1 Folie Susanne Dröge Leakage Workshop 4 February 2008 Tackling Leakage in a World of Unequal Carbon Prices Climate Strategies Workshop, 4 February 2008, Paris supported by:

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1Folie

Susanne DrögeLeakage Workshop4 February 2008

Tackling Leakage in a World of Unequal Carbon Prices

Climate Strategies Workshop, 4 February 2008, Paris

supported by:

2Folie

Susanne DrögeLeakage Workshop4 February 2008

www.climatestrategies.org

1. Assist solving collective action problems for policy makers in Europe and worldwide

2. Trans-boundary and neutral agent between academics (science), government (bureaucracy), and geopolitical boundaries (politics)

3. Sponsored and funded by EU governments and companies

4. Three major themes:– The EU emissions trading scheme– CDM– East-West Investment

3Folie

Susanne DrögeLeakage Workshop4 February 2008

Background

Global carbon market unlikely in near futurecarbon leakage likely

Parallel policy processes: EU and other nations Bali Action Plan: Copenhagen2009

Unilateral commitments EU (stricter ETS after 2013): regional carbon market(s)

Analyses of competitiveness and leakage effects from EU carbon pricing (Climate Strategies Report 2007: Differentiation and Dynamics of EU ETS Industrial Competitiveness Impacts)

Policies to address leakage:need careful analyses w.r.t. effectiveness and implicationfor global progress

4Folie

Susanne DrögeLeakage Workshop4 February 2008

Climate Strategies Project: „Tackling Leakage ...“

Point of Departure: EU ETS and leakage; interactions with(a) other countries’ ETS and leakage policy (AUS, NZ, Japan; US? Can?); (b) the international negotiations for a new global climate treaty

Packages– I: Illustrating leakage and competitiveness for selected industries:

measuring leakage, synergies/trade-offs with competitiveness; unintended feedbacks

from climate policy; relevant sectors in different MS; regional differences; – II: Free Allocation: determination of relevant sectors and allocation criteria;

effects on leakage; Implications for the EU sectors, regions, ETS; – III: Adjustments at the border: import allowances; tariffs on imports,

compensation for exporters, technical issues of implementation (legal, economic, fiscal); political implications.

– IV: Implications for Post-2012: parallel policy/negotiation processes; politicaleconomy of measures; political implications of EU and other countries measuresagainst leakage (esp. emerging economies) for climate regime and trade regime(s).

5Folie

Susanne DrögeLeakage Workshop4 February 2008

Aim of the Workshop

To convene researchers and stakeholders and induce in-depth discussions on the leakage potential created by the EU ETS.

To discuss research results and to identify research needs in the fields mentioned, not least along the needs of stakeholders (industry, governments, NGOs).

To cultivate an open exchange on all options to address leakage, the trade-offs in terms of effectiveness, efficiency and for the future regional and global climate regime (and other regimes).

6Folie

Susanne DrögeLeakage Workshop4 February 2008

9.30 – 9.45 Welcome and Introduction The CS Project and Aims of the Workshop, Susanne Dröge, SWP The EU ETS Review and Leakage, Karsten Neuhoff, Cambridge

9.45 – 10.45

Session I

Leakage and Competitiveness: Evidence, Synergies and Trade-offs (Chair: Karsten Neuhoff) Macro-economic Leakage Effects, Onno Kuik, IVM Ex-Post Evaluation of the EU ETS on the European Aluminium Industry, Julia Reinaud, IEA Potential Feedbacks of Climate Policy on Leakage: the Building Sector, Philippe Quirion, CIRED

10.45 – 11.00 Coffee Break

11.00 – 13.00

Session II

Tackling Leakage Under the EU ETS (Chair: Michel Colombier) Potential Policy Tools - An Overview, Karsten Neuhoff, Cambridge Two Policies to Address Leakage: Border Adjustments and Output-Based Allocation, Philippe Quirion, CIRED Border Tax Adjustment to Address Leakage, Olivier Godard, CNRS The Legal Framework: What are the Limitations to Border Taxes?, Roland Ismer, University of Munich

13.00 – 14.00 Lunch Break

Workshop Agenda – I

7Folie

Susanne DrögeLeakage Workshop4 February 2008

13.00 – 14.00 Lunch Break

14.00 – 15.15 Session III

Major EU Trade Partners’ Policies to Address Leakage (Chair: Michael Grubb) US Climate Policy - Trade Policy Intersections: Current Status, Prospects and Implications for Carbon Leakage, Thomas Brewer, Georgetown University The China Factor, Bernice Lee, Chatham House Japanese and East Asian Perspectives, Akiko Sato, Imperial College

15.15 – 15.30 Coffee Break

15.30 – 16.30 Session IV

Trade and Climate Policy: Implications for the Post2012 Process (Chair: S. Dröge) Linking Trade and Climate Regimes? Analytical Needs, John Whalley, University of Western Ontario Addressing Leakage in a Post-2012 World: Legal and Political Considerations, Harro van Asselt, IVM Global Trade Perspectives And North-South Concerns, Malena Sell and Mahesh Sugathan, ICTSD

16.30 – 17.15 WS -Wrap Up and Project’s Work Programme

End of Workshop

Workshop Agenda – I I

8Folie

Susanne DrögeLeakage Workshop4 February 2008

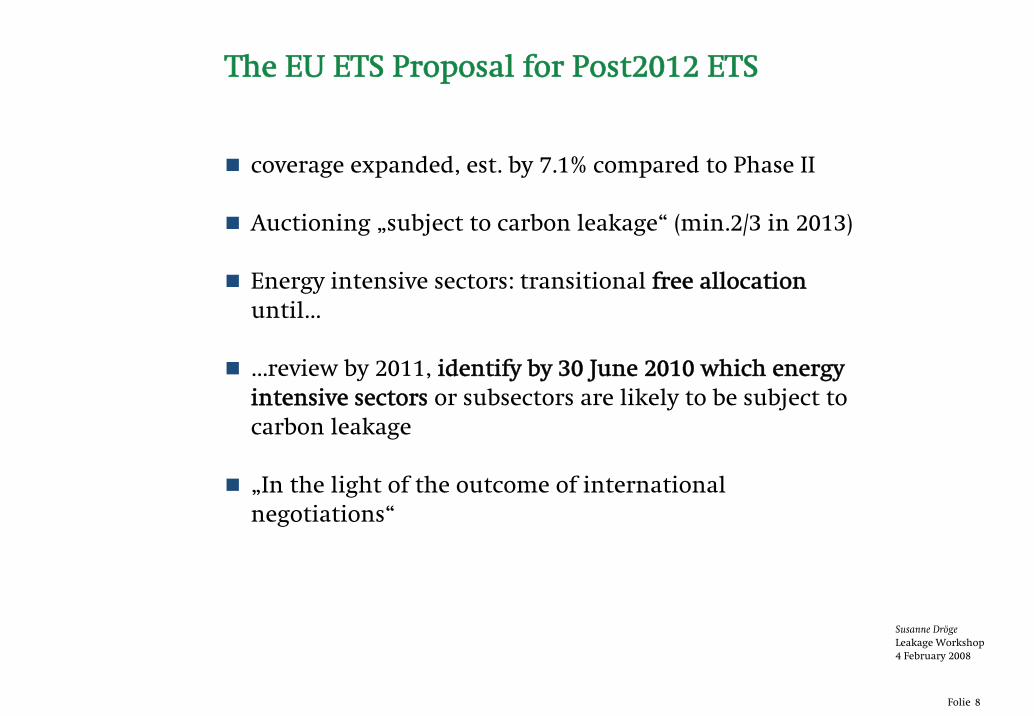

The EU ETS Proposal for Post2012 ETS

coverage expanded, est. by 7.1% compared to Phase II

Auctioning „subject to carbon leakage“ (min.2/3 in 2013)

Energy intensive sectors: transitional free allocationuntil…

…review by 2011, identify by 30 June 2010 which energy intensive sectors or subsectors are likely to be subject to carbon leakage

„In the light of the outcome of international negotiations“

9Folie

Susanne DrögeLeakage Workshop4 February 2008

Tackling Leakage in a World of Unequal Carbon Prices

Climate Strategies Workshop, 4 February 2008, Paris

supported by:

Policy options for addressing leakage impacts

Karsten NeuhoffFaculty of Economics, Cambridge University

www.electricitypolicy.org.uk/tsec/2

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

• The EU ETS Review and Leakage• Leakage and Competitiveness: Evidence,

Synergies and Trade-offs• Potential Policy Tools - An Overview

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

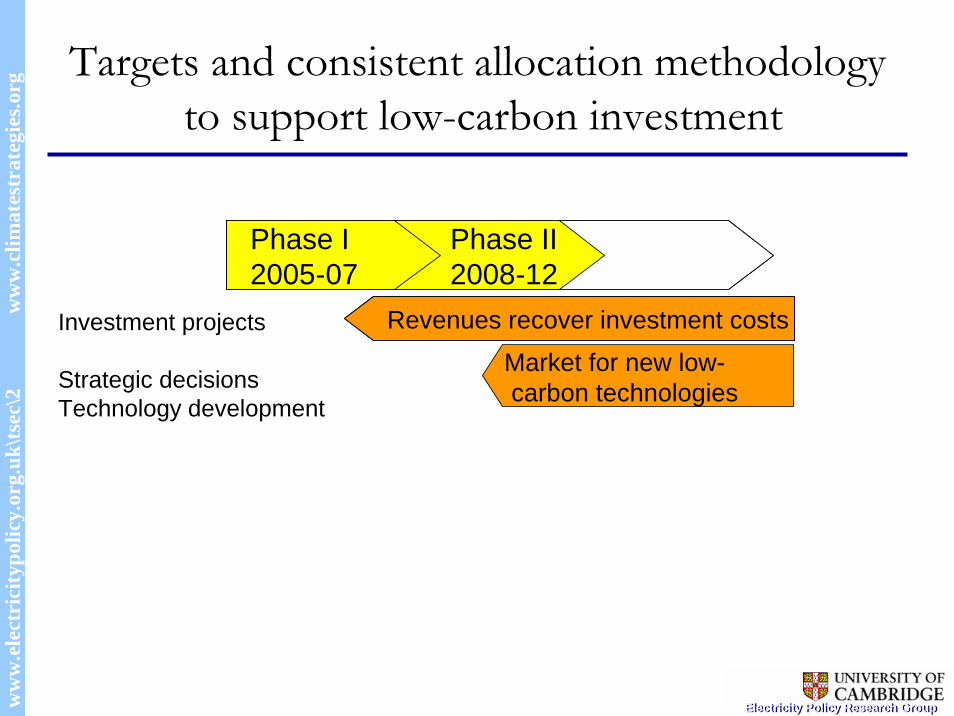

Targets and consistent allocation methodologyto support low-carbon investment

revenues finance investmentrevenues finance investment

Phase I2005-07

Phase II2008-12

Revenues recover investment costs

Phase I2005-07

Phase II2008-12

Market for new low-carbon technologies

Investment projects

Strategic decisionsTechnology development

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

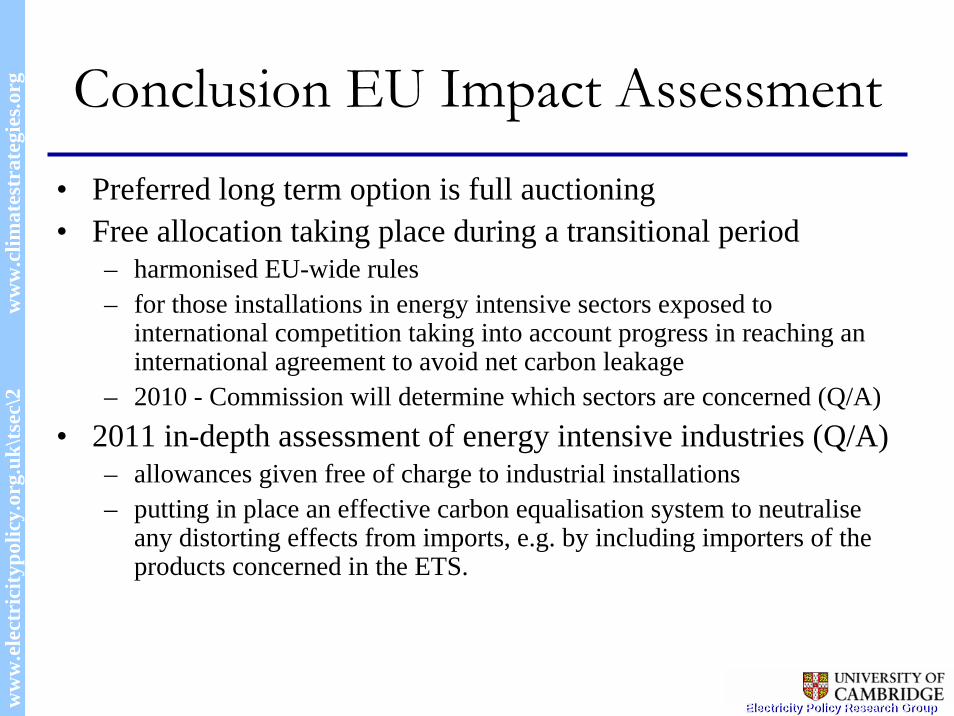

Conclusion EU Impact Assessment • Preferred long term option is full auctioning• Free allocation taking place during a transitional period

– harmonised EU-wide rules– for those installations in energy intensive sectors exposed to

international competition taking into account progress in reaching an international agreement to avoid net carbon leakage

– 2010 - Commission will determine which sectors are concerned (Q/A)• 2011 in-depth assessment of energy intensive industries (Q/A)

– allowances given free of charge to industrial installations – putting in place an effective carbon equalisation system to neutralise

any distorting effects from imports, e.g. by including importers of the products concerned in the ETS.

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

Sectors covered• Energy intensive industries are defined as business entities

where the purchase of energy products and electricity amounts to at least 3.0% of the production value

• 50 sub-sectors might require price increases for their products ranging from 0.1 to 5% to recoup costs imposed by an carbon price of €20 per tonne of CO2: cement and lime production, primary steel (blast oxygen furnace), aluminium production, production of primary container glass and some basic chemicals (ammonia, nitric acid, fertilizer production) [DG Economic and Financial Affairs Economic Paper n° 297, forthcoming]

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

Measures proposed by Commission I

• Global sectoral agreements assuming realistic efforts by other regions– greater GHG reductions at the global level – positive, albeit modest, effect on the output performance of energy intensive

industries. – Not much overall economic effects (in terms of GDP)

• Free allocation of ETS allowances to energy intensive industries– On the basis of benchmarks – Contributes very strongly towards avoiding significant output losses – Without compromising total economy-wide performance – CO2 and electricity prices are hardly affected. – This instrument seems to be a very powerful tool to offset carbon leakage and

adverse effects on energy intensive industries. – This is even more the case if the free allocation would also allow for the

compensation for indirect costs

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

Pyramid of distortions – summary of experience from phase I

Excess carbon-intensive capacity

Inefficient fuel choice

Less energy-efficiency investment

Distortions

AuctionCapacity X

Capacity and technology X XHistoric output X X

Historic output and technology X X XHistoric emissions X X X X

Discourage clo

sure of plants

Discourage clo

sure of ineffic

ient plant

Increase operation of in

efficient plants

Reduce incentives fo

r

Efficiency-

improving investm

ent

Allocation method

Distortions increase emissions and/or price impacts

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

European comparison of NAP2 – fall 2006

Source: Neuhoff, K., Rogge, K., Schleich, J., Sijm, J., Tuerk, A., Kettner, C., Walker, N., Åhman, M., Betz, R.,Cludius, J., Ferrario, F., Holmgren, K., Pal, G., Grubb, M. and Matthes F., 2006, Implications of announced Phase National Allocation Plans for the EU ETS, Climate Policy 6(5) pp. 411-422.

Installed capacity P P P

Projection for productionP P

Historic production P O

Installed capacityProjections of production P

Historic ProductionProjections O O P / O P / O P

Historic Emissions O O-Not defP / O P / O P / O O P / O P / O P / OAT* BE -W BE - F BE - B CY CZ** DE DK** EE ES* FI FR GR

Installed capacityProjection for productionP P / O

Historic productionInstalled capacity P

Projections of productionP P P / O P / O

Historic ProductionProjections P / O O P P / O P / O O

Historic Emissions P P / O O P / O P / O P / O P P / O P / O P / O P / O P / O P / OHU* IE IT* LT LU LV MT NL PL PT SE SI SK UK

Ben

chm

arki

ng

Uni

form

Tech

/ Fu

el s

pec.

Emission based Incr

easi

ng D

isto

rtion

NA

P II

not

ana

lyse

dye

t / N

o tra

nsla

tion

avai

labl

e

NA

P II

not

ava

ilabl

e

NA

P II

not

ava

ilabl

e

Uni

form

Ben

chm

arki

ng

Emission based

Tech

/ Fu

el s

pec.

P – Power sectorO – Other sectors

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

Measures proposed by Commission II

• Inclusion of importers – positively on energy intensive industries' + additional

global GHG reductions.– Creates an important pressure on the ETS allowance price

• Access to CDM – significantly limits the output losses– reduces carbon leakage considerably– Positive for welfare / energy intensive industry. – Reduces GHG reductions achieved internally

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

CO2 prices across scenarios -> is reducing CO2 prices a measure?

CO

2 pr

ice

(eur

o/t)

0

510

1520

25

3035

40

Ref

eren

ce

25%

CD

M

Sec

tora

l

Sec

+fre

eal

loc

Sec

+Im

ports

Sec

+Ind

irect

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

PACE results presented by Commission for Impact Assessment (I)

-20.0%-10.0%

0.0%10.0%20.0%30.0%40.0%50.0%60.0%EU

Emis

sion

s(r

el 1

990)

Car

bon

leak

age

(202

0)

Wor

ldem

issi

ons

(rel

199

0)

Elec

pric

e(r

el B

AU)

Wel

fare

(rel

202

0BA

U)

Reference25% CDMSectoralSec+free allocSec+ImportsSec+Indirect

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

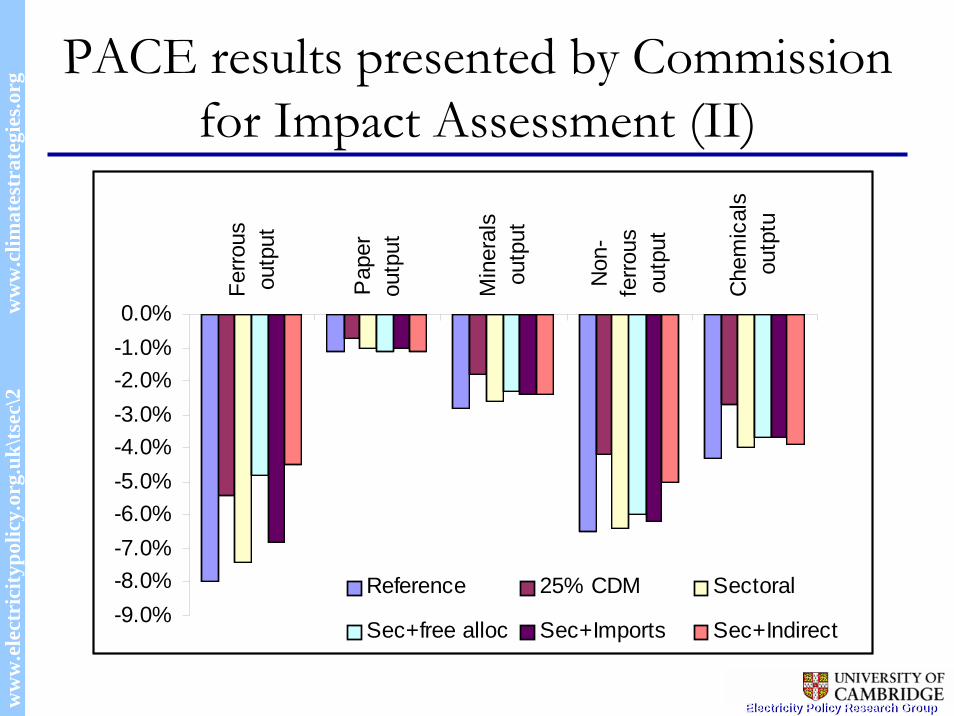

PACE results presented by Commission for Impact Assessment (II)

-9.0%-8.0%-7.0%-6.0%-5.0%-4.0%-3.0%-2.0%-1.0%0.0%

Ferro

usou

tput

Pap

erou

tput

Min

eral

sou

tput

Non

-fe

rrous

outp

ut

Che

mic

als

outp

tu

Reference 25% CDM Sectoral

Sec+free alloc Sec+Imports Sec+Indirect

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

• The EU ETS Review and Leakage• Leakage and Competitiveness: Evidence,

Synergies and Trade-offs• Potential Policy Tools - An Overview

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

CO2 cost screen: Sectors potentially exposed under unilateral CO2 pricing

Pot

entia

l Max

imum

gV

aAt

Sta

ke (M

VAS

)an

d N

et g

Va

At S

take

(NV

AS)

Hourcade Demailly, Neuhoff and Sato Differentiation and dynamics of EU ETS industrial competitiveness impacts. Embargoed until publication Nov 2007.

Potential impacts of the EU ETS on leakage are focused on a few sub-sectors

Cem

ent

Bas

ic ir

on &

ste

elLime

Fertilisers & Nitrogen

Alu

min

ium

Other inorganicbasic chemicals

Pulp &Paper

MaltCoke oven

Industrial gasesNon-wovens

Refined petroleum

Household paper

Hollow glass

Finishing of textiles

Rubber tyres & tubes

CopperCasting of iron

UK GDP

Allocation dependent (direct) CO2 costs / GVAElectricity (indirect) CO2 costs / GVA

Price increase assumption: CO2 = €20/t CO2; Electricity = €10/MWh

Flat glassVeneer sheets

0%

10%

20%

30%

40%

0.0% 0.2% 0.4% 0.6% 0.8% 1.0%

4%2%

Pot

entia

l Max

imum

gV

aAt

Sta

ke (M

VAS

)an

d N

et g

Va

At S

take

(NV

AS)

Cem

ent

Bas

ic ir

on &

ste

elLime

Fertilisers & Nitrogen

Alu

min

ium

Other inorganicbasic chemicals

Pulp &Paper

MaltCoke oven

Industrial gasesNon-wovens

Refined petroleum

Household paper

Hollow glass

Finishing of textiles

Rubber tyres & tubes

CopperCasting of iron

UK GDP

Allocation dependent (direct) CO2 costs / GVAElectricity (indirect) CO2 costs / GVA

Price increase assumption: CO2 = €20/t CO2; Electricity = €10/MWh

Flat glassVeneer sheets

0%

10%

20%

30%

40%

0.0% 0.2% 0.4% 0.6% 0.8% 1.0%

4%2%

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

• The EU ETS Review and Leakage• Leakage and Competitiveness: Evidence,

Synergies and Trade-offs• Potential Policy Tools - An Overview

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

Three principle approaches can address leakage for an exposed sector

Price level

CO2costs

Price levelPrice level

CO2 costsCO2 costs

Cos

t

Conditionalfree allocation

Cos

tC

ost

Government leadsectoral agreement

Export taxes Border adjustment

Cos

t

Export taxes Border adjustmentExport taxes Border adjustment

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

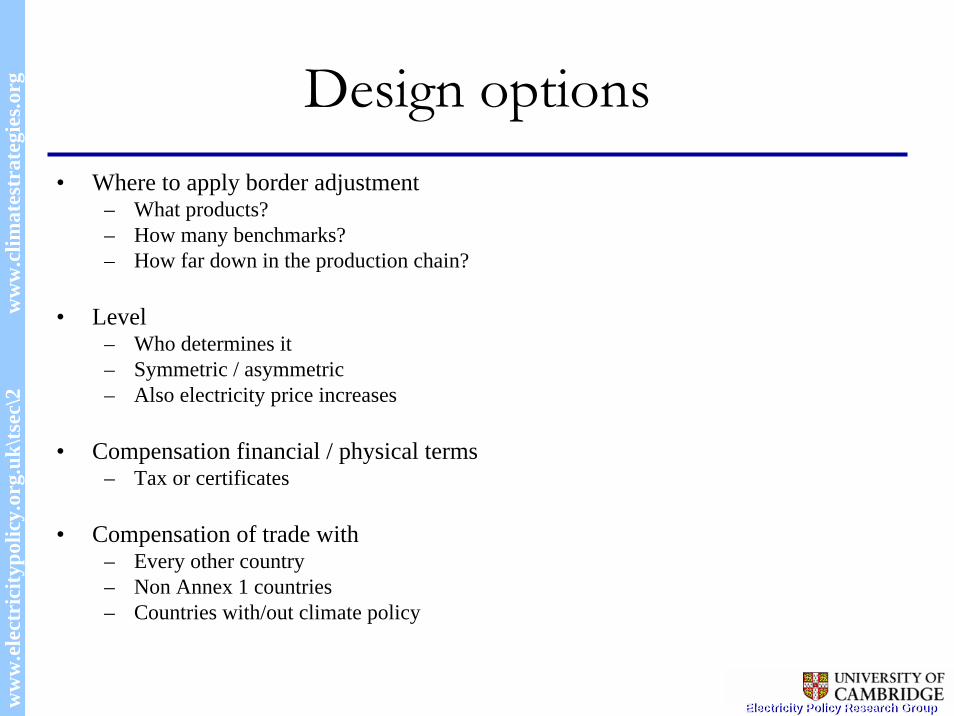

Design options• Where to apply border adjustment

– What products?– How many benchmarks?– How far down in the production chain?

• Level– Who determines it– Symmetric / asymmetric– Also electricity price increases

• Compensation financial / physical terms – Tax or certificates

• Compensation of trade with– Every other country– Non Annex 1 countries– Countries with/out climate policy

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

Steel sector

• Most exposure from BOF (and possible coke oven)• Steel can be transported at semi-finished stage

0%

10%

20%

30%

40%

50%

0 500 1000 1500 2000 2500 3000 3500Gross value added (million Euro)

Elec

tric

ity G

VAS/

CO

2 G

VAS

Cost increase electricity

Cost increase ele+CO2

Cost increase electricityfrom slab

Cost increase ele+CO2from slab

Semi Finished

Hot rolled

iron& steel

Illustrative for UK - but numbers can still change significantly

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

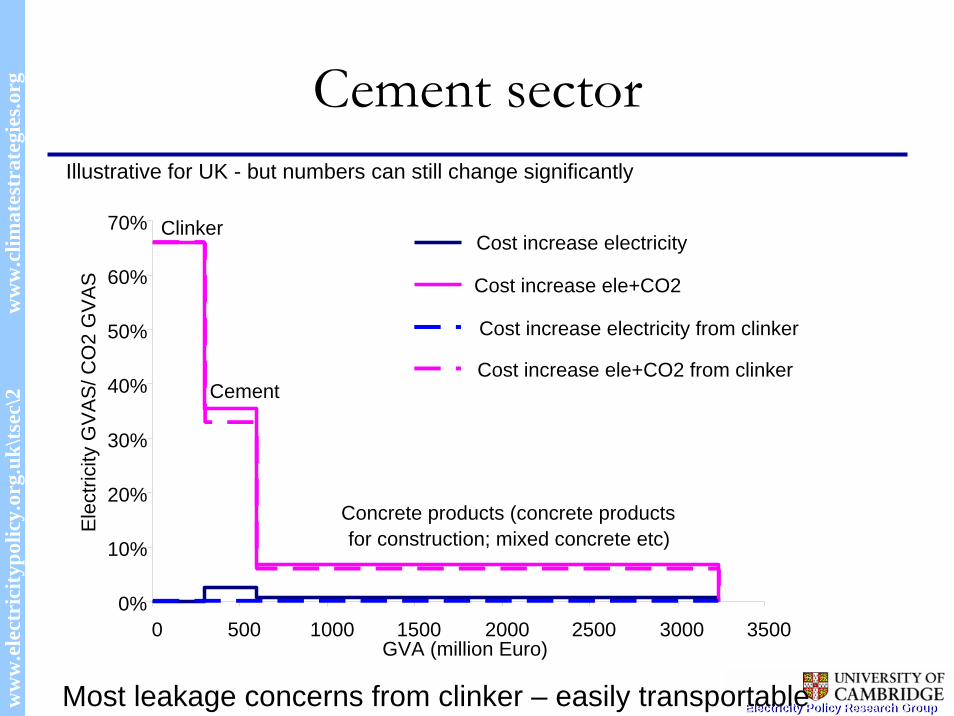

Cement sectorIllustrative for UK - but numbers can still change significantly

Most leakage concerns from clinker – easily transportable

0%

10%

20%

30%

40%

50%

60%

70%

0 500 1000 1500 2000 2500 3000 3500GVA (million Euro)

Ele

ctric

ity G

VA

S/ C

O2

GV

AS

Cost increase electricity

Cost increase ele+CO2

Cost increase electricity from clinker

Cost increase ele+CO2 from clinker

Clinker

Cement

Concrete products (concrete products for construction; mixed concrete etc)

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

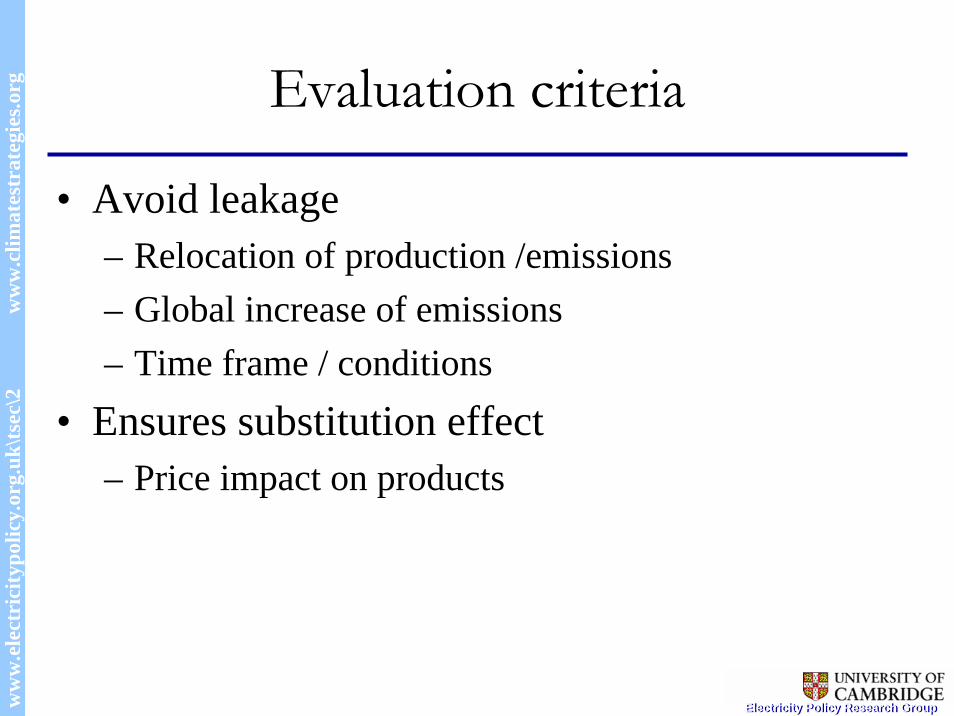

Evaluation criteria

• Avoid leakage– Relocation of production /emissions– Global increase of emissions– Time frame / conditions

• Ensures substitution effect – Price impact on products

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

A carbon price works through the value chain. This can be supported by policies that address leakage.

Clinker Cement Concrete Building

Other building materials

LeanerstructuresLower clinker

content

Sub

stitu

tion

Clinkerimports Cement imports

Leak

age

Efficiency

Some leakage • Without measures • With unconditional allocation

Forgone substitution/innovation• Without measures• With free allocation

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

Evaluation criteria

• Avoid leakage– Relocation of production /emissions– Global increase of emissions– Time frame / conditions

• Ensures substitution effect – Price impact on products

• Supports efficiency of cap and trade schemes – Avoid early action issues relating to free allocation

• Support cooperation on climate policy

Electricity Policy Research Groupww

w.e

lect

rici

typo

licy.

org.

uk\ts

ec\2

ww

w.c

limat

estr

ateg

ies.o

rg

Electricity Policy Research Group

Three principle approaches can address leakage for an exposed sector

Price level

CO2costs

Price levelPrice level

CO2 costsCO2 costs

Cos

t

Conditionalfree allocation

Cos

tC

ost

Government leadsectoral agreement

Export taxes Border adjustment

Cos

t

Export taxes Border adjustmentExport taxes Border adjustment

•Little substitution to low carbon products/services

•Distorts investment•Bureaucratic constraints for innovation

•Risk of lock-in

•Has to be aligned with international climate engagement

•Requires at least informal international cooperation

•Requires strong policies of developing countries

•Risk of low common denominator

Initial evaluation

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 1/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

INTERNATIONAL CARBON LEAKAGE

INTERPRETING CGE'S AND ASSESSING THE IMPLICATIONS OF

INTERNATIONAL TECHNOLOGY SPILLOVERS

Climate Strategies Workshop Tackling Leakage in a World of Unequal Carbon Prices

4 Feb 2008, Paris, France

Reyer Gerlagh Onno Kuik Economics Institute for Environmental Studies School of Social Sciences Faculty of Earth and Life Sciences University of Manchester Vrije Universiteit, Amsterdam [email protected] [email protected]

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 2/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

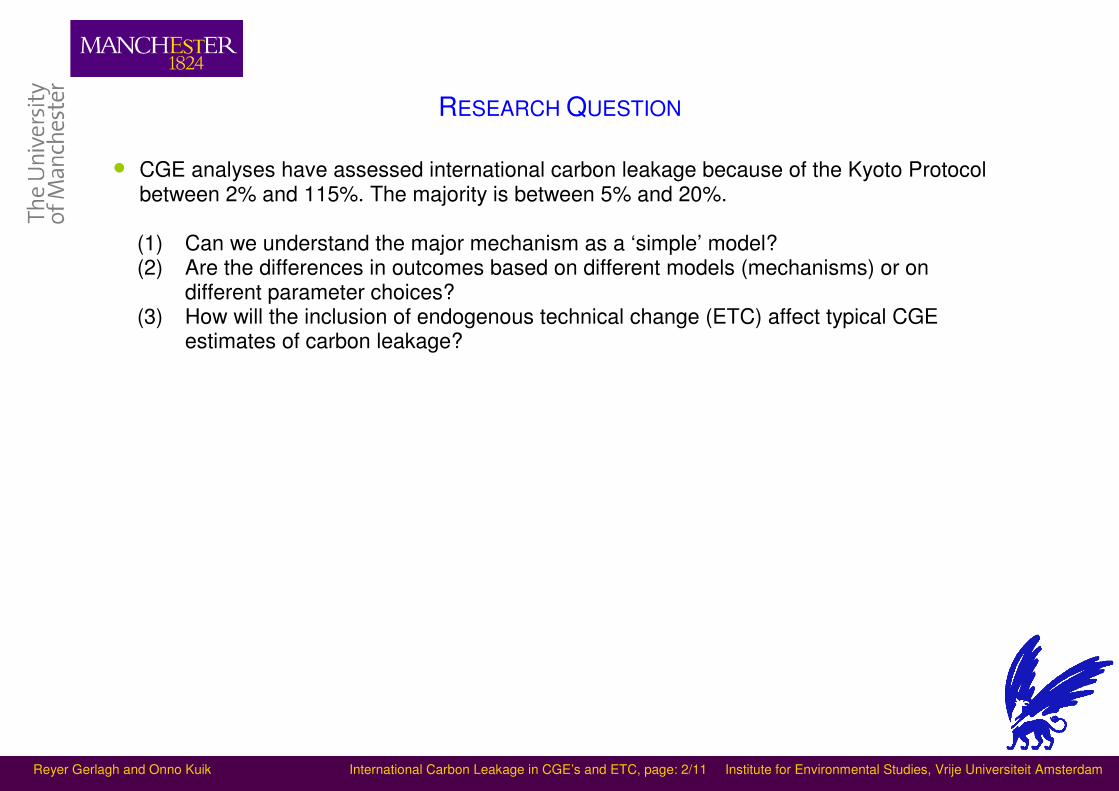

RESEARCH QUESTION

• CGE analyses have assessed international carbon leakage because of the Kyoto Protocol between 2% and 115%. The majority is between 5% and 20%.

(1) Can we understand the major mechanism as a ‘simple’ model? (2) Are the differences in outcomes based on different models (mechanisms) or on

different parameter choices? (3) How will the inclusion of endogenous technical change (ETC) affect typical CGE

estimates of carbon leakage?

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 3/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

TWO SIMPLE CARBON LEAKAGE MODELS, 7-EQUATIONS, SAME BASICS,

• Two countries: Abating A and non-abating B

• θ share of country A in world carbon-energy use

• YA, YB relative change in energy-intensive sector output

• EA, EB relative change in carbon-energy input

• qA, qB output price change

• pA, pB carbon-energy price change

• τA carbon tax in abating country

• ε elasticity of demand for energy-intensive goods

• α carbon-energy share in production costs

• µ elasticity of substitution between carbon-energy and other production factors

• ψ price elasticity of global carbon-energy supply

Define the carbon leakage rate

LR = –[(1–θ)/θ]EB/EA (1)

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 4/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

TWO COMPETING MODELS

• Pollution Haven Model (similar to Di Maria and Smulders 2004): One world market for

energy-intensive intermediates/goods with one output price q

• Energy Market Model: One world market for carbon-energy with one carbon-energy price p

Pollution Haven Model World market Domestic market Carbon-energy X Energy-intensive intermediates (e.g. chemicals) X Energy Market Model World market Domestic market Carbon-energy X Energy-intensive intermediates (e.g. chemicals) X

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 5/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

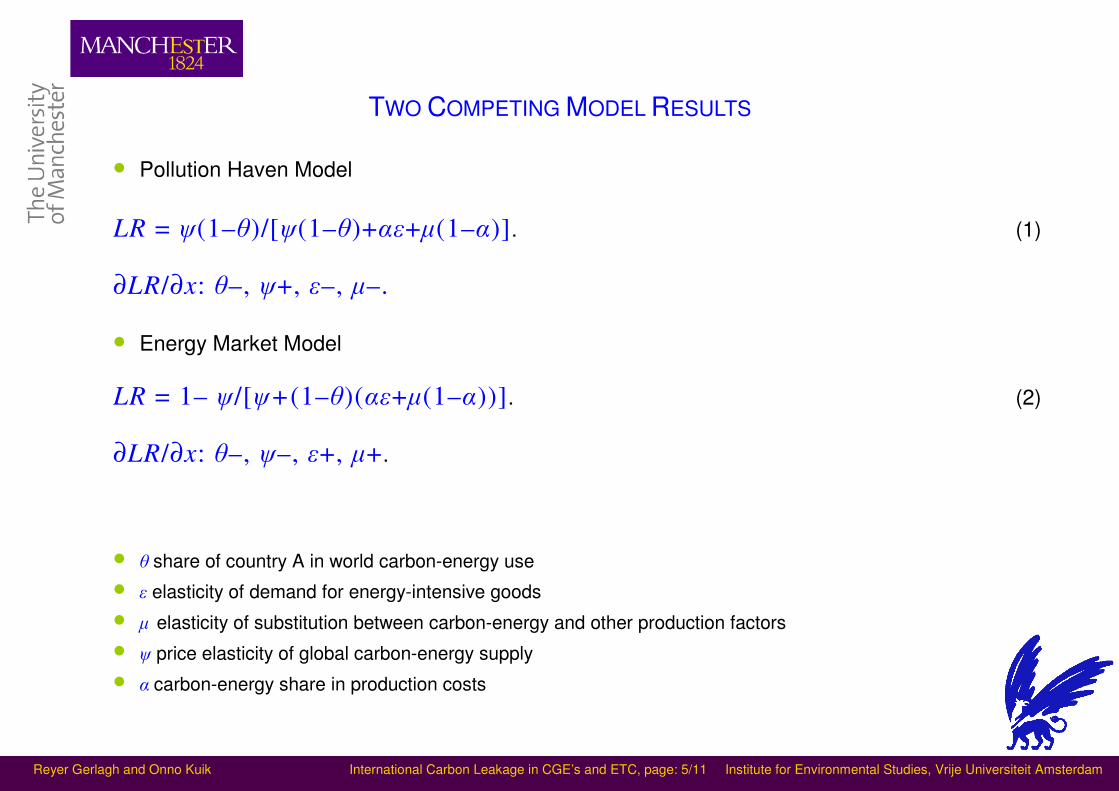

TWO COMPETING MODEL RESULTS

• Pollution Haven Model

LR = ψ(1–θ)/[ψ(1–θ)+αε+µ(1–α)]. (1)

∂LR/∂x: θ–, ψ+, ε–, µ–.

• Energy Market Model

LR = 1– ψ/[ψ+(1–θ)(αε+µ(1–α))]. (2)

∂LR/∂x: θ–, ψ–, ε+, µ+.

• θ share of country A in world carbon-energy use

• ε elasticity of demand for energy-intensive goods

• µ elasticity of substitution between carbon-energy and other production factors

• ψ price elasticity of global carbon-energy supply

• α carbon-energy share in production costs

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 6/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

TESTING THE MODELS WITH CGE CARBON LEAKAGE RATES Table 1. Key results and elasticities in CGEs* Model Source LR ν ψ DEEP Kallbekken,2006,2004 0.06 4 1 G-Cubed McKibbin&Wilcoxon, 1999 0.06 1 1 Gem-E3 Bernard&Vielle, 2000 0.13 6 1 Gem-E3 Bernard&Vielle, 2000 0.04 6 1 GREEN Burniaux&O.Martins, 2000 0.05 4 8 GREEN Burniaux&O Martins, 2000 0.02 4 8 GTAP-E Burniaux&Truong,2002 0.04 19 5 GTAP-E Burniaux&Truong,2002 0.04 19 5 GTAP-E Kuik&Gerlagh,2003 0.16 7 1 GTAP-E Gerlagh&Kuik, this paper 0.14 5 0.6 GTAP-EG Paltsev, 2001 0.11 4 1 MIT-EPPA Babiker&Jacoby, 1999 0.06 3 2.9 MIT-EPPA Babiker,2005 0.20 8 0.8 MS-MRT BMR, 1999 0.19 4 1.5 MS-MRT BMR, 1999 0.16 4 1.5 WorldScan Bollen, 2004 0.17 10 3 Light Light etal,1999 0.21 4 0.5 MIT-EPPA Babiker,2005 1.15 ∞ 0.8 GTAP-E Kuik, 2006 0.15 3.3 0.6

ν = Armington elasticity between imported and domestic energy-intensive goods

ψ = carbon-energy supply elasticity *source: Kuik (2005) with Babiker (2005) and own calculations added

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 7/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

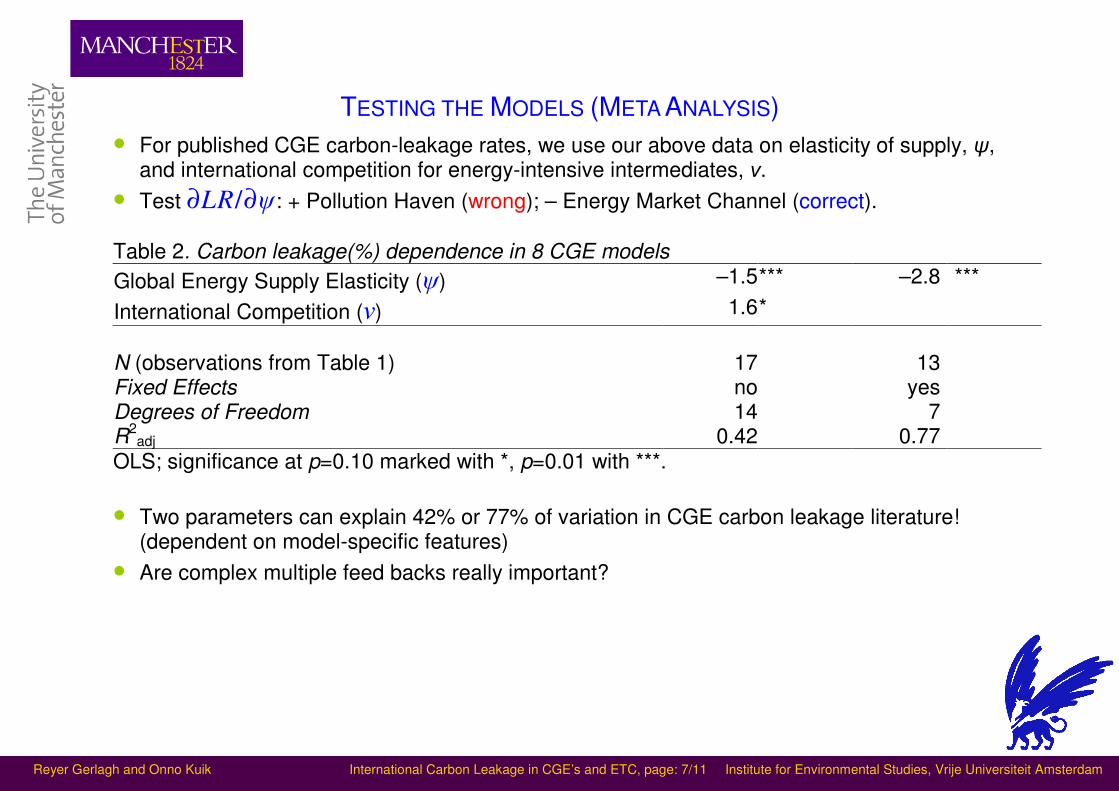

TESTING THE MODELS (META ANALYSIS)

• For published CGE carbon-leakage rates, we use our above data on elasticity of supply, ψ, and international competition for energy-intensive intermediates, ν.

• Test ∂LR/∂ψ: + Pollution Haven (wrong); – Energy Market Channel (correct).

Table 2. Carbon leakage(%) dependence in 8 CGE models

Global Energy Supply Elasticity (ψ) –1.5*** –2.8 ***

International Competition (ν) 1.6*

N (observations from Table 1) 17 13 Fixed Effects no yes Degrees of Freedom 14 7 R2

adj 0.42 0.77 OLS; significance at p=0.10 marked with *, p=0.01 with ***.

• Two parameters can explain 42% or 77% of variation in CGE carbon leakage literature! (dependent on model-specific features)

• Are complex multiple feed backs really important?

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 8/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

WHAT IS INPUT-SAVING TECHNOLOGICAL CHANGE? (WING 2005)

X1 (capital & labour)

X2 (

en

erg

y)

Technology shift: σ–µ= γσ

A

B

blue line: long-term elasticity with ETC = σ

red and green line: elasticity with fixed technology = µ when energy becomes more expensive, equilibrium moves along red line from A to B. Technology adjusts and iso-output line moves from red line to green line. Equilibrium moves from B to C.

C

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 9/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

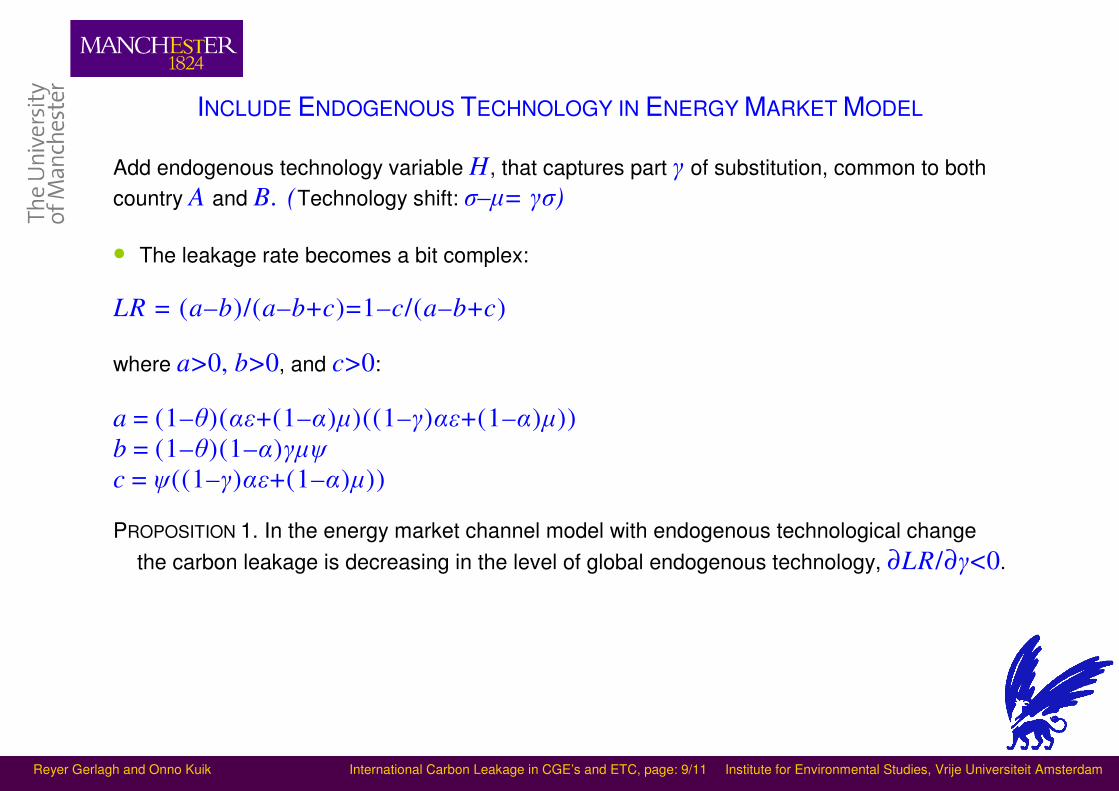

INCLUDE ENDOGENOUS TECHNOLOGY IN ENERGY MARKET MODEL

Add endogenous technology variable H, that captures part γ of substitution, common to both

country A and B. (Technology shift: σ–µ= γσ)

• The leakage rate becomes a bit complex:

LR = (a–b)/(a–b+c)=1–c/(a–b+c)

where a>0, b>0, and c>0:

a = (1–θ)(αε+(1–α)µ)((1–γ)αε+(1–α)µ))

b = (1–θ)(1–α)γµψ

c = ψ((1–γ)αε+(1–α)µ))

PROPOSITION 1. In the energy market channel model with endogenous technological change

the carbon leakage is decreasing in the level of global endogenous technology, ∂LR/∂γ<0.

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 10/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

RESULTS OF GTAP-E WITH INPUT-SAVING LBD TECHNOLOGY

• Carbon leakage decreasing in coalition size + decreasing in technology spillover

-10%

-5%

0%

5%

10%

15%

20%

0.00 0.10 0.20 0.30 0.40

Gamma

Leakage r

ate

(%

)

Annex I + US + Australia Annex I - US - Australia

Reyer Gerlagh and Onno Kuik International Carbon Leakage in CGE’s and ETC, page: 11/11 Institute for Environmental Studies, Vrije Universiteit Amsterdam

OVERALL CONCLUSIONS

• Research answers (1) We can understand carbon leakage in CGEs through a 7-equation model (2) Differences between LR’s assessed by CGE models can largely be attributed to

different parameter values (3) Carbon leakage decreases substantially with ETC and ITS

• Policy answers (4) International technology spillovers can substantially reduce carbon leakage, thus (5) Unilateral climate change policy might be more effective than often suggested (based

on typical economic models that do not acknowledge ETC and ITS)

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Julia ReinaudJulia ReinaudEnergy Efficiency and Environment DivisionEnergy Efficiency and Environment Division

International Energy AgencyInternational Energy Agency©© OECD/IEA,OECD/IEA, 2008

ExEx--post Evaluation of the EU ETS: post Evaluation of the EU ETS: Impacts on the Primary Impacts on the Primary

Aluminium SectorAluminium Sector

““Tackling Leakage in a World of Unequal Tackling Leakage in a World of Unequal Carbon PricesCarbon Prices””

Climate StrategiesClimate StrategiesFebruary 4 2008, ParisFebruary 4 2008, Paris

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Overview1. Competitiveness of the European producers

Sector boundariesTrade flowsEvolution of production costs – focus on power costs

2. Impact of EU Emissions Trading SchemeStatistical tests and analysis on trade flows

3. Preliminary conclusions

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Primary smelters

Alu remelters Alu refiners

Primary ingots

Extrusion (billets): round

Rolling (slabs & billets): rectangular

80% new scrap

Plate, sheet, strip, foilstock, etc.

Rods, sections, shapes,tubes, profiles, etc.

Wires and cable

15% primary and old scrap

Production processesSemi-finished

Casting

Cast ingots, bars, billets and slabs- alloyed/unalloyed

Focus on primary aluminum

Primary Rolling ExtrusionAverage European electricity consumption (kWh/tAl) 15 390 624 667

Source: EAA

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

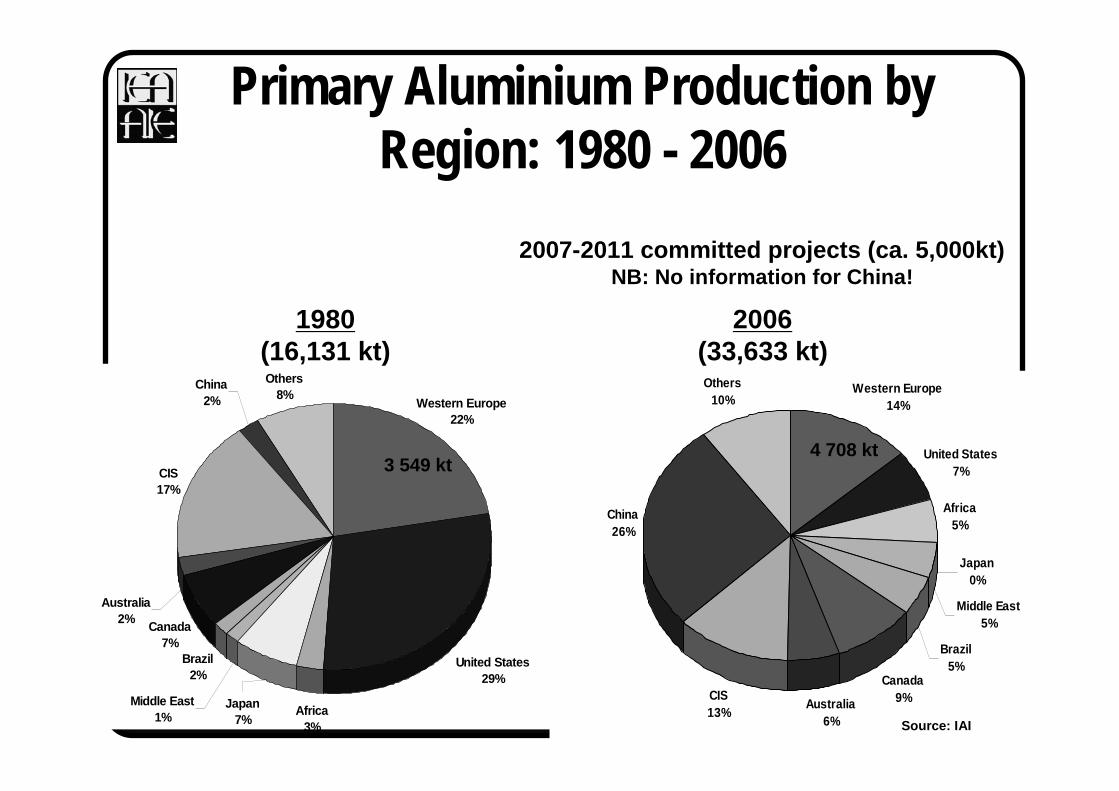

United States29%

Western Europe22%

Others8%

China2%

CIS17%

Australia2%

Africa3%

Brazil2%

Canada7%

Middle East1%

Japan7%

1980(16,131 kt)

2006(33,633 kt)

Primary Aluminium Production by Region: 1980 - 2006

Western Europe14%

United States7%

Africa5%

Japan0%

Middle East5%

Brazil5%

Canada9%Australia

6%

CIS13%

China26%

Others10%

4 708 kt3 549 kt

2007-2011 committed projects (ca. 5,000kt)NB: No information for China!

Source: IAI

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

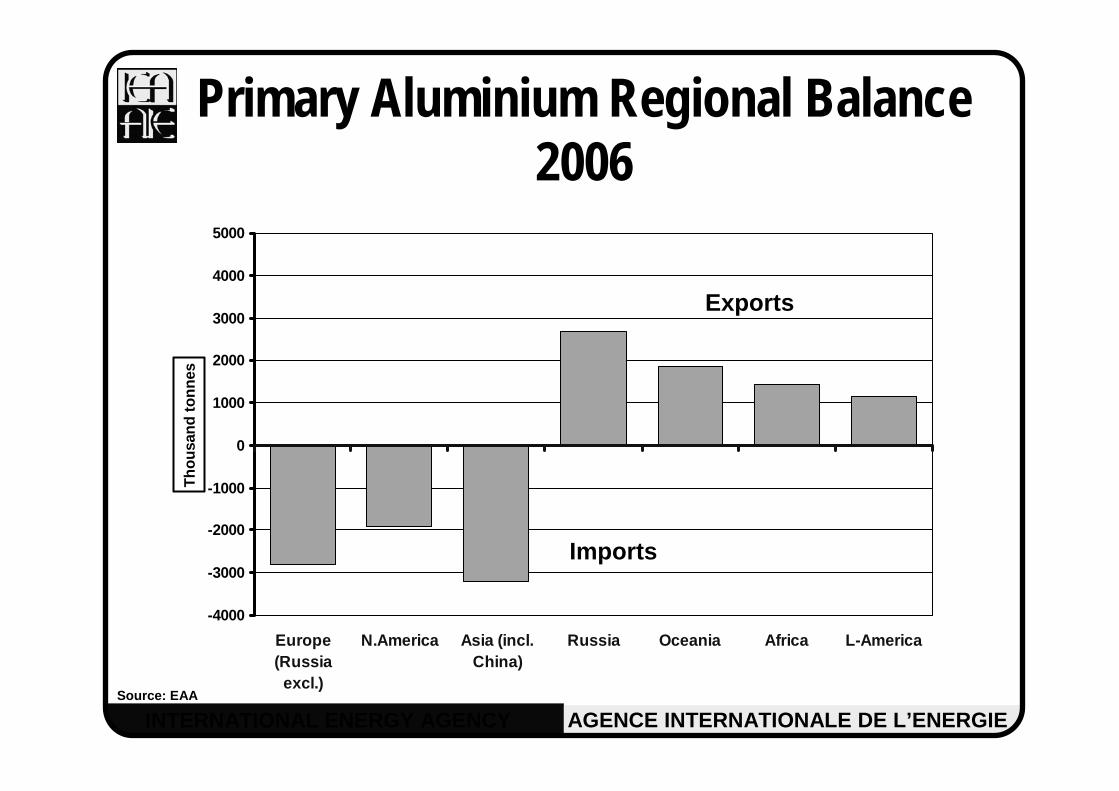

Primary Aluminium Regional Balance 2006

Source: EAA

Exports

Imports

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

Europe(Russia

excl.)

N.America Asia (incl.China)

Russia Oceania Africa L-America

Th

ou

san

d t

on

nes

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1Q/99

4Q

/99

3Q/00

2Q

/01

1Q/02

4Q

/02

3Q/03

2Q

/04

1Q/05

4Q

/05

3Q/06

2Q

/07

ton

nes

NB: Quarterly data = annual * 4

EU 27 exports(intra trade not included)

EU 27 imports(intra trade not included)

EU ETS

EU 27 primary aluminium trade

EU 27 production 2006: 3 055 kt

Source: EAA

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

EU-27 imports of primary aluminium by country of origin (intra EU 27 excluded)

Source: EAA

Top 5 countries represent 71% of total EU imports

since 19990

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1Q/9

9 4Q

/99

3Q/0

0 2Q

/01

1Q/0

2 4Q

/02

3Q/0

3 2Q

/04

1Q/0

5 4Q

/05

3Q/0

6 2Q

/07

China

South Africa

Canada

United ArabEmirates

Iceland

Brazil

Mozambique

Russia

Norway

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

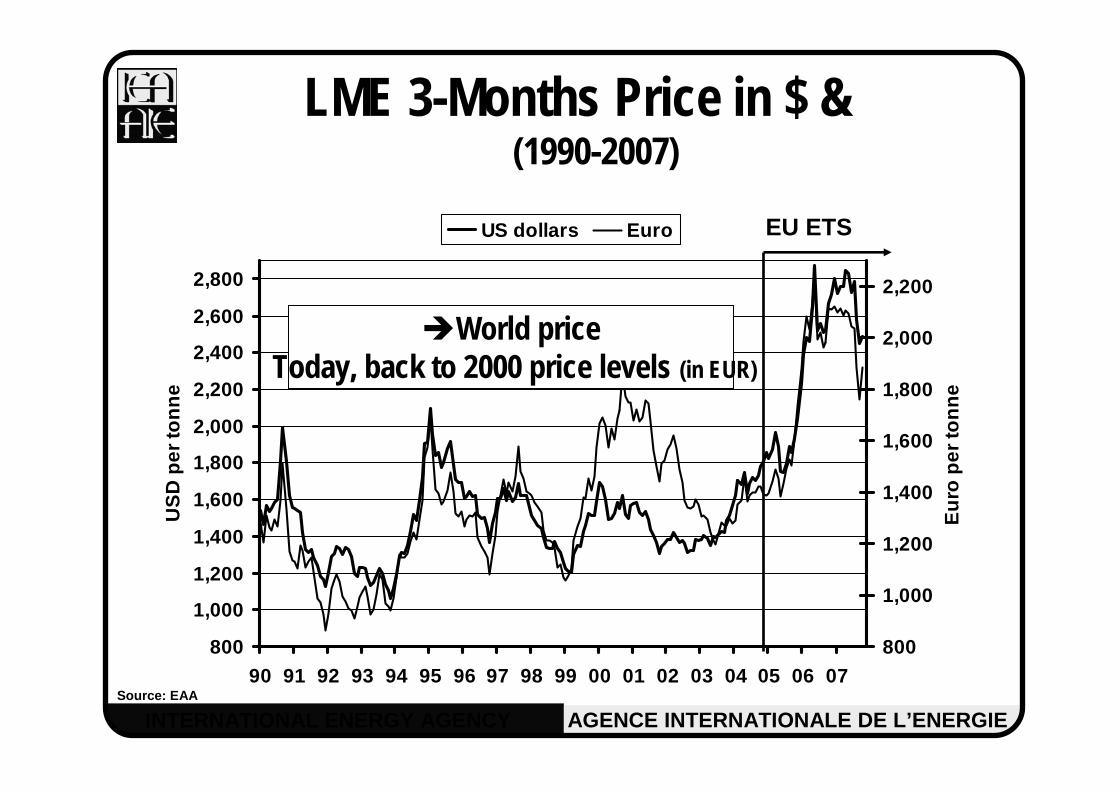

LME 3-Months Price in $ & (1990-2007)

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

US

D p

er to

nn

e

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Eu

ro p

er to

nn

e

US dollars Euro EU ETS

World priceToday, back to 2000 price levels (in EUR)

Source: EAA

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

0

500

1000

1500

2000

Icel

and

No

rway

Ch

ina

Afr

ica

Mid

dle

Eas

t

Ru

ssia

Bra

zil

Can

ada

Wo

rld

EU

27

$/t

Alumina Carbon Anode Labour Power Other

+ 66%+ 50%+ 26%

+ 29%

+ 35%+ 44%

+ 48%

+ 40%

+ 31%+ 44%

2006 cost estimates Variations since 1999

/USD = +16%

Source: CRU www.crugroup.com

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

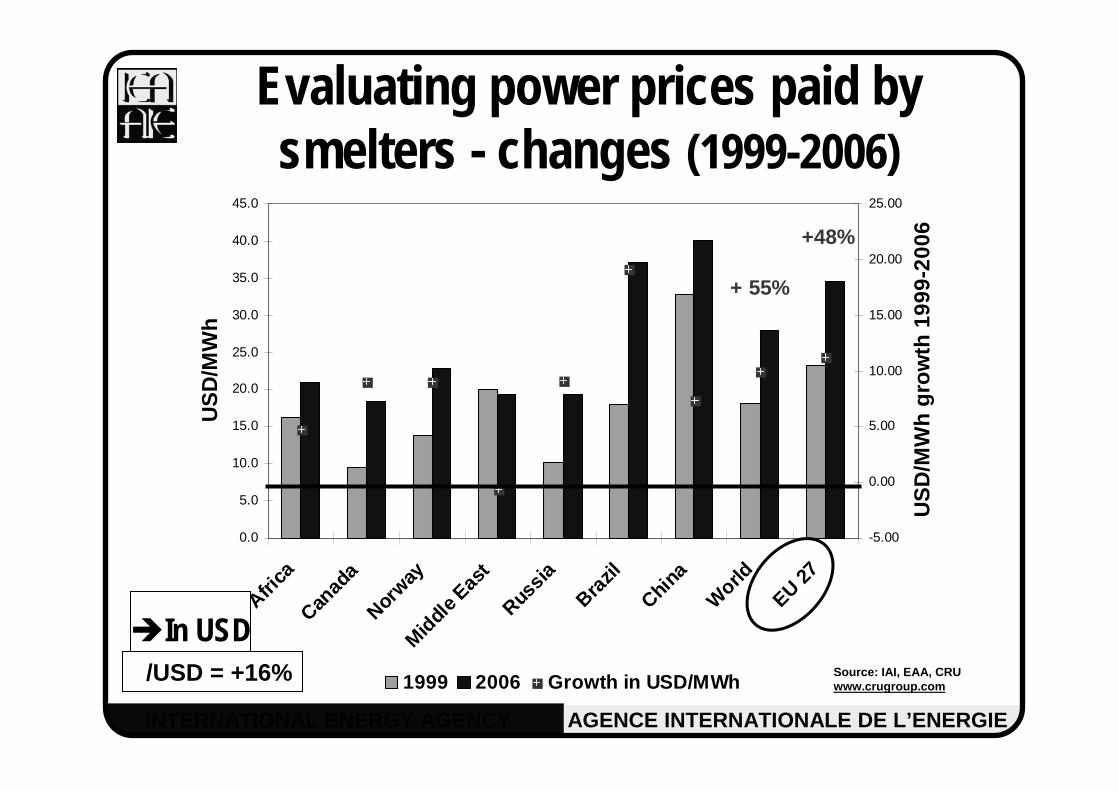

Evaluating power prices paid by smelters - changes (1999-2006)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Africa

Canad

aNor

wayM

iddl

e Eas

tRus

sia

Brazil

China

World

EU 27

US

D/M

Wh

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

US

D/M

Wh

gro

wth

199

9-20

06

1999 2006 Growth in USD/MWh

+ 55%

+48%

In USDSource: IAI, EAA, CRU www.crugroup.com

/USD = +16%

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Estimated power prices paid by smelters (1999 & 2006)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Germ

any

Nether

lands

Easte

rn E

urope

Icela

ndNorw

ay UKFra

nce Italy

SpainEU 2

7

EU

R/M

Wh

0.00

5.00

10.00

15.00

20.00

25.00

EU

R/M

Wh

gro

wth

199

9-20

06

1999 2006 GrowthBased on CRU and EAA www.crugroup.com

Today, only 18% of EU capacity running on wholesale pricesAll long term supply contracts will expire by 2016

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

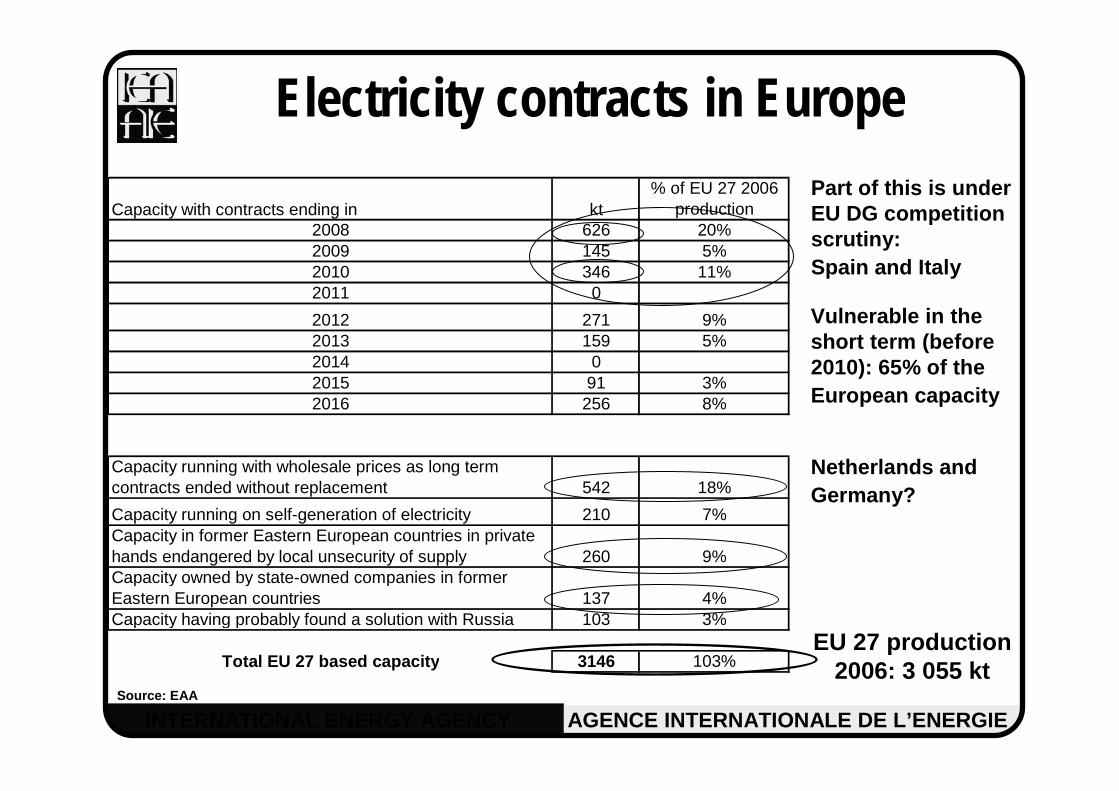

Capacity with contracts ending in kt% of EU 27 2006

production2008 626 20%2009 145 5%2010 346 11%2011 0

2012 271 9%2013 159 5%2014 02015 91 3%2016 256 8%

Capacity running with wholesale prices as long term contracts ended without replacement 542 18%

Capacity running on self-generation of electricity 210 7%Capacity in former Eastern European countries in private hands endangered by local unsecurity of supply 260 9%Capacity owned by state-owned companies in former Eastern European countries 137 4%Capacity having probably found a solution with Russia 103 3%

Total EU 27 based capacity 3146 103%

Electricity contracts in Europe

Vulnerable in the short term (before 2010): 65% of the European capacity

Netherlands and Germany?

Part of this is under EU DG competition scrutiny:Spain and Italy

EU 27 production 2006: 3 055 kt

Source: EAA

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Regional features of European electricity markets

Market prices set by the marginal generator or bidderScandinavia : prices formed on NORD POOL ('merit order' principle – hourly marginal cost of generation)

“Screen prices” with trading of blocks for baseload needsUK : "screen pricing" with trading of blocks (daily, monthly, trimester) + intra-day adjustment mechanisms. Exception to “screen pricing”: CentricaContinental Europe : "screen pricing" for sale of annual blocks + “spot” (day-ahead) + intra-day adjustments

Annual contractsItaly : annual contracts via tenders (fixed or indexed prices)

Regulated tariffsSpain : “regulated” tariffs may be a chosen option – negotiation between industry and generators since 2006 for long term contracts (generation costs based on domestic coal-fired plants) Italy Reinaud, 2007

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Impacts of the EU ETSTrade Flows

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Statistical analysisTesting for CO2 price impact on trade flows of primary aluminium

Quarterly data: Q1 1999 to Q2 2007

Variable: net trade flows in EU 27 EU 27 consumption and productionAluminium price: LME (3 month ahead delivery)

Price premium for delivery in EuropeUS/EUR exchange rateCO2 price

Year ahead price, used as reference for electricity contracts over the next calendar yearAssuming full pass through of CO2 allowance price in electricity prices

Testing for structural change before and after EU ETS

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Statistical results - Europe

No structural changes in trade flows between 1999 and 2006 in Europe

Some details R2 = 0.82Exchange rate USD/EUR: insignificantSignificant variables (in order of importance):

World aluminium priceConsumption CO2 price (starting 2Q 2004)

Negative Negative correlation between COcorrelation between CO22 and net imports: and net imports: invalidates our modelinvalidates our model’’s assumption that COs assumption that CO22 prices should prices should lead to higher importslead to higher imports

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Conclusion (1)Have CO2 prices, through their impact on electricity prices, affected:

EU trade flows of primary aluminium? Not conclusive at EU wide level or at country level

However, looking at electricity costs:EU electricity costs have not increased more than the global averageBut country-by-country analysis shows large differences

Difficult to sort out the role of the ETS: Most smelters are still under long term electricity contracts – some of which are indexed to aluminium prices (high level since 2005)

Has there been carbon leakage? At this stage of the analysis, it is not possible to conclude

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Conclusions (2)However, the story may change…

Post 2012: Direct emissions are coveredHow will trade exposed industries be “treated” in the EU ETS?

End of long term electricity contractsNew business models for electricity contracts?

Source: EAA

Rolling Extrusion RemeltingAnode produced on-

sitePurchased

carbon anodeAverage 2005 emissions (tCO2/t primary aluminium) 2.79 2.39 0.135 0.155 0.184

Primary

Source: IEA, CRU www.crugroup.com

With anode production

Without anode production

Average Europe 46% 45%

Increase in costs (%)

02 mai 2007

Philippe Quirion (CIRED)Based on materials by the IMACLIM-R team at CIRED,

especially Renaud Crassous

0

5

10

15

20

25

2000 2020 2040 2060 2080 2100

A1b. A1f. A1t .A2. B1. B2.REF 450 ppm

An intermediate BAU scenario and a 450 ppm (F4) scenario, peaking in 2020

stabilisation at 450 ppm implies emissions around 4 GtC in 2050, i.e. ½ tC/capita

0

5

10

15

20

25

30

35

2000 2010 2020 2030 2040 2050

€05/

tCO

2

Europe Rest Annex 1Non-Annex 1

0

50

100

150

200

250

300

350

400

2000 2010 2020 2030 2040 2050

€05/

tCO

2

Europe Rest Annex 1Non-Annex 1

CO2 prices in REF and F4 (450 ppm) scenarios

REF F4

- Exogenous emissions trajectory

- Same CO2 price in all sectors but not in all regions

- Hybrid modelling, coupling:- POLES, a partial equilibrium model of the energy sector (+ cement, steel and aluminium) (LEPII, IPTS)

- IMACLIM-R, a recursive general equilibrium model with explicit technologies in residential and transport sectors (CIRED)

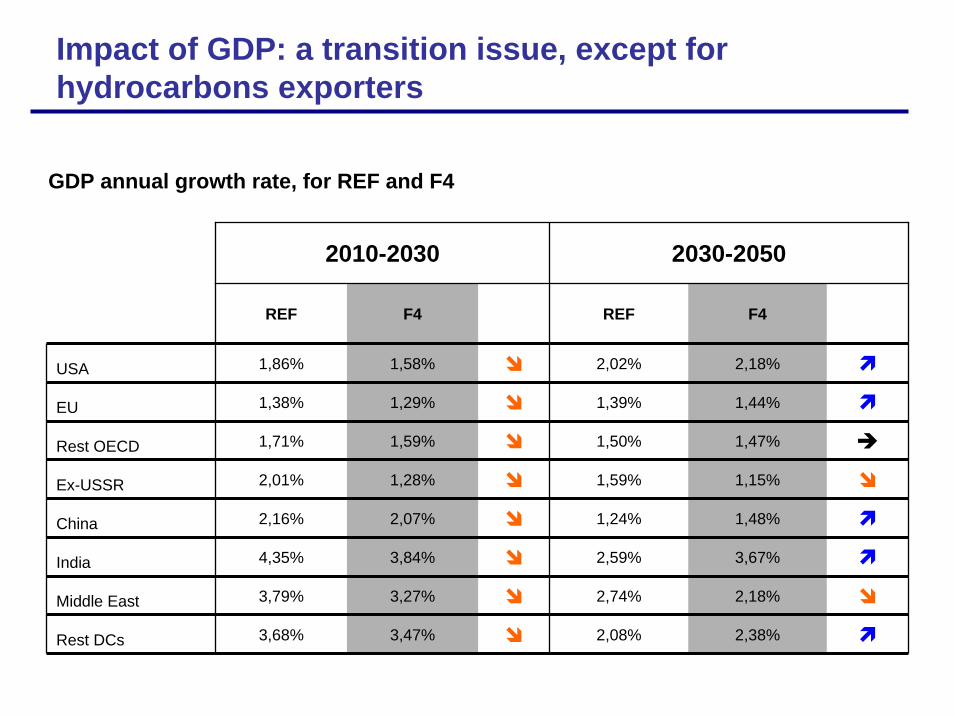

Impact of GDP: a transition issue, except for hydrocarbons exporters

2010-2030 2030-2050

REF F4 REF F4

USA 1,86% 1,58% 2,02% 2,18%

EU 1,38% 1,29% 1,39% 1,44%

Rest OECD 1,71% 1,59% 1,50% 1,47%

Ex-USSR 2,01% 1,28% 1,59% 1,15%

China 2,16% 2,07% 1,24% 1,48%

India 4,35% 3,84% 2,59% 3,67%

Middle East 3,79% 3,27% 2,74% 2,18%

Rest DCs 3,68% 3,47% 2,08% 2,38%

GDP annual growth rate, for REF and F4

Accelerated penetration of low energy dwellings

REF F4

Penetration of Low Energy Dwellings

0%10%20%30%40%50%60%70%80%90%

100%

2000 2010 2020 2030 2040 2050

Standard

Low energy

Very low energy

Penetration of Low Energy Dwellings

0%

20%

40%

60%

80%

100%

2000 2010 2020 2030 2040 2050

Standard

Low energy

Very low energy

Transports: large decrease in oil consumption, very low increase in alternative fuels

REF F4

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2001 2008 2015 2022 2029 2036 2043 2050

Mto

e

Hydrogène

Biocarburants

Electricité

Charbon

Pétrole

Gaz 0

500

1 000

1 500

2 000

2 500

3 000

3 500

2001 2008 2015 2022 2029 2036 2043 2050

Mto

e

Hydrogène

Biocarburants

Electricité

Charbon

Pétrole

Gaz

Impact of the F4 (450 ppm) scenario on materials demand

Steel demand by sector in F4 compared to REF

REF F4

• Steel consumption in buildings: + 22 % in 2050 – Because more re-construction– Despite less steel per building

• Steel consumption in transports: - 32 % in 2050– Because less steel per vehicle– Despite a higher renewal rate

• Steel consumption in other sectors: - 11% in 2050• Overall: - 9% in 2050

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2000 2010 2020 2030 2040 2050

Con

sum

ptio

n (M

t)

Rest

Transport

Building

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Con

sum

ptio

n (M

t)Rest

Transport

Building

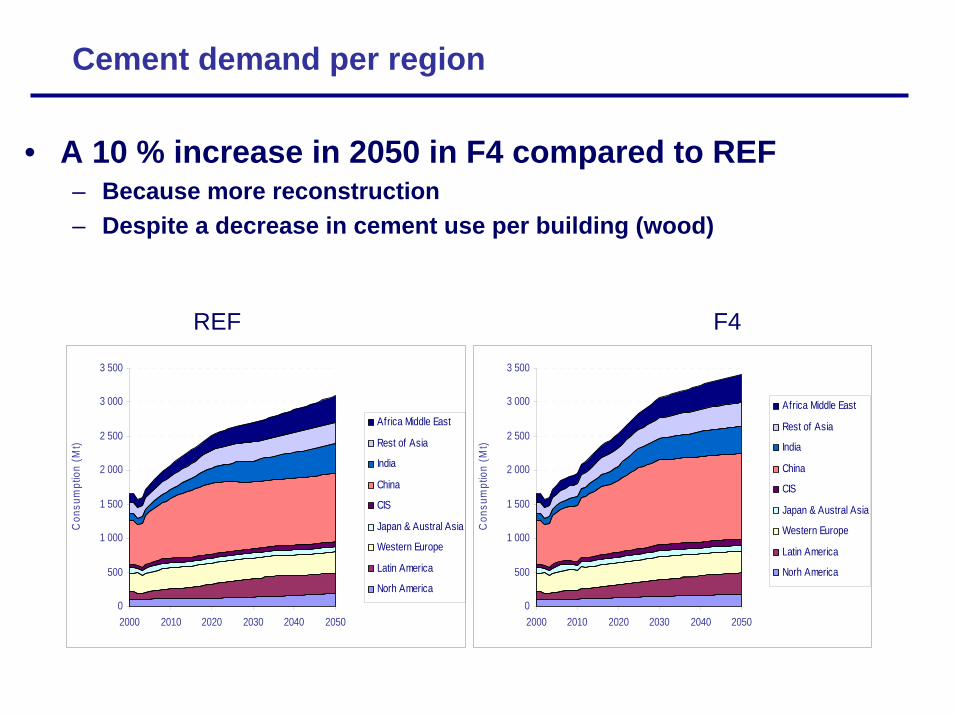

Cement demand per region

REF F4

• A 10 % increase in 2050 in F4 compared to REF– Because more reconstruction – Despite a decrease in cement use per building (wood)

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2000 2010 2020 2030 2040 2050

Con

sum

ptio

n (M

t)

Africa Middle East

Rest of Asia

India

China

CIS

Japan & Austral Asia

Western Europe

Latin America

Norh America0

500

1 000

1 500

2 000

2 500

3 000

3 500

2000 2010 2020 2030 2040 2050

Con

sum

ptio

n (M

t)

Africa Middle East

Rest of Asia

India

China

CIS

Japan & Austral Asia

Western Europe

Latin America

Norh America

Aluminium demand per region

REF F4

• Slight decrease (-7% in 2050) in F4 / REF

0

10

20

30

40

50

60

70

80

2000 2010 2020 2030 2040 2050

Con

sum

ptio

n (M

t)

Africa Middle East

Rest of Asia

India

China

CIS

Japan & Austral Asia

Western Europe

Latin America

Norh America0

10

20

30

40

50

60

70

80

2000 2010 2020 2030 2040 2050

Con

sum

ptio

n (M

t)

Africa Middle East

Rest of Asia

India

China

CIS

Japan & Austral Asia

Western Europe

Latin America

Norh America

Flat glass demand per region

REF F4

• + 63 % in 2050 in F4 / REF– Massive development of double & triple glazing and solar water heaters– More reconstruction

0

20

40

60

80

100

120

2000 2010 2020 2030 2040 2050

Con

sum

ptio

n (M

t)

Africa Middle East

Rest of Asia

India

China

CIS

Japan & Austral Asia

Western Europe

Latin America

Norh America

0

20

40

60

80

100

120

2000 2010 2020 2030 2040 2050

Con

sum

ptio

n (M

t)

Africa Middle East

Rest of Asia

India

China

CIS

Japan & Austral Asia

Western Europe

Latin America

Norh America

What impact on leakage?

• Summary: Glass + 63%, Cement + 10%, Steel - 9%, Aluminium - 7%• For cement, ongoing econometric study on the determinants of net

exports (exports – imports) in the short run– With Neil Walker (UCD) – Separate regressions for France, UK, Germany, Spain and Portugal– 1976-2005– Tested variables: relative cost, available capacities, EU ETS

• Results – EU ETS: never significant– Relative cost: significant only in France and Spain– Available capacities: significant in all countries

• Weakly in France and Germany (hidden by reunification)• Strongly in the UK, Portugal and Spain: 1 more ton of available capacities

0.5 more ton of net exports

• In the short run, increase in cement consumption leakage• What about the long run, i.e., new capacities?

Table 1. Results of model 1

RHS variables (expected sign of the coefficient)

AvailCapi (+) AvailCapSpain (-)

Country Adj. R²

Coefficient Significance level

Coefficient Significance level

France 0.08 0.13 8% NT

UK (1978-2002)

0.53 0.46 1% NT

Germany (1978-89)

0.41 0.06 12% NT

Portugal** 0.45 0.53 1% -0.03 5%

Spain* 0.51 0.42 1% NT

NT: not tested because no relationship expected. * The Durbin-Watson statistic is in the uncertainty zone.

** The Durbin-Watson statistic indicates a positive autocorrelation of residuals

Philippe QUIRION (CNRS, CIRED)Based on a joint work with Damien Demailly (formerly CIRED)

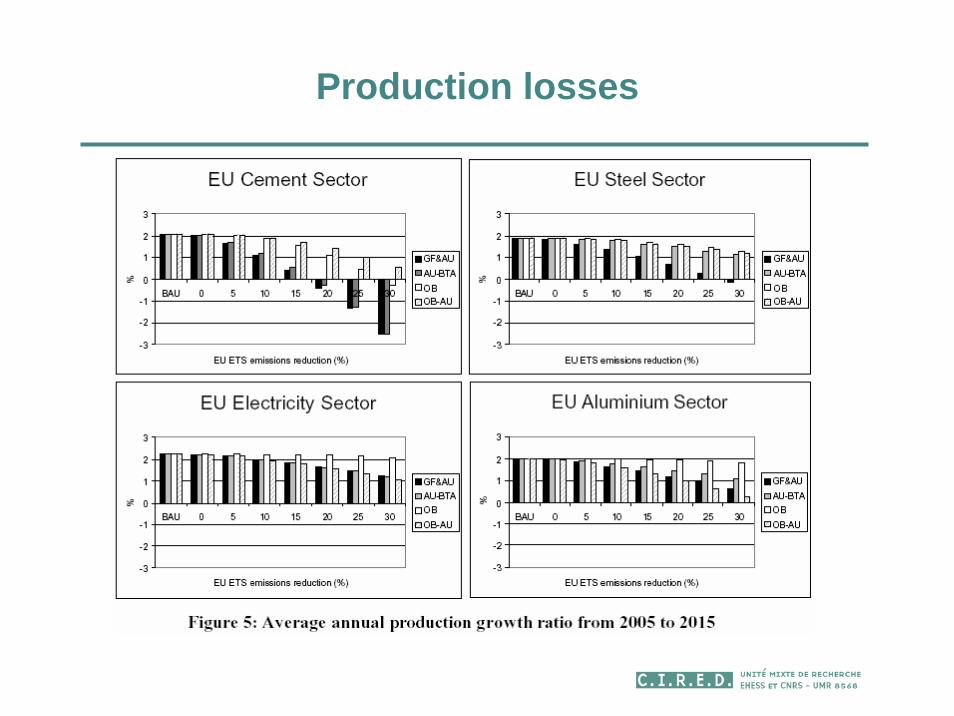

Two Policies to Address Leakage: Border Adjustments and Output-Based Allocation

Climate Strategies Workshop Tackling Leakage in a World of Unequal Carbon Prices

4 February 2008

Free allocation in the EU ETS

• The 2003 directive:• Neither pure lump-sum allocation (as in the US SO2 scheme)

nor pure output-based allocation, rather capacity-based• Various motives for free allocation

1. maintain profits in the covered sectors2. address leakage

• The 2008 revision:• Free allocation mostly in sectors at risk of leakage• Unclear how the free allowances will be distributed

• Economic analysis:• Pure lump-sum allocation cannot address leakage• Output-based allocation can, but is less efficient at least in a

closed economy (e.g. Fischer, 2001; Haites, 2003; Demailly & Quirion, 2006)

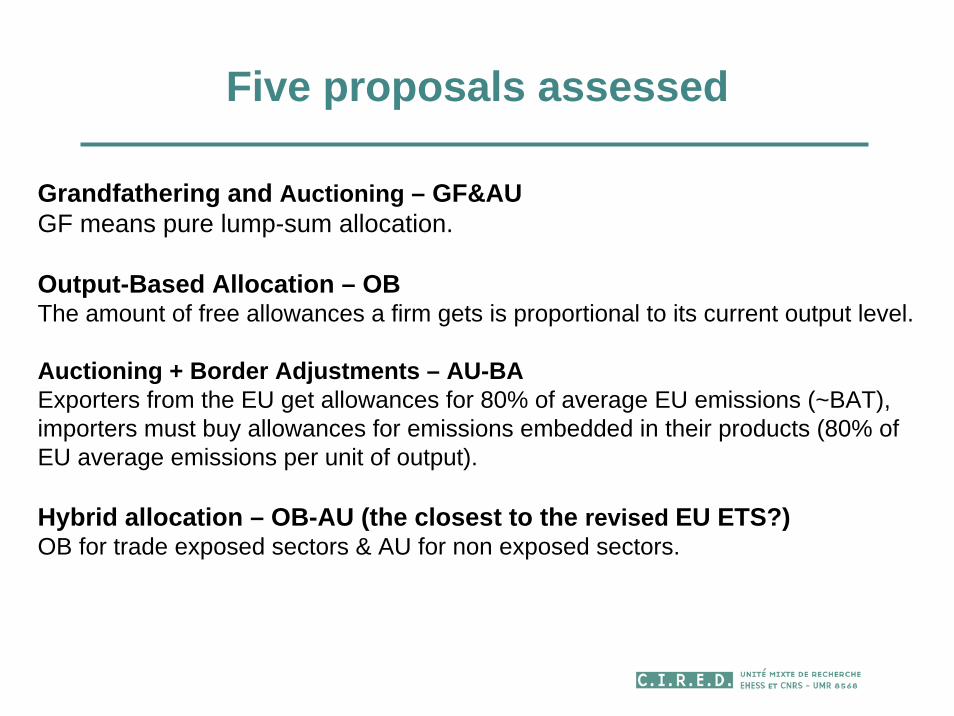

Five proposals assessed

Grandfathering and Auctioning – GF&AUGF means pure lump-sum allocation.

Output-Based Allocation – OBThe amount of free allowances a firm gets is proportional to its current output level.

Auctioning + Border Adjustments – AU-BAExporters from the EU get allowances for 80% of average EU emissions (~BAT), importers must buy allowances for emissions embedded in their products (80% of EU average emissions per unit of output).

Hybrid allocation – OB-AU (the closest to the revised EU ETS?) OB for trade exposed sectors & AU for non exposed sectors.

CASE: 4 sectors and 2 regions

CO2 prices

Production losses

CO2 leakage ratio RoW

UE

EE

Δ=−Δ

EU Welfare lossesw/o benefits of abatement, not accounting for leakage

EU welfare lossesw/o benefits of abatement, accounting for leakage

EU welfare lossesw/o benefits of abatement, accounting for leakage and foreign

welfare losses

Wealth transfers from the RoW to the EU

AU & GF:Increase prices for EU exported goodsTransfer wealth from foreign consumers to EU firms (GF) or budget (AU)

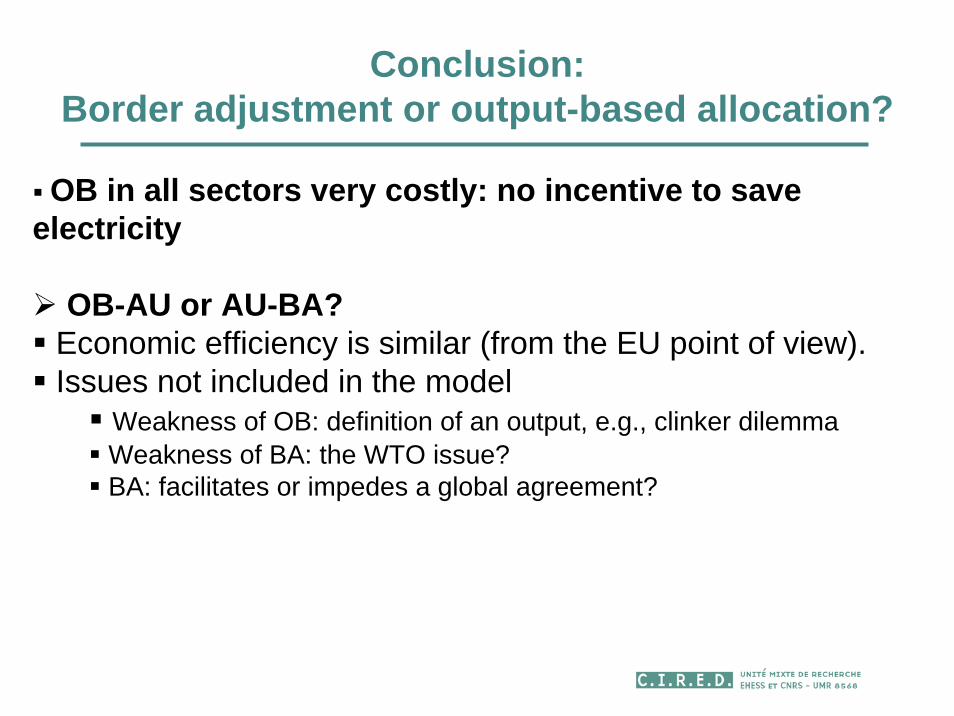

Conclusion: Border adjustment or output-based allocation?

OB in all sectors very costly: no incentive to save electricity

OB-AU or AU-BA?Economic efficiency is similar (from the EU point of view).Issues not included in the model

Weakness of OB: definition of an output, e.g., clinker dilemmaWeakness of BA: the WTO issue?BA: facilitates or impedes a global agreement?

A non-Protectionist Border Economic Adjustment in the Context of

Unilateral EU Post-Kyoto climate Commitments

Olivier GodardCnrs et Ecole polytechnique, Paris

Paris, February 4, 2008

Workshop onTackling Leakage in a World of

Unequal Carbon Prices

• Either no global Post-Kyoto regime is arrived at by 2010, or final national commitments reflect significantly different rates of effort, leading to heterogeneous shadow prices of carbon in different regions of the world

• No international sectoral agreements for exposed sectors (steel, aluminium, cement…)

• The EU sticks to its own agenda (- 20% in 2020 emissions; - 75% in 2050)

• The EU still wants to preserve future options of international cooperation with other states

• The EU remains concerned to set-up domestic measures compatible with WTO rules

• The EU maintains limits to the use of CDM credits in the ETS

Olivier Godard

Assumptions

1. Border economic adjustment (BEA) becomes an obstacle to reaching a multilateral agreement:

(a) because it is perceived as an hostile attitude and cut the willingness of other states to cooperate(b) because some states among key LDCs or other industrialized countries sue the EU before the WTO and take retaliation measures

2. The EU takes unilateral climate commitments without any BEA(a) This self-punishment option is advantageous for import from non-EU countries and reinforces incentive given to them to free-ride, which becomes an additional obstacle to reaching a Multilateral Climate Agreement (MCA)(b) Carbon leakage through loss of markets shares on the EU market and worldwide(c) By losing some industrial power, the EU is weakening its project to become a competitive knowledge economy and losing influence on the international arena.

Two self-defeating strategies

Olivier Godard

1. The BEA should make the new situation less favourable for Non-EU countries than a unilateral climate commitment without BEA, but still more favourable for them than the absence of unilateral commitment of the EU and the corresponding level of industrial competition

2. The EU unilateral commitment and BEA should be presented as one indivisible package

3. BEA should be so designed that it is made the more palatable to the WTO rules as possible

4. BEA should be conceived as a way to supplement and improve rules of ETS, which is a condition for the EU climate targets to be reached

5. Harnessing the BEA as a dynamic incentive leading the technological competition to benefit the climate policy

Key strategic directions for the design of BEA

Olivier Godard

1. Scope:only basic materials (iron, cement, glass, aluminium) and energy products (fuels) being internationally traded and submitted to direct or indirect (impact of increased electricity prices due to carbon constraints) significant CO2 constraints within the Post-2012 ETS perimeter

2. Targets:Every imports of those products from non-EU countries (non-discrimination principle) and, symmetrically exports from EU producersCountries involved in a Post-Kyoto MEA take similar BEA measures regarding the EU and other countries (same as is done for consumer or VAT taxes)

3. Two bases of adjustment:the EU sectoral rate of effort and the BAT counterfactual

Features of a EU Border Economic Adjustment

Olivier Godard

4. Principles:1. combining action on imports and action on exports2. Imposing on imports an effort inferior to the EU one3. Avoiding cumbersome task of searching information on

specific production processes abroad and making it through the reference to BAT

5. A preferred way for implementation2. An obligation for importers to buy Q permits on the EU

GHG market or CDM and JI credits Q = Qimp X effort rate X BAT specific rate of direct and indirect (electricity) emissions with Qimp = quantities of imported products

Avoids the first source of carbon leakage3. Remittance of GHG quotas to EU exporters from a

dedicated reserve taken from the gross capAvoids the second source of carbon leakage

(assumption of indivisible productive assets for both the EU market and exports for the world market)

Features of a EU Border Economic Adjustment

Olivier Godard

6. The formula:• A European sectoral rate of effort would have two

components:– The gap between the sectoral EU BAU emissions and the

sectoral amount of EUAs allocated for free:

Features of a EU Border Economic Adjustment

Olivier Godard

)r)(g(eeergee

iiielect

iciiielect isectorEU eachrate for Effort−+

−−+

+

+=11)(

)1)(1()(

With et the direct emissions in reference year t,eelec

i the amount of EUAs incorporated in power consumption needed to get the output of sector i, ec the share of EUAs given for free for the next period,g the expected growth rate of the sectors covered by the scheme for the next period,r the rate of carbon efficiency progress expected in the sector per product for the next period

7. An example with the sector of cement:• Emission rate of BAT: 0.7tCO2eq/tcement;• Sectoral rate of effort: 20%;• Candidate to imports: 40 Mt cement• BEAcement = 40 M X .20 X .7 = 5.60 MtCO2eq to buy on

the market• If the value of 1 EUA by 2013 is 30 €, it means an

overcost to import of 168 M€, or 4.2 €/tcement.• With a EU price of cement of 65€/t, it means a BEA of

6,5% of the cement’s price • With full auction for the EU cement sector, the BEA

would come to 32.5% of the EU market price• The only difference between importers and EU

producers would then find its origin in technological efficiency

Features of a EU Border Economic Adjustment

Olivier Godard

8. A mechanism delivering incentives both for EU and non-EU producers

– The more EU producers incorporate BAT technologies, the more they reduce the gap of treatment between them and importers on the EU market and the more they benefit of restitutions of quotas for exports, and.

– Non-EU producers have an incentive to develop new climate-friendly technologies: it will change the BAT and increase their benefits from the gap between the BAT and EU current technology.

industrial competition will become a driver for enhancing climate policy Olivier Godard

Features of a EU Border Economic Adjustment

Compatibility depends on several conceptual assimilations:

• Can the obligation of EU firms to surrender EUAs at the end of each period be said a tax in WTO words? Yes (compulsory, without counterpart, EUAs have a market value)

• Can GHGs emissions be said inputs of production processes? Yes since they are consumptions of units of carrying capacity of the atmosphere under a climate limit

• Can the atmosphere be said a scarce non renewable resource as regards the climate issue? Yes since, for any human time horizon, interference with the climate system will last for numerous centuries

Conclusion: which compatibility with WTO rules?

Olivier Godard

BEA meets several WTO requirements• Imported products are not treated less favourably than domestic

ones (principle of national treatment – Article III of GATT)

• Border measures for protecting non renewable resources are accepted (authorized environmental exceptions - Article XX(g))

• The BEA is not arbitrary and is based on sound justifications regarding the environmental goal (avoiding carbon leakage and enhancing international cooperation to address a global issue (chapeau of Article XX)

• The BEA is respectful of the sovereignty of other countries (it doesnot impose domestic technologies to others)

• The BEA dos not introduce unjustified discrimination betweennon-EU countries

• The EU has a direct interest in having the global climate protectedfrom a dangerous evolution

Conclusion: which compatibility with WTO rules?

Olivier Godard

Roland Ismer(Faculty of Law)

The Legal FrameworkWhat are the Limitations to Border Taxes?

Border Tax Adjustments

Roland Ismer February 4, 2008 2

I. Border Tax Adjustments – The Rationale

- Climate change requires price signal on

Carbon

- Different willingness in different countries

- Result may be leakage

- BTA as a „Decompression Chamber“

(Godard)

Border Tax Adjustments

Roland Ismer February 4, 2008 3

II. Definition

Border Tax Adjustments (BTA) are fiscal measures designed to

(i) relieve exported products of some or all of the tax charged in the exporting country in respect of similar domestic products sold to consumers on the home market; or

(ii) impose on imported products some or all of the tax charged in the importing country on similar domestic products

Border Tax Adjustments

Roland Ismer February 4, 2008 4

III. Importance of Legality under WTO

- Otherwise possible retribution

- Maintains good-will

- Provides confidence for investors (long-term

sustainability of scheme)

- No clearance mechanism

- NB: WTO-Legality may not be absolutely

necessary

Border Tax Adjustments

Roland Ismer February 4, 2008 5

III. Importance of Legality under WTO

- Illegal subsidy/discrimination?

- Justification for discrimination?

Avoid discrimination illegal

subsidy/

AND/OR

Provide justification

Border Tax Adjustments

Roland Ismer February 4, 2008 6

1. Illegal Subsidy/Discrimination

a) EXPORTS: Avoid Illegal Subsidy!

- Prior-stage cumulative taxes adjustable

- Allowances as taxes?

- Adjustable taxes? Only if incorporated!

Fn. 61 to Annex II?

- At what level?

- Generally no justification for subsidies (but: symmetry as

overriding argument?)

Border Tax Adjustments

Roland Ismer February 4, 2008 7

1. Illegal Subsidy/Discrimination

• IMPORTS: Avoid discrimination under Art. III: 2 Sent. 1 GATT ("like products")

- Product based- Energy input incorporated?- No discrimination if deemed usage of best

available technology (P of recycling)- Issue: Electricity!- Alternative: use average, and allow for

refuting conjecture (American Superfund)?

Border Tax Adjustments

Roland Ismer February 4, 2008 8

1. Illegal Subsidy/Discrimination

c) IMPORTS: Avoid Discrimination under Art. III: 2 Sent. 2 GATT (Directly competitive and substitutable products)

Border Tax Adjustments

Roland Ismer February 4, 2008 9

1. Illegal Subsidy/Discrimination

• IMPORTS: Most Favored Nation Treatment under GATT (Art. I GATT)

Participation in Kyoto or succeeding Protocol as reason for different treatment? Possibility of linking schemes?

Border Tax Adjustments

Roland Ismer February 4, 2008 10

1. Justification under Art. XX GATT

Two tier structure:

a) Any of the eight headingsb) Châpeau

Judiciary has sometimes been generous;yet example of ECJ suggests, where available,avoiding discrimination is safer option

Border Tax Adjustments

Roland Ismer February 4, 2008 11

V. Lawyers Can be Creative: How to Implement It?

- How to adjust: Taxes or allowances? - Framework convention (as under Customs

Law)?- Imputation of export taxes?- Imputation of costs for allowances in home

country? (Linking)- Definition of BAT?

Border Tax Adjustments

Roland Ismer February 4, 2008 12

VI. Conclusion

Issues• BAT or Average Technology as Refutable

Conjecture • Electricity?• Subsidies for exports not justifiable?!

US Climate Policy – Trade Policy Intersections: Current Status,

Prospects and Implications for Carbon Leakage

Thomas L. Brewer

Presentation for Climate Strategies Workshop – Paris -– 4 February 2008

Brewer - Climate and Trade Policy Intersections

2

Outline of Comments

I. Objectives

II. Overview of types of climate-trade intersections

III. Two Key Senate Bills

IV. Political context

V. Suggestions

Brewer - Climate and Trade Policy Intersections

3

Objectives

Agenda setting

Issue framing

Problem solving

Brewer - Climate and Trade Policy Intersections

4

Overview of types ofclimate-trade intersections

• Offsetting border measures• Tariff and NTB reductions• Aviation and shipping industries• Export and outward FDI promotion• International technology cooperation agreements• Program budgets• Subsidies for renewables and energy efficiency• Product labeling and standards• Government procurement

Brewer - Climate and Trade Policy Intersections

5

Two Key Cap-and-Trade Proposals in US Senate

Bingaman-Specter (S.1766, Title V)Lieberman-Warner (S. 2191, Title VI)Offsetting border measures from: American

Electric Power & International Brotherhood of Electrical Workers

Require US importers to purchase GHG emission allowances to offset …‘covered’ goods from ‘covered’ countries

Issue Framing

International competitiveness issue

International trade ‘level playing field’ issue

Not climate change ‘carbon leakage’ issue

Brewer - Climate and Trade Policy Intersections

6

Brewer - Climate and Trade Policy Intersections

7

Political Situation

>Trade is problematic issue for Democrats>Split within business community:

opposition by National Foreign Trade Council

>Climate change is still partisan issueLieberman-Warner (S. 2191) passed committee by 11-8 vote…For: 10 Dems + 1 RepAgainst: 8 Reps + 0 Dems

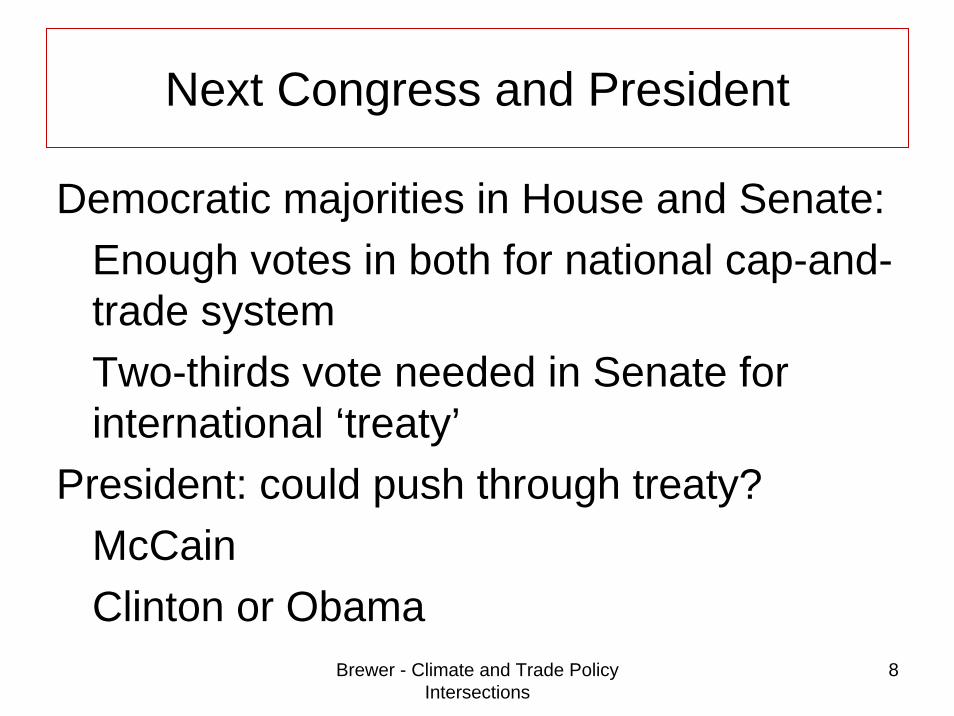

Next Congress and President

Democratic majorities in House and Senate:Enough votes in both for national cap-and-trade systemTwo-thirds vote needed in Senate for international ‘treaty’

President: could push through treaty?McCainClinton or Obama

Brewer - Climate and Trade Policy Intersections

8

Brewer - Climate and Trade Policy Intersections

9

Suggestions

• Include explicit statement in legislation: US support for multilateral climate and trade institutions

• Allow participation of US importers in foreign offset projects as well as purchases of USG ‘international allowances’

• Incorporate offsetting border measures in post-2012 ‘sectoral’ agreements

• Propose (jointly with EU) free-rider trade sanctions in post-2012 multilateral climate regime

Brewer - Climate and Trade Policy Intersections

10

For further information and comments

www.usclimatechange.com

The China Factor

Major EU Trade Partners’ Policies to Address Leakage

Bernice LeeHead, Energy, Environment and Development Programme

4th February 2008

2

The China factor

Key challengesPositive signals on climate changeWhat China really wants, or needs…Areas for EU-China cooperation

3

Growing energy consumption and emissions

Consumption: Until 2030, expected to grow by 2.9% in China p.a.

High net importer of oil: until 2030, China will import 80% of its oil supply.

Emissions: preliminary estimates for 2006 China topped the list of CO2 emitting countries. But per capita energy consumption in China is three times less than the EU.

Six key sectors: Metals, power, steel, oil refining, chemicals and construction materials consume 70% of China’s energy for industry.

4

Increasing concerns over climate change and environmental impacts

Managing domestic climate change impacts: water stress, shifting agricultural zones, and extreme weather events.

Environmental impacts: Farms are losing over US2.5Bn a year to pollution. (SEPA, 2007) Sixteen out of the world’s twenty most polluted cities are in China. (World Bank, 2007)

China is vulnerable to environmentally driven social stresses: land degradation, water reductions and predicted decreases in Chineseagricultural output by 10-30%. Initial evaluation by SEPA – around 10 million hectares of farmland (10%) is polluted.

Managing external instability: China, like the EU, has strong interests in reducing the risk of climate change driven instability in Central Asia, Africa and the Middle East.

5

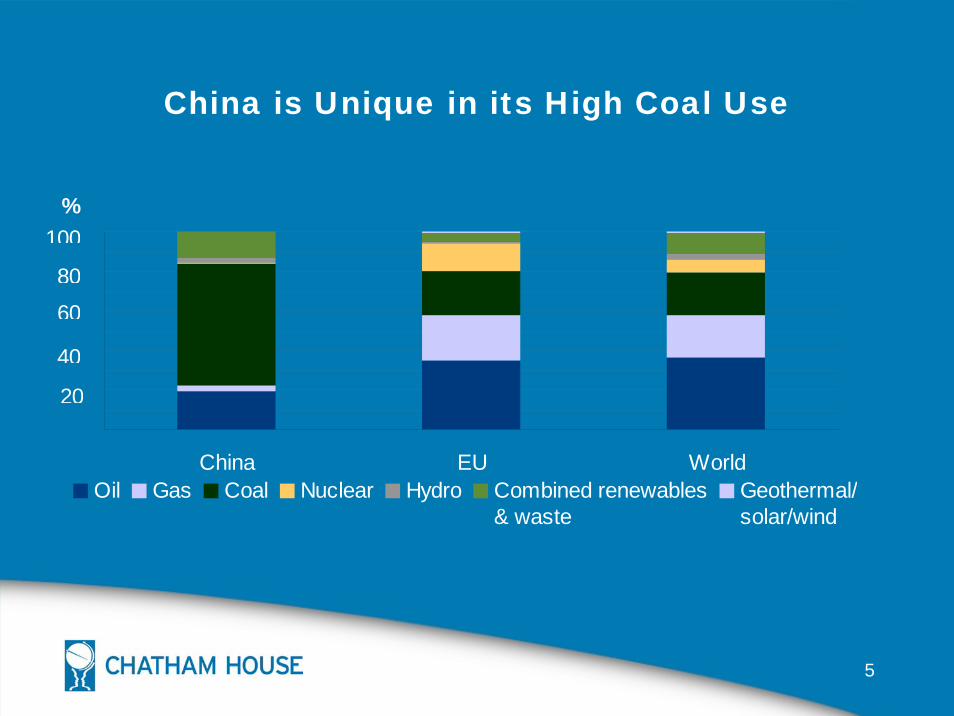

China is Unique in its High Coal Use

China EU WorldOil Gas Coal Nuclear Hydro Combined renewables

& wasteGeothermal/solar/wind

40

20

60

80

100%

6

Challenges:Aging infrastructure means significant new energy investment anticipated in China, the EU and the US

Source: IEA, 2006; Euroelectric 2007

New Electricity Capacity 2005-2030 GW

0

200

400

600

800

1000

1200

US EU Japan Russia China India MiddleEast

Africa LatinAmerica

7

Narrow opportunity to avoid locking-in new power capacity by 2030

China, total new capacity 1258 GWCoal

50 GW to close900 GW additional to 2005 capacity

EU, total new capacity 435 GW, 427 GW replacementCoal

Closure 100-200 GW30 GW of additional to 2005 capacity

Constructing these facilities with conventional technology would both increase emissions immediately and reduce opportunities for switching to less polluting sources in the future

China will invest before Europe and could help drive down the cost of low emission power technologies

8

57%25%

7%

11% 6%

4%

9%

5%14%

16%

32%

27%7%

9%

21%

4%

45%

14%

22%

19%

6%4%9%

16%Space heating Cooling Water heating Cooking Lighting Others

EU residential buildngs’ energy use EU commercial buildings’ energy use

China residential buildings’ energy use China commercial buildings’ energy use

• Accounts for 20% of China’s final energy consumption (compared to 40% of the EU)

• By 2020, new buildings in China total 20 billion m2 = total EU-15 current building stock

• China housing program uses 20% of steel and 17.6% cement.

China has yet to lock-in inefficiency in the building sector

9

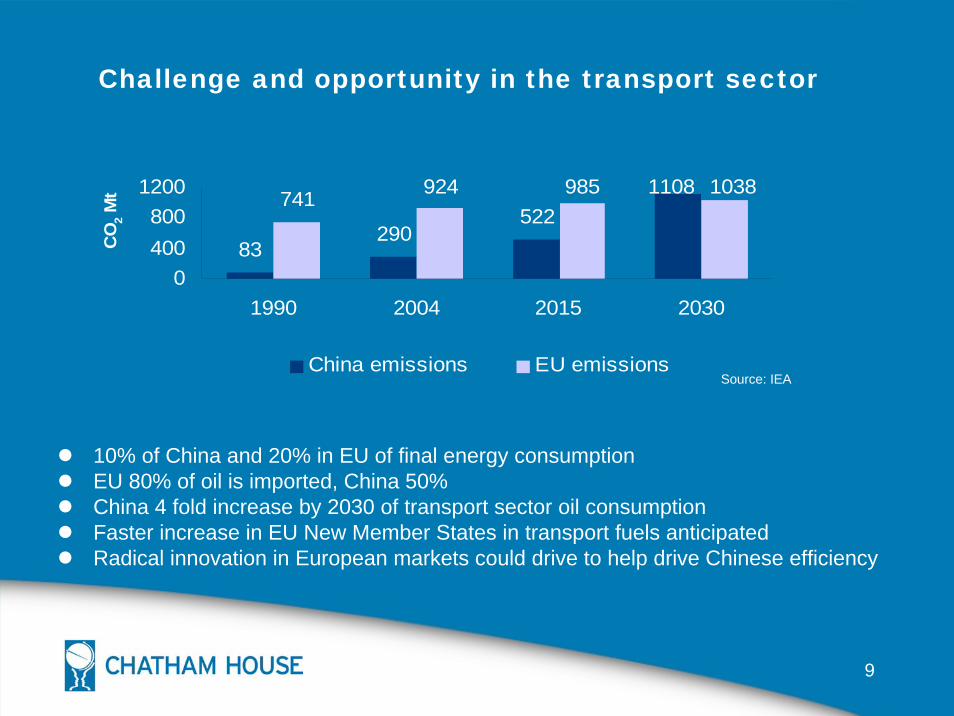

Challenge and opportunity in the transport sector

10% of China and 20% in EU of final energy consumptionEU 80% of oil is imported, China 50%China 4 fold increase by 2030 of transport sector oil consumptionFaster increase in EU New Member States in transport fuels anticipatedRadical innovation in European markets could drive to help drive Chinese efficiency

Source: IEA

83290

522741 924 985 1108 1038

0400800

1200

1990 2004 2015 2030

China emissions EU emissions

CO

2 Mt

10

Energy and climate concerns threaten Chinese domestic stability

More important

Less important

Harder Easier

Political stability

Food security

Relations with resource rich

regions

Energy services

for all

Employment creation

Energy independence/ Price stability

Reducing emissions

Clean coal technologies

Clean water

Extending growth to

poor regions

Tackling climate impacts

Maintaining Economic

growth

Domestic Stability

Energy Security

Improving energy

efficiency

Water security

Reform of State-owned enterprises

Territorial dispute in the South China

Sea

Clean air Improving

environmental protectionClimate security &

dealing with environmental

degradation

Reducing external threats Reducing

trade surplus

Dealing with external threats

Increased weight in

international affairs

Value addition

production

Increasing technological

know-how

Improve relations with neighbours

Respect in the

international system

Regional influence

Economic Security

Increasing Role in International

Affairs

11

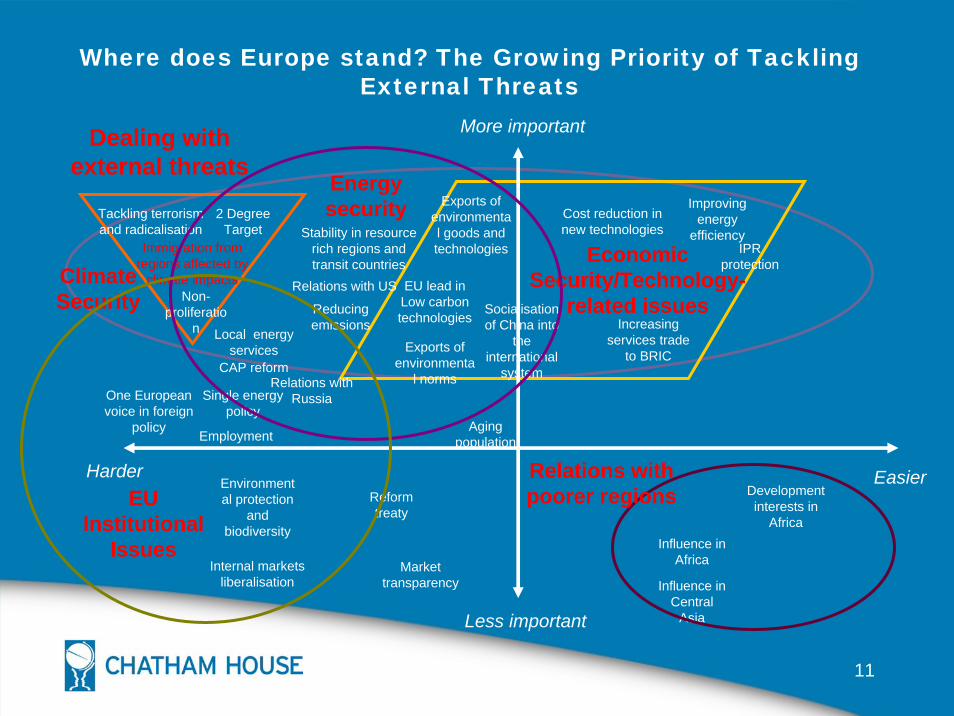

Where does Europe stand? The Growing Priority of Tackling External Threats

More important

Less important

Harder Easier

Immigration from regions affected by

climate impacts

Stability in resource rich regions and transit countries

EU lead in Low carbon technologies

Aging population

Local energy services

Reducing emissions

CAP reform

Tackling terrorism and radicalisation

2 Degree Target

Climate Security

Energy security

Dealing with external threats

Exports of environmenta

l norms

Exports of environmental goods and technologies

One European voice in foreign

policy

Relations with Russia

Relations with US

Employment

Single energy policy

Non-proliferatio

n Increasing services trade

to BRIC

Improving energy

efficiencyEconomic

Security/Technology-related issues

Cost reduction in new technologies

IPR protection

Socialisation of China into

the international

system

Development interests in

AfricaInfluence in

Africa

Influence in Central

Asia

Environmental protection

and biodiversity

EU Institutional

Issues

Reform treaty

Market transparency

Internal markets liberalisation

Relations with poorer regions

12

Hard Easy

Important

Not important

Hard Easy

Important

Not important

EUChina

Mapping Common Interests between the EU and China

Tackling climate impacts

Climate security and dealing

with environmental degradation

Energy Security

Dealing with external threats

Economic Security

Domestic Stability

Energy security

Dealing with

external threats

Climate Security

Economic Security/

Technology-related issues

13

Some positive political signals from China on climate change

1. First National Climate Change Assessment (Dec 2006)

2. China’s National Climate Change Programme (Jun 2007)

3. Public action on energy conservation and pollutant discharge reduction issued by the State Council (May 2007)

4. Policy statements around G-8 (Jul 2005 and Jun 2007)

5. Premier Wen Jiabao (State Council Executive Meeting, 11 Jul 07), "All levels of government must realize fully the grimness and urgency of achieving the energy saving and emission reduction targets." Xinhua

6. National Medium-and Long-term Science and Technology Development Plan (2006-2020) –an innovation oriented economy

7. Middle and Long Term Program of Renewable Energy Development Sep 2007 issued by the NDRC

8. 17th Party Congress: ‘science-based development’ Oct 2007

9. Wen Jiabao statement in the East Asia Summit (Nov 2007) On climate change, "China will shoulder its due international responsibilities and obligations.”

14

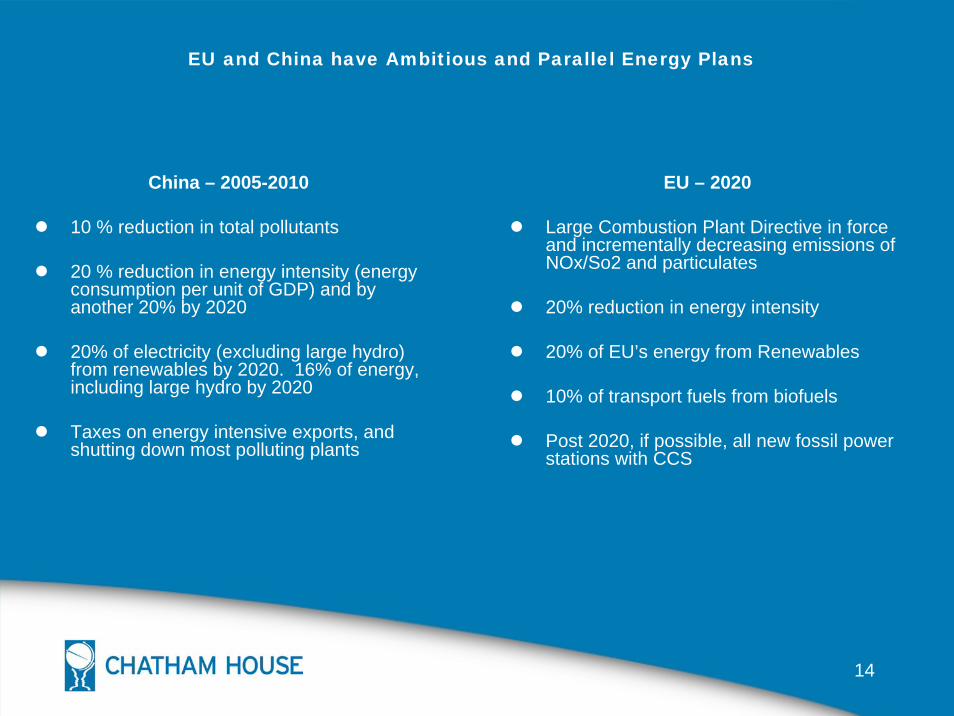

EU and China have Ambitious and Parallel Energy Plans

China – 2005-2010

10 % reduction in total pollutants

20 % reduction in energy intensity (energy consumption per unit of GDP) and by another 20% by 2020

20% of electricity (excluding large hydro) from renewables by 2020. 16% of energy, including large hydro by 2020

Taxes on energy intensive exports, and shutting down most polluting plants

EU – 2020

Large Combustion Plant Directive in force and incrementally decreasing emissions of NOx/So2 and particulates

20% reduction in energy intensity

20% of EU’s energy from Renewables

10% of transport fuels from biofuels

Post 2020, if possible, all new fossil power stations with CCS

15

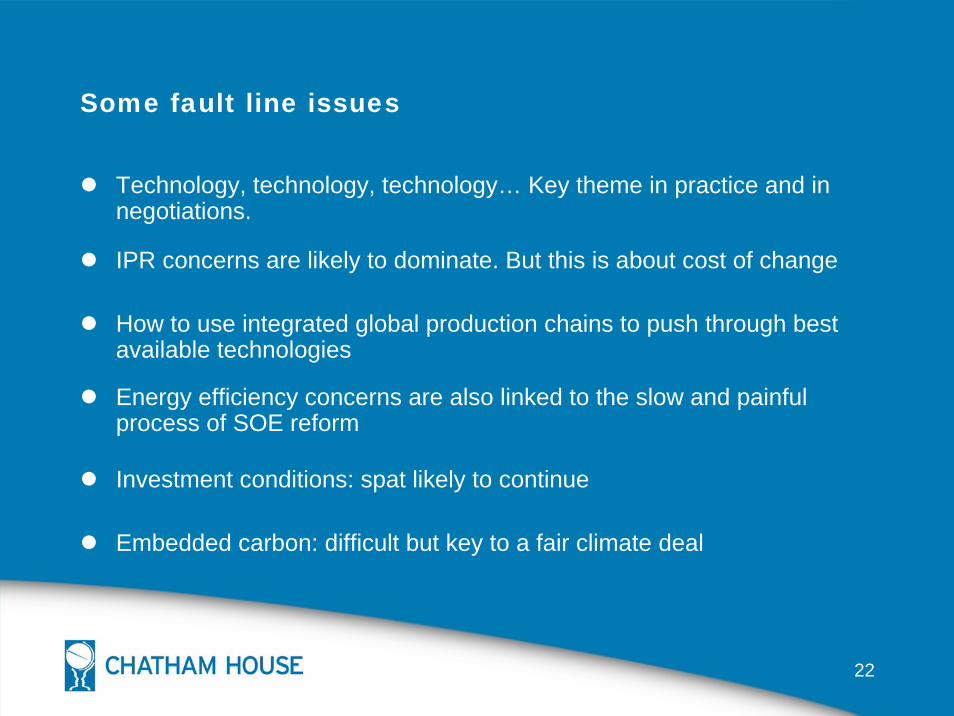

Use of Financial and trade-related instruments

1. Financial and regulatory tools

Bank loans to energy-consuming and high-polluting sectors slowed down in 2007. These include oil processing and coking, chemicals, construction materials, iron and steel, non-ferrous metals, and power generation.