TBS Real Property Policy Reset Progress Update RPIC Real Property Na8onal Workshop November 16, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TBS Real Property Policy Reset Progress Update

RPIC Real Property Na8onal Workshop November 16, 2016

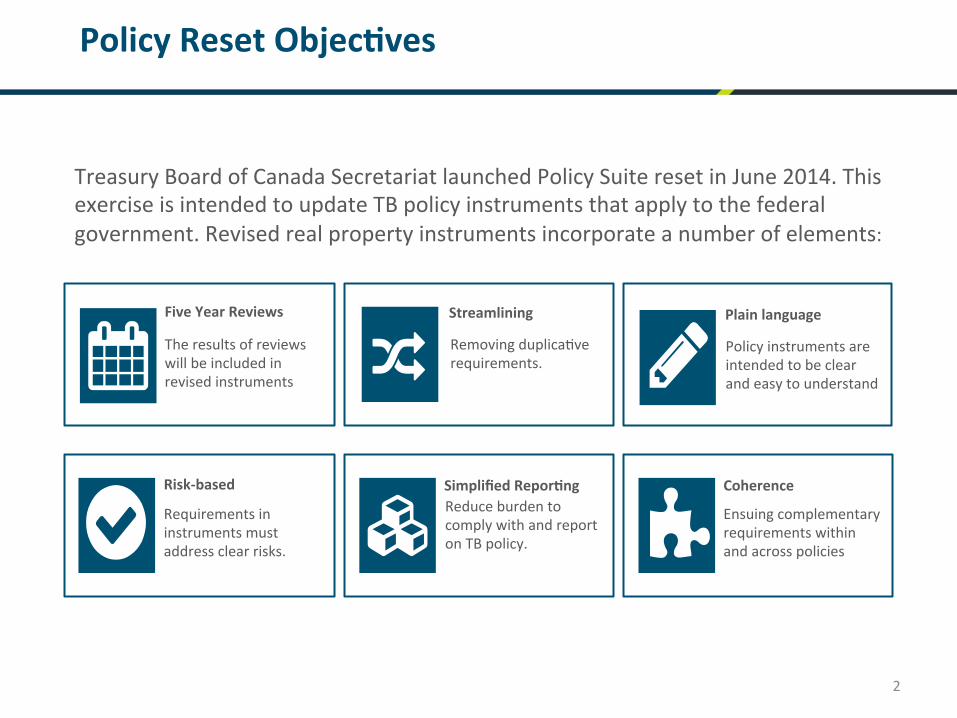

Treasury Board of Canada Secretariat launched Policy Suite reset in June 2014. This exercise is intended to update TB policy instruments that apply to the federal government. Revised real property instruments incorporate a number of elements:

Five Year Reviews

The results of reviews will be included in revised instruments

Plain language

Policy instruments are intended to be clear and easy to understand

Streamlining

Removing duplicaEve requirements.

Coherence

Ensuing complementary requirements within and across policies

Simplified Repor8ng Reduce burden to comply with and report on TB policy.

Risk-‐based

Requirements in instruments must address clear risks.

2

Policy Reset Objec8ves

3

Current Policy Suite for Assets and Acquired Services

ASAS func8ons

Investment Planning

Project Management

Capacity Building for

ASAS communi8es

Materiel

Real Property

Procurement

• Current Acquired Services and Assets Sector (ASAS) Policy Suite consists of: o 1 framework o 8 policies o 6 standards o 7 direcEves o 12 guidelines

• 22 Mandatory • 12 Non-‐mandatory

• ASAS works to build and maintain vibrant professional communiEes

• Treasury Board policies for the management of assets and acquired services set the direcEon to ensure that the conduct of these acEviEes provide value for money and sound stewardship

34 ASAS policy instruments

4

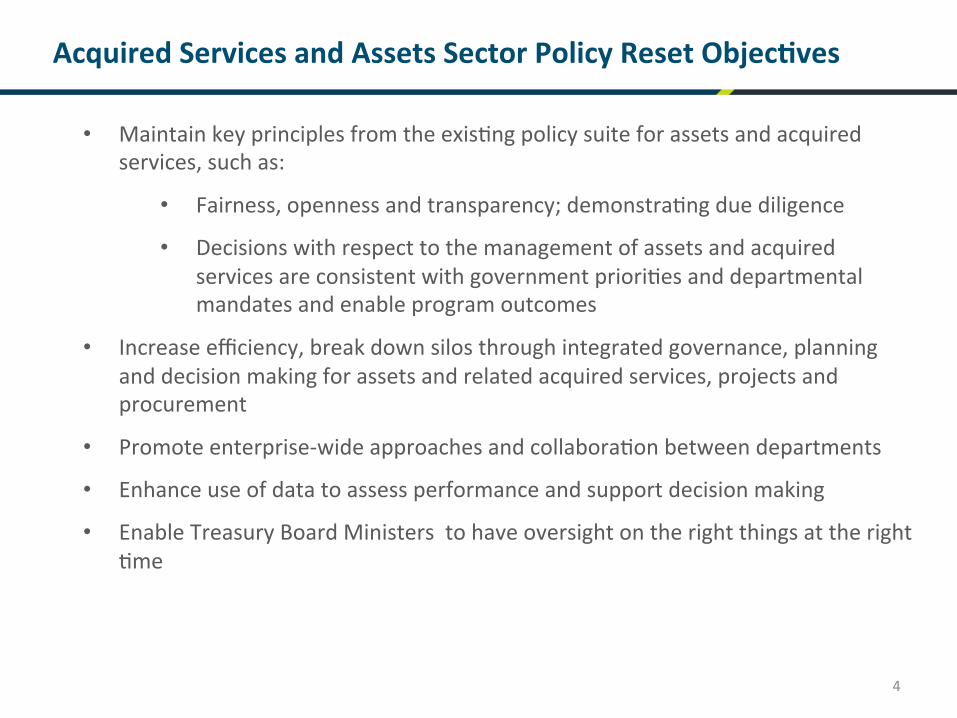

Acquired Services and Assets Sector Policy Reset Objec8ves

• Maintain key principles from the exisEng policy suite for assets and acquired services, such as:

• Fairness, openness and transparency; demonstraEng due diligence

• Decisions with respect to the management of assets and acquired services are consistent with government prioriEes and departmental mandates and enable program outcomes

• Increase efficiency, break down silos through integrated governance, planning and decision making for assets and related acquired services, projects and procurement

• Promote enterprise-‐wide approaches and collaboraEon between departments

• Enhance use of data to assess performance and support decision making

• Enable Treasury Board Ministers to have oversight on the right things at the right Eme

5

Proposed ASAS Policy Suite

Policy on Management of Assets, Procurement and Projects Sound stewardship

Open & Fair Transparent

Value for money Life-‐cycle approach

Support program delivery Investment Planning Capacity building

Procurement DirecEve

Real Property DirecEve

Materiel DirecEve Management of Projects DirecEve

• Eight ASAS policies are integrated into one policy – Policy on Management of Assets, Procurement and Projects

• Policy is supported by four func8onal area direc8ves with suppor8ng Mandatory Procedures • TB approval limits for projects, real property transac8ons and contracts are addressed in the

policy and corresponding func8onal direc8ves, as appropriate

6

Proposed Policy on the Management of Assets, Procurement and Projects

6 6

§ A single policy is intended to drive more integrated decision-making and reinforce life-cycle management

§ Requirement to assign responsibilities to appropriate senior officials

§ Encourages departments to consolidate requests for project, real property and procurement approvals by the Treasury Board

§ Capacity-building is brought to the forefront of the policy – similar to Financial Management and Internal Audit policies

§ Alignment with the new Policy on Results to support departments’ program delivery with a focus on outcomes

§ The Policy communicates the importance of assets and acquired services from the deputy head’s perspective

§ Directives, mandatory procedures, and guidance will communicate the “how”

Context

Planning

Acquisi8on

Asset Management Life Cycle

Ongoing assessment of asset performance to meet program

needs

People Governance & controls

Opera8ng & Maintenance

Disposal

Key Features

Five-‐year review: • Policy instruments effecEve in achieving

results

• Desire for more guidance vs. more policy

• Clarify disposal requirements

• Recognize that not all surplus properEes can be disposed

• DisEncEon between rouEne and strategic disposals is not clear

• Rust-‐out is a significant concern

Government priori8es: • Increase emphasis on relaEonship with

Indigenous Peoples and greening government operaEons

What we heard

Maintaining: • Life cycle approach • Decentralized custody model

Key Changes: • Adding self governing Indigenous

groups to priority list for disposals

• Requiring a strategy for underuElized real property

• EliminaEng rouEne/strategic disposal classificaEon

• AllocaEng appropriate investment in repair, maintenance and recapitalizaEon throughout the life cycle

• Allowing transfers of administraEon at nominal value, with tailored due diligence

• Strengthen requirements for consultaEon with Indigenous Peoples

• LimiEng the environmental footprint of real property operaEons

• IdenEfying opportuniEes for departments to share their special purpose real property

What we are proposing

Direc8ve on the Management of Real Property

7

8

Planning and Governance

GOVERNANCE

PLANNING

PROCESSES AND SYSTEMS

INVESTMENT IN ASSETS

InvesEng in assets; avoid deferral of maintenance.

Timely, informed real property decisions are supported by processes, systems and asset performance data.

Asset management strategies are based on performance informaEon and inform departmental investment plans.

Requirements targeted to a designated senior real property official, named by deputy head.

9

Stewardship

SHARING REAL PROPERTY

GREENING

ABORIGINAL RIGHTS AND INTERESTS

STREAMLINED AND CLARIFIED

Requirements from exisEng Appraisal and Es,mates Standard, Accessibility Standard and Fire Protec,on Standard have been streamlined and clarified.

Strengthening requirements to consult and engage Aboriginal groups throughout the life cycle.

LimiEng the environmental footprint of real property in a manner consistent with government objecEves for sustainable development and GHG reducEon.

Encourages an enterprise –wide focus by removing barriers to co-‐locaEon, with the objecEve of encouraging porholio raEonalizaEon and shared use of real property assets.

10

Acquisi8on

ASSESSMENT OF NEED

OPTIONS ANALYSIS

DUE DILIGENCE

REAL ESTATE PRACTICES

Due diligence requirements prior to acquisiEon of real property are clarified.

ExaminaEon of opEons prior to acquisiEon to support decisions that are cost-‐effecEve over the life cycle of the asset.

Need to acquire real property should be based on program requirements and government-‐wide objecEves.

Acquire real property in a fair and transparent manner.

11

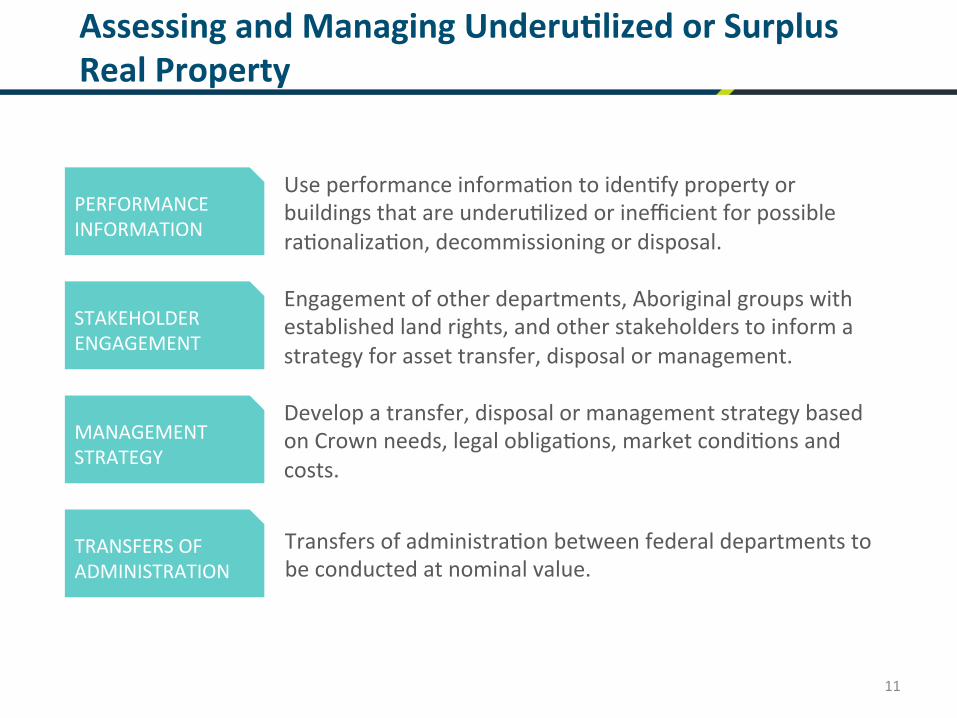

Assessing and Managing Underu8lized or Surplus Real Property

PERFORMANCE INFORMATION

STAKEHOLDER ENGAGEMENT

MANAGEMENT STRATEGY

TRANSFERS OF ADMINISTRATION

Develop a transfer, disposal or management strategy based on Crown needs, legal obligaEons, market condiEons and costs.

Engagement of other departments, Aboriginal groups with established land rights, and other stakeholders to inform a strategy for asset transfer, disposal or management.

Use performance informaEon to idenEfy property or buildings that are underuElized or inefficient for possible raEonalizaEon, decommissioning or disposal.

Transfers of administraEon between federal departments to be conducted at nominal value.

12

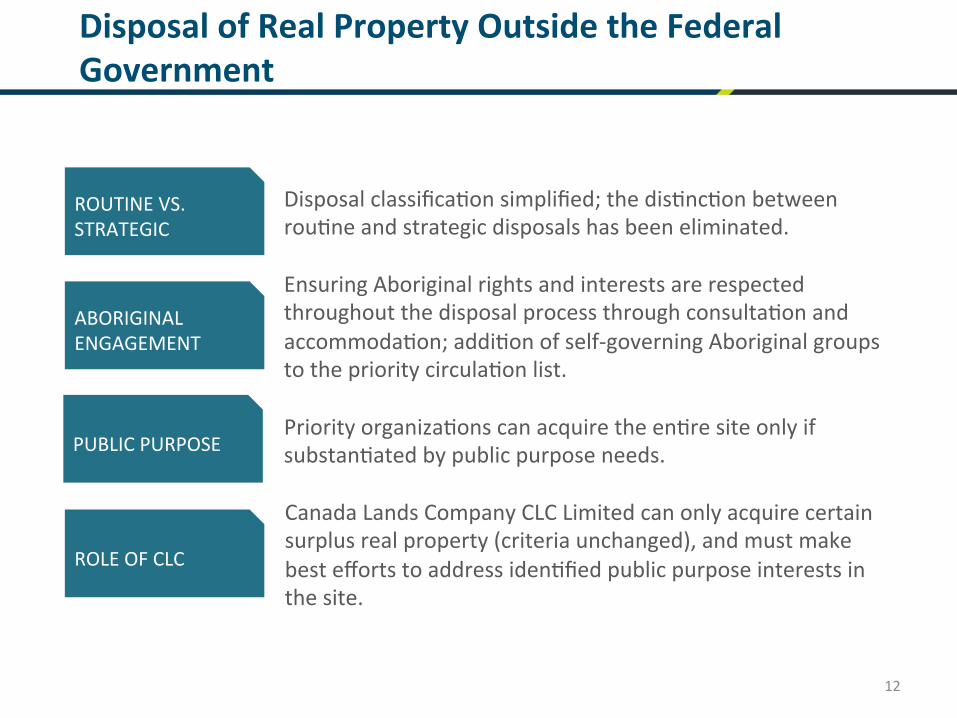

Disposal of Real Property Outside the Federal Government

ROUTINE VS. STRATEGIC

ABORIGINAL ENGAGEMENT

PUBLIC PURPOSE

ROLE OF CLC

Priority organizaEons can acquire the enEre site only if substanEated by public purpose needs.

Ensuring Aboriginal rights and interests are respected throughout the disposal process through consultaEon and accommodaEon; addiEon of self-‐governing Aboriginal groups to the priority circulaEon list.

Disposal classificaEon simplified; the disEncEon between rouEne and strategic disposals has been eliminated.

Canada Lands Company CLC Limited can only acquire certain surplus real property (criteria unchanged), and must make best efforts to address idenEfied public purpose interests in the site.

Horizontal Engagement -‐ Cross funcEonal focus groups organized to discuss the

Policy, how to promote integraEon and improve management pracEces.

Func8onal Communi8es -‐ Engagement of exisEng working groups and communiEes

of pracEce. -‐ Focus groups on key themes/issues as required.

Wri]en Feedback -‐ Drak instruments on GCPedia. -‐ Formal request for wrilen feedback. -‐ Discussion on GC Connex.

Approach to Consulta8ons

13

14

Next Steps

• Complete consultaEons with key stakeholders and revise drak policy instruments

• External to government discussion with key interest groups.

• Seek internal approvals within TBS, followed by Treasury Board

• Release approved policies and develop guidance, tools and training prior to implementaEon date

• Implement and monitor revised instruments and support users through the first year, to ensure effecEveness and determine whether any adjustments are required

Related Documents