Taxation, Investment and International Trade INTERNATIONAL TAX JUSTICE ACADEMY 1st – 6th, December 2014, Machakos, Kenya The Political Economy of Global Value Chains and their Relationship with Taxation Edgar Odari, Econews Africa

Taxation, Investment and International Trade INTERNATIONAL TAX JUSTICE ACADEMY 1st – 6th, December 2014, Machakos, Kenya The Political Economy of Global.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Taxation, Investment and International Trade

INTERNATIONAL TAX JUSTICE ACADEMY1st – 6th, December 2014, Machakos, Kenya

The Political Economy of Global Value Chains and their Relationship with Taxation

Edgar Odari, Econews Africa

In today’s global political economy, international production, trade and investments are structured within Global Value Chains (GVCs) where the different stages of the production process are located in different countries.

The reality of GVCs is a strong incentive for companies to restructure their operations internationally through outsourcing and off-shoring of activities.

Companies optimise their production processes by locating the various stages across different sites according to the most optimal location factors across countries.

The international dispersion of value chain activities include design, production, marketing, distribution e.t.c.

The emergence of GVCs challenges traditional perspectives of economic globalization and particularly the policies to be developed around it.

Introduction and Background

TRADE POLICY

Tariff barriers and non-tariff measures (which include

administrative and customs procedures as well as standards) are more significantly felt within GVCs.

Tariff measures mean significant trade costs across multiple jurisdictions especially when goods cross borders multiple times.

Protectionist policies risk having a negative impact on the integration of production processes across borders. This could hurt the competitiveness of domestic industries within GVCs.

There is therefore a push for countries to lower their tariff barriers. This has a negative implication on their ability to raise revenue.

Effects of GVCs on Various Policy Domains

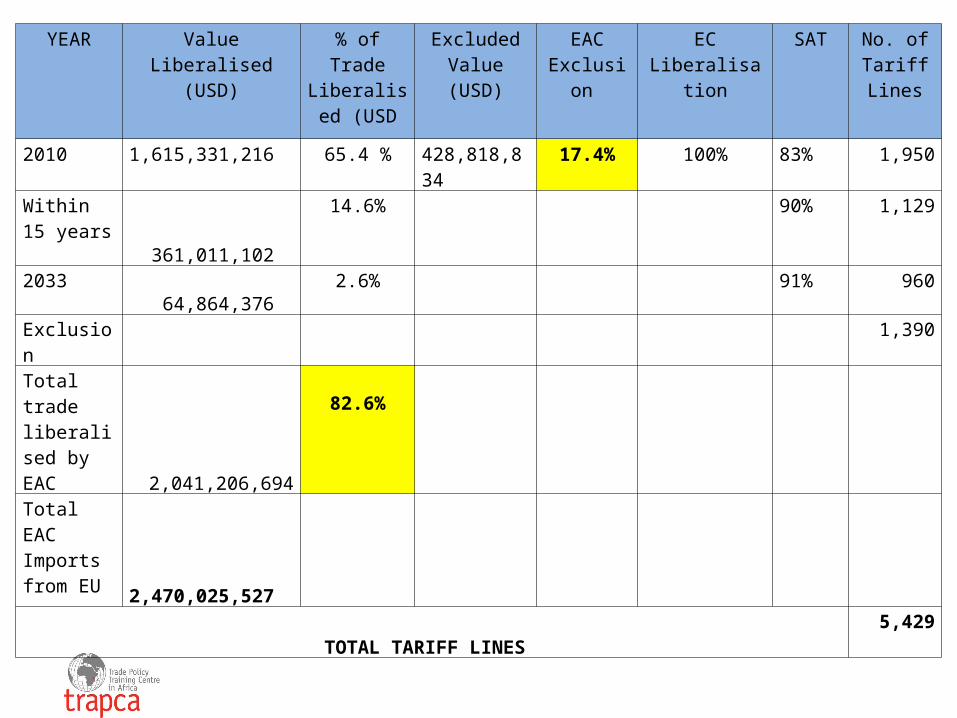

YEAR Value Liberalised(USD)

% of Trade Liberalised

(USD

Excluded Value (USD)

EAC Exclusion

EC Liberalisation

SAT No. of Tariff Lines

2010 1,615,331,216 65.4 % 428,818,834 17.4% 100% 83% 1,950

Within 15 years

361,011,102

14.6% 90% 1,129

2033 64,864,376

2.6% 91% 960

Exclusion

1,390

Total trade liberalised by EAC

2,041,206,694

82.6%

Total EAC Imports from EU

2,470,025,527 TOTAL TARIFF LINES 5,429

INVESTMENT POLICY

GVCs compel governments in their design of investment policies to provide greater incentives aimed at particular sections of GVCs which are seen as being more value-adding. This leads to incentives competition for specific parts of the value chain. (TAX COMPETITION AND THE “RACE TO THE BOTTOM”)

TRANSFER PRICING: This is a challenge many governments face with investors. The growth of GVCs present multinational companies (MNCs) with opportunities to adjust their accounting of value-added so as to maximize earnings in the lowest-cost tax jurisdictions within their international investment framework. (BITs, DTAs, RTAs, Bali)

DEVELOPMENT POLICY

To achieve integration into GVCs, countries need to adjust their border (trade and investment) and “behind the border” policies in areas such as innovation, skills and infrastructure.

However, integration into GVCs is mostly done through affiliates of MNCs. This approach therefore risks the burden of increasingly footloose investors (Investor-State Arbitration)

Effects of GVCs on Various Policy Domains

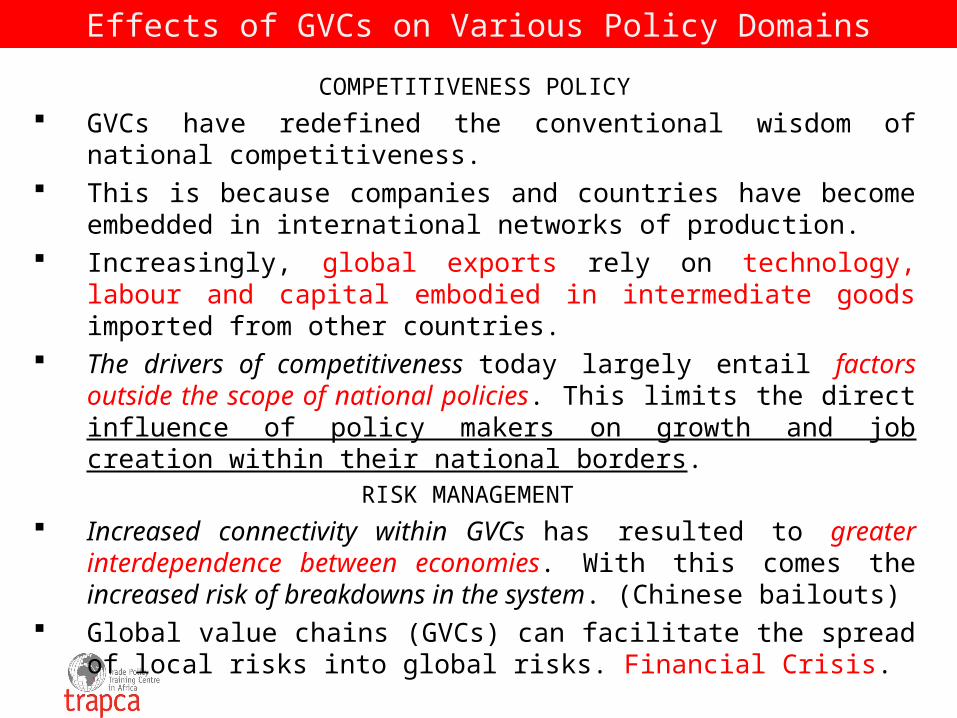

COMPETITIVENESS POLICY

GVCs have redefined the conventional wisdom of national competitiveness.

This is because companies and countries have become embedded in international networks of production.

Increasingly, global exports rely on technology, labour and capital embodied in intermediate goods imported from other countries.

The drivers of competitiveness today largely entail factors outside the scope of national policies. This limits the direct influence of policy makers on growth and job creation within their national borders.

RISK MANAGEMENT

Increased connectivity within GVCs has resulted to greater interdependence between economies. With this comes the increased risk of breakdowns in the system. (Chinese bailouts)

Global value chains (GVCs) can facilitate the spread of local risks into global risks. Financial Crisis.

Effects of GVCs on Various Policy Domains

EAC/US Bilateral Investment Treaty: Negotiations ongoing; EAC commissioned study; process of developing model text.

In March 2013, Ecuador took concrete steps towards annulling Ecuador-US BIT saying “favor foreign investors over human beings.” (Bolivia, Ecuador, Venezuela)

Australia has decided not to include investor-state arbitration in future BITs;

The Transatlantic Trade and Investment Partnership (TTIP) between the US and the European Union (EU) had to be suspended for PUBLIC CONSULTATIONS on the inclusion of investor-state dispute settlement. (fracking, agribusiness). Policy space?

US is revisiting the scope of protection it accords foreign investors in its BITs;

South Africa, the DTI admits that prior to 1994, South Africa “had no history of negotiating BITs,” did not fully appreciate the risks that BITs posed, and as a result “entered into agreements that were heavily stacked in favour of investors without the necessary safeguards to preserve flexibility in a number of critical policy areas.”

Implications for PIDA?

Issues: Low Tax Jurisdictions (Mauritius)

The World Investment Report 2010 identified Mauritius as a favourable and tax efficient platform for African investments.

The country is also listed on the “white list” which entails jurisdictions that have implemented the internationally agreed tax standard and are therefore not considered tax havens by the OECD.

Being the choice country for many cross-border investments into Africa has to do with the country’s incentive for companies to reduce their tax burden in countries they invest in within Africa.

Mauritius currently has DTTs with 13 African states (Botswana, Lesotho, Madagascar, Mozambique, Namibia, Rwanda, Senegal, Seychelles, Swaziland, South Africa, Tunisia, Uganda, Zimbabwe and Kenya).

It has signed DTTs with three other states (Congo, Zambia and Nigeria) which are awaiting ratification and is negotiating with Burkina Faso, Algeria, Tanzania, Egypt, Gabon, Malawi and Ghana.

Implications for MNCs and their role and impact on regional and Africa’s value chains in total.

Implications for PIDA?

Issues: Low Tax Jurisdictions (Mauritius)

Tax avoidance

Challenges: Africa’s GVCs Activity Limited to MNC Affiliates

Category 1 Global Business License Companies

Aircraft Financing and Leasing Consultancy services

Employment services Financial services

Assets management ICT Services

Funds management Operational headquarters

Insurance Pension funds

Logistics, Licensing and franchising of marketing

Shipping trading and ship management

THE MAURITIUS SPECIAL ECONOMIC ZONES

• Zero tax rate on corporate profits. The country has exempted such entities from income tax payable for income years up to and including the income year ending 31 December 2013. The corporate tax rate applicable to processing and transformation activities is 15%.

• Exemption from Customs duties and Value Added Tax (VAT) on all goods and equipment imported into the Freeport zone.

• A reduction in fees related to port handling charges for all goods destined for re-export

• Free repatriation of profits from the Freeport operations.

• Full ownership (100%) where no immoveable property is to be held in Mauritius.

• An allowance to sell a quota of 20% of total goods re-exported into the local market where normal tax rates will apply.

Challenges: Africa’s GVCs & Special Economic Zones

• Mauritius belongs to regional RECs including SADC, COMESA and IOR-ARC. • The nature of Special Economic Zones established by Mauritius have made the

country attractive to exogenous countries or private equity funds to establish any Africa Fund, holding companies or trading companies.

• The fastest growing economies today see Mauritius as a gateway to tapping the African continent. China, for example, is making a wave of strategic investments to take advantage of the COMESA and SADC FTAs. The country recently invested USD 700 million in a Special Economic Zone (SEZ) in Mauritius to service its expansion in Africa. (Regional Value Chain Development?)

• India plans to build a logistics and services hub in the SEZ within the Mauritius.

• South Africa has a similar strategy for Africa. (policy think-tank)

Challenges: Africa’s GVCs & BRICS Threat

Exemption From Capital Gains Tax (CGT): Most jurisdictions on the African continent levy CGT at a rate ranging from 30-35 per cent. In Mauritius DTTs, restriction on taxation rights on capital gains to the country of residence of the seller’s assets. Mauritius CGT is 0%.

Limitation of Withholding Tax on Dividends: In many African countries, dividends paid out to non-residents attract withholding tax ranging from between 10% and 20%. In Mauritius DTTs, rates are generally 0%, 5% or 10%. This therefore enables companies resident in Mauritius to make savings of ranging from 5% to 20% depending on the country they are investing in.

SUMMARY: Low tax rates, generous tax credits; no withholding tax on dividends, interest and royalties paid; no Capital Gains Tax; free repatriation of profits, capital and interest; no estate duty, inheritance, wealth or gift tax as well as full protection of assets.

• Global companies are liable to Corporate tax at 15% but may claim a foreign tax credit in respect of the actual foreign tax suffered or 80% presumed foreign tax credit, WHICHEVER IS HIGHER (legal language for raising ceilings).

• This effectively means that a Global Business License Company is taxed at a MAXIMUM EFFECTIVE RATE OF 3%.

Benefits of Mauritius DTTs to MNCs

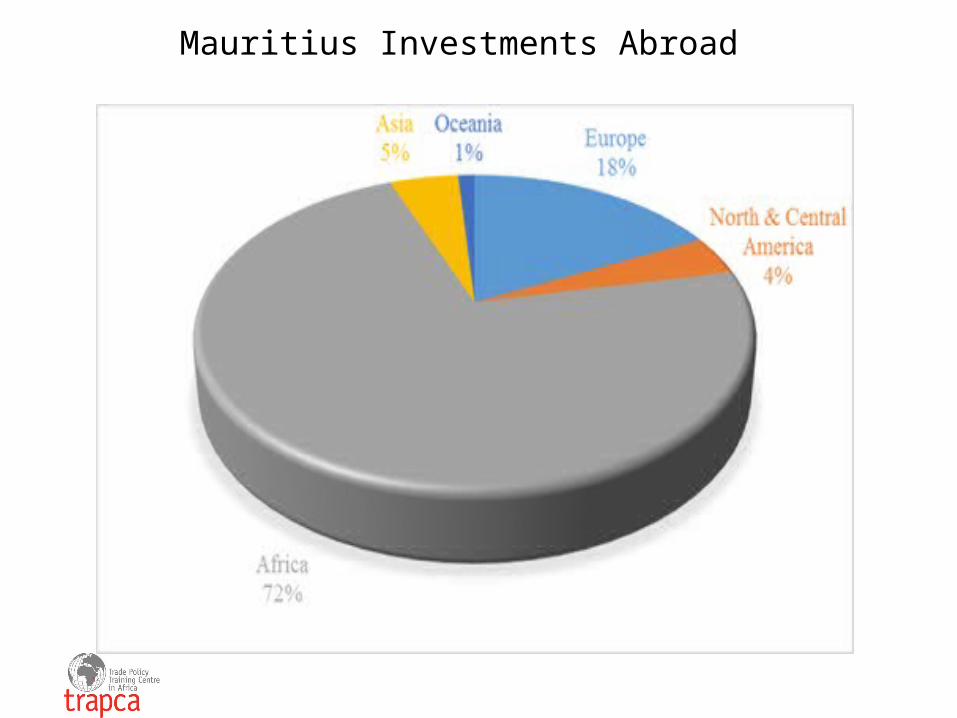

Mauritius FDI in Africa: Sector

Mauritius Investments Abroad

FDI and “FDI” (from Africa) into Mauritius

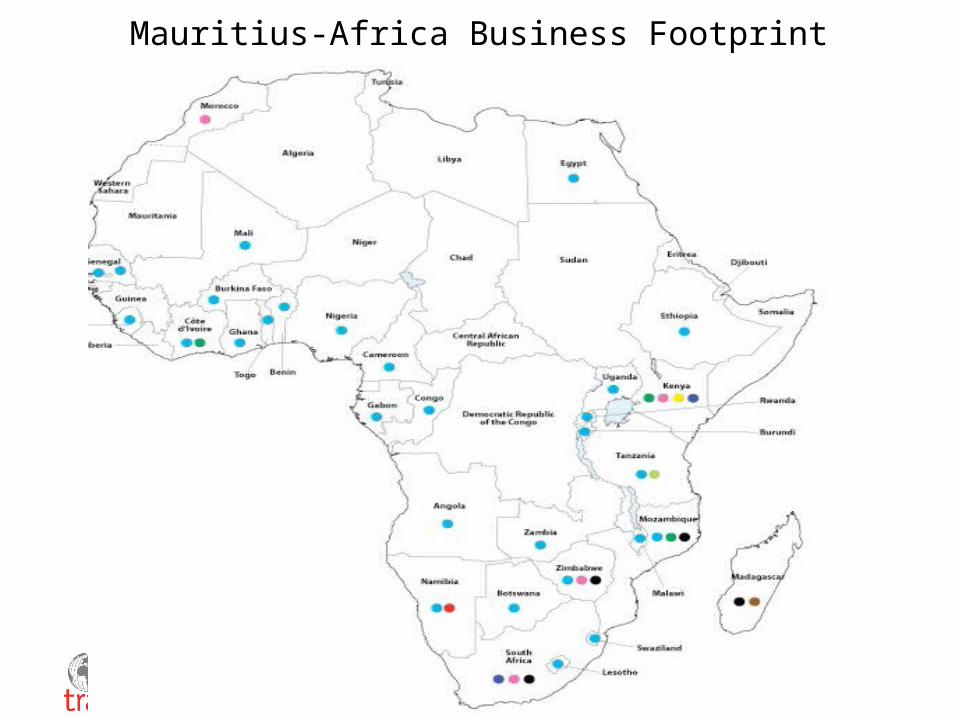

Mauritius-Africa Business Footprint

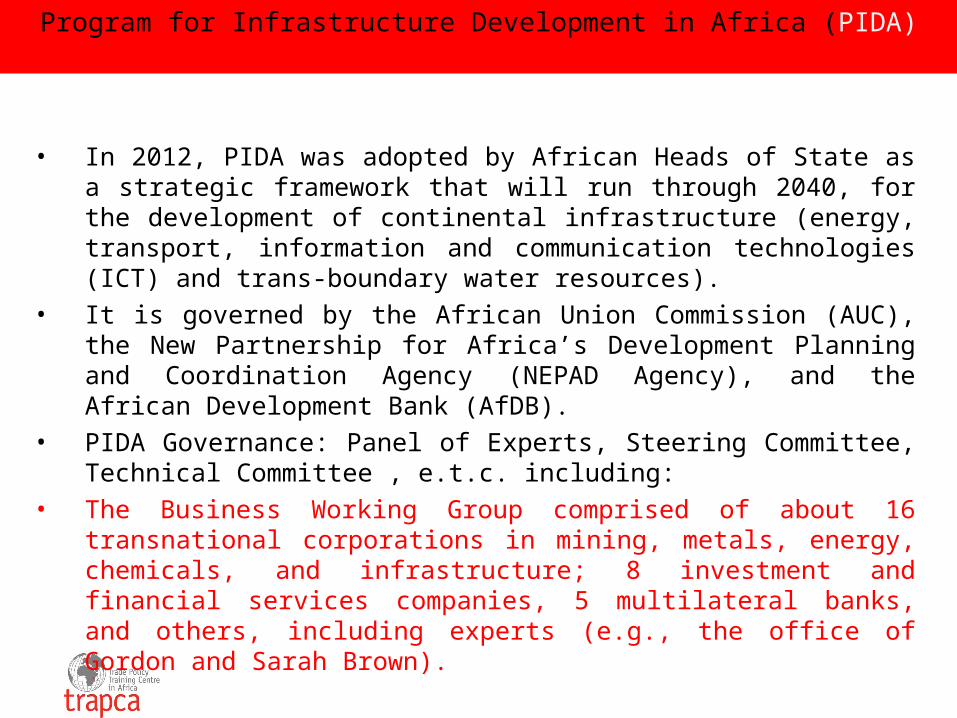

• In 2012, PIDA was adopted by African Heads of State as a strategic framework that will run through 2040, for the development of continental infrastructure (energy, transport, information and communication technologies (ICT) and trans-boundary water resources).

• It is governed by the African Union Commission (AUC), the New Partnership for Africa’s Development Planning and Coordination Agency (NEPAD Agency), and the African Development Bank (AfDB).

• PIDA Governance: Panel of Experts, Steering Committee, Technical Committee , e.t.c. including:

• The Business Working Group comprised of about 16 transnational corporations in mining, metals, energy, chemicals, and infrastructure; 8 investment and financial services companies, 5 multilateral banks, and others, including experts (e.g., the office of Gordon and Sarah Brown).

Program for Infrastructure Development in Africa (PIDA)

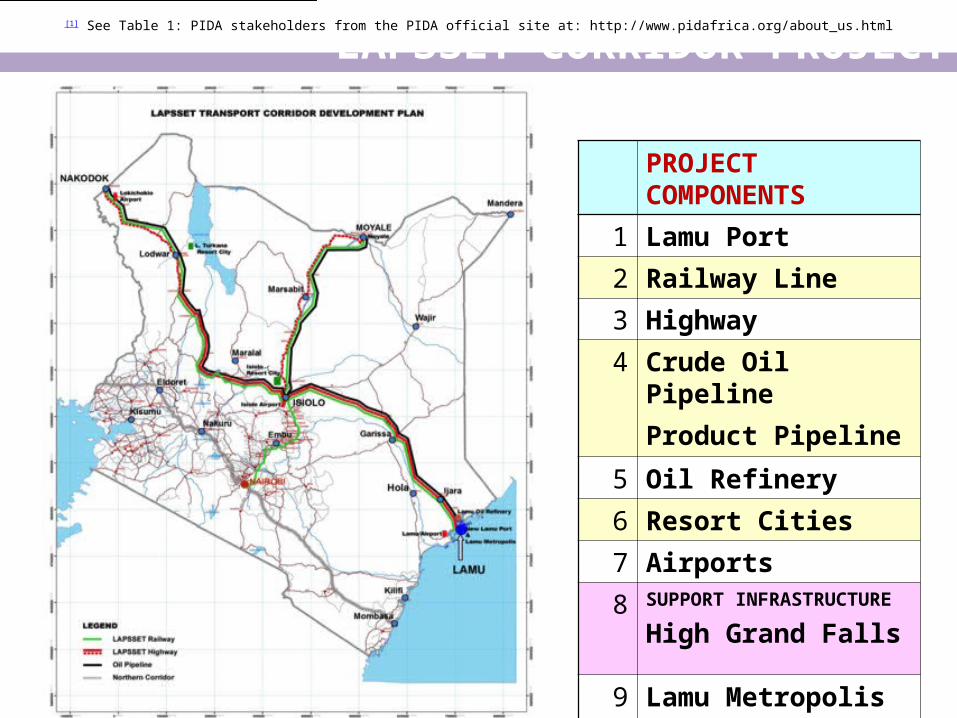

LAPSSET CORRIDOR PROJECT

PROJECT COMPONENTS

1 Lamu Port

2 Railway Line

3 Highway

4 Crude Oil Pipeline

Product Pipeline

5 Oil Refinery

6 Resort Cities

7 Airports

8 SUPPORT INFRASTRUCTURE

High Grand Falls

9 Lamu Metropolis

In 2012, PIDA was adopted by African Heads of State as a strategic framework that will run through 2040, for the development of continental infrastructure (energy, transport, information and communication technologies (ICT) and trans-boundary water resources). (All PIDA projects are listed in Attachment 1). It is governed by the African Union Commission (AUC), the New Partnership for Africa ’s Development Planning and Coordination Agency (NEPAD Agency), and the African Development Bank (AfDB). [1] Thus, it appears that there are African institutions in charge – including the Regional Economic Communities (RECs).

[1] See Table 1: PIDA stakeholders from the PIDA official site at: http://www.pidafrica.org/about_us.html

STANDARD GAUGE RAILWAY MASTERPLAN

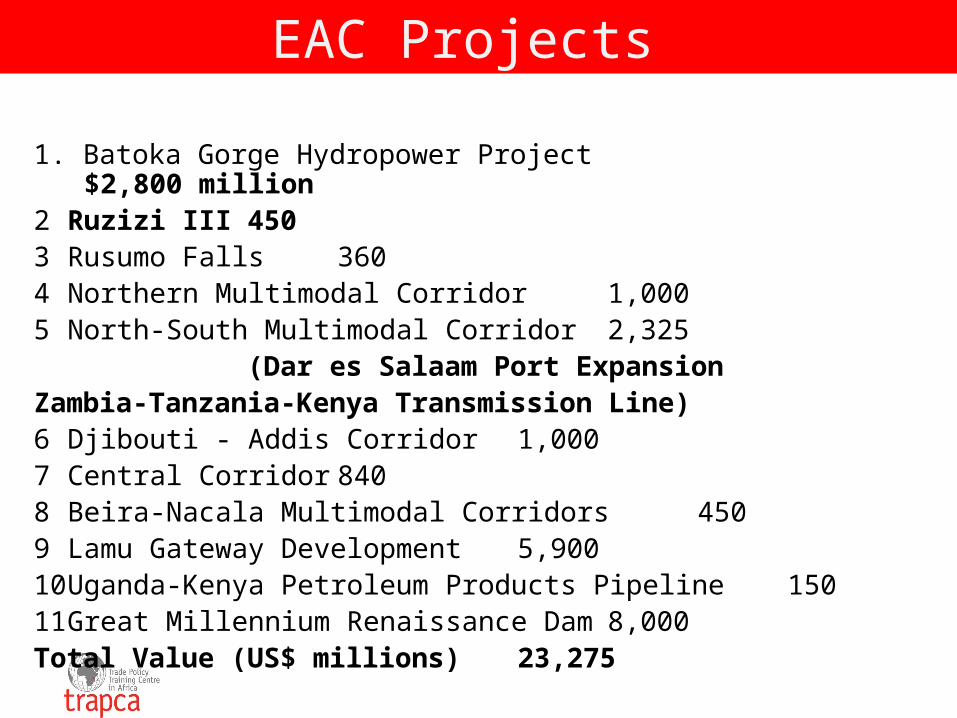

1. Batoka Gorge Hydropower Project $2,800 million2 Ruzizi III 4503 Rusumo Falls 3604 Northern Multimodal Corridor 1,0005 North-South Multimodal Corridor 2,325 (Dar es Salaam Port ExpansionZambia-Tanzania-Kenya Transmission Line)6 Djibouti - Addis Corridor 1,0007 Central Corridor 8408 Beira-Nacala Multimodal Corridors 4509 Lamu Gateway Development 5,90010 Uganda-Kenya Petroleum Products Pipeline 15011 Great Millennium Renaissance Dam 8,000Total Value (US$ millions) 23,275

EAC Projects

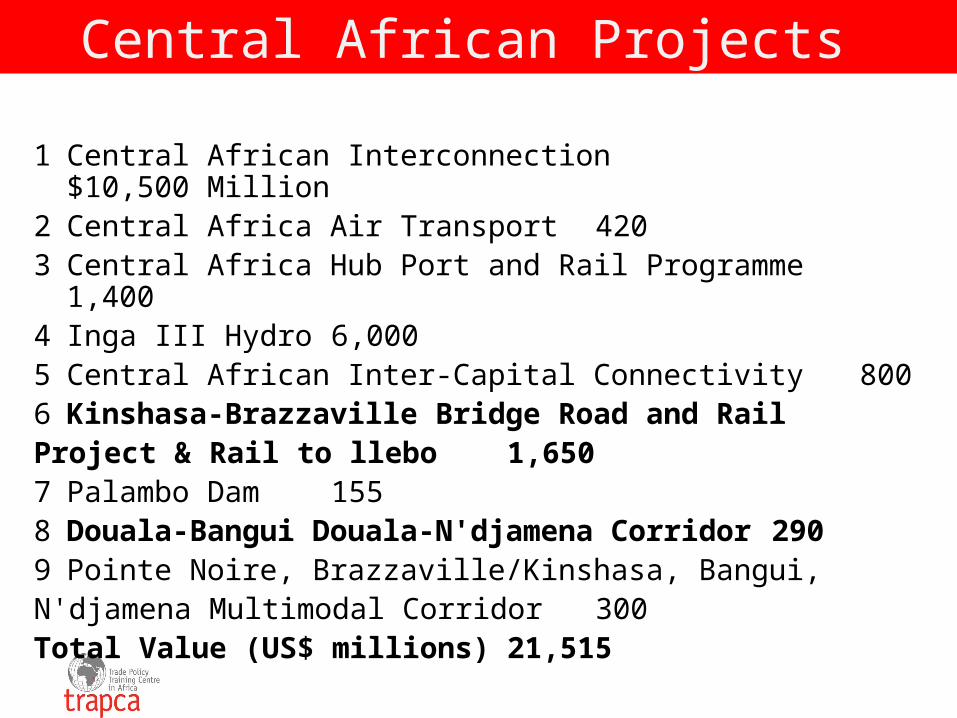

1 Central African Interconnection $10,500 Million2 Central Africa Air Transport 4203 Central Africa Hub Port and Rail Programme 1,4004 Inga III Hydro 6,0005 Central African Inter-Capital Connectivity 8006 Kinshasa-Brazzaville Bridge Road and Rail Project & Rail to llebo 1,6507 Palambo Dam 1558 Douala-Bangui Douala-N'djamena Corridor 2909 Pointe Noire, Brazzaville/Kinshasa, Bangui, N'djamena Multimodal Corridor 300Total Value (US$ millions) 21,515

Central African Projects

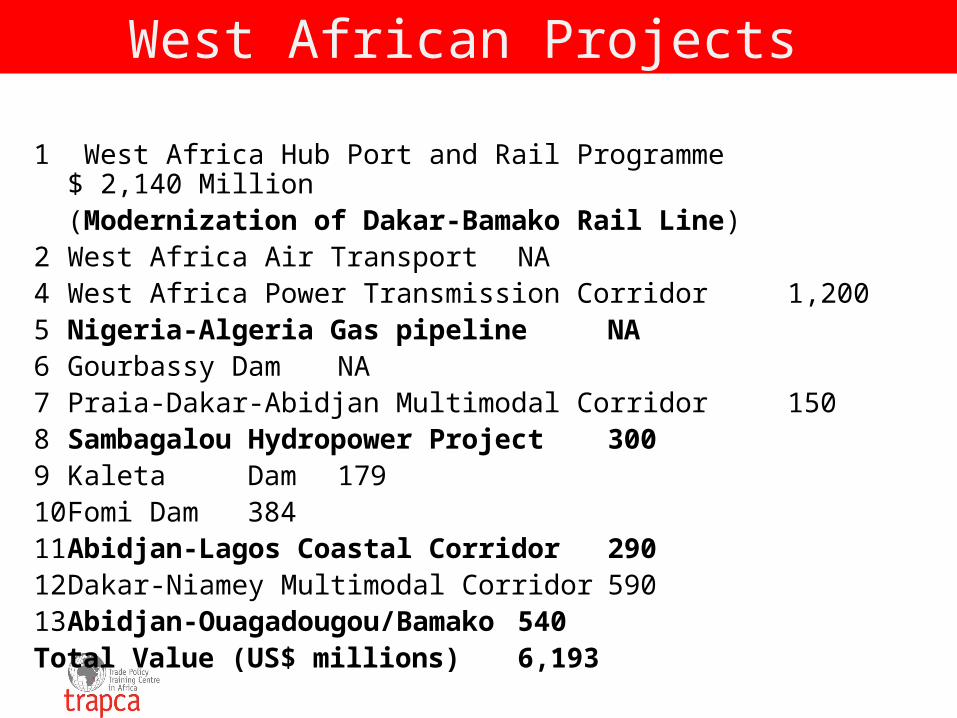

1 West Africa Hub Port and Rail Programme $ 2,140 Million(Modernization of Dakar-Bamako Rail Line)

2 West Africa Air Transport NA4 West Africa Power Transmission Corridor 1,2005 Nigeria-Algeria Gas pipeline NA6 Gourbassy Dam NA7 Praia-Dakar-Abidjan Multimodal Corridor 1508 Sambagalou Hydropower Project 3009 Kaleta Dam 17910 Fomi Dam 38411 Abidjan-Lagos Coastal Corridor 29012 Dakar-Niamey Multimodal Corridor 59013 Abidjan-Ouagadougou/Bamako 540Total Value (US$ millions) 6,193

West African Projects

1 Southern Africa Hub Port and Rail Programme $2,270million

2 Multisectoral Investment opportunity Studies 13 North - South Power Transmission Corridor 6,0004 Mphamda-Nkuwa Dam 2,4005 Lesotho HWP phase II hydropower component 8006 Lesotho HWP Phase II - water transfer component 1,100Total Value (US$ millions)

12,571

SADC Projects

• Africa should rethink its regulatory frameworks on trade and investment.

• We should define infrastructural needs based on what is able to promote linkages in the African economy.

• Need to create coherent policy that feed into promoting regional integration.

• The signing of Double Taxation Agreements should follow a carefully thought process that looks at national needs before committing to Mauritius-style agreements.

Conclusions

Related Documents