@TheBusJourney #SMEJourney Ian McMonagl e

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

@TheBusJourney #SMEJourney

Ian McMonagle

Chartered AccountantsChartered Tax Advisers

Business Development Specialists

Today’s agendaDIVIDENDS

Back to basics / legal aspects

Tax on dividends

Potential tax planning opportunities

Back to basicsOMB/ Private company limited by shares

Shareholders = owners, with limited liabilityDirectors have fiduciary dutiesCompany Act 2006Memo & Arts = power to declare dividends

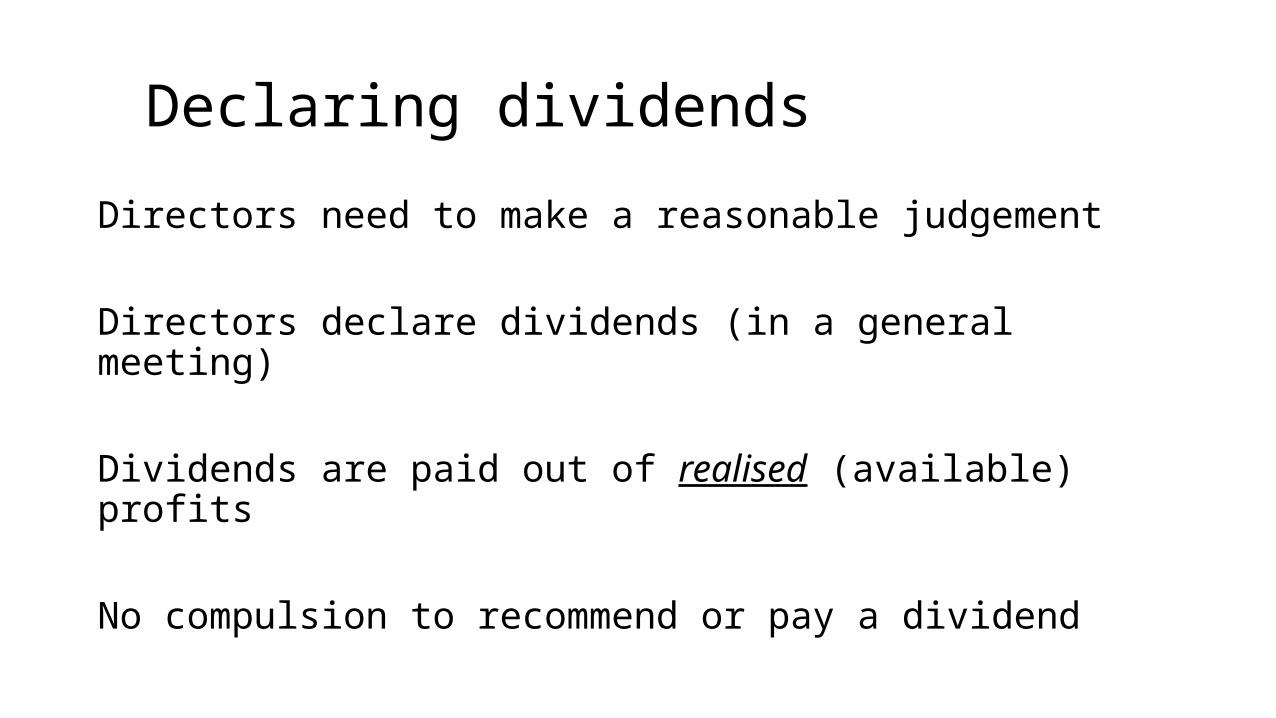

Declaring dividendsDirectors need to make a reasonable judgement

Directors declare dividends (in a general meeting)

Dividends are paid out of realised (available) profits

No compulsion to recommend or pay a dividend

Extract from HMRC websiteYour company mustn’t pay out more in dividends than its availableprofits from current and previous financial years.

You must usually pay dividends to all shareholders

To pay a dividend, you must:Hold a director’s meeting to ‘declare’ the dividendKeep minutes of the meeting, even if you’re the only director

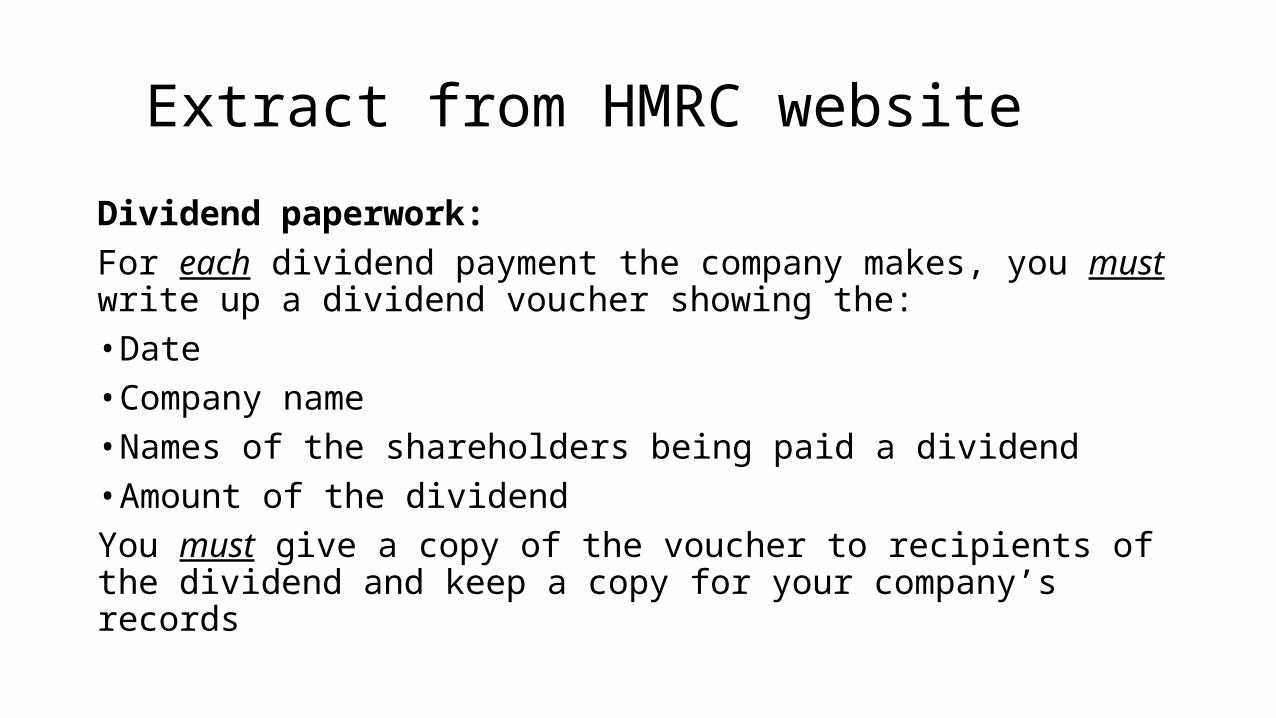

Extract from HMRC websiteDividend paperwork:For each dividend payment the company makes, you must write up a dividend voucher showing the:• Date• Company name• Names of the shareholders being paid a dividend• Amount of the dividendYou must give a copy of the voucher to recipients of the dividend and keep a copy for your company’s records

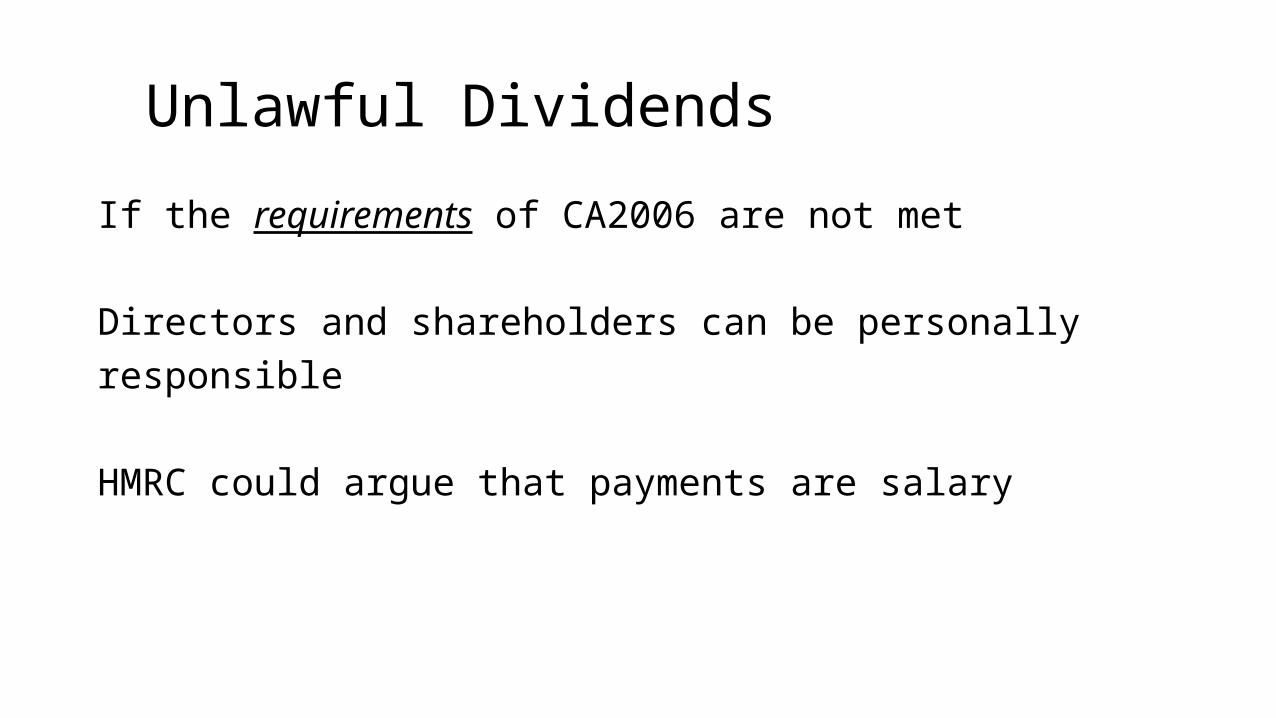

Unlawful DividendsIf the requirements of CA2006 are not met

Directors and shareholders can be personally responsible

HMRC could argue that payments are salary

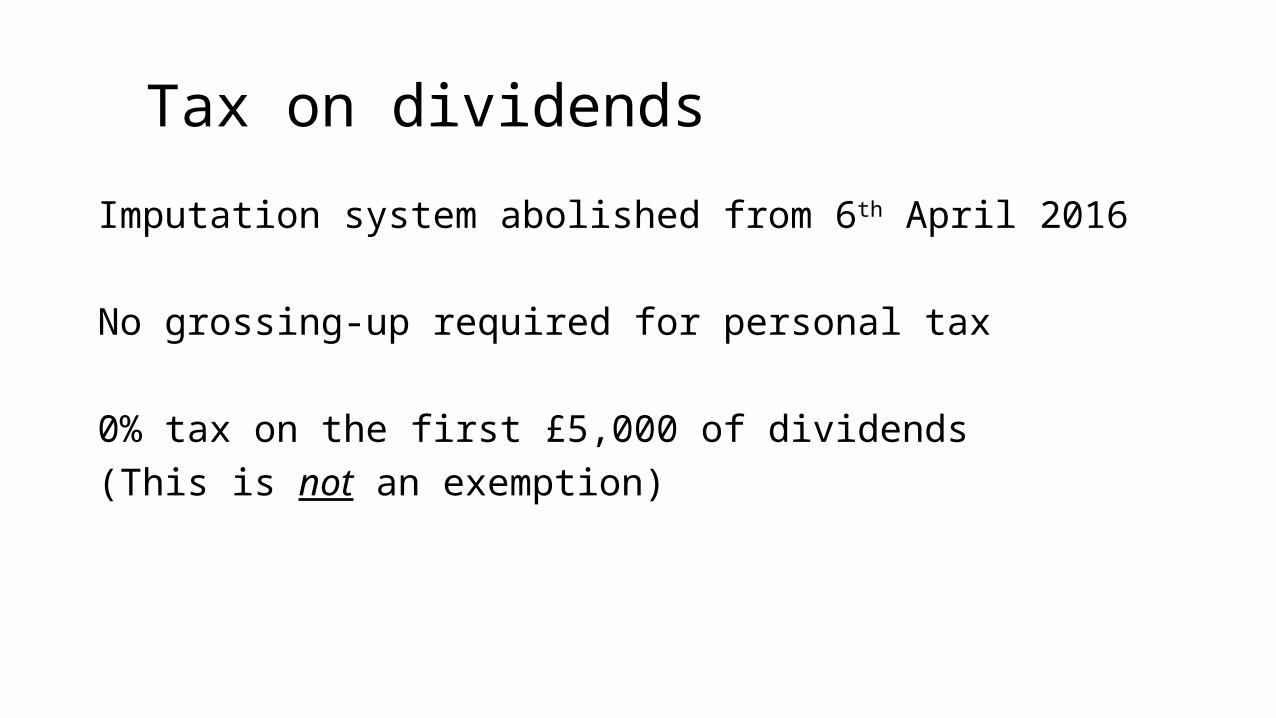

Tax on dividendsImputation system abolished from 6th April 2016

No grossing-up required for personal tax

0% tax on the first £5,000 of dividends(This is not an exemption)

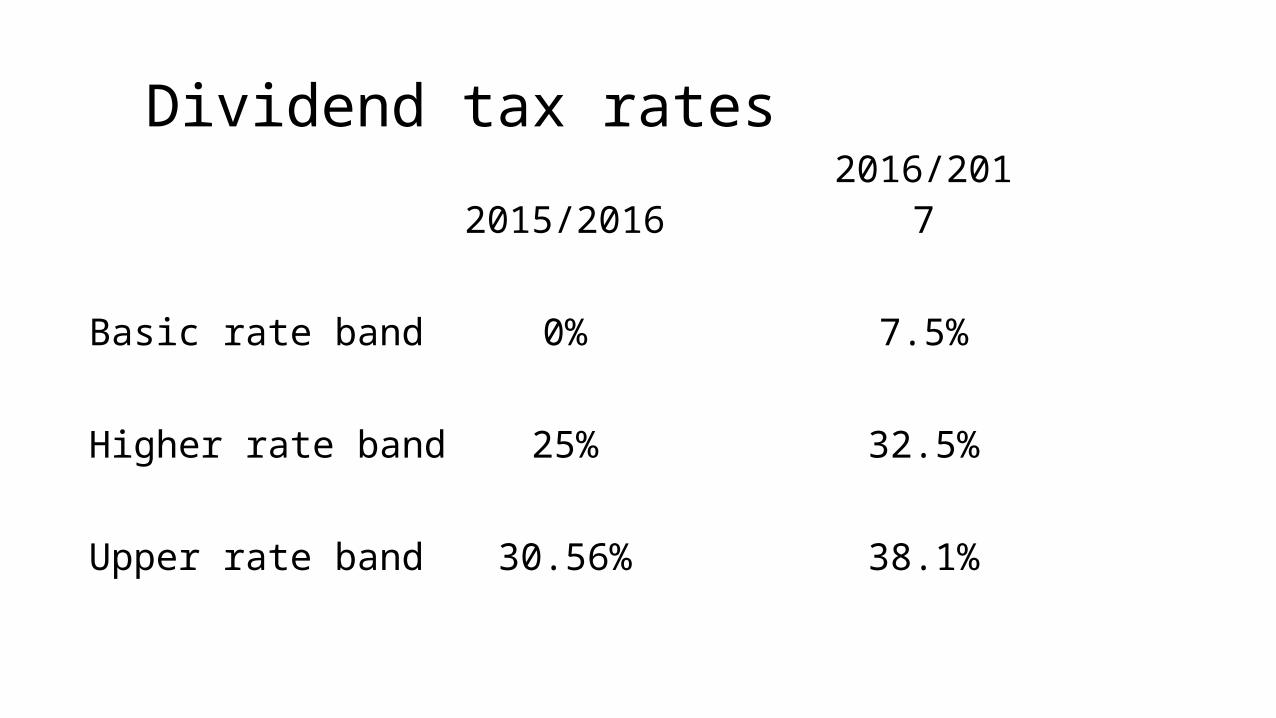

Dividend tax rates2015/2016 2016/2017

Basic rate band 0% 7.5%

Higher rate band 25% 32.5%

Upper rate band 30.56% 38.1%

Tax on dividendsIt’s difficult to directly compare

Tax and NIC free 2015/2016: £38,9532016/2017: £16,000

Basic rate ceiling 2015/2016: £38,953 = £0 tax2016/2017: £43,000 = £2,025 tax

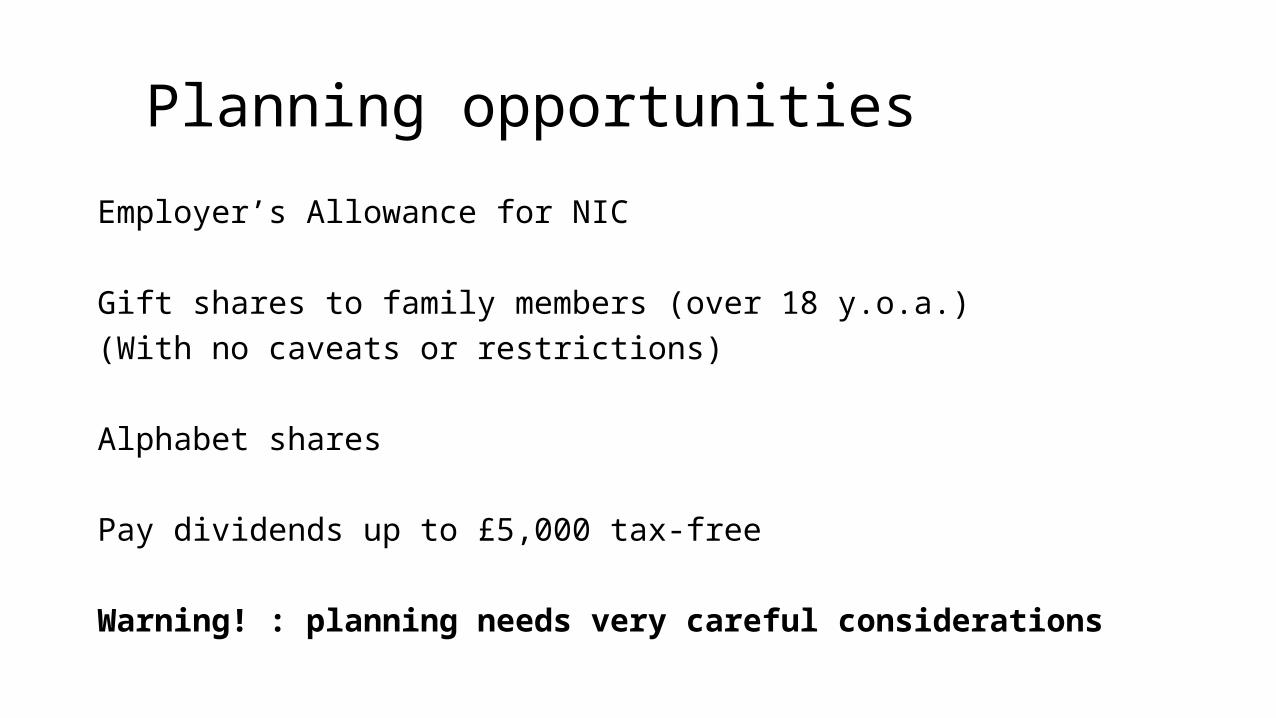

Planning opportunitiesEmployer’s Allowance for NIC

Gift shares to family members (over 18 y.o.a.) (With no caveats or restrictions)

Alphabet shares

Pay dividends up to £5,000 tax-free

Warning! : planning needs very careful considerations

In summary:Get the paperwork right each time

Prepare for potentially higher tax bills

Consider tax planning and share reconstruction

Get advice!

@TheBusJourney #SMEJourney

Thank you.

Related Documents