TAX CERTIFICATE AS TO ARBITRAGE AND THE PROVISIONS OF SECTIONS 103 AND 141-150 OF THE INTERNAL REVENUE CODE OF 1986 In connection with the sale and issuance by The City of St. Louis, Missouri (the "City") of its $231,275,000 Airport Revenue Refunding Bonds, Series 2007A (Non-AMT) (Lambert-St. Louis International Airport) (the "2007A Bonds") and its $104,735,000 Airport Revenue Refunding Bonds Series, 2007B (AMT) (Lambert-St. Louis International Airport) (the "2007B Bonds" and together with the 2007A Bonds, the "Bonds") and in furtherance of the covenants of the City contained in Section 6.05 of the Fourteenth Supplemental Indenture ofTrust between the City and UMB Bank, N.A., as trustee (the "Trustee"), dated as of January 1, 2007 (the "Fourteenth Supplemental Indenture") and Section 5.05 of the form of the Fifteenth Supplemental Indenture of Trust between the City and the Trustee, dated as of January 1, 2007 (the "Fifteenth Supplemental Indenture"), both of which amend and supplement (or will amend and supplement) the Amended and Restated Indenture of Trust dated as of October 15, 1984 and amended and restated as of September 10, 1997, between the City and UMB Bank, N.A., as trustee, as amended and supplemented (the "Restated Indenture" and together with the Fourteenth Supplemental Indenture and the Fifteenth Supplemental Indenture, the "Indenture"), and pursuant to Treas. Reg. §1.148-2(b)(2), the City makes and enters into the following Tax Certificate. SECTION 1. DEFINITIONS. Capitalized terms, if not defined herein shall have the meanings set forth in Appendix I or, where not so defined, in the Indenture. SECTION 2. REPRESENTATIONS. (a) Purpose. The 2007A Bonds are being issued on the date hereof (the "Delivery Date") to: (1) advance refund a portion of the City's Airport Revenue Bonds, Series 2001A (Airport Development Program) (Non-AMT) (the "Refunded 2001A Bonds"), (2) advance refund a portion of the City's Airport Revenue Bonds, Series 2002A (Capital Improvement Program) (Non-AMT) (the "Refunded 2002A Bonds" and together with the Refunded 2001A Bonds, the "Refunded Bonds"), (3) pay the bond insurance and surety premiums for the Bonds and to pay the costs of issuance of the 2007A Bonds. The 2007B Bonds are to be issued on April 3, 2007 (the "Forward Delivery Date") to: (1) current refund a portion of the City's Airport Revenue Bonds, Series 1997B (1997 Capital Improvement Program) Lambert-St. Louis International Airport (AMT) (the "Refunded 1997B Bonds"), and (2) to pay the bond insurance and surety premiums for the Bonds and to pay the costs of issuance of the 2007B Bonds. Attached as Exhibit D is a form of supplemental tax certificate (the "Supplemental Tax Certificate") to be executed by the City on the Forward Delivery Date. (b) Single Issue. All of the Bonds: (a) were sold at substantially the same time (i.e., within 15 days); (b) were sold pursuant to the same plan of financing; and (c) are reasonably expected to be paid from substantially the same source of funds, determined without regard to guarantees from unrelated parties. No other obligations will be: (a) sold at substantially the same time as the Bonds (i.e., less than 15 days from the date that the bond purchase agreements were 10254197.5 Confidential [email protected] 2020-01-16 13:59:27 +0000

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TAX CERTIFICATE AS TO ARBITRAGE AND THE PROVISIONS OF SECTIONS 103 AND 141-150 OF

THE INTERNAL REVENUE CODE OF 1986

In connection with the sale and issuance by The City of St. Louis, Missouri (the "City") of its $231,275,000 Airport Revenue Refunding Bonds, Series 2007A (Non-AMT) (Lambert-St. Louis International Airport) (the "2007A Bonds") and its $104,735,000 Airport Revenue Refunding Bonds Series, 2007B (AMT) (Lambert-St. Louis International Airport) (the "2007B Bonds" and together with the 2007 A Bonds, the "Bonds") and in furtherance of the covenants of the City contained in Section 6.05 of the Fourteenth Supplemental Indenture ofTrust between the City and UMB Bank, N.A., as trustee (the "Trustee"), dated as of January 1, 2007 (the "Fourteenth Supplemental Indenture") and Section 5.05 of the form of the Fifteenth Supplemental Indenture of Trust between the City and the Trustee, dated as of January 1, 2007 (the "Fifteenth Supplemental Indenture"), both of which amend and supplement (or will amend and supplement) the Amended and Restated Indenture of Trust dated as of October 15, 1984 and amended and restated as of September 10, 1997, between the City and UMB Bank, N.A., as trustee, as amended and supplemented (the "Restated Indenture" and together with the Fourteenth Supplemental Indenture and the Fifteenth Supplemental Indenture, the "Indenture"), and pursuant to Treas. Reg. §1.148-2(b)(2), the City makes and enters into the following Tax Certificate.

SECTION 1. DEFINITIONS. Capitalized terms, if not defined herein shall have the meanings set forth in Appendix I or, where not so defined, in the Indenture.

SECTION 2. REPRESENTATIONS.

(a) Purpose. The 2007A Bonds are being issued on the date hereof (the "Delivery Date") to: (1) advance refund a portion of the City's Airport Revenue Bonds, Series 2001A (Airport Development Program) (Non-AMT) (the "Refunded 2001A Bonds"), (2) advance refund a portion of the City's Airport Revenue Bonds, Series 2002A (Capital Improvement Program) (Non-AMT) (the "Refunded 2002A Bonds" and together with the Refunded 2001A Bonds, the "Refunded Bonds"), (3) pay the bond insurance and surety premiums for the Bonds and to pay the costs of issuance of the 2007 A Bonds.

The 2007B Bonds are to be issued on April 3, 2007 (the "Forward Delivery Date") to: (1) current refund a portion of the City's Airport Revenue Bonds, Series 1997B (1997 Capital Improvement Program) Lambert-St. Louis International Airport (AMT) (the "Refunded 1997B Bonds"), and (2) to pay the bond insurance and surety premiums for the Bonds and to pay the costs of issuance of the 2007B Bonds. Attached as Exhibit D is a form of supplemental tax certificate (the "Supplemental Tax Certificate") to be executed by the City on the Forward Delivery Date.

(b) Single Issue. All of the Bonds: (a) were sold at substantially the same time (i.e., within 15 days); (b) were sold pursuant to the same plan of financing; and (c) are reasonably expected to be paid from substantially the same source of funds, determined without regard to guarantees from unrelated parties. No other obligations will be: (a) sold at substantially the same time as the Bonds (i.e., less than 15 days from the date that the bond purchase agreements were

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

signed: January 10, 2007); (b) sold pursuant to the same plan of financing as the Bonds; and (c) reasonably expected to be paid from substantially the same source of funds as the Bonds, determined without regard to guarantees from unrelated parties.

(c) No Replacement; Average Maturity. No portion ofthe amounts received from the sale of the Bonds will be used as a substitute for other funds which were otherwise to be used as a source of financing for the projects financed with the Refunded Bonds or the Refunded 1997B Bonds or the refunding of the Refunded Bonds and the Refunded 1997B Bonds. The weighted average maturity of the 2007A Bonds (15.1895 years) does not exceed 120 percent of the weighted average economic life of the projects financed by the Refunded Bonds (the "NonAMT Project"). The weighted average maturity of the 2007B Bonds (14.8321 years) does not exceed the weighted average maturity of the Refunded 1997B Bonds (14.8639 years) and does not exceed 120 percent of the weighted average economic life of the projects financed by the Refunded 1997B Bonds (the "AMT Project"). Thus, neither the 2007A Bonds nor the 20007B Bonds are expected to be outstanding longer than the period reasonably necessary to accomplish the governmental purposes of such bonds.

10254197.5

(d) Refunded Bonds and Refunded 1997B Bonds.

(1) 1997 Bonds. On September 9, 1997, the City issued $40,420,000 of its Airport Revenue Bonds, Series 1997 A (1997 Capital Improvement Program) Lambert-St. Louis International Airport (Non-AMT) (the "1997A Bonds") and $159,185,000 of its Airport Revenue Bonds, Series 1997B (1997 Capital Improvement Program) Lambert-St. Louis International Airport (AMT) (the "1997B Bonds" and, collectively with the 1997A Bonds, the "1997 Bonds"). The City is current refunding a portion of the 1997B Bonds as further described in Exhibit F.

(2) 2001A Bonds. The City issued its $435,185,000 Airport Revenue Bonds, Series 2001A (Airport Development Program) (the "2001A Bonds") on May 15, 2001. The 2001A Bonds were issued to fund a portion of the cost of the acquisition of land adjacent to the Airport and the acquisition, design, construction, improvement, renovation, expansion, rehabilitation, and equipping of certain airport facilities and to capitalize interest on the 2001A Bonds, pay the bond insurance and surety bond premium, and pay the costs of issuance of the 2001A Bonds. The City is advance refunding a portion of the 2001A Bonds as further described in Exhibit F.

(3) 2002 Bonds. On December 19, 2002, the City issued $117,985,000 aggregate principal amount of Airport Revenue Bonds, Series 2002 (Capital Improvement Program) in three sub-series, the $69,195,000 Airport Revenue Bonds, Series 2002A (Capital Improvement Program) (Non-AMT) (the "Series 2002A Bonds"), the $31,755,000 Airport Revenue Bonds, Series 2002B (Capital Improvement Program) (AMT) (the "Series 2002B Bonds") and the $17,035,000 Airport Revenue Refunding Bonds, Series 2002C (AMT) (the "Series 2002C Bonds" and together with the 2002A Bonds and the 2002B Bonds, the "2002 Bonds"). The 2002 Bonds were issued for the purposes described below. The City is advance refunding a portion of the 2002A Bonds as further described in Exhibit F.

-2-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

(e) Multipurpose Issue Rule--Application to Refunded Bonds and Refunded 1997B Bonds. As set forth in the Tax Certificate as to Arbitrage and the Provisions of Sections 141-150 of the Internal Revenue Code of 1986 for the 2002 Bonds (the "2002 Tax Certificate"), the 2002 Bonds are a.Multipurpose Issue consisting of the following portions that are treated as separate issues under §1.148-9(h) and §1.150-1(c)(3): (1) the 2002A Bonds were issued to finance or reimburse a portion of the cost of the construction, improvement, renovation, expansion, rehabilitation and equipping of certain capital improvement projects for roadways, bridges, parking garages, light rail, airfield and other public facilities, (2) the 2002B Bonds were issued to finance or reimburse a portion of the cost of the construction, improvement, renovation, expansion, rehabilitation and equipping of certain capital improvement projects for terminal, concourse and other airline tenant improvements, and (3) the 2002C Bonds were issued to refund all of the City's outstanding Airport Revenue Refunding and Improvement Bonds, Series 1992, Lambert-St. Louis International Airport Project. The proceeds of the 2007 A Bonds being used to advance refund a portion of the 2001A Bonds and the 2002A Bonds and are not being used to refund the 2002B Bonds, the 2002C Bonds or the 1997 Bonds.

As set forth in the Arbitrage and Tax Certificate for the 1997 Bonds (the "1997 Tax Certificate"), the 1997 Bonds are a Multipurpose Issue consisting of the following portions that are treated as separate issues under §1.148-9(h) and §1.150-l(c)(3): (1) 1997A Bonds, which are allocable to costs of roadways and curbside improvements, design of the communications/electronics center, noise monitoring system, airfield maintenance facilities, ramp scrubber drain and storm sewer interceptor, and (2) the 1997B Bonds, as further described in the 1997 Tax Certificate, were further allocated for purposes of § 1.148-9(h) and § 1.150-l(c)(3) into two separate portions issued to finance (a) a 37.5% portion allocable to the apron and taxiway repellent cover and electrical vault seismic upgrades, and (b) a 62.5% portion allocable to terminal and parking improvements. The proceeds of the 2007B Bonds are to be used to current refund a portion of the 1997B Bonds and not being used to refund the 1997 A Bonds, the 2001A Bonds or the 2002 Bonds.

(t) Multipurpose Issue Rule--Application to 2007 A Bonds and 2007B Bonds. The Bonds are a Multipurpose Issue consisting of the following portions that are treated as separate issues under §1.141-13(d) (as revised and amended in a Notice ofProposed Rulemaking published in the Federal Register on September 26, 2006), §1.148-9(h) and §1.150-l(c)(3): (1) the portion allocable to the advance refunding of the Refunded Bonds, and (2) the portion allocable to the current refunding of the Refunded 1997B Bonds, and within the Refunded 1997B Bonds, two pro rata portions allocable to the two purposes described in paragraph (e) above. The Bonds are hereby allocated to the refunding of the Refunded Bonds and the Refunded 1997B Bonds in a manner that reflects the aggregate principal and interest payable in each Bond Year that is less than, equal to, or proportionate to, the aggregate principal and interest payable on the Refunded Bonds and the Refunded 1997B Bonds, respectively, in each Bond Year. Under this allocation, the 2007 A Bonds are allocable to the advance refunding of the Refunded Bonds and the 2007B Bonds are allocable to the current refunding of the Refunded 1997B Bonds. For this purpose, the common costs of the Bonds are allocated between the two purposes as follows: (1) costs of issuance were either allocated on a pro rata basis, based on costs specifically related to a particular series of bonds (e.g., underwriter's discount, trustee fees), or, with respect to the costs of issuance contingency, equally between the two series, (2) qualified guarantee fees (i.e., bond insurance and surety bonds) were allocated based on the fees

- 3-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

charged for each series of bonds, and (3) amounts deposited into the debt service reserve subaccounts and debt service sub-account were allocated based on the required deposits under the Fourteenth Supplemental Indenture and the Fifteenth Supplemental Indenture. See Exhibit F.

(g) Refunded Bonds, Refunded 1997B Bonds and Bonds Not Hedge Bonds. With respect to the Refunded 1997B Bonds, on the issue date of that issue, the City reasonably expected that at least 85 percent of the Spendable Proceeds of the 1997 Bonds would be used to carry out the governmental purpose of the 1997 Bonds within the three year period beginning on the date of issuance of the 1997 Bonds. Not more than 50 percent of the proceeds of the 1997 Bonds were be invested in Nonpurpose Investments having substantially guaranteed yields for four years or more.

In addition, with respect to the 2001A Bonds and the 2002 Bonds, at least 10 percent of the Spendable Proceeds of each such issue were reasonably expected by the City to be used to carry out the governmental purpose of each issue within the one year period beginning on the date of issuance of each such issue, at least 30 percent of the Spendable Proceeds of each such issue were reasonably expected by the City to be used to carry out the governmental purpose of each such issue within the two year period beginning on the date of issuance of each such issue, at least 60 percent of the Spendable Proceeds were reasonably expected by the City to be used to carry out the governmental purpose of each such issue within the three year period beginning on the date of issuance of each such issue, and at least 85 percent of the Spendable Proceeds were reasonably expected by the City to be used to carry out the governmental purpose of each such issue within the three year period beginning on the date of issuance of each such issue. All costs ofissance with respect to the 2001A Bonds and the 2002 Bonds were each reasonably expected by the City to be paid within 180 days of the date of issuance of each such issue and none of such costs were contingent.

Pursuant to Section 149(g)(3)(C)(i), the Bonds are not "hedge bonds" within the meaning of Section 149(g) of the Code because the 1997 Bonds, the 2001A Bonds and the 2002 Bonds satisfied the requirements of that section.

(h) Operating Rule. Pursuant to Treasury Regulations Section 1.148-9(i), each issue of which the Refunded Bonds are a part has been, as of the Delivery Date, or with respect to the Refunded 1997B Bonds will be, as of the Forward Delivery Date, separated into two portions, the refunded portion of each issue and the unrefunded portion of each issue. The refunded portion of each issue is based on a fraction (1) the numerator of which is the principal amount of each issue to be paid with proceeds of the 2007 A Bonds and the 2007B Bonds, as applicable; and (2) the denominator of which is the outstanding principal amount of each issue, determined as of the Delivery Date of the 2007A Bonds or the Forward Delivery Date of the 2007B Bonds, as applicable. For each issue that is being partially refunded, the unspent proceeds of each issue are allocated ratably, as of the Delivery Date or the Forward Delivery Date, as applicable, between the refunded and unrefunded portions of each issue. For purposes of this Section, "principal amount" means, in reference to a Plain Par Bond, its stated principal amount, and in reference to any other bond, its present value. The application of Treasury Regulations Section 1.148-9(i) to each ofthe 1997 Bonds, 2001A Bonds and 2002 Bonds is adjusted to take into account the fact that previously the City has partially refunded some of such bonds. The adjustment excludes from the denominator of the foregoing fraction the maturities of those bonds previously refunded

-4-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

and excludes from the ratable allocation of the unspent Proceeds of such issue, the Proceeds previously allocated to said maturities.

(i) Statement as to Facts, Estimates and Circumstances. The facts and estimates set forth in this Tax Certificate on which the City's expectations as to the amount and use of the Gross Proceeds of the Bonds are based are made to the best of the knowledge and belief of the undersigned officer of the City, and the City's expectations are reasonable.

(j) Responsible Person. The undersigned is an officer of the City responsible for the issuance of the Bonds, and has made due inquiry with respect to and is fully informed as to the matters set forth herein.

SECTION 3. REASONABLE EXPECTATIONS OF THE CITY AS TO FACTS, ESTIMATES AND CIRCUMSTANCES. The City makes the following representations and statements of fact and expectation on the basis of which it is not expected that the proceeds of the Bonds will be used in a manner that will cause the Bonds to be "arbitrage bonds" within the meaning of Section 148 of the Code:

10254197.5

(a) Application of Sale Proceeds-2007A Bonds.

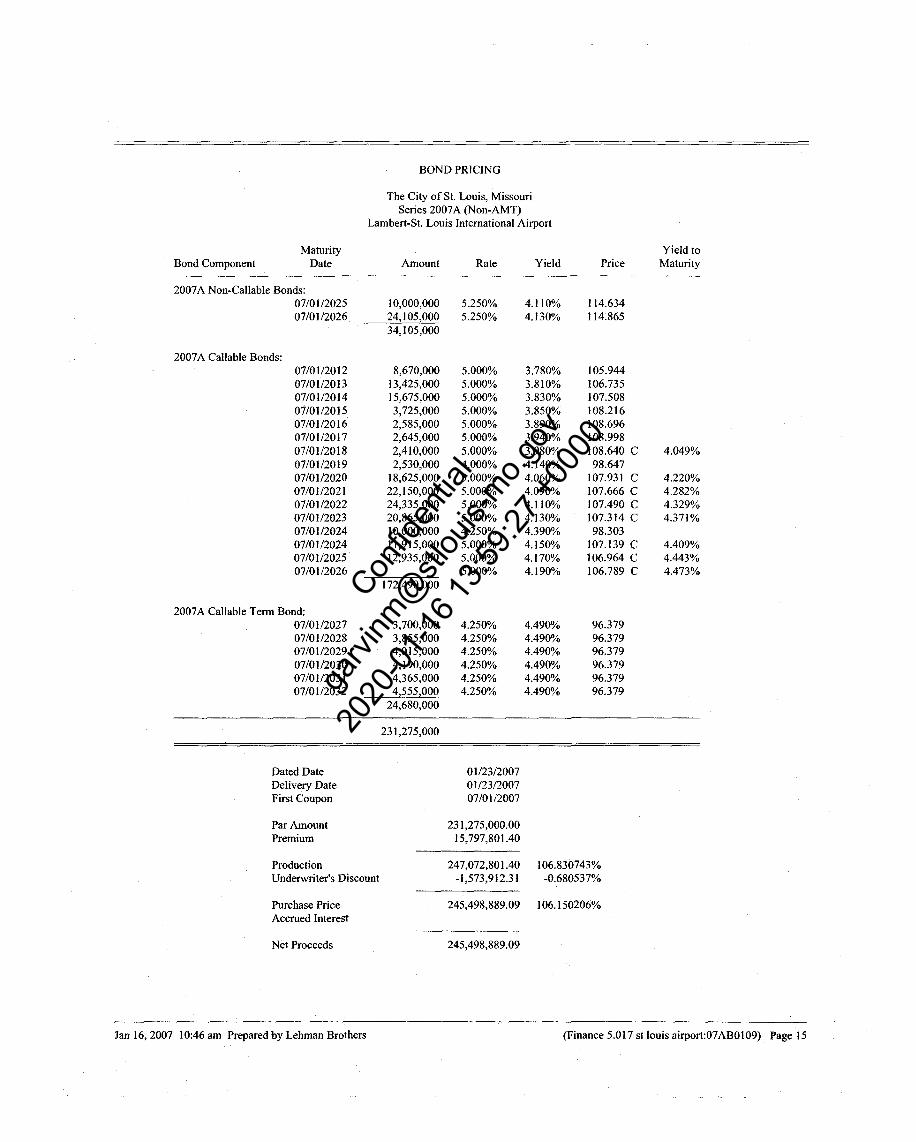

(1) Sale Proceeds; No Overissuance. The Sale Proceeds of the 2007A Bonds will be $247,072,801.40, which amount consists of the aggregate principal amount of the 2007A Bonds of $231,275,000.00 plus net original issue premium of $15,797,801.40. The Sale Proceeds and the investment earnings thereon do not exceed the amount necessary for the purpose set forth in Section 2(a) hereof.

(2) Escrow Fund. An amount of the Sale Proceeds of the 2007 A Bonds equal to $241,932,790.20 will be deposited on the date hereof in an escrow fund (the "2007 A Escrow Fund") and used to purchase United States Treasury Securities-State and Local Government Series ("SLGS") and to fund the beginning cash balance ($6.20) that will be used to pay the principal of, redemption premium and interest on the Refunded Bonds.

(3) Costs of Issuance. An amount of the Sale Proceeds equal to $1,003,995.03, will be deposited into the 2007A Costs of Issuance Sub-Account and will be expended within six months after the Delivery Date to provide for the payment of expenses incurred in connection with the issuance of the 2007 A Bonds, including, but not limited to Bond Counsel fees, financial advisor fees and printing costs. The rounding amount of $2,136.32 will also be deposited into the 2007A Costs of Issuance SubAccount.

(4) Underwriters' Discount. An amount of the Sale Proceeds equal to $1,573,912.31 will be used on the date hereof for the payment of the underwriters' discount with respect to the 2007 A Bonds.

(5) Bond Insurance. An amount of the Sale Proceeds equal to $2,559,967.54 will be used on the Delivery Date to purchase a bond insurance policy for the 2007 A

- 5-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

Bonds from Financial Security Assurance (the "Insurer") and to acquire a surety policy to fund the Debt Service Reserve Fund for the 2007A Bonds (the bond insurance policy and the surety policy are referred to as, the "2007 A Bond Insurance")

(b) Application of Sale Proceeds-2007B Bonds.

(1) Sale Proceeds; No Overissuance. On the Forward Delivery Date, the Sale Proceeds of the 2007B Bonds will be $111,059,499.30, which amount consists of the aggregate principal amount of the 2007B Bonds of $104,735,000.00 plus net original issue premium of $6,324,499.30. The Sale Proceeds and the investment earnings thereon do not exceed the amount necessary for the purpose set forth in Section 2(a) hereof.

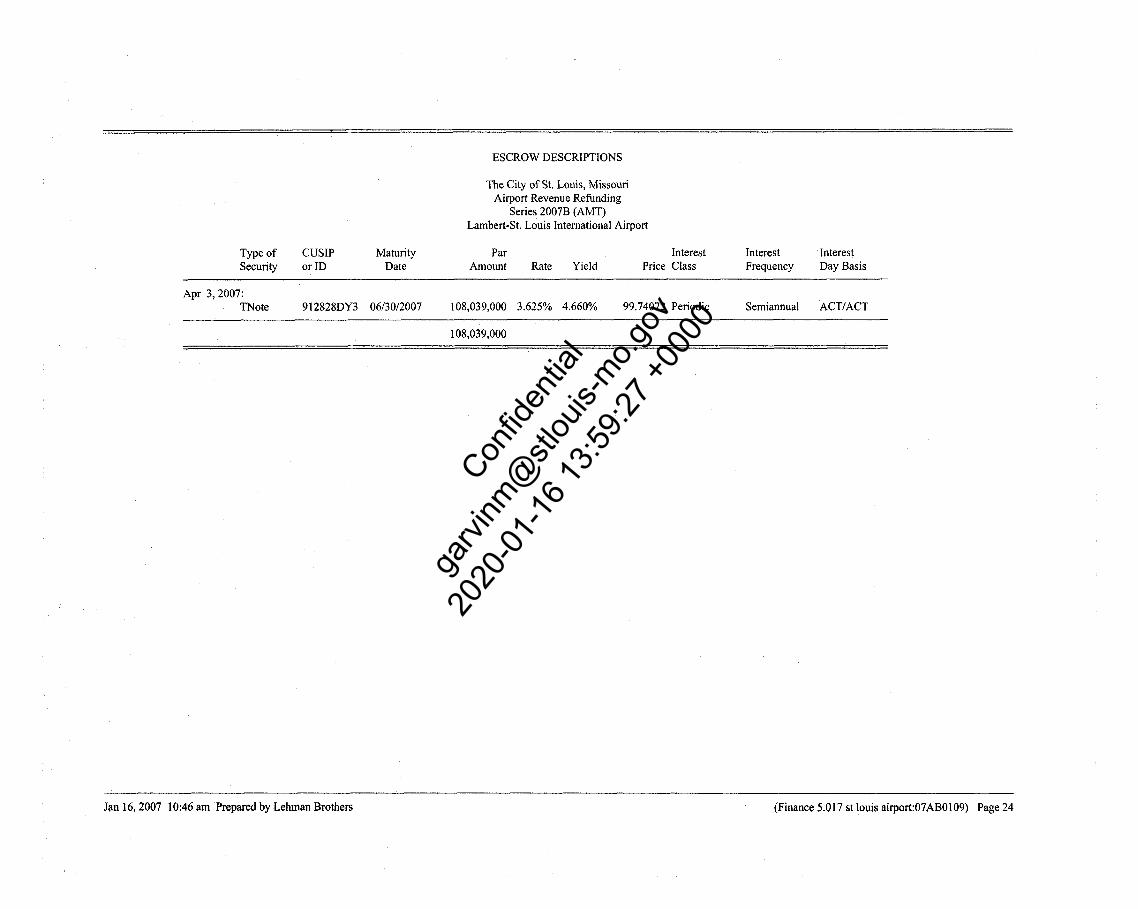

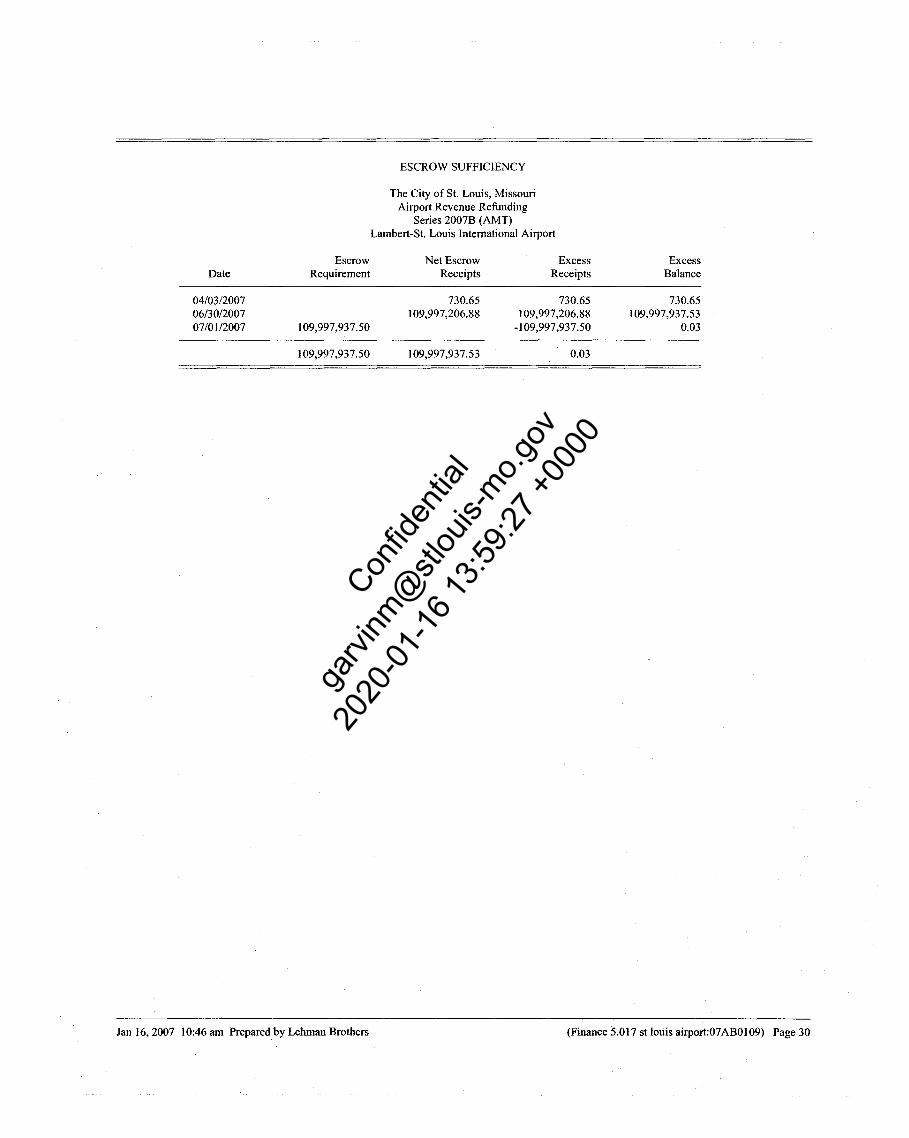

(2) Escrow Fund. An amount of the Sale Proceeds of the 2007B Bonds equal to $108,765,757.62 will be deposited on the Forward Delivery Date in an escrow fund (the "2007B Escrow Fund") and used to purchase a United States Treasury Note (the "TNote") and to fund the beginning cash balance ($730.65) that will be used to pay the principal of, redemption premium and interest on the Refunded 1997B Bonds.

(3) Costs of Issuance. An amount ofthe Sale Proceeds equal to $474,004.97, will be deposited into the 2007B Costs oflssuance Sub-Account on the Forward Delivery Date and will be expended within six months after the Forward Delivery Date to provide for the payment of expenses incurred in connection with the issuance of the 2007B Bonds, including, but not limited to Bond Counsel fees, financial advisor fees and printing costs. The rounding amount of$3,757.08 will also be deposited into the 2007B Costs of Issuance Sub-Account.

(4) Underwriters' Discount. An amount of the Sale Proceeds equal to $737,299.14 will be used on the Forward Delivery Date hereof for the payment of the underwriters' discount with respect to the 2007B Bonds.

(5) Bond Insurance. An amount of the Sale Proceeds equal to $1,078,680.49 will be used on the Forward Delivery Date to purchase a bond insurance policy for the 2007B Bonds from the Insurer and to acquire a surety policy to fund the Debt Service Reserve Fund for the 2007B Bonds (the bond insurance policy and the surety policy are referred to as, the "2007B Bond Insurance").

(c) Investment Proceeds. Earnings on amounts held in the 2007A Debt Service Sub-Account (the "2007 A Debt Service Sub-Account"), the 2007B Debt Service Sub-Account (the "2007B Debt Service Sub-Account"), the 2007 A Debt Service Reserve Sub-Account (the "2007 A Debt Service Reserve Sub-Account") and the 2007B Debt Service Reserve SubAccount (the "2007B Debt Service Reserve Sub-Account"), will be transferred to the Revenue Fund. Earnings on amounts in the Arbitrage Rebate Fund shall be retained therein. Earnings on amounts in the Operations and Maintenance Fund, Renewal and Replacement Fund, the Contingency Fund, the Debt Service Stabilization Fund, the PFC Account and the Development Fund will be retained in such respective accounts or transferred to the Revenue Fund as provided under the Indenture.

-6-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

10254197.5

(d) Funds on Hand Related to the Refunded Bonds.

(1) Debt Service Reserve Account. There are Proceeds of the Refunded 2002A Bonds on deposit in the 2002A Debt Service Reserve Sub-Account equal to $4,604,681.00. These amounts will be deposited in the 2007 A Debt Service Reserve Sub-Account.

(2) Debt Service Account. There are amounts on deposit in the 2002A Debt Service Sub-Account and the 2001A Debt Service Sub-Account relating to the Refunded Bonds totaling $996,986.56 that were deposited into such accounts after the date the 2007 A Bonds were sold and before the Delivery Date. Had the 2007 A Bonds not been issued, these amounts would have been used to pay debt service on the Refunded Bonds on July 1, 2007. These amounts will be deposited into the 2007A Debt Service SubAccount and used to pay debt service on the 2007A Bonds on July 1, 2007.

(3) Construction Fund. There are Proceeds of the Refunded Bonds on deposit in the Construction Fund that will be used to fund the governmental purposes as the Refunded Bonds (i.e., the Non-AMT Project).

(4) No Other Amounts. Other than the amounts described in this subsection (d), there are no original, investment, or transferred proceeds of the Refunded Bonds that remain unspent on the Delivery Date or amounts that would, absent the issuance of the 2007 A Bonds, have been used to pay debt service on the Refunded Bonds.

(e) Funds on Hand Related to the Refunded 1997B Bonds.

(1) Debt Service Reserve Account. There are proceeds of the Refunded 1997B Bonds on deposit in the 1997B Debt Service Reserve Sub-Account equal to $7,783,490.00. These amounts will be deposited in the Series 2007B Debt Service Reserve Sub-Account.

(2) Debt Service Account. There are amounts on deposit in the 1997B Debt Service Sub-Account relating to the Refunded 1997B Bonds in the amount of $464,406.25 that were deposited into such account after the date the 2007B Bonds were sold and before the Delivery Date. In addition, between the Delivery Date and the Forward Delivery Date, an amount equal to $928,812.50 is expected to be deposited into the 1997B Debt Service Sub-Account relating to the Refunded 1997B Bonds. Had the 2007B Bonds not been issued, these amounts would have been used to pay debt service on the Refunded 1997B Bonds on July 1, 2007. On the Forward Delivery Date, these amounts will be deposited into the 2007B Debt Service Sub-Account and used to pay debt service on the 2007B Bonds on July 1, 2007.

(3) Construction Fund. There are Proceeds of the Refunded 1997B Bonds on deposit in the Construction Fund that will be used to fund the governmental purposes as the Refunded 1997B Bonds (i.e., the AMT Project).

- 7-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

10254197.5

(4) No Other Amounts. Other than the amounts described in this subsection (e), there are no original, investment, or transferred proceeds of the Refunded 1997B Bonds that remain unspent on the Delivery Date or amounts that would, absent the issuance of the 2007B Bonds, have been used to pay debt service on the Refunded 1997B Bonds.

(f) Funds and Accounts.

(1) Airport Revenue Fund and 2007 A Debt Service Sub-Account. Revenues will be transferred to the Airport Revenue Fund and such amounts will be transferred to the 2007 A Debt Service Sub-Account to the extent necessary for the amounts on deposit in the 2007A Debt Service Sub-Account to satisfy the principal and interest requirements of the 2007 A Bonds. Amounts on deposit in the 2007 A Debt Service Sub-Account will be used to pay principal of and interest on the Bonds and other bonds issued under the Indenture.

The 2007A Debt Service Sub-Account and the Revenue Fund (to the extent reasonably expected to pay debt service on the Bonds) (the "2007A Debt Service Fund") will be used primarily to achieve a proper matching of revenues and debt service on the 2007 A Bonds in each Bond Year and will be depleted at least once each year except for a reasonable carryover amount not exceeding the greater of (i) the earnings on such accounts for the immediately preceding bond year, or (ii) one-twelfth of the principal of and interest payments on the 2007 A Bonds for the immediately preceding bond year.

(2) Airport Revenue Fund and 20078 Debt Service Sub-Account. Revenues will be transferred to the Airport Revenue Fund and such amounts will be transferred to the 2007B Debt Service Sub-Account to the extent necessary for the amounts on deposit in the 2007B Debt Service Sub-Account to satisfy the principal and interest requirements of the 2007B Bonds. Amounts on deposit in the 2007B Debt Service Sub-Account will be used to pay principal of and interest on the 2007B Bonds and other bonds issued under the Indenture.

The 2007B Debt Service Sub-Account and the Revenue Fund (to the extent reasonably expected to pay debt service on the Bonds) (the "2007B Debt Service Fund") will be used primarily to achieve a proper matching of revenues and debt service on the 2007B Bonds in each Bond Year and will be depleted at least once each year except for a reasonable carryover amount not exceeding the greater of (i) the earnings on such accounts for the immediately preceding bond year, or (ii) one-twelfth of the principal of and interest payments on the 2007B Bonds for the immediately preceding bond year.

(3) Debt Service Reserve Sub-Account. Funds in the 2007 A Debt Service Reserve Sub-Account will be transferred to the 2007 A Debt Service Sub-Account, if needed, to make up any deficiency therein. In the event of a temporary interruption of revenues, the 2007A Debt Service Reserve Sub-Account is intended to provide for the

- 8-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

10254197.5

payment of debt service on the 2007 A Bonds. Lehman Brothers, as representative of the underwriters for the 2007 A Bonds (the "2007 A Underwriter"), has represented that, the establishment and continued existence of the 2007 A Debt Service Reserve Sub-Account (as provided in the Indenture) was and is a vital and necessary factor in obtaining the 2007 A Bond Insurance and the 2007 A Bond Insurance was a vital and necessary factor in the marketing of the 2007 A Bonds to the public at the yields and terms that the 2007 A Bonds were sold.

Funds in the 2007B Debt Service Reserve Sub-Account will be transferred to the 2007B Debt Service Sub-Account, if needed, to make up any deficiency therein. In the event of a temporary interruption of revenues, the 2007B Debt Service Reserve SubAccount is intended to provide for the payment of debt service on the 2007B Bonds. Merrill Lynch & Co., as representative of the underwriters for the 2007B Bonds (the "2007B Underwriter"), has represented that, the establishment and continued existence of the 2007B Debt Service Reserve Sub-Account (as provided in the Indenture) was and is a vital and necessary factor in obtaining the 2007B Bond Insurance and the 2007B Bond Insurance was a vital and necessary factor in the marketing of the 2007B Bonds to the public at the yields and terms that the 2007B Bonds were sold.

To the extent the amount of Gross Proceeds of the Bonds on deposit in the Debt Service Reserve Fund does not exceed the limitations contained in section 3(h)(2) of this Tax Certificate, such fund will constitute a ''reasonably required reserve or replacement fund."

( 4) Debt Service Stabilization Fund; PFC Account. The amounts on deposit in the Debt Service Stabilization Fund will be used for transfers to the Debt Service Fund to the extent Revenues are insufficient therefore, for emergency debt service needs with respect to debt issued for the Airport, or for other Airport operational emergencies.

Pledged PFC Revenues not required to be used for debt service on certain bonds under the Indenture will be transferred by the City to the PFC Account and, provided certain conditions of the Indenture are satisfied, such amounts may be used by the City for various purposes. Under the Indenture, it is reasonably expected that Pledged PFC Revenues will be accumulated in the PFC Account and required to be held to pay debt service on the 2007 A Bonds and other bonds secured by such Pledged PFC Revenues.

(5) No Other Funds. Other than the 2007 A Costs of Issuance Sub-Account, the 2007B Costs of Issuance Sub-Account, the 2007 A Escrow Fund, the 2007B Escrow Fund, the 2007 A Debt Service Sub-Account, the 2007 A Debt Service Reserve SubAccount, the 2007B Debt Service Sub-Account, the 2007B Debt Service Reserve SubAccount, the Revenue Fund, the Operations and Maintenance Fund, the Contingency Fund, the Renewal and Replacement Fund, the Development Fund, the Debt Service Stabilization Fund, and the Arbitrage Rebate Fund, no fund or account which secures or otherwise relates to the Bonds has been established, nor are any funds or accounts expected to be established, pursuant to any instrument. With respect to the amounts on deposit in the ·Development Fund, the Operations and Maintenance Fund, the

-9-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

Contingency Fund, the Arbitrage Rebate Fund and the Renewal and Replacement Fund, the amounts deposited therein are not reasonably expected to be used to pay debt service on the Bonds, nor is there is a reasonable assurance that amounts on deposit therein will be available to pay debt service on the Bonds in the event that the City encounters financial difficulties, including any amount held under an agreement to maintain the amount at a particular level for the direct or indirect benefit of the bondholders or a guarantor of the Bonds.

(g) Compliance with Reimbursement Regulations. To the extent Proceeds of the Refunded Bonds or the Refunded 1997B Bonds are to be used or were used to reimburse the City for costs of the Non-AMT Project or the AMT Project, respectively, the City or its authorized representative satisfied the requirements of Section 1.150-2 of the Treasury Regulations. That section provides that, except for "preliminary expenditures" (within the meaning of Treasury Regulation Section 1.150-2(f)(2)) or an amount not in excess of$100,000, all of the expenditures to be reimbursed must be paid no earlier than 60 days before the date the City passed its declaration of intent to reimburse an original expenditure with proceeds of an obligation. Except for preliminary expenditures or an amount not in excess of $100,000, the reimbursement allocation must be made not later than 18 months after the later of (1) the date the original expenditures were paid; or (2) the date the project is placed in service or abandoned, but in no event more than three years after the original expenditures were paid. All of the amounts to be reimbursed must be Capital Expenditures or expenditures otherwise described in Section 1.150-2(d)(3) of the Treasury Regulations. Other than amounts deposited into a bona fide debt service fund (as defined in Treasury Regulation Section 1.148-1 ), funds corresponding to the reimbursed amounts may not be used in a manner that results in the creation of Replacement Proceeds of any bonds.

10254197.5

(h) Transferred Proceeds.

(1) General. At the time that Proceeds of the 2007A Bonds or 2007B Bonds discharge any of the outstanding principal of the Refunded Bonds or the Refunded 1997B Bonds, as applicable, proceeds of the Refunded Bonds or Refunded 1997B Bonds become transferred proceeds of the 2007 A Bonds or the 2007B Bonds ("Transferred Proceeds") and cease to be proceeds of the Refunded Bonds or Refunded 1997B Bonds. The amount of proceeds of the Refunded Bonds or Refunded 1997B Bonds that become Transferred Proceeds is an amount equal to the total proceeds of the Refunded Bonds or Refunded 1997B Bonds at the time of that discharge multiplied by a fraction, the numerator of which is the principal amount of the Refunded Bonds or Refunded 1997B Bonds discharged with Proceeds of the 2007 A Bonds or 2007B Bonds, as applicable, and the denominator of which is the total outstanding principal amount of the Refunded Bonds or Refunded 1997B Bonds, as applicable, immediately prior to that discharge. For purposes of this section, "principal amount" means, in reference to a Plain Par Bond, its stated principal amount, and in reference to any other bond, its present value. See Section 2(h) and Appendix VI.

(2) Allocation. Investments of proceeds of the Refunded Bonds or the Refunded 1997B Bonds are allocated to the Transferred Proceeds by consistent application of either the ratable allocation method or the representative allocation

- 10-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

10254197.5

method. Under the ratable allocation method, a ratable portion of each investment of proceeds of the Refunded Bonds or Refunded 1997B Bonds is allocated to Transferred Proceeds. Under the representative allocation method, representative portions of the portfolio of investments of proceeds of the Refunded Bonds or Refunded 1997B Bonds are allocated to the Transferred Proceeds. Whether a portion is representative is based on all the facts and circumstances, including, without limitation, whether the current yields, maturities and current unrealized gains and losses on the particular allocated investments are reasonably comparable to those of the unallocated investments in the aggregate. In addition, if a portion of Nonpurpose Investments is otherwise representative, it is within the City's discretion to allocate the portion from whichever source of funds it deems appropriate.

(3) Unspent Proceeds. The only unspent Proceeds of the Refunded Bonds on the date hereof are Proceeds deposited in the 2007A Debt Service Reserve Sub-Account and the Construction Fund. The only unspent Proceeds of the Refunded 1997B Bonds on the date hereof are Proceeds deposited in the 2007B Debt Service Reserve Sub-Account and the Construction Fund.

(i) Bond Yield.

(1) In general. The yield on the Bonds (the "Bond Yield") is the discount rate that, when used in computing the present value on the Delivery Date of all the expected payments of principal and interest and fees for qualified guarantees and qualified hedges that are paid and to be paid on the Bonds, produces an amount equal to the present value, using the same discount rate, of the aggregate issue price of the Bonds on the Delivery Date.

(2) Issue Price. Based on the representations the 2007 A Underwriter, as of the Delivery Date the aggregate issue price of the Bonds (the "2007A Issue Price") is $247,072,801.40 (the face amount of the Bonds ($231,275,000.00), plus original issue premium ($15,797,801.40). See Exhibit A-1.

Based on the representations the 2007B Underwriter, as of the Forward Delivery Date the aggregate issue price of the Bonds (the "2007B Issue Price" and together with the 2007A Issue Price, the "Issue Price") is $111,059,499.30 (the face amount of the Bonds ($104,735,000.00), plus original issue premium ($6,324,499.30). See ExhibitA-2.

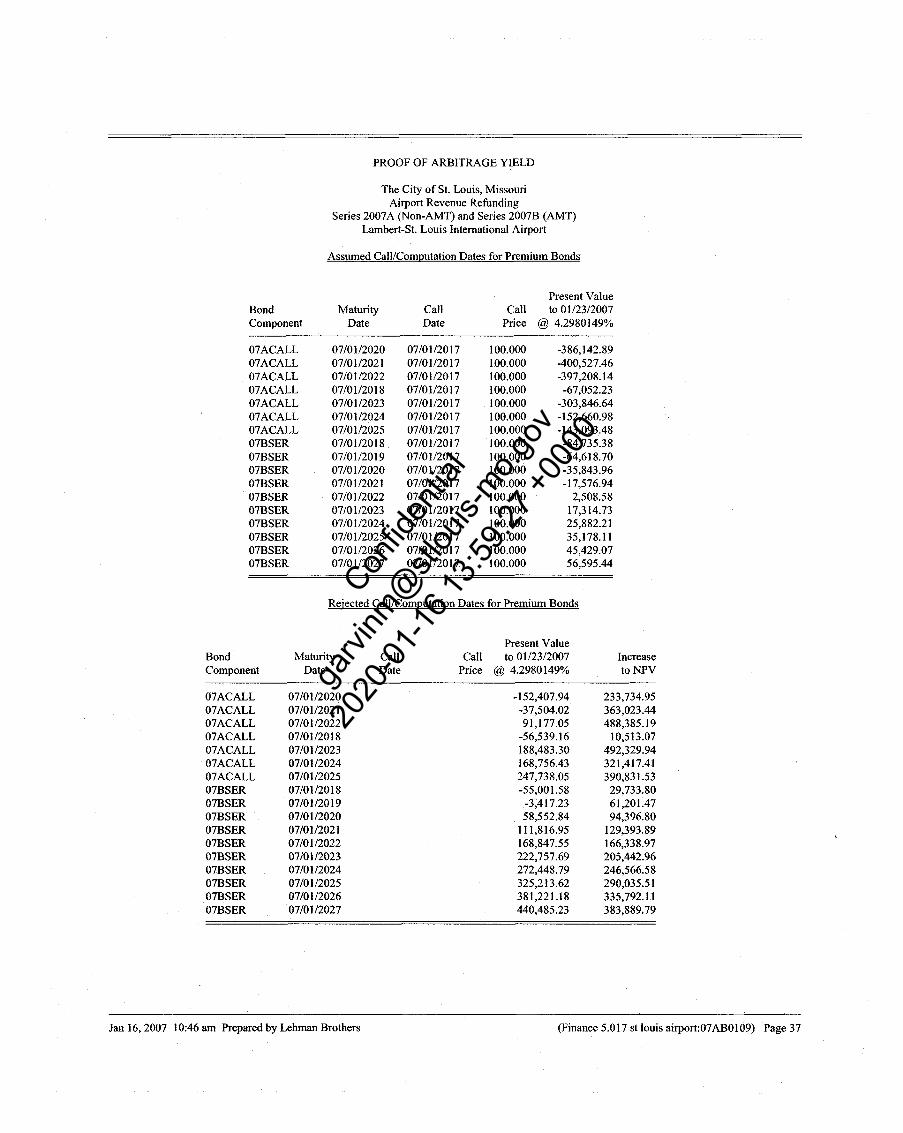

(3) Callable Premium Bonds. A portion of the Bonds (the "Callable Premium Bonds") are subject to optional early redemption and were sold at an issue price that exceeds the stated redemption price at maturity by more than ~ of 1 percent multiplied by the product of the stated redemption price at maturity and the number of complete years to the first optional redemption date for the Callable Premium Bonds. In accordance with Treasury Regulation Section 1.148-4(b )(3 ), the yield on the Bonds has been calculated by treating the Callable Premium Bonds as redeemed on the call date that produces the lowest yield on the Bonds. Accordingly, the yield on the Bonds was calculated by treating each of the Callable Premium Bonds as redeemed on July 1, 2017 at par.

- 11-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

10254197.5

( 4) Qualified Guarantee. Based in part on the representations of the 2007 A Underwriter, the 2007B Underwriter and the Insurer, the Issuer makes the following representations regarding the 2007 A Bond Insurance and the 2007B Bond Insurance:

(i) Interest savings. The Issuer reasonably expects that the present value of the fees for the 2007 A Bond Insurance and the 2007B Bond Insurance will be less than the present value of the expected interest savings on the 2007 A Bonds and the 2007B Bonds, as applicable, as a result of the 2007 A Bond Insurance and the 2007B Bond Insurance. For this purpose, present value is computed using the yield on each of the 2007 A Bonds and the 2007B Bonds as the discount rate (determined with regard to payments for the 2007 A Bond Insurance and the 2007B Bond Insurance, as applicable), but treating the Callable Premium Bonds as remaining outstanding until their stated maturity.

(ii) Guarantee in substance. The 2007 A Bond Insurance and the 2007B Bond Insurance each create a guarantee in substance. The 2007 A Bond Insurance and the 2007B Bond Insurance each impose a secondary liability that unconditionally shifts substantially all of the credit risk for all or part of the payments, such as payments for principal and interest, redemption prices, or tender prices, on the 2007 A Bonds and the 2007B Bonds, as applicable. The Insurer is not a co-obligor on the Bonds. The Insurer does not expect to make any payments on the Bonds. The Insurer (or any related party) is not using any portion of the proceeds of the Bonds.

(iii) Reasonable charge. Fees for the each of the 2007A Bond Insurance and the 2007B Bond Insurance do not exceed a reasonable, arm'slength charge for the transfer of credit risk. None of the fees for the 2007 A Bond Insurance and the 2007B Bond Insurance include any payment for any direct or indirect services other than the transfer of credit risk.

Based on the foregoing, Bond Counsel has advised the City that the fees paid to the Insurer for the 2007 A Bond Insurance and the 2007B Bond Insurance will constitute payments for a "qualified guarantee" within the meaning of Treasury Regulation Section 1.148-4(f). See Exhibits A and C. Consistent with Treasury Regulation Section 1.148-4(f)(6), the payments for the qualified guarantees will be allocated to the Bonds and to Computation Periods in a manner that properly reflects the proportionate credit risk for which the guarantor is compensated.

(5) Qualified Hedge. The City has not and does not expect to enter into any "hedge" (within the meaning of Treasury Regulation Section 1.148-4(h)(2)(i)) with respect to the Bonds.

(6) Computation. Based upon calculations performed by the 2007 A Underwriter and the 2007B Underwriter, and verified in the Verification Report of Grant Thornton dated as ofthe date hereof(the "Verification Report"), the yield on the Bonds is not less than 4.2980 percent.

- 12-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

(7) Single Issue. As described in Section 2(b) hereof, all of the Bonds are part of a single issue within the meaning of Section 1.150-1 (c) of the Treasury Regulations. To the extent that the 2007B Bonds are unexpectedly not issued on the Forward Delivery Date, the City will consult with Bond Counsel and take such action as is, in the opinion of Bond Counsel, necessary to ensure that the interest on the Bonds is excludable from gross income for Federal income tax purposes.

(j) Expectations Regarding Yield Limitations.

(1) Generally.

Fund or Temporary Restriction Excepted Account** Period of After From

Unrestricted Temporary Rebate Investment Period* (Y)/(N)

Construction Fund None Bond Yield N plus 118th of 1

percentage point

2007 A Debt Service Reserve Sub- Unlimited NIA N Account; 2007B Debt Service Reserve Sub-Account-not in

excess of Reserve Limit

2007 A Debt Service Reserve Sub- None Bond Yield N Account; 2007B Debt Service plus 1/8th of 1

Reserve Sub-Account-in excess percentage of Reserve Limit point

2007 A Debt Service Fund; 2007B 13 months Bond Yield N Debt Service Fund plus 111 oooth

ofl percentage

point

Replacement Proceeds 30 days Bond Yield N plus 1/1 oooth

of1 percentage

point

Investment Earnings - 1 Year from Receipt Bond Yield N Construction Fund plus 1/8th of 1

Percent

Costs of Issuance 90 days Bond Yield N

- 13-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

Investment Earnings - 2007 A One Year Bond Yield N Debt Service Fund, 2007B Debt

Service Fund, 2007 A Debt Service Reserve Sub-Account, 2007B Debt

Service Reserve Sub-Account, Debt Service Stabilization Fund;

PFCAccount

2007 A Escrow Fund None Bond Yield N plus 111 oooth

of1 percentage

point

2007B Escrow Fund 90 days Bond Yield y plus 111 oooth of1 Percent

Debt Service Stabilization Fund; 30 days Bond Yield N PFCAccount plus 111 oooth

of1 percentage

point

* In the event that any Gross Proceeds are subject to a materially higher yield spread of the Bond Yield plus 1/8 of 1 percentage point and any other Gross Proceeds are subject to materially higher yield spread of the Bond Yield plus 1/1000 of 1 percentage point, then all of the Gross Proceeds are subject to a materially higher yield spread of the Bond Yield plus 111000 of one percent.

** Amounts in the Arbitrage Rebate Fund are subject to arbitrage rebate and yield restriction and rebate only to the extent that they constitute Proceeds of the Bonds. The City will consult with Bond Counsel if Proceeds of the Bonds are deposited into the Arbitrage Rebate Fund.

10254197.5

(2) Debt Service Reserve Account. The amounts in the Debt Service Reserve Fund may be invested without regard to yield restriction to the extent that such amount does not exceed the least of (i) 10 percent of the Issue Price of the Bonds ($35,813,230.07), (ii) maximum annual principal of and interest on the Bonds ($42,118,162.50) or (iii) 125 percent of the average annual principal of and interest on the Bonds ($28, 782, 798.00) (the "Reserve Limit"). To the extent the amount in the Debt Service Reserve Fund exceeds the Reserve Limit, such excess will be invested at a yield not in excess of the Bond Yield either directly or by making the appropriate "yield reduction payments" if permitted under Treasury Regulation 1.148-5(c), or will be invested in bonds the interest on which is excludable from gross income under section 103 of the Code (other than "specified private activity bonds" within the meaning of Section 57(a)(5)(C) of the Code).

(3) 2007 A Escrow Fund. The Sale Proceeds of the 2007 A Bonds on deposit in the 2007 A Escrow Fund have been invested in SLGs at a yield not in excess of the Bond Yield. The City waives any applicable temporary period applicable to these

- 14-

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

investments. Based upon calculations performed by 2007 A Underwriter and the 2007B Underwriter, and verified in the Verification Report, the yield on the SLGs is not more than 4.2976 percent. See Exhibit H.

(4) 2007B Escrow Fund. The Sale Proceeds of the 2007B Bonds to be deposited into the 2007B Escrow Fund on the Forward Delivery Date are to be invested in the TNote, and are expected to satisfy the 6-month exception to the arbitrage rebate requirement described in Section 4. The TNote is being acquired by the City using a bidding procedure intended to comply with the requirements of Treasury Regulation Section 1.148-5(d)(6)(iii). See Exhibit E, with contains forms of bidding agent and provider certificates to be executed with respect to the purchase of the TNote on the Forward Delivery Date.

(5) Debt Service Stabilization Fund; PFC Account. Amounts on deposit in the Debt Service Stabilization Fund and the PFC Account must be allocated among the bonds secured thereby and may not be invested at a yield in excess of the yield on the related bonds.

(6) Temporary Period for Refunded Bonds and Refunded 1997B Bonds. The proceeds of the Refunded Bonds and the Refunded 1997B Bonds may not be invested at a yield in excess of the yield on the related issue of Refunded Bonds or Refunded 1997B Bonds, provided that Proceeds of such bonds on deposit in the 2007 A Debt Service Reserve Sub-Account and the 2007B Debt Service Reserve Sub-Account may be invested without regard to yield prior to becoming Transferred Proceeds of the Bonds to the extent they do not exceed the Reserve Limit.

(7) Existing Investments. An allocable portion of the investments previously used for amounts deposited into the 2001A Debt Service Sub-Account and the 2002A Debt Service Sub-Account is being modified and transferred to the 2007A Debt Service Sub-Account. An allocable portion of the investment for the Proceeds on deposit in the 1997 Debt Service Reserve Sub-Account is being transferred to the 2007B Debt Service Reserve Sub-Account.

(k) Excess Gross Proceeds. All Gross Proceeds deposited into the 2007 A Escrow Fund will be used to pay debt service on the Refunded Bonds except for the ending cash balance therein. In addition, except as described in subsections (a) through (f) hereof, there are no other amounts which constitute sale, investment or transferred proceeds of the Refunded Bonds, Sale Proceeds or Transferred Proceeds of the 2007 A Bonds, or investment earnings on such Sale Proceeds or Transferred Proceeds. All Gross Proceeds (including Sale Proceeds, Investment Proceeds and Transferred Proceeds) of the 2007A Bonds allocable to the refunding of the Refunded Bonds will consist of Gross Proceeds allocable to (i) the payment of, interest, or call premium on the Refunded Bonds; (ii) interest on the 2007 A Bonds that accrues for a period up to the completion date of any capital project for which the Refunded Bonds were issued, plus one year; (iii) a reasonably required reserve or replacement fund for the 2007 A Bonds or investment proceeds of such a fund; (iv) the payment of costs of issuance of the 2007 A Bonds; (v) the payment of administrative costs allocable to repaying the Refunded Bonds, carrying and repaying the 2007ABonds, or investments of the Proceeds of the 2007A Bonds; (vi) Transferred

- 15-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

Proceeds that will be used or maintained for the governmental purpose of the Refunded Bonds; (vii) interest on Purpose Investments; (viii) Replacement Proceeds that will be used or maintained for the governmental purpose of the 2007 A Bonds; and (ix) qualified guarantee fees for the 2007A Bonds or the Refunded Bonds. For purposes of this subsection (k), all unspent proceeds of the Refunded Bonds shall, as of the Delivery Date, be treated as Transferred Proceeds of the 2007 A Bonds.

SECTION 4. REBATE REQUIREMENT, CALCULATIONS AND PAYMENT. The City has covenanted to comply with the Rebate Requirement of Section 148(t) of the Code. The regulations promulgated thereunder are described in Appendix II. The regulations provide various spending exceptions to the Rebate Requirement which provides generally that if certain spenddown and other requirements are satisfied earnings on certain proceeds are excepted from the Rebate Requirement. The spending exceptions to the Rebate Requirement are described in Appendix V.

SECTION 5. ALLOCATION AND ACCOUNTING RULES. The City has covenanted to comply with this Tax Certificate which includes the allocation and accounting rules described in Appendix III for purposes of allocating Gross Proceeds to the Bonds, allocating Gross Proceeds to investments, and allocating Gross Proceeds to expenditures.

SECTION 6. PROHIBITED INVESTMENTS AND DISPOSITIONS. Upon the purchase or sale of a Nonpurpose Investment, Gross Proceeds of an issue are not allocated to a payment for that Nonpurpose Investment in an amount greater than, or to a receipt from that Nonpurpose Investment in an amount less than, the fair market value of the Nonpurpose Investment as of the purchase or sale date. The fair market value of a Nonpurpose Investment is adjusted to take into account Qualified Administrative Costs allocable to the investment. Thus, Qualified Administrative Costs increase the payments for, or decrease the receipts from, a Nonpurpose Investment. The City shall comply with the procedures with respect to compliance with these requirements contained in Appendix IV.

SECTION 7. NO FEDERAL GUARANTEE. The Bonds are not federally guaranteed within the meaning of section 149(b) of the Code. A bond will be federally guaranteed if (A) the payment of principal or interest with respect to such bond is guaranteed (in whole or in part) by the United States (or any agency or instrumentality thereof), (B) such bond is issued as part of an issue and 5 percent or more of the proceeds of such issue is to be (i) used in making loans the payment of principal or interest with respect to which are to be guaranteed (in whole or in part) by the United States (or any agency or instrumentality thereof), or (ii) invested (directly or indirectly) in federally insured deposits or accounts, or (C) the payment of principal or interest on such bond is otherwise indirectly guaranteed (in whole or in part) by the United States (or an agency or instrumentality thereof). Notwithstanding the foregoing, the Issuer may invest the Proceeds of the Bonds in any investment guaranteed by the following agencies of the United States: (a) the Federal Housing Administration; (b) the Veterans Administration; (c) the Federal National Mortgage Association; (d) the Federal Home Loan Mortgage Corporation; and (e) the Government National Mortgage Association. Moreover, the Issuer may invest the Proceeds of the Bonds (a) during an initial temporary period until such proceeds are needed for the purpose for which the Bonds were issued; (b) in a bona fide debt service fund; (c) in a reasonably required reserve or replacement fund; (d) in obligations issued by the United States Treasury; (e)

- 16-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

in obligations issued pursuant to Section 21B(d)(3) of the Federal Home Loan Bank Act, as amended by Section 511(a) of the Financial Institutions Reform, Recovery, and Enforcement Act of 1989, or any successor provision; or (f) in a refunding escrow.

SECTION 8. 2007 A BONDS-RESTRICTIONS ON NONGOVERNMENTAL USE.

(a) Generally. The 2007A Bonds are "state or local bonds" that are not ''private activity bonds" under Section 103 of the Code. The City covenants that (a) no more than five percent or $5 million in the aggregate of the Sale Proceeds of the 2007 A Bonds will be used to make or finance loans (other than loans which enable the borrower to finance any governmental tax or assessment of general application for an essential governmental function or which are used to acquire or carry Nonpurpose Investments) to any person other than a governmental unit ("Private Loans"); (b) no more than the lesser of (i) 10 percent or (ii) $15 million of the Sale Proceeds of the 2007 A Bonds will be used in any trade or business carried on by any natural person or any activity carried on by anyone other than a natural person or a state or local governmental unit (a "Private Business Use"). In addition, no more than 5 percent of such proceeds shall be used for ''unrelated" or "disproportionate related" Private Business Use. For purposes of this section, any use of the Non-AMT Project as a member of the general public shall be disregarded. The City covenants to obtain an opinion of Bond Counsel as to the continuing tax-exempt status of the interest on the 2007A Bonds in the event that the use of the 2007 A Bond proceeds changes or is to be changed in a manner that would violate these restrictions.

The Proceeds of the Refunded Bonds were and will be used for improvements that relate to portions of the Airport that are not leased or otherwise used for a Private Business Use by any airline or other nongovernmental person. For example, no portion of the Proceeds of the 2007A Bonds will be used to finance improvements of portions of Airport terminals leased to nongovernmental persons.

The airfield improvements will not be used for a Private Business Use. With respect to the airfield improvements, those facilities will be available for take-off, landings, and other use by any operator of an aircraft desiring to use the airport, including general aviation operators who are natural persons not engaged in a trade or business. It is reasonably expected that most of the actual use of the runway will be by private air carriers in connection with the airport terminals leased by those carriers. These leases for the use of terminal space provide no priority rights or other preferential benefits to the air carriers for use of the runways and related improvements. Under the leases, the lease payments are determined without taking into account the revenues generated by runway landing fees (that is, the lease payments are not determined on a residual basis). Signatory Airlines currently pay fees for landings pursuant to a rate schedule different from that applicable to other airlines. These different rates are customary and reasonable and the City does not and will not limit the availability of these rates to Signatory Airlines. Any new use agreements with the airlines will contain similar provisions and will be submitted to Bond Counsel for a determination that such agreements will not adversely affect the exclusion from gross income of interest on the 2007 A Bonds.

(b) Rules of Application. The rules described in paragraph (a) are referred to as the "Private Activity Bond Limitations." The City will not permit any additional Private

- 17-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

Business Use or Private Loans with respect to the proceeds of the 2007A Bonds unless an opinion of Bond Counsel is obtained prior to such use or loans that the exclusion from gross income of interest on the Bonds will not be adversely affected by such use or loans. The Private Activity Bond Limitations are imposed individually against each issue of bonds without regard to the use of proceeds of any other issue of outstanding bonds. The City understands from discussions with Bond Counsel that in applying the Private Activity Bond Limitations it must take into account both its reasonable expectations as of the date hereof regarding the expected uses of the proceeds of the 2007 A Bonds (and the facilities financed with such proceeds) throughout the stated term of the 2007A Bonds (that is, until the final stated maturity date) as well as any deliberate actions that may occur during the term of the 2007A Bonds (without regard to those reasonable expectations).

(c) Private Business Use. Any activity carried on by a person other than a natural person is treated as a trade or business. Both actual and beneficial use by a nongovernmental person may be treated as Private Business Use. In most cases, there is Private Business Use only if a nongovernmental person has special legal entitlements to use the financed property under an arrangement with the issuer. In general, a nongovernmental person is treated as a private business user of proceeds and financed property as a result of ownership; actual or beneficial use of property pursuant to a lease, or a management or incentive payment contract; or certain other arrangements such as a take or pay or other output-type contract. Use as a member of the general public is not Private Business Use. With respect to property that is not available for use by the general public, Private Business Use may be established on the basis of a "special economic benefit" to one or more nongovernmental persons, even if they have no special legal entitlements to use of the property. Appendix VII and VIII set forth guidelines for management or service contracts and certain other uses that will not constitute Private Business Use.

(d) Measurement Period for Refunding Portion. The average amount of Private Business Use of the Non-AMT Project from the issue dates ofthe Refunded Bonds until the Delivery Date does not exceed the limitation on Private Business Use described in Section 8(a) ofthis Tax Certificate.

SECTION 9. 2007B BONDS-COMPLIANCE WITH QUALIFIED PRIVATE ACTIVITY BOND REQUIREMENTS. The Proceeds of the 2007B Bonds will be used to refinance the Refunded 1997B Bonds, which were issued for improvements that relate to the terminal, concourse and other airline tenant improvements. Pursuant to the separate issue election made in Section 2(c) hereof, the 2007B Bonds is a separate issue of qualified private activity bonds under Section 142(a)(1) ofthe Code. The City covenants, warrants and represents that the following private activity bond requirements have been met with respect to the 2007B Bonds:

(a) Average Maturity. The weighted average maturity of the 2007B Bonds does not exceed 120% of the average reasonably expected economic life of the AMT Project.

(b) Public Approval. The issuance of the 1997B Bonds was approved by the Mayor of the City on September 10, 1997 following a public hearing on August 4, 1997, notification of which was published on July 20, 1997 in the St. Louis Post-Dispatch. Attached hereto as Exhibit I is a copy of the notice of public hearing required by Section 147(f) of the Code, and

- 18-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

Mayor's approval. The weighted average maturity of the 2007B Bonds (14.8321 years) is not later than the weighted average maturity of the Refunded 1997B Bonds (14.8639 years), and therefore, no approval with respect to the 2007B Bonds is required, as provided in Section 147(f)(2)(D) ofthe Code.

(c) Prohibited Facilities. The City will not use any of the Proceeds of2007B Bonds to finance or refinance any airplane, skybox or other private luxury box, facility used for gambling, massage parlors, stadiums or store the principal business of which is the sale of alcoholic beverage for consumption off premises.

(d) Qualified Costs. At least ninety-five percent (95%) of the Net Proceeds of the 2007B Bonds will finance or refinance qualified costs constituting an exempt airport facility under Section 142(a)(l) ofthe Code.

(e) Public Use. The AMT Project is part of the Airport which serves or is available on a regular basis for general public use.

(f) Functionally Related. To the extent the AMT Project includes facilities that are functionally related and subordinate to the Airport, such facilities are of a character and size commensurate with the character and size of the Airport.

(g) Office. Any office financed or refinanced by the 2007B Bonds is located on the premises of the Airport and will be used exclusively for purposes directly related to the Airport's day-to-day operations.

(h) Facility Restrictions. The AMT Project does not include any of the following:

(1) any lodging facility;

(2) any retail facilities (including food and beverage facilities) if they are in excess of a size necessary to serve passengers and employees at the Airport;

(3) any retail facilities (other than parking) for passengers or the general public (including rental car lots) located outside the terminal;

(4) office buildings for individuals who are not employees of a governmental unit or of the operating authority for the Airport; and

(5) industrial parks or manufacturing facilities.

(i) Safe Harbor Leases. The AMT Project is owned by the City and any lease or management contract of any portion of such projects will meet the following requirements.

(1) the lessee will make an irrevocable election not to claim depreciation or investment tax credit with respect to such property;

- 19-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

(2) the lease term is no more than eighty percent (80%) of the reasonably expected economic useful life of the property used (determined in the same manner as under Section 147(b) of the Code); and

(3) there is no option to purchase at other than fair market value (as of the time the option is exercised).

(j) Volume Cap. No volume cap allocation is required for the 2007B Bonds under Section 146(g)(3) of the Code.

(k) Land. Less than 25% of the Net Proceeds of the 2007B Bonds was or will be used to finance or refinance the acquisition of land.

(I) New Property. No portion of the Proceeds of the 2007B Bonds will be used to finance or refinance the acquisition of an interest in any property unless the first use of such property was pursuant to such acquisition.

(m) Costs of Issuance. No more than two percent of the Sale Proceeds of the 2007B Bonds will be used to pay expenses incurred in connection with the issuance of the 2007B Bonds, including, but not limited to, underwriters' discount, bond counsel fees and printing costs.

SECTION 10. REFUNDING LIMITATIONS. The Refunded Bonds being advance refunded using Proceeds of the 2007 A Bonds are entitled to be advance refunded under the restrictions imposed by section 149( d). The Refunded Bonds being advance refunded are being retired using the Proceeds of the 2007 A Bonds and such amounts are sufficient to accomplish this refunding. The issuance of the 2007 A Bonds will result in the City realizing present value debt service savings, and accordingly, the Refunded Bonds being advance refunded are being redeemed not later than the earliest date on which such Refunded Bonds may be redeemed.

The Refunded 1997B Bonds are being current refunded using Proceeds of the 2007B Bonds, which bonds are being issued within 90 days of the call date of the Refunded 1997B Bonds.

SECTION 11. INFORMATION REPORTING. The City has reviewed the Internal Revenue Service Form 8038-G to be filed in connection with the issuance ofthe 2007A Bonds, a copy of which is attached hereto as Exhibit B-1, and all of the information contained therein is, to the best of the City's knowledge, true and complete. The City has reviewed the Internal Revenue Service Form 8038 to be filed in connection with the issuance of the 2007B Bonds, a copy of which is attached hereto as Exhibit B-2, and all of the information contained therein is, to the best of the City's knowledge, true and complete.

SECTION 12. BONDS ISSUED IN REGISTERED FORM. In accordance with Section 149(a) of the Code, the Bonds are being issued in registered form.

SECTION 13. NOT POOLED FINANCING BONDS. No proceeds of the Bonds will be used to make or finance loans to 2 or more ultimate borrowers within the meaning of Section 149( t) of the Code.

-20-

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

SECTION 14. RECORD KEEPING. The City covenants to maintain records to support the representations, certifications and expectations set forth in this Tax Certificate until the date six ( 6) years after the last of the Bonds will be retired, and if any of the Bonds are refunded with the proceeds of tax-exempt obligations other than the Bonds ("Refunding Obligations"), the date six (6) years after the last of the Refunding Obligations will be retired. The records that must be retained include, but are not limited to:

(a) Basic records and documents relating to the Bonds;

(b) Documentation evidencing the expenditure of Bond proceeds;

(c) Documentation evidencing the use of a project by public and private sources (i.e., copies of management contracts, research agreements, leases, etc.);

(d) Documentation evidencing all sources of payment or security for the Bonds;

(e) Documentation evidencing compliance with the timing and allocation of expenditures of Bond proceeds;

(t) Documentation pertaining to any investment of Bond proceeds (including the purchase and sale of securities, SLGs subscriptions, yield calculations for each class of investments, actual investment income received from the investment of proceeds, guaranteed investment contracts, and rebate calculations);

(g) Records of all amounts paid to the United States pursuant to Section 4 above.

SECTION 15. AMENDMENTS. This Tax Certificate has been executed pursuant to Section 6.05 of the Fourteenth Supplemental Indenture and Section 5.05 of the Fifteenth Supplemental Indenture wherein the City has covenanted to comply with the provisions of this Tax Certificate in order to maintain the exclusion of interest on the Bonds from gross income for purposes of Federal income taxation. This Tax Certificate sets forth the information, representations, and procedures necessary in order for Bond Counsel to render its opinion regarding the exclusion of interest on the Bonds from gross income for purposes of Federal income taxation and may be amended or supplemented from time to time to maintain such exclusion only with the approval of Bond CounseL

Notwithstanding any other provision herein, the covenants and obligations contained herein may be and shall be deemed modified to the extent the City secures an opinion of Bond Counsel that any action required hereunder is no longer required or that some further action is required in order to maintain the exclusion of interest on the Bonds from gross income for purposes of Federal income taxation.

-21 -

10254197.5

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

SECTION 16. SUPPLEMENTATION OF THIS CERTIFICATE. The City understands the need to supplement this Tax Certificate periodically to reflect further developments in the Federal income tax laws governing the exclusion from Federal gross income of interest on the Bonds and will, periodically, seek the advice of its Bond Counsel as to the propriety of seeking the review of and supplements to this Tax Certificate from Bond Counsel.

Dated: January 23, 2007 THE CITY OF ST. LOUIS, MISSOURI

By: &~k-.-Darlene Green r Comptroller

22

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

Exhibit A-t

Initial Issue Price Certificate-2007 A Bonds

The City of St. Louis St. Louis, Missouri

Hardwick Law Firm, LLC Kansas City, Missouri

Nixon Peabody LLP New York, New York

January 23,2007

Re: $231,275,000 The City of St. Louis, Missouri, Airport Revenue Refunding Bonds, Series 2007 A (Non-AMT) (Lambert-St. Louis International Airport)

Gentlemen and Ladies:

We have served as representative of the underwriters (the "Underwriter") in connection with the issuance by The City of St. Louis, Missouri (the "Issuer") of its $231,275,000 Airport Revenue Refunding Bonds, Series 2007A (Non-AMT) (Lambert-St. Louis International Airport) (the "Bonds").

We hereby certify that:

a. Based on our records and other information available to us which we have no reason to believe is not correct, all of the Bonds have been the subject of a bona fide initial offering to the public (excluding bond houses, brokers or similar persons or organizations acting in the capacity of underwriters or wholesalers) at prices no higher than, or yields no lower than, those shown on the inside cover of the Official Statement ofthe Issuer dated January 10, 2007, as supplemented on January 22, 2007, relating to the Bonds (the "Official Statement").

b. Based on our records and other information available to us which we have no reason to believe is not correct, at least 10 percent of each maturity of the Bonds was first sold to the public (excluding bond houses, brokers or similar persons or organizations acting in the capacity of underwriters or wholesalers) at initial offering prices no higher than, or yields no lower than, those shown on the inside cover of the Official Statement.

c. At the time we agreed to purchase the Bonds, based upon then prevailing market conditions, we had no reason to believe any of the Bonds would be initially sold to the public (excluding such bond houses, brokers or similar persons or organizations acting in the capacity of underwriters or wholesalers) at prices higher than the prices, or yields no lower than, those shown on the inside cover of the Official Statement.

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

d. The prices at which the Bonds were sold did not exceed the fair market value of the Bonds on the sale date of the Bonds.

e. The issue price of the Bonds is $247,072,801.40.

£ In connection with the issuance of the Bonds, a premium (the "Insurance Premium") is being paid to Financial Security Assurance, Inc. (the "Insurer") for a policy of municipal bond insurance for the Bonds (the "Bond Insurance") and a surety bond policy for the 2007 A Debt Service Reserve Sub-Account (the "Surety Bond" and together with the Bond Insurance, the "Policy"). Based on that information and the Underwriter's knowledge and experience and, as to (2) below, based on an estimate by the Underwriter of the yields at which such obligations would have sold in the absence of the Policy: (1) the aggregate premium paid for the Policy does not exceed a reasonable charge for the transfer of credit risk, taking into account charges by bond insurers in similar transactions with which the Underwriter is familiar; and (2) the present value ofthe premiums paid for the Policy is less than the present value of the interest reasonably expected to be saved on the Bonds as a result of the Policy, for which purpose present value is computed by using the yield-to-maturity on the Bonds (taking into account the premiums paid for the Policy) as the discount rate.

g. In the opinion of the Underwriter, based on its knowledge of the financial markets, the establishment and continued existence of the 2007 A Debt Service Reserve SubAccount (as provided in the Indenture securing the Bonds) was and is a vital and necessary factor in obtaining the Bond Insurance and the Bond Insurance was a vital and necessary factor in the marketing of the Bonds to the public at the yields and terms that the Bonds were sold.

We understand that Hardwick Law Firm, LLC and Nixon Peabody LLP may rely upon this certification, among other things, in providing an opinion that interest on the Bonds is excluded from gross income for Federal income tax purposes.

LEHMAN BROTHERS

2

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

ExhibitA-2

Initial Issue Price Certificate-2007B Bonds

The City of St. Louis St. Louis, Missouri

Hardwick Law Firm, LLC Kansas City, Missouri

Nixon Peabody LLP New York, New York

January 23, 2007

Re: $104,735,000 The City of St. Louis, Missouri, Airport Revenue Refunding Bonds, Series 2007B (AMT) (Lambert-St. Louis International Airport)

Gentlemen and Ladies:

We have served as representative of the underwriters (the "Underwriter") in connection with the issuance by The City of St. Louis, Missouri (the "Issuer") of its $104,735,000 Airport Revenue Refunding Bonds, Series 2007B (AMT) (Lambert-St. Louis International Airport) (the "Bonds").

We hereby certify that:

a. Based on our records and other information available to us which we have no reason to believe is not correct, all of the Bonds have been the subject of a bona fide initial offering to the public (excluding bond houses, brokers or similar persons or organizations acting in the capacity of underwriters or wholesalers) at prices no higher than, or yields no lower than, those shown on the inside cover of the Official Statement of the Issuer dated January 10, 2007 relating to the Bonds (the "Official Statement").

b. Based on our records and other information available to us which we have no reason to believe is not correct, at least 10 percent of each maturity of the Bonds was first sold to the public (excluding bond houses, brokers or similar persons or organizations acting in the capacity of underwriters or wholesalers) at initial offering prices no higher than, or yields no lower than, those shown on the inside cover of the Official Statement.

c. At the time we agreed to purchase the Bonds, based upon then prevailing market conditions, we had no reason to believe any of the Bonds would be initially sold to the public (excluding such bond houses, brokers or similar persons or organizations acting in the capacity of

Confid

entia

l

garvi

nm@

stlou

is-mo.g

ov

2020

-01-16

13:59

:27 +0

000

underwriters or wholesalers) at prices higher than the prices, or yields no lower than, those shown on the inside cover of the Official Statement.

d. The prices at which the Bonds were sold did not exceed the fair market value of the Bonds on the sale date of the Bonds.

e. The issue price of the Bonds is $111,059,499.30.