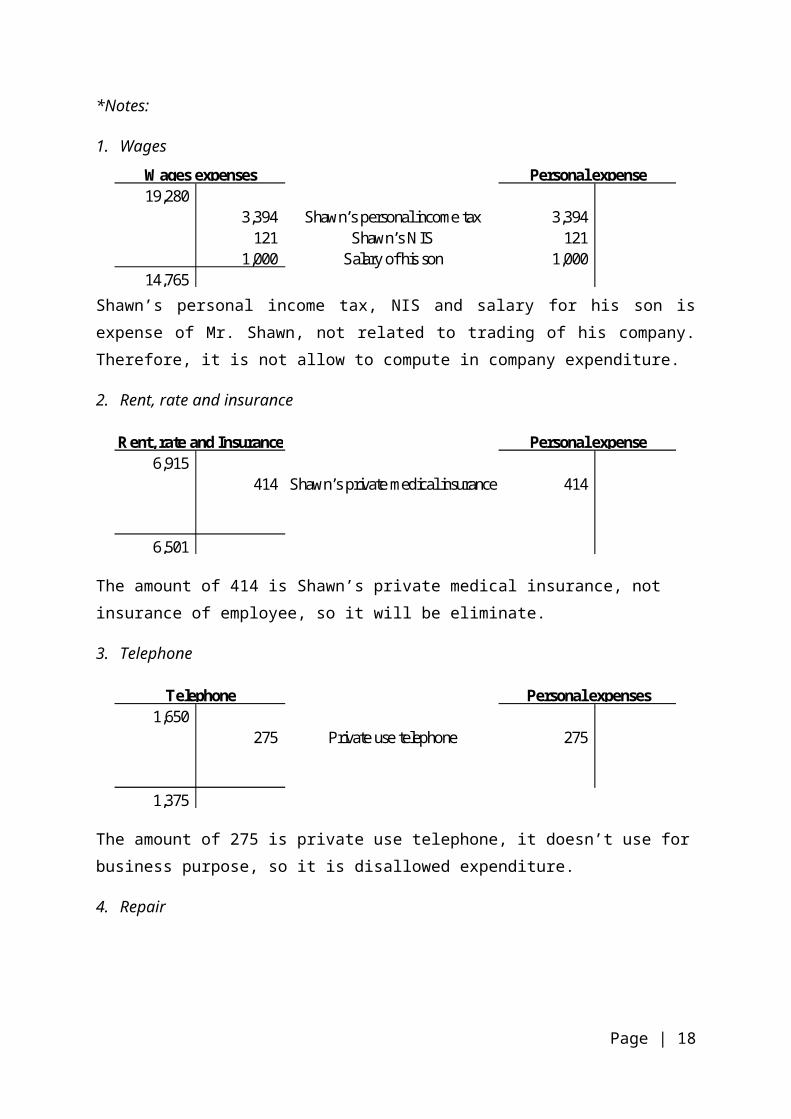

TAX ENVIRONMENT AND PERSONAL TAX PREPARE BY: AN DUC KIEN – SPOCK CLASS: F06B STUDENT NO.: F06-066 SUBMISSION DEADLINES: 16 th April 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TAXENVIRONMENT

ANDPERSONAL

TAX

PREPARE BY: AN DUC KIEN – SPOCK

CLASS: F06B

STUDENT NO.: F06-066

SUBMISSION DEADLINES: 16th April2015

Table of ContentsINTRODUCTION.................................................1

1.1 Describing the UK tax environment........................2

1.1.1 HM (Her Majesty) Revenue & Customs...................2

1.1.2 Sources of Tax law...................................2

1.1.3 Main taxes...........................................4

1.1.4 Tax year.............................................6

1.2 Analyzing the role and responsibilities of the tax practitioner.................................................6

1.2.1 The roles of tax practitioner........................7

1.2.2 Responsibility of tax practitioner...................7

1.3 Explaining the tax obligations of tax payers or their agents and the implications of non-compliance................8

2.1/2.2 Calculate the relevant income, expenses and allowances; Calculate taxable amounts and tax payable, for employed and self-employed individuals, and advise on payment dates for the above cases...................................11

Problem 2: Compute Shawn’s trading profit (before deduction of capital allowances) for the year ended 31 December 2009 11

Problem 3: Compute each partner's trading income for 2006-07 through to 2009-10........................................15

2.3 Complete relevant documentation and tax returns.........17

CONCLUSION..................................................26

References..................................................27

INTRODUCTION

As a part of UK society, it is responsible for individualand company to pay tax to the government. The government willuse this money to support and improve the life standard ofpeople.

This report is set up in order to provide information forclients of company. In the first part of the report, the taxpractitioner will work with Mr. Shawn, a self-employed whohave no knowledge about the UK tax environment. The taxadviser will compute the accurate amount of tax Mr. Shawn haveto pay as well as the payment date for him. The second part ofthe report related to taxation of partnerships. The admissionof new partner have effect on the profit of company and thetaxation of each of them.

Page | 1

1.1 Describing the UK tax environment

As a part of UK citizen, Mr. Shawn have to pay tax to the

government, so that they can have enough money to maintain the

operation of administration and the living standard.

Therefore, it is necessary for Shawn to understand the UK tax

environment.

1.1.1 HM (Her Majesty) Revenue & Customs

In UK, HM Revenue & Customs (HMRC) department responsible

for administration and collection of taxes. When it comes to

tax year, Mr. Shawn will be received a notice from HMRC in

order to remind about paying tax. Beside taxation, HMRC also

responsible for other different aspects include: National

Insurance contributions, the distribution of child benefit and

some other forms of state support including the Child Trust

Fund, payments of Tax Credits .etc… (Anon., 2012). The

department is arranged in four operational groups, which are

Personal Tax, Benefits and Credits, Business Tax and

Enforcement and Compliance. So if Mr. Shawn need any support

from government, especially related to his taxation, he can

contact to HMRC

1.1.2 Sources of Tax law

There is no single sources of tax law. In his book “The UK

Tax System: An Introduction”, Malcolm James described that there are

nine sources of UK taxation law and practices (James, 2009).

Some of these sources are:

Page | 2

1. Statue law

UK taxation laws are consisted in statue law. These are

some of major act:

Table 1: Major Taxation Act (James, 2009)

These laws are changed each year by Finance Act. These

changing could be added new sections, amend and repeal

others. As a result, the number of acts has increased and

make people confused. Therefore, the HMRC started a

project call the Tax Rewrite Project in order to

rewriting the tax legislation in a clearer and easier way

to understand. The result of this project is that a

number of legislations were rewritten and substituted.

For example, sections relating to income tax in the

Income and Corporation Taxes Act 1988 was replaced by the

Income Tax (Earnings and Pensions) Act 2003, the Income

Tax (Trading and Other Income) Act 2005 and the Income

Tax Act 2007 (HM Revenue & Customs, n.d.). Even though

there are many laws, since the Finance Act is the

headline fiscal (budgetary) legislation enacted by the UK

Parliament, containing multiple provisions as to taxes,

Page | 3

duties, exemptions and reliefs at least once per year,

and in particular setting out the principal tax rates for

each fiscal year. Therefore, Mr. Shawn need to keep track

on Finance Act every fiscal year to keep traces on the

changing of tax and duty. For example, the Finance Act

(No.2) 2010 reduced the headline rate of Capital Gain tax

(CGT) to 18%. If Mr. Shawn didn’t update information, he

might still paid more money on his CGT to HMRC.

2. European Union law

Since UK joined European Community, the UK has been

affected by legislations originating from the EU. If

there is any conflict between UK and EU laws, EU law

prevails. An oblivious example for this is the VAT.

Normally, when selling something online, people have to

pay VAT at the rate set by their country, which is UK.

However, under the EU VAT rule call “VATMOSS” (MacDonald,

2014), they must pay tax at the rate set by the buyer’s

country.

UK tax law is also influenced by the judgments of

European Courts of Justice (ECJ). For example, in the

case Hoechst/Metallgesellschaft, the ECJ found that “the UK tax law

on intra-group dividends and Advance Corporation Tax (ACT) – in place until 5

April 1999 – discriminated against non-UK EU parent companies and was

incompatible with the EC Treaty right to freedom of establishment” (Martel

& Clark, 2001). In result, under the decision of the

court, UK government had to pay reparation and changed

the law.

Page | 4

These EU laws will apply in case Mr. Shawn’s company does

business in other countries of European Union, but if his

company only operate in UK, then he has just need to

concern about UK law.

3. HM Revenue & Customers Concession

Even though the congress make any effort to make sure

that the law will operate as its purpose, there are some

cases that certain taxpayer feel unfair. In that case,

the HMRC will issue a statement call Extra Statutory

Concession, in which state that they will “observe the spirit

rather than the strict letter of the law” (James, 2009). For example,

the Extra Statutory Concession A19 (ESC A19) (HM Revenue

& Customs, n.d.) stated that HMRC would consider repaying

tax to the person who have already paid Income Tax or

Capital gain tax under these circumstances:

- HMRC received information which affected taxpayer’s tax

code.

- HMRC failed to make proper and timely use of that

information.

- Failed to notify taxpayer of the underpayment within 12

months of the end of the tax year in which HMRC

received the information.

- It was reasonable for taxpayer to believe your tax

affairs were in order.

Therefore, if Mr. Shawn have any question or feel unfair

which the tax he have to pay, he can complaint to HMRC.

If the complaint is right, then HMRC will release a

Page | 5

concession, so that the right of Mr. Shawn can be

guarantee and help him avoid losing money.

4. Case law

Although the statue law cover every area of taxation,

there are some areas, in which the statue law provides

very little instruction, such as the distinct between

capital and revenue expenditure. In order to identify

these instructions, it is necessary to look in case law.

The judgments of the court in these cases have

contributed to the UK tax law system. So if Mr. Shawn

face with any problems, which is not related to any

regulation in statue law, the court will review all the

case laws which is relevant to the problem and then treat

it according to this case. If there isn’t any case laws

like Mr. Shawn’s case, then the court will hear Mr. Shawn

alleging and will decide what should be done.

1.1.3 Main taxes

There are three main taxes in the UK tax systems: Income

tax, corporation tax and capital gain tax

- Income Tax: the tax that is charged to any individual

who is resident in the UK. The income tax is computed

and base on total income a person earn in tax year. The

total income is computed by all the of taxpayer income,

including both income in UK and from overseas. These

income could include: earnings from employment, pension

income, interest, dividend, rental income. The Income

Tax mainly base on Capital Allowances Act 2001(CAA

Page | 6

2001); Income Tax (Earnings and Pensions) Act 2003

(ITEPA 2003); Income Tax (Trading and Other Income) Act

2005(ITTOIA 2005): Income Tax Act 2007(ITA 2007) (BPP

Learning Media, 2010). Mr. Shawn can have different

sources of income that aside from the profit he receive

from the company. In that case, because Mr. Shawn is

owner of a business, his income tax will be computed

separately from his company tax. Furthermore, the

corporation tax is only applied whether Mr. Shawn start

a corporation. In this case, since Mr. Shawn is a self-

employed or sole trader, then he will be liable to

income tax.

- Corporation Tax: this is the tax charged on the profit

company earn due to its operation. Taxable profit

include the amount of money that company make from:

doing business, investment and selling assets. Under

the source rule, profit are only charged to corporation

tax if they belong to one of the following schedule and

are not exempted by provision of Taxes Act:

Figure 2: UK Scheduler System (HM Revenue & Customs, 2007)

Mr. Shawn is a self-employed, or sole trader. He don’t

have a corporation, then the corporation tax won’t be

apply to him. But he still need to know this

information because some days, his business will growth

to become a corporation.

Page | 7

- Capital gain tax was introduced in 1965 in order to

taxing any gain arising on the trading of capital

assets. A CGT liability may arise when a "chargeable

person" makes a "chargeable disposal" of a "chargeable

asset" (Melville, 2009). The chargeable person could

be: individual, business partner, trustees or

representatives of the deceased. The oblivious example

of chargeable disposal is the sale of chargeable asset,

such as, the sale of a land, or part of this land. So

when Mr. Shawn sold an asset, both private and

company’s asset, he have to pay capital gain tax.

However, not all the income are taxable. The figure below

shows the non-taxable income. Therefore, if Mr. Shawn have

income belonging to one of these types, he mustn’t count that

income in the tax calculation.

Figure 3: Non-taxable income

1.1.4 Tax year

Taxes are generally imposed and collect by HMRC for a

year at a time. The tax year is not the regularly time of a

year, which is from January 1 to December 31, but it is

Page | 8

different. For individual, a tax year, or fiscal year, year of

assessment, start from April 6 and end in April 5 of the next

year. For instance, the tax year 2013-2014 started from April

6, 2013 and ended on April 5, 2014. The corporation tax year

(known as financial years) is different from individual tax

year. It begin on April 1 and end on the following March 31

and is referred to by the year in which it begins. Since Mr.

Shawn is sole trader, then he has just need concentrate on

year of assessment, which is from April 6 to April 5 of the

next year. Mr. Shawn need to aware this timetable because if

he miss it, there will be a penalty for him.

Summary

In conclusion, with the information was provided about, Mr.

Shawn can have an idea about the UK taxation environment.

These information is essentially important for Mr. Shawn

because he can use these information to avoid any unnecessary

damage caused by lack of knowledge, especially he is owner of

a company, in which government is very strictly about

taxation.

1.2 Analyzing the role and responsibilities of

the tax practitioner

It is responsibility of Mr. Shawn and his company to pay

tax for the government. Nevertheless, he need to have

understanding about tax payment and tax practitioner will help

him to prepare tax report base on Mr. Shawn’s transactions in

the past and also give some advices.

Page | 9

1.2.1 The roles of tax practitionerFirstly, as intermediaries between HMRC and tax payer,

the role of tax practitioner is “to help tax payer deal with HMRC in

preparing the tax payments report” (BPP Learning Media, 2010), which

include Mr. Shawn’s income tax, his corporation tax, capital

gain tax and others. It means that the tax practitioner have

responsible to collect and investigate the information about

all the relevant income of Mr. Shawn or his company in order

to calculate the exact amount of tax which Mr. Shawn have to

pay and propose an accuracy and honestly taxation report to

the HMRC. This job require tax practitioner to review all the

record of Mr. Shawn’s transactions as well as interview him in

consideration of getting enough information. Tax practitioner

also need to ensure client to prepare a good tax return and

give them advices if necessary in order to help client avoid

any problems.

Secondly, tax practitioner “plays an important role in the

transmission and translation of legal rules and meanings for taxpayers” (Beck,

et al., 1989) in a clearly and honestly way based on the

understanding about tax laws and regulations. The purpose of

this is to provide knowledge for Mr. Shawn in order to let him

know what he should do and should not so that he can

understand the tax law and prepare a good tax return.

Therefore, tax practitioner need to keep up-to-date with any

changes in taxation laws and practice so that they can inform

and explain to tax payer in time in order to help them avoid

mistakes during the tax report preparation process.

Page | 10

Finally, based on the understanding about tax laws and

regulations, tax practitioner is “able to help taxpayers reduce his tax

liabilities in a legal way” (This is money, 2013). Mr. Shawn can save

thousands of taxes over the years. For example, Mr. Shawn is a

self-employed, he can spread income tax payments among the

family. If Mr. Shawn have children over 16 and still living

out of his pocket, he could put them to work in the business

in the holidays and make them earn their keep. It’s good for

them, and the wage is “tax deductible to the business” (This is money,

2013)

1.2.2 Responsibility of tax practitionerFirst of all, tax practitioner have “a serious responsibility to

prepare a proper taxation return to HMRC” (Meldman, 1963). This is

essential important because tax practitioner represent Mr.

Shawn to work with HMRC in this situation, which mean that tax

practitioner have to prepare all the document related to Mr.

Shawn’s taxes. Mr. Shawn will base on these documents to pay

money. Therefore, any carelessness resulting in damages, the

practitioner will be liable to the taxpayer. If there is an

understatement of tax on the original return, which later

result in an insufficiency upon audit, the practitioner may be

liable because of his negligence. He may have to pay for the

additional interest on the deficiency upon audit.

Tax practitioner “has responsible for keeping client’s information

confidentially” (Meldman, 1963) because they can access to a wide

range of personal information. This is extremely important,

especially for business, because the competitor could get this

Page | 11

information and use it as a tool to taking advantage.

Therefore, tax practitioner must not reveal any information

related to Mr. Shawn’s affairs to a third party without his

permission.

Furthermore, tax practitioner has responsible for “asking

from taxpayers any information and records in order to deliver a correct tax return”

(Meldman, 1963). In this scenario, because Mr. Shawn look for

tax practitioner and he have no background about the UK tax

systems rules and procedures, the tax practitioner will

represent Mr. Shawn to deal with HMRC, which include calculate

tax. Therefore, tax practitioner will need all the information

in order to propose correctly tax report to Mr. Shawn and

HMRC. HM Revenue & Customs can inspect these records if they

believe it is necessary to check a tax position.

1.3 Explaining the tax obligations of tax

payers or their agents and the implications

of non-compliance

Taxpayer refer to a person or organization subject to a tax

on income, which in that case is Mr. Shawn and his company.

Tax agent is the one who was entrusted by taxpayer to act for

their responsibility as on working with HMRC. Since Mr. Shawn

have no background information about taxation and he decided

to hire tax agents, the tax agent will represent Mr. Shawn to

prepare taxation return. There are some obligations that Mr.

Shawn and his agent have to follow. There will be penalties

for the non-compliance of these obligation.

Page | 12

Tax obligation:

o Mr. Shawn and his agent need to ensure that they

make an accurate return for income tax, national

insurance contributions, corporation tax and VAT.

This is essentially important because there is a

penalty for making inaccurate return. Furthermore,

making inaccurate return lead to the result that Mr.

Shawn have to pay more money for the government.

o Mr. Shawn and his agent have duty to inform to HMRC

if they notice any errors in tax return report and

explaining how the error was made because by

informing to HMRC, Mr. Shawn can show his

responsibility and HMR may not charge him a penalty.

Reporting the error also prevent the additional lost

on Mr. Shawn budget. For example, instead of paying

£100, Mr. Shawn have paid £200 for HMRC because of

an error in preparing tax report. If Mr. Shawn

notice the error, he will have chance to fix it and

only pay £100.

o They have obligation to retain all records required.

By keeping the records, Mr. Shawn and his agent can

review it when coming to tax years. This will enable

them to make and deliver a correct tax return.

Furthermore, if HMRC have any doubt about his tax

report, he can use these records as evidence support

the report.

o Mr. Shawn must deliver a tax return before the

filing due date if he doesn’t want to be charged a

Page | 13

penalty for it. Any late returns will be charged an

amount of fees which could result a bad influence

for Mr. Shawn business.

Implication of non-compliance

If Mr. Shawn fail to comply with tax regulations, then he will

be charged penalty by HMRC. The HMRC will base on the types of

violation and sufficient evidences for breaching the

regulation to determine penalty for Mr. Shawn. Below is some

of the actions and their penaltities:

- Penalties for error: A penalty may be levied if Mr.

Shawn make an inaccurate tax return and it result in an

understatement of the his liability, a false or

increased loss or repayment of tax to the taxpayer. The

amount of penalty will be decided base on the Potential

Lost Revenue (PLR) to HMRC as a result of the error

Type of error Maximum penalty

payableCareless 30% of PLR

Deliberate not

concealed

70% of PLR

Deliberate and

concealed

100% of PLR

Table 1: Penalties for errors ( (BPP Learning Media, 2010)

However, this penalty may be reduce if Mr. Shawn inform

HMRC about the error (disclosure). An umprompted

disclosure is one made at a time when taxayer has no

reason to believe HMRC has discovered the error (BPP

Page | 14

Learning Media, 2010). The minimum penaltises for

disclosure is showed on the table below:

Type of error Unprompted

disclosure

Prompted

disclosureCareless 0% of PLR 15% of PLR

Deliberate not

concealed

20% of PLR 35% of PLR

Deliberate and

concealed

30% of PLR 50% of PLR

Table 2: Unprompted and Prompted disclosure penalties (BPP Learning Media, 2010)

- Penalties for late filling: If Mr. Shawn submit a tax

return late, he will be charged a penalties, base on

the amount of time he was late:

Time late Maximum penaltiesReturn up to 6 months late £100

Return more than 6 months but

less than 12 months late

£200

Return more than 12 months

late

£200 +100% of the tax

liabilityTable 3: Penalties for late filling (BPP Learning Media, 2010)

Therefore, Mr. Shawn need to be very carefull in

keeping up the timetable to avoid losing additional

money, especially for return more than 12 months late.

In that case, Mr. Shawn have to pay his tax twice plus

£200. That is a lot of money. Nevertheless, Mr. Shawn

can avoid these penalties by giving a reasonable excuse

for a late filing if a failure occured because of a

Page | 15

outside factors such as: a fire or flood have

destructed his tax record.

- Penalties for failure to keep records: Every taxpayers

are required to keep all records in case HMRC want to

inspect these records in order to determine the

accuracy of tax return. Records must be retained until

the later of:

o 5 years after the 31 January following the tax

year where taxpayer is in business or

o 1 year after the 31 January following the tax

otherwise.

As a result, Shawn and his company need to keep records

of all the transactions during the identify time. If he

fail to do that, he will take a penalty of £3,000/tax

year for each failure to keep and retain records, which

means if during the period of 2009-2013, he doesn’t

keep record of two years, then the penalty for him is

£6,000.

Page | 16

2.1/2.2 Calculate the relevant income, expensesand allowances; Calculate taxable amounts and tax payable, for employed and self-employed individuals, and advise on payment dates for the above cases

Problem 2: Compute Shawn’s trading profit (before deduction of capital allowances) for the year ended 31 December 2009

£ £ £Net profit for the year (9,142)

Add:Disallowed expenditureW ages paid for Shawn's son (Note 1) 1,000

Personal incom e tax (Note 1) 3,394 Personal NICS (Note 1) 121

Private m edical insurance (Note 2) 414 Telephone (Note 3) 275

Repair (Note 4) 750 Loss on disposal of m otor vehicle (Note 5) 422

Speeding fine (Note 5) 700 M otor expense private use (Note 5) 459

Business entertaining (Note 6) 3,320 Political donation (Note 6) 200

General allowance for bad debt (Note 7) (100) Lease prem ium am ortisation 700

Depreciation 8,749 20,404 Trading income not shown in the account

Owner consum ption (20/80th of £220) (Note 8) 55 20,459 11,317

Less:Non-trading income shown in the accountInterest receivable 212

Surplus on sale of office equipm ent 300 512 Allowable expenditure not shown in the account

Lease prem ium (1/10th of 82% of £7,000) (Note 9) 574 1,086 Trading profit (before capital allowances) 10,231

Page | 17

*Notes:

1. Wages

19,280 3,394 Shawn’s personal income tax 3,394 121 Shawn’s NIS 121

1,000 Salary of his son 1,000 14,765

W ages expenses Personal expense

Shawn’s personal income tax, NIS and salary for his son isexpense of Mr. Shawn, not related to trading of his company.Therefore, it is not allow to compute in company expenditure.

2. Rent, rate and insurance

6,915 414 Shawn’s private medical insurance 414

6,501

Rent, rate and Insurance Personal expense

The amount of 414 is Shawn’s private medical insurance, not insurance of employee, so it will be eliminate.

3. Telephone

1,650 275 Private use telephone 275

1,375

Telephone Personal expenses

The amount of 275 is private use telephone, it doesn’t use forbusiness purpose, so it is disallowed expenditure.

4. Repair

Page | 18

2,286 750 Repairs to a newly-acquired fork lift truck 750

1,536

AssetRepairs expenses

The repair of lift truck in here is not allowed to count asexpenditure because it is a newly acquired asset and if therepairs are required in order to put the asset into usablecondition, it is disallowed expenditure.

5. Motor expenses

5,712 422 Loss on disposal of motor vehicle 422 700 Fine for speeding by Shawn 700

4,590 459 Private use motor 459

4,131

Personal expenseM otor expenses Profit loss

The loss on disposal of motor vehicle is not an expenditure ofShawn’s company as well as speeding fine of Shawn and privateuse. It said that “one-tenth of motor expenses relate to private use”, whichmeans that the private use expense will be calculated afterthe deducted of loss on disposal and speeding fine.

The private use expense is equal to(5,712−422−700)10

=459. Then

the private use expense will be discharged from company’sexpenditure.

6. Sundry expenses

4,777 3,320 Business entertaining200 Political donation

1,257

Sundry expenses

Page | 19

Business entertaining here is the cost of entertainingcompany’s customers, so it is disallowed. Since there is noinformation about the political donation, so it is assumedthat this expense will be disallowed.

7. Doubtful debt

The general allowance for doubtful debts are not allowed incalculating company expenditure. Furthermore, because thescenario mentioned that the amount of general allowances hadbeen collected by Shawn’s company and it was counted astrading income of company. Therefore, when calculating thetrading profit, this amount will be deducted in the expense

500 460 100360

860

Bad and Doubtful debt Specific allowance General Allowances

8. Owner consumption

According to the scenario, Shawn appropriated trading stockcosting £220 from the business for personal use. But ITTOIA2005 requires that “owner consumption of trading stock is accounted for atmarket value” (Melville, 2009). This means that the profit of thebusiness for tax purposes should be increased by the sellingprice of the goods. The scenario mentioned that the grossprofit percentage on turnover is 20%., which mean when sellingthe asset, the company will earn 20%. It cost company £220 toproduce the trading stock, so in order to earn 20% in return,the company have to sell the stock at the market price of20%80%

∗220=£55 more.

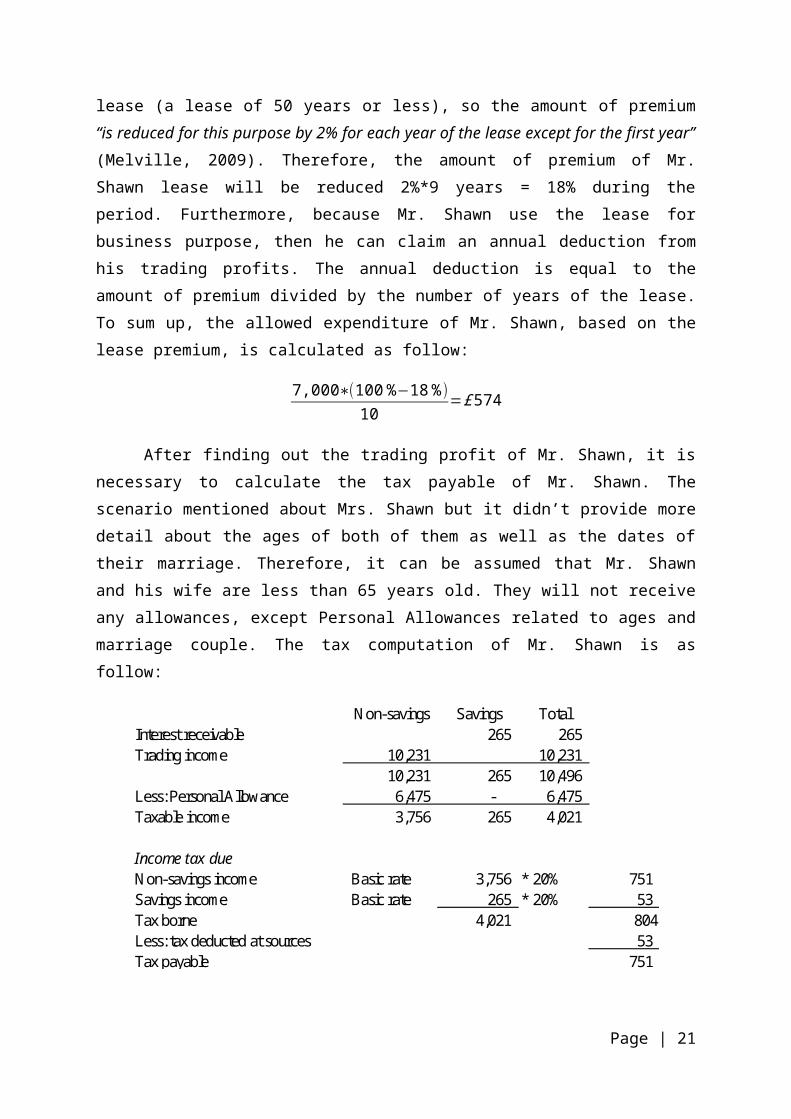

9. Lease premium

Mr. Shawn has a 10-year lease on the premises and paid apremium of £7,000 in order to obtain the lease. It is a short

Page | 20

lease (a lease of 50 years or less), so the amount of premium“is reduced for this purpose by 2% for each year of the lease except for the first year”(Melville, 2009). Therefore, the amount of premium of Mr.Shawn lease will be reduced 2%*9 years = 18% during theperiod. Furthermore, because Mr. Shawn use the lease forbusiness purpose, then he can claim an annual deduction fromhis trading profits. The annual deduction is equal to theamount of premium divided by the number of years of the lease.To sum up, the allowed expenditure of Mr. Shawn, based on thelease premium, is calculated as follow:

7,000∗(100 %−18 %)10

=£574

After finding out the trading profit of Mr. Shawn, it isnecessary to calculate the tax payable of Mr. Shawn. Thescenario mentioned about Mrs. Shawn but it didn’t provide moredetail about the ages of both of them as well as the dates oftheir marriage. Therefore, it can be assumed that Mr. Shawnand his wife are less than 65 years old. They will not receiveany allowances, except Personal Allowances related to ages andmarriage couple. The tax computation of Mr. Shawn is asfollow:

Non-savings Savings TotalInterest receivable 265 265 Trading income 10,231 10,231

10,231 265 10,496 Less: Personal Allowance 6,475 - 6,475 Taxable income 3,756 265 4,021

Income tax dueNon-savings income Basic rate 3,756 * 20% 751 Savings income Basic rate 265 * 20% 53 Tax borne 4,021 804Less: tax deducted at sources 53 Tax payable 751

Page | 21

From the tax of Mr. Shawn, the tax agent will give adviceabout the date of payment. There are three date of payment,according to HMRC. The first date is on 31 January in the taxyear, the second date is on 31 July and the third date is on31 January after the tax year. Since the income statement ofMr. Shawn was prepared on 31 December, 2009 then theappropriate payment date for Mr. Shawn is 31 January 2010.

Problem 3: Compute each partner's trading income for 2006-07 through to 2009-10

Nick Emma Catherine Totaly/e 30/06/2007Profit (shared equally) 8,500 8,500 - 17,000

y/e 30/06/2008Profit (shared 5:4:1) 11,000 8,800 2,200 22,000

y/e 30/06/2009Profit (shared 5:4:1) 14,500 11,600 2,900 29,000

For the y/e 30/06/2007, because Catherine hasn’t entered thepartnerships yet, the profit share between Nick and Emma are50:50. Therefore, their profit will be £8,500 each. From theperiod 30/06/2008, the profit share ratios is changed to5:4:1. Therefore, the profit they received also change.

Page | 22

NickYear Period W orking Trading income

2006-2007 1/7/06 - 5/4/07 8500*9/12 6,375 2007-2008 y/e 30/6/07 8,500 2008-2009 y/e 30/6/08 11,000 2009-2010 y/e 30/6/09 14,500

EmmaYear Period W orking Trading income

2006-2007 1/7/06 - 5/4/07 8500*9/12 6,375 2007-2008 y/e 30/6/07 8,500 2008-2009 y/e 30/6/08 8,800 2009-2010 y/e 30/6/09 11,600

CatherineYear Period W orking Trading income

2007-2008 1/7/07-5/4/08 2200*9/12 1,650 2008-2009 y/e 30/6/08 2,200 2009-2010 y/e 30/6/09 2,900

The period from 1/7/06 to 5/4/07 is called Overlap periodsince the company’s accounting date is different than 5 April.Overlap profits are Nick £6,375, Emma £6,375 and Catherine£1,650. These overlap profits will be relieved when therelevant partner leaves the partnership (or on a change ofaccounting date).

From the computation of trading income, tax agent willcalculate the amount of tax for each of partnership. Assumingthat all of them are under 65 years old, which means theywon’t have age allowances.

Page | 23

Nick2006-2007 2007-2008 2008-2009 2009-2010

Trading income 6,375 8,500 11,000 14,500 Less: P.A 5,035 5,225 6,035 6,475 Taxable income 1,340 3,275 4,965 8,025 Income tax due 295 721 993 1,605

Emma 6,375 8,500 8,800 11,600 Less: P.A 5,035 5,225 6,035 6,475 Taxable income 1,340 3,275 2,765 5,125 Income tax due 295 721 553 1,025

Catherine 1,650 2,200 2,900 Less: P.A (1,650) (2,200) (2,900) Taxable income - - - Income tax due

As it was calculated, the taxable income of partnershipsbelongs to basic rate band. For two period 2006-2007 and 2007-2008, the basic rate band is 22%, which means the calculationof income tax due for these two periods are equal to taxableincome multiply 22%. These other periods are equal to taxableincome multiply 20%. For Catherine, since her income is lessthan the Personal allowance, she won’t be charged income tax.

Tax adviser also give advice about the payment date forthe partnerships. For Emma and Nick, because their income taxdue are less than 1,000, they should pay their tax on 31January on the next period. For the period 2009-2010, Nick andEmma income tax is more than 1,000, so they should dividetheir taxation to two period. The first payment date is on 31January 2010, they should pay 50% of their tax, and the firstpayment date is 31 July 2010.

Page | 24

2.3 Complete relevant documentation and tax returns.

After computing Mr. Shawn taxation, the tax agent prepare the tax report for him

Page | 25

Page | 26

Page | 27

Page | 28

Page | 29

Page | 30

Page | 31

Page | 32

Page | 33

CONCLUSION

The report have provide a wide range of knowledge for Mr.Shawn about the UK taxation environment. Mr. Shawn can knowhow the tax laws in UK are set up as well as different kind oftaxes in UK. Furthermore, through the calculation of hiscompany trading profit, the tax practitioner can come up withhis income tax due. Moreover, the report also clearly statethe role and responsibilities of taxpayers and tax advisersand the implication for non-compliance. The tax practitioneralso compute the tax liable for partnerships: Nick, Emma andCatherine. Finally, a standard taxation return report areprepared to summit to HMRC.

Page | 34

ReferencesAnon., 2012. HM Revenue & Customs uktradeinfo – Home. [Online] Available at: https://www.uktradeinfo.com/Pages/Home.aspx[Accessed 15 March 2015].Beck, P. J., Davis, J. S. & Woon, J. O., 1989. The Role of Tax Practitioners in Tax Reporting:. Illinois: s.n.BPP Learning Media, 2010. Auditing and Financial Systems and Taxation. London: BPP Learning Media.HM Revenue & Customs, 2007. Property Income Manual PIM1001 — Introduction: overview. [Online] Available at: http://www.hmrc.gov.uk/manuals/pimmanual/PIM1001.htm[Accessed 16 March 2015].HM Revenue & Customs, n.d. Changes to Legislation. [Online] Available at: http://www.legislation.gov.uk/changes?affected-title=Income%20and%20Corporation%20Taxes%20Act[Accessed 15 March 2015].HM Revenue & Customs, n.d. HMRC delays/errors in using information. [Online] Available at: http://www.hmrc.gov.uk/dealingwith/esc.htm#1[Accessed 15 March 2015].James, M., 2009. The UK Tax System: An Introduction. 2nd ed. London: Spiramus Press Ltd.MacDonald, K., 2014. Is a New EU Tax Law Screwing Over Indie Developers?. [Online] Available at: http://www.kotaku.co.uk/2014/12/17/new-eu-tax-law-screwing-indie-developers[Accessed 15 March 2015].Martel, A. & Clark, M., 2001. Practical Implications of Hoechst/Metallgesellschaft. [Online] Available at: http://www.tax.org.uk/tax-policy/tax-adviser-articles/2001/practical-implications-of-

Page | 35

hoechstmetallgesellschaft[Accessed 15 March 2015].Meldman, L. L., 1963. The Legal Responsibilities of the Person Preparing Tax Returns and Furnishing Tax Advice and Reliance Upon Advice of Counsel. s.l.:s.n.Melville, A., 2009. Introduction to capital gains tax. In: Taxation Finance Act . London: s.n., p. 247.Melville, A., 2009. Taxation Finance Act. 15th ed. s.l.:s.n.This is money, 2013. Put more money in your pocket: Ten tips to avoid overpaying tax if you're self-employed. [Online] Available at: http://www.thisismoney.co.uk/money/smallbusiness/article-2323791/Ten-legal-ways-avoid-overpaying-tax-youre-self-employed.html[Accessed 21 March 2015].

Page | 36

Related Documents