AUTHOR QUERY FORM Journal title: RRP Article Number: 475191 Dear Author/Editor, Greetings, and thank you for publishing with SAGE. Your article has been copyedited, and we have a few queries for you. Please respond to these queries when you submit your changes to the Production Editor. Thank you for your time and effort. Please assist us by clarifying the following queries: No Query 1 Please check that all authors are listed in the proper order; clarify which part of each author’s name is his or her surname; and verify that all author names are correctly spelled/punctuated and are presented in a manner consistent with any prior publications. 2 Please confirm whether the given conflict of interest statement is accurate. 3 Please confirm whether the given funding statement is accurate. 475191RRP

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AUTHOR QUERY FORM

Journal title: RRP

Article Number: 475191

Dear Author/Editor,

Greetings, and thank you for publishing with SAGE. Your article has been copyedited, and we have a few queries for you. Please respond to these queries when you submit your changes to the Production Editor.

Thank you for your time and effort.

Please assist us by clarifying the following queries:

No Query

1 Please check that all authors are listed in the proper order; clarify which part of each author’s name is his or her surname; and verify that all author names are correctly spelled/punctuated and are presented in a manner consistent with any prior publications.

2 Please confirm whether the given conflict of interest statement is accurate.

3 Please confirm whether the given funding statement is accurate.

475191 RRP

Review of Radical Political EconomicsXX(X) 1 –9

© 2013 Union for Radical Political Economics

Reprints and permission: http://www.sagepub.com/journalsPermissions.nav

DOI: 10.1177/0486613412475191http://rrpe.sagepub.com

XXX10.1177/0486613412475191Review of Radical Political EconomicsDuggan2013

1Keene State College, Keene, NH, USA

Date accepted: March 1, 2012

Corresponding Author:Marie Christine Duggan, Economics, Keene State College, 229 Main St., Keene, NH 03435, USA. Email: [email protected]

Taking Back Globalization: A China-United States Counterfactual Using Keynes’s 1941 International Clearing Union

Marie Christine Duggan1[AQ: 1]

Abstract

Many Americans believe free trade destroyed the U.S. industrial base, and blame foreign work-ers for taking their jobs. During World War II, Keynes had similar misgivings about the effect of postwar free trade on Britain’s economy. Yet for Keynes, economic forces are never inevitable, and capital rather than labor was the cause of trouble. His 1941 proposal for an International Clearing Union suggested capital controls, forced creditor adjustment, and an international fiat reserve as remedies for deindustrialization. This framework channeled financing toward produc-tion rather than speculation, leading to a rising standard of living for workers. A counterfactual with balance of payments data for the United States and China since 1982 suggests his ICU would have prevented U.S. deindustrialization, while yet permitting export-led growth in China.

JEL classification: B22, E42, F55, N22, N25.

Keywords

Keynes, Bretton Woods, capital controls, deindustrialization

For working people in the United States, international trade seems to inexorably erode the manu-facturing base, and with it the standard of living of all but the highly educated. The reaction is often anger at foreign workers, captured in Detroit graffiti (Moore 1989): “If you like Japanese cars, go on Japanese welfare.” The object of the fear has shifted from the Japanese in the 1980s to the Chinese in the early 21st century, but the belief remains that only if it is illegal to buy foreign products will American workers get back to a decent standard of living.

Keynes suggested controlling capital rather than demonizing foreign workers when Britain faced a similar situation of deindustrialization as a result of free trade in 1944. His proposed International Clearing Union (ICU) would have redirected capital from speculation to produc-tion, and managed exchange rates to stabilize global aggregate demand. While the ICU affected

2 Review of Radical Political Economics XX(X)

debate, Keynes’s ideas were not implemented; rather, the U.S.-controlled International Monetary Fund (IMF) came into being. An exercise imagining “what if” the ICU were in effect since 1982 serves to clarify Keynes’s ideas and also suggests the cause of U.S. deindustrialization was not industrialization elsewhere, so much as escape from long-term investment in production into short-term speculation.

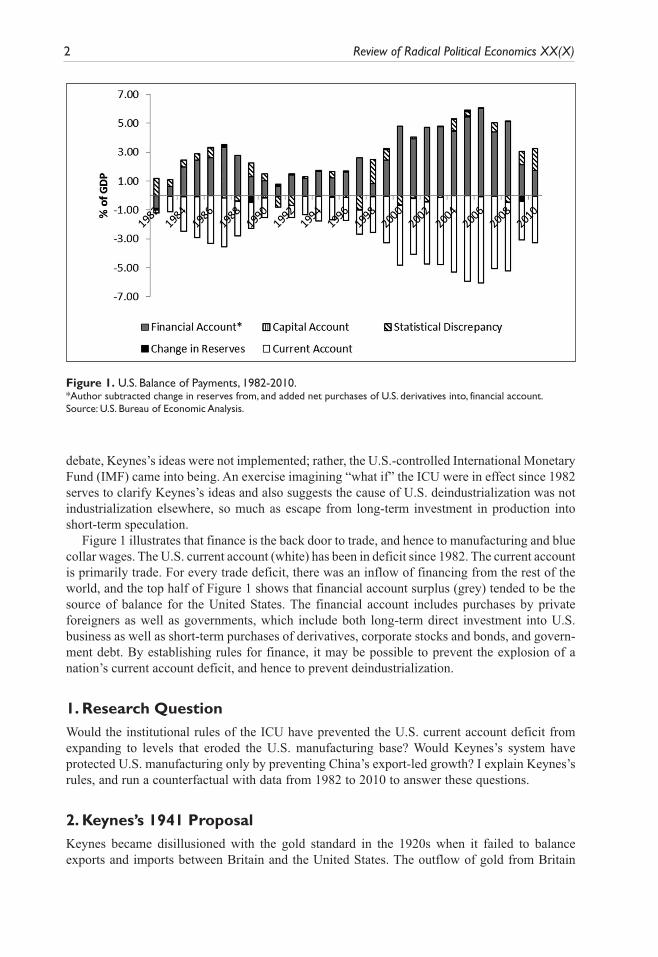

Figure 1 illustrates that finance is the back door to trade, and hence to manufacturing and blue collar wages. The U.S. current account (white) has been in deficit since 1982. The current account is primarily trade. For every trade deficit, there was an inflow of financing from the rest of the world, and the top half of Figure 1 shows that financial account surplus (grey) tended to be the source of balance for the United States. The financial account includes purchases by private foreigners as well as governments, which include both long-term direct investment into U.S. business as well as short-term purchases of derivatives, corporate stocks and bonds, and govern-ment debt. By establishing rules for finance, it may be possible to prevent the explosion of a nation’s current account deficit, and hence to prevent deindustrialization.

1. Research QuestionWould the institutional rules of the ICU have prevented the U.S. current account deficit from expanding to levels that eroded the U.S. manufacturing base? Would Keynes’s system have protected U.S. manufacturing only by preventing China’s export-led growth? I explain Keynes’s rules, and run a counterfactual with data from 1982 to 2010 to answer these questions.

2. Keynes’s 1941 ProposalKeynes became disillusioned with the gold standard in the 1920s when it failed to balance exports and imports between Britain and the United States. The outflow of gold from Britain

Figure 1. U.S. Balance of Payments, 1982-2010.*Author subtracted change in reserves from, and added net purchases of U.S. derivatives into, financial account. Source: U.S. Bureau of Economic Analysis.

Duggan 3

into the United States to pay for Britain’s trade deficit should have pushed up U.S. prices, while decreasing Britain’s. Inflation would then have priced U.S. exports out of international markets, and reduced the U.S. trade surplus; deflation in Britain should have reduced Britain’s trade deficit. However, the United States sterilized inflows of gold, so prices did not rise. Furthermore, Britain borrowed gold to reduce tensions over wage cuts, and British exports remained uncom-petitive (Ahamed 2009; Keynes 2010 [1925]).

The lesson was that the gold standard did not force creditor nations to invest their surpluses, nor to expand domestic demand for imports, nor to increase the price level at home. Instead, creditor nations had the option to hoard gold. Debtor nations, on the other hand, were forced to take action. They could raise interest rates in order to instigate inflows of short-term capital. High interest rates would cause deflation, lower incomes, and decrease imports; by pushing wages down, exports would be more competitive. In 1926, Britain overvalued the pound, ran a trade deficit, raised interest rates, and insisted that coal miners take a 10 percent wage cut (Keynes 1925 in [1931]). This involved a 12-day strike of 1.75 million people which split the populace along class lines. Equal pressure on creditors and debtors to adjust current account imbalance would be part of Keynes’s proposal, with an eye toward removing the pressure on workers in deficit nations.

In Keynes’s proposal, surpluses above a certain level would be confiscated at the end of the year (1980 [1941]: 36). Keynes did not anticipate actual confiscation, but rather assumed that threat would lead nations to import, or invest the funds into plant and equipment in other nations (1980 [1941]: 49). A third option was to donate the money abroad. Investment in foreign stocks and bonds was excluded because international flows of short-term capital could assist the wealthy in evading taxes. Such restrictions would have redirected international funds into long-term, job-inducing investment rather than speculation.

Keynes wanted a “use it or lose it” system, but one with wide choices for how the surplus nation could spend. An international fiat reserve issued by the ICU (Bancor) would replicate the multilateral nature of the gold standard. A nation with a financial surplus in Bancor could spend it in any ICU member nation, not simply in the nation to which it had exported. Creation of a fiat reserve was also a tactic to get deficit nations out of the position of begging for gold from the United States. Keynes would give a generous portion of Bancor to every nation, equal to one-half the annual five year moving average of exports plus imports. Unlike gold, Bancor could not be hoarded, as it had to be spent within the ICU. The fiat reserve would also give the ICU political independence, in contrast to the IMF, which relies on donors for funding. Issuing the reserve meant the ICU could create larger liquidity than any mechanism that relied upon donations for its funding.

Keynes’s ICU was based on “the banking principle” (Dam 1982: 78). A domestic bank takes depositors’ savings and lends them out to borrowers. In contrast, no funds would be deposited in Keynes’s ICU. Rather, nations would be granted overdraft quotas. Bancor would come into exis-tence when a nation activated the overdraft. Bancor credit would be created in the account of its creditor nation, with the deficit nation’s overdraft limit reduced one-for-one. Where one typically thinks of banks as obtaining loanable funds from customers who save, in the ICU nations that borrowed would be the source of credits in the accounts of nations that sold.

Gold could be converted to Bancor; however, Bancor could never be converted to gold. One-way convertibility meant threat of confiscation would ensure that Bancor above quota would be spent by the end of the year, rather than converted to gold for hoarding.

With the ICU, national currencies would have fixed but adjustable rates to Bancor. Keynes saw devaluation as destabilizing for the system, and as the desperate way out of a balance of payments deficit. Fixed exchange rates were desirable, but if deficits reached 25 percent of a nation’s overdraft quota, devaluation would be optional, and when deficits reached 50 percent of

4 Review of Radical Political Economics XX(X)

a nation’s overdraft quota, devaluation would be automatic. Similarly, if nations had a surplus 25 percent as large as overdraft quota, they could revalue, and upon reaching surplus levels 50 per-cent of overdraft, would be required to revalue.

3. Specific HypothesisThe hypothesis is that Keynes’s ICU would have prevented deindustrializing levels of current account deficit in the United States, without preventing China from pursuing export-led growth. The ICU would have forced the United States to devalue the dollar substantially and sooner, and would have forced China to either revalue, invest directly into production in other countries, or to donate aid.

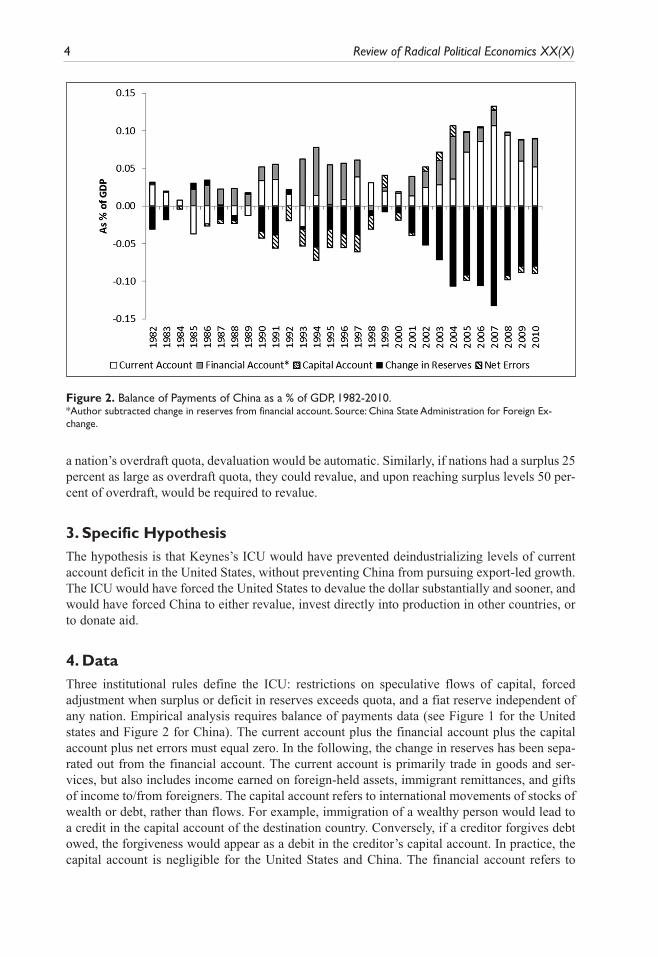

4. DataThree institutional rules define the ICU: restrictions on speculative flows of capital, forced adjustment when surplus or deficit in reserves exceeds quota, and a fiat reserve independent of any nation. Empirical analysis requires balance of payments data (see Figure 1 for the United states and Figure 2 for China). The current account plus the financial account plus the capital account plus net errors must equal zero. In the following, the change in reserves has been sepa-rated out from the financial account. The current account is primarily trade in goods and ser-vices, but also includes income earned on foreign-held assets, immigrant remittances, and gifts of income to/from foreigners. The capital account refers to international movements of stocks of wealth or debt, rather than flows. For example, immigration of a wealthy person would lead to a credit in the capital account of the destination country. Conversely, if a creditor forgives debt owed, the forgiveness would appear as a debit in the creditor’s capital account. In practice, the capital account is negligible for the United States and China. The financial account refers to

Figure 2. Balance of Payments of China as a % of GDP, 1982-2010.*Author subtracted change in reserves from financial account. Source: China State Administration for Foreign Ex-change.

Duggan 5

flows such as foreign portfolio investment (purchases/sales by private foreign sector or foreign governments of stocks and bonds) as well as foreign direct investment. The financial account “other” includes government to government loans, bank loans, loans to and from international organizations, and trade credits. Since the dollar is the global reserve, U.S. financial inflows typically include foreign government purchases of U.S. government debt.

Capital, current, and financial accounts would balance were it not for errors. Furthermore, if balance is obtained only by drawing down reserves, the nation has a balance of payments deficit, while a balance of payments surplus results in an increase to reserves.1

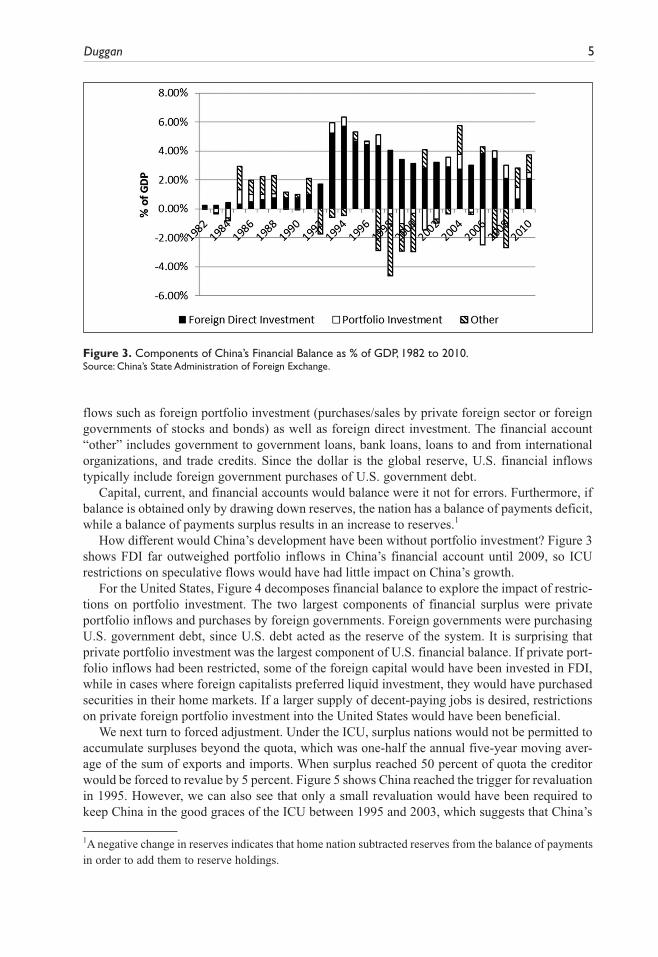

How different would China’s development have been without portfolio investment? Figure 3 shows FDI far outweighed portfolio inflows in China’s financial account until 2009, so ICU restrictions on speculative flows would have had little impact on China’s growth.

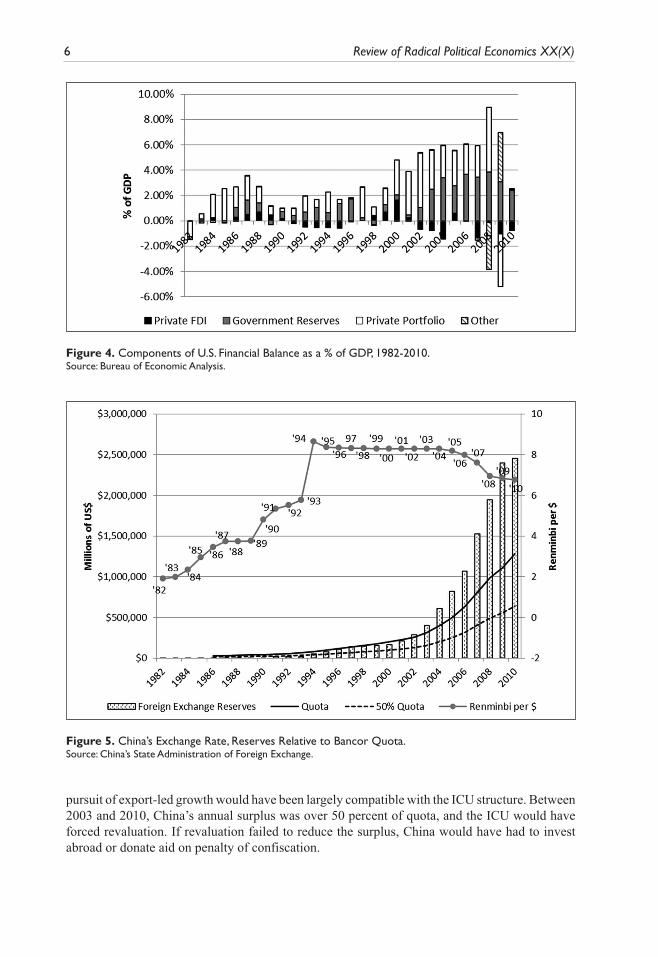

For the United States, Figure 4 decomposes financial balance to explore the impact of restric-tions on portfolio investment. The two largest components of financial surplus were private portfolio inflows and purchases by foreign governments. Foreign governments were purchasing U.S. government debt, since U.S. debt acted as the reserve of the system. It is surprising that private portfolio investment was the largest component of U.S. financial balance. If private port-folio inflows had been restricted, some of the foreign capital would have been invested in FDI, while in cases where foreign capitalists preferred liquid investment, they would have purchased securities in their home markets. If a larger supply of decent-paying jobs is desired, restrictions on private foreign portfolio investment into the United States would have been beneficial.

We next turn to forced adjustment. Under the ICU, surplus nations would not be permitted to accumulate surpluses beyond the quota, which was one-half the annual five-year moving aver-age of the sum of exports and imports. When surplus reached 50 percent of quota the creditor would be forced to revalue by 5 percent. Figure 5 shows China reached the trigger for revaluation in 1995. However, we can also see that only a small revaluation would have been required to keep China in the good graces of the ICU between 1995 and 2003, which suggests that China’s

Figure 3. Components of China’s Financial Balance as % of GDP, 1982 to 2010.Source: China’s State Administration of Foreign Exchange.

1A negative change in reserves indicates that home nation subtracted reserves from the balance of payments in order to add them to reserve holdings.

6 Review of Radical Political Economics XX(X)

pursuit of export-led growth would have been largely compatible with the ICU structure. Between 2003 and 2010, China’s annual surplus was over 50 percent of quota, and the ICU would have forced revaluation. If revaluation failed to reduce the surplus, China would have had to invest abroad or donate aid on penalty of confiscation.

Figure 4. Components of U.S. Financial Balance as a % of GDP, 1982-2010.Source: Bureau of Economic Analysis.

Figure 5. China’s Exchange Rate, Reserves Relative to Bancor Quota.Source: China’s State Administration of Foreign Exchange.

Duggan 7

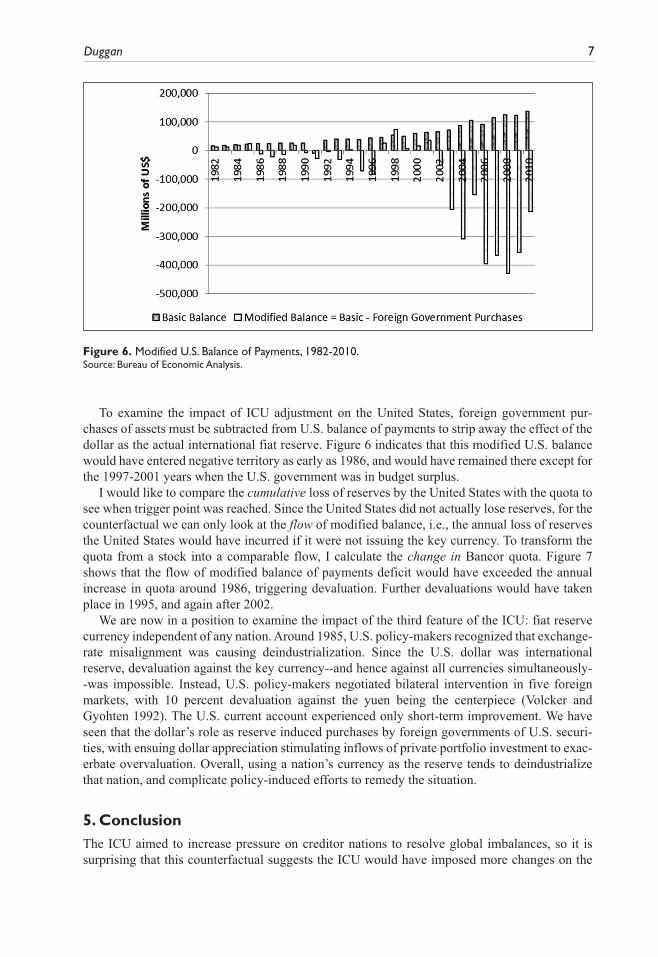

To examine the impact of ICU adjustment on the United States, foreign government pur-chases of assets must be subtracted from U.S. balance of payments to strip away the effect of the dollar as the actual international fiat reserve. Figure 6 indicates that this modified U.S. balance would have entered negative territory as early as 1986, and would have remained there except for the 1997-2001 years when the U.S. government was in budget surplus.

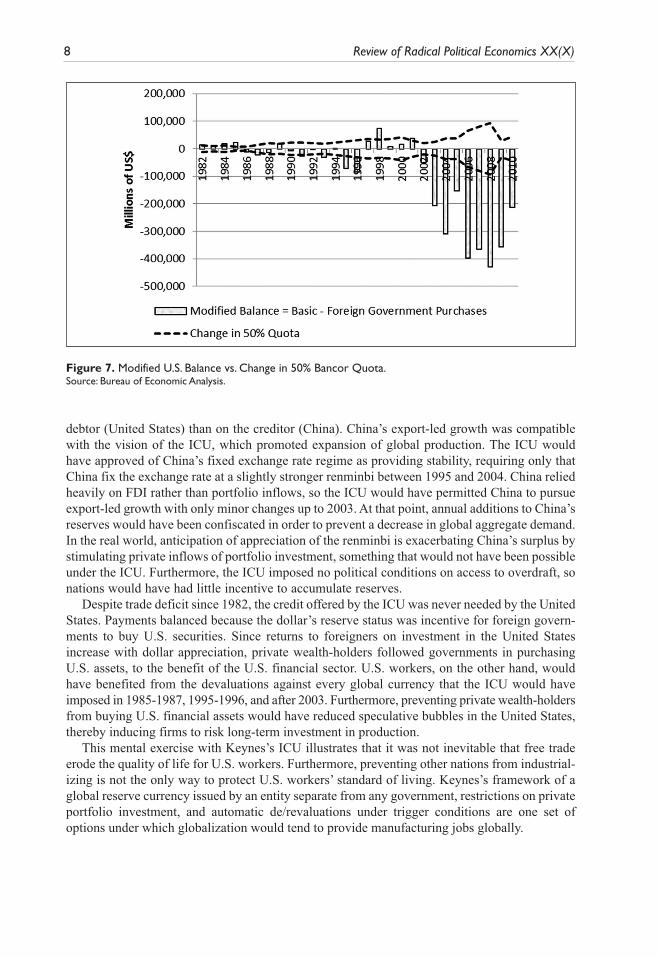

I would like to compare the cumulative loss of reserves by the United States with the quota to see when trigger point was reached. Since the United States did not actually lose reserves, for the counterfactual we can only look at the flow of modified balance, i.e., the annual loss of reserves the United States would have incurred if it were not issuing the key currency. To transform the quota from a stock into a comparable flow, I calculate the change in Bancor quota. Figure 7 shows that the flow of modified balance of payments deficit would have exceeded the annual increase in quota around 1986, triggering devaluation. Further devaluations would have taken place in 1995, and again after 2002.

We are now in a position to examine the impact of the third feature of the ICU: fiat reserve currency independent of any nation. Around 1985, U.S. policy-makers recognized that exchange-rate misalignment was causing deindustrialization. Since the U.S. dollar was international reserve, devaluation against the key currency--and hence against all currencies simultaneously--was impossible. Instead, U.S. policy-makers negotiated bilateral intervention in five foreign markets, with 10 percent devaluation against the yuen being the centerpiece (Volcker and Gyohten 1992). The U.S. current account experienced only short-term improvement. We have seen that the dollar’s role as reserve induced purchases by foreign governments of U.S. securi-ties, with ensuing dollar appreciation stimulating inflows of private portfolio investment to exac-erbate overvaluation. Overall, using a nation’s currency as the reserve tends to deindustrialize that nation, and complicate policy-induced efforts to remedy the situation.

5. ConclusionThe ICU aimed to increase pressure on creditor nations to resolve global imbalances, so it is surprising that this counterfactual suggests the ICU would have imposed more changes on the

Figure 6. Modified U.S. Balance of Payments, 1982-2010.Source: Bureau of Economic Analysis.

8 Review of Radical Political Economics XX(X)

debtor (United States) than on the creditor (China). China’s export-led growth was compatible with the vision of the ICU, which promoted expansion of global production. The ICU would have approved of China’s fixed exchange rate regime as providing stability, requiring only that China fix the exchange rate at a slightly stronger renminbi between 1995 and 2004. China relied heavily on FDI rather than portfolio inflows, so the ICU would have permitted China to pursue export-led growth with only minor changes up to 2003. At that point, annual additions to China’s reserves would have been confiscated in order to prevent a decrease in global aggregate demand. In the real world, anticipation of appreciation of the renminbi is exacerbating China’s surplus by stimulating private inflows of portfolio investment, something that would not have been possible under the ICU. Furthermore, the ICU imposed no political conditions on access to overdraft, so nations would have had little incentive to accumulate reserves.

Despite trade deficit since 1982, the credit offered by the ICU was never needed by the United States. Payments balanced because the dollar’s reserve status was incentive for foreign govern-ments to buy U.S. securities. Since returns to foreigners on investment in the United States increase with dollar appreciation, private wealth-holders followed governments in purchasing U.S. assets, to the benefit of the U.S. financial sector. U.S. workers, on the other hand, would have benefited from the devaluations against every global currency that the ICU would have imposed in 1985-1987, 1995-1996, and after 2003. Furthermore, preventing private wealth-holders from buying U.S. financial assets would have reduced speculative bubbles in the United States, thereby inducing firms to risk long-term investment in production.

This mental exercise with Keynes’s ICU illustrates that it was not inevitable that free trade erode the quality of life for U.S. workers. Furthermore, preventing other nations from industrial-izing is not the only way to protect U.S. workers’ standard of living. Keynes’s framework of a global reserve currency issued by an entity separate from any government, restrictions on private portfolio investment, and automatic de/revaluations under trigger conditions are one set of options under which globalization would tend to provide manufacturing jobs globally.

Figure 7. Modified U.S. Balance vs. Change in 50% Bancor Quota.Source: Bureau of Economic Analysis.

Duggan 9

Declaration of Conflicting InterestsThe author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.[AQ: 2]

FundingThe author(s) received no financial support for the research, authorship, and/or publication of this article.[AQ: 3]

References

Ahamed, L. 2009. Lords of finance. New York: Penguin Press.Dam, K. W. 1982. The rules of the game. Chicago: University of Chicago Press.Keynes, J. M. 2010[1925]. Economic consequences of Mr. Churchill. In Essays in persuasion, ed. D. Mog-

gridge. London: Palgrave Macmillan.Keynes, J. M. 1980[1941]. The origins of the clearing union. In Collected writings of John Maynard Keynes,

ed. D. Moggridge, vol. 25. Cambridge: Cambridge University Press.Moore, M. 1989. Roger & me.Robertson, D. H. 1943. The post-war monetary plans. Economic Journal 53: 352-360.Skidelsky, R. 2003. John Maynard Keynes 1883-1946. London: Penguin Books.Volcker, P., and T. Gyohten. 1992. Changing fortunes. New York: Times Books.

Author Biography

Marie Christine Duggan, Associate Professor of Economics, Keene State College, New Hampshire; she received her PhD from the New School, and teaches history of economic thought, economic history, and macroeconomics.

Related Documents