>> 0 >> 1 >> 2 >> 3 >> 4 >> TAXATION OF LLP CA CHANDRASHEKHAR V. CHITALE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

>> 0 >> 1 >> 2 >> 3 >> 4 >>

TAXATION OF LLP

CA CHANDRASHEKHAR V. CHITALE

>> 0 >> 1 >> 2 >> 3 >> 4 >>

TOPICS COVERED1. LLP – BASICS FOR INCOME TAX LAW2. WHY LLP?3. ASSESSMENT OF LLP4. CONVERSION INTO LLP & TAXATION5. DTC, 20106. SUM UP

>> 0 >> 1 >> 2 >> 3 >> 4 >>

L

LLP – BASICS for

INCOME TAX LAW

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Section 2(31) “person” includes—(i) ……., (ii) ……….., (iii) ………,

(iv) Firm, (v) Association of persons orBody of individuals , whether incorporatedor not, (vi) ………, (vii) ……..

TAX IS ON PERSON & RESIDENCE

‘PERSON’ is defined under the Income tax Act, 1961

>> 0 >> 1 >> 2 >> 3 >> 4 >>

SECTION 2(23)(i)• Firm• “firm” shall mean firm as defined

under Indian Partnership Act, 1932 and shall also include within its ambit LLP as defined in in the Limited Liability Partnership Act, 2008.

>> 0 >> 1 >> 2 >> 3 >> 4 >>

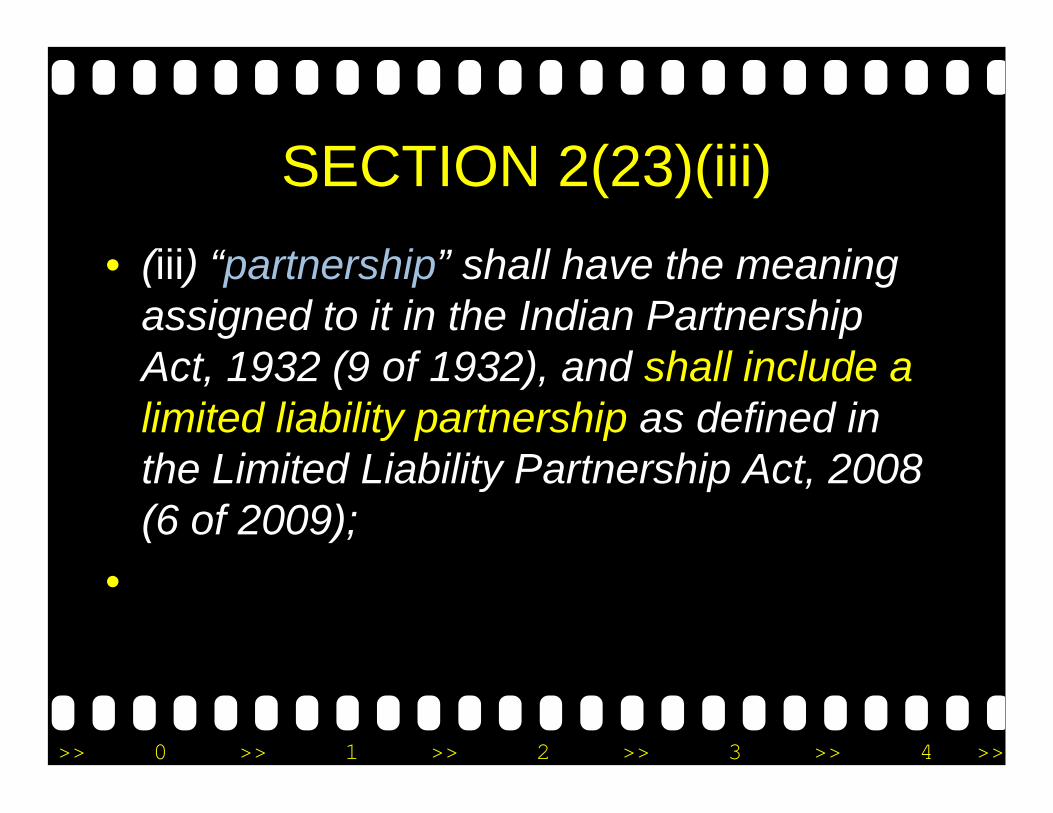

SECTION 2(23)(iii)• (iii) “partnership” shall have the meaning

assigned to it in the Indian Partnership Act, 1932 (9 of 1932), and shall include a limited liability partnership as defined in the Limited Liability Partnership Act, 2008 (6 of 2009);

•

>> 0 >> 1 >> 2 >> 3 >> 4 >>

SECTION 2(23)(i)Implications:• LLP shall be treated separate taxable

entity.• All provisions of IT Act applicable to Firm

are applicable to LLP.

>> 0 >> 1 >> 2 >> 3 >> 4 >>

SECTION 2(23)(i)Implications:• Foreign LLP• Not a LLP as per Indian LLP Act, hence

would not be treated as firm.• May be treated as Company u/s 2(17)(ii)

as a foreign body corporate.

>> 0 >> 1 >> 2 >> 3 >> 4 >>

SECTION 2(23)(ii)• “partner” shall have the meaning assigned to

it in the Indian Partnership Act, 1932 (9 of 1932), and shall include,—

• (a) any person who, being a minor, has been admitted to the benefits of partnership; and

• (b) a partner of a limited liability partnership as defined in the Limited Liability Partnership Act, 2008 (6 of 2009)

•

>> 0 >> 1 >> 2 >> 3 >> 4 >>

SECTION 2(23)(ii)

Implications:• All the provision (except tax

liability) as applicable to partners of firm would also applicable to partner of LLP

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Residential Status• Tax Resident of India unless control and

management of affairs is situated wholly outside India [S.6(2)]

• It would be treated as resident even if control and management of affairs is partly situated in India.

• Meaning of : ‘control and management', ‘affairs’, ‘situated’ and ‘wholly’

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Residential Status• ‘control and management‘ controlling

and directive power, ‘the head and brain’ as it is called. Means de facto control and management and not merely the right or power to control and manage.

• ‘affairs’ must mean affairs which are relevant to the purpose of business

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Residential Status

• ‘situated’ implies the functioning of such power at a particular place with some degree of performance,

• ‘wholly’ would seem to recognise the possibility of the seat of such power being divided between two distinct and separated places.

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Residential StatusCase Law:• CIT v. Nandlal Gandlal [1960] 40 ITR 1 (SC), • CIT V. V.V.R.N.M. Subbiah Chettiar [1947]

15 ITR 502 (Mad.) & [1951] 19 ITR 168 (SC),• B R Naik V. CIT [1945] 13 ITR 124 (Bom.)

>> 0 >> 1 >> 2 >> 3 >> 4 >>

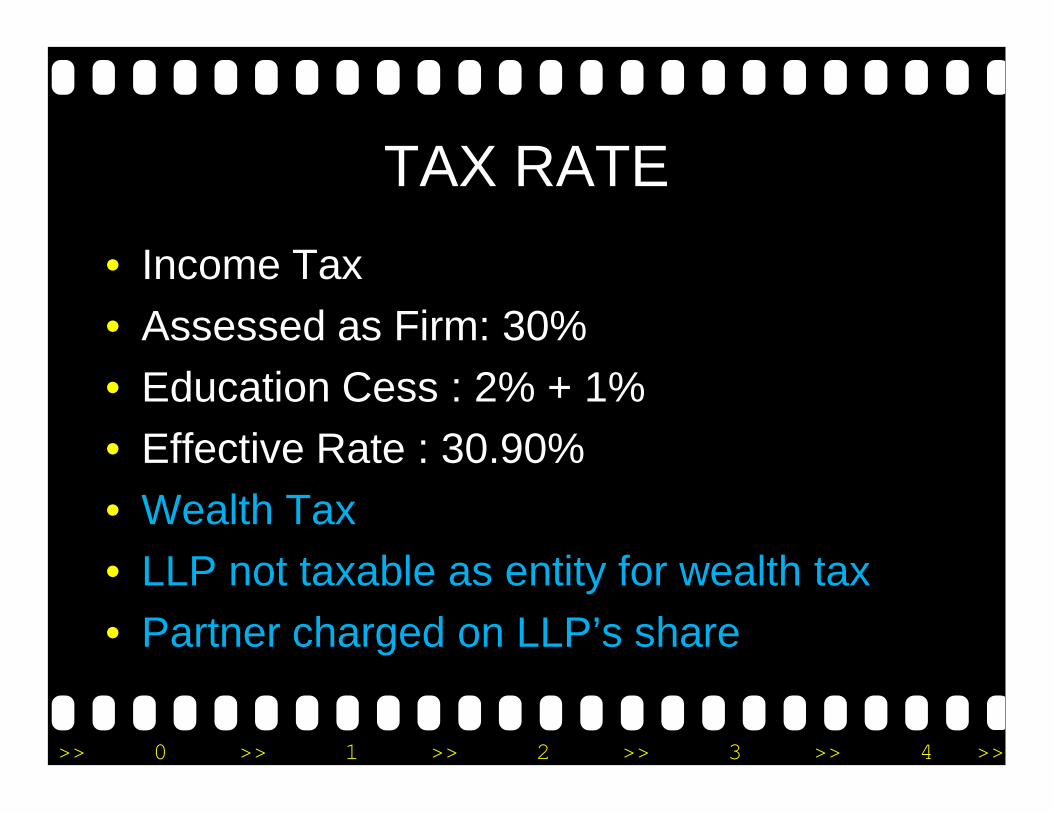

TAX RATE• Income Tax• Assessed as Firm: 30%• Education Cess : 2% + 1%• Effective Rate : 30.90%• Wealth Tax• LLP not taxable as entity for wealth tax• Partner charged on LLP’s share

>> 0 >> 1 >> 2 >> 3 >> 4 >>

L

WHY LLP?

>> 0 >> 1 >> 2 >> 3 >> 4 >>

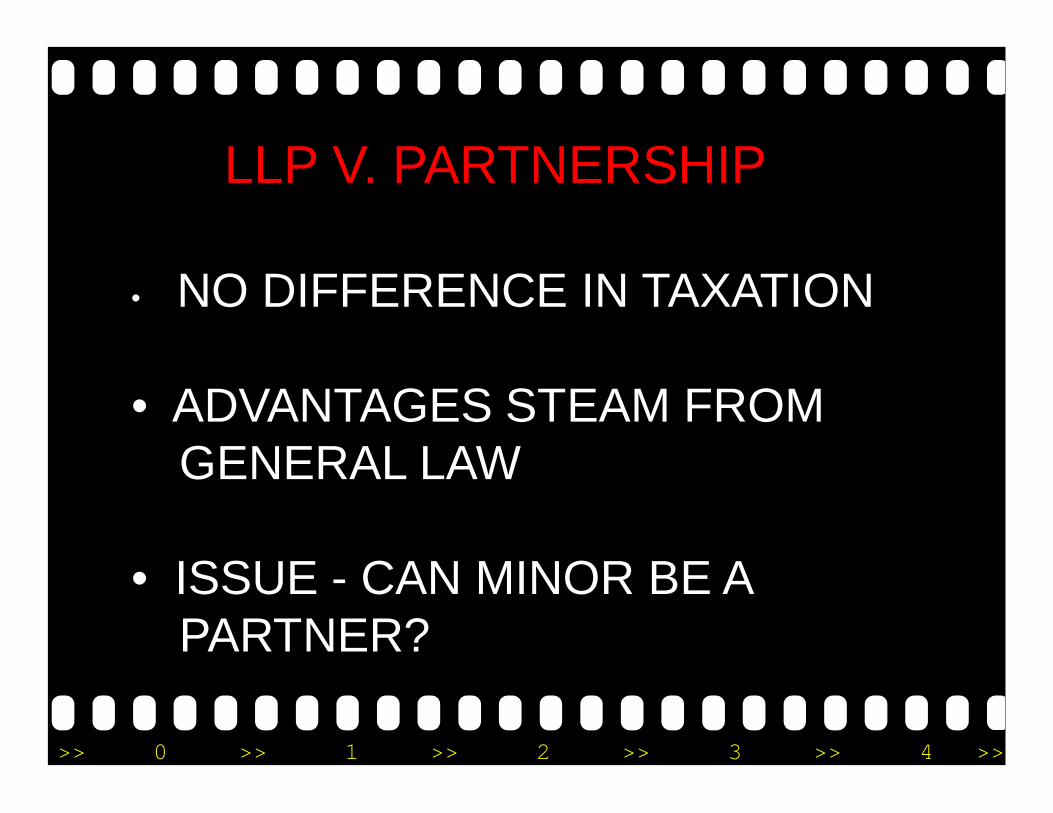

LLP V. PARTNERSHIP

• NO DIFFERENCE IN TAXATION

• ADVANTAGES STEAM FROM GENERAL LAW

• ISSUE - CAN MINOR BE A PARTNER?

>> 0 >> 1 >> 2 >> 3 >> 4 >>

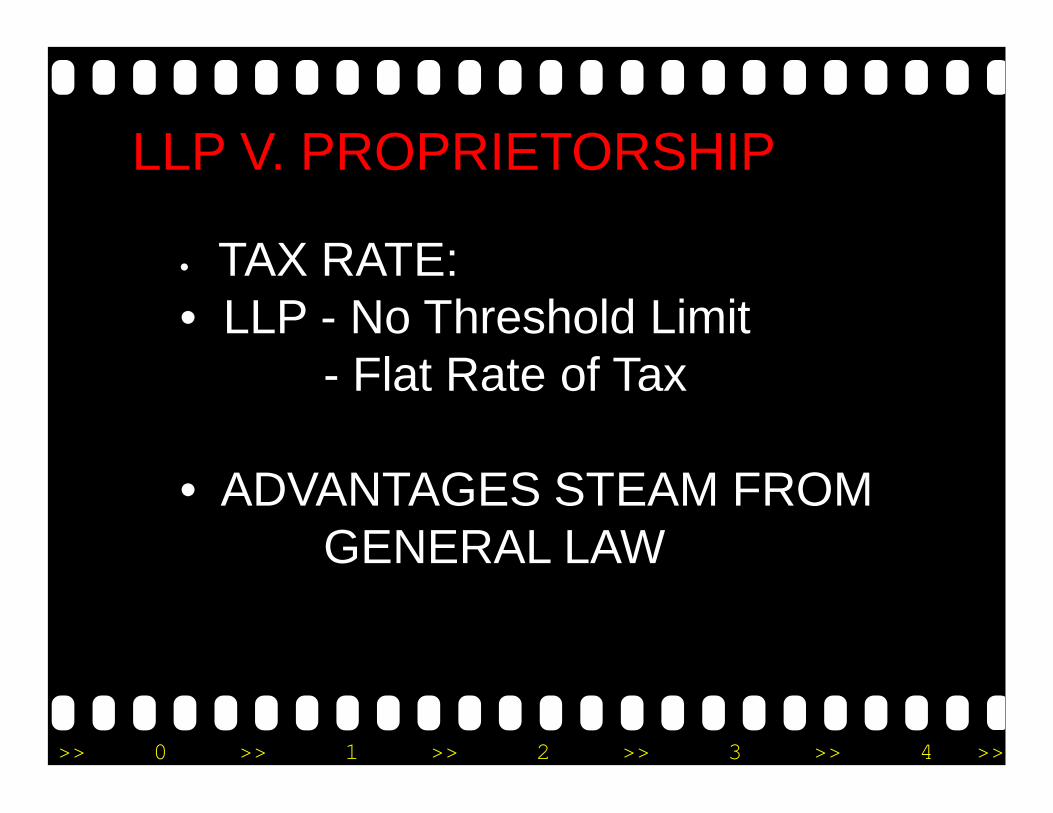

LLP V. PROPRIETORSHIP

• TAX RATE:• LLP - No Threshold Limit

- Flat Rate of Tax

• ADVANTAGES STEAM FROM GENERAL LAW

>> 0 >> 1 >> 2 >> 3 >> 4 >>

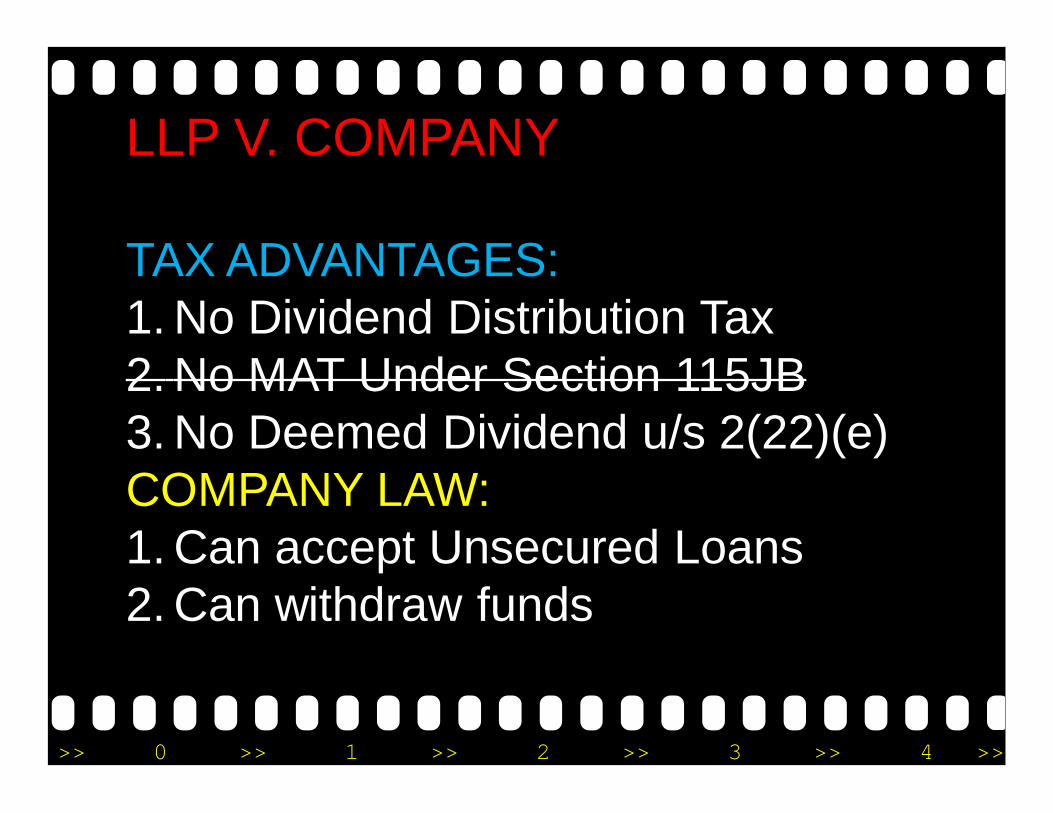

LLP V. COMPANY

TAX ADVANTAGES:1. No Dividend Distribution Tax2. No MAT Under Section 115JB3. No Deemed Dividend u/s 2(22)(e)COMPANY LAW:1. Can accept Unsecured Loans2. Can withdraw funds

>> 0 >> 1 >> 2 >> 3 >> 4 >>

L

ASSESSMENT0f

LLP

>> 0 >> 1 >> 2 >> 3 >> 4 >>

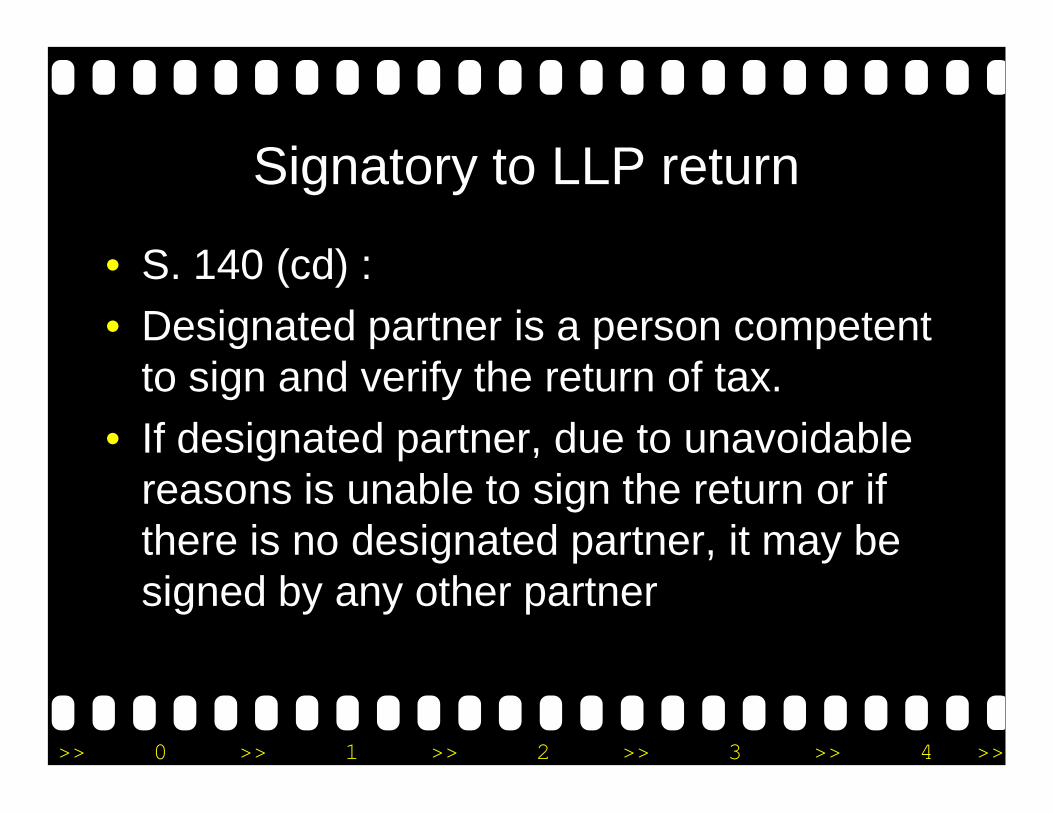

Signatory to LLP return

• S. 140 (cd) :• Designated partner is a person competent

to sign and verify the return of tax.• If designated partner, due to unavoidable

reasons is unable to sign the return or if there is no designated partner, it may be signed by any other partner

>> 0 >> 1 >> 2 >> 3 >> 4 >>

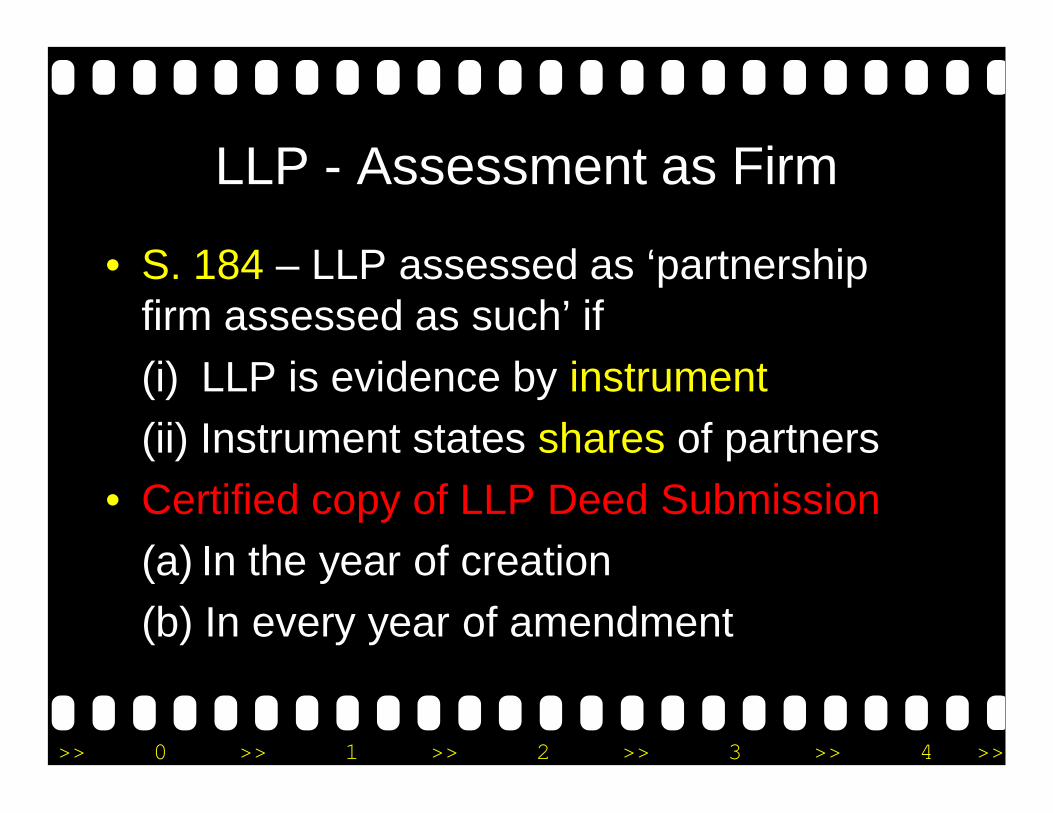

LLP - Assessment as Firm

• S. 184 – LLP assessed as ‘partnership firm assessed as such’ if(i) LLP is evidence by instrument(ii) Instrument states shares of partners

• Certified copy of LLP Deed Submission(a) In the year of creation(b) In every year of amendment

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Non Compliance of Sec. 184• If provisions of Section 184 are not

complied, then :• For LLP - No deduction for

(i) Partner’s salary, (ii) Interest on Capital• For Partners –

Salary and Interest – Not taxable

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Assessment u/s Sec. 144• If LLP is assessed u/s 144, then :• For LLP - No deduction for

(i) Partner’s salary, (ii) Interest on Capital• For Partners –

Salary and Interest – Not taxable

>> 0 >> 1 >> 2 >> 3 >> 4 >>

PARTNER’S REMUNERATION

• PAYMENT TO WORKING PARTNERS• Partner – Working V. Designated• Working partner can be designated

partner as well as non designated partner

>> 0 >> 1 >> 2 >> 3 >> 4 >>

PARTNER’S REMUNERATION

Provisions S 40A• Ref. Syntholab Chemicals & Research v

ACIT[2008] 172 Taxman 38 (Mum.) (Mag.)• Remuneration to nominee who act as

a designated partner• Whether such nominee is partner ?• S. 40(b)(v) v/s S.37 (1)

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Interest on partners capital

• S.36(1)(iii) – Interest• Capital contribution of partners are capital

borrowed for the purposes of business and profession and for allowance of deduction of interest payments, requirement of s.36(1)(iii) need to fulfill

• Ref. Munjal Sales corp. vs CIT [2008] 298 ITR 298 (SC)

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Interest on partners capital

• S.40(b)(iv) – Restrictions• LLP agreement to provide allowance of

such interest to partner• Maximum interest rate - 12% p.a. simple• Interest on capital balance after reducing

withdrawals• Ref. Architectural Associates v. A CIT [2005]

277 ITR (AT) 35.

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Interest on partners capital• Increase in credit balance of bank

account due to revaluation of assets• Ref ACIT v Sant Shoe Store [2004] 88 ITD 524

(Cha), ITO v. Amar Garage[2004] I SOT 331 (Kol)

• S. 36(1)(iii) v/s 40(b)• S. 40(b) is collolry to section 30 to 38• S. 40(b)(iv) only restricts the deductibility

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Issues• Implication under e – filling of tax

returns?• Non submission of certified copy of

partnership along with return of income is a procedural default which can be cured during the course of assessment proceedings – New Ajantha Road Lines v. ITO [2002] 254 ITR (AT) 85 (Jab.)

>> 0 >> 1 >> 2 >> 3 >> 4 >>

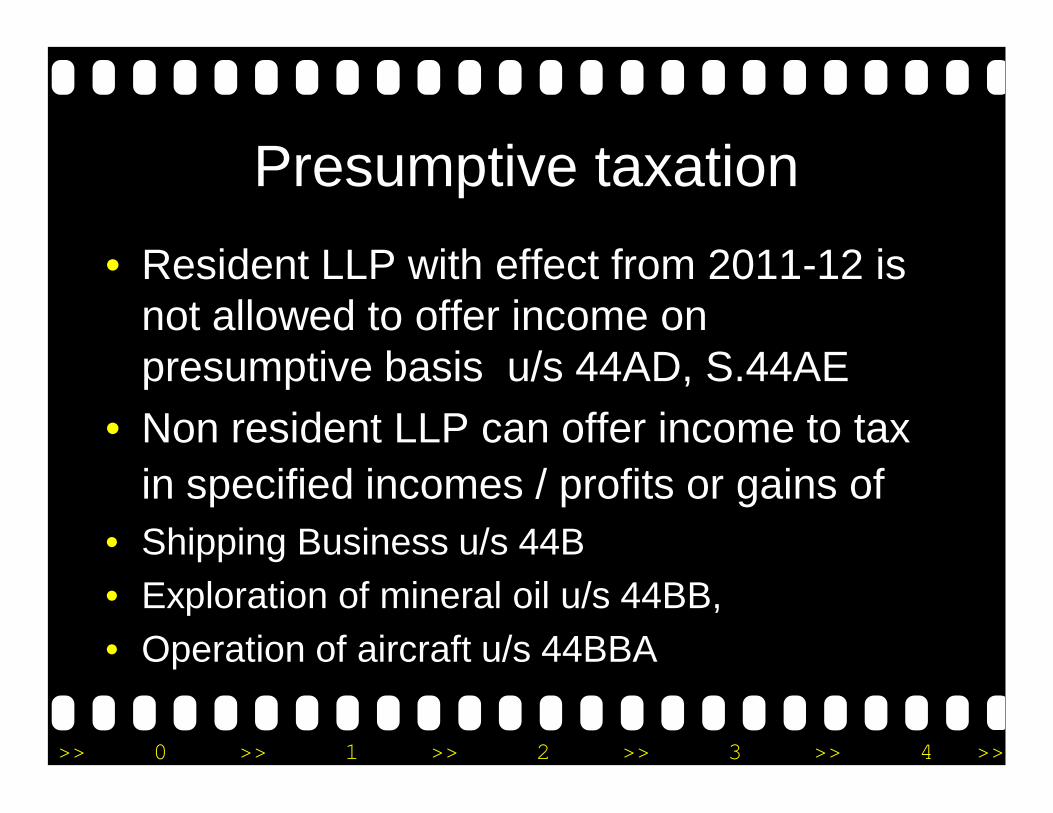

Presumptive taxation

• Income-tax Act provides • Certain types of income earned by resident SME can be

offered to tax on presumptive basis.• Certain business operation of non-resident may also

offer income on presumptive basis.• In case income is offered on presumptive basis

assessee is exempt from fulfilling certain requirements of IT Act eg maintenance of books of accounts

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Presumptive taxation• Resident LLP with effect from 2011-12 is

not allowed to offer income on presumptive basis u/s 44AD, S.44AE

• Non resident LLP can offer income to tax in specified incomes / profits or gains of

• Shipping Business u/s 44B• Exploration of mineral oil u/s 44BB,• Operation of aircraft u/s 44BBA

>> 0 >> 1 >> 2 >> 3 >> 4 >>

L

Transactions With

Partners

>> 0 >> 1 >> 2 >> 3 >> 4 >>

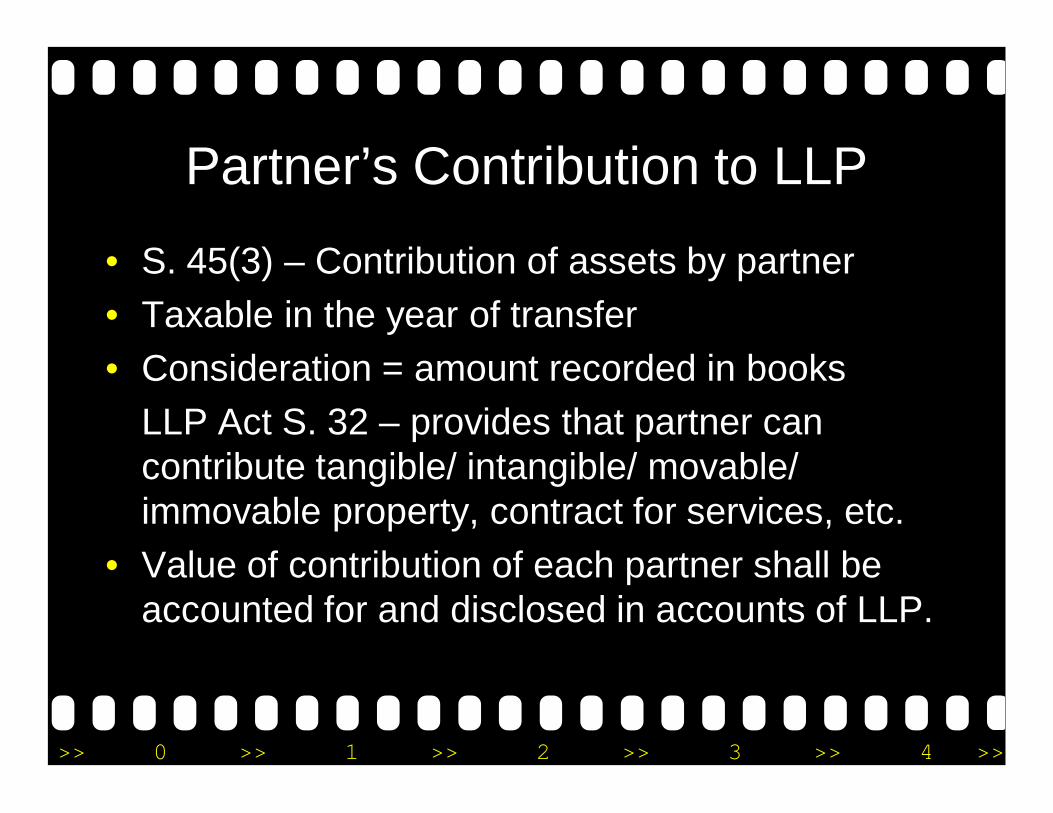

Partner’s Contribution to LLP

• S. 45(3) – Contribution of assets by partner • Taxable in the year of transfer • Consideration = amount recorded in books

LLP Act S. 32 – provides that partner can contribute tangible/ intangible/ movable/ immovable property, contract for services, etc.

• Value of contribution of each partner shall be accounted for and disclosed in accounts of LLP.

>> 0 >> 1 >> 2 >> 3 >> 4 >>

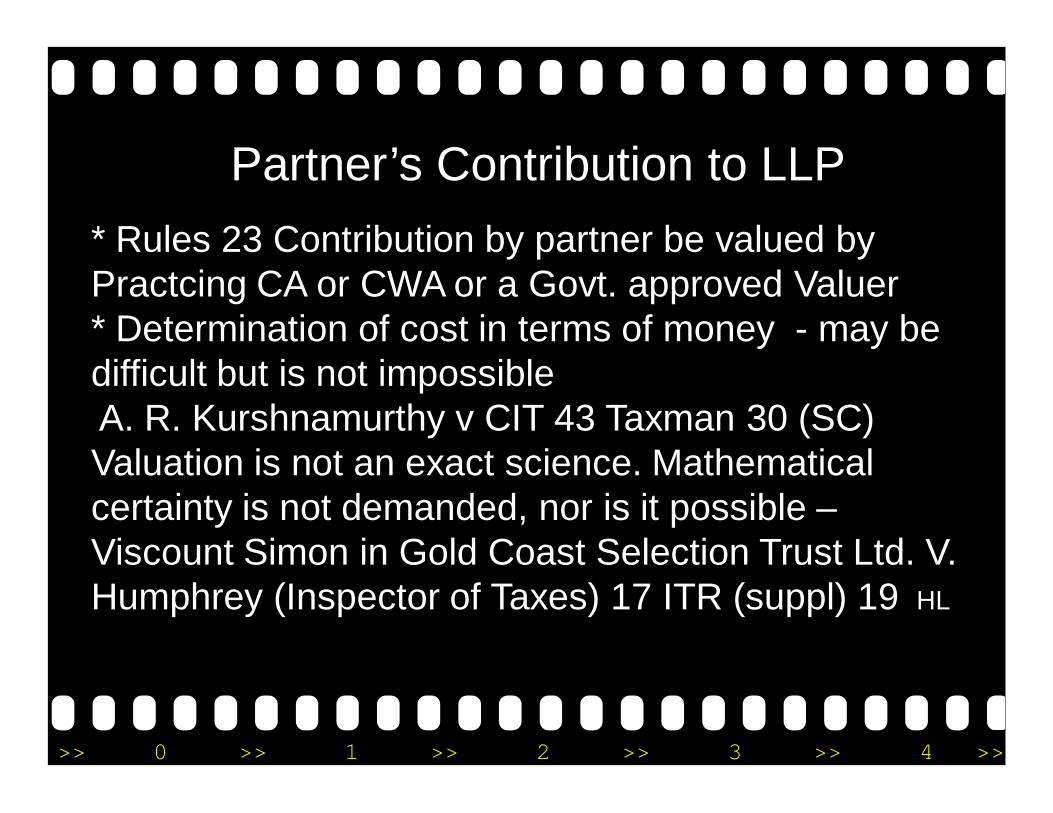

* Rules 23 Contribution by partner be valued by Practcing CA or CWA or a Govt. approved Valuer* Determination of cost in terms of money - may be difficult but is not impossible A. R. Kurshnamurthy v CIT 43 Taxman 30 (SC)Valuation is not an exact science. Mathematical certainty is not demanded, nor is it possible –Viscount Simon in Gold Coast Selection Trust Ltd. V. Humphrey (Inspector of Taxes) 17 ITR (suppl) 19 HL

Partner’s Contribution to LLP

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Distribution of Assets by LLP

• S. 45(4) – Distribution of capital asset by firm to partner on dissolution of firm or otherwise

• Chargeable to tax in the year of transfer• Consideration : FMV of Asset on date of transfer

• S. 63 of LLP Act - Winding up of an LLP• Distribution of assets of the LLP on wound up provision

>> 0 >> 1 >> 2 >> 3 >> 4 >>

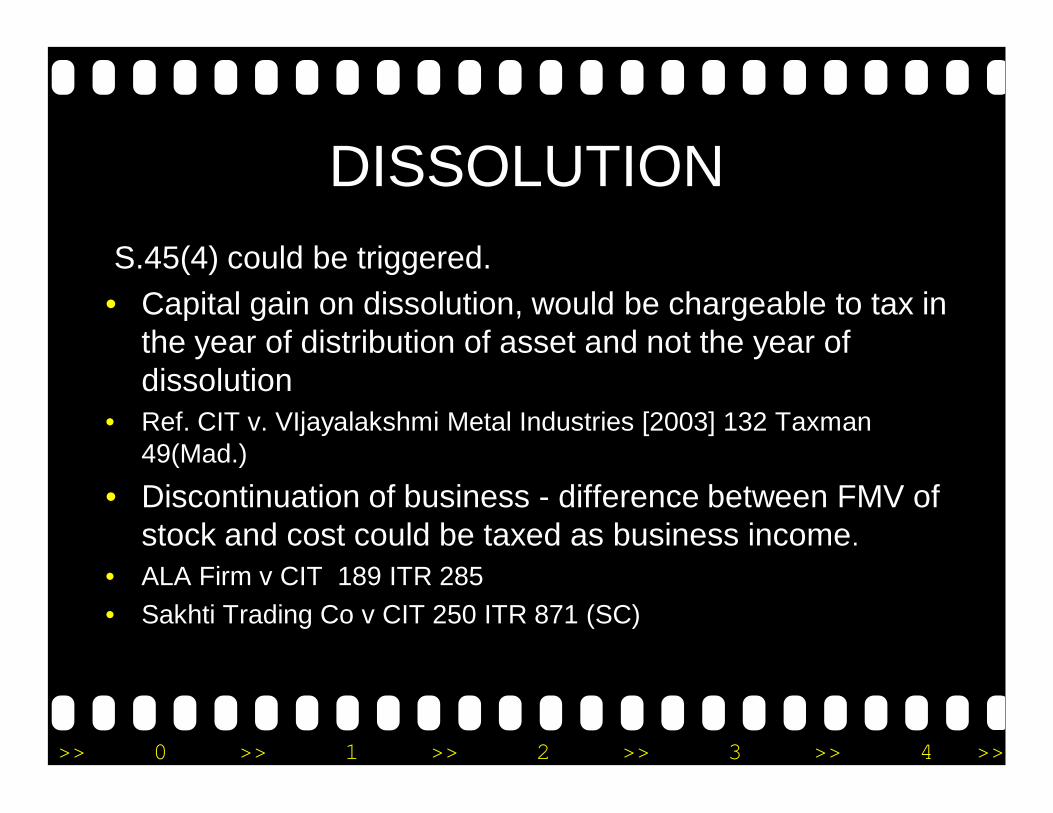

DISSOLUTIONS.45(4) could be triggered.• Capital gain on dissolution, would be chargeable to tax in

the year of distribution of asset and not the year of dissolution

• Ref. CIT v. VIjayalakshmi Metal Industries [2003] 132 Taxman 49(Mad.)

• Discontinuation of business - difference between FMV of stock and cost could be taxed as business income.

• ALA Firm v CIT 189 ITR 285• Sakhti Trading Co v CIT 250 ITR 871 (SC)

>> 0 >> 1 >> 2 >> 3 >> 4 >>

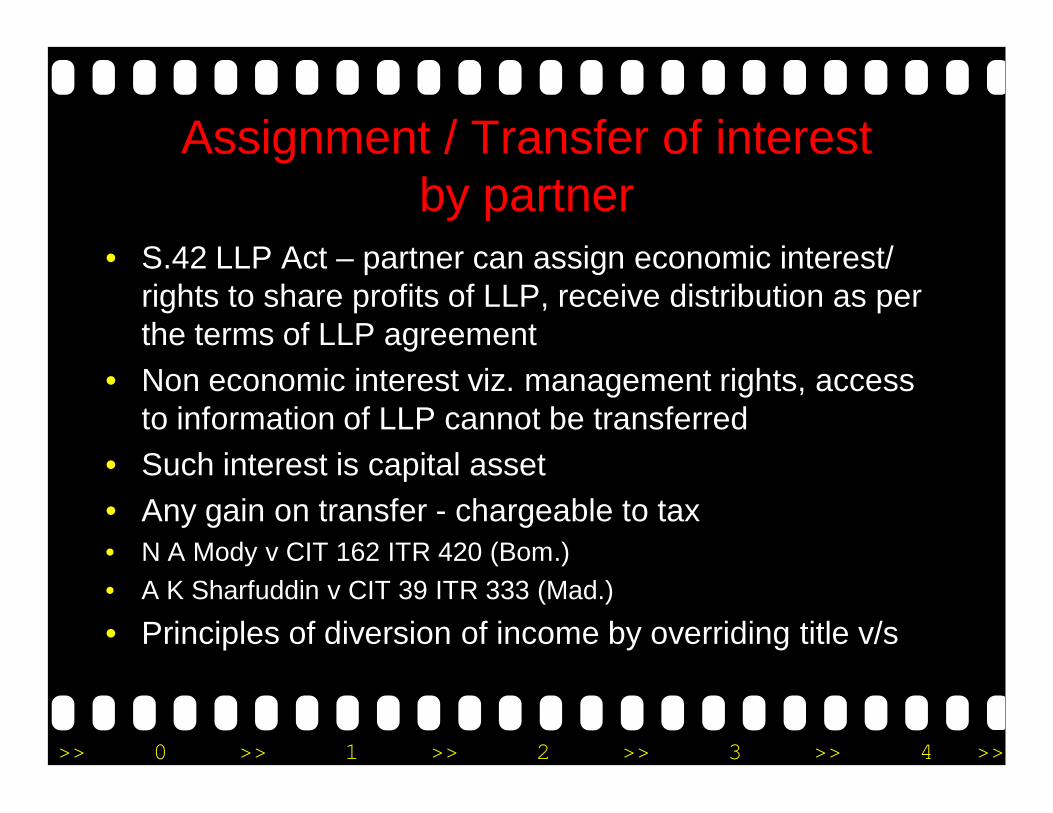

Assignment / Transfer of interest by partner

• S.42 LLP Act – partner can assign economic interest/ rights to share profits of LLP, receive distribution as per the terms of LLP agreement

• Non economic interest viz. management rights, access to information of LLP cannot be transferred

• Such interest is capital asset • Any gain on transfer - chargeable to tax • N A Mody v CIT 162 ITR 420 (Bom.) • A K Sharfuddin v CIT 39 ITR 333 (Mad.)

• Principles of diversion of income by overriding title v/s

>> 0 >> 1 >> 2 >> 3 >> 4 >>

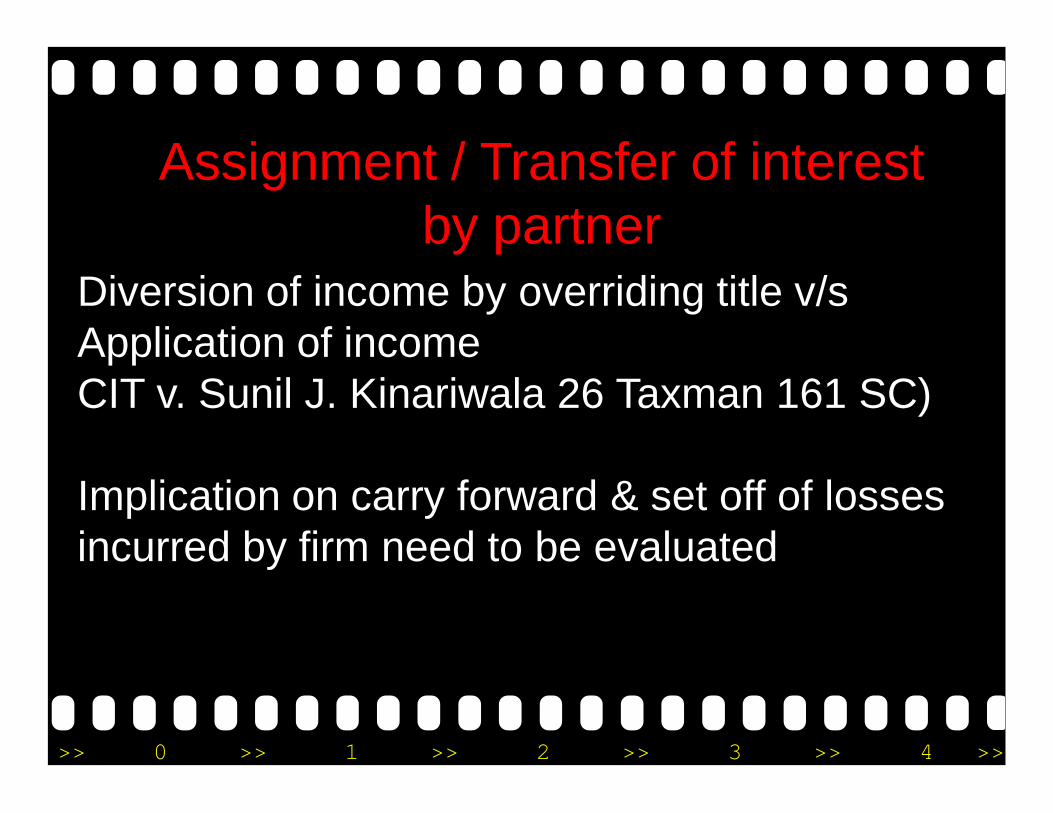

Diversion of income by overriding title v/sApplication of income CIT v. Sunil J. Kinariwala 26 Taxman 161 SC)

Implication on carry forward & set off of losses incurred by firm need to be evaluated

Assignment / Transfer of interest by partner

>> 0 >> 1 >> 2 >> 3 >> 4 >>

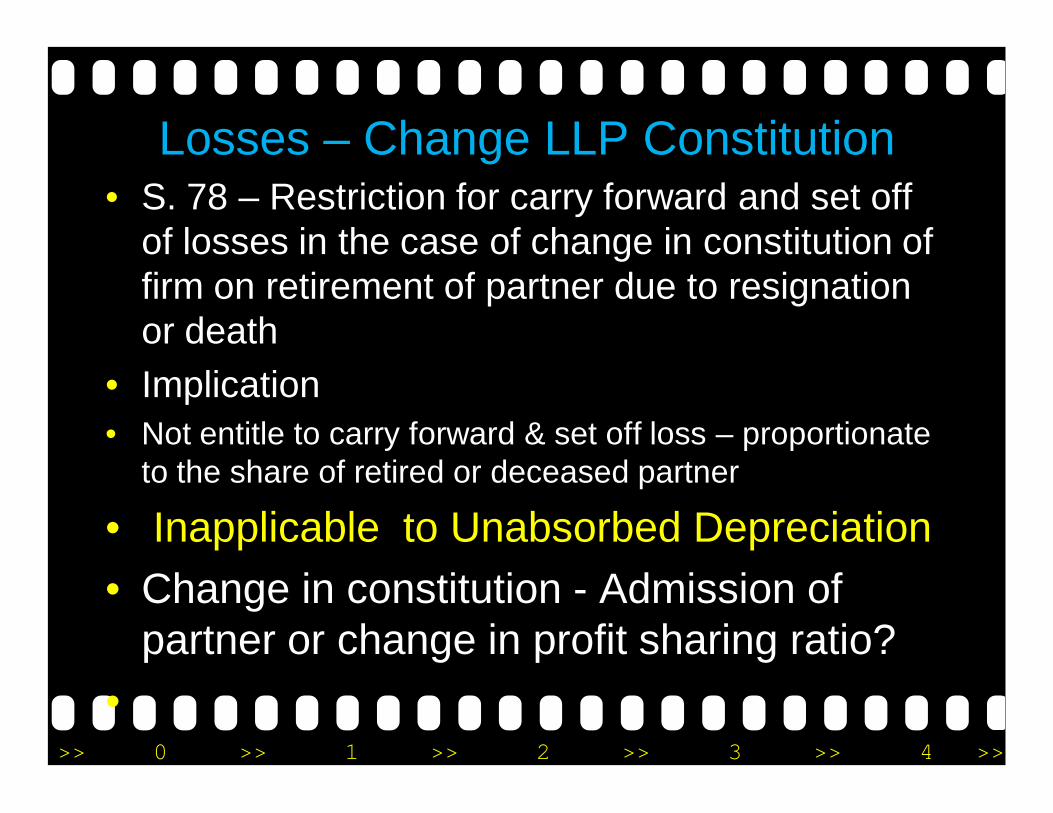

Losses – Change LLP Constitution• S. 78 – Restriction for carry forward and set off

of losses in the case of change in constitution of firm on retirement of partner due to resignation or death

• Implication• Not entitle to carry forward & set off loss – proportionate

to the share of retired or deceased partner

• Inapplicable to Unabsorbed Depreciation• Change in constitution - Admission of

partner or change in profit sharing ratio?•

>> 0 >> 1 >> 2 >> 3 >> 4 >>

L

CONVERSION into LLP

& TAXATION

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Conversions of private or unlisted public co Tax neutral - Finance Act, 2010Conditions to be complied for claiming tax neutrality at the time of conversionWhether all conditions are cumulative and need to be complied?

TAX NEUTRAL

>> 0 >> 1 >> 2 >> 3 >> 4 >>

No amount to be paid either directly or indirectly to any partner out of accumulated profits standing in the accounts of the company for the period of 3 years from the date of conversion Accumulated profit not definedCurrent years profits till date conversion include or excluded

CONDITION

>> 0 >> 1 >> 2 >> 3 >> 4 >>

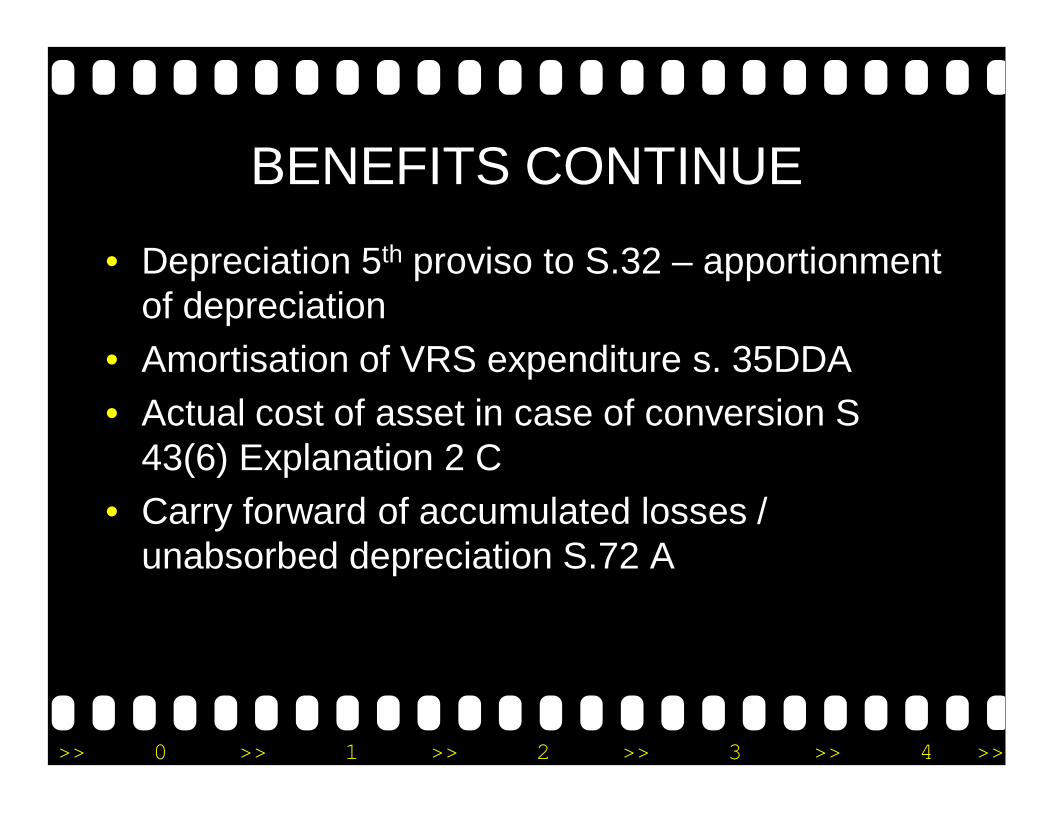

BENEFITS CONTINUE

• Depreciation 5th proviso to S.32 – apportionment of depreciation

• Amortisation of VRS expenditure s. 35DDA • Actual cost of asset in case of conversion S

43(6) Explanation 2 C• Carry forward of accumulated losses /

unabsorbed depreciation S.72 A

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Shareholders taxability • S. 47 (xiib) also provides that any transfer of shares held

by shareholders in the company involved in conversion of LLP will not to be regarded as transfer of fulfillment of specified conditions

• Applicable to both Equity and Preference shares

• Further s 49 (2AAA) provided cost of share in LLP period of holding of shares in company will all be reckoned

• Implication in case specified conditions not fulfilled?

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Conversion of LLP

• No explicit provisions under LLP Act or Other law for conversion LLP to other business entity

• In order to convert into any other form of entity such LLP may be required to wound upAnd assets to be distributed in the hands of partner who may form another entity

• No tax neutrality provisions on conversions of LLP to such other business entities

>> 0 >> 1 >> 2 >> 3 >> 4 >>

L

LLP – TAXATIONSUM UP

>> 0 >> 1 >> 2 >> 3 >> 4 >>

• LLP affords • Administrative simplicity• Operational flexibility• and• Tax advantages• Therefore, coming decade will see this

entity flooding business scean

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Thank you!

>> 0 >> 1 >> 2 >> 3 >> 4 >>

Any questions?

Related Documents