Tax is levied on total income of assesse. Under the provisions of Income-tax Act, 1961 the total income of each person is based upon his residential status. Section 6 of the Act divides the assessable into three categories: (i) Ordinary Resident; (ii) Resident but Not Ordinarily Resident; and (iii) Non-Resident. Meaning of Residential Status Residential status is a term coined under Income Tax Act and has nothing to do with nationality or domicile of a person. An Indian, who is a citizen of India can be non-resident for Income-tax purposes, whereas an American who is a citizen of America can be resident of India for Income-tax purposes. Residential status of a person depends upon the territorial connections of the person with this country, i.e., for how many days he has physically stayed in India. The residential status of different types of persons is determined differently. Similarly, the societal status of the assesse is to be determined each year with reference to the “previous year”. The residential status of the assesse may change from year to year. What is essential is the status during the previous year and not in the assessment year. 1. Residential Status in a previous year . Residential status is to be determined for each previous year. It implies that- (a) Residential status of assessment year is not important. (b) A person may be resident in one previous year and a non- resident in India in another previous year, e.g., Mr. A is

Tax Law

Dec 25, 2015

residential status, income tax act india,

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Tax is levied on total income of assesse. Under the provisions of Income-tax Act, 1961 the

total income of each person is based upon his residential status. Section 6 of the Act divides

the assessable into three categories:

(i) Ordinary Resident; (ii) Resident but Not Ordinarily Resident; and (iii) Non-Resident.

Meaning of Residential Status

Residential status is a term coined under Income Tax Act and has nothing to do with

nationality or domicile of a person. An Indian, who is a citizen of India can be non-resident

for Income-tax purposes, whereas an American who is a citizen of America can be resident of

India for Income-tax purposes. Residential status of a person depends upon the territorial

connections of the person with this country, i.e., for how many days he has physically stayed

in India.

The residential status of different types of persons is determined differently. Similarly, the

societal status of the assesse is to be determined each year with reference to the “previous

year”. The residential status of the assesse may change from year to year. What is essential is

the status during the previous year and not in the assessment year.

1. Residential Status in a previous year. Residential status is to be determined

for each previous year. It implies that-

(a) Residential status of assessment year is not important.

(b) A person may be resident in one previous year and a non-resident in India in another

previous year, e.g., Mr. A is resident in India in the previous year 2008-09 and in the very

next year he becomes a non-resident in India.

2. Duty of Assessee. It is assessee’s duty to place relevant facts, evidence and

material before the Income Tax Authorities supporting the determination of Residential

status.

3. Dual Residential Status is possible. A person may be resident of one or more

countries in a relevant previous year e.g., Mr. X may be resident of India during previous

year 2009-10 and he may also be resident/non-resident in England in the same previous year.

The emergence of such a situation depends upon the following:

(a) the existence of the Residential status in countries under considerations

(b) the different set of rules having laid down for determination of residential status.

Determination of Residential status of different

‘Persons’

Income tax is charged on every person. The term ‘Person’ has been defined under section 2(31) includes:

(i) An individual

(ii) Hindu Undivided Family

(iii) Firm

(iv) Company

(v) AOP/BOI

(vi) Local authority

(vii) Every other artificial juridical person not falling in preceding six sub-classes.

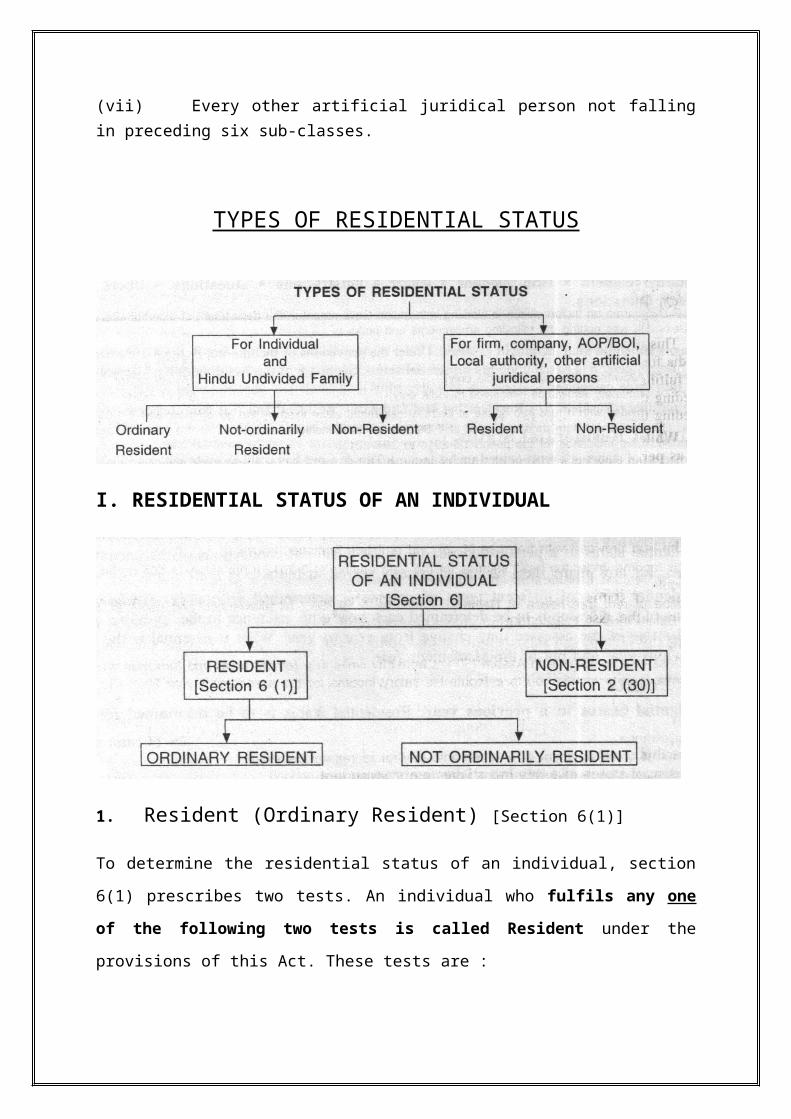

TYPES OF RESIDENTIAL STATUS

I. RESIDENTIAL STATUS OF AN INDIVIDUAL

1. Resident (Ordinary Resident) [Section 6(1)]

To determine the residential status of an individual, section 6(1) prescribes two tests. An

individual who fulfils any one of the following two tests is called Resident under the

provisions of this Act. These tests are :

(a) If he is in India during the relevant previous year for a period amounting in all to 182

days or more.

OR

(b) If he was in India for a period or periods amounting in all to 365 days or more during

the four years preceding the relevant previous year and he was in India for a period or

periods amounting in all to 60 days or more in that relevant previous year.

Explanation— (a) In case of individual being a citizen of India who leaves India in any

previous year as a member of the crew of an Indian ship as defined in clause (18) of

section 3 of the Merchant Shipping Act 1958 (44 of 1958) or for the purposes of

employment outside India the provisions of sub¬-clause (b) as given above shall apply

in relation to that year as if the words “sixty days” have been substituted by “182 days”.

(b) In case of an individual being a citizen of India, or a person of Indian origin

within the meaning of explanation to clause (e) of section 115 C, who being outside

India, comes on a visit to India in any previous year, the provisions of sub-clause (b)

shall apply in relation to that year as if for the words. ‘Sixty days occurring therein the

words One hundred and eighty two days had been substituted. ’

After fulfilling one of the above two tests, an individual becomes resident of India but to

become in ordinary resident of India an individual has to fulfill both the following two

conditions:

(1) He has been resident of India (fulfilling at least one test given above) in at least 2

previous years out of 10 previous years immediately prior to the previous year in

question.

(2) He has stayed in India for at least 730 days in 7 previous years immediately preceding

the previous year in question.

This means that an individual will not become an ordinary resident of India by simply staying

in India for a period of 182 days or more in a previous year. He will become ordinary resident

only if he fulfils one of these two tests and was also fulfilling one of the tests in at least 2

previous years preceding the relevant previous year and did stay in India for at least 730 days

in 7 previous years preceding the relevant previous year.

As per decision of Authority for Advance Rulings, both, day of departure from India

and day of arrival in India are to be counted as stay in India.

Tests explained

Test No. 1. Stay in India for 182 days or more

If an individual is to become resident of India during any previous year, his/her personal stay

in India during that year is a must although the number of days of stay differs in the two tests.

It means that if an individual does not stay in India at all in any previous year, he cannot be

resident of India in that year. Stay in India means that the individual should have stayed in

Indian Territory and anywhere (cities, villages, hills, even Indian territorial waters) for such

number of days.

The period of 182 days need not be at a stretch. But physical presence for an aggregate of 182

days in the relevant previous year is enough. The status of resident is not linked with any

particular place or town or house.

The onus to prove the number of days of stay in India lies on the assessee. It is for him to

prove, if he desires to be taxed as non-resident or not ordinarily resident.

Test No. 2. Presence for 365 days during the four preceding previous years

A person may be a frequent visitor to India. In his case, the residential status will be

determined on the basis of his presence in India for 365 days in four years immediately

preceding the relevant previous year. Along with this his presence for 60 days during the

relevant previous year is another essential condition to be fulfilled. The purpose, object or

reason of visit to and stay in India has nothing to do with the determination of residential

status.

For Indian citizen going abroad on a job or as a member of crew of an Indian ship

[Explanation (a)]

In case of an Indian citizen:

(a) Who is going outside India for a job and his contract for such employment

outside India has been approved by the Central Government; or

(b) He is a member of crew of an Indian ship;

test (a) u/s 6(1) remains the same but in test (b) 60 days have been replaced by 182 days. The

practical effect of this explanation is that in case of persons of Indian citizenship going

abroad on a job approved by the Central Government only test (a) is to be applied during the

year he is leaving India.

For Indian citizens and persons of Indian origin [Explanation (b)]

For such persons test (a) remains the same but in test (b) words ‘60 days' have been replaced

by 182 days.

The practical effect of this provision is that those persons who are Indian citizens or persons

of Indian origin living outside India and when they come to visit India only test (a) of 6 (1) is

to be applied.

A person shall be deemed to be of Indian origin if he or either of his parents or any of his

grandparents was born in India or undivided India [Section 115 (c) explanation to clause (c)].

2. Resident but not Ordinarily Resident [Section 6(6)]

An individual who is resident u/s 6(1) can claim the beneficial status of N.O.R. if he can prove

that :

(a) He was non-resident in India for 9 previous years out of 10 previous years preceding

the relevant previous year.

OR

(b) He was in India for a period or periods aggregating in all to 729 days or less during

seven previous years preceeding the relevant previous year.

An individual who is Resident u/s 6(1) can be subdivided into two categories:

(a) Ordinary Resident; or (b) Not ordinarily Resident

Ordinary Resident Resident But Not Ordinarily Resident

(a) He was in India for a period or periods totaling in all to 182 days or more during relevant previous year.

OR(b) He was in India for a period or periods totaling in all

to 60 days or more during relevant previous year and 365 days or more during four previous years preceding the relevant previous year.

AndMust be resident of India (by fulfilling atleast one of two above mentioned tests) in atleast 2 out of 10 previous years preceding the relevant previous year.

AndMust have stayed in India for 730 days or more during 7 previous years preceding the relevant previous year.

(a) He was in India for a period or periods totaling in all to 182 days or more during relevant previous year.

OR(b) He was in India for a period or periods totaling in all

to 60 days or more during relevant previous year and 365 days or more during four previous years preceding the relevant previous year.

AndWas non-resident in India in 9 or 10 previous years out of 10 previous years preceding the relevant previous year.

ORWas in India for less than 730 days during 7 previous years preceding the relevant previous year.

3. Non-Resident [Section 2(30)]

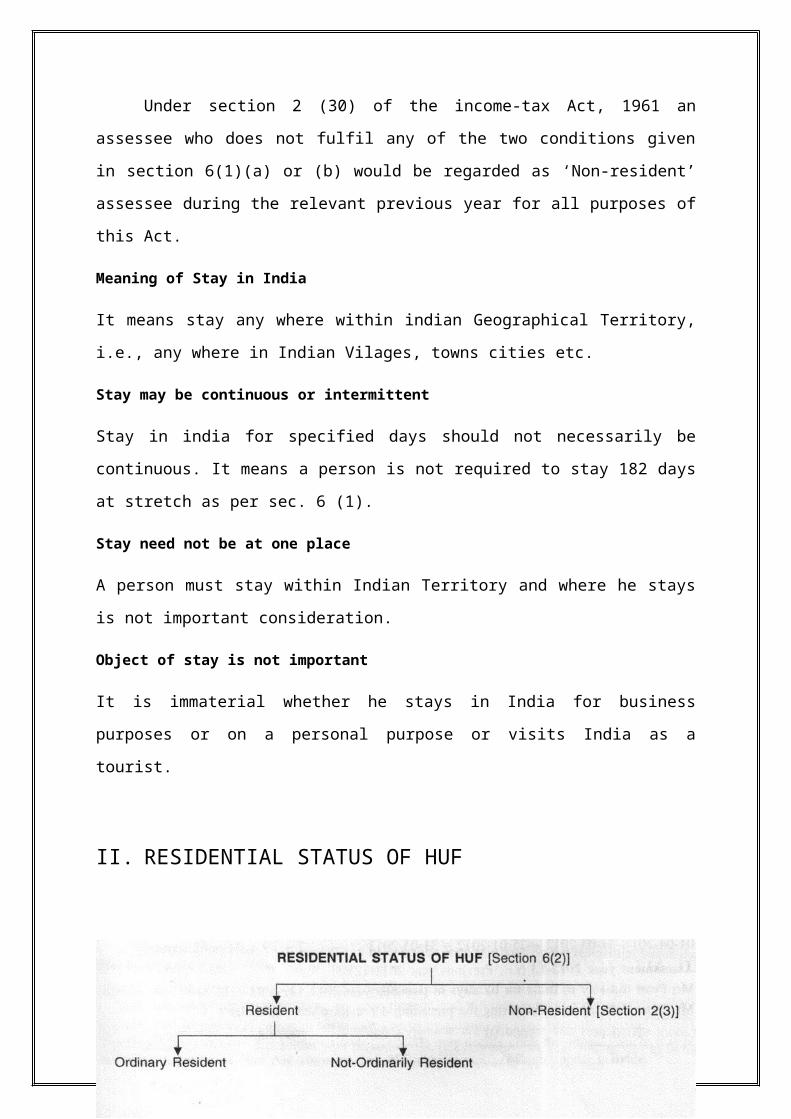

Under section 2 (30) of the income-tax Act, 1961 an assessee who does not fulfil any

of the two conditions given in section 6(1)(a) or (b) would be regarded as ‘Non-resident’

assessee during the relevant previous year for all purposes of this Act.

Meaning of Stay in India

It means stay any where within indian Geographical Territory, i.e., any where in Indian

Vilages, towns cities etc.

Stay may be continuous or intermittent

Stay in india for specified days should not necessarily be continuous. It means a person is not

required to stay 182 days at stretch as per sec. 6 (1).

Stay need not be at one place

A person must stay within Indian Territory and where he stays is not important consideration.

Object of stay is not important

It is immaterial whether he stays in India for business purposes or on a personal purpose or

visits India as a tourist.

II. RESIDENTIAL STATUS OF HUF

1. Ordinary Resident [Section 6(2)]

HUF, is said to be resident in every case except where during that year the control and

management of its affairs is situated wholly outside India. It means that if a HUF is

controlled from India even partially it will be resident assessee.

The control and management of affairs refers to the controlling and directing power, the head

and the brain. It means that decision making power for vital affairs is situated in India. The

control and management means de-facto control and management and not merely the right to

control or manage.

2. Not Ordinarily Resident [Section 6(6) (b)]

It is only HUF besides individual, which can claim the advantageous status of Not Ordinarily

Resident. A HUF will be ‘Not Ordinarily Resident’ if:

(i) its manager (Karta) has not been resident in India in nine out of ten previous years

preceding the relevant accounting year; or

(ii) the manager had not, during the seven previous years preceding the relevant previous

year been present in India for a period or periods amounting in all to 730 days. [Section

6(6)(b)].

These two tests have to be applied in case of manager (Karta) of such HUF. In case the Karta

has been succeeded by some other man, for computing the presence in India, the length of

presence in India of each succeeding Karta will be added.

While determining the residential status of a HUF it should be noted that residential status of

coparceners of a HUF is of immaterial consideration. What is important to note is that from

where the business of HUF is being controlled.

Not ordinarily resident status of HUF is linked with the status of its Karta. So if Karta taken

as an individual is not ordinarily resident then the status of his HUF shall also be not

ordinarily resident.

3. Non-Resident [Section 2(30)]

HUF, shall be non-resident in India if the control and management of affairs is situated

wholly outside India.

Ordinary Resident Not Ordinarily Resident Non-Resident

If control or management of such HUF was wholly or partially in India during relevant the previous year.

This status is allowed only to HUF along with individuals. HUF shall be NOR if its Karta can fulfill any one of the two tests given u/s 6(6) for an individual.

If control or management of such HUF was wholly outside India during relevant the previous year.

III. ALL OTHER PERSONS

IIIA. RESIDENTIAL STATUS OF FIRM AND AOP, OR BOI

1. Ordinary Resident [Section 6(2)]

IIIA. RESIDENTIAL STATUS OF FIRM AND AOP, OR BOI

1. Ordinary Resident [Section 6(2)]

A firm, an Association of persons (AOP) or body of individuals (BOI) is said to be resident in

every case except where during that year the control and management of its affairs is situated

wholly outside India. It means that if A firm, an association of persons (AOP) or body of

individuals (BOI) is controlled from India even partially it will be resident assessee.

The control and management of affairs refers to the controlling and directing power, the head

and the brain. It means that decision-making power for vital affairs is situated in India. The

control and management means de-facto control and management and not merely the right to

control or manage.

In case of a firm, it is said that the control and management of firm is situated at a place

where partners meet to decide the affairs of the firm. If such place is outside India, it will be

said that the control and management is outside India.

There may be a situation where all the partners of a firm are resident in India but even then

that firm may be non-resident if its full control and management lies outside India.

2. Not Ordinarily Resident

A firm, an Association of Persons (AOP) or body of individuals (BOI) cannot claim the status

of Not Ordinarily Resident. All these assessees shall be either resident in India or non-

resident in India.

3. Non-Resident [Section 2(30)]

A firm, or association of persons shall be non-resident if the control and management of

affairs is situated wholly outside India.

Ordinary Resident Not Ordinarily Resident Non-Resident

If control or management of such a firm, an Association of Persons (AOP) or body of individuals (BOI) was wholly or partially in India during the relevant previous year.

A firm, an Association of Persons (AOP) or body of individuals (BOI) cannot claim this status.

If control or management of such a firm, an Association of Persons (AOP) or body of individuals (BOI) was wholly outside India during relevant previous year.

IIIB. RESIDENTIAL STATUS OF A COMPANY [Section 6(3)]

The residential status of a company is to be determined on the basis of its incorporation or

registration. Section 6(3) provides the following tests in this connection.

1. Resident

A company is resident in India if:

(i) it is an India company, or

(ii) during the previous year, control and management of its affairs is situated wholly

in India.

2. Not Ordinarily Resident

A company cannot have this status. It can either be resident or non-resident.

3. Non-resident [Section 2(30)]

A company shall be ‘non-resident’ if it is not resident in India during the relevant accounting

year. It means that, a company whose control and management is situated wholly or partially

outside India, will be non-resident company.

IIIC. RESIDENTIAL STATUS OF EVERY OTHER PERSON

[Section 6(4)]

Every other person includes body of individuals, a local authority and an artificial juridical

person. They are either ‘Resident’ or “Non-Resident” but they cannot be Not ordinarily

resident.

The test to be applied shall be that of control and management. If it is situated wholly outside

India, the assessee will be non-resident. If the control and management is wholly or partially

situated in India, the status will be that of ‘Resident’.

Ordinary Resident Not Ordinary Resident Non-Resident

COMPANYEvery Indian company [i.e. which is incorporated under Indian Law or is is deemed as comapny under any law of the country] is Resident company. In case of any other company, which is incorporated outside India but has its control or management in India during relevant previous year it is also a resident company.

A company cannot enjoy this status.

Any company, which is incorporated outside India and has its control or management outside India during relevant previous year is non-resident company.

IN CASE OF EVERY OTHER PERSONIn case of every other person, which has its control or management wholly in India during relevant previous year is resident.

Any other person cannot enjoy this status.

Any other person, who has its control or management wholly outside India during relevant previous year is non-resident.

1. Whether an assessee is Resident or non-Resident, it is a question of fact. The onus to

prove all the facts before the requisite authorities lies on the assessee.

2. An assessee cannot have different residential status for different sources of income. If a

person is resident in India for one source of income in a particular previous year, he shall

be deemed to be resident in that particular previous year in respect of all of his other

sources of income. [Section 6(5)].

3. The residential status of a company would change with change in place of control and

management of its affairs. A company can be resident in one year and non-resident in

another.

RESIDENTIAL STATUS IN NUTSHELL

Ordinary Resident Resident But NOR Non-Resident

INDIVIDUAL(a) He was in India for a period or periods totaling in all to 182 days or more during relevant previous year

OR(b) He was in India for a period or periods totaling in all to 60 days or more during relevant previous year and 365 days or more during four previous years preceding the relevant previous year. And

(a) He was in India for a period or periods totaling in all to 182 days or more during relevant previous year OR(b) He was in India for a period or periods totaling in all to 60 days or more during relevant previous year and 365 days or more during four previous years preceding the relevant previous year. And

He fails to fulfill both the tests of section 6(1).

Must be Resident in India in 2 out of 10 previous years preceding the relevant previous year ; And Must be in India for 730 days or more during 7 previous years preceding the relevant previous year.

U/s 6(6) was non resident in 9 or 10 previous years out of 10 previous years preceding relevant previous year ; ORwas in India for less than 730 days during 7 previous years preceding the relevant previous year.

IIUF, FIRM, AOP, BOIIf control or management of HUF, FIRM, AOP, BOI was wholly or partially in India during relevant previous year.

This status is allowed only to HUF and others cannot claim it. HUF shall be NOR if its Karta can fulfill any one of the two tests given u/s 6(6) for an individual.

If control or management of such HUF. FIRM, AOP, BOI was wholly outside India during relevant previous year.

COMPANYEvery Indian compnay [i.e. which is incorporated under Indian Law or is deemed as company under any law of the country] is Resident company.In case of any other company, which is incorporated outside India but has its control or management in India during relevant previous year is also a resident company.

A company cannot enjoy this status. Any company, which is incorporated outside India and has its control or management outside India during relevant previous year is non-resident company.

IN CASE OF EVERY OTHER PERSONIn case of every other person, which has its control or management wholly in India during relevant previous year is resident.

Any other person cannot enjoy this status. Any other person, which has its control or management wholly outside India during relevamt previous year is non-resident.

INCIDENCE OF TAX (SCOPE OF TOTAL INCOME)

The tax is levied on total income of a person. The total income is based upon the residential

status of an assessee. Section 5 provides the scope of total income which varies on the basis

of status. Section 5 provides :

1. Subject to the provisions of this Act, the total income for any previous year of a

person who is resident includes all incomes from whatever source derived, which,

(a) is received or is deemed to be received in India in such year by or on behalf of such

person; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year; or

(c) accrues or arises to him outside India during such year;

Provided that, in the case of a person not ordinarily resident in India within the

meaning of sub-section (6) of section 6 the income which accrues or arises to him

outside India shall not be included unless it is derived from business controlled in or

a profession set up in India.

2. Subject to the provisions of this Act. the total income of any previous year of a person

who is a non-resident includes all incomes from whatever source derived, which,

(a) is received or is deemed to be received in India in such year by or on behalf of such

person; or

(b) accrues or arises or is deemed to accrue or arise to him in India.

The above provisions of section 5 can be expressed in following manner:

(i) Scope of total income of ‘a Resident’ [Section 5(1)]

(a) Income received or deemed to be received in India during the relevant accounting year. The place and date of accrual is immaterial.

(b) Income which accrues or arises or is deemed to accrue or arise in India during the relevant accounting year irrespective of the date and place of its receipt.

(c) Income accruing during the relevant accounting year outside India whether it is brought or not in India during the year.

Scope of Income = Indian Income + Foreign Income

(ii) Scope of total income of ‘Not Ordinarily Resident’ [Section 5(1)]

(a) Income received or deemed to be received in India during the relevant accounting year. The date and place of accrual is immaterial.

(b) Income which accrues or arises or is deemed to accrue or arise in India during the relevant accounting year irrespective of the date and place of its receipt.

(c) Income accruing or deemed to accrue or deemed to be received outside India during the relevant accounting year from a business set up in and controlled from India.

Scope of Income = Indian Income + One particular type of foreign income

(iii) Scope of total income of ‘Non-Resident’ [Section 5(2)]

(a) Income received or deemed to be received in India during the relevant accounting year. The date and place of accrual is immaterial.

(b) Income which accrues or arises or is deemed to accrue or arise in India during the relevant accounting year irrespective of the date and place of its receipt.

Scope of Income = Indian Income

TYPES OF INCOMES

Broadly income can be divided into two categories :

(a) Indian Income

(b) Foreign Income.

A. Indian Income

Indian income is called by various words and names. These are :

(1) Income earned in India.

(2) Income accrues and arises in India.

(3) Income received or deemed to be received in India.

(4) Income payable in India. Income may have been earned in a foreign country but it is payable in India.

(5) Income earned (or accrues) in India but is is received or payable outside India.

B. Foreign Income

Following types of incomes are called foreign incomes:

(1) Income earned (or accrues) outside India and also received outside India.

(2) Any income which is not earned or accrues or arises in India.

(a) Income received in India. Receipt of a particular income in India attracts tax

liability. The essential fact is that a person must receive income in India during the relevant

previous year. The income may be received by the assessee himself or by his agent, banker or

broker on his behalf in India. It is not essential that a person must receive income either from

business or salary. Assessee may receive income from any source.

All persons are assessable on income received in India during the relevant previous year

irrespective of the residential status.

Income received in money or money’s worth is taxable. Only thing essential is that it must be

certain that the receipt in the form of money’s worth must be income.

(b) Income deemed to be received in India. Such incomes which are not actually

received by a person, but law considers them as receipt or incomes, are called incomes

deemed to be received in India. The term ‘Statutory receipts’ can be easily used to cover this

term. Following are the instances of incomes deemed to be received :

Tax deducted at source is income deemed to be received by a person even though he never

receives such income (u/s 198), Section 7 - Employer’s contribution to provident fund,

Interest accrued on provident fund balance, Taxable portion of transferred balance of URPF

to RPF, Tax deducted at source.etc.

(c) Income which ‘Accrues’ or ‘Arises’ in India. Income can be held to accrue or arise

to an assessee only when the assessee obtains a right to receive that income. No amount can

be said to accrue unless it is actually due.

(d) Income deemed to Accrue or Arise in India. Under section 9(1) of the Indian Income-tax Act, the following incomes are deemed to accrue or arise in India :

(i) Income arising from business connection in India [Section 9(l)(i)]

(ii) Income from any property held in India and assets or sources of income located in India

(iii) Income from transfer of capital assets situated in India

(iv) Apportionment of profits [Explanation to section 9(l)(i)]

(v) Purchase of goods in India for export (Exp. to section 9)

(vii) Salaries for Government service outside India [Section 9(1) (iii)]

(viii) Dividend paid abroad by Indian Company [Section 9(l)(iv)]

(ix) Income by way of interest [Section 9(l)(v)]

(x) Income by way of royalty [Section 9(l)(vi)]

(xi) Income by way of fees for technical services [Section 9(1) (vii)]

(xii) Income from shooting of any picture in India [Explanation to section 9(1) (i)(d)]

SUMMARISED CHART

Different kinds of Incomes Different Types of Status

Resident Not Ordinarily Resident

Non-Resident

1. Income received or deemed to be

received in India. It is immaterialwhether it is earned in India or in aforeign country. Taxable Taxable Taxable

2. Income earned in India whetherreceived, paid in India or outsideIndia. Taxable Taxable Taxable

3. Income earned and received outside

India from a business controlled orprofession set up in India. Income mayor may not be remitted to India. Taxable Taxable Not

4. Income earned or received outside India

from a business controlled or professionset-up outside India. Taxable Not Not

5. Income earned and received outside

India from any other source (Exceptincome under point 3). Taxable Not Not

6. Income earned and received outside

India in the years preceding theprevious year in question and if thesame is remitted to India during thecurrent previous year. Not Not Not

BIBLIOGRAPHY

Gaur.V.P: Narang D.B : Income Tax Law And Practice: 42nd Edn; Kalyani Publishers.

Singhania, V.K; Taxmann Students Guide to Income Tax: 46th edn.

Related Documents