© Prof. Evelyn Brody Chicago-Kent College of Law Room 841, 312-906-5276 Spring 2009 TAXATION OF BUSINESS ENTERPRISES EXAMPLES NOTE: These examples follow the order that the class will cover the material in your book: I. Overview II. C Corporations: Chapters 2, 8, and 5. III. Partnerships: Chapters 10, 4, and 7. IV. S Corporation: Chapter 3 (no examples here). The examples are numbered by the class (1 through 56) to which they pertain. I. OVERVIEW Example 2-1 (comparison of entities: summary overview of formation and operation): Moe, Larry and Curley want to form a new business to sell novelties. Moe will contribute cash of $1,000. Larry will contribute land that he paid $1,500 for but that is now worth $1,000. Curley will contribute squirting lapel pins and other inventory worth $1,000, in which Curley's basis is $100. In the first year, the business earns $900 from the sale of Curley’s inventory. It makes a distribution of $100 to each owner. What are the tax consequences to everyone? (And should each have separate counsel?!) It depends on the type of entity they have formed for tax purposes. < C Corporation Assume they incorporated the business. 1) Formation: No gain to the corporation on receiving the cash and assets. No gain to Curley on contributing the inventory. No loss to Larry on contributing the land. Moe's basis in his stock: $1,000. Larry’s basis in his stock (and the corporation’s basis in the land): Larry’s basis is

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© Prof. Evelyn BrodyChicago-Kent College of Law

Room 841, 312-906-5276Spring 2009

TAXATION OF BUSINESS ENTERPRISES

EXAMPLES

NOTE: These examples follow the order that the class will cover the material in your book:

I. OverviewII. C Corporations: Chapters 2, 8, and 5.III. Partnerships: Chapters 10, 4, and 7.IV. S Corporation: Chapter 3 (no examples here).

The examples are numbered by the class (1 through 56) to which they pertain.

I. OVERVIEW

Example 2-1 (comparison of entities: summary overview of formation and operation):

Moe, Larry and Curley want to form a new business to sell novelties. Moe will contributecash of $1,000. Larry will contribute land that he paid $1,500 for but that is now worth $1,000.Curley will contribute squirting lapel pins and other inventory worth $1,000, in which Curley'sbasis is $100.

In the first year, the business earns $900 from the sale of Curley’s inventory. It makes adistribution of $100 to each owner.

What are the tax consequences to everyone? (And should each have separate counsel?!) It depends on the type of entity they have formed for tax purposes.

< C Corporation

Assume they incorporated the business.

1) Formation: No gain to the corporation on receiving the cash and assets. No gain toCurley on contributing the inventory. No loss to Larry on contributing the land.

Moe's basis in his stock: $1,000.Larry’s basis in his stock (and the corporation’s basis in the land): Larry’s basis is

E. Brody / Business Tax / Spring 2009 / Examples / p. 2

$1,500 and the corporation’s basis is limited to its $1,000 value; alternatively, the partiescan elect to give Larry a $1,000 basis in the stock and the corporation takes a $1,500 basisin the land.

Curley’s basis in his stock (and the corporation’s basis in the inventory): $100.

2) Income: The corporation owes tax at the rate of 34 percent (ignore the graduated ratesfor small corporations).

$900 x .34 = $300

Note that this leaves an after-tax profit of $600 (and cash of $700) plus the $1,000originally contributed by Moe in the corporation.

The distribution of $100 to each shareholder is taxed to them at, let’s say, 15 percent.

$100 x .15 = $15, or $45 for all three shareholders.

The combined tax on the income, distributed and retained, in year 1 is $345. When thecorporation distributes the rest of the after-tax profit, the shareholders will owe tax.

The distribution has no effect on the shareholder's basis in their stock.

< S Corporation

Again, assume the enterprise is incorporated, but it makes an S election.

1) Formation: Same as for a C corporation (for Larry’s starting basis, see above).

2) Income: The corporation owes no tax. Rather, all of the $900 income is taxed to theshareholders, as ordinary income from the sale of inventory, whether the profits aredistributed or not. The income is allocated one-third to each.

$900 x .30 = $270, $90 tax paid by each.

When income is taxed to the shareholders, it increases their basis in their stock.

Moe’s basis is now: $1,000 + $300 = $1,300.Larry’s basis is either: $1,500 + $300 = $1,800 or $1,000 + $300 = $1,300.Curley’s basis is now: $100 + $300 = $400.

The distribution of $100 to each shareholder is not taxed to them — it’s just giving them

E. Brody / Business Tax / Spring 2009 / Examples / p. 3

previously taxed income. The distribution does, however, reduce their basis in their stock.

Moe’s basis is now: $1,300 - $100 = $1,200.Larry’s basis is now: $1,800 - $100 = $1,700 or $1,300 - $100 = $1,200.Curley’s basis is now: $400 - $100 = $300.

The combined tax on the income, whenever distributed, is $270.

< Partnership

If the entity does not incorporate, the results are as follows.

1) Formation: Similar rules as for a corporation: No gain or loss; a substituted basis forthe partners and a carryover basis for the partnership (even for the loss propertycontributed by Larry; but if an asset with more than $250,000 in built-in loss iscontributed, the partnership’s basis is limited to fair market value).

2) Income: The partnership owes no tax. Rather, as for an S corporation, all of the $900income is taxed to the partners, as ordinary income from the sale of inventory, whetherthe profits are distributed or not. But which partners bear the tax?

If a partner contributes property whose basis is less than or greater than its value, theamount of built-in gain or built-in loss at the time of the contribution is frozen. This gainor loss, as and when realized by the partnership, must be allocated to the contributingpartner. Thus Curley is allocated all of the $900 in income.

Just like for S corporations, income taxed to a partner increases his or her basis in thepartnership interest.

Moe’s basis is still $1,000.Larry’s basis is still $1,500. Curley’s basis is now: $100 + $900 = $1,000.

The distribution of $100 to each partner is not taxed to them — like the rule for Scorporations, it’s treated first as return of basis in their partnership interest.

Moe’s basis is now: $1,000 - $100 = $900.Larry’s basis is now: $1,500 - $100 = $1,400.Curley’s basis is now: $1,000 - $100 = $900.

Similarly, if the partnership sells the land Larry contributed, the first $500 of loss (ifrealized) will be allocated to Larry, reducing his basis in his partnership interest.

E. Brody / Business Tax / Spring 2009 / Examples / p. 4

II. CORPORATE (SUBCHAPTER C) EXAMPLES

! Chapter 2: C Corporation Operations

Example 3-1 (tax liability): Corporation X earns $150,000 of taxable income. Itdistributes all of its after-tax income to its sole shareholder, Adelbert, as a dividend.Assume Adelbert pays federal income tax on his ordinary income at a 30% rate, but,under the 2003 legislation, at a 15% rate on dividends received. Using only these factsand section 11, how much tax is due from the corporation and from Adelbert? What isthe total tax if X were an S corporation?

Example 3-2 (Temporary Provisions for Investment and Domestic Manufacturing)

(a) Section 179 includes a temporary provision that increases the section 179expensable limit to $125,000, adjusted for inflation ($128,000 in 2008), phased outbeginning when the taxpayer buys more than $500,000 (also indexed; $510,000 in 2008)of equipment. After 2010, the maximum deduction drops back down to $25,000, but the“Tax Reduction and Reform Act,” introduced by Ways & Means Chairman Rangel inOctober 2007, proposes to make the extension permanent. In February 2008, Congress“doubled” (i.e., without indexing for inflation) the maximum write-off to $250,000 forcapital expenditures incurred in 2008 and increased the phase-out threshold to $800,000in 2008.

(b) In February 2008, Congress adopted a temporary provision allowingbusinesses to write off fifty percent of the cost of depreciable property (e.g., equipment,tractors, computers) acquired in 2008. In subsequent years, the taxpayer will continue todepreciate the remaining basis of depreciable property under the current-law depreciationschedule. The committee report provides the following example:

The interaction of the additional first-year depreciation allowance with theotherwise applicable depreciation allowance may be illustrated as follows.Assume that in 2008, a taxpayer purchases new depreciable property and places itin service.14 [14 Assume that the cost of the property is not eligible forexpensing under section 179.] The property’s cost is $1,000, and it is 5-yearproperty subject to the half-year convention. The amount of additional first-yeardepreciation allowed under the provision is $500. The remaining $500 of the costof the property is deductible under the rules applicable to 5-year property. Thus,20 percent, or $100, is also allowed as a depreciation deduction in 2008. The totaldepreciation deduction with respect to the property for 2008 is $600. Theremaining $400 cost of the property is recovered under otherwise applicable rulesfor computing depreciation.

E. Brody / Business Tax / Spring 2009 / Examples / p. 5

(c) Thanks to the 2004 Jobs Act, new section 199 allows “as a deduction anamount equal to 9 percent of the lesser of – (A) the qualified production activities incomeof the taxpayer for the taxable year, or (B) taxable income (determined without regard tothis section) for the taxable year.” In general, at a 34% corporate tax rate, amanufacturing company effectively achieves a 3% lower tax rate. (This deduction is alsoavailable to pass-through entities.) However, the deduction amount is limited to 50% ofwages paid. This deduction for manufacturing activities will create a host of interpretiveissues. What do you make of the Starbucks (?!) example in footnote 27 of the conferencecommittee report?

The conferees intend that food processing, which generally is a qualifiedproduction activity under the conference agreement, does not include activitiescarried out at retail establishment. Thus, under the conference agreement while thegross receipts of a meat packing establishment are qualified domestic productiongross receipts, the activities of a master chef who creates a venison sausage for hisor her restaurant menu cannot be construed as a qualified production activity.

The conferees recognize that some taxpayers may own facilities at whichthe predominant activity is domestic production as defined in the conferenceagreement and other facilities at which they engage in the retail sale of thetaxpayer’s produced goods and also sell food and beverages. For example, assumethat the taxpayer buys coffee beans and roasts those beans at a facility, the primaryactivity of which is the roasting and packaging of roasted coffee. The taxpayersells the roasted coffee through a variety of unrelated third-party vendors and alsosells roasted coffee at the taxpayer’s own retail establishments. In addition, at thetaxpayer’s retail establishments, the taxpayer prepares brewed coffee and otherfoods. The conferees intend that to the extent that the gross receipts of thetaxpayer’s retail establishment represent receipts from the sale of its roastedcoffee beans to customers, the receipts are qualified domestic production grossreceipts, but to the extent that the gross receipts of the taxpayer’s retailestablishment represent receipts from the sale of brewed coffee or food preparedat the retail establishment, the receipts are not qualified domestic production grossreceipts. However, the conferees intend that, in this case, the taxpayer mayallocate part of the receipts from the sale of the brewed coffee as qualifieddomestic production gross receipts to the extent of the value of the roasted coffeebeans used to brew the coffee. The conferees intend that the Secretary provideguidance drawing on the principles of section 482 by which such a taxpayer canallocate gross receipts between qualified and nonqualified gross receipts. Theconferees observe that in this example, the taxpayer’s sales of roasted coffeebeans to unrelated third parties would provide a value for the beans used inbrewing a cup of coffee for retail sale.

E. Brody / Business Tax / Spring 2009 / Examples / p. 6

Treasury proposed regulations under § 199 in October 2005. You are not responsible forthese rules. Chairman Rangel would repeal section 199, raising over $10 billion a year.

Example 5-1 (sale of property): Adelbert, the sole shareholder of Corporation X,contributes land to the corporation with a value of $160,000 and a basis to Adelbert of$10,000. As we will see in Assignment 12, the corporation takes a “carryover” basis inthe contributed asset. Therefore, the corporation has a basis of $10,000 in the land. Nowthe corporation sells the land for $160,000, and distributes all the after-tax proceeds toAdelbert. How much cash does he wind up with after tax? [Assume that the corporationhas enough “earnings and profits” to cover the entire distribution; we study “e & p” inAssignment 15.] Note that corporations do not enjoy a special tax rate on capital gains.

Example 5-2 (distribution of property): In Example 5-1, would the tax consequences beany different if Adelbert, immediately after contributing the land to the corporation,realized the folly of his ways and had the corporation distribute the land back to him? See section 311. Ooops!

Example 5-3 (multiple shareholders): Assume instead that corporation X has twoshareholders, individual I and corporation Z. X distributes two parcels of land, one toeach shareholder. The value of each parcel is $100, and X’s basis in parcel 1 is $60 andin parcel 2 is $75. What are the tax consequences? Under section 311, X recognizes $40gain on parcel 1 and $25 gain on parcel 2. Each shareholder has a distribution of $100,treated as provided under section 301. Each shareholder takes a basis of $100 in theparcel received. (We return to the shareholder consequences in Assignment 13; seeExample 13-5.)

Example 5-4 (distribution of loss property): Assume the same facts as in Example 5-3except that X’s basis in parcel 1 is $120. What are the tax results? Under section 311X still recognizes the $25 gain in parcel 2, but cannot recognize the $20 loss in parcel 1. The tax consequences to the shareholders are the same as in Example 5-1. Thus, therecipient of parcel 1 takes a $100 basis in the land, and the $20 of built-in loss will neverbe recognized. What should be done to avoid this result? The corporation should sellparcel 1 to a third party – not to the shareholder (although the loss disallowance rule ofsection 267(a) would apply here only if the shareholders were related, because neithershareholder owns more than 50 percent). Corporations, of course, cannot claim netcapital losses (unlike individuals, who get a measly $3,000 a year), but in this case, X hasenough capital gain from the other parcel to absorb the loss.

E. Brody / Business Tax / Spring 2009 / Examples / p. 7

Example 8-1 (dividends received deduction): The “Tax Reduction and Reform Act,”introduced by Ways & Means Chairman Rangel in October 2007, proposes to replace the70% DRD with a 60% DRD, and to replace the 80% DRD with a 70% DRD. Preliminaryestimates pegged these changes at raising revenue of about $500 million a year.

! Chapter 8: C Corporation Contributions

Example 9-1 (contribution for stock): B transfers land with a basis to him of $80 and aFMV of $100 to newly formed corporation X for all of corporation X’s stock. How muchgain is recognized? What is B’s basis in the stock he gets? What is corporation X’s basisin the land?

Example 9-2 (loss asset): What if in Example 9-1 B’s basis in the land instead were$120? What is the effect of section 362(e)?

Example 11-1 (boot): Same facts as in Example 9-1 except that B also receives $5 cash. (Assume the corporation borrowed the money.) How much gain does B recognize?

Example 11-2 (basis in stock): Assume the same facts as in Example 11-1, above. Thatis, B contributes an asset worth $100 and with a basis of $80 for X corp, in exchange forall of X corp’s stock (worth $95) and $5 in cash. We saw that B’s amount of realizedgain is $20, but that his amount of recognized gain is the $5 cash. What is B’s basis inhis stock?

Example 11-3 (corporation's basis): In Example 11-1, what’s the corporation’s basis inthe asset?

Example 11-4 (boot in excess of realized gain): Same facts as in Example 9-1 exceptthat B also receives $30 cash. How much gain is recognized?

Example 11-5 (stock basis where boot exceeded realized gain): Assume the same factsas in Example 11-4, above. That is, B receives $30 in cash instead of $5, and the stockreceived accordingly is worth $70. What’s B’s basis in the stock?

E. Brody / Business Tax / Spring 2009 / Examples / p. 8

Example 11-6 (inside basis where boot exceeded realized gain): In Example 11-4,what’s the corporation’s basis in the asset?

Example 12-1 (encumbered property): A few years ago, D borrowed $20 and took $40of his own money and bought land for $60. He contributes the land, now worth $100,subject to the debt, to a newly formed corporation for all of its stock.

" What’s D’s stock worth?

" What’s D’s realized gain?

" What’s D’s recognized gain?

" What’s D’s basis in the stock?

" What’s the corporation’s basis in the land?

What if instead of assuming the debt, the corporation distributed $20 to D, and he paidoff the debt? (Assume the corporation borrowed the cash.)

Example 12-2 (bad purpose debt): Suppose I have land worth $100 that I want tocontribute to a new corporation for all of its stock. I paid $60 for the land a while ago. Immediately before I contribute the land, I load it up with $20 of debt – that is, I borrow$20 from a bank, secured by the land. I take the $20 and buy a Maserati. The corporationtakes over the debt; that is, the corporation, not I, will repay the bank.

" What’s my stock worth?

" What’s my realized gain?

" What’s my recognized gain?

" What’s my basis in the stock?

" What’s the corporation’s basis in the land?

Note that the result is the same as if I contributed land in return for stock and $20 cash.

E. Brody / Business Tax / Spring 2009 / Examples / p. 9

Example 12-3 (debt in excess of basis): A few years ago, E borrowed $40 and took $20of her own money and bought depreciable property for $60. Now the property is worth$100 and has an adjusted basis of $30. E contributes this property, subject to the debt, toa newly formed corporation for all of its stock.

" What’s the value of E’s stock?

" What’s E’s realized gain?

" What’s E’s recognized gain?

" What’s E’s basis in the stock?

" What’s the corporation’s basis in the land?

! Chapter 5: C Corporation Distributions

Part A: Dividends – Distributions of Property; Earnings & Profits

Example 13-1 (dividend treatment): B forms X corporation by contributing $5,000 cash. In the first year, X earns $100. Ignoring the graduated rates, X pays $34 to the IRS. If Xdistributes $66 (or anything less) to B, it's a taxable dividend. If, however, X distributes$75, the first $66 is still a taxable dividend and the remaining $9 is a return of basis. Thatis, B's $5,000 basis in her stock goes down to $4,991.

Example 13-2 (preferences "wash out"): The facts are the same as in Example 13-1,except that the $100 of income earned in the first year is tax-exempt interest income. That is, the corporation owes no tax, and thus has $100 more cash at the end of the year. If the corporation distributes $66 (or anything less) should B still have a taxabledividend? What if X distributes $75 (or anything between $66 and $100)?

Note: When the Bush Administration proposed a top 15% tax rate on dividendsreceived by individuals, the low rate would have been available only if thecorporation made the distribution out of income that had borne U.S. corporate tax. (The Nov. 1, 2005 report of the President’s Tax Reform Panel similarly conditionsfavorable shareholder tax treatment on the dividends’ having borne U.S. corporatetax.) Why didn’t Congress go along with this part of the proposal? We return tothis issue later.

E. Brody / Business Tax / Spring 2009 / Examples / p. 10

Example 13-3 (effect of dividend on e & p): Return to Example 13-1. When X earned$100 and paid tax of $34, e & p is increased by the $100 but reduced by the $34. That’ssimply not money available to shareholders – it’s gone (for a good cause!). So e & p nowstands at $66. If X took the $66 and bought new equipment, e & p is still at $66. Thus ifX then distributed $20 to B (perhaps from the cash B originally contributed), B wouldhave a $20 taxable dividend. The $20 dividend is not, of course, deductible from X’staxable income, but it does reduce e & p. Thus, the e & p account stands at $46, which isthe remaining amount of income from year 1 that will be subject to double tax.

Example 13-4 (distribution of appreciated property): Return to Examples 5-1 and 5-2. How will the distributions to Adelbert be treated under section 301? First, what happenswhen the corporation sells the asset and then distributes $110,000 (the cash left afterpaying corporate tax) to Adelbert? (Assume that the corporation had no e & p prior to thesale and distribution.)

Alternatively, what happens if the corporation instead distributes the asset to itsshareholder? (Again, assume no pre-distribution e & p.)

Where did Corporation X get the money from to pay the corporate tax? If Adelbertcontributed the money to the corporation, how, if at all, would that affect your answers? (The other way to do this is to reduce the amount of the distribution by the corporate taxliability Adelbert assumes as transferee. See section 301(b).)

Example 13-5 (multiple shareholders and properties): What happens to the corporationand the shareholders in Example 5-3? Assume I’s basis in the stock is $90, and X’s basisis $55.

Example 15-1 (complete redemption): X corp is owned one-third each by shareholdersA, B, C (none of whom is related to another). Assume that each shareholder has a zerobasis in his or her stock. The corporation has assets consisting entirely of $300 cash (allfrom retained earnings), and so the stock of each shareholder is worth $100. Whathappens if X redeems A’s stock for $100? B and C increase from one-third shareholdersto one-half shareholders. However, the value of their stock remains at $100; because thecorporation took $100 cash to redeem A’s stock, B and C own one-half of a corporationhaving $200 in assets. Accordingly, section 302 treats the transaction between thecorporation and A as a sale of A’s stock (i.e., resulting in capital gain).

E. Brody / Business Tax / Spring 2009 / Examples / p. 11

Example 15-2 (redemption versus cross-purchase): Assume the same facts as inExample 15-1, except that Shareholder A retires, and under a shareholders’ agreementand an agreement with the corporation, A’s stock will either be redeemed or purchased bythe continuing shareholders. Assume that under Rev. Rul. 69-608, the shareholders arenot primarily obligated.

(a) As described in Example 15-1, if A is redeemed for a distribution of $100 cash, Agets redemption treatment under section 302, resulting in $100 capital gain, and B and Chave no tax consequences.

(b) If B and C purchase A’s stock, A will again have capital gain. B and C will have acost basis in this stock. That is, they will each continue to have a zero basis in the stockthey already own (worth $100) and a $50 basis in the shares (worth $50) they buy from A. The corporation still has cash of $300, so B and C now own stock worth a total of $150each.

(c) Ah, but B and C don’t have the money to fund the cross-purchase. They lookhungrily at the cash sitting in the corporation. What if they have the corporation make a$33.33 distribution to each shareholder? If X distributes $33.33 each to A, B, and C,there is plenty of e & p, so each shareholder has dividend income of $33.33 (taxed, atmost, at 15%). The corporation has just depleted its assets to $200, so each shareholder'sstock is now worth $66.66. With the $33.33 dividends they each received, B and C buyA’s stock for a total of $66.66. A now has capital gain of $66.66 (recall the zero basis inher stock). B and C take a cost basis in this new stock. Thus, they each own stock worth$66.66 with a zero basis and stock worth $33.33 with a $33.33 basis – a total of $100worth, its value before A’s retirement. At the cost of current dividend income from thedividend (for A as well), they reduced their future capital gain. (This is not a verydramatic example when dividend rates are as low as capital gains rates!)

Note: If the corporation didn’t have cash to distribute and instead distributedproperty (either in redemption of A or as a dividend to the shareholders),the corporation recognizes gain (but not loss!) under section 311, andincreases e & p by the after-tax gain recognized.

Example 16-1 (redemption incident to a divorce): H and W are in the process ofdivorcing. H and W each owns 50% of the stock of X Corp. As part of the propertysettlement between H and W, X Corp redeems all of the stock held by W. What tax goal

E. Brody / Business Tax / Spring 2009 / Examples / p. 12

are the parties trying to achieve (and what tax result are they trying to avoid)? Do youthink it should work?

Part B: Attribution rules

What’s the purpose of the attribution rules? It lets the Code put together what man hasrendered asunder.

Example 16-1 (family attribution):

A B C

\ 1/3 | / 1/3 \ | / 1/3

\ | /

X

If A is the father, B is the son, and C is the daughter, who owns what?

A: One-third directly, plus 2/3 indirectly.B: One-third directly, plus 1/3 indirectly.C: Same as B.

Note: No re-attribution applies to make B and C the constructive owners of each other’s stock.

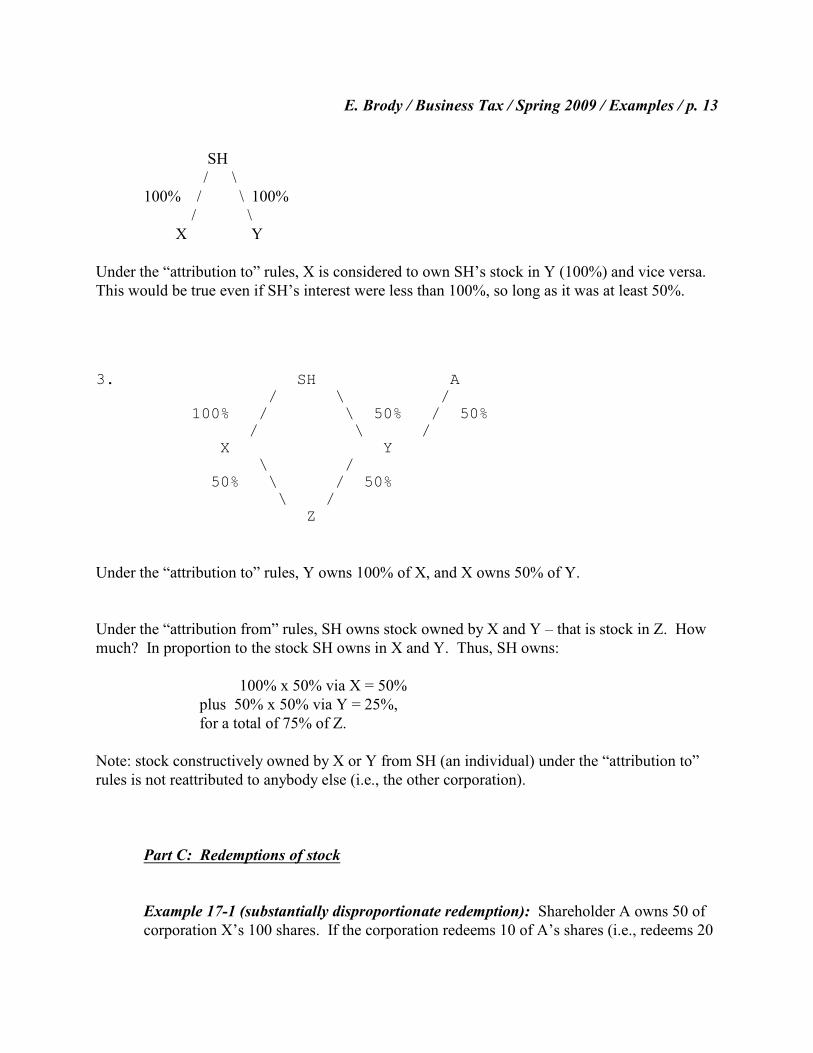

Example 16-2 (entity attribution):

Note: Assume SH is an individual.

1. SH | | 100% | X

2. What if SH splits up her interest into 2 corporations?

E. Brody / Business Tax / Spring 2009 / Examples / p. 13

SH / \

100% / \ 100%/ \

X Y

Under the “attribution to” rules, X is considered to own SH’s stock in Y (100%) and vice versa. This would be true even if SH’s interest were less than 100%, so long as it was at least 50%.

3. SH A / \ /

100% / \ 50% / 50% / \ / X Y

\ / 50% \ / 50%

\ / Z

Under the “attribution to” rules, Y owns 100% of X, and X owns 50% of Y.

Under the “attribution from” rules, SH owns stock owned by X and Y – that is stock in Z. Howmuch? In proportion to the stock SH owns in X and Y. Thus, SH owns:

100% x 50% via X = 50% plus 50% x 50% via Y = 25%, for a total of 75% of Z.

Note: stock constructively owned by X or Y from SH (an individual) under the “attribution to”rules is not reattributed to anybody else (i.e., the other corporation).

Part C: Redemptions of stock

Example 17-1 (substantially disproportionate redemption): Shareholder A owns 50 ofcorporation X’s 100 shares. If the corporation redeems 10 of A’s shares (i.e., redeems 20

E. Brody / Business Tax / Spring 2009 / Examples / p. 14

percent of his stock), does he satisfy section 302(b)(2)?

a) 50% Test. After the redemption, does A own less than 50 percent of the corporation? Yes, because:

(50 - 10)/(100 - 10) = 40 / 90 = 44 percent.

b) 80% Test. What was A’s percentage ownership before the redemption? 50/100 = 50percent. What’s 80 percent of 50 percent? 40 percent. But since A’s post-redemptionownership is 44 percent, he flunks the 80 percent test. What happened? Don’t forget thatthe corporation has fewer shares after the redemption – because the denominator issmaller, you’re not safe if you redeem just 20 percent of the shareholder’s stock!

Example 17-2 (pro-rata redemption): Consider X corp in Example 15-2, above. Insteadof redeeming A’s interest, however, what if X corp purported to redeem one-third of thestock held by each shareholder for $33.33? If the shareholders sold their stock to a thirdparty on the stock exchange, they could get capital gain treatment. But note that in such acase, (1) outsiders will have some control over the entity, and (2) the $100 cash is stillsitting in the corporation to be taxed as dividends (assuming enough e & p) whendistributed to A, B, C, and the purchasers. By contrast, if the corporation could do a pro-rata redemption with A, B, and C, those three shareholders could preserve their relativeownership of the corporation and achieve a bailout of the $100 at capital gains rates.

Example 18-1 (attribution rules in complete termination): Husband owns all of Xcorp’s stock. H gives 25 percent to his wife, and one week later the corporation redeemsher stock. She can “get out and stay out” under the safe harbor, but H has succeeded inbailing out dividends at capital gains rates. The statute prevents redemption treatment forsuch cases unless the taxpayer can establish no tax avoidance motive. The anti-abuse rulealso prevents the corporation from redeeming H's stock within 10 years of his transfer toW, if H retains effective control of the business (say, W does not participate inmanagement).

Example 18-2 (bootstrap acquisition): [Note: When the tax rate on dividends is higherthan the capital gains rate, this transaction is more contested between buyer and seller!]

(i) Corporation X has two shareholders, A and B. Each owns 50 percent of the

E. Brody / Business Tax / Spring 2009 / Examples / p. 15

Compare Litton Industries – where Nestle’s bought the stock and the promissory note1

for the declared dividend!

stock. Corporation X's assets consist of $1,000 cash. If the corporation takes half of itsassets and redeems the stock of A, this leaves B as the 100 percent owner (of acorporation worth half of what it previously was). Note: As we saw in Example 15-1, theredemption of A does not result in dividend treatment to B.

(ii) But assume instead that C buys (from the corporation) stock of corporation Xsufficient to give C a one-third interest. Say, corporation X was worth $1,000; C buys$500 worth of stock. Now the corporation is worth $1500. One minute later, X redeemsthe stock of A. This leaves B and C owning 50 percent each of a corporation worth thesame as it was previously ($1,000). Economically, A has sold her stock to C. A getscapital gain from the redemption, and C takes a $500 cost basis in the stock.

(iii) Let’s get more realistic. I said that the corporation had assets of $1,000 cash,but let’s say it has assets of $100 cash and a $900 piece of land. I’m also happy to tellyou that the $100 cash represents retained earnings, and moreover, that the corporationdoes not need the $100 cash to operate the business. If C wanted to buy the productiveassets of the corporation (that is, the land), he’d have to pay only $900 for it; but a sale ofthe land would trigger a gain to the corporation. If instead, C bought all the stock of thecorporation, he would have to pay A and B $1,000.

But why should C pay money to get money? (Particularly since a distribution ofthat $100 to C would be taxed to him as a dividend and not a reduction of his $1000basis!) If the corporation first distributed its cash to A and B – thereby reducing the valueof the corporation from $1,000 to $900 – C would only have to come up with $900 toacquire the corporation. How does money come out of the corporation and into the1

hands of A and B? Today, regardless of the treatment, the appreciation will be taxed at15%. If it’s a dividend, A and B will get basis recovery on the sale of the stock to C. If itqualifies as a redemption (see Zenz), they still pay 15% on the entire capital gain of $1000($100 from the corporation, $900 from C).

Example 20-1 (basis in a failed redemption): IRS Announcement 2006-30 (May 8,2006) – which revoked the proposed regulation mentioned in your Syllabus – includes thefollowing statements:

[T]he IRS and Treasury Department are interested in comments on whether adifference should be drawn between a redemption in which the redeemedshareholder continues to have direct ownership of stock in the redeemedcorporation (whether the same class of stock as that redeemed or a different class)

E. Brody / Business Tax / Spring 2009 / Examples / p. 16

and a redemption in which the redeemed shareholder only constructively ownsstock in the redeemed corporation. The IRS and Treasury Department are alsointerested in comments in the following two areas: (i) whether a differentapproach is warranted for corporations filing consolidated income tax returns; and(ii) whether a different approach is warranted for section 304(a)(1) transactions.

Additionally, the IRS and Treasury Department are studying other basisissues that arise in redemptions that are treated as section 301 distributions.Specifically, the IRS and Treasury Department are studying whether, undersection 301(c)(2), basis reduction should be limited to the basis of the sharesredeemed or whether it is appropriate to reduce the basis of both the retained andredeemed shares before applying section 301(c)(3). The preamble to T.D. 9250,2006-11 I.R.B. 588 [71 FR 8802], indicated that the IRS and Treasury Departmentbelieve that the better view of current law is that only the basis of the sharesredeemed may be recovered under section 301(c)(2). However, the IRS andTreasury Department are considering other approaches. For example, anotherapproach would be to allocate the section 301(c)(2) portion of the distribution prorata among the redeemed shares and the retained shares. A third approach wouldbe to shift the basis of the shares redeemed to the remaining shares and thenreduce the basis of those shares pursuant to section 301(c)(2). The IRS andTreasury Department request comments about these approaches or otherapproaches regarding circumstances in which section 301(c)(2) applies.

Part D: Liquidation of Corporation

Example 21-1 (comparison of entities; liquidating the enterprise):

Note: Refer back to the Three Stooges facts presented in Example 2-1 –Not surprisingly, Moe, Larry and Curley turn out not to have good heads for business, andthey decide to liquidate the business a few years later.

< C Corporation

The corporation owns Larry’s land, which is still worth $1,000 – with a basis tothe corporation of $1,000 (or $1,500 if Larry and the corporation jointly elect for him toreduce his stock basis up-front under § 362(e)(2)) – as well as the $1,000 cash Moecontributed, plus the $400 of retained sales income from year 1, for total assets worth$2,400. Assume no other income or loss that year. Splitting everything three ways looksfair, and corresponds to everyone holding equal percentages of the stock, but can youmake an argument why it would not be fair to Moe or Larry?

E. Brody / Business Tax / Spring 2009 / Examples / p. 17

Assuming the corporation has a $1,500 basis in the land, what happens when thecorporation sells or distributes the land as part of a complete liquidation? Generally,under section 336, the corporation can (finally!) recognize a loss. By the way, can thiscorporation use the loss (a reason for Larry not to reduce his stock basis oncontribution!)? (We will ignore a couple of anti-abuse rules in section 336(d), which,while still on the books, no longer seem to make sense in light of new section 362(e)’sprevention of doubled losses.)

< S Corporation

A liquidation of an S corporation also results in gain or loss at the corporate level.However, the shareholders – and not the entity – bear the tax or enjoy the loss. AssumingLarry had reduced his stock basis up front, the $500 loss is allocated one-third ($167) toeach shareholder. Losses of an S corporation do not carry forward or back, as they do in aC corporation. Rather, they pass out to the shareholders and reduce their stock bases. (But, as we will see, losses in excess of stock basis are “suspended” until theshareholder’s basis later increases, if ever.) Cash distributions also reduce basis, as wehave seen. Cash distributed in excess of basis is taxed as gain. Any stock basis remainingat liquidation is written off as a capital loss. On the distribution of the land and $1,700 –

Moe’s basis is now: $1,200 - $167 loss on land - $567 cash - $333 FMV of land= $133.

This is written off as a capital loss.

Larry’s basis is now (with our assumption): $1,200 - $167 - $567 - $333 = $133.

Curley: $300 - $167 - $567 - $333 = ($767).Because basis cannot be negative, this is a capital gain.

< Partnership

The big difference between a corporation and a partnership is that property(generally) comes out of a partnership at a carryover basis, rather than in a gain or lossrecognition event. Further, in a partnership, unlike in a corporate structure (particularlythe inflexible S corporation), the built-in gain or loss cannot be shifted to the otherowners.

E. Brody / Business Tax / Spring 2009 / Examples / p. 18

Where did P’s basis come from? Perhaps it contributed money and/or assets with a2

basis reaching $600,000 in a section 351 transfer. Alternatively, it could have purchased thestock of S from someone else for $600,000. Additionally, it could have formed or purchased Sfor some different amount, but made subsequent adjustments to its stock in S. For example,under our intercompany transfer rules that apply to a consolidated group, P’s basis in its stock ofS goes up as S earns income and goes down as S makes distributions to P.

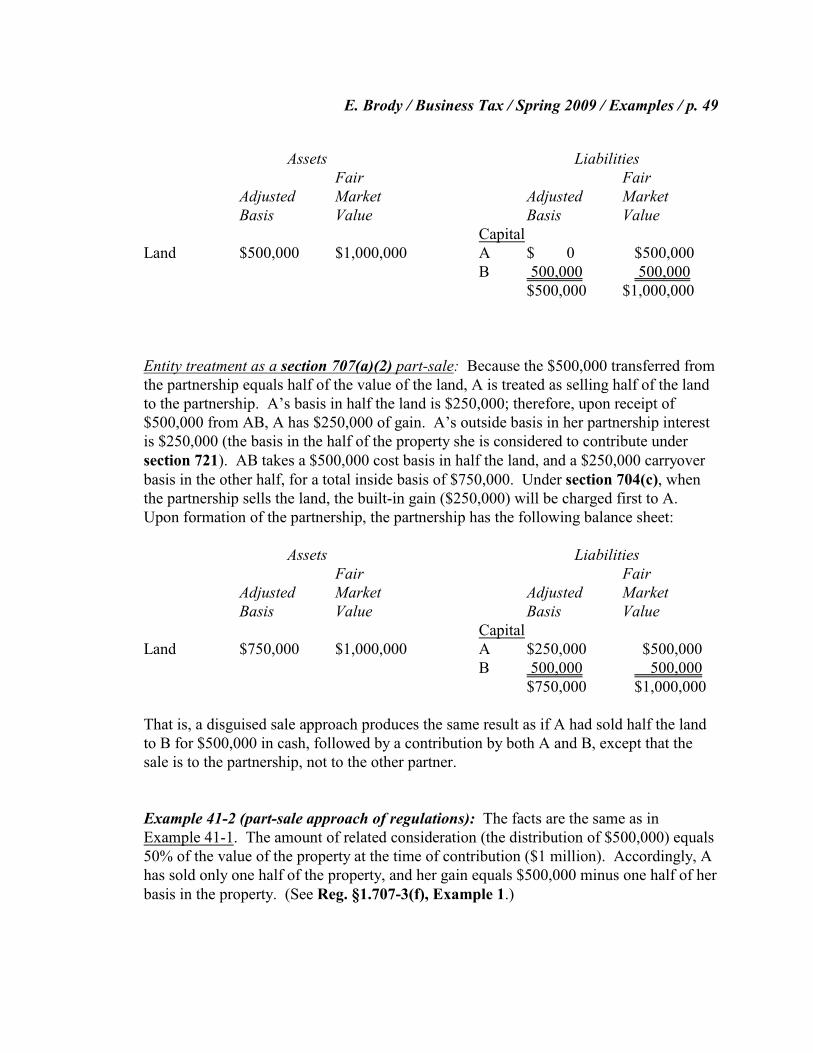

Example 21-2 (distribution of liabilities): If the liquidating corporation distributesliabilities as well as assets, the amount realized by the shareholders is only the net value. Assume the following simplified case:

ASSETS LIABILITIES

Fair FairAdjusted Market Adjusted MarketBasis Value Basis Value

Land 100 100 Liabilities: 80 80

SH Equity:___ Jones 5 20

___100 100 85 100

The corporation liquidates by distributing the land in complete liquidation to its soleshareholder, Jones. Either the distribution is subject to the debt (this requires the lender’spermission) or the shareholder pays off the debt. Either way, Jones’ gain is $15 ($20 netamount realized minus his $5 stock basis). Think of it this way: What would a third partyhave paid Jones for his stock?

If instead the corporation’s basis in its land were less than $100, the corporationwould recognize gain, and the net value of the distribution to Jones would further fall bythe amount of corporate tax (paid either by the corporation or, more realistically underthese facts, by Jones on its behalf).

Example 22-1 (100 percent ownership): P corp owns all the stock of S corp. P’s basisin its stock of S is $600,000. Let’s call this “outside basis.” S’s FMV is $750,000; thus2

this is the FMV of P’s S stock. S’s basis in its assets (“inside basis”) is $400,000. Scompletely liquidates into P. Under the rules:

E. Brody / Business Tax / Spring 2009 / Examples / p. 19

For those numerical or verbal dyslexics out there, don’t confuse section 3183

(attribution rules) with section 381 (tax attributes)!

Ultra-cool tax theory phrase. A great-sounding putdown, but raised too often. There4

are cases where there's really nothing wrong with allowing taxpayers to elect different tax resultsfor separate parts of a transaction. E.g., purchasing some assets (triggering gain but obtaining aFMV basis) and taking other assets at carryover basis (with no gain).

1. S recognizes no gain or loss on the liquidation. Code sections 337; 336(d)(3).

2. P has no gain or loss. Section 332.

3. P takes the S assets at a carryover ($400,000) basis; any depreciation recapture willoccur only upon a recognition event at the P level. Code section 334(b). P's $600,000basis in its S stock goes away – even if P recently bought the S stock for $600,000 withthe hope of obtaining its assets (now worth $750,000). (I will mention Code section 338in class, but you’re not responsible for this election to treat certain stock purchases asasset purchases.)

4. S’s “tax attributes” carry over to P, as if S had been part of P all along. Section 381. 3

What are attributes? Tax attributes are various tax characteristics of a corporation, suchas its method of accounting, its earnings and profits account, and its net operating losscarryover account. Some attributes are desirable, some are undesirable. Tax attributesare not really an issue where P has owned S for a long time. But you can see thatCongress gets a little concerned where P buys S and immediately liquidates it in order toget its tax favorable attributes, such as the NOL account. Special rules apply for NOLsafter a change in ownership.

Example 22-2 (80 percent ownership): The facts are the same except that P owns 80percent of S, individual I owns 10 percent and corporation X owns the remaining 10percent. As to the assets distributed to P, the results are the same as in Example 22-1,parts 1, 2 & 3.

What about the distribution of 10 percent of the assets to I and 10 percent to X? S willrecognize gain – but not loss (see section 336(d)(3)) – perhaps this rule is designed toprevent the obvious temptation of distributing loss assets to the minority shareholders; theCode frowns on “elective selectivity.” I and X will recognize gain or loss on their stock. 4

I and X will take the assets at a FMV basis. See section 334(a) & (b)(2).

E. Brody / Business Tax / Spring 2009 / Examples / p. 20

As for part 4 of Example 22-1, P inherits all of the attributes of S, not just 80 percent. Indeed, many attributes cannot be partitioned, like an accounting method. But it initiallyappears that this result punishes P’s shareholders as to e & p, and rewards them as toNOLs. However, S’s e & p will be reduced by the value of the distributions to theminority shareholders, regardless of who gets distributions first. See Reg. § 1.381(c)(2)-(c)(2). (It’s most realistic to assume that the minority shareholders will get cash and Pwill get the assets.) Similarly, the NOLs will be reduced to the extent gain is realized bythe distribution of appreciated property to the minority shareholders.

Example 23-1 (dividends-received relief for individuals)

In 2003, the Bush administration and others made a variety of proposals to reducethe tax burden on distributed earnings from C corporations. Try to identify thedifferences in fairness, efficiency, administrability, cost, effect on corporate governance,and political “sale-ability” among the following:

1. Exclude C corp dividends from income. (What about a cap of, say, $200 pertaxpayer?) [One proposal would have applied only to dividends paid by publicly-traded companies.]

2. Allow individuals a tax credit (at, say, 15%) for dividends received. (Amountcould be capped.)

3. Allow C corporations to deduct dividends paid.

4. Tax dividends at capital gains rates. (These proposals would also simplify, ifnot lower, capital gains rates.)

The final version takes the form of a 15% top rate on dividends and long-termcapital gains. (The rate is 5% for those otherwise in the 10% or 15% brackets – and zerofor these taxpayers after 2007.) See § 1(h)(11). Why do these caps expire after 2010?

Note: While taxed at the same rate, dividends are NOT capital gains – that is, youdo not offset dividend income and capital losses.

Note, too, that different holding periods apply: To get long-term capital gaintreatment, the gain must be from an asset held for more than one year; to get 15%dividend treatment, the taxpayer must have held the stock for more than 60 days. See § 1(h)(11)(B)(iii)(1) and § 246(c). (Will taxpayers comply?!)

E. Brody / Business Tax / Spring 2009 / Examples / p. 21

Finally, recall that these special rules are not extended to corporations (but compare thecorporate dividends-received deduction we already studied).

Example 24-1 (broker reporting of customer’s basis): As amended by the EmergencyEconomic Stabilization Act of 2008 (signed October 3, 2008), section 6045(g)(2)(A)provides: “The information required under paragraph (1) to be shown on a return withrespect to a covered security of a customer shall include the customer’s adjusted basis insuch security and whether any gain or loss with respect to such security is long-term orshort-term (within the meaning of section 1222).” Covered securities include stock, debt,commodities, derivatives, and any other assets specified by the Treasury. The JointCommittee on Taxation estimated that this reporting provision would raise $6.67 billionin revenue through September 30, 2018. The new reporting requirement appliesbeginning January 1, 2011 (and later for certain securities).

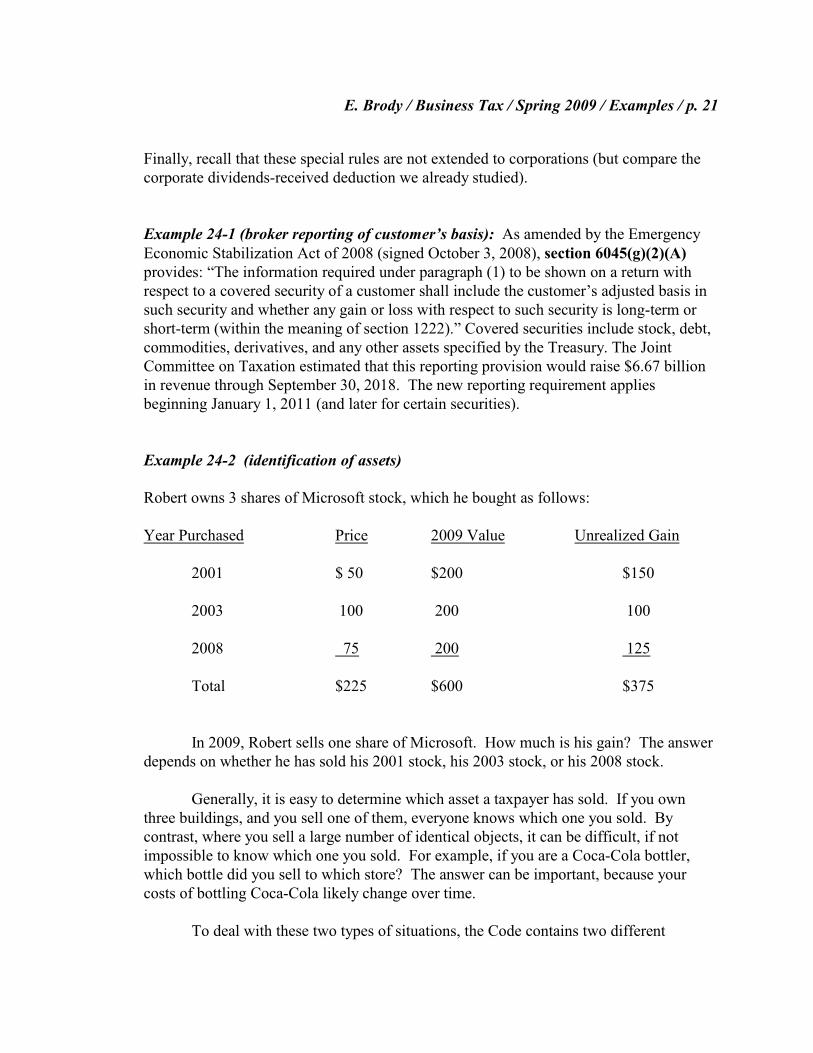

Example 24-2 (identification of assets)

Robert owns 3 shares of Microsoft stock, which he bought as follows:

Year Purchased Price 2009 Value Unrealized Gain

2001 $ 50 $200 $150

2003 100 200 100

2008 75 200 125

Total $225 $600 $375

In 2009, Robert sells one share of Microsoft. How much is his gain? The answerdepends on whether he has sold his 2001 stock, his 2003 stock, or his 2008 stock.

Generally, it is easy to determine which asset a taxpayer has sold. If you ownthree buildings, and you sell one of them, everyone knows which one you sold. Bycontrast, where you sell a large number of identical objects, it can be difficult, if notimpossible to know which one you sold. For example, if you are a Coca-Cola bottler,which bottle did you sell to which store? The answer can be important, because yourcosts of bottling Coca-Cola likely change over time.

To deal with these two types of situations, the Code contains two different

E. Brody / Business Tax / Spring 2009 / Examples / p. 22

accounting schemes. For all assets other than “inventory” the taxpayer is free to identifywhich asset he sold. For inventory, the taxpayer must choose from an approved inventorymethod, and follow it consistently. (See section 471.) Common methods include “first-in, first-out” (FIFO), “last-in, first-out” (LIFO), and a weighted average method.

You might think the shares of stock in the same company are fungible(interchangeable) in the same way inventory is. However, Robert is not a securitiesdealer; he is an investor. Amazingly, then, the law does not require investors in stock tobe consistent in any way. Instead, a taxpayer may designate which share he is selling. InRobert’s case, he would pay the least tax if he designated the 2003 stock as the one hesold, since his basis in that stock is the highest. If Robert then sold a second share, hewould designate the 2008 stock as the share sold (but watch the question of holdingperiod and the difference between short-term and long-term gain). If a taxpayer fails todesignate, the law imposes a FIFO regime, which, in an era of rising stock values, wouldproduce the most gain.

Note: In 1996, President Clinton proposed substituting a proration requirementfor the specific-identification option. This proposal has gone nowhere. In 2007,Chairman Rangel proposal to repeal LIFO would raise over $10 billion a year!

Finally, to make things more complicated, even a dealer in a particular type ofasset can hold items of that type for investment! For example, a real estate dealer isentitled to capital gain if he sells real estate held for investment.

Example 24-3 (short sales)

Return to Robert in Example 24-2. Investors can “sell short” in the stock market. For example, assume that Microsoft stock now trades at $200 a share. Robert believesthat Microsoft will soon fall in value. Accordingly, he borrows 1,000 shares of Microsoftstock from his broker, promising to return 1,000 shares to her in 30 days. He pays a smallsum for this privilege, and he also pays the broker any amounts “in lieu of” dividendsMicrosoft pays on the stock during this period. Robert immediately sells the borrowedshares. (His broker is also likely holds these sale proceeds, as security for the borrowedstock!) At the end of 30 days, Robert must deliver 1,000 shares of Microsoft back to hisbroker. He acquires these shares by buying stock in the open market. If, as he hoped, thevalue has declined in the meantime, he will make a profit. If, however, the price of thestock rose above $200 a share, he will lose money on his “bet.”

Note: In financial market lingo, a person who is “short” has sold property that hedoes not own; thus he has effectively promised to buy property. A person who is“long” owns property. In this example, Robert is short, but there are 2 longs! –

E. Brody / Business Tax / Spring 2009 / Examples / p. 23

his broker (whose stock Robert has borrowed) and the buyer of the borrowedstock. There can be only one “owner” for tax purposes, however. This is thebuyer of the borrowed stock that Robert borrowed and sold; only this buyer isentitled to any dividends paid by Microsoft. That is why Robert has promised tomake “in lieu of” payments to his broker, who would otherwise have received thedividends if Robert hadn’t borrowed the stock.

Many people feel nervous about short sales. Indeed, Wall Street has an expression:

He who sells what isn't his'nBuys it back or goes to prison.

Nevertheless, assuming a healthy public market in the good that is sold short, there isnothing worrisome or suspicious about such a transaction. Think about the short seller’srisk: She’s betting that prices will fall, allowing her to cover (repay the loan) with cheaperproperty. What’s the short seller’s greatest fear? That someone else will bid up themarket before she’s had a chance to buy!

Robert has gain or loss on the short sale at the time he “closes” the sale bydelivery. That is when he knows how much he has made (or even lost) on the deal. Eventhough payment is received up front, the short seller does not know his or her investment(basis) in the contract until he or she performs. In effect, this transaction looks“backwards.” In the ordinary case, at any given time the taxpayer knows his or her basisin the property, but not necessarily the amount for the property can be sold. In a shortsale, the taxpayer has received the purchase price but does not yet know basis. Assumethat on Day 29 Robert buys Microsoft stock for $195 a share; when he delivers the stockto his broker the next day, he has $5 per share gain, and the gain is short-term capital gainbecause he held the stock only one day. Gain (or loss) is short-term or long-termdepending on the amount of time Robert held the stock delivered to close the short sale.

Example 24-4 (“short-against-the-box” and other constructive sales)

Recall from Example 24-2, however, that Robert already owns shares ofMicrosoft stock. Why would he short 1,000 shares – at the least, why doesn’t he simplysell the shares he already owns and short the rest? First, he wants to defer the gain intothe year he closes the sale. In addition, Robert is particularly concerned with the shareshe bought in 2008. If he sells that stock today, he has capital gain, but if he hasn’t held itfor more than a year, it’s short-term capital gain and not the favorable long-term capitalgain. In order to “age” the gain yet lock in his profit on this stock, he might try to shortthe stock he already owns, making sure that the delivery date is more than a year laterthan the date in 2008 that he acquired his share of stock. We call this a “short sale against

E. Brody / Business Tax / Spring 2009 / Examples / p. 24

the box.” (The box refers to the old days, when you locked up your stock certificates inyour safe deposit box; today, usually your broker holds your stock certificates – or simplytracks your ownership through “book entries.”) A short sale against the box was doneonly for tax purposes, and this tax purpose, in general, no longer works.

As to the “aging” issue, the Code provides that the sale of the borrowed stock orbonds suspends the short seller’s holding period in any substantially similar propertyowned. This prevents the seller from claiming a longer holding period for the stock at thetime of delivery.

As to the bigger issue, Congress in the Taxpayer Relief Act of 1997 deprived theRoberts of this world from benefiting from deferring the gain (long-term or short-term)into the year the short sale is closed. Congress was inspired by a notorious transactionentered into by the Estee Lauder family. Two founding shareholders (including Esteeherself) had made a public offering of shares borrowed from other family members –deferring $340 million in gain until the short sale closed. However, because of Codesection 1014 none of this gain would ever be recognized if the short sales could stay openuntil death! [Let’s have a moment of silence for Estee, who died in 2004.]

New Code section 1259 eliminated deferral of gain in appreciated capital assetsalready owned when the taxpayer enters into a short sale or other “constructive sale.” Importantly, section 1259 does not treat the transaction as a sale for all purposes; rather itsimply decrees that a taxpayer recognizes gain on an appreciated financial position to theextent there is such a constructive sale of the property. We are still awaiting the proposalof regulations under section 1259!

III. PARTNERSHIP (SUBCHAPTER K) EXAMPLES

! Chapter 6: Partnership Operations

Parts E & F: Distinguishing Partnership from Other Entities

Example 27-1 (elections): In 2006, Jean and John – who have operated separate boatcharter businesses for many years – decided to operate jointly. They incurred $10,000 ofordinary and necessary expenses in merging their operations. But Jean and John did notrealize that they formed a partnership for tax purposes – and did not file a partnershipreturn – until an IRS audit in 2009 disallows their aggregate $10,000 deduction becausethe costs are start-up expenses. Start-up expenses must be capitalized under section 195unless the new business makes an election for the year the new business began. (The

E. Brody / Business Tax / Spring 2009 / Examples / p. 25

2004 Jobs Act complicated the consequences of the election: It now allows the taxpayer adeduction for up to $5,000 in start-up expenditures, but with any excess – up to $50,000 –allowed as a deduction ratably over the 180-month period beginning with the month inwhich the active trade or business begins.) Temporary regulations issued in 2008eliminated the requirement to file a separate election statement to deduct costs undersection 195(b), instead providing that the taxpayer is deemed to make the election for theyear in which the partnership begins business. Does this mean that filing a late return (thestatute of limitations is still open) is good enough? It would have been too late under theprior rules.

Example 27-2 (timing): John Capital financed the construction of an office building. JoeLabor agreed to construct the building for 50% of the rental profits. All parties are cashmethod taxpayers. The parties agreed that Labor would be paid his share of the rentalsshortly after the close of the year in which they are collected. Net rentals in Year 1 were$100; Capital paid $50 to Labor on January 15 of Year 2. If Labor is Capital’s employee,the parties’ tax results are as follows:

Year 1: Capital has $100 of net profits.

Year 2: Labor has $50 of income; Capital has a $50 compensation deduction.

If, instead, the parties have formed a partnership, the parties' tax results are as follows:

Year 1: Capital has $50 of income; Labor has $50 of income.

Year 2: No tax consequences from the payment of $50 to Labor.

Example 27-3 (character): Wheeler and Perrault agree to develop real estate. They arenot dealers, nor will the enterprise be a dealer. Perrault will obtain the financing;Wheeler will provide the services. Upon sale of the property, after Perrault recovers hisinvestment, Wheeler will be entitled to 25% of net profits. The parties sell the project for$100 profit (after return of Perrault’s investment). If the parties have formed apartnership, Perrault recognizes $75 of capital gain, and Wheeler recognizes $25 ofcapital gain. If, on the other hand, Perrault is Wheeler’s employer, Perrault recognizes$100 of capital gain and is entitled to a $25 ordinary deduction for compensation paid;Wheeler recognizes $25 of ordinary income. (See Wheeler, 37 TCM 883 (1978).)

E. Brody / Business Tax / Spring 2009 / Examples / p. 26

! Chapter 10: Partnership Contributions

Part A.1 — Formation of Partnership or Transfers for a Partnership Interest

Example 28-1 (contributions of property): Smith and Jones have agreed to form anequal general partnership that will engage in trucking. Smith contributes to thepartnership a truck that he has held for two years in his independent trucking business.The truck has a fair market value of $100 and an adjusted basis to him of $50. Jonescontributes $100 in cash. Neither the partnership nor the partners recognize any gain orloss on formation. Section 721.

Example 28-2 (contribution of services for capital interest): Smith and Jones form ageneral partnership. Smith is the “service partner,” who contributes nothing but theobligation to run the business of the partnership. Jones is the “money partner,” whocontributes $100 in cash. The partners agree that, should the partnership be liquidated atany time, Smith and Jones are each entitled to half of partnership capital, includingJones’s $100 contribution. As a result of this agreement, Smith receives compensationincome of $50 on the date the partnership is formed. Section 721. Jones gets a $50compensation deduction. See the Preamble to the § 721 Proposed Regulations.

Example 28-3 (formation of partnership with services and non-cash property): Sameas Example 28-2 except that Jones contributes land worth $100 in which Jones’ basis is$30. Jones is viewed as “selling” half of the land, thus triggering half of the $70 built-ingain. Jones still gets the $50 compensation deduction. See the citation to the McDougalcase in the Preamble to the § 721 Proposed Regulations. [By contrast, note that under theProposed Regulations, if an interest in an existing partnership is issued for services, thepartnership will not recognize any gain.]

Example 28-4 (contribution of services for profits interest): Assume the same facts asin Example 28-2 except that, in contrast, the partners agree that Jones is credited with$100 in his initial capital account, and Smith is credited with $0, so that Jones is entitledto receive back his entire capital contribution before Smith gets 50% of partnershipearnings. In this case, Smith has merely received an interest in partnership profits, and sohas no current income (and Jones gets no deduction). The § 721 Proposed Regulationsand the accompanying proposed revenue procedure reach this result in a somewhatconvoluted way, by allowing Smith to make an 83(b) election to report the “liquidationvalue” of Smith’s interest as zero. The New York State Bar suggests that the finalregulations make this result mandatory, and simply exclude profits interests: After all, asincome is earned and allocated, it will be taxed to the right people at the right time.

E. Brody / Business Tax / Spring 2009 / Examples / p. 27

Part 4.A: Computation of Gross Income and Deductions

Example 29-1 (separately stated items): Investment Fund Partners has two equalpartners, I (an individual) and C (a C corporation). In Year 1, the partnership earned $100of dividend income and $40 of long-term capital gain. In the same year, I recognized aseparate $20 long-term capital loss. C had no other capital gains or losses. Thepartnership files a return separately stating $100 of dividend income (line 6b of ScheduleK) and $40 of long-term capital gain (line 9a of Schedule K). The Schedule K-1 for eachpartner reports $50 of dividend income and $20 of long-term capital gain. On her Form1040, I reports $50 of dividend income, and nets the $20 of partnership long-term capitalgain against her unrelated $20 long-term capital loss. On its Form 1120, C reports $20 oflong-term capital gain and $50 of dividends, for which C is entitled to a 70%dividends-received deduction under section 243.

What if I and C say, “Hmmm, let's allocate $70 of dividends to C, and $40 oflong-term capital gain and $30 of dividends to I”? Stay tuned for our discussion of whenpartnership allocations will be respected for tax purposes. (Example 35-1.)

Example 29-2 (character): On January 1 of Year 1, Smith buys a 10% partnershipinterest in an existing partnership. On February 1 of Year 1, the partnership sells a capitalasset that it has held for two years, for a $100 gain. Smith’s holding period in hispartnership interest begins on January 1 of Year 1. However, since the partnership heldthe capital asset more than 12 months, Smith’s $10 share of the gain qualifies aslong-term capital gain.

Example 29-3 (effect of operations on outside basis): Smith and Jones form an equalpartnership. Each contributes $50 in cash. The partnership uses the $100 to buy a bondthat pays taxable interest. After one year, the partnership has $10 of taxable interest.Smith and Jones report $5 of income each, and each increases her outside basis by $5, to$55. The partnership interest of each is worth $55 (one half of the $100 bond plus theundistributed $10 of interest earned). Accordingly, if Smith sells her partnership interestfor $55, she would have no further gain.

Example 29-4 (tax-exempt interest): Assume the same facts as in Example 29-3, exceptthat the bond pays tax-exempt interest. Again, Smith’s partnership interest is worth $55after the partnership receives the first year’s interest payment. Her outside basis must alsobe increased by her share of this tax-exempt item so that she will not realize artificial gain

E. Brody / Business Tax / Spring 2009 / Examples / p. 28

on the sale of her partnership interest. See section 705(a)(1)(B).

Part 10.A.2 -- Basis as a Gain/Loss Preservation Mechanism

Example 30-1 (outside basis): Assume the same facts as in Example 28-1. Smithrealizes $50 of gain, but the deferred recognition is reflected in his outside basis of $50.Jones’s outside basis is $100. See section 722.

Example 30-2 (holding period): Again assume the same facts as in Example 28-1.Smith’s holding period in his partnership interest includes his two-year holding period forthe truck. Jones’s holding period begins on the date of contribution.

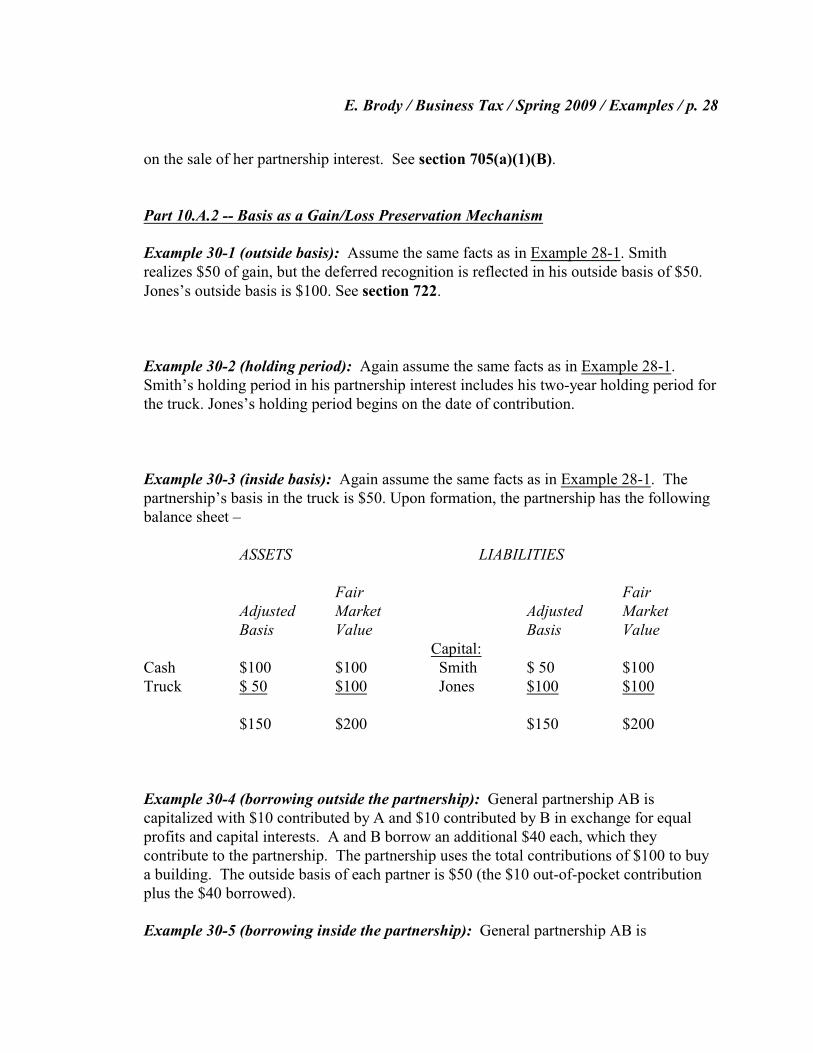

Example 30-3 (inside basis): Again assume the same facts as in Example 28-1. Thepartnership’s basis in the truck is $50. Upon formation, the partnership has the followingbalance sheet –

ASSETS LIABILITIES

Fair FairAdjusted Market Adjusted MarketBasis Value Basis Value

Capital:Cash $100 $100 Smith $ 50 $100Truck $ 50 $100 Jones $100 $100

$150 $200 $150 $200

Example 30-4 (borrowing outside the partnership): General partnership AB iscapitalized with $10 contributed by A and $10 contributed by B in exchange for equalprofits and capital interests. A and B borrow an additional $40 each, which theycontribute to the partnership. The partnership uses the total contributions of $100 to buya building. The outside basis of each partner is $50 (the $10 out-of-pocket contributionplus the $40 borrowed).

Example 30-5 (borrowing inside the partnership): General partnership AB is

E. Brody / Business Tax / Spring 2009 / Examples / p. 29

capitalized with $10 contributed by A and $10 contributed by B in exchange for equalprofits and capital interests. AB borrows an additional $80 from a bank and buys a truckfor $100. AB’s basis (which is the inside basis) in the truck is $100. (See Crane, 331 U.S.1 (1947) (a borrower’s basis in property acquired with borrowed funds includes theamount of the debt).) Each partner’s basis increases by one-half of the partnership’s debt. Section 752. Total outside basis for each is $50 ($10 actually contributed plus $40deemed contributed).

Note: We examine the effects of partnership debt in detail in Assignment 34.

Example 30-6 (contribution of encumbered property): A, B, C, and D form an equalgeneral partnership. A, B, and C contribute $100 cash each. D contributes a buildingworth $140, which is subject to a recourse mortgage of $40; D’s basis in the building is$75. The partnership takes a carryover basis in D’s building, $75. Each partner’s outsidebasis begins with the amount of money or the basis in property contributed and isincreased by the partner’s 25% share of the mortgage. At the same time, D’s basis isdecreased by the full amount of the mortgage. See section 752. The calculations are asfollows:

A: $100 + $10 = $110B: $100 + $10 = $110C: $100 + $10 = $110D: $75 + $10 - $40 = $45

Does this look like tax alchemy to you? To prove that A, B, and C (and to some extentD) aren’t getting something for nothing, sell the partnership’s assets and liquidate thepartnership. Where does the first $40 of cash go?

If this were an S corporation, what would the result be? Recall that an Scorporation is a corporation. Under section 357 the corporation’s assumption of debt oncontributed property is not boot to the contributing shareholder (with exceptions notrelevant here), but rather reduces the contributing shareholder’s basis in the stock.However, the shareholders do not get basis for entity-level borrowing. Thus, basis instock is:

A: $100B: $100C: $100D: $75 - $40 = $35

E. Brody / Business Tax / Spring 2009 / Examples / p. 30

Example 30-7 (multiple liabilities: “full netting”): A, B, and C contribute thefollowing parcels of land to equal general partnership ABC:

A B C

FMV $200 $200 $200Basis 50 20 10Liabilities 100 100 100

If A were the only partner contributing encumbered property, she would recognize gain tothe extent the liability assumed ($100) exceeds her basis (her $50 substituted basis plusher $33 share of the debt), that is, $17. Where there is more than one liability, however,all the section 752 increases and decreases happen at the same time. Thus, A is protectedfrom gain because, at the same time B and C are treated as taking over some of herobligation to repay, she is also taking over her share of their debts. A’s initial outsidebasis is $50 + $33 + $33 + $33 - $100 = $50. Likewise, B and C wind up with an initialoutside basis equal to their prior basis in the asset contributed. What if instead ABC werea corporation? See section 357.

Example 30-8 (taxable year): Black, an individual, is a partner in a partnership that hasadopted a calendar year. I Year 1, the partnership earned $100, $10 of which is allocatedto Black. Section 706 requires Black to include on her return all partnership items fromthe partnership’s tax year that ends with or within her year (which is of, course, thecalendar year). Black must include her $10 share on her own Year 1 Form 1040, whichshe files by April 15 of Year 1. Assume instead the partnership has (properly) elected afiscal year ending on January 31. The $10 allocated to Black from the partnership's yearbeginning February 1 of Year 1 and ending January 31 of Year 2 will be taken intoaccount on her Year 2 Form 1040, filed on April 15 of Year 3.

! Chapter 4

Part 4.B: Partnership Allocations -- Substantial Economic Effect

Debt Interlude.

Let's spend some time reviewing the tax treatment of debt. We will lookclosely at Reg. § 1.1001-2.

E. Brody / Business Tax / Spring 2009 / Examples / p. 31

Example 31-1 (income tax treatment of debt): ABC Partnership borrows $1,000 fromthe bank and spends it. Although you won’t find the rule anywhere in the Code, themoney borrowed is not income. Because of ABC's offsetting obligation to repay thebank, we do not view the partnership as being richer. What is ABC’s tax treatment whenit repays the $1,000? Again, nothing. ABC may not deduct its repayment; becauserepayment extinguishes its obligation to the bank, ABC is not any poorer.

Example 31-2 (effect of debt on basis): ABC Partnership takes the borrowed $1,000 andbuys a building. ABC’s basis in the building includes the amount borrowed. Thus, ABCcan claim depreciation deductions on the bank's money. (Of course, as just described,ABC must later repay the debt with after-tax income.)

For example, assume ABC sells the building for $1,000 after fully depreciatingthe building for tax purposes. That is, ABC has a $0 basis in the building. Accordingly,ABC has $1,000 of taxable gain – but no cash to pay the tax, because (assuming noprincipal amortization) ABC must pay all $1,000 to the bank in repayment of the loan.

Example 31-3 (transfer of property where buyer assumes debt): Assume that ABCPartnership borrows $1,000, buys a building, and sells it before claiming any depreciationdeductions. Assume further that the buyer “assumes” (takes over) the debt (this usuallyrequires the lender’s permission). If the building is worth $1,200, how much will thebuyer pay ABC in cash for the building? Do you see why the answer is $200? After all,the $1,200 building comes with a $1,000 string attached!

How much is ABC’s gain on the sale? We know ABC’s basis ($1,000), so thereal question is what is the “amount realized” (tax-ese for consideration). The amountrealized is not $200!! Granted, that is the amount of cash in the deal, but ABC alsobenefited from the $1,000 of debt taken over by the buyer. (See Reg. § 1.1001-2(a) & (c)(Example 1).) The amount realized is $1,200, basis is $1,000, and so gain is $200.

Finally, do you see why – regardless of whether Buyer pays $1,200 cash or insteadpays $200 and assumes the debt – Buyer's basis is $1,200?

Confused? For some reason, the economics of debt assumption is one of the mostdifficult concepts for non-business people to grasp. Look at it this way: the building isworth $1,200. ABC is indifferent between (i) receiving $1,200 from the buyer, and using$1,000 of it to pay off the bank, and (ii) receiving $200, with the buyer now responsiblefor paying off the bank. In either case, ABC is $200 to the good. (Gain would be higherif ABC had in the meantime taken depreciation deductions, which reduce basis; however,

E. Brody / Business Tax / Spring 2009 / Examples / p. 32

tax gain and cash profit are two different questions when debt is involved.)

Still confused? Perhaps you have bought (or sold) a house with an assumablemortgage. The house is worth what the house is worth; it does not matter if there is debton the property. Rather, the existence of debt, and who has to pay it off, instead affectsthe amount of cash in the deal. A $100,000 house with no debt on it will require thebuyer to bring $100,000 to the closing (probably funded by the buyer's own borrowing!);a $100,000 house with a $20,000 assumable debt will (if the buyer assumes the debt)require the buyer to come up with only $80,000 in cash at closing. In either case, theseller’s amount realized is $100,000. The seller’s gain depends, of course, on the seller’sbasis.

Example 31-4 (nonrecourse debt): The tax rules on debt are even more confusingbecause the results sometimes depend on whether the loan is recourse or nonrecourse. The starting point, again, is Reg. § 1.1001-2, a very old regulation that might take adifferent approach if the Treasury were issuing it today. (See Justice O’Connor’sconcurrence in Tufts, where she sighs: “We do not write on a clean slate.”)

Let’s say Seller, a partnership, owns a building worth $100. The building securesa mortgage for $40. If the partnership transfers the building to buyer, there are severalpossible scenarios. If the debt is recourse, the Buyer could (with the lender's approval)assume the debt. In this case, Buyer will pay Seller $60 cash; and Seller's amountrealized will be $100. (See Reg. § 1.1001-2(a)(4)(ii).) Alternatively if the debt isrecourse, Buyer could refuse to assume the debt; in this case, Buyer will pay Seller $100,and Seller's amount realized is $100. Finally, if the debt is nonrecourse, and Buyer takesthe property “subject to” the debt, the regulations provide a special rule deeming thistransaction to relieve Seller of a liability. (See Reg. § 1.1001-2(a)(4)(i) & (c) (Example2).) After all, by definition no borrower has personal liability for a nonrecourse loan, sothe Seller is not otherwise being “relieved.” Thus, if the debt is nonrecourse, the amountrealized is still $100, whether Buyer pays only $60 and takes the property subject to thedebt, or whether Buyer simply pays $100 and the Seller pays off the debt.

The problem raised in the famous footnote 37 in Crane, and finally decided inTufts, is, “what is the tax result if the property securing the nonrecourse debtsubsequently falls in value to less than the amount of the nonrecourse debt?” How canthe amount realized on a sale exceed the value of the property transferred? Too bad – youlive by the sword, you die by the sword. After all, the amount did not produce incomewhen borrowed, and, moreover, if you included the full amount of the debt in basis,you’ve been benefiting all along by those juicy depreciation deductions. Including theremaining debt in amount realized preserves the tax treatment of the full loan. This is theconcept called “minimum gain” by the regulations described in the next assignment: You

E. Brody / Business Tax / Spring 2009 / Examples / p. 33

will always have gain realized at least equal to the principal balance of the debt minusbasis in the asset.

Unfortunately, though, we have two different tax treatments for that excess debt,depending on the type of debt. Let’s say the property is now worth only $30 but the debtis $40. (The lender must be acting very negligently to let the situation slide this far.) TheBuyer, of course, will only assume $30 of the debt (or pay $30 for a debt-free property). If the debt is recourse, the Seller is still on the hook for the extra $10; if the lenderforgives it, it is COD income (ordinary income, eligible for section 108 relief). Bycontrast, if the debt is nonrecourse, the Seller is nevertheless treated as having $40 ofamount realized. The Seller’s gain (and it’s capital gain) is measured by the differencebetween $40 and her basis in the property; that actual fair market value of the property isless than $40 is irrelevant. (See section 7701(g).) Justice O’Connor would treat theexcess as COD in both cases.

Example 32-1 (economic effect for income): Wilma and Fred form a generalpartnership. Wilma contributes $1000 and Fred contributes $500. However, nothingunder state law requires them to share taxable items in the same ratio as theircontributions (2:1). Unlike S corporations, which require one class of stock, partnershipsare flexible in how they can allocate income and loss – provided the allocations have“substantial economic effect” under section 704(b). This means that the tax items mustgo the same way the parties intend the real dollars to go.

Let’s say Wilma and Fred want to allocate income and loss 50%-50%. This isfine under state law. It’s also fine by the IRS provided that the partners are eventuallyentitled to cash in the same amount as the income was taxed to them. If the partnershipearns $100 in the first year, the income can get taxed $50 to each, but only if this incomeallocation gives Wilma the right only to an additional $50 and gives Fred the right to anadditional $50. (Note that the partnership does not have to distribute the money now – itjust has to increase the partners’ right to the amounts on which they were taxed.)

Wilma Fred

Starting $1000 $500Year 1 income/(loss) 50 50After Year 1 $1050 $550

But what if this is not the partners’ deal? What if Wilma and Fred intend all

E. Brody / Business Tax / Spring 2009 / Examples / p. 34

earnings to be distributed in the same ratio as their initial contributions? That is, the $100of year 1 earnings will eventually be distributed $66.66 to Wilma and $33.33 to Fred. The IRS can't tell you how cash will go – it can only say that because the parties intendedthe cash to go 2/3-1/3, the tax items will also have to be allocated 2/3-1/3. Accordingly,under section 704(b), the IRS will reallocate the year 1 income $66.66 to Wilma and$33.33 to Fred. (Why do you suppose the parties wanted the tax liability to go a differentway from the cash?)

Wilma Fred

Starting $1000 $500Year 1 income/(loss) 67 33After Year 1 $1067 $533

As a result of the reallocation, the amount of cash that the parties are entitled to reflectstheir total after-tax investment in the partnership.

Example 33-1 (loss suspension): Jack and Jill are equal general partners in J&JPartnership, a calendar-year partnership. Jack contributes $25 in cash, giving him astarting outside basis of $25; Jill contributes $10, giving her a starting outside basis of$10. See section 722. In Year 1, the partnership's expenses exceed gross income by $30. In Year 2, gross income exceeds expenses by $30. Thus over the two years, thepartnership breaks even.

Since Jack and Jill are equal partners, each is allocated $15 of loss in Year 1 and$15 of income in Year 2. These allocations have substantial economic effect. (AssumeJill has promised to pay back the $5 deficit that shows up in her capital account at the endof year 2.) Under section 705, the allocation in Year 1 of a $15 loss to Jack reduces hisoutside basis to $10; the allocation of $15 net income in Year 2 increases his outsidebasis back up to $25. He recognizes the $15 loss on his Year 1 income tax return (subjectto any special rules, like the passive activity loss rules, which we do not study); and herecognizes the $15 of income in Year 2.