Name: Syed Hayat Enterprise Risk Management Table of Contents Case Study - Risk Analysis of Eastman Kodak ............................................................................... 2 Problem Statement ................................................................................................................. 2 Introduction ............................................................................................................................ 3 A Look into the Board and its Oversight ................................................................................... 4 Risk Factor Disclosure .............................................................................................................. 5 Market risk analysis ............................................................................................................. 6 Irrelevant statements found in the proxy disclosure. ........................................................... 6 Conclusion .................................................................................................................................. 7 References .................................................................................................................................. 8 Appendix A –2010 ....................................................................................................................... 9 Boards Oversight - Def 14A ...................................................................................................... 9 Interesting Note .................................................................................................................. 9 Risk Factor Disclosure ............................................................................................................ 10 Proxy Statement - 10-k ...................................................................................................... 10 Market Risk ....................................................................................................................... 17 Appendix B –2006 ..................................................................................................................... 19 Boards Oversight - Def 14A .................................................................................................... 19 Risk Factor Disclosure ............................................................................................................ 19 Proxy Statement 10-k ........................................................................................................ 19 Market Risks ...................................................................................................................... 26 Appendix C- SOX Summary ........................................................................................................ 28

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Name: Syed Hayat

Enterprise Risk Management

Table of Contents Case Study - Risk Analysis of Eastman Kodak ............................................................................... 2

Problem Statement ................................................................................................................. 2

Introduction ............................................................................................................................ 3

A Look into the Board and its Oversight ................................................................................... 4

Risk Factor Disclosure .............................................................................................................. 5

Market risk analysis ............................................................................................................. 6

Irrelevant statements found in the proxy disclosure. ........................................................... 6

Conclusion .................................................................................................................................. 7

References .................................................................................................................................. 8

Appendix A –2010 ....................................................................................................................... 9

Boards Oversight - Def 14A ...................................................................................................... 9

Interesting Note .................................................................................................................. 9

Risk Factor Disclosure ............................................................................................................ 10

Proxy Statement - 10-k ...................................................................................................... 10

Market Risk ....................................................................................................................... 17

Appendix B –2006 ..................................................................................................................... 19

Boards Oversight - Def 14A .................................................................................................... 19

Risk Factor Disclosure ............................................................................................................ 19

Proxy Statement 10-k ........................................................................................................ 19

Market Risks ...................................................................................................................... 26

Appendix C- SOX Summary ........................................................................................................ 28

Problem Statement

For this case study, you will need to access Eastman Kodak’s From 10-K for the years

ending December 31, 2010 and December 31, 2006 along with the proxy statements for

these two years. Your case study response should be written in complete sentences, and

it should include a link or a copy of the relevant material from these source documents.

Hint: For SEC filings, it may be best to either use the link or copy the relevant items and

paste into a Word document. Printing SEC filings is tricky since the document page

number will not correspond to the print page number.

1. Describe how Eastman Kodak Company’s Board performs its risk oversight

responsibilities. State and explain whether or not you feel the Board’s risk

oversight is adequate.

2. In light of its bankruptcy filing, compare and contrast the risk factor disclosures in

the 10-K filings.

3. Are there any risk factor disclosures in the 10-K filing that surprised you? List

them and explain why you were surprised.

4. List any risk factor disclosures in the 10-K filing that appear to be somewhat

generic (i.e. are these standard industry risks or may they apply to other

industries).

5. Explain whether or not you feel that the market risks outlined in Item 7A were

significant.

6. Are there any Sarbanes-Oxley disclosures that may indicate significant risks?

7. Review and comment on the Board qualifications as noted in the most recent

proxy. Is there adequate risk management experience?

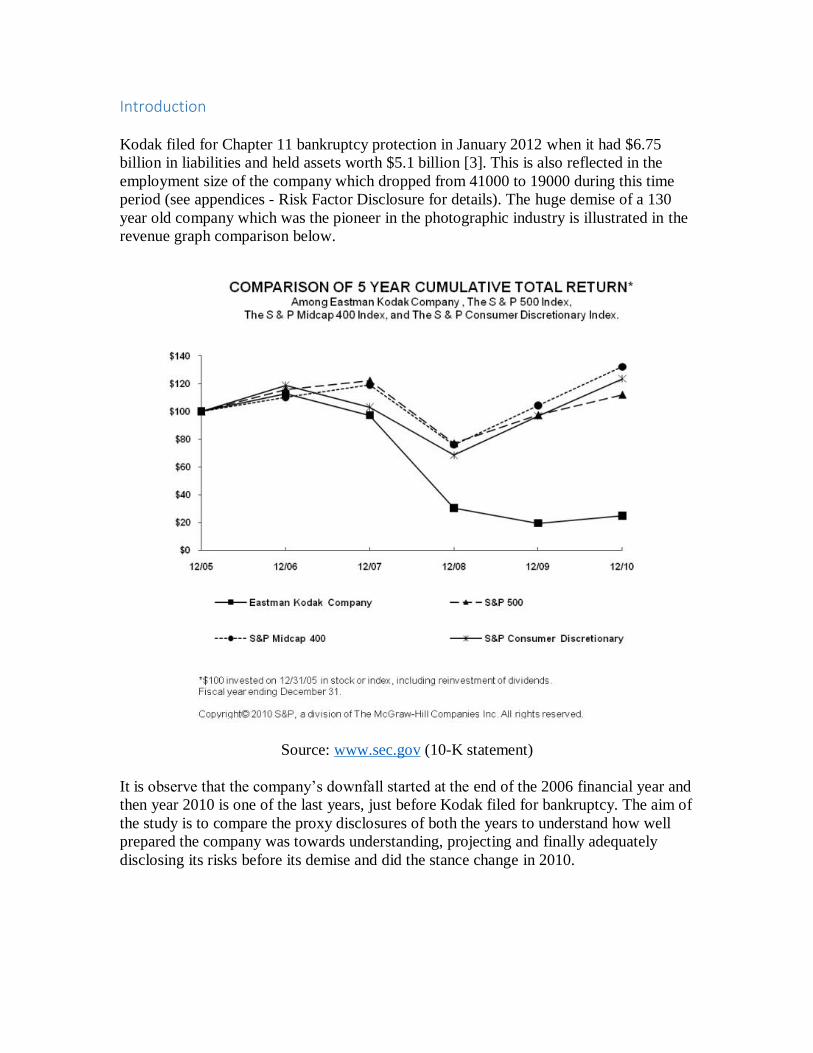

Introduction

Kodak filed for Chapter 11 bankruptcy protection in January 2012 when it had $6.75

billion in liabilities and held assets worth $5.1 billion [3]. This is also reflected in the

employment size of the company which dropped from 41000 to 19000 during this time

period (see appendices - Risk Factor Disclosure for details). The huge demise of a 130

year old company which was the pioneer in the photographic industry is illustrated in the

revenue graph comparison below.

Source: www.sec.gov (10-K statement)

It is observe that the company’s downfall started at the end of the 2006 financial year and

then year 2010 is one of the last years, just before Kodak filed for bankruptcy. The aim of

the study is to compare the proxy disclosures of both the years to understand how well

prepared the company was towards understanding, projecting and finally adequately

disclosing its risks before its demise and did the stance change in 2010.

A Look into the Board and its Oversight In 2006 the board oversaw risk through finance committee with focus on risk

management programs and insurance risks. In contrast, a sense of urgency starts to creep

in, evident from the tone of the report which when read gives a feeling of seeking out to

eliminate all possible risks. A whole new section on risk management is seen in 2010

which was quite absent in 2006. Perhaps this is because the board is trying to steer the

company out of its looming bankruptcy fears. An instance points out the employee

conflict of interest arising from a VP being the spouse of a SVP (read Appendix B-

Interesting Note for details).

1. The initiative the board aggressively shifts focus to address the issue of executive

compensation focus in 2010 i.e. to award fixed salary so as to inhibit employees

taking excessive risks to gain compensation benefits. In line with the above

policy, another method to mitigate agency problem [4] was launched i.e. to give

share ownership to executives to promote management decision incentivizing

shareholders interest.

An excerpt reads:

“The Committee also considered the volatility associated with the timing of new

intellectual property arrangements when setting this threshold in order to remove

a potential risk of incenting arrangements that may not be in the best long-term

interest of shareholders.”

And at another place

“A significant portion of each executive’s compensation should be at risk, with a

positive correlation between the degree of risk and the level of the executive’s

responsibility.”

2. An interesting observation that arises out of the comparison is that suddenly the

profiles of the existing board members e.g. Richard S. Braddock now reflect

experience in risk management and evidently no mention of the same could be

found in the 2006 profile. This observation certainly raises doubt into the

credibility of the profiles listed and can be carried forward to the profiles of the

new board members who joined after 2009; and all of them seem to have risk

management expertise. Hence a need arises to explicitly state the risk experience

of all these people?

3. Audit committee is now reporting to the board on ERM profile of the company

which was previously only reporting on executive compensation.

4. Commodity price risks were added in 2010 to the role of financial committee

which had been mainly responsible for overseeing risk in the past as well.

5. Even though the board is now strongly overseeing executive compensation and

the company has been exercising strong cost cutting strategies we see no decrease

in pay of the chief executive, Perez fixed salary remains over a million dollar

unchanged.

Risk Factor Disclosure Some of the main risks important to the company (the top 2 being critical) have been

identified and ranked in the order of importance from its proxy disclosures.

1. Unable to transform and adjust to digital transformation of the company and

changing customer preferences (2006).

This is re-emphasized in 2010:

If we are unsuccessful with our strategic investment decisions, our financial

performance could be adversely affected.

Comment: the fundamental reason of Kodak’s demise. It continued to focus on

reinventing its secondary line of business of ink jet printers while constantly

stressing the risk it faced if it didn’t readjust its core line of imaging business to

the needs of the digital customers. This is an unfortunate event in which the

management could not shift its attention to the risk. It seemed Kodak considered

the risk to be far off and ignored the velocity with which it was about to impact it.

2. Unable to exercised patents and licensing regulations to curtail competition

(2006). This is reemphasized in 2010 as well but more seriously now.

Comment: It is found out later that when filing bankruptcy and in the post 2010

era, Kodak is helpless tries to enforce its patent infringements and tries to

leverage them by selling them [5] but unfortunately its too late and gets meager

bargains out of them.

3. Failure to meet credit agreements (2006)

Comment: An important risk is again adequately disclosed. The first thing leading

to bankruptcy is the inability to pay off debt. The risk was exposed during post

2010 period.

4. Third party risk and putting heavy reliance on it (2006) (2010)

Comment: This risk was correctly recognized but it did not greatly affect the

demise

5. Our future pension and other postretirement plan cost contributions could

be unfavorably impacted by changes in actuarial assumptions (2010)

Comment: Actuaries and their valuations is an important part of financial

statement. From a SOX (see appendix-C) perspective this is a big deviation and

should have been found in SOX discrepancies as they closely pertain to material

weaknesses in financial statements.

6. If we are unable to provide competitive financing arrangements to our

customers or if we extend credit to customers whose creditworthiness

deteriorates, this could adversely impact our revenues, profitability and

financial position. (2010)

Comment: credit risk is now a threat which was not seen a threat in 2006.

7. We may be required to recognize additional impairments in the value of our

goodwill and/or other long-lived assets, which would increase expenses and

reduce profitability (2010)

Comment: As the company has now treaded on the downhill path, good will and

other intangibles now seem over-valued. Reputation risks are being correctly

recognized here because the same, in post 2010 period significantly decreases the

market value of a lot of tangible and intangible assets of the company.

Sarbanes Oxley law (SOX) in short requires [1] that (a) company must maintain adequate

controls over financial reporting (b) the company must provide a statement about the

method the company uses for evaluating their control over financial reporting controls (c)

the company must disclose any material weaknesses in their accounting controls (d) the

company's auditor issue an attestation regarding the managements own assessment of its

financial reporting capabilities.

Reviewing the above analysis on SOX and the explicit notion of SOX not doing a good

job at handling legal and reputational risk [2], it can be said that the proxy disclosure

does a fairly good job by stating the reputational risks correctly in 2010 on its own. Not

much financial or reporting discrepancy and risks have been mentioned (other than point

no 5 above).

Market risk analysis In 2006 company mentions hedging through future contracts to mitigate foreign currency

exchange risk due to its global operations. Also tries to lower risk of interest rates through

studies and sensitivity analysis. Credit risk is written to be managed well through strict

procedures and the company doesn’t see it as a big threat. In 2010 when borrowings have

increased and interest rate impact on the company has increased. Also commodity price

hedging techniques and their risks are now explicitly stated e.g. with silver.

Credit risk is again undermined in 2010 and not given much importance whereas it is

mentioned to be a big risk in the proxy disclosure of 2010. The item 7A and 1A sections

do not quite resonate with the same frequency in 2010.

Irrelevant statements found in the proxy disclosure. We see more non-trivial statements in 2006 when the company was doing good. It did not

have to make up many in 2010

2006- Delays in our plans to improve manufacturing productivity and control cost of

operations could negatively impact our gross margins.

Comment: this is common sense.

2006- If we cannot protect our reputation due to product quality and liability issues, our

business could be harmed.

Comment: Of course bad product and qualities will affect reputation.

2010- If we fail to manage distribution of our products and services properly, our

revenue, gross margins and earnings could be adversely impacted.

Comment: this is common sense. 2006- The competitive pressures we face could harm our revenue, gross margins and

market share.

Comment: this is common sense. Cookie cutter statement.

2010- Continued weakness or worsening of economic conditions could continue to

adversely affect our financial performance and our liquidity.

Comment: General industry statement not pertinent.

2006- Economic uncertainty in developing markets could adversely affect our revenue and

earnings.

Comment: developing markets are categorized under developing and underdeveloped for

the same reason. This is like trying to redefine what developing markets are.

From the analysis above, it is gathered that the top critical risks that led to the downfall of

Kodak Eastman were correctly and timely recognized and disclosed in the proxy

disclosure statement. It was the disability of the management and the board to focus and

adhere to those risks that led to the demise of the company. Hence it is very important

from an ERM perspective to not get dwelled into a lot of information and to keep the top

risks with highest impact and likelihood in constant monitoring and focus.

In my point of view the format of the proxy disclosure statement should be changed

immediately to rank the risks in order of importance so that a lesson is learnt from this

study and importance can be given to the lethal risks.

“We are drowning in data but starving for information” – paraphrase of John Naisbitt

[1] An Excerpt on SOX

http://www.llx.com/SOX/

[2] Enterprise Risk Management: Today’s Leading Research and Best Practices for

Tomorrow’s Executives by John Fraser and Betty J. Simkins, 2010

[3] Kodak emerges from bankruptcy

http://news.cnet.com/8301-1001_3-57601221-92/kodak-emerges-from-bankruptcy-with-

new-focus/

[4] “Agency Problem” see Fundamentals of Corporate Finance by Ross, Westerfield &

Jordan. McGraw-Hill

[5] Kodak to Sell its Patents

http://www.nytimes.com/2012/12/20/business/kodak-to-sell-patents-for-525-million.html

Boards Oversight - Def 14A Details on:

http://www.sec.gov/Archives/edgar/data/31235/000120677411000659/kodak_def14a.htm

Risk Management Our Board oversees an enterprise-wide approach to risk management, designed to support the achievement of the Company's objectives, including strategic objectives, to improve long-term performance and enhance shareholder value. A fundamental part of risk management is not only identifying and prioritizing the risks the Company faces and monitoring the steps management is taking to manage those risks, but also determining the level of risk that is appropriate for the Company. As an integral part of its review and approval of the Company’s strategic plan, the Board considers the appropriate level of risk for the Company to accept. The full Board also participates in an annual enterprise risk assessment which is led by the Company's Chief Compliance Officer. Through this process, risk is assessed throughout the Company, focusing on four primary categories of risk: strategic, operational, legal/compliance and financial reporting. In 2010, the Board received a report on the results of the Company's enterprise risk assessment. The Board also receives regular reports on management’s progress in mitigating key risks. While the Board has assumed oversight responsibility for the Company's enterprise risk management process, the Board has delegated to its Committees responsibility for the oversight of the Company’s risk management in specific risk areas. For example:

The Audit Committee oversees the Company’s financial reporting (including internal controls) and compliance risk management.

The Executive Compensation and Development Committee oversees risk management relating to the Company's compensation programs and awards.

The Finance Committee oversees risk management relating to the Company’s capital structure and insurance program.

The Governance Committee oversees the Company’s health, safety and environmental risk management program.

In 2010, the Compensation Committee reviewed a report from management on an assessment of risks relating to the Company’s compensation programs and awards. The assessment concluded, and the Compensation Committee agreed, that such programs and awards do not present any material adverse risks to the Company.

Compensation

A.M. Perez 2010 $1,096,168 — $1,701,290 $0 $341,000 $2,259,538 $320,194 $5,718,190

Interesting Note The Governance Committee reviewed one interested transaction with a related party occurring in 2010 that did not fall within any of the pre-approved interested transactions described above, as follows:

Dolores Kruchten, a Vice President of the Company, is the spouse of Brad Kruchten, a Senior Vice President and Section 16 Officer of the Company. There is no employment reporting relationship between Mr. Kruchten and Ms. Kruchten. Ms. Kruchten earned the following compensation in 2010: $277,127, consisting of base salary and non-equity variable pay.

Risk Factor Disclosure

Proxy Statement - 10-k http://www.sec.gov/Archives/edgar/data/31235/000003123511000025/ek2010_10k.htm

ITEM 1A. RISK FACTORS The competitive pressures we face could harm our revenue, gross margins and market share. The markets in which we do business are highly competitive with large, entrenched, and well financed

industry participants. In certain markets where Kodak is a relatively new entrant, we have not achieved the

scale of distribution that our competitors have. In addition, we encounter aggressive price competition for

all our products and services from numerous companies globally. Over the past several years, price competition in the market for digital products, film products and services has been particularly intense as

competitors have aggressively cut prices and lowered their profit margins for these products. Our results of

operations and financial condition may be adversely affected by these and other industry wide pricing

pressures. If our products, services and pricing are not sufficiently competitive with current and future

competitors, we could also lose market share, adversely affecting our revenue and gross margins.

9

If our commercialization and manufacturing processes fail to prevent product reliability and quality

issues, our product launch plans may be delayed, our financial results may be adversely impacted,

and our reputation may be harmed. In developing, commercializing and manufacturing our products and services, we must adequately address

reliability and other quality issues, including defects in our engineering, design and manufacturing

processes, as well as defects in third-party components included in our products. Because our products are

becoming increasingly sophisticated and complicated to develop and commercialize with rapid advances in

technologies, the occurrence of defects may increase, particularly with the introduction of new product

lines. Unanticipated issues with product performance may delay product launch plans which could result in

additional expenses, lost revenue and earnings. Although we have established internal procedures to

minimize risks that may arise from product quality issues, there can be no assurance that we will be able to

eliminate or mitigate occurrences of these issues and associated liabilities. Product reliability and quality

issues can impair our relationships with new or existing customers and adversely affect our brand image, and our reputation as a producer of high quality products could suffer, which could adversely affect our

business as well as our financial results. Product quality issues can also result in recalls, warranty, or other

service obligations and litigation. If we are unsuccessful with our strategic investment decisions, our financial performance could be

adversely affected. We have made a decision to focus our investments on businesses in large growth markets that are positioned for technology and business model transformation, specifically, consumer inkjet, commercial

inkjet (including our Prosper line of products based upon the Company’s Stream technology), packaging

solutions, and workflow software and services. We believe each of these businesses has significant growth

potential. The introduction of successful innovative products and the achievement of scale are necessary

for us to grow these businesses, improve margins and achieve our financial objectives. If we are

unsuccessful in growing our investment businesses as planned, our financial performance could be

adversely affected. If we cannot effectively anticipate technology trends and develop and market new products to

respond to changing customer preferences, our revenue, earnings and cash flow, could be adversely

affected. We must develop and introduce new products and services in a timely manner to keep pace with

technological developments and achieve customer acceptance. If we are unable to anticipate new

technology trends, for example in consumer electronics, and develop improvements to our current

technology to address changing customer preferences, this could adversely affect our revenue, earnings and cash flow. Due to changes in technology and customer preferences, the market for traditional film and

paper products and services is in decline. Our success depends in part on our ability to manage the decline

of the market for these traditional products by continuing to reduce our cost structure to maintain

profitability. Continued weakness or worsening of economic conditions could continue to adversely affect our

financial performance and our liquidity. The global economic recession and declines in consumption in our end markets have adversely affected

sales of both commercial and consumer products and profitability for such products. Further, global

financial markets have been experiencing volatility. Consumer discretionary spending may not return to

pre-recession levels in certain geographies. Continued slower sales of consumer digital products due to the

uncertain economic environment could lead to reduced sales and earnings while inventory

increases. Economic conditions could also accelerate the continuing decline in demand for traditional

products, which could also place pressure on our results of operations and liquidity. While the company is

seeking to increase sales in markets that have already experienced an economic recovery such as Asia,

there is no guarantee that anticipated economic growth levels in those markets will continue in the future,

or that the company will succeed in expanding sales in these markets. In addition, accounts receivable and

past due accounts could increase due to a decline in our customers’ ability to pay as a result of the economic downturn, and our liquidity, including our ability to use credit lines, could be negatively

impacted by failures of financial instrument counterparties, including banks and other financial

institutions. If the global economic weakness and tightness in the credit markets continue for a greater

period of time than anticipated or worsen, our profitability and related cash generation capability could be

adversely affected and, therefore, affect our ability to meet our anticipated cash needs, impair our liquidity

or increase our costs of borrowing.

10

If we cannot attract, retain and motivate key employees, our revenue and earnings could be harmed. In order for us to be successful, we must continue to attract, retain and motivate executives and other key

employees, including technical, managerial, marketing, sales, research and support positions. Hiring and

retaining qualified executives, research and engineering professionals, and qualified sales representatives,

particularly in our targeted growth markets, is critical to our future. The market for experienced

employees with digital skills is highly competitive and, therefore, our ability to attract such talent will

depend on a number of factors, including compensation and benefits, work location and persuading

potential employees that we are well positioned for success in the digital markets in which we are

operating. Given that our compensation plans are highly performance based and given the potential impact

of the global economy on our current and future performance, it may become more challenging to retain

key employees. We also must keep employees focused on our strategic initiatives and goals in order to be

successful. Our past restructuring actions harm our efforts to attract and retain key employees. If we

cannot attract properly qualified individuals, retain key executives and employees or motivate our

employees, our business could be harmed. Our future pension and other postretirement plan costs and required level of contributions could be

unfavorably impacted by changes in actuarial assumptions, future market performance of plan

assets and obligations imposed by legislation or pension authorities which could adversely affect our

financial position, results of operations, and cash flow. We have significant defined benefit pension and other postretirement benefit obligations. The funded

status of our U.S. and non U.S. defined benefit pension plans and other postretirement benefit plans, and

the related cost reflected in our financial statements, are affected by various factors that are subject to an

inherent degree of uncertainty, particularly in the current economic environment. Key assumptions used to

value these benefit obligations, funded status and expense recognition include the discount rate for future payment obligations, the long term expected rate of return on plan assets, salary growth, healthcare cost

trend rates, and other economic and demographic factors. Significant differences in actual experience, or

significant changes in future assumptions or obligations imposed by legislation or pension authorities could

lead to a potential future need to contribute cash or assets to our plans in excess of currently estimated

contributions and benefit payments and could have an adverse effect on our consolidated results of

operations, financial position or liquidity. If we cannot continue to license or enforce the intellectual property rights on which our business

depends, or if third parties assert that we violate their intellectual property rights, our revenue,

earnings, expenses and liquidity may be adversely impacted. We rely upon patent, copyright, trademark and trade secret laws in the United States and similar laws in

other countries, and non-disclosure, confidentiality and other types of agreements with our employees,

customers, suppliers and other parties, to establish, maintain and enforce our intellectual property

rights. Despite these measures, any of our direct or indirect intellectual property rights could, however, be

challenged, invalidated, circumvented, infringed or misappropriated, or such intellectual property rights

may not be sufficient to permit us to take advantage of current market trends or otherwise to provide

competitive advantages, which could result in costly product redesign efforts, discontinuance of certain

product offerings or other competitive harm. Further, the laws of certain countries do not protect proprietary rights to the same extent as the laws of the United States. Therefore, in certain jurisdictions, we

may be unable to protect our proprietary technology adequately against unauthorized third party copying,

infringement or use, which could adversely affect our competitive position. Also, because of the rapid pace

of technological change in the information technology industry, much of our business and many of our

products rely on key technologies developed or licensed by third parties, and we may not be able to obtain

or continue to obtain licenses and technologies from these third parties at all or on reasonable terms. We have made substantial investments in new, proprietary technologies and have filed patent applications

and obtained patents to protect our intellectual property rights in these technologies as well as the interests

of our licensees. There can be no assurance that our patent applications will be approved, that any patents

issued will adequately protect our intellectual property or that such patents will not be challenged by third

parties. The execution and enforcement of licensing agreements protects our intellectual property rights and

provides a revenue stream in the form of up-front payments and royalties that enables us to further innovate

and provide the marketplace with new products and services. Our ability to execute our intellectual

property licensing strategies, including litigation strategies, such as our legal actions against Apple Inc. and

Research in Motion Limited, could also affect our revenue and earnings. Additionally, the uncertainty

around the timing, outcome and

11

magnitude of our intellectual property-related litigation (including our legal action against Apple Inc. and

Research in Motion Limited before the International Trade Commission), judgments and settlements could

have an adverse effect on our financial results and liquidity. Our failure to develop and properly manage

new intellectual property could adversely affect our market positions and business

opportunities. Furthermore, our failure to identify and implement licensing programs, including identifying

appropriate licensees, could adversely affect the profitability of our operations. In addition, third parties may claim that we, our customers, licensees or other parties indemnified by us are

infringing upon their intellectual property rights. Such claims may be made by competitors seeking to

block or limit our access to digital markets. Additionally, in recent years, individuals and groups have

begun purchasing intellectual property assets for the sole purpose of making claims of infringement and

attempting to extract settlements from large companies like ours. Even if we believe that the claims are

without merit, the claims can be time consuming and costly to defend and distract management’s attention

and resources. Claims of intellectual property infringement also might require us to redesign affected

products, enter into costly settlement or license agreements or pay costly damage awards, or face a

temporary or permanent injunction prohibiting us from marketing or selling certain of our products. Even

if we have an agreement to indemnify us against such costs, the indemnifying party may be unable to

uphold its contractual obligations. If we cannot or do not license the infringed technology at all, license the

technology on reasonable terms or substitute similar technology from another source, our revenue and earnings could be adversely impacted. Finally, we use open source software in connection with our

products and services. Companies that incorporate open source software into their products have, from

time to time, faced claims challenging the ownership of open source software and/or compliance with open

source license terms. As a result, we could be subject to suits by parties claiming ownership of what we

believe to be open source software or noncompliance with open source licensing terms. Some open source

software licenses require users who distribute open source software as part of their software to publicly

disclose all or part of the source code to such software and/or make available any derivative works of the

open source code on unfavorable terms or at no cost. Any requirement to disclose our source code or pay

damages for breach of contract could be harmful to our business results of operations and financial

condition. Due to the nature of the products we sell and our worldwide distribution, we are subject to changes

in currency exchange rates, interest rates and commodity costs that may adversely impact our results

of operations and financial position. As a result of our global operating and financing activities, we are exposed to changes in currency

exchange rates and interest rates, which may adversely affect our results of operations and financial

position. Exchange rates and interest rates in markets in which we do business tend to be volatile and at

times, our sales can be negatively impacted across all of our segments depending upon the value of the U.S. dollar, the Euro and other major currencies. In addition, our products contain silver, aluminum, petroleum

based or other commodity-based raw materials, the prices of which have been and may continue to be

volatile. If the global economic situation remains uncertain or worsens, there could be further volatility in

changes in currency exchange rates, interest rates and commodity prices, which could have negative effects

on our revenue and earnings. If we are unable to provide competitive financing arrangements to our customers or if we extend

credit to customers whose creditworthiness deteriorates, this could adversely impact our revenues,

profitability and financial position. The competitive environment in which we operate may require us to provide financing to our customers in

order to win a contract. Customer financing arrangements may include all or a portion of the purchase

price for our products and services. We may also assist customers in obtaining financing from banks and

other sources and may provide financial guarantees on behalf of our customers. Our success may be

dependent, in part, upon our ability to provide customer financing on competitive terms and on our

customers’ creditworthiness. The tightening of credit in the global financial markets has adversely affected

the ability of our customers to obtain financing for significant purchases, which resulted in a decrease in, or

cancellation of, orders for our products and services, and we can provide no assurance that this trend will

not continue. If we are unable to provide competitive financing arrangements to our customers or if we

extend credit to customers whose creditworthiness deteriorates, this could adversely impact our revenues,

profitability and financial position.

12

Our sales are typically concentrated in the last four months of the fiscal year, therefore, lower than

expected demand or increases in costs during that period may have a pronounced negative effect on

our results of operations. The demand for our consumer products is largely discretionary in nature, and sales and earnings of our

consumer businesses are linked to the timing of holidays, vacations, and other leisure or gifting

seasons. Accordingly, we have typically experienced greater net sales in the fourth fiscal quarter as

compared to the other three quarters. Developments, such as lower-than-anticipated demand for our

products, an internal systems failure, increases in materials costs, or failure of or performance problems

with one of our key logistics, components supply, or manufacturing partners, could have a material adverse

impact on our financial condition and operating results, particularly if such developments occur late in the third quarter or during the fourth fiscal quarter. Further, with respect to the Graphic Communications

Group segment, equipment and consumable sales in the commercial marketplace peak in the fourth quarter

based on increased commercial print demand. Tight credit markets that limit capital investments or a weak

economy that decreases print demand could negatively impact equipment or consumable sales. In addition,

our inability to achieve intellectual property licensing revenues in the timeframe and amount we anticipate

could adversely affect our revenues, earnings and cash flow. These external developments are often

unpredictable and may have an adverse impact on our business and results of operations. If we fail to manage distribution of our products and services properly, our revenue, gross margins

and earnings could be adversely impacted. We use a variety of different distribution methods to sell and deliver our products and services, including

third party resellers and distributors and direct and indirect sales to both enterprise accounts and

customers. Successfully managing the interaction of direct and indirect channels to various potential

customer segments for our products and services is a complex process. Moreover, since each distribution

method has distinct risks and costs, our failure to implement the most advantageous balance in the delivery

model for our products and services could adversely affect our revenue, gross margins and earnings. Due

to changes in our go to market models, we are more reliant on fewer distributors than in past periods. This

has concentrated our credit and operational risk and could result in an adverse impact on our financial performance. We have outsourced a significant portion of our overall worldwide manufacturing, logistics and back

office operations and face the risks associated with reliance on third party suppliers. We have outsourced a significant portion of our overall worldwide manufacturing, logistics, customer

support and administrative operations to third parties. To the extent that we rely on third party service providers, we face the risk that those third parties may not be able to: develop manufacturing methods appropriate for our products;

maintain an adequate control environment;

quickly respond to changes in customer demand for our products;

obtain supplies and materials necessary for the manufacturing process; or

mitigate the impact of labor shortages and/or disruptions.

As a result of such risks, our costs could be higher than planned and the reliability of our products could be

negatively impacted. Other supplier problems that we could face include electronic component shortages,

excess supply, risks related to duration of our contracts with suppliers for components and materials and

risks related to dependency on single source suppliers on favorable terms or at all. If any of these risks

were to be realized, and assuming alternative third party relationships could not be established, we could

experience interruptions in supply or increases in costs that might result in our inability to meet customer

demand for our products, damage to our relationships with our customers, and reduced market share, all of

which could adversely affect our results of operations and financial condition. We may be required to recognize additional impairments in the value of our goodwill and/or other

long-lived assets, which would increase expenses and reduce profitability. Goodwill represents the excess of the amount we paid to acquire businesses over the fair value of their net

assets at the date of the acquisition. We test goodwill for impairment annually or whenever events occur or

circumstances change that would more likely than not reduce the fair value of a reporting unit below its

carrying amount. Additionally, our other long-lived assets are evaluated for impairments whenever events or changes in circumstances indicate the carrying value may not be recoverable. Either of these situations

may occur for

13

various reasons including changes in actual or expected income or cash. We continue to evaluate current

conditions to assess whether any impairment exists. Impairments could occur in the future if market or

interest rate environments deteriorate, expected future cash flows of our reporting units decline, silver

prices increase significantly, or if reporting unit carrying values change materially compared with changes

in respective fair values. Our failure to implement plans to reduce our cost structure in anticipation of declining demand for

certain products or delays in implementing such plans could negatively affect our consolidated

results of operations, financial position and liquidity. We recognize the need to continually rationalize our workforce and streamline our operations to remain

competitive in the face of an ever-changing business and economic climate. If we fail to implement cost

rationalization plans such as restructuring of manufacturing, supply chain, marketing sales and

administrative resources ahead of declining demand for certain of our products and services, our operations

results, financial position and liquidity could be negatively impacted. Additionally, if restructuring plans

are not effectively managed, we may experience lost customer sales, product delays and other unanticipated

effects, causing harm to our business and customer relationships. Finally, the timing and implementation

of these plans require compliance with numerous laws and regulations, including local labor laws, and the failure to comply with such requirements may result in damages, fines and penalties which could adversely

affect our business. Our future results could be harmed if we are unsuccessful in our efforts to expand sales in emerging

markets. Because we are seeking to expand our sales and number of customer relationships outside the United States, and specifically in emerging markets in Asia, Latin America and Eastern Europe, our business is

subject to risks associated with doing business internationally, such as: supporting multiple languages;

recruiting sales and technical support personnel with the skills to design, manufacture, sell and support

our products;

complying with governmental regulation of imports and exports, including obtaining required import

or export approval for our products;

complexity of managing international operations;

exposure to foreign currency exchange rate fluctuations;

commercial laws and business practices that may favor local competition;

multiple, potentially conflicting, and changing governmental laws, regulations and practices, including

differing export, import, tax, anti-corruption, labor, and employment laws;

difficulties in collecting accounts receivable;

limitations or restrictions on the repatriation of cash;

reduced or limited protection of intellectual property rights;

managing research and development teams in geographically disparate locations, including Canada,

Israel, Japan, China, and Singapore;

complicated logistics and distribution arrangements; and

political or economic instability.

There can be no assurance that we will be able to market and sell our products in all of our targeted

international markets. If our international efforts are not successful, our business growth and results of

operations could be harmed. We are subject to environmental laws and regulations and failure to comply with such laws and

regulations or liabilities imposed as a result of such laws and regulations could have an adverse effect

on our business, results of operations and financial condition. We are subject to environmental laws and regulations in the jurisdictions in which we conduct our business,

including laws regarding the discharge of pollutants, including greenhouse gases, into the air and water, the

need for environmental permits for certain operations, the management and disposal of hazardous

substances and wastes, the cleanup of contaminated sites, the content of our products and the recycling and

treatment and disposal of our products. If we do not comply with applicable laws and regulations in

connection with the use and management of hazardous substances, then we could be subject to liability

and/or could be prohibited from operating certain facilities, which could have a material adverse effect on

our business, results of operations and financial condition.

14

Our inability to effectively complete, integrate and manage acquisitions, divestitures and other

significant transactions could adversely impact our business performance including our financial

results. As part of our business strategy, we frequently engage in discussions with third parties regarding possible

investments, acquisitions, strategic alliances, joint ventures, divestitures and outsourcing transactions and

enter into agreements relating to such transactions in order to further our business objectives. In order to

pursue this strategy successfully, we must identify suitable candidates and successfully complete

transactions, some of which may be large and complex, and manage post closing issues such as the

integration of acquired companies or employees and the assessment of such acquired companies’ internal

controls. Integration and other risks of transactions can be more pronounced for larger and more

complicated transactions, or if multiple transactions are pursued simultaneously. If we fail to identify and

complete successfully transactions that further our strategic objectives, we may be required to expend

resources to develop products and technology internally, we may be at a competitive disadvantage or we

may be adversely affected by negative market perceptions, any of which may have an adverse effect on our revenue, gross margins and profitability. In addition, unpredictability surrounding the timing of such

transactions could adversely affect our financial results. Our substantial leverage could adversely affect our ability to fulfill our debt obligations and may

place us at a competitive disadvantage in our industry. Our significant debt and debt service requirements could adversely affect our ability to operate our business

and may limit our ability to take advantage of potential business opportunities. A breach of any of the covenants contained in our Credit Agreement or our other financing arrangements, or our inability to

comply with the required financial ratio in our Credit Agreement, when applicable, could result in an event

of default under the Credit Agreement or our other financing arrangements, subject to applicable grace and

cure periods. If any event of default occurs and we are not able either to cure it or obtain a waiver from the

requisite lenders under the Credit Agreement and noteholders under our other financing arrangements, the

administrative agent of the Credit Agreement may, and at the request of the requisite lenders shall, and the

trustee or the requisite noteholders under our other financing arrangements may, and at the request of the

requisite noteholders shall, declare all of our outstanding obligations under the Credit Agreement and our

other financing arrangements, respectively, together with accrued interest and fees, to be immediately due and payable, and the agent under the Credit Agreement may, and at the request of the requisite lenders

shall, terminate the lenders' commitments under the Credit Agreement and cease making further loans, and

if applicable, the agent and/or trustee could institute foreclosure proceedings against our pledged assets. Continued investment, capital needs, restructuring payments and servicing our debt require a

significant amount of cash and our ability to generate cash may be affected by factors beyond our

control. Our business may not generate cash flow in an amount sufficient to enable us to pay the principal of, or

interest on, our indebtedness, or to fund our other liquidity needs, including working capital, capital

expenditures, product development efforts, strategic acquisitions, investments and alliances, and other

general corporate requirements. Our ability to generate cash is subject to general economic, financial, competitive, litigation, regulatory and

other factors that are beyond our control. We cannot assure you that: our businesses will generate sufficient cash flow from operations;

our plans to generate cash proceeds through the sale of non-core assets will be successful;

we will be able to repatriate or move cash to locations where and when it is needed;

we will realize cost savings, revenue growth and operating improvements resulting from the execution

of our long-term strategic plan; or

future sources of funding will be available to us in amounts sufficient to enable us to fund our liquidity

needs.

If we cannot fund our liquidity needs, we will have to take actions such as raising additional capital;

reducing or delaying capital expenditures, product development efforts, strategic acquisitions, and

investments and alliances; selling assets; restructuring or refinancing our debt; or seeking additional equity

capital. Such actions could further negatively impact our ability to generate cash flows. We cannot assure

you that any of these remedies could, if necessary, be effected on commercially reasonable terms, or at all,

or that they would permit us to meet our scheduled debt service obligations. Certain of our debt

instruments limit the use of the proceeds from any disposition of assets and, as a result, we may not be

allowed, under those instruments, to use the proceeds from such dispositions to satisfy all current debt service obligations. In addition, if we incur additional debt, the risks associated with our substantial

leverage, including the risk that we will be unable to service our debt or generate enough cash flow to fund

our liquidity needs, could intensify.

Market Risk ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK The Company, as a result of its global operating and financing activities, is exposed to changes in foreign currency exchange rates, commodity prices, and interest rates, which may adversely affect its results of

operations and financial position. In seeking to minimize the risks associated with such activities, the

Company may enter into derivative contracts. The Company does not utilize financial instruments for

trading or other speculative purposes. Foreign currency forward contracts are used to hedge existing foreign currency denominated assets and liabilities, especially those of the Company’s International Treasury Center, as well as forecasted foreign

currency denominated intercompany sales. Silver forward contracts are used to mitigate the Company’s

risk to fluctuating silver prices.

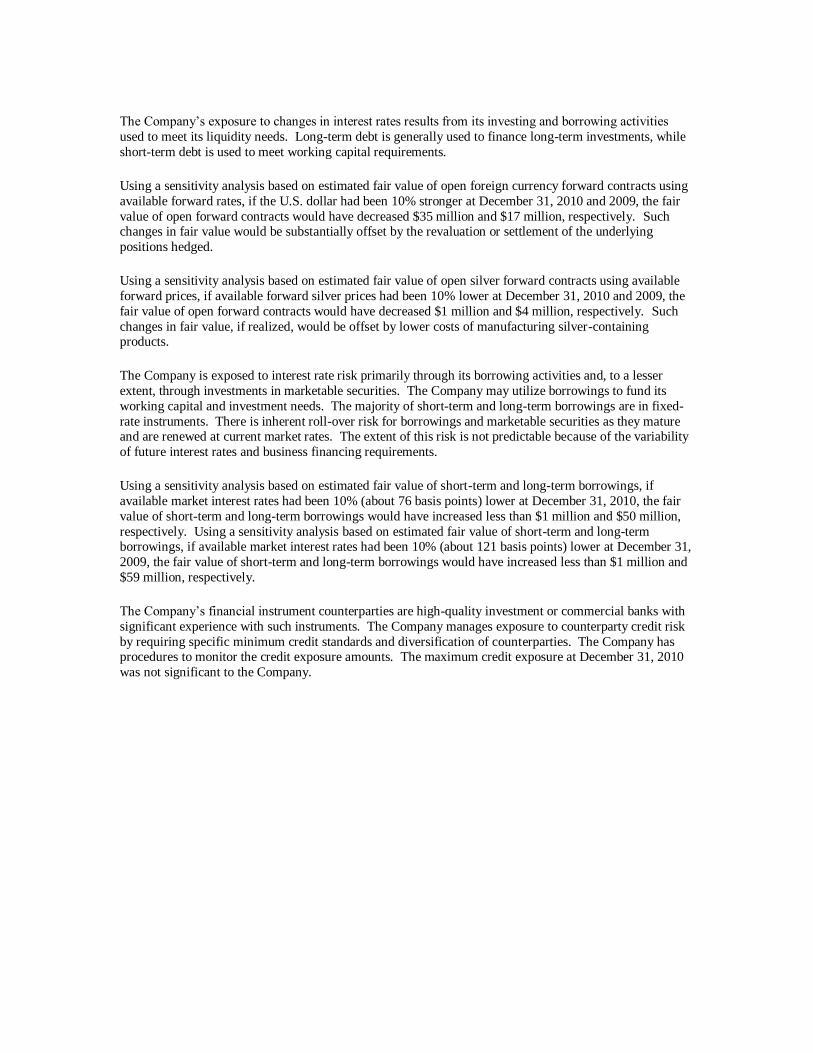

The Company’s exposure to changes in interest rates results from its investing and borrowing activities

used to meet its liquidity needs. Long-term debt is generally used to finance long-term investments, while

short-term debt is used to meet working capital requirements. Using a sensitivity analysis based on estimated fair value of open foreign currency forward contracts using

available forward rates, if the U.S. dollar had been 10% stronger at December 31, 2010 and 2009, the fair

value of open forward contracts would have decreased $35 million and $17 million, respectively. Such changes in fair value would be substantially offset by the revaluation or settlement of the underlying

positions hedged. Using a sensitivity analysis based on estimated fair value of open silver forward contracts using available

forward prices, if available forward silver prices had been 10% lower at December 31, 2010 and 2009, the

fair value of open forward contracts would have decreased $1 million and $4 million, respectively. Such

changes in fair value, if realized, would be offset by lower costs of manufacturing silver-containing products. The Company is exposed to interest rate risk primarily through its borrowing activities and, to a lesser

extent, through investments in marketable securities. The Company may utilize borrowings to fund its

working capital and investment needs. The majority of short-term and long-term borrowings are in fixed-

rate instruments. There is inherent roll-over risk for borrowings and marketable securities as they mature and are renewed at current market rates. The extent of this risk is not predictable because of the variability

of future interest rates and business financing requirements. Using a sensitivity analysis based on estimated fair value of short-term and long-term borrowings, if

available market interest rates had been 10% (about 76 basis points) lower at December 31, 2010, the fair

value of short-term and long-term borrowings would have increased less than $1 million and $50 million,

respectively. Using a sensitivity analysis based on estimated fair value of short-term and long-term borrowings, if available market interest rates had been 10% (about 121 basis points) lower at December 31,

2009, the fair value of short-term and long-term borrowings would have increased less than $1 million and

$59 million, respectively. The Company’s financial instrument counterparties are high-quality investment or commercial banks with

significant experience with such instruments. The Company manages exposure to counterparty credit risk

by requiring specific minimum credit standards and diversification of counterparties. The Company has procedures to monitor the credit exposure amounts. The maximum credit exposure at December 31, 2010

was not significant to the Company.

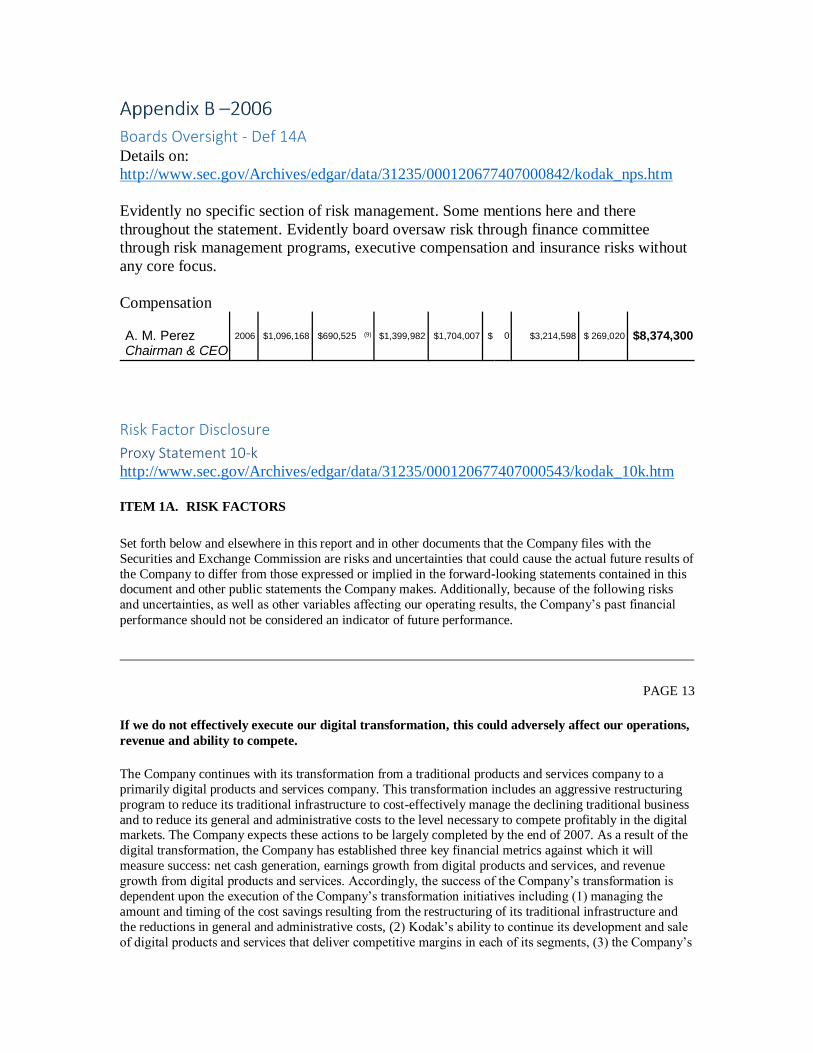

Boards Oversight - Def 14A Details on:

http://www.sec.gov/Archives/edgar/data/31235/000120677407000842/kodak_nps.htm

Evidently no specific section of risk management. Some mentions here and there

throughout the statement. Evidently board oversaw risk through finance committee

through risk management programs, executive compensation and insurance risks without

any core focus.

Compensation A. M. Perez Chairman & CEO

2006 $1,096,168 $690,525 (9) $1,399,982 $1,704,007 $ 0 $3,214,598 $ 269,020 $8,374,300

Risk Factor Disclosure

Proxy Statement 10-k http://www.sec.gov/Archives/edgar/data/31235/000120677407000543/kodak_10k.htm

ITEM 1A. RISK FACTORS

Set forth below and elsewhere in this report and in other documents that the Company files with the

Securities and Exchange Commission are risks and uncertainties that could cause the actual future results of

the Company to differ from those expressed or implied in the forward-looking statements contained in this document and other public statements the Company makes. Additionally, because of the following risks

and uncertainties, as well as other variables affecting our operating results, the Company’s past financial

performance should not be considered an indicator of future performance.

PAGE 13

If we do not effectively execute our digital transformation, this could adversely affect our operations,

revenue and ability to compete.

The Company continues with its transformation from a traditional products and services company to a

primarily digital products and services company. This transformation includes an aggressive restructuring

program to reduce its traditional infrastructure to cost-effectively manage the declining traditional business

and to reduce its general and administrative costs to the level necessary to compete profitably in the digital markets. The Company expects these actions to be largely completed by the end of 2007. As a result of the

digital transformation, the Company has established three key financial metrics against which it will

measure success: net cash generation, earnings growth from digital products and services, and revenue

growth from digital products and services. Accordingly, the success of the Company’s transformation is

dependent upon the execution of the Company’s transformation initiatives including (1) managing the

amount and timing of the cost savings resulting from the restructuring of its traditional infrastructure and

the reductions in general and administrative costs, (2) Kodak’s ability to continue its development and sale

of digital products and services that deliver competitive margins in each of its segments, (3) the Company’s

ability to manage the traditional business for cash generation in a cost-effective manner and (4) the

Company’s ability to continue to successfully integrate its acquisitions, including KPG and Creo. If Kodak

cannot continue to successfully execute its transformation initiatives, the Company’s ability to compete as a

profitable and growing digital company could be negatively affected, which could adversely affect its

results of operations and its ability to generate cash.

If we fail to comply with the covenants contained in our Secured Credit Agreement, including the

two financial covenants, our ability to meet our financial obligations could be severely impaired.

There are affirmative, negative and financial covenants contained in the Company’s Secured Credit

Agreement. These covenants are typical for a secured credit agreement of this nature. The Company’s

failure to comply with these covenants could result in a default under the Secured Credit Agreement. If an

event of default were to occur and is not waived by the lenders, then all outstanding debt, interest and other

payments under the Secured Credit Agreement could become immediately due and payable and any unused

borrowing availability under the revolving credit facility of the Secured Credit Agreement could be

terminated by the lenders. The failure of the Company to repay any accelerated debt under the Secured Credit Agreement could result in acceleration of the majority of the Company’s unsecured outstanding debt

obligations.

If we cannot effectively manage transitions of our products and services, this could adversely affect

our revenues.

The industries in which Kodak competes are rapidly changing and becoming increasingly more complex.

Kodak’s ability to successfully transition its existing products to new offerings requires that the Company

make accurate predictions of the product development schedule as well as volumes, product mix, customer demand, sales channels, and configuration. The process of developing new products and services is

complex and often uncertain due to the frequent introduction of new products by competitors that offer

improved performance and pricing. Kodak may anticipate demand and perceived market acceptance that

differs from the product’s realizable customer demand and revenue stream. Further, in the face of intense

industry competition, any unanticipated delay in implementing certain product strategies (including digital

products, category expansion and digitization) or in the development, production or marketing of a new

product could decrease any advantage Kodak may have to be the first or among the first to market and

could adversely affect Kodak’s revenues. Kodak’s failure to carry out a product rollout in the time frame

anticipated and in the quantities appropriate to customer demand, or at all, could adversely affect future

demand for the Company’s products and services and have an adverse effect on its business. This risk is

exacerbated when a product has a short life cycle or a competitor introduces a new product just before

Kodak’s introduction of a similar product.

Our results are subject to risks related to our significant investment in developing and introducing new

products, such as consumer inkjet printers and CMOS semiconductors. These risk include: difficulties and

delays in the development, production, testing and marketing of products; customer acceptance of products;

resources we must devote to the development of new technology; and the ability to differentiate our

products and compete with other companies in the same markets.

PAGE 14

If we cannot effectively anticipate trends and respond to changing customer preferences, this could

aversely affect our revenues.

Due to changes in technology, the market for traditional photography products and services is in decline

and, as a result, product development has focused on digital capture devices (digital cameras and scanners)

designed to improve the image acquisition or digitalization process, software products designed to enhance

and simplify the digital workflow, output devices (thermal and inkjet printers and commercial printing

systems and solutions) designed to produce high quality documents and images, and media (thermal and

silver halide) optimized for digital workflows. Kodak’s success depends in part on its ability to develop and

introduce new products and services in a timely manner that keep pace with technological developments

and that are accepted in the market. The Company continues to introduce new consumer and commercial

digital product offerings, however, there can be no assurance that the Company will be successful in anticipating and developing new products, product enhancements or new solutions and services to

adequately address changing technologies and customer requirements. In addition, if the Company is

unable to anticipate and develop improvements to its current technology, to adapt its products to changing

customer preferences or requirements or to continue to produce high quality products in a timely and cost-

effective manner in order to compete with products offered by its competitors, this could adversely affect

the revenues of the Company.

If we cannot adequately protect our intellectual property, our business could be harmed.

Kodak has made substantial investments in technologies and has filed patent applications and obtained patents to protect its intellectual property rights as well as the interests of the Company licensees. The

execution and enforcement of licensing agreements protects the Company’s intellectual property rights and

provides a revenue stream in the form of royalties that enables Kodak to further innovate and provide the

marketplace with new products and services. There is no assurance that such measures alone will be

adequate to protect the Company’s intellectual property.

Our revenue and earnings may suffer if we cannot continue to implement our intellectual property

licensing strategies.

The Company’s ability to execute its intellectual property licensing strategies could also affect the

Company’s revenue and earnings. Kodak’s failure to develop and properly manage new intellectual

property could adversely affect market positions and business opportunities. Furthermore, the Company’s

failure to identify and implement licensing programs, including identifying appropriate licensees, could

adversely affect the profitability of Kodak’s operations.

Our revenue, earnings and expenses may suffer if we cannot continue to license or enforce our

intellectual property rights.

Kodak relies upon patent, copyright, trademark and trade secret laws in the United States and similar laws in other countries, and agreements with its employees, customers, suppliers and other parties, to establish,

maintain and enforce its intellectual property rights. Any of the Company’s direct or indirect intellectual

property rights could, however, be challenged, invalidated or circumvented, or such intellectual property

rights may not be sufficient to permit the Company to take advantage of current market trends or otherwise

to provide competitive advantages, which could result in costly product redesign efforts, discontinuance of

certain product offerings or other competitive harm. Further, the laws of certain countries do not protect

proprietary rights to the same extent as the laws of the United States. Therefore, in certain jurisdictions,

Kodak may be unable to protect its proprietary technology adequately against unauthorized third party

copying or use, which could adversely affect its competitive position. Also, because of the rapid pace of

technological change in the information technology industry, much of our business and many of our

products rely on key technologies developed or licensed by third parties, and we may not be able to obtain

or continue to obtain licenses and technologies from these third parties at all or on reasonable terms.

PAGE 15

Our revenue, earnings and expenses may suffer if third parties assert that we violate their

intellectual property rights.

Third parties may claim that the Company or customers indemnified by Kodak are infringing upon their

intellectual property rights. In recent years, individuals and groups have begun purchasing intellectual

property assets for the sole purpose of making claims of infringement and attempting to extract settlements

from large companies like the Company. Even if Kodak believes that the claims are without merit, the

claims can be time-consuming and costly to defend and distract management’s attention and resources.

Claims of intellectual property infringement also might require the Company to redesign affected products, enter into costly settlement or license agreements or pay costly damage awards, or face a temporary or

permanent injunction prohibiting Kodak from marketing or selling certain of its products. Even if the

Company has an agreement to indemnify it against such costs, the indemnifying party may be unable to

uphold its contractual agreement to Kodak. If we cannot or do not license the infringed technology at all or

on reasonable terms or substitute similar technology from another source, our revenue and earnings could

suffer.

If we are not successful in transitioning certain financial processes and administrative functions to a

global shared services model and outsourcing some of the work to third parties, our business

performance, cost savings and cash flow could be adversely impacted.

The Company continues to migrate various administrative and financial processes, such as general

accounting, accounts payable, credit and collections, call centers and human resources processes to a global

shared services model to more effectively manage its costs. Delays in the migration to the global shared

services model and to third party vendors could adversely impact the Company’s ability to meet its cost

reduction goals. Also, if third party vendors do not perform to Kodak’s standards, such as a delay in

collection of customer receipts, the Company’s cash flow could be negatively impacted.

Our inability to develop and implement e-commerce strategies that align with industry standards,

could adversely affect our business.

In the event Kodak were unable to develop and implement e-commerce strategies that are in alignment with

consumer trends, the Company’s business could be adversely affected. The availability of software and

standards related to e-commerce strategies is of an emerging nature. Kodak’s ability to successfully align

with the industry standards and services and ensure timely solutions requires the Company to make

accurate predictions of the future accepted standards and services.

System integration issues could adversely affect our revenues and earnings.

Portions of our IT infrastructure may experience interruptions, delays or cessations of service or product

errors in connection with systems integration or migration work that takes place from time to time; in

particular, installation of SAP within our Graphic Communications Group. We may not be successful in

implementing new systems and transitioning data, which could cause business disruptions and be more

expensive, time consuming, disruptive and resource-intensive. Such disruption could adversely affect our

ability to fulfill orders and interrupt other processes. Delayed sales, higher costs or lost customers resulting

from these disruptions could adversely affect our financial results, stock price and reputation.

Our inability to effectively manage our acquisitions could adversely impact our revenues and

earnings.

In 2005, Kodak completed two large business acquisitions in its Graphic Communications Group segment

in order to strengthen and diversify its portfolio of businesses, while establishing itself as a leader in the

graphic communications market. The Company is accelerating the current restructuring of its traditional

manufacturing infrastructure. In the event that Kodak fails to effectively manage the continuing decline of

its more traditional businesses while simultaneously integrating these acquisitions, it could fail to obtain the

expected synergies and favorable impact of these acquisitions. Such a failure could cause Kodak to lose

market opportunities and experience a resulting adverse impact on its revenues and earnings.

PAGE 16

Our inability to complete divestitures and other portfolio actions could adversely impact our

financial position.

In January 2007, Kodak announced that it has reached an agreement to sell the Health Group to Onex

Corporation. The transaction is expected to close in the first half of 2007. In the event that the Company is

unable to complete the divestiture of the Health Group, it could fail to realize the favorable impacts to the

Company created through the reduction of debt and other uses. Such a failure could cause Kodak to

experience an adverse impact on its financial position.

Economic trends in our major markets could adversely affect net sales.

Economic downturns and declines in consumption in Kodak’s major markets may affect the levels of both

commercial and consumer sales. Purchases of Kodak’s consumer products are to a significant extent

discretionary. Accordingly, weakening economic conditions or outlook could result in a decline in the level

of consumption and could adversely affect Kodak’s results of operations.

If we do not timely implement our planned inventory reductions, this could adversely affect our cash

flow.

Unanticipated delays in the Company’s plans to continue inventory reductions in 2007 could adversely impact Kodak’s cash flow outlook. Planned inventory reductions could be compromised by slower sales

due to the competitive environment for digital products, and the continuing decline in demand for

traditional products, which could also place pressures on Kodak’s sales and market share. In the event

Kodak is unable to successfully manage these issues in a timely manner, they could adversely impact the

planned inventory reductions.

Delays in our plans to improve manufacturing productivity and control cost of operations could

negatively impact our gross margins.

Kodak’s failure to successfully manage operational performance factors could delay or curtail planned

improvements in manufacturing productivity. Delays in Kodak’s plans to improve manufacturing

productivity and control costs of operations, including its ongoing restructuring actions to significantly

reduce its traditional manufacturing infrastructure, could negatively impact the gross margins of the

Company. Furthermore, if Kodak is unable to successfully negotiate raw material costs with its suppliers,

or incurs adverse pricing on certain of its commodity-based raw materials, reduction in the gross margins

could occur.

We depend on third party suppliers and, therefore, our revenue and gross margins could suffer if we

fail to manage supplier issues properly.

Kodak’s operations depend on its ability to anticipate the needs for components, products and services and

Kodak’s suppliers’ ability to deliver sufficient quantities of quality components, products and services at

reasonable prices in time for Kodak to meet its schedules. Given the wide variety of products, services and

systems that Kodak offers, the large number of suppliers and contract manufacturers that are dispersed

across the globe, and the long lead times that are required to manufacture, assemble and deliver certain

components and products, problems could arise in planning production and managing inventory levels that

could seriously harm Kodak. Other supplier problems that Kodak could face include component shortages,

excess supply and risks related to terms of its contracts with suppliers.

PAGE 17

We have outsourced a significant portion of our overall worldwide manufacturing operations and

face the risks associated with relying on third party manufacturers and external suppliers.

We have outsourced a significant portion of our overall worldwide manufacturing operations to third