Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101) TEACHER’S DELIVERY GUIDE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Pearson LCCI Level 4 Certifi cate in Financial Accounting

(ASE20101)

TEACHER’S DELIVERY GUIDE

L4FATGD_cover.indd 1 26/02/2016 09:11

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101):Teacher’s Delivery Guide

A01_LCCI9007_01_CUS_PR.indd 1 21/04/2016 11:32

Pearson Education LimitedEdinburgh GateHarlow CM20 2JEUnited KingdomTel: +44 (0)1279 623623Web: www.pearson.com/uk

First published 2016

© Pearson Education Limited 2016

Compiled from:Selected material written by Sally Sturman (Introduction and Chapters 1, 2, 3, 4, 7) with Chapters 1, 3 and 7 revised by Mike SeagroveSeries consultant: Steve Jakubowski

All questions for Chapter 1 and 2, Questions 4.5 to 4.9, 5.10 and 7.6 were created by Eileen Roddy

Questions 4.1 to 4.4, 6.1 to 6.5, and 7.1 to 7.4 fromAccounting and Finance: An IntroductionSeventh editionEddie McLaney and Peter AtrillISBN: 978-1-292-01256-8© Pearson Education Limited 2014 (print and electronic)

Questions 5.3 to 5.9 fromFrank Wood’s Business Accounting 1Twelfth editionFrank Wood and Alan SangsterISBN: 978-0-273-78918-8© Pearson Education Limited 2002, 2007, 2008, 2012

Questions 6.6 to 6.7 and 7.5 fromFinancial and Management Accounting Sixth editionPauline WeetmanISBN: 978-0-273-78921-5© Pearson Education Limited 2013 (print and electronic)

Questions 6.8 to 6.17 fromFrank Wood’s Business Accounting 2Twelfth editionFrank Wood and Alan SangsterISBN: 978-0-273-76779-4© Pearson Education Limited 2002, 2007, 2008, 2012

Questions 3.1 to 3.10 by Steve Jakubowski

The print publication is protected by copyright. Prior to any prohibited reproduction, storage in a retrieval system, distribution or transmission in any form or by any means, electronic, mechanical, recording or otherwise, permission should be obtained from the publisher or, where applicable, a licence permitting restricted copying in the United Kingdom should be obtained from the Copyright Licensing Agency Ltd, Saffron House, 6-10 Kirby Street, London EC1N 8TS.

ISBN: 978-1-784-48900-7

Typeset in Charter ITC 9.5/12.5 pt by Fakenham Prepress Solutions, Fakenham, Norfolk NR21 8NN

Pearson Education Limited is not responsible for the content of any external internet sites. It is essential for tutors to preview each website before using it in class so as to ensure that the URL is still accurate, relevant and appropriate. We suggest that tutors bookmark useful websites and consider enabling students to access them through the school/college intranet.

A01_LCCI9007_01_CUS_PR.indd 2 21/04/2016 11:32

Contents

Introduction v

1 What’s new 1

2 Delivery guidance 3

3 Scheme of work 5

4 Preparing learners for external assessment 21

5 Exam command words 25

6 Practice exercises 27

7 Further reading and resource suggestions 67

8 IAS glossary 69

iii

A01_LCCI9007_01_CUS_PR.indd 3 21/04/2016 11:32

A01_LCCI9007_01_CUS_PR.indd 4 21/04/2016 11:32

v

Introduction

Welcome to the Teacher’s Delivery Guide for Pearson LCCI Level 4 Certifi cate in Financial Accounting (ASE20101). We are delighted that you are interested in teaching this qualifi cation, and have provided this free resource – written by teachers – to support your delivery of the specifi cation. It was created to support both new and existing LCCI teachers and is based on the content of the latest specifi cations.

LCCI qualifi cations (set up originally by the London Chamber of Commerce and Industry) have an established reputation dating back to 1887, when the fi rst exams were set in Bombay (now Mumbai). In 2011 this qualifi cation suite became par t of the Pearson portfolio, which also includes academic qualifi cations (e.g. GCSE and GCE Level) and vocational qualifi cations (e.g. BTEC). Now, these qualifi cations are off ered in over 90 countries and over 250,000 LCCI exams are taken annually by learners all over the globe.

Some of the key features and benefi ts of the new fi nance and quantitative qualifi ca-tions include:

● Comprehensive support – Each qualification in the new suite is supported by a free Teacher’s Delivery Guide; marketing materials to help you recruit learners; and past papers with mark schemes as well as full examiner reports following each exam.

● Professional body recognition – We have received a number of exemptions from Professional Bodies such as ACCA, CIMA and ICAEW. For more information, please visit the Progression area within the Pearson website (qualifications.pearson.com/lcci).

● Higher body recognition – UCAS points are due to be confirmed on the new LCCI Level 3 titles in 2016, so look on the website for details.

● Employer recognition – LCCI qualifications have a long history of being sought after by local employers, particularly in some countries where the brand is regarded as the market-leading finance qualification.

● 100% external assessment – All the exams are set and marked by Pearson, which gives the qualification credibility amongst external stakeholders (like employers, Higher Education) and means you can be confident of the standards of the qualifi-cation. These qualifications will also follow the same awarding process as general (academic) qualifications, and grade boundaries will be set for each exam and published after the exam has been set, to ensure that standards remain consistent over time.

● Mapped to International Accounting Standards (IAS) – This will ensure learners understand the accounting practices that countries are increasingly adopting.

● Clear specification and exam format – The specification is laid out in a more concise format, and the mark scheme clearly outlines how mark allocation works and is consistent between the levels and qualifications.

A02_LCCI9007_01_CUS_INTR.indd 5 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

vi

● Assessment objectives – These detail all the different ways that content may be assessed in the exam. For example, listing ‘depreciation’ under assessment objective 1 (memo-rise) may require learners to recall or state methods of depreciation, whilst for assess-ment objective 2 (perform procedures) learners may be required to demonstrate using methods of depreciation, and so on.

It is essential that you familiarise yourself with the full requirements of the specification through close reading of the document. This guide is purely for support purposes and is not designed to be a substitute for the specification itself.

Below is an overview of the different features to be included in the delivery guide including:

● What’s new – provides a useful summary of key changes between the old and the new specification, as well as highlighting the key aspects of the new course.

● Delivery guidance – provides suggestions on how to plan and teach the new LCCI suite of qualifications.

● Scheme of work – contains a table illustrating how to deliver the qualifications within the Guided Learning Hours (GLH) with ideas for possible activities and resources to use with learners.

● Preparing learners for external assessment – guidance on how to help prepare learners for the external assessment in the new LCCI qualifications.

● Command words – a list of the key command words and their definitions used in the sample assessment material.

● Practice exercises – questions for you to use with learners to develop their skills, which are additional to the questions provided in the student textbook.

● Further reading and resource suggestions – suggestions of further printed and online resources that you may find beneficial when delivering the new LCCI qualification.

● IAS glossary – detailing the key IAS terminology used in the new suite.

We hope you find this guide of use when teaching.We encourage you to check the Pearson website (qualifications.pearson.com/lcci)

and search for this qualification to download a range of free learner resources and further support for your delivery of this qualification.

A02_LCCI9007_01_CUS_INTR.indd 6 21/04/2016 11:32

1

Chapter 1What’s new

Background and context

The Pearson LCCI Level 4 Certifi cate in Financial Accounting (ASE20101) is a single unit qualifi cation which is part of the redeveloped suite of LCCI Finance and Accounting quali-fi cations. It builds upon candidates ability to prepare and interpret fi nancial accounting statements in accordance with IAS accounting standards and the accounting framework. It develops candidates’ understanding of the conceptual aspects of fi nancial accounting. This qualifi cation is suitable for people who intend to work in a senior accounting role or extend their studies.

It is ideal for students looking to progress on the path to becoming a fully qualifi ed accountant and gives access to professional accounting qualifi cations. It is also recognised as an ACCA accredited programme.

Emphasis has been placed on preparation of fi nancial statements for di� erent organisa-tions at the level required in a professional environment.

The new syllabus has been divided into fi ve sections:

● The regulatory framework and governance responsibilities

● Accounting systems

● The principles of financial statements for single entities, partnerships and groups

● Financial statements

● The analysis of business performance using financial statements.

These have been subdivided into subject content and ‘what the students need to learn’.Specifi c detail is provided on each topic to facilitate smooth delivery. Teachers should

concentrate on, and deliver, the knowledge, skills and understanding outlined in the ‘what students need to learn’ section of the specifi cation to enable full understanding of the unit.

M01_LCCI9007_01_CUS_C01.indd 1 21/04/2016 11:32

M01_LCCI9007_01_CUS_C01.indd 2 21/04/2016 11:32

3

Chapter 2Delivery guidance

This new suite of LCCI fi nance and accounting qualifi cations aims to prepare learners for the accounting profession. Qualifi cations range from Level 1 to Level 4 covering aspects of manual and computerised bookkeeping, accounts and statistics. Levels 1–3 are aimed at learners aged 16+. Level 4 is aimed at learners who are 18+ and already in th e workplace.

As these are vocational qualifi cations, it is imperative that you use a variety of delivery methods to engage learners and ensure they develop the appropriate knowledge, under-standing and skills, which will help them to be successful in their future careers.

Planning:

● Prior to recruiting learners onto the course, it is important to establish what qualifica-tion level they are already working at and that they have the sufficient motivation and interest in accounting to enable them to be successful. Their previous academic history and prior qualifications will help you to determine this.

● The minimum age of learners in the specification should be used as a guide for recruit-ment, rather than as a compulsory requirement.

● It is essential that you read the whole specification to familiarise yourself with its requirements.

● If you are already experienced in delivering LCCI finance and quantitative qualifica-tions, it is worth familiarising yourself with the differences between the old and new specification, which is also summarised in the ‘What’s new’ section of the delivery guide.

● It is important to plan sufficient time to deliver the whole course. The Guided Learning Hours (GLH) for each qualification provides an indication of how long is needed to deliver the course in its entirety. The example Scheme of Work provides you with a suggestion of how to plan the time over the course.

Delivery:

● Visit the website qualifications.pearson.com/lcci and search for this qualification to find supporting resources to use with your learners.

● Use International Accounting Standards (IAS) terminology with learners from the outset of the course. A glossary is included in the qualification specification, in this guide and on the qualification website that you can give to learners.

M02_LCCI9007_01_CUS_C02.indd 3 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

4

● Recap the previous session at the start of each lesson. This will provide an opportunity to monitor learner progress and encourage questions.

● Develop each new topic from simple to complex incorporating realistic examples.

● In order to engage learners you should incorporate a variety of delivery methods which allow for different learning styles. For example, pair and group work. It is recommended that you have a maximum group size of three as learners do not get enough chance to speak in large groups.

● Change the pace of the lesson by breaking things up a bit, i.e. different activities, timed tasks and different materials.

● Let the students make mistakes. They need to. We all learn best through making mistakes.

● It’s a good idea to let learners check their answers with each other before feeding back to you.

● Use practice exercises to develop learners’ skills. These could be class based or set as a homework assignment.

● You should encourage learners to complete additional tasks – for example, exercises from suitable textbooks, real-life scenarios from business and financial pages in newspapers or from websites to help contextualise the content for learners.

● At the end of each topic you can incorporate, into your teaching, a mini test to help consolidate learning.

It is important that you ensure learners’ understanding over time and encourage learners to develop good study skills from the beginning of the course. It will make it easier when it comes to revision.

M02_LCCI9007_01_CUS_C02.indd 4 21/04/2016 11:32

5

Chapter 3Scheme of work

Level 4 Financial Accounting

This scheme of work is intended to be an example and not prescriptive. It is provided to help you make the most of your planning time. You can adjust the session order to suit your circumstances and customise it by adding your own activities/lesson ideas to the ‘Activities’ column. There are opportunities to add subject matter individual to your students, e.g. consolidation sessions. Note that the order of unit content given here may not be the same as in the qualifi cation specifi cation.

Learners’ skills will be developed to enable them to perform accounting procedures in the workplace. The scheme of work allows lots of practice tasks which should be as near as possible to the tasks required at this level in the workplace.

The scheme of work has been written to introduce topics slowly before consolidating all areas ready for examination.

Guided learning hours: 130 Number of lessons: 52 Duration of lessons: 2.5 hours

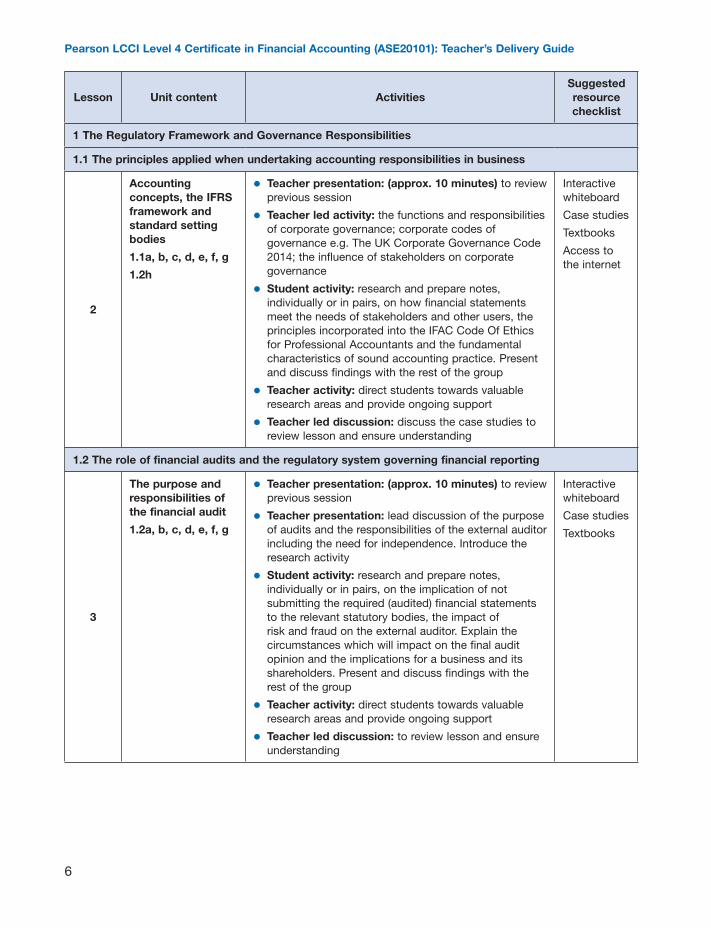

Lesson Unit content ActivitiesSuggested resource checklist

1

Unit introduction ● Teacher presentation (approx. 10 minutes) to introduce the unit: outline the nature of the key topics and terms and assessment verbs. Outline the method of assessment in this unit

● Ice breaker: this could consist of a getting-to-know-you or team-working activity depending on the structure and size of the group

● Group discussion: to assess any prior experience/learning/knowledge

● Teacher presentation: an introduction to the external regulatory framework, international standard-setting bodies and their influence on the accounting function; other regulatory bodies including the role of the professional associations and the stock exchange; the influence of company law on accounting practices. Implications for the professional accountant

● Student activity: small group discussion, case studies on code of ethics and feedback to other groups

● Teacher led discussion: to review lesson and ensure understanding

Specification

Interactive whiteboard

Ice breaker activities

Access to the internet

M03_LCCI9007_01_CUS_C03.indd 5 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

6

Lesson Unit content ActivitiesSuggested resource checklist

1 The Regulatory Framework and Governance Responsibilities

1.1 The principles applied when undertaking accounting responsibilities in business

2

Accounting concepts, the IFRS framework and standard setting bodies

1.1a, b, c, d, e, f, g

1.2h

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher led activity: the functions and responsibilities of corporate governance; corporate codes of governance e.g. The UK Corporate Governance Code 2014; the influence of stakeholders on corporate governance

● Student activity: research and prepare notes, individually or in pairs, on how financial statements meet the needs of stakeholders and other users, the principles incorporated into the IFAC Code Of Ethics for Professional Accountants and the fundamental characteristics of sound accounting practice. Present and discuss findings with the rest of the group

● Teacher activity: direct students towards valuable research areas and provide ongoing support

● Teacher led discussion: discuss the case studies to review lesson and ensure understanding

Interactive whiteboard

Case studies

Textbooks

Access to the internet

1.2 The role of financial audits and the regulatory system governing financial reporting

3

The purpose and responsibilities of the financial audit

1.2a, b, c, d, e, f, g

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: lead discussion of the purpose of audits and the responsibilities of the external auditor including the need for independence. Introduce the research activity

● Student activity: research and prepare notes, individually or in pairs, on the implication of not submitting the required (audited) financial statements to the relevant statutory bodies, the impact of risk and fraud on the external auditor. Explain the circumstances which will impact on the final audit opinion and the implications for a business and its shareholders. Present and discuss findings with the rest of the group

● Teacher activity: direct students towards valuable research areas and provide ongoing support

● Teacher led discussion: to review lesson and ensure understanding

Interactive whiteboard

Case studies

Textbooks

M03_LCCI9007_01_CUS_C03.indd 6 21/04/2016 11:32

Chapter 3 Scheme of work

7

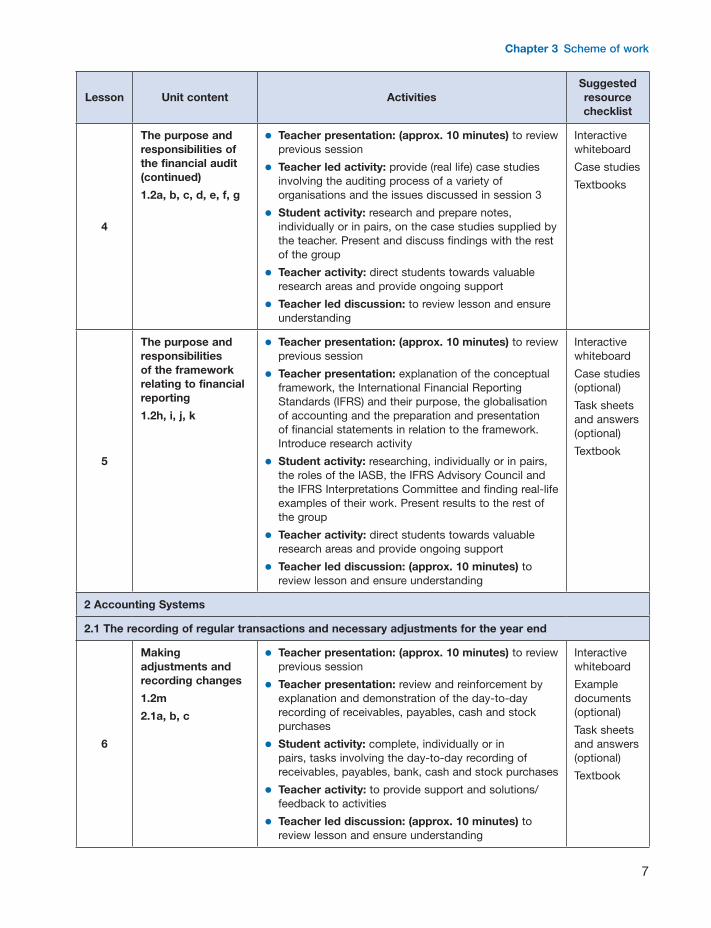

Lesson Unit content ActivitiesSuggested resource checklist

4

The purpose and responsibilities of the financial audit (continued)

1.2a, b, c, d, e, f, g

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher led activity: provide (real life) case studies involving the auditing process of a variety of organisations and the issues discussed in session 3

● Student activity: research and prepare notes, individually or in pairs, on the case studies supplied by the teacher. Present and discuss findings with the rest of the group

● Teacher activity: direct students towards valuable research areas and provide ongoing support

● Teacher led discussion: to review lesson and ensure understanding

Interactive whiteboard

Case studies

Textbooks

5

The purpose and responsibilities of the framework relating to financial reporting

1.2h, i, j, k

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explanation of the conceptual framework, the International Financial Reporting Standards (IFRS) and their purpose, the globalisation of accounting and the preparation and presentation of financial statements in relation to the framework. Introduce research activity

● Student activity: researching, individually or in pairs, the roles of the IASB, the IFRS Advisory Council and the IFRS Interpretations Committee and finding real-life examples of their work. Present results to the rest of the group

● Teacher activity: direct students towards valuable research areas and provide ongoing support

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Case studies (optional)

Task sheets and answers (optional)

Textbook

2 Accounting Systems

2.1 The recording of regular transactions and necessary adjustments for the year end

6

Making adjustments and recording changes

1.2m

2.1a, b, c

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: review and reinforcement by explanation and demonstration of the day-to-day recording of receivables, payables, cash and stock purchases

● Student activity: complete, individually or in pairs, tasks involving the day-to-day recording of receivables, payables, bank, cash and stock purchases

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Example documents (optional)

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 7 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

8

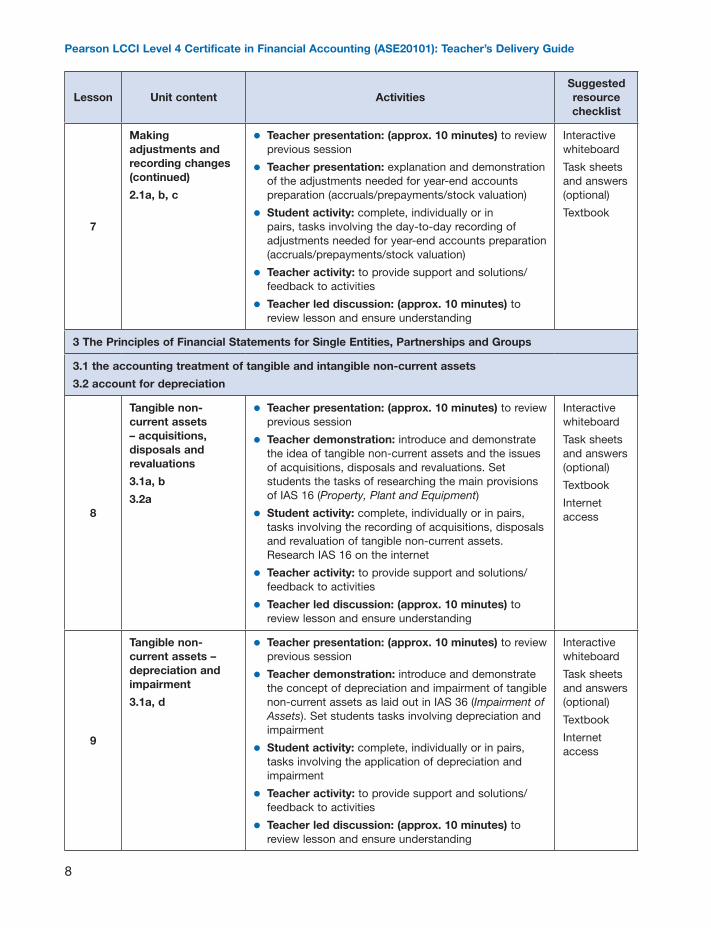

Lesson Unit content ActivitiesSuggested resource checklist

7

Making adjustments and recording changes (continued)

2.1a, b, c

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explanation and demonstration of the adjustments needed for year-end accounts preparation (accruals/prepayments/stock valuation)

● Student activity: complete, individually or in pairs, tasks involving the day-to-day recording of adjustments needed for year-end accounts preparation (accruals/prepayments/stock valuation)

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

3 The Principles of Financial Statements for Single Entities, Partnerships and Groups

3.1 the accounting treatment of tangible and intangible non-current assets

3.2 account for depreciation

8

Tangible non-current assets – acquisitions, disposals and revaluations

3.1a, b

3.2a

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: introduce and demonstrate the idea of tangible non-current assets and the issues of acquisitions, disposals and revaluations. Set students the tasks of researching the main provisions of IAS 16 (Property, Plant and Equipment)

● Student activity: complete, individually or in pairs, tasks involving the recording of acquisitions, disposals and revaluation of tangible non-current assets. Research IAS 16 on the internet

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

Internet access

9

Tangible non-current assets – depreciation and impairment

3.1a, d

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: introduce and demonstrate the concept of depreciation and impairment of tangible non-current assets as laid out in IAS 36 (Impairment of Assets). Set students tasks involving depreciation and impairment

● Student activity: complete, individually or in pairs, tasks involving the application of depreciation and impairment

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

Internet access

M03_LCCI9007_01_CUS_C03.indd 8 21/04/2016 11:32

Chapter 3 Scheme of work

9

Lesson Unit content ActivitiesSuggested resource checklist

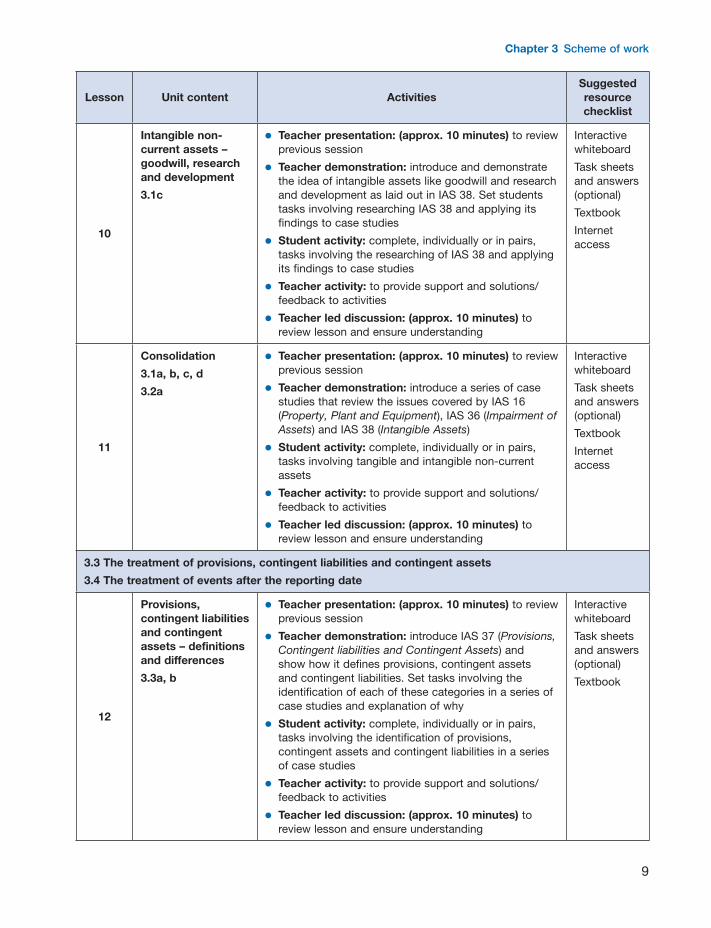

10

Intangible non-current assets – goodwill, research and development

3.1c

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: introduce and demonstrate the idea of intangible assets like goodwill and research and development as laid out in IAS 38. Set students tasks involving researching IAS 38 and applying its findings to case studies

● Student activity: complete, individually or in pairs, tasks involving the researching of IAS 38 and applying its findings to case studies

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

Internet access

11

Consolidation

3.1a, b, c, d

3.2a

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: introduce a series of case studies that review the issues covered by IAS 16 (Property, Plant and Equipment), IAS 36 (Impairment of Assets) and IAS 38 (Intangible Assets)

● Student activity: complete, individually or in pairs, tasks involving tangible and intangible non-current assets

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

Internet access

3.3 The treatment of provisions, contingent liabilities and contingent assets

3.4 The treatment of events after the reporting date

12

Provisions, contingent liabilities and contingent assets – definitions and differences

3.3a, b

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: introduce IAS 37 (Provisions, Contingent liabilities and Contingent Assets) and show how it defines provisions, contingent assets and contingent liabilities. Set tasks involving the identification of each of these categories in a series of case studies and explanation of why

● Student activity: complete, individually or in pairs, tasks involving the identification of provisions, contingent assets and contingent liabilities in a series of case studies

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 9 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

10

Lesson Unit content ActivitiesSuggested resource checklist

13

Provision, contingent liabilities and contingent assets – the accounting treatment

3.3a, b

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: explain the implications of IAS 37 on the accounting treatment of provisions, contingent assets and contingent liabilities. Set tasks involving the identification of each of these categories in a series of case studies and explanation of why

● Student activity: complete, individually or in pairs, tasks involving the treatment of provisions, contingent assets and contingent liabilities and explanation of why

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

14

Adjusting and non-adjusting events

3.4a, b

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: introduce and explain the concept of adjusting events and non-adjusting events and the disclosure requirements under IAS 10 (Events after the Reporting Period)

● Student activity: complete, individually or in pairs, tasks involving classification of items as adjusting and non-adjusting events and deciding on the appropriate treatment to give them

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Case studies (optional)

Task sheets and answers (optional)

Textbook

3.5 Accounting policies

3.6 Revenue recognition

15

Changes in accounting policies and accounting estimates

3.5a, b, c

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher activity: Explain the purpose, importance and implications of accounting policies. Explain the main aspects covered by ISA 8 (Accounting Policies, Changes in Accounting Estimates and Errors) in respect of accounting policies and estimates. Explanation and demonstration of how IAS 8 requires organisations to handle changes in accounting policies and estimates. Introduce case studies

● Student activity: research IAS 8, individually or in pairs, and present findings to the rest of the group. Complete case studies involving application of the requirements of IAS 8

● Teacher activity: to provide support and collate solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Case studies (optional)

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 10 21/04/2016 11:32

Chapter 3 Scheme of work

11

Lesson Unit content ActivitiesSuggested resource checklist

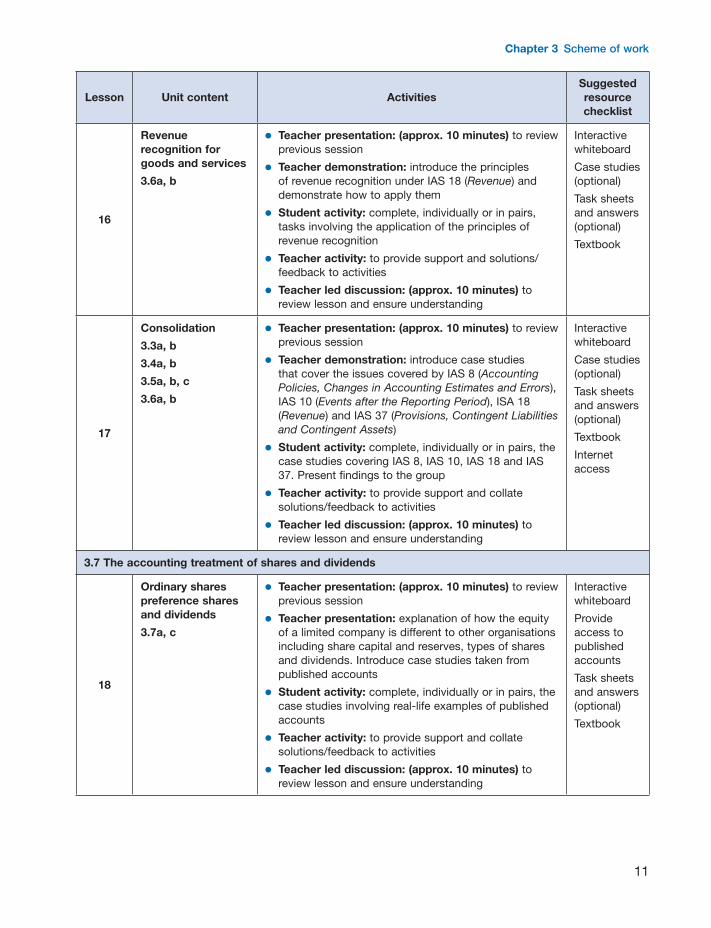

16

Revenue recognition for goods and services

3.6a, b

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: introduce the principles of revenue recognition under IAS 18 (Revenue) and demonstrate how to apply them

● Student activity: complete, individually or in pairs, tasks involving the application of the principles of revenue recognition

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Case studies (optional)

Task sheets and answers (optional)

Textbook

17

Consolidation

3.3a, b

3.4a, b

3.5a, b, c

3.6a, b

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: introduce case studies that cover the issues covered by IAS 8 (Accounting Policies, Changes in Accounting Estimates and Errors), IAS 10 (Events after the Reporting Period), ISA 18 (Revenue) and IAS 37 (Provisions, Contingent Liabilities and Contingent Assets)

● Student activity: complete, individually or in pairs, the case studies covering IAS 8, IAS 10, IAS 18 and IAS 37. Present findings to the group

● Teacher activity: to provide support and collate solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Case studies (optional)

Task sheets and answers (optional)

Textbook

Internet access

3.7 The accounting treatment of shares and dividends

18

Ordinary shares preference shares and dividends

3.7a, c

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explanation of how the equity of a limited company is different to other organisations including share capital and reserves, types of shares and dividends. Introduce case studies taken from published accounts

● Student activity: complete, individually or in pairs, the case studies involving real-life examples of published accounts

● Teacher activity: to provide support and collate solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Provide access to published accounts

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 11 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

12

Lesson Unit content ActivitiesSuggested resource checklist

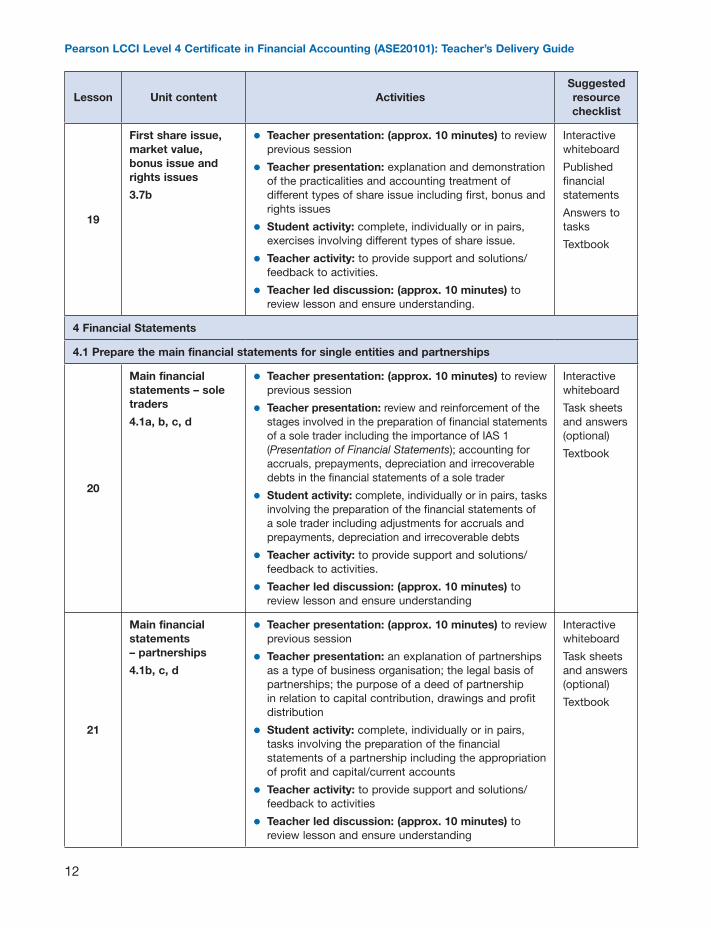

19

First share issue, market value, bonus issue and rights issues

3.7b

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explanation and demonstration of the practicalities and accounting treatment of different types of share issue including first, bonus and rights issues

● Student activity: complete, individually or in pairs, exercises involving different types of share issue.

● Teacher activity: to provide support and solutions/feedback to activities.

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding.

Interactive whiteboard

Published financial statements

Answers to tasks

Textbook

4 Financial Statements

4.1 Prepare the main financial statements for single entities and partnerships

20

Main financial statements – sole traders

4.1a, b, c, d

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: review and reinforcement of the stages involved in the preparation of financial statements of a sole trader including the importance of IAS 1 (Presentation of Financial Statements); accounting for accruals, prepayments, depreciation and irrecoverable debts in the financial statements of a sole trader

● Student activity: complete, individually or in pairs, tasks involving the preparation of the financial statements of a sole trader including adjustments for accruals and prepayments, depreciation and irrecoverable debts

● Teacher activity: to provide support and solutions/feedback to activities.

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

21

Main financial statements – partnerships

4.1b, c, d

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: an explanation of partnerships as a type of business organisation; the legal basis of partnerships; the purpose of a deed of partnership in relation to capital contribution, drawings and profit distribution

● Student activity: complete, individually or in pairs, tasks involving the preparation of the financial statements of a partnership including the appropriation of profit and capital/current accounts

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 12 21/04/2016 11:32

Chapter 3 Scheme of work

13

Lesson Unit content ActivitiesSuggested resource checklist

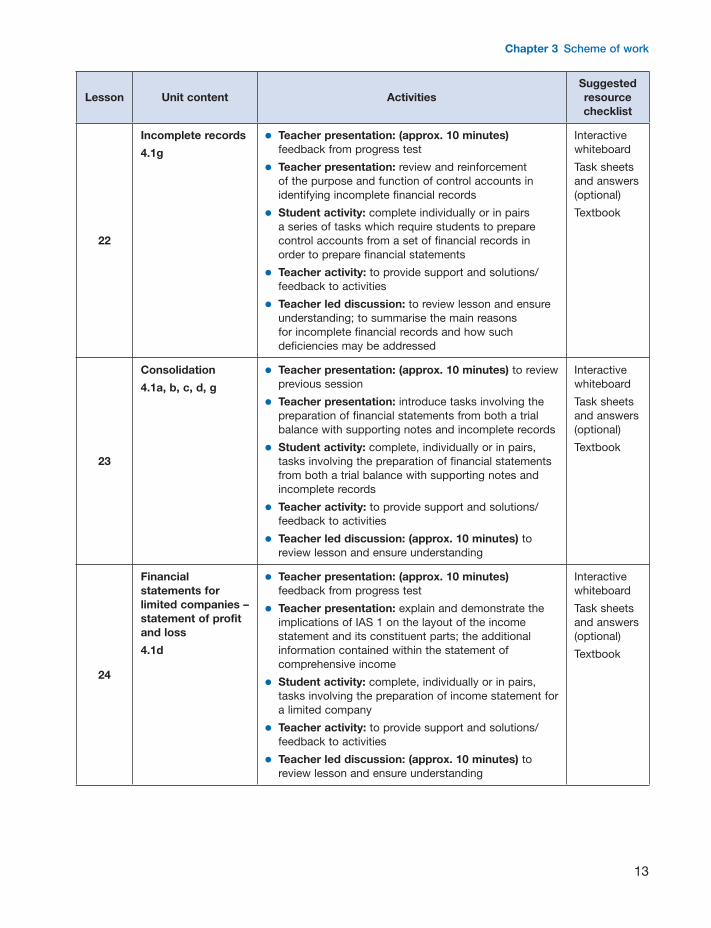

22

Incomplete records

4.1g

● Teacher presentation: (approx. 10 minutes) feedback from progress test

● Teacher presentation: review and reinforcement of the purpose and function of control accounts in identifying incomplete financial records

● Student activity: complete individually or in pairs a series of tasks which require students to prepare control accounts from a set of financial records in order to prepare financial statements

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: to review lesson and ensure understanding; to summarise the main reasons for incomplete financial records and how such deficiencies may be addressed

Interactive whiteboard

Task sheets and answers (optional)

Textbook

23

Consolidation

4.1a, b, c, d, g

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: introduce tasks involving the preparation of financial statements from both a trial balance with supporting notes and incomplete records

● Student activity: complete, individually or in pairs, tasks involving the preparation of financial statements from both a trial balance with supporting notes and incomplete records

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

24

Financial statements for limited companies – statement of profit and loss

4.1d

● Teacher presentation: (approx. 10 minutes) feedback from progress test

● Teacher presentation: explain and demonstrate the implications of IAS 1 on the layout of the income statement and its constituent parts; the additional information contained within the statement of comprehensive income

● Student activity: complete, individually or in pairs, tasks involving the preparation of income statement for a limited company

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 13 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

14

Lesson Unit content ActivitiesSuggested resource checklist

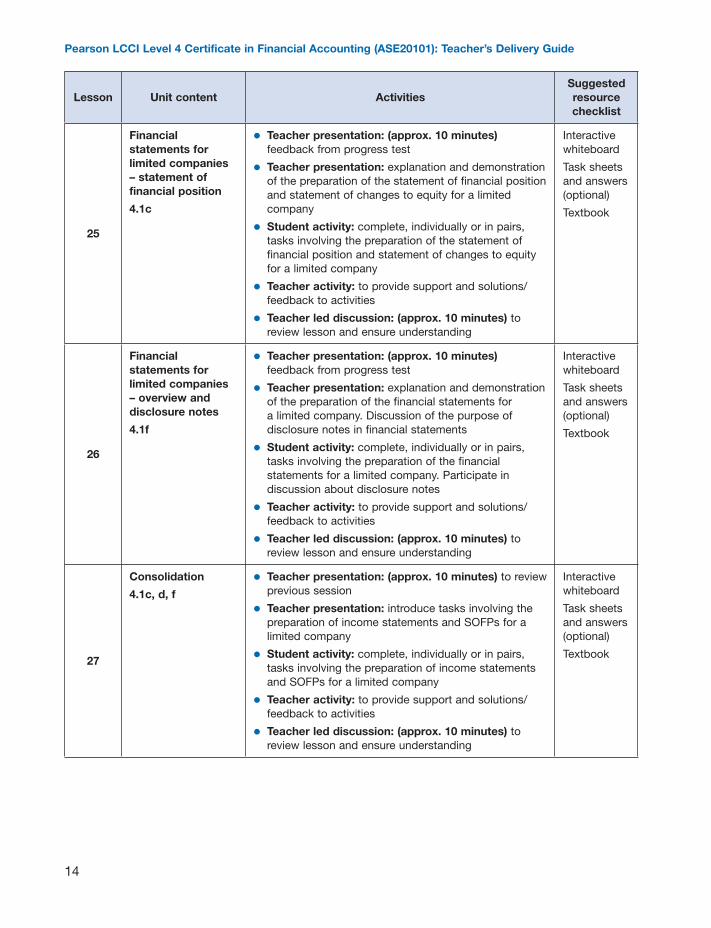

25

Financial statements for limited companies – statement of financial position

4.1c

● Teacher presentation: (approx. 10 minutes) feedback from progress test

● Teacher presentation: explanation and demonstration of the preparation of the statement of financial position and statement of changes to equity for a limited company

● Student activity: complete, individually or in pairs, tasks involving the preparation of the statement of financial position and statement of changes to equity for a limited company

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

26

Financial statements for limited companies – overview and disclosure notes

4.1f

● Teacher presentation: (approx. 10 minutes) feedback from progress test

● Teacher presentation: explanation and demonstration of the preparation of the financial statements for a limited company. Discussion of the purpose of disclosure notes in financial statements

● Student activity: complete, individually or in pairs, tasks involving the preparation of the financial statements for a limited company. Participate in discussion about disclosure notes

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

27

Consolidation

4.1c, d, f

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: introduce tasks involving the preparation of income statements and SOFPs for a limited company

● Student activity: complete, individually or in pairs, tasks involving the preparation of income statements and SOFPs for a limited company

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 14 21/04/2016 11:32

Chapter 3 Scheme of work

15

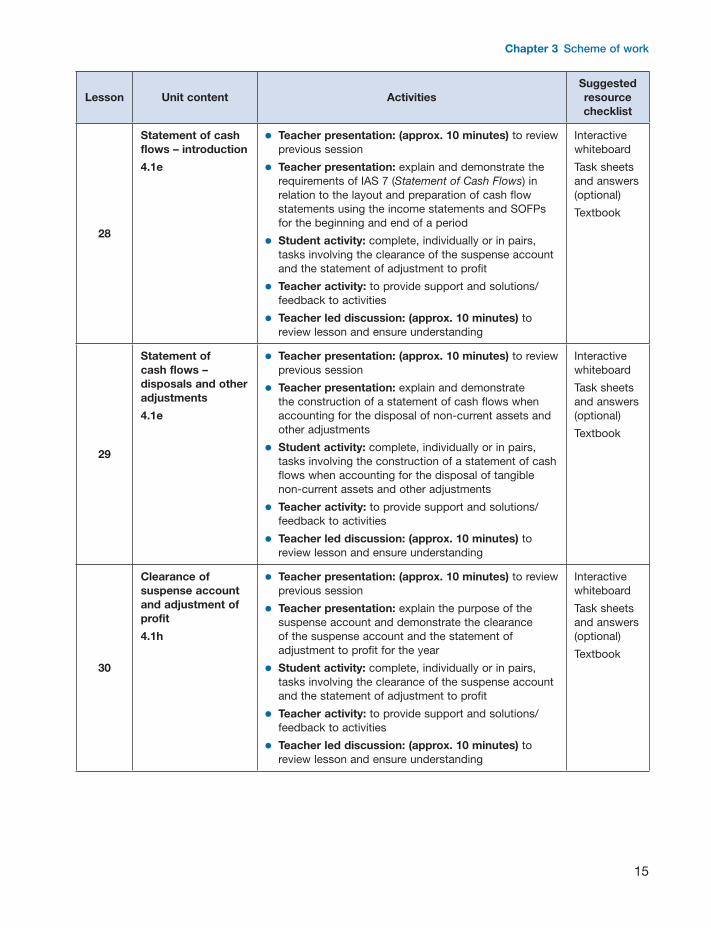

Lesson Unit content ActivitiesSuggested resource checklist

28

Statement of cash flows – introduction

4.1e

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explain and demonstrate the requirements of IAS 7 (Statement of Cash Flows) in relation to the layout and preparation of cash flow statements using the income statements and SOFPs for the beginning and end of a period

● Student activity: complete, individually or in pairs, tasks involving the clearance of the suspense account and the statement of adjustment to profit

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

29

Statement of cash flows – disposals and other adjustments

4.1e

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explain and demonstrate the construction of a statement of cash flows when accounting for the disposal of non-current assets and other adjustments

● Student activity: complete, individually or in pairs, tasks involving the construction of a statement of cash flows when accounting for the disposal of tangible non-current assets and other adjustments

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

30

Clearance of suspense account and adjustment of profit

4.1h

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explain the purpose of the suspense account and demonstrate the clearance of the suspense account and the statement of adjustment to profit for the year

● Student activity: complete, individually or in pairs, tasks involving the clearance of the suspense account and the statement of adjustment to profit

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 15 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

16

Lesson Unit content ActivitiesSuggested resource checklist

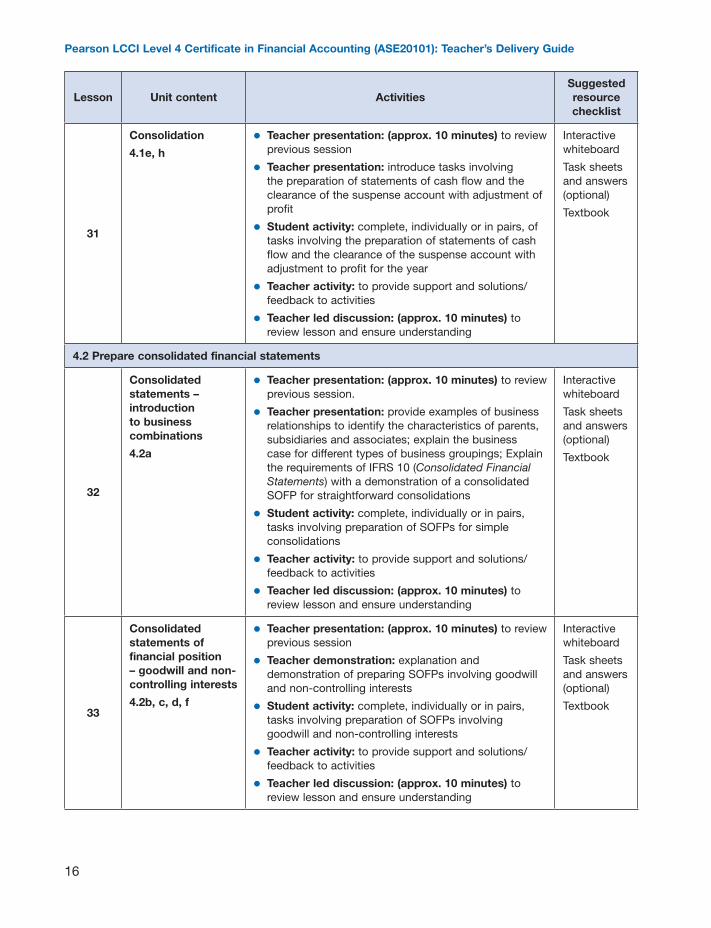

31

Consolidation

4.1e, h

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: introduce tasks involving the preparation of statements of cash flow and the clearance of the suspense account with adjustment of profit

● Student activity: complete, individually or in pairs, of tasks involving the preparation of statements of cash flow and the clearance of the suspense account with adjustment to profit for the year

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

4.2 Prepare consolidated financial statements

32

Consolidated statements – introduction to business combinations

4.2a

● Teacher presentation: (approx. 10 minutes) to review previous session.

● Teacher presentation: provide examples of business relationships to identify the characteristics of parents, subsidiaries and associates; explain the business case for different types of business groupings; Explain the requirements of IFRS 10 (Consolidated Financial Statements) with a demonstration of a consolidated SOFP for straightforward consolidations

● Student activity: complete, individually or in pairs, tasks involving preparation of SOFPs for simple consolidations

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

33

Consolidated statements of financial position – goodwill and non-controlling interests

4.2b, c, d, f

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: explanation and demonstration of preparing SOFPs involving goodwill and non-controlling interests

● Student activity: complete, individually or in pairs, tasks involving preparation of SOFPs involving goodwill and non-controlling interests

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 16 21/04/2016 11:32

Chapter 3 Scheme of work

17

Lesson Unit content ActivitiesSuggested resource checklist

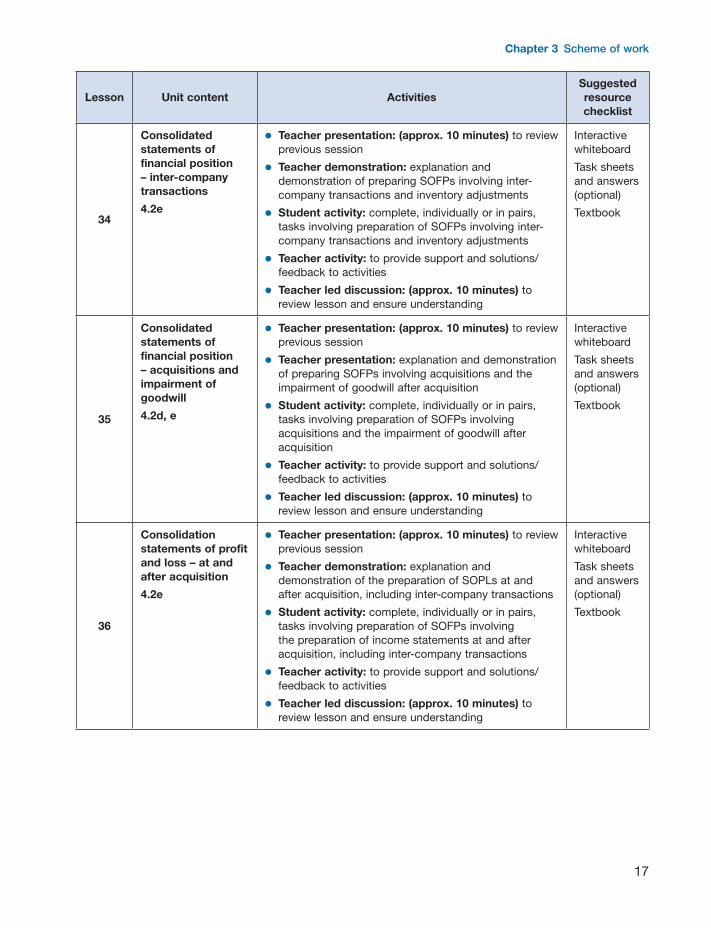

34

Consolidated statements of financial position – inter-company transactions

4.2e

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: explanation and demonstration of preparing SOFPs involving inter-company transactions and inventory adjustments

● Student activity: complete, individually or in pairs, tasks involving preparation of SOFPs involving inter-company transactions and inventory adjustments

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

35

Consolidated statements of financial position – acquisitions and impairment of goodwill

4.2d, e

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explanation and demonstration of preparing SOFPs involving acquisitions and the impairment of goodwill after acquisition

● Student activity: complete, individually or in pairs, tasks involving preparation of SOFPs involving acquisitions and the impairment of goodwill after acquisition

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

36

Consolidation statements of profit and loss – at and after acquisition

4.2e

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher demonstration: explanation and demonstration of the preparation of SOPLs at and after acquisition, including inter-company transactions

● Student activity: complete, individually or in pairs, tasks involving preparation of SOFPs involving the preparation of income statements at and after acquisition, including inter-company transactions

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 17 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

18

Lesson Unit content ActivitiesSuggested resource checklist

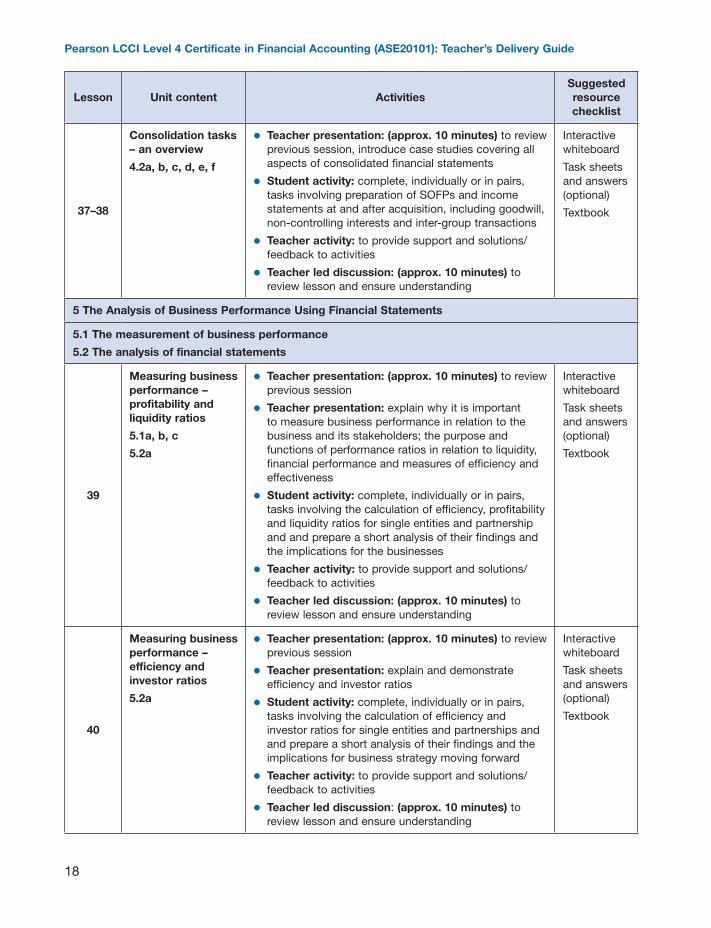

37–38

Consolidation tasks – an overview

4.2a, b, c, d, e, f

● Teacher presentation: (approx. 10 minutes) to review previous session, introduce case studies covering all aspects of consolidated financial statements

● Student activity: complete, individually or in pairs, tasks involving preparation of SOFPs and income statements at and after acquisition, including goodwill, non-controlling interests and inter-group transactions

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

5 The Analysis of Business Performance Using Financial Statements

5.1 The measurement of business performance

5.2 The analysis of financial statements

39

Measuring business performance – profitability and liquidity ratios

5.1a, b, c

5.2a

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explain why it is important to measure business performance in relation to the business and its stakeholders; the purpose and functions of performance ratios in relation to liquidity, financial performance and measures of efficiency and effectiveness

● Student activity: complete, individually or in pairs, tasks involving the calculation of efficiency, profitability and liquidity ratios for single entities and partnership and and prepare a short analysis of their findings and the implications for the businesses

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

40

Measuring business performance – efficiency and investor ratios

5.2a

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: explain and demonstrate efficiency and investor ratios

● Student activity: complete, individually or in pairs, tasks involving the calculation of efficiency and investor ratios for single entities and partnerships and and prepare a short analysis of their findings and the implications for business strategy moving forward

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 18 21/04/2016 11:32

Chapter 3 Scheme of work

19

Lesson Unit content ActivitiesSuggested resource checklist

41

Measuring business performance – interpretation and limitations

5.2a, b, c

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: Explain and demonstrate how to interpret accounting ratios as well as the limitations and drawbacks of using accounting ratios

● Student activity: complete, individually or in pairs, comparative case studies involving the interpretation of the accounting ratios and identifying the drawbacks of those ratios

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

42–43

Consolidation tasks

5.1a, b, c

5.2a, b, c

● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher presentation: to introduce case studies involving the calculation and interpretation of all of the performance ratios

● Student activity: complete, individually or in pairs, case studies involving the calculation of all the accounting ratios and present a short business case in support of a strategy for addressing deficiencies in business performance

● Teacher activity: ensure student tasks are correct and provide ongoing support

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

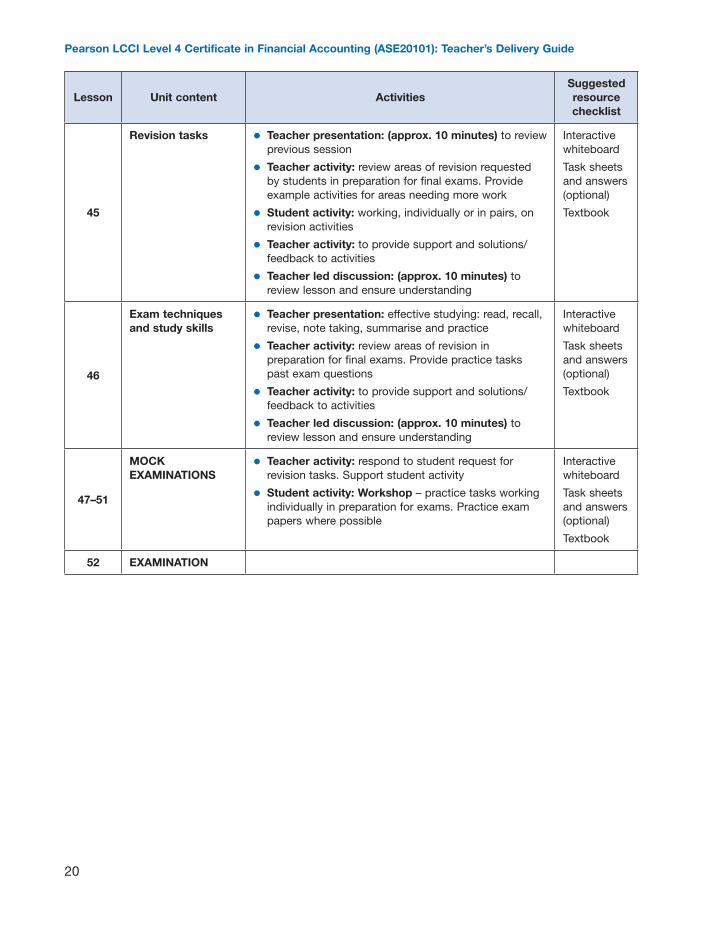

Review, revision and exam preparation

44

Revision tasks ● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher activity: review areas of revision requested by students in preparation for final exams. Provide example activities for areas needing more work

● Student activity: working, individually or in pairs, on revision activities

● Teacher activity: ensure student tasks are correct and provide ongoing support

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

M03_LCCI9007_01_CUS_C03.indd 19 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

20

Lesson Unit content ActivitiesSuggested resource checklist

45

Revision tasks ● Teacher presentation: (approx. 10 minutes) to review previous session

● Teacher activity: review areas of revision requested by students in preparation for final exams. Provide example activities for areas needing more work

● Student activity: working, individually or in pairs, on revision activities

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

46

Exam techniques and study skills

● Teacher presentation: effective studying: read, recall, revise, note taking, summarise and practice

● Teacher activity: review areas of revision in preparation for final exams. Provide practice tasks past exam questions

● Teacher activity: to provide support and solutions/feedback to activities

● Teacher led discussion: (approx. 10 minutes) to review lesson and ensure understanding

Interactive whiteboard

Task sheets and answers (optional)

Textbook

47–51

MOCK EXAMINATIONS

● Teacher activity: respond to student request for revision tasks. Support student activity

● Student activity: Workshop – practice tasks working individually in preparation for exams. Practice exam papers where possible

Interactive whiteboard

Task sheets and answers (optional)

Textbook

52 EXAMINATION

M03_LCCI9007_01_CUS_C03.indd 20 21/04/2016 11:32

21

Chapter 4Preparing learners for external assessment

Learners will expect preparation for examinations and assessment and this should be included in the delivery of the course. However your main focus must be on the eff ective learning of the full breadth and depth of the curriculum indicated by the specifi cation and example scheme of work provided for each qualifi cation.

It is important that you encourage learners to develop their study skills from the beginning of the course as this will assist in their revision later in the course.

At the beginning of the course you will lead in the incorporation of assessment/revision based activities. As the course progresses learners should be able to take a greater responsi-bility for their own revision. This should be encouraged.

Each qualifi cation specifi cation has details about when assessment is available. To gain access to the assessment, learners have to be entered by the entry deadline. Please refer to the exam timetable and Operations Guide for Centres on the website. It is important to enter learners for the examination when they are ready, and not just at the fi rst available assessment window.

The specifi cation also details the expected characteristics of those working at either pass or distinction grade (merit falls between the two, although it is not explicitly defi ned). This is worth examining, as it will help you to identify which target grade your learners are likely to be aiming for. Crucially, the assessment objectives in the specifi cation illustrate all the diff erent ways that content may be tested in the exam. It is important that you familiarise yourself with them, so you can help learners prepare.

The following guidance is provided to help you prepare your learners for external assessment. It is subdivided to distinguish between teacher-led, learner-led activities and examination techniques.

Examples of teacher-led activities:

● Explain the principles of assessment at induction so that learners have an understanding of the assessment process.

● Explain the rubric of the exam paper to your learners.

● Use practice exercises to develop learners’ skills. This could be class based or set as a homework assignment.

● You should encourage learners to complete additional tasks – for example, exercises from suitable textbooks, real-life scenarios from business and financial pages in newspapers or from websites to help contextualise the content for learners.

M04_LCCI9007_01_CUS_C04.indd 21 21/04/2016 11:32

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

22

● Introducing assessment as early as possible in the course will help develop confidence in learners.

● Use sample assessment materials as mock exams with learners, so they can practise their exam technique and time management skills. Over the lifespan of the specification, past papers along with accompanying mark schemes and examiner reports will become avail-able, which can also assist with practice.

● Help familiarise learners with the range of questions they may face in the exam by going through the different question types in the sample assessment material. The specifica-tions contain guidance on the typical command words used.

● The examination papers will include topics taken from any part of the specification. You should not assume that all papers will be the same as the sample assessment provided.

● In order to engage learners, use a variety of delivery methods to help learners prepare for the exam – for example, mock exams, pair and group work, and setting homework/assignments to test learners’ understanding throughout the course.

● At the end of each topic you can incorporate, into your teaching, a mini test to help consolidate learning.

● Clearly explain where your learners can make improvements.

● Recap the previous session at the start of each lesson as this will provide an opportunity to monitor learner progress and encourage questions.

Examples of learner-led activities:

● Advise your learners how to put together a revision timetable to help plan their time and study in preparation for the exam. This should include regular breaks and achiev-able targets (e.g. coverage of a particular area of content). Making a revision timetable not only reflects a disciplined nature of studying but also makes the learner prepare beforehand.

● Learners could revise in a variety of ways, including completing practice exercises, creating revision notes/cards, and reading relevant reference materials to broaden their understanding (e.g. textbooks and the internet).

● Through undertaking practice tests, it should be possible to identify learners’ weaker areas of understanding. This will allow them to focus their personal revision and self-study on those areas.

● Help the learner identify subject topics which are not fully understood.

● You should encourage your learners to:

– Give themselves enough time to study. – Organise a study space. – Plan a revision timetable. – Use diagrams: even in a financial environment these can be helpful. – Practice on old exam papers (where available). – Explain answers to others. – Take regular breaks during revision. – Make summary notes – making notes is by far the best way to memorise lots of infor-

mation.

M04_LCCI9007_01_CUS_C04.indd 22 21/04/2016 11:32

Chapter 4 Preparing learners for external assessment

23

● Advise learners of any special requirements for the examination, e.g. non-programmable calculator, identification requirements and any change in venue.

Examination techniques for learners

Tell your learners to:

● Allow themselves plenty of time to get to the venue before the exam starts.

● Read the examination paper fully before starting.

● Identify the questions they can answer with the most ease, and answer those first.

● Be aware that the marks allocated to each question provide an indication of the time required to complete it. Do not spend too much time on any one question.

● Be aware of the amount of time left.

● Aim to answer all questions on the paper even if some are left incomplete.

● Allow time at the end of the examination to check work.

● Be sure they answer the question as it is written, and not what they hoped it would be.

For more study skill advice and activities that you can download and give to your learners, visit the website qualifications.pearson.com/lcci and search for this qualification.

M04_LCCI9007_01_CUS_C04.indd 23 21/04/2016 11:32

M04_LCCI9007_01_CUS_C04.indd 24 21/04/2016 11:32

25

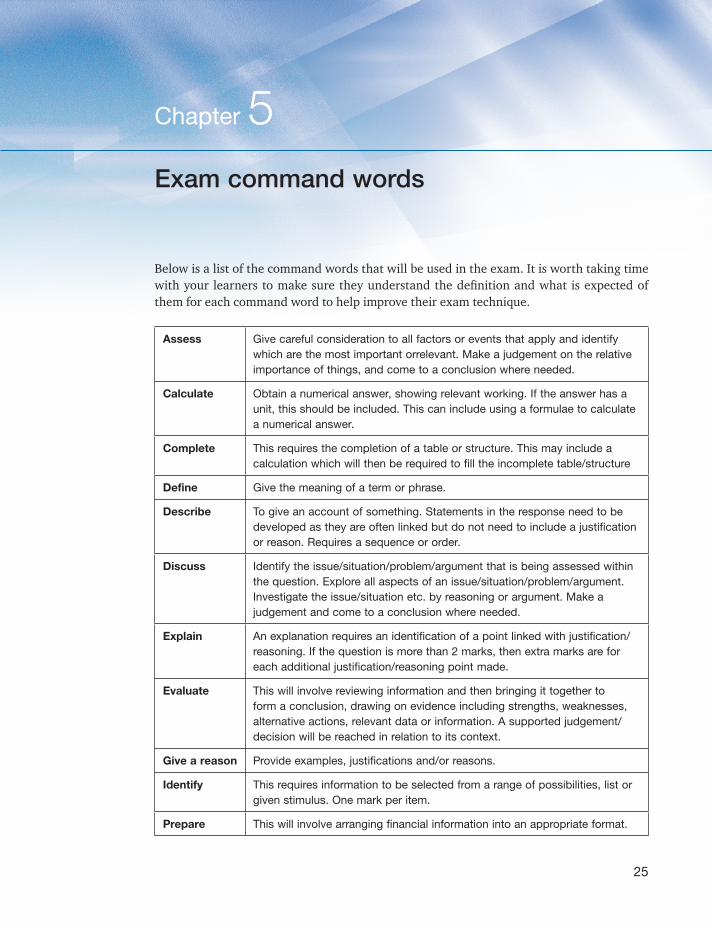

Chapter 5Exam command words

Below is a list of the command words that will be used in the exam. It is worth taking time with your learners to make sure they understand the definition and what is expected of them for each command word to help improve their exam technique.

Assess Give careful consideration to all factors or events that apply and identify which are the most important orrelevant. Make a judgement on the relative importance of things, and come to a conclusion where needed.

Calculate Obtain a numerical answer, showing relevant working. If the answer has a unit, this should be included. This can include using a formulae to calculate a numerical answer.

Complete This requires the completion of a table or structure. This may include a calculation which will then be required to fill the incomplete table/structure

Define Give the meaning of a term or phrase.

Describe To give an account of something. Statements in the response need to be developed as they are often linked but do not need to include a justification or reason. Requires a sequence or order.

Discuss Identify the issue/situation/problem/argument that is being assessed within the question. Explore all aspects of an issue/situation/problem/argument. Investigate the issue/situation etc. by reasoning or argument. Make a judgement and come to a conclusion where needed.

Explain An explanation requires an identification of a point linked with justification/reasoning. If the question is more than 2 marks, then extra marks are for each additional justification/reasoning point made.

Evaluate This will involve reviewing information and then bringing it together to form a conclusion, drawing on evidence including strengths, weaknesses, alternative actions, relevant data or information. A supported judgement/decision will be reached in relation to its context.

Give a reason Provide examples, justifications and/or reasons.

Identify This requires information to be selected from a range of possibilities, list or given stimulus. One mark per item.

Prepare This will involve arranging financial information into an appropriate format.

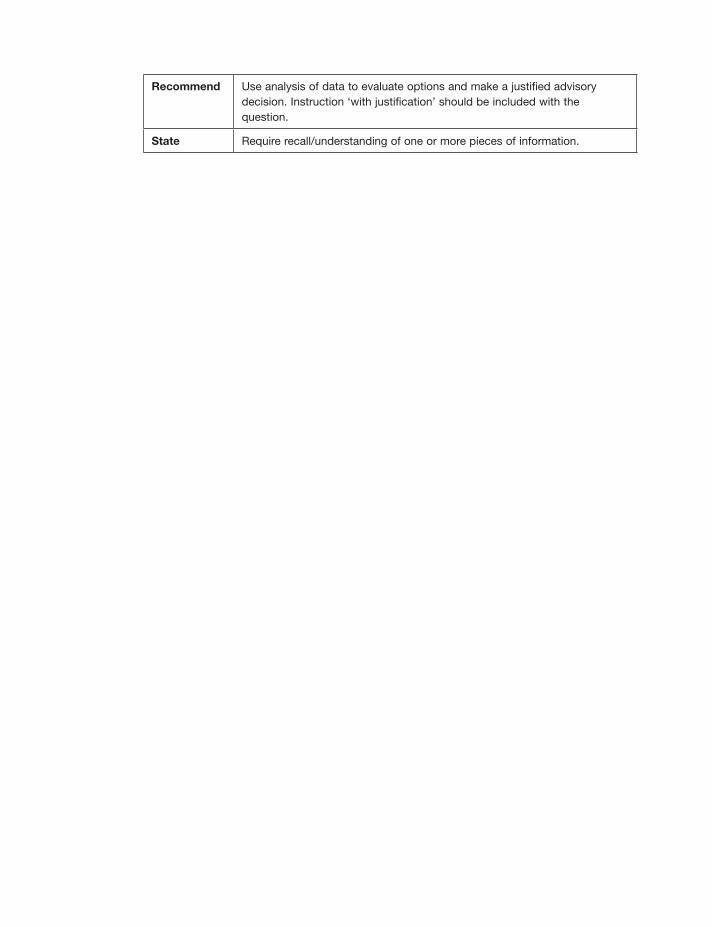

Recommend Use analysis of data to evaluate options and make a justified advisory decision. Instruction ‘with justification’ should be included with the question.

State Require recall/understanding of one or more pieces of information.

27

Chapter 6Practice exercises

Please note: these exercises are intended for use in the classroom to embed knowledge, and are not a replacement for exam preparation. To best prepare learners for examinations, please refer to the Sample Assessment Materials and Past Papers, which can be found on the Pearson website (qualifi cations.pearson.com/lcci)

Chapter 1

1.1 Prepare a summary of what is included in Parts A, B and C of the IFAC Code of Ethics for Professional Accountants.

1.2 Explain the fundamental principles you would expect to fi nd in a corporate code of governance.

1.3 What is the diff erence between an executive and non-executive director?

1.4 Explain the ‘materiality convention’ when applied to the preparation of fi nancial statements.

1.5 What are four important qualities that should govern accounting information?

Chapter 2

2.1 Detail three of the responsibilities of the external auditor.

2.2 What are the responsibilities of the directors in the audit activity?

2.3 Identify the fundamental diff erences between the company’s accountant and the company’s external auditor?

2.4 Explain the accruals convention and the impact it has on cash, bank and profi t balances in the accounts.

2.5 Explain the principles-based approach to standard with reference to (i) the advice provided by the IFRS and (ii) the role of the external audit function.

M06_LCCI9007_01_CUS_C06.indd 27 26/04/2016 08:52

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

28

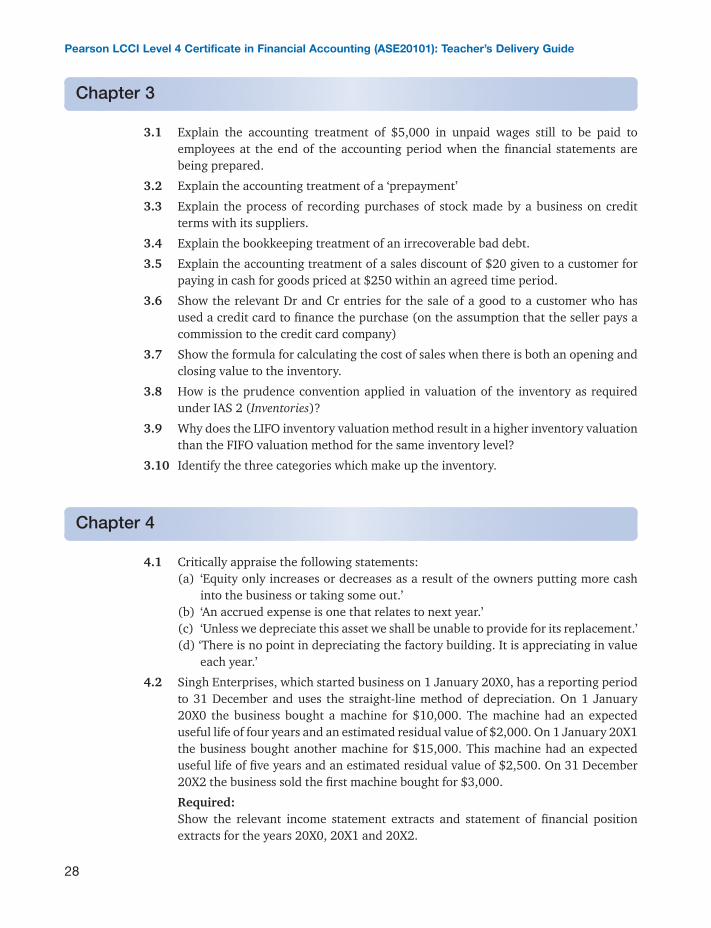

Chapter 3

3.1 Explain the accounting treatment of $5,000 in unpaid wages still to be paid to employees at the end of the accounting period when the financial statements are being prepared.

3.2 Explain the accounting treatment of a ‘prepayment’

3.3 Explain the process of recording purchases of stock made by a business on credit terms with its suppliers.

3.4 Explain the bookkeeping treatment of an irrecoverable bad debt.

3.5 Explain the accounting treatment of a sales discount of $20 given to a customer for paying in cash for goods priced at $250 within an agreed time period.

3.6 Show the relevant Dr and Cr entries for the sale of a good to a customer who has used a credit card to finance the purchase (on the assumption that the seller pays a commission to the credit card company)

3.7 Show the formula for calculating the cost of sales when there is both an opening and closing value to the inventory.

3.8 How is the prudence convention applied in valuation of the inventory as required under IAS 2 (Inventories)?

3.9 Why does the LIFO inventory valuation method result in a higher inventory valuation than the FIFO valuation method for the same inventory level?

3.10 Identify the three categories which make up the inventory.

Chapter 4

4.1 Critically appraise the following statements:(a) ‘Equity only increases or decreases as a result of the owners putting more cash

into the business or taking some out.’(b) ‘An accrued expense is one that relates to next year.’(c) ‘Unless we depreciate this asset we shall be unable to provide for its replacement.’(d) ‘There is no point in depreciating the factory building. It is appreciating in value

each year.’

4.2 Singh Enterprises, which started business on 1 January 20X0, has a reporting period to 31 December and uses the straight-line method of depreciation. On 1 January 20X0 the business bought a machine for $10,000. The machine had an expected useful life of four years and an estimated residual value of $2,000. On 1 January 20X1 the business bought another machine for $15,000. This machine had an expected useful life of five years and an estimated residual value of $2,500. On 31 December 20X2 the business sold the first machine bought for $3,000.

Required:Show the relevant income statement extracts and statement of financial position extracts for the years 20X0, 20X1 and 20X2.

M06_LCCI9007_01_CUS_C06.indd 28 26/04/2016 08:52

Chapter 6 Practice exercises

29

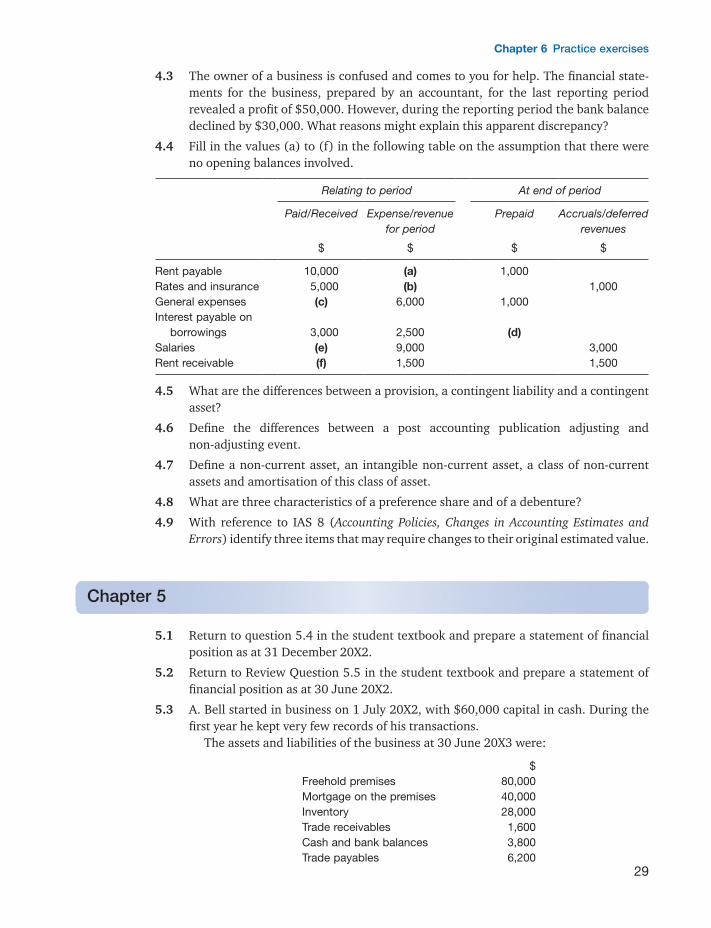

4.3 The owner of a business is confused and comes to you for help. The financial state-ments for the business, prepared by an accountant, for the last reporting period revealed a profit of $50,000. However, during the reporting period the bank balance declined by $30,000. What reasons might explain this apparent discrepancy?

4.4 Fill in the values (a) to (f) in the following table on the assumption that there were no opening balances involved.

Relating to period At end of period

Paid/Received Expense/revenue for period

Prepaid Accruals/deferred revenues

$ $ $ $

Rent payable 10,000 (a) 1,000Rates and insurance 5,000 (b) 1,000General expenses (c) 6,000 1,000Interest payable on

borrowings

3,000

2,500

(d)Salaries (e) 9,000 3,000Rent receivable (f) 1,500 1,500

4.5 What are the differences between a provision, a contingent liability and a contingent asset?

4.6 Define the differences between a post accounting publication adjusting and non-adjusting event.

4.7 Define a non-current asset, an intangible non-current asset, a class of non-current assets and amortisation of this class of asset.

4.8 What are three characteristics of a preference share and of a debenture?

4.9 With reference to IAS 8 (Accounting Policies, Changes in Accounting Estimates and Errors) identify three items that may require changes to their original estimated value.

Chapter 5

5.1 Return to question 5.4 in the student textbook and prepare a statement of financial position as at 31 December 20X2.

5.2 Return to Review Question 5.5 in the student textbook and prepare a statement of financial position as at 30 June 20X2.

5.3 A. Bell started in business on 1 July 20X2, with $60,000 capital in cash. During the first year he kept very few records of his transactions.

The assets and liabilities of the business at 30 June 20X3 were:

$Freehold premises 80,000Mortgage on the premises 40,000Inventory 28,000Trade receivables 1,600Cash and bank balances 3,800Trade payables 6,200

M06_LCCI9007_01_CUS_C06.indd 29 26/04/2016 08:52

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

30

During the year, Bell withdrew $12,000 cash for his personal use but he also paid $4,000 received from the sale of his private car into the business bank account.

Required:From the above information, prepare a statement of financial position showing the financial position of the business at 30 June 20X3 and indicating the profit for the year.

5.4 Black, Brown and Cook are partners. They share profits and losses in the ratios of 2/9, 1/3 and 4/9 respectively.

For the year ending 31 July 20X2, their capital accounts remained fixed at the following amounts:

$Black 60,000Brown 40,000Cook 20,000

They have agreed to give each other 6 per cent interest per annum on their capital accounts.

In addition to the above, partnership salaries of $30,000 for Brown and $18,000 for Cook are to be charged.

The profit for the year of the partnership, before taking any of the above into account was $111,000. You are required to draw up the appropriation account of the partnership for the year ending 31 July 20X2.

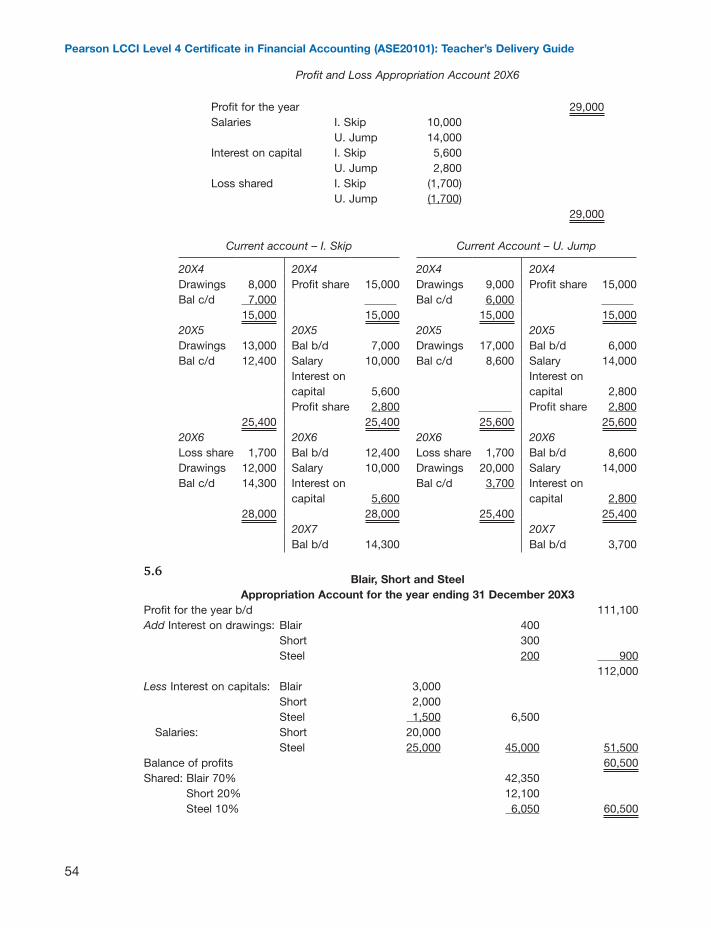

5.5 I. Skip and U. Jump sell toys. Their individual investments in the business on 1 January 20X4 were: Skip $80,000, Jump $40,000.

For the year to 31 December 20X4, the profit for the year was $30,000 and the partners’ drawings were: Skip $8,000, Jump $9,000.

For 20X4 (their first year), the partners agreed to share profits and losses equally, but they decided that from 1 January 20X5:

(i) The partners should be entitled to annual salaries of: Skip $10,000; Jump $14,000.

(ii) Interest should be allowed on capital at 7 per cent per annum.(iii) The profit remaining should be shared equally (as should losses).

Drawings

Profit for the year Skip Jumpbefore dealing

with partners’ items$ $ $

20X5 38,000 13,000 17,00020X6 29,000 12,000 20,000

Required:Prepare the profit and loss appropriation accounts and the partners’ current accounts for the three years.

5.6 Draw up a profit and loss appropriation account for the year ending 31 December 20X3 and statement of financial position extract at that date, from the following:

M06_LCCI9007_01_CUS_C06.indd 30 26/04/2016 08:52

Chapter 6 Practice exercises

31

(i) Profits for the year $111,100.(ii) Interest to be charged on capitals: Blair $3,000; Short $2,000; Steel $1,500.(iii) Interest to be charged on drawings: Blair $400; Short $300; Steel $200.(iv) Salaries to be credited: Short $20,000; Steel $25,000.(v) Profits to be shared: Blair 70%; Short 20%; Steel 10%.(vi) Current accounts: balances b/d Blair $18,600; Short $9,460; Steel $8,200.(vii) Capital accounts: balances b/d Blair $100,000; Short $50,000; Steel $25,000.(viii) Drawings: Blair $39,000; Short $27,100; Steel $16,800.

5.7 Frame and French are in partnership sharing profits and losses in the ratio 3:2. The following is their trial balance as at 30 September 20X2.

Dr Cr$ $

Buildings (cost $210,000) 160,000Fixtures at cost 8,200Provision for depreciation: Fixtures 4,200Trade receivables 61,400Trade payables 26,590Cash at bank 6,130Inventory at 30 September 20X1 62,740Revenue 363,111Purchases 210,000Carriage outwards 3,410Discounts allowed 620Loan interest: P. Prince 3,900Office expenses 4,760Salaries and wages 57,809Irrecoverable debts 1,632Allowance for doubtful debts 1,400Loan from P. Prince 65,000Capitals: Frame 100,000Capitals: French 75,000Current accounts: Frame 4,100Current accounts: French 1,200Drawings: Frame 31,800Drawings: French 28,200

640,601 640,601

Required:Prepare an income statement and profit and loss appropriation account for the year ending 30 September 20X2, and a statement of financial position as at that date.

(a) Inventory, 30 September 20X2, $74,210.(b) Expenses to be accrued: Office Expenses $215; Wages $720.(c) Depreciate fixtures 15 per cent on reducing balance basis, buildings $5,000.(d) Reduce provision for doubtful debts to $1,250.(e) Partnership salary: $30,000 to Frame. Not yet entered.(f) Interest on drawings: Frame $900; French $600.(g) Interest on capital account balances at 5 per cent.

5.8 The statements of financial position of A. Vantuira, a sole trader, for two successive

M06_LCCI9007_01_CUS_C06.indd 31 26/04/2016 08:52

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

32

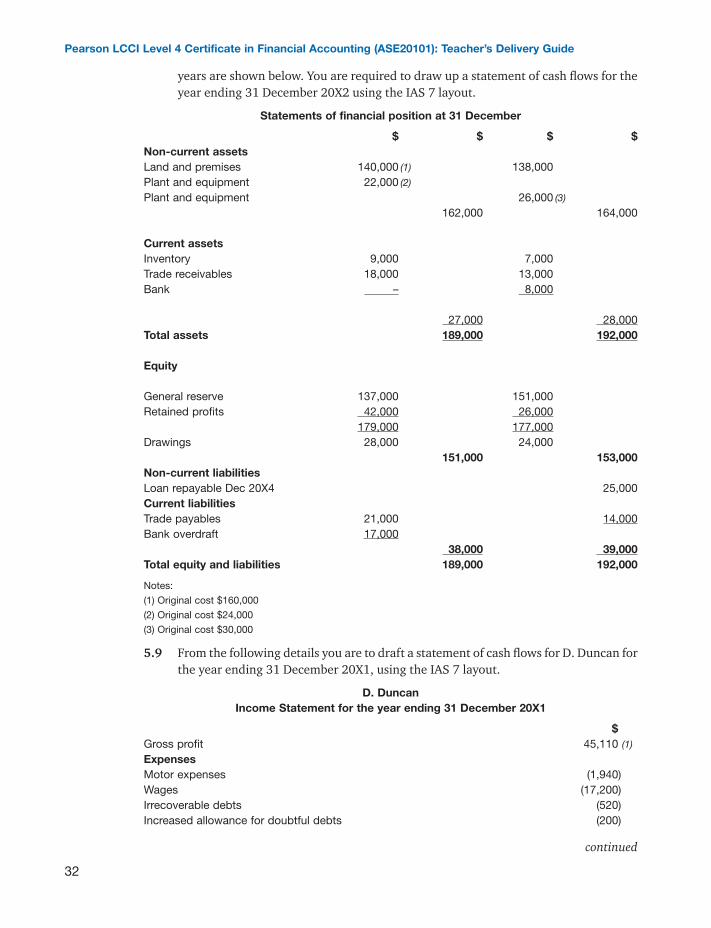

years are shown below. You are required to draw up a statement of cash flows for the year ending 31 December 20X2 using the IAS 7 layout.

Statements of financial position at 31 December

$ $ $ $Non-current assetsLand and premises 140,000 (1) 138,000Plant and equipment 22,000 (2)

Plant and equipment 26,000 (3)

162,000 164,000

Current assetsInventory 9,000 7,000Trade receivables 18,000 13,000Bank – 8,000

27,000 28,000Total assets 189,000 192,000

Equity

General reserve 137,000 151,000Retained profits 42,000 26,000

179,000 177,000Drawings 28,000 24,000

151,000 153,000Non-current liabilitiesLoan repayable Dec 20X4 25,000Current liabilitiesTrade payables 21,000 14,000Bank overdraft 17,000

38,000 39,000Total equity and liabilities 189,000 192,000

Notes:(1) Original cost $160,000(2) Original cost $24,000(3) Original cost $30,000

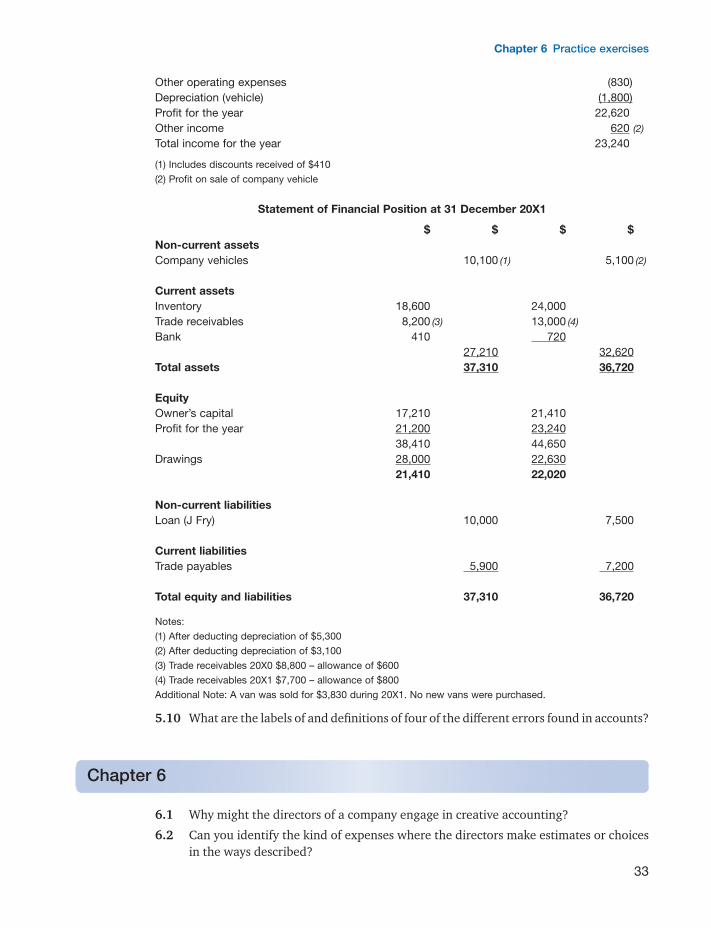

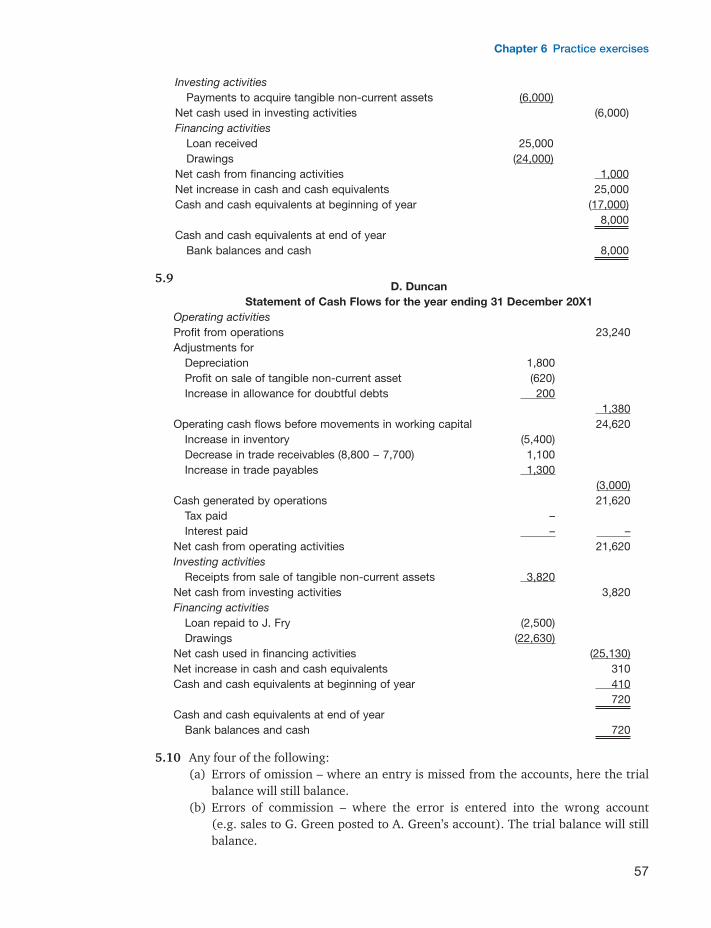

5.9 From the following details you are to draft a statement of cash flows for D. Duncan for the year ending 31 December 20X1, using the IAS 7 layout.

D. DuncanIncome Statement for the year ending 31 December 20X1

$Gross profit 45,110 (1)

ExpensesMotor expenses (1,940)Wages (17,200)Irrecoverable debts (520)Increased allowance for doubtful debts (200)

continued

M06_LCCI9007_01_CUS_C06.indd 32 26/04/2016 08:52

Chapter 6 Practice exercises

33

Other operating expenses (830)Depreciation (vehicle) (1,800)Profit for the year 22,620Other income 620 (2)

Total income for the year 23,240

(1) Includes discounts received of $410(2) Profit on sale of company vehicle

Statement of Financial Position at 31 December 20X1

$ $ $ $Non-current assetsCompany vehicles 10,100 (1) 5,100 (2)

Current assetsInventory 18,600 24,000Trade receivables 8,200 (3) 13,000 (4)

Bank 410 72027,210 32,620

Total assets 37,310 36,720

EquityOwner’s capital 17,210 21,410Profit for the year 21,200 23,240

38,410 44,650Drawings 28,000 22,630

21,410 22,020

Non-current liabilitiesLoan (J Fry) 10,000 7,500

Current liabilitiesTrade payables 5,900 7,200

Total equity and liabilities 37,310 36,720

Notes:(1) After deducting depreciation of $5,300(2) After deducting depreciation of $3,100(3) Trade receivables 20X0 $8,800 – allowance of $600(4) Trade receivables 20X1 $7,700 – allowance of $800Additional Note: A van was sold for $3,830 during 20X1. No new vans were purchased.

5.10 What are the labels of and definitions of four of the different errors found in accounts?

Chapter 6

6.1 Why might the directors of a company engage in creative accounting?

6.2 Can you identify the kind of expenses where the directors make estimates or choices in the ways described?

M06_LCCI9007_01_CUS_C06.indd 33 26/04/2016 08:52

Pearson LCCI Level 4 Certificate in Financial Accounting (ASE20101): Teacher’s Delivery Guide

34

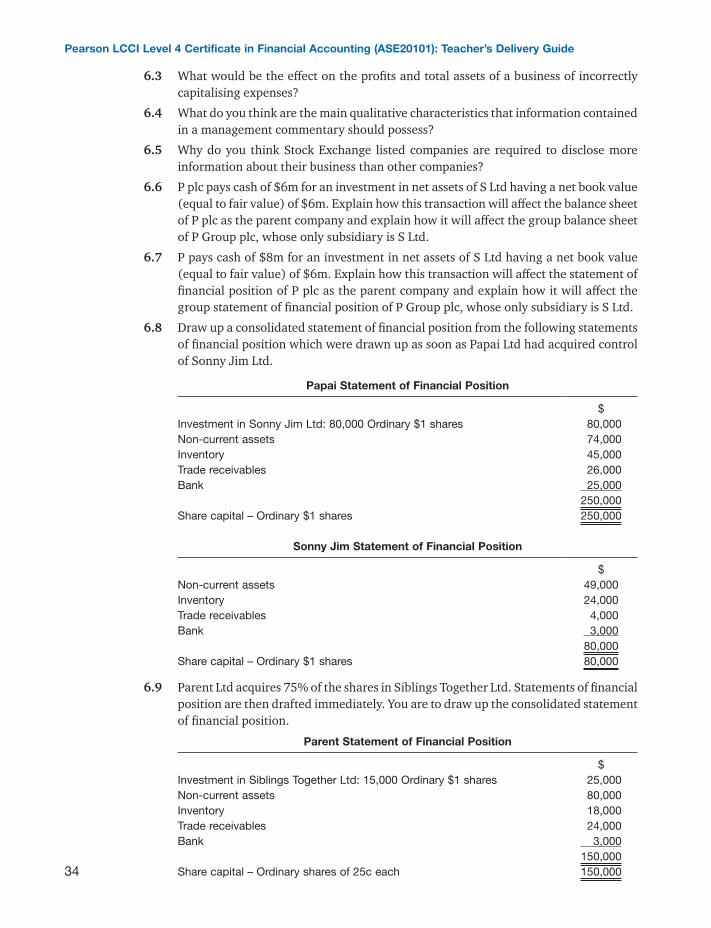

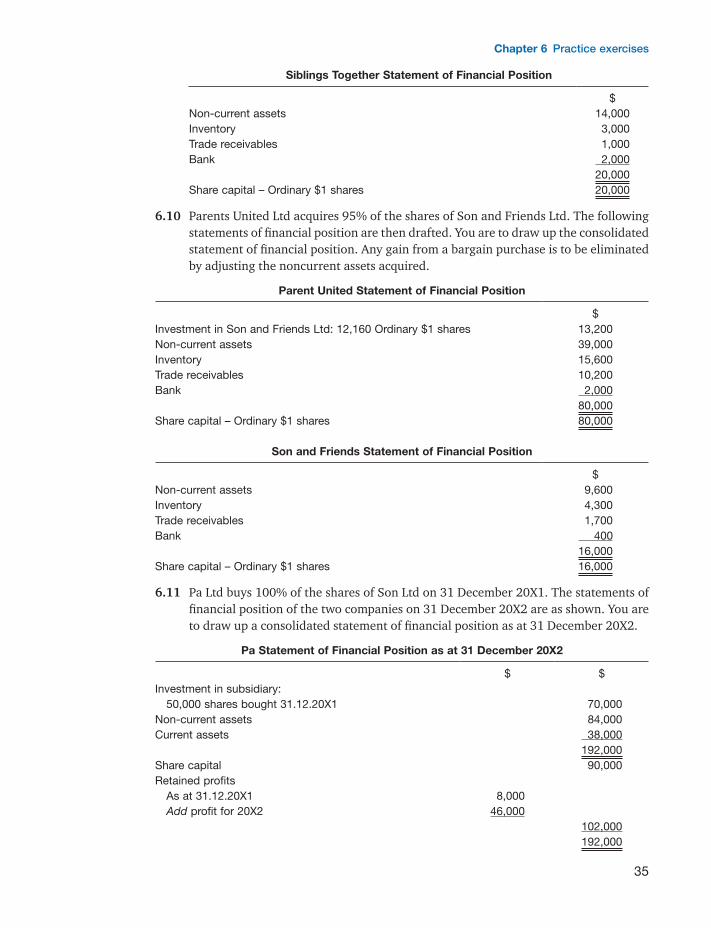

6.3 What would be the effect on the profits and total assets of a business of incorrectly capitalising expenses?

6.4 What do you think are the main qualitative characteristics that information contained in a management commentary should possess?

6.5 Why do you think Stock Exchange listed companies are required to disclose more information about their business than other companies?