THE BILLY BOOK CASE LOWERING PROCUREMENT COST IN ORDER TO INCREASE PROFIT FOR IKEA IPAG BUSINESS SCHOOL PARIS 2014 A PURCHASING REPORT BY: - HANNES STAHRERG - IRENE FELIPE DIAZ - YOLANDA MORENO-ABADIA PEREZ - CAROLINA DIAZ JMZ LAURENT - SELENE CHANE

Team_A IKEA_Report_final version_BBA3_ERASMUS_IPAG_2014

Aug 06, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE BILLY BOOK CASE

LOWERING PROCUREMENT COST IN

ORDER TO INCREASE PROFIT FOR IKEA

I P A G B U S I N E S S S C H O O L

P A R I S 2 0 1 4

A P U R C H A S I N G R E P O R T B Y :

- H A N N E S S T A H R E R G

- I R E N E F E L I P E D I A Z

- Y O L A N D A M O R E N O - A B A D I A P E R E Z

- C A R O L I N A D I A Z J M Z L A U R E N T

- S E L E N E C H A N E

2

E X E C U T I V E S U M M A RY ABSTRACT OF THE BILLY BOOKCASE PURCHASING PROJECT

Keywords: Procurement, IKEA, Supplier(s), Purchasing

The content of this report concerns a purchasing and supply scenario for IKEA

regarding one of their products: The Billy bookcase.

The question at hand is the following statement: “How can the IKEA group create a

reality of the opportunity of lowering the procurement cost on the Billy bookcase in

order to increase the profit made from the product?”

To answer this question, our group came up with two plans, (A) Investing in new

machinery for IKEA’s current Billy bookcase supplier Gyllensvaans Möbler, AB and

(B) Change the material ABS plastic to ASA plastic which is a cheaper material to work

with.

Our conclusion is the following: The two plans mentioned in the report gave three

possibilities to achieve the goal of lowering procurement cost to increase profit. Plan

(A) where IKEA invest in new machinery for their supplier Gyllensvaans Möbler, AB

to decrease kWh consumption and increase production ratio. The second plan (B) was

to change the ABS to ASA plastic which is cheaper in kilo price. The third option,

which we recommended, was to combine the two plans if possible in order to reach the

best possible outcome for potential profit. If combining the plan is not possible for the

IKEA group, we recommend to invest in plan A since it is a more long-term

commitment with an already strong supplier relationship. In both plans, dividing the

increased profit of 2 € per unit (which is saved from a lowered procurement cost on the

Billy bookcase) is necessary as it works as an incentive for Gyllensvaans to approve of

the plans. This is because investing in new machinery would mean that Gyllensvaans

would have to pay as well. Changing the material might also come with an additional

cost. Therefore, dividing the increased profit (1 € per unit to IKEA and 1 € per unit to

Gyllensvaans) would be a gesture showing good faith in each other.

3

TA B L E O F C O N T E N T

Abstract of the billy bookcase purchasing project ...2

Methodology – Background – Opportunity .............4

1.1 Methodology ......................................................4

1.2 Background ........................................................4

1.2 Opportunity description .....................................5

Current situation.......................................................6

Where are we going? ...............................................7

Plans & recommendation .........................................8

4.1 Plan A – Invest in new machinery .....................8

4.1.1 Plan A – KPI & budget overview ...................9

4.2 Plan B – Change the materials .........................10

4.2.1 Plan B – KPI & budget overview .................10

4.3 Recommendation .............................................11

Effectiveness control following the plans ..............12

5.1 Control of the new machinery ..........................12

5.2 Control of the new material .............................12

Report conclusion for the IKEA group ..................13

Appendix list 1 - 6..................................................15

1. Product description ............................................15

- Package measurement and weight .......................15

- Assembled size ....................................................15

- Product description ..............................................16

- BILLY B. Prices in EU (€): .................................16

2. Company hierarchy (IKEA) ...............................16

3. Geography – Area of importance .......................17

4. PSTO ..................................................................18

4.1 Supplier policies of ikea...................................18

4.1.1 Value chains ..................................................19

4.1.2 TOWS-table of IKEA ...................................20

4.2 Strategic ...........................................................20

4.2.1 The strategic triangle.....................................21

4.2.2 The product portfolio ....................................21

4.2.3 The supplier portfolio ...................................21

5. Tactical ...............................................................22

5.1 Specification ....................................................22

5.2 Selecting supplier & Contracting .....................23

6. Operations ..........................................................23

6. Illustrations ........................................................24

Reference list .........................................................25

4

1 . I N T RO D U C T I O N METHODOLOGY – BACKGROUND – OPPORTUNITY

1.1 METHODOLOGY

Through-out this project, our group has worked a lot together during meetings at school.

Our primary source has been the IKEA website along with the documents they provide

from there. Another greatly appreciated source has been the documentary

“MEGAFACTORIES” made in 2009 featuring IKEA which told us a lot about the

manufacturing process of the Billy bookcase.

In this report, Irene Felipe Diaz has worked with the situation assessment, Carolina

Diaz Jmz Laurent has done the objectives, Yolanda Moreno-Abadia Perez has worked

with the appendix featured after the conclusion and Hannes Stahrberg has worked with

the plans, kpi and control. However, a lot of work has been done together which cannot

be neglected.

1.2 BACKGROUND

IKEA is known through-out the world as the giant among furniture retail stores.

Founded in 1943 in Sweden by Ingvar Kamprad, the company has become known since

for their affordable and quality orientated products. From the beginning, IKEA sold for

example pens and matches, but today the products include wardrobes, kitchen wares

and living room furnitures, all being closely looked at in regard of price, quality and

design (The IKEA concept, 2012).

One of these products which has become a time classic and international bestseller for

IKEA going on over thirty years is the “Billy bookcase” (National Geographic Channel,

2009). This bookcase was designed (similar to other IKEA standards) with the purpose

of being functional, durable and timeless and it certainly lived up to those expectations

since they have sold over 40 million units in three decades so it is understandable why

it is an IKEA bestseller (National Geographic Channel, 2009).

5

With this said, IKEA continuously tries to improve the value of the product and one of

the methods used frequently for this is trying to lower the cost of buying the product

(IKEA, 2014). It should therefore be important for IKEA to have good and reliable

relationships with their suppliers in order for them to discuss situations like this and at

the same time create value for both them and their supplier(s).

The supplier connected to this case is “Gyllensvaans Möbler, AB” whom are

responsible for manufacturing the Billy bookcase. Located in Kättilstorp, Sweden, the

company was created in 1946 by Nils Gyllensvaan and is since then managed and

owned by the family. The company generally manufactures bookcases, including the

Billy series, and has since 1952 been a continuous supplier to IKEA (Gyllensvaans

Möbler, AB, 2014).

1.2 OPPORTUNITY DESCRIPTION

To begin this section, it is important for the reader to understand that no general problem

has been found regarding the purchasing process of the Billy bookcase. However, since

IKEA’s relationship with Gyllensvaans goes back a long time, it would be reasonable

enough that they together can achieve an improvement regarding the buying and selling

of the Billy bookcase. Therefore, this section is not stated as a problem but rather an

opportunity description due to the fact that nothing regarding the profit made on the

Billy bookcase is a right out problem. It can only be stated that there is a potential

opportunity in making more profit by lowering procurement cost.

From this opportunity an important question arise, which will be the theme through-out

this report. The question which arises is the following statement:

How can the IKEA group create a reality of the opportunity of lowering

the procurement cost on the Billy bookcase in order to increase the

profit made from the product?

In order to find the most plausible and feasible solution, the report is divided into four

main categories to give a better overview. The main categories are: situation

assessment, objectives, plan and control.

6

The situation assessment will explain the current state of the purchasing process

concerning the product. It explains the current selling price and procurement cost for

IKEA.

2 . S I T UAT I O N A S S E S M E N T CURRENT SITUATION

As IKEA started in Sweden, we decided to focus our project in Älmhult, the place

where the first IKEA opened and where they still have large presence.

The product, the Billy bookcase, has a current selling price at an average of 18 € (IKEA,

2014) and with this price IKEA has an estimated current profit of 2 € for each Billy

bookcase sold. The current cost for buying the product (i.e. the procurement cost) is

now at 10.2 € per unit which they pay to their supplier Gyllensvaans Möbler who

manufacture the bookcases as stated before (See the value chains for IKEA and its

supplier in appendix 5.1.1).

The aim of this project is as mentioned to increase the profit made by the Billy bookcase

by lowering the procurement cost. To understand how this cost is going to be lowered

it is important to understand how IKEA do purchasing. The example which will soon

be stated explains how the purchasing of the product for one month at IKEA Älmhult

works. However, before this part is mentioned, it is important to have introduced the

main actors of this process.

The three main actors in this case are as follows:

The IKEA group, Älmhult

Gyllensvaans Möbler, AB

IKEA Industry Hultsfred AB - Former Swedwood (IKEA Industry, 2013)

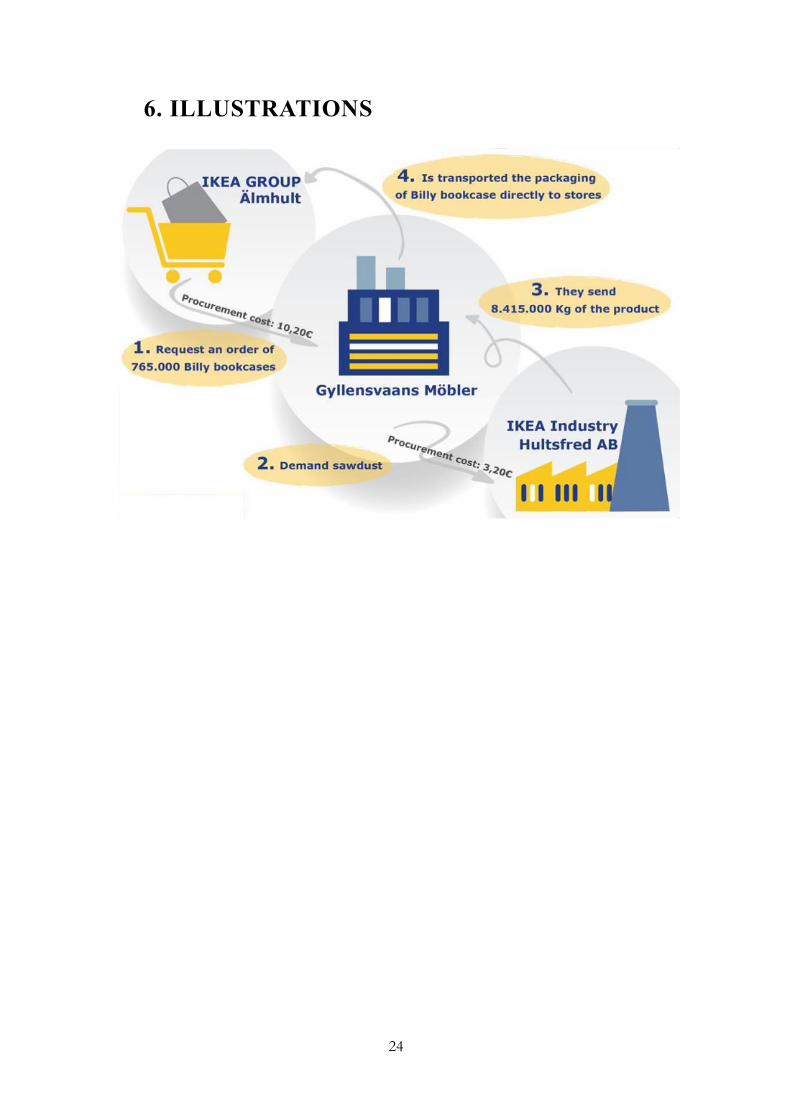

As for the current purchasing process regarding the Billy bookcase. First, the IKEA

group in Älmhult is going to issue an order of the quantity of the units they need, which

is estimated to 765.000 Billy bookcases per month (remember that the procurement cost

for each unit is 10.2 €). The supplier, Gyllensvaans, accepts the order and demands the

basic materials in order to make the bookcases which mostly consist of particle boards

made out of compressed and heated sawdust (National Geographic Channel, 2009).

Gyllensvaans issue this order with its specification to IKEA Industry Hultsfred AB in

Hultsfred. IKEA Industry receives the order and starts cutting wood to then process it

7

into sawdust. The approximate amount of sawdust that one bookcase contain is 11 kg

and the procurement cost of this is estimated to 3.2 €. To make 765.000, IKEA industry

has to send 8.415 tons of sawdust to Gyllensvaans where it is processed into particle

boards and then produced into the bookcases. The finished products is then boxed and

sent directly to the store in Älmhult where it then gets sold. To see an illustration of this

process, see appendix 6.

With the current purchasing situation for the Billy bookcase stated, it is important to

again highlight the fact that IKEA in this situation has an opportunity to work with and

not a problem. The opportunity is, as stated, to make more profit from the product.

After having revised the method how IKEA do purchasing, two suggestions to achieve

an increase in profit were made which will be stated in the next section of this report.

2 . O B J E C T I V E S

WHERE ARE WE GOING?

“The overall purpose of Inter IKEA Group is to secure continuous improvement and a

long life of the IKEA Concept. As this will require investments in both good and bad

times we strive to be financially independent” (Inter IKEA group, 2012). So we ask

ourselves: Where are we going?

Our main objective is to lower our procurement cost by two euros in one year, i.e.

reducing the cost from 10.20 € per unit to 8.20 €, keeping our quality and our supplier,

Gyllensvaans Möbler as our continued long-term contract.

Our policy is based on partnerships, identifying and executing potential business

improvements together. The objective must keep the same quality of the Billy bookcase

using the KPI stated under the control part as our guideline.

Our strategy is performance based partnership with Gyllensvaans, because instead of

making the product, IKEA buys it and therefore the partnership between the supplier

and IKEA should remain.

As written before IKEA has a long-term relationship with Gyllensvaans for over 60

years they have done business, so our Tactic is lower the procurement by 2 €.

Regarding the operation in our report; we have two plans: Plan A - Investing in new

machinery. By investing in new machinery, Gyllensvaans Möbler AB will be able to

8

produce more Billy bookcase in less time along with a reduction in electricity

consumption. Plan B includes changing materials (ABS plastics) to cheaper version of

plastic.

4 . P RO P O S A L S TAT E M E N T PLANS & RECOMMENDATION

After having done constructive research on the opportunity at hand, stating the current

situation and objectives, plan “A” and “B” were made in order to give two feasible

ways of reaching the goal of lowering procurement in order to increase the profit margin

on the Billy bookcase. The two plans differ from each other of course. However, the

scenario of combining the two is not out of the question which we will discuss further

more of later in this report.

4.1 PLAN A – INVEST IN NEW MACHINERY

As stated earlier in this report, IKEA works close with their suppliers (IKEA, 2014)

and Gyllensvaans is definitely not an exception. However, the question is if IKEA is

willing to make an investment in their suppliers. Looking at Gyllensvaans, what could

IKEA invest in so that the result becomes a lower procurement cost for the Billy

bookcase?

To lower this cost, it can be assumed that looking at the production of the bookcase

itself can be a possible source of opportunity. Gyllensvaans factory involves a lot of

machines that are all under heavy pressure to keep producing the product (National

Geographic Channel, 2009) and having an assessment of these in order to notice cost

leakages in forms of kWh consumption, missed optimization of the production ratio

and so on, could be beneficial in the quest for a cheaper bookcase.

Plan A therefore includes IKEA investing in the machinery that Gyllensvaans own and

use to produce the Billy bookcase. The intention of the investment is to update the

machinery in order to improve the production and save cost, both for IKEA but also for

Gyllensvaans. As stated in the objectives, the goal is to lower procurement cost from

10.2 € to 8.2 €. However, since it is an investment in machinery that Gyllensvaans own,

9

it would mean that Gyllensvaans have to be convinced that updating the machinery will

be a gain for them as well. Therefore, the cost saved (i.e. increased profit) ought to be

divided between Gyllensvaans and IKEA, meaning that the 2 € made should be a profit

increase of 1 € for IKEA and 1 € for Gyllensvaans. The fact that the profit is divided

between the two parties should work as an incentive for Gyllensvaans to approve of the

plan and acquire new manufacturing machinery.

4.1.1 PLAN A – KPI & BUDGET OVERVIEW

The key performance indicators for plan A are as follows:

i. Cost of the investment with Gyllensvaans machinery

ii. Quality of the purchased machinery (which in the effectiveness control would

measure kWh consumption and production ratio)

iii. Final selling price of the product

iv. Time before goal of lowered procurement is achieved

v. Budget forecast for the product after plan A has been implemented

i. The cost of the investment will be an estimate sum of 1.8 million euros. This figure

is worked out from the current assets of Gyllensvaans in 2013 along with the yearly

increase of the current assets from 2011. The calculations for this can be found in

Appendix XX page XX.

ii. The quality of the purchased machinery is vital if the objectives are going to be

reached. Since the plan includes lowering the kWh consumption along with improving

the production ratio, it is important that the new machinery actually manages to fulfill

the plan, hence why the quality of the machines must be sufficient.

iii. The final selling price of the product will remain at an average of 18 € since

increasing the profit is of interest for this project. Therefore, the lowering or increasing

the price is not of any relevance in this plan, or the overall report.

10

iv. It will take at least one year to have this plan fully implemented. An estimation of

six months research on the machinery needing replacement or update along with six

months installation process for the newly purchased machinery.

v. The budget forecast for the first year concerning the procurement of the Billy

bookcase is an estimate of 86 million euros. This is the sum of the total amount of Billy

bookcases bought (with the new procurement cost of 9.2 € / unit) plus the initial cost of

1.8 million euros investment.

4.2 PLAN B – CHANGE THE MATERIALS

Another way of looking at the opportunity to lower the procurement cost is to change

the materials instead of changing the machines that produces the product. The current

product description of the Billy bookcase can be found under Appendix 2 in order for

the reader to see what the bookcase is made of. From the description it can be read that

the bookcase contains ABS plastic which have an average price of 0.82 € per kilo in

the EU (Plasticker, 2014). Another plastic called ASA has the lower price of 0.60 € per

kilo and changing the current ABS plastic to the cheaper version will help IKEA lower

the procurement also.

The profit made will still be divided between IKEA and Gyllensvaans since changing

the material is something the supplier must do in order to achieve the goal. However,

making more profit will most likely still work as an incentive for Gyllensvaans to

approve of plan B as well.

4.2.1 PLAN B – KPI & BUDGET OVERVIEW

The key performance indicators for plan A are as follows:

i. Cost of the introducing the new ASA plastic in the product

ii. Quality of the product after having introduced the new ASA plastic

iii. Final selling price of the product

iv. Time before goal of lowered procurement is achieved

v. Budget forecast for the product after plan B has been implemented

11

i. The cost of plan B will be an estimate sum of 1 million euros. This is the estimated

cost of testing the newly introduced material. The testing of IKEA products takes place

at IKEA Test Lab in Älmhult (National Geographic Channel, 2009) and the cost will

derive from here.

ii. With this plan there are some risks when looking at the quality factors of the product.

Since IKEA’s products are quality and safety tested, the new ASA plastic might

introduce an unforeseen quality threat to the product which could as a worst case

scenario be harmful to its consumer. Therefore, thorough product testing is required,

hence why the cost of the plan might be higher than expected.

iii. The final selling price will remain the same for the same reasons stated in plan A

section 4.1.1.

iv. The time for executing and implementing plan B will be six months since it would

only require to change the one material. The factor which takes the most amount of

time in this plan is the time to test the newly introduced material.

v. The budget forecast after having implemented plan B is 84.5 million euros. This is

calculated the same way as in the budget forecast for plan A save for exchanging the

investment cost for the quality testing cost of 1 million euros.

4.3 RECOMMENDATION

If IKEA were going to have to choose between the two plans presented in this report,

our research suggests going with plan A – investing in machinery. The plan looks at a

more long-term perspective than the other, since it allows an investment with a current

supplier, strengthening the already solid bond between IKEA and Gyllensvaans. per

kilo and changing the current ABS plastic to the cheaper version will help IKEA lower

the procurement also.

However, it should be stated that combining both plan A and B is a possible solution

which will have to be addressed at some point. Investing in new machinery does not

exclude the possibility of changing the ABS plastic. In fact, it would be better to do

execute simultaneously since changing the materials might need to have a certain

technology in the machines. Therefore, it would be preferable to be able to sync the

machines to suit the newly introduced ASA plastic.

12

Therefore, our belief is to combine both plan A and B for the best possible chance to

be able to lower the procurement of the Billy bookcase.

5 . C O N T RO L EFFECTIVENESS CONTROL FOLLOWING THE PLANS

This section includes the effectiveness control of the chosen plan(s). Its purpose is to

give the reader an overview of how the monitoring of the implementation will look like.

5.1 CONTROL OF THE NEW MACHINERY

Two variables are measured here. The first (Q1) is the current kWh consumption

compared to the previous numbers. The equation would (roughly speaking) look like

this: current kWh < previous. This control is achieved by comparing monthly cost for

the electricity bound to the machines. The kWh ought to be lower than previous

machines’ electricity consumption since otherwise it would be a bad investment.

Research on what kind of machinery that will be introduced is therefore vitally

important.

The second variable, Q2, is the production ratio. This is achieved by measuring the

capability of the production and the time to produce each unit. This equation looks like

this instead: New production ratio > previous production (measured in time).

Therefore, it would be preferable to be able to sync the machines to suit the newly

introduced ASA plastic.

It is assumed that our supplier Gyllensvaans will be the party responsible for collecting

the data since having a successful implementation of the plan is of their concern as well.

5.2 CONTROL OF THE NEW MATERIAL

There are three variables included in the effectiveness control after having introduced

the new ASA plastic as a material in the Billy bookcase. These are the variables that

are tested at the IKEA Test Lab situated in Älmhult. (Q1) Normal field testing, which

include testing the product during everyday use for a simulated use of 10 years. In order

for the product to pass the requirements, the product has to withstand at least 10 years

of simulated usage. Therefore, the equation for the test is as follows: simulated years of

13

testing > 10 years otherwise it fails to meet requirements. The second variable (Q2) is

the resistibility test which includes a simulation of sun damage, liquid damage and so

on. This is also measured in time and has to pass a simulation of 10 years of resistibility

to the factors mentioned previously. Therefore, the basic equation is the same as

variable (Q1) but is performed differently. The last variable in need of control is the lab

test (Q3) or fire test since testing the rate of fire spreading seems to be a priority. The

test is measured time and how long it will take for the fire to burn out. If the fire is

extinguished before 10 minutes the product will pass the requirement. Therefore, the

equation is as follows: extinguishing time < 10 minutes (National Geographic Channel,

2009). The tests will be performed by scientists at IKEA Test Lab in Älmhult.

6 . C O N C L U S I O N REPORT CONCLUSION FOR THE IKEA GROUP

How can the IKEA group create a reality of the opportunity of lowering

the procurement cost on the Billy bookcase in order to increase the

profit made from the product?

The two plans mentioned in the report gave three possibilities to achieve the goal of

lowering procurement cost to increase profit. Plan (A) where IKEA invest in new

machinery for their supplier Gyllensvaans Möbler, AB to decrease kWh consumption

and increase production ratio. The second plan (B) was to change the ABS to ASA

plastic which is cheaper in kilo price. The third option, which we recommended, was

to combine the two plans if possible in order to reach the best possible outcome for

potential profit. If combining the plan is not possible for the IKEA group, we

recommend to invest in plan A since it is a more long-term commitment with an already

strong supplier relationship. In both plans, dividing the increased profit of 2 € per unit

(which is saved from a lowered procurement cost on the Billy bookcase) is necessary

as it works as an incentive for Gyllensvaans to approve of the plans. This is because

investing in new machinery would mean that Gyllensvaans would have to pay as well.

Changing the material might also come with an additional cost. Therefore, dividing the

14

increased profit (1 € per unit to IKEA and 1 € per unit to Gyllensvaans) would be a

gesture showing good faith in each other.

15

8 . A P P E N D I X

APPENDIX LIST 1 - 6

This appendix contains a lot of the work which is referred to through-out the report. Its

content is here to complement the power point presentation, so that it is made easier for

the reader to follow and understand the content of this report without having to look at

the power point presentation.

1. PRODUCT DESCRIPTION

The following details are important to describe the product that we have chosen to work

with. It is interesting to gain perspective of the Billy bookcase and using that

information to come to a purchasing conclusion.

- PACKAGE MEASUREMENT AND WEIGHT

Packages: 1

Article Number: 802.638.32

Width: 38 cm

Height: 6 cm

Length: 108 cm

Weight: 11.4 kg

Quantity 1

- ASSEMBLED SIZE

Depth: 28 cm

Height: 106 cm

Width: 40 cm

Max. load/shelf: 14 kg

16

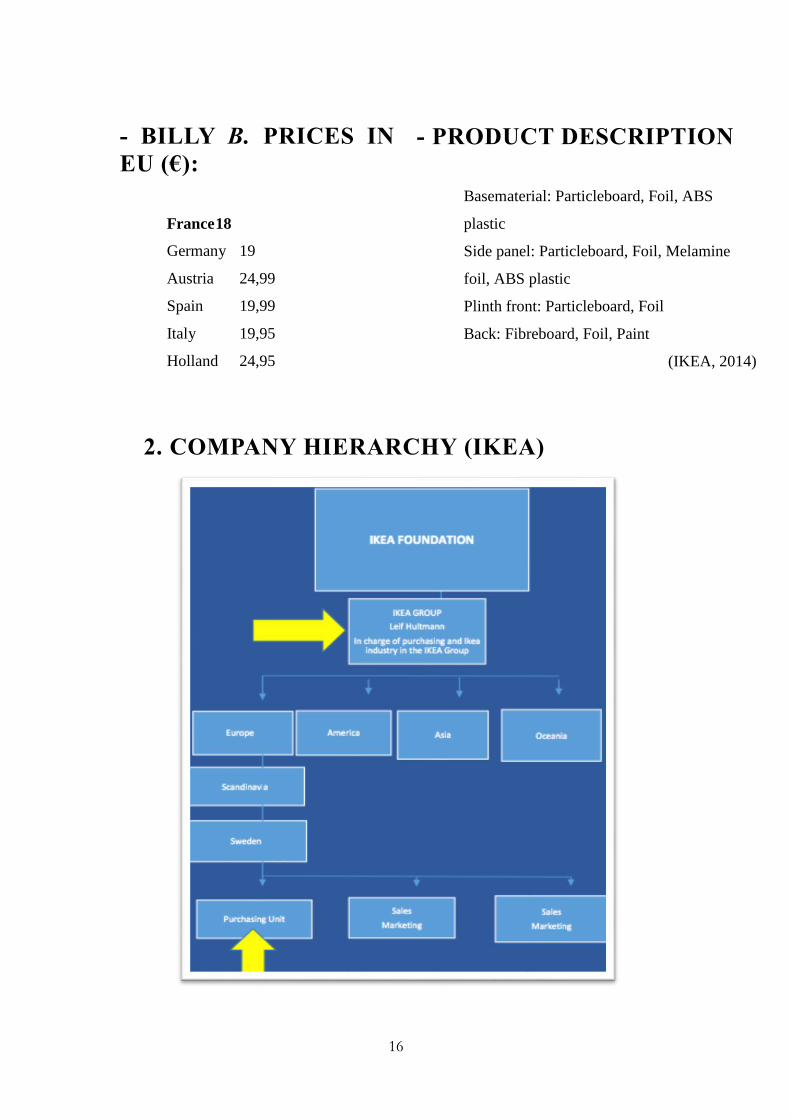

- BILLY B. PRICES IN

EU (€):

France 18

Germany 19

Austria 24,99

Spain 19,99

Italy 19,95

Holland 24,95

2. COMPANY HIERARCHY (IKEA)

- PRODUCT DESCRIPTION

Basematerial: Particleboard, Foil, ABS

plastic

Side panel: Particleboard, Foil, Melamine

foil, ABS plastic

Plinth front: Particleboard, Foil

Back: Fibreboard, Foil, Paint

(IKEA, 2014)

17

IKEA seems to work with a hybrid approach. That means managing only the global

processes that can deliver the benefits of the centralized approach, while leaving the

local parts of quality management that deliver the benefits of a decentralized approach.

In this hierarchy we had located our audience that belong to the IKEA Group

management team, whose name is Leif Hultman, and where is our team the Ikea

purchasing unit (IKEA, 2014).

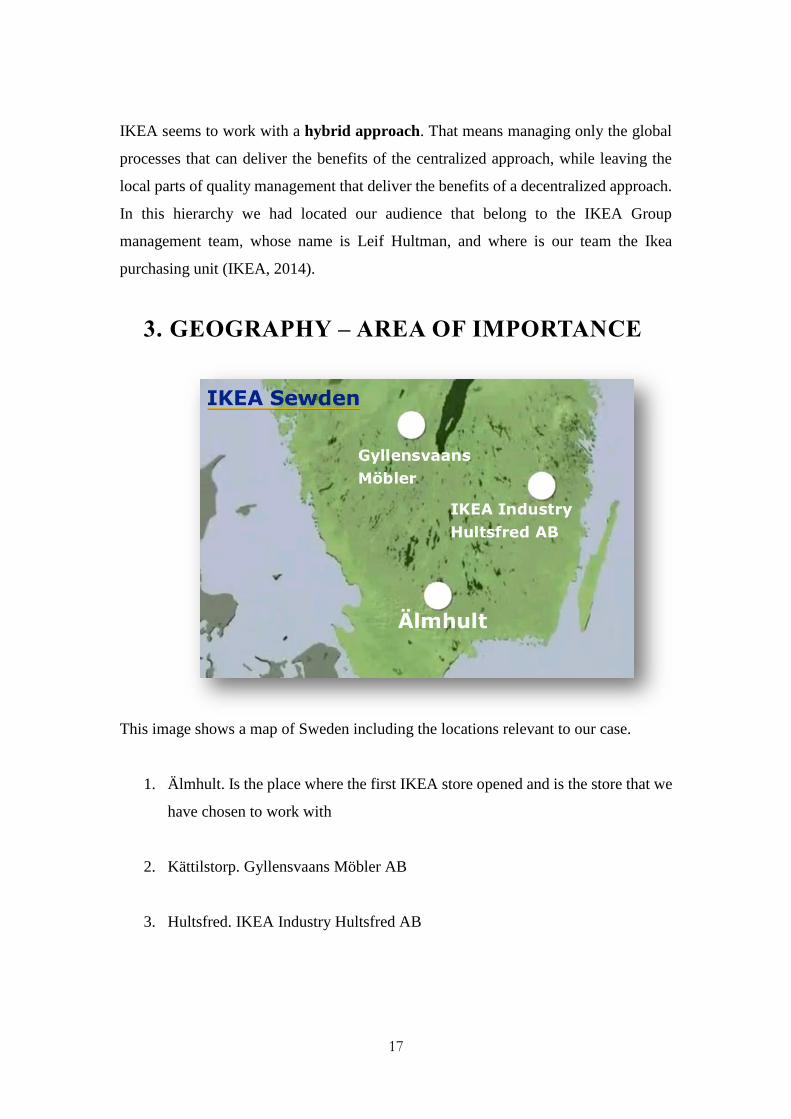

3. GEOGRAPHY – AREA OF IMPORTANCE

This image shows a map of Sweden including the locations relevant to our case.

1. Älmhult. Is the place where the first IKEA store opened and is the store that we

have chosen to work with

2. Kättilstorp. Gyllensvaans Möbler AB

3. Hultsfred. IKEA Industry Hultsfred AB

18

4. PSTO

- Policies, Strategic, Tactical and Operations

4.1 SUPPLIER POLICIES OF IKEA

- Gyllensvaans has been delivering furnitures to IKEA since 1952.

- The IKEA group aims to achieve long-term partnerships with their supplier.

- Partnerships are about identifying potential and executing business

improvements together.

- Business improvements are executed using resources from both IKEA and the

suppliers.

19

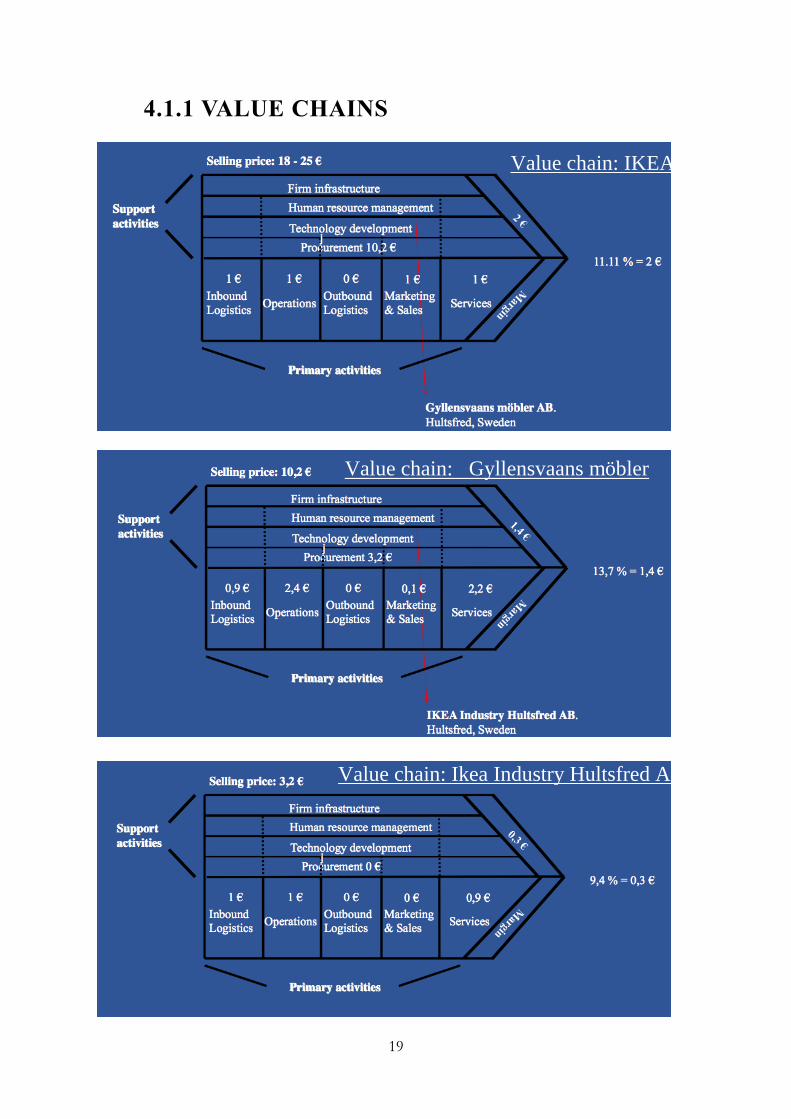

Value chain: IKEA

Value chain: Gyllensvaans möbler

AB

Value chain: Ikea Industry Hultsfred AB

4.1.1 VALUE CHAINS

20

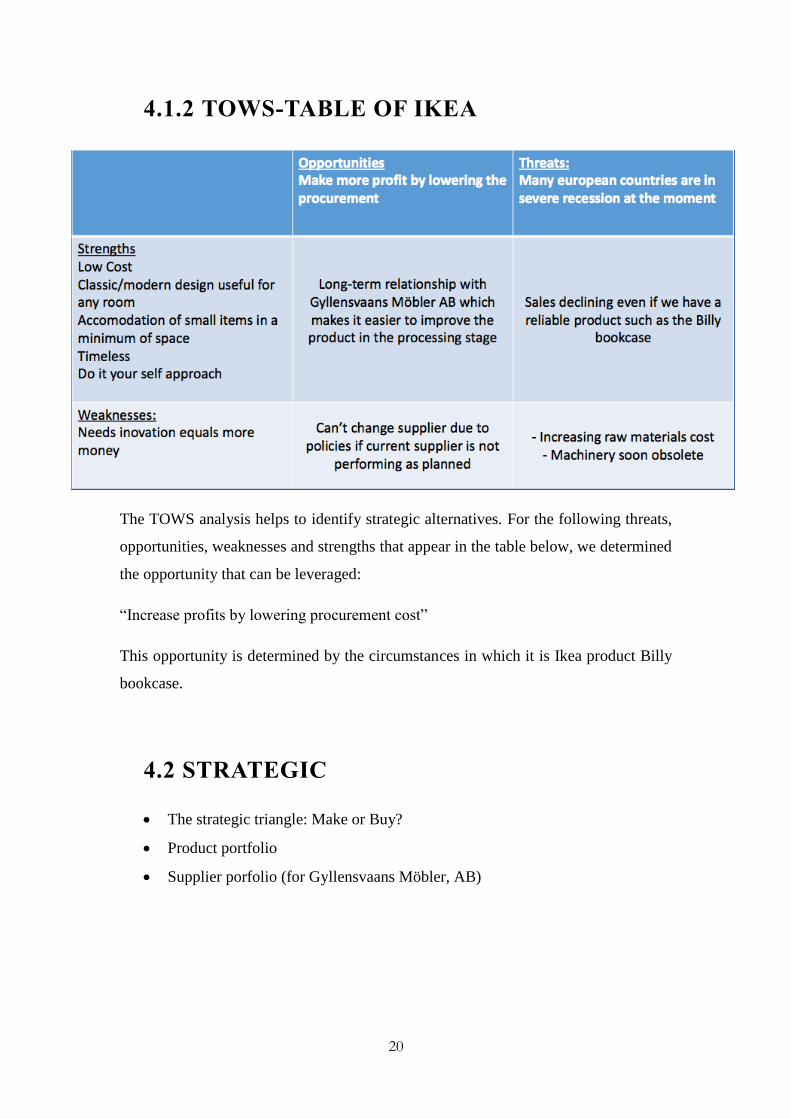

4.1.2 TOWS-TABLE OF IKEA

The TOWS analysis helps to identify strategic alternatives. For the following threats,

opportunities, weaknesses and strengths that appear in the table below, we determined

the opportunity that can be leveraged:

“Increase profits by lowering procurement cost”

This opportunity is determined by the circumstances in which it is Ikea product Billy

bookcase.

4.2 STRATEGIC

The strategic triangle: Make or Buy?

Product portfolio

Supplier porfolio (for Gyllensvaans Möbler, AB)

21

4.2.1 THE STRATEGIC TRIANGLE

Our strategy will be to buy the product and keeping the relationship with our supplier since to

Gyllensvaans was one of the first companies that was commissioned to make BILLY for IKEA

(Gyllensvaans Möbler, AB, 2014).

With this Long-term relationship with Gyllensvaans we manage to receive a lower price, more

reliable service and improved support.

4.2.2 THE PRODUCT PORTFOLIO

PERMFORMANCE BASED PARTNERSHIP - Invest for growth. The Billy bookcase,

began in 1979, no one in their wildest dreams could have imagined what a success it

would be. Since then, the world’s most versatile bookcase has moved into the homes

of millions of people (IKEA, 2009).

We decide to go for PLAN A includes IKEA investing in the machinery that

Gyllensvaans own and use to produce the Billy bookcase. The intention of the

investment is to update the machinery in order to improve the production and save cost,

both for IKEA but also for Gyllensvaans. We want to be strategic with our products,

we seek the performance based on partnership to keep buying from our main supplier

for the production of the bookcase to be able to lower our procurement and create more

dividends for IKEA. In the Purchasing product portfolio the purchasing’s impact on

financial result of the performance based on partnership the risk is higher but there are

more dividends and better financial results to be achieved.

4.2.3 THE SUPPLIER PORTFOLIO

Gyllensvaans Möbler is a family-owned company situated in the small town of

Kättilstorp, just outside Falköping in southern Sweden. The company was established

in 1946 by Nils Gyllensvaan and now employs about 250 people. Gyllensvaans’ main

production area is bookcases, including IKEA’s world famous “BILLY”. The company

manufacturers 170,000 bookcases every week for distribution all over the world.

(Gyllensvaans Möbler, AB, 2014).

The purchasing from our supplier impact on the financial result, we decide to have a

strategic, exploit balance or diversity, which balance and gives an equal partnership

22

plus mutual commitment between Gyllensvaans Möbler and IKEA, this also means,

invest in new machinery for their supplier Gyllensvaans Möbler, AB to decrease kWh

consumption and increase production ratio.

5. TACTICAL

Specification

Selecting supplier

Contracting

5.1 SPECIFICATION

CRITERIA Gyllensvaans möbler AB

Approach to the environment Sesam’s excellence

Lower energy costs

Producction of a Billy bookcase 3-5 seconds New bookcase every three seconds

Supplier selection IKEA Industry Hultsfred AB. Hultsfred

A considerable number of employees > 150 About 250 people employees

Specialization in production of bookcase Gyllensvaans’ main production area is

bookcases

23

5.2 SELECTING SUPPLIER &

CONTRACTING

IKEA has a long-term relationship with Gyllensvaans Möbler, AB and the plans stated

in this report do not require IKEA to select a different supplier, since the current

supplier fulfill all the criterias of the specification IKEA demands.

Therefore, contracts will continue to be relevant between IKEA and its supplier.

However, arrangements have to be made in order for the plans to be implementet and

contracts concerning the implementations and agreements made are needed.

6. OPERATIONS

Expediting: the same quantity of units ordered, as figured in the situational assessment, will remain at 765.000 units / month.

Quality control with the supplier Gyllensvaans will continue as per usual.

24

6. ILLUSTRATIONS

25

R E F E R E N C E S REFERENCE LIST

Content Media Partner Nordic AB. 2014. Largest companies.

http://www.largestcompanies.se/foretag/Gyllensvaans-Mobler-AB-

8990/bokslut-och-nyckeltal

(Accessed 2014-11-18)

Gyllensvaans Möbler, AB. 2014.

http://www.gyllensvaan.se/

(Accessed 2014-11-18)

IKEA. 2009. Billy turns 30.

http://www.ikea.com/ms/en_CA/img/pdf/Billy_Anniv_en.pdf

(Accessed 2014 – 11 – 18)

IKEA. 2010. The IKEA concept.

http://www.ikea.com/ms/en_GB/this-is-ikea/the-ikea-concept/index.html

(Accessed 2014 – 11 – 18)

IKEA Industry AB. 2014.

http://www.swedwood.com/

(Accessed 2014-11-18)

Inter IKEA Holding SA. 2012. Business in brief.

http://inter.ikea.com/en/about-us/business-in-brief/

(Accessed 2014-11-18)

National Geographic Channel. 2009. Megafactories – IKEA.

http://vimeo.com/15555713

(Accessed 2014-11-18)

Plasticker. 2014. Real Time Price List.

http://plasticker.de/preise/pms_en.php?show=ok&make=ok&aog=A&kat=

Mahlgut

(Accessed 2014-11-18)

Related Documents

![Software Requirement Analysis for Digital Watch Systemdslab.konkuk.ac.kr/.../TEAM_A/T1/[2019SE_A][T3]SRA-ver3.pdf · 2019-11-11 · Ver. 2.0 [텍스트 입력] T3 Team 1 Software](https://static.cupdf.com/doc/110x72/5eaa5b4653fd8b2cbe13c308/software-requirement-analysis-for-digital-watch-2019seat3sra-ver3pdf-2019-11-11.jpg)

![Software Requirement Analysis for AAA Systemdslab.konkuk.ac.kr/.../TEAM_A/T1/[2019SE_A][T4]SRA-ver3.pdf · 2019-11-11 · Ver. 1.0 AAA System YKK Team 1 Software Requirement Analysis](https://static.cupdf.com/doc/110x72/5f0d8ebf7e708231d43af361/software-requirement-analysis-for-aaa-2019seat4sra-ver3pdf-2019-11-11-ver.jpg)