INCEIF The Global University in Islamic finance Kuala Lumpur, Malaysia CIFP part 2 TK2002 Takaful and Actuarial Practices Title Takaful Industry: Challenges and Unique Selling Propositions Semester Sept 2013 Name: Fatima Zahra Habib Eddine Matric No: 1300135

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INCEIF

The Global University in Islamic finance

Kuala Lumpur, Malaysia

CIFP part 2 TK2002 Takaful and Actuarial Practices

Title Takaful Industry:

Challenges and Unique Selling Propositions

Semester Sept 2013

Name: Fatima Zahra Habib Eddine Matric No: 1300135

Fatima Zahra Habib Eddine 1300135

2

Introduction

Takaful is considered to be the Islamic equivalent of the conventional insurance. It aims to alleviate

the hardships and to provide material security and assistance for those who face an expected risk or

distress.

The word takaful comes from the Arabic word kafala that means guarantee and it refers to the fact

that in takaful concept a group of persons share the risks among them through a financial

contribution that is based on the donation (tabarru’). These donations compensate the person of the

group affected by a misfortune, based on the hadith narrated by Abu Huraira (r.a.) in Sahih al-

Bukhari that the Prophet Mohammad peace be upon him said: “Whosoever removes a worldly

hardship from a believer, Allah (SWT) will remove from him one of the hardships of the day of

judgement. Whosoever alleviates form one, Allah (SWT) will alleviate his lot in this world and the

next”.

Therefore, there are no prohibited elements by Shariah in this form of mutual assistance, in

particular: gharar (uncertainty) and maisir (gambling) do not exist as the fund is composed by

donations; riba also is avoided, as the money donated is not invested in non-Shariah interest earned

instruments.

The source of takaful comes from the Quran and the Sunna. Since the takaful contract contains the

element of mutual assistance the contract is binding both to the operator and the participant under

the Islamic law.

Islamic Banking Industry started to grow thirty years ago and has boomed, while the takaful

industry is still in its infancy stage.

In this brief research we will analyse peculiarities and performance of the takaful industry, focusing

mainly on the experience of the countries where the takaful business is important in terms of size.

In the first part we will also assess the industry performance and discuss that challenges faced

today. In the second part we will discuss the potentials of the takaful market and how can be

developed further to create a competitive advantage, compared to conventional insurance, that can

be marketed as a unique selling proposition or propositions.

Fatima Zahra Habib Eddine 1300135

3

1. Brief history

Most likely takaful transactions have been practiced before the Islam. It has been embraced and

encouraged by the Quran and the practice of the Prophet Mohammad peace be upon him and the

Sahaba, and developed over the centuries. In fact, the concept is revealed in the Quran, in the

Chapter dedicated to Prophet Yusuf (a.s.) when he interpreted the dream of the King of Egypt as a

command from Allah to store the surplus grains and distribute it during the famine in the following

years.

Then, in the pre-Islamic Arabia the concept of Al-‘Aqila was a common practice among tribes

leaders. The tribes that are blood related were supporting each other financially to pay a financial

reward in case of murder done by one of their tribe member. The money was given to the family of

the murdered on behalf of the killer. The Prophet Mohammad peace be upon him embraced this

practice, becoming part of the Sunna and subject to regulations by the Shariah. Therefore, in

Islamic Law, the damages for victims of death or body injuries caused intentionally were awarded

based on the principles of Al-Diyya or blood money and Al-Daman or compensation.

Also, the first Constitution of Madina, known as Charter of Madina (622 AD) contained elements

of insurance, including the religious minorities living in the city, that have been protected by the

new born Islamic Community.

In the 19th century a Hanafi lawyer, Ibn Abidin (1784 – 1836) has developed the legal concept of

insurance contract looking at marine insurance that was the first form of insurance that have been

developed in Islamic countries.

Fatima Zahra Habib Eddine 1300135

4

2. Assessing Takaful Industry

2.1 Insurance in emerging markets

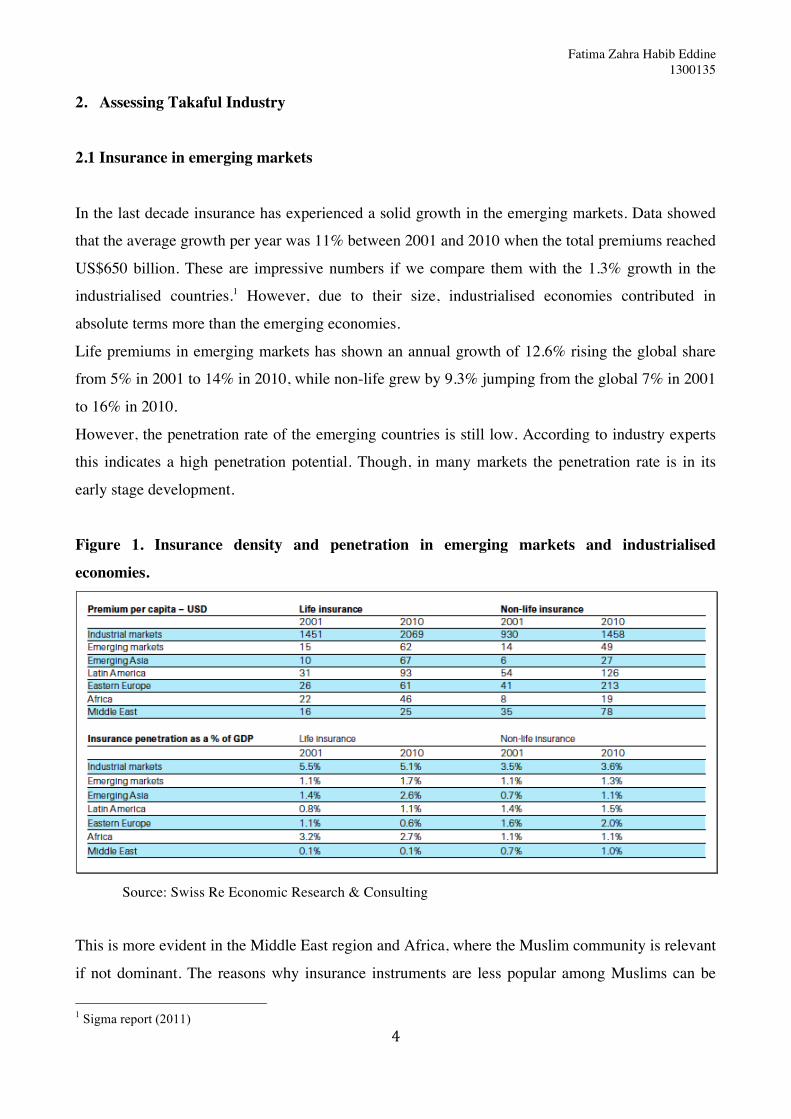

In the last decade insurance has experienced a solid growth in the emerging markets. Data showed

that the average growth per year was 11% between 2001 and 2010 when the total premiums reached

US$650 billion. These are impressive numbers if we compare them with the 1.3% growth in the

industrialised countries.1 However, due to their size, industrialised economies contributed in

absolute terms more than the emerging economies.

Life premiums in emerging markets has shown an annual growth of 12.6% rising the global share

from 5% in 2001 to 14% in 2010, while non-life grew by 9.3% jumping from the global 7% in 2001

to 16% in 2010.

However, the penetration rate of the emerging countries is still low. According to industry experts

this indicates a high penetration potential. Though, in many markets the penetration rate is in its

early stage development.

Figure 1. Insurance density and penetration in emerging markets and industrialised

economies.

Source: Swiss Re Economic Research & Consulting

This is more evident in the Middle East region and Africa, where the Muslim community is relevant

if not dominant. The reasons why insurance instruments are less popular among Muslims can be

1 Sigma report (2011)

Fatima Zahra Habib Eddine 1300135

5

searched among several factors: first of all, conventional insurance system is not permissible

according to the Islamic law mainly because it contains elements of uncertainty and gambling, and

also because the insurance funds are ordinarily invested in financial instruments based on the

interest rate profit. Therefore, many Muslims are reluctant towards insurance activities and this

intolerability is often extended to takaful services. The takaful industry is also under-represented

relative to the size of the global Muslim population. In countries where the potential of growth is

high insurance is a new concept and takaful too.

Another reason can be the low income of the majority of the Islamic population, therefore they do

not feel the need of risk protection especially in societies where they can still rely on family and

group provisions.

However, the Muslim population growth forecasted for the next decade is huge. According to Pew

Research Center, it represented 23% in 2012, reaching 1.6 billion Muslims and expected to increase

by 35% in the next 20 years accounting for 2.2 billion.

Figure 2: Muslims growth compared to the world’s population.

Source: Pew Research Center 2011.

These numbers bring high expectations for insurance and insurance and takaful firms as they

indicate a huge potential of growth, and takaful can play a key role rising the insurance awareness

Fatima Zahra Habib Eddine 1300135

6

among Muslims populations. In fact, takaful industry penetration is expected to surpass the

conventional rate in countries with high Muslim concentration.

2.2 Takaful Market

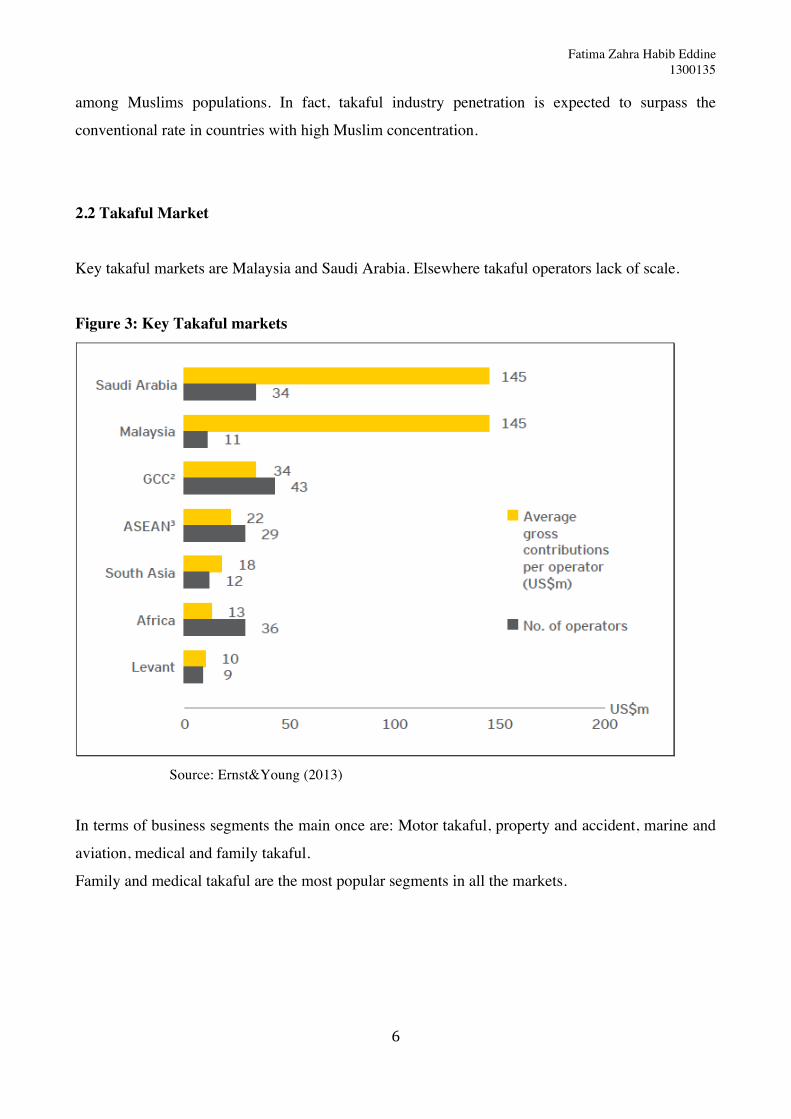

Key takaful markets are Malaysia and Saudi Arabia. Elsewhere takaful operators lack of scale.

Figure 3: Key Takaful markets

Source: Ernst&Young (2013)

In terms of business segments the main once are: Motor takaful, property and accident, marine and

aviation, medical and family takaful.

Family and medical takaful are the most popular segments in all the markets.

Fatima Zahra Habib Eddine 1300135

7

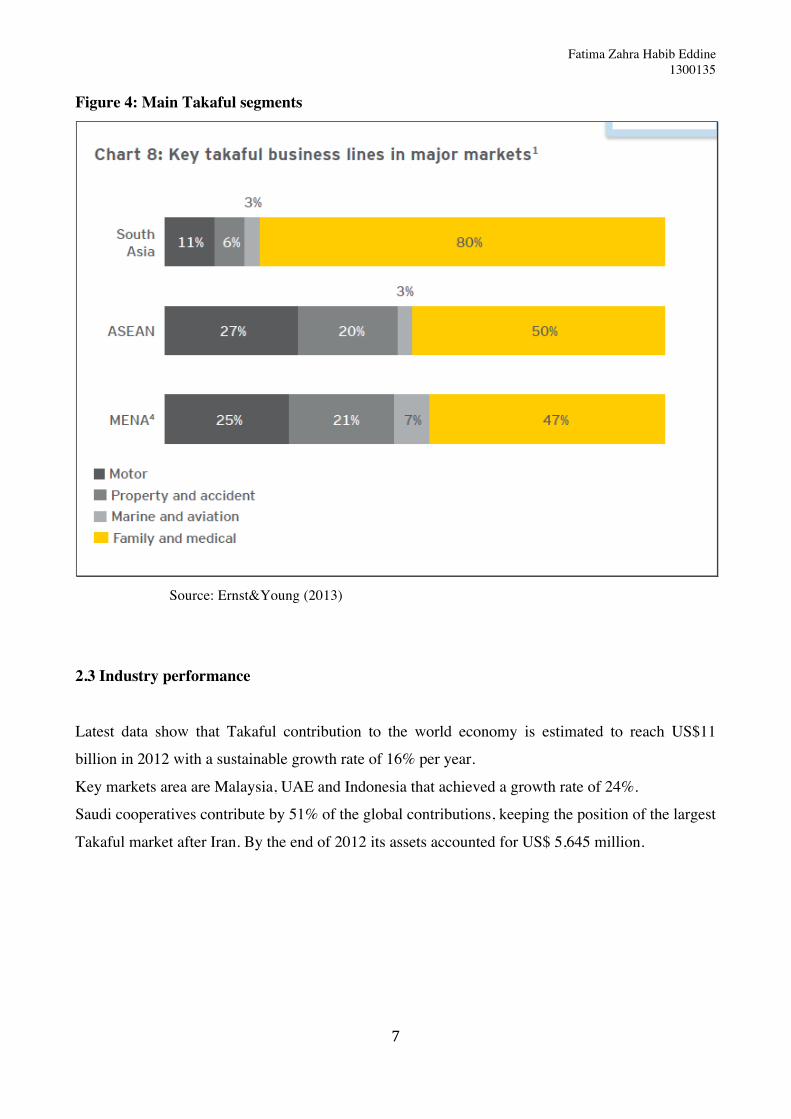

Figure 4: Main Takaful segments

Source: Ernst&Young (2013)

2.3 Industry performance

Latest data show that Takaful contribution to the world economy is estimated to reach US$11

billion in 2012 with a sustainable growth rate of 16% per year.

Key markets area are Malaysia, UAE and Indonesia that achieved a growth rate of 24%.

Saudi cooperatives contribute by 51% of the global contributions, keeping the position of the largest

Takaful market after Iran. By the end of 2012 its assets accounted for US$ 5,645 million.

Fatima Zahra Habib Eddine 1300135

8

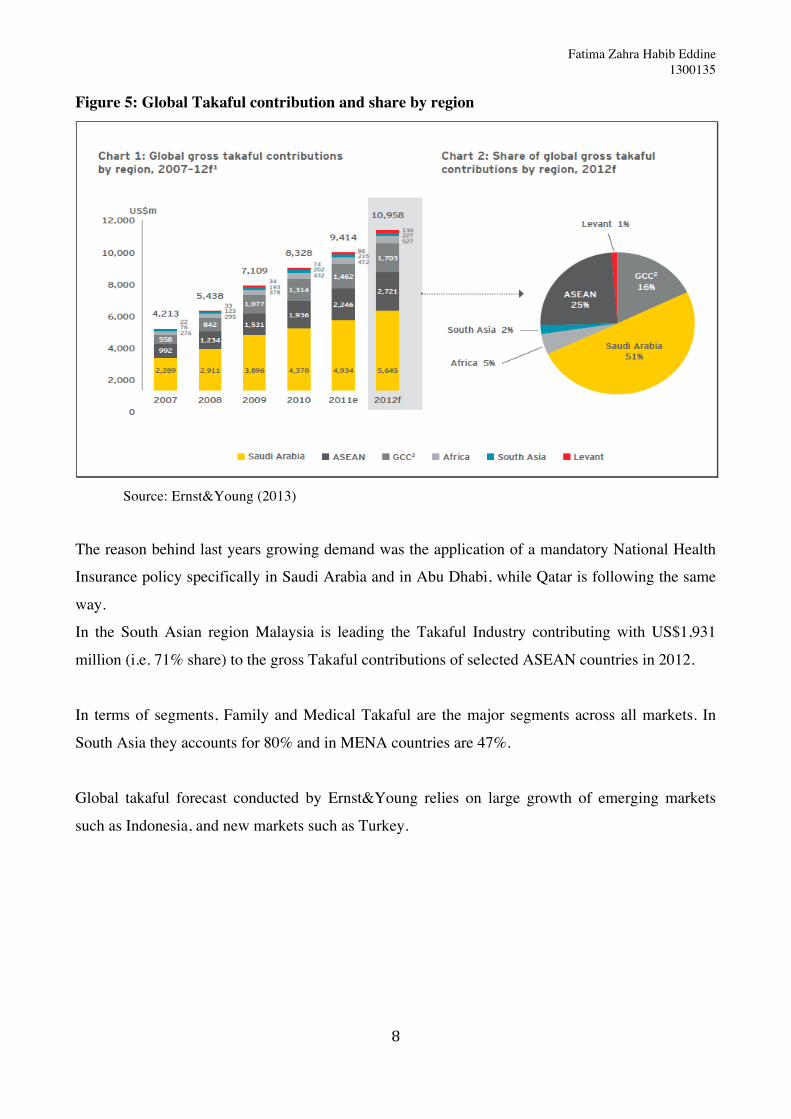

Figure 5: Global Takaful contribution and share by region

Source: Ernst&Young (2013)

The reason behind last years growing demand was the application of a mandatory National Health

Insurance policy specifically in Saudi Arabia and in Abu Dhabi, while Qatar is following the same

way.

In the South Asian region Malaysia is leading the Takaful Industry contributing with US$1,931

million (i.e. 71% share) to the gross Takaful contributions of selected ASEAN countries in 2012.

In terms of segments, Family and Medical Takaful are the major segments across all markets. In

South Asia they accounts for 80% and in MENA countries are 47%.

Global takaful forecast conducted by Ernst&Young relies on large growth of emerging markets

such as Indonesia, and new markets such as Turkey.

Fatima Zahra Habib Eddine 1300135

9

Figure 6: Expected global Takaful contribution

Source: Ernst&Young (2013)

2.4 Financial Performance

We want to discuss financial performance of takaful operators here because is a challenge in many

markets. In fact the impressive growth of the industry does not necessarily translate into

profitability.

In 2012 average return on equity (ROE) are struggling for profitability in Saudi Arabia (4%) and

GCC area (0.4%) in general. However, compared to last years, it finally turned positive. In

Malaysia instead, the ROE has been positive over the last three years and is growing year by year

(2012: 13%).

Combined operation ratio (COR) measures insurance underwriting profitability. It expresses total

operating costs of claims as a percentage of premiums. Again the figures are not optimistic: overall

main markets the COR is just below 100% in 2012 while in 2011 they were above. But there is a

Fatima Zahra Habib Eddine 1300135

10

slight improvement. However, in GCC takaful industry is paying out more money in claims rather

than receiving it from premiums, while conventional insurers are making underwriting profit.

The expense ratio measures the insurer’s business efficiency to investors. The average ratio of

takaful operators in the analysed regions is narrowed, because they can’t control costs being still far

from reaching an economy of scale.

And finally, the reinsurance ratio reveals that in Saudi Arabia and in GCC transfer a higher

proportion of their underwriting business to reinsurers because they focus more in general takaful

plans which needs more reinsurance cover, while in Malaysia is more focused on the family takaful

plans.

Takaful financial performance is a challenge for takaful operators in many markets. It indicates that

the industry has lack of profitability, long-term sustainability, solvency and limited premiums as a

consequence of high level of competition. Therefore, if they will not be able to differentiate

themselves from their conventional peers as well as among themselves they would likely survive.

2.5 Takaful models in practice

Takaful industry has produced different models of Islamic insurance reflecting different

interpretations and experiences.2

Takaful Ta’awuni model

Was the first model adopted by a takaful company, being build in Sudan in 1979 when the first

takaful operator started his business. The regulator then made it mandatory for takaful operators. In

this model the profit and surplus belongs only to participants.

Mudaraba Model

It has been the main implemented model in Malaysia for nearly 20 years and it is practiced also in

Brunei. According to this model profit is shared between participants and operators.

Wakalah Model

2 Akhter (2010)

Fatima Zahra Habib Eddine 1300135

11

This model has been practiced in Malaysia and in Bahrain where government made it mandatory for

takaful and re-takaful companies. The model is becoming popular because it is considered to be

more transparent and because the Shariah issues involved on it are less than other models.

Mixed Model (Mudaraba + Wakala)

The mixed model is dominant in GCC and practiced by companies across the world. Pioneers of

this model believe that it can facilitate a standardisation process versus a unified model in all the

world.

Wakala Model with Waqf fund

This model was practice in Pakistan and South Africa. Under this model the operator does not have

an obligation to distribute the surplus but he could define a sharing ratio of distribution.

2.6 Challenges

Ernest&Young takaful report (2013) remarks the intense competition that erodes the already

challenging industry margins. Discussed below some of the challenges that affects theprofitability

of new industry.

Marketing takaful

So far takaful operators relied only on the Shariah compliancy of their product to drive the sector.

This non-strategy resulted limited the access of the takaful industry to a high range of population in

many countries that the can benefit from takaful services and drive the industry growth rate. It has

been noted a lack in marketing strategy, in communication, in segmentation, in product

differentiation and so on.

For these reasons takaful is still far from achieving a success comparing with conventional

counterpart.

Segmentation and product differentiation

Takaful operators compete mainly on prices rather than product differentiation or customer

segmentation. They rely on low-value products while they need to manage high volumes in order to

generate high revenue and hence profitability. Thus, having in general a low penetration rate of

insurance activities in the countries where takaful are operating and facing a big competition by

Fatima Zahra Habib Eddine 1300135

12

new takaful players attracted by the impressive growth rate of the industry, the profitability within

the industry at this time is a big question mark.

A business segment still not explored by takaful business is the commercial business. The

specificities of this segment are high risks but also high profitability. Also, takaful needs to

establish solid relationships with Islamic corporations in order to address them with takaful

products and create synergies between the industries.

Lack of regulations and standardisation

The only countries that have issued specific laws on takaful are Malaysia, Pakistan and Bahrain.3

Lately Qatar issued Islamic Finance Amendments Rules (2012) to close the operation of all Islamic

windows operated by conventional firms, with limited exceptions. The other markets suffer lack of

regulations. The Industry suffers from absence of standardisation that affects their business

especially companies with cross-border selling.

Lack of consistent regulations and standardisation is also a constraint to the rapid expansion of the

industry regionally and globally. Due to the different interpretations of the Shariah Scholars and to

the lack of regulations, there are different takaful models. Also, International entities such as the

Islamic Finance Services Board (IFSB) and the Accounting and Auditing Organization for Islamic

and Financial Institutions (AAOIFIC) established core principles to be applied to takaful

companies.

Regulations are continuing to evolve in the different markets but still with the characteristic to be

different according to the national legislation practices and the different interpretations of the

Shariah.

Industry experts are concerned about this gap in particular for what concerns open issues such as

surplus distribution, the rights of participants in takaful companies and the obligations for provision

Qardul Hasan to cover deficits on participants’ fund.4

3 Ernst&Young (2012) 4 Ernst&Young (2013)

Fatima Zahra Habib Eddine 1300135

13

3. Takaful today: which Selling Proposition?

3.1 Shariah compliancy

Shariah compliancy is not a competitive advantage on its own because the factors involved on a

business are many. Takaful companies have relied until now on the religious characteristics of their

products to market them, which means that they sold without extra effort relying on the Islamic

peculiarity of the products. But any commercial product needs to be built, branded and

communicated in order to reach customers. Yet takaful operators have built a strategy to position

their products neither to communicate them.

However, the compliancy of the takaful to the Islamic Law can be enforced and collocated in a

more spiritual dimension for Muslims customers. Indeed the peculiarity of takaful versus

conventional companies is the concept of tabarru’, donation: the insurance premium is paid on the

basis of tabarru’ (donations). Participants that donate to the funds agree to cooperate and be

mutually responsible to help one another in the case one of them suffers a defined loss. Therefore,

participants in takaful are generally lead by spiritual purposes: they select a Shariah compliant

insurance provider over a conventional one and they gain a hasana, a spiritual reward or good deed.

Than they make a donation to the fund in case one of the members is in need, and that is another

hasana, as in Islam the good intention alone is accountable as such. If a member suffers a loss he

will be covered by the fund and for participants that is ten hasanat (Based on the hadith Sahih).

Therefore, the concept of tabarru’ has the potential to be developed further and create something

unique that can constitute its comparative advantage and attract Muslims and non-Muslims at the

same level because of its ethical purposes.5

For instance, one of the proposals advanced in the book edited by Jaffer (2007) is that a Family

takaful might offer participants the possibility to donate the money after their death to charity, in a

way that the deceased can get rewarded also after his death and in the Hereafter. Or, the takaful

surplus can be donated for specific project to a local mosque or charity, or used in microfinance or

microtakaful projects to alleviate the poverty of local communities, since in most of the countries

where takaful operators are operating are the poverty is not rare. In this way the takaful companies

pursue business and ethical activities distinguishing themselves from their conventional peers,

gaining customers trust and loyalty and also, and also overcoming the common idea that insurance

5 Jaffer (2007)

Fatima Zahra Habib Eddine 1300135

14

cannot be halal, contributing in this way to increase the penetration rate of the takaful among the

emerging economies.

3.2 Mutual cooperation

Therefore, developing further the Shariah compliancy characteristic of the takaful and thanks to the

cooperative nature of takaful concept, there are high opportunities for operators to achieve a deeper

and meaningful relationship with customers beyond the traditional relationship company-customers.

It increases the potential of takaful services to provide a high level of quality service resulting in

high customer satisfaction.

Customers are different and some wants material benefits some others spiritual benefits. Having an

insurance that is also Shariah compliant that gives the benefit of doing good deeds and supporting

the economic and spiritual development of both individuals and local communities, is a powerful

motivation factor for Muslims “to buy”, as they believe the benefits of doing good deeds are of

great value. This can attract non-Muslims as well: today more people are becoming more conscious

about ethics, transparency and justice.

3.3 Surplus Distribution

At time of writing6 all takaful operators in Malaysia offer to share the net surplus of income over

liabilities in the takaful funds, according to a pre-agreed ratio such as 50:50, 40:60 etc. The

opportunity of receiving a refund is an attractive value proposition to many customers, no matter

what is their faith, since conventional insurance in Malaysia do not offer this option. Therefore,

many Malaysian assume that surplus sharing is a feature unique to takaful, and many non-Muslims

customers were attracted by it. However, customers expect takaful operators to offer also the same

benefits as conventional insurers, yet remaining Shariah compliant. But not all participants

welcome the surplus distribution practice. In fact, such practice led to disappointment among

participants because they recognise it as an innovation to the original takaful concept and therefore

they have concern about its legitimacy on Shariah.7 Therefore, it is important to develop products

that match the expectations of customers: instead of distributing surplus with operators a valid

6 Ibid. 7 WB (2013).

Fatima Zahra Habib Eddine 1300135

15

alternative could be offering participants the possibility to choose to whom to donate them within a

range of not-for profit activities such as microtakaful, microfinance, waqf, etc. This can be another

solid strategy of creating an added value from a genuine Shariah compliant product, but will also

contribute in standardisation of the best practices within the takaful industry.

Finally, in order to compete takaful companies need to differentiate themselves by offering value-

added services that conventional insurance cannot, that are widely accepted and with the potential

to be developed further and to be enhanced within the industry.

3.4 Branding Takaful

One of the criticisms that have been made to the takaful industry is the lack of marketing strategies.

As a matter of fact the business suffers the lack of branding efforts that identifies and differentiates

it from conventional insurance.

Consumers and prospects need to see takaful products as a specific Shariah compliant solutions

built to offer them solutions for their wellbeing. This is the main way to make takaful products

attractive to prospects and willing to go for them. The customers than will give the takaful products

a personality i.e. how they will perceive the products according to the benefits they feel they can

provide them.

A Brand to be such has to have a mission and values. Takaful mission and values is clear and it

constitutes its competitive advantage over the conventional competitor. The spiritual benefits of

takaful is its identity, therefore it is a perfect starting point to build a specific identity for takaful. In

fact, some customers are happy to pay a premium in choosing takaful plans rather than going for the

equivalent counterpart. There are also strong evidences that conventional insurance is not able to

fulfil the needs of Muslims customers while takaful has the potential to fulfil the needs of both,

Muslims and non-Muslims.

Therefore it is important to move from just a Shariah compliant insurance product to an established

brand well positioned in the mind of the customers and in the insurance market.

3.5 Segmentation

Many operators continue to offer a standardised product proposition to all customers, which lead

them to compete only in prices paying high rates in terms of profitability. Instead, a detailed

customer analysis is needed in order to understand their needs and match target customers with

Fatima Zahra Habib Eddine 1300135

16

customised propositions for specific segments. They will be able then to differentiate themselves in

addressing attractive segments, build a suitable product offer, pricing and accessing opportunities

that have been untapped until now.

Therefore, differentiation is a key to success against the strong and established competition of their

conventional peers.

An unexplored area of business is commercial and corporate sector. Underwriting bigger and more

sophisticated commercial risks will drive to high profitability.8

Which segmentation for takaful companies?

Operators can segment their target by:

o Geographic segmentation: responding to the needs of regions, or countries, cities or rural

communities.

o Behavioural: response to events, products, attitudes, reactions, knowledge, etcetera.

o Segmentation by occasions: such as Hajj, ‘Umra, Islamic festivities, marriage, new-born

babies, and so on.

o Segmentation by benefits: according to the benefits that a product may provide.

o Product differentiation between takaful and conventional insurance and, at another level,

differentiation between takaful products themselves.

3.6 Efficiency in customer service

Entering in such a competitive and globalised industry i.e. the insurance business, requires branding

goes hand in hand with customer service. Because of the level of sophistication and competition

insurance companies compete mainly in the quality service offered to customers. Therefore, takaful

operators have to build their business strategies in order to deliver high products and services to

meet their customers’ needs.

In order to customise their products according to customers’ preferences and meet their

expectations, operators have to conduct quality survey and investigate customer experience and

expectations. Indeed, it is likely that customers choose a company that is concerned about their

needs and how they feel, making efforts to satisfy them. In fact, customer service is not only about

8 Ernst&Young (2013)

Fatima Zahra Habib Eddine 1300135

17

the results you deliver but it is more about the experience you create and deliver whether the

customer is in need or is not.

This subject becomes more important if we look at the Shariah view. Prophet Mohammad peace be

upon him said what it can be translated as: “It is better for anyone of you to help his brother fulfil

his need than observing l’i’tikaaf9 at my mosque for two months.” (Reported by Haakim).

In another hadith the Prophet of Islam peace be upon him said what can be translated as:

“I swear by the One Whose Hand my soul is in that you will not enter paradise until you believe.

And you won’t believe until you love one another. May I tell you something that if you practice it

you will love another, spread the salaam (Islamic greeting) among you”. (Reported by Muslim).

Therefore, takaful operators have one more reason upon their counterpart to excel in service

delivery and i.e. the religious factor. Being a Shariah compliancy service company should grant also

a Shariah compliant quality service to customers as it is expected, because customers measure also

the quality of the service expecting to see the Islamic values reflected on it.

Therefore a high quality service within the Islamic Finance industry in general and within the

takaful services in particular is a potential opportunity to offer a unique selling proposition gaining

the satisfaction of the Muslim customers and attracting Non-Muslims clients.

3.7 Distribution channels

Takaful industry at beginning was relating to synergy business from Islamic Banks and

government-related business, being less competitive to the conventional counterpart. But with more

players entering the takaful market, the competition increased and now more companies are using a

variety of distribution channels10.

The takaful business is retail-based, and it has lack of identification of most effective forms of

distribution. In fact, the commonly used channels are branches, agents and Islamic Banks known as

Bancatakaful. This is the most preferred mode of distribution, followed by agency-based

distribution.

9 L’i’tikaf is the spiritual retreat in the mosque. 10 Islamic Finance News Supplement (2012)

Fatima Zahra Habib Eddine 1300135

18

Agencies are fast gaining ground and identified as a relatively more efficient form of distribution,

because more customers reached at lower expenses. In Malaysia takaful companies use six main

distribution channels, which are:

o Retail and corporate agencies;

o Bancatakaful;

o Corporate direct channels;

o Brokers;

o Direct marketing channels, although it is less prevalent.

It was noticed that agents are more effective in penetrating non-Muslim customers and in expanding

both Family and General Takaful products.

Technology also is becoming an important element in enhancing cross-border distribution of

Takaful products.

Bankatakaful can be the best instrument to distribute takaful products in markets with very low

penetration rate. Studies show that Bancassurance is still very popular (see Swiss Re sigma No

5/2007, “Bancassurance: emerging trends, opportunities and challenges”) but it carries very high

costs compared to the other channels.

3.8 Human resources

The demand for human capital in the Islamic Financial Industry is high and it is increasing with its

growth. The Industry suffers from lack of trained human resources capital that provides competitive

customer service and technical expertise together with a sound knowledge in Shariah.

The expected growth of takaful industry will create a larger demand of high quality resources.

Hence the takaful industry has the opportunity to create a competitive advantage that can be

transformed in a unique selling proposition attracting and retaining high quality human capital. This

will affect its costs in the short term but will also drive its competitiveness and profitability in the

long-term.11

Also, in terms of education programmes it is necessary that governments support post-graduate

takaful education programmes in order to increase the competitive advantage of the industry

creating a pool of professional experts. Malaysia and Bahrain are the only countries at this date

involved in such initiatives to support the industry.

11 Ernst&Young (2012)

Fatima Zahra Habib Eddine 1300135

19

Conclusion

In this brief research we have learned about takaful industries, performance and challenges. We

have also found out that the areas to be developed are many and they are all with the potential to

create a unique service to Muslim and non-Muslim communities both in industrialised and in

emerging countries.

Takaful products and services have to be treated as any “normal” products to be placed and sold in

the market. So, it needs a proper business plan comprehensive of feasibility studies, business plan,

identification of market targets and creation of a brand. Customer service also is not optional, on the

contrary it is crucial in maintaining a good customer base and identifying new needs that can help in

differentiate the products offered.

Today’s global takaful performance demonstrates that it is not enough to focus on the Shariah

compliancy of the takaful products to make the best sale of them but there are needs to develop the

concept of Shariah compliant products and investigate the roots of takaful concept to come out with

new business ideas that can boost and spread the takaful spirit as a mutual-assistance concept.

Takaful industry has high potential to grow and many sectors to develop in order to differentiate

itself and create a brand that it is not only halal, but above all, it is a unique product and a unique

experience.

Fatima Zahra Habib Eddine 1300135

20

References:

Books:

Serap O. Gonulal (2013), Takaful and Mutual Insurance. Alternative Approaches to Managing

Risks, Washington DC: The World Bank.

“Islamic Insurance: Trends, Opportunities and the Future of Takaful”, 2007, edited by Sohail

Journals and reports:

W. Akhter (2010), “Takaful models and global practices” MPRA Paper No. 40010, posted 12, July

2012.

F.S. Hamid (2001), “Measuring service quality in the takaful industry”, SEGi Review, Vol 4, No. 1.

S. Weber (2012), “Takaful: more than just green shoots”, Islamic Finance News, February 2012.

Islamic Finance news Supplement (2012), “The Takaful and Re-Takaful industry”, May 2012.

Sigma Re (2008), “Insurance in the emerging markets: overview and prospects for Islamic

insurance”, Swiss Reinsurance Company Ltd, No. 5/2008.

Sigma Re (2011), “Insurance in the emerging markets: growth drivers and profitability, Swiss

Reinsurance Company Ltd, No. 5/2011.

Ernst&Young (2011), “World Takaful Report 2011: Transforming Operating Performance”.

Ernst&Young (2012), “The world Takaful report 2012”.

Ernst&Young (2013), “Global Takaful Insights 2013: Finding growth markets”.

Data from the net:

http://www.pewforum.org/2012/12/18/global-religious-landscape-muslim/

http://www.pewforum.org/2011/01/27/the-future-of-the-global-muslim-population/

http://www.islamicfinancenews.com/listing_article_ID.asp?nm_id=25600

Related Documents