* * I PO 135 THE WORLD BANK Internal Discussion Paper SOUTH ASIA REGION Report No. IDP-135 Taxation of Foreign Investment in South Asia Jack Mintz and Thomas Tsiopoulos December 1993 Office of the Chief Economist SASVP The views presented here are those of the author, and they should not be interpreted as reflecting those of the World Bank. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

* * I PO 135THE WORLD BANK

Internal Discussion Paper

SOUTH ASIA REGION

Report No. IDP-135

Taxation of Foreign Investmentin South Asia

Jack Mintz and Thomas Tsiopoulos

December 1993

Office of the Chief Economist SASVP

The views presented here are those of the author, and they should not be interpreted as reflecting those of the World Bank.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

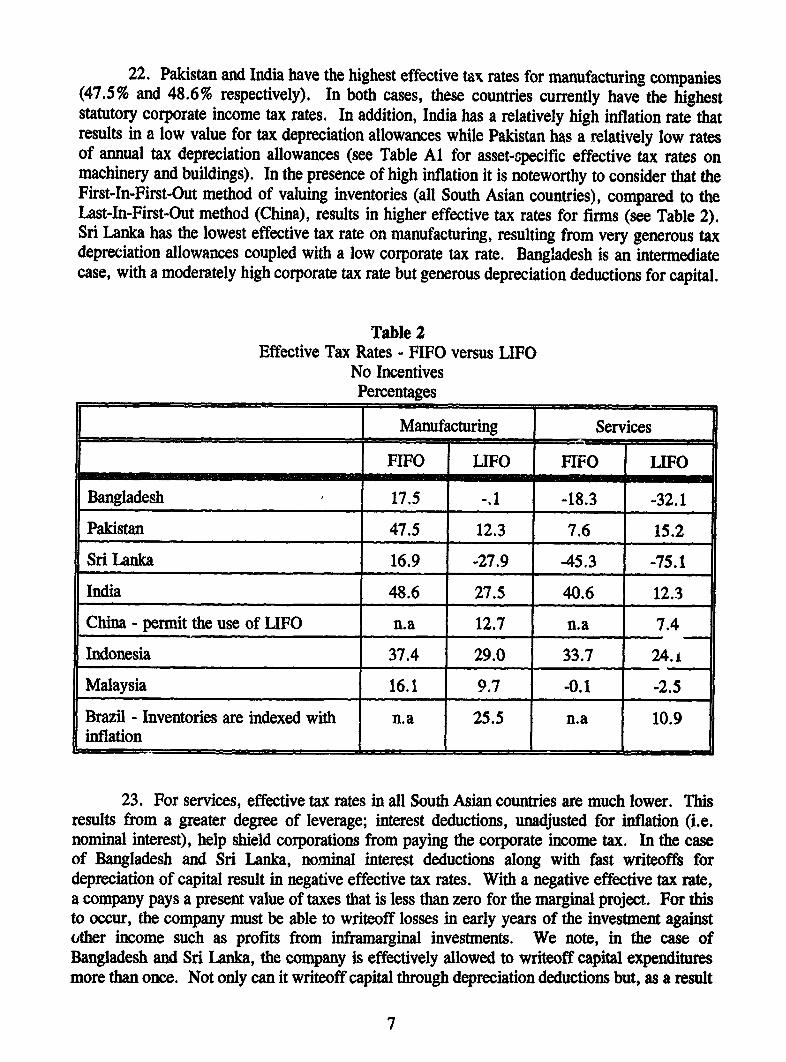

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

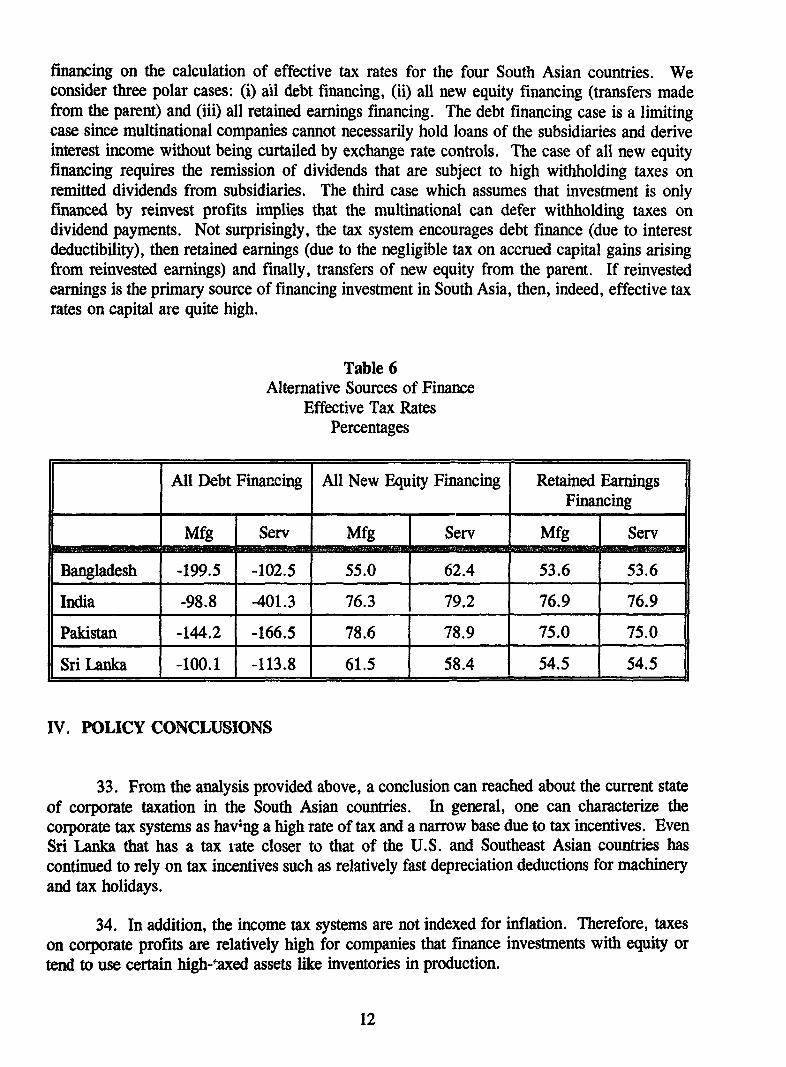

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

SOUTH ASIA REIOAL_SERIES

]]ide Autho9. 2Ml OrdainatorI~b~

IDP1 11 How Composition of Public ExpenditureAffects Competitiveness: The Case ofBangladesh K. Matin March 1992 P. Mitra (80419)

IDP1 21 Labor Retrenchment and RedundancyCompensation in State Owned Enterprises:The Case of Sri Lanka A. Fiszbein December 1992 G. Nankani (84641)

IDP1 28 Some Guidelines for the Appraisal ofLarge Projects W. Jack February 1993 A. Estache (81442)

IDP109 Reforming Higher Secondary Education inIn South Asia: The Case of Nepal H. Abadzi May 1993 H. Abadal (80375)

IDP1 27 Some Lessons for South Asia fromDeveloping Country Experience withForeign Direct Investment M. Fry June 1993 A. Estache (81442)

IDPI29 Ouasi-Fisoal Deficits: Latin AmericanLessons for South Asia C. A. Rodriguez August 1993 A. Estache (81442)

IDP1 31 The Impact of Rural Infrastructure onRural Poverty: Lessons for South Asia E. Goldstein June 1993 G. Nankani (84641)

IDP134 Infrastructure and Industrial Policy inSouth Asia: Achieving the Transition toa New Regulatory Environment P. Seabright December 1993 A. Estohe (81442)

IDPI 35 Taxation of Foreign Investment in South Asia J. MintzT. Telopoulos December 1993 A. Estache (81442)

TAXATION OF FOREIGN INVESTMENT

IN SOUTH ASIA

Jack M. Mintz and Thomas Tsiopoulos

University of Toronto

June 1993

We would like to thank Pedro Alba, Orsalia Kalantzopoulos, Samuel Otoo, Shekhar Shah andAntonio Estache for their helpful comments and suggestions.

TABLE OF CONTENTS

I. Introduction ............................................ 1

II. Background ............................................ 3a) Corporate Tax Rates ................................... 3b) Depreciation Allowances ................................ 4c) Inventory Costs ...................................... 4d) Tax Holidays ....................................... 4e) W ithholdingTaxes .................................... 5f) Comparisons to OtherCountries............................ 5

M . Tax Competitiveness of SouthAsia.............................. 6

IV. Policy Conclusions....................................... 12

V. Bibliography .......................................... 15

VI. Appendix ........................................... 16

List of Tables

Table 1: Effective Tax Rates - No Incentives Percentages .................. 6

Table 2: Effective Tax Rates - FIFO Versus LIFO ...................... 7

Table 3: Effective Tax Rates - Various Incentives Percentages ............... 8

Table 4: Effective Tax Rates - Various Debt/Asset Ratios ................. 10

Table 5: Effective Tax Rates - Various Inflation Rates ................... 11I

Table 6: Alternative Sources of Finance - Effective Tax Rate Percentages ....... 12

Table Al: No Incentives/ByAsset ................................ 23

Table A2: Effective Tax Rates - Alternative Real Interest Rates Percentages ...... 23

Table A3: Summary ofInputs................................... 24

TAXATION OF FOREIGN INVESTMENTIN SOUTH ASIA

I. INTRODUCTION

1. Taxation is one of several key determinants which affect the profitability of foreigninvestment in a country. Similar to many other countries throughout the world, South Asiannations have been concerned about how their tax as well as regulatory policies affect theircompetitiveness in attracting foreign capital. Recently, many developing countries have takena more positive attitude towards foreign investment since it can contiibute to increasedproductivity of their domestic industries. After all, with foreign direct investment, countries notonly obtain new sources of capital but also competent management for private sector production.

2. The purpose of this report is to consider how four South Asian economies -Bangladesh, India, Pakistan and Sri Lanka - compare amongst themselves and other developingcountries with respect to their corporate tax policies that affect foreign direct investment. Forthese four countries, we examine the effect of the corporate income tax and non-residentwithholding taxes on the profitability of foreign investments for typical manufacturing andservice investments.' We wish to determine whether tax burdens on foreign investment isgreater or lower than that found in competing countries seeking foreign investment. Thecountries that are considered as competitors are China, Indonesia, Malaysia and Brazil.

3. As any astute investor knows, the effect of corporate taxation on the investment'sprofitability depends on more than just the corporate income tax rate that is assessed by agovernment. Other provisions of the tax code such as deductions for depreciation, inventory andinterest costs affect the degree to which capital is taxed. Moreover, governments may use taxincentives such as tax holidays, accelerated depreciation and investment tax credits to furtherencourage investment.

4. To capture all the effects of the corporate income and withholding taxes on capital,we measure a summary statistic called the effective tax rate on capital'. The effective tax rate

1 Data on manufacturing and service projects were obtained from World Bank project information gathered by theForeign Investment Advisory Service of the International Finance Corporation.

2 Effective tax rate calculations began with King and Fullerton [19841 and Boadway, Bruce and Mintz [19841. Adifferent methodology is employed by David Dunn and Anthony Pellechio [19901. In their methodology, they fix agross-of-corporate and personal tax rate of return (20%) on capital for a project that operates ten years in measuring theeffective tax rate. Although their methodology is called "marginal effective tax rate" analysis, it is only so for a specificcase of financial arbitrage assumed in their analysis: "fixed-p" in King and Fullerton [1984] terminology. This caseassumes that all assets earn the same gross-of-tax rate of return (implying that assets like buildings and machinery areperfect substitutes in production). It would not be possible to use their methodology if another financial arbitragecondition was used to calculate effective tax rates. For example, if a financial arbitrage was assumed in which acompany is indifferent between issuing bonds and equity claims in markets, a fixed gross-of-tax rate of return on capital

is the percentage of tax paid on profits generated by marginal investments that earn a net-of-taxrate of return on capital just sufficient to compensate owners for the opportunity cost of theirsavings. For example, suppose an investment in South Asia earns a risk-adjusted rate of returnon capital equal to 15% and pays corporate and withholding taxes equal to 33% of gross profits.The net-of-tax rate of return to capital would, therefore, be 10%. If 10% is also the risk-adjusted rate of return on capital that is available to owners who can invest in alternativeopportunities throughout the world, then the investment in South Asia is just profitable for theinvestors. Any lower net-of-tax rate of return on capital would be insufficient to attractinvestments since the investors can find a better opportunity elsewhere.

5. The effective tax rate that is calculated below for foreign investment in South Asiaassumes that the investment earns a risk-adjusted net-of-tax rate of return equal to that found inthe United States and other countries. In the calculations below, we ignore other taxes that canimpinge on the return to capital such as property taxes, excise taxes and tariffs on capital goodsand capital asset taxes. Only the corporate income tax and non-resident withholding taxes areincluded in the calculations.' We also assume that the investment made in South Asia originatesfrom the United States. The U.S. multinational only pays corporate income and withholdingtaxes to the host country; no tax is paid to the U.S. government on remitted income.4

6. In the next section, we discuss some of the details of the corporate taxes found in thefour South Asian countries considered in this report. In Section III, we examine the taxcompetitiveness of the four countries and in Section IV conclude with some observations aboutcurrent corporate tax policy found in the four South Asian countries.

is not an appropriate capital market equilibrium. Instead, interest rates on bonds and equity would be determined byfinancial markets: gross-of-tax rates of return on specific assets would vary according to tax provisions. Moreover, anytax policy changes would cause the gross-of-tax rate of return on assets to adjust since, in equilibrium, firms invest incapital until the gross-of-tax rate of return on capital is equal to the cost of capital adjusted for taxes. For foreign directinvestment, the open economy assumption is more appropriate which would imply that interest rates on financial claimsissued by multinationals would be determined by international markets. This would imply that the corporate income taxprovisions in a particular host country is relevant to investment decisions; personal tax provisions in a host country wouldhave no influence on the cost of capital for the multinational. Our modelling is based on these arbitrage assumptions.For a discussion of financial arbitrage and implications for effective tax rate analysis, see Boadway [19871.

3 In a recent piece, we have included all taxes that affect the investment decision. See Jack Mintz and ThomasTsiopoulos, "Latin American Taxation of Foreign Direct Investment in a Global Economy", prepared for the ForeignInvestment Advisory Service of the World Bank, manuscript, 1993.

4 This situation is referred to as the "excess foreign tax credit" case. Under U.S. law, a multinational can creditqualifying foreign corporate and withholding taxes deemed to be paid against U.S. tax liabilities on remitted income,subject to certain restrictions. If foreign taxes are more than U.S. tax, no U.S. tax is paid; excess credits can be carriedback or carried forward for a limited number years. It is assumed that the U.S. parent has so much excess credit thatit never pays U.S. tax on remitted income. For an analysis of taxation for the so-called "deficient tax credit" case, seeChad Leechor and Jack Mintz 11993].

2

II. BACKGROUND

7. Corporate tax policies in South Asia are undergoing reform or being considered forreform, following recent worldwide trends. The aim of the tax reforms is to improve theefficiency of the tax system. Each country has implemented or is considering theimplementation of tax policies that would reduce tax rates and broaden, at least to some degree,the tax base by curtailing tax incentives. Of the four countries, Sri Lanka has progressed thefastest with its reforms while India has been slowest in adopting any changes. Bangladesh hasmade only modest changes and Pakistan has only just begun implementing several importantchanges to its tax code.s However, even in the case of Sri Lanka, significant reforms aimedat reducing tax rates and broadening the tax base has not been achieved. In particular, taxholidays remain in all four South Asian countries despite severe disadvantages that arise withsuch tax incentives, as to be discussed in more detail below.

8. We briefly summarize the corporate tax systems found in Bangladesh, India, Pakistanand Sri Lanka as follows (see Table A3 in the Appendix for a summary of tax and otherinformation used for analysis):

a. Corporate Tax Rates:

9. Similar to many developing countries, the four South Asian countries use a dual ratecorporate tax whereby private companies are taxed at a rate, usually 5%, more than that appliedto public companies with a significant degree of domestic and dispersed ownership'. Foreigncompanies usually prefer majority, if not full, ownership of subsidiaries operating in a hostcountry. Thus, to a large extent, the foreign companies operate as private companies preferringto pay extra taxes rather than giving up control by becoming a public corporation. In ouranalysis below, we assume that the private corporate tax rate is the regular tax rate faced byU.S. multinationals in each of the countries.

10. In general, the corporate tax rates for private companies in the South Asiancountries, except Sri Lanka, are relatively high by world standards. For example, compared toa U.S. rate of 34% (38% including U.S. state corporate income taxes), India's corporate incometax rate is quite high (57.5%). Pakistan has a corporate tax rate of 55% although, as notedabove, it is to be reduced. Bangladesh has a two rates, 45% for manufacturing and 55% forother companies. Sri Lanka's corporate tax rate (including a 15% surcharge) is 46% but to be

5 For example, the Pakistan corporate tax rate is to be reduced over several years beginning this year. However,we did not have any information on the planned changes in the corporate tax rate.

6 Sri Lanka is eliminating the difference between public and private corporate income tax rates. Until April 1,1994, a 15% corporate tax surcharge applies to all companies. The surcharge is included in our analysis presentedbelow.

3

reduced, as noted above, to 40.25%. As well, in comparison to other neighbouring countries,China, Malaysia and Indonesia, the corporate income tax rates in the South Asian countries(except Sri Lanka) are ten to twenty percentage points higher.

b. Depreciation Allowances:

11. Depreciation allowances in the South Asian countries are based on the historical costof assets. In all countries, annual depreciation allowances are given at prescribed rates. InPakistan, the general rates are 5% (declining balance) for buildings and 10% (declining balance)for machinery. Rates in Bangladesh are twice as fast as Pakistan's on a declining balance basis.India's annual depreciation rate is 10% to 20% for buildings and 25% for machinery (bothdeclining balance). Sri Lanka has the fastest rates of depreciation: in general, three yearwriteoffs for machinery and 14 years for buildings.

12. In addition, Bangladesh and Pakistan, initial depreciation is given for investmentsin buildings (10%) and machinery (20% to 25%).' They also allow companies to claim fasterrates of annual depreciation if machinery is used in multiple shifts during the day (depreciationrates are adjusted upwards by 50% for two shifts and 100% for three shifts). Given thedifficulty of monitoring this tax provision, it likely results in companies claiming annualdeductions for machinery depreciation at twice the prescribed rate for ordinary once-a-day shifts.Bangladesh also allows a company to elect accelerated depreciation instead of normaldepreciation or a tax holiday (80% of assets expensed in the first year, the balance written inthe year thereafter). Also, Bangladesh provides an investment tax credit equal to 15% of theinvestment expenditure.'

c. Inventory Costs

13. In all four countries, inventory costs are based on the original cost or fair marketvalue which even is lower. This provision is similar to those countries that only allow First-in-First-out (FIFO) methods for accounting.

d. Tax Holidays

14. In all four countries, companies can qualify for tax holidays which permit the firmto begin a project of which its income is taxed at preferential rates or not at all. The length of

7 At the time of writing, we were not able to determine whether the initial depreciation allowances reduce the asset'scapital cost base in determining annual depreciation allowances. Our assumption is that the capital cost base is notreduced by the initial depreciation allowance in determining the annual depreciation deductions.

8 Pakistan also provides a 15% to 30% tax credit for new share issues used to finance public companies operatingin qualifying areas. It is assumed that foreign companies do not take advantage of this provision.

4

holidays vary by location, the type of business and certain activities (e.g. export). The longestholidays are found in Bangladesh (twelve years) and the shortest in Pakistan (three years). Ingeneral, holidays seem to be 5 or 8 years in length.

15. As discussed by Mintz [1990], the value of tax holidays depends in part as towhether companies must write down assets for depreciation purposes during the holiday. Ifdepreciation deductions are mandatory, the company can find that, after the holiday period ends,tax depreciation deductions may be inadequate relative to the cost of replacing assets. Thus, atax holiday can result in a positive tax rate on depreciable long-lived assets such as structureseven though the company may be exempt from paying taxes during the holiday. We note thatin all four countries, depreciation deductions seem to be mandatory. In some cases, likeBangladesh and Pakistan, depreciation deductions must be taken as long as there are taxableprofits earned by the company (prior years' losses must be applied first). Unused depreciationdeductions may be carried forward indefinitely.

e. Withholding Taxes:

16. All four countries impose withholding taxes on dividends remitted by foreigncompanies to non-resident owners. The rates vary as low as 10% (Pakistan for U.S. companies)to 25% (India). In addition, a foreign company that sells off shares of companies held in aSouth Asian country will be subject to capital gains taxes levied by the host country.

f. Comparisons to Other Countries

17. As mentioned above, the South Asian countries have relatively higher corporate taxrates compared to China, Indonesia and Malaysia. Moreover, in comparison to Brazil, corporateincome tax rates are generally higher. In addition, the South Asian countries do not index theirtax systems for inflation. Except for Brazil that indexes profits for inflation (and has a very highinflation rate), Sri Lanka and Pakistan face inflation rates that are considerably high.Bangladesh's and India's inflation rate is similar to China and Indonesia while Malaysia has theonly inflation rate below 5%.

18. More importantly, the South Asian countries allow firms to write down capital ata rate similar to Brazil, Malaysia, China and Indonesia. Brazil permits the fastest rate ofdepreciation if an allowance is made for firms taking deductions for triple-shift days formachinery and buildings even if the capital is not used that much. As for inventory costdeductions, only China permits foreign companies to use the Last-in-First-out (LIFO) rather thanFIFO. In times of rising prices, the LIFO method is more generous since the company can usean inventory cost closer to the price at which inventories are being replaced.

19. Finally, the four countries used to compare effective tax rates with South Asiancountries have similar withholding tax rates and provisions for tax holidays.

5

III. TAX COMPETITIVNNESS OF SOUTH ASIA

20. Effective tax rates are calculated for investments made by manufacturing and serviceindustries for four South Asian countries and the four other competing countries seeking foreigninvestment. It is assumed that the structure of capital used for production is the same across allcountries but differ across industries (see the Appendix for weights). Also, it is assumed thatthe leverage ratio is the same across the countries although differs by industry (services are morelevered). We examine the impact of leverage on effective tax rates below. Finally, the net-of-tax rate of return earned by the multinational parents is 5% for all eight countries based on U.S.data; divergence in the cost of investment arises solely from the tax system which, of course,varies by country.

21. Table 1 provides 1993 estimates of effective corporate tax rates on the major SouthAsian countries in comparison to four selected countries. Calculations are undertaken for bothmanufacturing and service industries. It is assumed that there are no incentives for capital.Table Al in the appendix provides a breakdown of effective tax rates by major asset categories(structures, machinery, inventory and land). Table A2 provides calculations of effective taxrates which allow for different real interest rates according to interest and inflation rate dataobserved in the first quarter of 1993.9 Data on specific tax and economic variables is providedin Table A3.

Table 1Effective Tax Rates

No IncentivesPercentages

Manufacturing Services

Bangladesh 17.5 -18.3

Pakistan 47.5 7.6

Sri Lanka 16.9 -45.3

India 48.6 40.6

China 12.7 7.4

Indonesia 37.4 33.7

Malaysia 16.1 -0.1

Brazil 25.5 10.9

9 Results primarily changed for Pakistan. Data provided for us suggest that Pakistan's required net-of-tax rate of

return is only 1%. This makes the tax value of depreciation and nominal interest expenses much more generous, therebydriving down the effective tax rate on capital in Pakistan.

6

22. Pakistan and India have the highest effective tax rates for manufacturing companies(47.5% and 48.6% respectively). In both cases, these countries currently have the higheststatutory corporate income tax rates. In addition, India has a relatively high inflation rate thatresults in a low value for tax depreciation allowances while Pakistan has a relatively low ratesof annual tax depreciation allowances (see Table Al for asset-specific effective tax rates onmachinery and buildings). In the presence of high inflation it is noteworthy to consider that theFirst-In-First-Out method of valuing inventories (all South Asian countries), compared to theLast-In-First-Out method (China), results in higher effective tax rates for firms (see Table 2).Sri Lanka has the lowest effective tax rate on manufacturing, resulting from very generous taxdepreciation allowances coupled with a low corporate tax rate. Bangladesh is an intermediatecase, with a moderately high corporate tax rate but generous depreciation deductions for capital.

Table 2Effective Tax Rates - FIFO versus LIFO

No IncentivesPercentages

Manufacturing Services

FIFO LIFO FIFO LIFO

Bangladesh 17.5 -. 1 -18.3 -32.1

Pakistan 47.5 12.3 7.6 15.2

Sri Lanka 16.9 -27.9 -45.3 -75.1

India 48.6 27.5 40.6 12.3

China - permit the use of LIFO n.a 12.7 n.a 7.4

Indonesia 37.4 29.0 33.7 24.1

Malaysia 16.1 9.7 -0.1 -2.5

Brazil - Inventories are indexed with n.a 25.5 n.a 10.9inflation

23. For services, effective tax rates in all South Asian countries are much lower. Thisresults from a greater degree of leverage; interest deductions, unadjusted for inflation (i.e.nominal interest), help shield corporations from paying the corporate income tax. In the caseof Bangladesh and Sri Lanka, nominal interest deductions along with fast writeoffs fordepreciation of capital result in negative effective tax rates. With a negative effective tax rate,a company pays a present value of taxes that is less than zero for the marginal project. For thisto occur, the company must be able to writeoff losses in early years of the investment againstother income such as profits from inframarginal investments. We note, in the case ofBangladesh and Sri Lanka, the company is effectively allowed to writeoff capital expendituresmore than once. Not only can it writeoff capital through depreciation deductions but, as a result

7

of nominal interest deductibility, the company can writeoff part of the real value of the debt'sprincipal which is an second deduction for investment expenditures.' 0

24. In comparison to the other four countries, Pakistan and India have the highesteffective tax rates in manufacturing and services (except services in Indonesia and Brazil). SriLanka has the lowest effective tax rates (except for China and Malaysia in the case ofmanufacturing). Bangladesh also has relatively competitive tax rates.

25. In all countries, special incentives are given for capital investments. In Table 3, wecompare effective tax rates for investments made in each country if the foreign investor taxesadvantage of a particular tax incentive.

Table 3Effective Tax RatesVarious Incentives

Percentages

Manufacturing Services

I angladesh - 12 year tax holiday 14.8 15.7

Bangladesh - accelerated depreciation -8.3 -343.5

Pakistan - 5 year tax holiday 21.9 17.3

Pakistan - additional depreciation (double anift) 16.4 -130.9

Pakistan - additional depreciation (triple shift) -1.5 -289.1

Sri Lanka - 5 year tax holiday 18.3 20.8

India - 8 year tax holiday (30% of profits 21.8 10.1exempt from taxation)

China - 2 year tax holiday with next 3 years 20.7 15.550% reduction of corporate income tax rate

Malaysia - 10 year tax holiday and investment 5.8 3.7allowance

Brazil - 10 year tax holiday 14.6 11.6

10 Nominal interest is a payment to lenders of the company for postponing their consumption as well as protectingthe lender's capital from inflation that erodes the real value or purchasing power of the debt's principal. Whengovernments allow nominal interest to be deducted from the tax base, they permit the company to write down part ofthe real value of debt's principal.

8

26. We note that the presence of either tax holidays or accelerated depreciation generallyallow the South Asian countries to be tax competitive with the other countries. Pakistancompanies face a much lower effective tax rate if they report triple shifts for machineryinvestment rather than single shifts to claim higher depreciation allowances. India still has arelatively high effective tax rate for manufacturing but the tax holiday does provide someincentive for investment. Sri Lanka and Bangladesh impose effective tax rates on capitalcomparable to China, Malaysia and Brazil.

27. However, sometimes the tax incentive, particularly tax holidays, works perversely.For example, in the case of Bangladesh services, the effective tax rate under the tax holiday caseis actually higher than under "no tax incentive" case. The reason for this is that the tax holidaywhich exempts a company from paying taxes, reduces the ability of the investor to use generousdeductions (e.g. for debt interest) against other income during the holiday period (thesedeductions can only be carried forward and, in the case of losses, may not be carried forwardbeyond the holiday period). We note that accelerated depreciation is more generous an incentivefor capital in Bangladesh."

28. As mentioned above, the leverage policy (debt-asset ratio) of the firm influences theeffective tax rate on capital by allowing the company to shelter investments from corporateincome taxation. The deductibility of interest, particularly nominal interest, reduces the amountof corporate income tax paid on investments. In fact, in the presence of inflation, a firm is ableto further reduce taxes paid by deducting the portion of interest expense that compensates thelender for the loss in the purchasing power of debt. In effect, the deductibility of the realprincipal of debt allows a firm to deduct investment expenditures more than once (first, viadepreciation allowances and second, via a portion of the real value of debt finance).

29. In Table 4, we show the impact of various leverage ratios on the effective tax ratesimposed on manufacturing capital for each of the eight countries (debt-asset ratios are set to beequal to 0%, 25% and 38%). Although not shown here, similar results are obtained forservices. Not surprisingly, the effective tax rate on capital in all countries is lowest when thedebt-asset ratio is 38% and highest when the debt-asset ratio is 0%. We do note, however, thatthe ranking of countries changes considerably when the debt-asset ratios are changed. Whenthere is no leverage, Brazil imposes the lowest effective tax rate on foreign direct investmentwhile India and Pakistan impose the highest tax rates. When debt-asset ratios are at 38%,China and Sri Lanka impose the lowest effective tax rates while Pakistan and India remain thehighest. However, we note that Sri Lanka and Indian effective tax rates fall quickly withleverage (approximately 30 points). This is a result of the high rates of inflation in thesecountries (over 10%) which implies that the tax value of nominal interest deductions are

I1 Many Bangladesh firms are not taking accelerated depreciation. The reason for this is related to a factor not

captured by the calculations in Table 2. It is well known that the tax holiday allows companies to shift income fromtaxpaying companies to associated holiday firms such as by levering the taxpaying company or using transfer pricingtechniques. Thus, the tax holiday is beneficial because the effective tax rate on taxpaying companies is reduced by theholiday granted to an associated firm. This is another problem with tax holidays. They have an unintended effect ofassisting non-qualifying investments since companies can shift income out of taxpaying entities into the holiday firm.

9

especially beneficial to companies in these countries.12

Table 4Effective Tax Rates - Various Debt/Asset Ratios

No Incentive / ManufacturingPercentages

Various Debt/Asset Ratios

38% 25% 0%

Bangladesh 17.5 33.2 55.0

Pakistan 47.5 62.7 78.6

Sri Lanka 16.9 37.3 61.5

India 48.6 61.3 76.3

China 12.7 27.7 49.7

Indonesia 37.4 46.9 60.0

Malaysia 16.1 27.7 45.6

Brazil 25.5 31.1 40.2

30. As indicated above, inflation affects the effective tax rates in some perverse ways.As is well known, inflation increases the tax burden on capital when countries do not indexdepreciation and inventory deductions for inflation. On the other hand, inflation can bebeneficial to firm since debt interest, unadjusted for inflation, is deductible from corporatetaxable income. The net effect of inflation on the effective tax rate is unknown as it dependson the importance of the first effect relative to the second. We note that Brazil's indexation ofprofits for inflation ameliorates the impact of inflation on the effective tax rate imposed oncapital.

30. In Table 5, we examine the impact of various inflation rates (0%, 5% and 10%) onthe effective tax rate imposed on manufacturing companies (similar results, not shown here, are

12 Bangladesh and China effective tax rates also fall by more than 35 points with inflation. The reason for this is

that the fast writeoffs for depreciation in Bangladesh and LIFO deductions for inventory in China help shield companiesfrom paying extra taxes on capital when there is high inflation. Thus the impact of leverage in reducing effective taxrates is greater in these two countries. Brazil's effective tax rate does not decline as much since corporate profits are

indexed for inflation.

10

obtained for services).' 3 We note inflation causes the effective tax rate to rise in Bangladesh,Pakistan and India and slightly fall in Sri Lanka. The fall in the effective corporate tax rate inSri Lanka reflects the very fast writeoffs for depreciation granted to manufacturing (straightlinerates up to 33% for machinery). Thus, inflation has only a small impact on the value of taxdepreciation allowances based on the original cost of machinery in Sri Lanka; thus, the increasein the value of interest deductions in the presence of inflation more than offsets the impact ofinflation on depreciation and inventory deductions.

Table 5Effective Tax Rates - Various Inflation Rates

No Incentive / ManufacturingPercentages

Various Inflation Rates

5% 10% 15%

Bangladesh 17.5 23.2 24.1

Pakistan 42.2 47.1 47.4

Sri Lanka 17.4 17.5 15.5

India 46.2 49.4 49.9

China 16.4 9.1 -4.2

Indonesia 36.6 37.5 37.2

Malaysia 18.4 20.6 20.0

Brazil 25.5 25.5 25.5

31. In China, the effective tax rate drops dramatically with inflation (falling from 16%to -4%). The reason for this abrupt reduction in effective tax rates arises from the use LIFOfor calculating inventory costs for tax purposes. In the presence of rising prices, LIFO allowscompanies to shelter inflationary profits earned by holding inventories since companies can usethe price of the newest inventory to cost inventories. This is quite different an FIFO used inSouth Asia since the cost of inventories is based on the price of the oldest inventory held instock. As discussed in Table 2, the use of LIFO rather than FIFO in the South Asian countrieswould dramatically reduce effective tax rates.

32. Table 6 provides more detailed analysis of the impact of different sources of

13 Note that interest rates on debt and the nominal cost of equity finance adjust point for point with higher inflation

rates. This relationship arises from our assumption of international financial arbitrage following purchasing power paritycondition. The implication of this assumption is that real rates of interest are the same across countries. See theappendix.

11 , . '

financing on the calculation of effective tax rates for the four South Asian countries. Weconsider three polar cases: (i) all debt financing, (ii) all new equity financing (transfers madefrom the parent) and (iii) all retained earnings financing. The debt financing case is a limitingcase since multinational companies cannot necessarily hold loans of the subsidiaries and deriveinterest income without being curtailed by exchange rate controls. The case of all new equityfinancing requires the remission of dividends that are subject to high withholding taxes onremitted dividends from subsidiaries. The third case which assumes that investment is onlyfinanced by reinvest profits implies that the multinational can defer withholding taxes ondividend payments. Not surprisingly, the tax system encourages debt finance (due to interestdeductibility), then retained earnings (due to the negligible tax on accrued capital gains arisingfrom reinvested earnings) and finally, transfers of new equity from the parent. If reinvestedearnings is the primary source of financing investment in South Asia, then, indeed, effective taxrates on capital ate quite high.

Table 6Alternative Sources of Finance

Effective Tax RatesPercentages

All Debt Financing All New Equity Financing Retained EarningsFinancing

Mfg Serv Mfg Serv Mfg Serv

Bangladesh -199.5 -102.5 55.0 62.4 53.6 53.6

India -98.8 -401.3 76.3 79.2 76.9 76.9

Pakistan -144.2 -166.5 78.6 78.9 75.0 75.0

Sri Lanka -100.1 -113.8 61.5 58.4 54.5 54.5

IV. POLICY CONCLUSIONS

33. From the analysis provided above, a conclusion can reached about the current stateof corporate taxation in the South Asian countries. In general, one can characterize thecorporate tax systems as hav;ng a high rate of tax and a narrow base due to tax incentives. EvenSri Lanka that has a tax ate closer to that of the U.S. and Southeast Asian countries hascontinued to rely on tax incentives such as relatively fast depreciation deductions for machineryand tax holidays.

34. In addition, the income tax systems are not indexed for inflation. Therefore, taxeson corporate profits are relatively high for companies that finance investments with equity ortend to use certain high-taxed assets like inventories in production.

12

35. These conclusions regarding the corporate tax policies of South Asian economiesshould be measured against the aims that governments are trying to achieve with regard to theircorporate tax policies. What should be the objectives of corporate tax systems in South Asiancountries? Arguably, there are three objectives:

(a) attract capital, particularly from foreign sources, to encourage economic growth,(b) raise revenue to finance government expenditures (including expenditures that add to

industrial capacity such as education and infrastructure), and(c) achieve consistency with the overall tax system (i.e. corporate tax policies assist with

the taxation of income accruing to residents and non-residents).

36. With respect to the first objective, the South Asian countries, except Sri Lanka, donot provide particularly attractive tax regimes for investment unless the company qualifies fora tax holiday, is highly levered or uses capital that is eligible for fast writeoffs. Although taxholidays shelter foreign investment from taxation for a certain period, ongoing establishedcompanies are taxed at relatively high rates in all four countries except for Sri Lanka.Moreover, tax holidays are more attractive to footloose industries with short-lived capital, notthe kind of foreign investments that assist with the long run development of the economy.

37. As for raising revenue, the tax holidays and accelerated depreciation measuresgranted by the South Asian countries are rather inefficient tax incentives especially when theyare available to companies at the same time. As is well known, tax holidays have a very highrevenue cost in delivering tax benefits to companies since income can be shifted from associatedtaxpaying companies to holiday firm to avoid payment of the corporate income tax. Forinstance, debt is issued by the taxpaying company rather than holiday firm so that interestdeductions can be maximized. Or alternatively, tax holiday companies can lease capital fromtaxpaying companies and effectively transfer depreciation deductions from the holiday companyto the associated taxpaying firm. Leasing will especially lead to tax avoidance if the taxpayingcompany can also take advantage of accelerated depreciation that some countries like Bangladeshand Sri Lanka provide. Moreover, to make up for large revenue losses, many of the SouthAsian countries have relied on relatively high corporate tax rates. This, in turn, encouragesmultinational companies to try to shift income out of a high tax rate jurisdiction (e.g. India) toanother with a lower corporate tax rate (e.g. Sri Lanka).

38. With respect to the final objective, the corporate tax system plays an important rolein ensuring that income accruing to residents and non-residents is taxed. In effect, the corporateincome tax is a withholding tax on income earned by shareholders. If the government pursuesthe taxation of income at the personal level, the corporate income tax is an appropriatemechanism to ensure that individuals cannot escape income taxes by leaving their income in thecorporation 4. Moreover, if there are no capital gains taxes or low taxes on dividends, thecorporate income tax serves as a tax on equity income in lieu of personal income taxes. As fornon-residents, the corporate income tax ensures the withholding of income that may be difficultto tax under the non-resident withholding tax system. With the crediting of the corporate income

14 This calls for the integration of corporate and personal income taxes to ensure that equity income is not taxedtwice. India, for example, does not provide for integration of personal and corporate income taxes.

13

tax against foreign tax liabilities paid by multinationals to home countries (e.g. Japan, the UnitedKingdom and the United States), a capital importing country has an additional incentive toimpose a corporate tax that, in its absence, would simply lead to an increase in revenue receivedby foreign treasuries. Thus, a broad-based corporate tax consistent with international standardswith a low rate of tax would implement the objective to withholding taxes on income accruingto residents and non-residents. In this respect, the four South Asian countries do not have a verygood corporate tax system to withholding income. The existence of tax holidays and generousdepreciation allowances creates differential rates of taxation on company income. Some ownersof capital enjoy low rates of taxation if their firms qualify for incentives. In fact, someprofitable companies may not be paying taxes at all as they incur substantial losses for taxpurposes. Others may be faced with relatively high rates of taxation.

39. The corporate income tax systems of the four South Asian countries fail in achievingthe objectives that are being sought. The corporate tax system is of limited attractiveness foronly some companies that can make use of the tax holiday and fast writeoffs for depreciation andinterest costs. However, the tax incentives lead to large revenue loss and compromise therevenue-raising and withholding roles of the corporate income tax.

40. A better corporate tax would be achievable if a number of reforms were to beadopted. The first would be abolish tax holidays that lead to a large revenue losses. Instead,companies could be taxed at a lower rate (consistent with international standards), therebyencouraging investments in long-lived projects rather than footloose industries. Moreover, ifsome incentive is desired, an investment tax credit that is directed to new investment andprovides immediate cash to the company could be provided instead.15

41. The policy prescription enunciated above requires further investigation for eachcountry to assess its revenue implications. If corporate taxes were kept the same in eachcountry, a new corporate tax rate and an investment tax credit would need to be measured asa replacement for tax holidays and accelerated depreciation. These calculations are impossibleto do at this time.

42. One may remark, however, that the above suggested corporate tax policies for SouthAsian countries is consistent with the important changes occurring in Sri Lanka. Sri Lanka ,which has recently lowered its corporate tax rate and cut back on some incentives, has been ableto provide a more tax competitive environment for investments. Sri Lanka could even do morethan what it has accomplished so far. By eliminating tax holidays and scaling back depreciationdeductions, Sri Lanka could adopt a much lower corporate tax rate, perhaps signalling to theinternational investors that it is the "Chile" of South Asia.

15 In this sense, the accelerated depreciation deductions (including the impossible-to-monitor allowance for increased

depreciation for more shifts in the day) should be also be eliminated in favour of a single rate of depreciation reflecting

the normal use of capital.

14

Bibliography

Boadway, Robin W., "The Theory and Measurement of Effective Tax Rates", The Impact ofTaxation on Business Activity, ed. by Jack M. Mintz and Douglas D. Purvis, John DeutschInstitute, Kingston, Ontario, 1987.

Boadway, Robin W., Neil Bruce, and Jack M. Mintz, "Taxat;on, Inflation and the EffectiveMarginal Tax Rate on Capital in Canada". Canadian Journal of Economics 15 (1984): 278-293.

Dunn, David and Anthony Pellechio, "Analysing Taxes on Business Income with the MarginalEffective Tax Rate Model", World Bank Discussion Paper 79, Washington, D.C. 1990.

King, M. A., and D. Fullerton. The Taxation of Income from Capital: A Comparative Studyof the United States, United Kingdom, Sweden, and West Germany. Chicago: University ofChicago Press, 1984.

Leechor, Chad and Jack Mintz, "On the Taxation of Multinational Corporate Investment whenthe Deferral Method is Used by the Capital Exporting Country", Journal of Public Economics,Vol. 51, May 1993, 75-96.

Mintz, Jack M., and Thomas Tsiopoulos. "Latin American Taxation of Foreign DirectInvestment in a Global Economy". Foreign Investment Advisory Service, World Bank,manuscript, 1993.

15

APPENDIX

Calculating the Effective Tax Rates

This appendix provides additional details of the methodology, assumptions, and datasources used to calculate the effective tax rates. The methodology is based on the open economyanalysis of Boadway, Bruce, and Mintz (1984, 1987). The work is similar to that of King andFullerton (1984) and the OECD (1991). The main differences in the methodology used here andthat of the OECD, for example, is that actual interest rates and inflation rates are used tomeasure the effective tax rates.

The methodology used to estimate the effective tax rates rests on a number ofassumptions. To start, companies are assumed to maximize profits, implying that they investin capital to the point where the return on capital equals the cost of capital. It is also assumedthat companies choose the level of debt and equity needed to minimize their cost of finance.Cost minimization of financing implies that companies issue debt until the tax benefits fromadditional debt equals the bankruptcy and agency costs associated with incremental debt. Inaddition, the eight host countries of this study, Bangladesh, Brazil, Pakistan, India, China, SriLanka, Indonesia and Malaysia are treated as small open economies. In a small open economy,corporations have the option of acquiring financing from domestic and international marketswhile, at the same time, the domestic market interest rate for a country is determined byinternational trading of currencies.

Furthermore, the analysis explicitly deals with those investments of multinationalcorporations whose home country is the United States of America. While the United States isthe capital-exporting country, the host countries are the capital-importers.

The tax incentives incorporated into the analysis include tax holidays offered by all thehost countries with the exception of Indonesia, and accelerated depreciation offered byBangladesh and Pakistan. Aside from the base effective tax rate estimations, various simulationswere also considered, specifically; alternate inflation rates; alternate debt/asset ratios; and, theuse of LIFO for valuing inventories for those countries that only permit FIFO.

Tim multinational is assumed, in the base calculations, to finance capital in the hostcountry using two sources of money. The first is debt raised in the host country and the secondis equity invested by the multinational parent in the subsidiary operating in the host country.The mathematical expression for the net-of-tax rate of return on these sources of capital, orsavings, is;

rn= {fi'(1-u')+(1-3)g'-p')(1-y)+y(i-p) (a.1)

All home (capital-exporting) country variables are denoted by the / symbol. Those characterswithout the / symbol represent host (capital-importing) country variables. The term i is thenominal interest rate; 8 is the portion of multinational parent's capital financed by debt in thehome country, while y represents that portion of the multinational subsidiary's investment

16

financed by debt in the host country; g' is the nominal home country cost of equity finance; andp' is the expected rate of inflation of the home country (p is also the inflation rate of the hostcountry). The rate of return on capital held by the owners of the multinational parent, asformulated above, is essentially a weighted average of the rate of return available to owners ofdebt, y(i-p) (or y(i'-p') for firms that borrow from the home country), and owners of equity, [(1-B)g'+fii(1-u')p1]. The host country rate of return on capital from holding equity is itself aweighted average of both home country equity, (1-)g', and the rate of return on corporate bondsin the home country, li'(1-u).

It is assumed that international interest rates are determined in the long run by arbitragein international markets. Assuming purchasing power parity to hold in the long run to determinethe host country's interest rate relative to the home country, the following equation is assumedto hold:

i = i'-(p'-p) (a.2)

The owner of a multinational parent is assumed to be a typical G-7 country investor. Theinvestor is assumed to face a weighted average of tax rates imposed at the personal level acrossthe G-7 countries. It is important to note that the net-of-personal tax rate of return earned onbonds is assumed to equal the rate return earned on equity held by the marginal investor in theU.S. parent. This relationship between the rate of return earned by bonds and equity impliesthe following expression:

i(1-m)

The variable, i', is the personal income tax paid on interest (the rate used was 31 percent). Thevariable, 0', is the tax on equity income for the average OECD investor. This tax rate isassumed to be a weighted average of personal tax rates on dividends and capital gains and foundto equal 13.6 percent.

The nominal interest rate is operationally defined as the 1991 lending rate, while theannual change in the consumer price index was used as the inflation rate. Both variables, for allcountries were collected from the IMF International Financial Statistics. The rates used for eachcountry are presented in Tables A3.

The data used for the debt-to-total-assets ratio (8), the debt-to- asset-ratio of themultinational company's investment within the host country (y), and the economic depreciationrates (6) were estimated from World Bank project data for all countries. The components of thedebt data included debentures and loan stocks, loans from financial institutions, loans andadvancements from headquarters and subsidiaries, short-term borrowing, and other creditors.The debtlasset ratio was estimated for each of the three industries. The debt-to-asset andeconomic depreciation parameters used are summarized as follows:

17

Manufacturing Services

29 44

y 38 50

& - Bldg 3 4

6 - Mach 14 22

The statutory annual depreciation rates and relevant tax rates, such as the corporate,income, and dividend tax rates, were obtained from the International Bureau of FiscalDocumentation, 1990 edition, and Price Waterhouse International Taxation of Corporate Income.Actual rates used are provided in Tables A3.

1. Rental Cost of Capital & Effective Tax Rate

For a profit-maximizing company, capital is acquired until the return on capital, gross of taxes,and depreciation equals the rental price of capital. The rental price of capital (applicable to thehost countries except Brazil), for buildings and machinery, is mathematically defined as,

FmlB = (8 +r) (1 -a, -A)(a4uMeairdg (1-a) (a.4)

where F represents the return per dollar of capital (gross of depreciation and taxes), 6 theeconomic depreciation rate, r the real cost of finance, and u is the corporate income tax rate.The variable a, represents the investment tax credit offered for investments in machinery andstructures. The term A is the tax value of the annual depreciation allowances, non-indexed, perdollar of capital expenditure:

[U a ) , Non-indexed(42 +R-(p'-p))

A= a2 I ndexed (a.5)

(4+r)

where a2 is the annual declining balance (or equivalent) depreciation rate. For all countries

18

with the exception of Brazil depreciation for machinery and structures are indexed by theinflation rate. The term r represents the company's real cost of financing, which is definedas;

Ipi'(1-ai)+(1-p)g'-p'}(1-y) +yQp(-) nee+ y {(i-p)(1-u)} Indexed

{ i(-'+1-rg}1y (a.6)+ y {i(1-u) +p'-pl -p') , Non-IndexedI. (1-x)

and R= r + p'

The cost of finance is similar to the net-of-tax return on capital (equation a. 1) except for twoterms. The first incorporates the interest deductibility of debt in the host country ((i-p)(1-u)).The second incorporates the term x, which represents the weighted average host countrywithholding tax on dividends and capital gains.

The user cost of capital for inventories is defined as:

(r+oup) (a.7)I'(1 - u)

such that = 0 for indexed and LIFO inventory valuation and 4= 1 for FIFO. Also, forBrazil, the cost of finance, r, is indexed as expressed in equation (a.6).

Finally, eliminating physical depreciation and tax depreciation allowances, the usercost of capital for land is expressed as follows:

rFLmd = (a.8)

The effective corporate tax rate (U), defined as the difference between the risk-adjusted cost of capital, net of economic depreciation, rg, and the net-of-tax rate of returnrequired to compensate savers for their savings that are to be invested in the company's

19

particular capital, is for the purpose of this study defined as;

(r, -r8 )U = (a.9)

where

(a.10)

As stated previously, the host country economic depreciation rate used, 6, for buildings andmachinery was derived from World Bank project data.

2. Tax Holidays:

Seven of the eight host countries offer tax holidays to incoming investments. Thecost of capital for the firm qualifying for tax holidays is expressed as follows;

6 +ro (1+rd(A,-At- 1)F = (1-As) +

(1-ud (1-uD (a.1

The term ro is the indexed cost of finance with the exception that the domesticcorporate income tax rate, for interest deductibility reasons, is set to zero. The effective taxrates are calculated as indicated from equation (a. 13).

The expression A, represents the present value of depreciation allowances. Theexpression for At is;

At = Us41 + [ UozO(1-Y) + axZI+0d t (a.12)

for t*-t > 0.

(1 + R)aZt = (a. 13)a2 + R

and,

20

Y (1 -a2) **(a. 14)

However, some countriessuch as China offer a five year tax holiday where the first two years fully exempt profitsfrom taxation while for the next three years 50% of profits are taxable. This particular taxholiday arrangement results in a different formulation for the present value of depreciationallowances, which are redefined as;

(1+O,) t*-1 (1-a_____)__- + (1+02) (.5As=ua z, Y (a. 15)t 1a 2 ( +d(+Oj s (1 +RI -(p'-p))Y'(10

Where we start with a zero corporate income tax rate from period t1 to t2 and thenmove to a higher corporate income tax rate (50% the legal statutory rate for China) forperiod t2 to the end of the tax holiday t. In addition the following terms are defined;

(1+R)a2 ad y (1 -a2) -Z __= __ (nd, Y, (a.16)(e2 + R,) 2 ( +J -(p'-p))

6. Aggregation

The aggregation of the effective tax rates for each industry for each country involvedthe individual weighting of r. and r, by the corresponding capital stock weight (csw) for thefour assets in each industry. The aggregation of the effective tax rates for either themanufacturing or service sectors can be more formally expressed as;

4 4~1

U ]=1 f=3 1

UAW40 4 1(a.17)

]= 1

where j represents the four capital stocks. The capital stock weights used for the six LatinAmerican countries were derived from World Bank project data and are presented below.

21

Capital Stock Weights Manufacturing Services

Land 5.4 22.0

Buildings 27.0 22.1

Machinery 39.9 49.0

Inventories 27.7 6.9

Total 100.0 100.0

Table A3 summarize the relevant input data used to calculate the user costs of capitaland effective tax rates for all four countries.

22

APPENDIX

Table AlNo Incentives / By Asset

Effective Tax RatesPercentages

Bangladesh India Pakistan Sri Lanka

Mfg Serv Mfg Serv Mfg Serv Mfg Serv

Buildings 2.8 -17.9 9.3 -89.3 -7.4 -81.1 -29.6 -90.5

Machinery -12.4 -53.2 47.0 52.1 41.4 46.7 -12.9 -20.8

Inventories 56.7 58.7 73.9 67.5 77.7 72.5 65.2 58.0

Land 14.0 -28.7 -25.7 -475.9 -166.4 -129.8 -64.9 -366.5

Aggregate 17.5 -18.3 48.6 40.6 47.5 7.6 16.9 -45.3

Table A2Effective Tax Rates

Alternative Real Interest RatesPercentages

Manufacturing Services

Base* Alternative" Base* Alternative"

Bangladesh 17.3 21.7 -18.3 13.9

India 48.6 51.4 40.6 46.1

Pakistan 47.5 87.5 7.6 -391.5

* The Base effective tax rate estimations for all three countries assume a 5% real interest rate.

** The Alternative case effective tax rates use the following expected inflation and nominalinterest rates:

a) Bangladesh - expected inflation = 5%, nominal interest rates = 17%b) India - expected inflation = 8%, nominal interest rates = 19%c) Pakistan - expected inflation = 12%, nominal interest rates = 13%

23

Table A3Summary of Inputs

Pakistan Sri Lanka Bangladesh India

Corporate Income tax 55% 40.25% 45% mfg 57.5%55% serv

Expected Inflation Rate 12.0% 12.0% 5.0% 8.0%

Nominal Interest Rate 17.0% 17.0% 10.0% 13.0%

Annual Depreciation - Machinery / 10%-db 30%-si 20%-db 25%-dbServices

Annual Depreciation - Machinery / 10%-db 30%-si 20%-db 25%-dbManufacturing

Annual Depreciation - Buildings / 5%-db 6.6%-sl 10%-db 10%-dbServices

Annual Depreciation - Buildings / 5%-db 6.6%-si 10%-db 10%-dbManufacturing

Initial Depreciation Allowance - 25% 0% 20% 0%Machinery / Services

Initial Depreciation Allowance - 25% 0% 20% 0%Machinery / Manufacturing

Initial Depreciation Allowance - 10% 0% 10% 0%Buildings / Services

Initial Depreciation Allowance - 10% 0% 10% 0%Buildings / Manufacturing

Capital Gains Tax 25% 5% 15% 20%

Dividend Withholding Tax 10% 15% 15% 25%

Inventory Valuation Method FIFO FIFO FIFO FIFO

Tax Holiday 3/5/8 yrs 5 years 4/12 years 8-yrs

Investment Tax Credit No No 15% No

Extra Depreciation Reduction 50% - 2 shifts and No 50% -2 shifts and No100% - 3 shifts 100% -3 shifts

Accelerated Depreciation No No 80% first year No20% year two

24

Table A3Summary of Inputs

Brazil Malaysia China Indonesia

Corporate Income Tax 41.73 35% 33% 35%

Expected Inflation Rate 655% 2.75% 8% 8%

Nominal Interest Rate 650% 7.75% 13% 13%

Annual Depreciation - Machinery / 20%-sl 22.5%-db 10%-si 25%-dbServices

Annual Depreciation - Machinery / 20%-sI 22.S%-db 10%-s 25 %-dbManufacturing

Annual Depreciation - Buildings / Services 8%-sl 4.25%-db 5%-sl 10%-db

Annual Depreciation - Buildings / 8%-st 4.25 %-db 5%-si 10%-dbManufacturing

Initial Depreciation Allowance - Machinery 0% 20% 0% 0%/ Services

Initial Depreciation Allowance - Machinery 0% 20% 0% 0%/ Manufacturing

Initial Depreciation Allowance - Buildings 0% 10% 0% 0%/ Services

Initial Depreciation Allowance - Buildings 0% 10% 0% 0%/ Manufacturing

Capital Gains Tax 5% 0% 10% 20%

Dividend Withholding Tax 25% 20% 10% 25%

Inventory Valuation Method Indexed FIFO LIFO FIFO

Tax Holiday 10 years 10 years 5-yrs None

Investment Tax Credit [C] / Allowance [A] no 60% [AJ No No

Extra Depreciation Deductions 2 shifts 80% and No No No3 shifts 100%

Accelerated Depreciation No No No No

25

Related Documents