Country Sustainability Ranking Update – May 2017 Sweden re-takes the lead Scandinavian countries still in front Political risks still elevated India resumes its upward trend Emerging giants facing demographic headwinds This semi-annual report provides a succinct summary and analysis of the Environmental, Social, and Governance (ESG) profiles of 65 countries around the globe. It builds on the results of RobecoSAM’s proprietary Country Sustainability Ranking (CSR) tool which collects and analyzes ESG data from 22 developed and 43 emerging market economies 1 via a structured and comprehensive framework to calculate an overall country score. The resulting scores offer insights into the investment risks and opportunities associated with each country and provide investors with a better frame of reference for making comparisons among countries and regions from a risk-return perspective. The summary outlined here complements findings gained from the more traditional country risk assessment and is particularly focused on integrating long-term perspectives 2 . For a more detailed outline of the methodology used, please refer to our brochure “Measuring Country Intangibles” 3 . The global risk landscape remains heavily shaped by ESG factors and their multifold interlinkages with macroeconomic and fiscal developments. Figure 1 is a global risk matrix based on a risk perception survey of around 750 experts among the World Economic Forum’s multi-stakeholder communities. It maps 30 global risks over a 10-year time horizon in terms of their perceived likelihood of occurring and their potential global impact. The assessment of these risks – categorized as economic, environmental, societal/social, technological, and geopolitical (which largely corresponds to governance in RobecoSAM’s terminology)—confirms that in 2017, environmental, societal/social, and governance (ESG) risks continued to dominate (shape) the landscape of risks both in terms of impact as well as likelihood on a global scale. Nine of the top ten risks belong to these categories in stark comparison to just a few years ago, when economic risks were more prevalent, especially at the height of the 2008-10 financial crisis. 1 Bulgaria, Pakistan and Vietnam were newly added to the coverage 2 There has been no change in the set of indicators, data sources or ranking approach in this update, except for the revised index methodology of the Energy Trilemma Index (ETI) and the partial replacement/complement of the World Bank’s GINI coefficient data with data from the OECD. Both, the ETI and the GINI coefficient are input factors for the environmental and social scores, respectively. (The ETI, developed by the World Energy Council and Oliver Wyman, ranks 125 countries in view of their ability to provide a secure, affordable, and environmentally sustainable energy system. The revised methodology includes more indicators, measures for the quality of supply and a review of the resilience of a country’s energy system.) Comparisons with past scores are always based on the scores that were originally published in previous reports. 3 “Measuring Country Intangibles”, June 2015, available on the RobecoSAM website: http://www.robecosam.com/en/sustainability-insights/about- sustainability/country-sustainability-ranking.jsp

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Country Sustainability Ranking Update – May 2017

Sweden re-takes the lead

Scandinavian countries still in front

Political risks still elevated

India resumes its upward trend

Emerging giants facing demographic headwinds

This semi-annual report provides a succinct summary and analysis of the Environmental, Social, and Governance (ESG) profiles

of 65 countries around the globe. It builds on the results of RobecoSAM’s proprietary Country Sustainability Ranking (CSR) tool

which collects and analyzes ESG data from 22 developed and 43 emerging market economies1 via a structured and

comprehensive framework to calculate an overall country score. The resulting scores offer insights into the investment risks and

opportunities associated with each country and provide investors with a better frame of reference for making comparisons

among countries and regions from a risk-return perspective. The summary outlined here complements findings gained from

the more traditional country risk assessment and is particularly focused on integrating long-term perspectives2. For a more

detailed outline of the methodology used, please refer to our brochure “Measuring Country Intangibles” 3.

The global risk landscape remains heavily shaped by ESG factors and their multifold interlinkages with macroeconomic and fiscal

developments. Figure 1 is a global risk matrix based on a risk perception survey of around 750 experts among the World

Economic Forum’s multi-stakeholder communities. It maps 30 global risks over a 10-year time horizon in terms of their perceived

likelihood of occurring and their potential global impact. The assessment of these risks – categorized as economic,

environmental, societal/social, technological, and geopolitical (which largely corresponds to governance in RobecoSAM’s

terminology)—confirms that in 2017, environmental, societal/social, and governance (ESG) risks continued to dominate

(shape) the landscape of risks both in terms of impact as well as likelihood on a global scale. Nine of the top ten risks belong to

these categories in stark comparison to just a few years ago, when economic risks were more prevalent, especially at the height

of the 2008-10 financial crisis.

1 Bulgaria, Pakistan and Vietnam were newly added to the coverage 2 There has been no change in the set of indicators, data sources or ranking approach in this update, except for the revised index methodology of the Energy Trilemma Index (ETI) and the partial replacement/complement of the World Bank’s GINI coefficient data with data from the OECD. Both, the ETI and the GINI coefficient are input factors for the environmental and social scores, respectively. (The ETI, developed by the World Energy Council and Oliver Wyman, ranks 125 countries in view of their ability to provide a secure, affordable, and environmentally sustainable energy system. The revised methodology includes more indicators, measures for the quality of supply and a review of the resilience of a country’s energy system.) Comparisons with past scores are always based on the scores that were originally published in previous reports. 3 “Measuring Country Intangibles”, June 2015, available on the RobecoSAM website: http://www.robecosam.com/en/sustainability-insights/about-sustainability/country-sustainability-ranking.jsp

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 2

Figure 1: The global risks landscape 2017

Source: “The Global Risks Report 2017”, World Economic Forum, Switzerland; https://www.weforum.org/reports/the-global-

risks-report-2017

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 3

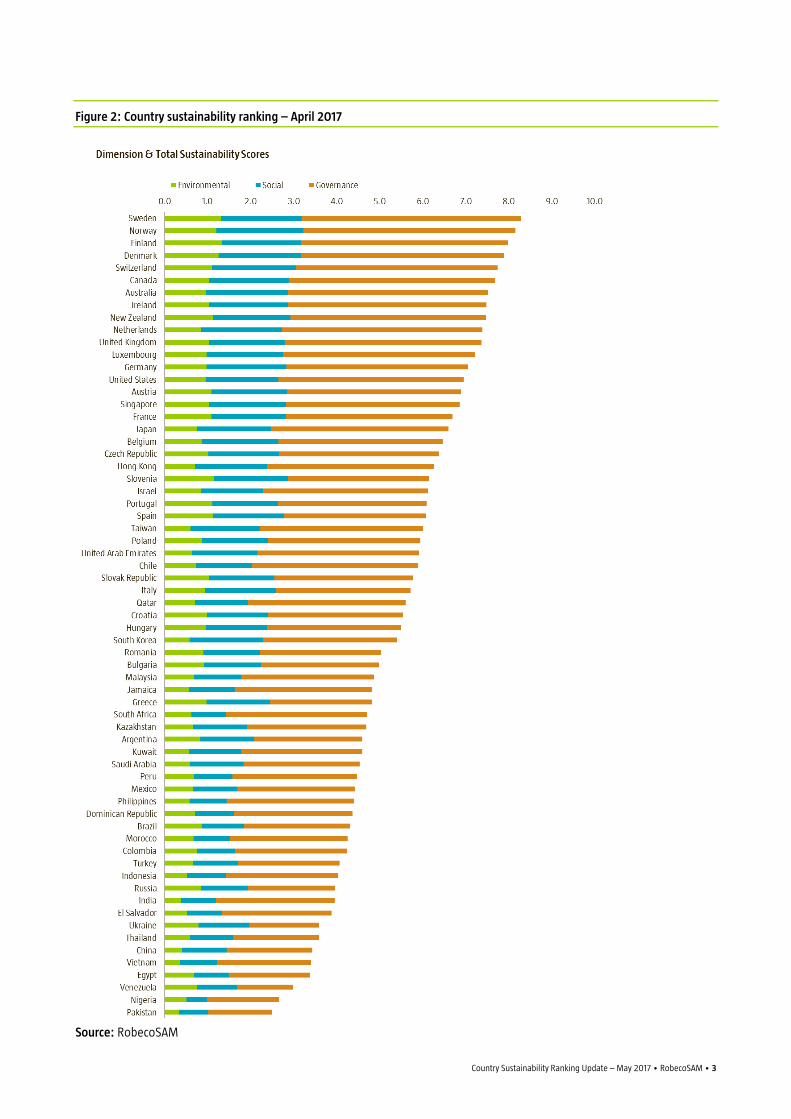

Figure 2: Country sustainability ranking – April 2017

Source: RobecoSAM

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 4

Positive Movements and Improvements—Sweden regains the crown

After having been temporarily stripped away by Norway, Sweden has regained its position at the top; followed by its three

Nordic neighbors and Switzerland further south. Sweden is, together with Denmark, also the only advanced economy that has

seen a notable increase in its score; the other countries with positive advances (most notably the UAE and Israel) are within

emerging markets. Countries showing an improvement in their sustainability performance generally benefitted from an

improved political risk rating, better political rights & civil liberties assessments, more favorable aging-related cost estimates,

and from upward revisions in social indicators. The list of improvers also includes Nigeria—however, gains were not sufficient

to significantly improve its overall country ranking where it still falls behind crisis-ridden Venezuela and only ahead of newly

added Pakistan. For the complete list of country rankings see Figure 2 above.

Losing Ground—South Korea in flux

Governments and countries are dynamic and changing for the better and for the worse and these changes are reflected in their

ESG scores. Among countries whose scores have deteriorated are the Ukraine and South Korea. The political situation in the

Ukraine continues to be marked by strain and confusion, while South Korea was rocked following the removal of former

President Park Geun-hye in a corruption scandal this past year. To add fuel to the flame, tensions with North Korea are flaring

once again as illustrated in the decline of its PRS Group political risk rating (77.5 to 75.5 from October 2016 to March 2017). The

election of Moon Jae-in on May 9 could bring a welcomed calm to the country’s turbulent political landscape given he has

promised to address corruption, curb conglomerate’s influence and take a more conciliatory approach towards its Northern

neighbor. However, a return to Park’s “Sunshine Policy” will prove difficult and success highly uncertain, as the regime in North

Korea remains unpredictable. Recall, the North launched its most recent missile tests just days after Moon’s election victory. For

a list of winners and losers and major score changes, please see Figure 3.

Figure 3: Major changes in country ESG scores – Oct 2016 vs Apr 2017

Source: RobecoSAM

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 5

ESG country ranking also reflected in newly-created SDG index

The newest country ranking (see Figure 3) is also closely correlated with the newly developed “Sustainable Development Goals”

(SDG) index (see Figure 4). The SDG index has been created by the Bertelsmann Stiftung and the United Nations Sustainable

Development Solutions Network in response to the 17 SDGs agreed upon by the UN in 2015. The SDGs provide a tool to help

countries identify national priorities and track SDG achievements 4. The index is designed to show which countries are leading

the world in advancing and fulfilling SDG goals. Out of 149 countries, the Nordics once again take the top four places followed

by Switzerland. The close correlation between the country ESG scores and the SDG index is not surprising, as many of the SDGs

are in some form measured by our Country Sustainability Ranking.

Figure 4: Country ESG score & SDG index in comparison

Source: Bertelsmann Stiftung, Sustainable Development Solutions Network, RobecoSAM

Politics—still the main ESG risk driver

Though mainstream politicians prevailed in Austrian and Dutch elections, and Marine Le Pen suffered a clear defeat in the

French presidential voting, it would still be premature to declare that the populist uprising has peaked. True, Emmanuel

Macron’s victory offers hope for France as well as the EU, as his chances of making progress on crucial reforms looks better than

those of his predecessors. However, it remains to be seen whether Macron’s “En Marche!” movement can leverage current

momentum into a similar win in next month’s legislative elections, greatly facilitating his reform agenda. But even so, he will

have no easy ride and is certain to face strong public opposition that could force him to dilute his reform plans. Recall that a

third of French voters backed the leader of an overly xenophobic and far-right party in the same election that brought him

victory.

In the US, the first 100 days of the Trump presidency were not exactly a success story. Already before the Comey scandal it

proved to be difficult to unite Congress and the White House on any topic. This will not get any easier as President Trump has

alienated supporters in Congress and continues to stoke controversy with mounting allegations linking his presidential

campaign to cyber-crime and the Kremlin. Some members of Congress have even begun to discuss the possibility of

impeachment. In any case, the latest developments have added more uncertainty to US politics, giving rise to concerns about

4 Bertelsmann Stiftung & United Nations Sustainable Development Solutions Network (SDSN): SDG Index & Dashboards – A Global Report, July 2016

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 6

increasing policy paralysis and a potential constitutional crisis. This period saw also the release of more details of Trump’s federal

budget proposal on May 22, which cuts deeply into programs for the poor, from health care and food stamps to student loans

and disability payments, which would negatively affect social indicators. However, the budget is unlikely to pass Congress in its

current form.

Hence, one should not prematurely conclude that political risks have markedly diminished in recent months, the more so, as

rising inequalities within many countries and pent-up resentment over having missed out on economic growth – often touted

as key factors for the rise of populism and nationalism – have not disappeared. As already outlined in a recent article5, persistent

disparities both within and between countries continue to impair prospects for sustainable development by threatening

economic and socio-political stability. Instability in one country can easily spread to others as large-scale involuntary emigrations

from one country trigger populist backlashes in destination countries.

Populism on the Bottom, Scandals at the Top

Political and social developments are also a key aspect to watch when assessing the sustainability performance in several large

emerging economies, such as Argentina, Brazil, China, India, Mexico, Philippines, South Africa, South Korea, Thailand, and

Venezuela. While the latter has been on the brink of collapse for quite some time, Latin American heavyweight Brazil is faced

with a kind of political déjà-vu, as impeachment calls once again threaten economic recovery. Corruption allegations against

President Michel Temer have rattled financial markets in recent days signaling fresh worries about political risk and worsening

reform prospects.

The Top 10—What’s Changed and what remains the Same

Consistently Stable

The composition of the group of top-10 ESG performers in April 2017 is identical with that of the previous October 2016 ranking—

with one exception. Ireland moved up and in, while Luxembourg, previously ranked at 10, moved down and out. All leading

countries exhibit very solid and balanced overall sustainability profiles. For its part, Norway was the only country to rank in the

top quintile in all three dimensions (Economic, Social, and Governance) scores within its peer group of high-income advanced

economies (see Figure 8 for country comparisons). All other Nordics exhibited a score within the top quintile for at least two of

the three ESG dimensions, reflecting their fairly inclusive, sustainable and “green” growth models, favorable gender and income

equality structures, an encompassing social safety net, stable political conditions, and a generally high quality of life.

Switzerland Gets Even Greener

Switzerland has established itself as the Nordics closest contender in the ranking and is currently in an important strategic policy-

making period that will affect its future sustainability profile. After having rejected two environmental/energy-related

referendums last year – one on implementing a green economy and one on limiting the use of existing nuclear power stations

– Swiss voters embraced the government’s “energy strategy 2050” on May 21 with 58.2% in favor. The plan aims to gradually

withdraw from nuclear power (which accounted for approx. 40% of the domestic energy production in recent years), cut

nationwide energy usage by 43% by 2035, and promote renewable resources such as wind and solar energy. On September 24

this year, the Swiss people will vote on the controversial pension reform package “Altersvorsorge 2020”, intended to secure

funding for old age pensions. Key features of the reform include an increase of the retirement age for women by one year to

the age of 65, a reduction of pension payments for retirees, and an increase of the VAT to finance the reform.

5 RobecoSAM: “Political risks threaten the 2017 country ESG landscape”, February 2017

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 7

Figure 5: Top 10 country ESG scores

Source: RobecoSAM

ESG ranking within the EMU: troubles ahead for Ireland?

Finland consolidated its leading position among European Monetary Union (EMU) member states (see Figure 6 for the EMU

score comparisons). The country claims most of the “Nordic model” characteristics and distinguishes itself through its high living

standard, excellent education system, low income inequality, a healthy population and the environmental quality. Even though

the country has been hit hard by several shocks in recent years it has been able to maintain its high level of well-being; however,

continuing economic weakness and a rapidly aging population could nevertheless erode the country’s economic and social

model over time.

Among the economic heavyweights, France has been able to show a small improvement, primarily based on a more favorable

political risk rating from the PRS Group—presumably in expectation of a Marine Le Pen’s defeat in the presidential election.

Germany, which saw a slight deterioration in its political risk score in early 2017, should see a reversal in this decline given the

strong showing of Merkel’s conservatives in the recent state polls in Saarland, Schleswig-Holstein and North Rhine Westphalia.

These regional victories should provide the CDU (Christian Democratic Union) a strong boost for the federal elections in

September and further weaken the far-right and populist AfD (Alternative for Germany) party.

Behind Finland in the EMU ranking comes Ireland, which continued to stabilize its overall sustainability profile, confirming its

astonishing comeback from the financial crisis that crippled other European peripheral economies (notably Greece, Italy,

Portugal, and Spain). Ireland’s strong profile is based on a robust governance framework and a favorable political and social

climate, all of which are reflected in leading positions in the Political Risk, Fragile States, and Social Progress Indexes. The

country can also rely on a well-developed welfare system that has not only helped to maintain social cohesion, but also its

readiness to accept painful and needed structural reforms to overcome the 2008-12 financial crisis.

However, having successfully emerged from this crisis period, the country is now faced with another major uncertainty brought

about by the UK’s Brexit decision. Given Ireland’s close ties economically, financially, geographically, and politically, Brexit could

have far-reaching consequences for the country. Since the accession of Ireland and Britain to the EEC in 1973, the two countries

have always been closely aligned and have traditionally found a common position on matters of trade, regulation, and financial

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 8

services legislation. Now, Britain’s withdrawal from the EU, particularly a “hard” Brexit outcome, could damage British-Irish

cooperation with unintended consequences in areas such as trade, foreign direct investment, energy, migration, and the

Republic’s future relationship with Northern Ireland. All of these could have potential ramifications for the country’s

sustainability profile, above all in areas such as political risk and competitiveness.

Figure 6: ESG scores for EMU countries

Source: RobecoSAM

Progress stalls in ESG trends among peripherals

Greece—Again in the Spotlight

The European peripheral countries did not make further progress in their sustainability performance. Greece is once again in

negotiations for a new debt relief deal with EU officials and the IMF. The IMF has made it clear that its support would be

contingent on further debt concessions from European member states. Negotiations have stymied as Germany and some

northern European countries are opposed to further lending. On May 22, Greece’s creditors failed to reach a deal, which would

have released vital rescue funds for the country. Talks are expected to continue over the coming weeks ahead of the next

meeting of EU finance ministers on June. A few days before, on May 14, the Greek government slashed its GDP growth forecast

for 2017 by 1 percentage to 1.8% as it moved towards implementing new austerity measures which will further aggravate socio-

economic conditions and put renewed pressure on the Tsipras government. As indicated by subsequent protests, social and

political tensions are thus likely to rise again, which is also reflected in the further deterioration of the political risk score since

October last year. As a result, Greece will continue to occupy the bottom position among EMU members in the foreseeable

future.

Spain’s Slow March Towards Progress slowed down for now

As already outlined, Ireland is the clear sustainability leader in the EMU group. With a score of 7.41 (#8), the country ranks

significantly ahead of Italy (5.71/# 31) and Spain (6.07/#25), as also illustrated by a comparison of their sustainability profiles

(see Figure 7). Italy as well as Spain have overcome gaps in their score from March 2011; for its part, Spain has always been

able to maintain a slightly superior profile compared to Italy with regard to most ESG criteria. However, its initial progress made

in the early stages of the recovery phase just after the financial crisis, has stalled during the last two years. Much of this

stagnation in the ESG performance can be explained by the delicate socio-economic conditions and the political uncertainty that

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 9

has marked recent years. In Spain, the crisis has left deep sores that are still visible in the high unemployment, inequality,

poverty and inadequate education, areas in which the country is also displaying major gaps in its sustainability profile relative

to its peers. As the political situation continues to stabilize under the leadership of Mariano Rajoy’s minority government and

as the economic situation continues to improve, Spain’s ESG profile could gradually improve. That said, the government still

faces obstacles from all sides including finding the right balance in its reform ambitions. Moreover, the Catalonia secession

issue is far from being resolved and could still get worse – probably the biggest peril for the country at the moment.

Italy’s Struggles

Italy also looks back on some politically turbulent months, mirrored in a renewed decline of its political risk rating, after a

temporary recovery in 2016. Even though the country has initiated some reforms, the business climate is still impaired by

considerable inefficiencies in public administration, slow judicial processes, inadequate regulations, and a lack of competition-

which are reflected in the following indicators: Government Efficiency, Rule of Law, Regulatory Quality and Competitiveness in

Figure 7. The country displays inadequate literacy levels and a pronounced job-skill mismatch, which contributes to low earnings,

high unemployment and widespread poverty, in particular in the Mezzogiorno. Further reform efforts will be needed to improve

the business environment, workers’ skills and reduce poverty, all of which are essential for more sustainable economic growth.

In the more immediate future, Italy needs to restore political stability that would allow these kinds of policy measures to be

implemented. In the recent leadership challenge, former prime minister Matteo Renzi has been re-elected as leader of the

country’s governing Partito Democratico (PD), conferring some tailwind to the PD, which will now start to prepare the next

elections to be held no later than May 2018. The Eurosceptic and populist Five Star Movement is currently still riding high in the

polls – neck and neck with the center-left PD – and it could well be that the next election will not produce a clear winner, leaving

Italy in a situation similar to what we have seen in Spain. A continued fragile political situation with the threat of post-election

policy paralysis currently appears as the biggest risk driver from a country ESG perspective.

Figure 7: Country sustainability profiles in comparison

Source: RobecoSAM

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 10

Figure 8: Country sustainability profiles in comparison

Source: RobecoSAM

India resumes upward trend – Turkey in dangerous waters

Singapore defends its clear leadership in sustainability performance in the emerging markets (EM) universe as well as in the

sub-group of high-income emerging economies. With a score of 6.85 and rank 16 it displays not only a solid lead over its nearest

pursuer – the Czech Republic (ESG score of 6.33/#20) – but is also outpacing several advanced economies. Singapore’s

dominance is also visible from the sustainability profile comparison in Figure 8, where it shows a top quintile score in terms of

the overall ESG score as well as all three ESG dimensions— the only country in its peer group to do so. At the other end of the

ranking, the group of bottom 10 is still composed, by and large, of the same countries. These include two of the three newly

added economies, Vietnam and Pakistan, whose overall ESG profile displays major shortcomings in various ESG areas. Factors

Sweden Luxembourg

Norway Germany

Finland United States

Denmark Austria

Switzerland France

Canada Japan

Australia Belgium

Ireland Portugal

New Zealand Spain

Netherlands Italy

United Kingdom Greece

Singapore Chile

Czech Republic Slovak Republic

Hong Kong Qatar

Slovenia Croatia

Israel Hungary

Taiwan Korea, South

Poland Kuwait

UAE Saudi Arabia

Romania Dominican Rep.

Bulgaria Brazil

Malaysia Colombia

Jamaica Turkey

South Africa Russia

Kazakhstan Thailand

Argentina China

Peru Venezuela

Mexico

Philippines Ukraine

Morocco Vietnam

Indonesia Egypt

India Nigeria

El Salvador Pakistan

ESG performance in the top quintile of peers ESG performance below peer average

ESG performance above peer average ESG performance in the lowest quintile of peers

* Country classification according to World Bank. For the 2017 fiscal year, the World Bank defines low-income

economies as those with a GNI per capita of $1,025 or less in 2015; lower middle-income economies as those with a

GNI per capita of $1,026 and $4,035; upper middle-income economies as those with a GNI per capita between $4,036

and $12,475, and high-income economies as those with a GNI per capita of $12,476 or above.

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 11

that resulted in score improvements or deteriorations were similar to those mentioned for other countries, with changes in

political risk indicators like political rights & civil liberties playing a large role.

Figure 9: Bottom 10 country ESG scores

Source: RobecoSAM

India has resumed its gradual upward trend moving from position 59 to 56. The withdrawal of the 500 and 1000 rupee notes

in the latter half of last year in an attempt to target corruption, does not appear to have had a major impact on Narendra Modi’s

popularity. To the contrary—thanks to the BJP’s (Bharatiya Janata Party) major victory in legislative elections in India’s most

populous state Uttar Pradesh in March this year, Modi has been able to consolidate his power, which augurs well for future

plans. As Modi will also eye a return to power in the 2019 election with an even stronger mandate, he is also likely to continue

to pursue his rather gradual and cautious approach to reforms. On the other hand, political risk remains an important threat,

as India remains vulnerable to sudden outbreaks of ethnic and religious strife between Hindus and Muslims, as well as well as

recurrent escalations of the Kashmir conflict with Pakistan.

India also suffers from major shortcomings with respect to key social factors that produce a drag on the country’s overall ESG

profile. While it is true that strong growth in recent years has raised incomes and reduced poverty, inequalities remain sizable

as well as disparities in living standards. Large parts of the population still lack access to basic public services, such electricity,

clean water, adequate sanitation, and/or health services. One key positive aspect is demographics, which is outlined in more

detail later.

After the people voted in a bitterly contested referendum in favor of a new constitution with a Turkish-style Executive Presidency

in mid-April, political uncertainty in Turkey remains high and is the most important risk driver for the country’s future ESG trend.

Ironically, its political risk rating from the PRS Group has slightly improved since the previous update. This was most likely in

expectation of an end to electoral uncertainties after the referendum and an increased focus on economic policies and reforms

now that Erdogan authority is concentrated and secured. However, the first signs post referendum have not been very

encouraging. Erdogan has continued his crackdown on opponents, has been re-elected leader of the ruling AKP (Justice &

Development) party, and has resumed talks on re-introducing the death penalty—indicators pointing towards an increasingly

authoritarian future for Turkey. Obviously, this would not bode well for the Turkish economy, its political stability, or a return to

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 12

normalized relations with the EU and other western countries. It gives strong indications of a continued trend that began in

2013 which is reflected in its ESG score, its sovereign ratings, and its CDS spread developments as shown in Figure 10. For more

details on Turkey’s overall ESG performance, please refer to the country briefing from December 2016, available on the

RobecoSAM website6.

Figure 10: Turkey’s woes reflected in rating & spread developments

Source: Rating Agencies (Fitch, Moody’s, S&P), Markit, RobecoSAM

Emerging giants facing diverging demographic headwinds

An increasing number of emerging market countries share a common problem with more mature economies: a rapidly

worsening demographic transition which will adversely affect their economic growth potential while posing considerable fiscal

challenges. The three emerging economic heavyweights – Brazil, China, and India - too, are not immune from this

development, but they are affected in widely varying degrees. This trend is most acute in China, which shows the sharpest

increase in the old-age dependency ratio, i.e. the number of elderly people (aged 65+), compared to the number of people of

working age (15-64 years old), as illustrated in Figure 11. China has already seen the share of its working-age population

shrink by 1 percentage point to 73.2% from 2010 to 2015 and will further decline to 58.9% by 2050, according to UN

projections. A similar, albeit slightly less pronounced, trend is projected for Brazil. In contrast, the percentage of working age

persons in India is expected to slightly expand from 65.6% in 2015 to 67.1% in 2050.

The ageing population will also pose challenges for increasing old age pensions and health-related expenditures which will

require further investments in social security systems and add additional strain on public finances. In this regard, Brazil

appears to be the worst off. Current IMF estimates put the Net Present Value (NPV) of Pension Spending Change 2015-50 at

135.9% of GDP – significantly up from last year’s estimate of 98.9%. The corresponding NPV of Brazil’s Health Care Spending

Change amounts to 61.8% of GDP. These figures are much higher than the equivalent estimates for China (83.7%/47.1%) and,

6 RobecoSAM: “Country ESG trends in Turkey: a country going astray”, December 2016

*=Average rating of Fitch, Moody's & S&P

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 13

in particular, India (-5.5%/14.3%)7, which is in the best fiscal position. Already in 2015, pension and health spending in Brazil

claimed half of total public spending (i.e. 16% of GDP) and is projected to increase to 21% of GDP by as early as 20258. This

suggests that the aging problem will rapidly become a major ESG driver for Brazil and that reforms are becoming increasingly

urgent, not least given the country’s already notoriously deficient fiscal accounts.

Figure 11: Emerging giants facing different demographic headwinds

Source: RobecoSAM

7 IMF: “Fiscal Monitors”, April 2017 and April 2016 8 IMF: “Fiscal Challenges of Population Aging in Brazil”, IMF Working Paper – WP/17/99, March 2017

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 14

“A proper country sustainability assessment provides additional information and valuable insights into a country’s underlying risk drivers that we believe are critical to making balanced investment decisions”.

Max Schieler

Senior Country Risk Specialist

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 15

Appendix

Data sources

ta sources

Environmental Status Yale; Environmental Performance Index

http://epi.yale.edu/

Energy World Energy Council/Oliver Wyman; Energy Trilemma Index

https://trilemma.worldenergy.org/

United Nations; Energy Statistics

http://unstats.un.org/unsd/default.htm

Environmental Risk Bündnis Entwicklung Hilft; World Risk Report

http://www.entwicklung-hilft.de/home.html

Germanwatch; Global Climate Risk Index

https://germanwatch.org/en/cri

Social Indicators Social Progress Imperative; Social Progress Index

http://www.socialprogressimperative.org/

UNDP; Gender Inequality Index

http://hdr.undp.org/en/data

UNICEF; Child Labour

https://data.unicef.org/

World Bank; World Development Indicators – GINI Index

http://databank.worldbank.org/data/

OECD; Income Distribution Database

http://www.oecd.org/social/income-distribution-database.htm

Human Development UNDP; Human Development Report

http://hdr.undp.org/en

Social Unrest Fund for Peace; Fragile States Index

http://fsi.fundforpeace.org/

Liberty & Inequality Freedom House; Political Rights & Civil Liberties

https://freedomhouse.org/reports

Competitiveness World Economic Forum; The Global Competitiveness Report 2016-2017, WEF, Switzerland, 2016

https://www.weforum.org/reports/the-global-competitiveness-report-2016-2017-1/

Political Risk PRS Group; Political Risk Services (PRS)

http://www.prsgroup.com/

Accountability World Bank; Worldwide Governance Indicators

http://info.worldbank.org/governance/wgi/index.aspx#home

Stability World Bank; Worldwide Governance Indicators

http://info.worldbank.org/governance/wgi/index.aspx#home

Effectiveness World Bank; Worldwide Governance Indicators

http://info.worldbank.org/governance/wgi/index.aspx#home

Regulatory Quality World Bank; Worldwide Governance Indicators

http://info.worldbank.org/governance/wgi/index.aspx#home

Rule of Law World Bank; Worldwide Governance Indicators

http://info.worldbank.org/governance/wgi/index.aspx#home

Corruption World Bank; Worldwide Governance Indicators

http://info.worldbank.org/governance/wgi/index.aspx#home

Aging IMF - Fiscal Monitor; NPV of Pension & Health Care Spending Change 2015-50

http://www.imf.org/external/

UN – Population Division; Old Dependency Ratio & Old Dependency Ratio 2050

https://esa.un.org/unpd/wpp/

World Bank – Women, Business and the Law; Retirement Age

http://wbl.worldbank.org/

Institutions World Economic Forum; The Global Competitiveness Report 2016-2017, WEF, Switzerland, 2016

https://www.weforum.org/reports/the-global-competitiveness-report-2016-2017-1/

Country Sustainability Ranking Update – May 2017 • RobecoSAM • 16

About RobecoSAM Founded in 1995, RobecoSAM is an investment specialist focused exclusively on Sustainability Investing. It offers asset management, indices, impact analysis and investing, sustainability assessments, and benchmarking services. The company’s asset management capabilities cater to institutional asset owners and financial intermediaries and cover a range of ESG-integrated investments, featuring a strong track record in resource efficiency-themed strategies. Together with S&P Dow Jones Indices, RobecoSAM publishes the globally recognized Dow Jones Sustainability Indices (DJSI) as well as the S&P ESG Index series, the first index family to treat ESG as a standalone performance factor using the RobecoSAM Smart ESG methodology. Based on its Corporate Sustainability Assessment (CSA), an annual ESG analysis of over 3,900 listed companies, RobecoSAM has compiled one of the world’s most comprehensive databases of financially material sustainability information. The CSA data is also included in USD 86.5 billion of assets under management by the subsidiaries of the Robeco Group.

RobecoSAM is a sister company of Robeco, the Dutch investment management firm founded in 1929. Both entities are subsidiaries of the Robeco Group, whose shareholder is ORIX Corporation. As a reflection of its own commitment to advancing sustainable investment practices, RobecoSAM is a signatory of the PRI and UN Global Compact, a member of Eurosif, Swiss Sustainable Finance, Carbon Disclosure Project (CDP), Ceres and Portfolio Decarbonization Coalition (PDC). As of December 31, 2016, RobecoSAM had client assets under management, advice and/or license of approximately USD 16.1 billion.

Disclaimer

No warranty: This publication is derived from sources believed to be accurate and reliable, but neither its accuracy nor completeness is

guaranteed. The material and information in this publication are provided “as is” and without warranties of any kind, either expressed or

implied. RobecoSAM AG and its related, affiliated and subsidiary companies disclaim all warranties, expressed or implied, including, but not

limited to, implied warranties of merchantability and fitness for a particular purpose. Any opinions and views in this publication reflect the

current judgment of the authors and may change without notice. It is each reader’s responsibility to evaluate the accuracy, completeness

and usefulness of any opinions, advice, services or other information provided in this publication.

Limitation of liability: All information contained in this publication is distributed with the understanding that the authors, publishers and

distributors are not rendering legal, accounting or other professional advice or opinions on specific facts or matters and accordingly assume

no liability whatsoever in connection with its use. In no event shall RobecoSAM AG and its related, affiliated and subsidiary companies be

liable for any direct, indirect, special, incidental or consequential damages arising out of the use of any opinion or information expressly or

implicitly contained in this publication.

Copyright: Unless otherwise noted, text, images and layout of this publication are the exclusive property of RobecoSAM AG and/or its

related, affiliated and subsidiary companies and may not be copied or distributed, in whole or in part, without the express written consent

of RobecoSAM AG or its related, affiliated and subsidiary companies.

No Offer: The information and opinions contained in this publication constitutes neither a solicitation, nor a recommendation, nor an offer

to buy or sell investment instruments or other services, or to engage in any other kind of transaction. The information described in this

publication is not directed to persons in any jurisdiction where the provision of such information would run counter to local laws and

regulation.

Copyright © 2017 RobecoSAM AG

RobecoSAM | Josefstrasse 218 | 8005 Zurich | Switzerland | T +41 44 653 10 10 | F + 41 44 653 10 80 | www.robecosam.com |

Related Documents