the calendar year will report their portions of Partnership income in their taxable years in which or with which the Partnership taxable year ends. All schedules are prepared on a calendar year basis. Therefore, Unit Holders with taxable years other than a calendar year or who are unable to use Schedule A should use Schedules B and C. Schedules B and C are prepared by quarter on a per Unit basis to permit Unit Holders to obtain their tax information by computing the relevant information for each quarter during the taxable year and then combining the results of each quarter. In accordance with the Partnership Agreement, income and deductions of the Partnership for each quarter are allocated to the Unit Holders of record on the last business day of that quarter. The taxable year for reporting a Unit Holder’s share of the remaining items of the Trust, for example, interest income and administration expenses, is controlled by his taxable year. The taxable year of the Trust is irrelevant, as is the period in which distributions are made by the Trust. (c) Unit Multiplication. Because Schedules B and C show only results per Unit, it will be necessary to multiply the results shown by the number of Units owned by the Unit Holder during the applicable period to obtain the amount to be reported on his tax return. Income and deductions other than depletion may be taken directly from the appropriate schedules. Depletion per Unit must be computed as provided in paragraph 2 below. (d) Individual Taxpayer. For Unit Holders who held Units as an investment during 2009 and who file Form 1040, it is suggested that the items of income and deduction for 2009 be reported in the following manner: Item Form 1040

Partnership Income (Royalties) Line 4, Part I, Schedule E

Depletion Line 20, Part I, Schedule E

Interest Income Line 1, Part I, Schedule B

Administration Expense Line 23, Schedule A

Royalty income is considered portfolio income. Since all income from the Partnership is royalty income, this amount, net of depletion, is portfolio income and, subject to certain exceptions and transitional rules, this royalty income cannot be offset by losses from passive businesses. Additionally, interest income is portfolio income. Administration expense is an investment expense. See Exhibits I through III for examples of how to report the items listed above. (e) Widely Held Fixed Investment Trust Information. The Trustee assumes that some Units are held by a middleman, as such term is broadly defined in U.S. Treasury Regulations (and includes custodians, nominees, certain joint owners, and brokers holding an interest for a custodian in street name). Therefore, the Trustee considers the Trust to be a non-mortgage widely held fixed investment trust (“WHFIT”) for U.S. federal income tax purposes. The Bank of New York Mellon Trust Company, N.A. (“Trustee”), 919 Congress Avenue, Austin, Texas 78701, telephone number 1-800-852-1422, is the representative of the Trust that will provide tax information in accordance with applicable U.S. Treasury Regulations governing the information reporting requirements of the Trust as a WHFIT. Notwithstanding the foregoing, the middlemen holding Units on behalf of Unit Holders, and not the Trustee of the Trust, are solely responsible for complying with the information reporting requirements under the U.S. Treasury Regulations with respect to such Units, including the issuance of IRS Forms 1099 and certain written tax statements. Unit Holders whose Units are held by middlemen should consult with such middlemen regarding the information that will be reported to them by the middlemen with respect to the Units.

- 3 -

2. Computation of Depletion. Subject to the date restrictions for percentage depletion discussed herein, each Unit Holder should determine his depletion allowance by taking the greater of cost or percentage depletion allowable. In years prior to 1991, percentage depletion was not available; therefore, Unit Holders needed only to determine cost depletion. However, as a result of the Revenue Reconciliation Act of 1990 (the “1990 Act”), Unit Holders may be eligible for percentage depletion with respect to royalty income attributable to Units acquired after October 11, 1990. Consequently, if Units were acquired on or before October 11, 1990, Unit Holders need only determine cost depletion. (a) Cost Depletion. Each Unit Holder is entitled to compute cost depletion with respect to his share of royalty income received through the Partnership based on his basis in the overriding royalty interest (equivalent to a 25% net profits interest) in certain productive oil and gas properties (the “Royalty”). Unit Holders who acquired their Units in the initial distribution from Tenneco Offshore Company, Inc. and continued to hold those Units through December 31, 2009 need not compute cost depletion since that computation has been done and the amount is shown on Schedule C, Part I (on a per Unit basis). All other Unit Holders must compute cost depletion by multiplying their Royalty basis (original cost of the Units, less prior years’ depletion, and, for Unit Holders who acquired their units on or before December 17, 1984, less basis allocated to the sale by the Trust of Offshore II stock in 1984) by the depletion percentages listed on Schedule C, Part II, for each quarter for which he was a Unit Holder of record, and then combining the results. Unit Holders who acquired Units after December 17, 1984 will have a Royalty basis equal to the purchase price of those Units, less prior years’ depletion. (b) Percentage Depletion. Generally, prior to the 1990 Act, the transferee of an oil and gas property could not claim percentage depletion with respect to production from that property if it was proven at the time of transfer. As a result of the 1990 Act, this rule will not be applicable in the case of transfers of properties after October 11, 1990. Thus eligible Unit Holders that acquired Units after October 11, 1990, are entitled to claim an allowance for percentage depletion with respect to royalty income attributable to those Units to the extent that this allowance exceeds cost depletion as computed above for the relevant period. Percentage depletion with respect to these Units may be calculated using the per Unit factor on Schedule C, Part III. This factor was obtained by multiplying the corresponding Royalty income factor on Schedule B by the statutory percentage depletion rate of 15%. Percentage depletion should then be compared to the cost depletion calculated for the relevant period for these Units. The depletion allowance with respect to Units acquired after October 11, 1990, will be the greater of cost or percentage depletion. 3. Sale of Units. The sale, exchange or other disposition of a Unit is treated for federal income tax purposes as the sale of an interest in the Partnership. Gain or loss is computed under the usual tax principles as the difference between selling price and adjusted basis of a Unit. The adjusted basis of a Unit is the original cost or other basis of the Unit reduced by any depletion allowed or allowable, and, for Unit Holders who acquired their Units on or before December 17, 1984, less basis allocated to the sale by the Trust of Offshore II stock in 1984. This amount should also be adjusted for any increases or decreases in the Reserve Account during the time the Units were owned. Effective for property placed in service after December 31, 1986, the amount of gain, if any, realized upon the disposition of oil and gas property is treated as ordinary income to the extent of the intangible drilling and development costs incurred with respect to the property and depletion claimed with respect to that property to the extent it reduced the taxpayer’s basis in the property. Depletion attributable to a positive Section 743(b) adjustment of a Unit acquired after 1986 will be subject to recapture as ordinary income upon disposition of the Unit or upon disposition of an oil and gas property to which the depletion is attributable. The balance of any gain or any loss will be capital gain or loss if that Unit was held by the Unit Holder as a capital asset, either long-term or short-term depending on the holding period of the Unit. That capital gain or loss will be long-term if a Unit Holder’s holding period for those Units exceeded one year as of the date of sale or exchange. A long-term capital gains rate of 15% applies to most capital assets sold with a holding period of more than one year. Capital gain or loss will be short-term if the Unit has not been held for more than one year at the time of disposition. Capital gain or loss should be reported on Schedule D, Form 1040 for an individual.

- 4 -

4. Reconciliation of Net Income and Cash Distributions - Reserve Account. The difference between the per Unit net income for a period and the per Unit cash distributions reported for that period (even though distributed in a later period) is attributable to adjustments in the Reserve Account. The Reserve Account is increased by expenditures which are not deductible and by increases in the cash reserve established by the Trustees for the payment of future expenditures. The Reserve Account is decreased by the recoupment of capital items and by reductions in previously established cash reserves. 5. Foreign Persons. The federal income taxation of non-resident aliens and foreign corporations is highly complex, and it is recommended that these persons consult their own tax advisors. 6. Tax-Exempt Organizations. The Royalty and interest income of the Partnership should not be unrelated business taxable income so long as, generally, a Unit Holder did not incur debt to acquire a Unit or otherwise incur or maintain a debt that would not have been incurred or maintained if that Unit had not been acquired. Legislative proposals have been made from time to time which, if adopted, would result in the treatment of Royalty income as unrelated business taxable income. 7. Adjustments to Basis. Each Unit Holder should reduce his tax basis in his Units by the amount of depletion allowable. Each Unit Holder should also increase his basis in the Units by his pro rata share of any increase in the Reserve Account and decrease his basis in the Units by his pro rata share of any decrease in the Reserve Account. II. STATE INCOME TAX RETURNS Income attributable to the Royalty is not derived from any specific state since the leases are federal offshore leases. Therefore, the laws of the state of residence of each Unit Holder should determine if the Unit Holder will be subject to a state tax liability on income received as a result of ownership of Units. Unit Holders should consult their own tax advisors regarding the applicability of state income tax laws to their individual circumstances. The Bank of New York Mellon Trust Company, N.A. Corporate Trustee 919 Congress Avenue Austin, TX 78701 (800) 852-1422

Partnership Trust TrustUnits Income Interest Administration

Date Held (Royalties) Income Expense

100 $0.00 $0.01 $6.98100 0.00 $0.01 $4.44100 0.00 $0.00 $4.94100 0.00 $0.00 $4.08

Totals $0.00 $0.02 $20.44

Line 4, Line 1, Line 23,Part I, Part I, Schedule A

Schedule E Schedule B

NET INCOME: Partnership Income (Royalties) $0.00 Trust Interest Income 0.02 Less: Trust Administration Expense (20.44)DECREASE (INCREASE) IN RESERVE* 20.42TOTAL (Equals Cash Distribution)** $0.00

** Includes taxes withheld from amounts distributable to non-resident aliens and foreign corporations.

TEL OFFSHORE TRUSTEIN 76-6004064

TAX INFORMATION FOR THE YEAR 2009

Schedule A: Unit Holder Calculations

4,751,510 Units Outstanding

For Unit Holders Who File Returns On The Calendar Year Basis And The Cash Method

EXAMPLEThe calculations below are based on 100 Units held each record date.

December 31, 2009

(See Schedule B for factors used in the calculations).

* Increase or decrease in the reserve account has no tax effect (other than its effect on the tax basis of a Unit) and is shown for information purposes only.

Reconciliation Of Net Income And Cash Distribution

March 31, 2009June 30, 2009September 30, 2009

- 5 -

Partnership Trust TrustIncome Interest Administration

Date (Royalties) Income Expense

$0.000000 $0.000121 $0.0697870.000000 0.000080 0.0444390.000000 0.000043 0.0494090.000000 0.000037 0.040836

Totals $0.000000 $0.000281 $0.204471

Line 4, Line 1, Line 23,Part I, Part I, Schedule A

Schedule E Schedule B

NET INCOME: Partnership Income (Royalties) $0.000000 Trust Interest Income 0.000281 Less: Trust Administration Expense (0.204471)DECREASE (INCREASE) IN RESERVE* 0.204190TOTAL (Equals Cash Distribution)** $0.000000

** Includes taxes withheld from amounts distributable to non-resident aliens and foreign corporations.

TEL OFFSHORE TRUSTEIN 76-6004064

TAX INFORMATION FOR THE YEAR 2009

(See examples on pages 9 through 11.)

EXAMPLEMultiply amounts per Unit shown below by the number of Units owned on each

record date. Combine the results and report where indicated on Form 1040.

4,751,510 Units Outstanding

Schedule B: One Unit Factors

For Unit Holders Who File Returns On The Calendar Year Basis And The Cash Method

* Increase or decrease in the reserve account has no tax effect (other than its effect on the tax basis of a Unit) and is shown for information purposes only.

Reconciliation Of Net Income And Cash Distribution

March 31, 2009June 30, 2009September 30, 2009December 31, 2009

- 6 -

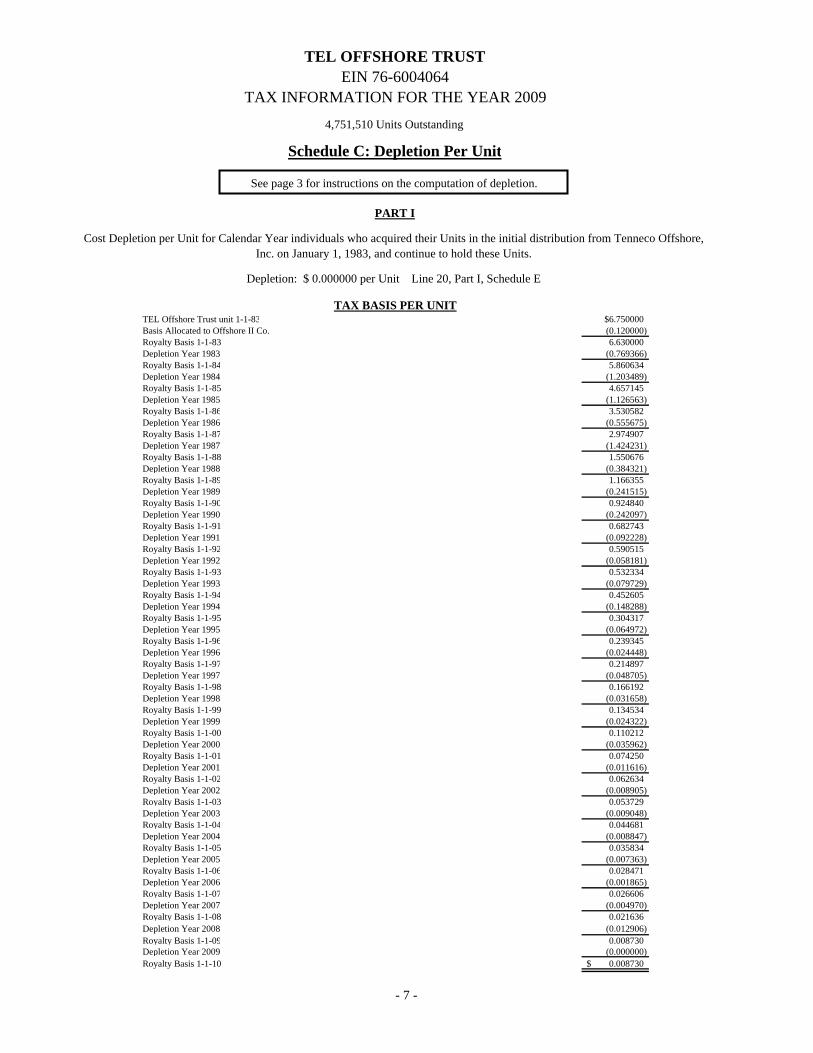

TEL Offshore Trust unit 1-1-83 $6.750000Basis Allocated to Offshore II Co. (0.120000)Royalty Basis 1-1-83 6.630000Depletion Year 1983 (0.769366)Royalty Basis 1-1-84 5.860634Depletion Year 1984 (1.203489)Royalty Basis 1-1-85 4.657145Depletion Year 1985 (1.126563)Royalty Basis 1-1-86 3.530582Depletion Year 1986 (0.555675)Royalty Basis 1-1-87 2.974907Depletion Year 1987 (1.424231)Royalty Basis 1-1-88 1.550676Depletion Year 1988 (0.384321)Royalty Basis 1-1-89 1.166355Depletion Year 1989 (0.241515)Royalty Basis 1-1-90 0.924840Depletion Year 1990 (0.242097)Royalty Basis 1-1-91 0.682743Depletion Year 1991 (0.092228)Royalty Basis 1-1-92 0.590515Depletion Year 1992 (0.058181)Royalty Basis 1-1-93 0.532334Depletion Year 1993 (0.079729)Royalty Basis 1-1-94 0.452605Depletion Year 1994 (0.148288)Royalty Basis 1-1-95 0.304317Depletion Year 1995 (0.064972)Royalty Basis 1-1-96 0.239345Depletion Year 1996 (0.024448)Royalty Basis 1-1-97 0.214897Depletion Year 1997 (0.048705)Royalty Basis 1-1-98 0.166192Depletion Year 1998 (0.031658)Royalty Basis 1-1-99 0.134534Depletion Year 1999 (0.024322)Royalty Basis 1-1-00 0.110212Depletion Year 2000 (0.035962)Royalty Basis 1-1-01 0.074250Depletion Year 2001 (0.011616)Royalty Basis 1-1-02 0.062634Depletion Year 2002 (0.008905)Royalty Basis 1-1-03 0.053729Depletion Year 2003 (0.009048)Royalty Basis 1-1-04 0.044681Depletion Year 2004 (0.008847)Royalty Basis 1-1-05 0.035834Depletion Year 2005 (0.007363)Royalty Basis 1-1-06 0.028471 Depletion Year 2006 (0.001865) Royalty Basis 1-1-07 0.026606 Depletion Year 2007 (0.004970) Royalty Basis 1-1-08 0.021636 Depletion Year 2008 (0.012906) Royalty Basis 1-1-09 0.008730 Depletion Year 2009 (0.000000)Royalty Basis 1-1-10 0.008730$

4,751,510 Units Outstanding

TAX BASIS PER UNIT

Depletion: $ 0.000000 per Unit Line 20, Part I, Schedule E

TEL OFFSHORE TRUSTEIN 76-6004064

TAX INFORMATION FOR THE YEAR 2009

Cost Depletion per Unit for Calendar Year individuals who acquired their Units in the initial distribution from Tenneco Offshore, Inc. on January 1, 1983, and continue to hold these Units.

See page 3 for instructions on the computation of depletion.

Schedule C: Depletion Per Unit

PART I

- 7 -

Depletion AsA Percent of

Date Royalty Basis

March 31, 2009 0.0000%June 30, 2009 0.0000%September 30, 2009 0.0000%December 31, 2009 0.0000%

TOTAL 0.0000%

TentativePercentageDepletion

Date Per Unit

March 31, 2009 $0.000000June 30, 2009 $0.000000September 30, 2009 $0.000000December 31, 2009 $0.000000

TOTAL $0.000000

Schedule C: Depletion Per Unit

See page 3 for instructions on the computation of depletion.

Percentage Depletion per Unit for Calendar Year individuals who acquired their Units after October 11, 1990.

PART III

Cost Depletion for Calendar Year individuals who acquired their Units subsequent to the distribution in January, 1983.

PART II*

* For Unit Holders acquiring Units other than in the initial distribution from Tenneco Offshore Company, Inc. and prior to Dec. 17, 1984, their Royalty basis should be equal to 98.2533% of their basis in their Units. Unit Holders who acquired their Units after Dec. 17, 1984 will have a basis in the Royalty equal to the purchase price of these Units, less depletion for the years 1985 through 2009.

4,751,510 Units Outstanding

TEL OFFSHORE TRUSTEIN 76-6004064

TAX INFORMATION FOR THE YEAR 2009

- 8 -

- 9 -

TEL OFFSHORE TRUST EIN 76-6004064

Exhibit I

Individual Unit Holder’s Specific Location Of Items On Schedule E

Royalty Income

Depletion

- 10 -

TEL OFFSHORE TRUST EIN 76-6004064

Exhibit II

Individual Unit Holder’s Specific Location Of Administration Expense On Schedule A

Administration Expense

- 11 -

TEL OFFSHORE TRUST EIN 76-6004064

Exhibit III

Individual Unit Holder’s Specific Location Of Interest Income On Schedule B

Interest Income

(This page has been left blank intentionally.)

(This page has been left blank intentionally.)

Related Documents

![Federal Income Tax - Basic Federal Income Tax, 1st Ed. - Westin - Law ...[1]](https://static.cupdf.com/doc/110x72/577d34ae1a28ab3a6b8e9712/federal-income-tax-basic-federal-income-tax-1st-ed-westin-law-1.jpg)