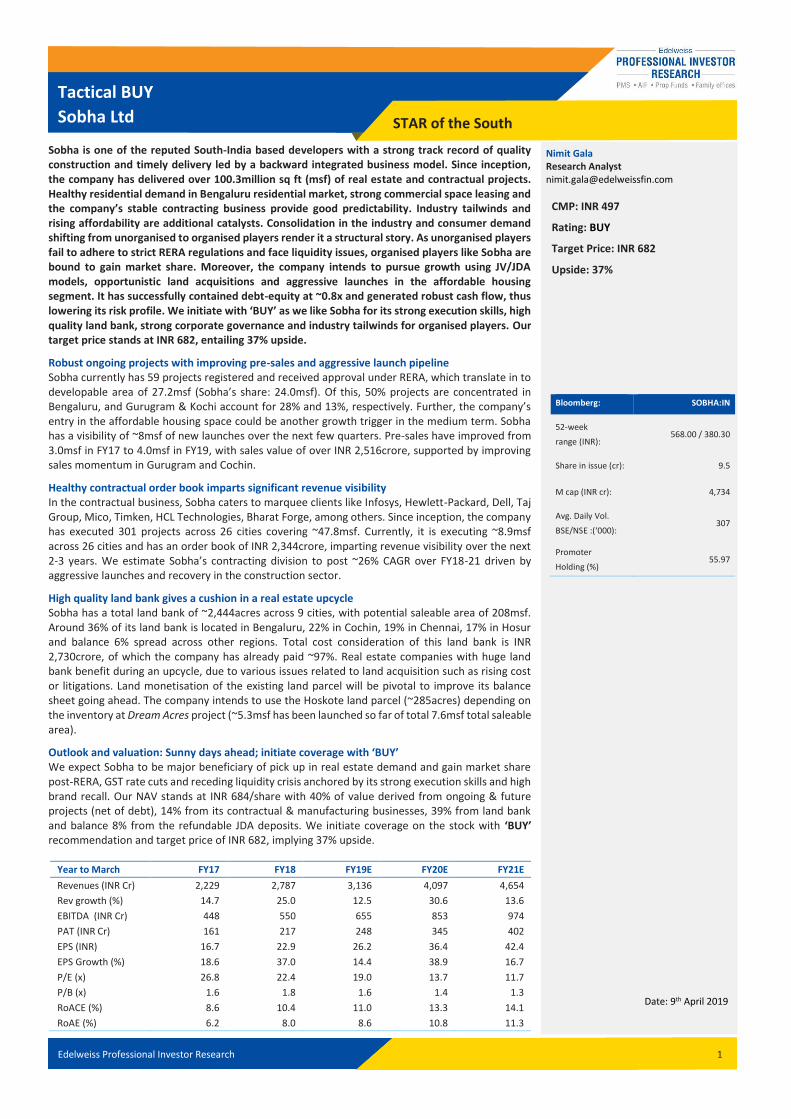

Edelweiss Professional Investor Research Insightful. Independent. Decisive. Tactical BUY: Sobha Ltd Date: 09th April 2019 Nimit Gala Research Analyst [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Edelweiss Professional Investor Research Insightful. Independent. Decisive.

Tactical BUY: Sobha Ltd

Date: 09th April 2019

Nimit Gala

Research Analyst

Edelweiss Professional Investor Research

Tactical BUY

Sobha Ltd STAR of the South

1

Nimit Gala Research Analyst [email protected]

CMP: INR 497

Rating: BUY

Target Price: INR 682

Upside: 37%

Bloomberg: SOBHA:IN

52-week

range (INR): 568.00 / 380.30

Share in issue (cr): 9.5

M cap (INR cr): 4,734

Avg. Daily Vol.

BSE/NSE :(‘000): 307

Promoter

Holding (%) 55.97

Date: 9th April 2019

Sobha is one of the reputed South-India based developers with a strong track record of quality construction and timely delivery led by a backward integrated business model. Since inception, the company has delivered over 100.3million sq ft (msf) of real estate and contractual projects. Healthy residential demand in Bengaluru residential market, strong commercial space leasing and the company’s stable contracting business provide good predictability. Industry tailwinds and rising affordability are additional catalysts. Consolidation in the industry and consumer demand shifting from unorganised to organised players render it a structural story. As unorganised players fail to adhere to strict RERA regulations and face liquidity issues, organised players like Sobha are bound to gain market share. Moreover, the company intends to pursue growth using JV/JDA models, opportunistic land acquisitions and aggressive launches in the affordable housing segment. It has successfully contained debt-equity at ~0.8x and generated robust cash flow, thus lowering its risk profile. We initiate with ‘BUY’ as we like Sobha for its strong execution skills, high quality land bank, strong corporate governance and industry tailwinds for organised players. Our target price stands at INR 682, entailing 37% upside.

Robust ongoing projects with improving pre-sales and aggressive launch pipeline Sobha currently has 59 projects registered and received approval under RERA, which translate in to developable area of 27.2msf (Sobha’s share: 24.0msf). Of this, 50% projects are concentrated in Bengaluru, and Gurugram & Kochi account for 28% and 13%, respectively. Further, the company’s entry in the affordable housing space could be another growth trigger in the medium term. Sobha has a visibility of ~8msf of new launches over the next few quarters. Pre-sales have improved from 3.0msf in FY17 to 4.0msf in FY19, with sales value of over INR 2,516crore, supported by improving sales momentum in Gurugram and Cochin.

Healthy contractual order book imparts significant revenue visibility In the contractual business, Sobha caters to marquee clients like Infosys, Hewlett-Packard, Dell, Taj Group, Mico, Timken, HCL Technologies, Bharat Forge, among others. Since inception, the company has executed 301 projects across 26 cities covering ~47.8msf. Currently, it is executing ~8.9msf across 26 cities and has an order book of INR 2,344crore, imparting revenue visibility over the next 2-3 years. We estimate Sobha’s contracting division to post ~26% CAGR over FY18-21 driven by aggressive launches and recovery in the construction sector.

High quality land bank gives a cushion in a real estate upcycle Sobha has a total land bank of ~2,444acres across 9 cities, with potential saleable area of 208msf. Around 36% of its land bank is located in Bengaluru, 22% in Cochin, 19% in Chennai, 17% in Hosur and balance 6% spread across other regions. Total cost consideration of this land bank is INR 2,730crore, of which the company has already paid ~97%. Real estate companies with huge land bank benefit during an upcycle, due to various issues related to land acquisition such as rising cost or litigations. Land monetisation of the existing land parcel will be pivotal to improve its balance sheet going ahead. The company intends to use the Hoskote land parcel (~285acres) depending on the inventory at Dream Acres project (~5.3msf has been launched so far of total 7.6msf total saleable area).

Outlook and valuation: Sunny days ahead; initiate coverage with ‘BUY’ We expect Sobha to be major beneficiary of pick up in real estate demand and gain market share post-RERA, GST rate cuts and receding liquidity crisis anchored by its strong execution skills and high brand recall. Our NAV stands at INR 684/share with 40% of value derived from ongoing & future projects (net of debt), 14% from its contractual & manufacturing businesses, 39% from land bank and balance 8% from the refundable JDA deposits. We initiate coverage on the stock with ‘BUY’ recommendation and target price of INR 682, implying 37% upside.

Year to March FY17 FY18 FY19E FY20E FY21E

Revenues (INR Cr) 2,229 2,787 3,136 4,097 4,654

Rev growth (%) 14.7 25.0 12.5 30.6 13.6

EBITDA (INR Cr) 448 550 655 853 974

PAT (INR Cr) 161 217 248 345 402

EPS (INR) 16.7 22.9 26.2 36.4 42.4

EPS Growth (%) 18.6 37.0 14.4 38.9 16.7

P/E (x) 26.8 22.4 19.0 13.7 11.7

P/B (x) 1.6 1.8 1.6 1.4 1.3

RoACE (%) 8.6 10.4 11.0 13.3 14.1

RoAE (%) 6.2 8.0 8.6 10.8 11.3

Edelweiss Professional Investor Research 2

Table of Contents

Structure ............................................................................................................................ 3

Share Price History .............................................................................................................. 4

Focus Charts 1 .................................................................................................................... 5

Focus Charts 2 .................................................................................................................... 6

I. Robust ongoing projects with improving pre-sales and aggressive launches.................. 8

II. Healthy contractual division order book imparts ample revenue visibility .................... 11

III. High quality land bank gives a cushion in a real estate upcycle .................................... 12

Outlook and Valuations ..................................................................................................... 14

Peer comparison ................................................................................................................. 15

Business Model .................................................................................................................. 18

Management Profile .......................................................................................................... 22

Timeline ............................................................................................................................. 23

Financial Analysis ............................................................................................................... 24

Financials ........................................................................................................................... 27

Annexure ............................................................................................................................ 30

Annexure Company Overview ............................................................................................ 31

Annexure Sector Overview ................................................................................................. 35

Edelweiss Professional Investor Research

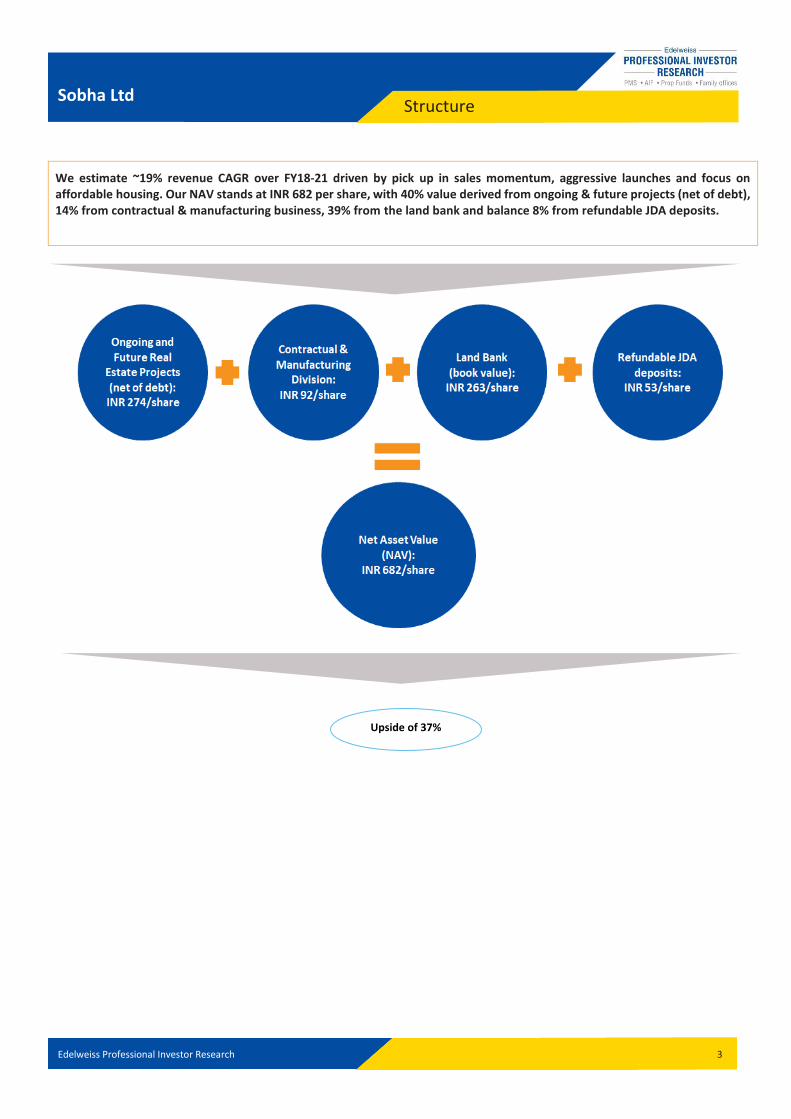

Structure Sobha Ltd

3

We estimate ~19% revenue CAGR over FY18-21 driven by pick up in sales momentum, aggressive launches and focus on affordable housing. Our NAV stands at INR 682 per share, with 40% value derived from ongoing & future projects (net of debt), 14% from contractual & manufacturing business, 39% from the land bank and balance 8% from refundable JDA deposits.

Upside of 37%

Edelweiss Professional Investor Research

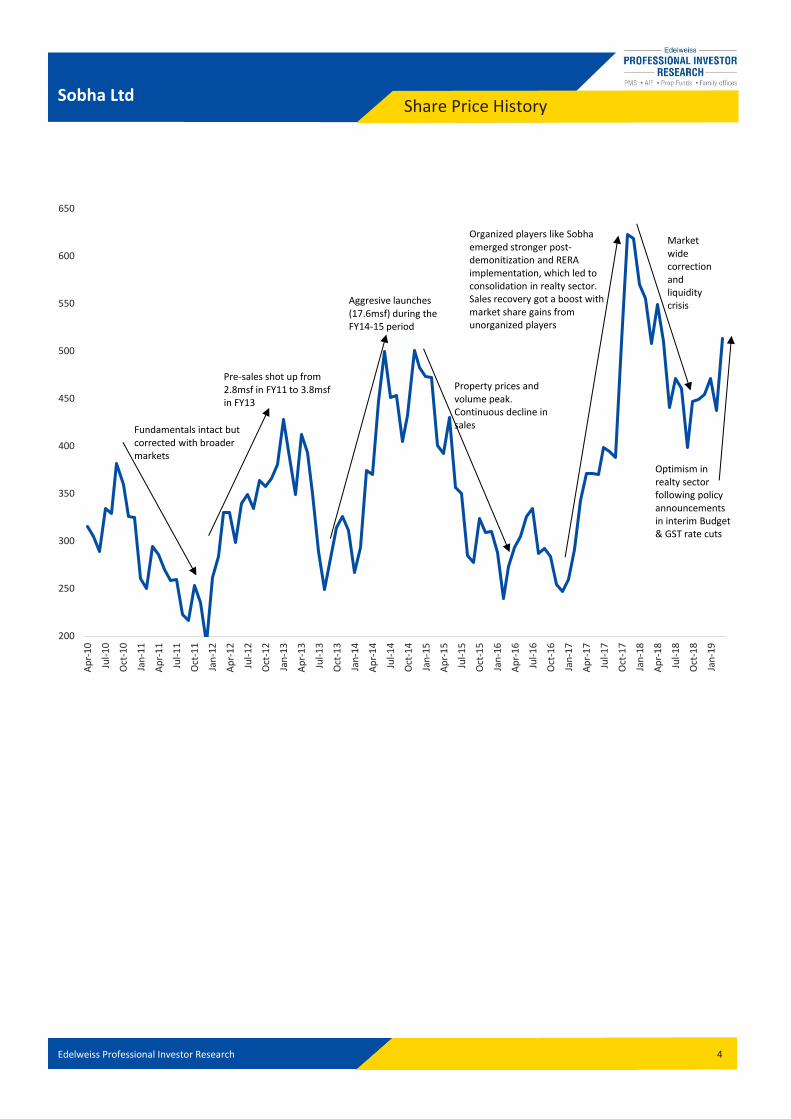

Share Price History Sobha Ltd

4

200

250

300

350

400

450

500

550

600

650

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Fundamentals intact but corrected with broader markets

Pre-sales shot up from 2.8msf in FY11 to 3.8msf in FY13

Aggresive launches (17.6msf) during theFY14-15 period

Property prices and volume peak. Continuous decline in sales

Organized players like Sobha emerged stronger post-demonitization and RERA implementation, which led to consolidation in realty sector. Sales recovery got a boost with market share gains from unorganized players

Marketwide correction and liquidity crisis

Optimism in realty sector following policyannouncements in interim Budget& GST rate cuts

Edelweiss Professional Investor Research

Focus Charts Sobha Ltd

5

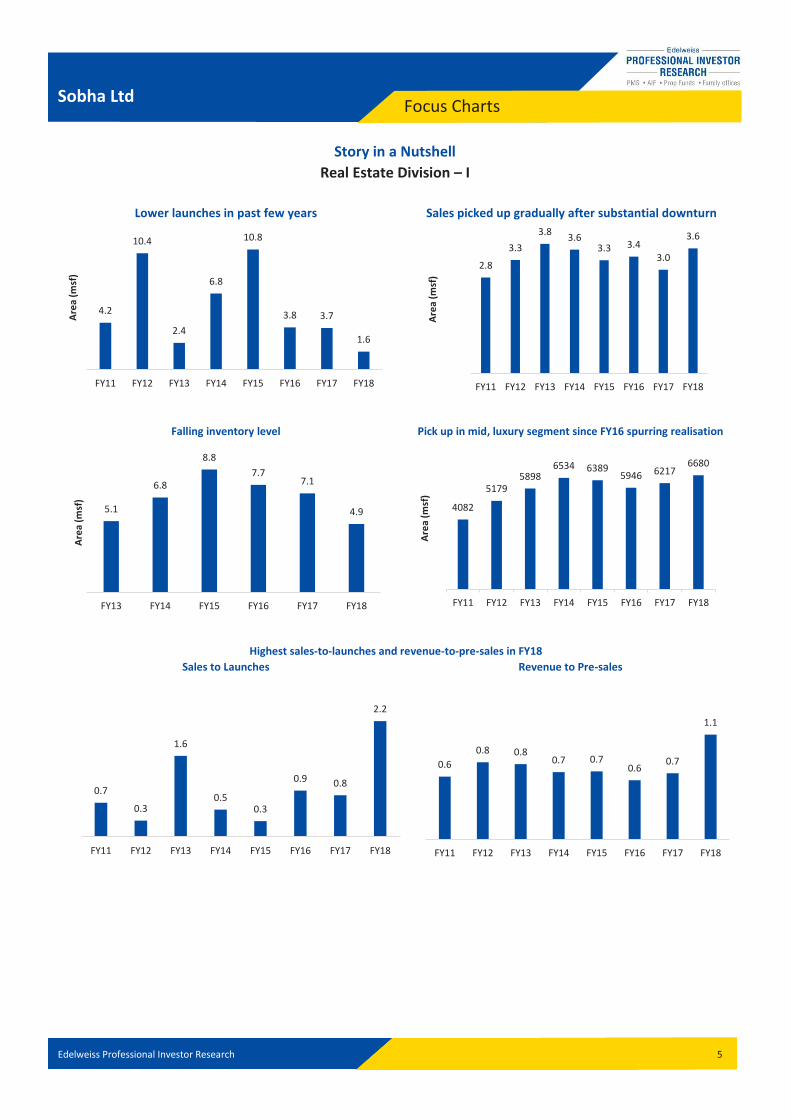

Story in a Nutshell

Real Estate Division – I

Lower launches in past few years Sales picked up gradually after substantial downturn

Falling inventory level Pick up in mid, luxury segment since FY16 spurring realisation

Highest sales-to-launches and revenue-to-pre-sales in FY18 Sales to Launches Revenue to Pre-sales

4.2

10.4

2.4

6.8

10.8

3.8 3.7

1.6

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Are

a (m

sf)

2.8

3.3

3.83.6

3.3 3.43.0

3.6

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Are

a (m

sf)

5.1

6.8

8.8

7.77.1

4.9

FY13 FY14 FY15 FY16 FY17 FY18

Are

a (m

sf)

4082

51795898

6534 63895946 6217

6680

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Are

a (m

sf)

0.7

0.3

1.6

0.50.3

0.9 0.8

2.2

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

0.6

0.8 0.80.7 0.7

0.60.7

1.1

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Edelweiss Professional Investor Research

Focus Charts Sobha Ltd

6

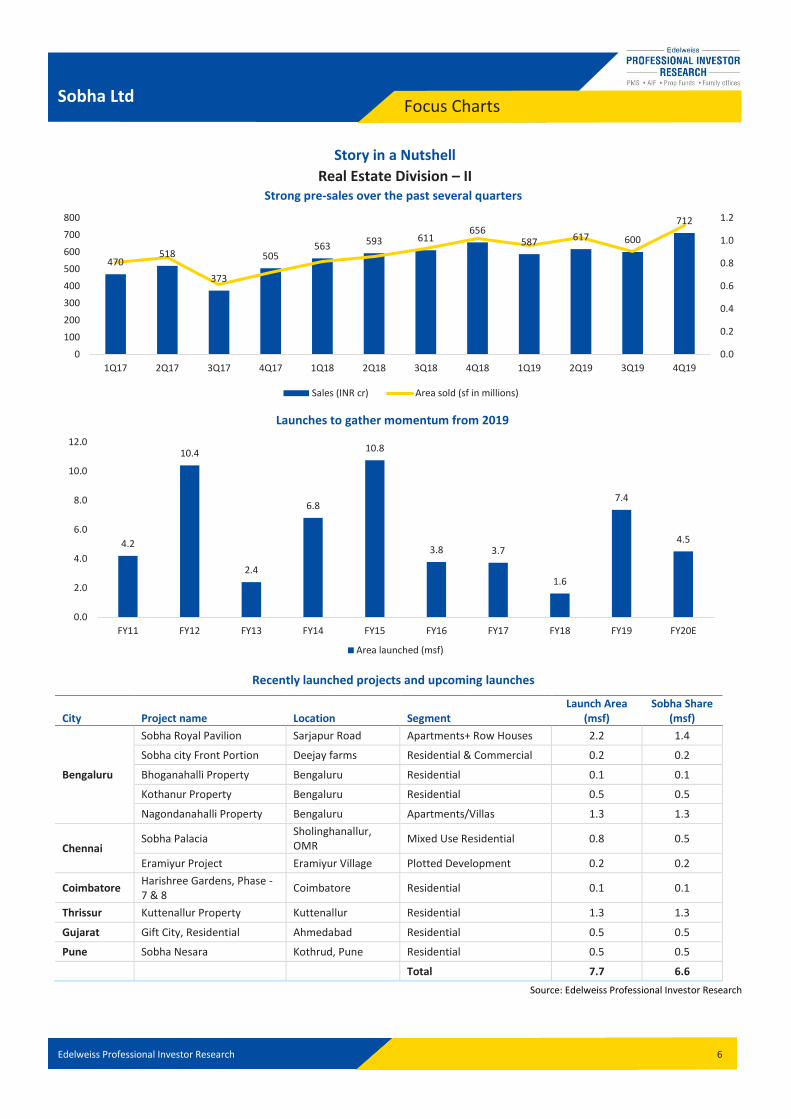

Story in a Nutshell

Real Estate Division – II Strong pre-sales over the past several quarters

Launches to gather momentum from 2019

Recently launched projects and upcoming launches

City Project name Location Segment Launch Area

(msf) Sobha Share

(msf)

Bengaluru

Sobha Royal Pavilion Sarjapur Road Apartments+ Row Houses 2.2 1.4

Sobha city Front Portion Deejay farms Residential & Commercial 0.2 0.2

Bhoganahalli Property Bengaluru Residential 0.1 0.1

Kothanur Property Bengaluru Residential 0.5 0.5

Nagondanahalli Property Bengaluru Apartments/Villas 1.3 1.3

Chennai Sobha Palacia

Sholinghanallur, OMR

Mixed Use Residential 0.8 0.5

Eramiyur Project Eramiyur Village Plotted Development 0.2 0.2

Coimbatore Harishree Gardens, Phase - 7 & 8

Coimbatore Residential 0.1 0.1

Thrissur Kuttenallur Property Kuttenallur Residential 1.3 1.3

Gujarat Gift City, Residential Ahmedabad Residential 0.5 0.5

Pune Sobha Nesara Kothrud, Pune Residential 0.5 0.5

Total 7.7 6.6

Source: Edelweiss Professional Investor Research

470518

373

505563 593 611

656587 617 600

712

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0

100

200

300

400

500

600

700

800

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Sales (INR cr) Area sold (sf in millions)

4.2

10.4

2.4

6.8

10.8

3.8 3.7

1.6

7.4

4.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E

Area launched (msf)

Edelweiss Professional Investor Research

Focus Charts Sobha Ltd

7

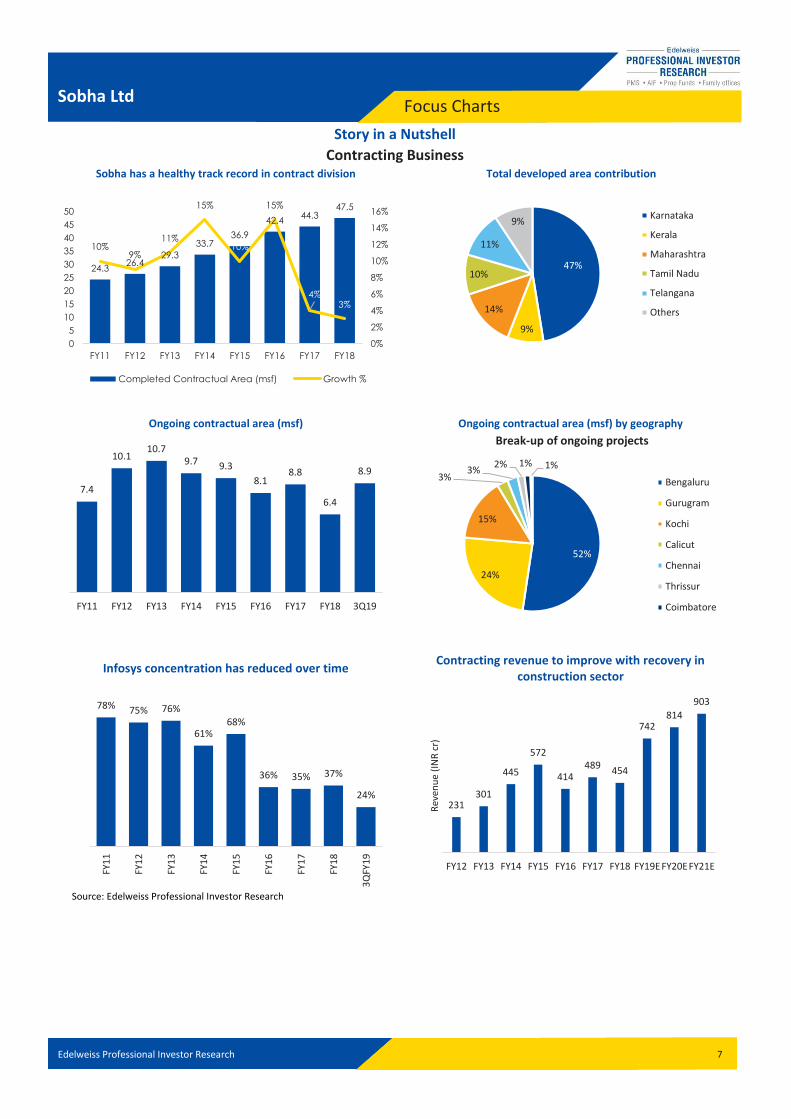

Story in a Nutshell

Contracting Business Sobha has a healthy track record in contract division Total developed area contribution

Ongoing contractual area (msf) Ongoing contractual area (msf) by geography

Infosys concentration has reduced over time Contracting revenue to improve with recovery in

construction sector

Source: Edelweiss Professional Investor Research

24.326.4

29.3

33.736.9

42.444.3

47.5

10%9%

11%

15%

10%

15%

4%3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

5

10

15

20

25

30

35

40

45

50

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Completed Contractual Area (msf) Growth %

47%

9%

14%

10%

11%

9%Karnataka

Kerala

Maharashtra

Tamil Nadu

Telangana

Others

7.4

10.110.7

9.7 9.3

8.18.8

6.4

8.9

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 3Q19

52%

24%

15%

3%3%

2% 1% 1%

Break-up of ongoing projects

Bengaluru

Gurugram

Kochi

Calicut

Chennai

Thrissur

Coimbatore

78% 75% 76%

61%68%

36% 35% 37%

24%

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

3Q

FY1

9

231301

445

572

414489

454

742814

903

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19EFY20EFY21E

Rev

enu

e (I

NR

cr)

Edelweiss Professional Investor Research 8

Investment Hypothesis Sobha Ltd

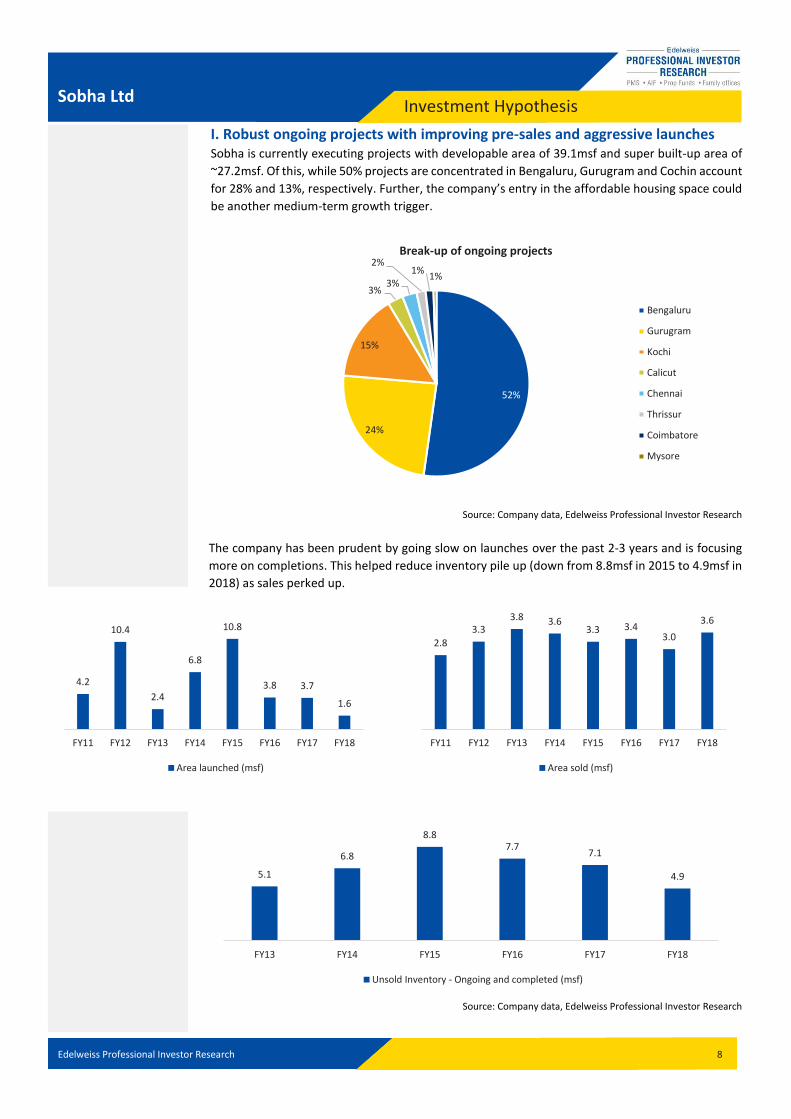

I. Robust ongoing projects with improving pre-sales and aggressive launches Sobha is currently executing projects with developable area of 39.1msf and super built-up area of

~27.2msf. Of this, while 50% projects are concentrated in Bengaluru, Gurugram and Cochin account

for 28% and 13%, respectively. Further, the company’s entry in the affordable housing space could

be another medium-term growth trigger.

Source: Company data, Edelweiss Professional Investor Research

The company has been prudent by going slow on launches over the past 2-3 years and is focusing

more on completions. This helped reduce inventory pile up (down from 8.8msf in 2015 to 4.9msf in

2018) as sales perked up.

Source: Company data, Edelweiss Professional Investor Research

52%

24%

15%

3%3%

2%1%

1%

Break-up of ongoing projects

Bengaluru

Gurugram

Kochi

Calicut

Chennai

Thrissur

Coimbatore

Mysore

4.2

10.4

2.4

6.8

10.8

3.8 3.7

1.6

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Area launched (msf)

2.8

3.33.8 3.6

3.3 3.43.0

3.6

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Area sold (msf)

5.1

6.8

8.87.7

7.1

4.9

FY13 FY14 FY15 FY16 FY17 FY18

Unsold Inventory - Ongoing and completed (msf)

Edelweiss Professional Investor Research 9

Investment Hypothesis Sobha Ltd

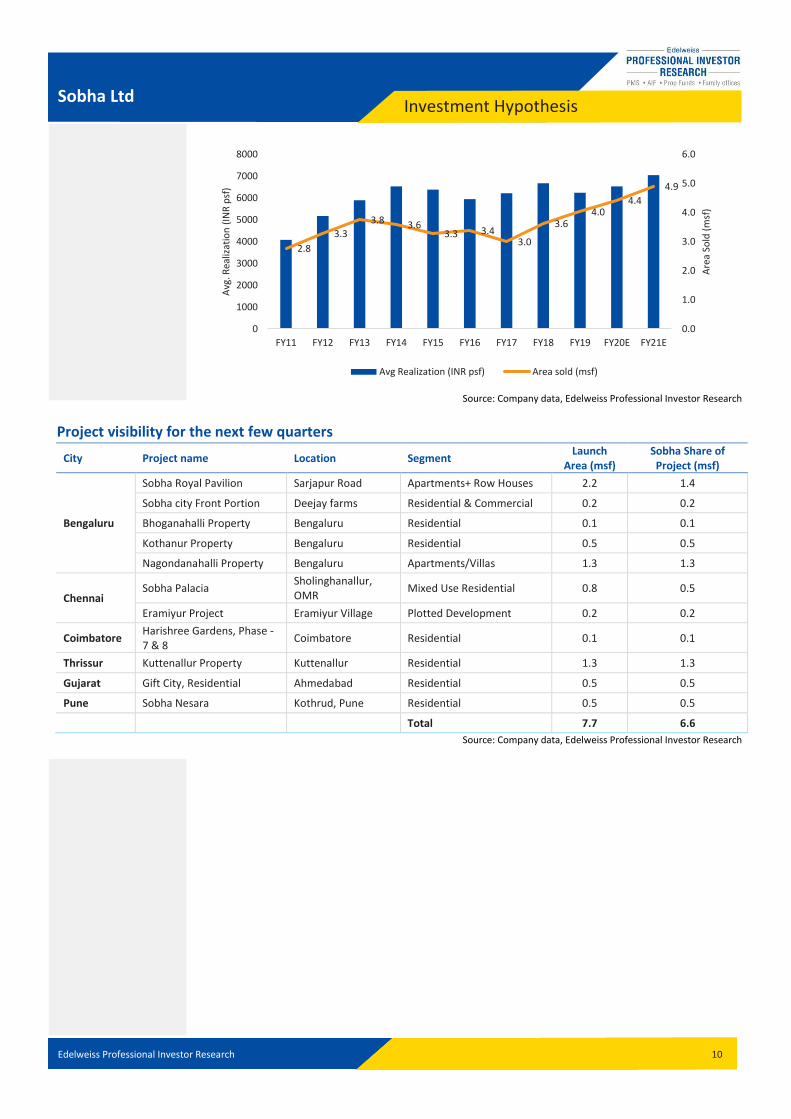

Sobha’s pre-sales improved from 3.0msf in FY17 to 4.0msf in FY19, with sales value of over INR

2,516crore in FY19, supported by stable sales in core market of Bengaluru and improving sales

momentum in Gurugram and Cochin. Sales in Cochin rebounded strongly after Q2FY19, where

Kerala had been severely affected by floods. The company recorded pre-sales of 1.1msf in Q4FY19

(+11% YoY) which was the highest ever quarterly sales achieved by the company.

Source: Company data, Edelweiss Professional Investor Research

The sales to launches ratio in 2018 touched the highest level since 2013 at 2.2, indicating aggressive

sales compared to launches. This, coupled with falling inventory (lowest since 2013), implies

aggressive launches ahead.

Source: Company data, Edelweiss Professional Investor Research

Sobha is planning to launch projects spanning ~8msf over the next few quarters. Bengaluru still

continues to be the focus area—contributing ~56% of new launches—followed by Thrissur and

Chennai, which will comprise 17% and 12% of launches, respectively. We expect these launches to

drive the company’s growth over the next few years and clock around 4.4msf and 4.9msf in FY20

and FY21, respectively. Also, we expect average realisation to start improving going ahead with

stablization in prices led by lower expected supply and sales recovery in Gurugram and Cochin.

470518

373

505563 593 611

656587 617 600

712

1.1

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0

100

200

300

400

500

600

700

800

900

1000

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Pre-sales have continued to be strong over the last several quarters

Sales (INR cr) Area sold (sf in millions)

Highest ever quarterly sales for the company

0.3

1.6

0.50.3

0.90.8

2.2

FY12 FY13 FY14 FY15 FY16 FY17 FY18

High ratio of sales to launches means aggressive project launches ahead

Sales to Launches (msf)

Edelweiss Professional Investor Research 10

Investment Hypothesis Sobha Ltd

Source: Company data, Edelweiss Professional Investor Research

Project visibility for the next few quarters

City Project name Location Segment Launch

Area (msf) Sobha Share of

Project (msf)

Bengaluru

Sobha Royal Pavilion Sarjapur Road Apartments+ Row Houses 2.2 1.4

Sobha city Front Portion Deejay farms Residential & Commercial 0.2 0.2

Bhoganahalli Property Bengaluru Residential 0.1 0.1

Kothanur Property Bengaluru Residential 0.5 0.5

Nagondanahalli Property Bengaluru Apartments/Villas 1.3 1.3

Chennai Sobha Palacia

Sholinghanallur, OMR

Mixed Use Residential 0.8 0.5

Eramiyur Project Eramiyur Village Plotted Development 0.2 0.2

Coimbatore Harishree Gardens, Phase - 7 & 8

Coimbatore Residential 0.1 0.1

Thrissur Kuttenallur Property Kuttenallur Residential 1.3 1.3

Gujarat Gift City, Residential Ahmedabad Residential 0.5 0.5

Pune Sobha Nesara Kothrud, Pune Residential 0.5 0.5

Total 7.7 6.6

Source: Company data, Edelweiss Professional Investor Research

2.8

3.3

3.8 3.63.3 3.4

3.0

3.64.0

4.4

4.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

1000

2000

3000

4000

5000

6000

7000

8000

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E FY21E

Are

a So

ld (

msf

)

Avg

. Rea

lizat

ion

(IN

R p

sf)

Avg Realization (INR psf) Area sold (msf)

Edelweiss Professional Investor Research 11

Investment Hypothesis Sobha Ltd

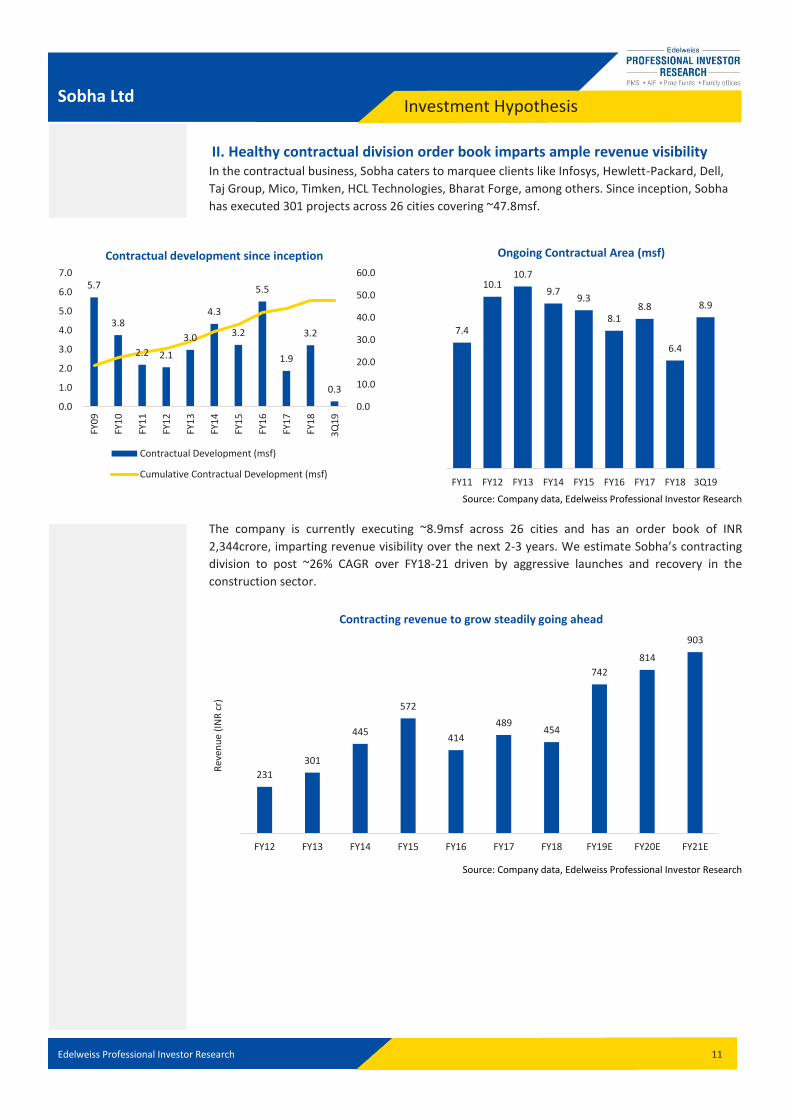

II. Healthy contractual division order book imparts ample revenue visibility In the contractual business, Sobha caters to marquee clients like Infosys, Hewlett-Packard, Dell,

Taj Group, Mico, Timken, HCL Technologies, Bharat Forge, among others. Since inception, Sobha

has executed 301 projects across 26 cities covering ~47.8msf.

Source: Company data, Edelweiss Professional Investor Research

The company is currently executing ~8.9msf across 26 cities and has an order book of INR

2,344crore, imparting revenue visibility over the next 2-3 years. We estimate Sobha’s contracting

division to post ~26% CAGR over FY18-21 driven by aggressive launches and recovery in the

construction sector.

Source: Company data, Edelweiss Professional Investor Research

5.7

3.8

2.2 2.1

3.0

4.3

3.2

5.5

1.9

3.2

0.3

0.0

10.0

20.0

30.0

40.0

50.0

60.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

3Q

19

Contractual development since inception

Contractual Development (msf)

Cumulative Contractual Development (msf)

7.4

10.110.7

9.79.3

8.18.8

6.4

8.9

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 3Q19

Ongoing Contractual Area (msf)

231

301

445

572

414

489454

742

814

903

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Rev

enu

e (I

NR

cr)

Contracting revenue to grow steadily going ahead

Edelweiss Professional Investor Research 12

Investment Hypothesis Sobha Ltd

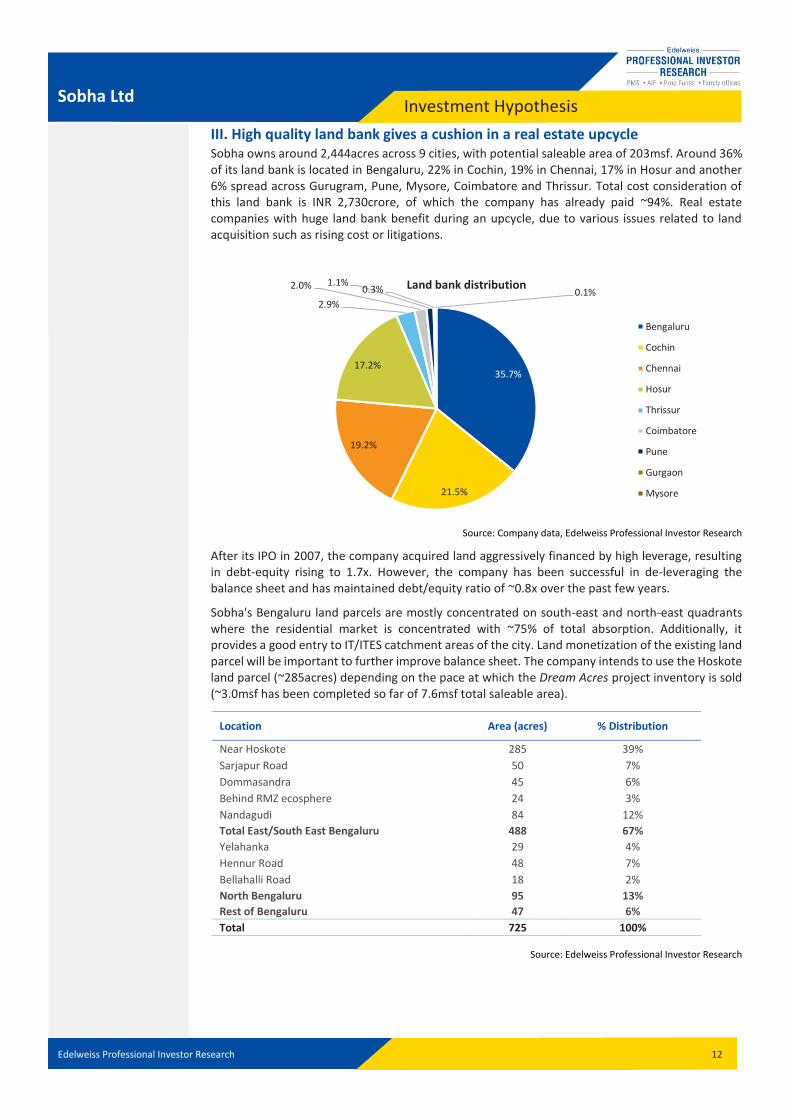

III. High quality land bank gives a cushion in a real estate upcycle Sobha owns around 2,444acres across 9 cities, with potential saleable area of 203msf. Around 36% of its land bank is located in Bengaluru, 22% in Cochin, 19% in Chennai, 17% in Hosur and another 6% spread across Gurugram, Pune, Mysore, Coimbatore and Thrissur. Total cost consideration of this land bank is INR 2,730crore, of which the company has already paid ~94%. Real estate companies with huge land bank benefit during an upcycle, due to various issues related to land acquisition such as rising cost or litigations.

Source: Company data, Edelweiss Professional Investor Research

After its IPO in 2007, the company acquired land aggressively financed by high leverage, resulting in debt-equity rising to 1.7x. However, the company has been successful in de-leveraging the balance sheet and has maintained debt/equity ratio of ~0.8x over the past few years.

Sobha's Bengaluru land parcels are mostly concentrated on south-east and north-east quadrants where the residential market is concentrated with ~75% of total absorption. Additionally, it provides a good entry to IT/ITES catchment areas of the city. Land monetization of the existing land parcel will be important to further improve balance sheet. The company intends to use the Hoskote land parcel (~285acres) depending on the pace at which the Dream Acres project inventory is sold (~3.0msf has been completed so far of 7.6msf total saleable area).

Source: Edelweiss Professional Investor Research

35.7%

21.5%

19.2%

17.2%

2.9%

2.0% 1.1%0.3% 0.1%

Land bank distribution

Bengaluru

Cochin

Chennai

Hosur

Thrissur

Coimbatore

Pune

Gurgaon

Mysore

Location Area (acres) % Distribution

Near Hoskote 285 39%

Sarjapur Road 50 7%

Dommasandra 45 6%

Behind RMZ ecosphere 24 3%

Nandagudi 84 12%

Total East/South East Bengaluru 488 67%

Yelahanka 29 4%

Hennur Road 48 7%

Bellahalli Road 18 2%

North Bengaluru 95 13%

Rest of Bengaluru 47 6%

Total 725 100%

Edelweiss Professional Investor Research 13

Investment Hypothesis Sobha Ltd

Key Risks Regional concentration: While Sobha is actively trying to diversify its regional exposure,

Bengaluru still accounts for ~50% of the ongoing projects portfolio. Weakness in this market

can dent the company’s prospects.

Macroeconomic factors: Demand in the real estate sector is correlated to economic activity

and a slowdown in the economy can hamper the ongoing recovery.

Interest rate risk: The real estate sector is interest rate sensitive and any delay in rate cuts or

rise in interest rates could negatively impact sales volume.

Regulatory risk: The company is executing a large number of real estate projects in new

geographies. Any delay in securing regulatory approvals could negatively impact project

delivery, which in turn will push up project costs and hit profitability.

Edelweiss Professional Investor Research

Outlook and Valuations Sobha Ltd

14

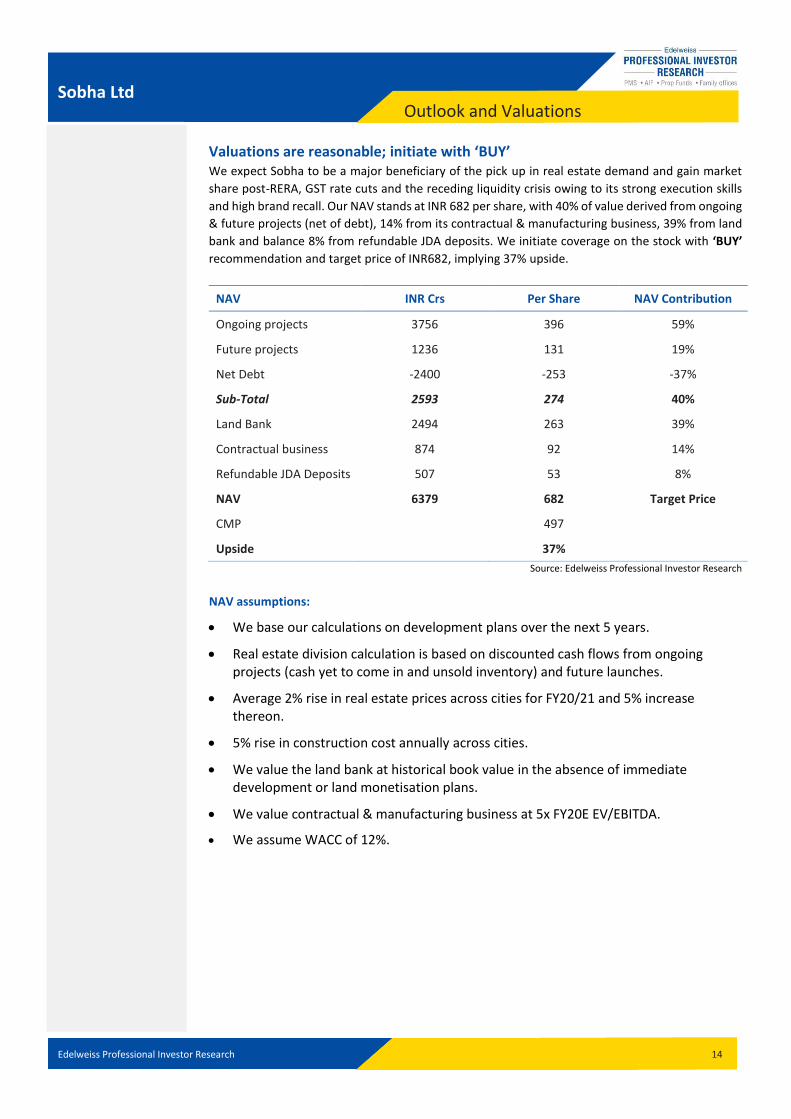

Valuations are reasonable; initiate with ‘BUY’ We expect Sobha to be a major beneficiary of the pick up in real estate demand and gain market

share post-RERA, GST rate cuts and the receding liquidity crisis owing to its strong execution skills

and high brand recall. Our NAV stands at INR 682 per share, with 40% of value derived from ongoing

& future projects (net of debt), 14% from its contractual & manufacturing business, 39% from land

bank and balance 8% from refundable JDA deposits. We initiate coverage on the stock with ‘BUY’

recommendation and target price of INR682, implying 37% upside.

NAV INR Crs Per Share NAV Contribution

Ongoing projects 3756 396 59%

Future projects 1236 131 19%

Net Debt -2400 -253 -37%

Sub-Total 2593 274 40%

Land Bank 2494 263 39%

Contractual business 874 92 14%

Refundable JDA Deposits 507 53 8%

NAV 6379 682 Target Price

CMP 497

Upside 37%

Source: Edelweiss Professional Investor Research

NAV assumptions:

We base our calculations on development plans over the next 5 years.

Real estate division calculation is based on discounted cash flows from ongoing projects (cash yet to come in and unsold inventory) and future launches.

Average 2% rise in real estate prices across cities for FY20/21 and 5% increase thereon.

5% rise in construction cost annually across cities.

We value the land bank at historical book value in the absence of immediate development or land monetisation plans.

We value contractual & manufacturing business at 5x FY20E EV/EBITDA.

We assume WACC of 12%.

Edelweiss Professional Investor Research

Peer Comparison Sobha Ltd

15

Source: Edelweiss Professional Investor Research

Source: Edelweiss Professional Investor Research

Source: Edelweiss Professional Investor Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19

Quarterly Sales Trend - Volume terms (in msf)

Sobha Ltd Brigade Enterprises Prestige Estates Godrej Properties Oberoi Realty

0

200

400

600

800

1000

1200

1400

1600

1800

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19

Quarterly Sales Trend - Value terms (INR cr)

Sobha Ltd Brigade Enterprises Prestige Estates Godrej Properties Oberoi Realty

0

5000

10000

15000

20000

25000

30000

35000

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19

Average Sales Realization (INR psf)

Sobha Ltd Brigade Enterprises Prestige Estates Godrej Properties Oberoi Realty

Edelweiss Professional Investor Research

Peer Comparison Sobha Ltd

16

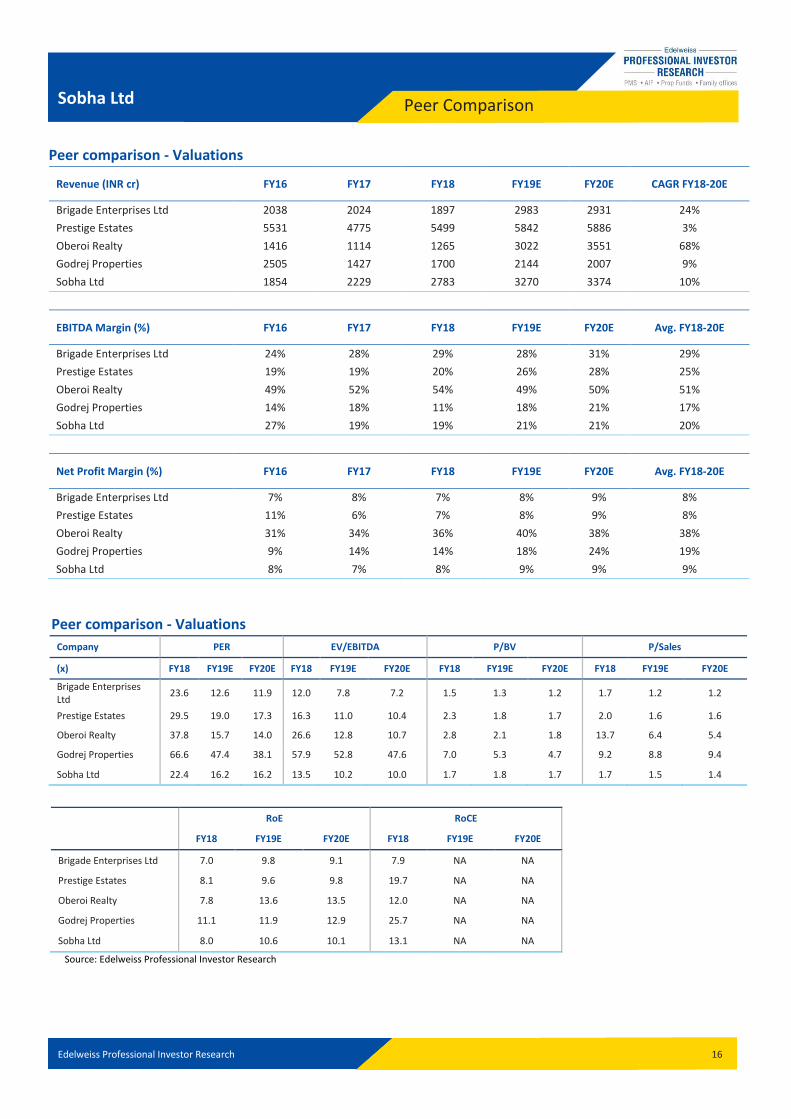

Peer comparison - Valuations

Revenue (INR cr) FY16 FY17 FY18 FY19E FY20E CAGR FY18-20E

Brigade Enterprises Ltd 2038 2024 1897 2983 2931 24%

Prestige Estates 5531 4775 5499 5842 5886 3%

Oberoi Realty 1416 1114 1265 3022 3551 68%

Godrej Properties 2505 1427 1700 2144 2007 9%

Sobha Ltd 1854 2229 2783 3270 3374 10%

EBITDA Margin (%) FY16 FY17 FY18 FY19E FY20E Avg. FY18-20E

Brigade Enterprises Ltd 24% 28% 29% 28% 31% 29%

Prestige Estates 19% 19% 20% 26% 28% 25%

Oberoi Realty 49% 52% 54% 49% 50% 51%

Godrej Properties 14% 18% 11% 18% 21% 17%

Sobha Ltd 27% 19% 19% 21% 21% 20%

Net Profit Margin (%) FY16 FY17 FY18 FY19E FY20E Avg. FY18-20E

Brigade Enterprises Ltd 7% 8% 7% 8% 9% 8%

Prestige Estates 11% 6% 7% 8% 9% 8%

Oberoi Realty 31% 34% 36% 40% 38% 38%

Godrej Properties 9% 14% 14% 18% 24% 19%

Sobha Ltd 8% 7% 8% 9% 9% 9%

Peer comparison - Valuations

Company PER EV/EBITDA P/BV P/Sales

(x) FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E

Brigade Enterprises Ltd

23.6 12.6 11.9 12.0 7.8 7.2 1.5 1.3 1.2 1.7 1.2 1.2

Prestige Estates 29.5 19.0 17.3 16.3 11.0 10.4 2.3 1.8 1.7 2.0 1.6 1.6

Oberoi Realty 37.8 15.7 14.0 26.6 12.8 10.7 2.8 2.1 1.8 13.7 6.4 5.4

Godrej Properties 66.6 47.4 38.1 57.9 52.8 47.6 7.0 5.3 4.7 9.2 8.8 9.4

Sobha Ltd 22.4 16.2 16.2 13.5 10.2 10.0 1.7 1.8 1.7 1.7 1.5 1.4

RoE RoCE

FY18 FY19E FY20E FY18 FY19E FY20E

Brigade Enterprises Ltd 7.0 9.8 9.1 7.9 NA NA

Prestige Estates 8.1 9.6 9.8 19.7 NA NA

Oberoi Realty 7.8 13.6 13.5 12.0 NA NA

Godrej Properties 11.1 11.9 12.9 25.7 NA NA

Sobha Ltd 8.0 10.6 10.1 13.1 NA NA

Source: Edelweiss Professional Investor Research

Edelweiss Professional Investor Research 17

Case Scenarios Sobha Ltd

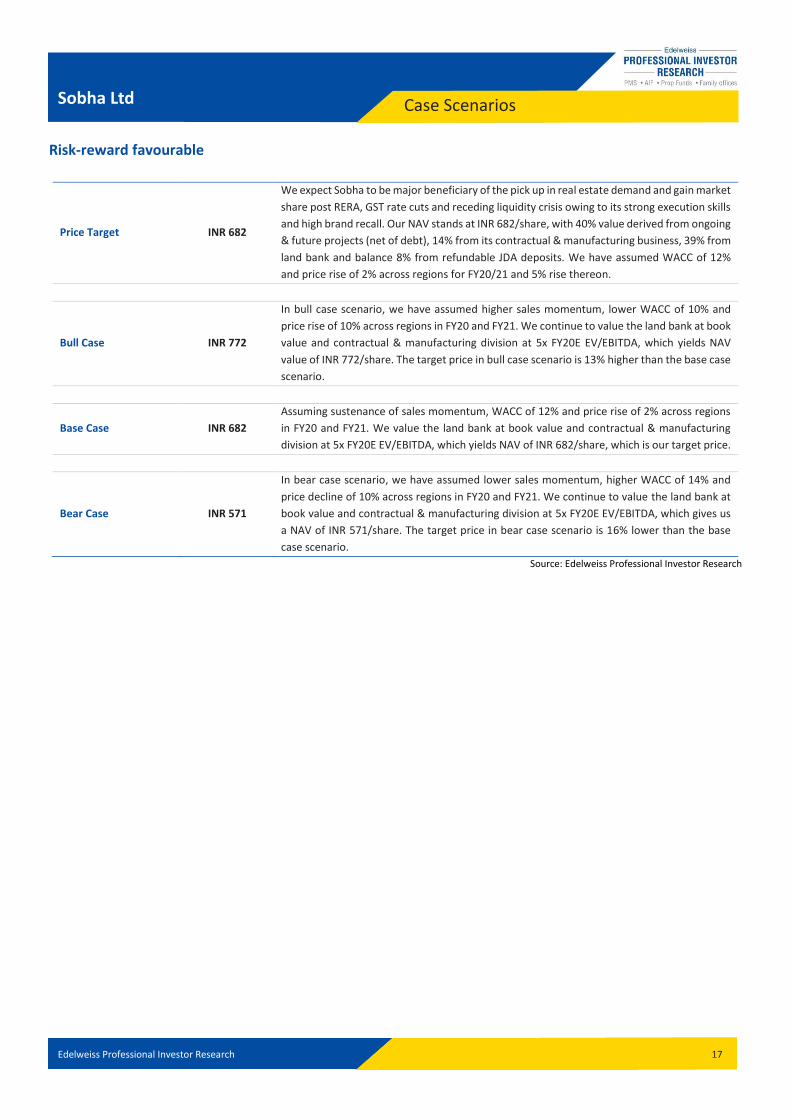

Risk-reward favourable

Price Target INR 682

We expect Sobha to be major beneficiary of the pick up in real estate demand and gain market

share post RERA, GST rate cuts and receding liquidity crisis owing to its strong execution skills

and high brand recall. Our NAV stands at INR 682/share, with 40% value derived from ongoing

& future projects (net of debt), 14% from its contractual & manufacturing business, 39% from

land bank and balance 8% from refundable JDA deposits. We have assumed WACC of 12%

and price rise of 2% across regions for FY20/21 and 5% rise thereon.

Bull Case INR 772

In bull case scenario, we have assumed higher sales momentum, lower WACC of 10% and

price rise of 10% across regions in FY20 and FY21. We continue to value the land bank at book

value and contractual & manufacturing division at 5x FY20E EV/EBITDA, which yields NAV

value of INR 772/share. The target price in bull case scenario is 13% higher than the base case

scenario.

Base Case INR 682

Assuming sustenance of sales momentum, WACC of 12% and price rise of 2% across regions

in FY20 and FY21. We value the land bank at book value and contractual & manufacturing

division at 5x FY20E EV/EBITDA, which yields NAV of INR 682/share, which is our target price.

Bear Case INR 571

In bear case scenario, we have assumed lower sales momentum, higher WACC of 14% and

price decline of 10% across regions in FY20 and FY21. We continue to value the land bank at

book value and contractual & manufacturing division at 5x FY20E EV/EBITDA, which gives us

a NAV of INR 571/share. The target price in bear case scenario is 16% lower than the base

case scenario.

Source: Edelweiss Professional Investor Research

Edelweiss Professional Investor Research

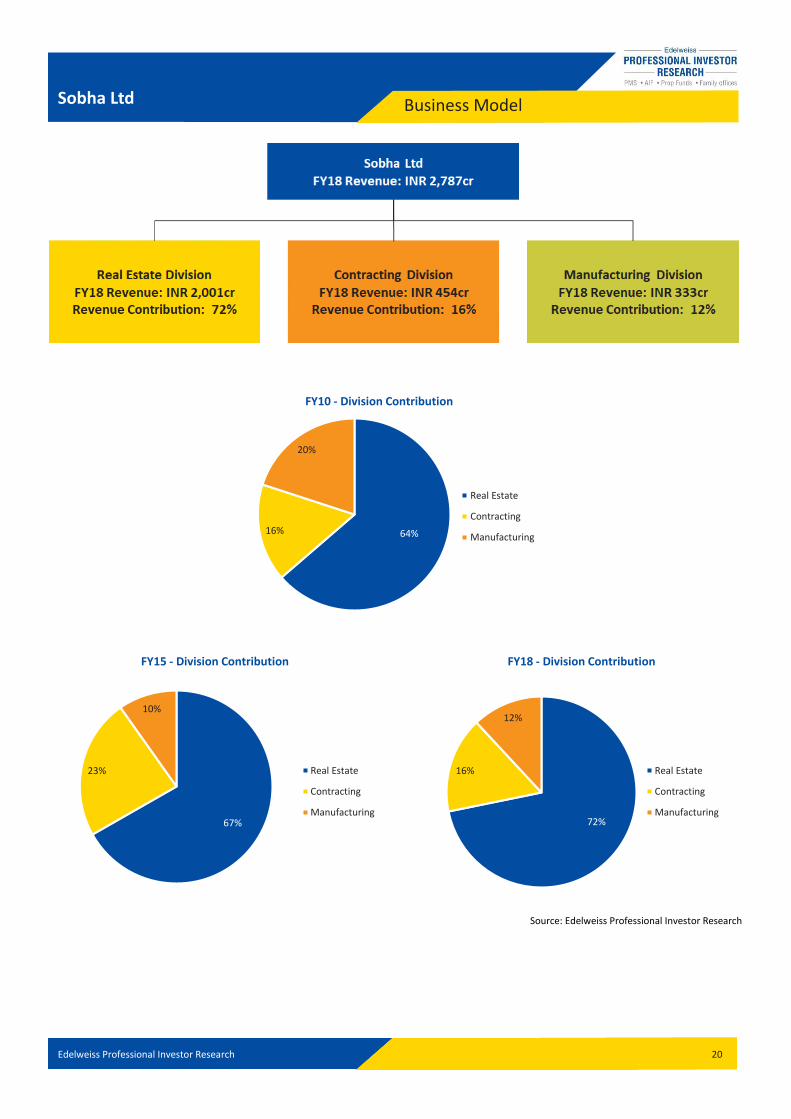

Business Model Sobha Ltd

18

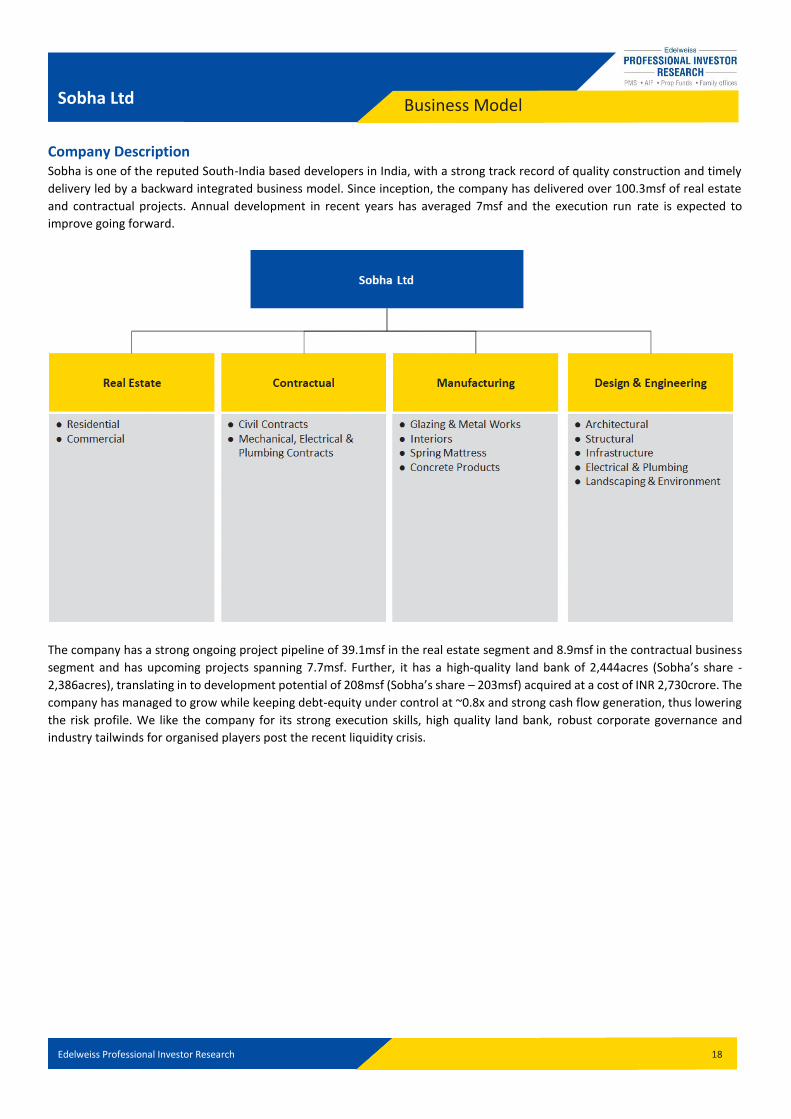

Company Description Sobha is one of the reputed South-India based developers in India, with a strong track record of quality construction and timely

delivery led by a backward integrated business model. Since inception, the company has delivered over 100.3msf of real estate

and contractual projects. Annual development in recent years has averaged 7msf and the execution run rate is expected to

improve going forward.

The company has a strong ongoing project pipeline of 39.1msf in the real estate segment and 8.9msf in the contractual business

segment and has upcoming projects spanning 7.7msf. Further, it has a high-quality land bank of 2,444acres (Sobha’s share -

2,386acres), translating in to development potential of 208msf (Sobha’s share – 203msf) acquired at a cost of INR 2,730crore. The

company has managed to grow while keeping debt-equity under control at ~0.8x and strong cash flow generation, thus lowering

the risk profile. We like the company for its strong execution skills, high quality land bank, robust corporate governance and

industry tailwinds for organised players post the recent liquidity crisis.

Edelweiss Professional Investor Research

Business Model Sobha Ltd

19

Business Model

Sobha is purely in to residential development with primary focus on the Bengaluru market. The company has a unique backward integrated model with presence of key competencies and in-house resources to deliver a project from conceptualization to completion. Backward integration includes an architectural and design studio for a team of qualified architects, concrete block making plant, metal & glazing factory, interiors & wood working factory, mechanical, electrical & plumbing division, and project implementation team. Backward integration ensures projects meet high quality standards and delivered in a timely manner. Unlike some of its peers, which have developed a rental portfolio or ventured in to the hospitality business, Sobha has continued to focus solely on development projects.

Strategic Positioning

Sobha’s backward integrated model has helped deliver projects in timely manner, maintain high quality and command a premium over peers. The company is now actively diversifying operations to regions other than Bengaluru to reduce regional concentration. Also, management maintains that it will continue to focus on core operation i.e., residential development, and not venture in rental/hospitality segment in the near term.

Competitive Edge The only backward integrated player in India with clear focus on residential development has helped Sobha build a strong brand. Huge land bank purchased at legacy prices gives an advantage in a real estate upcycle.

Financial Structure The company has managed to maintain healthy balance sheet with debt/equity of 0.8x despite tough times in the sector over the past few years and is expected to dip further to 0.6x by FY21E. Also, land monetization will be key monitorable for any further deleveraging.

Key Competitors Brigade Enterprises, Prestige Estates, Godrej Properties, Puravankara, etc.

Industry Revenue Drivers Policy announcements by the government in the recent Budget, GST rate cuts, economic recovery, healthy job growth environment and low interest rate to boost real estate demand.

Shareholder Value Proposition

We initiate coverage on the stock with ‘BUY’ and target price of INR 682, implying 37% upside. We believe the company is the best play on real estate recovery across regions, robust demand in Bengaluru and a key beneficiary of sector consolidation after RERA and the recent liquidity crisis.

Edelweiss Professional Investor Research

Business Model Sobha Ltd

20

Source: Edelweiss Professional Investor Research

64%16%

20%

FY10 - Division Contribution

Real Estate

Contracting

Manufacturing

67%

23%

10%

FY15 - Division Contribution

Real Estate

Contracting

Manufacturing72%

16%

12%

FY18 - Division Contribution

Real Estate

Contracting

Manufacturing

Edelweiss Professional Investor Research 21

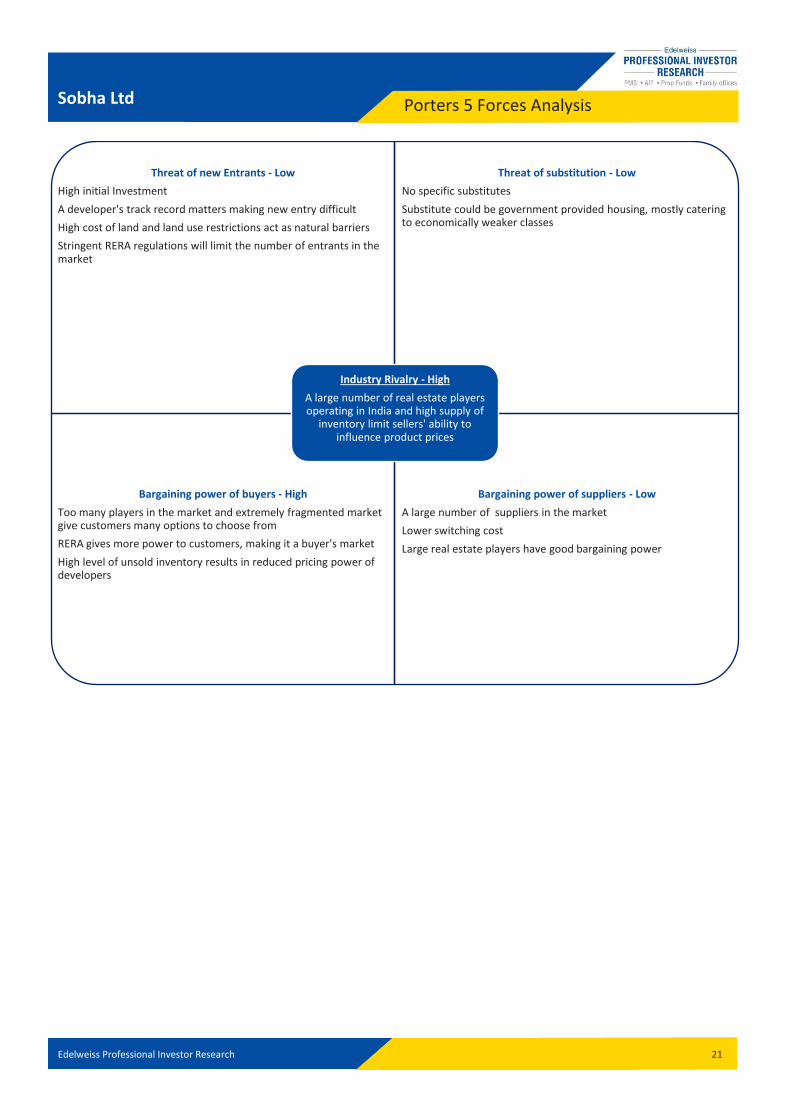

Porters 5 Forces Analysis Sobha Ltd

Threat of new Entrants - Low

High initial Investment

A developer's track record matters making new entry difficult

High cost of land and land use restrictions act as natural barriers

Stringent RERA regulations will limit the number of entrants in the market

Threat of substitution - Low

No specific substitutes

Substitute could be government provided housing, mostly catering to economically weaker classes

Bargaining power of buyers - High

Too many players in the market and extremely fragmented market give customers many options to choose from

RERA gives more power to customers, making it a buyer's market

High level of unsold inventory results in reduced pricing power of developers

Bargaining power of suppliers - Low

A large number of suppliers in the market

Lower switching cost

Large real estate players have good bargaining power

Industry Rivalry - High

A large number of real estate players operating in India and high supply of

inventory limit sellers' ability to influence product prices

Edelweiss Professional Investor Research

Management Profile Sobha Ltd

22

Name Designation Profile

Mr. P.N.C. Menon Chairman Emeritus

Mr. P.N.C. Menon is the founder of Sobha Group of companies. A first generation entrepreneur, Mr. Menon began his professional career by setting up an interior decoration firm in the Sultanate of Oman in 1976. He has since incorporated several companies in the Sultanate of Oman, United Arab Emirates and Qatar, and also expanded in construction and real estate development. He founded Sobha Developers in Bengaluru in 1995.

Mr. Ravi Menon Chairman

As part of the succession plan in June 2012, Mr. Ravi Menon was appointed as the Chairman of Sobha. Soon after his graduation in Civil Engineering with distinction from Purdue University, US, he joined the company in 2004. Subsequent to joining the organization, he has handled Project Execution, Quality, Technology, Process & IT, Customer Relationship Management, Engineering & Design and many other facets of the business. He played a key role in the successful integration of pre-cast technology in construction methodology.

Mr. J.C. Sharma Vice Chairman & Managing Director

Mr. J.C. Sharma has a bachelor’s degree in Commerce (Hons.) from Xavier College, Calcutta. He is a qualified chartered accountant and company secretary with over 25 years of experience in diversified industries such as automobiles, textiles, steel and real estate in the areas of finance and management. He has previously served as General Manager, Auto Distributors; General Manager - Finance, Bhoruka Steels; and General Manager- Commerce and Finance, Grasim Industries. Mr. Sharma has been associated with Sobha since June 2001 and is entrusted with the responsibility of managing the overall affairs of the company, especially finances, land acquisition and legal functions.

Dr. S.K. Gupta Independent Director

Dr. S.K. Gupta is an Independent Director. He is a Metallurgical Engineer with a Ph.D. (Tech.) and D.Sc. (Tech.) from Moscow. He has over 59 years of experience in metallurgy, engineering and management in the steel and allied domain. He has been associated with several reputed organisations such as Jindal Saw, JSW Steel, Rourkela Steel Plant/Steel Authority of India and Mishra Dhatu Nigam (Ministry of Defence), Metallurgical and Engineering Consultants (Mecon) in varied capacities.

Dr. Punita Kumar - Sinha Independent Director

Dr. Punita Kumar-Sinha is an Independent Director of the company. She has a career spanning over 28 years focused on investment management. She is the founder of Pacific Paradigm Advisors (PPA), an independent investment advisory and management firm focused on Asia. She is also a Senior Advisor and serves as an Independent Director on boards of public and private companies in India. Prior to PPA, she was a Senior Managing Director at the Blackstone Group, leading Blackstone Asia Advisors and serving as the CIO for The India Fund (the largest India Fund in the US for almost 15 years), The Asia Tigers Fund and The Asia Opportunities Fund.

Mr. R V S Rao Independent Director

Mr. R.V.S. Rao is an Independent Director of the company. He holds a bachelor’s degree in Commerce from the University of Mysore and a bachelor’s degree in law from Bengaluru University. He is a fellow member of the Indian Institute of Banking and Finance. Mr. Rao has over 46 years of experience in banking and finance. He has served on the board of the Housing Development Finance Corporation. As a United States Agency for International Development (USAID) Consultant, he was the team leader that reviewed operations and made recommendations for the Housing Finance Company, Ghana, Africa.

Mr. Anup Shah Independent Director

Mr. Anup Shah is an Independent Director of the company. He has a bachelor’s degree in commerce from HR College, Mumbai, and a degree in law from Government Law College, Mumbai. He has over 34 years of experience in the field of law, specifically real estate law. Since founding his own firm in 1993, he has advised developers, builders and foreign and domestic investors in structuring real estate transactions, leases, development agreements and joint ventures.

Edelweiss Professional Investor Research 23

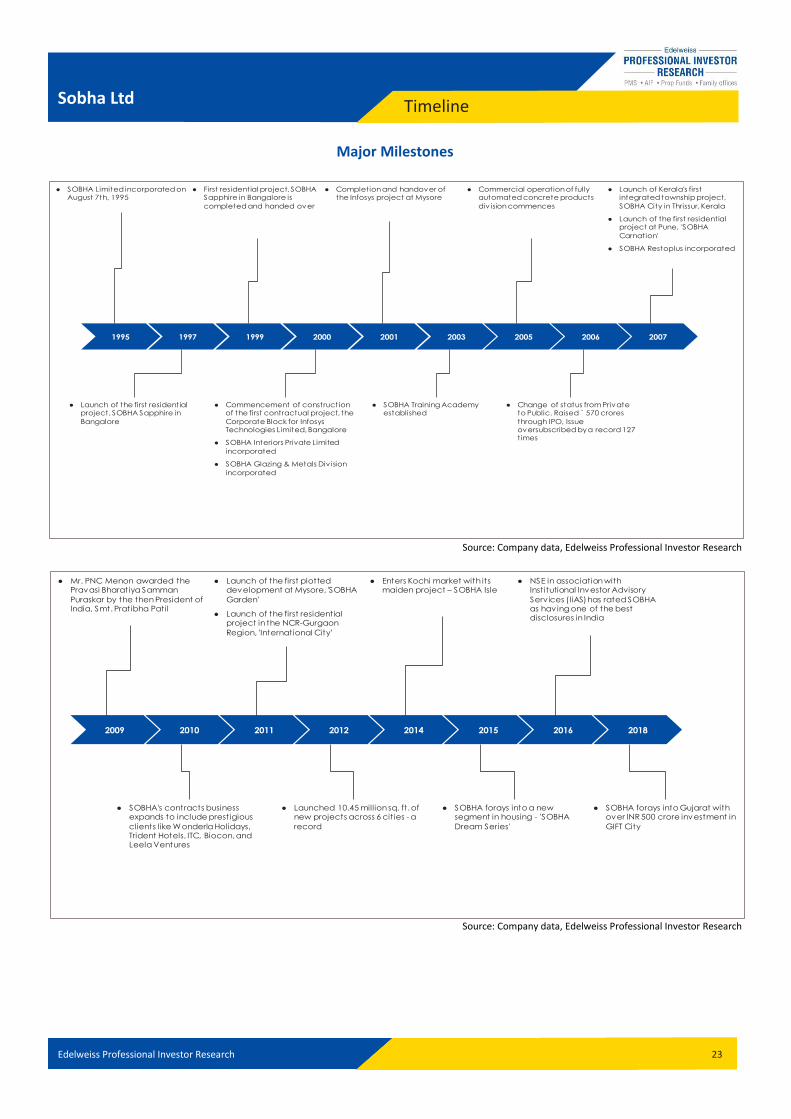

Timeline Sobha Ltd

Major Milestones

Source: Company data, Edelweiss Professional Investor Research

Source: Company data, Edelweiss Professional Investor Research

1995 1997 1999 2000 2001 2003 2005 2006 2007

● SOBHA Limited incorporated on August 7th, 1995

● Launch of the first residential project, SOBHA Sapphire in

Bangalore

● First residential project, SOBHA Sapphire in Bangalore is

completed and handed over

● Commencement of construction of the first contractual project, the

Corporate Block for Infosys Technologies Limited, Bangalore

● SOBHA Interiors Private Limited

incorporated

● SOBHA Glazing & Metals Div ision

incorporated

● Completion and handover of the Infosys project at Mysore

● SOBHA Training Academy established

● Commercial operation of fully automated concrete products

div ision commences

● Change of status from Private to Public. Raised ` 570 crores

through IPO, Issue oversubscribed by a record 127 times

● Launch of Kerala's first integrated township project,

SOBHA City in Thrissur, Kerala

● Launch of the first residential project at Pune, 'SOBHA

Carnation'

● SOBHA Restoplus incorporated

2009 2010 2011 2012 2014 2015 2016 2018

● Mr. PNC Menon awarded the Pravasi Bharatiya Samman

Puraskar by the then President of India, Smt. Pratibha Patil

● SOBHA's contracts business expands to include prestigious

clients like Wonderla Holidays, Trident Hotels, ITC, Biocon, and Leela Ventures

● Launch of the first plotted development at Mysore, 'SOBHA

Garden'

● Launch of the first residential project in the NCR-Gurgaon

Region, 'International City’

● Launched 10.45 million sq. ft. of new projects across 6 cities - a

record

● Enters Kochi market with its maiden project – SOBHA Isle

● SOBHA forays into a new segment in housing - 'SOBHA

Dream Series'

● NSE in association with Institutional Investor Advisory

Serv ices (IiAS) has rated SOBHA as having one of the best disclosures in India

● SOBHA forays into Gujarat with over INR 500 crore investment in

GIFT City

Edelweiss Professional Investor Research 24

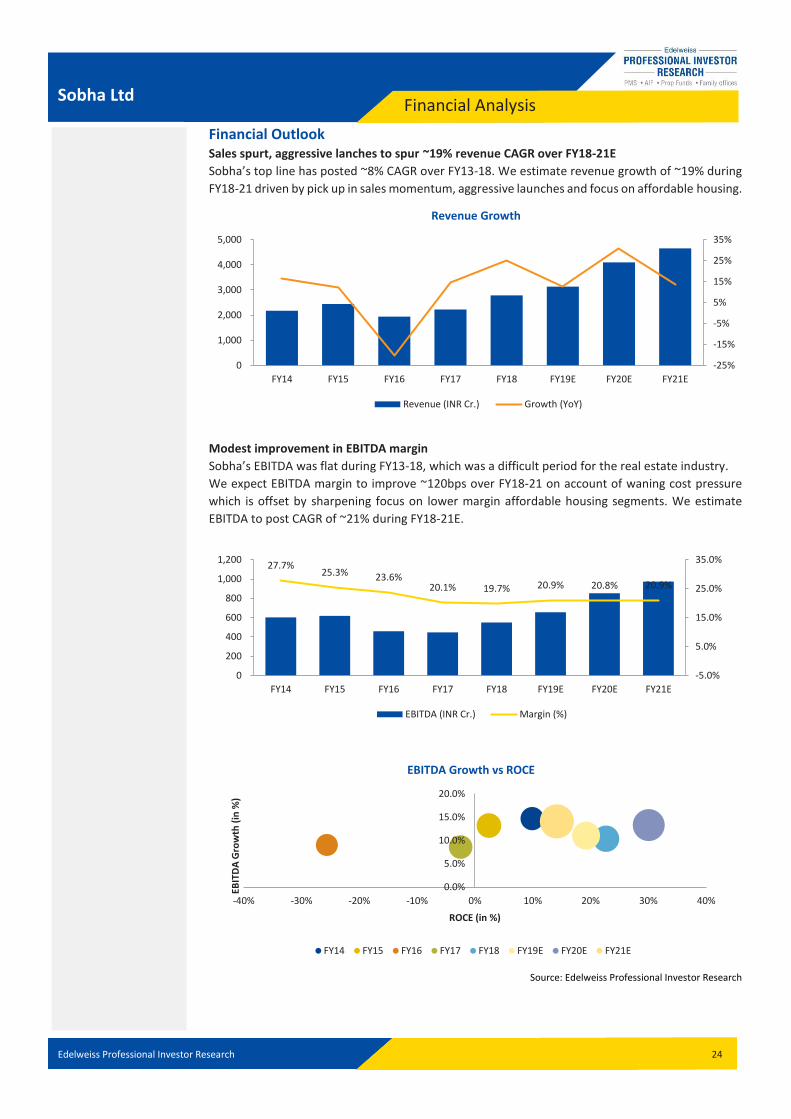

Financial Analysis Sobha Ltd

Financial Outlook Sales spurt, aggressive lanches to spur ~19% revenue CAGR over FY18-21E

Sobha’s top line has posted ~8% CAGR over FY13-18. We estimate revenue growth of ~19% during

FY18-21 driven by pick up in sales momentum, aggressive launches and focus on affordable housing.

Modest improvement in EBITDA margin

Sobha’s EBITDA was flat during FY13-18, which was a difficult period for the real estate industry.

We expect EBITDA margin to improve ~120bps over FY18-21 on account of waning cost pressure

which is offset by sharpening focus on lower margin affordable housing segments. We estimate

EBITDA to post CAGR of ~21% during FY18-21E.

Source: Edelweiss Professional Investor Research

-25%

-15%

-5%

5%

15%

25%

35%

0

1,000

2,000

3,000

4,000

5,000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Revenue Growth

Revenue (INR Cr.) Growth (YoY)

27.7%25.3% 23.6%

20.1% 19.7% 20.9% 20.8% 20.9%

-5.0%

5.0%

15.0%

25.0%

35.0%

0

200

400

600

800

1,000

1,200

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

EBITDA (INR Cr.) Margin (%)

0.0%

5.0%

10.0%

15.0%

20.0%

-40% -30% -20% -10% 0% 10% 20% 30% 40%

EBIT

DA

Gro

wth

(in

%)

ROCE (in %)

EBITDA Growth vs ROCE

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Edelweiss Professional Investor Research 25

Financial Analysis Sobha Ltd

PAT to post 23% CAGR over FY18-21

The company’s PAT growth was flat during the FY13-18. However, with robust top-line growth

underpinned by strong sales momentum and marginal EBITDA margin expansion, we estimate PAT

to post 23% CAGR over FY18-21.

Debt to dip going forward

Management’s focus on generating cash flows has bolstered Sobha’s growth, maintaining its

gearing ratio at around 0.8x since FY16, well below the industry average of ~1.3x. Sobha’s net

operational cash flow, after financial outflow, has catapulted from INR10cr in FY15 to INR375cr in

FY18. We estimate the company’s debt/equity to improve to 0.7x by FY21E.

Net Cash Flow after Financial Outflow

Source: Edelweiss Professional Investor Research

8.2%1.2%

-42.0%

16.5%

34.9%

14.4%

38.9%

16.7%

-50.0%

-30.0%

-10.0%

10.0%

30.0%

50.0%

0

50

100

150

200

250

300

350

400

450

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

PAT (INR Cr.) Growth (YoY)

0.0

0.2

0.4

0.6

0.8

1.0

0

500

1000

1500

2000

2500

3000

FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Debt/Equity

Borrowings (INR Cr.) Debt/Equity (x)

199.6

367.3

10.2

155.3

299.8

374.6

FY13 FY14 FY15 FY16 FY17 FY18

(IN

R c

r)

Edelweiss Professional Investor Research 26

Financial Analysis Sobha Ltd

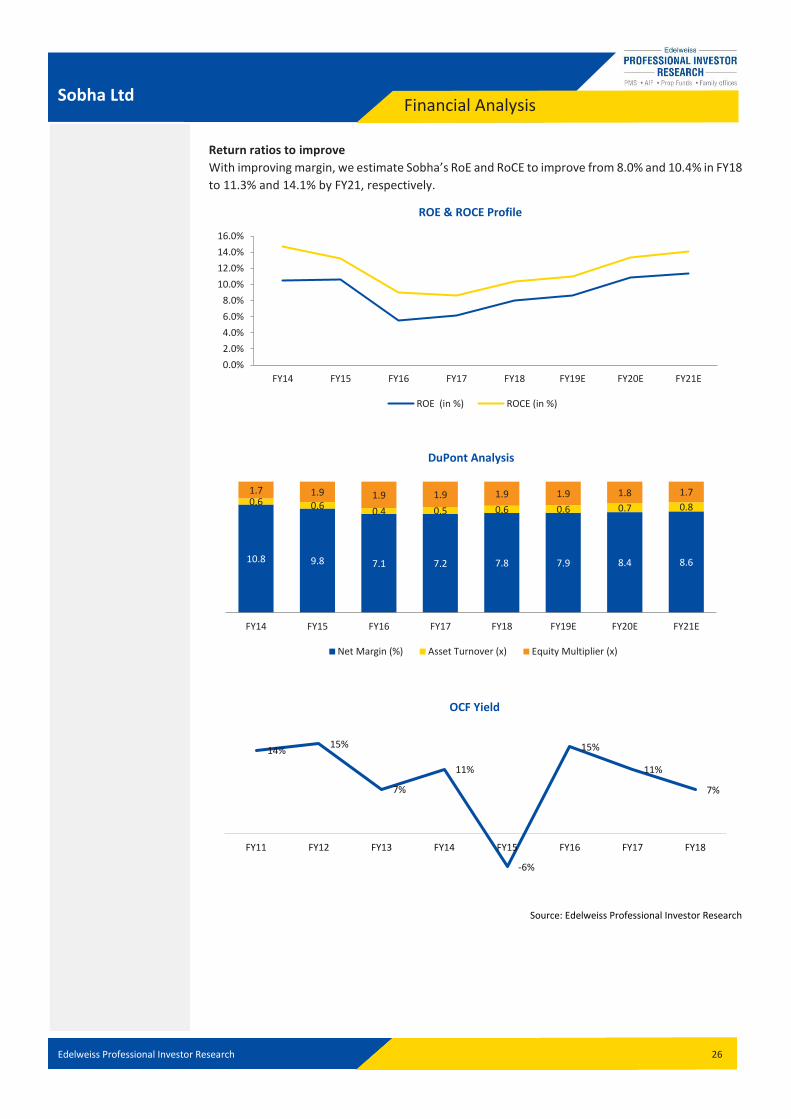

Return ratios to improve

With improving margin, we estimate Sobha’s RoE and RoCE to improve from 8.0% and 10.4% in FY18

to 11.3% and 14.1% by FY21, respectively.

Source: Edelweiss Professional Investor Research

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

ROE & ROCE Profile

ROE (in %) ROCE (in %)

10.8 9.8 7.1 7.2 7.8 7.9 8.4 8.6

0.6 0.60.4 0.5 0.6 0.6 0.7 0.8

1.7 1.9 1.9 1.9 1.9 1.9 1.8 1.7

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

DuPont Analysis

Net Margin (%) Asset Turnover (x) Equity Multiplier (x)

14%15%

7%

11%

-6%

15%

11%

7%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

OCF Yield

Edelweiss Professional Investor Research 27

Financials Sobha Ltd

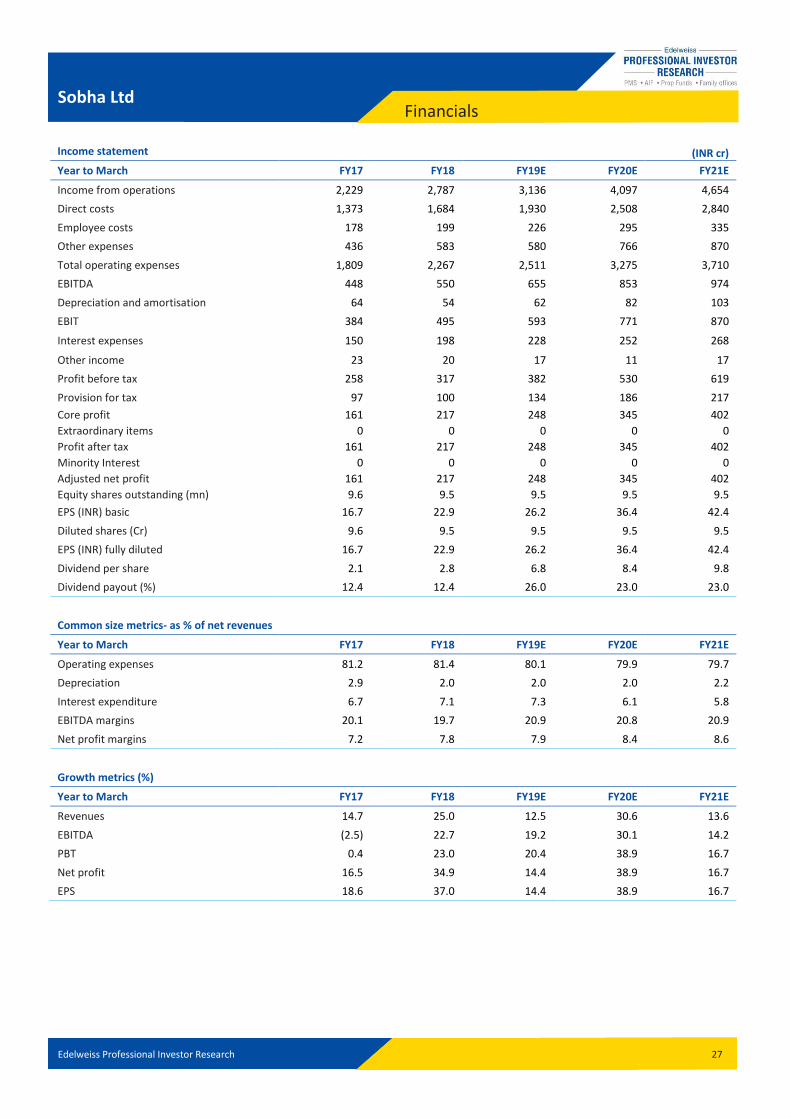

Income statement (INR cr)

Year to March FY17 FY18 FY19E FY20E FY21E

Income from operations 2,229 2,787 3,136 4,097 4,654

Direct costs 1,373 1,684 1,930 2,508 2,840

Employee costs 178 199 226 295 335

Other expenses 436 583 580 766 870

Total operating expenses 1,809 2,267 2,511 3,275 3,710

EBITDA 448 550 655 853 974

Depreciation and amortisation 64 54 62 82 103

EBIT 384 495 593 771 870

Interest expenses 150 198 228 252 268

Other income 23 20 17 11 17

Profit before tax 258 317 382 530 619

Provision for tax 97 100 134 186 217

Core profit 161 217 248 345 402

Extraordinary items 0 0 0 0 0

Profit after tax 161 217 248 345 402

Minority Interest 0 0 0 0 0

Adjusted net profit 161 217 248 345 402

Equity shares outstanding (mn) 9.6 9.5 9.5 9.5 9.5

EPS (INR) basic 16.7 22.9 26.2 36.4 42.4

Diluted shares (Cr) 9.6 9.5 9.5 9.5 9.5

EPS (INR) fully diluted 16.7 22.9 26.2 36.4 42.4

Dividend per share 2.1 2.8 6.8 8.4 9.8

Dividend payout (%) 12.4 12.4 26.0 23.0 23.0

Common size metrics- as % of net revenues

Year to March FY17 FY18 FY19E FY20E FY21E

Operating expenses 81.2 81.4 80.1 79.9 79.7

Depreciation 2.9 2.0 2.0 2.0 2.2

Interest expenditure 6.7 7.1 7.3 6.1 5.8

EBITDA margins 20.1 19.7 20.9 20.8 20.9

Net profit margins 7.2 7.8 7.9 8.4 8.6

Growth metrics (%)

Year to March FY17 FY18 FY19E FY20E FY21E

Revenues 14.7 25.0 12.5 30.6 13.6

EBITDA (2.5) 22.7 19.2 30.1 14.2

PBT 0.4 23.0 20.4 38.9 16.7

Net profit 16.5 34.9 14.4 38.9 16.7

EPS 18.6 37.0 14.4 38.9 16.7

Edelweiss Professional Investor Research 28

Financials Sobha Ltd

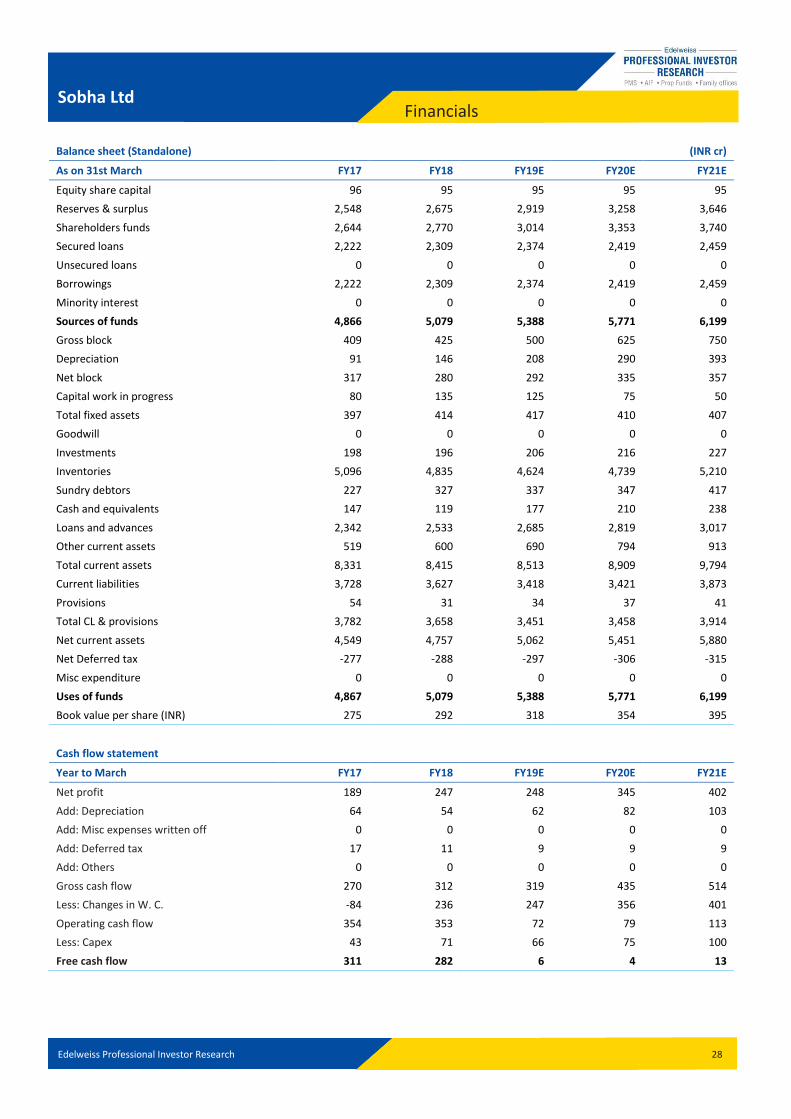

Balance sheet (Standalone) (INR cr)

As on 31st March FY17 FY18 FY19E FY20E FY21E

Equity share capital 96 95 95 95 95

Reserves & surplus 2,548 2,675 2,919 3,258 3,646

Shareholders funds 2,644 2,770 3,014 3,353 3,740

Secured loans 2,222 2,309 2,374 2,419 2,459

Unsecured loans 0 0 0 0 0

Borrowings 2,222 2,309 2,374 2,419 2,459

Minority interest 0 0 0 0 0

Sources of funds 4,866 5,079 5,388 5,771 6,199

Gross block 409 425 500 625 750

Depreciation 91 146 208 290 393

Net block 317 280 292 335 357

Capital work in progress 80 135 125 75 50

Total fixed assets 397 414 417 410 407

Goodwill 0 0 0 0 0

Investments 198 196 206 216 227

Inventories 5,096 4,835 4,624 4,739 5,210

Sundry debtors 227 327 337 347 417

Cash and equivalents 147 119 177 210 238

Loans and advances 2,342 2,533 2,685 2,819 3,017

Other current assets 519 600 690 794 913

Total current assets 8,331 8,415 8,513 8,909 9,794

Current liabilities 3,728 3,627 3,418 3,421 3,873

Provisions 54 31 34 37 41

Total CL & provisions 3,782 3,658 3,451 3,458 3,914

Net current assets 4,549 4,757 5,062 5,451 5,880

Net Deferred tax -277 -288 -297 -306 -315

Misc expenditure 0 0 0 0 0

Uses of funds 4,867 5,079 5,388 5,771 6,199

Book value per share (INR) 275 292 318 354 395

-0 0 0 0 0

Cash flow statement

Year to March FY17 FY18 FY19E FY20E FY21E

Net profit 189 247 248 345 402

Add: Depreciation 64 54 62 82 103

Add: Misc expenses written off 0 0 0 0 0

Add: Deferred tax 17 11 9 9 9

Add: Others 0 0 0 0 0

Gross cash flow 270 312 319 435 514

Less: Changes in W. C. -84 236 247 356 401

Operating cash flow 354 353 72 79 113

Less: Capex 43 71 66 75 100

Free cash flow 311 282 6 4 13

Edelweiss Professional Investor Research 29

Financials Sobha Ltd

Ratios

Year to March FY17 FY18 FY19E FY20E FY21E

ROAE (%) 6.2 8.0 8.6 10.8 11.3

ROACE (%) 8.6 10.4 11.0 13.3 14.1

Debtors (days) 37 43 39 31 33

Current ratio 2.2 2.3 2.5 2.6 2.5

Debt/Equity 0.8 0.8 0.8 0.7 0.7

Inventory (days) 834 633 538 422 409

Payable (days) 126 94 86 68 62

Cash conversion cycle (days) 746 582 491 385 380

Debt/EBITDA 5.0 4.2 3.6 2.8 2.5

Adjusted debt/Equity 0.8 0.8 0.7 0.7 0.6

Valuation parameters

Year to March FY17 FY18 FY19E FY20E FY21E

Diluted EPS (INR) 16.7 22.9 26.2 36.4 42.4

Y-o-Y growth (%) 18.6 37.0 14.4 38.9 16.7

CEPS (INR) 23.3 28.6 32.8 45.0 53.3

Diluted P/E (x) 26.8 22.4 19.0 13.7 11.7

Price/BV(x) 1.6 1.8 1.6 1.4 1.3

EV/Sales (x) 2.9 2.5 2.2 1.7 1.5

EV/EBITDA (x) 14.3 12.8 10.5 8.1 7.1

Diluted shares O/S 9.6 9.5 9.5 9.5 9.5

Basic EPS 16.7 22.9 26.2 36.4 42.4

Basic PE (x) 26.8 22.4 19.0 13.7 11.7

Dividend yield (%) 0.4% 0.6% 1.3% 1.6% 1.9%

Edelweiss Professional Investor Research 30

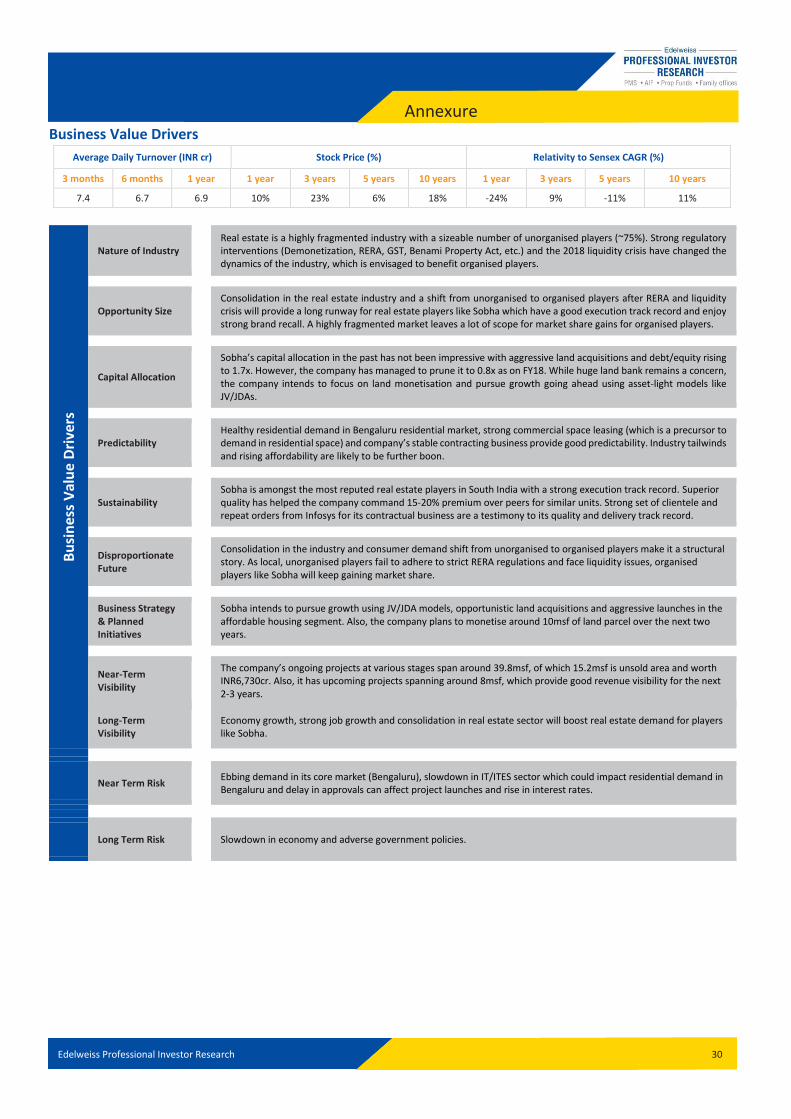

Annexure Business Value Drivers

Average Daily Turnover (INR cr) Stock Price (%) Relativity to Sensex CAGR (%)

3 months 6 months 1 year 1 year 3 years 5 years 10 years 1 year 3 years 5 years 10 years

7.4 6.7 6.9 10% 23% 6% 18% -24% 9% -11% 11%

Bu

sin

ess

Val

ue

Dri

vers

Nature of Industry Real estate is a highly fragmented industry with a sizeable number of unorganised players (~75%). Strong regulatory interventions (Demonetization, RERA, GST, Benami Property Act, etc.) and the 2018 liquidity crisis have changed the dynamics of the industry, which is envisaged to benefit organised players.

Opportunity Size Consolidation in the real estate industry and a shift from unorganised to organised players after RERA and liquidity crisis will provide a long runway for real estate players like Sobha which have a good execution track record and enjoy strong brand recall. A highly fragmented market leaves a lot of scope for market share gains for organised players.

Capital Allocation

Sobha’s capital allocation in the past has not been impressive with aggressive land acquisitions and debt/equity rising to 1.7x. However, the company has managed to prune it to 0.8x as on FY18. While huge land bank remains a concern, the company intends to focus on land monetisation and pursue growth going ahead using asset-light models like JV/JDAs.

Predictability Healthy residential demand in Bengaluru residential market, strong commercial space leasing (which is a precursor to demand in residential space) and company’s stable contracting business provide good predictability. Industry tailwinds and rising affordability are likely to be further boon.

Sustainability Sobha is amongst the most reputed real estate players in South India with a strong execution track record. Superior quality has helped the company command 15-20% premium over peers for similar units. Strong set of clientele and repeat orders from Infosys for its contractual business are a testimony to its quality and delivery track record.

Disproportionate Future

Consolidation in the industry and consumer demand shift from unorganised to organised players make it a structural story. As local, unorganised players fail to adhere to strict RERA regulations and face liquidity issues, organised players like Sobha will keep gaining market share.

Business Strategy & Planned Initiatives

Sobha intends to pursue growth using JV/JDA models, opportunistic land acquisitions and aggressive launches in the affordable housing segment. Also, the company plans to monetise around 10msf of land parcel over the next two years.

Near-Term Visibility

The company’s ongoing projects at various stages span around 39.8msf, of which 15.2msf is unsold area and worth INR6,730cr. Also, it has upcoming projects spanning around 8msf, which provide good revenue visibility for the next 2-3 years.

Long-Term Visibility

Economy growth, strong job growth and consolidation in real estate sector will boost real estate demand for players like Sobha.

Near Term Risk Ebbing demand in its core market (Bengaluru), slowdown in IT/ITES sector which could impact residential demand in Bengaluru and delay in approvals can affect project launches and rise in interest rates.

Long Term Risk Slowdown in economy and adverse government policies.

Edelweiss Professional Investor Research 31

Annexure – Company Overview

Company Overview: Strong execution track record with a unique backward integrated model

Sobha has a strong track record in real estate development and construction, with focus on

residential and contractual projects. The company has a unique backward integrated model wherein

it harnesses in-house resources to execute a project from conceptualization to completion.

Backward integration includes an architectural and design studio for a team of 150 plus qualified

architects, a fully automated concrete block making plant (~350,000sf), a metal & glazing factory

(~120,000sf), an interiors & wood working factory (~325,000sf), mechanical, electrical & plumbing

division and a project implementation team.

The backward integration model with contract and manufacturing business provides much needed

certainty over execution time-frame, enhances sourcing ability and ensures consistency in delivery

of superior quality. Sobha has successfully differentiated itself from competitors through timely

completion of projects with a tight leash on quality—one of the reasons of the company enjoying

high brand recall in South India.

Source: Edelweiss Professional Investor Research

Impressive development track record

Since inception, Sobha has executed over 436 projects, comprising total development area of over

100msf. Annual development in recent years has averaged 7msf and the execution run rate is

expected to improve going ahead.

Source: Company data, Edelweiss Professional Investor Research

Interiors

Glazing and Metal Factory

Building Materials Division

Mechanical Electrical & Plumbing Division

Architecture & Interiors Studio

Project Implementation Team

SOBHA’s

BACKWARD INTEGRATION

MODEL

9.2

5.9

7.6

5.24.5

6.77.6

11.1

5.15.8

7.8

0.0

20.0

40.0

60.0

80.0

100.0

120.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 3Q19

Annual Development (msf) Cumulative Development (msf)

Edelweiss Professional Investor Research 32

Annexure – Company Overview

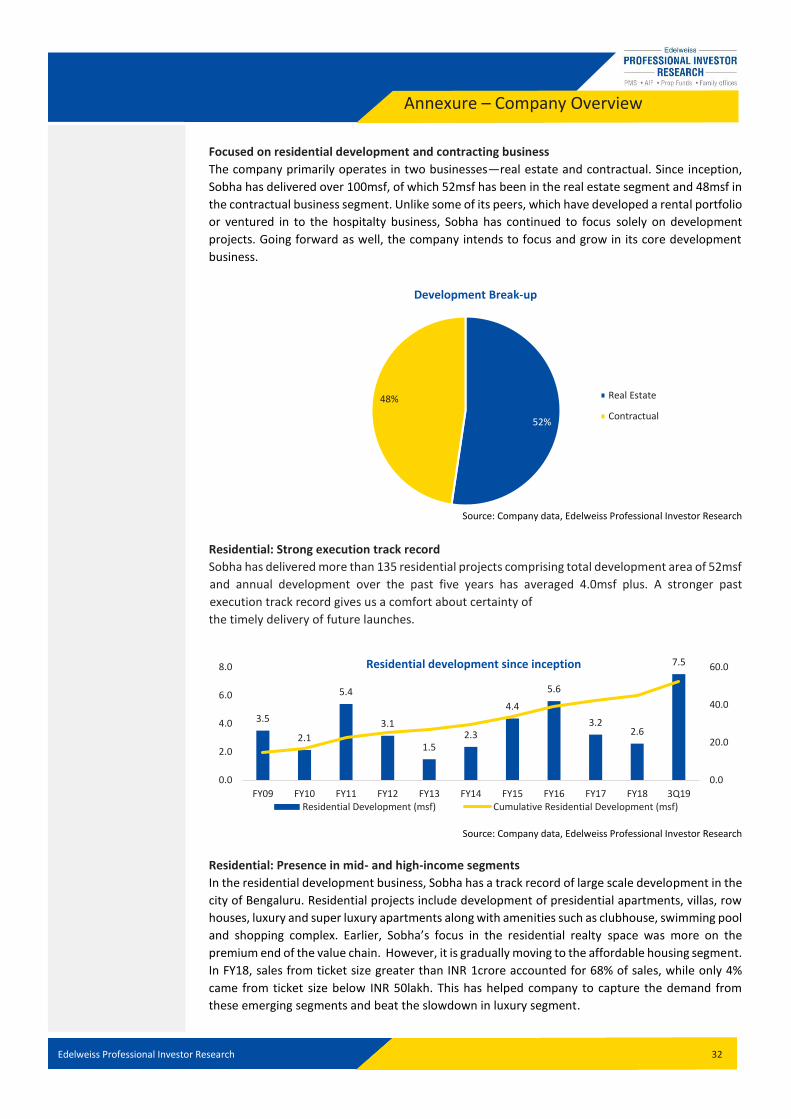

Focused on residential development and contracting business The company primarily operates in two businesses—real estate and contractual. Since inception,

Sobha has delivered over 100msf, of which 52msf has been in the real estate segment and 48msf in

the contractual business segment. Unlike some of its peers, which have developed a rental portfolio

or ventured in to the hospitalty business, Sobha has continued to focus solely on development

projects. Going forward as well, the company intends to focus and grow in its core development

business.

Source: Company data, Edelweiss Professional Investor Research

Residential: Strong execution track record

Sobha has delivered more than 135 residential projects comprising total development area of 52msf

and annual development over the past five years has averaged 4.0msf plus. A stronger past

execution track record gives us a comfort about certainty of

the timely delivery of future launches.

Source: Company data, Edelweiss Professional Investor Research

Residential: Presence in mid- and high-income segments

In the residential development business, Sobha has a track record of large scale development in the

city of Bengaluru. Residential projects include development of presidential apartments, villas, row

houses, luxury and super luxury apartments along with amenities such as clubhouse, swimming pool

and shopping complex. Earlier, Sobha’s focus in the residential realty space was more on the

premium end of the value chain. However, it is gradually moving to the affordable housing segment.

In FY18, sales from ticket size greater than INR 1crore accounted for 68% of sales, while only 4%

came from ticket size below INR 50lakh. This has helped company to capture the demand from

these emerging segments and beat the slowdown in luxury segment.

52%

48%

Development Break-up

Real Estate

Contractual

3.5

2.1

5.4

3.1

1.52.3

4.4

5.6

3.22.6

7.5

0.0

20.0

40.0

60.0

0.0

2.0

4.0

6.0

8.0

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 3Q19

Residential development since inception

Residential Development (msf) Cumulative Residential Development (msf)

Edelweiss Professional Investor Research 33

Annexure – Company Overview

Source: Company data, Edelweiss Professional Investor Research

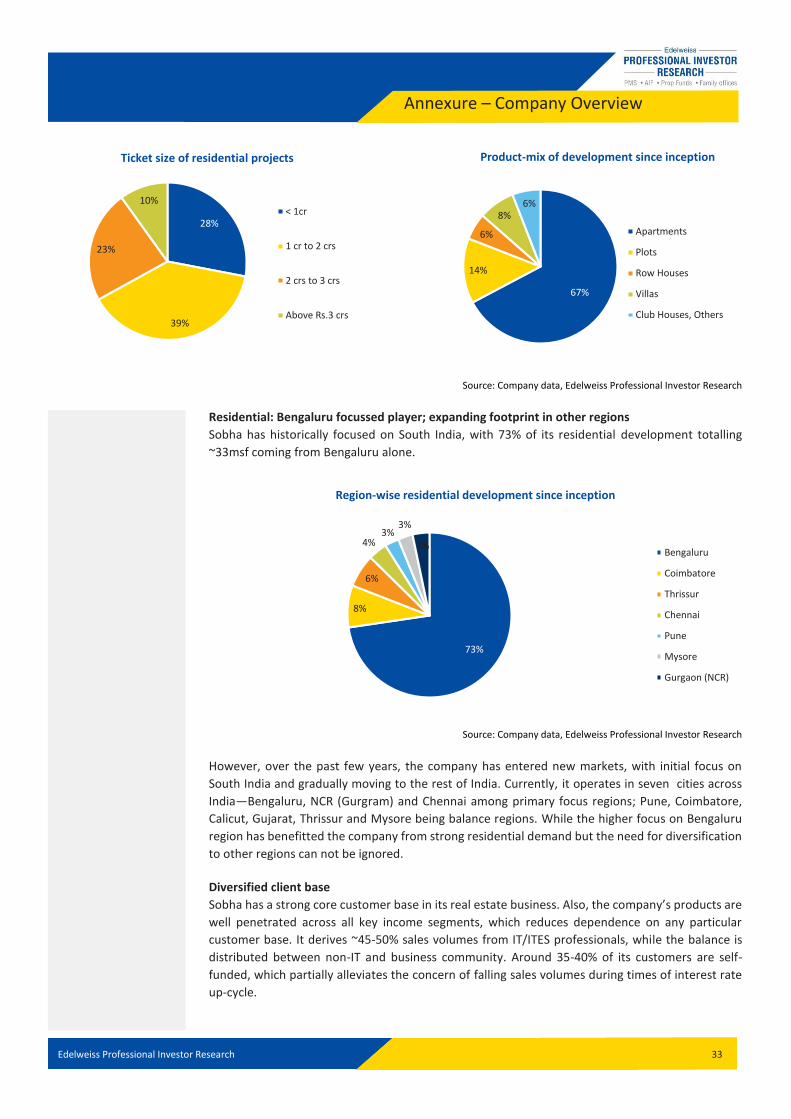

Residential: Bengaluru focussed player; expanding footprint in other regions

Sobha has historically focused on South India, with 73% of its residential development totalling

~33msf coming from Bengaluru alone.

Source: Company data, Edelweiss Professional Investor Research

However, over the past few years, the company has entered new markets, with initial focus on

South India and gradually moving to the rest of India. Currently, it operates in seven cities across

India—Bengaluru, NCR (Gurgram) and Chennai among primary focus regions; Pune, Coimbatore,

Calicut, Gujarat, Thrissur and Mysore being balance regions. While the higher focus on Bengaluru

region has benefitted the company from strong residential demand but the need for diversification

to other regions can not be ignored.

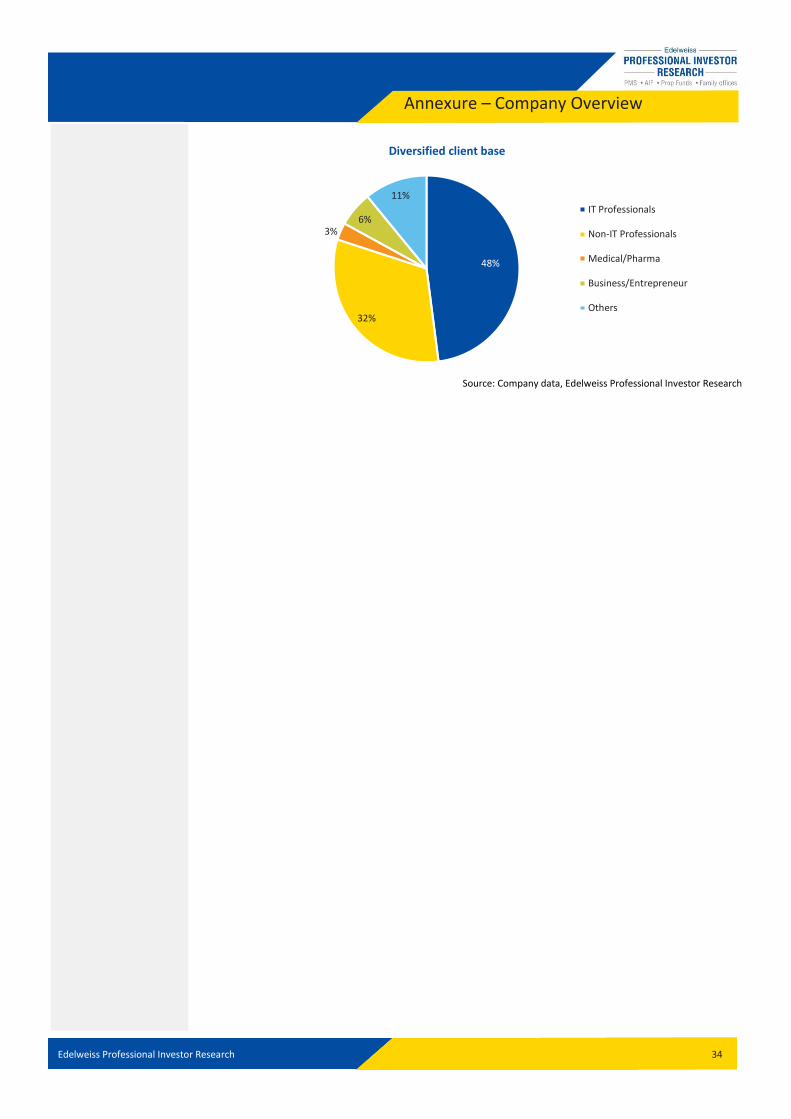

Diversified client base

Sobha has a strong core customer base in its real estate business. Also, the company’s products are

well penetrated across all key income segments, which reduces dependence on any particular

customer base. It derives ~45-50% sales volumes from IT/ITES professionals, while the balance is

distributed between non-IT and business community. Around 35-40% of its customers are self-

funded, which partially alleviates the concern of falling sales volumes during times of interest rate

up-cycle.

28%

39%

23%

10%

Ticket size of residential projects

< 1cr

1 cr to 2 crs

2 crs to 3 crs

Above Rs.3 crs

67%

14%

6%

8%6%

Product-mix of development since inception

Apartments

Plots

Row Houses

Villas

Club Houses, Others

73%

8%

6%

4%3%

3%

3%

Region-wise residential development since inception

Bengaluru

Coimbatore

Thrissur

Chennai

Pune

Mysore

Gurgaon (NCR)

Edelweiss Professional Investor Research 34

Annexure – Company Overview

Source: Company data, Edelweiss Professional Investor Research

48%

32%

3%6%

11%

Diversified client base

IT Professionals

Non-IT Professionals

Medical/Pharma

Business/Entrepreneur

Others

Edelweiss Professional Investor Research 35

Annexure – Sector Overview

Residential Real Estate Sector: An overview The real estate sector in India has seen a prolonged slowdown with weak demand and burgeoning unsold inventory since 2010.

Unaffordable prices, poor execution from developers and wrong ticket size led to the sector losing momentum. As a result, real

estate players have gone slow on launches over the past few years. Additionally, several regulatory reforms such as

Demonization, RERA and GST along with the recent liquidity crisis further disrupted the industry and delayed recovery. Till 2017

end, while developers continued to remain in wait-and-watch mode to prepare for the new RERA/GST regime, buyers sat on the

fence expecting significant price correction. With policy announcements in the latest budget and recent GST rate cuts, we believe

the sector recovery will pick up pace.

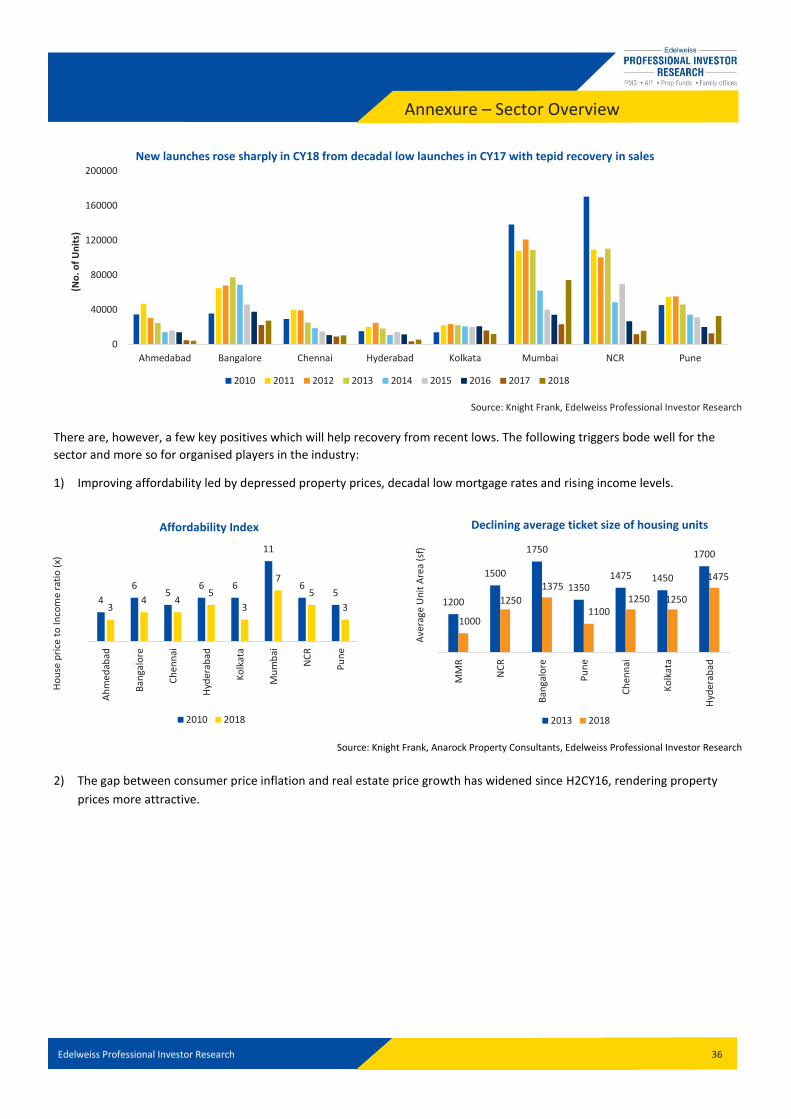

Consistent fall in demand (CY17 sales at decadal low); greenshoots visible in CY18 sales

Demand for real estate housing units has been on a continuous downtrend since 2013 in the top-8 cities with Mumbai and NCR

being the worst affected (downtrend started in 2011). Following reasons can be attributed to the declining demand:

1) Focus on investor demand rather than end-user demand.

2) Launches in wrong ticket size.

3) Poor execution track record (delay in project delivery) resulting in ebbing consumer confidence.

Total absorption in CY17 was lowest in a decade due to a host of regulatory factors such as demonetization, RERA and GST

disrupting industry and decelerating demand further. Absorption in 2018, however, has recovered modestly as the industry is

gradually stabilising.

Source: Knight Frank, Edelweiss Professional Investor Research

New launches also plummeted to decadal low in CY17; zoomed ~76% in CY18

Following slowing demand and rising inventory levels along with the pressure to service burgeoning debt, most real estate

players have pruned launches over the past few years. NCR recorded lowest launches amongst major cities over CY10-18—down

26% CAGR. However, launches jumped significantly in CY18 as players slowly adapted to the new RERA/GST regime.

0

20000

40000

60000

80000

100000

120000

Ahmedabad Bangalore Chennai Hyderabad Kolkata Mumbai NCR Pune

No

. of

un

its

Total residential demand in Tier 1 cities declined by ~30% from peak of CY10-12, with NCR and Mumbai being hit the most

2010 2011 2012 2013 2014 2015 2016 2017 2018

Edelweiss Professional Investor Research 36

Annexure – Sector Overview

Source: Knight Frank, Edelweiss Professional Investor Research

There are, however, a few key positives which will help recovery from recent lows. The following triggers bode well for the

sector and more so for organised players in the industry:

1) Improving affordability led by depressed property prices, decadal low mortgage rates and rising income levels.

Source: Knight Frank, Anarock Property Consultants, Edelweiss Professional Investor Research

2) The gap between consumer price inflation and real estate price growth has widened since H2CY16, rendering property

prices more attractive.

0

40000

80000

120000

160000

200000

Ahmedabad Bangalore Chennai Hyderabad Kolkata Mumbai NCR Pune

(No

. of

Un

its)

New launches rose sharply in CY18 from decadal low launches in CY17 with tepid recovery in sales

2010 2011 2012 2013 2014 2015 2016 2017 2018

4

65

6 6

11

65

34 4

5

3

7

5

3

Ah

med

abad

Ban

galo

re

Ch

enn

ai

Hyd

erab

ad

Ko

lkat

a

Mu

mb

ai

NC

R

Pu

ne

Ho

use

pri

ce t

o In

com

e ra

tio

(x)

Affordability Index

2010 2018

1200

1500

1750

13501475 1450

1700

1000

1250

1375

11001250 1250

1475

MM

R

NC

R

Ban

galo

re

Pu

ne

Ch

enn

ai

Ko

lkat

a

Hyd

erab

ad

Ave

rage

Un

it A

rea

(sf)

Declining average ticket size of housing units

2013 2018

Edelweiss Professional Investor Research 37

Annexure – Sector Overview

Source: Knight Frank, Edelweiss Professional Investor Research

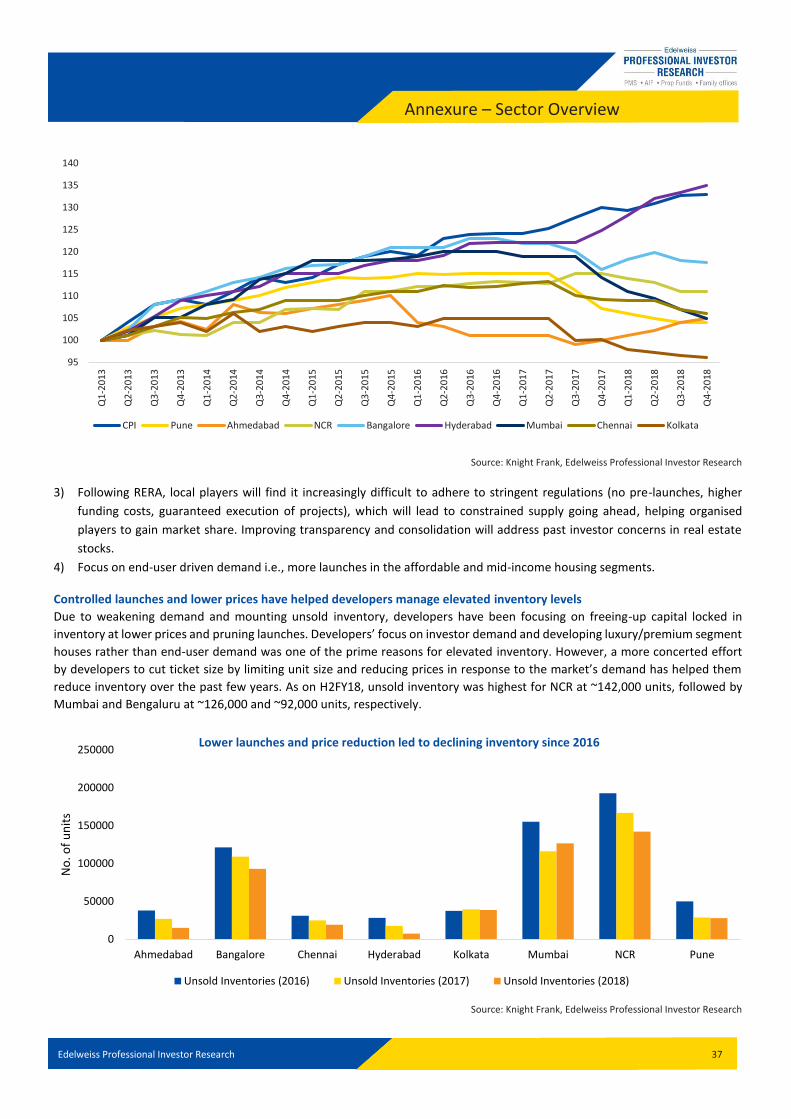

3) Following RERA, local players will find it increasingly difficult to adhere to stringent regulations (no pre-launches, higher

funding costs, guaranteed execution of projects), which will lead to constrained supply going ahead, helping organised

players to gain market share. Improving transparency and consolidation will address past investor concerns in real estate

stocks.

4) Focus on end-user driven demand i.e., more launches in the affordable and mid-income housing segments.

Controlled launches and lower prices have helped developers manage elevated inventory levels

Due to weakening demand and mounting unsold inventory, developers have been focusing on freeing-up capital locked in

inventory at lower prices and pruning launches. Developers’ focus on investor demand and developing luxury/premium segment

houses rather than end-user demand was one of the prime reasons for elevated inventory. However, a more concerted effort

by developers to cut ticket size by limiting unit size and reducing prices in response to the market’s demand has helped them

reduce inventory over the past few years. As on H2FY18, unsold inventory was highest for NCR at ~142,000 units, followed by

Mumbai and Bengaluru at ~126,000 and ~92,000 units, respectively.

Source: Knight Frank, Edelweiss Professional Investor Research

95

100

105

110

115

120

125

130

135

140

Q1

-20

13

Q2

-20

13

Q3

-20

13

Q4

-20

13

Q1

-20

14

Q2

-20

14

Q3

-20

14

Q4

-20

14

Q1

-20

15

Q2

-20

15

Q3

-20

15

Q4

-20

15

Q1

-20

16

Q2

-20

16

Q3

-20

16

Q4

-20

16

Q1

-20

17

Q2

-20

17

Q3

-20

17

Q4

-20

17

Q1

-20

18

Q2

-20

18

Q3

-20

18

Q4

-20

18

CPI Pune Ahmedabad NCR Bangalore Hyderabad Mumbai Chennai Kolkata

0

50000

100000

150000

200000

250000

Ahmedabad Bangalore Chennai Hyderabad Kolkata Mumbai NCR Pune

No

. of

un

its

Lower launches and price reduction led to declining inventory since 2016

Unsold Inventories (2016) Unsold Inventories (2017) Unsold Inventories (2018)

Edelweiss Professional Investor Research 38

Annexure – Sector Overview Also, the number of quarters required to sell (quarters required to relinquish unsold inventory at current sales velocity) the

current inventory has dipped for most cities since 2016, indicating sales recovery coupled with lower launches. Hyderabad and

Pune witnessed the highest decline in number of quarters to sell.

According to Knight Frank, while quarters to sell for Hyderabad have plummeted from 8.0 in 2016 to just 1.9 in H2FY18, Pune’s

fell from 5.8 in 2016 to 3.3 in H1FY18 for. NCR followed by Kolkata and Bengaluru will take 15.0, 12.6 and 10.3 quarters to sell

existing inventory, respectively.

Source: Knight Frank, Edelweiss Professional Investor Research

As on Q3CY18, ~19% of unsold inventory in the top-7 cities is more than 3 years old, according to ANAROCK Property Consultants.

MMR and Pune particularly have ~50% of inventory older than 2 years. Healthy sales momentum is evident in Hyderabad, where

~75% of the unsold inventory is less than 2 years old. Chennai has ~30% of ready-to-move inventory, the highest amongst the

top-7 cities.

Source: Anarock Property Consultants, Edelweiss Professional Investor Research

Interim Budget FY20: Constructive for real estate

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Ahmedabad Bangalore Chennai Hyderabad Kolkata Mumbai NCR Pune

Qu

arte

rs t

o s

ell

Declining Quarters to Sell for most of the cities since 2016

Quarters to sell (2016) Quarters to sell (2017) Quarter to Sell (2018)

15%

30%16% 13% 10% 12% 9%

37%

33%

35%28%

20%24%

17%

19%

18%

23%

26%

21%

25%

21%

15%

10% 21%

16%

14%

18%

21%

14% 9% 6%17%

35%21%

32%

0%

25%

50%

75%

100%

Bangalore Chennai Hyderabad Kolkata Mumbai NCR Pune

Unsold Inventory Age

RTM < 1Yr 1 to 2 Yrs 2 to 3 Yrs >3 Yrs

Edelweiss Professional Investor Research 39

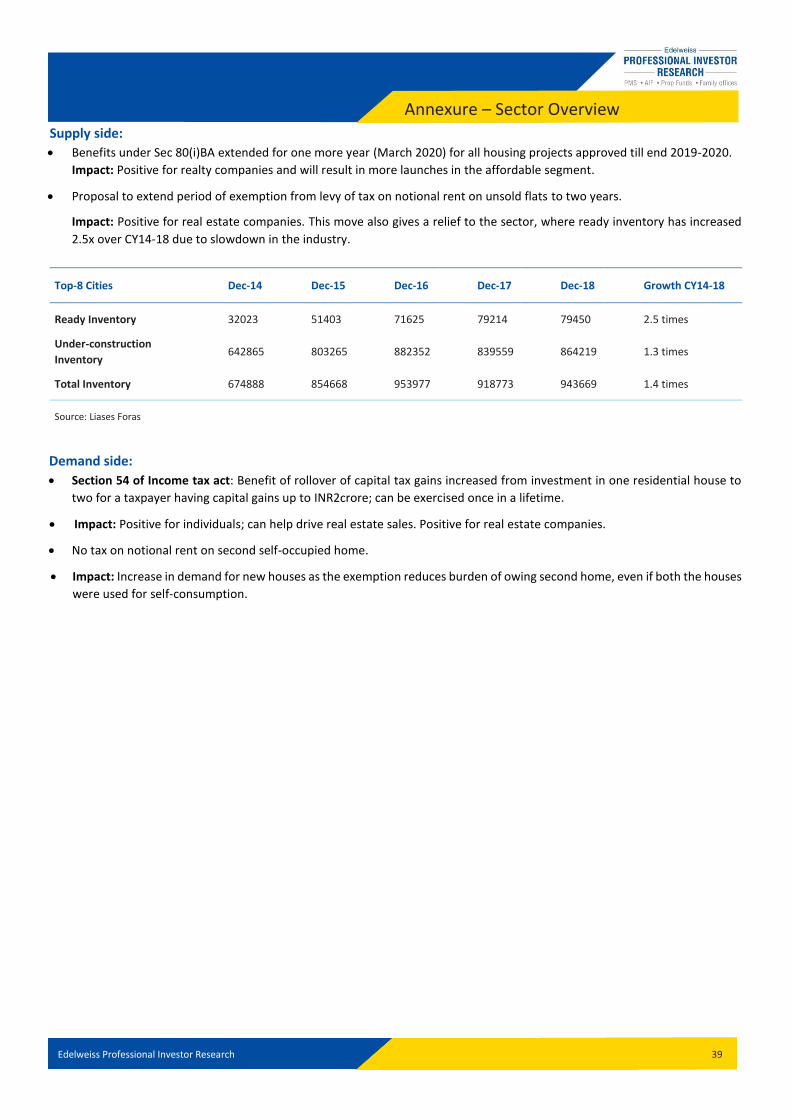

Annexure – Sector Overview Supply side:

Benefits under Sec 80(i)BA extended for one more year (March 2020) for all housing projects approved till end 2019-2020.

Impact: Positive for realty companies and will result in more launches in the affordable segment.

Proposal to extend period of exemption from levy of tax on notional rent on unsold flats to two years.

Impact: Positive for real estate companies. This move also gives a relief to the sector, where ready inventory has increased

2.5x over CY14-18 due to slowdown in the industry.

Top-8 Cities Dec-14 Dec-15 Dec-16 Dec-17 Dec-18 Growth CY14-18

Ready Inventory 32023 51403 71625 79214 79450 2.5 times

Under-construction

Inventory 642865 803265 882352 839559 864219 1.3 times

Total Inventory 674888 854668 953977 918773 943669 1.4 times

Source: Liases Foras

Demand side:

Section 54 of Income tax act: Benefit of rollover of capital tax gains increased from investment in one residential house to

two for a taxpayer having capital gains up to INR2crore; can be exercised once in a lifetime.

Impact: Positive for individuals; can help drive real estate sales. Positive for real estate companies.

No tax on notional rent on second self-occupied home.

Impact: Increase in demand for new houses as the exemption reduces burden of owing second home, even if both the houses

were used for self-consumption.

Edelweiss Professional Investor Research 40

Annexure – Sector Overview

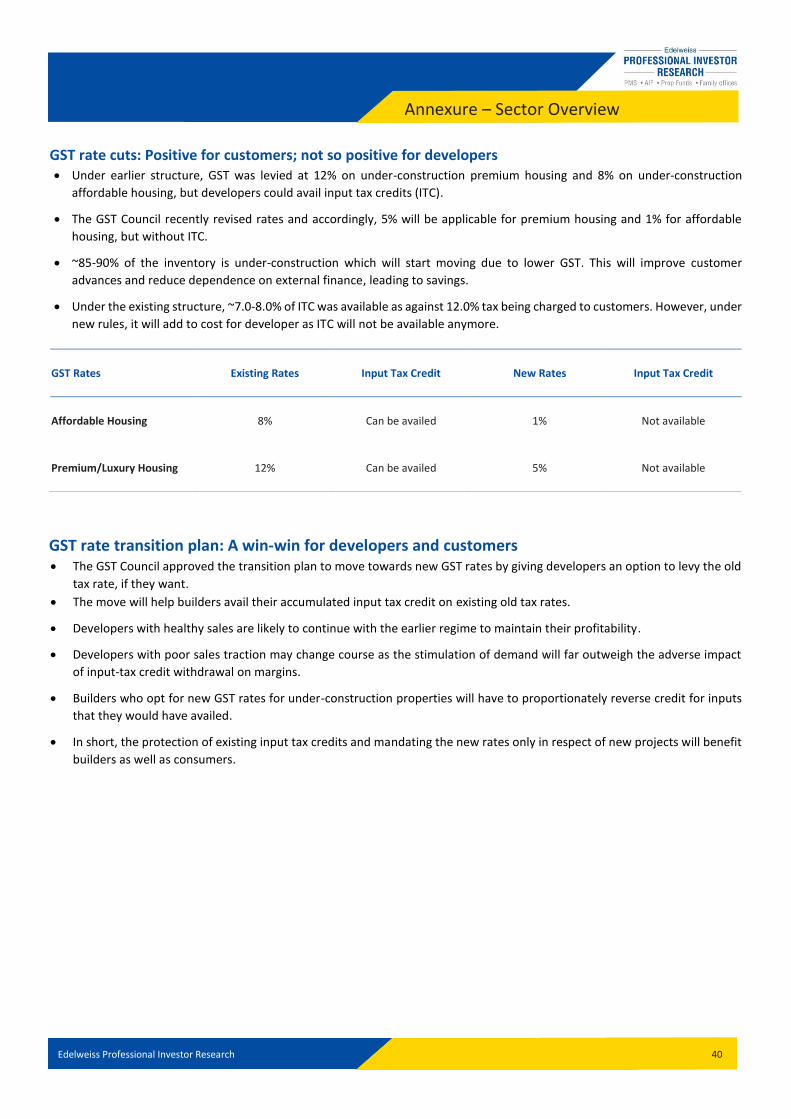

GST rate cuts: Positive for customers; not so positive for developers Under earlier structure, GST was levied at 12% on under-construction premium housing and 8% on under-construction

affordable housing, but developers could avail input tax credits (ITC).

The GST Council recently revised rates and accordingly, 5% will be applicable for premium housing and 1% for affordable

housing, but without ITC.

~85-90% of the inventory is under-construction which will start moving due to lower GST. This will improve customer

advances and reduce dependence on external finance, leading to savings.

Under the existing structure, ~7.0-8.0% of ITC was available as against 12.0% tax being charged to customers. However, under

new rules, it will add to cost for developer as ITC will not be available anymore.

GST Rates Existing Rates Input Tax Credit New Rates Input Tax Credit

Affordable Housing 8% Can be availed 1% Not available

Premium/Luxury Housing 12% Can be availed 5% Not available

GST rate transition plan: A win-win for developers and customers The GST Council approved the transition plan to move towards new GST rates by giving developers an option to levy the old

tax rate, if they want.

The move will help builders avail their accumulated input tax credit on existing old tax rates.

Developers with healthy sales are likely to continue with the earlier regime to maintain their profitability.

Developers with poor sales traction may change course as the stimulation of demand will far outweigh the adverse impact

of input-tax credit withdrawal on margins.

Builders who opt for new GST rates for under-construction properties will have to proportionately reverse credit for inputs

that they would have availed.

In short, the protection of existing input tax credits and mandating the new rates only in respect of new projects will benefit

builders as well as consumers.

Edelweiss Professional Investor Research 41

Edelweiss Broking Limited, 1st Floor, Tower 3, Wing B, Kohinoor City Mall, Kohinoor City, Kirol Road, Kurla(W)

Board: (91-22) 4272 2200

Vinay Khattar

Head Research

Rating Expected to

Buy appreciate more than 15% over a 12-month period

Hold appreciate between 5-15% over a 12-month period

Reduce Return below 5% over a 12-month period

40

60

80

100

120

140

160

180

200

220

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Ap

r-1

9

(In

de

xed

)

Sobha Sensex

Edelweiss Professional Investor Research 42

Disclaimer Edelweiss Broking Limited (“EBL” or “Research Entity”) is regulated by the Securities and Exchange Board of India (“SEBI”) and is licensed to carry on the business of broking, depository

services and related activities. The business of EBL and its Associates (list available on www.edelweissfin.com) are organized around five broad business groups – Credit including Housing

and SME Finance, Commodities, Financial Markets, Asset Management and Life Insurance.

Broking services offered by Edelweiss Broking Limited under SEBI Registration No.: INZ000005231; Name of the Compliance Officer: Mr. Brijmohan Bohra, Email ID:

[email protected] Corporate Office: Edelweiss House, Off CST Road, Kalina, Mumbai - 400098; Tel. 18001023335/022-42722200/022-40094279

This Report has been prepared by Edelweiss Broking Limited in the capacity of a Research Analyst having SEBI Registration No.INH000000172 and distributed as per SEBI (Research