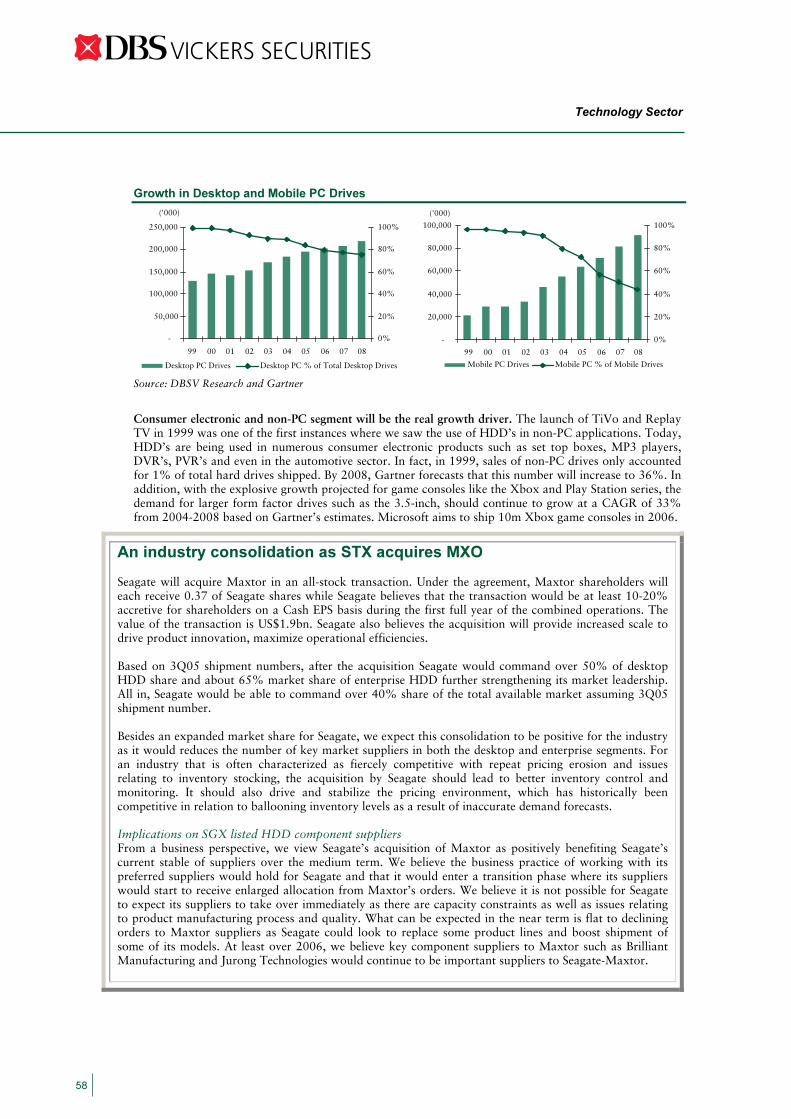

12 January 2006 Sector Focus Singapore Equity Research Refer to important disclosures at the end of this report In addition to the disclaimer at the end of this report, please note that DBS Vickers Securities (Singapore) Pte Ltd has been appointed as the designated market maker of structured warrant(s) Creative, CSM and Venture Corporation issued by DBS Bank. Technology Sector 2006 • Neutral weighting for 1Q06 • Promising outlook in 2006 driven by communications and consumer electronics segments • Still advocates stock picking and favors CSM, UTAC, ElectroTech, Magnecomp, DMX, FIRST & HUAN www.dbsvickers.com SINGAPORE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

12 January 2006

Sector Focus

Singapore Equity Research

Refer to important disclosures at the end of this report In addition to the disclaimer at the end of this report, please note that DBS Vickers Securities (Singapore) Pte Ltdhas been appointed as the designated market maker of structured warrant(s) Creative, CSM and VentureCorporation issued by DBS Bank.

Technology Sector 2006

• Neutral weighting for 1Q06 • Promising outlook in 2006 driven by communications

and consumer electronics segments • Still advocates stock picking and favors CSM, UTAC,

ElectroTech, Magnecomp, DMX, FIRST & HUAN

ww

w.d

bsv

icke

rs.c

om

ww

w.d

bsv

icke

rs.c

om

SIN

GA

POR

E

Technology Sector

Table of Contents

Investment Summary 3

Technology – Still Neutral for now 8

Technology – Crystal ball gazing in 2006 11

25

Computers 30

Communications 34

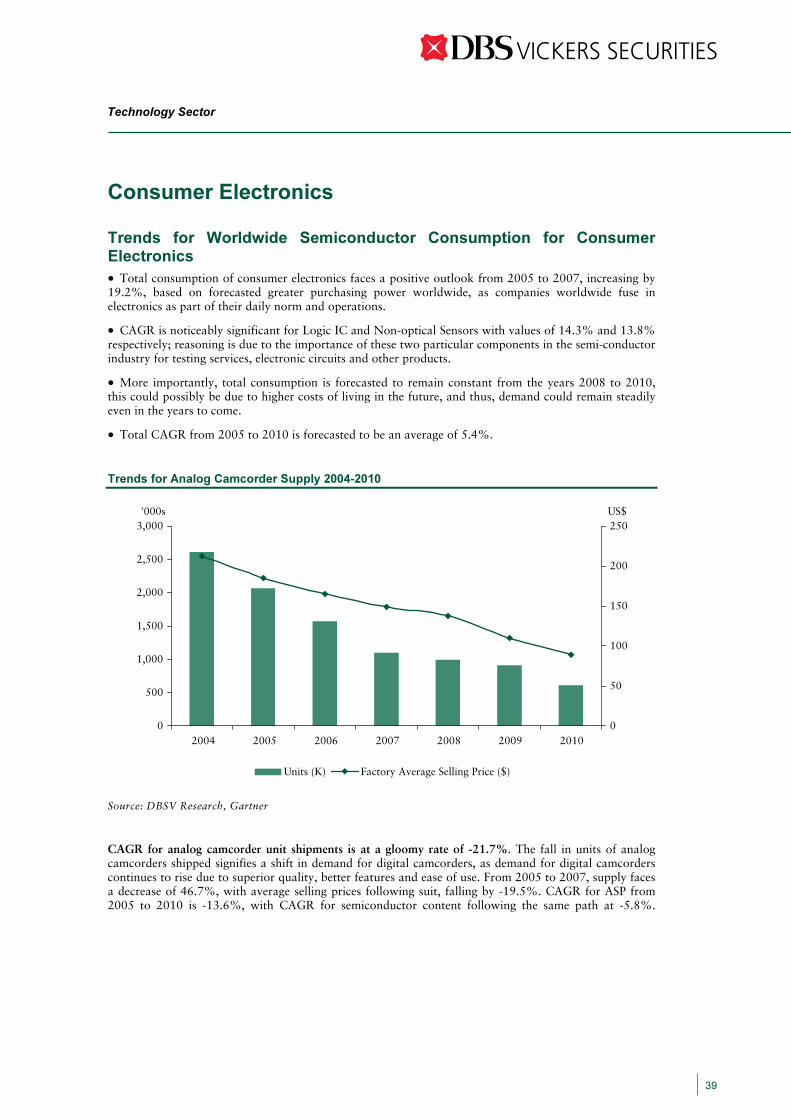

Consumer Electronics 39

Outlook for the Hard Disk Drive Segment 57

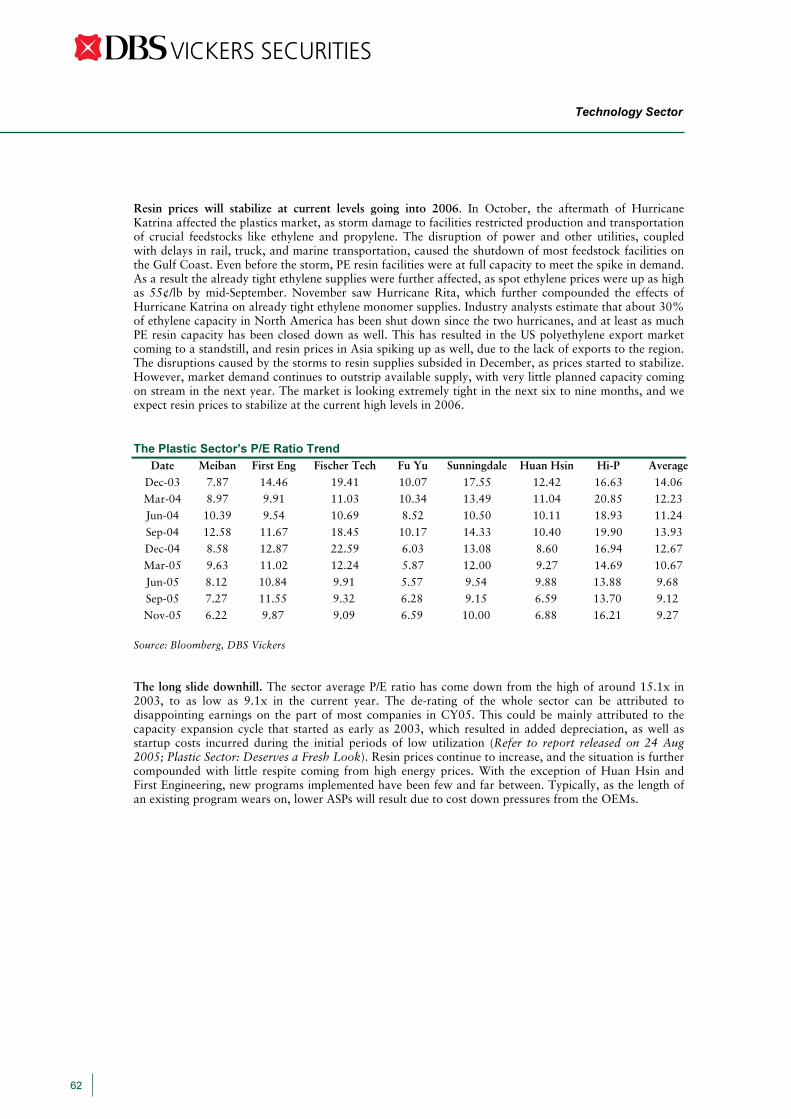

Outlook for the Plastic Manufacturing Segment 61

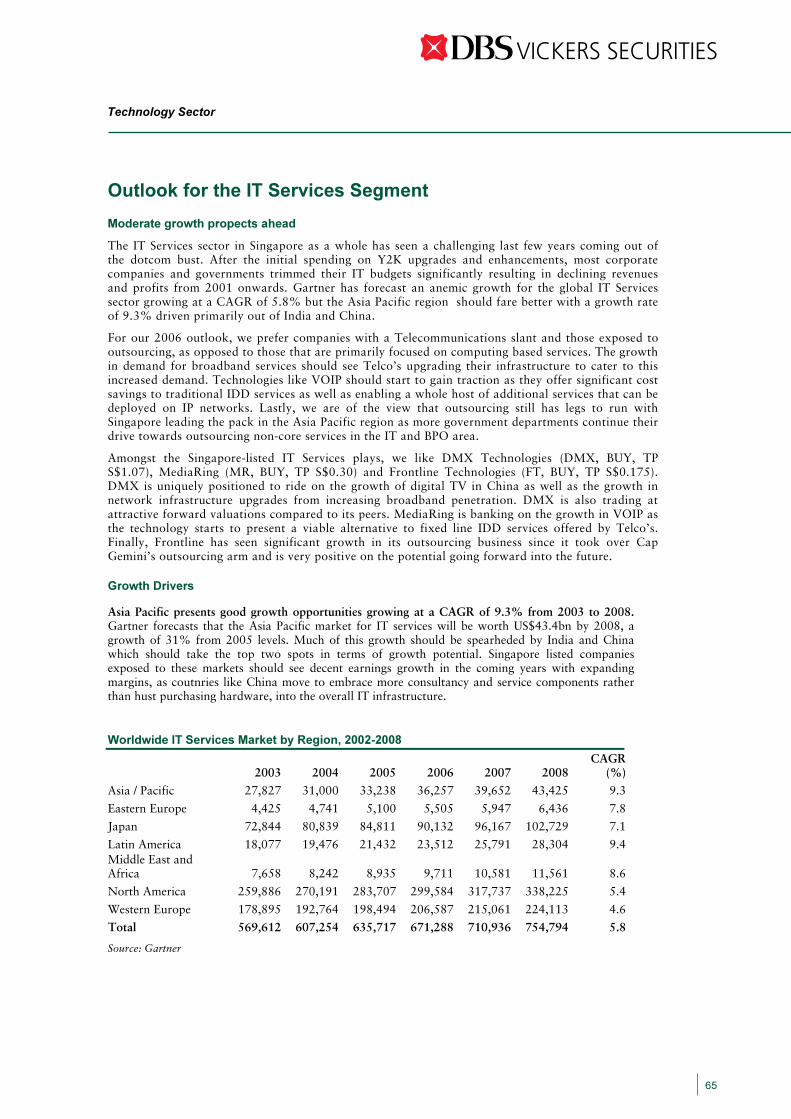

Outlook for the IT Services Segment 65

Company Focus

Chartered Semiconductor 68

DMX 70

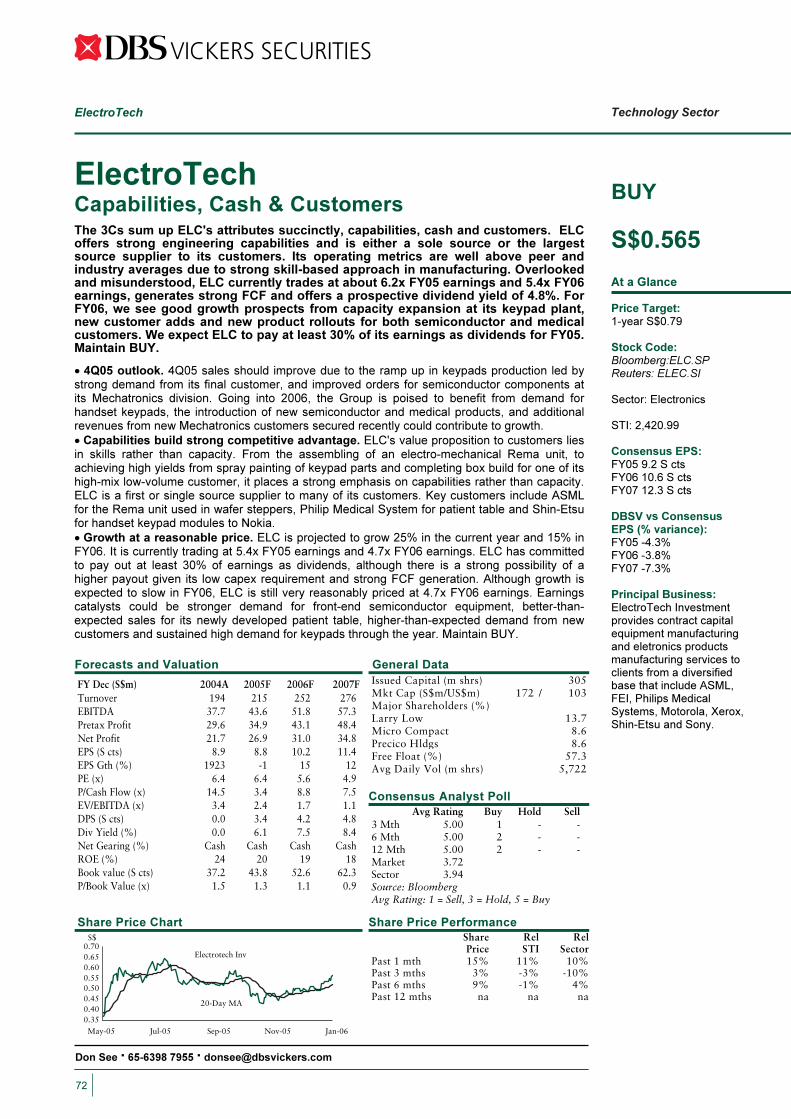

Electrotech 72

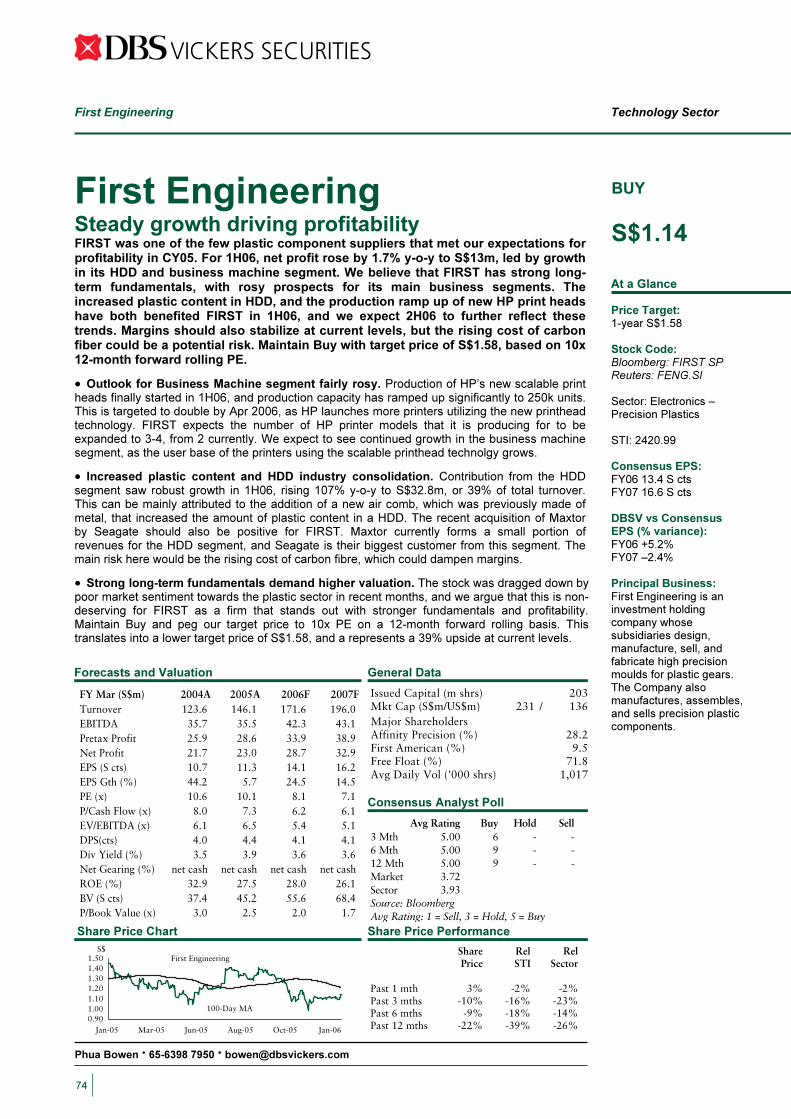

First Engineering 74

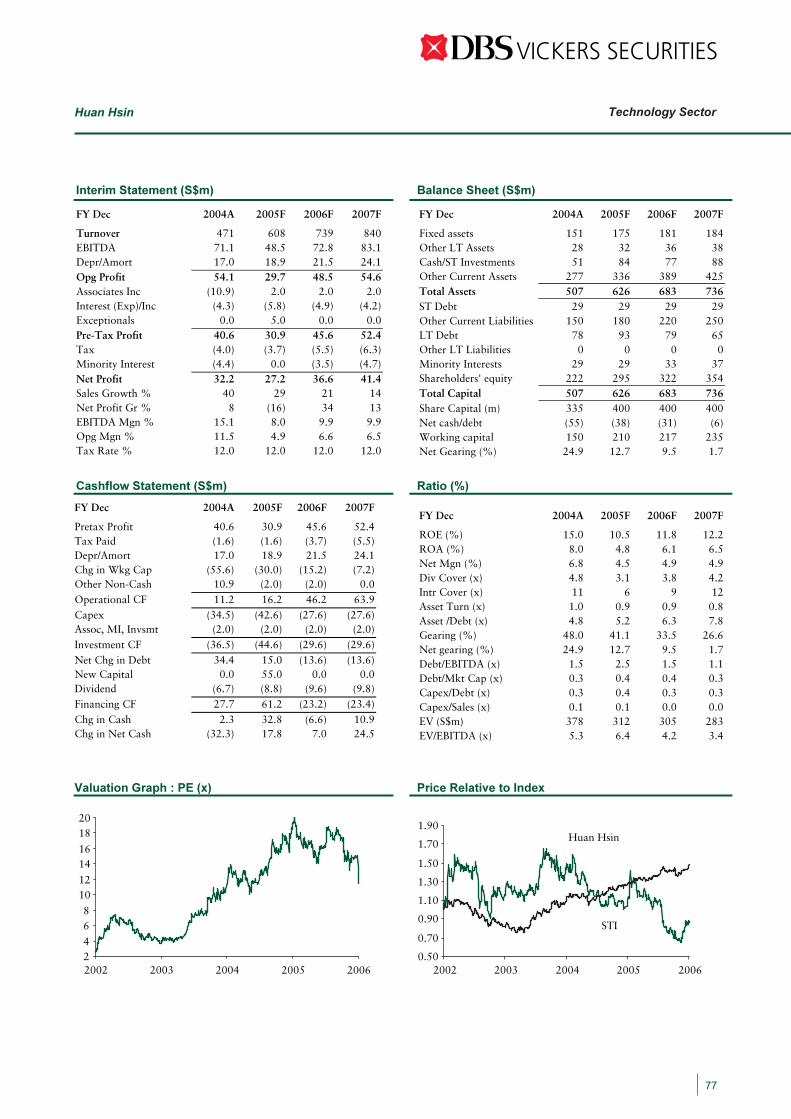

Huan Hsin 76

Magnecomp 78

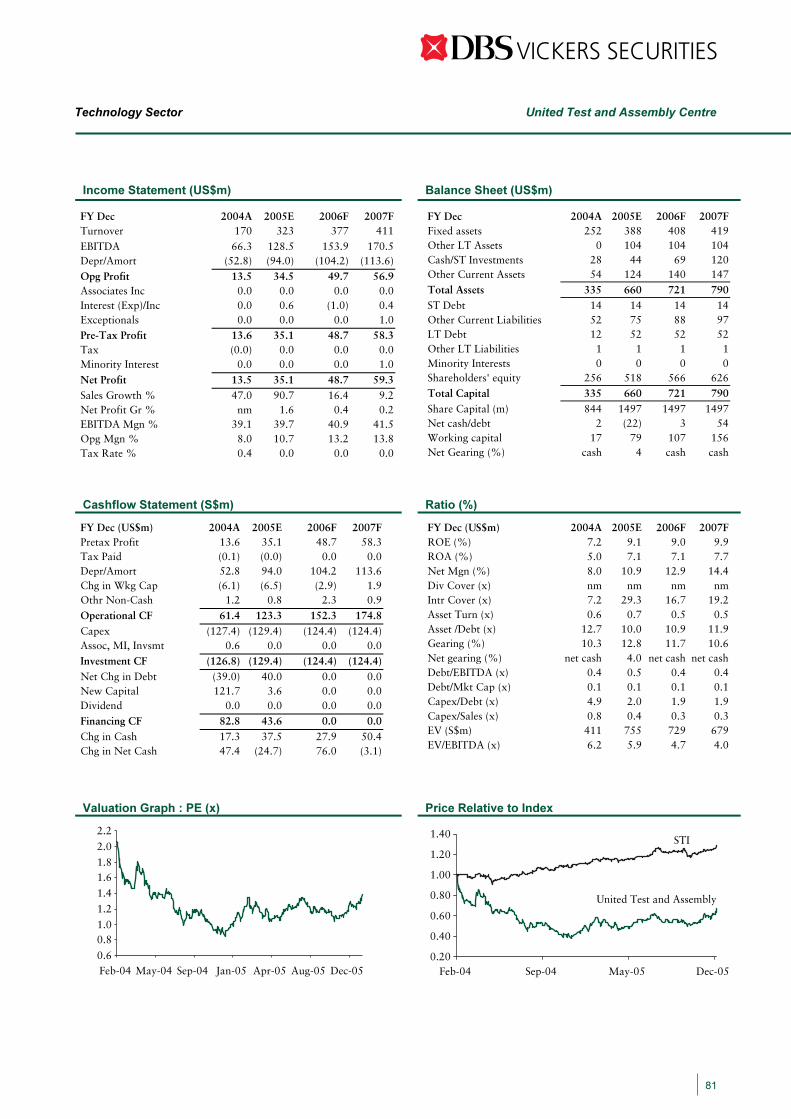

United Test & Assembly Centre 80

MITA (P) NO. 065/10/2005

Don See (65) 6398 7955 Equity Analyst [email protected] Phua Bowen (65) 6398 7950 Equity Analyst [email protected] Dinesh Chandiramani (65) 6398 7967 Equity Analyst [email protected] Dr Chua Hak Bin (65) 6878 5396 Economist [email protected]

2

Technology – Risks abound, nothing is for sure

Semiconductors 26

Technology Sector

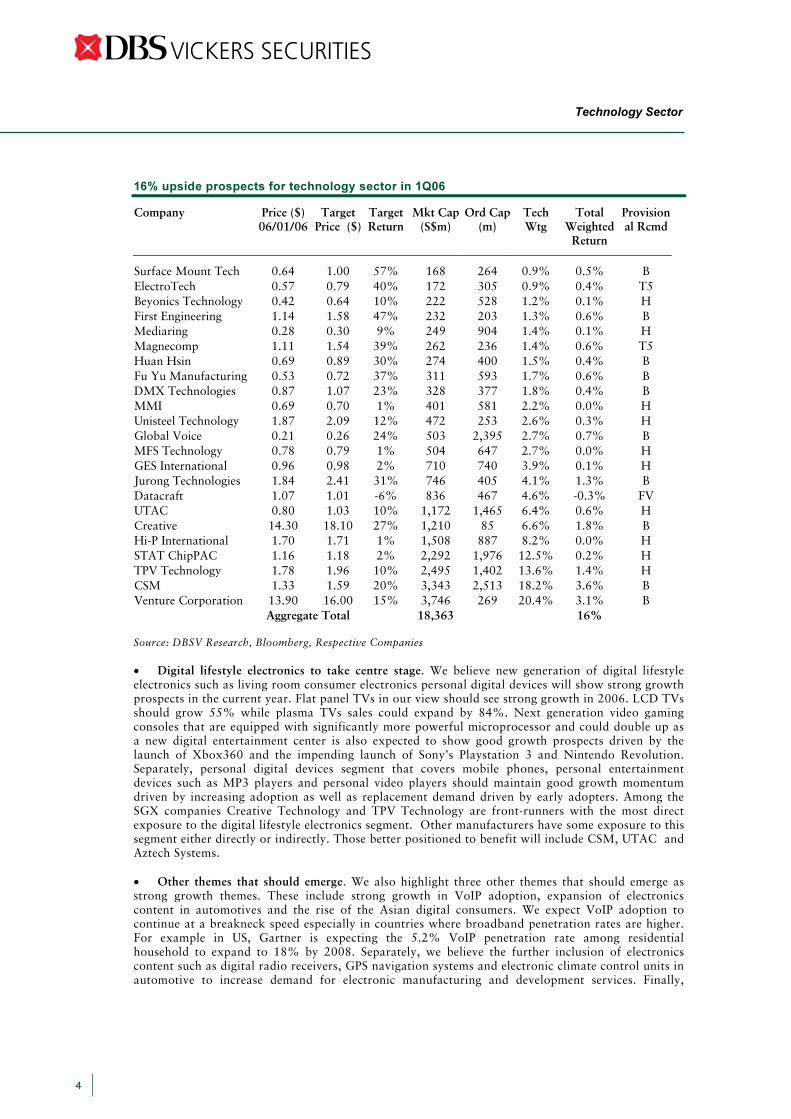

Investment Summary • Maintain Neutral Weight. We were overweight on the tech sector and suggested accumulation in 3Q05 and 4Q05 mainly because DBS ELI and several leading indicators were pointing towards a recovery in the sector in 2H05. We were forecasting growth for between 4 to 5 quarters in June as we believe the recovery is likely to be short and shallow due to shortening IT cycles. One of the shortest expansion lasted three quarters and that was in 1999. Our latest DBS ELI reading has flattened over the previous reading. Also US new orders to inventory and to shipment ratios are also leveling off. Together with falling non-oil retain imports and falling PMI reading in November and December respectively, we believe the first sign of slow down in the Singapore electronics exports and shipment could start to appear in 1Q06. • Baseline scenario – Shallow and short tech recovery. We have developed a baseline scenario and believe the current tech recovery should be a short and shallow one. Our house is of the view that electronics growth should continue to taper off in 2H05 and the manufacturing sector in Singapore could revert to single digit growth. We however have a positive bias and believe that sustained positive global growth momentum, better than expected take up rate in some product segments and a sustained capex discipline could yield better than expected returns for the tech sector. Semiconductor sales, barometer of the health of the global technology sector are expected to grow about 7%-8% over 2005, a marginal growth rate over 2005. Within the sector, the foundry segment is expected to lead the charge as the segment is expected to expand by 16% this year. NAND flash memory will expand by about 40% while outsourced test and assembly sales is forecasted to grow by about 8.0%. We believe if the various segments in the semiconductor sector can meet or exceed the projected growth, it should have a positive implication on the downstream suppliers and consequently the outlook of the technology sector. • Sector now only offers 16% upside compared to 24% and 20% at the beginning of 3Q05 and 4Q05 respectively. In 3Q05, when DBS ELI started to turn up, we recommended overweight on the sector. Based on a universe of stocks under our coverage, which has a market cap of at least US$100m and above, the sector then offered a return of about 24%. In 4Q05, when we continued to reiterate overweight, the same universe of stocks collectively offered about 20% return. Since then the prospects have declined to about 16%. The sector has had a decent run since July 2005 although the upside is still a relatively attractive 16%, we believe a neutral rating at this stage is apt since our leading indicators have started to show signs of weakness and we believe earnings growth momentum should slow on a sequential basis especially, when we have just passed the seasonally

3

stronger holiday quarter.

16% upside prospects for technology sector in 1Q06

Company Price ($) 06/01/06

Target Price ($)

Target Return

Mkt Cap (S$m)

Ord Cap (m)

Tech Wtg

Total Weighted

Return

Provisional Rcmd

Surface Mount Tech 0.64 1.00 57% 168 264 0.9% 0.5% B ElectroTech 0.57 0.79 40% 172 305 0.9% 0.4% T5 Beyonics Technology 0.42 0.64 10% 222 528 1.2% 0.1% H First Engineering 1.14 1.58 47% 232 203 1.3% 0.6% B Mediaring 0.28 0.30 9% 249 904 1.4% 0.1% H Magnecomp 1.11 1.54 39% 262 236 1.4% 0.6% T5 Huan Hsin 0.69 0.89 30% 274 400 1.5% 0.4% B Fu Yu Manufacturing 0.53 0.72 37% 311 593 1.7% 0.6% B DMX Technologies 0.87 1.07 23% 328 377 1.8% 0.4% B MMI 0.69 0.70 1% 401 581 2.2% 0.0% H Unisteel Technology 1.87 2.09 12% 472 253 2.6% 0.3% H Global Voice 0.21 0.26 24% 503 2,395 2.7% 0.7% B MFS Technology 0.78 0.79 1% 504 647 2.7% 0.0% H GES International 0.96 0.98 2% 710 740 3.9% 0.1% H Jurong Technologies 1.84 2.41 31% 746 405 4.1% 1.3% B Datacraft 1.07 1.01 -6% 836 467 4.6% -0.3% FV UTAC 0.80 1.03 10% 1,172 1,465 6.4% 0.6% H Creative 14.30 18.10 27% 1,210 85 6.6% 1.8% B Hi-P International 1.70 1.71 1% 1,508 887 8.2% 0.0% H STAT ChipPAC 1.16 1.18 2% 2,292 1,976 12.5% 0.2% H TPV Technology 1.78 1.96 10% 2,495 1,402 13.6% 1.4% H CSM 1.33 1.59 20% 3,343 2,513 18.2% 3.6% B Venture Corporation 13.90 16.00 15% 3,746 269 20.4% 3.1% B Aggregate Total 18,363 16% Source: DBSV Research, Bloomberg, Respective Companies • Digital lifestyle electronics to take centre stage. We believe new generation of digital lifestyle electronics such as living room consumer electronics personal digital devices will show strong growth prospects in the current year. Flat panel TVs in our view should see strong growth in 2006. LCD TVs should grow 55% while plasma TVs sales could expand by 84%. Next generation video gaming consoles that are equipped with significantly more powerful microprocessor and could double up as a new digital entertainment center is also expected to show good growth prospects driven by the launch of Xbox360 and the impending launch of Sony’s Playstation 3 and Nintendo Revolution. Separately, personal digital devices segment that covers mobile phones, personal entertainment devices such as MP3 players and personal video players should maintain good growth momentum driven by increasing adoption as well as replacement demand driven by early adopters. Among the SGX companies Creative Technology and TPV Technology are front-runners with the most direct exposure to the digital lifestyle electronics segment. Other manufacturers have some exposure to this segment either directly or indirectly. Those better positioned to benefit will include CSM, UTAC and Aztech Systems. • Other themes that should emerge. We also highlight three other themes that should emerge as strong growth themes. These include strong growth in VoIP adoption, expansion of electronics content in automotives and the rise of the Asian digital consumers. We expect VoIP adoption to continue at a breakneck speed especially in countries where broadband penetration rates are higher. For example in US, Gartner is expecting the 5.2% VoIP penetration rate among residential household to expand to 18% by 2008. Separately, we believe the further inclusion of electronics content such as digital radio receivers, GPS navigation systems and electronic climate control units in automotive to increase demand for electronic manufacturing and development services. Finally,

Technology Sector

4

Asian consumers, especially, in fast developing countries such as India and China, should continue to assert their influence in the purchase of digital and consumer electronic devices in 2006. VoIP plays in our view include MediaRing, Creative Technology and Aztech Systems. Automotive electronics beneficiaries should include Sunningdale Tech, First Engineering and Venture Corporation. With the rise of Asian digital consumerism, this will add a new dimension of growth and should benefit global companies and consequently their suppliers with a substantial exposure to the market. • Continues to advocate bottom up stock picking as our preferred investment approach. Without a clear sign that a strong tech growth is in place, we remain advocates of stock picking from a bottom up approach. Industry players are projecting semiconductor sales, a good electronics indicator, to grow a median 7.5% over an expected 6% in 2005. The growth remains positive although it is just marginally higher over the previous one. Nevertheless, we believe there are pockets of strength within the tech sector and companies with significant exposure to these segments should benefit more from others. Meanwhile, supply chain consolidation and market share expansion should continue to influence the prospects of companies. We view those preferred partners to large global companies with expanding market share to benefit most as a result of the supply chain consolidation exercise. At the start of this year, we have picked Chartered Semiconductor (CHRT SP), United Test & Assembly Center (UTAC SP), Electrotech (ELC SP), DMX (DMX SP), Magnecomp (MGCP SP), First Engineering (FIRST SP) and Huan Hsin (HUAN SP) as our preferred tech picks. • 2006 should see another robust year of growth for HDD sector driven by increased demand for consumer electronic products like DVR/PVR’s, MP3 players and selected areas from the automotive segment. Industry estimates forecast a total unit shipment of 403m drives in 2006; a healthy 18% increase from 2005. While PC shipments will continue to form the base of the industry, non-PC demand for HDD’s is what will really drive demand growing at a CAGR of 50% from 2004-2009 as forecast by Gartner. US majors Seagate and Western Digital have also raised their coming quarter guidance citing increased demand in the Christmas quarter. Our top pick for this sector is Magnecomp (MGCP, TP$1.54). Key risks would include intensifying competition from NAND flash as price points come down, and a buildup in inventory during 1Q06 forcing HDD vendors to slash prices thereby affecting component suppliers. • Plastic segment’s outlook should continue to improve. Plastic component suppliers have been on a downslide since the start of 2005 due to negative market sentiment generated by disappointing results seen in most of the comanies in the sector. However, we believe that the sector has reached the trough in terms of earnings decline, and 2006 should see some earnings growth return to most of the plastic component suppliers. With resin prices likely to stablilize in 2006, and rising utilization levels at the expand plant, we think that margins will start to expand from the levels seen in 2005. The macro environment for consumer electronics, handsets and PCs is looking fairly bright, and this will be a key indicator of the demand for plastic components. Most of the sector has been trading at three-year lows in terms of PE multiples in 2005, and we are starting to see a steady uprating of the plastic component suppliers with the prospects of a better 2006. The key risks for the sector remains the price of plastic resins, as well as over expansion of production capacity. We are currently Neutral on the plastic sector, as we believe that the market has priced in the prospect of earnings growth in 2006 with the recent revival of sorts, but the magnitude of the recovery will remain the key question. Within the sector, our top picks are Huan Hsin (TP: S$0.89) and First Engineering (TP:S$1.58). • For our 2006 outlook, we prefer companies with a Telecommunications slant and those exposed to outsourcing, as opposed to those that are primarily focused on computing based services. The growth in demand for broadband services should see Telco’s upgrading their infrastructure to cater to this increased demand. Technologies like VOIP should start to gain traction as they offer significant cost savings to traditional IDD services as well as enabling a whole host of additional services that can be deployed on IP networks. Lastly, we are of the view that Outsourcing still has legs to run with Singapore leading the pack in the Asia Pacific region as more government departments continue their drive towards outsourcing non-core services in the IT and BPO area. Top picks in this sector are DMX (DMX, TP: $1.07) MediaRing (MR TP: $0.30) and Frontline Technologies (FT TP: $0.17). Key risks would include long AR days that are common for IT Svcs companies and a downturn of the economy cycles that might slow down IT spending.

Technology Sector

5

Technology Sector

•

dependent upon consumer confidence and consumer purchase. Slowdown in global and more specific economic growth (a/c for >20% of global GDP) should affect the health of end demand. Sustained interest rate hike should also have an adverse impact on the sector’s outlook while volatilities in prices of raw materials and shortages in certain key components could affect overall health of the sector. Meanwhile, with most currencies expected to depreciate against the USD, this could once again affect reported earnings of some companies with significant exposure to USD sales and production costs denominated in Asian currencies. Other “out of our control” or unpredictable risks type such as natural catastrophes, flu epidemic and terrorist attacks could spring a global surprise and affect global growth negatively. This should have negative implications on the sector.

6

Risk factors. For the sector, macroeconomic risk should be most influential. Demand is

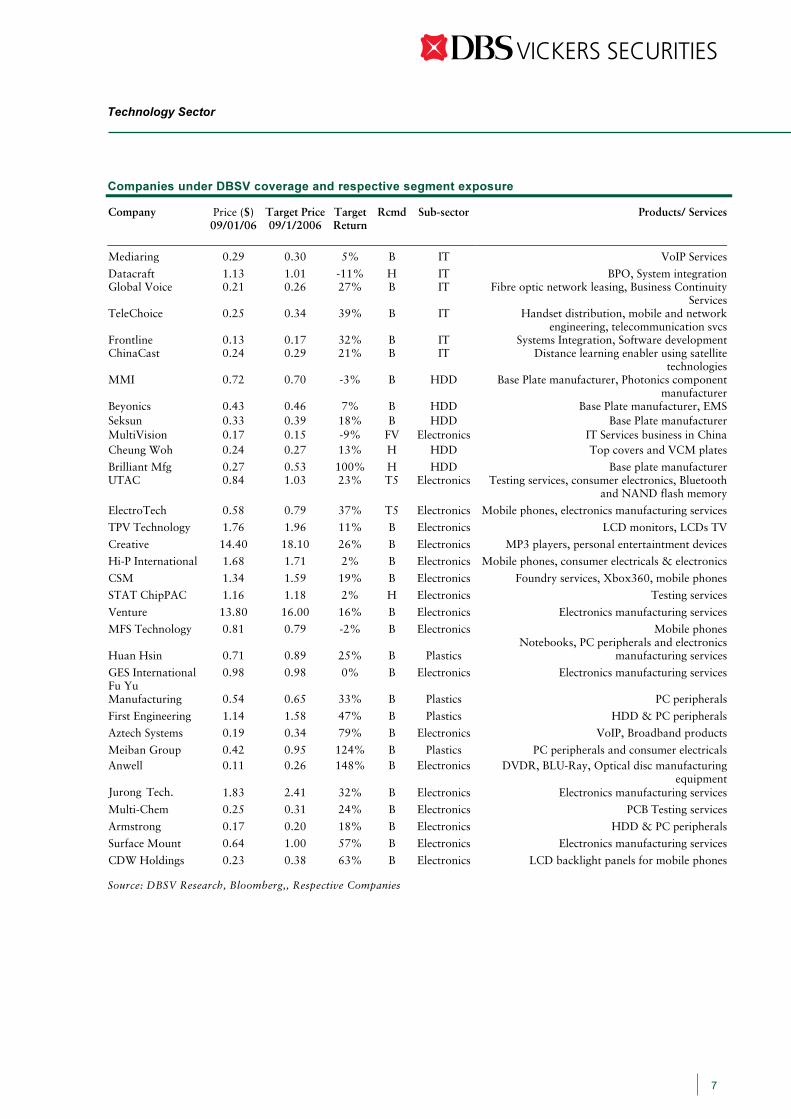

Companies under DBSV coverage and respective segment exposure

Company Price ($) 09/01/06

Target Price 09/1/2006

Target Return

Rcmd Sub-sector Products/ Services

Mediaring 0.29 0.30 5% B IT VoIP Services

Datacraft 1.13 1.01 -11% H IT BPO, System integrationGlobal Voice 0.21 0.26 27% B IT Fibre optic network leasing, Business Continuity

ServicesTeleChoice 0.25 0.34 39% B IT Handset distribution, mobile and network

engineering, telecommunication svcsFrontline 0.13 0.17 32% B IT Systems Integration, Software developmentChinaCast 0.24 0.29 21% B IT Distance learning enabler using satellite

technologiesMMI 0.72 0.70 -3% B HDD Base Plate manufacturer, Photonics component

manufacturerBeyonics 0.43 0.46 7% B HDD Base Plate manufacturer, EMSSeksun 0.33 0.39 18% B HDD Base Plate manufacturerMultiVision 0.17 0.15 -9% FV Electronics IT Services business in ChinaCheung Woh 0.24 0.27 13% H HDD Top covers and VCM plates

Brilliant Mfg 0.27 0.53 100% H HDD Base plate manufacturerUTAC 0.84 1.03 23% T5 Electronics Testing services, consumer electronics, Bluetooth

and NAND flash memory

ElectroTech 0.58 0.79 37% T5 Electronics Mobile phones, electronics manufacturing services

TPV Technology 1.76 1.96 11% B Electronics LCD monitors, LCDs TV

Creative 14.40 18.10 26% B Electronics MP3 players, personal entertaintment devices

Hi-P International 1.68 1.71 2% B Electronics Mobile phones, consumer electricals & electronics

CSM 1.34 1.59 19% B Electronics Foundry services, Xbox360, mobile phones

STAT ChipPAC 1.16 1.18 2% H Electronics Testing services

Venture 13.80 16.00 16% B Electronics Electronics manufacturing services

MFS Technology 0.81 0.79 -2% B Electronics Mobile phones

Huan Hsin 0.71 0.89 25% B Plastics Notebooks, PC peripherals and electronics

manufacturing services

GES International 0.98 0.98 0% B Electronics Electronics manufacturing servicesFu Yu Manufacturing 0.54 0.65 33% B Plastics PC peripherals

First Engineering 1.14 1.58 47% B Plastics HDD & PC peripherals

Aztech Systems 0.19 0.34 79% B Electronics VoIP, Broadband products

Meiban Group 0.42 0.95 124% B Plastics PC peripherals and consumer electricalsAnwell 0.11 0.26 148% B Electronics DVDR, BLU-Ray, Optical disc manufacturing

equipmentJurong 1.83 2.41 32% B Electronics Electronics manufacturing services

Multi-Chem 0.25 0.31 24% B Electronics PCB Testing services

Armstrong 0.17 0.20 18% B Electronics HDD & PC peripherals

Surface Mount 0.64 1.00 57% B Electronics Electronics manufacturing services

CDW Holdings 0.23 0.38 63% B Electronics LCD backlight panels for mobile phones

Source: DBSV Research, Bloomberg,, Respective Companies

Technology Sector

7

Tech.

Technology – Still to Neutral for now

Maintain Neutral weighting on SGX Technology sector

During 4Q04, we saw a positive rebound in stock price performance for the technology segment and we believe the optimism in the sector could be sustained through the first half of 1Q06. Much of the optimism in the technology sector stemmed from better than expected US holiday sales over Thanksgiving, especially with electronics goods. In addition, one by one, 18 of 21 technology majors revised their earnings guidance upwards from mid-October. We also had confirmation of the upturn for technology stocks in Singapore with better than expected October and November IPI figures for the Singapore electronics industry.

We expect prices of tech stocks to remain buoyant during the first two months of the quarter due to the Capricorn effect, positive news flow from the sector, mostly in relation to earnings announcements and marginally upbeat growth forecasts painted for various technology segments.

DBS Electronics Leading Index – Near term weakness

Source: DBSV Research

Coming from a buoyant 4Q04 which we had an Overweight call, we have shifted to a neutral weight stance in the current quarter. Our DBS Electronics Leading Index - which leads by 3 to 6 months - has leveled off after rising over the last few months. Growth in US new orders for electronics and computer products appear to be easing, with leading indicators such as the US new orders to inventory and US new orders to shipment ratios leveling off. Non-oil retained imports for Singapore, a leading indicator for exports going forward, also fell off sharply in November. The electronic cycle appears to be getting shorter. There are also some signs that US electronic inventories are no longer falling, and may be rising slightly. A scenario of a modest and shallow positive tech recovery represents our baseline scenario, until more positive data confirms otherwise. If global chip sales achieve earlier forecast to grow 7.9% in 2006 compared to 6.8% in 2005, a modest improvement, we might see a scenario that beats our expectation. Regionally, the anticipated pick up in global electronics demand has translated into stronger electronics exports growth in Asian economies over the last few months, particularly Korea, Taiwan and Singapore. Electronics exports rose 8.5% in Oct 2005 in Singapore, the highest growth rate in 2005. Electronic exports in Korea and Taiwan remained robust at about 8.3% and 19.5% respectively in Nov 2005. This will help to lift GDP growth in the 4Q05 and 1H06 across tech-dependent Asian economies, bearing in mind that electronics and exports did little to contribute to growth in the first 9 months of 2005.

-60

-40

-20

0

20

40

60

Jan-99 Apr-00 Jul-01 Oct-02 Jan-04 Apr-05

-60

-40-20

020

40

6080

100120

140DBS ELIGlobal chip sales (3mma, %yoy)SGX: electronics (rhs)

% yoy

Latest: Dec05

3mma,% yoy

Technology Sector

8

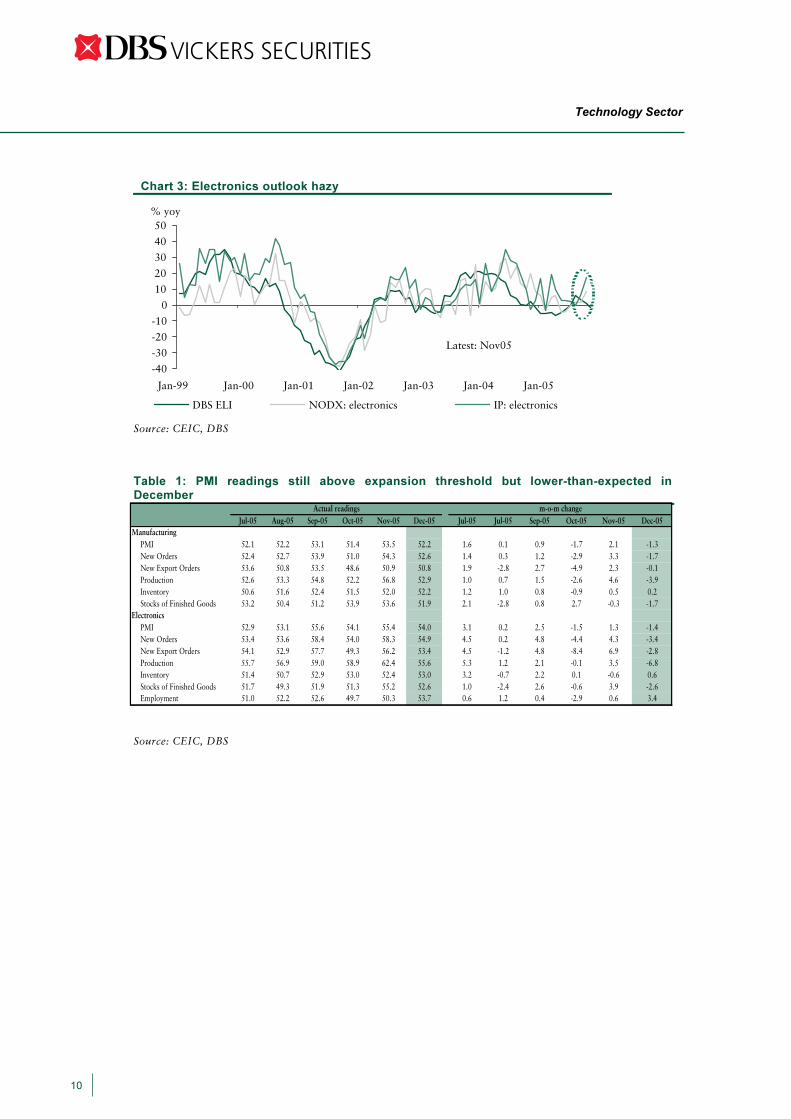

Lower-than-expected PMI readings in December The purchasing managers’ index (PMI) for overall manufacturing posted a lower reading of 52.2 in December from 53.5 in November - below consensus expectations of 53.8 and our forecast of 53.3. All sub-indices, except inventory, moderated. Production almost reversed its 4.9-point gain in November, declining 3.9 points in December. New orders from the domestic market weakened, while new export orders were largely unchanged. Electronics PMI similarly shed 1.4 points in December, but with major sub-indices particularly new orders, new export orders, and production falling more sharply (Chart 1). The saving grace was a 3.4-point jump in the employment sub-index, which is consistent with company expectations to increase hiring in 4Q05. Electronic leading indices easing; a shallow tech recovery The latest PMI readings is in line with our view that IPI growth in December will moderate from the accelerated pace in October and November (Chart 2). Pharmaceuticals will likely see a dip given the high base in Dec 2005. The electronics sector has, of late, posted double-digit growth while the transport and engineering sector has been outstanding throughout 2005. The weaker December PMI suggests that the electronics recovery could be quite modest and shallow. Our DBS Electronics Leading Index (ELI) is showing some signs of weakness, contracting 1.8% y-o-y in November (Chart 3). Singapore’s non-oil retained imports declined sharply, while stocks of finished goods, an inversely-related indicator, rose. US indicators have also been stuttering, with both the semiconductor book-to-bill and electronics shipment-to-inventory ratios falling. Our DBS ELI leads electronics output by about 3 to 6 months. These telltale signs suggest that the slowdown in electronics output and exports could be evident by end-1Q06. Our 2006 GDP growth forecast of 5.3% already factors in a baseline scenario of a modest and shallow tech recovery. Manufacturing will likely revert to high single-digit growth in 2006, from the blistering double-digit growth seen in the second half of 2005. Electronics growth is expected to taper off in the second half of this year, while non-electronics, such as oil rig construction and biomed, should remain robust.

Chart 1: Lower electronics PMI readings in Dec05

Chart 2: Weak overall manufacturing output in Dec05

Source: SIPMM, CEIC, DBS

35

40

45

50

55

60

65

70

75

80

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05

Electronics PMI

Production

New export orders

Index

Latest: Dec05

40

42

44

46

48

50

52

54

56

58

60

-40

-30

-20

-10

0

10

20

30

40

Mfg PMI: productionIPI (rhs)

Index

Latest: Dec05

% yoy

Source: SIPMM, CEIC, DBS

Technology Sector

9

Chart 3: Electronics outlook hazy

Source: CEIC, DBS

Table 1: PMI readings still above expansion threshold but lower-than-expected in December

Source: CEIC, DBS

-40

-30

-20

-10

0

10

20

30

40

50

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05

DBS ELI NODX: electronics IP: electronics

% yoy

Latest: Nov05

Jul-05 Aug-05 Sep-05 Oct-05 Nov-05 Dec-05 Jul-05 Jul-05 Sep-05 Oct-05 Nov-05 Dec-05Manufacturing

PMI 52.1 52.2 53.1 51.4 53.5 52.2 1.6 0.1 0.9 -1.7 2.1 -1.3New Orders 52.4 52.7 53.9 51.0 54.3 52.6 1.4 0.3 1.2 -2.9 3.3 -1.7New Export Orders 53.6 50.8 53.5 48.6 50.9 50.8 1.9 -2.8 2.7 -4.9 2.3 -0.1Production 52.6 53.3 54.8 52.2 56.8 52.9 1.0 0.7 1.5 -2.6 4.6 -3.9Inventory 50.6 51.6 52.4 51.5 52.0 52.2 1.2 1.0 0.8 -0.9 0.5 0.2Stocks of Finished Goods 53.2 50.4 51.2 53.9 53.6 51.9 2.1 -2.8 0.8 2.7 -0.3 -1.7

ElectronicsPMI 52.9 53.1 55.6 54.1 55.4 54.0 3.1 0.2 2.5 -1.5 1.3 -1.4New Orders 53.4 53.6 58.4 54.0 58.3 54.9 4.5 0.2 4.8 -4.4 4.3 -3.4New Export Orders 54.1 52.9 57.7 49.3 56.2 53.4 4.5 -1.2 4.8 -8.4 6.9 -2.8Production 55.7 56.9 59.0 58.9 62.4 55.6 5.3 1.2 2.1 -0.1 3.5 -6.8Inventory 51.4 50.7 52.9 53.0 52.4 53.0 3.2 -0.7 2.2 0.1 -0.6 0.6Stocks of Finished Goods 51.7 49.3 51.9 51.3 55.2 52.6 1.0 -2.4 2.6 -0.6 3.9 -2.6Employment 51.0 52.2 52.6 49.7 50.3 53.7 0.6 1.2 0.4 -2.9 0.6 3.4

Actual readings m-o-m change

Technology Sector

10

Technology – Crystal ball gazing in 2006 Last year, 2005, marked an interesting year for the global technology sector as a whole. New technology services and innovative products were introduced throughout the year. Many gained early acceptance while others became ubiquitous. There was no lack of trend shift as we saw the great promise of micro hard disk drives snubbed by NAND flash storage memory. Early prediction of mass adoption of DDRII memory fell below expectations as chipset shortages hindered the shift. Meanwhile, we also saw the merits of design, innovation and powerful brand exercises that helped to expand market share of some companies, notably, - Apple and Motorola. IP telephony also powered ahead strongly this year, which culminated in Ebay buying Skype for US$2.6bn. Earlier, we have identified 3G phones, notebooks, MP3 players and flat screen display monitors and TVs as the faster growing products for the year. With the exception of 3G phones (which nevertheless still saw growth) the demand for the other products, as we had expected, was strong given anecdotal evidence as well as the subsequent revision to earlier projections by various industry forecasters such as Gartner and iSuppli. For the current year, 2006, we identify several macro/product drivers that may influence and shape the global technology landscape. This exercise is critical as it shapes and formulates our expectations for the technology sector for the year. Subsequently, this will flow into our assumptions and expectations behind our forecasts and evaluations for companies that fall under the SGX Technology sector. The key trends we believe will play an important role in shaping the demand landscape for global technology companies and their related component suppliers are: a. Scope broadens and deepens for the Digital Home b. Proliferation and convergence of personal digital products c. Internet Telephony and Video Communication d. Electronics content in automotive set to expand e. Rise of the Asian Digital Consumers Scope broadens and deepens for the Digital Home

The digital home should continue to grab more limelight this year as we expect various new initiatives to encourage consumers to replace ageing home entertainment system, electronics home appliances and home desktop PCs. The arena is exciting and the prospects are very good given the paraphernalia available out there to lure increased purchase. Let’s review the prospects.

Flat panel display (FPD)

With falling panel prices, flat screen TVs, increasingly, are becoming ubiquitous in households. Besides its aesthetic factor, increased digital broadcasting of high definition TV (HDTV) programs are motivating consumers to upgrade and replace in order to receive these new digital programs. According to a survey done by the Consumer Electronics Association (CEA) market research team, the percentage of people who say their next TV will definitely be a HDTV has jumped to 21% from 12% in 2003. Meanwhile the popularity of high resolution DVD movie playback has coincided with consumers’ quest to build a home theater system. Hence the adoption of high resolution, high definition wide but flat screen TVs expanded. The two most popular flat screen TVs are LCD TVs and Plasma TVs. The more popular LCD TV is expected to register a 55% growth in 2006 while Plasma TV should see shipment increase by 84%

Digital Video Recorders (DVR)

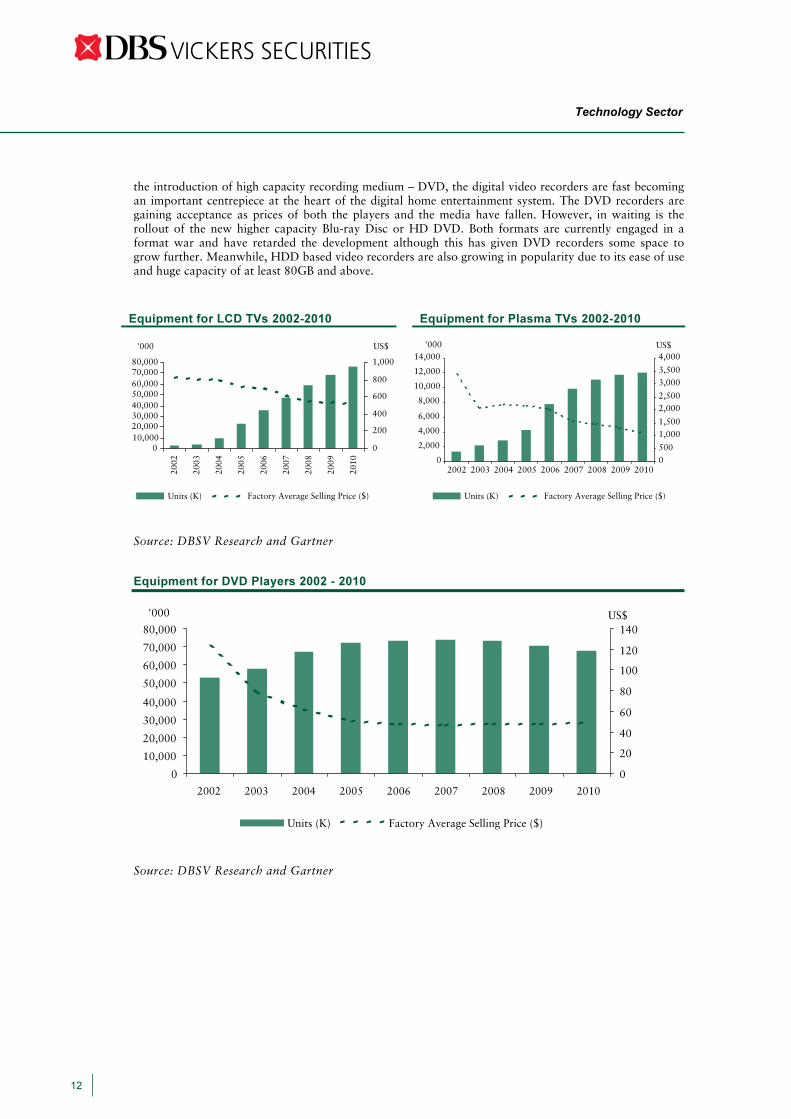

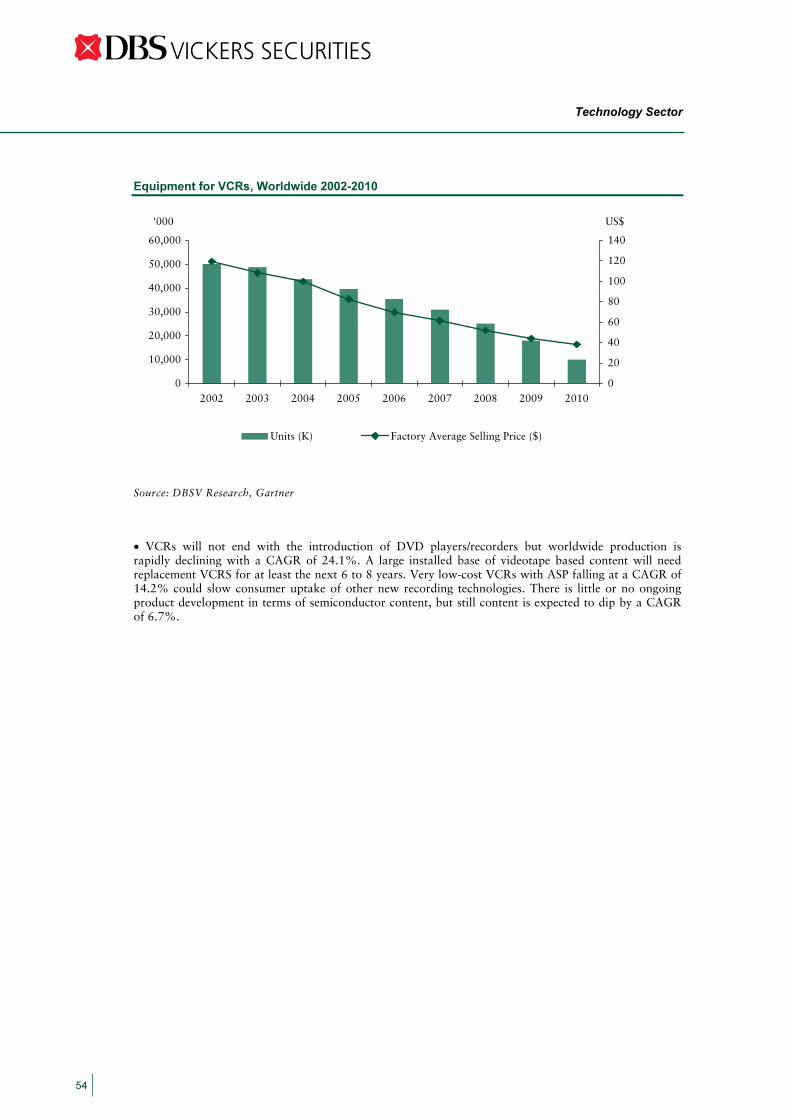

After the first VHS Video Camera Recorder was released in 1977, it swept consumers off their feet as it finally freed them off the very sticky relationship with the google box. Previously, TV viewers had no way to record TV programs that they would miss and this has inconvenienced many. The liberation was significant as it was thought 20 years after the introduction of the VCR. The video rental business in US generated revenues of US$7.7bn during the period. With the gradual proliferation of HD TV content and

Technology Sector

11

the introduction of high capacity recording medium – DVD, the digital video recorders are fast becoming an important centrepiece at the heart of the digital home entertainment system. The DVD recorders are gaining acceptance as prices of both the players and the media have fallen. However, in waiting is the rollout of the new higher capacity Blu-ray Disc or HD DVD. Both formats are currently engaged in a format war and have retarded the development although this has given DVD recorders some space to grow further. Meanwhile, HDD based video recorders are also growing in popularity due to its ease of use and huge capacity of at least 80GB and above.

Equipment for LCD TVs 2002-2010 Equipment for Plasma TVs 2002-2010

Source: DBSV Research and Gartner

Equipment for DVD Players 2002 - 2010

Source: DBSV Research and Gartner

010,00020,00030,00040,00050,00060,00070,00080,000

'000

0

200

400

600

800

1,000

US$

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

'000

0

20

40

60

80

100

120

140US$

Units (K) Factory Average Selling Price ($)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2002 200520042003 2006 2009 201020082007

2002 200520042003 2006 2009 201020082007

2002

2005

2004

2003

2006

2009

2010

2008

2007

'000

0500

1,0001,500

2,0002,500

3,0003,500

4,000US$

Units (K) Factory Average Selling Price ($) Units (K) Factory Average Selling Price ($)

Technology Sector

12

Digital Music Players/ System

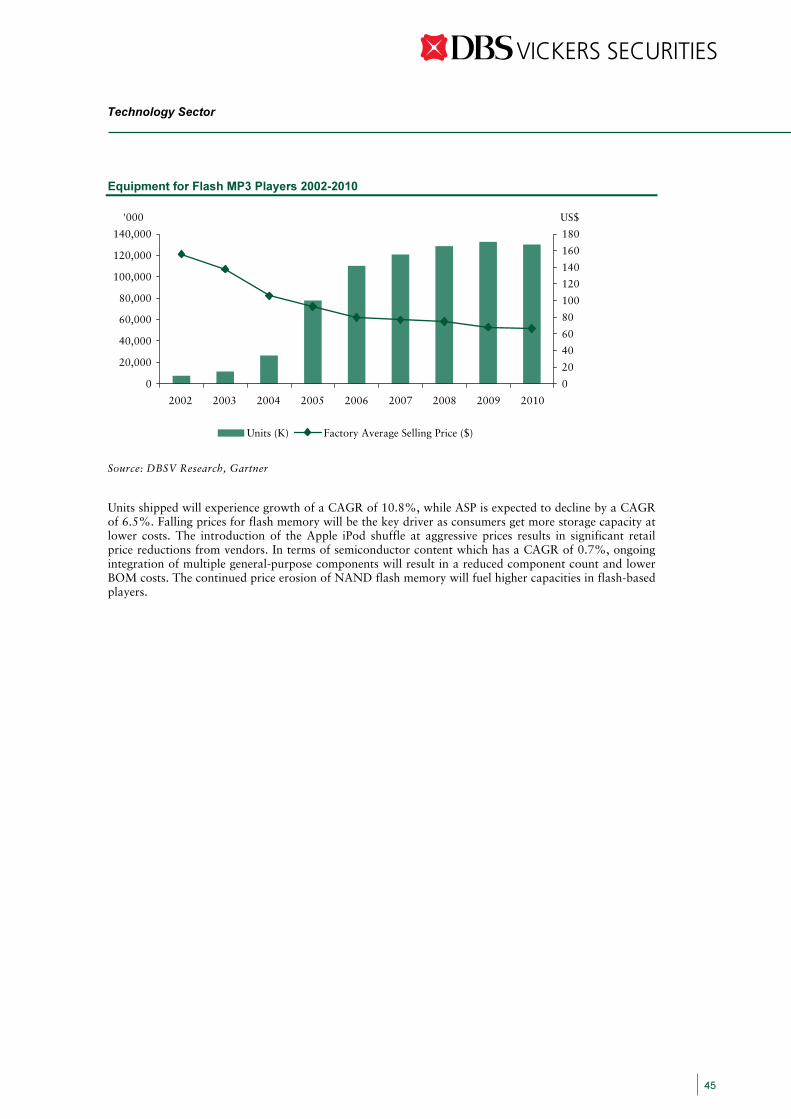

Digital audio or music players will continue to see significant demand growth through 2010. Technologies transition from analog recordings to digital ones is sweeping the music recording industry. Earlier music piracy, the use of file sharing networks and the threat of billions of lost revenues have spurred the recording industry to initiate a legal battle in which they won. While some thought it marked the end of the digital music era, who would have guessed that Apple successfully launched legitimized iTunes music download service which integrate seamlessly with its hugely successful iPods series of digital audio players. When more than 100m songs were downloaded from iTunes in 2004, other service providers, mainly Internet portals with huge audience base, started to offer similar music download services. With the emergence of licensed digital music and its subsequent boom, it fired sales of digital MP3 players. This growth is expected to continue through 2010, according to Gartner’s projection. Although it was optimistic of strong growth for 1” hard drive players back in May 2005, Apple’s latest iPod Nano have resulted in a resurgence of Flash Memory digital audio players as the fastest growing product category. However, HDD digital audio players will remain sought after due to its larger storage capacity, low price per megabyte and a shrinking form factor. Flash memory digital audio players will be sought after mainly for its form factor and efficient power consumption. Based on its latest revision, which came after the launch of the iPod Nano in Sep 2005, Gartner now expects HDD digital audio player shipment to peak in 2007 with 33m units (from 14m units in 2004). Similarly, shipment of Flash memory audio players will peak in 2009 with more than 132m units (from 27m units in 2004) manufactured. For HDD players, unit CAGR growth and revenue CAGR growth between 2005 and 2010 are –2.2% and –7.6% respectively. For Flash players, unit CAGR growth and revenue CAGR growth between 2005 and 2010 are +10.8% and +3.6% respectively. Nevertheless, HDD players are poised to register a 27% unit shipment growth while flash memory players should register a 42% unit shipment growth.

Equipment for Flash MP3 Players 2002-2010 Equipment for HDD MP3 Players 2002-2010

Source: DBSV Research, Bloomberg, and Gartner

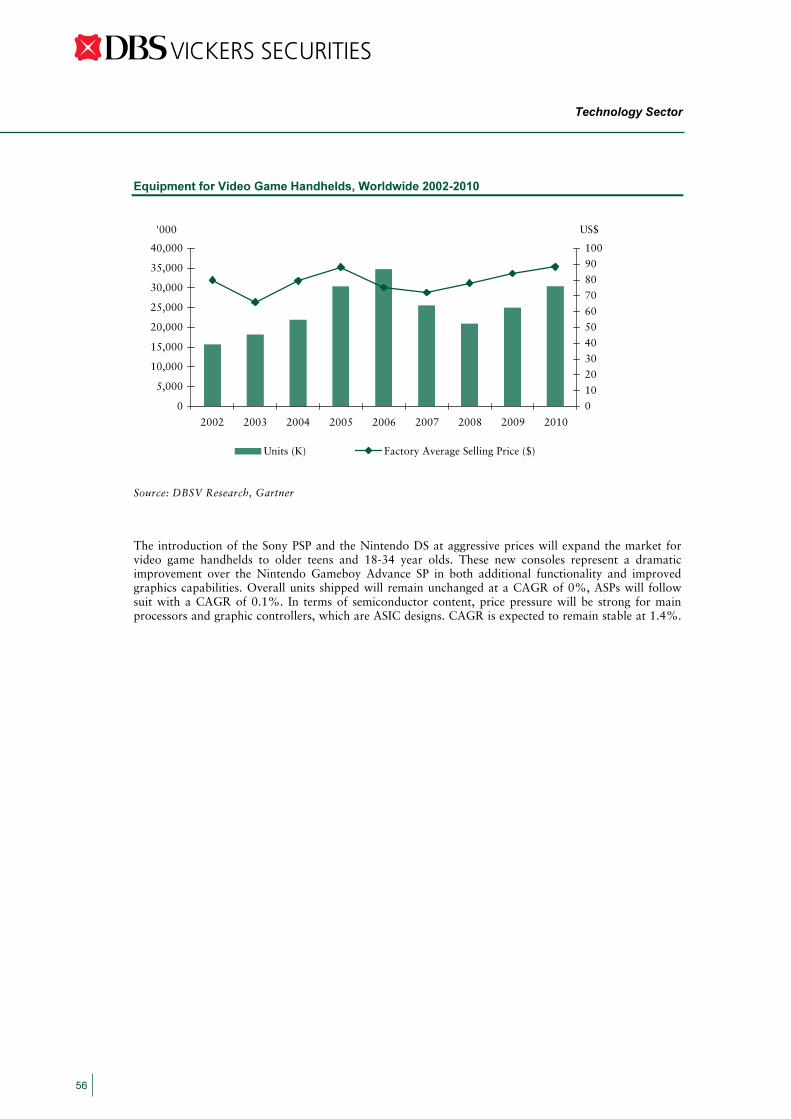

Game Consoles

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

'000

020406080100120140160180

US$

Units (K) Factory Average Selling Price ($) Units (K) Factory Average Selling Price ($)

2002 200520042003 2006 2009 2010200820070

5,000

10,000

15,000

20,000

25,000

30,000

35,000

'000

0

50

100

150

200

US$

2002 200520042003 2006 2009 201020082007

Technology Sector

13

The stage has been set for strong year of growth in 2006. The launch of Xbox360 was done amid much pomp and fanfare and the current shortfall in supply seem to be well orchestrated to create further hype. Sony’s Playstation 3 will be launched within the first quarter of the year and all eyes will be on its rollout and the market’s response towards the product. With Microsoft having established the early lead, Sony will be hard pressed to avoid any further delay to its planned product launched. Nintendo Revolution, Nintendo’s answer for the next generation video game console will be launched in 1H06. With the three hardware game console vendors already or slated to launch their respective next generation video game consoles, 2006 should herald an exceptional year for their electronic gaming hardware industry. According to a market research from Consumer Electronics Association, shipment revenues are expected to increase 18% to US$3.72bn in 2005 from US$3.16bn in 2004 and a further 35% to US$5.04bn in 2006. These next generation video game consoles sport much higher processing capabilities and the

Semiconductor consumption for Video Games Consoles 2002-2010

Source: DBSV Research and Gartner

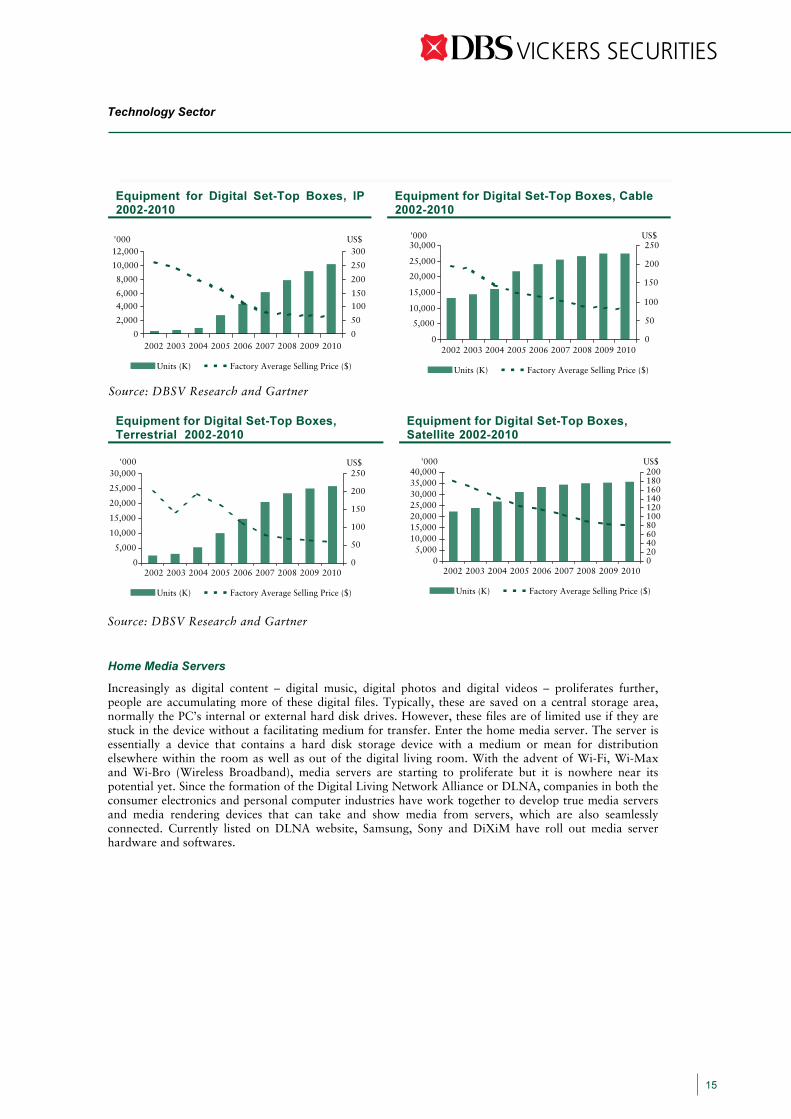

Set-top Boxes

A Set-top box is a household device that is connected to a television and an external signal source e.g. a TV program broadcaster. The box is a medium where the signal is decoded and converted into content on the television screen. Set-top boxes can be classified into digital, cable, IP and terrestrial ones. IP and terrestrial set-top boxes are expected to register stronger growth rates. IP set-top boxes will be supplied by IPTV network companies and it is really a medium that facilitates two-way communications on an IP network and the decoding of video streaming media. Terrestrial set-top boxes, on the other hand will decode signals, which are radio frequencies that are similar to analog TV signals. However, the key differences are the quality of the TV definition and audio and the more important fact that it uses multiplex transmitters that allow for the reception of multiple channels on a single frequency range.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000'000

0

20

40

60

80

100

120

140

160

180

200US$

Units (K) Factory Average Selling Price ($)

2002 200520042003 2006 2009 201020082007

Technology Sector

14

Xbox360 and PS3 will also support high definition video, built-in wireless connectivity, wireless controllers and removable hard disk storage according to CEA. Besides these improvements, the next generation gaming console is also heading towards the arena where it will attempt to establish itself as the hub of the digital home (Respective Company’s strategy).

Equipment for Digital Set-Top Boxes, IP 2002-2010

Equipment for Digital Set-Top Boxes, Cable 2002-2010

Source: DBSV Research and Gartner

Equipment for Digital Set-Top Boxes, Terrestrial 2002-2010

Equipment for Digital Set-Top Boxes,

Source: DBSV Research and Gartner

Home Media Servers

Increasingly as digital content – digital music, digital photos and digital videos – proliferates further, people are accumulating more of these digital files. Typically, these are saved on a central storage area, normally the PC’s internal or external hard disk drives. However, these files are of limited use if they are stuck in the device without a facilitating medium for transfer. Enter the home media server. The server is essentially a device that contains a hard disk storage device with a medium or mean for distribution elsewhere within the room as well as out of the digital living room. With the advent of Wi-Fi, Wi-Max and Wi-Bro (Wireless Broadband), media servers are starting to proliferate but it is nowhere near its potential yet. Since the formation of the Digital Living Network Alliance or DLNA, companies in both the consumer electronics and personal computer industries have work together to develop true media servers and media rendering devices that can take and show media from servers, which are also seamlessly connected. Currently listed on DLNA website, Samsung, Sony and DiXiM have roll out media server hardware and softwares.

0

2,000

4,000

6,000

8,000

10,000

12,000'000

0

50

100

150

200

250

300US$

0

5,000

10,000

15,000

20,000

25,000

30,000'000

0

50

100

150

200

250US$

Units (K) Factory Average Selling Price ($)

2002 200520042003 2006 2009 201020082007

05,000

10,00015,00020,00025,00030,00035,00040,000

'000

020406080100120140160180200

US$

Units (K) Factory Average Selling Price ($)

2002 200520042003 2006 2009 2010200820070

5,000

10,000

15,000

20,000

25,000

30,000'000

0

50

100

150

200

250US$

Units (K) Factory Average Selling Price ($)

2002 200520042003 2006 2009 201020082007

Units (K) Factory Average Selling Price ($)

2002 200520042003 2006 2009 201020082007

Technology Sector

15

Satellite 2002-2010

Digital Entertainment Centre

The digital entertainment centre really works by putting a power PC processor together with built in state of the art digital multimedia and AV components such as a DVR, digital music player and TV and FM tuners. The medium is driven by media server operating system, currently with the Windows Media Centre Edition as the most commonly one available. A good example is the HP Entertainment Centre, with its specification as highlighted here: HP Z558 Home Entertainment Centre.

Intel Pentium 4 processor 640 with HT Technology, enhanced

Intel SpeedStep (3.2GHz) 802.11 a/b/g wireless adapter

Windows XP Media Center Personal video recorder with dual NTSC TV tuners, over-air ATSC

TV tuner 1GB PC3200 DDR SDRAM Remote 300GB 7200 rpm hard drive Media drive bay

300GB HP Personal Media Drive One-year limited warranty SuperMulti DVD drive, DVD±R/RW drive with LightScribe, CD writer

capabilities

Intel High Definition Audio

NVIDIA GeForce 6600 graphics card 9-in-1 digital media card reader

Source: DBSV Research and HP

Proliferation and convergence of personal digital products

As highlighted by the recent trends seen in mobile handsets, a convergence of personal digital products into a single package has never been more prevalent. As the popularity of multimedia phones for consumers and enhanced smartphones for enterprise users grows, we are likely to enter into an arena of constant product innovation and falling prices.

Multimedia Mobile Phones

Source: DBSV Research, Gartner

The second half of 2005 saw major handset vendors like Nokia and Sony Ericsson launching phones with a focus on multimedia functions. The emphasis was specifically on features like music media playback and storage capability, and cameras with resolution in excess of 1.3 mega pixels. Sony Ericsson leveraged on its reputation in portable music players to launch its Walkman range of handsets in August, which have been very well received. Nokia recently also released its N-series range of handsets, with specific models like the N92 aimed at users of portable music players. With the recent product launches, it is indicative of

020,00040,00060,00080,000

100,000120,000140,000160,000180,000200,000

2004 2005 2006 2007 2008 2009

Growth

0%

50%

100%

150%

200%

250%

300%Units ('000s)

Multimedia Phones Growth

Technology Sector

16

the fact that mobile phones featuring portable music devices are clearly gaining traction with mobile subscribers. This shift in the function of mobile handsets away from being entirely voice/text-centric started in the late 1990s. Currently, falling prices and emerging telecommunication markets in developing economies are continuing to support the demand for the handsets with lower end features. However, as the availability and popularity of multimedia feature rich handsets (such as MP3 playback, MPEG-4 decoders, FM radios, speakerphone operation, SD card slots, USB connectivity) continue to grow, subscribers are expected to switch from basic enhanced handsets.

3G Mobile Phones

Source: DBSV Research, Gartner

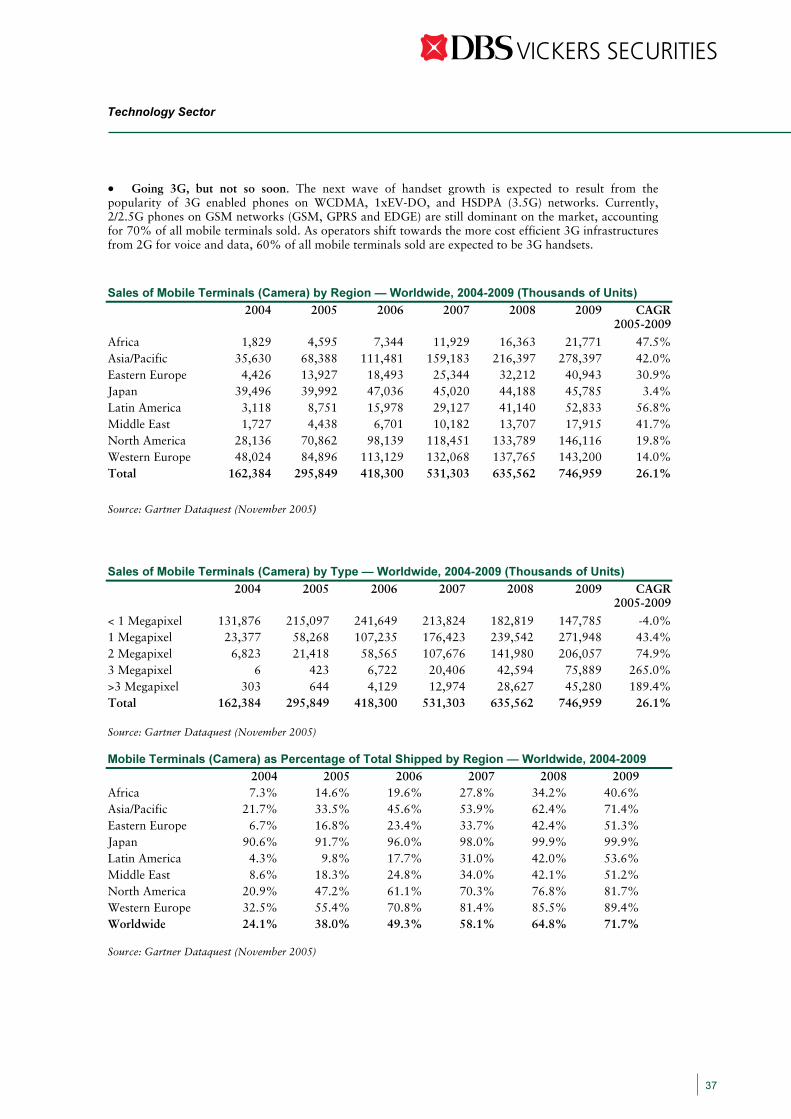

The next wave of handset growth is expected to be fueled by the popularity of 3G enabled phones on WCDMA, 1xEV-DO, and HSDPA (3.5G) networks. Currently, 2/2.5G phones on GSM networks (GSM, GPRS and EDGE) are still dominant in the market, accounting for 70% of all mobile terminals sold. As operators shift towards the more cost efficient 3G infrastructure from 2G for voice and data, 60% of all mobile terminals sold are expected to be 3G handsets by 2010. The applications that might drive consumer demand for 3G handsets could be mobile content like music downloads and video broadcast. While it is probably a safe bet that the popularity of 3G handsets will continue to rise, only selected markets are ready for it. 3G handset shipments to developed markets are expected to continue increasing, while 2/2.5G handsets will still be dominant in the emerging markets.

Enhanced Smart phones

Source: DBSV Research, Gartner

0

20,000

40,000

60,000

80,000

100,000

120,000

2004 2005 2006 2007 2008 2009

Growth

0%

100%

200%

300%

400%

500%

600%

700%Units ('000s)

Enhanced Smartphones Growth

0

100,000

200,000

300,000

400,000

500,000

600,000

2004 2005 2006 2007 2008 2009

Growth

0%

100%

200%

300%

400%

500%

600%Units ('000s)

3G Handsets Growth

Technology Sector

17

While enhanced smartphones (with enterprise capabilities like wireless e-mail, personal information management software, security and device management features) currently form a small percentage of the total mobile market as a whole, they do provide significantly higher margins than low-end phones for manufacturers. Lower end PDAs have seen their market share decline, as more affordable and feature packed smartphones came onto the market. The switch of users from lower end PDAs to enhanced smartphones, and increased enterprise users have seen shipment units grow by nearly seven-fold in 2004 and an estimated 230% increase in 2005. This trend of growth is expected to continue, albeit at a more modest pace. By 2009, enhanced smartphones are expected to comprise nearly 10% of total handset units shipped, up from 1.6% in 2005.

Internet Telephony and Video Communication

Internet Telephony, Voice over Internet Protocol or VoIP is set to see sharp growth with the number of residential VoIP users expected to increase to 197.2m by 2010 from 4.8m in 2004 and along the way powers wireline VoIP sales to $24.5bn from $8.04bn in 2004over the next years, causing market revenue for wireline VoIP equipment to more than triple from 2004 to reach $24.5bn in annual revenue in 2010, according to iSuppli Corp. The residential segment is expected to be the fastest growing segment with revenue expanding to $10.6bn by 2010 from $1.4bn currently. Japan and America are expected to dominate the residential VoIP subscriber market. They currently account for 83% of subscribers and even by 2010, they should account for more than 56.4% of VoIP subscribers. VoIP telephony service among US households is growing. According to Gartner’s assessment and forecast over VoIP telephony services among residential users, we can expect further growth over the next three years. Accordingly, VoIP connections could account for as much as 18% of US household telephony lines by 2008, up from just 5.2% expected this year, 2005. Although we recognize the fact that broadband penetration rates are among the highest in US, which is a key driver of VoIP usage, growth of VoIP services is undeniably strong among residential households. We expect these growth rates to be replicated in other countries and see the highest growth rates emerge from countries with a well developed broadband infrastructure.

Technology Sector

18

Household Wireline Telephony Service, 2002-2008 (Millions of Lines)

2002 2003 2004 2005 2006 2007 2008CAGR

(%) Household Telephony Lines Traditional PSTN Lines 124.4 121.4 119.2 116.0 111.2 104.6 99.2 -4.0Growth (%) -2.1 -2.4 -1.8 -2.6 -4.1 -5.9 -5.2 -VoIP Connections 0.0 0.1 2.3 6.4 10.7 16.2 21.8 174.1Growth (%) NA NA 1528.4 176.6 68.5 51.5 34.5 -Total Household Telephony Lines 124.4 121.6 121.5 122.4 121.9 120.9 121.0 -0.1Growth (%) -2.1 -2.3 -0.1 0.7 -0.4 -0.9 0.1 -Distribution of Lines Primarily for Voice Communications PSTN (%) 100.0 99.9 98.1 94.8 91.2 86.6 82.0 -VoIP (%) 0.0 0.1 1.9 5.2 8.8 13.4 18.0 -

Source: DBSV Research and Gartner

Business IP telephony

Besides the residential market, we are also seeing the traditional PBXs used widely in business enterprises gradually being replaced by IP enabled or pure IP-PBX equipment. The key driver behind the shift as identified by Gartner is really for new business process applications. Seamless connectivity and wider applications for unified communications across technology infrastructures are supporting the rising popularity. The chart documents the growing trend and the wider adoption of pure IP-PBX lines among business enterprises.

Business Telephony Lines by Shipment

Source: Gartner

Electronics content in automotive set to expand

We are expecting electronics content in automotive to continue to expand further in 2006. The value of semiconductor content, which is a good indicator of the level of electronics content in automotive expanded 5.6% in 2005 and is expected to expand 7.8% and 8.3% respectively in 2006 and 2007. Key segments that are expected to drive growth are air bags, digital auto stereo receivers, climate control unit, dashboard instrument cluster, GPS Navigation Systems and Keyless Entry.

Although the automotive market growth has remained rather flat over the last five years, strongly emerging economies in China, Brazil and Thailand look poised to drive growth further. Besides

Technology Sector

19

improvement in economies, another area of expansion is the amount of electronics content in car. Gartner is expecting the value of electronics of cars to reach about 30% of the cost of a new car by 2014. Besides the current stable of automotive electronics in car, new technologies and standards are likely to drive the use of electronics in automotive further. For example, Gartner believes networking technologies for electronic modules and systems such as Local Interconnect Network, Media Oriented Systems Transport and Safe-by-Wire Plus to have an impact on the use of electronics in automotive.

Currently, the highest values of electronics (semiconductor) content in automotive are airbags, antilock-braking systems, dashboard instrument clusters, GPS Navigation Systems and Engine control units. Car information and entertainment systems and safety enhancement systems would drive new areas of growth for electronics content in automotive. For safety systems, new enhancements such as active steering, brake-by-wire, Electronic Stability Program/ Electronic Stability Control, Auto Pilot, head up displays and lane departure warning and night vision enhancement systems are likely areas where new electronic content can be found. For car information and entertainment systems, there is likely convergence with current home, office or mobile electronics and the common electronic systems already found commonly could start to emerge in automotive. Those we expect to be included in automotives are flash memory storage, hard disk drive storage; CMOS image cameras, Bluetooth, remote diagnostics, digital radio, GPS systems and telematics.

Hype Circle for Automotive Electronics

Source: Gartner

Technology Sector

20

Electronics content in automotive expands

Source: Mentor Graphics

Semiconductor Consumption by Application, Worldwide, 2001-2010 (Millions of Dollars)

2004 2005 2006 2007 2008 2009 2010 CAGR

2005-2010

Automotive Electronics 15,759 16,645 17,952 19,434 21,315 21,553 23,241 6.9% Airbags 1,987 2,200 2,420 2,681 2,969 3,017 3,191 7.7% Antilock Braking Systems 1,653 1,680 1,737 1,821 2,000 1,996 2,123 4.8% Auto Stereo, Analog Receivers 795 731 736 745 777 707 695 -1.0% Auto Stereo, Digital Receivers 215 240 316 425 567 582 636 21.5% Climate Control Units 659 688 787 870 970 958 1,071 9.3% Dashboard InstrumentClusters 1,061 1,124 1,233 1,296 1,393 1,346 1,396 4.4% GPS Navigation Systems 1,732 2,000 2,309 2,599 3,015 3,337 3,788 13.6% Engine Control Units 2,891 2,986 3,159 3,376 3,675 3,611 3,736 4.6% Remote or Keyless Entry 230 246 271 285 320 315 336 6.4% Other Automotive Electronics 4,535 4,751 4,983 5,338 5,630 5,684 6,269 5.7%

Source: DBSV Research and Gartner

Technology Sector

21

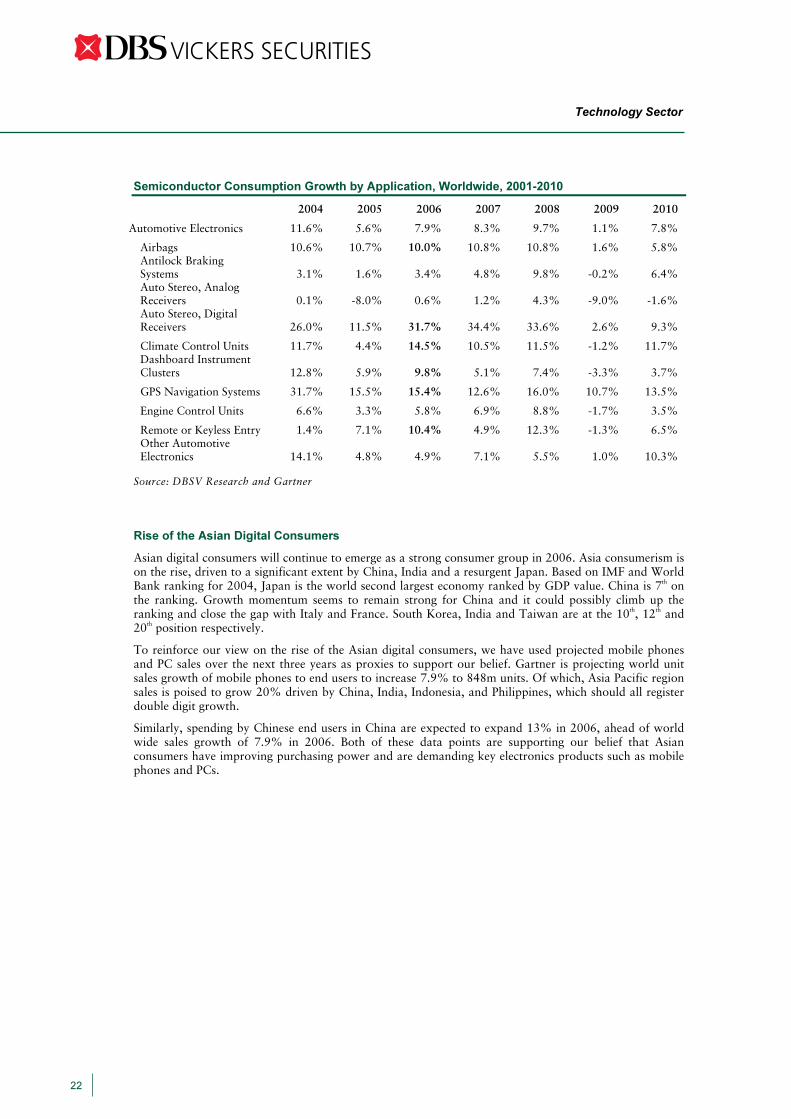

Semiconductor Consumption Growth by Application, Worldwide, 2001-2010

2004 2005 2006 2007 2008 2009 2010

Automotive Electronics 11.6% 5.6% 7.9% 8.3% 9.7% 1.1% 7.8%

Airbags 10.6% 10.7% 10.0% 10.8% 10.8% 1.6% 5.8%Antilock Braking Systems 3.1% 1.6% 3.4% 4.8% 9.8% -0.2% 6.4%Auto Stereo, Analog Receivers 0.1% -8.0% 0.6% 1.2% 4.3% -9.0% -1.6%Auto Stereo, Digital Receivers 26.0% 11.5% 31.7% 34.4% 33.6% 2.6% 9.3%

Climate Control Units 11.7% 4.4% 14.5% 10.5% 11.5% -1.2% 11.7%Dashboard Instrument Clusters 12.8% 5.9% 9.8% 5.1% 7.4% -3.3% 3.7%

GPS Navigation Systems 31.7% 15.5% 15.4% 12.6% 16.0% 10.7% 13.5%

Engine Control Units 6.6% 3.3% 5.8% 6.9% 8.8% -1.7% 3.5%

Remote or Keyless Entry 1.4% 7.1% 10.4% 4.9% 12.3% -1.3% 6.5%Other Automotive Electronics 14.1% 4.8% 4.9% 7.1% 5.5% 1.0% 10.3%

Source: DBSV Research and Gartner

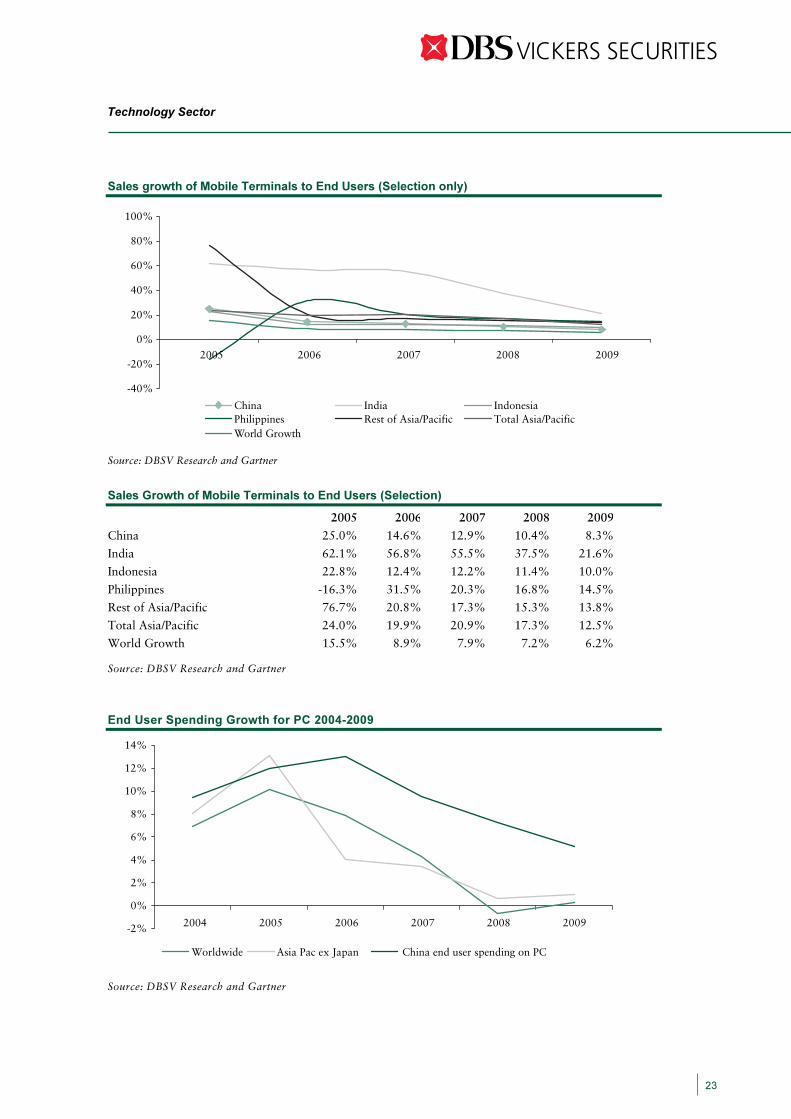

Rise of the Asian Digital Consumers

Asian digital consumers will continue to emerge as a strong consumer group in 2006. Asia consumerism is on the rise, driven to a significant extent by China, India and a resurgent Japan. Based on IMF and World Bank ranking for 2004, Japan is the world second largest economy ranked by GDP value. China is 7th on the ranking. Growth momentum seems to remain strong for China and it could possibly climb up the ranking and close the gap with Italy and France. South Korea, India and Taiwan are at the 10th, 12th and 20th position respectively.

To reinforce our view on the rise of the Asian digital consumers, we have used projected mobile phones and PC sales over the next three years as proxies to support our belief. Gartner is projecting world unit sales growth of mobile phones to end users to increase 7.9% to 848m units. Of which, Asia Pacific region sales is poised to grow 20% driven by China, India, Indonesia, and Philippines, which should all register double digit growth.

Similarly, spending by Chinese end users in China are expected to expand 13% in 2006, ahead of world wide sales growth of 7.9% in 2006. Both of these data points are supporting our belief that Asian consumers have improving purchasing power and are demanding key electronics products such as mobile phones and PCs.

Technology Sector

22

Sales growth of Mobile Terminals to End Users (Selection only)

-40%

-20%

0%

20%

40%

60%

80%

100%

2005 2006 2007 2008 2009

2005 20062004 2007 2008 2009

China India IndonesiaPhilippines Rest of Asia/Pacific Total Asia/Pacific

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Worldwide Asia Pac ex Japan

World Growth

Source: DBSV Research and Gartner

Sales Growth of Mobile Terminals to End Users (Selection)

2005 2006 2007 2008 2009

China 25.0% 14.6% 12.9% 10.4% 8.3%

India 62.1% 56.8% 55.5% 37.5% 21.6%

Indonesia 22.8% 12.4% 12.2% 11.4% 10.0%

Philippines -16.3% 31.5% 20.3% 16.8% 14.5%

Rest of Asia/Pacific 76.7% 20.8% 17.3% 15.3% 13.8%

Total Asia/Pacific 24.0% 19.9% 20.9% 17.3% 12.5%

World Growth 15.5% 8.9% 7.9% 7.2% 6.2% Source: DBSV Research and Gartner

End User Spending Growth for PC 2004-2009

Source: DBSV Research and Gartner

China end user spending on PC

Technology Sector

23

End User Spending Growth for PC 2004-2009

2004 2005 2006 2007 2008 2009Worldwide 6.9% 10.2% 7.9% 4.3% -0.6% 0.3%Asia Pac ex Japan 8.0% 13.1% 4.0% 3.4% 0.6% 0.9%China end user spending on PC 9.5% 12.0% 13.0% 9.5% 7.2% 5.2% Source: DBSV Research and Gartner Similarly, spending by Chinese end users in China are expected to expand 13% in 2006, ahead of world wide sales growth of 7.9% in 2006. Both of these data points are supporting our belief that Asian consumers have improving purchasing power and are demanding key electronics products such as mobile phones and PCs. GDP Growth

East Asia and Pacific 2003 2004 2005 2006 2007 GDP growth at market prices 8.0 8.3 7.4 6.9 7.2 GDP per capita, current USD 1154.3 1281.5 1469.4 1657.8 1976.3 Real per capita GDP growth 7.0 7.3 6.4 6.0 6.4 World 2003 2004 2005 2006 2007GDP growth at market prices 2.5 3.9 3.1 3.1 3.2GDP per capita, current USD 6099.2 6707.7 7194.9 7513.2 8010.2Real per capita GDP growth 1.4 2.7 2.0 2.1 2.2 Europe and Central Asia 2003 2004 2005 2006 2007GDP growth at market prices 5.9 6.8 5.5 4.9 5.0GDP per capita, current USD 2994.5 3634.9 4729.5 4849.4 4926.3Real per capita GDP growth 5.9 6.8 5.4 4.9 5.0 High Income Countries 2003 2004 2005 2006 2007GDP growth at market prices 1.9 3.2 2.4 2.6 2.6GDP per capita, current USD 30916.1 34038.3 36221.3 37957.6 40434.1Real per capita GDP growth 1.3 2.7 1.9 2.2 2.2 Source: DBSV Research, IMF and World Bank

Technology Sector

24

Technology – Risks abound, nothing is for sure

SGX’s tech related counters endured a tumultuous year in 2005 as several key factors influenced negatively on much of the sector’s earnings prospects. Sharp climb in various metals, oil and oil derivatives prices resulted in rising costs and lowered profitability at major technology companies. Extensive capacity expansion also drove profit lower as a result of start up losses, higher operating leverage and consequently lower factory utilization level. Interest rates hikes also hurt companies with higher gearing while demand uncertainty, especially in the United States that arose from the effect of two hurricanes and rising energy prices, also affected shipment and sales.

Raw material/ Energy price volatility

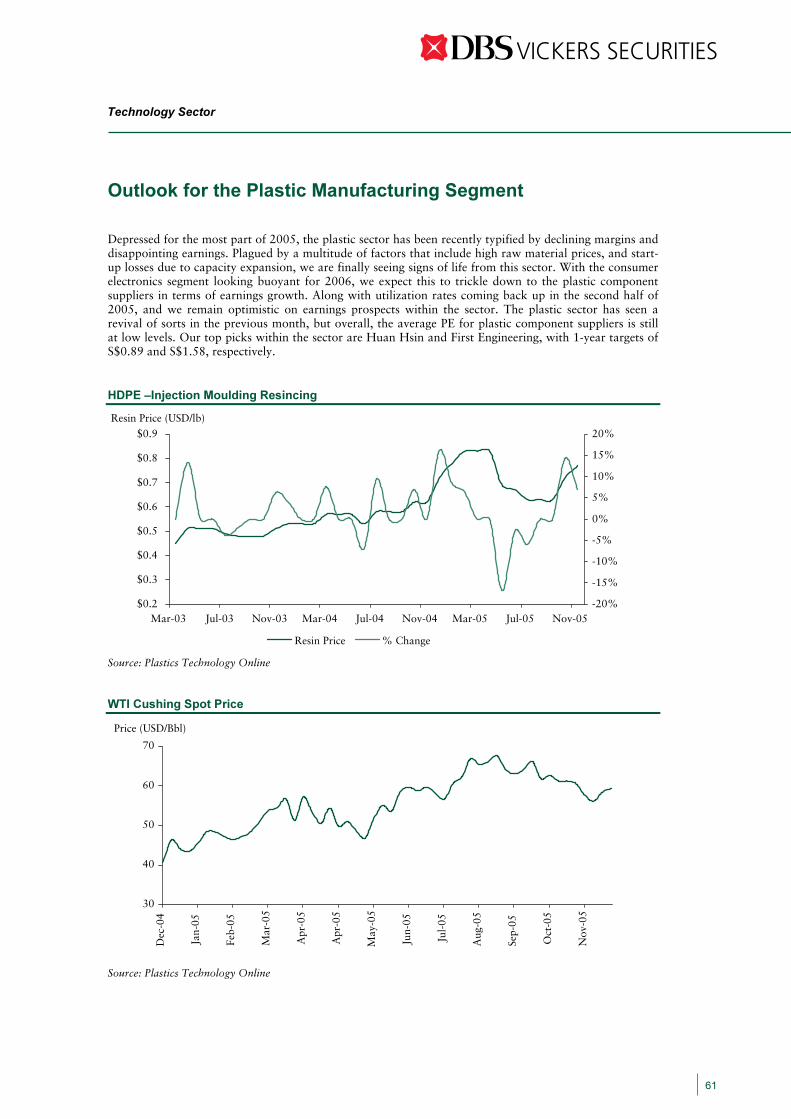

We are expecting oil price to remain stable and trade at an average rate of US$53 for 2006. Oil prices have been cited as the key factor that drives tech companies’ profitability lower in 2005. The impact of oil came either directly in the form of higher energy and component prices or indirectly through lower and more uncertain end demand as consumer tightens their purse and became more selective. Higher prices of oil derivatives such as plastic resins affected plastic manufacturing companies’ margins both directly and indirectly although recent capacity expansion and the lower utilization rates were also important factors in driving profits lower. Capacity/ Supply imbalances

Since 2000, the capacity and supply imbalances among technology companies have been monitored closely and kept in check. Companies and manufacturers are adding capacity carefully and are more disciplined in their approach towards it. Very clearly, we can see it from the pace of capacity expansion by semiconductor companies, where current cost to build a state of the art 300mm wafer fab could cost up to US$3bn. LCD manufacturing companies were facing oversupply issue in early 2005 but that has eased with the stronger than expected demand for the flat screen TV. The supply imbalances need to be monitored closely and companies need to ensure that any expansion keeps pace with demand expansion.

Strength of end demand

End demand health will always be a source of risk for companies and especially for companies with significant exposure to the consumer segment. Global GDP is expected to expand to 3.1% in 2005 and with US consumer confidence on the rise, it bodes well for consumer demand in 2006. At the same time, Asian consumers continue to assert its influence with important markets in South Korea, China, India and Indonesia maintaining its growth. As Japan seems to be emerging from a long period of deflationary pressure and benefiting from improving economic sentiment and consumer confidence, this second largest economy could play an important role in determining the direction and strength of global consumption of IT and digital products in 2006. Foreign exchange and interest rate volatilities

Sustained rate hikes in the United States drove the USD higher as capital flows into the country for investments in long-term asset instruments. The stronger USD was positive for most SGX listed tech companies as it resulted in favourable currency exposure since most had a significant portion of sales denominated in USD and cost of production incurred in a variety of other currencies, mostly Asian. For the current year, we are forecasting USD to decline against major currencies and the Asian currencies to strengthen against it. We expect this to have negative implications on tech companies with significant exposure to the respective currencies and this will be a critical risk to our SGD earnings assumptions.

Technology Sector

25

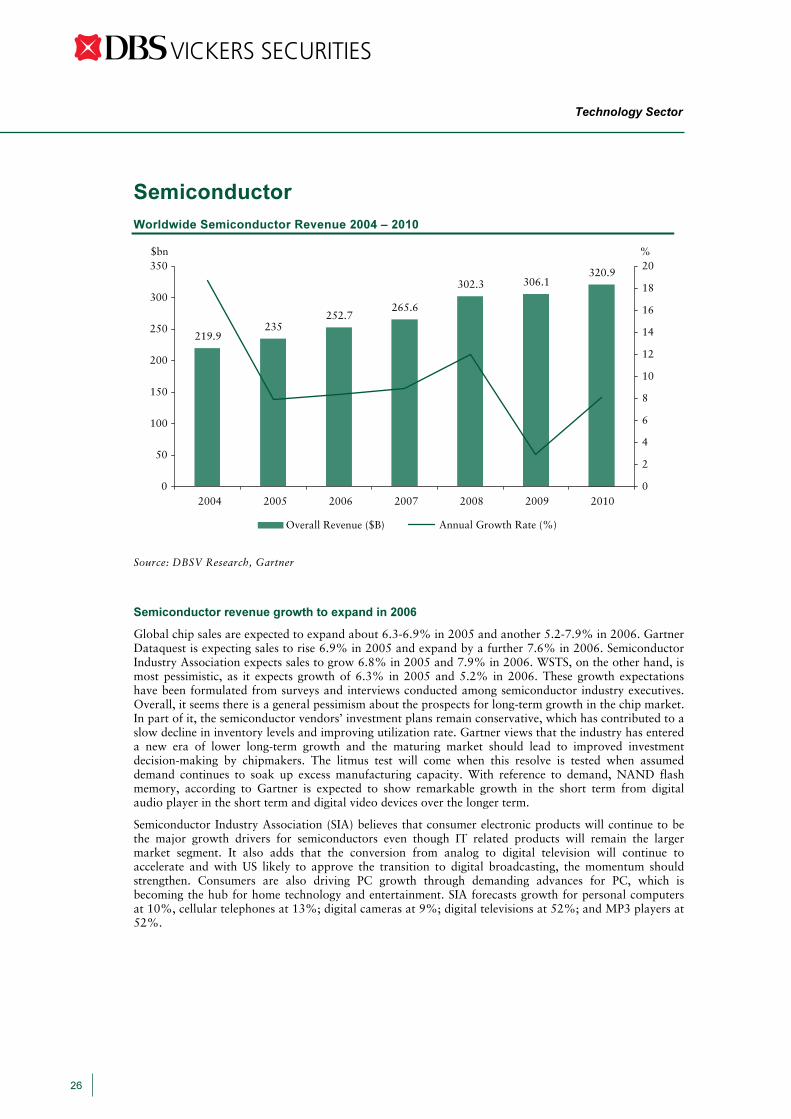

Semiconductor Worldwide Semiconductor Revenue 2004 – 2010

219.9235

252.7265.6

302.3 306.1320.9

0

50

100

150

200

250

300

350

0

2

4

6

8

10

12

14

16

18

20

Overall Revenue ($B)

20052004 2006 2009 201020082007

Source: DBSV Research, Gartner

Semiconductor revenue growth to expand in 2006

Global chip sales are expected to expand about 6.3-6.9% in 2005 and another 5.2-7.9% in 2006. Gartner Dataquest is expecting sales to rise 6.9% in 2005 and expand by a further 7.6% in 2006. Semiconductor Industry Association expects sales to grow 6.8% in 2005 and 7.9% in 2006. WSTS, on the other hand, is most pessimistic, as it expects growth of 6.3% in 2005 and 5.2% in 2006. These growth expectations have been formulated from surveys and interviews conducted among semiconductor industry executives. Overall, it seems there is a general pessimism about the prospects for long-term growth in the chip market. In part of it, the semiconductor vendors’ investment plans remain conservative, which has contributed to a slow decline in inventory levels and improving utilization rate. Gartner views that the industry has entered a new era of lower long-term growth and the maturing market should lead to improved investment decision-making by chipmakers. The litmus test will come when this resolve is tested when assumed demand continues to soak up excess manufacturing capacity. With reference to demand, NAND flash memory, according to Gartner is expected to show remarkable growth in the short term from digital audio player in the short term and digital video devices over the longer term.

Semiconductor Industry Association (SIA) believes that consumer electronic products will continue to be the major growth drivers for semiconductors even though IT related products will remain the larger market segment. It also adds that the conversion from analog to digital television will continue to accelerate and with US likely to approve the transition to digital broadcasting, the momentum should strengthen. Consumers are also driving PC growth through demanding advances for PC, which is becoming the hub for home technology and entertainment. SIA forecasts growth for personal computers at 10%, cellular telephones at 13%; digital cameras at 9%; digital televisions at 52%; and MP3 players at 52%.

Annual Growth Rate (%)

$bn %

Technology Sector

26

Semiconductor Revenue Breakdown 2004 - 2010

48 49.6 51.7 46.7 57.1 53.7 47.9

171.9 185.4201 218.9

245.2 252.4 273

0

50

100

150

200

250

300

350

Memory Revenue ($B) Nonmemory Revenue ($B)

20052004 2006 2009 201020082007

Semiconductor revenue growth to expand in 2006

Gartner Dataquest expects semiconductor sales to reach US$252.7bn in 2006, a 7.5% increase of 2005. Memory sales are expected to increase 4.2% to US$51.7bn in 2006. NAND flash memory is expected to drive sales in the segment, expanding about 37% to US$14.7bn while DRAM revenues will decline to US$20.1bn from US$25.3bn according to estimates. Despite the decline in DRAM revenues, ASP per bit for DRAM is not expected to decline excessively as DRAM makers are able to convert some excess capacity to produce NAND flash memory. At the same time, weaker pricing in 1H05 has slowed capacity expansion plans by various vendors. Along with the tighter capacity and the switch to produce more NAND flash memory to cope with the burgeoning demand by makers of consumer electronics appliances; this has help to avert a similar boom-bust cycle that DRAM memory tends to see.

NAND flash memory demand is driven by strong demand for digital consumer electronics products where high capacity, low cost, low power data storage is required. The explosive demand for NAND flash memory has led to new entrants, especially DRAM makers such as Hynix Semiconductor, Infineon Technologies, Micron Technology, Powerchip Semiconductor and STMicroelectronics into the industry. Production capacity can be switched rather quickly from DRAM to NAND flash and this has resulted in a capacity increase. Incumbent vendors such as Samsung and Toshiba/ Sandisk and soon new entrant Intel/ Micron are also planning substantial capacity increase in what they view as an explosive market.

Technology Sector

27

Source: DBSV Research, Gartner

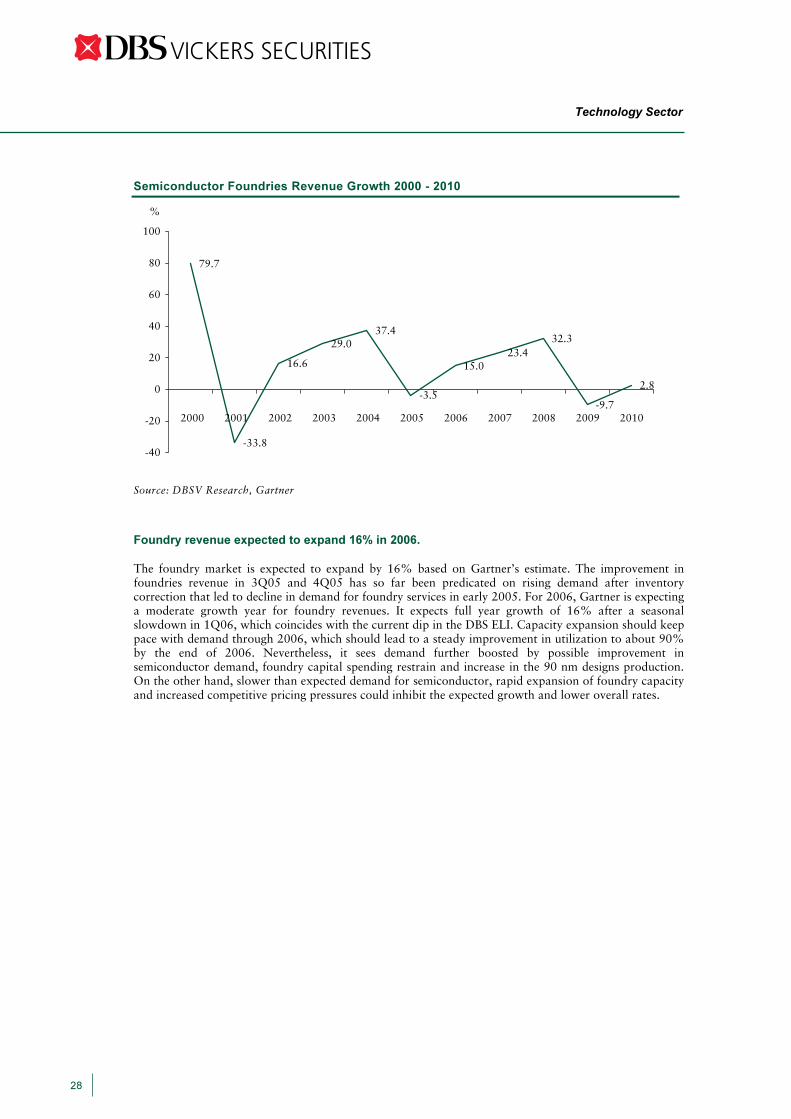

Semiconductor Foundries Revenue Growth 2000 - 2010

Source: DBSV Research, Gartner

Foundry revenue expected to expand 16% in 2006.

The foundry market is expected to expand by 16% based on Gartner’s estimate. The improvement in foundries revenue in 3Q05 and 4Q05 has so far been predicated on rising demand after inventory correction that led to decline in demand for foundry services in early 2005. For 2006, Gartner is expecting a moderate growth year for foundry revenues. It expects full year growth of 16% after a seasonal slowdown in 1Q06, which coincides with the current dip in the DBS ELI. Capacity expansion should keep pace with demand through 2006, which should lead to a steady improvement in utilization to about 90% by the end of 2006. Nevertheless, it sees demand further boosted by possible improvement in semiconductor demand, foundry capital spending restrain and increase in the 90 nm designs production. On the other hand, slower than expected demand for semiconductor, rapid expansion of foundry capacity and increased competitive pricing pressures could inhibit the expected growth and lower overall rates.

79.7

-33.8

16.6

29.037.4

-3.5

15.023.4

32.3

-9.7

2.8

-40

-20

0

20

40

60

80

100

%

2002 2005200420032000 2001 2006 2009 201020082007

Technology Sector

28

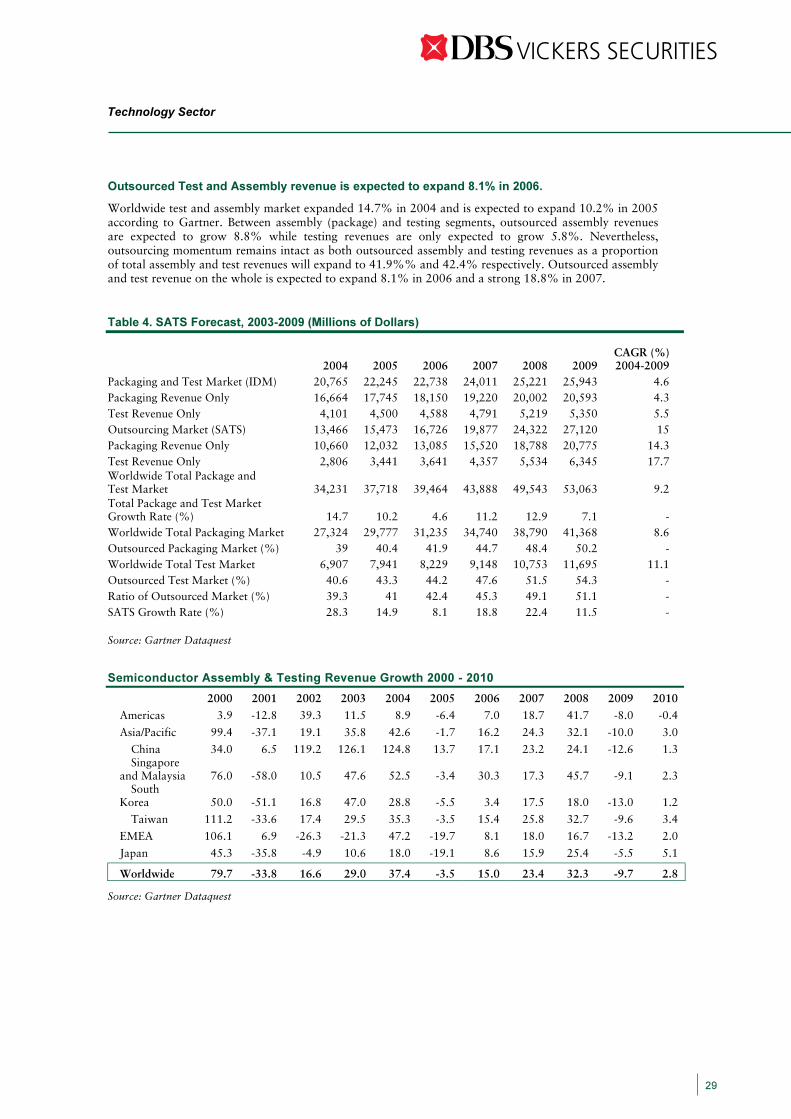

Outsourced Test and Assembly revenue is expected to expand 8.1% in 2006.

Worldwide test and assembly market expanded 14.7% in 2004 and is expected to expand 10.2% in 2005 according to Gartner. Between assembly (package) and testing segments, outsourced assembly revenues are expected to grow 8.8% while testing revenues are only expected to grow 5.8%. Nevertheless, outsourcing momentum remains intact as both outsourced assembly and testing revenues as a proportion of total assembly and test revenues will expand to 41.9%% and 42.4% respectively. Outsourced assembly and test revenue on the whole is expected to expand 8.1% in 2006 and a strong 18.8% in 2007.

Table 4. SATS Forecast, 2003-2009 (Millions of Dollars)

2004 2005 2006 2007 2008 2009 CAGR (%)2004-2009

Packaging and Test Market (IDM) 20,765 22,245 22,738 24,011 25,221 25,943 4.6Packaging Revenue Only 16,664 17,745 18,150 19,220 20,002 20,593 4.3Test Revenue Only 4,101 4,500 4,588 4,791 5,219 5,350 5.5Outsourcing Market (SATS) 13,466 15,473 16,726 19,877 24,322 27,120 15Packaging Revenue Only 10,660 12,032 13,085 15,520 18,788 20,775 14.3Test Revenue Only 2,806 3,441 3,641 4,357 5,534 6,345 17.7Worldwide Total Package and Test Market 34,231 37,718 39,464 43,888 49,543 53,063 9.2Total Package and Test Market Growth Rate (%) 14.7 10.2 4.6 11.2 12.9 7.1 -Worldwide Total Packaging Market 27,324 29,777 31,235 34,740 38,790 41,368 8.6Outsourced Packaging Market (%) 39 40.4 41.9 44.7 48.4 50.2 -Worldwide Total Test Market 6,907 7,941 8,229 9,148 10,753 11,695 11.1Outsourced Test Market (%) 40.6 43.3 44.2 47.6 51.5 54.3 -Ratio of Outsourced Market (%) 39.3 41 42.4 45.3 49.1 51.1 -SATS Growth Rate (%) 28.3 14.9 8.1 18.8 22.4 11.5 -

Source: Gartner Dataquest

Semiconductor Assembly & Testing Revenue Growth 2000 - 2010

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Americas 3.9 -12.8 39.3 11.5 8.9 -6.4 7.0 18.7 41.7 -8.0 -0.4

Asia/Pacific 99.4 -37.1 19.1 35.8 42.6 -1.7 16.2 24.3 32.1 -10.0 3.0

China 34.0 6.5 119.2 126.1 124.8 13.7 17.1 23.2 24.1 -12.6 1.3 Singapore

and Malaysia 76.0 -58.0 10.5 47.6 52.5 -3.4 30.3 17.3 45.7 -9.1 2.3 South

Korea 50.0 -51.1 16.8 47.0 28.8 -5.5 3.4 17.5 18.0 -13.0 1.2

Taiwan 111.2 -33.6 17.4 29.5 35.3 -3.5 15.4 25.8 32.7 -9.6 3.4

EMEA 106.1 6.9 -26.3 -21.3 47.2 -19.7 8.1 18.0 16.7 -13.2 2.0

Japan 45.3 -35.8 -4.9 10.6 18.0 -19.1 8.6 15.9 25.4 -5.5 5.1

Worldwide 79.7 -33.8 16.6 29.0 37.4 -3.5 15.0 23.4 32.3 -9.7 2.8 Source: Gartner Dataquest

Technology Sector

29

Computers

Robust growth of PCs in 2005 likely to slow going into 2006. According to Gartner, The current forecast for the growth in PC unit shipments for 2005 is likely to come in around 13%. Overall, PC shipments for 2006 and 2007 are still forecasted to continue growing, albeit at a slowing pace. Desktop-based PCs are expected to experience decelerating growth, while mobile PCs are projected to continue doing the same. From 2004-09, the total number of units shipped is expected to grow at a CAGR of 8.9%, from 136.2m to 169.1m.

Computers Growth in 2006 - Global PC Unit Forecast by Major Market and Form Factor, 2004-2009

2004 2005 2006 2007 2008 2009 CAGR (%) 2004-

2009Deskbased Units ('000)

136,188 145,573 151,206 155,305 161,912 169,101 4.4

Unit Growth (%) 8.4 6.9 3.9 2.7 4.3

4.4

Mobile Units ('000) 47,180 60,836 73,570 86,351 99,140 111,683 18.8Unit Growth (%) 23.0 28.9 20.9 17.4 14.8 12.8 All Units ('000) 183,367 206,409 224,776 241,656 261,051 280,785 8.9Unit Growth (%) 11.8 12.9 8.9 7.5 8.0 7.6 Source: Gartner Dataquest

Computers Growth in 2006 - Global PC ASP Forecast by Major Market and Form Factor, 2004-2009

2004 2005 2006 2007 2008 2009 CAGR (%) 2004-2009

Deskbased ASP ($) 958 836 751 685 631 584 -9.4Growth (%) -9.7 -12.7 -10.2 -8.8 -7.9 -7.4 Mobile ASP ($) 1,509 1,322 1,188 1,084 997 919 -9.4Growth (%) -6.8 -12.4 -10.2 -8.8 -8.1 -7.8 All PC ASP ($) 1,099 980 894 827 770 717 -8.2Growth (%) -7.7 -10.9 -8.7 -7.5 -7.0 -6.8 Source: Gartner Dataquest

Decreasing prices leading growth in demand. The main reason behind the growth in PC unit shipments continue to be falling ASPs. The increased affordability of a PC (desktop or mobile) has spurred double-digit growth in most regions, led by the emerging countries. Combined, ASPs for both desk-based and mobile PCs have fallen by 11%, from US$1,099 to US$980 per unit. Also, with the price gap between mobile and desk-based PCs narrowing, we are seeing more desktop users switch to mobile PCs.

Risks to growth in PC market. The forecast for continued growth in 2006 and 2007 could come under threat, depending on the launch date of Windows Vista, which is scheduled for a launch in 4Q06. If the new operating system (OS) is launched at the end of 4Q06, shipments for the quarter will be adversely affected, with buyers likely to wait for the new OS to be available before making the purchase.

Technology Sector

30

Computers Growth in 2006 – Global Computer Sales Forecast

Source: DBSV Research, Gartner Forecast from 2006 to 2009 –Unit Shipments and Growth by Form Factor Breakdown

Source: DBSV Research, Gartner

-

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

140,000.00

Desktop PCs Notebook PCs

Desktop PCs 130,479.60 121,721.60 113,551.20 106,380.50 102,158.90 98,754.40

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2004 2005 2006 2007 2008 2009

2004 2005 2006 2007 2008 2009

Number of Units

0

5

10

15

20

25

30

35

%Growth

Deskbased PCs Mobile PCs Mobile Growth Deskbased Growth

Notebook PCs 71,224.80 80,377.60 87,436.80 93,657.60 98,802.70 102,652.30

Technology Sector

31

Forecast from 2006 to 2009 – Revenues, and ASPs by Form Factor Breakdown

Source: DBSV Research, Gartner

• Developed countries will still lead global consumption for PCs. Currently, Western European countries and the US account for 57% of all PC units shipped in 2005, and this figure is expected to drop to 50% by 2009. However, as a proportion of total revenues, they form 61% of the total amount spent on PCs globally, and this is expected to increase to 70% by 2009. This trend can be partly attributed to computer users in these countries switching from desk-based PCs to mobile replacements, as the trend of price convergence continues.

• Emerging countries to provide the growth in PC units shipped. The growth in PC unit shipments will be mostly be driven by emerging countries, as falling ASPs make PCs more affordable. Eastern European countries and the Asia Pacific region is expected to contribute the bulk of the growth, with CAGR of 16.5% and 11.5%, respectively.

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

ASP in US$

0

200

400

600

800

1,000

1,200

1,400

1,600

Global Spending US$ ('000s)

Deskbased Spending Mobile Spending Deskbased ASP Mobile ASP

20052004 2006 200920082007

Technology Sector

32

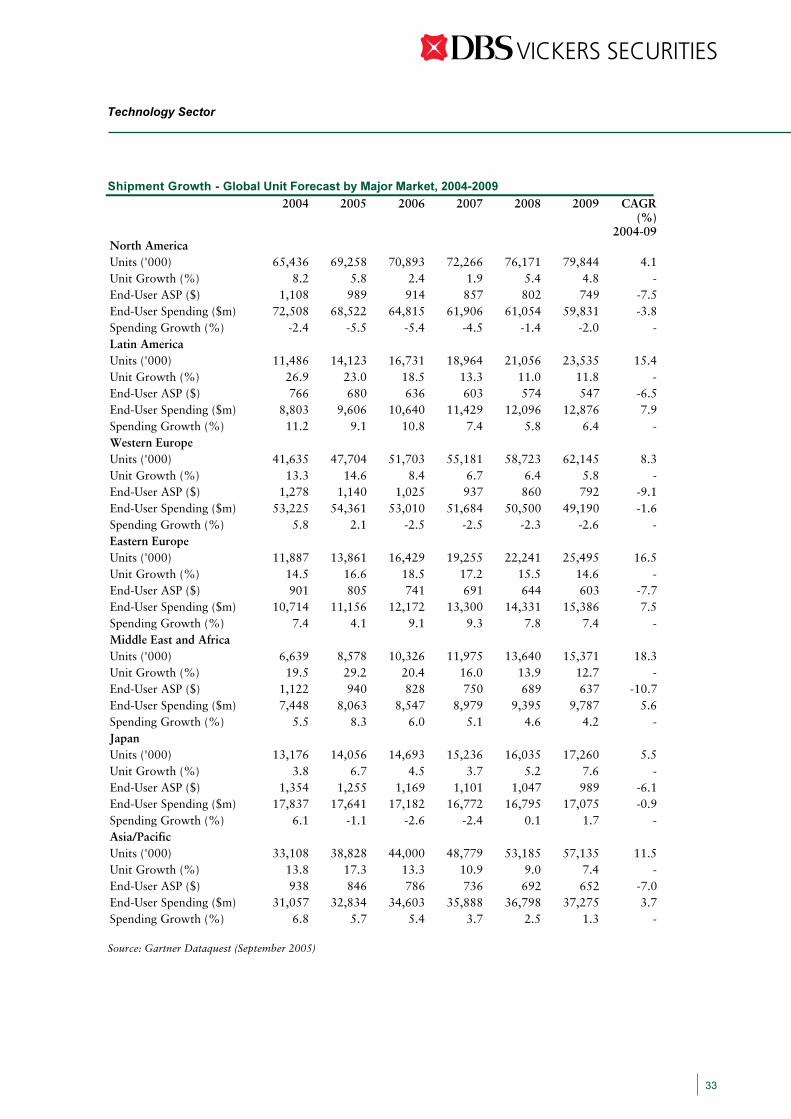

Shipment Growth - Global Unit Forecast by Major Market, 2004-2009

2004 2005 2006 2007 2008 2009 CAGR (%)

2004-09North America Units ('000) 65,436 69,258 70,893 72,266 76,171 79,844 4.1Unit Growth (%) 8.2 5.8 2.4 1.9 5.4 4.8 -End-User ASP ($) 1,108 989 914 857 802 749 -7.5End-User Spending ($m) 72,508 68,522 64,815 61,906 61,054 59,831 -3.8Spending Growth (%) -2.4 -5.5 -5.4 -4.5 -1.4 -2.0 -Latin America Units ('000) 11,486 14,123 16,731 18,964 21,056 23,535 15.4Unit Growth (%) 26.9 23.0 18.5 13.3 11.0 11.8 -End-User ASP ($) 766 680 636 603 574 547 -6.5End-User Spending ($m) 8,803 9,606 10,640 11,429 12,096 12,876 7.9Spending Growth (%) 11.2 9.1 10.8 7.4 5.8 6.4 -Western Europe Units ('000) 41,635 47,704 51,703 55,181 58,723 62,145 8.3Unit Growth (%) 13.3 14.6 8.4 6.7 6.4 5.8 -End-User ASP ($) 1,278 1,140 1,025 937 860 792 -9.1End-User Spending ($m) 53,225 54,361 53,010 51,684 50,500 49,190 -1.6Spending Growth (%) 5.8 2.1 -2.5 -2.5 -2.3 -2.6 -Eastern Europe Units ('000) 11,887 13,861 16,429 19,255 22,241 25,495 16.5Unit Growth (%) 14.5 16.6 18.5 17.2 15.5 14.6 -End-User ASP ($) 901 805 741 691 644 603 -7.7End-User Spending ($m) 10,714 11,156 12,172 13,300 14,331 15,386 7.5Spending Growth (%) 7.4 4.1 9.1 9.3 7.8 7.4 -Middle East and Africa Units ('000) 6,639 8,578 10,326 11,975 13,640 15,371 18.3Unit Growth (%) 19.5 29.2 20.4 16.0 13.9 12.7 -End-User ASP ($) 1,122 940 828 750 689 637 -10.7End-User Spending ($m) 7,448 8,063 8,547 8,979 9,395 9,787 5.6Spending Growth (%) 5.5 8.3 6.0 5.1 4.6 4.2 -Japan Units ('000) 13,176 14,056 14,693 15,236 16,035 17,260 5.5Unit Growth (%) 3.8 6.7 4.5 3.7 5.2 7.6 -End-User ASP ($) 1,354 1,255 1,169 1,101 1,047 989 -6.1End-User Spending ($m) 17,837 17,641 17,182 16,772 16,795 17,075 -0.9Spending Growth (%) 6.1 -1.1 -2.6 -2.4 0.1 1.7 -Asia/Pacific Units ('000) 33,108 38,828 44,000 48,779 53,185 57,135 11.5Unit Growth (%) 13.8 17.3 13.3 10.9 9.0 7.4 -End-User ASP ($) 938 846 786 736 692 652 -7.0End-User Spending ($m) 31,057 32,834 34,603 35,888 36,798 37,275 3.7Spending Growth (%) 6.8 5.7 5.4 3.7 2.5 1.3 - Source: Gartner Dataquest (September 2005)

Technology Sector

33

Communications Handset Sales in 2006 – Handset Sales Forecast 2004-2009 (‘000 units)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000Number of Units

0%

5%

10%

15%

20%

25%

30%

35%% Growth

Basic Phones Enhanced Phones Basic Smartphones

Enhanced Smartphones Wireless Cellular PDAs Overall Growth

20052004 2006 200920082007

Source: DBSV Research, Gartner Total Mobile Terminal Market — Worldwide, 2004-2009

2004 2005 2006 2007 2008 2009 CAGR 2005-2009

Sales to End Users ('000s) 674,002 778,751 847,725 914,414 980,704 1,041,808 7.5%Growth 29.6% 15.5% 8.9% 7.9% 7.2% 6.2% Wholesale Price ($) 173.9 168.3 167.9 165.3 162.2 161.6 -1.0%Total Revenue ($m) 117,190 131,097 142,339 151,165 159,063 168,398 6.5%Revenue Growth 22.5% 11.9% 8.6% 6.2% 5.2% 5.9% Retirements ('000s) 384,797 496,217 616,246 700,158 788,564 878,932 15.4%Installed Base ('000s) 1,548,748 1,813,236 2,044,715 2,258,971 2,451,111 2,613,986 9.6%Installed Base Growth 23.0% 17.1% 12.8% 10.5% 8.5% 6.6%

Source: Gartner Dataquest (July 2005)

Technology Sector

34

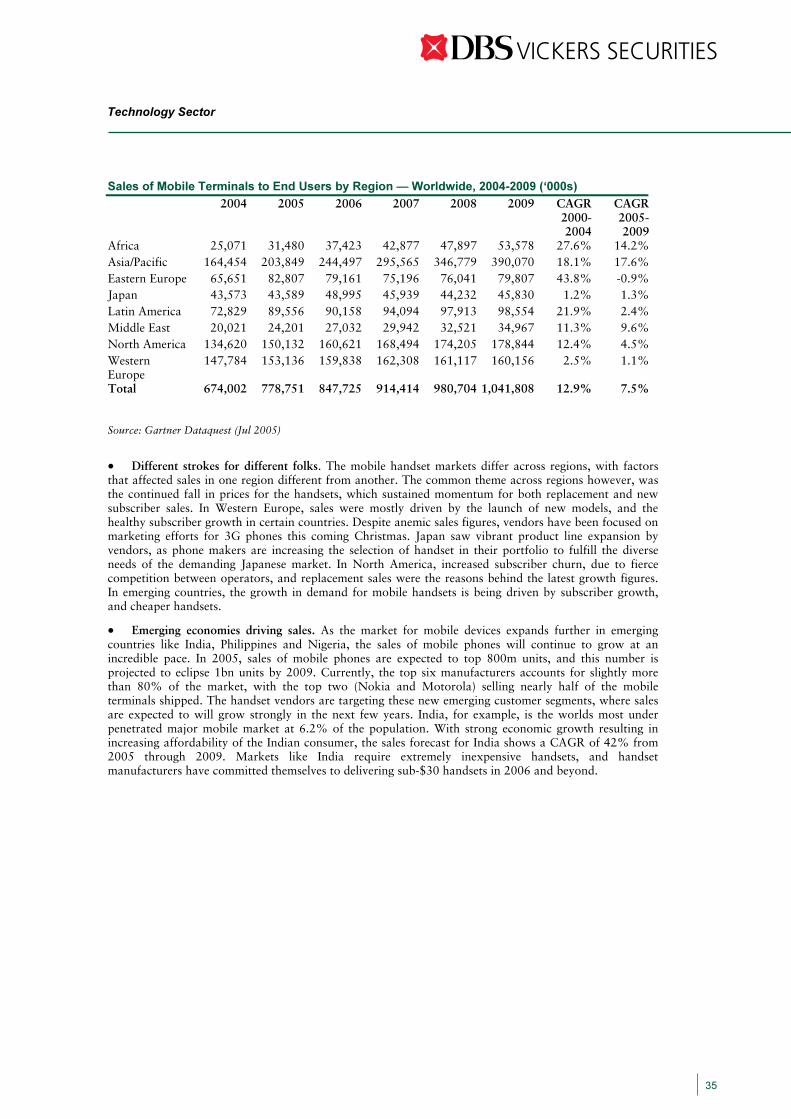

Sales of Mobile Terminals to End Users by Region — Worldwide, 2004-2009 (‘000s)

2004 2005 2006 2007 2008 2009 CAGR 2000-2004

CAGR 2005-2009

Africa 25,071 31,480 37,423 42,877 47,897 53,578 27.6% 14.2% Asia/Pacific 164,454 203,849 244,497 295,565 346,779 390,070 18.1% 17.6% Eastern Europe 65,651 82,807 79,161 75,196 76,041 79,807 43.8% -0.9% Japan 43,573 43,589 48,995 45,939 44,232 45,830 1.2% 1.3% Latin America 72,829 89,556 90,158 94,094 97,913 98,554 21.9% 2.4% Middle East 20,021 24,201 27,032 29,942 32,521 34,967 11.3% 9.6% North America 134,620 150,132 160,621 168,494 174,205 178,844 12.4% 4.5% Western Europe

147,784 153,136 159,838 162,308 161,117 160,156 2.5% 1.1%

Total 674,002 778,751 847,725 914,414 980,704 1,041,808 12.9% 7.5% Source: Gartner Dataquest (Jul 2005)

• Different strokes for different folks. The mobile handset markets differ across regions, with factors that affected sales in one region different from another. The common theme across regions however, was the continued fall in prices for the handsets, which sustained momentum for both replacement and new subscriber sales. In Western Europe, sales were mostly driven by the launch of new models, and the healthy subscriber growth in certain countries. Despite anemic sales figures, vendors have been focused on marketing efforts for 3G phones this coming Christmas. Japan saw vibrant product line expansion by vendors, as phone makers are increasing the selection of handset in their portfolio to fulfill the diverse needs of the demanding Japanese market. In North America, increased subscriber churn, due to fierce competition between operators, and replacement sales were the reasons behind the latest growth figures. In emerging countries, the growth in demand for mobile handsets is being driven by subscriber growth, and cheaper handsets.