Technological Innovation and Intellectual Capital BUA5FTS – WEEK 1

Technological Innovation and Intellectual Capital BUA5FTS – WEEK 1.

Mar 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Technological Innovation and Intellectual Capital

BUA5FTS – WEEK 1

Bontis on Intellectual capital

Intellectual capital has been considered by many, defined by some, understood by a select few and formally valued by practically no one.

(Bontis, 1998: 622)

Technological innovation is defined as:

‘A unique chronological process involving science,technology, economics, entrepreneurship, andmanagement is the medium that translates scientificknowledge into physical realities that are changingsociety. This process of technological innovation is the heart of the basic understanding which the competentmanager, the effective technologists, the sound governmentofficial, and the educated member of society should have inthe world of tomorrow’

James Bright

Could you please identify some industries that have strong technological innovation?

Introduction

The dominance of intellectual capital in wealth creation in all industries is highly evident today and some of the technologies are: Superconductivity Virtual Reality Robots Artificial Intelligence High-tech Medicine Biotechnology/Genetic Engineering Telecommunications

Intellectual capital concept First use of the term Intellectual capital in 1969

(Hudson 1993) Not yet agreed on its definition, its decomposition and

methods for valuation. The intangible assets of skill, knowledge and

information (Wall et al. 2004). "packaged useful knowledge" (Steward 1997:10) "knowledge, applied experience, organizational

technology, customer relationships and professional skills" (Edvinsson and Malone 1997)

Intellectual Capital

Intellectual Capital is defined as:

'Intellectual material that has been

formalized, captured, and leveraged to

produce a higher-valued asset.'

(Professor David Klein and Laurence Prusak of IBM )

Intellectual Capital

Relational capital/customer capital: Who you know and who knows and values you.

Intellectual capital

Human capital

Structural capital

Relational capital

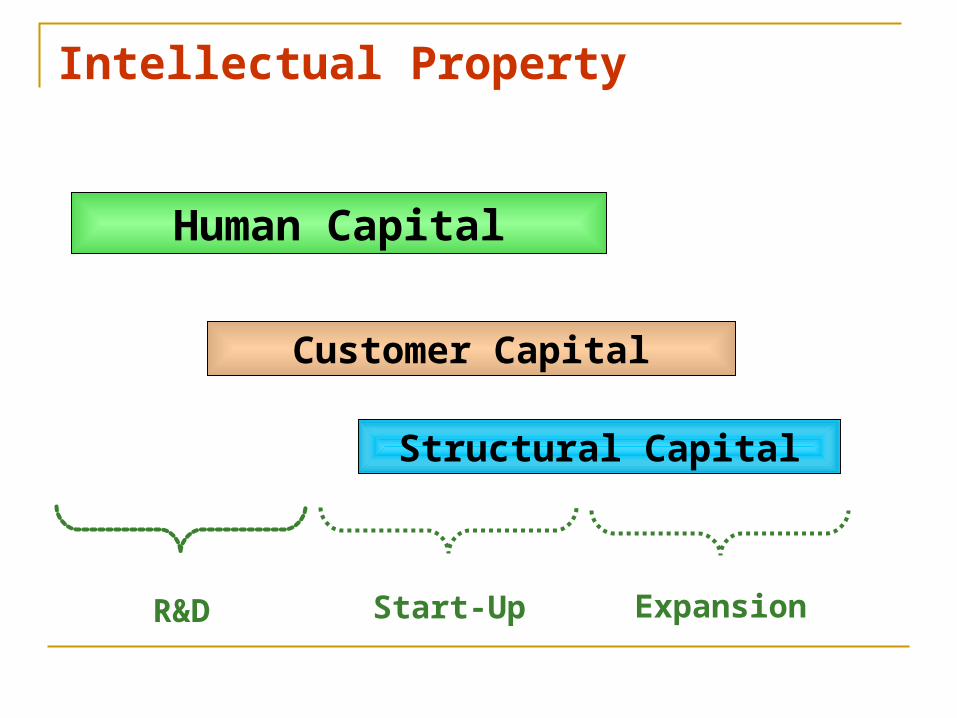

Intellectual Property

Human Capital

Customer Capital

Structural Capital

R&D Start-Up Expansion

Ideageneration

Ideageneration R&DR&D Final

ProductFinal

ProductPrototypePrototype

Cash FlowsCash Flows

ValueValue

Intellectual Capital and Firm Value

Valuation of Intellectual Property

Company Market Value Added Microsoft $253 billionIntel $78 billionMerck $62 billionPfizer $131 billionCisco Systems $45 billionBristol-Myers Squibb $119 billionLogitech $2 billion

Company Market Value Added Microsoft $253 billionIntel $78 billionMerck $62 billionPfizer $131 billionCisco Systems $45 billionBristol-Myers Squibb $119 billionLogitech $2 billion

Source: Yahoo Finance, December 2009MVA = market value of equity - equity capital suppliedTable 2.1 Creators of Wealth - 2009

Measuring Intellectual CapitalA model was developed by Skandia AFS:

Market Value

Financial

Capital

IntellectualCapital

HumanCapital

StructuralCapital

CustomerCapital

Organisational Capital

InnovationCapital

ProcessCapital

Economic Benefit

The primary objective of the firm is to maximise shareholders’ wealth

It is typically accountable to a dispersed group of stakeholders – lenders, customers, investors, governments, employees, community members, suppliers, citizens

The value of an intellectual asset is measured by the benefit it generates to the stakeholders and firm

‘Benefit’ would normally refer to monetary gain or economic value to the shareholders and firm

Definition of economic value is the present value of the expected earnings from using the asset

Economic Benefit Strong competition Associated rapid diffusion of innovations

reduce the returns to innovation an appropriate framework of intellectual property rights

is important to ensure that innovators receive an adequate return on their investment while at the same time encouraging the rapid diffusion of these innovations (OECD 2000).

Lehman (1996) suggests that economic growth and competitiveness will be determined by the ability to create, own, preserve and protect intellectual property.

Intellectual Capital Financial

Management Framework Involves the process of analysing the

financial issues facing a technology start-up In terms of economic trade-offs or financial

implications in relation to decisions about business investment, operations or financing

The process entails understanding the business environment by evaluating and then developing a proper financial strategy for the venture

Intellectual Capital Financial Management Framework Incorporates the optimal business structure for

the venture as well as utilising the appropriate tools for evaluating the financial problem or issue

Free Cash Flows

Value of Equity Value of the Firm

EBIT/EBT

Discount RateCAPM WACC

Traditional DCF

- Growth- TV

Start-up Project

Static Analysis

Dynamic Analysis

Option-based NPV Model

Real Options Valuation

Abandon(Put Option)

Defer(Call Option)

Expand(Call Option)

NPVInvestmentDecision

Financing:Venture kDebtIPOsOther

Source: Oh (2002)

Technology Start-ups Valuation Framework

Alternative Forms of Business Organization for Technology Startups

Sole proprietorshipAdvantages:

Ease of formation Subject to few regulations No corporate income taxes

Disadvantages: Limited life Unlimited liability Difficult to raise capital

Alternative Forms of Business Organization for Technology Startups PartnershipA partnership has roughly the sameadvantages and disadvantages as a soleproprietorship.

Alternative Forms of Business Organization for Technology Startups CorporationAdvantages:

Unlimited life Easy transfer of ownership Limited liability Ease of raising capital

Disadvantages: Double taxation Cost of set-up and report filing

Goals of the Corporation The primary goal is owner wealth (value)

maximization, which translates to maximizing firm’s value.

The factors that affect value of the firm are:

(i) Projected cash flows to owners

(ii) Timing of the cash flow stream

(iii) Riskiness of the cash flows

(i) Cash Flow

Long-term source of funds for the firm Internally generated Net income Retained earnings and depreciation provisions Free cash flows No historical data in most cases and this makes

it difficult to forecast cash flow patterns (i.e. economic fundamentals and comparable firms analysis)

(ii) Timing of Cash Flows

Implications for the owner wealth A dollar received today is worth more than a dollar received

sometime in the future (time value of money) Opportunity cost Discounting and compounding

(iii) Riskiness of Cash Flows

Factors that affect the level and riskiness of cash flows:

Decisions made by financial managers Investment decisions Financing decisions (the relative use of debt

financing) Dividend policy decisions The external environment

New Technology Venture Finance Focuses on how firms, both start-ups and large

firms, manage the financial process of new product/technology development from conception to ultimate commercialisation

requires managers to understand the balance sheet; valuation; financial tools; financial markets, and related issues and their impact on the financial

performance of the firm.

Early-stage Technology Valuation

Business Entity and its Value: Generally, comprised of the same basic

elements being monetary assets, tangible assets and intangible assets

More intangible assets Their aggregate value represents the value of the

business enterprise The financing of these assets could come from

two basic sources, namely equity and debt

Early-stage Technology Valuation Balance Sheet

Debit Credit

BusinessEnterprise

MonetaryAssets

TangibleAssets

IntangibleAssets

Equity

Debts

Asset = Liability + Equity

= =

Monetary +

Tangible Assets

Monetary +

Tangible Assets

IntangibleAssetsInternal

R&DProcessesCulture

KnowledgeExternal

CustomersSupply Chain

Others

IntangibleAssetsInternal

R&DProcessesCulture

KnowledgeExternal

CustomersSupply Chain

Others

EquityEquity

DebtsDebts

BookValue

+Stock Price Premium

BookValue

+Stock Price Premium

==

+

Balance Sheet

Total Assets Total Capital

+

Firm’s Market Value

Firm’s Market Value

Financial StatementsFinancial Statements

They are important because they portray the They are important because they portray the underlying financial performance and position underlying financial performance and position of the project. They are also a tool used for of the project. They are also a tool used for monitoring investment and business activitymonitoring investment and business activity

IAS 38 ‘Intangibles Assets’ standard -IAS 38 ‘Intangibles Assets’ standard -specifies and requires certain disclosure specifies and requires certain disclosure criteria to be met by intangible assetscriteria to be met by intangible assets

Financial StatementsFinancial Statements

Contentious issues:

It specifies that internally generated intangible assets such as goodwill, brands, mastheads, publishing titles, customer base and the likes should not be treated as assets;

IAS 38 does not allow an assignment of infinite useful life to an intangible asset; and

Many acquired intangible assets will not be allowed to be re-valued upwards because of the absence of an active market for such assets.

Balance SheetBalance Sheet

The The balance sheet (statement of financial balance sheet (statement of financial position) attempts to show the financial position) attempts to show the financial position of a project at a point in time anposition of a project at a point in time and d shows all the resources controlled by the shows all the resources controlled by the enterprise and all the obligations due by the enterprise and all the obligations due by the project. project.

The balance sheet equation:The balance sheet equation:

Assets = Liabilities + EquityAssets = Liabilities + Equity

Income StatementStatement of financial performance:

Sales

COGS

Other expenses

EBITDA

Depreciation and amortisation

EBIT

Interest expense

Taxes

Net income

Cash Flow StatementOperating activitiesNet incomeAdd – Sources of cashIncrease A/PIncrease in accrualsDepreciationLess – Uses of cashIncrease in A/RIncrease in inventory= Net cash provided by operations

minus Long-term investing activitiesInvestment in fixed assets

plus Financing activitiesIncrease in notes payableIncrease in long-term debtNet cash from financing

= Net change in cashAdd cash at the beginning of the year= Cash at the end of the year

Financial Reporting for IC

The economic rationale by the proponents for recognition of intellectual capital in financial reporting focuses on the balance sheet treatment of competitive advantages of the firm, proposals include: broadening of intangible asset recognition criteria (i.e.

capitalization of R&D, marketing and human resource expenditures)

measurement of contractual positions at fair value new definition of ‘revenue accounting’ to capture the critical

events of the value creation cycle of new economy firms

Technology Valuation

Implications of Technological Development for Business:

• Globalisation: resource allocation, manufacturing, MNCs and comparative advantage/competitive advantage e.g. India in software development

• Time compression: shortened product life & life cycle of a project e.g. Moore’s law (i.e. from initiation to completion), decreasing payback periods

• Technology integration: for development and commercialisation, e.g. IT + Biotech (see core technologies)

• Costs: better economies of scale and efficiency

Technology Valuation

• When technology is not mature, more time is needed in the early stages of the project

• If only incremental technology innovation, or when technology is mature, the early stages may be short and activities are likely to be confined to the execution and implementation of the project

• The project life cycle

Project Life Cycle

Early-stage technology is defined as technology that has not been commercialised or proven beyond laboratory experiments and this broad category includes: Untested ideas Bench-top technology Prototype technology

Project Life Cycle

All technology projects evolve over a number of stages, generally from conception to research and development (R&D) to commercialisation. The exact specification of the stages will depend very much on the nature of the project and the industry in which the technology is applied.

Time

Cos

t

Conceptual Definition Production Operation Divestment

A typical five-phase project life cycle sequence:

Project Life Cycle

In the pharmaceutical industry the stages are:Preliminary research (before filing a patent);Preclinical studies (done prior to an initial new drug application - IND), andClinical trials – Phases 1, 2 and 3.

In the aerospace industry the stages are:Concept definition;Concept Development;Implementation, andLaunch and operations.

Other IP Valuation Purposes Other than for determining how much money is required

for a technology start-up, there are other reasons why intellectual property is valued: Transaction support sale Bankruptcy Licensing Strategic alliances Infringement damages Intercompany transactions Collateral based financing Accounting requirements Regulatory requirements

Preparing resources

The focus in FTS is on Financial resources

Financial Strategy Framework

The three financial management decision

areas common to all business are:I. Investment decisions;

II. Financing decisions, and

III. Dividend payout decisions (in the case of technology ventures: exit options)

Financial Strategy Framework

I. Investment decisions The efficient allocation of resources to develop

the new technology for commercialisation They are the source of future cash flows, growth,

support for the venture’s continued viability and are based on detailed plans (capital budgets) for committing new funds to predominantly three areas of activity: Major spending programs such as R&D and marketing Working capital Physical assets

Financial Strategy Framework

II. Financing decisions

Form of financing: Debt, equity or convertible securities (Is this a good option? Why?)

Optimal capital structure consideration May varies over different stages

Owner facing trade-off decision Other potential financiers of the venture, such as

venture capital companies Profit allocation decision

Financing the entrepreneur firm Four factors:

Uncertainty Asymmetric information The nature of its assets Market conditions

Financial Strategy Framework

III. Dividend payout decisions (exit options) For a venture, the relevant decision in this

context would be the exit options available to the entrepreneurs and equity funding parties.

Opportunity

Business Strategy

R&DOperationsGrowthFinancingMarketingValue Creation

FinancialStrategy

RiskReturnReal options

Sources

DebtEquityStrategic AllianceHybrids

Figure 2.5 Financial Strategy

Critical Variables in Fund Raising

Gompers et al. (2002) identified four broad categories of

factors that influence the source of funds are identified as: Uncertainty: the dispersion of potential outcomes relating to

information, competition, marketing etc.; Asymmetric information: moral hazards and adverse

selection problems; Market conditions: supply of capital, cost of capital, capital

structure, and Monitoring and evaluation: relationship between investors

and entrepreneurs

Critical Variables in Fund RaisingThe following factors determine the nature and type of the

financing for the venture:

Accomplishments and performance

Investor’s perceived risk

Industry and technology

Venture upside potential and anticipated exit timing

Venture anticipated growth rate

Venture age and stage of development

Required rate of return (IRR)

Capital required and prior valuation of venture

Founders’ goals regarding growth, control, liquidity and harvesting

Relative bargaining position

Investor’s required terms and covenants

Project Life Cycle & Funding

Funds

Required

Planning Development Implementation

Aeroscape

Industry: Concept Development > Development > Building > Launch

Pharmaceutical

Industry: Basic Research >Phase I & II > Phase III > LT Phase IV > Pre-clinical

Technology Valuation

The project life cycle can be used to defined 3

key financial concepts:

1. Funding requirements (timing of funding)

2. Risk-return trade-off (cash flow lag)

3. Financial strategies (debt or equity?)

New Venture/Entrepreneurial Finance State of play in technology finance:

Most financial techniques or methodologies are suitable for mature technology contexts, where there is low level of uncertainty.

Maturity of Technology

Stage of Market Development

Early Late

Low

High

Difficult to apply

Most useful

FOCUS: Technological Entrepreneurial Finance

Study the issues relating

1. Technology valuation

2. Valuation of IP/intangibles

3. Project financing

4. Financing strategy

1. Technology Valuation

Highly idiosyncratic and depends on maturity of technologies

Lower maturity results in higher uncertainty about cash-flows/marketability

2. Valuation of IP/Intangibles

Assessing the value of IP Market valuation of IP Valuation of R&D Value of a knowledge intensive firm

3. Project Financing

Sources of finance Matching sources to projects at different

stages of maturity

4. Financing Strategy

Differences b/w start-ups & large firms Business plan Market signalling Relevant financial information How information is factored into the value of

a knowledge intensive firm

Lecture summary

Technology innovation and Intellectual capital Intellectual capital valuation and firm value Cash flow, timing and risk factor in valuation Financial strategy framework Focus: Technological Entrepreneurial Finance

Related Documents