Tax Increment Financing and New Markets Tax Credit Incentives for Real Estate Development Materials Prepared for Discussion Courtney D. Pogue, CCIM, CEcD, LEED AP, CPM

Tax Increment Financing and New Markets Tax Credit Incentives for Real Estate Development Materials Prepared for Discussion Courtney D. Pogue, CCIM, CEcD,

Dec 31, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Tax Increment Financing and New Markets Tax Credit

Incentives for Real Estate Development

Materials Prepared for Discussion Courtney D. Pogue, CCIM, CEcD, LEED AP, CPM

development cost

development cost

front-end

costs

amount financed

mortgage-financing

costs

mortgage-financing

costs

debt service

operating costs

operating costs

cash flow

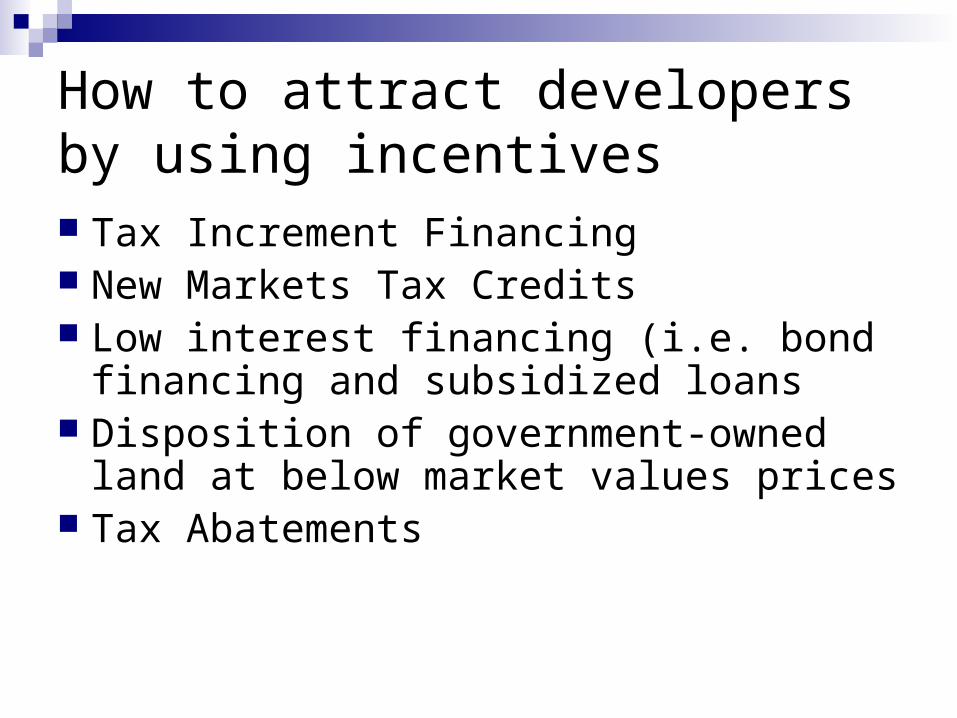

How to attract developers by using incentives Tax Increment Financing New Markets Tax Credits Low interest financing (i.e. bond financing

and subsidized loans Disposition of government-owned land at

below market values prices Tax Abatements

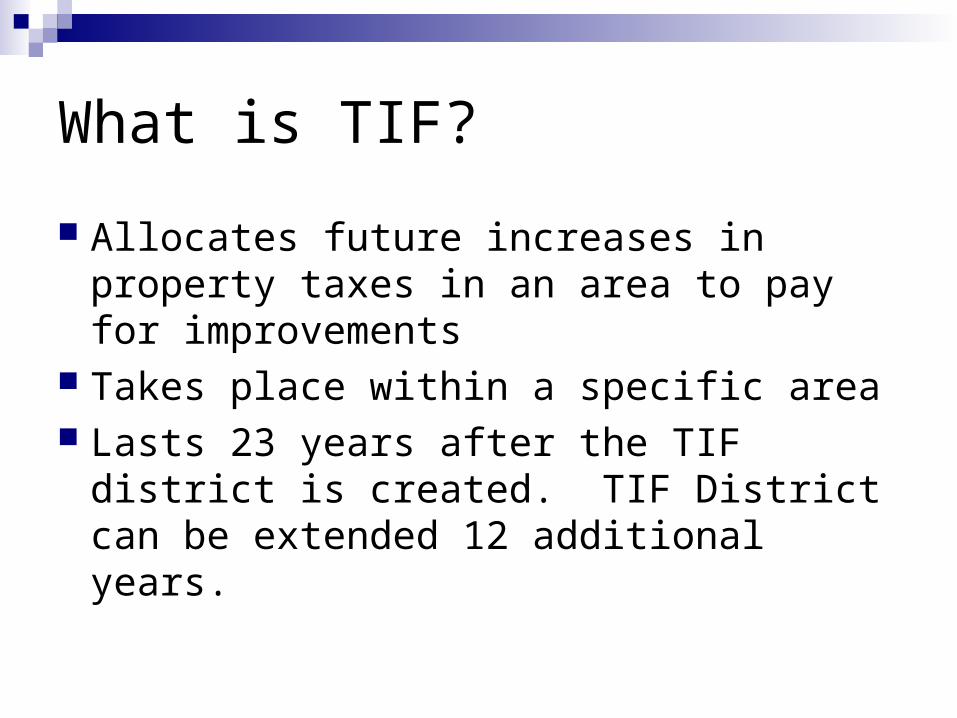

What is TIF?

Allocates future increases in property taxes in an area to pay for improvements

Takes place within a specific area Lasts 23 years after the TIF district is

created. TIF District can be extended 12 additional years.

Tax Increment Financing Eligible Costs Property Assembly Costs Site Preparation Rehabilitation existing structures Low-income housing construction (50% of Hard Costs Eligible) Public works or improvements Studies, surveys, planning, legal, financial consultants, and

administration Developer’s interest costs Relocation Job training and Retraining Programs Day care Financing costs associated with debt obligations Soft Costs related to TIF Eligible Hard Costs

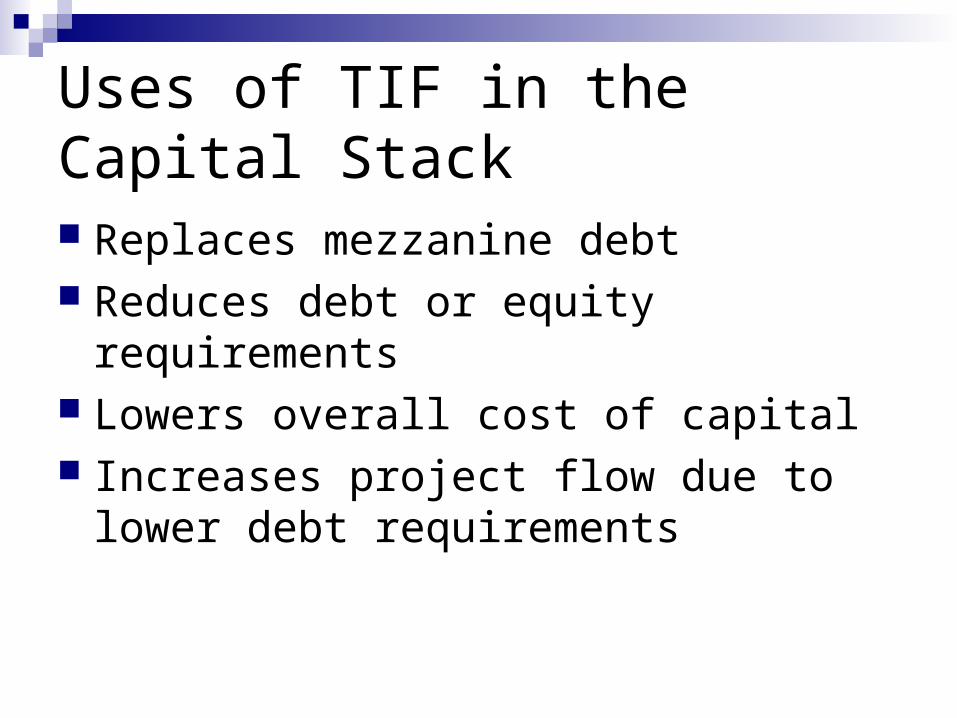

Uses of TIF in the Capital Stack

Replaces mezzanine debt Reduces debt or equity requirements Lowers overall cost of capital Increases project flow due to lower debt

requirements

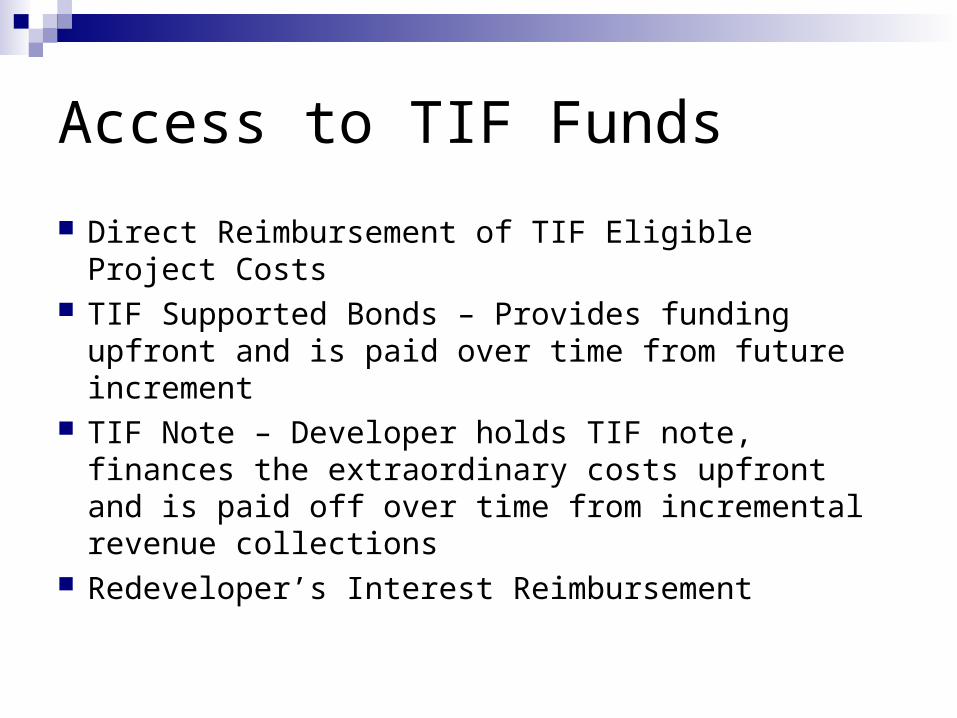

Access to TIF Funds

Direct Reimbursement of TIF Eligible Project Costs

TIF Supported Bonds – Provides funding upfront and is paid over time from future increment

TIF Note – Developer holds TIF note, finances the extraordinary costs upfront and is paid off over time from incremental revenue collections

Redeveloper’s Interest Reimbursement

Basic TIF Gap Analysis

Project w/o TIF Project with TIF

Project Revenue $23,668,297 $27,868,297

Total Development Costs (TDC) $25,553,070 $25,553,070

Profit/(Loss) ($1,884,773) $2,315,227

TIF Amount $0 $4,200,000

Profit as % of TDC (7.38%) 9.06%

TIF Request as % of TDC 0.0% 15.1%

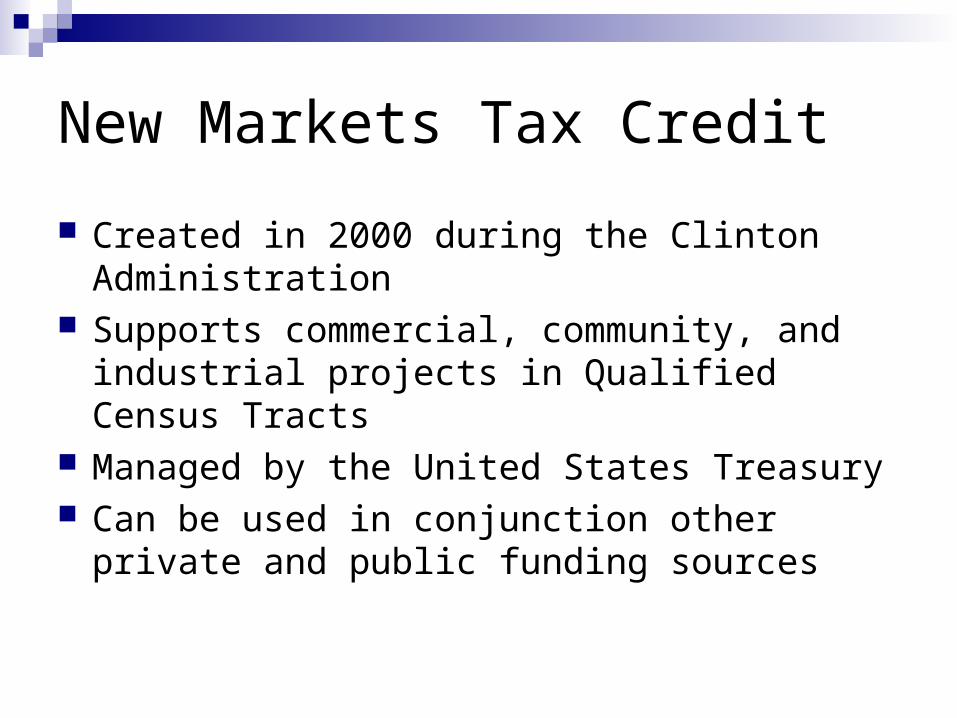

New Markets Tax Credit

Created in 2000 during the Clinton Administration Supports commercial, community, and industrial

projects in Qualified Census Tracts Managed by the United States Treasury Can be used in conjunction other private and

public funding sources

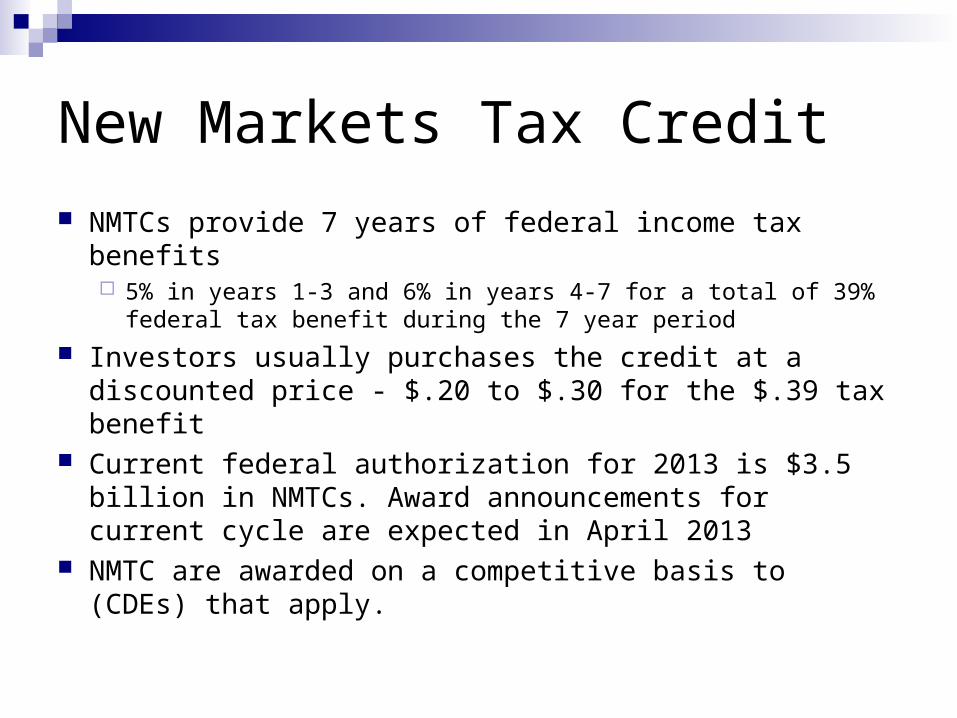

New Markets Tax Credit

NMTCs provide 7 years of federal income tax benefits 5% in years 1-3 and 6% in years 4-7 for a total of 39% federal

tax benefit during the 7 year period

Investors usually purchases the credit at a discounted price - $.20 to $.30 for the $.39 tax benefit

Current federal authorization for 2013 is $3.5 billion in NMTCs. Award announcements for current cycle are expected in April 2013

NMTC are awarded on a competitive basis to (CDEs) that apply.

New Markets Tax Credit Benefits to the Real Estate Developer

Lower capital costs Loan forgiveness Additional sources provided to the capital stack

20% to 30% of the capital stack Can be combined with other capital sources Fills the financing gap with inexpensive capital

Benefits to the NMTC Investor Equity Investment in Qualified Census Tract Returns only expected from NMTC tax benefits

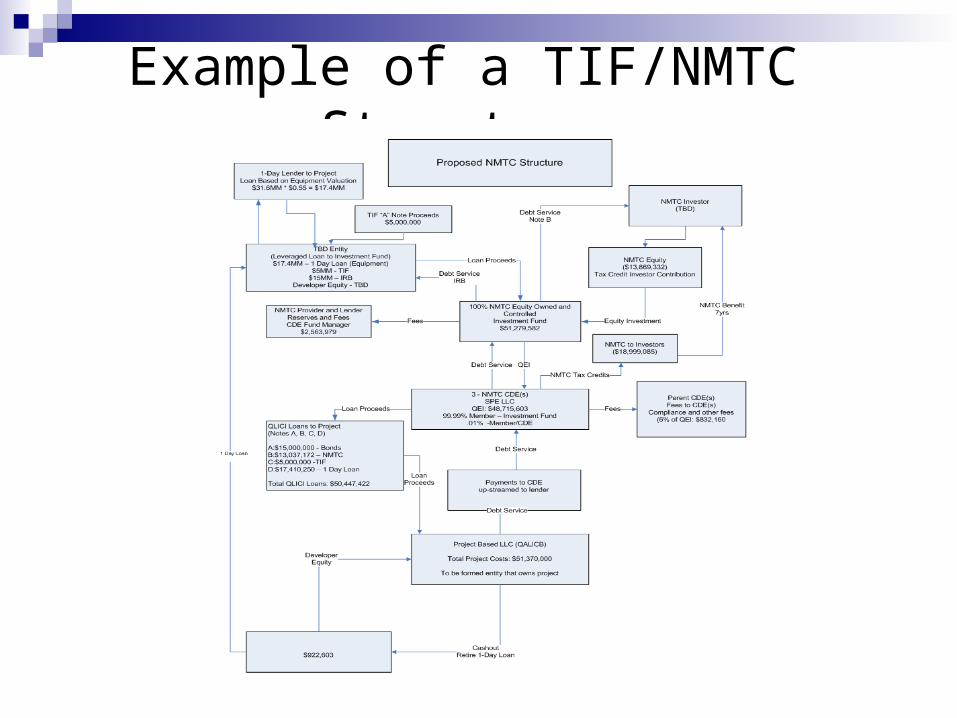

Example of a TIF/NMTC Structure

Overview of TIF and NMTC

Projects today require multiple financing tools Public-private partnerships have become more common Capital providers are becoming more comfortable with

the mixed-finance deal structures Each project and deal structure is unique Developers, financial advisors, and attorneys understand

the level of creativity and patience needed to close a transaction

NMTC and/or TIF during the economic downturn aided in helping numerous projects being completed.

Related Documents