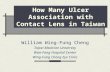

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 01 March 2013 Asia Pacific/Taiwan Equity Research Healthcare Taiwan Contact Lens Sector INITIATION Clear opportunity in sight Figure 1: BRICs to lead growth in global contact lens market 1.9% 5.0% 5.9% 6.2% 6.9% 15.1% 19.8% 0% 5% 10% 15% 20% 25% Japan Asia Pacific EMEA World Americas BRICs China CAGR (2011-2016) Source: Cooper, Credit Suisse estimates ■ Initiating on the Taiwan contact lens sector with an OVERWEIGHT call. In tandem, we initiate coverage on Ginko with an OUTPERFORM rating and St. Shine with a NEUTRAL rating. We expect the global contact lens market to see a 6.2% CAGR during 2012-16 with BRICs leading the market on a 15.1% CAGR during the same period. This is driven by increased penetration and consumer upgrading on the back of economic growth. ■ China market to take off. We found that within Asia, contact lens penetration picks up significantly once GDP per capita is close to US$10k. Contact lens penetration in China is now only 5% compared with 23-25% for developed Asian countries. We forecast China’s contact lens market will double from US$312 mn to US$642 mn by 2016, implying a 19.8% CAGR during 2012-16. ■ Multiple entry barriers to support high margins to continue. The Global contact lens market is oligopolistic: gross profit margins are >60%. We expect the high margins to continue behind multiple entry barriers, including: 1) increased difficulty getting product licenses; 2) rapidly rising advertising costs, and; 3) distribution channels already dominated by multinational brands. ■ We believe select Taiwan contact lens players, e.g., Ginko, have the best positioning to capture China’s strong growth. We initiate on Ginko with an OUTPERFORM rating and target price of NT$540 (29% implied upside), based on 0.9x 2013E PEG. Our forecast 2013/2014 EPS are 9%/17% higher than consensus due to higher sales growth assumptions. We also initiate on St. Shine with a NEUTRAL rating and target price of NT$504 (flat with the trading price), based on 18x 2013E EPS. This tepid view, is based on longer-term concerns that ~80% of its sales come from the saturated Japanese and Taiwanese markets. Risks to our forecasts include failure to ramp capacity, slower-than-expected penetration and migration to substitutes — LASIK surgery or silicone hydrogel lens. Research Analysts Jeremy Chen 886 2 2715 6368 [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

01 March 2013

Asia Pacific/Taiwan

Equity Research

Healthcare

Taiwan Contact Lens Sector INITIATION

Clear opportunity in sight

Figure 1: BRICs to lead growth in global contact lens market

1.9%

5.0%

5.9%

6.2%

6.9%

15.1%

19.8%

0% 5% 10% 15% 20% 25%

Japan

Asia Pacific

EMEA

World

Americas

BRICs

China

CAGR (2011-2016) Source: Cooper, Credit Suisse estimates

■ Initiating on the Taiwan contact lens sector with an OVERWEIGHT call.

In tandem, we initiate coverage on Ginko with an OUTPERFORM rating and

St. Shine with a NEUTRAL rating. We expect the global contact lens market

to see a 6.2% CAGR during 2012-16 with BRICs leading the market on a

15.1% CAGR during the same period. This is driven by increased

penetration and consumer upgrading on the back of economic growth.

■ China market to take off. We found that within Asia, contact lens

penetration picks up significantly once GDP per capita is close to US$10k.

Contact lens penetration in China is now only 5% compared with 23-25% for

developed Asian countries. We forecast China’s contact lens market will

double from US$312 mn to US$642 mn by 2016, implying a 19.8% CAGR

during 2012-16.

■ Multiple entry barriers to support high margins to continue. The Global

contact lens market is oligopolistic: gross profit margins are >60%. We

expect the high margins to continue behind multiple entry barriers, including:

1) increased difficulty getting product licenses; 2) rapidly rising advertising

costs, and; 3) distribution channels already dominated by multinational

brands.

■ We believe select Taiwan contact lens players, e.g., Ginko, have the

best positioning to capture China’s strong growth. We initiate on Ginko

with an OUTPERFORM rating and target price of NT$540 (29% implied

upside), based on 0.9x 2013E PEG. Our forecast 2013/2014 EPS are

9%/17% higher than consensus due to higher sales growth assumptions.

We also initiate on St. Shine with a NEUTRAL rating and target price of

NT$504 (flat with the trading price), based on 18x 2013E EPS. This tepid

view, is based on longer-term concerns that ~80% of its sales come from the

saturated Japanese and Taiwanese markets. Risks to our forecasts include

failure to ramp capacity, slower-than-expected penetration and migration to

substitutes — LASIK surgery or silicone hydrogel lens.

Research Analysts

Jeremy Chen

886 2 2715 6368

01 March 2013

Taiwan Contact Lens Sector 2

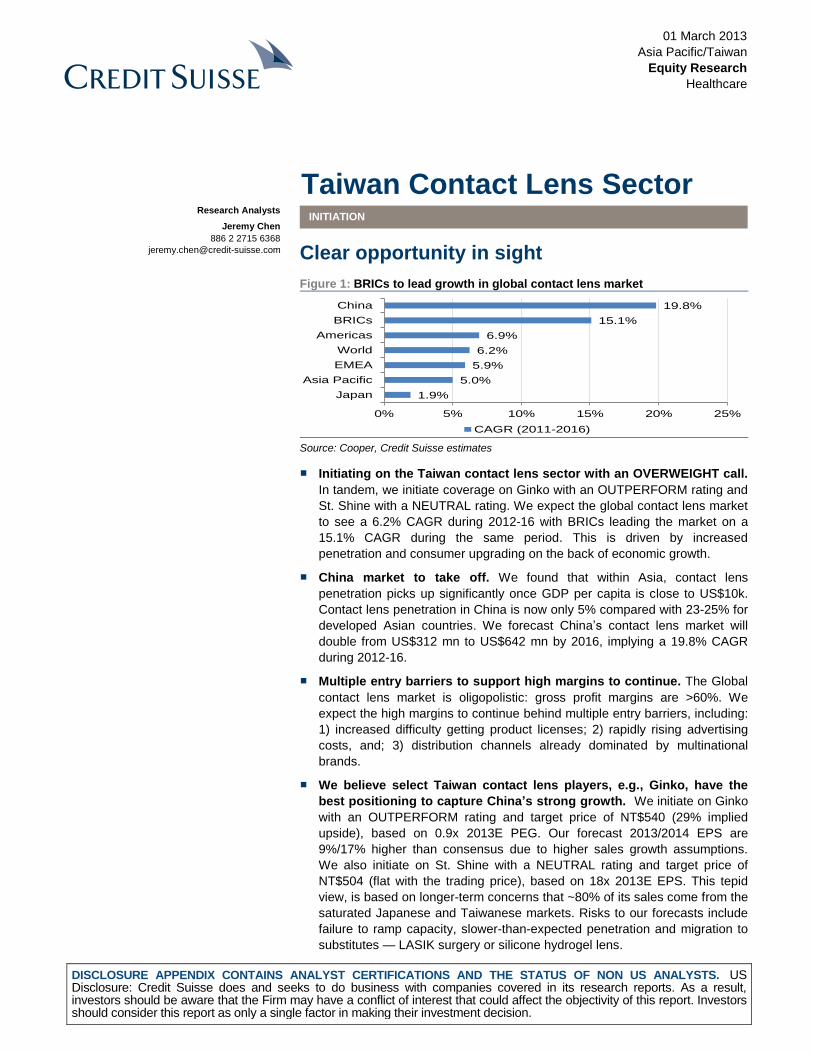

Focus charts Figure 2: Global contact lens market size Figure 3: Steeper penetration curve for Asian countries

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1996 2000 2004 2005 2006 2007 2008 2009 2010 2011

US$mn

Global market size yoy growth (RHS; %)

Source: Contact Lens Spectrum Source: Ginko, Credit Suisse estimates

Figure 4: Global contact lens market by brand - 2011 Figure 5: Global contact lens market by region - 2011

J&J42%

CIBA25%

Cooper17%

B&L11%

Other5%

America38%

Asia33%

Europe29%

Source: Ginko Source: Cooper

Figure 6: China contact lens market by brand - 2011 Figure 7: We expect China contact lens market to take off

on the back of rising affordability

Hydron28%

J&J27%

B&L21%

Weicon6%

CIBA3%

Other15%

- 2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,000 20,000

Tia

njin

Shanghai

Beiji

ng

Jia

ngsu

Zhejia

ng

Inner

Mongolia

Lia

onin

gG

uangdong

Fujia

nS

handong

Chin

aJili

nC

hongqin

gH

ubei

Hebei

Shaanxi

Nin

gxia

Heilo

ngjia

ng

Shanxi

Xin

jiang

Hunan

Qin

ghai

Hain

an

Henan

Sic

huan

Jia

ngxi

Anhui

Guangxi

Tib

et

Gansu

Yunnan

Guiz

hou

GDP per capita (US$) - 2016

Source: Ginko Source: Credit Suisse estimates

01 March 2013

Taiwan Contact Lens Sector 3

Clear opportunity in sight We expect BRICs to lead market growth during 2012-

16

The global contact lens market has seen a steady 7.5% CAGR in the past 15 years and is

expected to see a 6.2% CAGR through 2012-16. While the US (38% of the global market)

and Japan (20%) may witness relatively stable 7% and 2% CAGRs, respectively, we

expect BRICs, especially China, to lead the market with a 15.1% CAGR during the same

period, despite relatively small global share of 10% by 2016E. This is largely driven by

increased penetration and consumer upgrading on economic growth.

China market to take off

We uncovered that for Asian countries, contact lens penetration picks up significantly once

GDP per capita is close to the US$10k level. Currently, contact lens penetration in China is

only 5% and this compares with 23-25% penetration in Taiwan, Japan, Korea, Singapore

and Hong Kong. We forecast China’s contact lens market to double from US$312 mn to

US$642 mn by 2016, implying a 19.8% CAGR during 2012-16, driven by a faster-than-

expected increase in contact lens penetration on rising affordability.

Multiple entry barriers to support high margins to

continue

The global contact lens market is oligopolistic, where brand vendors enjoy at least 60%

gross margin. This high margin is protected by multiple entry barriers, including: 1)

Increased difficulty to get product licenses—Contact lenses are considered a “medical

device”. As such, governments have established stringent licensing standards for contact

lens manufacturing and distribution. For each product, vendors/OEM are required to

submit clinical data and get approvals from local regulators such as CE Certification

(Europe), FDA inspection (US), GMP (Taiwan), and SFDA (China). The approval process

generally takes one to two years from filing to official product launch; 2) Skyrocketing

advertising costs—Any newcomer to the market has to be prepared to spend heavily on

advertising and promotion. There is deep brand loyalty in this market: customers are not

keen to put an unproven product in their eyes and stay with brands that have proven

themselves over decades. And the game is changing : advertising per second on Chinese

TV costs 5x more now than in 2005, according to Ginko; 3) Distribution channels are

dominated by multinational brands—From a retail channel perspective, they will not

replace bestselling brands with any new brand on their shelf, given the cash conversion

cycle for the latter might be longer.

Stock calls

We initiate coverage on Ginko with an OUTPERFORM rating. With a strong EPS CAGR of

36% over 2012-2014, we set our target price of NT$540 (upside potential of 29%) based

on 0.9x 2013E PEG, given: 1) biggest sales channel in China; 2) full product offering at

competitive price points; 3) strong brand recognition ; and 4) a dedicated and experienced

management team. Our forecast 2013/2014 EPS are 9%/17% higher than consensus’ due

to higher sales growth assumptions.

We also initiate coverage on St. Shine with a NEUTRAL rating. We forecast a 15% EPS

CAGR during 2012-14 for St. Shine, compared with its peer group average of 20% CAGR.

We set our target price of NT$504 (flat with trading price) based on 18x 2013E EPS due to

the longer-term concern that ~80% of its revenue comes from the relatively saturated

Japanese (2% CAGR during 2008-2012) and Taiwanese markets, evidenced by

decelerating sales from a 27% CAGR during 2005-2010 to 10% in 2011 and -6% in 2012.

While the US and Japan are

expected to see relatively

stable 7% and 2% CAGRs,

respectively, we expect

BRICs to lead the market

with a 15.1% CAGR during

2012-16

We expect the China market

to see a 19.8% CAGR

through 2012-16

Global contact lens market

is oligopolistic; branded

vendors enjoy not less than

60% gross profit margin

We assign Ginko an

OUTPERFORM rating and

St. Shine a NEUTRAL rating

01 March 2013

Taiwan Contact Lens Sector 4

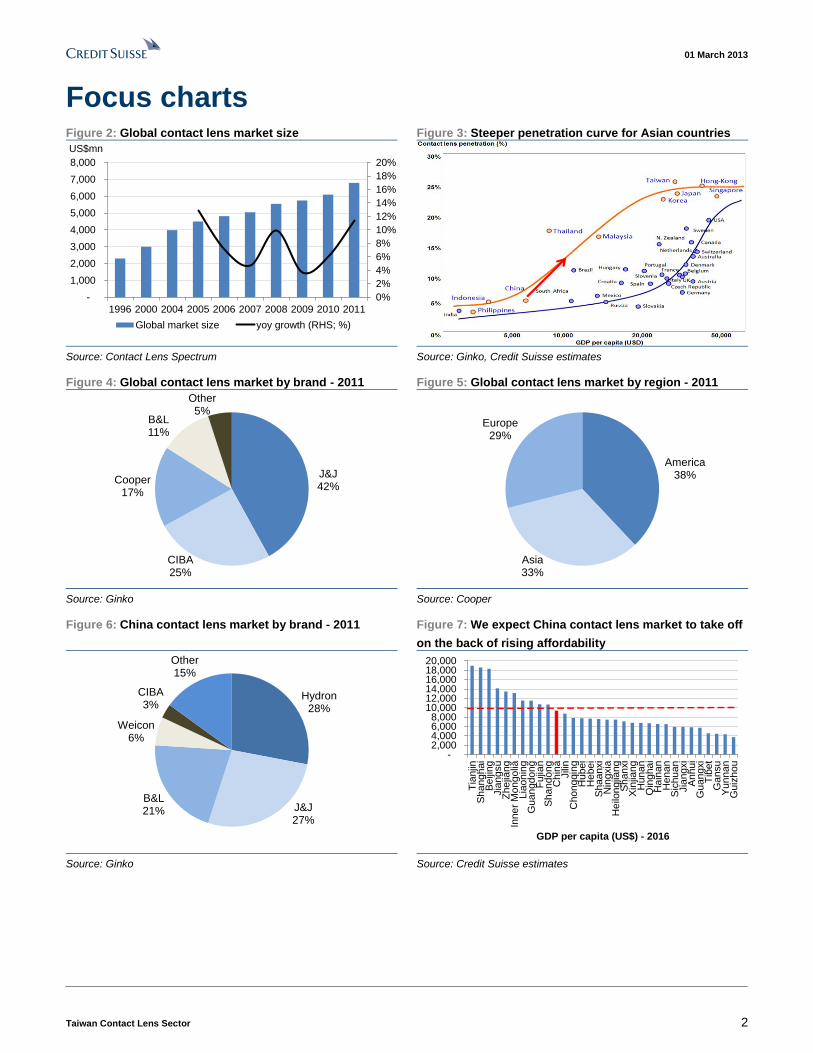

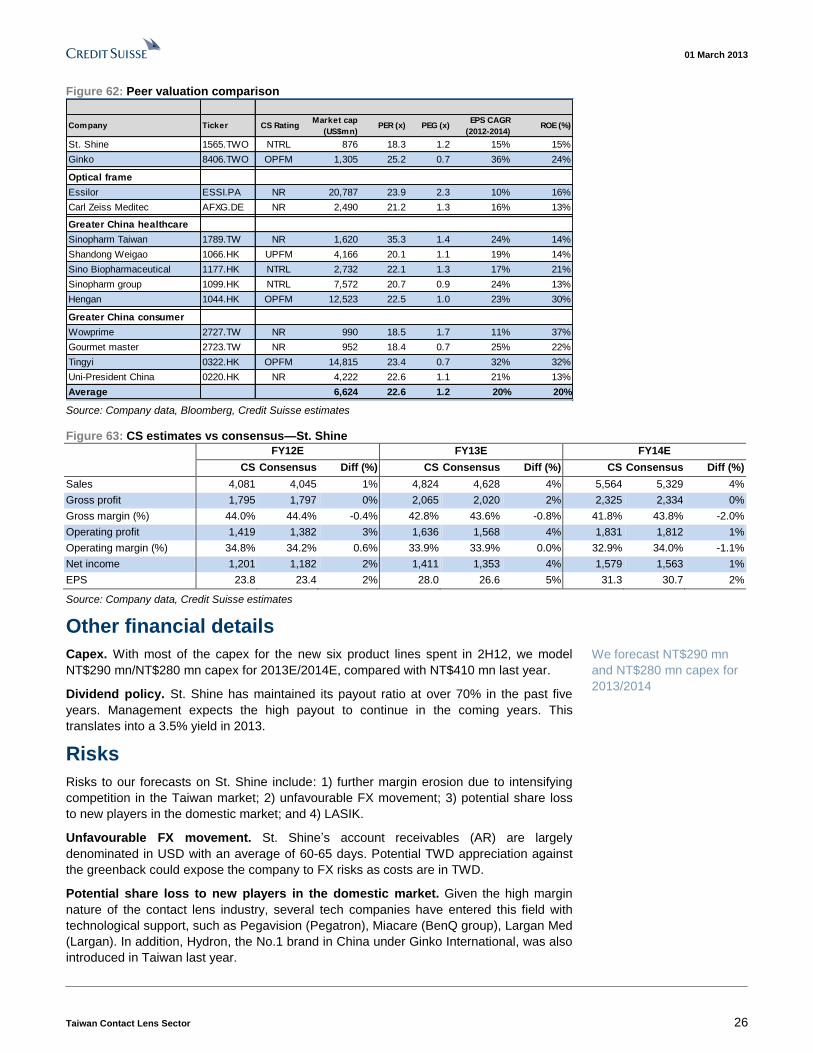

Figure 8: Sector valuation comparison

Company Ticker CS Rating Market cap

(US$mn)PER (x) PEG (x)

EPS CAGR

(2012-2014)ROE (%)

St. Shine 1565.TWO NTRL 876 18.3 1.2 15% 15%

Ginko 8406.TWO OPFM 1,305 25.2 0.7 36% 24%

Optical frame

Essilor ESSI.PA NR 20,787 23.9 2.3 10% 16%

Carl Zeiss Meditec AFXG.DE NR 2,490 21.2 1.3 16% 13%

Greater China healthcare

Sinopharm Taiwan 1789.TW NR 1,620 35.3 1.4 24% 14%

Shandong Weigao 1066.HK UPFM 4,166 20.1 1.1 19% 14%

Sino Biopharmaceutical 1177.HK NTRL 2,732 22.1 1.3 17% 21%

Sinopharm group 1099.HK NTRL 7,572 20.7 0.9 24% 13%

Hengan 1044.HK OPFM 12,523 22.5 1.0 23% 30%

Greater China consumer

Wowprime 2727.TW NR 990 18.5 1.7 11% 37%

Gourmet master 2723.TW NR 952 18.4 0.7 25% 22%

Tingyi 0322.HK OPFM 14,815 23.4 0.7 32% 32%

Uni-President China 0220.HK NR 4,222 22.6 1.1 21% 13%

Average 6,624 22.6 1.2 20% 20%

Source: Company data, Bloomberg, Credit Suisse estimates

Figure 9: P/E band - Ginko Figure 10: P/E band – St. Shine

200

250

300

350

400

450

500

550

600

Apr-

12

May-

12

May

-12

Jun-1

2

Jun-1

2

Jul-1

2

Jul-1

2

Aug-1

2

Aug-1

2

Sep-1

2

Sep-1

2

Sep-1

2

Oct

-12

Oct

-12

Nov-

12

Nov-

12

Dec-

12

Dec-

12

Jan-1

3

Jan-1

3

Feb-1

3

Feb-1

3

NT$

16 20 24 28 32 Share Price

Current Valuation: 25.2xHistorical Average

-

100

200

300

400

500

600

Apr-

04

Apr-

05

Apr-

06

Apr-

07

Apr-

08

Apr-

09

Apr-

10

Apr-

11

Apr-

12

NT$

12 14 16 18 20 Share Price

Current Valuation: 18.3x

Historical Average

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

01 March 2013

Taiwan Contact Lens Sector 5

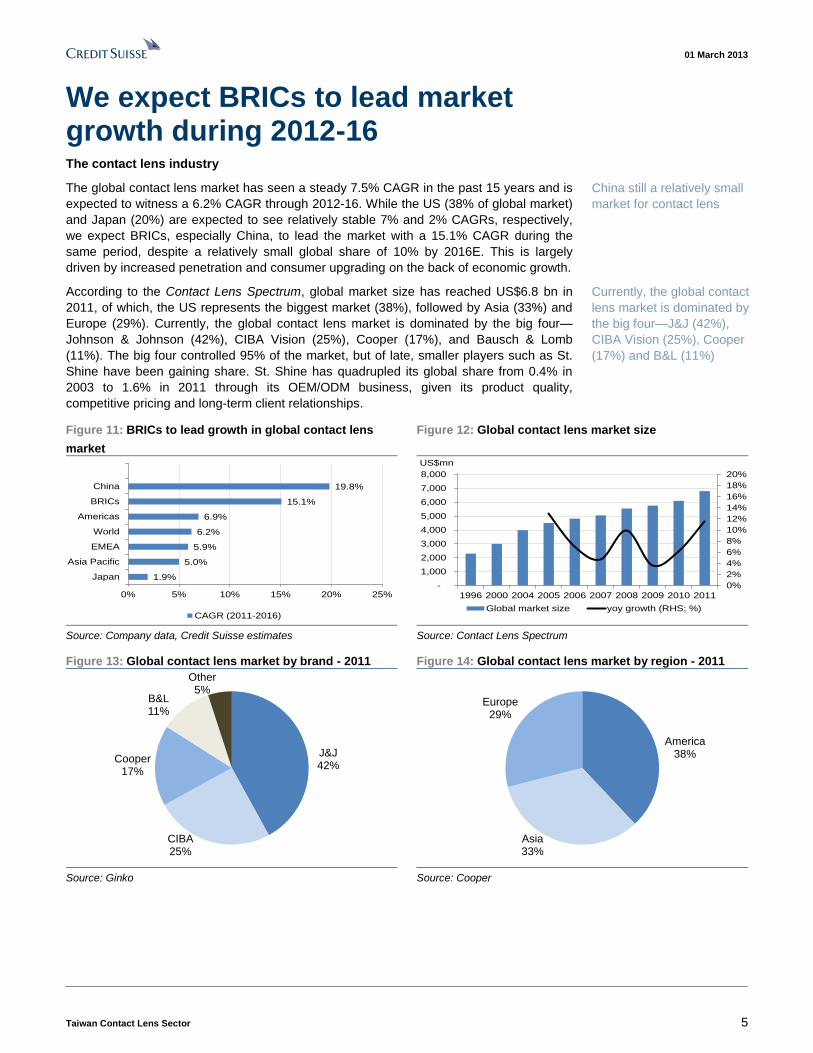

We expect BRICs to lead market growth during 2012-16 The contact lens industry

The global contact lens market has seen a steady 7.5% CAGR in the past 15 years and is

expected to witness a 6.2% CAGR through 2012-16. While the US (38% of global market)

and Japan (20%) are expected to see relatively stable 7% and 2% CAGRs, respectively,

we expect BRICs, especially China, to lead the market with a 15.1% CAGR during the

same period, despite a relatively small global share of 10% by 2016E. This is largely

driven by increased penetration and consumer upgrading on the back of economic growth.

According to the Contact Lens Spectrum, global market size has reached US$6.8 bn in

2011, of which, the US represents the biggest market (38%), followed by Asia (33%) and

Europe (29%). Currently, the global contact lens market is dominated by the big four—

Johnson & Johnson (42%), CIBA Vision (25%), Cooper (17%), and Bausch & Lomb

(11%). The big four controlled 95% of the market, but of late, smaller players such as St.

Shine have been gaining share. St. Shine has quadrupled its global share from 0.4% in

2003 to 1.6% in 2011 through its OEM/ODM business, given its product quality,

competitive pricing and long-term client relationships.

Figure 11: BRICs to lead growth in global contact lens

market

Figure 12: Global contact lens market size

1.9%

5.0%

5.9%

6.2%

6.9%

15.1%

19.8%

0% 5% 10% 15% 20% 25%

Japan

Asia Pacific

EMEA

World

Americas

BRICs

China

CAGR (2011-2016)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1996 2000 2004 2005 2006 2007 2008 2009 2010 2011

US$mn

Global market size yoy growth (RHS; %)

Source: Company data, Credit Suisse estimates Source: Contact Lens Spectrum

Figure 13: Global contact lens market by brand - 2011 Figure 14: Global contact lens market by region - 2011

J&J42%

CIBA25%

Cooper17%

B&L11%

Other5%

America38%

Asia33%

Europe29%

Source: Ginko Source: Cooper

China still a relatively small

market for contact lens

Currently, the global contact

lens market is dominated by

the big four—J&J (42%),

CIBA Vision (25%), Cooper

(17%) and B&L (11%)

01 March 2013

Taiwan Contact Lens Sector 6

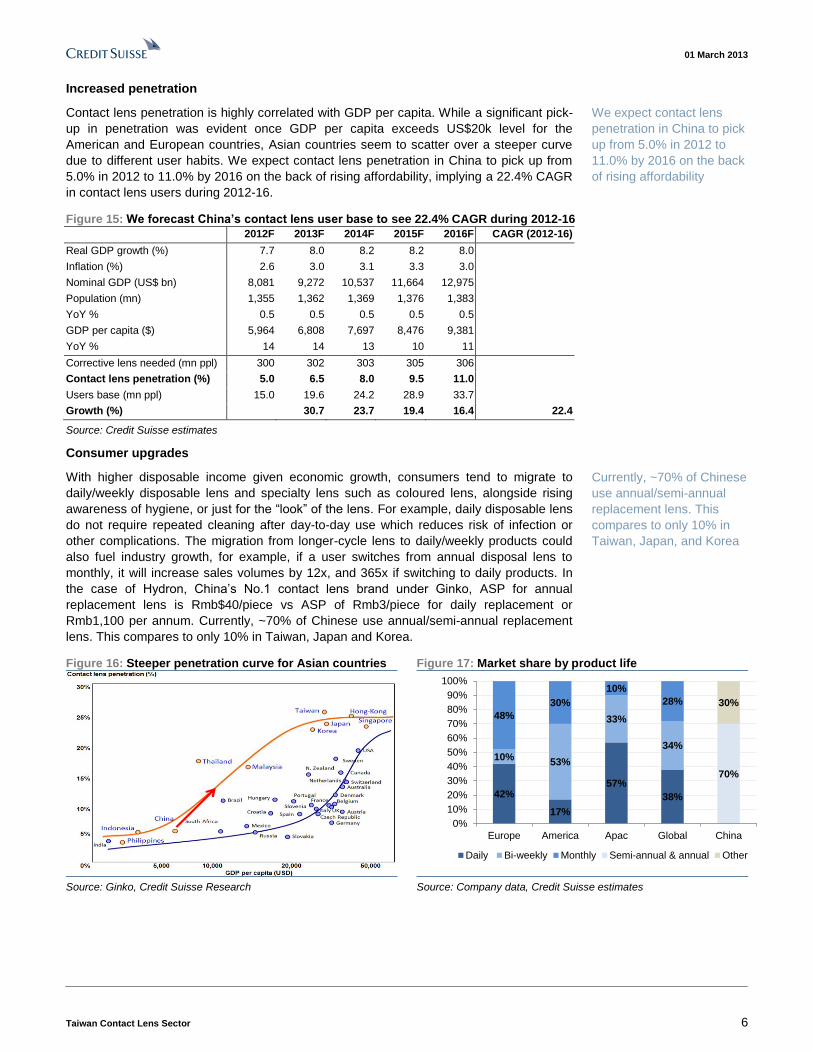

Increased penetration

Contact lens penetration is highly correlated with GDP per capita. While a significant pick-

up in penetration was evident once GDP per capita exceeds US$20k level for the

American and European countries, Asian countries seem to scatter over a steeper curve

due to different user habits. We expect contact lens penetration in China to pick up from

5.0% in 2012 to 11.0% by 2016 on the back of rising affordability, implying a 22.4% CAGR

in contact lens users during 2012-16.

Figure 15: We forecast China’s contact lens user base to see 22.4% CAGR during 2012-16

2012F 2013F 2014F 2015F 2016F CAGR (2012-16)

Real GDP growth (%) 7.7 8.0 8.2 8.2 8.0

Inflation (%) 2.6 3.0 3.1 3.3 3.0

Nominal GDP (US$ bn) 8,081 9,272 10,537 11,664 12,975

Population (mn) 1,355 1,362 1,369 1,376 1,383

YoY % 0.5 0.5 0.5 0.5 0.5

GDP per capita ($) 5,964 6,808 7,697 8,476 9,381

YoY % 14 14 13 10 11

Corrective lens needed (mn ppl) 300 302 303 305 306

Contact lens penetration (%) 5.0 6.5 8.0 9.5 11.0

Users base (mn ppl) 15.0 19.6 24.2 28.9 33.7

Growth (%) 30.7 23.7 19.4 16.4 22.4

Source: Credit Suisse estimates

Consumer upgrades

With higher disposable income given economic growth, consumers tend to migrate to

daily/weekly disposable lens and specialty lens such as coloured lens, alongside rising

awareness of hygiene, or just for the “look” of the lens. For example, daily disposable lens

do not require repeated cleaning after day-to-day use which reduces risk of infection or

other complications. The migration from longer-cycle lens to daily/weekly products could

also fuel industry growth, for example, if a user switches from annual disposal lens to

monthly, it will increase sales volumes by 12x, and 365x if switching to daily products. In

the case of Hydron, China’s No.1 contact lens brand under Ginko, ASP for annual

replacement lens is Rmb$40/piece vs ASP of Rmb3/piece for daily replacement or

Rmb1,100 per annum. Currently, ~70% of Chinese use annual/semi-annual replacement

lens. This compares to only 10% in Taiwan, Japan and Korea.

Figure 16: Steeper penetration curve for Asian countries Figure 17: Market share by product life

42%

17%

57%

38%

10%53%

33%

34%

48%

30%

10%

28%

70%

30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Europe America Apac Global China

Daily Bi-weekly Monthly Semi-annual & annual Other

Source: Ginko, Credit Suisse Research Source: Company data, Credit Suisse estimates

We expect contact lens

penetration in China to pick

up from 5.0% in 2012 to

11.0% by 2016 on the back

of rising affordability

Currently, ~70% of Chinese

use annual/semi-annual

replacement lens. This

compares to only 10% in

Taiwan, Japan, and Korea

01 March 2013

Taiwan Contact Lens Sector 7

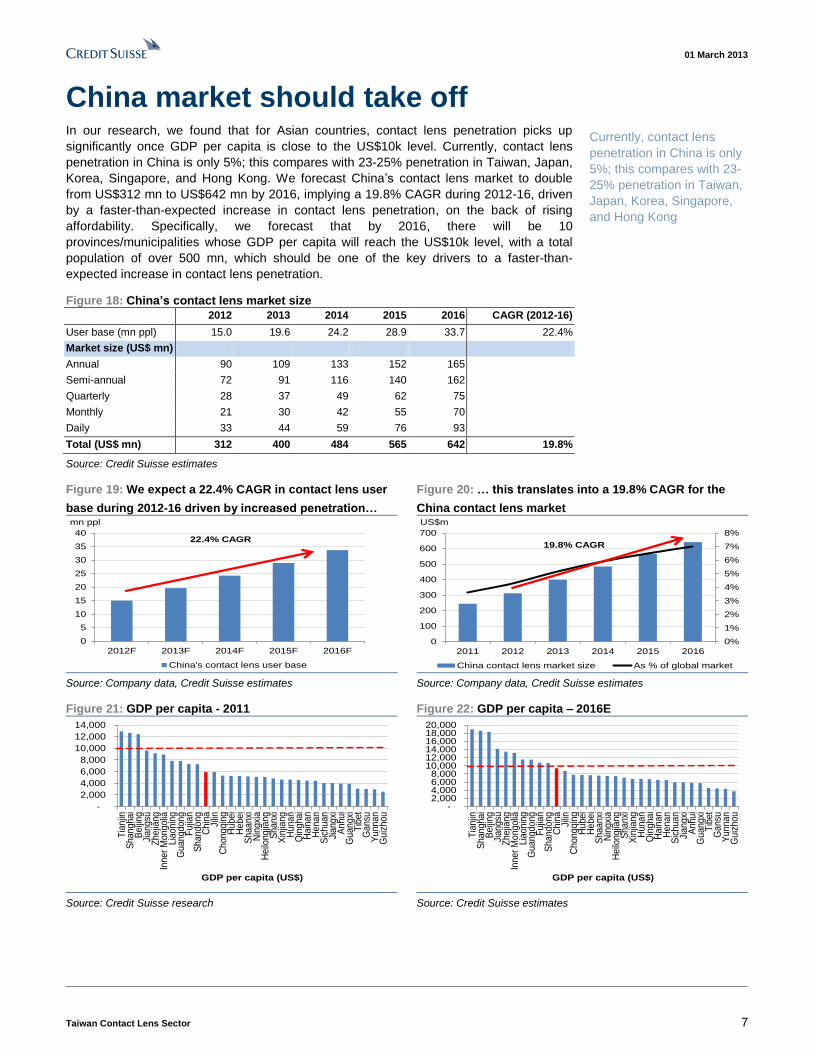

China market should take off In our research, we found that for Asian countries, contact lens penetration picks up

significantly once GDP per capita is close to the US$10k level. Currently, contact lens

penetration in China is only 5%; this compares with 23-25% penetration in Taiwan, Japan,

Korea, Singapore, and Hong Kong. We forecast China’s contact lens market to double

from US$312 mn to US$642 mn by 2016, implying a 19.8% CAGR during 2012-16, driven

by a faster-than-expected increase in contact lens penetration, on the back of rising

affordability. Specifically, we forecast that by 2016, there will be 10

provinces/municipalities whose GDP per capita will reach the US$10k level, with a total

population of over 500 mn, which should be one of the key drivers to a faster-than-

expected increase in contact lens penetration.

Figure 18: China’s contact lens market size

2012 2013 2014 2015 2016 CAGR (2012-16)

User base (mn ppl) 15.0 19.6 24.2 28.9 33.7 22.4%

Market size (US$ mn)

Annual 90 109 133 152 165

Semi-annual 72 91 116 140 162

Quarterly 28 37 49 62 75

Monthly 21 30 42 55 70

Daily 33 44 59 76 93

Total (US$ mn) 312 400 484 565 642 19.8%

Source: Credit Suisse estimates

Figure 19: We expect a 22.4% CAGR in contact lens user

base during 2012-16 driven by increased penetration…

Figure 20: … this translates into a 19.8% CAGR for the

China contact lens market

0

5

10

15

20

25

30

35

40

2012F 2013F 2014F 2015F 2016F

mn ppl

China's contact lens user base

22.4% CAGR

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015 2016

US$m

China contact lens market size As % of global market

19.8% CAGR

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 21: GDP per capita - 2011 Figure 22: GDP per capita – 2016E

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Tia

njin

Sh

an

gh

ai

Be

ijin

gJi

ang

suZ

hejia

ng

Inne

r M

ong

olia

Lia

on

ing

Gu

an

gd

on

gF

ujia

nS

han

do

ng

Ch

ina

Jilin

Ch

on

gq

ing

Hu

be

iH

ebe

iS

haa

nxi

Nin

gxi

aH

eilo

ng

jiang

Sh

an

xiX

injia

ng

Hu

na

nQ

ingh

ai

Ha

ina

nH

ena

nS

ich

ua

nJi

ang

xiA

nhu

iG

uan

gxi

Tib

et

Ga

nsu

Yu

nn

an

Gu

izh

ou

GDP per capita (US$)

- 2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,000 20,000

Tia

njin

Sh

an

gh

ai

Be

ijin

gJi

an

gsu

Zhe

jiang

Inne

r M

ong

olia

Lia

on

ing

Gu

an

gd

on

gF

ujia

nS

han

do

ng

Ch

ina

Jilin

Ch

on

gq

ing

Hu

be

iH

ebe

iS

haa

nxi

Nin

gxi

aH

eilo

ngjia

ng

Sh

an

xiX

injia

ng

Hu

na

nQ

ing

ha

iH

ain

an

He

na

nS

ich

ua

nJi

ang

xiA

nh

ui

Gu

an

gxi

Tib

et

Ga

nsu

Yu

nn

an

Gu

izh

ou

GDP per capita (US$)

Source: Credit Suisse research Source: Credit Suisse estimates

Currently, contact lens

penetration in China is only

5%; this compares with 23-

25% penetration in Taiwan,

Japan, Korea, Singapore,

and Hong Kong

01 March 2013

Taiwan Contact Lens Sector 8

Multiple entry barriers should continue to defend high margins The global contact lens market is oligopolistic where brand vendors enjoy at least 60%

gross margin; even ODM/OEM such as St. Shine earn >40% gross margin. These are the

sort of high margins that come from the defensive wall of multiple barriers to entry,

including:

(1) Increased difficulty in getting product licenses. Contact lens sit right on the

cornea, and, thus are classed as a “medical device”. As such, governments have

established stringent licensing standards for contact lens manufacturing and

distribution. For each product, vendors/OEM are required to submit clinical data and

get approvals from local regulators such as CE Certification (Europe), FDA inspection

(US), GMP (Taiwan), and SFDA (China). The approval process generally takes one to

two years from filing to the official product launch.

(2) Skyrocketing advertising costs create another entry barrier for new comers.

New comers to the market have to spend a lot more on advertising and promotions to

lure customers to switch from market leaders who have built strong brand loyalty with

proven product quality for decades. In particular, advertising per second on Chinese

TV costs 5x more now than in 2005, according to Ginko.

(3) Distribution channels dominated by multinational brands. From a retail channel

perspective, vendors will not replace bestselling brands with a new brand on their

shelves, given the cash conversion cycle for the latter will likely be longer.

Figure 23: Gross margin breakdown – own brand vs OEM

strategy

Figure 24: Cost structure comparison – Ginko adopts a

labour-light model

60%

20%

10%

40%

10%

10%

5%

3%

15%27%

0%

20%

40%

60%

80%

100%

Ginko St. Shine

Packaging materials Labor Depreciation Raw material Other

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 25: Product mix comparison – Ginko still has more

exposure to long-cycled lens products

Figure 26: Capacity comparison – St. Shine is running at a

larger scale

-

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011 2012 2013F 2014F

mn pieces/yr

Ginko St. Shine Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

We expect high margins to

continue behind the

protection of multiple

barriers to entry

Product approval generally

takes one to two years from

filing to official product

launch

Advertising per second on

Chinese TV costs 5x more

today than in 2005

01 March 2013

Taiwan Contact Lens Sector 9

Stock calls

We initiate coverage on Ginko with an OUTPERFORM rating. With strong EPS CAGR of

36% over 2012-2014, we set our target price of NT$540 (upside potential of 29%) based

on 0.9x 2013E PEG, given: 1) biggest sales channel in China; 2) full product offering at

competitive price points; 3) strong brand recognition ; and 4) a dedicated and experienced

management team. Our forecast 2013/2014 EPS are 9%/17% higher than consensus’ due

to higher sales growth assumptions.

We also initiate coverage on St. Shine with a NEUTRAL rating. We forecast a 15% EPS

CAGR during 2012-14 for St. Shine, compared with its peer group average of 20% CAGR.

We set our target price of NT$504 (flat with trading price) based on 18x 2013E EPS due to

the longer-term concern that ~80% of its revenue comes from the relatively saturated

Japanese (2% CAGR during 2008-2012) and Taiwanese markets, evidenced by

decelerating sales from a 27% CAGR during 2005-2010 to 10% in 2011 and -6% in 2012.

Risk

Risks to our forecasts include failure to ramp up capacity, slower-than-expected

penetration and user migration to substitutes of contact lens such as LASIK or silicone

hydrogel.

LASIK (Laser-Assisted in Situ Keratomileusis) is a type of refractive surgery for the

correction of myopia, providing a permanent alternative to eyeglasses or contact lenses.

Major side effects include halos, starbursts, night-driving problems, keratoconus (corneal

ectasia) and eye dryness. In addition, the patient’s eyesight could deteriorate and become

myopic again. Cost of LASIK surgery ranges from Rmb5-15,000 in China.

Silicone hydrogel contact lens is an advanced type of soft lens that allows 5x more

oxygen to pass through the lens to the cornea than the regular soft lenses, designed for

extended wear with improved comfort. According to Contact Lens Spectrum, silicone

hydrogel contact lens already took up 43% of the global market and 67% in the US given

user habit, insurance coverage and clinical recommendation, compared with less than

10% penetration in Asian countries. Price point for the silicone hydrogel lens is 2x the

ordinary hydrogel lens.

There are side effects

associated with LASIK

Price point for silicone

hydrogel lens is 2x the

ordinary hydrogel lens

01 March 2013

Taiwan Contact Lens Sector 10

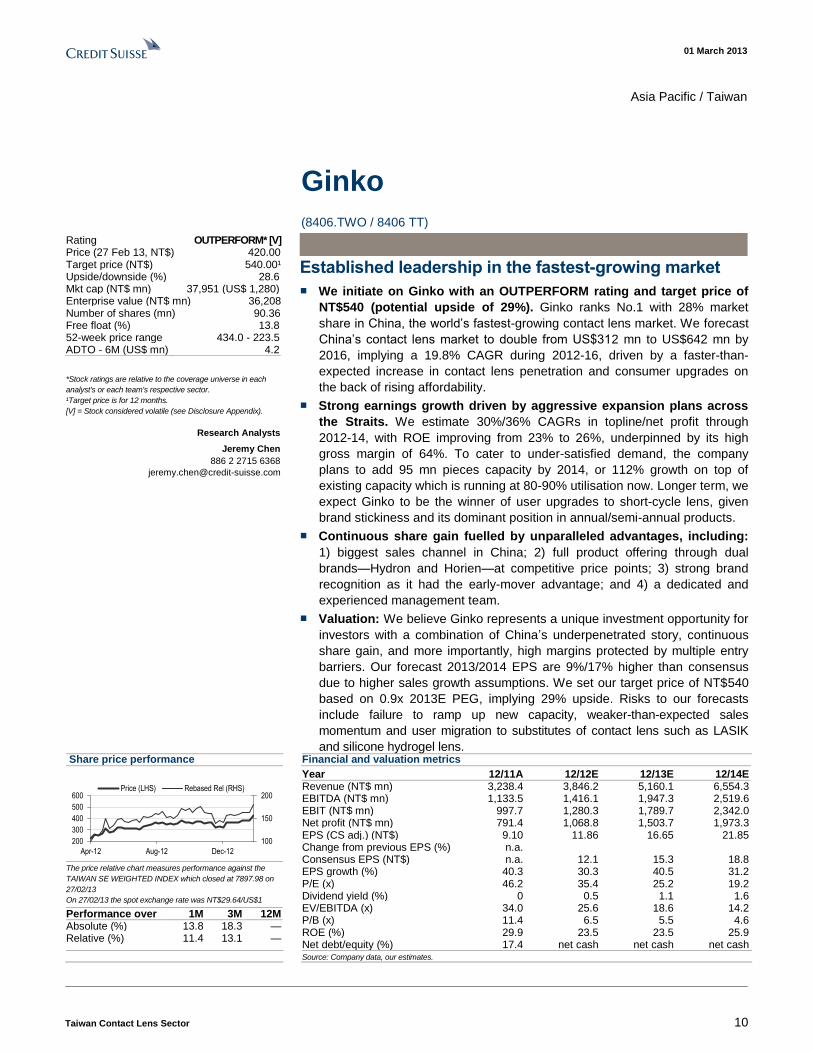

Asia Pacific / Taiwan

Ginko

(8406.TWO / 8406 TT)

Established leadership in the fastest-growing market

■ We initiate on Ginko with an OUTPERFORM rating and target price of

NT$540 (potential upside of 29%). Ginko ranks No.1 with 28% market

share in China, the world’s fastest-growing contact lens market. We forecast

China’s contact lens market to double from US$312 mn to US$642 mn by

2016, implying a 19.8% CAGR during 2012-16, driven by a faster-than-

expected increase in contact lens penetration and consumer upgrades on

the back of rising affordability.

■ Strong earnings growth driven by aggressive expansion plans across

the Straits. We estimate 30%/36% CAGRs in topline/net profit through

2012-14, with ROE improving from 23% to 26%, underpinned by its high

gross margin of 64%. To cater to under-satisfied demand, the company

plans to add 95 mn pieces capacity by 2014, or 112% growth on top of

existing capacity which is running at 80-90% utilisation now. Longer term, we

expect Ginko to be the winner of user upgrades to short-cycle lens, given

brand stickiness and its dominant position in annual/semi-annual products.

■ Continuous share gain fuelled by unparalleled advantages, including:

1) biggest sales channel in China; 2) full product offering through dual

brands—Hydron and Horien—at competitive price points; 3) strong brand

recognition as it had the early-mover advantage; and 4) a dedicated and

experienced management team.

■ Valuation: We believe Ginko represents a unique investment opportunity for

investors with a combination of China’s underpenetrated story, continuous

share gain, and more importantly, high margins protected by multiple entry

barriers. Our forecast 2013/2014 EPS are 9%/17% higher than consensus

due to higher sales growth assumptions. We set our target price of NT$540

based on 0.9x 2013E PEG, implying 29% upside. Risks to our forecasts

include failure to ramp up new capacity, weaker-than-expected sales

momentum and user migration to substitutes of contact lens such as LASIK

and silicone hydrogel lens. Share price performance

100

150

200

200

300

400

500

600

Apr-12 Aug-12 Dec-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

TAIWAN SE WEIGHTED INDEX which closed at 7897.98 on

27/02/13

On 27/02/13 the spot exchange rate was NT$29.64/US$1

Performance over 1M 3M 12M Absolute (%) 13.8 18.3 — Relative (%) 11.4 13.1 —

Financial and valuation metrics

Year 12/11A 12/12E 12/13E 12/14E Revenue (NT$ mn) 3,238.4 3,846.2 5,160.1 6,554.3 EBITDA (NT$ mn) 1,133.5 1,416.1 1,947.3 2,519.6 EBIT (NT$ mn) 997.7 1,280.3 1,789.7 2,342.0 Net profit (NT$ mn) 791.4 1,068.8 1,503.7 1,973.3 EPS (CS adj.) (NT$) 9.10 11.86 16.65 21.85 Change from previous EPS (%) n.a. Consensus EPS (NT$) n.a. 12.1 15.3 18.8 EPS growth (%) 40.3 30.3 40.5 31.2 P/E (x) 46.2 35.4 25.2 19.2 Dividend yield (%) 0 0.5 1.1 1.6 EV/EBITDA (x) 34.0 25.6 18.6 14.2 P/B (x) 11.4 6.5 5.5 4.6 ROE (%) 29.9 23.5 23.5 25.9 Net debt/equity (%) 17.4 net cash net cash net cash

Source: Company data, our estimates.

Rating OUTPERFORM* [V] Price (27 Feb 13, NT$) 420.00 Target price (NT$) 540.00¹ Upside/downside (%) 28.6 Mkt cap (NT$ mn) 37,951 (US$ 1,280) Enterprise value (NT$ mn) 36,208 Number of shares (mn) 90.36 Free float (%) 13.8 52-week price range 434.0 - 223.5 ADTO - 6M (US$ mn) 4.2

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

[V] = Stock considered volatile (see Disclosure Appendix).

Research Analysts

Jeremy Chen

886 2 2715 6368

01 March 2013

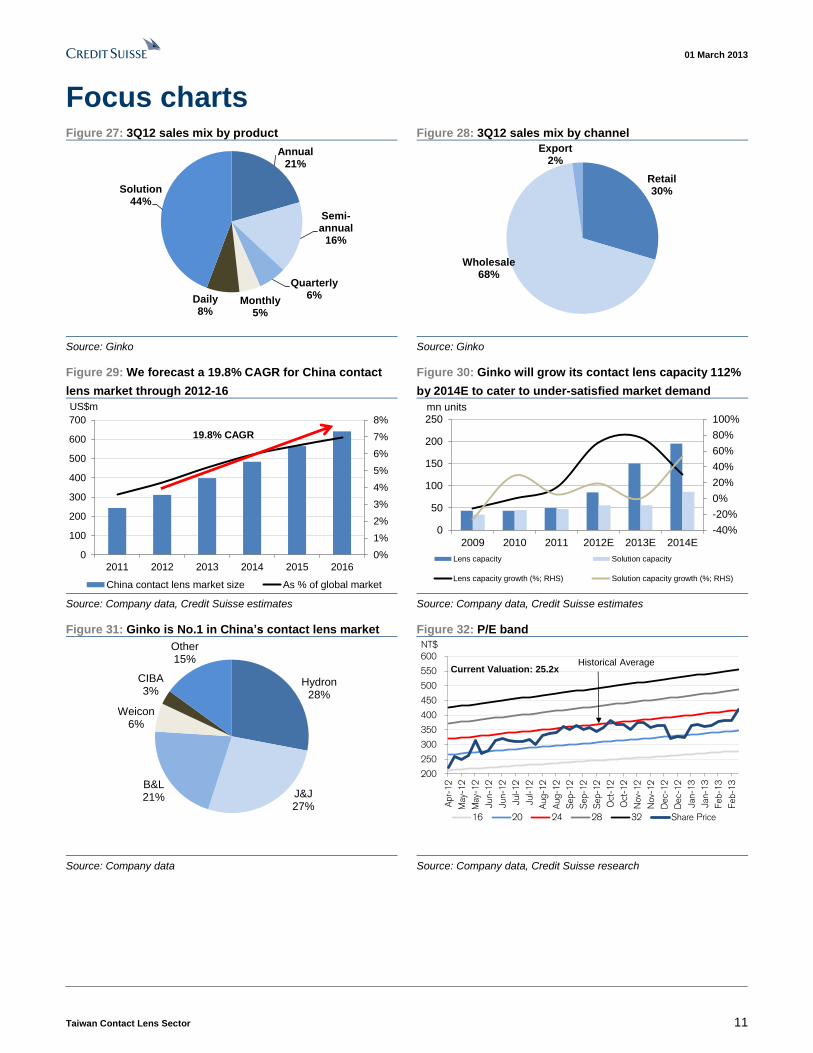

Taiwan Contact Lens Sector 11

Focus charts Figure 27: 3Q12 sales mix by product Figure 28: 3Q12 sales mix by channel

Annual 21%

Semi-annual

16%

Quarterly6%

Monthly5%

Daily8%

Solution44%

Retail30%

Wholesale68%

Export2%

Source: Ginko Source: Ginko

Figure 29: We forecast a 19.8% CAGR for China contact

lens market through 2012-16

Figure 30: Ginko will grow its contact lens capacity 112%

by 2014E to cater to under-satisfied market demand

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015 2016

US$m

China contact lens market size As % of global market

19.8% CAGR

-40%

-20%

0%

20%

40%

60%

80%

100%

0

50

100

150

200

250

2009 2010 2011 2012E 2013E 2014E

mn units

Lens capacity Solution capacity

Lens capacity growth (%; RHS) Solution capacity growth (%; RHS)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 31: Ginko is No.1 in China’s contact lens market Figure 32: P/E band

Hydron28%

J&J27%

B&L21%

Weicon6%

CIBA3%

Other15%

200

250

300

350

400

450

500

550

600

Apr-

12

May-

12

May-

12

Jun-1

2

Jun-1

2

Jul-1

2

Jul-1

2

Aug-1

2

Aug-1

2

Sep-1

2

Sep-1

2

Sep-1

2

Oct

-12

Oct

-12

Nov-

12

Nov-

12

Dec-

12

Dec-

12

Jan-1

3

Jan-1

3

Feb-1

3

Feb-1

3

NT$

16 20 24 28 32 Share Price

Current Valuation: 25.2xHistorical Average

Source: Company data Source: Company data, Credit Suisse research

01 March 2013

Taiwan Contact Lens Sector 12

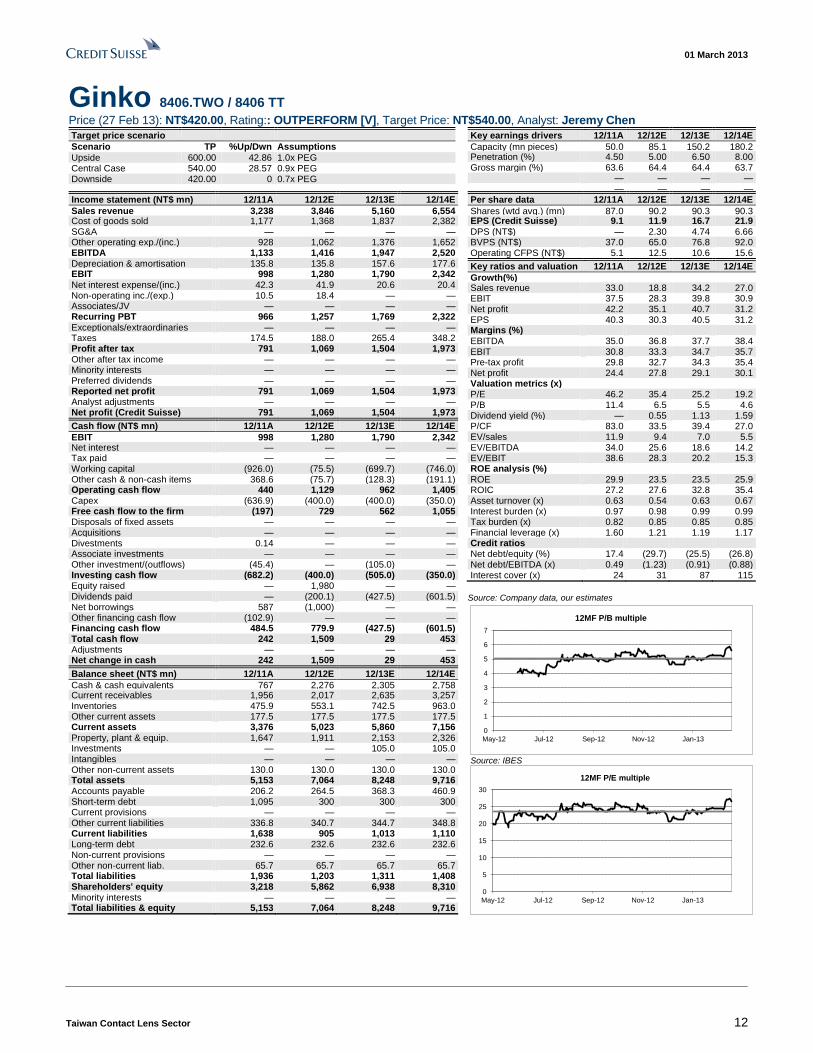

Ginko 8406.TWO / 8406 TT Price (27 Feb 13): NT$420.00, Rating:: OUTPERFORM [V], Target Price: NT$540.00, Analyst: Jeremy Chen

Target price scenario

Scenario TP %Up/Dwn Assumptions

Upside 600.00 42.86 1.0x PEG Central Case 540.00 28.57 0.9x PEG Downside 420.00 0 0.7x PEG

Key earnings drivers 12/11A 12/12E 12/13E 12/14E

Capacity (mn pieces) 50.0 85.1 150.2 180.2 Penetration (%) 4.50 5.00 6.50 8.00 Gross margin (%) 63.6 64.4 64.4 63.7 — — — — — — — —

Income statement (NT$ mn) 12/11A 12/12E 12/13E 12/14E

Sales revenue 3,238 3,846 5,160 6,554 Cost of goods sold 1,177 1,368 1,837 2,382 SG&A — — — — Other operating exp./(inc.) 928 1,062 1,376 1,652 EBITDA 1,133 1,416 1,947 2,520 Depreciation & amortisation 135.8 135.8 157.6 177.6 EBIT 998 1,280 1,790 2,342 Net interest expense/(inc.) 42.3 41.9 20.6 20.4 Non-operating inc./(exp.) 10.5 18.4 — — Associates/JV — — — — Recurring PBT 966 1,257 1,769 2,322 Exceptionals/extraordinaries — — — — Taxes 174.5 188.0 265.4 348.2 Profit after tax 791 1,069 1,504 1,973 Other after tax income — — — — Minority interests — — — — Preferred dividends — — — — Reported net profit 791 1,069 1,504 1,973 Analyst adjustments — — — — Net profit (Credit Suisse) 791 1,069 1,504 1,973

Cash flow (NT$ mn) 12/11A 12/12E 12/13E 12/14E

EBIT 998 1,280 1,790 2,342 Net interest — — — — Tax paid — — — — Working capital (926.0) (75.5) (699.7) (746.0) Other cash & non-cash items 368.6 (75.7) (128.3) (191.1) Operating cash flow 440 1,129 962 1,405 Capex (636.9) (400.0) (400.0) (350.0) Free cash flow to the firm (197) 729 562 1,055 Disposals of fixed assets — — — — Acquisitions — — — — Divestments 0.14 — — — Associate investments — — — — Other investment/(outflows) (45.4) — (105.0) — Investing cash flow (682.2) (400.0) (505.0) (350.0) Equity raised — 1,980 — — Dividends paid — (200.1) (427.5) (601.5) Net borrowings 587 (1,000) — — Other financing cash flow (102.9) — — — Financing cash flow 484.5 779.9 (427.5) (601.5) Total cash flow 242 1,509 29 453 Adjustments — — — — Net change in cash 242 1,509 29 453

Balance sheet (NT$ mn) 12/11A 12/12E 12/13E 12/14E

Cash & cash equivalents 767 2,276 2,305 2,758 Current receivables 1,956 2,017 2,635 3,257 Inventories 475.9 553.1 742.5 963.0 Other current assets 177.5 177.5 177.5 177.5 Current assets 3,376 5,023 5,860 7,156 Property, plant & equip. 1,647 1,911 2,153 2,326 Investments — — 105.0 105.0 Intangibles — — — — Other non-current assets 130.0 130.0 130.0 130.0 Total assets 5,153 7,064 8,248 9,716 Accounts payable 206.2 264.5 368.3 460.9 Short-term debt 1,095 300 300 300 Current provisions — — — — Other current liabilities 336.8 340.7 344.7 348.8 Current liabilities 1,638 905 1,013 1,110 Long-term debt 232.6 232.6 232.6 232.6 Non-current provisions — — — — Other non-current liab. 65.7 65.7 65.7 65.7 Total liabilities 1,936 1,203 1,311 1,408 Shareholders' equity 3,218 5,862 6,938 8,310 Minority interests — — — — Total liabilities & equity 5,153 7,064 8,248 9,716

Per share data 12/11A 12/12E 12/13E 12/14E

Shares (wtd avg.) (mn) 87.0 90.2 90.3 90.3 EPS (Credit Suisse) (NT$)

9.1 11.9 16.7 21.9 DPS (NT$) — 2.30 4.74 6.66 BVPS (NT$) 37.0 65.0 76.8 92.0 Operating CFPS (NT$) 5.1 12.5 10.6 15.6

Key ratios and valuation 12/11A 12/12E 12/13E 12/14E

Growth(%) Sales revenue 33.0 18.8 34.2 27.0 EBIT 37.5 28.3 39.8 30.9 Net profit 42.2 35.1 40.7 31.2 EPS 40.3 30.3 40.5 31.2 Margins (%) EBITDA 35.0 36.8 37.7 38.4 EBIT 30.8 33.3 34.7 35.7 Pre-tax profit 29.8 32.7 34.3 35.4 Net profit 24.4 27.8 29.1 30.1 Valuation metrics (x) P/E 46.2 35.4 25.2 19.2 P/B 11.4 6.5 5.5 4.6 Dividend yield (%) — 0.55 1.13 1.59 P/CF 83.0 33.5 39.4 27.0 EV/sales 11.9 9.4 7.0 5.5 EV/EBITDA 34.0 25.6 18.6 14.2 EV/EBIT 38.6 28.3 20.2 15.3 ROE analysis (%) ROE 29.9 23.5 23.5 25.9 ROIC 27.2 27.6 32.8 35.4 Asset turnover (x) 0.63 0.54 0.63 0.67 Interest burden (x) 0.97 0.98 0.99 0.99 Tax burden (x) 0.82 0.85 0.85 0.85 Financial leverage (x) 1.60 1.21 1.19 1.17 Credit ratios Net debt/equity (%) 17.4 (29.7) (25.5) (26.8) Net debt/EBITDA (x) 0.49 (1.23) (0.91) (0.88) Interest cover (x) 24 31 87 115

Source: Company data, our estimates

0

1

2

3

4

5

6

7

May-12 Jul-12 Sep-12 Nov-12 Jan-13

12MF P/B multiple

Source: IBES

0

5

10

15

20

25

30

May-12 Jul-12 Sep-12 Nov-12 Jan-13

12MF P/E multiple

01 March 2013

Taiwan Contact Lens Sector 13

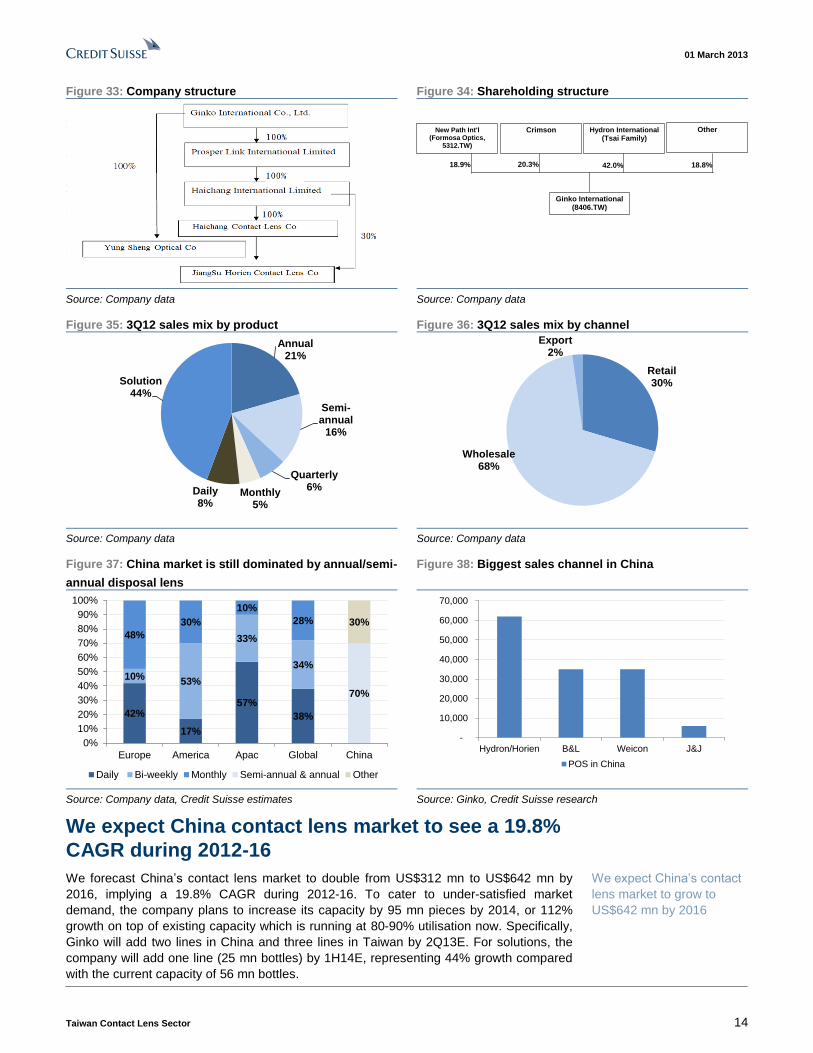

Established leadership in the fastest-growing market Company description

Hydron was first introduced in China in 1985 by Allergan, an US-based multi-specialty

health care company. In 1995, the Tsai family acquired Hydron’s facilities, formed a

company and later renamed it as Haichang Contact Lens in 1997. The holding company,

Ginko International (the listed entity), was founded in 2007, owning 100% in Haichang

Contact Lens and Jiangsu Horien Contact Lens, which run major operations in China.

Ginko acquired Yung Sheng Optical in 2010 and relocated the plant to Central Taiwan

Science Park, paving way for launching high-end made-in-Taiwan contact lens.

The founder of Ginko, Mr Tsai Kuo Chou has been engaged with the optical industry

across the Straits for more than 30 years. Tsai was once the biggest supplier to Formosa

Optical (5312.TW) owned by the Wang family. In 2001, Mr. Tsai lent NT$200m to bridge

the Wang family’s fleeting cash crunch and took over ownership of the company. Notably,

the Wang family still owns China Bao Dao Optical (unlisted), the biggest contact lens retail

chain in China with over 1,200 point-of-sales (POS) in 80 cities across the country. Ginko’s

products could easily penetrate into each China Bao Dao store owing to Mr Tsai’s strong

relationship with the Wang family. Formosa Optical is also Taiwan’s No.1 optical frame

retailer with 20% market share through multiple brands. We believe Tsai’s expertise in the

industry and extensive channel coverage provides Ginko an essentially uncontested

advantages over peers.

Based in Jiangsu, Ginko manufactures and distributes its own brand Hydron (mid-to-high

end) and Horien (mid-to-low end) across China through its extensive distribution network.

With 62,000 POS in the country, the company holds No.1 market share in both contact

lens (28%) and lens solution (41%) markets, and is gaining share from multi-national

brands such as J&J and CIBA vision. In 3Q12, contact lens and solution accounted for

56% and 44% of total sales, respectively. In particular, longer-cycled products such as

annual/semi-annual disposable lens represented two-thirds of Ginko’s contact lens sales,

as China market is dominated by annual/semi-annual disposal lens with a 70% share,

according to management. The company runs two production lines in Taiwan and four in

China with total capacity of 85.1 mn pieces, as at end-2012. Most of Ginko’s capacity are

mold-casting, a manufacturing method injecting monomer plastic into a mold, which is

designed for short-cycled disposable products. Ginko also sells the cleaning solution for

the lenses with gross margins as high as 65%. However, solution sales are expected to

fall in weighting as management expects disposable contact lens sales to outgrow

annual/semi-annual lens in the coming years. The company’s capacity for solution is 56

mn bottles, as of end-2012.

Ginko holds No.1 market

share in both contact lens

(28%) and solution (41%)

markets

Tsai family acquired

Hydron’s China assets in

1995

Leveraging on China’s

biggest contact lens

channel, China Bao Dao

Optical with over 1,200

point-of-sales

01 March 2013

Taiwan Contact Lens Sector 14

Figure 33: Company structure Figure 34: Shareholding structure

New Path Int'l(Formosa Optics,

5312.TW)

Crimson Hydron International

(Tsai Family)Other

Ginko International(8406.TW)

18.9% 20.3% 42.0% 18.8%

Source: Company data Source: Company data

Figure 35: 3Q12 sales mix by product Figure 36: 3Q12 sales mix by channel

Annual 21%

Semi-annual

16%

Quarterly6%

Monthly5%

Daily8%

Solution44%

Retail30%

Wholesale68%

Export2%

Source: Company data Source: Company data

Figure 37: China market is still dominated by annual/semi-

annual disposal lens

Figure 38: Biggest sales channel in China

42%

17%

57%

38%

10%53%

33%

34%

48%

30%

10%

28%

70%

30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Europe America Apac Global China

Daily Bi-weekly Monthly Semi-annual & annual Other

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Hydron/Horien B&L Weicon J&J

POS in China

Source: Company data, Credit Suisse estimates Source: Ginko, Credit Suisse research

We expect China contact lens market to see a 19.8%

CAGR during 2012-16

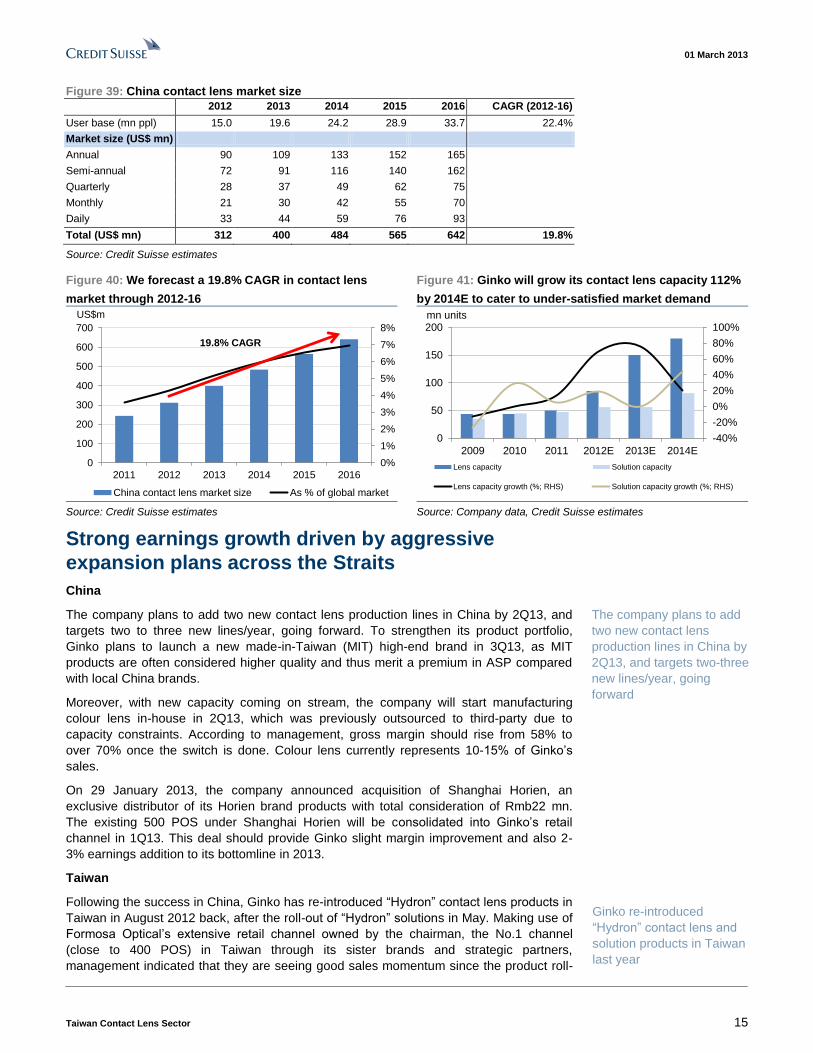

We forecast China’s contact lens market to double from US$312 mn to US$642 mn by

2016, implying a 19.8% CAGR during 2012-16. To cater to under-satisfied market

demand, the company plans to increase its capacity by 95 mn pieces by 2014, or 112%

growth on top of existing capacity which is running at 80-90% utilisation now. Specifically,

Ginko will add two lines in China and three lines in Taiwan by 2Q13E. For solutions, the

company will add one line (25 mn bottles) by 1H14E, representing 44% growth compared

with the current capacity of 56 mn bottles.

We expect China’s contact

lens market to grow to

US$642 mn by 2016

01 March 2013

Taiwan Contact Lens Sector 15

Figure 39: China contact lens market size

2012 2013 2014 2015 2016 CAGR (2012-16)

User base (mn ppl) 15.0 19.6 24.2 28.9 33.7 22.4%

Market size (US$ mn)

Annual 90 109 133 152 165

Semi-annual 72 91 116 140 162

Quarterly 28 37 49 62 75

Monthly 21 30 42 55 70

Daily 33 44 59 76 93

Total (US$ mn) 312 400 484 565 642 19.8%

Source: Credit Suisse estimates

Figure 40: We forecast a 19.8% CAGR in contact lens

market through 2012-16

Figure 41: Ginko will grow its contact lens capacity 112%

by 2014E to cater to under-satisfied market demand

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015 2016

US$m

China contact lens market size As % of global market

19.8% CAGR

-40%

-20%

0%

20%

40%

60%

80%

100%

0

50

100

150

200

2009 2010 2011 2012E 2013E 2014E

mn units

Lens capacity Solution capacity

Lens capacity growth (%; RHS) Solution capacity growth (%; RHS)

Source: Credit Suisse estimates Source: Company data, Credit Suisse estimates

Strong earnings growth driven by aggressive

expansion plans across the Straits

China

The company plans to add two new contact lens production lines in China by 2Q13, and

targets two to three new lines/year, going forward. To strengthen its product portfolio,

Ginko plans to launch a new made-in-Taiwan (MIT) high-end brand in 3Q13, as MIT

products are often considered higher quality and thus merit a premium in ASP compared

with local China brands.

Moreover, with new capacity coming on stream, the company will start manufacturing

colour lens in-house in 2Q13, which was previously outsourced to third-party due to

capacity constraints. According to management, gross margin should rise from 58% to

over 70% once the switch is done. Colour lens currently represents 10-15% of Ginko’s

sales.

On 29 January 2013, the company announced acquisition of Shanghai Horien, an

exclusive distributor of its Horien brand products with total consideration of Rmb22 mn.

The existing 500 POS under Shanghai Horien will be consolidated into Ginko’s retail

channel in 1Q13. This deal should provide Ginko slight margin improvement and also 2-

3% earnings addition to its bottomline in 2013.

Taiwan

Following the success in China, Ginko has re-introduced “Hydron” contact lens products in

Taiwan in August 2012 back, after the roll-out of “Hydron” solutions in May. Making use of

Formosa Optical’s extensive retail channel owned by the chairman, the No.1 channel

(close to 400 POS) in Taiwan through its sister brands and strategic partners,

management indicated that they are seeing good sales momentum since the product roll-

The company plans to add

two new contact lens

production lines in China by

2Q13, and targets two-three

new lines/year, going

forward

Ginko re-introduced

“Hydron” contact lens and

solution products in Taiwan

last year

01 March 2013

Taiwan Contact Lens Sector 16

out and expect 5% sales contribution this year with bi-weekly and colour lens to be

launched in 1Q13. Management also expects the launch of Hydron products in Taiwan to

help build the brand image for its upcoming new MIT premium brand in China this year.

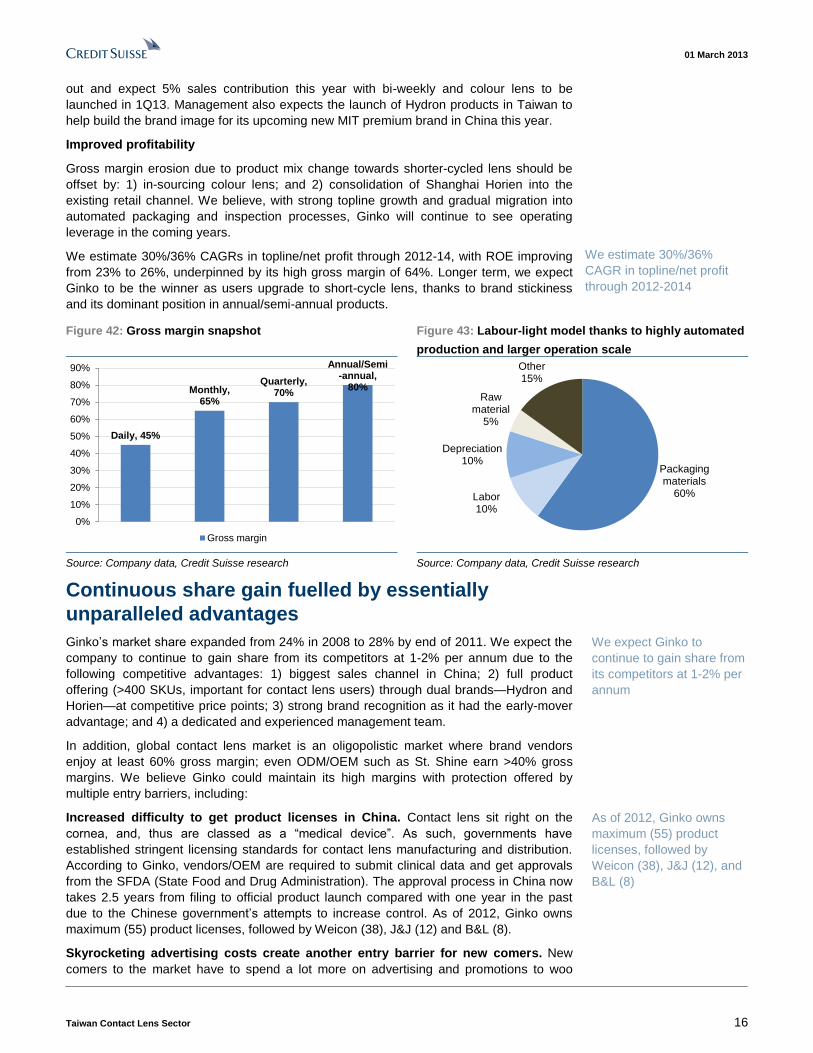

Improved profitability

Gross margin erosion due to product mix change towards shorter-cycled lens should be

offset by: 1) in-sourcing colour lens; and 2) consolidation of Shanghai Horien into the

existing retail channel. We believe, with strong topline growth and gradual migration into

automated packaging and inspection processes, Ginko will continue to see operating

leverage in the coming years.

We estimate 30%/36% CAGRs in topline/net profit through 2012-14, with ROE improving

from 23% to 26%, underpinned by its high gross margin of 64%. Longer term, we expect

Ginko to be the winner as users upgrade to short-cycle lens, thanks to brand stickiness

and its dominant position in annual/semi-annual products.

Figure 42: Gross margin snapshot Figure 43: Labour-light model thanks to highly automated

production and larger operation scale

Daily, 45%

Monthly, 65%

Quarterly, 70%

Annual/Semi-annual,

80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Gross margin

Packaging materials

60%Labor10%

Depreciation10%

Raw material

5%

Other15%

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

Continuous share gain fuelled by essentially

unparalleled advantages

Ginko’s market share expanded from 24% in 2008 to 28% by end of 2011. We expect the

company to continue to gain share from its competitors at 1-2% per annum due to the

following competitive advantages: 1) biggest sales channel in China; 2) full product

offering (>400 SKUs, important for contact lens users) through dual brands—Hydron and

Horien—at competitive price points; 3) strong brand recognition as it had the early-mover

advantage; and 4) a dedicated and experienced management team.

In addition, global contact lens market is an oligopolistic market where brand vendors

enjoy at least 60% gross margin; even ODM/OEM such as St. Shine earn >40% gross

margins. We believe Ginko could maintain its high margins with protection offered by

multiple entry barriers, including:

Increased difficulty to get product licenses in China. Contact lens sit right on the

cornea, and, thus are classed as a “medical device”. As such, governments have

established stringent licensing standards for contact lens manufacturing and distribution.

According to Ginko, vendors/OEM are required to submit clinical data and get approvals

from the SFDA (State Food and Drug Administration). The approval process in China now

takes 2.5 years from filing to official product launch compared with one year in the past

due to the Chinese government’s attempts to increase control. As of 2012, Ginko owns

maximum (55) product licenses, followed by Weicon (38), J&J (12) and B&L (8).

Skyrocketing advertising costs create another entry barrier for new comers. New

comers to the market have to spend a lot more on advertising and promotions to woo

We estimate 30%/36%

CAGR in topline/net profit

through 2012-2014

We expect Ginko to

continue to gain share from

its competitors at 1-2% per

annum

As of 2012, Ginko owns

maximum (55) product

licenses, followed by

Weicon (38), J&J (12), and

B&L (8)

01 March 2013

Taiwan Contact Lens Sector 17

customers and make the switch from market leaders who have built up strong brand

loyalty with proven product quality for years. In particular, advertising per second on

Chinese TV costs 5x more now than in 2005, according to Ginko.

Distribution channels preoccupied by market leaders. From a retail channel

perspective, they will not replace bestselling brands with a new brand on their shelves,

given the cash conversion cycle for the latter might be longer — despite more favourable

AR or rebate terms.

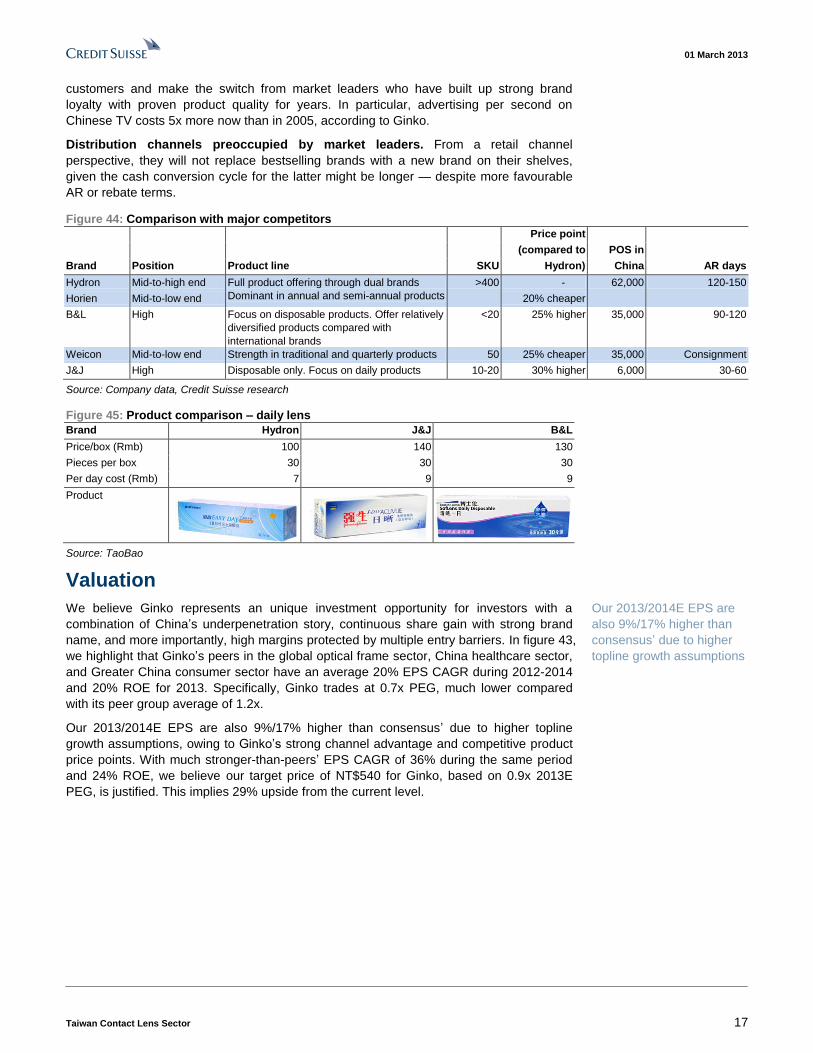

Figure 44: Comparison with major competitors

Price point

(compared to POS in

Brand Position Product line SKU Hydron) China AR days

Hydron Mid-to-high end Full product offering through dual brands

Dominant in annual and semi-annual products

>400 - 62,000 120-150

Horien Mid-to-low end 20% cheaper

B&L High Focus on disposable products. Offer relatively

diversified products compared with

international brands

<20 25% higher 35,000 90-120

Weicon Mid-to-low end Strength in traditional and quarterly products 50 25% cheaper 35,000 Consignment

J&J High Disposable only. Focus on daily products 10-20 30% higher 6,000 30-60

Source: Company data, Credit Suisse research

Figure 45: Product comparison – daily lens

Brand Hydron J&J B&L

Price/box (Rmb) 100 140 130

Pieces per box 30 30 30

Per day cost (Rmb) 7 9 9

Product

Source: TaoBao

Valuation

We believe Ginko represents an unique investment opportunity for investors with a

combination of China’s underpenetration story, continuous share gain with strong brand

name, and more importantly, high margins protected by multiple entry barriers. In figure 43,

we highlight that Ginko’s peers in the global optical frame sector, China healthcare sector,

and Greater China consumer sector have an average 20% EPS CAGR during 2012-2014

and 20% ROE for 2013. Specifically, Ginko trades at 0.7x PEG, much lower compared

with its peer group average of 1.2x.

Our 2013/2014E EPS are also 9%/17% higher than consensus’ due to higher topline

growth assumptions, owing to Ginko’s strong channel advantage and competitive product

price points. With much stronger-than-peers’ EPS CAGR of 36% during the same period

and 24% ROE, we believe our target price of NT$540 for Ginko, based on 0.9x 2013E

PEG, is justified. This implies 29% upside from the current level.

Our 2013/2014E EPS are

also 9%/17% higher than

consensus’ due to higher

topline growth assumptions

01 March 2013

Taiwan Contact Lens Sector 18

Figure 46: Peer valuation comparison

Company Ticker CS Rating Market cap

(US$mn)PER (x) PEG (x)

EPS CAGR

(2012-2014)ROE (%)

St. Shine 1565.TWO NTRL 876 18.3 1.2 15% 15%

Ginko 8406.TWO OPFM 1,305 25.2 0.7 36% 24%

Optical frame

Essilor ESSI.PA NR 20,787 23.9 2.3 10% 16%

Carl Zeiss Meditec AFXG.DE NR 2,490 21.2 1.3 16% 13%

Greater China healthcare

Sinopharm Taiwan 1789.TW NR 1,620 35.3 1.4 24% 14%

Shandong Weigao 1066.HK UPFM 4,166 20.1 1.1 19% 14%

Sino Biopharmaceutical 1177.HK NTRL 2,732 22.1 1.3 17% 21%

Sinopharm group 1099.HK NTRL 7,572 20.7 0.9 24% 13%

Hengan 1044.HK OPFM 12,523 22.5 1.0 23% 30%

Greater China consumer

Wowprime 2727.TW NR 990 18.5 1.7 11% 37%

Gourmet master 2723.TW NR 952 18.4 0.7 25% 22%

Tingyi 0322.HK OPFM 14,815 23.4 0.7 32% 32%

Uni-President China 0220.HK NR 4,222 22.6 1.1 21% 13%

Average 6,624 22.6 1.2 20% 20% Source: Company data, , Bloomberg, Credit Suisse estimates

Figure 47: CS estimates vs consensus—Ginko

FY12E FY13E FY14E

CS Consensus Diff (%) CS Consensus Diff (%) CS Consensus Diff (%)

Sales 3,846 3,861 -0.4% 5,160 4,756 8.5% 6,554 5,733 14.3%

Gross profit 2,478 2,485 -0.3% 3,323 3,038 9.4% 4,172 3,688 13.1%

Gross margin (%) 64.4% 64.4% 0.1% 64.4% 63.9% 0.5% 63.7% 64.3% -0.7%

Operating profit 1,280 1,278 0.2% 1,790 1,634 9.5% 2,342 2,026 15.6%

Operating margin (%) 33.3% 33.1% 0.2% 34.7% 34.4% 0.3% 35.7% 35.3% 0.4%

Net income 1,069 1,080 -1.0% 1,504 1,371 9.7% 1,973 1,690 16.7%

EPS 11.9 12.1 -2.0% 16.7 15.3 9.1% 21.9 18.8 16.5%

Source: Bloomberg, Credit Suisse estimates

Other financial details

Capex. With aggressive expansion plans across the Straits, we forecast NT$400

mn/NT$350 mn capex for 2013/2014, compared with NT$400 mn last year. According to

the company, capex needs can be met by internal cash flow.

Cash management. Management has attributed the relatively higher AR turnover days

(150-160 days if adjusted for VAT/rebate) largely to the business nature that vendors

generally give better settlement terms to distributors as incentives. The company expects

cash conversion cycle to remain stable in the years to come and believes working capital

needs to be fully covered by its strong operating cash flow.

Dividend policy. Payout ratio was low at 0-25% during 2009-2011. Going forward,

company has guided for at least 40% payout. This translates into a 1.1% yield in 2013.

Risks

Risks to our forecasts for Ginko include: 1) margin erosion caused by more aggressive

promotion/price-cut for market share; 2) failure to ramp up contact lens capacity as

scheduled; 3) worse-than-expected sales momentum; and 4) user migration to substitutes

of contact lens – LASIK and silicone hydrogel lens.

We forecast NT$400 mn

and NT$350 mn capex for

2013/2014

Company has guided for at

least 40% dividend payout

01 March 2013

Taiwan Contact Lens Sector 19

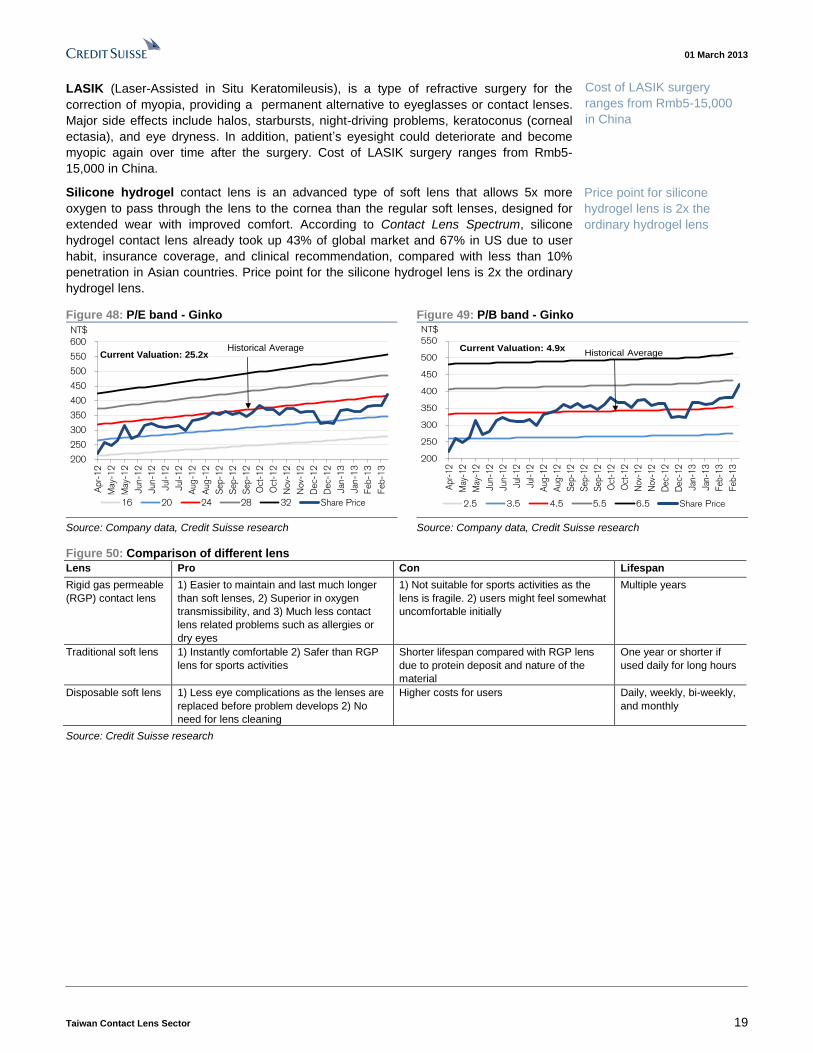

LASIK (Laser-Assisted in Situ Keratomileusis), is a type of refractive surgery for the

correction of myopia, providing a permanent alternative to eyeglasses or contact lenses.

Major side effects include halos, starbursts, night-driving problems, keratoconus (corneal

ectasia), and eye dryness. In addition, patient’s eyesight could deteriorate and become

myopic again over time after the surgery. Cost of LASIK surgery ranges from Rmb5-

15,000 in China.

Silicone hydrogel contact lens is an advanced type of soft lens that allows 5x more

oxygen to pass through the lens to the cornea than the regular soft lenses, designed for

extended wear with improved comfort. According to Contact Lens Spectrum, silicone

hydrogel contact lens already took up 43% of global market and 67% in US due to user

habit, insurance coverage, and clinical recommendation, compared with less than 10%

penetration in Asian countries. Price point for the silicone hydrogel lens is 2x the ordinary

hydrogel lens.

Figure 48: P/E band - Ginko Figure 49: P/B band - Ginko

200

250

300

350

400

450

500

550

600

Apr-

12

May-

12

May-

12

Jun-1

2

Jun-1

2

Jul-1

2

Jul-1

2

Aug-1

2

Aug-1

2

Sep-1

2

Sep-1

2

Sep-1

2

Oct

-12

Oct

-12

Nov-

12

Nov-

12

Dec-

12

Dec-

12

Jan-1

3

Jan-1

3

Feb-1

3

Feb-1

3

NT$

16 20 24 28 32 Share Price

Current Valuation: 25.2xHistorical Average

200

250

300

350

400

450

500

550

Apr

-12

May

-12

May

-12

Jun-

12

Jun-

12

Jul-12

Jul-12

Aug

-12

Aug

-12

Sep

-12

Sep

-12

Sep

-12

Oct

-12

Oct

-12

Nov

-12

Nov

-12

Dec

-12

Dec

-12

Jan-

13

Jan-

13

Feb

-13

Feb

-13

NT$

2.5 3.5 4.5 5.5 6.5 Share Price

Current Valuation: 4.9xHistorical Average

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

Figure 50: Comparison of different lens

Lens Pro Con Lifespan

Rigid gas permeable

(RGP) contact lens

1) Easier to maintain and last much longer

than soft lenses, 2) Superior in oxygen

transmissibility, and 3) Much less contact

lens related problems such as allergies or

dry eyes

1) Not suitable for sports activities as the

lens is fragile. 2) users might feel somewhat

uncomfortable initially

Multiple years

Traditional soft lens 1) Instantly comfortable 2) Safer than RGP

lens for sports activities

Shorter lifespan compared with RGP lens

due to protein deposit and nature of the

material

One year or shorter if

used daily for long hours

Disposable soft lens 1) Less eye complications as the lenses are

replaced before problem develops 2) No

need for lens cleaning

Higher costs for users Daily, weekly, bi-weekly,

and monthly

Source: Credit Suisse research

Cost of LASIK surgery

ranges from Rmb5-15,000

in China

Price point for silicone

hydrogel lens is 2x the

ordinary hydrogel lens

01 March 2013

Taiwan Contact Lens Sector 20

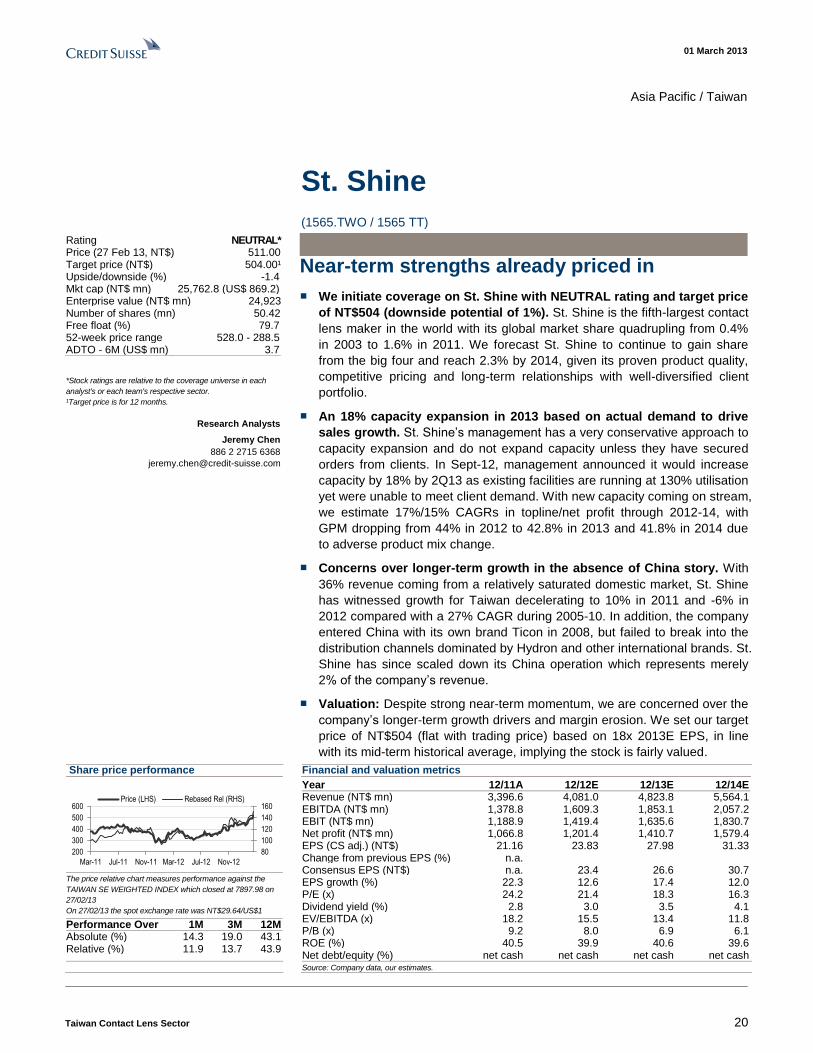

Asia Pacific / Taiwan

St. Shine

(1565.TWO / 1565 TT)

Near-term strengths already priced in

■ We initiate coverage on St. Shine with NEUTRAL rating and target price

of NT$504 (downside potential of 1%). St. Shine is the fifth-largest contact

lens maker in the world with its global market share quadrupling from 0.4%

in 2003 to 1.6% in 2011. We forecast St. Shine to continue to gain share

from the big four and reach 2.3% by 2014, given its proven product quality,

competitive pricing and long-term relationships with well-diversified client

portfolio.

■ An 18% capacity expansion in 2013 based on actual demand to drive

sales growth. St. Shine’s management has a very conservative approach to

capacity expansion and do not expand capacity unless they have secured

orders from clients. In Sept-12, management announced it would increase

capacity by 18% by 2Q13 as existing facilities are running at 130% utilisation

yet were unable to meet client demand. With new capacity coming on stream,

we estimate 17%/15% CAGRs in topline/net profit through 2012-14, with

GPM dropping from 44% in 2012 to 42.8% in 2013 and 41.8% in 2014 due

to adverse product mix change.

■ Concerns over longer-term growth in the absence of China story. With

36% revenue coming from a relatively saturated domestic market, St. Shine

has witnessed growth for Taiwan decelerating to 10% in 2011 and -6% in

2012 compared with a 27% CAGR during 2005-10. In addition, the company

entered China with its own brand Ticon in 2008, but failed to break into the

distribution channels dominated by Hydron and other international brands. St.

Shine has since scaled down its China operation which represents merely

2% of the company’s revenue.

■ Valuation: Despite strong near-term momentum, we are concerned over the

company’s longer-term growth drivers and margin erosion. We set our target

price of NT$504 (flat with trading price) based on 18x 2013E EPS, in line

with its mid-term historical average, implying the stock is fairly valued.

Share price performance

80

100

120

140

160

200

300

400

500

600

Mar-11 Jul-11 Nov-11 Mar-12 Jul-12 Nov-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

TAIWAN SE WEIGHTED INDEX which closed at 7897.98 on

27/02/13

On 27/02/13 the spot exchange rate was NT$29.64/US$1

Performance Over 1M 3M 12M Absolute (%) 14.3 19.0 43.1 Relative (%) 11.9 13.7 43.9

Financial and valuation metrics

Year 12/11A 12/12E 12/13E 12/14E Revenue (NT$ mn) 3,396.6 4,081.0 4,823.8 5,564.1 EBITDA (NT$ mn) 1,378.8 1,609.3 1,853.1 2,057.2 EBIT (NT$ mn) 1,188.9 1,419.4 1,635.6 1,830.7 Net profit (NT$ mn) 1,066.8 1,201.4 1,410.7 1,579.4 EPS (CS adj.) (NT$) 21.16 23.83 27.98 31.33 Change from previous EPS (%) n.a. Consensus EPS (NT$) n.a. 23.4 26.6 30.7 EPS growth (%) 22.3 12.6 17.4 12.0 P/E (x) 24.2 21.4 18.3 16.3 Dividend yield (%) 2.8 3.0 3.5 4.1 EV/EBITDA (x) 18.2 15.5 13.4 11.8 P/B (x) 9.2 8.0 6.9 6.1 ROE (%) 40.5 39.9 40.6 39.6 Net debt/equity (%) net cash net cash net cash net cash

Source: Company data, our estimates.

Rating NEUTRAL* Price (27 Feb 13, NT$) 511.00 Target price (NT$) 504.00¹ Upside/downside (%) -1.4 Mkt cap (NT$ mn) 25,762.8 (US$ 869.2) Enterprise value (NT$ mn) 24,923 Number of shares (mn) 50.42 Free float (%) 79.7 52-week price range 528.0 - 288.5 ADTO - 6M (US$ mn) 3.7

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Jeremy Chen

886 2 2715 6368

01 March 2013

Taiwan Contact Lens Sector 21

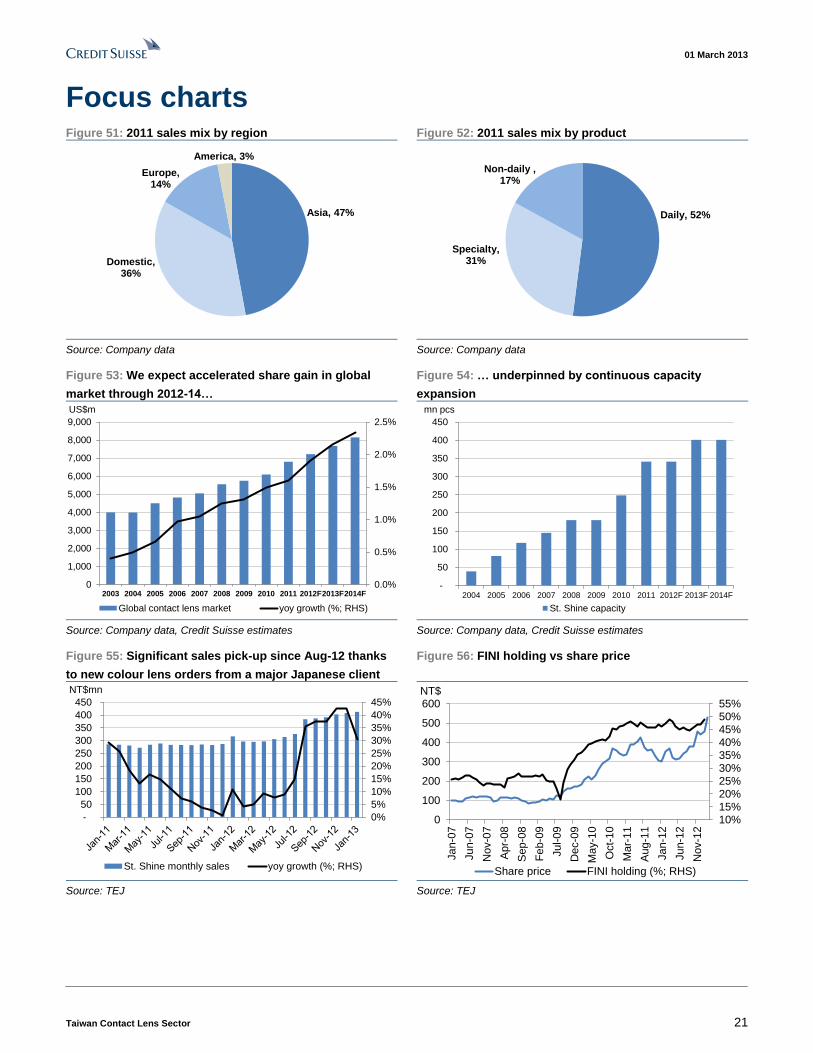

Focus charts Figure 51: 2011 sales mix by region Figure 52: 2011 sales mix by product

Asia, 47%

Domestic, 36%

Europe, 14%

America, 3%

Daily, 52%

Specialty, 31%

Non-daily , 17%

Source: Company data Source: Company data

Figure 53: We expect accelerated share gain in global

market through 2012-14…

Figure 54: … underpinned by continuous capacity

expansion

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012F2013F2014F

US$m

Global contact lens market yoy growth (%; RHS)

-

50

100

150

200

250

300

350

400

450

2004 2005 2006 2007 2008 2009 2010 2011 2012F 2013F 2014F

mn pcs

St. Shine capacity

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

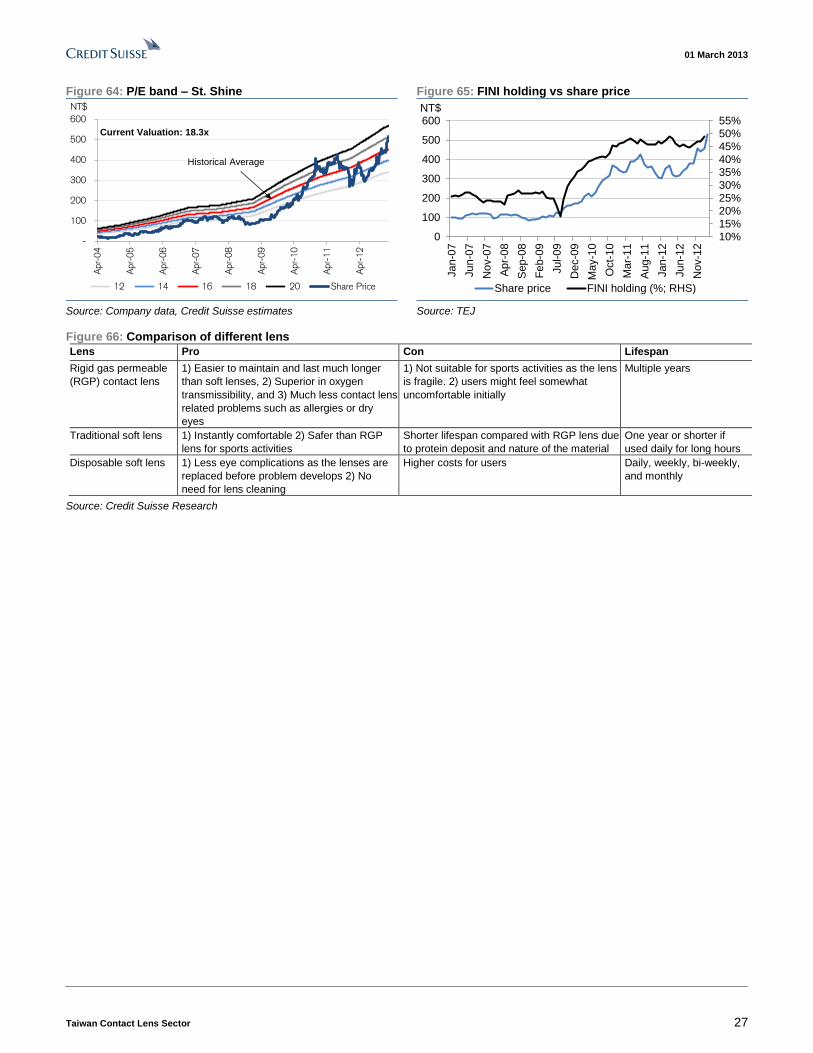

Figure 55: Significant sales pick-up since Aug-12 thanks

to new colour lens orders from a major Japanese client

Figure 56: FINI holding vs share price

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

-

50

100

150

200

250

300

350

400

450

NT$mn

St. Shine monthly sales yoy growth (%; RHS)

10%15%20%25%

30%35%40%

45%50%55%

0

100

200

300

400

500

600

Ja

n-0

7

Ju

n-0

7

No

v-0

7

Apr-

08

Sep

-08

Fe

b-0

9

Ju

l-0

9

De

c-0

9

Ma

y-1

0

Oct-

10

Mar-

11

Aug-1

1

Jan-1

2

Jun-1

2

Nov-1

2NT$

Share price FINI holding (%; RHS) Source: TEJ Source: TEJ

01 March 2013

Taiwan Contact Lens Sector 22

St. Shine 1565.TWO / 1565 TT Price (27 Feb 13): NT$511.00, Rating:: NEUTRAL, Target Price: NT$504.00, Analyst: Jeremy Chen

Target price scenario

Scenario TP %Up/Dwn Assumptions

Upside 560.00 9.59 20x 2013EPS Central Case 504.00 (1.37) 18x 2013EPS Downside 448.00 (12.33) 16x 2013EPS

Key earnings drivers 12/11A 12/12E 12/13E 12/14E

Capacity (mn pieces) 341.1 341.1 401.3 401.3 Gross margin (%) 47.6 44.0 42.8 41.8 — — — — — — — — — — — —

Income statement (NT$ mn) 12/11A 12/12E 12/13E 12/14E

Sales revenue 3,397 4,081 4,824 5,564 Cost of goods sold 1,779 2,286 2,759 3,239 SG&A — — — — Other operating exp./(inc.) 238.7 185.4 211.9 268.3 EBITDA 1,379 1,609 1,853 2,057 Depreciation & amortisation 189.9 189.9 217.4 226.5 EBIT 1,189 1,419 1,636 1,831 Net interest expense/(inc.) 3.2 0.3 0.6 (0.2) Non-operating inc./(exp.) 30.8 (39.6) (20.2) (19.9) Associates/JV — — — — Recurring PBT 1,216 1,379 1,615 1,811 Exceptionals/extraordinaries — — — — Taxes 149.6 178.0 204.1 231.5 Profit after tax 1,067 1,201 1,411 1,579 Other after tax income — — — — Minority interests — — — — Preferred dividends — — — — Reported net profit 1,067 1,201 1,411 1,579 Analyst adjustments — — — — Net profit (Credit Suisse) 1,067 1,201 1,411 1,579

Cash flow (NT$ mn) 12/11A 12/12E 12/13E 12/14E

EBIT 1,189 1,419 1,636 1,831 Net interest — — — — Tax paid — — — — Working capital (167.8) (48.1) (288.6) (68.7) Other cash & non-cash items 62.0 (18.8) 1.9 (15.4) Operating cash flow 1,083 1,353 1,349 1,747 Capex (239.4) (408.1) (289.4) (278.2) Free cash flow to the firm 844 944 1,059 1,468 Disposals of fixed assets 0.09 — — — Acquisitions — — — — Divestments — — — — Associate investments — — — — Other investment/(outflows) (8.9) — — — Investing cash flow (248.2) (408.1) (289.4) (278.2) Equity raised — — — — Dividends paid (731) (781) (901) (1,058) Net borrowings (70.3) — — — Other financing cash flow — — — — Financing cash flow (801) (781) (901) (1,058) Total cash flow 33.5 163.0 158.4 410.3 Adjustments 1,015 1,048 1,211 1,369 Net change in cash 1,048 1,211 1,369 1,780

Balance sheet (NT$ mn) 12/11A 12/12E 12/13E 12/14E

Cash & cash equivalents 1,048 1,211 1,369 1,780 Current receivables 551.7 627.7 742.0 855.9 Inventories 514.3 661.0 797.6 936.3 Other current assets 112.0 112.0 112.0 112.0 Current assets 2,226 2,612 3,021 3,684 Property, plant & equip. 1,507 1,725 1,797 1,849 Investments 145.6 136.3 127.0 117.6 Intangibles — — — — Other non-current assets 46.0 46.0 46.0 46.0 Total assets 3,925 4,519 4,991 5,697 Accounts payable 169.5 204.0 246.1 288.9 Short-term debt 64.0 64.0 64.0 64.0 Current provisions 33.8 164.3 74.7 205.9 Other current liabilities 517.8 527.3 537.1 547.0 Current liabilities 785 960 922 1,106 Long-term debt 306.8 306.8 306.8 306.8 Non-current provisions — — — — Other non-current liab. 15.8 15.8 15.8 15.8 Total liabilities 1,108 1,282 1,245 1,428 Shareholders' equity 2,802 3,222 3,731 4,253 Minority interests — — — — Total liabilities & equity 3,925 4,519 4,991 5,697

Per share data 12/11A 12/12E 12/13E 12/14E

Shares (wtd avg.) (mn) 50.4 50.4 50.4 50.4 EPS (Credit Suisse) (NT$)

21.2 23.8 28.0 31.3 DPS (NT$) 14.5 15.5 17.9 21.0 BVPS (NT$) 55.6 63.9 74.0 84.4 Operating CFPS (NT$) 21.5 26.8 26.8 34.6

Key ratios and valuation 12/11A 12/12E 12/13E 12/14E

Growth(%) Sales revenue 11.8 20.1 18.2 15.3 EBIT 1.8 19.4 15.2 11.9 Net profit 22.3 12.6 17.4 12.0 EPS 22.3 12.6 17.4 12.0 Margins (%) EBITDA 40.6 39.4 38.4 37.0 EBIT 35.0 34.8 33.9 32.9 Pre-tax profit 35.8 33.8 33.5 32.5 Net profit 31.4 29.4 29.2 28.4 Valuation metrics (x) P/E 24.2 21.4 18.3 16.3 P/B 9.2 8.0 6.9 6.1 Dividend yield (%) 2.84 3.03 3.50 4.11 P/CF 23.8 19.0 19.1 14.8 EV/sales 7.39 6.11 5.13 4.38 EV/EBITDA 18.2 15.5 13.4 11.8 EV/EBIT 21.1 17.6 15.1 13.3 ROE analysis (%) ROE 40.5 39.9 40.6 39.6 ROIC 51.7 54.5 55.5 56.9 Asset turnover (x) 0.87 0.90 0.97 0.98 Interest burden (x) 1.02 0.97 0.99 0.99 Tax burden (x) 0.88 0.87 0.87 0.87 Financial leverage (x) 1.39 1.40 1.33 1.33 Credit ratios Net debt/equity (%) (24.0) (26.0) (26.7) (33.0) Net debt/EBITDA (x) (0.49) (0.52) (0.54) (0.68) Interest cover (x) 373 4,395 2,635 (10,681)

Source: Company data, our estimates

0

1

2

3

4

5

6

7

8

9

2008 2009 2010 2011 2012 2013

12MF P/B multiple

Source: IBES

0

5

10

15

20

25

2008 2009 2010 2011 2012 2013

12MF P/E multiple

01 March 2013

Taiwan Contact Lens Sector 23

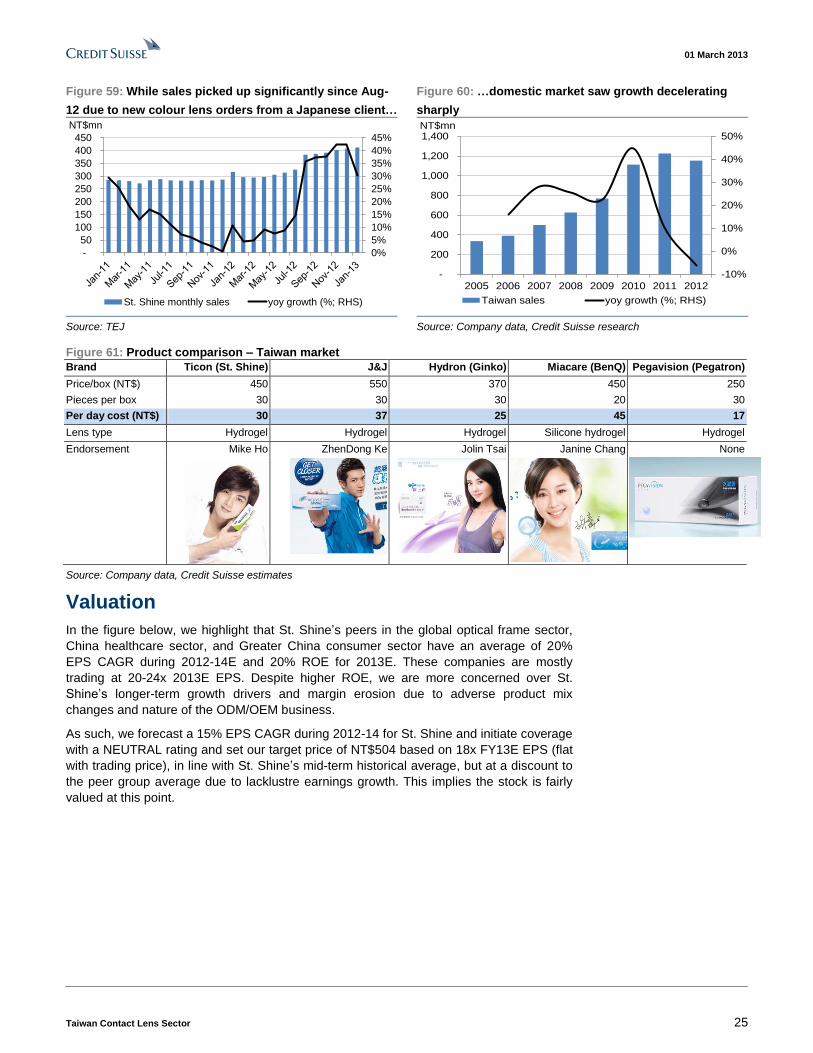

Near-term strengths already priced in Company description

The company was founded in 1981 by a consortium of experts in the contact lens industry

and was renamed as St. Shine Optical in 1986. Since its first cast-molding capacity set up

in 1992, St. Shine has successfully completed ISO system assessments, CE Certification

(Europe), FDA inspection (US) for production, and is GMP certified by the Taiwan health

authorities for both lathe-cut and cast-molding production lines over the years. For the past

25 years, St. Shine is providing a wide variety of products to more than 500 customers.

Most of its customers are distributors or medical suppliers who want to start their own

disposable contact lens brand. St. Shine’s products range from conventional lathe-cut to

cast-molding, from RGP (rigid gas permeable) lens to soft contact lens, and from longer-

cycled lens to disposable daily lens. The company also has its own brand named Ticon in

Taiwan, controlling 30% of the domestic market, following No.1 J&J (35%) closely.

In 2011, St. Shine derived 36% of total revenue from the domestic market with own brand

Ticon and the remaining 64% from OEM/ODM business, of which, 47% came from Asia,

14% from Europe, and 3% from America. By product mix, daily products contribute 52% to

overall sales, followed by specialty lens (traditional, toric and colour lens, 31%) and non-

daily disposable lens (17%). As of 2012, gross margin for Ticon could reach 55–60%

versus 35–50% for OEM/ODM products. By 2011, St. Shine ranked as the fifth-largest

contact lens maker in the world with 1.6% market share globally, following J&J (42%),

CIBA (25%), Cooper (17%) and B&L (11%).

As at end-2012, St. Shine ran 34 production lines (total capacity of 341 mn pieces) with all

its four factories located in New Taipei City. Most of St. Shine’s capacity are mold-casting,

similar to Ginko’s. To provide clients with various product specs, it requires intensive

labour participation in the manufacturing and packaging processes, and the company has

employed more than 2,000 staff by end-2012. Thus, labor cost accounts for 40% in COGS,

followed by packaging materials (20%), depreciation (10%) and raw material (3%).

Figure 57: Shareholding structure Figure 58: Cost structure comparison

FINI Management Other

St. Shine (1565.TW)

46.9% 10.1% 43.0%

60%

20%

10%

40%

10%

10%

5%

3%

15%27%

0%

20%

40%

60%

80%

100%

Ginko St. Shine

Packaging materials Labor Depreciation Raw material Other

Source: Company data Source: Company data, Credit Suisse research

An 18% capacity expansion in 2013 based on actual

demand to drive sales growth

St. Shine’s management have a very conservative approach to capacity expansion and

they do not expand capacity unless they have secured orders from clients. In September

2012, management announced their plan to add six product lines on top of the existing 34

which are running at 130% utilisation based on three shifts as they were still unable to

For the past 25 years, St.

Shine has provided a wide

variety of products for more

than 500 customers

(primarily distributors and

medial suppliers)

St. Shine is fifth-largest

contact lens maker in the

world and No.2 player in

Taiwan

Labour cost accounts for

40% in COGS, followed by

packaging materials (20%),

depreciation (10%) and raw

material (3%).

01 March 2013

Taiwan Contact Lens Sector 24

meet client demand. Total capex of NT$220 mn was invested starting 4Q12 and the

expansion will be completed by 2Q13. This will bring St. Shine’s total capacity from 341

mn pieces in 2012 to approximately 400 mn pieces, or 18% YoY growth.

Concerns over longer-term growth in the absence of

China story

Domestic market

St. Shine has been gaining shares in the domestic market since its listing in 2004, with

market share soaring from 14% in 2005 to 30% in 2012, thanks to its competitive price

points, strong brand image, and proven product quality.

With 36% revenue coming from a relatively saturated domestic market, St. Shine has

witnessed growth for Taiwan decelerating to 10% in 2011 and -6% in 2012 compared with

a 27% CAGR during 2005-10. We do not expect high growth in the Taiwan market to

continue in the coming years as: 1) the market has been saturated with contact lens

penetration reaching 25%, one of the highest in the world; 2) limited room for further share

gain due to intensifying competition—several tech companies have diversified into this

field lately, including Pegavision (Pegatron), Miacare (BenQ group), Largan Med (Largan),

etc. In addition, Hydron, the No.1 brand in China under Ginko International, was also

introduced in Taiwan last year. Looking ahead, management expects flat growth for

domestic market and target to maintain market share at 30%.

Japan

Japan is one of the largest contact lens markets in the world, representing approximately

20% of the global market (61% of Asia), thanks to high penetration (24%) and use of