Tech Mahindra CMP: INR1,036 TP: INR1,260 Buy Valuation summary (INR b) Y/E March 2013E 2014E 2015E Sales 68.6 76.5 81.2 EBITDA 14.5 15.2 15.0 Adj. PAT 12.6 13.9 15.8 Adj. EPS (INR) 95.5 105.0 120.0 EPS Gr. (%) 35.7 9.9 14.3 BV/Sh.(INR) 421.3 532.8 648.8 RoE (%) 23.4 22.7 21.0 RoCE (%) 22.5 20.5 19.8 Payout (%) 5.2 5.7 6.7 Valuation P/E (x) 10.8 9.9 8.6 P/BV (x) 2.5 1.9 1.6 EV/EBITDA (x) 8.6 8.2 7.6 Div. Yield (%) 0.5 0.6 0.8 22 February 2013 Update | Sector: Technology BSE SENSEX S&P CNX 19,325 5,852 Ashish Chopra ([email protected]) +91 22 3982 5424 eMerging stronger Benefits of integration go beyond de-risked profile Merger of TECHM with Mahindra Satyam (SCS) will derive synergies from [1] scale - qualifying the company for large sized deals, [2] cross sell of services and [3] opportunity to cut cost redundancies. Client mining potential remains a growth driver at Mahindra Satyam. Growth prospects are enhanced by increasing invitations in USD50m+ TCV deals. Expect TECHM to grow steadily despite challenges in Telecom on: [1] ramp ups in a couple of large deals, [2] continued growth in their 2nd largest account, which is ~23% of revenues and [3] traction in non BT-execution. Expect FY13-15 USD revenue CAGR of 12.2% and EPS CAGR of 12%. Buy with a target price of INR1,260 which discounts FY15E EPS by 10.5x. Integration benefits go beyond de-risking revenue profile TECHM's merger synergies with SCS go beyond de-risking revenue profile, and will potentially drive better revenue growth through: [1] cross sell of services, [2] higher scale (USD2.7b combined revenue in FY13) facilitating qualifications in much larger bids, and [3] Removal of cost redundancies, thereby enhancing the earnings potential further. SCS: growth potential from client mining after steadying the ship Having addressed its concerns around client retention, employee retention; legal battles and profitability, the management bandwidth can now focus fully on growth. With revenue per client at USD4.4m (annualized) ample growth potential exists from mining alone. Across the top-tier, the metric ranges between USD6.5m-USD11.2m. Greater number of invitations in USD50m+ TCV deals bode positively for its growth prospects. Expect double-digit growth despite onus on ~82% of the business Assuming revenues from HGS acquisition (USD169m per annum) and BT (assumed at USD370m per annum in FY14) to remain flat over FY13-15, this implies the onus of revenue growth on remaining ~82% of the business. Outside BT, TECHM grew revenues at 19-23% over FY09-12. Expect TECHM to grow steadily despite challenges in Telecom on: [1] ramp ups in a couple of large deals, [2] continued growth in their 2nd largest account, which is ~23% of revenues and [3] traction in non BT-execution, with the company chasing 5-6 large deals in advanced stages. Benefits from integration could drive the next leg of re-rating; Buy TECHM trades at 9.9x FY14E EPS and 8.6x FY15E EPS. We believe that better revenue growth opportunities following integration of SCS along with revenue de-risking will drive further re-rating in valuations. We value TECHM at a 25% discount to target multiple for HCLT, due to: [1] relatively smaller scale, [2] skew of revenues towards Telecom vertical, and [3] Increasing proportion of BPO revenues. Our target price is INR1,260, which discounts its FY15E EPS by 10.5x. Investors are advised to refer through disclosures made at the end of the Research Report. Shareholding pattern (%) As on Dec-12 Sep-12 Dec-11 Promoter 47.5 56.7 70.9 Dom. Inst 20.1 18.7 15.2 Foreign 22.6 15.5 5.3 Others 9.9 9.2 8.6 1 Bloomberg TECHM IN Equity Shares (m) 127.8 M.Cap. (INR b)/(USD b) 132/2.4 52-Week Range (INR) 1,069/579 1,6,12 Rel. Perf. (%) 9/12/52 Stock performance (1 year)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Tech MahindraCMP: INR1,036 TP: INR1,260 Buy

Valuation summary (INR b)Y/E March 2013E 2014E 2015E

Sa les 68.6 76.5 81.2

EBITDA 14.5 15.2 15.0

Adj. PAT 12.6 13.9 15.8

Adj. EPS (INR) 95.5 105.0 120.0

EPS Gr. (%) 35.7 9.9 14.3

BV/Sh.(INR) 421.3 532.8 648.8

RoE (%) 23.4 22.7 21.0

RoCE (%) 22.5 20.5 19.8

Payout (%) 5.2 5.7 6.7

Valuation

P/E (x) 10.8 9.9 8.6

P/BV (x) 2.5 1.9 1.6

EV/EBITDA (x) 8.6 8.2 7.6

Div. Yield (%) 0.5 0.6 0.8

22 February 2013

Update | Sector: Technology

BSE SENSEX S&P CNX

19,325 5,852

Ashish Chopra ([email protected]) +91 22 3982 5424

eMerging strongerBenefits of integration go beyond de-risked profile

Merger of TECHM with Mahindra Satyam (SCS) will derive synergies from [1] scale -

qualifying the company for large sized deals, [2] cross sell of services and [3] opportunity

to cut cost redundancies.

Client mining potential remains a growth driver at Mahindra Satyam. Growth prospects

are enhanced by increasing invitations in USD50m+ TCV deals.

Expect TECHM to grow steadily despite challenges in Telecom on: [1] ramp ups in a

couple of large deals, [2] continued growth in their 2nd largest account, which is ~23%

of revenues and [3] traction in non BT-execution.

Expect FY13-15 USD revenue CAGR of 12.2% and EPS CAGR of 12%. Buy with a target

price of INR1,260 which discounts FY15E EPS by 10.5x.

Integration benefits go beyond de-risking revenue profileTECHM's merger synergies with SCS go beyond de-risking revenue profile, and

will potentially drive better revenue growth through: [1] cross sell of services,

[2] higher scale (USD2.7b combined revenue in FY13) facilitating qualifications in

much larger bids, and [3] Removal of cost redundancies, thereby enhancing the

earnings potential further.

SCS: growth potential from client mining after steadying the shipHaving addressed its concerns around client retention, employee retention; legal

battles and profitability, the management bandwidth can now focus fully on

growth. With revenue per client at USD4.4m (annualized) ample growth potential

exists from mining alone. Across the top-tier, the metric ranges between

USD6.5m-USD11.2m. Greater number of invitations in USD50m+ TCV deals bode

positively for its growth prospects.

Expect double-digit growth despite onus on ~82% of the businessAssuming revenues from HGS acquisition (USD169m per annum) and BT (assumed

at USD370m per annum in FY14) to remain flat over FY13-15, this implies the onus

of revenue growth on remaining ~82% of the business. Outside BT, TECHM grew

revenues at 19-23% over FY09-12. Expect TECHM to grow steadily despite

challenges in Telecom on: [1] ramp ups in a couple of large deals, [2] continued

growth in their 2nd largest account, which is ~23% of revenues and [3] traction in

non BT-execution, with the company chasing 5-6 large deals in advanced stages.

Benefits from integration could drive the next leg of re-rating; BuyTECHM trades at 9.9x FY14E EPS and 8.6x FY15E EPS. We believe that better revenue

growth opportunities following integration of SCS along with revenue de-risking

will drive further re-rating in valuations. We value TECHM at a 25% discount to

target multiple for HCLT, due to: [1] relatively smaller scale, [2] skew of revenues

towards Telecom vertical, and [3] Increasing proportion of BPO revenues. Our

target price is INR1,260, which discounts its FY15E EPS by 10.5x.

Investors are advised to refer

through disclosures made at the end

of the Research Report.

Shareholding pattern (%)As on Dec-12 Sep-12 Dec-11

Promoter 47.5 56.7 70.9

Dom. Inst 20.1 18.7 15.2

Foreign 22.6 15.5 5.3

Others 9.9 9.2 8.6

1

Bloomberg TECHM IN

Equity Shares (m) 127.8

M.Cap. (INR b)/(USD b) 132/2.4

52-Week Range (INR) 1,069/579

1,6,12 Rel. Perf. (%) 9/12/52

Stock performance (1 year)

Tech Mahindra

22 February 2013 2

Integration benefits go beyond de-risking revenue profile......offer synergies on growth and costs

Integration with SCS de-risks the revenue profile with reduced dependency on top client

(BT will come down to 12% as per our estimates) and Telecom vertical; and also balances the

geography mix.

Revenue synergies emanate from larger scale of merged entity (USD2.7b in FY13) with

mature practices across diverse segments, qualifying it for larger deals.

Additionally, potential exists to cross-sell of Satyam's Enterprise services and Engineering

solutions to TECHM's clients.

Apart from economies of scale, the merger will create some synergies on the cost front as

well, with the company able to do away with redundancies in processes, facilities etc.

With only procedural aspects in the way of the merger of TECHM with SCS, we see the

combined entity benefit the prospects of the companies on the following fronts:

De-risking business profile through diversification:The combined entity will see much more balanced mix of geography-wise revenue

spread and reduction in dependency on top accounts. This de-risking bodes positively

for valuations in the long run. Geographically, TECHM derives a significant portion of

its revenues from Europe, while Mahindra Satyam's business is highly focused on

Americas. The amalgamated entity will have a more balanced share of revenue

contribution from three key geographies viz Americas, Europe and Rest of World.

Well balanced geographic exposure

Source: Company, MOSL

Merger of TECHM with

SCS de-risks geographic

exposure and clients

exposure

Tech Mahindra

22 February 2013 3

Secondly, despite contraction in absolute revenues obtained from BT, the client

continues to constitute ~1/3d of the revenues for TECHM. That dependency will come

down to 12% after the merger with SCS, after considering revenues from acquisition

of HGS, Comviva and Complex IT. Contribution from top-10 clients will get cut from

77% at TECHM currently to 57%.

Dependency on top client to reduce significantly post integration

Source: Company, MOSL

Facilitate revenue growth through cross sell of servicesTECHM's offerings and expertise have been mainly in services like ADM, BPO, Network,

ITO and Security. Integration with SCS lends company the ability to offer a wider

range of offerings like Enterprise Services and Engineering Services to current and

future customers. Conversely, there are services at TECHM, expertise in which would

be sellable to clients at SCS as well.

Working directly with companies in Telecom domain has forced TECHM's hand at

continuously building capabilities in areas like Mobility, Collaboration and Cloud

computing. The offerings in these areas are not restricted to the Telecom vertical

alone and will find demand in other verticals as well, which are addressed by SCS.

Revenue synergies from

the acquisition emanate

from cross-sell of

services and more

qualifications for larger

deals

To come down to 12% after

factoring acquisitions

BT dependency to reduce

Proportion of BT revenues

in 9MFY13 (%) 32.5

Stable state revenues

from BT (USD m) 370

Combined entity revenues

in FY14 (USD m) 3,081

BT dependency post

merger (%) 12.0

Tech Mahindra

22 February 2013 4

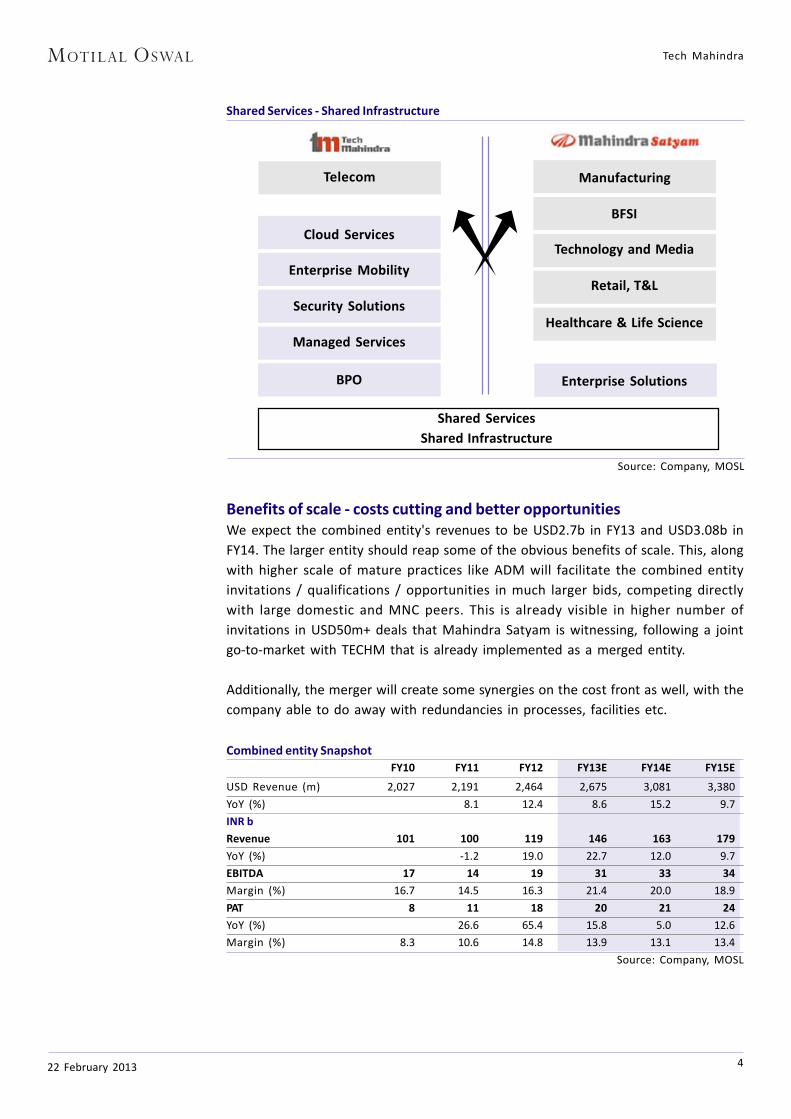

Shared Services - Shared Infrastructure

Source: Company, MOSL

Telecom

Cloud Services

Enterprise Mobility

Security Solutions

Managed Services

BPO

Manufacturing

BFSI

Technology and Media

Retail, T&L

Healthcare & Life Science

Enterprise Solutions

Shared Services

Shared Infrastructure

Benefits of scale - costs cutting and better opportunitiesWe expect the combined entity's revenues to be USD2.7b in FY13 and USD3.08b in

FY14. The larger entity should reap some of the obvious benefits of scale. This, along

with higher scale of mature practices like ADM will facilitate the combined entity

invitations / qualifications / opportunities in much larger bids, competing directly

with large domestic and MNC peers. This is already visible in higher number of

invitations in USD50m+ deals that Mahindra Satyam is witnessing, following a joint

go-to-market with TECHM that is already implemented as a merged entity.

Additionally, the merger will create some synergies on the cost front as well, with the

company able to do away with redundancies in processes, facilities etc.

Combined entity Snapshot

FY10 FY11 FY12 FY13E FY14E FY15E

USD Revenue (m) 2,027 2,191 2,464 2,675 3,081 3,380

YoY (%) 8.1 12.4 8.6 15.2 9.7

INR b

Revenue 101 100 119 146 163 179

YoY (%) -1.2 19.0 22.7 12.0 9.7

EBITDA 17 14 19 31 33 34

Margin (%) 16.7 14.5 16.3 21.4 20.0 18.9

PAT 8 11 18 20 21 24

YoY (%) 26.6 65.4 15.8 5.0 12.6

Margin (%) 8.3 10.6 14.8 13.9 13.1 13.4

Source: Company, MOSL

Tech Mahindra

22 February 2013 5

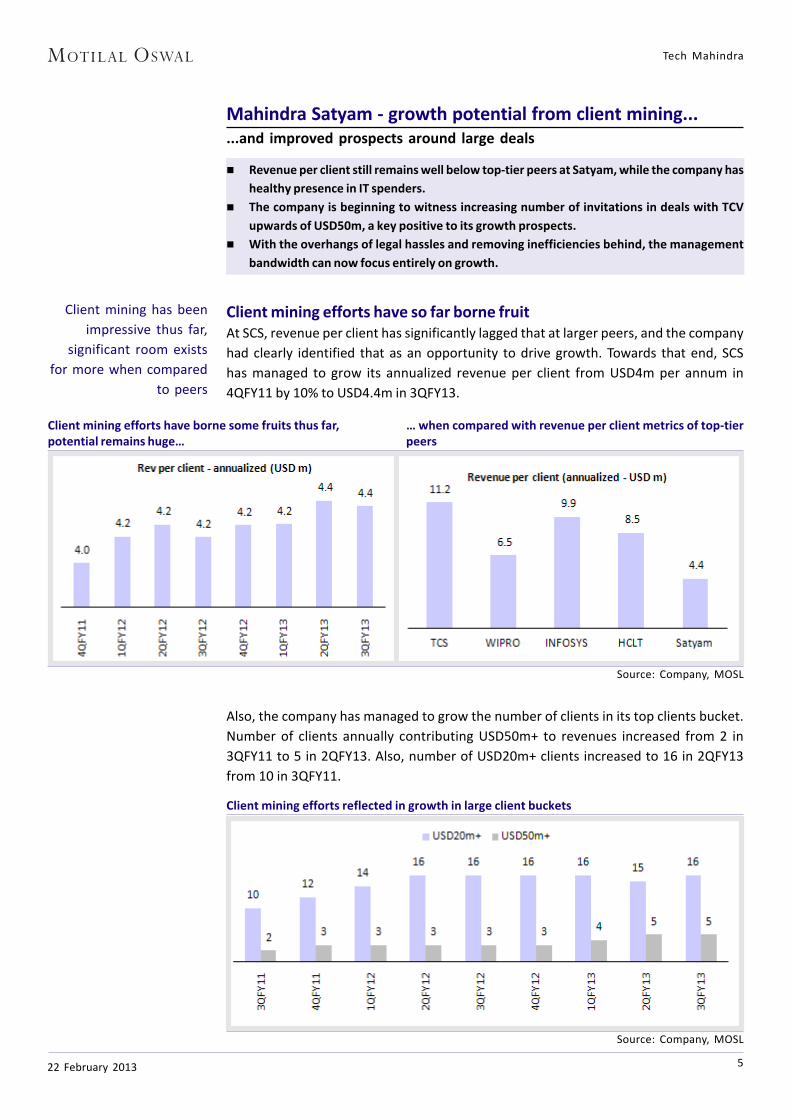

Mahindra Satyam - growth potential from client mining......and improved prospects around large deals

Revenue per client still remains well below top-tier peers at Satyam, while the company has

healthy presence in IT spenders.

The company is beginning to witness increasing number of invitations in deals with TCV

upwards of USD50m, a key positive to its growth prospects.

With the overhangs of legal hassles and removing inefficiencies behind, the management

bandwidth can now focus entirely on growth.

Client mining efforts have so far borne fruitAt SCS, revenue per client has significantly lagged that at larger peers, and the company

had clearly identified that as an opportunity to drive growth. Towards that end, SCS

has managed to grow its annualized revenue per client from USD4m per annum in

4QFY11 by 10% to USD4.4m in 3QFY13.

Client mining efforts have borne some fruits thus far, … when compared with revenue per client metrics of top-tierpotential remains huge… peers

Source: Company, MOSL

Also, the company has managed to grow the number of clients in its top clients bucket.

Number of clients annually contributing USD50m+ to revenues increased from 2 in

3QFY11 to 5 in 2QFY13. Also, number of USD20m+ clients increased to 16 in 2QFY13

from 10 in 3QFY11.

Client mining efforts reflected in growth in large client buckets

Client mining has been

impressive thus far,

significant room exists

for more when compared

to peers

Source: Company, MOSL

Tech Mahindra

22 February 2013 6

Source: Company, MOSL

2. Employee Retention: The company's attrition rate is down to 13.1% in 3QFY13

from 25% in 3QFY11. Although this is partly attributed to the environment, we

cannot ignore the fact that attrition is now among the lowest in the industry from

among the highest earlier.

Seeing higher number of qualifications in larger deals: While environment may not

be supporting potential signing of higher number of large deals, the turnaround at

SCS has held it in good stead. The pipeline of large deals remains impressive, and the

company cited marked improvement in invitations for larger opportunities. Earlier,

the company faced challenges in getting invited for USD30m-USD50m deals, but that

has changed now, with many invitations for deals upwards of USD50m each.

Clients who left SCS during the uncertain times have started returning to the Mahindra

Satyam fold. Clients that had imposed an embargo on awarding fresh projects, have

since revoked their decision. This has driven confidence of the management in

growing revenues in line with the industry going forward.

See management bandwidth focused on growth after addressing concernsWith contingencies largely dealt with, and the turnaround impressively completed,

the bandwidth can now focus on growth. The company has already started seeing the

number of invitations in USD50m+ TCV deals go up, which bodes positively for revenue

growth, along with ample potential to drive growth through client mining.

Concerns largely addressed: Mahindra Satyam has come a long way in its recovery

process which was focused on addressing the concerns around the following:

1. Customer Retention: Mahindra Satyam's focus on mining existing accounts better

has been a key driver of revenues over the past couple of years.

SCS has managed to continue increasing its customer base despite tainted recent-past

Higher number of

invitations for USD50m+

TCV deals augurs well for

growth

With key concerns

successfully addressed,

the management

bandwidth and now stay

fully focused on growth

Tech Mahindra

22 February 2013 7

Attrition was among the highest in the industry, is now among the lowest

Source: Company, MOSL

3. Dispute resolution: Most of the litigations are now behind the company, with the

only prominent ones being domestic in nature (companies of Raju family and

Income tax).

4. Improving profitability: 21.6% EBITDA margin in 3QFY13 has been a steady

improvement from 5.9% reported in 2QFY11.

EBITDA margin profile has completely turned around on impressive execution

Source: Company, MOSL

Tech Mahindra

22 February 2013 8

TECHM: Growth visibility despite a bleak outlook on TelecomMultiple growth drivers to make up for further potential declines in BT

Ramp-up in large deals lend visibility to growth in the near-term.

AT&T (2nd largest client) continues to be a growth account for the company. With wallet size

bigger than BT, potential to penetrate further remains.

Trends such as vendor consolidation, emerging technologies and under-outsourced players

continue to remain additional growth drivers despite weak Telecom environment.

Source: Company, MOSL

Ramp-ups in a couple of large deals won: The large deal that TECHM announced in

2Q is expected to yield only some revenues in 2HFY13. So, FY14 will be the first

full year of revenues from that account. Also, the company announced a

significantly large 5-year deal in 3Q, revenues from which will start flowing in

FY14.

Healthy large deal pipeline: The company is chasing 5-6 large deals in which it

either features among the last 2 short-listed candidates or it is in contract signing

stages.

Moving out of headwinds from weeding of unprofitable BPO accounts: Tech

Mahindra revenues have been impacted negatively by ~USD30m on account of

Etisalat, order cancellation by Cox communications and some rationalization in

low margin Indian BPO accounts. There will be no further impact next year from

these factors.

Why TECHM could match peer growth despite challenges in Telecom? Traction in second largest customer: Second largest customer grew 20%+ in FY12

and is growing in double digits in FY13. For FY14, the company expects growth to

taper off v/s FY13 on ~USD300m annual base. Growth outlook is close to double

digits in FY14.

Growth in top accounts excluding BT: Outside of BT, TECHM has managed

impressive growth in its top accounts over the past few years. Since 1QFY11,

revenue growth at TECHM has been driven by top 2-10 accounts - over 1QFY11-

2QFY13, top 2-5 accounts have grown at a CQGR of 5% and top 6-10 accounts have

growth at a CQGR of 4.5%.

Top 2-10 clients have driven growth at Tech Mahindra (3Q spike in top 2-5 on HGS acquistion)

Expect TECHM to grow

steadily despite

challenges in Telecom on:

[1] ramp ups in a couple

of large deals, [2]

continued growth in their

2nd largest account,

which is ~23% of

revenues and [3] traction

in non BT-execution, with

the company chasing 5-6

large deals in advanced

stages

Tech Mahindra

22 February 2013 9

Growth on a small base of multiple trends over the long runEmerging technologies have seen rapid growth in spends, albeit on a small base. The

wave in mobility puts TECHM in the right place in terms of the industry serviced by its

customer base, with following opportunities that could be tapped to grow:

growth in mobile devices has been driving investments in mobile data networks

and application development.

video is increasingly taking a major share of the mobile data traffic, driving TSPs

to invest in content delivery networks.

IT vendors will look to help companies seeking to monetize and benefit from

prominence of social networking and cloud computing

While these are trends capable of driving growth more over the longer term, their

base today is relatively low, and also the nature of services is largely discretionary.

However, growth drivers over the near term for TECHM continue to be:

[1] Under outsourced clients

[2] Vendor consolidation - where the vendors that largely face the threat of losing out

are local players and large MNC competition

[3] Emerging markets.

Tech Mahindra

22 February 2013 10

Expect double-digit revenue and earnings CAGR......despite onus of growth on 82% of the business

We expect USD revenue CAGR of 12.2% over FY13-15E and an EPS CAGR of 12% during this

period at the combined entity.

Assuming revenues from HGS (USD169m per annum) and BT (USD370m per annum from

FY14) to remain flat over FY13-15, this implies the onus of revenue growth is on remaining

82% of the business.

Outside BT, TECHM grew revenues at the rate of 19-23% over FY09-12, which should continue

to grow on the back of: [1] ramp ups in a couple of large deals, [2] continued growth in their

2nd largest account, which is ~23% of revenues and [3] traction in non BT-execution, with

the company chasing 5-6 large deals in advanced stages.

Expect revenue CAGR of 12.2% over FY13-15E in the combined entityWe expect USD revenue CAGR of 12.2% over FY13-15E and an EPS CAGR of 12% during

this period at the combined entity. Our estimates on growth assume the following:

We assume annualized revenues from BT stabilizing at USD370m going forward in

FY14 and FY15. This compares with USD430m in FY12 and USD200m in 1HFY13.

Revenue from acquisition of Hutchison Global Services (HGS) remains flat at

USD169m per annum.

Outside of acquisitions and BT, the implied CAGR in our growth estimate for Tech

Mahindra is 10% over FY13-15, without assuming any growth in Comviva. Over FY08-

FY12, non-BT revenues grew in the range of 19-23% in each year for the company, and

we see drivers like large deals, emerging geographies, gain share in AT&T and vendor

consolidation trend continue to fuel growth.

Revenues outside BT have grown at a healthy rate for TECHM, despite weak Telecom vertical

Source: Company, MOSL

Non-BT revenues have

grown in the range of 19-

23% over FY08-12,

despite weak spending in

Telecom

We note growth in non-BT revenues in FY13 is on the back of acquisitions at HGS and

Comviva, and on an organic basis , revenue growth has been softer due to weeding

our of some nom-profitable domestic BPO accounts and also impact of closure of

operations by Telecom clients following the 2G scam revelations.

Tech Mahindra

22 February 2013 11

Earnings growth will not lag given focus on marginsDeclining revenue base of BT and increasing proportion of revenues from service like

BPO and segments like emerging geographies have been key headwinds to operating

profit margins at TECHM. The margins saw a steep fall from 25.2% in 1QFY10 to 15.3%

in 2QFY12. However, impressive cost containment efforts on the part of the

management, along with the currency tailwinds have helped take the EBITDA margins

back to ~21%.

EBITDA margin has picked up from the low of 15.3% on cost containment measures, also aided bycurrency

Source: Company, MOSL

Over FY08-FY12, personnel costs as a % of revenue have increased from 41% to 52%, a

11pp hit on OPM. In the same period, non-personnel operating costs have improved

~600bp from 37% of revenues in FY08 to 31% of revenues in FY12. This was largely

facilitated by two cost items - Travel and Communication, which declined from 15.6%

of revenues in FY08 to 7.8% in FY12.

Rationalization in non-personnel operating expenses have helped curtail the margin slide

Source: Company, MOSL

Strong focus on cost

control in the past helped

avert potential margin

crisis, will keep

profitability steady going

forward

Tech Mahindra

22 February 2013 12

Source: Company, MOSL

For the combined entity, our EBITDA margin estimate for FY14 stands at 20% (-140bp)

and that in FY15 is 18.9% (-110bp). The drop in margins is largely the portion of

unabsorbed wage hikes, to cushion which, industry growth needs compare with the

yesteryears. Stable performance on margins coupled with our expectation of healthy

execution on growth drive our estimate of 12% EPS CAGR over FY13-15.

Expect earnings to map revenue growth going forward

Tech Mahindra

22 February 2013 13

Benefits from integration could drive re-rating; BuyTarget price discounts FY15E EPS by 10.5x; 25% discount to HCLT

Potential to re-rate comes from revenue and cost synergies at the merged entity in addition

to de-risking of business; and also healthy growth prospects at Satyam.

We value TECHM at 25% discount to HCLT due to smaller scale, higher exposure to Telecom

and BT.

Buy with a price target of INR1,260 based on 10.5x FY15E EPS.

TECHM currently trades at valuations that are closer to its median multiple over FY09-

FY13, when the Telecom vertical has seen the most challenges in technology spend.

The stock trades at 9.9x FY14E EPS and 8.6x FY15E EPS.

We see re-rating potential at TECHM given the following: [1] revenue and cost

synergies post integration with Satyam, [2] de-risking of business profile post the

integration, and [3] increased management focus on growth after completing the

turnaround at Satyam and having taken care of the contingencies

Tech Mahindra enjoys the scale that compares to tier-I players and margins at the

upper end of tier-II counterparts (and comparable to HCL Tech among tier-1). Scale of

the combined entity will help them qualify for greater number of multi-service bid.

We value TECHM at a 25% discount to our target multiple for HCLT, due to: [1]

comparatively smaller scale, [2] skew of revenues towards Telecom vertical, and [3]

Increasing proportion of BPO. Our target price for TECHM is INR1,260, which discounts

its FY15E EPS by 10.5x (25% discount to HCL Tech).

1 year forward P/E 1 year forward P/BV

Tech Mahindra

22 February 2013 14

Tech Mahindra: Financials and Valuation

Income Statement (INR Million)Y/E March 2011 2012 2013E 2014E 2015E

Sales 48,413 54,897 68,588 76,532 81,206

Change (%) 4.7 13.4 24.9 11.6 6.1

Total Expenses 38,518 45,703 54,065 61,343 66,248

EBITDA 9,895 9,194 14,523 15,188 14,959

% of Net Sales 20.4 16.7 21.2 19.8 18.4

Depreciation 1,435 1,614 1,931 2,133 2,233

Interest 999 1,413 1,060 1,170 1,030

Other Income 1,174 1,368 -553 747 1,293

PBT 8,635 7,535 10,978 12,632 12,989

Tax 1,315 1,438 2,409 2,969 3,117

Rate (%) 15.2 19.1 21.9 23.5 24.0

PAT 7,320 6,097 8,569 9,664 9,872

Minority Interest & EO items 652 714 125 230 264

Share of associate's profits 2,120 5,534 5,734 5,720 6,237

PAT before EO 8,788 10,918 14,178 15,153 15,845

Change (%) 6.3 24.2 29.9 6.9 4.6

Effect of restructuring fees -1,695 -1,618 -1,561 -1,285 0

PAT after RF before EO 7,093 9,299 12,617 13,868 15,845

Change (%) 7.4 31.1 35.7 9.9 14.3

Extraordinary Items (EO) 629 679 0 0 0

PAT after EO 7,722 9,978 12,617 13,868 15,845

Change (%) 15.5 29.2 26.4 9.9 14.3

Balance Sheet (INR Million)Y/E March 2011 2012 2013E 2014E 2015E

Share Capital 1,260 1,275 1,277 1,275 1,275

Share Premium 2,374 2,374 2,374 2,374 2,374

Reserves 29,881 39,658 50,208 64,464 79,286

Net Worth 33,514 43,307 53,858 68,112 82,934

Minority Interest 159 0 0 5 10

Loans 12,227 11,266 13,179 11,861 7,861

Deferred Revenue 5,837 0 0 0 0

Capital Employed 51,737 54,573 67,037 79,978 90,805

Gross Block 12,783 15,095 22,837 25,337 29,337

Less : Depreciation 6,613 8,227 10,158 12,291 14,524

Net Block 6,170 6,868 12,679 13,046 14,813

CWIP 1,105 1,629 2,126 1,500 1,500

Investments 29,080 35,876 42,258 35,298 34,913

Deferred Tax Assets 638 998 1,077 1,077 1,077

Curr. Assets 23,455 20,437 33,791 50,281 60,013

Debtors 12,468 13,172 22,196 21,223 23,114

Cash & Bank Balance 2,666 2,418 7,929 14,056 21,095

Loans & Advances 8,315 4,845 6,463 13,145 13,947

Other Current Assets 6 2 -2,797 1,857 1,857

Current Liab. & Prov 8,711 11,235 24,893 21,223 21,510

Creditors 5,631 10,377 10,076 9,726 10,672

Provisions 3,080 3,080 14,817 11,497 10,838

Net Current Assets 14,744 9,202 15,079 29,058 38,503

Application of Funds 51,737 54,573 67,037 79,978 90,805

E: MOSL Estimates

Tech Mahindra

22 February 2013 15

Tech Mahindra: Financials and Valuation

RatiosY/E March 2011 2012 2013E 2014E 2015E

Basic (INR)

EPS 56.3 72.9 98.7 108.5 124.0

Diluted EPS 54.3 70.4 95.5 105.0 120.0

Cash EPS 65.2 82.6 110.2 121.2 136.9

Book Value 266.0 339.7 421.3 532.8 648.8

DPS 4.0 4.0 5.0 6.0 8.0

Payout % 7.4 5.7 5.2 5.7 6.7

Valuation (x)

P/E 14.7 10.8 9.9 8.6

Cash P/E 12.5 9.4 8.6 7.6

EV/EBITDA 14.7 8.6 8.2 7.6

EV/Sales 2.5 1.8 1.6 1.4

Price/Book Value 3.0 2.5 1.9 1.6

Dividend Yield (%) 0.4 0.5 0.6 0.8

Profitability Ratios (%)

RoE 24.8 26.0 23.4 22.7 21.0

RoCE 18.5 21.4 22.5 20.5 19.8

Turnover Ratios

Debtors (Days) 86 85 94 104 100

Fixed Asset Turnover (x) 4.0 3.9 3.6 3.2 3.0

Leverage Ratio

Debt/Equity Ratio(x) 0.4 0.3 0.2 0.2 0.1

Cash Flow Statement (INR Million)Y/E March 2011 2012 2013E 2014E 2015E

CF from Operations 15,718 3,692 27,061 9,856 17,630

Change in Working Capital -11,261 7,778 -10,515 -6,451 -1,569

Net Operating CF 4,457 11,470 16,546 3,406 16,061

Net Purchase of FA 541 -2,836 -8,238 -1,874 -4,000

Net Purchase of Invest. 1,065 -6,796 -1,082 6,813 0

Net Cash from Invest. 1,606 -9,632 -9,321 4,939 -4,000

Inc./Dec in Equity & other rel. items -3,549 -528 -2,879 -2 0

Proceeds from LTB/STB -1,445 -961 1,913 -1,318 -4,000

Dividend Payments -590 -597 -748 -897 -1,023

Cash Flow from Fin. -5,584 -2,086 -1,714 -2,217 -5,023

Free Cash Flow 4,998 8,634 8,307 1,531 12,061

Net Cash Flow 479 -248 5,511 6,127 7,038

Opening Cash Balance 2,187 2,666 2,418 7,929 14,056

Add: Net Cash 479 -248 5,511 6,127 7,038

Closing Cash Balance 2,666 2,418 7,929 14,056 21,095

E: MOSL Estimates

Motilal Oswal Securities LtdMotilal Oswal Tower, Level 9, Sayani Road, Prabhadevi, Mumbai 400 025

Phone: +91 22 3982 5500 E-mail: [email protected]

DisclosuresThis report is for personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. This research report does not constitute an offer, invitation or inducement

to invest in securities or other investments and Motilal Oswal Securities Limited (hereinafter referred as MOSt) is not soliciting any action based upon it. This report is not for public distribution and has beenfurnished to you solely for your information and should not be reproduced or redistributed to any other person in any form.

Unauthorized disclosure, use, dissemination or copying (either whole or partial) of this information, is prohibited. The person accessing this information specifically agrees to exempt MOSt or any of its affiliatesor employees from, any and all responsibility/liability arising from such misuse and agrees not to hold MOSt or any of its affiliates or employees responsible for any such misuse and further agrees to hold MOSt

or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

The information contained herein is based on publicly available data or other sources believed to be reliable. While we would endeavour to update the information herein on reasonable basis, MOSt and/or itsaffiliates are under no obligation to update the information. Also there may be regulatory, compliance, or other reasons that may prevent MOSt and/or its affiliates from doing so. MOSt or any of its affiliates oremployees shall not be in any way responsible and liable for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report . MOSt or any of its affiliates

or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitnessfor a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations.

This report is intended for distribution to institutional investors. Recipients who are not institutional investors should seek advice of their independent financial advisor prior to taking any investment decisionbased on this report or for any necessary explanation of its contents.

MOSt and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency, MOSt has incorporated a Disclosure of Interest

Statement in this document. This should, however, not be treated as endorsement of the views expressed in the report.

Disclosure of Interest Statement Tech Mahindra1. Analyst ownership of the stock No2. Group/Directors ownership of the stock No3. Broking relationship with company covered No4. Investment Banking relationship with company covered No

Analyst CertificationThe views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject securities or issues, and no part of the compensation of the research analyst(s) was, is, orwill be directly or indirectly related to the specific recommendations and views expressed by research analyst(s) in this report. The research analysts, strategists, or research associates principally responsible

for preparation of MOSt research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues.

Regional Disclosures (outside India)This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary tolaw, regulation or which would subject MOSt & its group companies to registration or licensing requirements within such jurisdictions.

For U.K.This report is intended for distribution only to persons having professional experience in matters relating to investments as described in Article 19 of the Financial Services and Markets Act 2000 (FinancialPromotion) Order 2005 (referred to as "investment professionals"). This document must not be acted on or relied on by persons who are not investment professionals. Any investment or investment activity towhich this document relates is only available to investment professionals and will be engaged in only with such persons.

For U.S.Motilal Oswal Securities Limited (MOSL) is not a registered broker - dealer under the U.S. Securities Exchange Act of 1934, as amended (the"1934 act") and under applicable state laws in the United States.In addition MOSL is not a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended (the "Advisers Act" and together with the 1934 Act, the "Acts), and under applicable statelaws in the United States. Accordingly, in the absence of specific exemption under the Acts, any brokerage and investment services provided by MOSL, including the products and services described herein

are not available to or intended for U.S. persons.This report is intended for distribution only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the Exchange Act and interpretations thereof by SEC (henceforth referred to as "major institutionalinvestors"). This document must not be acted on or relied on by persons who are not major institutional investors. Any investment or investment activity to which this document relates is only available to major

institutional investors and will be engaged in only with major institutional investors. In reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended(the "Exchange Act") and interpretations thereof by the U.S. Securities and Exchange Commission ("SEC") in order to conduct business with Institutional Investors based in the U.S., MOSL has entered intoa chaperoning agreement with a U.S. registered broker-dealer, Marco Polo Securities Inc. ("Marco Polo"). Any business interaction pursuant to this report will have to be executed within the provisions of this

chaperoning agreement.This website and its respective contents does not constitute an offer or invitation to purchase or subscribe for any securities or solicitation of any investments or investment services and/or shall not be consideredas an advertisement tool. "U.S. Persons" are generally defined as a natural person, residing in the United States or any entity organized or incorporated under the laws of the United States. US Citizens living

abroad may also be deemed "U.S. Persons " under certain rules.The Research Analysts contributing to the report may not be registered /qualified as research analyst with FINRA. Such research analyst may not be associated persons of the U.S. registered broker-dealer, MarcoPolo, and therefore, may not be subject to NASD rule 2711 and NYSE Rule 472 restrictions on communication with a subject company, public appearances and trading securities held by a research analyst account.

For SingaporeMotilal Oswal Capital Markets Singapore Pte Limited is acting as an exempt financial advisor under section 23(1)(f) of the Financial Advisers Act(FAA) read with regulation 17(1)(d) of the Financial Advisors

Regulations and is a subsidiary of Motilal Oswal Securities Limited in India. This research is distributed in Singapore by Motilal Oswal Capital Markets Singapore Pte Limited and it is only directed in Singaporeto accredited investors, as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time.In respect of any matter arising from or in connection with the research you could contact the following representatives of Motilal Oswal Capital Markets Singapore Pte Limited:

Nihar Oza Kadambari BalachandranEmail: [email protected] Email : [email protected]: (+65) 68189232 Contact: (+65) 68189233 / 65249115

Office address: 21 (Suite 31), 16 Collyer Quay, Singapore 049318

Related Documents