Zane Wang, Founder & CEO China Rapid Finance LendIt 2017 New York, March 7, 2017 Taking the fast lane there is a lot less traffic there

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Zane Wang,Founder & CEO

China Rapid Finance

LendIt 2017New York, March 7, 2017

Taking the fast lane there is a lot less traffic

there

2

Consumer finance in the beginning of the century (2000)

US

✓Credit reporting – 3 major credit bureaus

✓Decision science – Scoring and decision engines

✓Consumer finance – Credit cards

What about China?

× No credit bureau × No decision science × No consumer

finance

But...Vast market opportunities

3

Consumer finance in the beginning of the century (2000)

China

4

Consumer finance today in 2017

✓Credit reporting – 3 major credit bureaus –Big data

✓Decision science – Scoring and Decision Engines –AI

✓Consumer finance –Credit cards –Alternative lending

US

What about China?

5

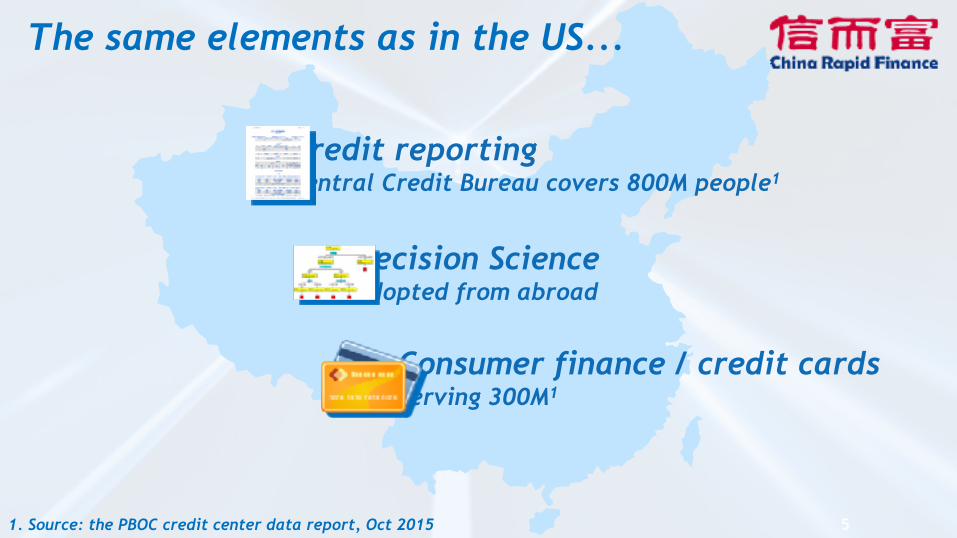

The same elements as in the US...

Credit reporting Central Credit Bureau covers 800M people1

Decision Science Adopted from abroad

Consumer finance / credit cards Serving 300M1

1. Source: the PBOC credit center data report, Oct 2015

24%

15%

9%

8%

Malaysia

Taiwan

Hong Kong

Thailand

China 2%

Non-Mortgage Credit as a Percentage of GDP

Size of China’s Internet consumer finance market Unit : billion yuan

3,398.34

1,942.89

998.34

436.71118.3561.860.68

2011 2012 2013 2015 2016 2017e 2018e 2019e

Growth {%y-o-y}

18.32

2014

174 223 546 269 129 95 75205

...and there is tremendous growth potential

Source: iResearch Inc.

60%

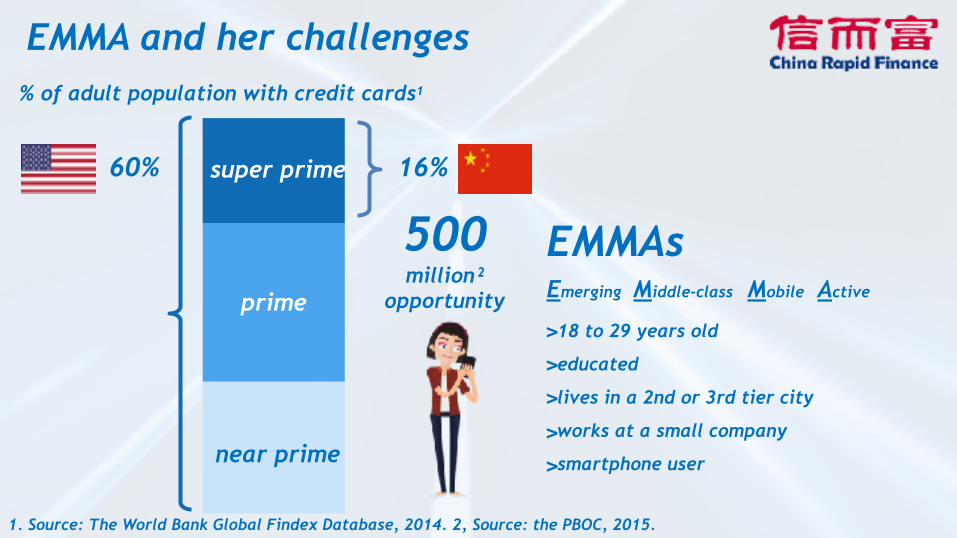

% of adult population with credit cards1

500 million²

opportunity

EMMAs

Emerging Middle-class Mobile Active

>18 to 29 years old

>educated

>lives in a 2nd or 3rd tier city

>works at a small company

>smartphone user

16%super prime

near prime

prime

EMMA and her challenges

1. Source: The World Bank Global Findex Database, 2014. 2, Source: the PBOC, 2015.

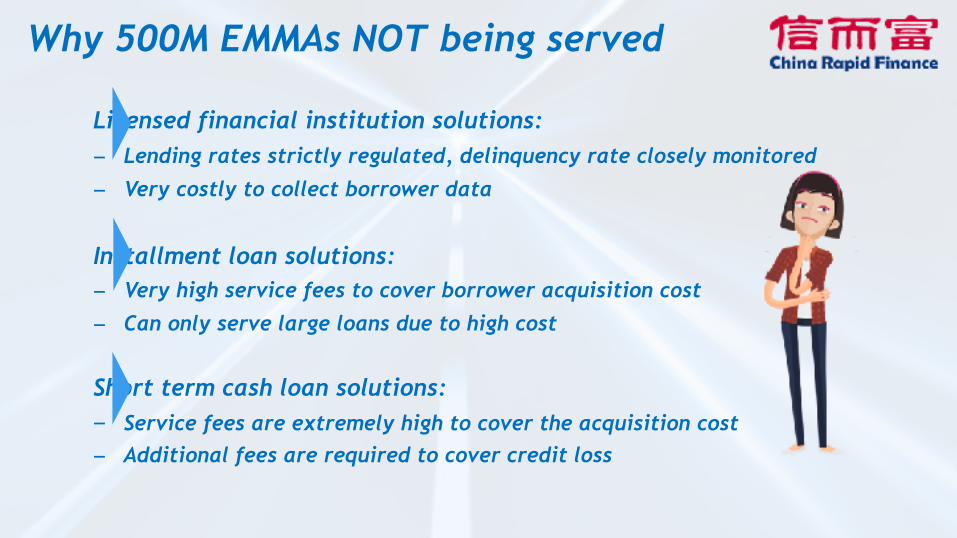

Why 500M EMMAs NOT being served

Licensed financial institution solutions: − Lending rates strictly regulated, delinquency rate closely monitored

− Very costly to collect borrower data

Installment loan solutions: − Very high service fees to cover borrower acquisition cost

− Can only serve large loans due to high cost

Short term cash loan solutions: − Service fees are extremely high to cover the acquisition cost − Additional fees are required to cover credit loss

While the fundamentals are strong:

How to make it happen?

High number of people employed with quality jobs ✓

Stable social economic status✓Rising amout of discretionary spending✓

It’s Technology!

Big data solution for “weak associations” models

Data and channel partners to cut down cost

Predictive Selection Technology drives large scale, low cost, and good quality borrower acquisition

RMB 500

consumption

RMB 500-

2,000

consumption

RMB 2,000- 5,000

consumption

RMB 5,000- 10,000

lifestyle

RMB 10,000- 50,000

lifestyle

Affordable lifetime credit needs

“Low and grow” strategy

Congrats! You are offered credit.

Automated Decision Technology drives credit usage, risk quality, and sustainable growth

Taking the fast lane there is a lot less traffic

there

Related Documents