INDUSTRIAL DISTRIBUTION TAPARIA TOOLS

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INDUSTRIAL DISTRIBUTION

TAPARIA TOOLS

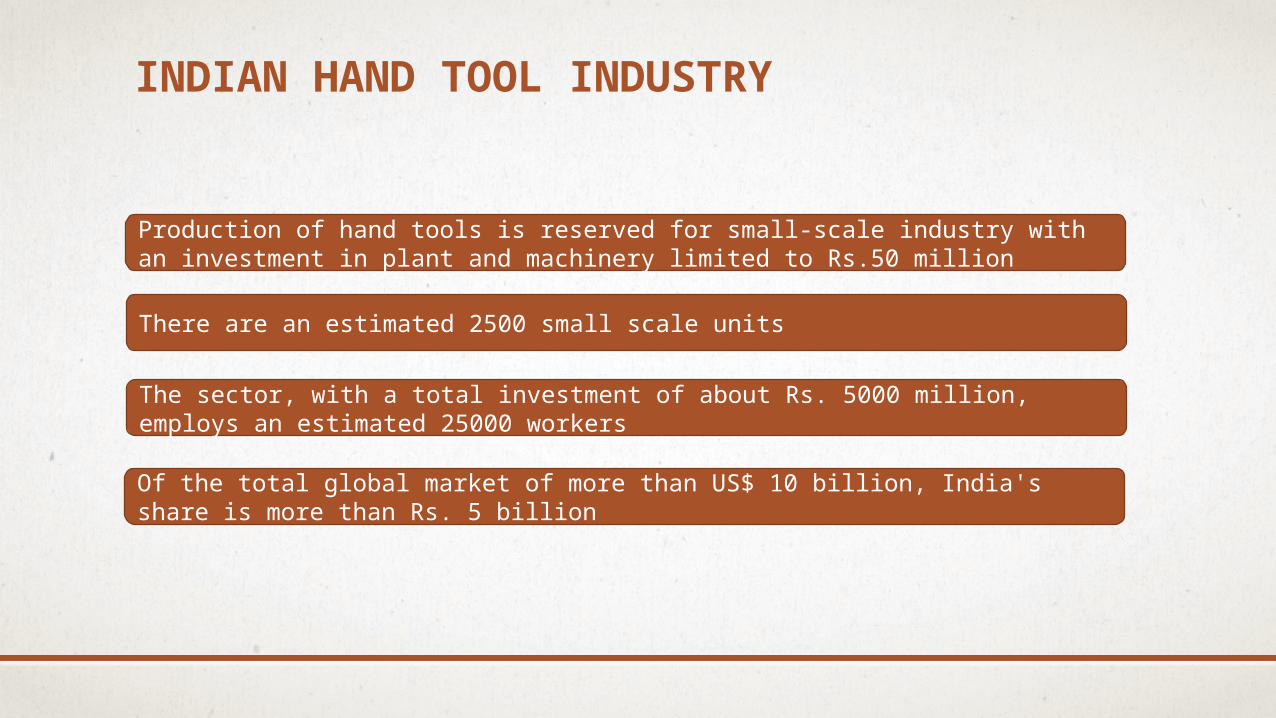

INDIAN HAND TOOL INDUSTRY

Production of hand tools is reserved for small-scale industry with an investment in plant and machinery limited to Rs.50 million

The sector, with a total investment of about Rs. 5000 million, employs an estimated 25000 workers

There are an estimated 2500 small scale units

Of the total global market of more than US$ 10 billion, India's share is more than Rs. 5 billion

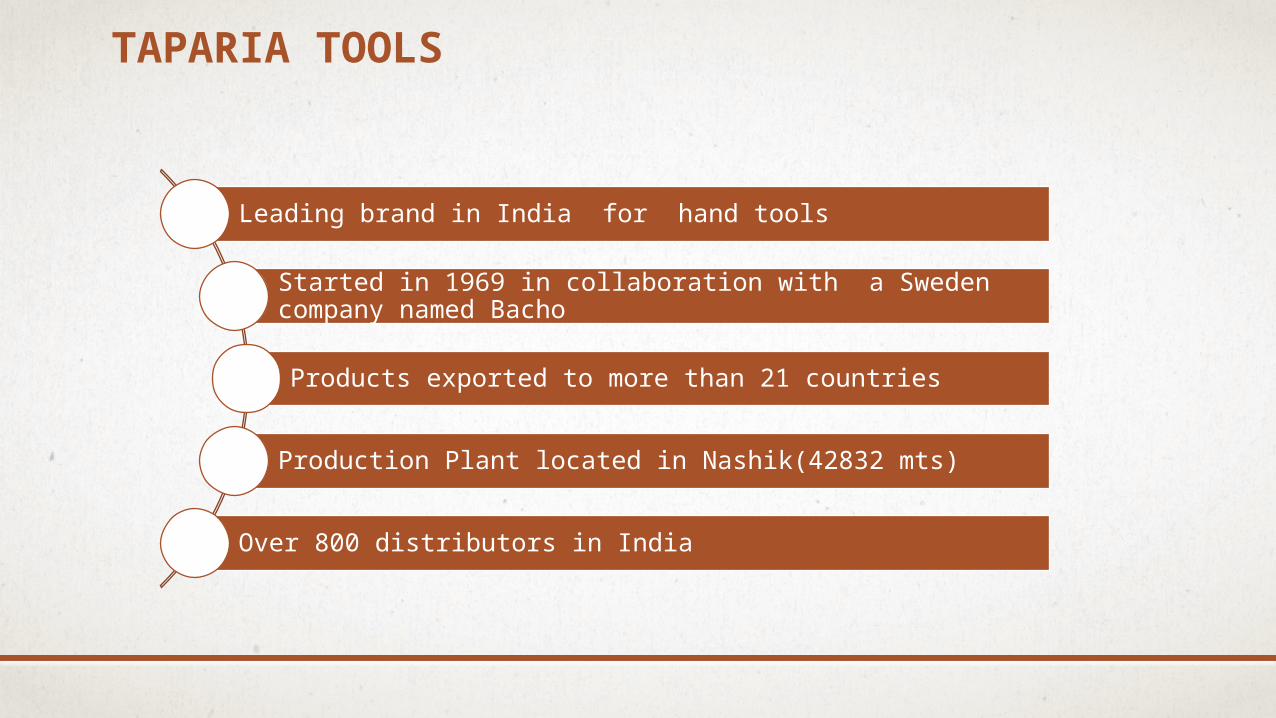

TAPARIA TOOLS

Leading brand in India for hand tools

Started in 1969 in collaboration with a Sweden company named Bacho

Products exported to more than 21 countries

Production Plant located in Nashik(42832 mts)

Over 800 distributors in India

PRODUCTS OF TAPARIA

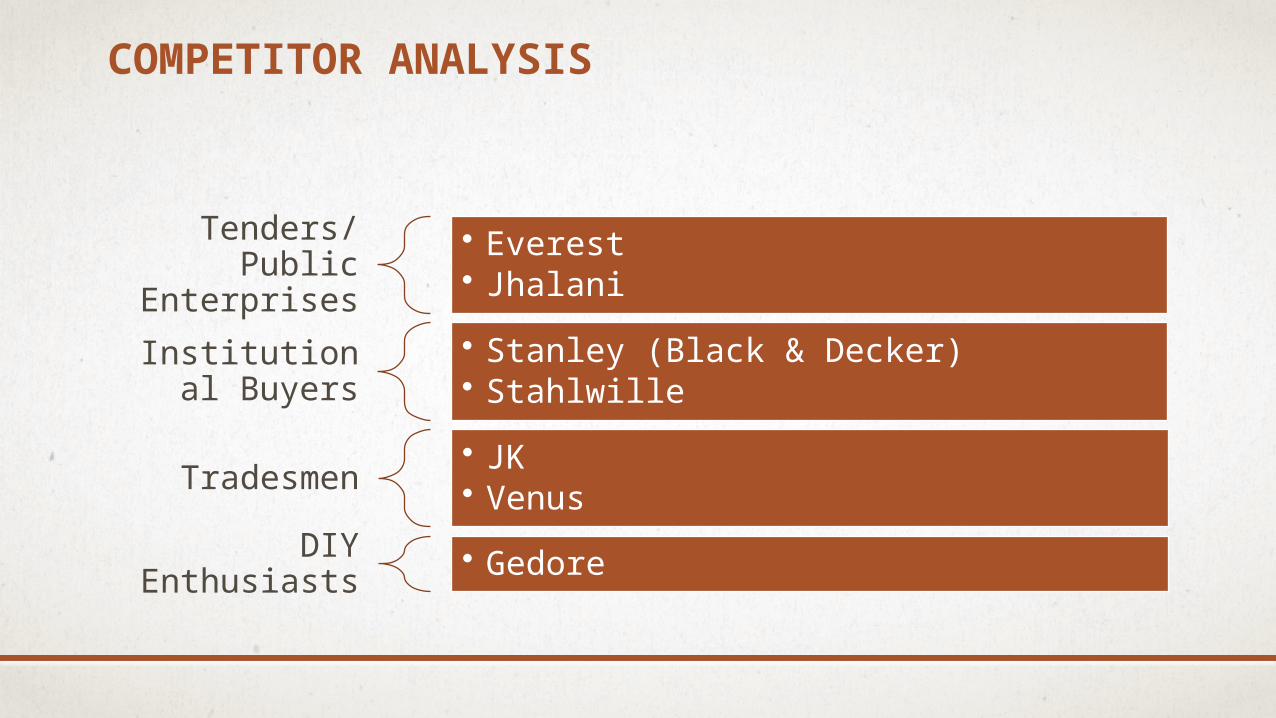

COMPETITOR ANALYSIS

Tenders/Public Enterprises

• Everest• Jhalani

Institutional Buyers

• Stanley (Black & Decker)• Stahlwille

Tradesmen• JK• Venus

DIY Enthusiasts • Gedore

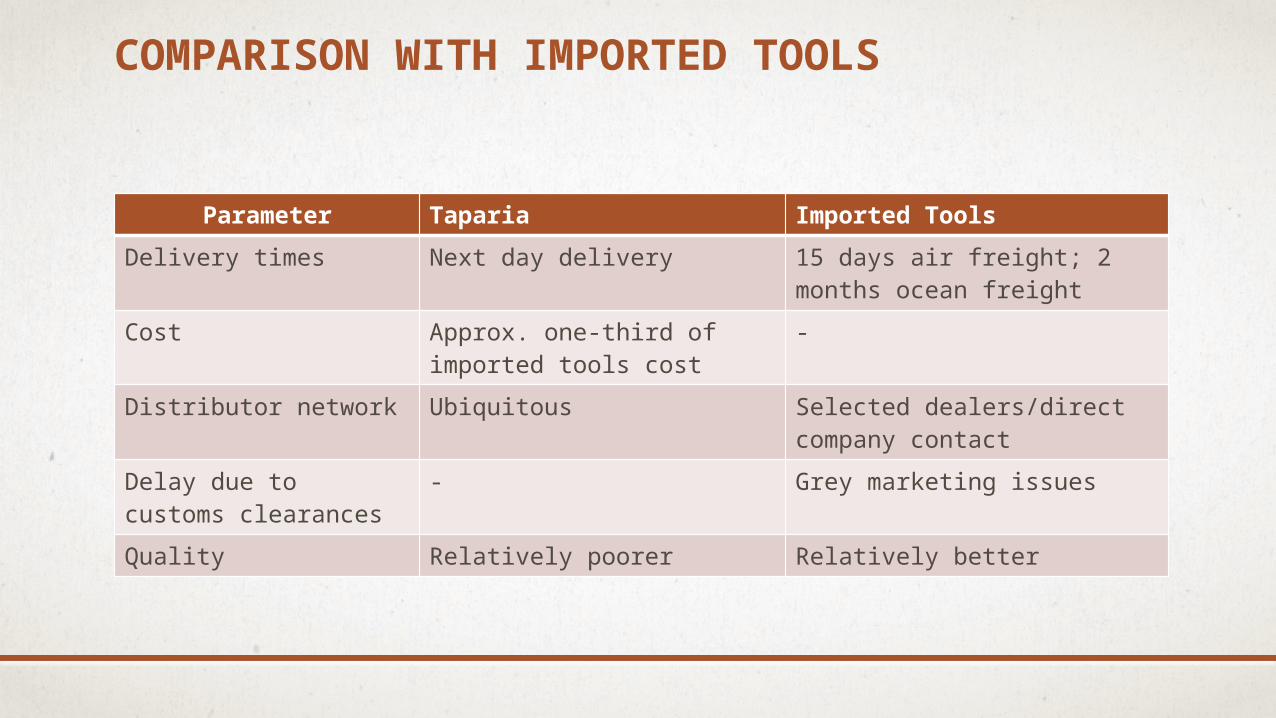

COMPARISON WITH IMPORTED TOOLS

Parameter Taparia Imported Tools

Delivery times Next day delivery 15 days air freight; 2 months ocean freight

Cost Approx. one-third of imported tools cost

-

Distributor network Ubiquitous Selected dealers/direct company contact

Delay due to customs clearances

- Grey marketing issues

Quality Relatively poorer Relatively better

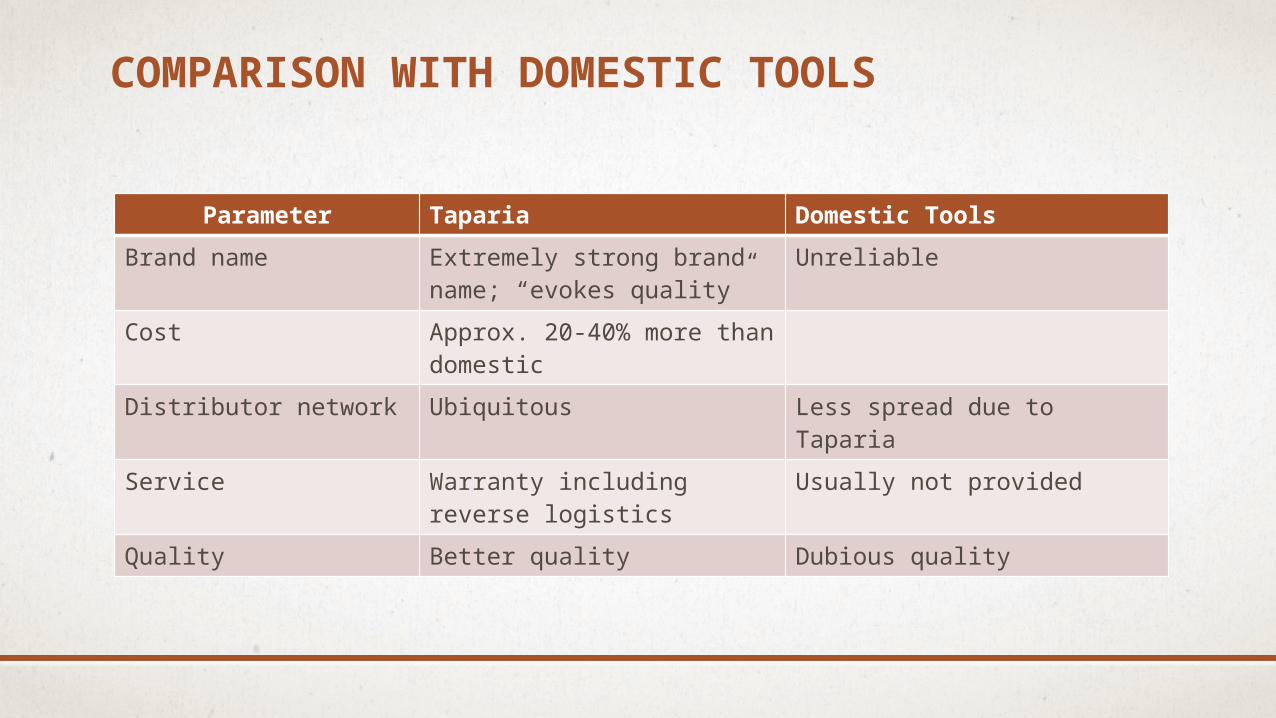

COMPARISON WITH DOMESTIC TOOLS

Parameter Taparia Domestic Tools

Brand name Extremely strong brand name; “evokes quality”

Unreliable

Cost Approx. 20-40% more than domestic

Distributor network Ubiquitous Less spread due to Taparia

Service Warranty including reverse logistics

Usually not provided

Quality Better quality Dubious quality

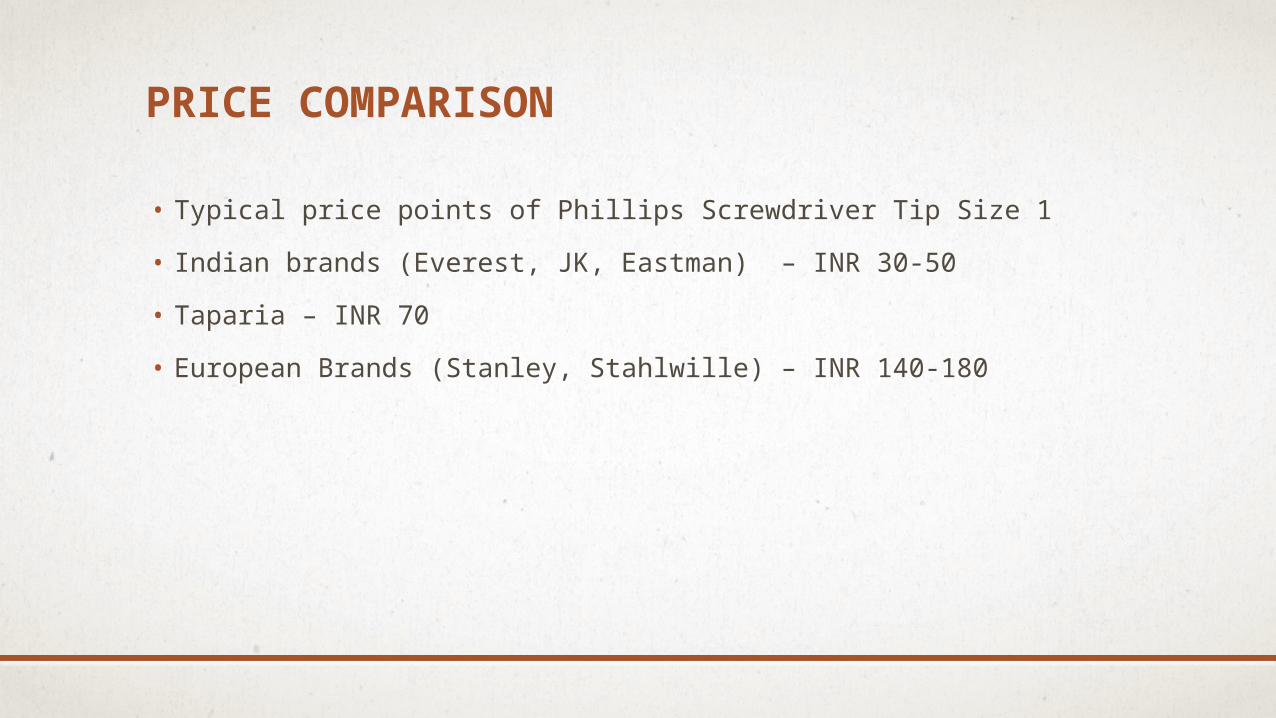

PRICE COMPARISON

• Typical price points of Phillips Screwdriver Tip Size 1

• Indian brands (Everest, JK, Eastman) – INR 30-50

• Taparia – INR 70

• European Brands (Stanley, Stahlwille) – INR 140-180

INSIGHTS

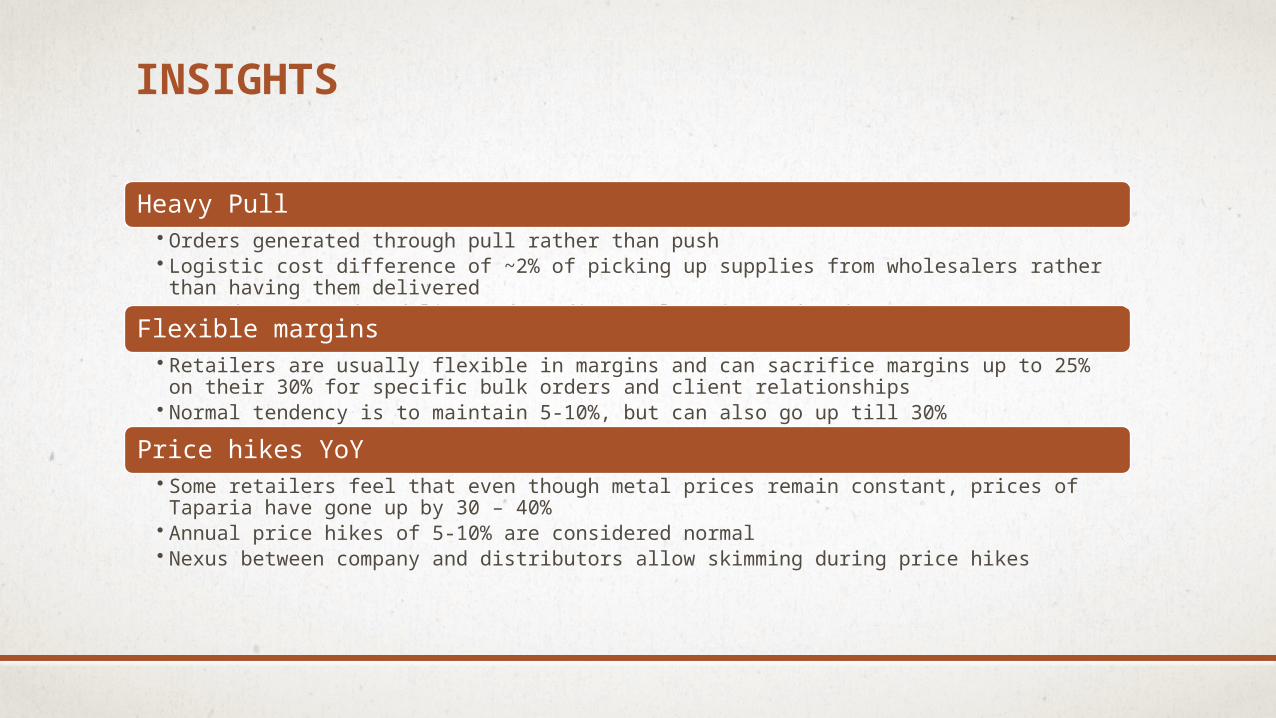

Heavy Pull• Orders generated through pull rather than push• Logistic cost difference of ~2% of picking up supplies from wholesalers rather than having them delivered• Same day or +1 day delivery depending on location and order

Flexible margins• Retailers are usually flexible in margins and can sacrifice margins up to 25% on their 30% for specific bulk

orders and client relationships• Normal tendency is to maintain 5-10%, but can also go up till 30%

Price hikes YoY• Some retailers feel that even though metal prices remain constant, prices of Taparia have gone up by 30 – 40%• Annual price hikes of 5-10% are considered normal• Nexus between company and distributors allow skimming during price hikes

INSIGHTS

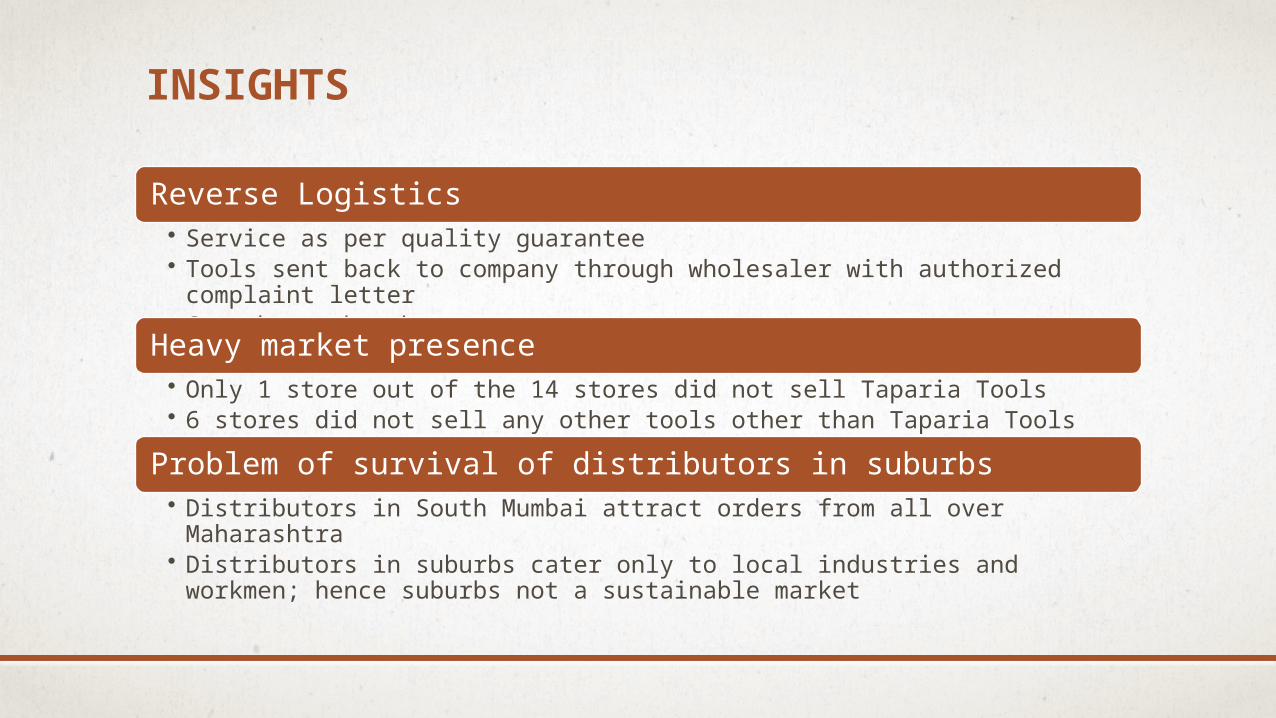

Reverse Logistics• Service as per quality guarantee• Tools sent back to company through wholesaler with authorized complaint letter• Cost borne by the company

Heavy market presence• Only 1 store out of the 14 stores did not sell Taparia Tools• 6 stores did not sell any other tools other than Taparia Tools

Problem of survival of distributors in suburbs• Distributors in South Mumbai attract orders from all over Maharashtra• Distributors in suburbs cater only to local industries and workmen; hence suburbs not a

sustainable market

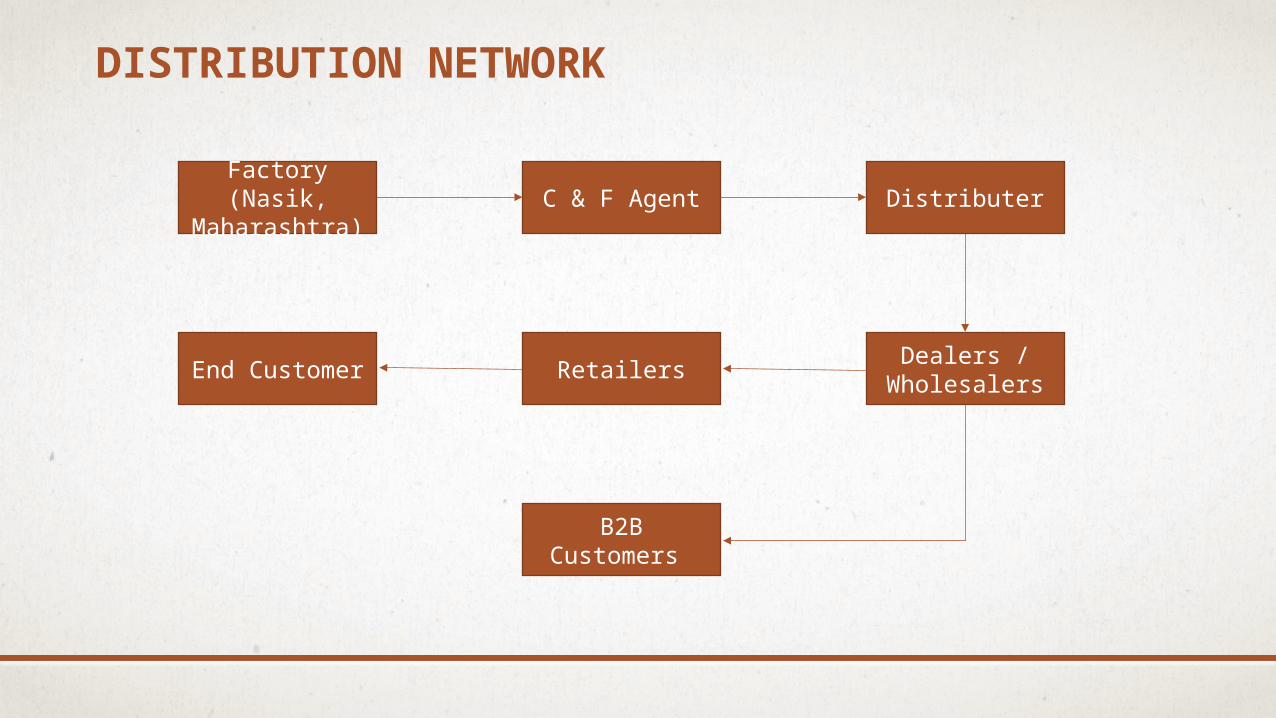

DISTRIBUTION NETWORK

Factory (Nasik, Maharashtra)

C & F Agent Distributer

Dealers / Wholesalers

RetailersEnd Customer

B2B Customers

MARGINS IN THE CHANNEL

Company Manufacturing 70% of list price

C&F Transportation 2%

Distributors Bulk break and Local taxes 3% to 5%

Dealers/ Wholesalers Reach Users with huge purchases

10% to 15%

RetailReach Home users/small mechanics and servicing

small purchases

10% to 15%

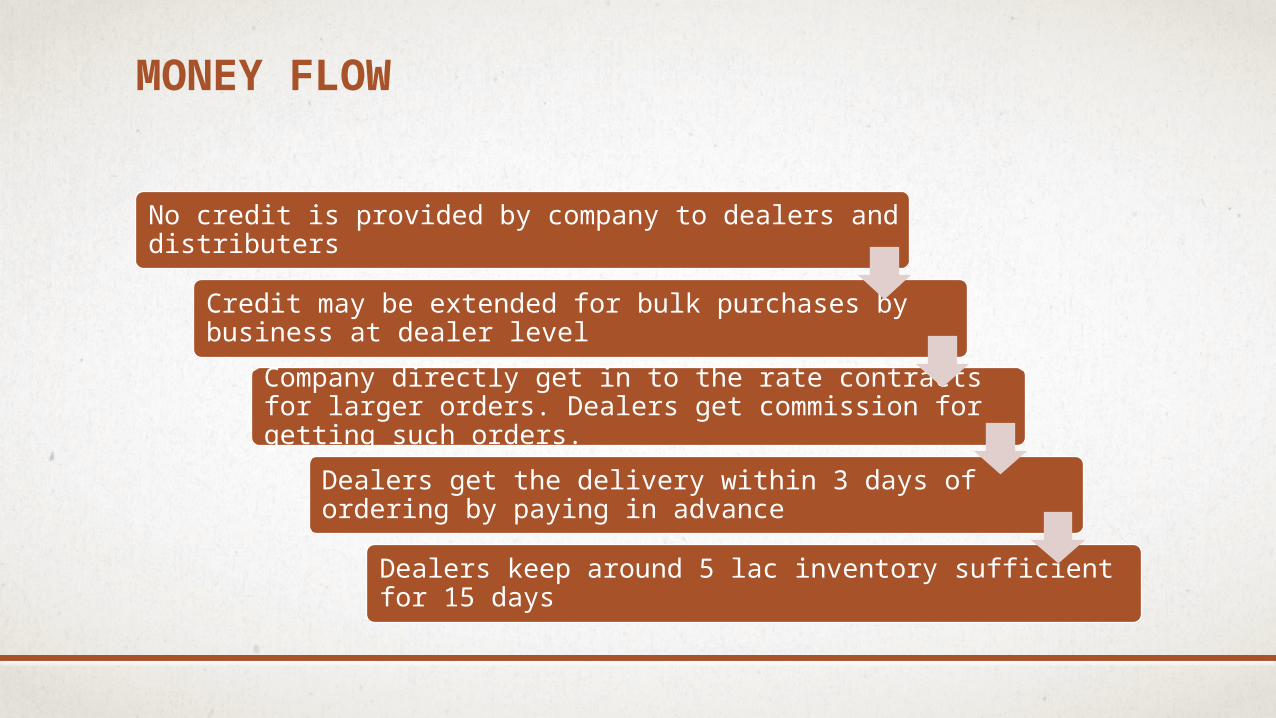

MONEY FLOW

No credit is provided by company to dealers and distributers

Credit may be extended for bulk purchases by business at dealer level

Company directly get in to the rate contracts for larger orders. Dealers get commission for getting such orders.

Dealers get the delivery within 3 days of ordering by paying in advance

Dealers keep around 5 lac inventory sufficient for 15 days

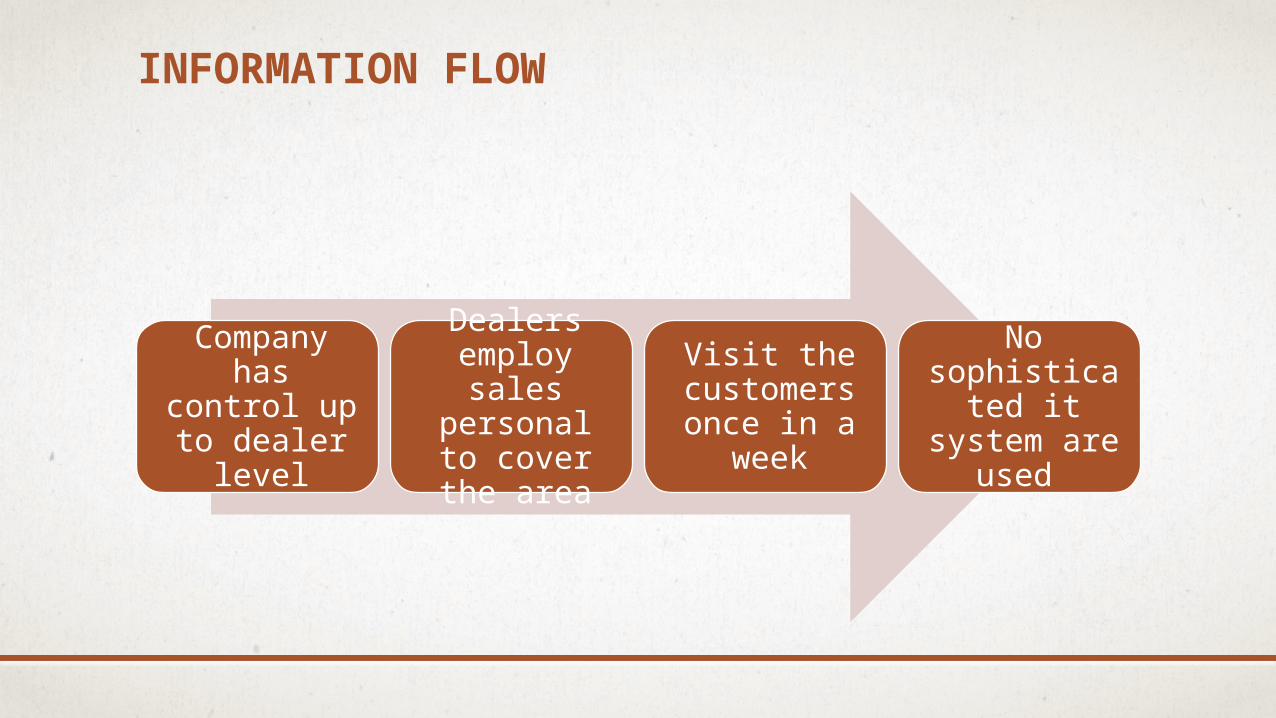

INFORMATION FLOW

Company has control up to dealer level

Dealers employ sales personal to

cover the area

Visit the customers

once in a week

No sophisticated it system are

used

BUSINESS DYNAMICS

Dealers stock multiple competitor products from India as well as imported products

Imported products are costly. Most of Indian competitors are regional players

Taparia do not have comprehensive range in tools and products are predominantly hand tools

Customers primarily buy main tools and then it is in the purview of dealer to push Taparia tools or competitors tools

Maintaining quality and availability of products is key for success

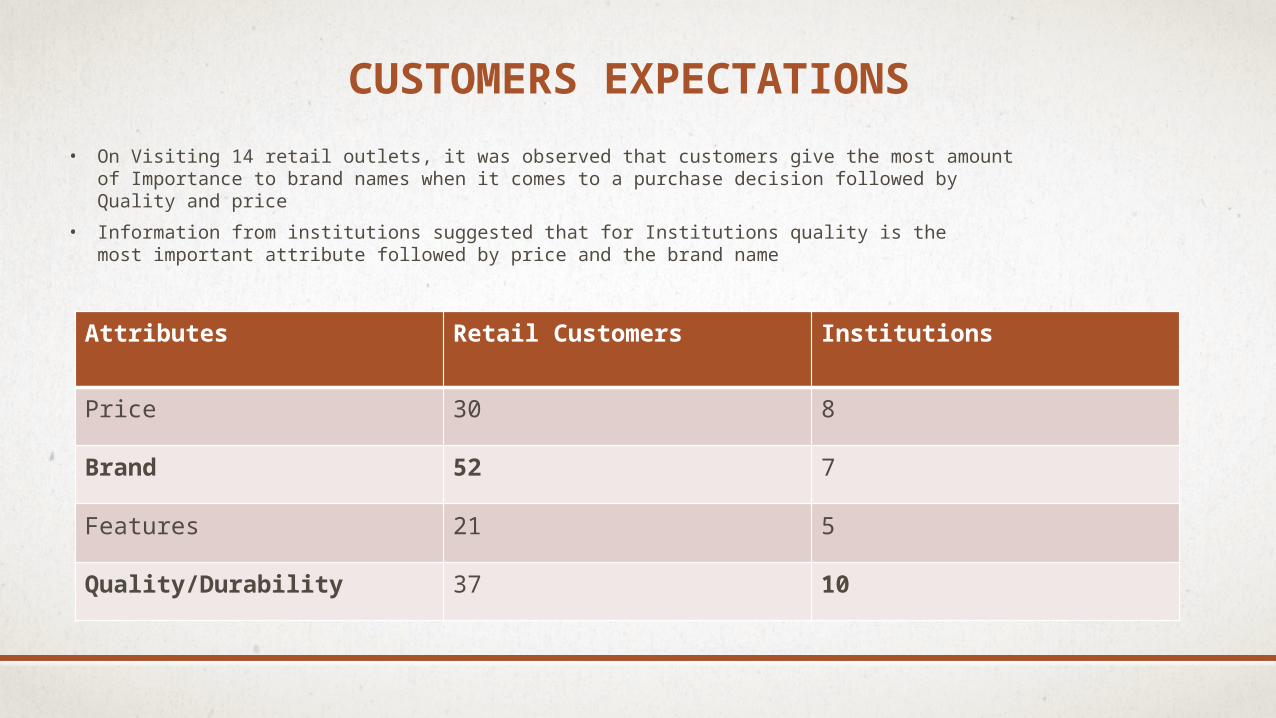

CUSTOMERS EXPECTATIONS

Attributes Retail Customers Institutions

Price 30 8

Brand 52 7

Features 21 5

Quality/Durability 37 10

• On Visiting 14 retail outlets, it was observed that customers give the most amount of Importance to brand names when it comes to a purchase decision followed by Quality and price

• Information from institutions suggested that for Institutions quality is the most important attribute followed by price and the brand name

“SWITCH TO TAPARIA AND EXPERIENCE THE DIFFERENCE”

Thank You

Group 7 : Rohan Pant | Aditya Anand Chegu

Karan Arora | Chinmaya Dandekar

Divya Gorantla | Kaivalya Desai

Related Documents