Taxation of Trusts - Old Square Tax Chambers | Tax … · Developments in the Taxation of Land Transactions Rory Mullan [email protected] 020 7242 2744. Tax charges on

Aug 31, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Tax charges on land

TAX CHARGES ON LANDTwo areas appear to have been targeted:

• Residential property held through companies / corporate entities for private use

• Multiple ownership of property by individuals for commercial use

TAX CHARGES ON LANDRecent amendments include:

• Transactions in land

• CGT rates for residential property

• Restrictions in deductions for interest

• Additional SDLT for second homes

TAX CHARGES ON LANDRecent amendments include:• ATED related gains• NRCGT• SDLT for corporate purchasers• ATED• IHT excluded property treatment for

companies with residential property

Transactions in land

TRANSACTIONS IN LAND“Significant amendments to the Finance Bill slipped in at committee stage set a disturbing precedent of avoiding proper consultation and scrutiny, the Law Society said today.The changes, which alter the way buy-to-let properties will be taxed, may result in many investors paying income tax rather than a capital gains tax on their investment, creating uncertainty for taxpayers.”

Law Society press release 24 August 2016

TRANSACTIONS IN LAND• Concern is that gains by buy-to-let investors

would be subject to income tax rather than capital gains tax

• This has not been trailed in legislation which is apparently aimed at offshore developers

TRANSACTIONS IN LAND• Section 79 FA 2016 inserts a new Part 9A

ITA 2007 entitled “Transactions in UK Land”

• Similar amendments for corporation tax purposes in section 77 FA 2016 inserting a new Part 8ZB CTA 2010

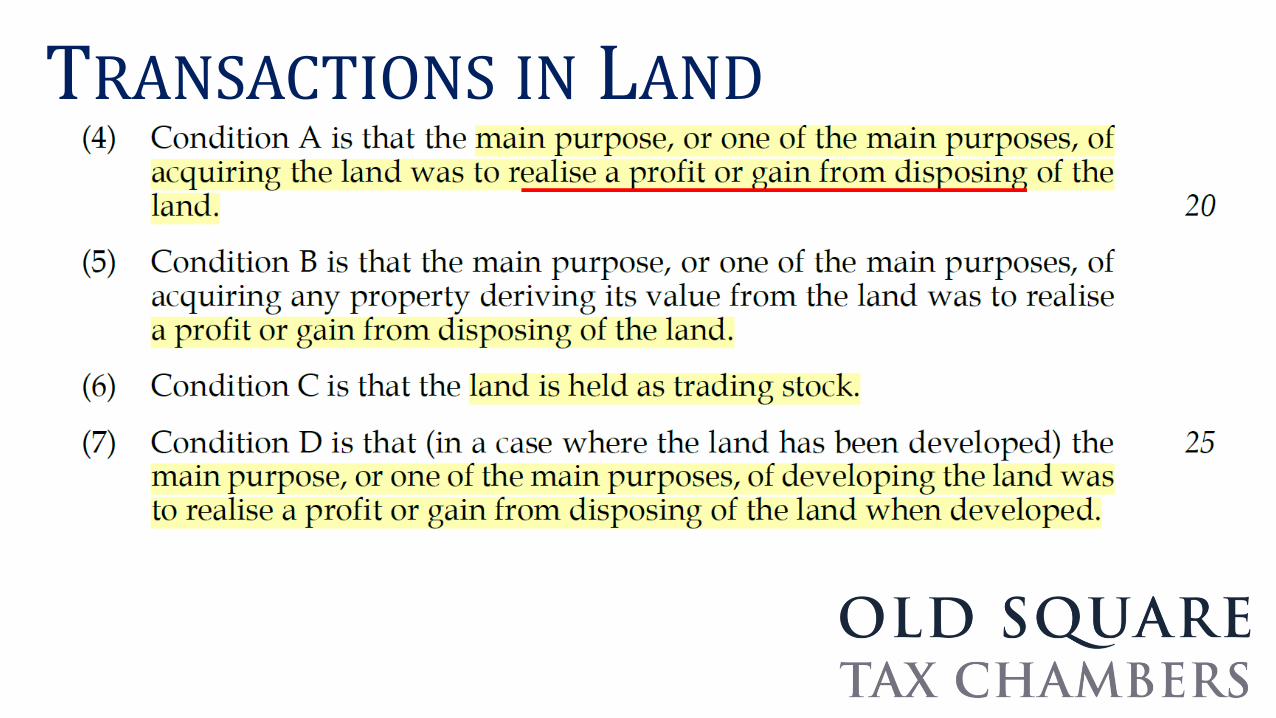

TRANSACTIONS IN LAND

TRANSACTIONS IN LAND

TRANSACTIONS IN LAND• What does condition A mean?

• Concern that primary reason for investing in buy to let is capital gain at end

• Does this bring the gain within the charge to income tax?

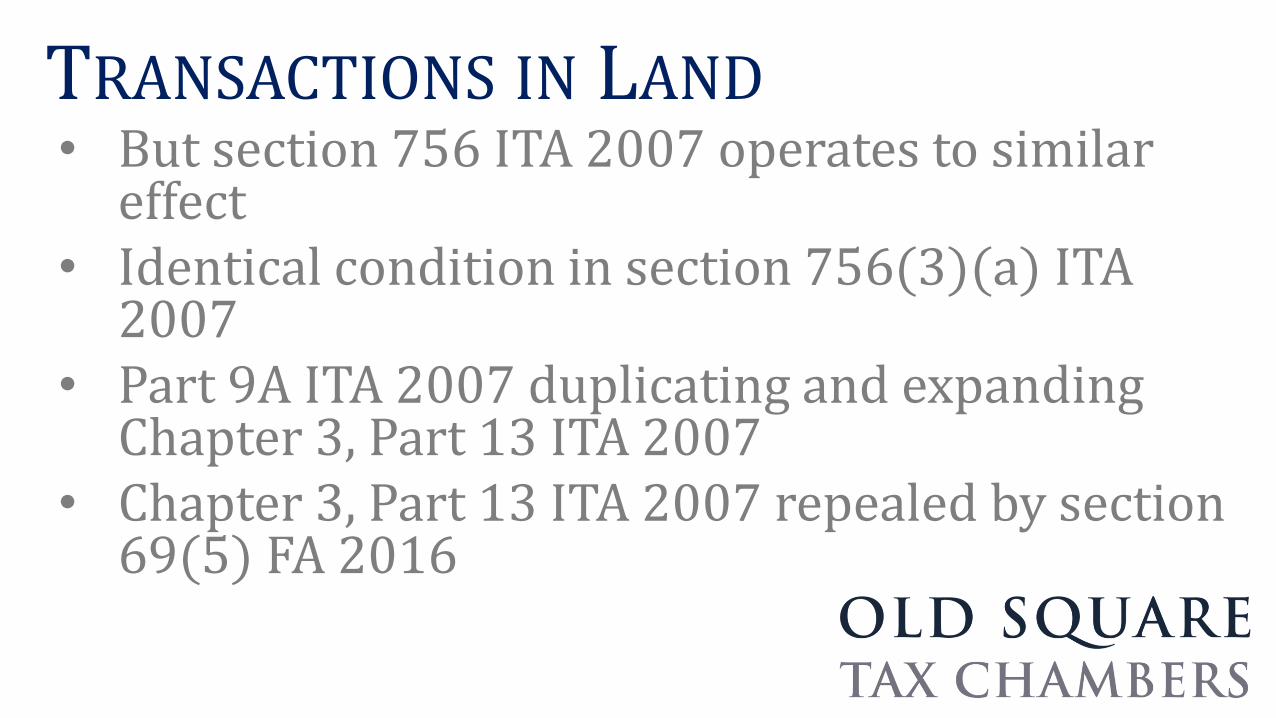

TRANSACTIONS IN LAND• But section 756 ITA 2007 operates to similar

effect• Identical condition in section 756(3)(a) ITA

2007• Part 9A ITA 2007 duplicating and expanding

Chapter 3, Part 13 ITA 2007• Chapter 3, Part 13 ITA 2007 repealed by section

69(5) FA 2016

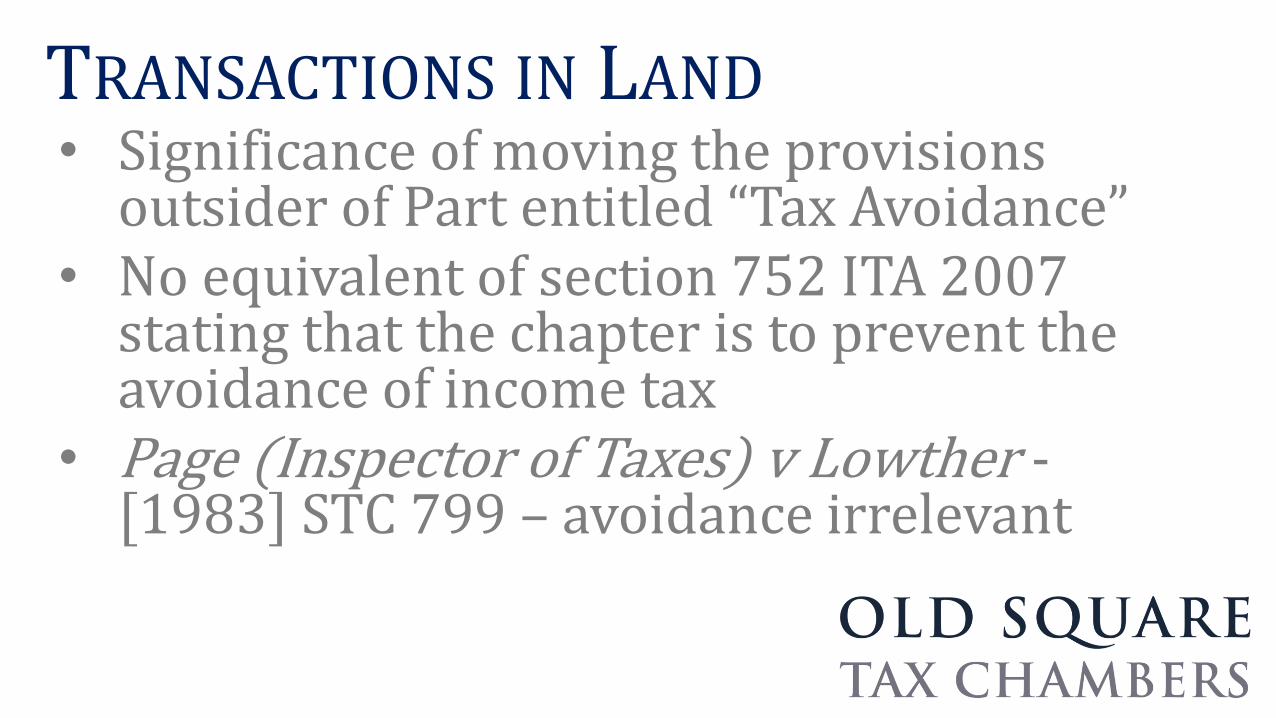

TRANSACTIONS IN LAND• Significance of moving the provisions

outsider of Part entitled “Tax Avoidance”• No equivalent of section 752 ITA 2007

stating that the chapter is to prevent the avoidance of income tax

• Page (Inspector of Taxes) v Lowther -[1983] STC 799 – avoidance irrelevant

TRANSACTIONS IN LAND• Significance of moving the provisions

outsider of Part entitled “Tax Avoidance”• No equivalent of section 752 ITA 2007

stating that the chapter is to prevent the avoidance of income tax

• Page (Inspector of Taxes) v Lowther -[1983] STC 799 – avoidance irrelevant

TRANSACTIONS IN LANDHMRC have indicated in correspondence with the NLA:“HMRC considers that generally propertyinvestors that buy properties to let out togenerate property income and some yearslater sell the properties will be subject tocapital gains on their disposals rather thanbeing charged to income on the disposal.”

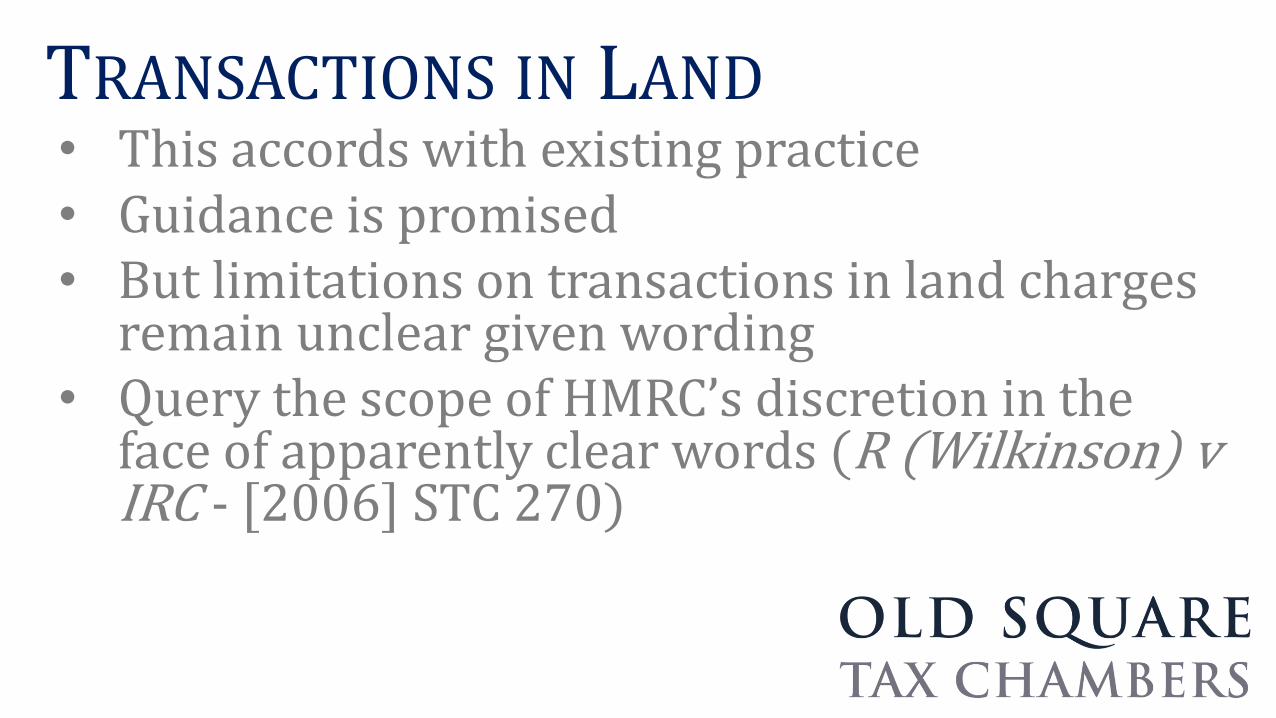

TRANSACTIONS IN LAND• This accords with existing practice• Guidance is promised• But limitations on transactions in land charges

remain unclear given wording• Query the scope of HMRC’s discretion in the

face of apparently clear words (R (Wilkinson) v IRC - [2006] STC 270)

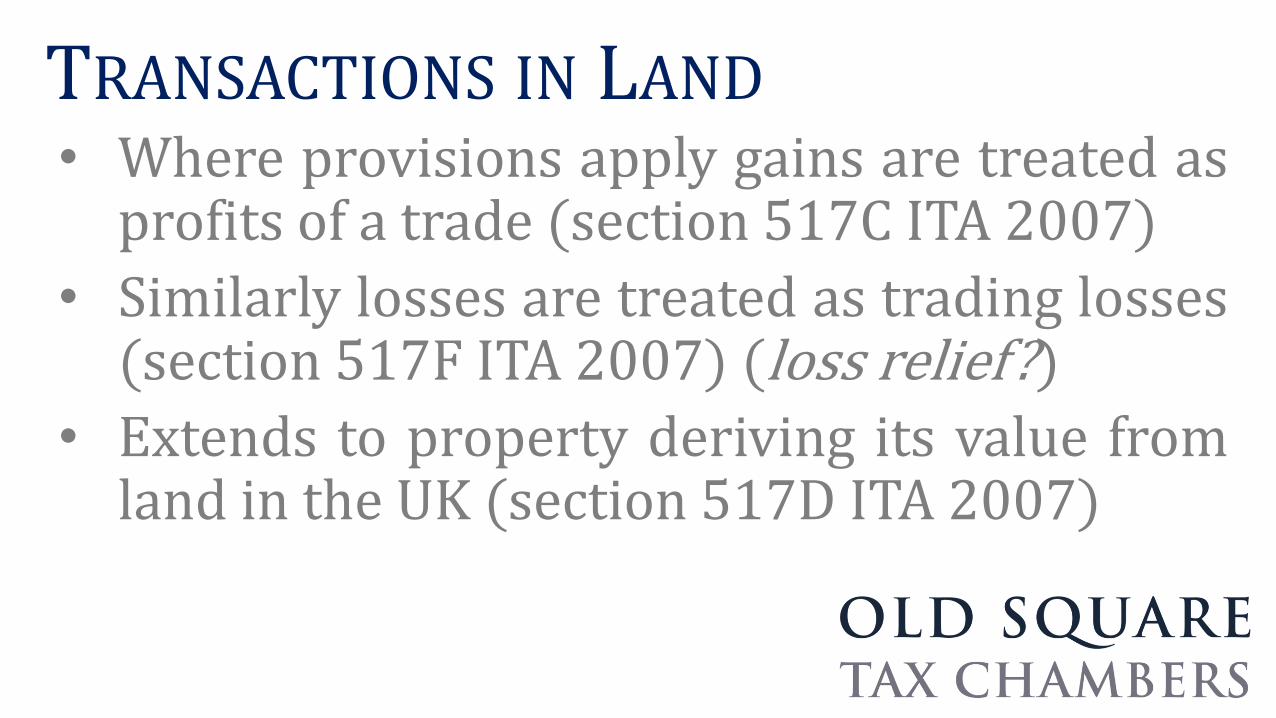

TRANSACTIONS IN LAND• Where provisions apply gains are treated as

profits of a trade (section 517C ITA 2007)

• Similarly losses are treated as trading losses(section 517F ITA 2007) (loss relief?)

• Extends to property deriving its value fromland in the UK (section 517D ITA 2007)

TRANSACTIONS IN LAND• Anti-avoidance provision in section 517K

ITA 2007 allows counteraction

• Includes tax advantage under a DTA but onlywhere contrary to the purpose of the DTA

• Exemption where PPR otherwise available(section 517M ITA 2007)

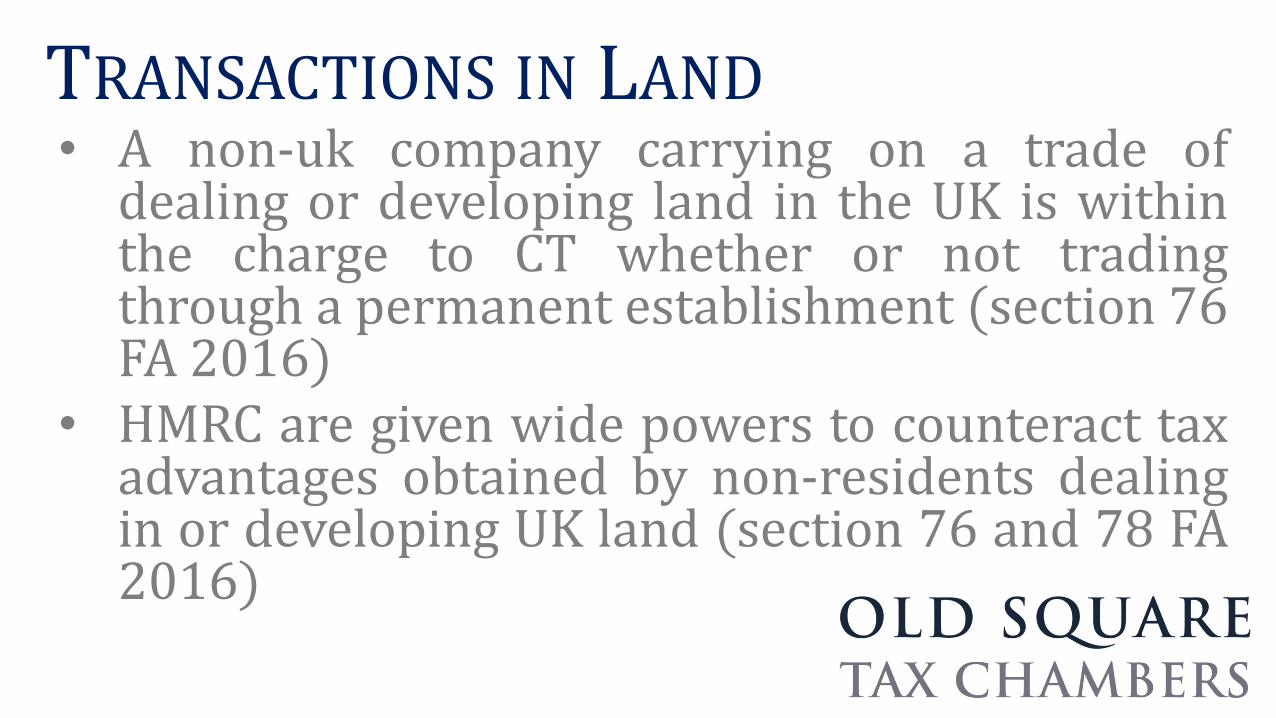

TRANSACTIONS IN LAND• A non-uk company carrying on a trade of

dealing or developing land in the UK is withinthe charge to CT whether or not tradingthrough a permanent establishment (section 76FA 2016)

• HMRC are given wide powers to counteract taxadvantages obtained by non-residents dealingin or developing UK land (section 76 and 78 FA2016)

CGT rates for residential property

CGT RESIDENTIAL PROPERTY RATES

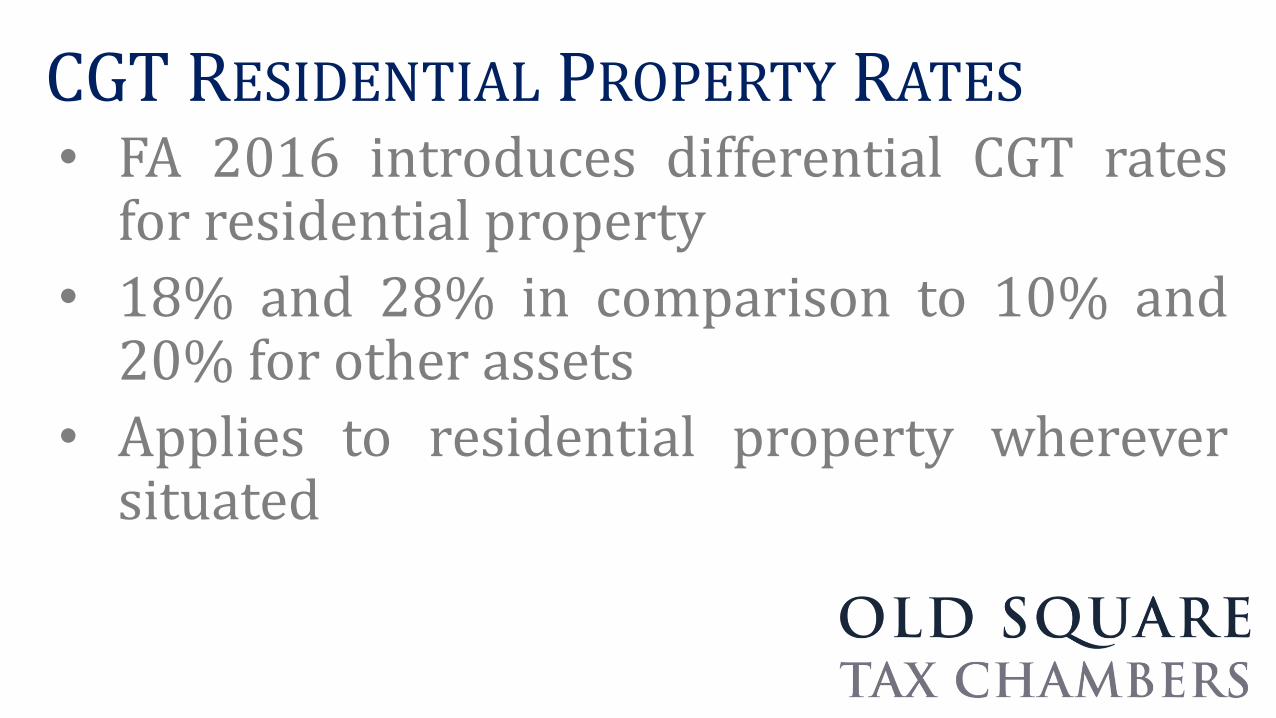

• FA 2016 introduces differential CGT ratesfor residential property

• 18% and 28% in comparison to 10% and20% for other assets

• Applies to residential property whereversituated

Restrictions in interest deductions

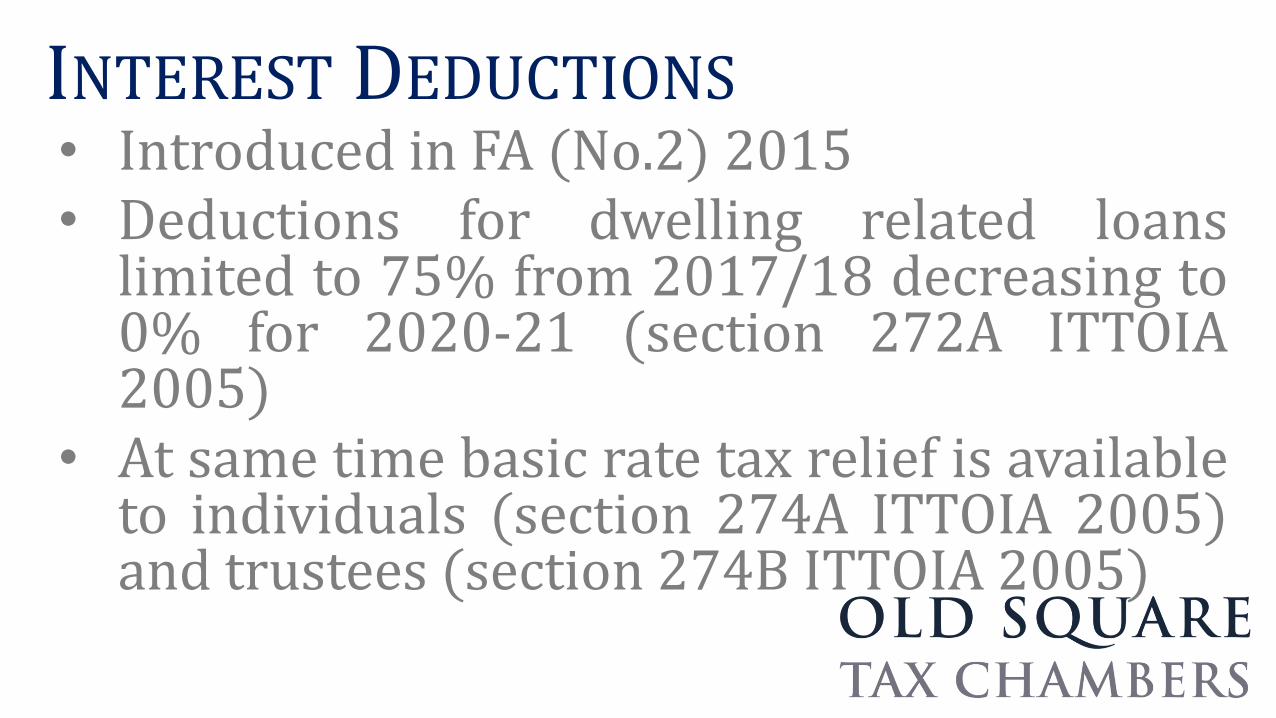

INTEREST DEDUCTIONS• Introduced in FA (No.2) 2015• Deductions for dwelling related loans

limited to 75% from 2017/18 decreasing to0% for 2020-21 (section 272A ITTOIA2005)

• At same time basic rate tax relief is availableto individuals (section 274A ITTOIA 2005)and trustees (section 274B ITTOIA 2005)

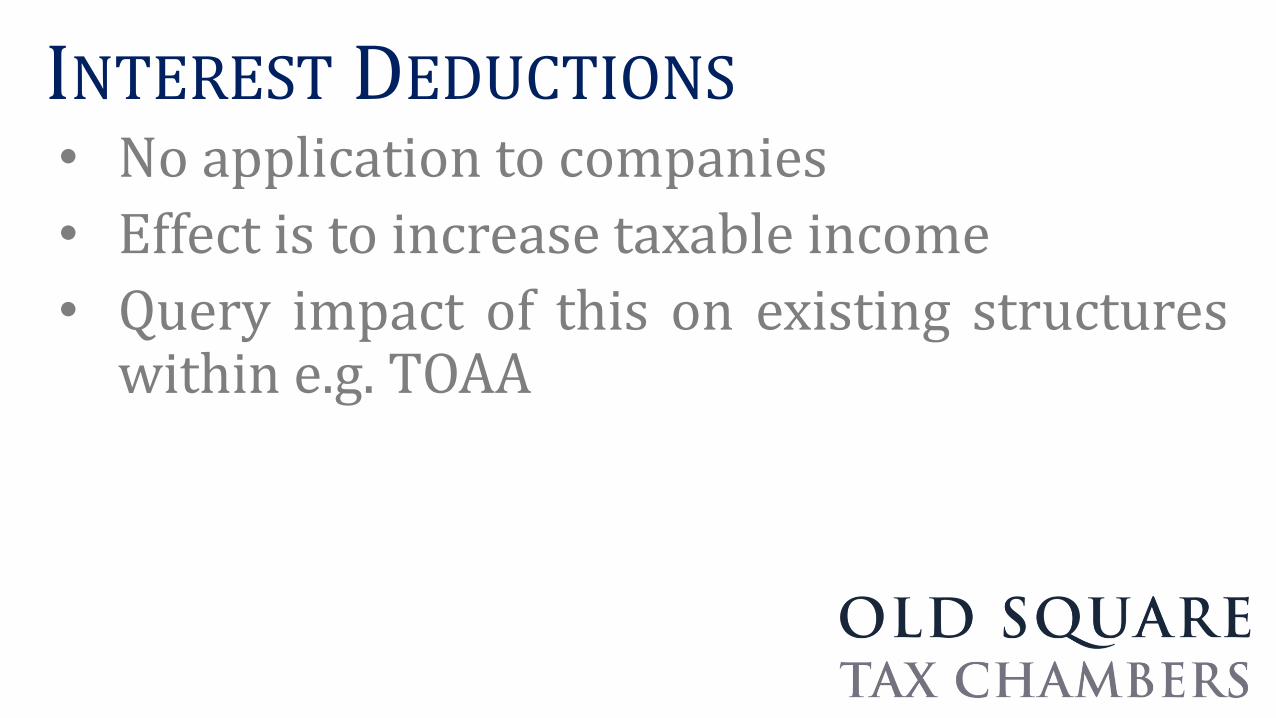

INTEREST DEDUCTIONS• No application to companies

• Effect is to increase taxable income

• Query impact of this on existing structureswithin e.g. TOAA

Excluded property for IHT

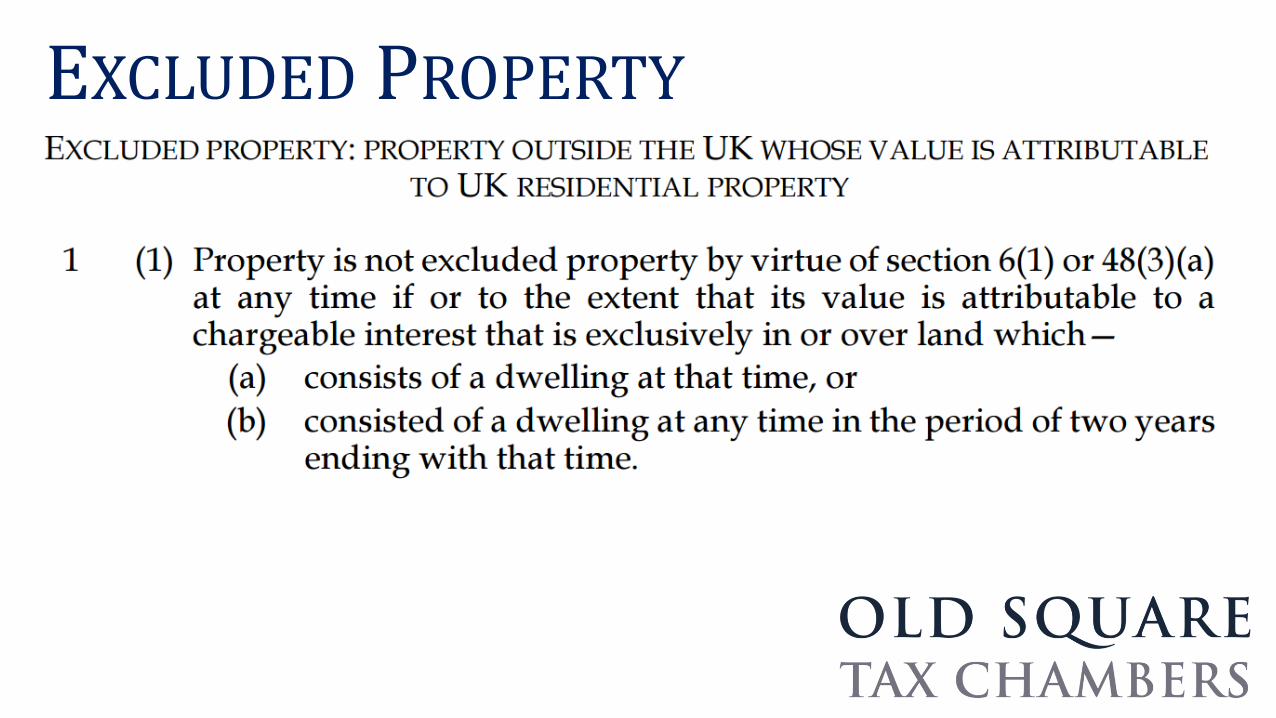

EXCLUDED PROPERTY

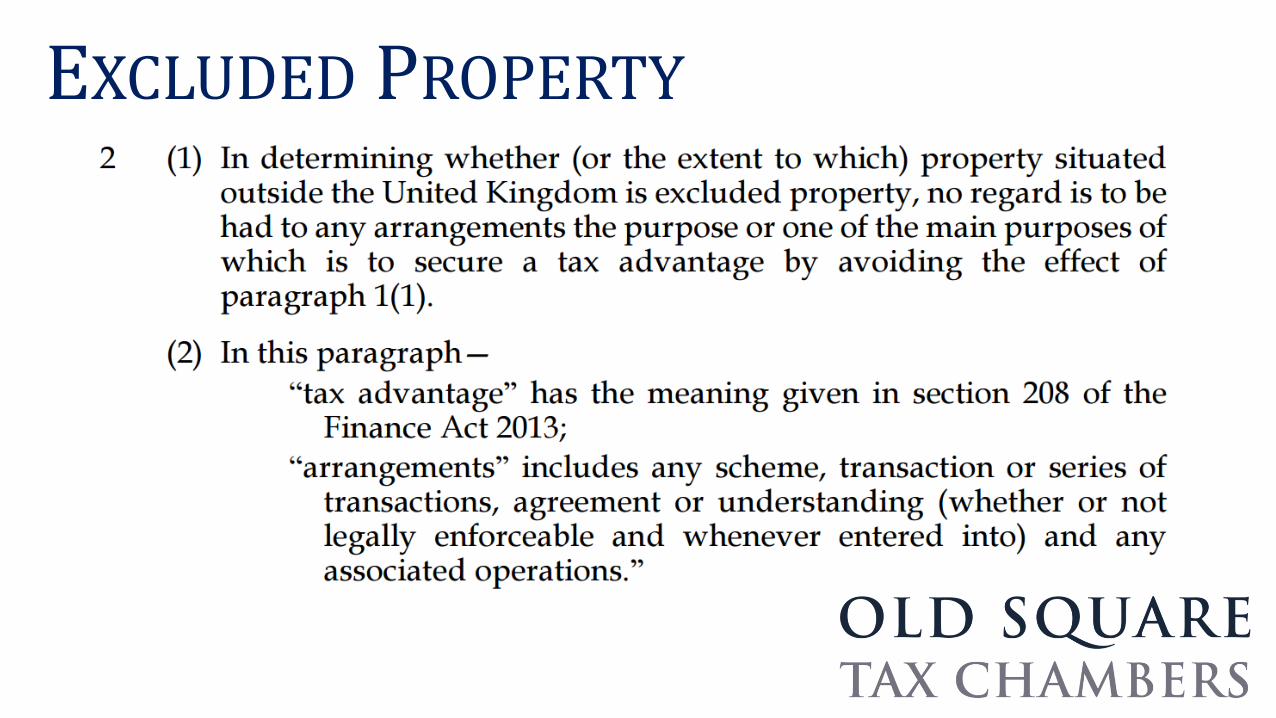

EXCLUDED PROPERTY

EXCLUDED PROPERTY

SDLT on additional dwellings

SDLT ON ADDITIONAL DWELLINGS• Introduced by section 128 FA 2016

• Creates a new Schedule 4ZA FA 2003

• Rates on additional purchases of residentialproperty 3% higher

• Does not apply is purchase is of mixedresidential and commercial

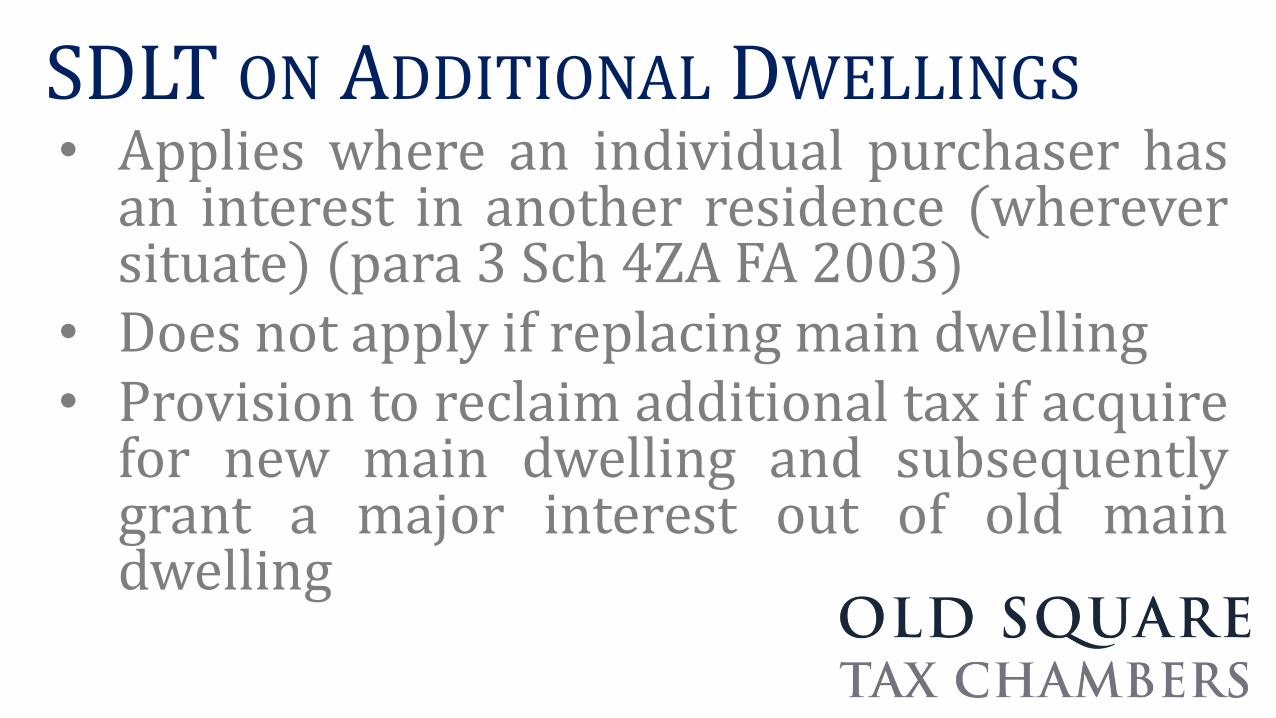

SDLT ON ADDITIONAL DWELLINGS• Applies where an individual purchaser has

an interest in another residence (whereversituate) (para 3 Sch 4ZA FA 2003)

• Does not apply if replacing main dwelling• Provision to reclaim additional tax if acquire

for new main dwelling and subsequentlygrant a major interest out of old maindwelling

SDLT ON ADDITIONAL DWELLINGS• Additional rate applies automatically where

purchaser is not an individual – even if thedwelling is not an “additional” one (para 4,Sch 4ZA FA 2003)

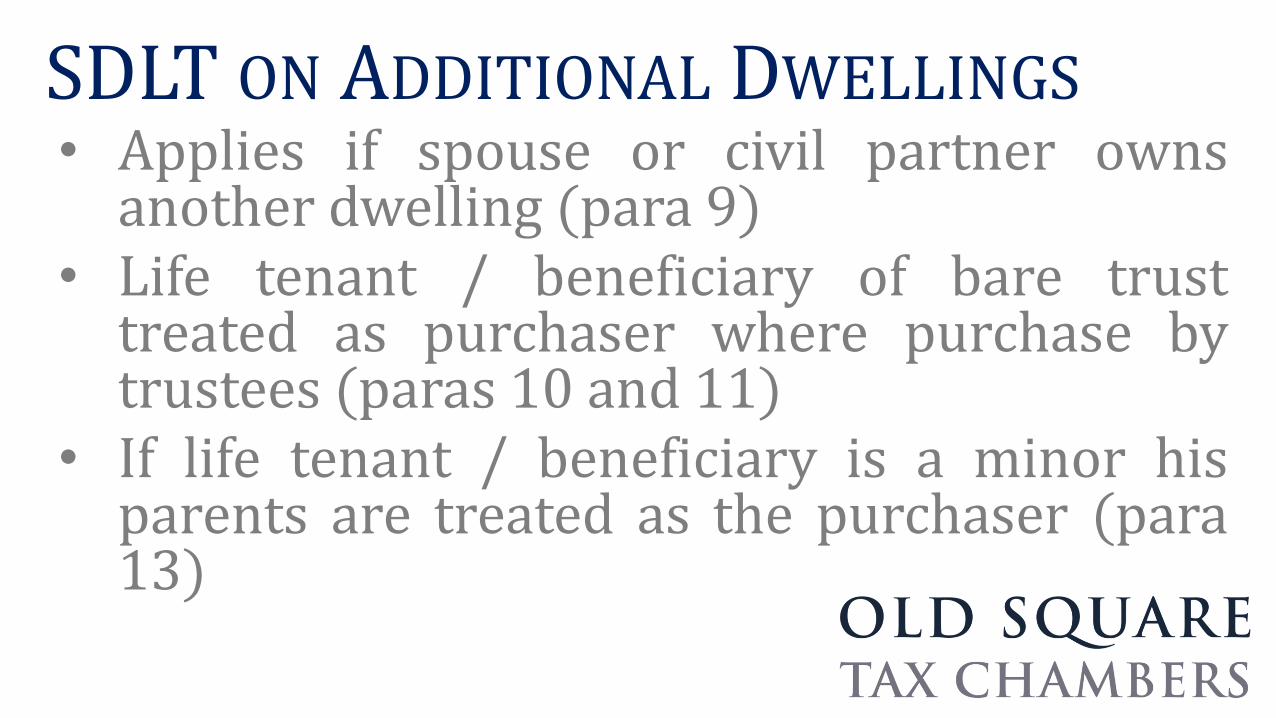

SDLT ON ADDITIONAL DWELLINGS• Applies if spouse or civil partner owns

another dwelling (para 9)• Life tenant / beneficiary of bare trust

treated as purchaser where purchase bytrustees (paras 10 and 11)

• If life tenant / beneficiary is a minor hisparents are treated as the purchaser (para13)

SDLT ON ADDITIONAL DWELLINGS• Purchase by a discretionary trust will be

caught by the charge (para 13)

• Inheritances of not more than 50% of adwelling are disregarded for 3 years (para16)

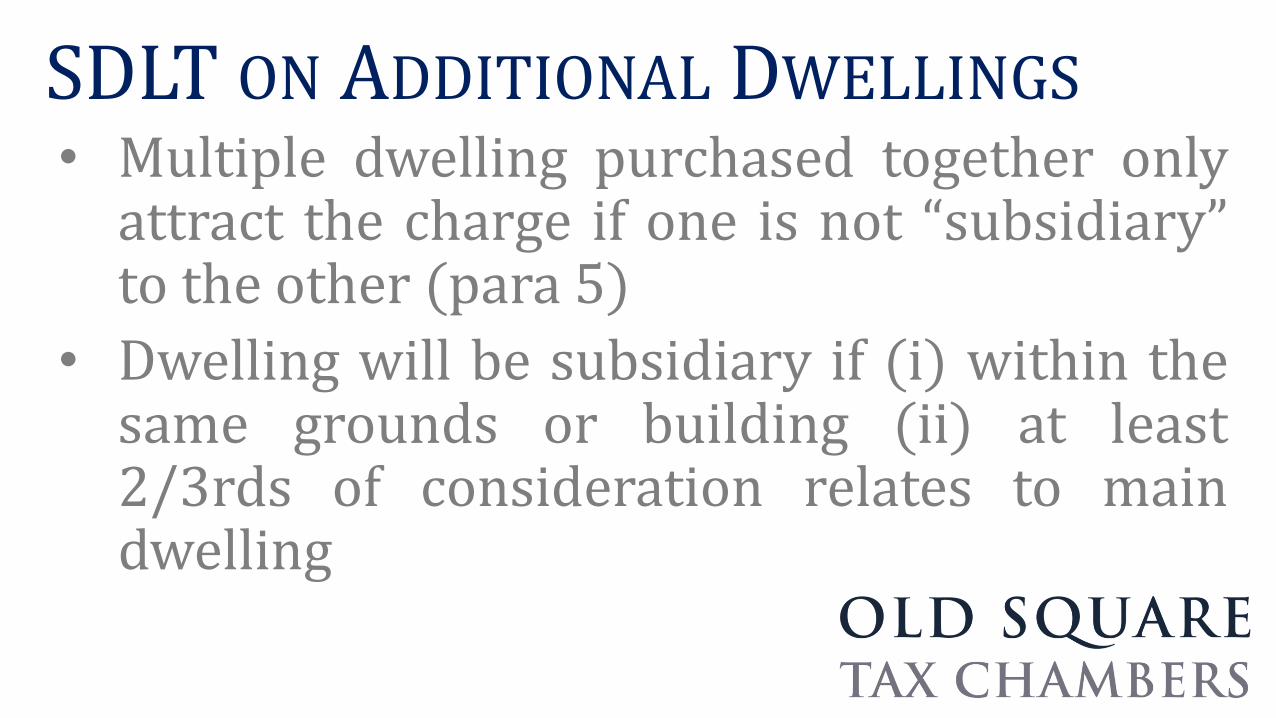

SDLT ON ADDITIONAL DWELLINGS• Multiple dwelling purchased together only

attract the charge if one is not “subsidiary”to the other (para 5)

• Dwelling will be subsidiary if (i) within thesame grounds or building (ii) at least2/3rds of consideration relates to maindwelling

Rory MullanOld Square Tax Chambers

15 Old Square

Lincoln’s Inn

London WC2A 3UE

020 7242 2744

Related Documents