Annals of the „Constantin Brâncuş i” University of Târgu Jiu, Economy Series, Issue 3/2016 „ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007 Table of Contens 1. GENERATION Z ATTITUDES TOWARD GREEN MARKETING: A CROSS COUNTRY AND GENDER ANALYSIS BARAN TAMER, POPESCU CĂTĂLIN 6 2. TRENDS IN USING THE LABOUR FORCE SUBSEQUENT TO THE CRISIS GHIZDEANU ION, RĂBONŢU IRINA-CECILIA 10 3. ORGANIZATIONAL COMMUNICATION FROM THE TOP DOWN TO S.C. ARTEGO S.A. DORU CÎRNU, GABRIELA BUȘAN, IRINA ELENA CHIRTOC 22 4. TAX EVASION THROUGH FICTITIOUS ECONOMIC OPERATIONS, OBSTACLE TO SUSTAINABLE DEVELOPMENT SERGIU-BOGDAN CONSTANTIN 26 5. URBAN GREEN AREAS – ISSUES AND ANSWERS FOR SUISTAINABLE DEVELOPMENT (CASE STUDY IN ROMANIA) LIVIU NEAMŢU, ADINA CLAUDIA NEAMŢU 30 6. GRADUATES’ WILLINGNESS TO BUILD A CAREER IN TOURISM. A VIEW POINT OF THE STUDENTS IN THE TOURISM PROFILE ACADEMIC PROGRAMMES FROM THE TRANSILVANIA UNIVERSITY OF BRAŞOV CODRUȚA ADINA BĂLTESCU 36 7. APPROACHES ON MEASURING SUSTAINABLE DEVELOPMENT IN CONTEMPORARY WORLD – BEYOND CLASSICAL INDICATORS ALECU ALEXANDRA, DUŞMĂNESCU DOREL 40 8. SEMIOTICS- INTEGRAL PART OF THE ECONOMIC HERMENEUTICS ANDA- LAURA LUNGU 49 9. PROPOSAL REGARDING THE REFORMATION OF THE ROMANIAN PUBLIC PENSION SYSTEM NICOLAE ECOBICI 57 10. METHODS FOR IMPROVING THE LEVEL OF MANAGEMENT INOVAȚIONAL COMPANIES ROMANESCU MARCEL LAURENȚIU 61 11. NGO 'S ROLE IN SOCIAL ECONOMY MARIANA CLAUDIA MUNGIU-PUPĂZAN 65 12. A SYSTHEMATIC METHOD FOR DETERMINING THE FACTORS INFLUENCING THE AMOUNT OF PENSIONS CARINA-ELENA STEGĂROIU 69 13. HOW TO MAKE A DESTINATION MORE COMPETITIVE IN TOURISM GABRIEL SANDA 74 14. ELECTRONIC COMMERCE, PART OF THE INFORMATION SOCIETY TEODORESCU ANA-MARIA 78 15. EVALUATION OF THE INVESTMENT DECISIONS IN AGRICULTURE VASILE BURJA, SORINA SIMONA BUMBESCU 82 16. IMPLEMENTING CLEANER PRODUCTION IN ROMANIAN INDUSTRIAL ENTERPRISES IN TERMS OF SUSTAINABLE DEVELOPMENT PAUL BOGDAN ZAMFIR 88 17. KISCH / UL AND DURABLE DEVELOPMENT OF THE REGIONS THAT HAVE A LARGE NUMBER OF RELIGIOUS SETTLEMENTS ENEA CONSTANTA, ENEA CONSTANTIN 93 18. IMPROVING PERFORMANCES BY USING COST CONTROLLING IN THE MINING INDUSTRY ENTITIES SORINEL CĂPUŞNEANU, DAN IOAN TOPOR, ILEANA – SORINA RAKOS, CORINA DUCU, ANAMARIA TEPEŞ-BOBESCU 98 19. MIGRATION WITHIN THE EU AND ITS IMPACT ON UNEMPLOYMENT RATE HARALAMBIE GEORGE ALIN 109 20. STAGES AND EVOLUTIONS IN STRATEGIC MANAGEMENT ACCOUNTING CĂRUNTU GENU ALEXANDRU 114 21. UNCONDITIONAL BASIC INCOME – IMPACT ON THE ECONOMY OANA-VALENTINA CERCELARU 118 3

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

Table of Contens

1. GENERATION Z ATTITUDES TOWARD GREEN MARKETING: A CROSS COUNTRY AND GENDER ANALYSIS BARAN TAMER, POPESCU CĂTĂLIN

6

2. TRENDS IN USING THE LABOUR FORCE SUBSEQUENT TO THE CRISIS GHIZDEANU ION, RĂBONŢU IRINA-CECILIA

10

3. ORGANIZATIONAL COMMUNICATION FROM THE TOP DOWN TO S.C. ARTEGO S.A. DORU CÎRNU, GABRIELA BUȘAN, IRINA ELENA CHIRTOC

22

4. TAX EVASION THROUGH FICTITIOUS ECONOMIC OPERATIONS, OBSTACLE TO SUSTAINABLE DEVELOPMENT SERGIU-BOGDAN CONSTANTIN

26

5. URBAN GREEN AREAS – ISSUES AND ANSWERS FOR SUISTAINABLE DEVELOPMENT (CASE STUDY IN ROMANIA) LIVIU NEAMŢU, ADINA CLAUDIA NEAMŢU

30

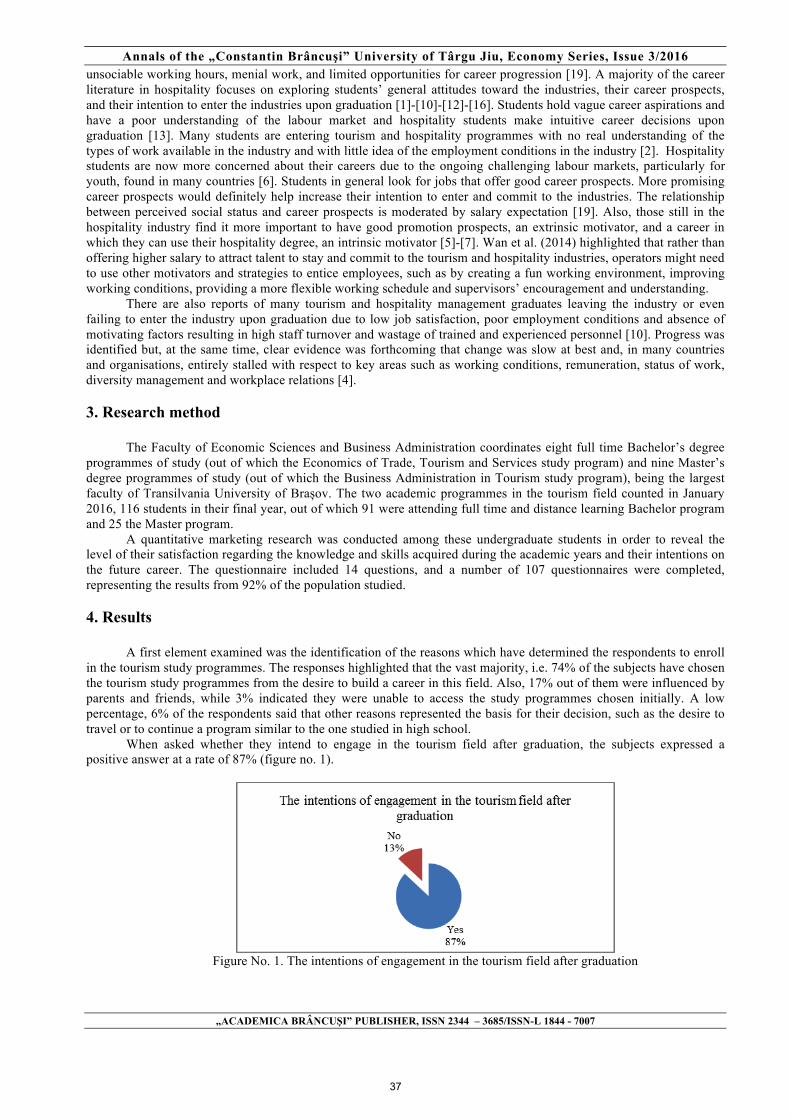

6. GRADUATES’ WILLINGNESS TO BUILD A CAREER IN TOURISM. A VIEW POINT OF THE STUDENTS IN THE TOURISM PROFILE ACADEMIC PROGRAMMES FROM THE TRANSILVANIA UNIVERSITY OF BRAŞOV CODRUȚA ADINA BĂLTESCU

36

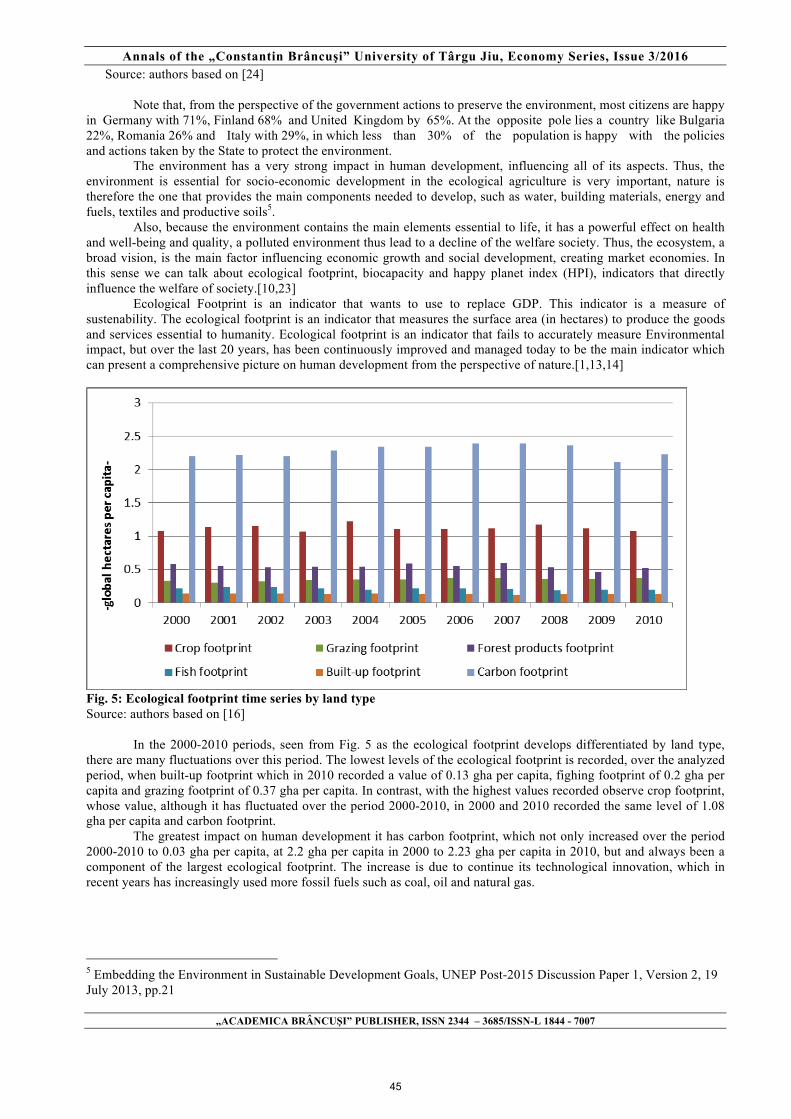

7. APPROACHES ON MEASURING SUSTAINABLE DEVELOPMENT IN CONTEMPORARY WORLD – BEYOND CLASSICAL INDICATORS ALECU ALEXANDRA, DUŞMĂNESCU DOREL

40

8. SEMIOTICS- INTEGRAL PART OF THE ECONOMIC HERMENEUTICS ANDA- LAURA LUNGU

49

9. PROPOSAL REGARDING THE REFORMATION OF THE ROMANIAN PUBLIC PENSION SYSTEM NICOLAE ECOBICI

57

10. METHODS FOR IMPROVING THE LEVEL OF MANAGEMENT INOVAȚIONAL COMPANIES ROMANESCU MARCEL LAURENȚIU

61

11. NGO 'S ROLE IN SOCIAL ECONOMY MARIANA CLAUDIA MUNGIU-PUPĂZAN

65

12. A SYSTHEMATIC METHOD FOR DETERMINING THE FACTORS INFLUENCING THE AMOUNT OF PENSIONS CARINA-ELENA STEGĂROIU

69

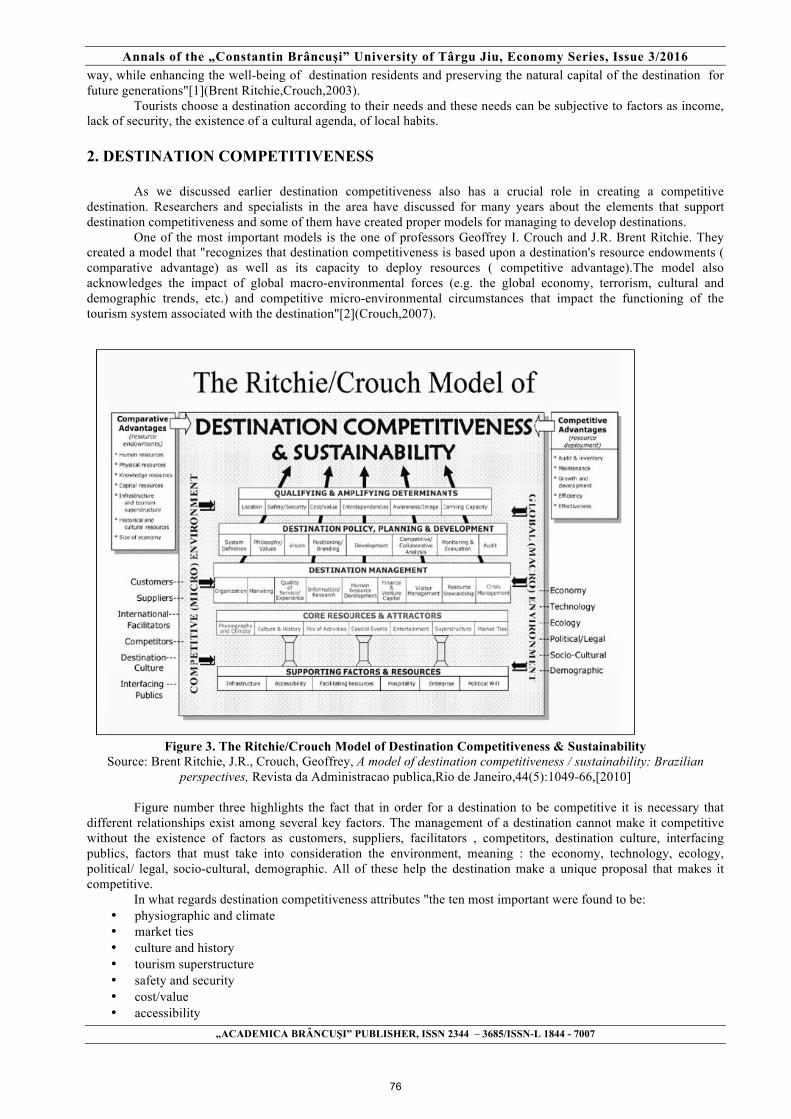

13. HOW TO MAKE A DESTINATION MORE COMPETITIVE IN TOURISM GABRIEL SANDA

74

14. ELECTRONIC COMMERCE, PART OF THE INFORMATION SOCIETY TEODORESCU ANA-MARIA

78

15. EVALUATION OF THE INVESTMENT DECISIONS IN AGRICULTURE VASILE BURJA, SORINA SIMONA BUMBESCU

82

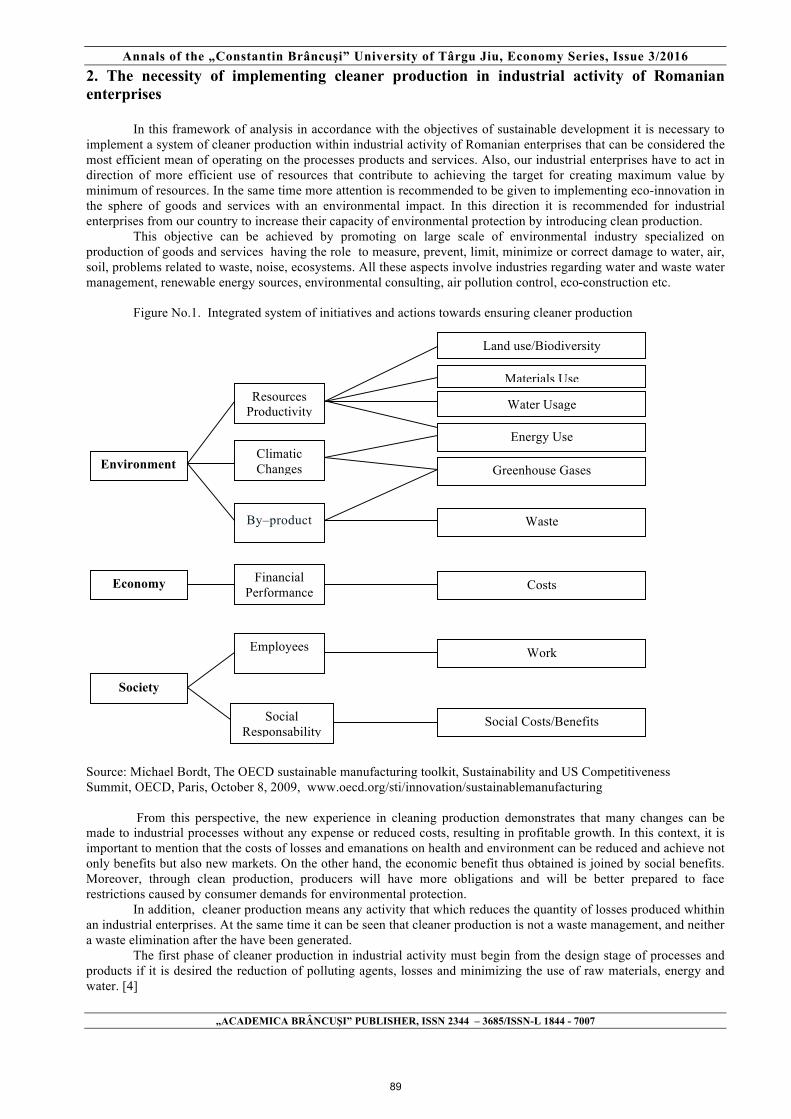

16. IMPLEMENTING CLEANER PRODUCTION IN ROMANIAN INDUSTRIAL ENTERPRISES IN TERMS OF SUSTAINABLE DEVELOPMENT PAUL BOGDAN ZAMFIR

88

17. KISCH / UL AND DURABLE DEVELOPMENT OF THE REGIONS THAT HAVE A LARGE NUMBER OF RELIGIOUS SETTLEMENTS ENEA CONSTANTA, ENEA CONSTANTIN

93

18. IMPROVING PERFORMANCES BY USING COST CONTROLLING IN THE MINING INDUSTRY ENTITIES SORINEL CĂPUŞNEANU, DAN IOAN TOPOR, ILEANA – SORINA RAKOS, CORINA DUCU, ANAMARIA TEPEŞ-BOBESCU

98

19. MIGRATION WITHIN THE EU AND ITS IMPACT ON UNEMPLOYMENT RATE HARALAMBIE GEORGE ALIN

109

20. STAGES AND EVOLUTIONS IN STRATEGIC MANAGEMENT ACCOUNTING CĂRUNTU GENU ALEXANDRU

114

21. UNCONDITIONAL BASIC INCOME – IMPACT ON THE ECONOMY OANA-VALENTINA CERCELARU

118

3

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

22. RISK AND THE FOREIGN DIRECT INVESTMENT - SYNTHETIC APPROACH LĂPĂDUŞI MIHAELA LOREDANA, CIURLĂU LOREDANA

123

23. THE SEPARATION BETWEEN ACCOUNTING PROFESSION AND TAX PROFESSION IN THE CONTEXT OF SUSTAINABLE DEVELOPMENT IN ROMANIA MIHAELA-NICOLETA BĂCANU

129

24. GREEN DEVELOPMENT FOR THE CITIES-INTEGRATED MANAGEMENT LIVIU NEAMŢU, ADINA CLAUDIA NEAMŢU

134

25. THE MANAGEMENT OF THE SUSTAINABLE DEVELOPMENT OF CAREER – GRAND SCULPTOR CONSTANTIN BRÂNCUȘI CORINA ANA BORCOȘI

139

26. INFORMATION SOCIETY AND FINANCIAL SUSTAINABILITY OF THE ROMANIAN HEALTH SYSTEM TATIANA BOGDAN

145

27. A SHORT ANALYSE OF THE DIALOGUE SOCIAL SYSTEMS AND THEIR ROLE IN THE ECONOMIC DEVELOPMENT CEAUSESCU IONUT

150

28. ARE LEISURE AND WORK PRODUCTIVITY CORRELATED? A MACROECONOMIC INVESTIGATION ANA-MARIA SAVA

155

29. REDUCING GREENHOUSE GAS EMISSIONS AND THE INFLUENCES ON ECONOMIC DEVELOPMENT ANGHELUȚĂ PETRICĂ SORIN

160

30. THE IMPACT OF CULTURE ON THE ECONOMIC CRISIS CARINA-ELENA STEGĂROIU

166

31. FINANCIAL PERFORMANCES MEASUREMENT TOOLS BÎRCĂ ALIONA

169

32. IMPORTANCE OF SMES IN EUROPEAN COUNTRIES ECONOMY ROMANESCU MARCEL LAURENȚIU

174

33. STUDY ON INCREASING THE SHARE CAPITAL BY NEW CONTRIBUTIONS IN CASH AND IN KIND CARUNTU GENU ALEXANDRU, HOLT GHEORGHE

178

34. USING PARAMETRIC METHODS FOR OPTIMIZIMG PRODUCTION COSTS IN ECONOMIC ENTITIES WOOD PROCESSING INDUSTRY GHEORGHE(DAMIAN) AURELIA, DAMIAN DORIAN FLORIN

182

35. TOURISM IN THE GORJ COUNTY-THE LAST 10 YEARS OF DEVELOPMENT GABRIEL SANDA

185

36. THE IMPACT OF ICT SECTOR ON THE SOCIAL PILLAR OF SUSTAINABLE DEVELOPMENT TEODORESCU ANA-MARIA

189

37. ANALYSIS OF THE DURATION OF UNEMPLOYMENT IN ROMANIA ROMANESCU GEORGE OCTAVIAN

193

38. RECENT ASPECTS ON TERRITORIAL DISPARITIES IN FINANCIAL BEHAVIOUR OF HOUSEHOLDS IN ROMANIA BABUCEA ANA-GABRIELA

198

39. THE NEW CLASSICAL ECONOMY AND COUNTER-REVOLUTION OF THE MONETARISM KRUME NIKOLOSKI

206

40. REVIEW OF ECONOMIC DEVELOPMENT IN THE REPUBLIC OF SERBIA IN TRANSITION CONDITIONS JELENA TOSKOVIC, SLOBODAN POPOVIC, JOVANA ADZIC

212

41. ROLE OF FINANCIAL SUBSIDIES ALLOCATED BY THE CAP AND OUT EMIGRATION IN ROMANIAN RURAL AREAS NICOLA GALLUZZO

218

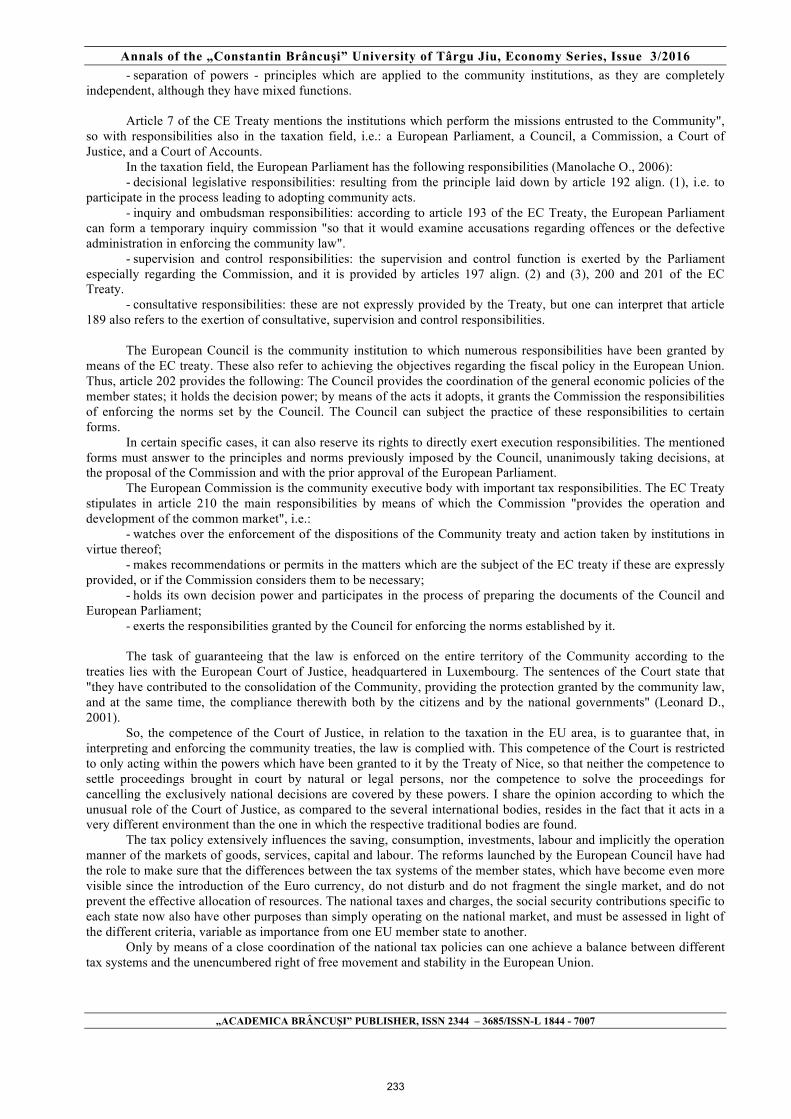

42. TOTAL REVENUE - TOTAL EXPENDITURE INTERDEPENDENCE FOR A HOUSEHOLD IN ROMANIA SAVU MIHAELA, VOICU OANA-LUMINIȚA

225

43. THE TAX POLICY WITHIN THE EUROPEAN UNION: CONCEPTS, INSTITUTIONS, TRENDS AND CHALLENGES CRISTINA COJOCARU (BOROVINA), RALUCA ELENA MOISESCU (DUICAN)

230

44. THE OPTIMIZATION OF THE ENTERPRISE FINANCIAL ANALYSIS TROUGH THE FINANCIAL SYSTEM OF CONTROL DU PONT GÂDOIU MIHAELA

236

45. CLUSTERS’ ROLE IN REGIONAL DEVELOPMENT 241

4

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

BORDEI CONSTANTIN 46. VIRTUAL CURRENCY "BITCOIN" – CHALLENGES AND CONTROVERSIES

ȘOAVĂ GEORGETA, MEHEDINȚU ANCA, SITNIKOV CĂTĂLINA 248

47. ACCOUNTING TREATMENT OF THE FINANCIAL INCOMES AND EXPENSES HOLT GHEORGHE

260

48. THE ANALYSIS OF RESOURCES, MARKET AND THE INDICATORS OF THE ACCOMODATION STRUCTURES FOR THE TOURISTIC PRODUCT BOCSA AREA GHERGHINA LILIANA

265

49. REFLECTIONS ON THE IMPLEMENTATION OF INFORMATION SOCIETY IN ROMANIA PAUL BOGDAN ZAMFIR

272

50. THE IMPORTANCE OF COLLECTING ECONOMIC AND OTHER GENERAL FACTORS’ INFLUENCE ON THE VALUE OF PUBLIC COMPANIES IN SERBIA SLOBODAN POPOVIĆ, DRAGAN ĐURANOVIĆ, JELENA TOŠKOVIĆ, MENSUR CEMALOVIC, RANKO MIJIĆ

277

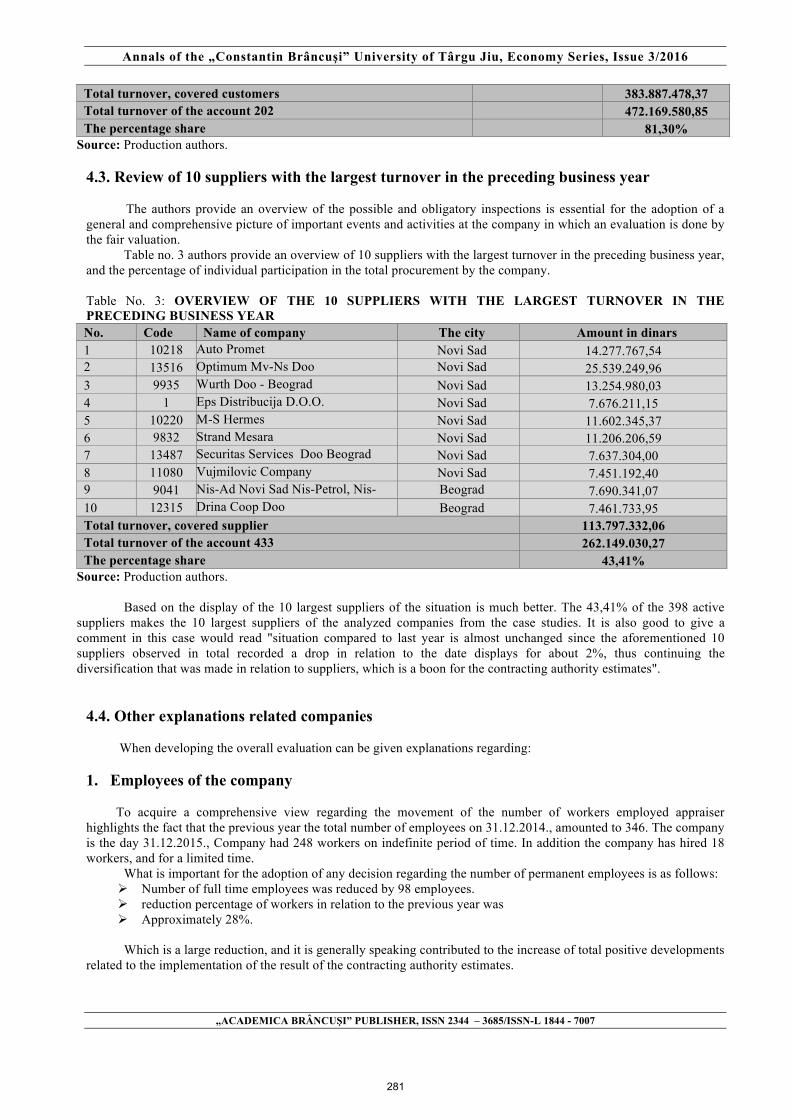

51. ARTIFICIAL CONDITIONS AND THE ABSORPTION OF EUROPEAN FUNDS IN THE FIELD OF AGRICULTURE IN ROMANIA DEACONU SORIN-CONSTANTIN

284

52. RESPONSABILITY AND TRANSPARENCY ON NON-FINANCIAL REPORTING GĂDĂU LIANA

291

53. PLACE AND ROLE OF THE STRUCTURAL FUNDS IN THE LOCAL BUDGET REVENUES CRISTINEL ICHIM

294

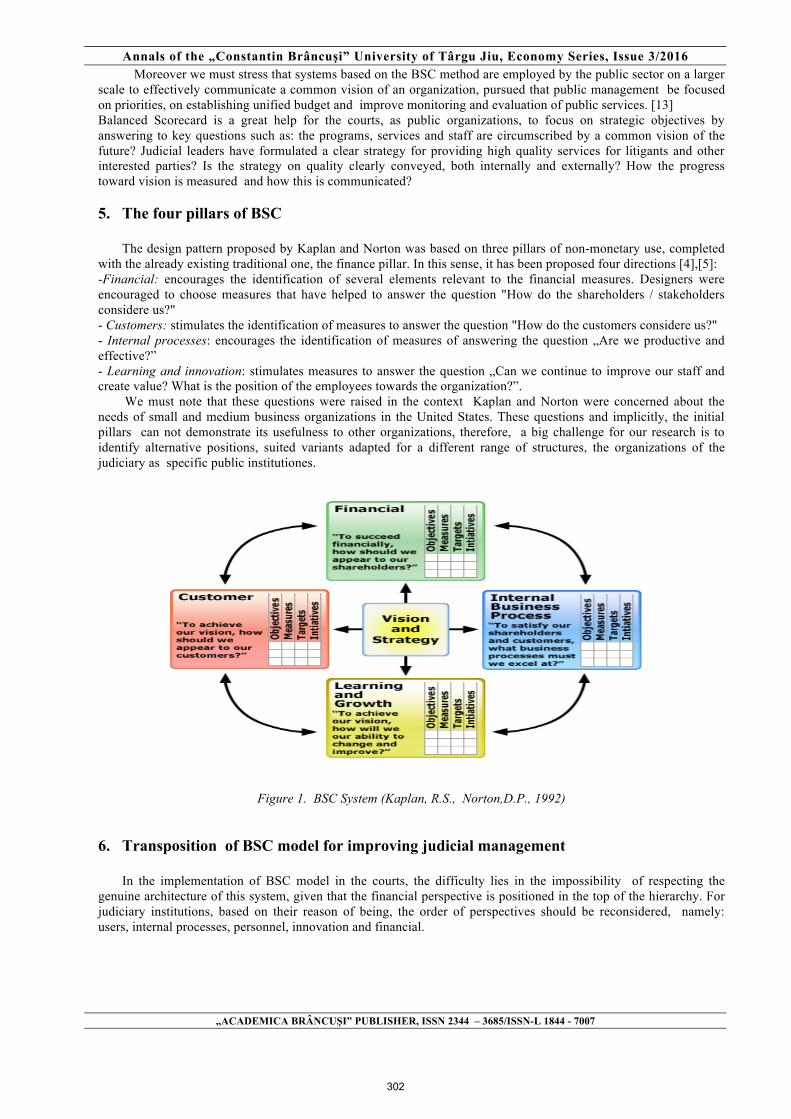

54. USES OF THE BALANCED SCORECARD SYSTEM IN THE STRATEGIC PLANNING AND THE IMPROVEMENT OF THE JUDICIARY FUNCTIONING HULPUŞ IOANA ALEXANDRA, MIRICESCU DAN

300

55. FINANCIAL RESOURCES MANAGEMENT AND THE IMPACT ON THE FINANCIAL POSITION OF THE ENTITIES IN THE ROMANIAN ENERGY SECTOR MIRON VASILE CRISTIAN IOACHIM, FOCȘAN ELEONORA IONELA, BOTA CRISTIAN FLORIN

306

56. ROMANIAN YOUNG LEADERS CAPABILITIES: AN EMPIRICAL SURVEY ANGELA-OLIMPIA LOBONEA OLTEAN

312

5

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

GENERATION Z ATTITUDES TOWARD GREEN MARKETING:

A CROSS COUNTRY AND GENDER ANALYSIS

BARAN TAMER LECTURER, PAMUKKALE UNIVERSITY, KALE VOCATIONAL SCHOOL, DENIZLI, TURKEY

POPESCU CĂTĂLIN PROFESSOR, PETROLEUM-GAS UNIVERSITY, BUSINESS ADMINISTRATION DPT.,

PLOIESTI, ROMANIA [email protected]

Abstract

In social marketing definition, green marketing is the improvement and marketing of products layout to as far as possible minimize adverse effect level on the physical environment. As for environmental marketing definition, green marketing is defined for organizations endeavour to produce, promote, package and reclaim products in a manner that susceptible or responsive to environmental concerns. In this context we define green marketing performing marketing activities which include product improvement, pricing, promote and placing so as to minimize harm to the environment regardless of sector. Related to this approach it will be made a survey in order to analyse the attitude of young generation toward green marketing. It will be created a questionnaire that could offer a perspective about the behaviour of young people concern the environmental issues and future challenges. Keywords: Green Marketing, Generation Z, Green Consumer, Green Consumption JEL Classification: M31, C18, C12 1. WHAT IS THE GREEN MARKETING? WHAT ISN’T?

In the marketing literature it’s possible to find many green marketing definitions. For example, Saha and Darnton (2005: 121-122) defined green marketing as the special product regarding improvement, pricing, promotion and placing that don’t harm the environment. From this definition, it can be clearly understood that green marketing is not only associated with promotion or products with environmental features, but also includes all of the marketing elements. On the other hand, Polonsky (1994: 2), in his study, stated that green marketing is composed of whole activities made up for satisfying human expectation, needs and desires, with minimum effect harm on the environment. One of the earliest definitions of green marketing stated by Henion and Kinnear (1976) defined green marketing as the work of positive and negative orientation of marketing activity on environmental pollution, energy and non-energy resources consuming. One of the most important points of this definition declared that green marketing is consisting of a subset of the overall marketing activities (Polonsky, 1994: 2). Further AMA (2015) develops green marketing definitions in terms of retailing, social marketing and environmental marketing. In this approach, in retailing, green marketing can be defined as marketing of products that are assumed to be environmentally secure. On the other hand in social marketing definition, green marketing represents the improvement and marketing of products’ layout to as possible to minimize adverse effect level on the physical environment. As regarding environmental marketing definition, green marketing is defined for organizations endeavour to produce, promote, package and reclaim products in a manner that is susceptible or responsive to environmental concerns (AMA, 2015).

According to green marketing definitions given above it can be pointed out that green marketing don’t harm the environment but not in the same way such as activities like tree planting, greening etc. In this context we define green marketing performing marketing activities which include product improvement, pricing, promote and placing in order to minimize the impact to the environment.

Green marketing is important for both, companies and people. By green marketing strategies, companies can take some advantages such as be more socially responsible (Davies, 1992; Freeman and Liedtka, 1991; Keller, 1987), overcoming to governmental pressure (Saha and Darnton, 2005: 131), competitive advantages from competitors (Saha and Darnton, 2005: 131) etc. On the other hand, consumers are interested not only in purchasing and consuming but also in production process and in environmental problems and, also, they are considering themselves as green consumers (Zinkhan and Carlson, 1995: 2).

6

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

Another critical issue is that there are so many studies about consumers’ environmental conscience. In this respect these studies have different findings that were revealed by authors. For example, based on Simmons Market Research Bureau’s (SMRB) or research of Kalafatis et. al. (1999: 442) is stated that consumers are not enthusiastic about purchasing environmental friendly products. On the contrary, Ottman (1993: 43) found that more than half of the 16 countries’ (included in his study) consumers are sensitive to environment pollution in his research. Similarly Fisher (1990), Cross (1990) and Donaton and Fitzgerald (1992) mentioned that consumers declared themselves as environmentalist (informed by Ay and Ecevit, 2005: 241). Similar findings were found by Turkish academicians. Aracıoğlu and Tatlıdil (2009: 459) found that Turkish consumers adopt an environmental protectionist attitude and when they have to make a selection, they choose the less harmful products to the environment option. Çoban and Sönmez (2014: 74) found that Turkish consumers have positive attitude towards green marketing. In this study, results showed that consumers are sensitive especially to the green products, green pricing and green promotion. According to Ay and Ecevit’s study (2005: 250) Turkish university students try to have environmentally-conscious behaviour. Aslan and Çınar (2015: 183) stated that Turkish students are consciousness about purchasing and using environmentally harmful products. Also according to the results of this study, students believe that there is a relation between the nature of consuming products and contribution to environmental protection, they are aware about the importance of packaging type in product buying decision and they understand not to disturb natural balance, they are trying to reduse or eliminate different types of wastes and keep the environment clean, they are willing to get information about pre-purchasing period related to the products features and what happen during the purchasing period, taking in account environmentalist products.

The meaning of these paragraphs is to establish the context of the paper. In this light the present paper is developed by bringing the specific literature first (quotations) and then is synthesized the current meaning of the investigated matter. In the following chapters are formulated the paper’ goal under the form of hypotheses, questions or matters treated and are explained the method approach and, in brief, necessary arguments. Based on a survey conducted in Turkey and Romania, were studied some features related to the Turkish and Romanian consumers.

2. GENERATION Z ATTITUDES TOWARDS GREEN MARKETING AND HYPOTHESIS DEVELOPMENT 2.1. Methodology

Sampling, Data Collection and Scaling The sampling was determined for the study by using convenience and judgement sampling methods. The data

gathered with a face-to-face questionnaire method were delivered from 135 respondents. Questionnaire was built up according to Roberts and Bacon’s (1997) ecologically conscious consumer scale and appropriately adopted for the study. Frequency analysis and Mann Whitney U Test were used for achieve the aims of the study through SPSS 20 statistical programme.

Findings Respondents’ demographics were given in detail in Table 1. As can be seen in this table almost 75% of the

respondents are Turkish consumers. More than half of total respondents are female. Moreover, major part of the respondents is having low income.

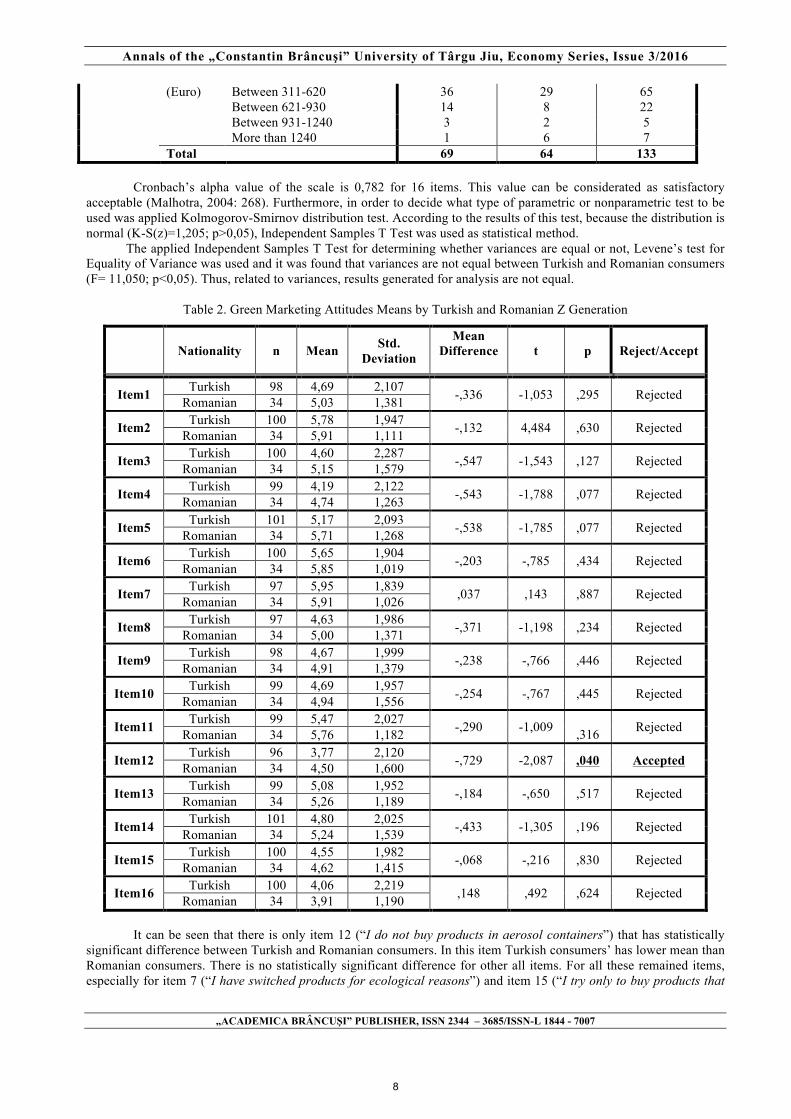

Table 1. Country*Gender*Income Cross Tabulation

Country Gender Total F M

Turkish Income (Euro)

Less than 310 5 15 20 Between 311-620 30 24 54 Between 621-930 12 5 17 Between 931-1240 2 1 3 More than 1240 1 4 5

Total 50 49 99 Romanian Income Less than 310 10 4 14 (Euro) Between 311-620 6 5 11 Between 621-930 2 3 5 Between 931-1240 1 1 2 More than 1240 0 2 2 Total 19 15 34 Total Income Less than 310 15 19 34

7

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

(Euro) Between 311-620 36 29 65 Between 621-930 14 8 22 Between 931-1240 3 2 5 More than 1240 1 6 7 Total 69 64 133

Cronbach’s alpha value of the scale is 0,782 for 16 items. This value can be considerated as satisfactory

acceptable (Malhotra, 2004: 268). Furthermore, in order to decide what type of parametric or nonparametric test to be used was applied Kolmogorov-Smirnov distribution test. According to the results of this test, because the distribution is normal (K-S(z)=1,205; p>0,05), Independent Samples T Test was used as statistical method.

The applied Independent Samples T Test for determining whether variances are equal or not, Levene’s test for Equality of Variance was used and it was found that variances are not equal between Turkish and Romanian consumers (F= 11,050; p<0,05). Thus, related to variances, results generated for analysis are not equal.

Table 2. Green Marketing Attitudes Means by Turkish and Romanian Z Generation

Nationality n Mean Std. Deviation

Mean Difference

t p Reject/Accept

Item1 Turkish 98 4,69 2,107 -,336 -1,053 ,295 Rejected Romanian 34 5,03 1,381

Item2 Turkish 100 5,78 1,947 -,132 4,484 ,630 Rejected Romanian 34 5,91 1,111

Item3 Turkish 100 4,60 2,287 -,547 -1,543 ,127 Rejected Romanian 34 5,15 1,579

Item4 Turkish 99 4,19 2,122 -,543 -1,788 ,077 Rejected Romanian 34 4,74 1,263

Item5 Turkish 101 5,17 2,093 -,538 -1,785 ,077 Rejected Romanian 34 5,71 1,268

Item6 Turkish 100 5,65 1,904 -,203 -,785 ,434 Rejected Romanian 34 5,85 1,019

Item7 Turkish 97 5,95 1,839 ,037 ,143 ,887 Rejected Romanian 34 5,91 1,026

Item8 Turkish 97 4,63 1,986 -,371 -1,198 ,234 Rejected Romanian 34 5,00 1,371

Item9 Turkish 98 4,67 1,999 -,238 -,766 ,446 Rejected Romanian 34 4,91 1,379

Item10 Turkish 99 4,69 1,957 -,254 -,767 ,445 Rejected Romanian 34 4,94 1,556

Item11 Turkish 99 5,47 2,027 -,290 -1,009 ,316 Rejected Romanian 34 5,76 1,182

Item12 Turkish 96 3,77 2,120 -,729 -2,087 ,040 Accepted Romanian 34 4,50 1,600

Item13 Turkish 99 5,08 1,952 -,184 -,650 ,517 Rejected Romanian 34 5,26 1,189

Item14 Turkish 101 4,80 2,025 -,433 -1,305 ,196 Rejected Romanian 34 5,24 1,539

Item15 Turkish 100 4,55 1,982 -,068 -,216 ,830 Rejected Romanian 34 4,62 1,415

Item16 Turkish 100 4,06 2,219 ,148 ,492 ,624 Rejected Romanian 34 3,91 1,190

It can be seen that there is only item 12 (“I do not buy products in aerosol containers”) that has statistically significant difference between Turkish and Romanian consumers. In this item Turkish consumers’ has lower mean than Romanian consumers. There is no statistically significant difference for other all items. For all these remained items, especially for item 7 (“I have switched products for ecological reasons”) and item 15 (“I try only to buy products that

8

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

can be recycled”) it is proved that they have the smallest difference. Even for all other items the mean difference for Turkey and Romania shows that they aren’t statistically significant. All these findings were shown in Table 2.

3. CONCLUSIONS

In this study it was studied a cross country comparison of Generation Z attitude towards green marketing. In this context after the description related to Generation Z and after were explained the concepts linked with green marketing, were gathered data through face-to-face questionnaire from 135 respondents coming from Turkey and Romania. Then, data were analysed using Independent Samples T Test to SPSS 20 statistical programme.

At the end of the analysis was found that there is no difference between Turkish and Romanian Z Generations towards green marketing. Some proves concern this conclusion could be found in other research (Asmali, 2015; Agaoglu, 2014). On other words Turkish and Romanian youths attitudes towards green marketing is similar. This finding can help especially for international companies which are operating to both countries. These companies can apply similar green marketing strategies in Turkey and Romania, as well.

Methods of data collecting and numbers of questionnaire can be considered as limitations of this paper. Also researchers can investigate to other type of consumers apart from youths in further researches.

4. REFERENCES [1]. Agaoglu F., Religious perspective of business ethics principles in Turkey and Romania: a cross country comparison, SEA-Practical Application of Science, Volume II, Issue 1 (3) / 2014, 11-22; [2]. Aracioglu B. & Tatlidil R., Tüketicilerin Satın Alma Davranışında Çevre Bilincinin Etkileri. Ege Academic Review, 9(2), 2009, 435-461; [3]. Aslan F. & Çınar, R., Yeşil Pazarlama Faaliyetleri Çerçevesinde Kafkas Üniversitesi Öğrencilerinin Çevreye Duyarli Ürünleri Kullanma Eğilimlerini Belirlemeye Yönelik Bir Araştirma. Kafkas Üniversitesi İktisadi ve İdari Bilimler Fakültesi Dergisi, 6(9), 2015; [4]. Asmali M., Bilki U., Duban C.A., A Comparison of the Turkish and Romanian students' willingness to communicate and its affecting factors in English, Journal of Language and Linguistic Studies, vol.11, no.1, 2015, 59-74; [5]. Canan A. Y. & Ecevit Z., Çevre Bilinçli Tüketiciler. Akdeniz University Faculty of Economics & Administrative Sciences Faculty Journal/Akdeniz Universitesi Iktisadi ve Idari Bilimler Fakultesi Dergisi, 5(10), 2005; [6]. Çoban S. & Sönmez Y., Yeşil Pazarlama Karmasına Yönelik Tüketici Tutumlarının Demografik Özelliklere Göre Farklılaşması: Ahi Evran Üniversitesi Örneği. Nevşehir Hacı Bektaş Veli Üniversitesi Sosyal Bilimler Enstitüsü Dergisi, 3, 2014, 65-82; [7]. Cross F. B., The weaning of the green: Environmentalism comes of age in the 1990s. Business Horizons, 33(5), 1990, 40-46; [8]. Davis Joel J., "Ethics and Green Marketing." Journal of Business Ethics 11 (2): 1992, 81-87; [9]. Donaton S. & Fitzgerald, K., Polls show ecological concern is strong. Advertising Age, 63(3), 1992, 19-23; [10]. Fisher A. B., What consumers want in the 1990s. Fortune, 121(3), 1990, 108-112; [11]. Freeman R. E. and Liedtka J., "Corporate Social Responsibility: A Critical Approach" Business Horizons, 1991, 34 (4): 92-98; [12]. Henion K. E., & Kinnear T. C., A guide to ecological marketing. Ecological Marketing. Columbus, Ohio: American Marketing Association, https://www.ama.org/resources/Pages/Dictionary.aspx?dLetter=G, 1976; [13]. Kalafatis S. P., Pollard M., East R. & Tsogas M. H., Green marketing and Ajzen's theory of planned behaviour: a cross-market examination. Journal of consumer marketing, 16(5), 1999, 441-460; [14]. Keller G. M., "Industry and the Environment: Toward a New Philosophy." Vital Speeches, 1987, 54 (5): 154-157; [15]. Malhotra N. K., Marketing research: An applied orientation, 4/e. Pearson Education New Jersey, 2004; [15]. Polonsky M. J., An introduction to green marketing. Electronic Green Journal, 1(2), 1994; [16]. Roberts J. A., & Bacon D. R., Exploring the subtle relationships between environmental concern and ecologically conscious consumer behavior. Journal of Business Research, 40(1), 1997, 79-89; [17]. Saha M., & Darnton G., Green Companies or Green Con-‐panies: Are Companies Really Green, or Are They Pretending to Be? Business and Society Review, 110(2), 2005, 117-157; [18]. Zinkhan G. M., & Carlson L., Green advertising and the reluctant consumer. Journal of Advertising, 24(2), 1995, 1-6.

9

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

TRENDS IN USING THE LABOUR FORCE SUBSEQUENT TO THE CRISIS

GHIZDEANU ION PRESIDENT OF THE NATIONAL COMMISSION OF PROGNOSIS, SENIOR RESEARCHER ROMANIAN ACADEMY, PROFESSOR PHD, CONSTANTIN BRANCUSI UNIVERSITY OF

TARGU JIU [email protected]

RĂBONŢU IRINA-CECILIA

PROFESSOR PH.D., CONSTANTIN BRANCUSI UNIVERSITY OF TARGU-JIU [email protected]

Abstract

The use of labour force acquires new aspects in the stages subsequent to the economic and financial crisis in Romania and we would like to present them in this paper. The imbalances caused by the Romanian economy restructuring were visible in the labour market evolution, offering a new dimension to the issue of adapting the labour force to the market requirements, within the regions and their counties. Through this paper, we want to offer an overview of the Romanian labour market, integrating it in the realities of the international labour market. We will thus seek to observe if the labour market responds, and to what extend if so, to the current requirements given by the realities emerged as a consequence of the crisis’ effects. In order to analyse what we had set to, we used the most recent statistical data on the official labour market but, in order to get an even clearer image of the field, we also appealed to data offered by the National Prognosis Commission, indicating the source. Analysing the practical features when taking into consideration the emigration possibility presents a major interest for completing this study, as lately we are witnesses to massive migration, especially of the qualified youth, which leads to a decrease in labour force quality in the country. Also, an analysis of the sectors with significant imbalances between the number of job vacancies and the number of employees may contribute to identifying the current labour market trends. Key word: labour market, crisis, trend, domestic and national employment, statistical indicators, economy, Romania 1. Introduction

Were we to try to define the labour market, we can state that it describes the relations series established between the capital holders, as buyers and the labour force holders, as sellers, through the labour market (salary), the free competition and other specific mechanisms which adjust the labour supply and demand. In the published literature, we either find the labour market1 designation, or the labour force market2 one.

Regardless of the name, the economic content of the ”labour market” concept (or “labour force market”, expresses the same objective reality and that is that the factor of production, the labour- is provided through the market in a market economy. Generally, the labour market works according to the market’s basic principles: demand, supply, price, competition, etc., but all these manifest in accordance with the work force, which establishes certain particularities to the labour market3, through its philosophical, psychological, social and moral particularities. The most important are:

a) on the labour market, not all the nation’s labour potential is negotiated, but only that which is required by the capital factor of production and is offered by the ones ready to use their work capacity.

b) Compared to the other markets, the labour market is more organised, more complex, the economic operators are not only sellers and buyers.

c) The contemporaneous labour market is a contractual and participative one, where negotiation and employment contract play an important role in determining the labour demand and supply. On this market the ratio between the labour demand and supply is specifically manifested in that the supply is

permanently higher than the demand, which determines the existence of unemployment. According the data from the National Statistics Institute, the resident population of Romania is 19, 94 million persons.

The study of the labour market begins and ends with the analysis of the labour demand and supply. On the labour demand side we have the firms, whose decisions regarding the labour force employment are influenced by the conditions on the three markets. On the labour supply side we have the employees and potential employees whose decisions on the workplace and whether to work are linked to their options regarding the spending of the time they 1 Marin Băbeanu, Marius Băbeanu, Piaţa şi sistemul pieţei, Fundaţia „Scrisul Românesc”, Craiova, AustRom IMPEX SRL Publishing House, 1998, p 149; 2 Gh. Creţoiu and colab., Economie politică, „Şansa” S.R.L. Publishing House, Bucharest, 1995, p. 395; I.D 3 Gheorghe MECU – Contents and Particularities of the Labor market http://www.revistadestatistica.ro/suplimente/2012/2/srrs2_2012a44.pdf

10

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

have. The main elements of the labour market are determined by the remuneration means and the working conditions; - the level of employment. These elements are the result of the action and functioning of the labour market. For their generation, both supply and demand are needed.

According to the data offered by the Labour Force Balance on January 1, 2015, the civil economically active population was 8910.0 thousand persons, representing 44,9% of the total population. From the gender division point of view, the situation of the active persons is: 53, 4% are male and 46, 6% are female. The civil employment was of 8431, 7 thousand persons, 4900, 7 thousand of which were employees. Most of the employees worked in the services sector (3014, 5 thousand persons), while 1772,4 thousand persons were working in industry and constructions. In agriculture, forestry and fishing, 113, 8 thousand persons were working. In the 3rd trimester of 2015, the employment rate of the working age population (15- 64 years old) was 63, 2%, with higher values for men (71,6% compared to 54,6% for women). 94.9% of the active female persons were employed and 5.1% were unemployed. In the active civil population, the employed population held a share of 94, 3%. 2. The statistical indicators system and expression

The complexity of the labour market does not only stem from the general features of the daily people flows between sub-sectors or the labour market inputs and outputs, but also from the Romanian economy particularities of structural and behavioural nature.

The labour market broadly includes issues linked to employment, unemployment and labour quality, productivity, gains and labour costs.4 The complexity and importance of the labour market is also reflected in the role designated within the Europe 2020 Strategy, that has the employment rate as main indicator and the creation of more and better jobs in the EU as general objective. Moreover, The European Union has detailed the future preoccupations and action directions for increasing employment within the European Employment Strategy and for assessing the evolutions in the labour market sector, a comprehensive analytical and statistical sector based on structural approach.

In order to capture as well as possible the complex diversity of employment in Romanian statistics, European indicators and statistics are used, as well as national indicators and surveys. To these, we add databases and wide administrative statistics for separate use, especially those from the National Agency for Fiscal Administration and labour inspections.

From this point of view, the labour statistics is the most comprehensive sectoral statistical system, surpassing in number of indicators and diversity of information all the other sectoral statistics (industrial, foreign trade statistics etc.).

Another argument in this direction is the fact that the same phenomenon, for example unemployment or employment, is analysed and statistically highlighted from different perspectives: that of the employee and that of the employer, of the one who considers he/she is unemployed, searching for a workplace or that of the one who actually addressed the competent public institution regarding employment. Moreover, the labour market is characterized not only by the employment indicators, but also by indicators highlighting the jobs. Under these circumstances, there is often the risk of using a statistical indicator concerning the labour market without explaining its expression or conferring it another expression.

The statistical researches of the National Statistical Institute are the following:5 o The statistical research on labour force in households, for data regarding employment and unemployment

(according to Regulation no. 577/ 1998 of the Counsel regarding the organization of a survey inquiry on the labour force in the community, with the ulterior HLFS modifications);

o The statistical research regarding the labour force cost in the economic and social units, for data regarding the number of employees (according to the Regulation no. 530/ 1999 of the European Parliament and of the Council regarding the statistics of the employees earnings and the labour force cost);

o The quarterly statistical research on job vacancies, for data regarding the vacancies rate (according to Regulation no. 453/ 2008 of the European Parliament and of the Council on the statistics regarding the job vacancies);

o The labour force balance for the data regarding the civil employment by activities of the national economy, ownership and by county. The statistical research resulting from the EU Regulations, compulsory for all member states, ensures the

comparativeness of the data series regarding the labour market published by Eurostat and offers thus adequate informational sources to the macroeconomic analyses and prognoses and subsequently for the establishment of public European and national policies.

From the statistical research, the following indicators detailing employment arise: 1. The number of employees (LFB);

4 Albu, L., L., Caraiani, P., Iordan, M. – The perspectives of the labour market in Romania in the context of the Europe 2020 strategy, study developed within the “Improving the institutional, assessment and macroeconomic policy formulation capacity in the field of economic convergence of the National Prognosis Commission with the European Union, code SMIS 27153” project, Ed. Economică, Bucharest, 2012 5 Details on the research are found in the Romanian Statistical Yearbook, NSI, 2015, as well as in the periodicals published by NSI, which present the results of the HLFS and LFB surveys.

11

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

2. The number of employees (HLFS); 3. The average number of employees (LFB and the survey regarding the labour force cost).

A first important conceptual difference between the indicators comes from the statistical research subject and is referring to the one giving information on the paid employment.

HLFS takes place in households, the interviewed person stating whether he/she is employed or not. Therefore, the number of employees6 is defined as being the number of the persons working based on a written or verbal consent (agreement, employment contract, employment relationship etc.) with the employer, in exchange for remuneration as salary, wage or in nature.

The survey regarding the LFB labour force cost is developed by the institutional employers, the commercial societies. As a consequence, the number of employees and the average number of employees represent the number of the persons holding a written employment contract and declared by the employers. That is why it is said that the two indicators show employment in the official sector, as they represent the number of employees officially declared by the economic operators.

As we can see, the main difference lies in the scope. In the first case, we are talking about all employees – regardless of the fact that they work either in an economic unit, for a particular person or within a household- while in the second case, we are talking about contract-based employees officially working in enterprises.

A second major difference is the temporal vision. The number of employees 7 illustrates the number of employees on the last day of the reference period, while the average number of employees8, although resulting from the same statistical research, refers to the average of the employees working and receiving a salary during the reference period.

Differences also emerge in relation with the employees’ statute: paid or non-paid employees, employees that are having or not having the main position at the reporting unit, employees detached abroad or not. Still, such differences are smaller and they do not modify significantly the ratios between the three indicators measuring employment.

In summary, it could be said that the whole employment is illustrated by the number of employees in the HLFS survey, the average number of employees being only the expression of the civil9 and official employment, of the fiscalised work, respectively (because this comes with a labour force cost and implicitly the taxation of the additional expenditures).

We want to highlight again that, given the particularities of each inquiry, the comparativeness, as well as the conclusions in the indicators’ analysis or the differences between them are not very exact. For example, the HLFS survey is a quarterly survey, the reference period for the statistical research being the middle month of a quarter.

By convention, the number of employees resulted from this survey is supposed to represent an average value, the annual data being obtained as an arithmetic mean of the 4 quarterly results. Unlike this indicator, the average number of employees in LFB is calculated by each economic operator based on the daily number of employees, as NSI only aggregates and conciliates the average number of employees transmitted by the economic operators.10

Still, the delimitations are not so categorical. There are employees working for self-employed persons that pay their contributions and taxes, but these add to other fiscal obligations. Yet, these employees are not included in the average number of employees due to this survey’s exclusive concern for the institutional employers. Also, the day labour is not included in the average number of employees, although it takes place in enterprises, because there is no employment contract involved.

In order to understand this compulsory difference, we highlight the case of the “day labourers”, who, despite working in enterprises, do not have employment contracts.

The daily workers law (Law no. 52/ 201111, modified and completed by Law no. 277/2013) establishes that the duration of the occasional activity that can be exerted under this law is of one day minimum, corresponding to 8

6 The number of employees includes the persons with a working contract in an economic or social unit- regardless of its ownership type- or the persons working for particular employers, in exchange for remuneration as salary, wage or in nature, as commission etc. 7 The number of employees at the end of the period is the number of employees employed with individual labour contract with definite or non-definite duration, full or part-time (including those with suspended labour contract/ agreement) existent in the enterprise records at the end of the year. The employees detached abroad and those who hold more than one position and are not having the main position at the reporting unit are not included. 8 The average number of employees represents a simple arithmetic mean resulted from the sum of daily employees number, including from the weekly rest days, legal holidays and other non-working days divided to the total calendar days of the year (365 days). In the daily number of employees taken into calculation for average number, there are not included: employees under unpaid leave, on strike, detached to work abroad. In weekends, legal holidays, other days off, the number of employees from the previous day is taken into calculation, less that or those whose labour contract ceased the same day. Employees who were not full-time employed are included in the average number of employees proportionally with the working time from the labour contract. 9 The average number of employees does not consider the employees in the defence sector and the staff treated as such in SRI, Ministry of Internal Affairs, etc., thus, the non-civil employees. 10 NSI- Statistical Research S1- The survey on salaries, where there is a chapter and a designated position for “the average number of employees”

12

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

hours of work. The daily duration for a daily labourer’s activity cannot exceed 12 hours. The daily labourers work without an employment contract, based on mutual agreement. The activity is registered in an evidence register.

Table no 1. Number of day labourers registered up to December 31

Activity field No. of registrations (in the evidence register of the daily labourers) 2011 2012 2013 2014

Total no. of registrations 2.342.010 6.406.375 10.874.942 19.891.662 of which: - agriculture 891.967 1.840.391 : 4.615.555 - hunting and fishing 4.942 24.445 : 60.191 - forestry 305.681 836.671 : 2.654.123 - fishery and aquaculture 8.776 18.377 : 40.182 - fruit and wine growing 473.225 1.109.793 : 2.641.624 - beekeeping 4.574 5.367 : 11.623 - livestock 59.515 164.504 : 319.272 Not indicated 269.558 1.438.779 : 7.238.601

Source: Labour Inspection – MMFPSPV (for 2013 the structure of the registrations has not been published) The beneficiary must pay the daily labourer the agreed remuneration at the end of each work day and provide

the labourer with the work and protection equipment. There is only one tax (16%) calculated for the gross remuneration and that is the beneficiary’s obligation. Day labourers cannot work for the same beneficiary for a period longer than 90 days during a calendar year. The labourer can work all year long for different beneficiaries, as the law does not prohibit that.

A specific significance is held by the number of employees, which reflects the filled in jobs, regardless of whether associated with an income or not.12 This indicator, associated with the job vacancies resulting from a statistical survey on this subject, provides the extent of the employment in economy. If we do not consider the reference period it could be said that the number of employees, expressed as difference between the number of employees and the average number of employees, designates the jobs filled in by persons who do not work in the specified period, being detached, in leave without pay, study leave etc. or who work part time. The expressiveness of the number of employees is also illustrated by the vacancies rate, which is an important indicator for the analysis of the balance between the demand and supply of labour force. The vacancies rate is the ratio between the number of job vacancies and the total number of jobs, expressed as:

100*100*LVLO

LVLtotaleLvacanteRLV

+==

where: LO – number of employees;

Lvacante, LV – job vacancies. If we refer to the latest data published by NIS in Q4 2015, when the average number of employees increased

by over 3%, the vacancies rate was 1.21%, increasing as compared to the previous quarter, highlighting the structural difficulties in meeting the labour demand with the labour supply, even if there is an improvement in the employment. As compared to the corresponding quarter in 2014 the vacancies rate increased by 0.3 percentage points.

3. The structure and evolution of the remunerated labour

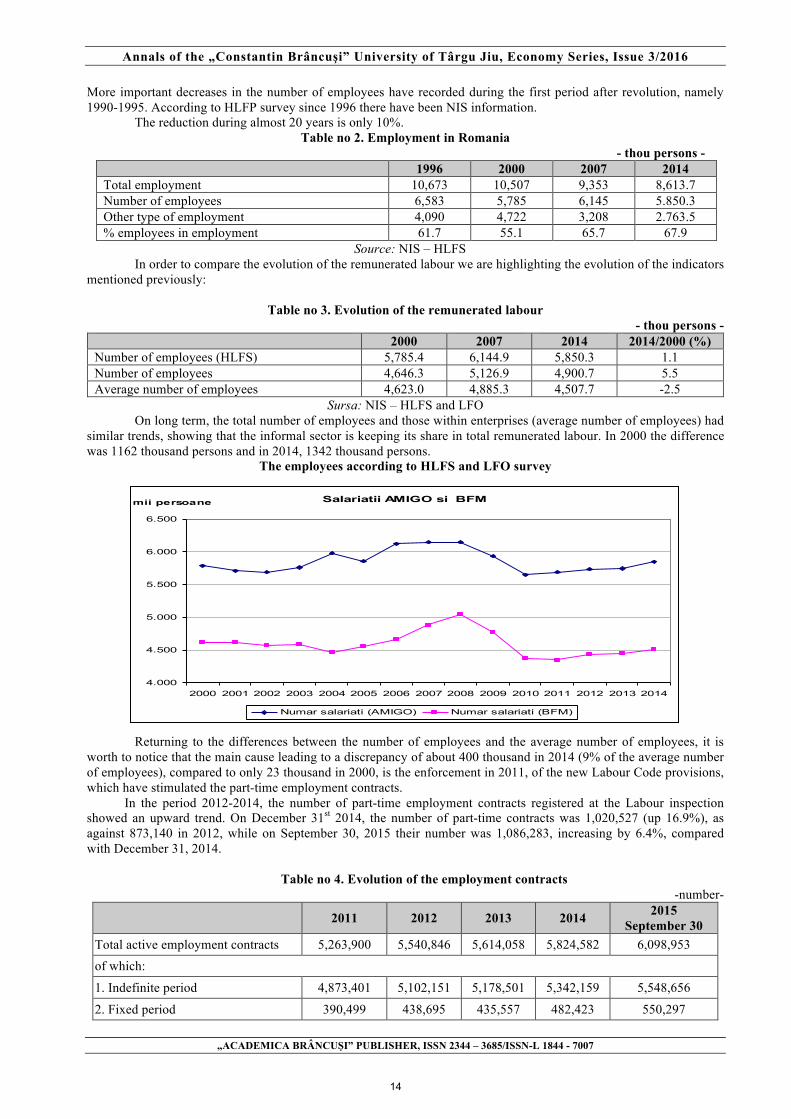

The problematic of a proper use of the employment indicators is as important as the temptation of using some indicators having in mind a desired conclusion to be highlighted is higher, thus neglecting their expressivity. Even in economic research some „errors” may occur, which unfortunately are distorting the research. For example, in the Romanian development strategy, soon published by the Romanian Academy it is stated that: “The average number of employees strongly decreased during transition period: from 8.1 million in 1990 to 4.9 million in 2014 (NIS, 2015)”13. It is compared the number of employees in 1990 when there was no informal labour and no contract labour with the average number of employees, namely those within the institutional sector. The number of employees did not decrease dramatically, it has another structure, according to the market economy specificities.

In 2014 Romania had 5850.3 thou employees out of which 4.5 million in civil institutional sector, namely in economic units.

What is mentioned in the Strategy published by the Romanian Academy is an example for another error, namely the use of jobs (number of employees) at the end of the year as compared to the number of employees during the full year period. In 2014 the average number of employees in the civil and official sector was 4.5 million persons, with a number of employees at the end of the year (31 December) of 4.9 million.

11 Law no. 52/ 15.04.2011 regarding the development of seasonal activities by day labourers, republished (Official Monitor no. 947/22.12.2015) 12 NSI – Methodological specifications, Press release no 46/ February 2016 13 Romanian Academy – Romania’s development strategy in the next 20 years, vol. II, Romanian Academy Publishing House, 2016,

p. 298

13

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

Salariatii AMIGO si BFM

4.000

4.500

5.000

5.500

6.000

6.500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

mii persoane

Numar salariati (AMIGO) Numar salariati (BFM)

More important decreases in the number of employees have recorded during the first period after revolution, namely 1990-1995. According to HLFP survey since 1996 there have been NIS information.

The reduction during almost 20 years is only 10%. Table no 2. Employment in Romania

- thou persons - 1996 2000 2007 2014

Total employment 10,673 10,507 9,353 8,613.7 Number of employees 6,583 5,785 6,145 5.850.3 Other type of employment 4,090 4,722 3,208 2.763.5 % employees in employment 61.7 55.1 65.7 67.9

Source: NIS – HLFS In order to compare the evolution of the remunerated labour we are highlighting the evolution of the indicators

mentioned previously:

Table no 3. Evolution of the remunerated labour - thou persons -

2000 2007 2014 2014/2000 (%) Number of employees (HLFS) 5,785.4 6,144.9 5,850.3 1.1 Number of employees 4,646.3 5,126.9 4,900.7 5.5 Average number of employees 4,623.0 4,885.3 4,507.7 -2.5

Sursa: NIS – HLFS and LFO On long term, the total number of employees and those within enterprises (average number of employees) had

similar trends, showing that the informal sector is keeping its share in total remunerated labour. In 2000 the difference was 1162 thousand persons and in 2014, 1342 thousand persons.

The employees according to HLFS and LFO survey

Returning to the differences between the number of employees and the average number of employees, it is worth to notice that the main cause leading to a discrepancy of about 400 thousand in 2014 (9% of the average number of employees), compared to only 23 thousand in 2000, is the enforcement in 2011, of the new Labour Code provisions, which have stimulated the part-time employment contracts.

In the period 2012-2014, the number of part-time employment contracts registered at the Labour inspection showed an upward trend. On December 31st 2014, the number of part-time contracts was 1,020,527 (up 16.9%), as against 873,140 in 2012, while on September 30, 2015 their number was 1,086,283, increasing by 6.4%, compared with December 31, 2014.

Table no 4. Evolution of the employment contracts

-number-

2011 2012 2013 2014 2015 September 30

Total active employment contracts 5,263,900 5,540,846 5,614,058 5,824,582 6,098,953 of which:

1. Indefinite period 4,873,401 5,102,151 5,178,501 5,342,159 5,548,656

2. Fixed period 390,499 438,695 435,557 482,423 550,297

14

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

of which:

1. Full time - 4,667,706 4,671,761 4,804,055 5,012,670

2. Part time - 873,140 942,297 1,020,527 1,086,283 Source: http://www.inspectiamuncii.ro/documents/66402/187655/Raport+anual+2014.pdf/

As a result, the share of the part-time contracts in total active employment has increased from 15.8% in 2012,

to 17.8% in September 2015. The extension of the part-time contracts is favored by the fact that there are no restrictions regarding the

part-time jobs. Moreover, the Labour Code provides the opportunity of both part time and full time jobs for the same business, but does not introduce any criterion to justify the need for a part-time job.

For example, what happens if similar activities include mostly part-time employment contracts, which in fact, is a way to reduce the tax burden of the employer? If they represented only a requirement for efficiency and full utilization of the workforce, it would have been sufficient to replace those contracts with a single full-time employment contract. In fact, the employees with part-time jobs usually exceed the norm established in the contract.

Analyzing the data on part-time wage employment (on the basis of the annual average equivalent), according to HLFS survey, one can notice that the impact on the number of employees is still low. The number of part time employees is still insignificant, accounting for less than 1% of total employees. Consequently, in 2014, from a total of 5.850,3 thousand employees, only 41.107 people were part time employed, of which, 75% were active in the field of services. Regarding the part time employed population, the share is similar, reaching about 1%, being influenced by over 700 thousand people working part time in agriculture (underemployment in this sector is also the main cause of low productivity). In 2014, the proportions were as follows: 0.7% for employees and 1% for the total employed population.

4. Domestic and national employment

The previously analyzed indicators have in view the resident population and therefore, the number of employees across the country, with Romanian citizenship. As can be seen, the criterion of territoriality is important, but this principle is not applied by the surveys described above.

Structuring employees according to the workplace is important, especially for the correlation with the economic growth process14.

First, the methodology of quantification considers the space where the economic agents operate, as being essential, without any restrictions, respectively: a country, a region or an economic area. A second criterion is the nationality of the economic operators.

The "domestic" category delimitates the contribution of the business agents operating on the economic territory, regardless their nationality; as long as the production is achieved within the country. From this point of view, the statistical units are grouped by “resident” and “non-resident”.

The "national" category delimitates the output of the national business agents; thus, the contribution of all national production factors is taken into account. Accordingly, from this point of view, the macroeconomic indicators measure the results of the national economy, no matter if the economic agent operates within or outside the country.

This criterion translates in the field of employment, by measuring the number of employees and the employed population participating at the achievement of the national accounts, the gross domestic product, respectively. The number of employees15 includes both residents and non-residents, working in resident production units (the "domestic employment" concept).

In the context of national accounts, the employed population16 is that who works for the resident production units in Romania and creates actually, the Romanian gross domestic product (“domestic employment” concept). The estimation of employment from the national accounts may differ, as compared to other statistics and surveys, in particular the Labour Force Survey (LFS - in Romania, AMIGO). Even though, employment is defined according to the criteria of the International Labour Organization (ILO). The differences are conceptual and depend on the sources which have been used.

Thus, in the context of the national accounts, the employment integrates information from multiple sources, such as surveys on employment, population censuses, surveys on business, labour cost surveys etc., seeking to combine information to get a complete and consistent estimate, related to other variables, such as GDP, output, remuneration, etc.

The distinction between the domestic and the national concept is important in terms of employment in Romania, because our country is facing a particular situation. Much of the resident population able to work, has performed seasonal work abroad, leaving the country temporarily. In order to improve statistics on population and

14 Ghizdeanu I. - Applied Macroeconomics, Ed.Bren, Bucharest, 2007, ISBN 978-973-648-677-7, p. 24 15 The number of employees represents all the full title working people, on the basis of a formal or informal contract, for a resident institutional unit, a salary or an equivalent remuneration (National Institute of Statistics - National Accounts, Bucharest, 2015). 16 The persons (employees and self-employed) that perform a productive activity within the European System of Accounts (ESA) corresponding production, concerning residents and non-residents working in resident production units.

15

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

economy, all people living and working within the national territory must be taken into account. Due to the fact that the employed persons are important in terms of national accounts, they are considered according to the domestic concept. The persons included in the employed population must have a job within the national territory. The unemployed and those people not included in the labour force should have Romanian residence, in order to be included in the total population.

According to the domestic concept, within the employed population of Romania, the following groups of population may be statistically included: Romanians living in Romania, foreigners with Romanian residence, foreigners with annual residence permits, seasonal workers, border workers living abroad and working in Romania, holders of short-term permits, asylum seekers, the Romanian staff working abroad in embassies, consulates and on cargo vessels. The staff of foreign embassies, consulates and international organizations located in Romania, the persons living in Romania and working abroad and the Romanians who live and work abroad are not included in this category.

More significant differences have been noticed by activities, due to the same principle used for the gross domestic product, i.e. the concept of homogeneous branches17. The homogeneous branch includes both main and secondary activities of the same kind, specific to different economic units, meaning that a branch refers actually, only to comparable goods and services obtained through a specific technology. The difficulty consists of separating the secondary activities, using on this purpose, information from multiple statistical and administrative sources and conventions for weighting the importance of the secondary activities of a homogeneous branch. As a result, LFS survey data regarding the employees reconciliates with the information included in the Annual Structural Survey of Enterprises (ASA), but also with the data submitted by the business agents within the balance sheets.

According to the national accounts, data have revealed that the employment went up by 0.8% in 2014, compared to 2013, accordingly to LFS survey18.

In case of employees, the two dynamics are as follows: 1.7%, according to the national accounts and 1.9%, in line with the LFS survey.

The insufficiency of the data sources concerning the foreign labour flows did not produce significant differences, compared to the results of the LFS survey.

Overall, the number of employees within the national accounts is lower than the result of LFS surveys, showing partly, that the number of Romanian employees officially working abroad is higher than the number of specialists and foreign workers in Romania.

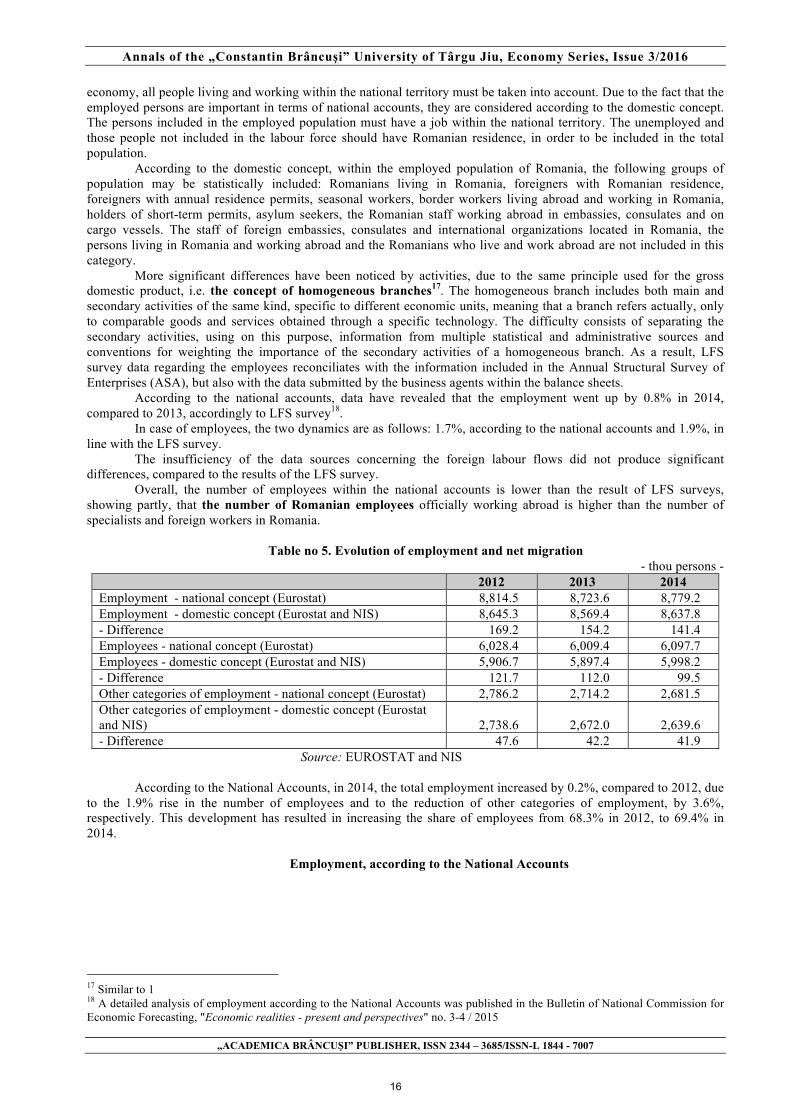

Table no 5. Evolution of employment and net migration

- thou persons - 2012 2013 2014

Employment - national concept (Eurostat) 8,814.5 8,723.6 8,779.2 Employment - domestic concept (Eurostat and NIS) 8,645.3 8,569.4 8,637.8 - Difference 169.2 154.2 141.4 Employees - national concept (Eurostat) 6,028.4 6,009.4 6,097.7 Employees - domestic concept (Eurostat and NIS) 5,906.7 5,897.4 5,998.2 - Difference 121.7 112.0 99.5 Other categories of employment - national concept (Eurostat) 2,786.2 2,714.2 2,681.5 Other categories of employment - domestic concept (Eurostat and NIS) 2,738.6 2,672.0 2,639.6 - Difference 47.6 42.2 41.9

Source: EUROSTAT and NIS

According to the National Accounts, in 2014, the total employment increased by 0.2%, compared to 2012, due to the 1.9% rise in the number of employees and to the reduction of other categories of employment, by 3.6%, respectively. This development has resulted in increasing the share of employees from 68.3% in 2012, to 69.4% in 2014.

Employment, according to the National Accounts

17 Similar to 1 18 A detailed analysis of employment according to the National Accounts was published in the Bulletin of National Commission for Economic Forecasting, "Economic realities - present and perspectives" no. 3-4 / 2015

16

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

5906,7 5897,4 5998,2

2738,6 2672,0 2639,6

0,0

2500,0

5000,0

7500,0

10000,0

2012 2013 2014

- mii p

ersoa

ne -

Salariati Alte categorii de populatie ocupata

8645,3 8569,4 8637,8

On long term, the trend described by the article regarding the relative stability in the number of employees, together with the reduction of employment due to the decline of non-wage employment activities, appears even more striking within the National Accounts. Evolution of employment is very suggestive for highlighting the productivity gains, because the National Accounts ensure the consistency between the gross domestic product and the employment who contributes to its achievement.

In 2016, the total employment was 20% lower than in 2000, due to a 46% decrease of the non-wage employment.

Table no 6.Employment in Romania -thou persons-

2000 2007 2014 Total employment 10,771.6 9,364.8 8,637.8 Number of employees 5,881.8 6,436.5 5,998.2 Other categories of employment 4,889.8 2,928.3 2,639.6 % of employees within employment 54.6 68.7 69.4

Source: NIS – National Accounts Relating to the reduction of non-wage employment, it is significant that, until the accession, this category has

diminished by almost 2 million persons, respectively by 40%. After the accession, the decrease was only by 288 thousand persons (almost 10%). The data are consistent with the intensity of the labour movement, from Romania to EU countries, before and after accession.

Within the concept of national accounts, the statistics regarding employment is important not only for international comparability – which is possible through the LFS survey - but especially for the derivative analysis, regarding for instance, productivity and competitiveness, where the equivalence between employees, remuneration and gross domestic product are necessary.

5. The unit labour costs

At the present times, after the economic and financial crisis particularly, competitiveness is a key parameter of the ability of an economy to cope with the competitive pressures within the European single market. Competitiveness is mainly analyzed by the correlation between wages and labour productivity and the productivity gains should not be cancelled by the wage policy of firms or governments.

In this perspective, competitiveness is analyzed by the unit labour costs in nominal and real terms. The unit labour costs has become, in fact, one of the most important indicators for assessing progress towards the Lisbon objectives and at the same time, one of the indicators forecasted by the European Commission (DG ECFIN) for all the Member States. The indicator is part of the dashboard, which monitors the macroeconomic imbalances in the EU.

The dashboard includes 11 significant indicators regarding the deficits and competitiveness19. Nominal unit labour costs are included within the dashboard (U.L.C.), which is calculated as an average of the percentage changes registered in the last 3 years, with an alert threshold for macroeconomic imbalances of plus 12, for the Member States outside the euro area20.

Especially in the view of economic forecasting, once a year, the national accounts system enables an accurate evaluation of labour costs for the whole economy, taking into account all labour costs. Such an approach is all the more necessary, as economies become increasingly economies for services. 19 Regulation (EU) no. 1176/2011 of the European Parliament and European Council from 16th of November 2011, regarding the prevention and correction of macroeconomic imbalances (OJ L 306 / 23.11.2011) 20 European Commission - Scoreboard for the surveillance of macroeconomic imbalances, February 2012

17

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

Basically, the unit labour costs compare the increase of total labour expenses, with labour productivity growth. The standard indicator – which is also included within the system of structural indicators - is calculated as the ratio between the unit growth of the employee remuneration and the increase of labour productivity21.

PQSRs

CUM =

Where: Rs -Remuneration of employees; S -Number of employees; Q -Gross domestic product; P - Employment.

In order to ensure data comparability between countries, concerning total employment and the number of employees, the same concepts and definitions (ESA 95) are being applied for all countries, consistent with the definitions of the International Labour Office (ILO). Problems of comparability between countries may occur, due to different structures and structural changes in their systems (e.g. the social security systems) and also as a result of different structures of employment (i.e. part-time employment and work opportunities).

The employee remuneration, as macroeconomic aggregate - generation of income account (D1 within the classification of the distribution transactions) is evaluated only in nominal values, within the Table of Integrated Economic Accounts. The assessment of this aggregate in real terms, induces approximations and in lack of a statistically determined price index for this aggregate, another deflator is used, by convention. Therefore, in terms of methodology, the Commission decided to use the second term of the report, in nominal and real terms, respectively the Gross Domestic Product.

According to the assessment of labour productivity - based on the nominal value of GDP and its real growth - there are two indicators, explaining the unit labour cost:

Ø The nominal unit labour costs - compensation per employee divided by the actual value of GDP per person employed;

Ø The real unit labour costs - compensation per employee divided by the nominal value of GDP per person employed.

Taking into consideration that prices can distort the accurate picture of the labour costs evolution - especially for countries like Romania, with higher inflation, but also with important differences between certain categories of prices - the real value is more expressive and it is more often used for analysis.

An increase in the real unit labour cost, due to higher employee remuneration as against productivity, may indicate both the difficulties in maintaining competitiveness and the demand-side pressures on inflation. There are, as well, approaches that emphasize negative values of dynamics for this indicator, due to differences in terms of employee remuneration. The comparison between the long-term evolution of real remuneration of labour with the percentage increase of the EU gross domestic product shows that the overall trend is improving the competitiveness.

During the period 1974-1985, the real remuneration in EU increased by 0.75 percentage points, corresponding to 1 per cent GDP growth, while in the period 1986-1990, the rate was 0.55/122. In recent times, after the economic and financial crisis of 2007-2008, a 0.5 percentage points increase of the real remuneration have corresponded to one per cent of economic growth.

Table no 7 The real unit labour costs

-annual percentage change- 2009 2010 2011 2012 2013 2014

France 3.4 -0.1 0.1 1.1 0.1 0.9 Germany 4.4 -2.0 -0.4 1.8 0.1 0.2 Italy 2.5 -0.3 -0.8 0.0 -0.4 -0.2 Poland -2.7 1.0 -2.2 -0.3 -0.1 -0.4 Czech Republic 0.0 1.5 0.8 1.7 -0.8 -2.3 Hungary -0.9 -3.5 -0.8 0.5 -2.1 -1.2

21 Remuneration of employees (part of gross value added) comprises the total payment, in cash (gross wages) or payment in kind, which an employer pays to an employee in return for a work carried out over a period of time, including the employer's contribution to Social Security. The employees (staff employed) are persons that work for a resident institutional unit and receive a salary, by agreement. Labour productivity is given by the ratio between the gross domestic product and employment, which includes both employees and private entrepreneurs. The number of people employed is calculated corresponding to the concepts of National Accounts (ESA 95), being different from the concepts of national statistics regarding employment. The accuracy of the data is monitored within the working group of Eurostat regarding the National Accounts. 22 Ciutacu C. - Labour Market, Ed. Expert, Bucharest, 2001, ISBN 973-8177-30-8, p. 226-227

18

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

Euro Zone 3.5 -1.4 -0.5 0.7 -0.1 0.2 EU28 3.2 -1.4 -0.9 0.5 -0.4 -0.3 Romania -1.5 -2.8 -10.0 -1.1 -3.9 1.4

Source: Eurostat Following the crisis, the real unit labour costs in EU, has recorded negative dynamics, showing a continuous

reduction in amplitude, which makes the concerns regarding competitiveness still valid, especially because Germany and France have recorded positive dynamics23 of the real unit labour costs, in the period 2012-2014 .

Romania was one of the few European countries with a high gain in competitiveness, after the economic and financial crisis. Besides the positive developments in the private sector, the dynamics presented in the table above were also encouraged by measures of adjusting personnel expenses in the public sector. In the period 2009-2013, the real unit labour costs in Romania were reduced by 18%, compared to 2008. Since 2014, a reverse trend of the real unit labour cost growth has occurred, which represent a concern for the stability and competitiveness. The 1.4% growth in 2014 is one of the highest in the European Union.

The positive development subsequent to the crisis was emphasized in the Country Report Romania 201624, which states: "Between 2009 and 2016, both productivity of the tradable sector and the nontradable sector rose by 6%, while employee remuneration increased by 2% and by 3%, respectively, during the same period".

In the same report, even if the evaluation refers to the total employment and not to the wage employment, the assessment of the positive trends actually regards the employees. As a result, we believe that two assessments of the European Commission are relevant, in comparison with the conclusions presented in the article. The document stresses that "labour market situation in Romania is generally better than in previous years" and "employment is particularly concentrated in sectors with high added value."

6. The unemployment after the economic crisis In statistical terms, the unemployment is measured - in two ways: total unemployment - as defined by the

International Labour Office (ILO - which focuses on availability and personal effort to find a job; evaluation is made quarterly, based on the " Labour Force Survey (AMIGO) "and the registered unemployment at the end of each month by the National Agency for Employment (NAE), only to the unemployed who have decided to seek a job through this agency.

In general, the developments of the two categories of unemployment are divergent, depending on the economic situation.

In 2010, after a 7.0% increase of the ILO and registered unemployment rate, in 2011 the ILO unemployment rate reached the highest value (7.2%), while the registered unemployment rate was 5.2%.

In 2012, the positive economic developments, led to a slight increase in employment and a reduction in the ILO unemployment rate (6.8%), the registered unemployment recording 5.4%.

In 2013, the impact on employment growth has been moderate and the unemployment rate was 7.1%. Among the economic factors that have influenced the evolution of unemployment one can mention: the large

share of the rural population, the existence of a state economic sector, the high percentage of the hidden economy, the existence of illegal work or “day labourers". As an argument, it is to notice that in 2013, the number of non-wage employed has increased by 2.3%, while the number of employees picked up by 0.2%.

During the periods of unemployment rate decreases (unpaid unemployed who have not renewed requests from NAE), the ILO the monthly unemployment rate seasonally adjusted has increased.

In 2015, the unemployment rate decreased from 5.54% in January to 4.9% in December, while the monthly rate of ILO unemployment in 2015 was identical to that in 2014, 6.8% respectively. In this period, the number of non-wage employees decreased by 1.5% in 2014 and 10.5% in 2015, while the number of employees increased by 1.9% in 2014 and 3.6% in 2015.

2010 2011 2012 2013 2014 2015

Total number of unemployed (ILO), thou persons 651.7 659.4 627.2 653.0 628.7 623.9

Unemployment rate (ILO), % 7.0 7.2 6.8 7.1 6.8 6.8 Number of unemployed registered at the end of the year, thou persons 627.0 461.0 493.8 512.3 478.3 436.2

Unemployment rate registered, % 7.0 5.2 5.4 5.7 5.4 4.9

23 "The forecast of the unit labour cost" from the Bulletin of National Commission for Economic Forecasting, "Economic realities - present and perspectives" no. 3/2006 24 European Commission, the Commission staff working paper "Country Report Romania 2016", the Romanian version, Brussels, 02.26.2016, SWD (2016) 91 final, p. 27

19

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 3/2016

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

Total number of unemployed in December (ILO), thou persons 624.0 672.9 631.6 650.4 609.6 616.0

Unemployment rate (ILO) in December, % 6.8 7.3 6.8 7.0 6.6 6.7

This evolution illustrates that the unemployment rate increases during periods of economic growth; the

existence of jobs makes many inactive people to seek employment on their own. In December 2015, the percentage difference between the two rates was 1.6 percentage points, close to the

gap before the crisis; in December 2008 there was a difference of 1.4 percentage points. The analysis of the monthly unemployment, seasonally adjusted, reveals that in the second half of the year,

once with the temporary passing of the graduates to unemployment (inactive population), between June and August 2015, the total unemployment rate was 6.8% and 6.9% in September, and the unemployment rate for adults (25-74 years) has increased to 5.6% and 5.7% respectively, versus 5.4% in March 2015.

In December, the number of unemployed aged 25-74 years corresponded to 77.6% of the total number of unemployed estimated for this month.

Overall, in the first six months the ILO monthly average unemployment rate (6.8%) was similar to that of previous years, reflecting the seasonality related to the school cycle and the registration as unemployed of 2015 graduates.

By gender, the unemployment rate for men (7.5%) was 1.7 percentage points higher than women (5.8%). At the end of 2015, the registered unemployment decreased by 42.1 thousand persons, compared to

December 2014. The decrease was due largely to measures included in the employment program 2015, providing bonuses and subsidies to employers who hire graduates (under 25 years and 25-29 years), resulting in significant reductions of unemployment (i.e. -10.5 and -5.9 thousand persons, respectively) in December 2015, compared to December 2014.

Due to the new jobs created and to the positive economic developments, other age groups have registered decreases in the unemployment rate; the most significant reductions have been recorded by the unemployed between 30 and 39 years, respectively by 13.4 thousand persons and also for the age group 40-49 years old (a reduction of 8.6 thousand persons).

In case of registered unemployment, as well, each year, one can notice the seasonality induced by the school cycle, thus, during the months following the end of school, the number of young unemployed (age under 25) have recorded significant increases (i.e. by 34.3 thousand people in August, compared to May 2015). In 2015, the social benefits were far below the employment.

A number of 124.5 thousand persons were employed and a number of 319.9 unemployed, which means a net employment of 195.4 (for unemployed). In 2015 the number of unemployed who receive compensations dropped from 140.3 in January, to 108.5 thousand persons in December, being the lowest number in the last 7 years; in the period 2009 - 2010 the number of unemployed receiving compensations was over 300 thousand persons in December (435.5 persons in December 2009 and 329.6 thousand persons in December 2010).

By age groups, the largest share is held by the unemployed aged 30 to 49 (48.1% at the end of 2015∗). Unemployed persons up to 25 years old accounted for 15.5% against 16.3% in December 2014 and those aged 25-29 years accounted for 7.6% against 8.2% in December 2014. Taking into account the fact that the increase of unemployed in July for youngsters aged under 25, as well as the reduction of the compensated unemployed by 57 thousand persons in July, as against December 2014 and by 32.5 thousand persons in December 2015, compared to December 2014, it may be appreciated that the level of ILO unemployment is explained by the high number of inactive persons, wishing to enter the labour market.

Within the inactive population, according to the NIS, there is a number of about 376 thousand persons who are not seeking for a job, could to start working if they had offers.; this category represents "the potential labour force" (4.1% of the labour force, compared to 3.9% at the EU level); in the future, this sample might fall temporarily within ILO unemployment, if new jobs will be created and the approach for the active search will not be difficult.

7. Conclusion The complexity of the labor market after the crisis is due to the specific features of the Romanian economy,